revenue levels rise 34 per cent - palfinger.ag

TRANSCRIPT

revenue levelSriSe 34 per cent interim report for the firSt three QuarterS of 2011

2 palfinger interim report 2011

<< back forward >> search Print

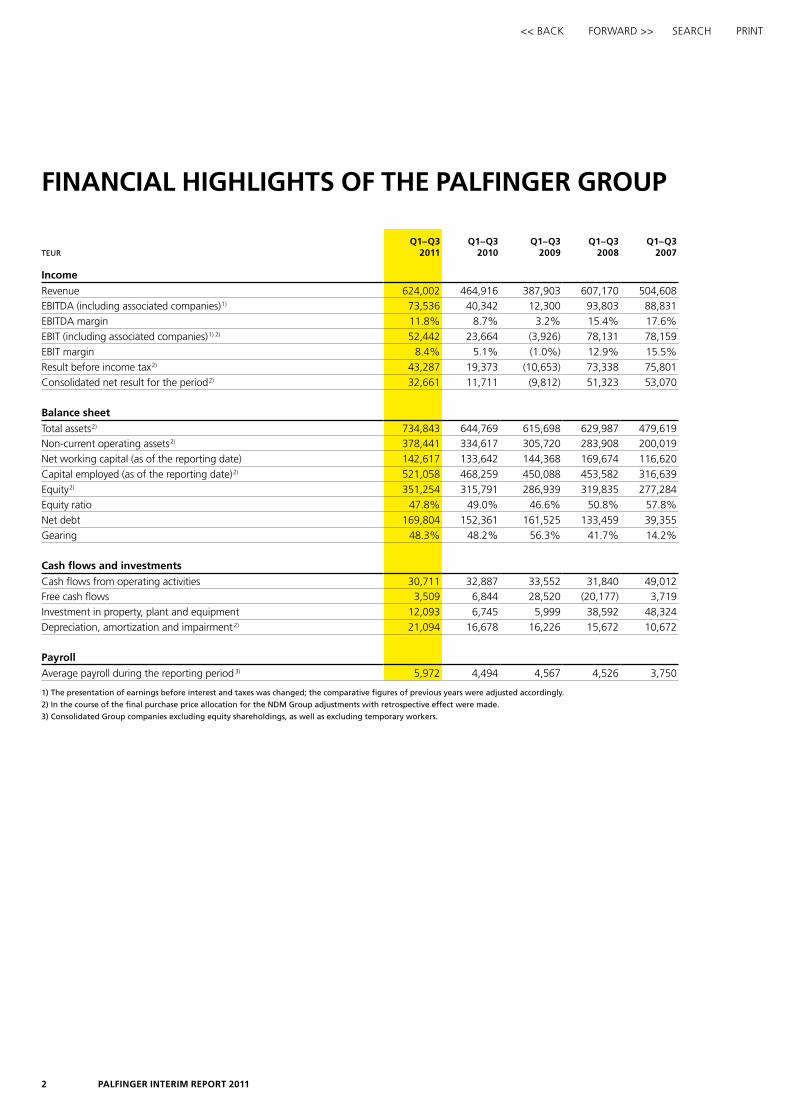

financial highlightS of the palfinger group

TEURQ1–Q3

2011Q1–Q3

2010Q1–Q3

2009Q1–Q3

2008Q1–Q3

2007

income

revenue 624,002 464,916 387,903 607,170 504,608ebitda (including associated companies) 1) 73,536 40,342 12,300 93,803 88,831ebitda margin 11.8% 8.7% 3.2% 15.4% 17.6%ebit (including associated companies) 1) 2) 52,442 23,664 (3,926) 78,131 78,159ebit margin 8.4% 5.1% (1.0%) 12.9% 15.5%result before income tax 2) 43,287 19,373 (10,653) 73,338 75,801consolidated net result for the period 2) 32,661 11,711 (9,812) 51,323 53,070

balance sheet

total assets 2) 734,843 644,769 615,698 629,987 479,619non-current operating assets 2) 378,441 334,617 305,720 283,908 200,019net working capital (as of the reporting date) 142,617 133,642 144,368 169,674 116,620capital employed (as of the reporting date) 2) 521,058 468,259 450,088 453,582 316,639equity 2) 351,254 315,791 286,939 319,835 277,284equity ratio 47.8% 49.0% 46.6% 50.8% 57.8%net debt 169,804 152,361 161,525 133,459 39,355Gearing 48.3% 48.2% 56.3% 41.7% 14.2%

cash flows and investments

cash flows from operating activities 30,711 32,887 33,552 31,840 49,012free cash flows 3,509 6,844 28,520 (20,177) 3,719investment in property, plant and equipment 12,093 6,745 5,999 38,592 48,324depreciation, amortization and impairment 2) 21,094 16,678 16,226 15,672 10,672

payroll

average payroll during the reporting period 3) 5,972 4,494 4,567 4,526 3,750

1) The presentation of earnings before interest and taxes was changed; the comparative figures of previous years were adjusted accordingly.

2) In the course of the final purchase price allocation for the NDM Group adjustments with retrospective effect were made.

3) Consolidated Group companies excluding equity shareholdings, as well as excluding temporary workers.

conSolidated management report

3palfinger interim report 2011

<< back forward >> search Print

conSolidated management report aS of 30 September 2011

economic environmentGlobal economic growth continued during the first three quarters of 2011, but slowed down marked- ly from mid-year onwards. according to the international Monetary fund (iMf), the global economy has been affected mainly by two related developments – slower growth in the advanced economies compared with 2010 and uncertainty on the financial markets.

Japan’s devastating natural disaster, the upheavals in numerous petrol-exporting countries of the Middle east, weak Us demand and the high debt levels of some european countries as well as Japanand the Usa have impacted on the real economy and harbour further downward risks. against thisbackdrop, the iMf has lowered its global growth forecast to a mere 4.0 per cent for 2011 and 2012.

in europe, the slowing of economic growth has also become increasingly evident in Germany and france, which have so far been considered the drivers of economic growth. the debt crisis in the eurozone has been expanding, and the risk of a spillover to other vulnerable countries and the euro-pean banking sector has been growing. for the eurozone, a growth rate of 1.6 per cent is forecast for 2011 and 1.1 per cent for 2012.

central and eastern europe has been indirectly affected by these developments, as the euro coun-tries are major export markets. accordingly, the growth forecast for this region has also been low-ered, to 4.3 per cent for 2011 and a mere 2.7 per cent for 2012.

in the Usa, the large national debt and the fiscal uncertainties have given rise to insecurities among businesses and private households. in september, the federal reserve adopted another stimulus ini-tiative, and expected GdP growth continues to be weak at 1.5 per cent for 2011 and 1.8 per cent for 2012.

Growth remains robust in Latin america, but the decline in foreign demand could lead to a signifi-cant slowdown of economic growth. to counter this development, brazil lowered its base rate in september despite high inflation. the iMf has forecast a growth rate of 3.8 per cent for 2011 and 3.6 per cent for 2012.

asia’s rising economies, first and foremost china, are still recording above-average growth. despite weakening growth in connection with global developments, exceptional growth rates of 9.5 and 9.0 per cent have been projected in china for 2011 and 2012, respectively.

in the first three quarters, the financial markets were marked by great uncertainty and hence high volatility. in the third quarter, many stock markets again experienced bouts of turbulence, with stock prices taking their sharpest plunge in years. fears of recession have also driven down commodity prices. after surging in the first quarter of 2011, the oil price fell, but at the end of the third quarter of 2011 the price of a barrel of brent crude was still at a high level, namely Usd 102.30.

Particularly in the third quarter of 2011, the euro dropped against the Us dollar and the chinese yuan and was valued at Usd 1.35 and cnY 8.62 respectively at the end of the quarter. however, the euro appreciated against the brazilian real and stood at brL 2.51.

conSolidated management report

4 palfinger interim report 2011

<< back forward >> search Print

performance of the palfinger group

the performance of the PaLfinGer Group over the first nine months of 2011 was extremely satis-factory. despite the new bouts of uncertainty over the further economic development of europe, PaLfinGer was able to utilize the distinct recovery of the markets to achieve significant organic growth, also in the third quarter, as compared with 2010. on the one hand, economic growth spurred demand in the period under review, while, on the other hand, the measures implemented in previous years took effect. by reducing costs and increasing flexibility, PaLfinGer has prepared it-self to face volatile markets, which materially supports sustainable and profitable growth both now and in the future.

in the third quarter, the completion of the takeover of the leading russian crane manufacturer inMan and of the service business of the british commercial tail lifts producer ross & bonnyman contributed to additional inorganic growth in revenue and earnings.

at eUr 624.0 million, the revenue generated in the first three quarters of 2011 was 34.2 per cent above the figure reported for 2010, when revenue was eUr 464.9 million. compared to the first three quarters of the difficult year 2009, revenue increased by a total of 60.9 per cent.

approximately one fourth of the increase compared to 2010 was due to inorganic growth through acquisitions made in 2010 and 2011. organic growth in revenue was generated largely in europe, although a positive trend was observed in all the regions. the level of revenue increase was particu-larly satisfactory in the areas asia and Pacific as well as india, areas which are still small in terms of revenue. in addition, the positive market development in the area north america was reflected in a marked increase in revenue, particularly in the third quarter.

PaLfinGer’s sophisticated trend monitoring was a key factor in enhancing predictability and there-fore, also, planning certainty, allowing the company to respond to any changes in the market envi-ronment at an early stage. in the third quarter, due to the prevailing uncertainty in some markets, the start of a slowdown in growth became apparent, especially in europe.

DEvElopMENT of REvENUE (TEUR)

624,

002

464,

916

387,

903

DEvElopMENT of EBIT INCl. assoCIaTED CoMpaNIEs(TEUR)

52,4

42

23,6

64

(3,9

26)

DEvElopMENT of REvENUE aND EBIT INCl. assoCIaTED CoMpaNIEs (EUR million)

RevenueEBITEBIT margin (in per cent)

0.2% 0.

8%

2.7%

6.5%

5.4%

7.2% 7.

9%

118.

7

117.

5

129.

4

168.

011

.0

167.

59.

1

186.

913

.5

191.

615

.1

0.3 3.6

222.

720

.99.

4%

0.9

209.

716

.57.

8%

Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011

240 12%

200 10%

160 8%

120 6%

80 4%

40 2%

0 0%

Q1 – Q3 2009

Q1 – Q3 2010

Q1 – Q3 2011

60,000

50,000

40,000

30,000

20,000

10,000

0

(10,000)

Q1 – Q3 2009

Q1 – Q3 2010

Q1 – Q3 2011

750,000

600,000

450,000

300,000

150,000

0

conSolidated management report

5palfinger interim report 2011

<< back forward >> search Print

in the first nine months of 2011, ebit (incl. associated companies) came to eUr 52.4 million as compared to eUr 23.7 million in the same period of 2010, corresponding to more than a doubling of the earnings before interest and taxes. this substantial improvement was achieved primarily as a result of significantly higher demand in all product divisions throughout all the areas, higher pro- ductivity in the facilities, and the effectiveness of the measures taken. the consolidated net result for the period almost tripled, rising from eUr 11.7 million in the first three quarters of 2010 to eUr 32.7 million in the period under review.

a comparison of performance over the individual quarters provides convincing evidence of a continuous upward trend since the beginning of 2010, taking into account the company holiday taken at the european sites in the third quarter of each year. in the third quarter of 2011, revenue came to eUr 209.7 million; the exceptionally large boost in ebit including associated companies resulted in an ebit margin of 7.8 per cent.

on the whole, the Group’s performance in europe was highly satisfactory. while revenue in numer-ous markets such as Germany, scandinavia, france, belgium, russia and Great britain significantly increased compared to the previous year, some weak markets such as Greece, spain, Portugal, italy and ireland continued to show a modest performance. Growing financial uncertainty over the third quarter was reflected in a lower order intake in europe in recent months, but to date has not yet had an impact on strong performers in terms of revenue such as Germany, france and austria.

the markets outside europe have been characterized by growth and/or stability at a satisfactory level. demand showed positive development in all product areas in north america, particularly in the second and third quarters of 2011, based on the expansion of production and the dealer network. PaLfinGer expects the upward trend in south america to be reinforced due to the upcoming in-vestments in infrastructure, especially those in brazil in connection with the fifa world cup in 2014 and the 2016 summer olympics.

strong growth rates were also recorded in russia. with approximately 3 per cent, the markets in asia currently still only account for a small share of PaLfinGer’s business. the sharp increase in revenue generated in the region demonstrates that these markets are gaining in importance. with production sites in china, Vietnam and – since the end of 2010 – also in india, PaLfinGer is well prepared for further growth.

conSolidated management report

6 palfinger interim report 2011

<< back forward >> search Print

financial poSition, caSh flowS and reSult of operationSat 47.8 per cent, the equity ratio was still at a high level at the end of the third quarter, albeit slightly below the year-end figure reported in 2010 (31 december 2010: 48.9 per cent). due to the satisfactory growth in earnings, equity rose from eUr 331.4 million as of 31 december 2010 to eUr 351.3 million as of 30 september 2011, despite payment of a dividend in the first half of 2011 and the effect of a stronger euro when translating the financial statements of the subsidiaries abroad. at the same time, the expansion of business volume led to an increase in total assets, from eUr 677.4 million as of 31 december 2010 to eUr 734.8 million as of 30 september 2011.

net working capital increased compared to the end of the second quarter by approximately eUr 8 million to eUr 142.6 million. the rise in inventories responsible for this increase was a con-sequence of the acquisition of inMan. in this context, capital employed as of 30 september 2011 came to eUr 521.1 million, i.e. around 3.6 per cent higher than on 30 June 2011. nevertheless, the ratio of net working capital to revenue remained almost constant, which demonstrates the sustainability of the measures taken to optimize net working capital.

at eUr 169.8 million, net debt as of 30 september 2011 was slightly above the year-end figure posted in 2010 (31 december 2010: eUr 160.9 million) and eUr 6.4 million above the figure reported for the second quarter of 2011. at 48.3 per cent, the gearing ratio once again remained below 50 per cent (31 december 2010: 48.6 per cent).

the reclassification of the tranches of the promissory note loan due in 2012 from non-current financial liabilities to current financial liabilities resulted in a 35.6 per cent reduction in non-current financial liabilities from eUr 123.6 million to eUr 79.6 million in the first three quarters of 2011. 82.7 per cent of PaLfinGer’s capital employed has been secured on a long-term basis. the capital employed management programme initiated in 2010 will be continued in the financial year 2011 so as to further optimize the Group’s financial structure.

cash flows from operating activities decreased from eUr 32.9 million in the same period of the previous year to eUr 30.7 million due to the effects described above. cash flows from investing activities came to –eUr 33.8 million. free cash flows amounted to eUr 3.5 million.

the year-on-year increase in revenue from eUr 464.9 million to eUr 624.0 million was primarily an indication of recovery in european markets. compared to the third quarter of 2010, another in-crease in revenue of eUr 42.2 million was reported in the third quarter of 2011. ebit (incl. associat-ed companies) in the amount of eUr 52.4 million (Jan–sep 2010: eUr 23.7 million) and the Group’s consolidated net result of eUr 32.7 million (Jan–sep 2010: eUr 11.7 million) demonstrate that PaLfinGer has emerged from the crisis stronger than before.

conSolidated management report

7palfinger interim report 2011

<< back forward >> search Print

other eventS

PaLfinGer realigned its strategic priorities in 2010. since the Group’s diversification targets have already been achieved, greater emphasis has been placed on further enhancing flexibility. in order to also obtain long-term balanced diversification in geographical terms, internationalization will continue to be at the core of the Group’s strategy together with innovation.

besides the Group-wide targeted capital employed management scheme, PaLfinGer also gives priority to further optimizing fixed-cost structures with a view to facilitating additional investment projects in the same magnitude from internal funding in order to support planned growth.

on 3 november 2011, PaLfinGer held an extraordinary General Meeting to be able to take corpo-rate actions facilitating greater flexibility in funding. the Meeting resolved on an authorized capital in the amount of eUr 10 million, enabling PaLfinGer to issue up to 10 million new shares. Moreover, the Management board was authorized to buy back shares in the magnitude of up to 10 per cent of the company’s share capital. these resolutions will make it possible for PaLfinGer to act quickly and flexibly, even when it comes to financing large-scale growth measures.

in early July 2011, PaLfinGer took a major strategic step in internationalization with the takeover of the leading russian crane manufacturer inMan. the Group thus generates value locally and has set up additional distribution channels in the large russian growth market. following the approval of the federal antimonopoly service of the russian federation, initial consolidation took place with effect of 26 august 2011. current integration priorities include market development, value creation and purchasing in order to quickly realize first potential synergies.

in order to promote the training of its employees, also with a view to expanding its business areas, PaLfinGer initiated further staff development programmes in 2011. the Palfinger Global Leadership Programme, for example, is aimed at promoting employees with potential management skills in all PaLfinGer companies worldwide. additional training programmes were set up in the production sector, for example welding academies in bulgaria and south america.

in an effort to highlight and expand PaLfinGer’s technology leadership, research and develop-ment was set as another priority of the financial year 2011. development of a new crane series, the completion of the product portfolio in the field of access platforms, revision of the north american transportable forklift model and regional adjustment of PaLfinGer’s products to the asian market are key issues in this connection. the further development of electronics and mechatronics is a sub-stantial success factor for PaLfinGer, and initiatives already started in these areas will be continued and expanded.

the project of building a new Group headquarters in austria was postponed, given the high level of uncertainty in the financial markets.

to meet the continued interest in PaLfinGer shares, PaLfinGer participated in international road shows and investor conferences in the period under review. after significantly outperforming the relevant stock exchange indices in 2010, the share price sagged lower than such indices during the past months of 2011 when volatility was high. as at 30 september 2011, the share price was eUr 15.91, 44.7 per cent below 2010’s year-end price of eUr 28.75.

conSolidated management report

8 palfinger interim report 2011

<< back forward >> search Print

performance by Segment

PaLfinGer implemented a new organizational structure at the beginning of 2010. it takes into account, on the one hand, the growth achieved in previous years, and on the other hand, the future challenges to be met in individual markets. since then, in line with the Group’s internal control structures, the segment figures reported have been broken down into the segments eUroPean Units and area Units and the VentUres unit.

DEvElopMENT of REvENUE By sEGMENT * (TEUR)

EUROPEAN UNITSAREA UNITS

* No revenues are generated in the VENTURES unit.

141,

101

45,7

7654,8

5611

2,65

8

171,

288

51,4

06

44,6

9314

6,88

3

148,

331

61,4

01Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011

200,000

175,000

150,000

125,000

100,000

75,000

50,000

25,000

0

conSolidated management report

9palfinger interim report 2011

<< back forward >> search Print

european unitS Segment

the eUroPean Units segment comprises the area eMea with the business units knuckle boom cranes, timber and recycling cranes, tail Lifts, access Platforms, hookloaders, transportable forklifts, railway systems, Production, the distribution company in Germany and the associated subsidiaries and, since the third quarter of 2010, the Marine systems business unit.

in the first three quarters of 2011, the eUroPean Units segment reported revenue in the amount of eUr 466.5 million. this corresponds to an increase of 38.0 per cent compared to the figure of eUr 338.1 million recorded in the first three quarters of 2010, or eUr 128.4 million. the new Marine systems business unit accounted for eUr 36.6 million of this growth.

the clear upward trend, which has been noticeable since 2010 thus continued into the first three quarters of 2011. it was observed primarily in the business units knuckle boom cranes, timber and recycling cranes and Production as well as in the distribution company in Germany. the recent performance of hookloaders and tail Lifts – and, from the second quarter of 2011 onwards, access Platforms – has been satisfactory as well.

at eUr 64.7 million, the segment result achieved in the first three quarters of 2011 was significantly above the previous year’s figure of eUr 34.5 million. this tremendous 87.2 per cent increase was due, on the one hand, to higher demand in major product areas and, on the other hand, to cost-cutting measures. in addition, the agreed sale of the non-controlling interest of 36 per cent in Palfinger southern africa (Pty.) Ltd. produced a positive one-off effect of eUr 2.0 million in June 2011.

Knuckle boom cranesthe marked revenue growth in the knuckle boom cranes business unit compared to the previous year continued in the third quarter in all major markets. notwithstanding the company holiday at the european production sites, it had a positive impact on earnings. the most successful markets includ-ed Germany, france, Great britain, scandinavia and south africa. spain, Portugal, the netherlands and the Middle east continued to be weak markets.

timber and recycling cranesthe highly positive performance achieved also continued in the field of ePsiLon timber and recy-cling cranes. revenue in the second and third quarters of 2011 almost doubled compared to the same periods in the previous year, with earnings consistently on a remarkably good level. brazil, north america and particularly russia are increasingly proving to be promising markets with great future potential.

tail liftsin the first three quarters of 2011, the tail Lifts business unit continuously reported a satisfactory rise in revenue as well as an exceptionally high increase in earnings. the takeover of the service business of ross & bonnyman in Great britain was completed in the third quarter of 2011 and has had a positive impact on the development of this business unit as well.

access platformsthe access Platforms business unit also reported considerable increases in revenue compared to the same period in 2010. the restructuring measures taken made it possible to generate positive earn-ings in the second and third quarters of 2011. the introduction of new products and the efforts made in the service area should have a positive impact on market development in 2012.

conSolidated management report

10 palfinger interim report 2011

<< back forward >> search Print

hookloadersthe success of the operational management of this business unit in france, which was restructured in 2010, was reflected by a sustainable turnaround achieved in the first three quarters of 2011. the measures taken in connection with the new structures, coupled with the onset of a market recovery, resulted in a clearly positive contribution to earnings from the second quarter of 2011 onwards. in addition, the technological and qualitative advantages of the products offered were reflected in the increase in demand, particularly in Germany.

transportable forkliftsin the transportable forklifts business unit, revenue soared by nearly 50 per cent compared to the first three quarters of 2010, primarily due to higher sales figures in Germany. as a consequence, this product area now also posts stable positive earnings, thereby contributing to the company’s success.

railway Systemsin contrast to the other business units, the volatile order situation in the railway systems business in 2010, in combination with the long lead times of projects, was reflected in weak positive earnings in the first three quarters of 2011. development of this business unit in the first three quarters was supported by the focus on the service strategy. an increase in incoming orders has been recorded since the beginning of 2011. however, it will take a couple of months for the railway systems business unit to return to its usual contribution to earnings.

productionimproved capacity utilization and optimized process and cost structures in the Production business unit resulted in an exceptionally large increase in earnings during the reporting period. Moreover, PaLfinGer has already established a reputation as a reliable partner with top quality products in the field of third-party manufacturing, which is reflected in the increased interest expressed by customers. in croatia, in order to further optimize production flows, Palfinger Marine d.o.o, skrljevo, was merged into Palfinger Proizvodna tehnologija hrvatska d.o.o., delnice, in the second quarter of 2011 and the delnice site was expanded. an expansion of production capacities by 30 per cent at the site in tenevo, bulgaria, was agreed upon with a view to ensuring the supply of all product areas with top-quality cylinders even if demand continues to increase.

marine Systemsthe advancing integration of the new Marine systems business unit is well underway, which is reflected in an increase in incoming orders and positive earnings. Primarily ned-deck Marine made substantial contributions to earnings. in the offshore wind energy sector, two important large-scale orders were won in the third quarter. this sector will remain a priority, enabling PaLfinGer to derive optimal benefit from the future potential of this growth market.

conSolidated management report

11palfinger interim report 2011

<< back forward >> search Print

area unitS Segment

the area Units segment comprises the areas north america, south america, asia and Pacific, india and cis together with their respective regional business units.

Most of the areas outside europe are still being developed, reinforced by the Group’s acquisitions and own initiatives. by integrating and further expanding its strategic initiatives – including the costs incurred in this connection initially – PaLfinGer aims to quickly enter the profit zone in the area Units on the basis of continued growth.

in the third quarter of 2011, PaLfinGer took over the leading crane producer in russia; the earnings posted by inMan have been included in this segment since 26 august.

revenue generated by the area Units segment rose by 24.2 per cent, from eUr 126.8 million in the first three quarters of 2010 to eUr 157.5 million in the period under review. this revenue growth was boosted primarily by the acceleration of demand in north america and a marked in-crease in revenue in asia. currently, areas outside europe account for 25.2 per cent of consolidated revenue.

the segment result improved from –eUr 5.7 million in the previous year to –eUr 5.3 million in the first three quarters of 2011. a comparison of performance over the individual quarters shows a clearly positive trend: after –eUr 2.6 million in the first quarter and –eUr 1.7 million in the second quarter, third quarter ebit came to –eUr 0.9 million.

north america in the area north america, the local product range was rounded off with the acquisition of eti, an access platform producer, in 2010. in the off-road sector of timber and recycling cranes, highly promising cooperation with caterpillar opened up new market opportunities for PaLfinGer. furthermore, all the business units in this area reported significant revenue growth, in particular during the second and third quarters, thereby bringing its result back into the black. PaLfinGer is still working hard to integrate the business units in terms of value creation as well as distribution and dealer networks in a move designed to generate additional potential for this area.

South americaPaLfinGer still sees south america as a growth market in which the Group consistently pursues the establishment of new products such as its ePsiLon timber and recycling cranes. in the second and third quarters of 2011, satisfactory increases in revenue were generated particularly in chile. increased efficiency in value creation through order-based manufacturing has already had a positive effect on this area’s results.

asia and pacificPaLfinGer achieved strong growth in the area asia and Pacific – albeit at a low level – with revenue up by approximately 41 per cent in the first three quarters of 2011 compared to the same period in the previous year. in china, having established a value-creation site in shenzhen, PaLfinGer is now intensively developing further strategic options designed to significantly enhance growth potential in this area for the PaLfinGer Group.

conSolidated management report

12 palfinger interim report 2011

<< back forward >> search Print

indiain the area india, results for the first three quarters of 2011 were impacted by the start-up costs in-curred in connection with the new assembly site in chennai. the intensified market development efforts made since 2010 have already brought about a satisfactory improvement in incoming orders. the introduction of a telescopic crane adapted to local needs promises a consolidation of this trend. Local value creation at the site in chennai, as well as local procurement, will be continually expanded.

ciSthe area cis has benefited considerably from the local sales organization implemented in 2009. the number of PaLfinGer dealers on both sides of the Ural was increased to more than 50, and the search for additional local partners is progressing well. sales figures for both cranes and access platforms have developed satisfactorily.

with the takeover of the leading crane manufacturer inMan, PaLfinGer reached another major milestone in expanding its local presence through distribution and value-creation structures. More-over, a locally recognized product was added to the Group’s product portfolio through this acquisi-tion. this expansion step has contributed considerably to russia becoming one of the most impor-tant individual markets for the PaLfinGer Group in the future.

ventureS unit

the VentUres unit comprises all major strategic projects for the future pursued by the PaLfinGer Group up to operational maturity. as the projects included in the VentUres unit do not generate revenue, the costs of such projects are reported.

in the first three quarters of 2011, projects for the further development of the indian and asian areas as well as for potential acquisitions or partnerships in this connection were devised. the acquisition project inMan was successfully completed in the third quarter of 2011; potential growth steps in china remain one of the most pressing priorities. the result for this unit for the first three quarters of 2011 was –eUr 6.9 million compared to –eUr 5.2 million for the same period in the previous year and reflected the Group’s stepped-up activities.

conSolidated management report

13palfinger interim report 2011

<< back forward >> search Print

outlooK

after the global economic crisis of previous years, PaLfinGer observed a clear trend reversal as early as 2010. the Group managed to grasp market opportunities and emerged from the crisis even stronger than before in all sectors, having obtained significant benefits from the incipient market growth. this positive trend also continued into 2011, although during the third quarter uncertainty in the european markets increased once again, causing the economic mood to take a negative turn.

the consistent pursuit of internationalization is thus being continued. in recent years, the strategic decision to grow towards the bric countries has already proven its worth: some of the formerly large european markets still have not recovered completely from the global economic crisis of 2008. in contrast, markets which are still young for PaLfinGer are performing very well.

at the moment, the internationalization focus is on asia and russia, where, along with economic growth, the market potential of PaLfinGer is on the rise as well. in russia, PaLfinGer has already taken a major step with the acquisition of inMan. in china, another important future market, PaLfinGer has been promoting target-oriented strategic development to increase local value creation.

flexibility is an essential competitive advantage for PaLfinGer, particularly when market demand is not stable. switching to order-based procurement, manufacturing and assembly has enabled PaLfinGer to respond to order fluctuations quickly without locking up excessive capital by increas-ing inventories. PaLfinGer will therefore continue to consistently pursue the flexibility route in all fields. an extraordinary General Meeting held at the beginning of november 2011 thus passed resolutions enabling PaLfinGer to take corporate actions facilitating greater flexibility in funding further growth.

the growing diversity of the Group’s products, expansion through acquisition, as well as the promo-tion of internationalization all make it necessary to concentrate more on complexity management. PaLfinGer regards this as a substantial challenge for the future. stepping up activities and increas-ing resources in this field should help the Group to expand this significant competitive advantage in the future.

the current developments in the financial markets in europe are likely to have an impact on the real economy as well and thus also on the markets that are of relevance for PaLfinGer. neverthe-less, PaLfinGer is confident that a decline in performance will not reach the same dimensions as in 2008: the optimized cost structure, enhanced processes and above all the reduction of inventories at all value-creation stages – from suppliers to dealers – enables PaLfinGer to flexibly respond to changes in market demand.

against this backdrop, the management expects the defined target of 20 per cent organic growth to be achieved in 2011. in addition, the areas north and south america and the business units access Platforms and hookloaders are expected to make even more substantial contributions to earnings.

interim conSolidated financial StatementS

14 palfinger interim report 2011

<< back forward >> search Print

interim conSolidated financial StatementS aS of 30 September 2011

interim conSolidated financial StatementS

15palfinger interim report 2011

<< back forward >> search Print

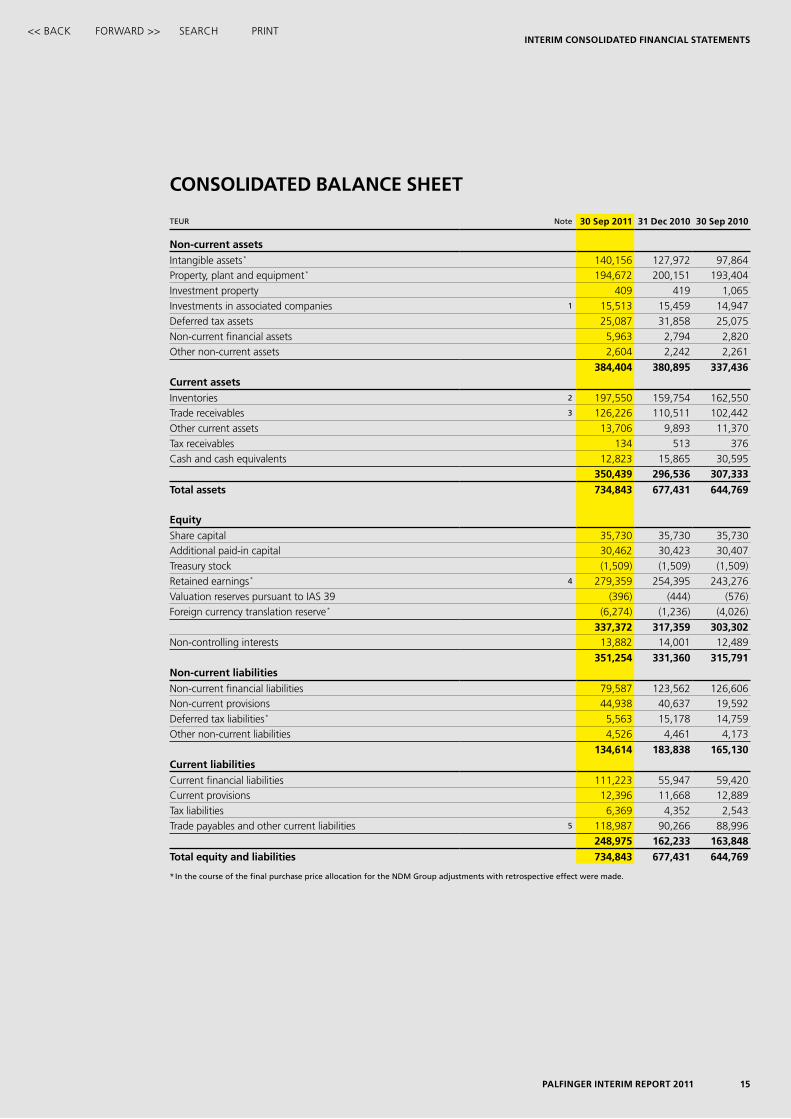

conSolidated balance Sheet

TEUR Note 30 Sep 2011 31 dec 2010 30 Sep 2010

non-current assets

intangible assets * 140,156 127,972 97,864Property, plant and equipment * 194,672 200,151 193,404investment property 409 419 1,065investments in associated companies 1 15,513 15,459 14,947deferred tax assets 25,087 31,858 25,075non-current financial assets 5,963 2,794 2,820other non-current assets 2,604 2,242 2,261

384,404 380,895 337,436current assets

inventories 2 197,550 159,754 162,550trade receivables 3 126,226 110,511 102,442other current assets 13,706 9,893 11,370tax receivables 134 513 376cash and cash equivalents 12,823 15,865 30,595

350,439 296,536 307,333

total assets 734,843 677,431 644,769

equity

share capital 35,730 35,730 35,730additional paid-in capital 30,462 30,423 30,407treasury stock (1,509) (1,509) (1,509)retained earnings * 4 279,359 254,395 243,276Valuation reserves pursuant to ias 39 (396) (444) (576)foreign currency translation reserve * (6,274) (1,236) (4,026)

337,372 317,359 303,302non-controlling interests 13,882 14,001 12,489

351,254 331,360 315,791non-current liabilities

non-current financial liabilities 79,587 123,562 126,606non-current provisions 44,938 40,637 19,592deferred tax liabilities * 5,563 15,178 14,759other non-current liabilities 4,526 4,461 4,173

134,614 183,838 165,130current liabilities

current financial liabilities 111,223 55,947 59,420current provisions 12,396 11,668 12,889tax liabilities 6,369 4,352 2,543trade payables and other current liabilities 5 118,987 90,266 88,996

248,975 162,233 163,848

total equity and liabilities 734,843 677,431 644,769

* In the course of the final purchase price allocation for the NDM Group adjustments with retrospective effect were made.

interim conSolidated financial StatementS

16 palfinger interim report 2011

<< back forward >> search Print

conSolidated income Statement 1)

TEUR NoteJuly–Sep

2011July–Sep

2010Jan–Sep

2011Jan–Sep

2010

revenue 209,732 167,514 624,002 464,916

changes in inventory 3,525 (3,509) 27,304 3,442own work capitalized 6 1,217 436 3,586 2,528other operating income 2,380 5,022 6,955 10,038Materials and external services (112,885) (87,640) (349,667) (247,343)employee benefits expenses (52,163) (43,144) (160,070) (128,762)depreciation, amortization and impairment expenses 2) 7 (6,948) (6,328) (21,094) (16,678)other operating expenses (29,457) (23,563) (84,226) (65,829)income from associated companies 1,049 330 5,652 1,352

earnings before interest and taxes – ebit 16,450 9,118 52,442 23,664

interest income 176 124 311 300interest expenses (2,889) (2,321) (8,471) (7,391)exchange rate differences (518) 552 (995) 2,778other financial result 0 (1) 0 22

net financial result (3,231) (1,646) (9,155) (4,291)

result before income tax 13,219 7,472 43,287 19,373income tax expense 2) (1,836) (2,277) (6,780) (5,818)

result after income tax 11,383 5,195 36,507 13,555

attributable to shareholders of palfinger ag (consolidated net result for the period) 10,090 4,440 32,661 11,711 non-controlling interests 1,293 755 3,846 1,844

EUR

earnings per share (undiluted and diluted) 4 0.29 0.13 0.92 0.33average number of shares outstanding 35,402,000 35,402,000 35,402,000 35,402,000

1) The statement’s structure was changed. for explanations go to “Changes in accounting and valuation methods” in the notes.

2) In the course of the final purchase price allocation for the NDM Group adjustments with retrospective effect were made.

interim conSolidated financial StatementS

17palfinger interim report 2011

<< back forward >> search Print

conSolidated Statement of comprehenSive income

TEURJuly–Sep

2011July–Sep

2010Jan–Sep

2011Jan–Sep

2010

result after income tax 11,383 5,195 36,507 13,555

Unrealized profits (+)/losses (–) from foreign currency translation * 557 (7,392) (5,093) 3,211

Unrealized profits (+)/losses (–) from cash flow hedge changes in unrealized profits (+)/losses (–) (210) 1,306 403 (828) deferred taxes thereon 176 65 (50) 85 effective taxes thereon 101 (407) (51) 111 realized profits (–)/losses (+) (44) 263 (343) 553 deferred taxes thereon 11 (43) 33 (43) effective taxes thereon 0 (20) 56 (91)

other comprehensive income 591 (6,228) (5,045) 2,998

total comprehensive income 11,974 (1,033) 31,462 16,553

attributable to shareholders of palfinger ag 10,417 (1,246) 27,762 14,759 non-controlling interests 1,557 213 3,700 1,794

* In the course of the final purchase price allocation for the NDM Group adjustments with retrospective effect were made.

19Palfinger interim rePort 201118 Palfinger interim rePort 2011

interim Consolidated finanCial statements interim Consolidated finanCial statements

Consolidated statement of Changes in equity

equity attributable to the shareholders of Palfinger ag equity attributable to the shareholders of Palfinger ag

TEUR Note share capitaladditional

paid-in capital treasury stockretainedearnings

Valuationreserves pursuant

to ias 39foreign currency

translation reserve totalnon-controlling

interests equity

as of 1 Jan 2010 35,730 30,363 (1,509) 231,453 (363) (7,287) 288,387 3,890 292,277

total comprehensive income Result after income tax * 0 0 0 11,711 0 0 11,711 1,844 13,555 Other comprehensive income Unrealized profits (+)/losses (–) from foreign currency translation * 0 0 0 0 0 3,261 3,261 (50) 3,211 Unrealized profits (+)/losses (–) from cash flow hedge 0 0 0 0 (213) 0 (213) 0 (213)

0 0 0 11,711 (213) 3,261 14,759 1,794 16,553transactions with shareholders Dividends 0 0 0 0 0 0 0 (1,085) (1,085) Changes in ownership interests in fully consolidated companies not resulting in a loss of control 0 0 0 113 0 0 113 (113) 0 Other changes 0 44 0 (1) 0 0 43 8,003 8,046

0 44 0 112 0 0 156 6,805 6,961

as of 30 sep 2010 35,730 30,407 (1,509) 243,276 (576) (4,026) 303,302 12,489 315,791

as of 1 Jan 2011 35,730 30,423 (1,509) 254,395 (444) (1,236) 317,359 14,001 331,360

total comprehensive income Result after income tax 0 0 0 32,661 0 0 32,661 3,846 36,507 Other comprehensive income Unrealized profits (+)/losses (–) from foreign currency translation 0 0 0 0 0 (4,947) (4,947) (146) (5,093) Unrealized profits (+)/losses (–) from cash flow hedge 0 0 0 0 48 0 48 0 48

0 0 0 32,661 48 (4,947) 27,762 3,700 31,462transactions with shareholders Dividends 4 0 0 0 (7,788) 0 0 (7,788) (3,811) (11,599) Other changes 0 39 0 91 0 (91) 39 (8) 31

0 39 0 (7,697) 0 (91) (7,749) (3,819) (11,568)

as of 30 sep 2011 35,730 30,462 (1,509) 279,359 (396) (6,274) 337,372 13,882 351,254

* In the course of the final purchase price allocation for the NDM Group adjustments with retrospective effect were made.

<< baCk fORwaRD >> seaRCh PRint

interim conSolidated financial StatementS

20 palfinger interim report 2011

<< back forward >> search Print

conSolidated Statement of caSh flowS

TEURJan–Sep

2011Jan–Sep

2010

result before income tax 43,287 19,373

cash flows from operating activities 30,711 32,887cash flows from investing activities (33,784) (30,752)cash flows from financing activities 244 (4,817)

total cash flows (2,829) (2,682)

free cash flows 3,509 6,844

TEUR 2011 2010

funds as of 1 Jan 15,865 33,073

effects of foreign exchange differences (213) 204total cash flows (2,829) (2,682)

funds as of 30 Sep 12,823 30,595

Segment reporting

revenue ebit

TEUR Jan–Sep2011

Jan–Sep2010

Jan–Sep2011

Jan–Sep2010 *

eUroPean Units 466,502 338,079 64,654 34,532area Units 157,500 126,837 (5,251) (5,679)VentUres – – (6,961) (5,189)

palfinger group 624,002 464,916 52,442 23,664

* In the course of the final purchase price allocation for the NDM Group adjustments with retrospective effect were made.

interim conSolidated financial StatementS

21palfinger interim report 2011

<< back forward >> search Print

noteS to the interim conSolidated financial StatementS

general

PaLfinGer aG is a publicly listed company headquartered in salzburg, austria. the main business activity is the production and sale of innovative lifting, loading and handling solutions.

reporting baSeS

these consolidated financial statements of PaLfinGer aG and its subsidiaries as of 30 september 2011 were prepared in line with ias 34. apart from the change regarding the structure of the consolidated income state-ment, which is explained below, the same accounting and valuation methods as those used in the consolidated financial statements for the financial year 2010 were applied when preparing these interim consolidated financial statements. the consolidated financial statements as of 31 december 2010 were prepared in line with the inter-national financial reporting standards (ifrs) valid at the reporting date and the relevant interpretations of the international financial reporting interpretations committee (ifric) to be applied within the european Union (eU). for further information on the individual accounting and valuation methods used, please refer to the consolidat-ed financial statements of PaLfinGer aG as of 31 december 2010.

the interim consolidated financial statements of PaLfinGer aG were reviewed by the Group’s auditor, ernst & Young wirtschaftsprüfungsgesellschaft m.b.h., salzburg, austria.

changeS in accounting and valuation methodS

PaLfinGer aG holds its associated companies for the exclusive purpose of supporting and optimizing the Group’s operating activities. one of the most important key performance indicators within PaLfinGer aG is “ebit plus income from associated companies”. these circumstances have now been taken into account, and the income statement has been adjusted accordingly by eliminating the subtotal “earnings before interest and taxes – ebit (before associated companies)” and instead inserting the subtotal “earnings before interest and taxes – ebit” after the item “income from associated companies”. the new structure has resulted in a clearer and more reliable presentation of the earnings situation of PaLfinGer aG.

no changes in accounting and valuation methods other than the one mentioned herein were made in 2011.

interim conSolidated financial StatementS

22 palfinger interim report 2011

<< back forward >> search Print

adJuStmentS made in the interim conSolidated financial StatementS

in the course of the final purchase price allocation for the ndM Group in the fourth quarter of 2010 the consoli-dated balance sheet as of 30 september 2010 was adjusted with retrospective effect as follows:

TEUR 30 Sep 2010 adjustment30 Sep 2010

adjusted

non-current assets intangible assets 98,109 (245) 97,864 Property, plant and equipment 192,601 803 193,404

equity retained earnings 243,289 (13) 243,276 foreign currency translation reserve (3,928) (98) (4,026)

non-current liabilities deferred tax liabilities 14,089 670 14,759

in the course of the final purchase price allocation for the ndM Group in the fourth quarter of 2010 the consoli-dated income statement as of 30 september 2010 was adjusted with retrospective effect as follows:

TEURJan–Sep

2010 adjustment

Jan–Sep2010

adjusted

depreciation, amortization and impairment expenses (16,623) (55) (16,678)other operating expenses (65,829) 0 (65,829)

earnings before interest and taxes – ebit 23,719 (55) 23,664result before income tax 19,428 (55) 19,373income tax expense (5,830) 12 (5,818)

result after income tax 13,597 (42) 13,555

attributable to shareholders of palfinger ag (consolidated net result for the period) 11,753 (42) 11,711 non-controlling interests 1,844 0 1,844

Scope of conSolidation

the following change in the corporate structure had no impact on the scope of consolidation:

the hamburg-based company schomäcker fahrzeugbau Gmbh, 100 per cent of which was taken over by Palfinger Gmbh, ainring, in the financial year 2010, was merged with Palfinger Gmbh, ainring, with effect from 1 January 2011.

interim conSolidated financial StatementS

23palfinger interim report 2011

<< back forward >> search Print

the following changes in the corporate structure had an impact on the scope of consolidation:

fully conSolidated companieSPalfinger Marine d.o.o., skrljevo, croatia, was merged into Palfinger Proizvodna tehnologija hrvatska d.o.o., delnice, croatia, as the absorbing company, as of 3 May 2011 in order to simplify the Group’s structure.

by articles of association dated 30 May 2011, Palfinger Marine- und beteiligungs-Gmbh, salzburg, founded the wholly-owned subsidiary Palfinger cis Gmbh, salzburg. the subsidiary was entered into the commercial regis-ter held at the Provincial court of salzburg acting as the commercial court on 17 June 2011. the company was founded to provide an optimized legal base for the progressing expansion in the cis countries.

the entry for Mbb Liftsystems Ltd. (in liquidation), cobham, Great britain, was finally deleted from the commercial register as of 29 June 2011.

aCqUIsITIoN of INMaNon 4 July 2011, PaLfinGer aG signed the contract for the takeover of the russian crane producer inMan (ischimbajskie neftianiye Manipuliatory, Jsc). the acquisition of 100 per cent of the shares in this company was closed on 26 august 2011.

with this acquisition, PaLfinGer aG is further expanding its business in russia. the company, which has its registered office in ishimbay in the republic of bashkortostan (Volga region), has been a producer and distributor of hydraulic lifting and loading systems, in particular knuckle boom cranes, since 1992.

aCqUIsITIoN of Ross & BoNNyMaN lTD. in 2010, the scottish access platform manufacturer ross & bonnyman decided to cease manufacture of commercial tail lifts. on 5 november 2010, ratcliff Palfinger Ltd. and ross & bonnyman signed a contract for the acquisition of the latter’s spare parts and service business. after having obtained the approval of the anti-trust authorities, the transaction was closed on 1 august 2011.

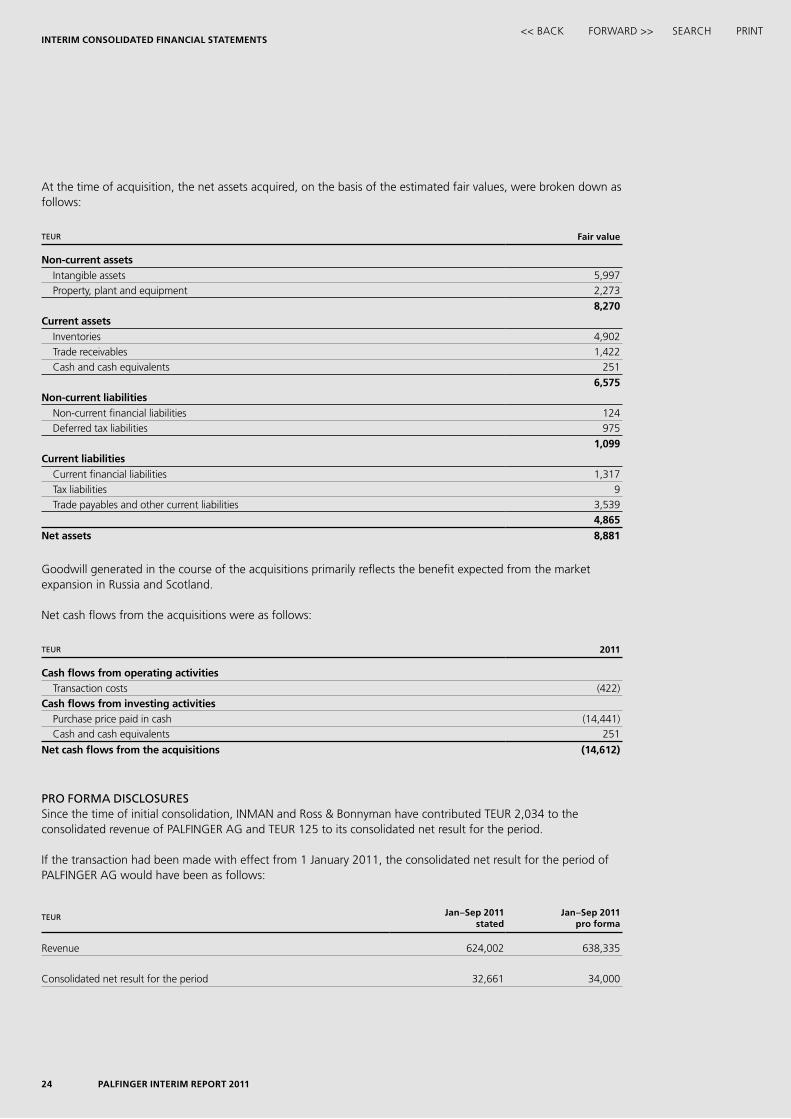

at the time of acquisition, the accumulated purchase price for both acquisitions was allocated on the basis of the estimated fair values as follows:

TEUR 2011

Purchase price paid in cash 14,441Portion of the purchase price not yet due 2,479

total purchase price 16,920

net assets (8,881)

goodwill 8,039

the goodwill generated cannot be used for tax purposes.

interim conSolidated financial StatementS

24 palfinger interim report 2011

<< back forward >> search Print

at the time of acquisition, the net assets acquired, on the basis of the estimated fair values, were broken down as follows:

TEUR fair value

non-current assets intangible assets 5,997 Property, plant and equipment 2,273

8,270current assets inventories 4,902 trade receivables 1,422 cash and cash equivalents 251

6,575non-current liabilities non-current financial liabilities 124 deferred tax liabilities 975

1,099current liabilities current financial liabilities 1,317 tax liabilities 9 trade payables and other current liabilities 3,539

4,865

net assets 8,881

Goodwill generated in the course of the acquisitions primarily reflects the benefit expected from the market expansion in russia and scotland.

net cash flows from the acquisitions were as follows:

TEUR 2011

cash flows from operating activities transaction costs (422)cash flows from investing activities Purchase price paid in cash (14,441) cash and cash equivalents 251

net cash flows from the acquisitions (14,612)

pRo foRMa DIsClosUREssince the time of initial consolidation, inMan and ross & bonnyman have contributed teUr 2,034 to the consolidated revenue of PaLfinGer aG and teUr 125 to its consolidated net result for the period.

if the transaction had been made with effect from 1 January 2011, the consolidated net result for the period of PaLfinGer aG would have been as follows:

TEUR Jan–Sep 2011stated

Jan–Sep 2011pro forma

revenue 624,002 638,335

consolidated net result for the period 32,661 34,000

interim conSolidated financial StatementS

25palfinger interim report 2011

<< back forward >> search Print

companieS conSolidated uSing the eQuity methodas of 1 april 2011, the remaining shares in Palfinger southern africa (Pty.) Ltd., amounting to 36 per cent, were sold to the former co-owners.

noteS to the conSolidated balance Sheet

(1) investments in associated companieschanges in investments in associated companies are shown in the following table:

TEUR 2011 2010

as of 1 Jan 15,459 15,726additions 0 1,026share in net result for the period 3,623 2,446dividends (1,906) (3,981)exchange rate differences (290) 242disposals (1,373) 0

as of 30 Sep/31 dec 15,513 15,459

(2) inventoriesinventories are broken down as follows:

TEUR 30 Sep 2011 31 dec 2010

Materials and production supplies 82,039 62,645work in progress 66,040 42,760finished goods and goods for resale 48,350 53,607Prepayments 1,121 742

total 197,550 159,754

(3) trade receivablestrade receivables include receivables from associated companies in the amount of teUr 7,036 (31 december 2010: teUr 4,991).

based on previous experience, an allowance for doubtful debts in the amount of teUr 6,751 (31 december 2010: teUr 6,972) was made to take insolvency risks into account.

(4) equitythe annual General Meeting held on 30 March 2011 approved a resolution for payment of a dividend in the amount of teUr 7,788 out of the 2010 profits. this dividend – paid to PaLfinGer aG shareholders on 5 april 2011 – was equivalent to a dividend of eUr 0.22 per share. no dividend was paid out for the previous year.

the amount of teUr 3,500 was paid to the non-controlling shareholders of ePsiLon kran Gmbh on 1 March 2011.

as in the previous year, shares outstanding amounted to 35,402,000.

on the basis of a consolidated net result for the period in the amount of teUr 32,661 (Jan–sep 2010: teUr 11,711), undiluted earnings per share were eUr 0.92 (Jan–sep 2010: eUr 0.33). due to the low dilution effect of the stock option programme, diluted earnings per share were identical to undiluted earnings per share.

interim conSolidated financial StatementS

26 palfinger interim report 2011

<< back forward >> search Print

(5) trade payables and other current liabilitiestrade payables and other current liabilities are broken down as follows:

TEUR 30 Sep 2011 31 dec 2010

trade payables 69,649 55,945Liabilities to associated companies 723 634Prepaid orders 9,318 5,153Liabilities on accepted bills of exchange 56 4Liabilities to employees 22,523 14,635Liabilities relating to social security and other taxes 11,101 9,902other liabilities 5,146 3,639deferred income 471 354

total 118,987 90,266

Liabilities to associated companies in the amount of teUr 723 (31 december 2010: teUr 634) resulted exclusively from the provision of goods and services (31 december 2010: teUr 631).

noteS to the conSolidated income Statement

(6) own work capitalizedown work capitalized resulted mainly from capitalized development expenditures from the divisions knuckle boom cranes, access platforms, services and railway as well as from local product developments in north america.

(7) depreciation on property, plant and equipmentdue to the relocation of departments, an impairment of buildings in the amount of teUr 1,603 was recorded.

related partieS

there were no substantial changes compared to 31 december 2010 with respect to business transactions with re-lated parties. all transactions with related parties are carried out at generally acceptable market conditions. Please refer to the consolidated financial statements of PaLfinGer aG as of 31 december 2010 for further information on individual business relations.

interim conSolidated financial StatementS

27palfinger interim report 2011

<< back forward >> search Print

StocK option programme

the stock option programmes which PaLfinGer aG has for members of its supervisory and Management boards are structured as follows:

herbertortner

christophKaml

wolfgangpilz

martinzehnder

alexanderexner

alexanderdoujak

number of stock options 40,000 40,000 25,000 25,000 25,000 25,000 25,000 25,000 10,000 0 15,000 15,000exercise price in eUr 10.12 10.12 16.57 16.57 10.12 10.12 10.12 10.12 10.12 10.12 10.12 10.12exercise period within12 weeks after the aGM 2012 2014 2013 2015 2012 2014 2012 2014 2012 2014 2012 2014

fair value of option in eUr as of valuation date * 2.58 2.56 4.73 5.77 2.58 2.56 2.58 2.56 2.58 2.56 2.58 2.56Underlying volatility 50.0% 40.0% 45.0% 45.0% 50.0% 40.0% 50.0% 40.0% 50.0% 40.0% 50.0% 40.0%Price in eUr as of valuation date 9.29 16.81 9.29 9.29 9.29 9.29

* valuation model used: Monte Carlo simulation

Please refer to the consolidated financial statements of PaLfinGer aG as of 31 december 2010 for further information on these stock option programmes.

changes in stock options were as follows:

Number of stock options 2011 2010

as of 1 Jan 300,000 250,000options granted 0 50,000options lapsed 30,000 0

as of 30 Sep/31 dec 270,000 300,000

alexander exner resigned from the supervisory board with effect from 30 March 2011. 30,000 of the stock options granted to him lapsed in connection with his resignation.

Key eventS after the reporting date

the extraordinary General Meeting held on 3 november 2011 resolved on an authorized capital in the amount of eUr 10 million, enabling PaLfinGer to issue up to 10 million new shares. Moreover, the Management board was authorized to buy back shares in the magnitude of up to 10 per cent of the share capital of the company.

report on the audit review

28 palfinger interim report 2011

<< back forward >> search Print

report on the audit review

introduction

we have reviewed the accompanying interim consolidated financial statements of PaLfinGer aG, salzburg, austria, for the nine-month period from 1 January 2011 to 30 september 2011. these in-terim consolidated financial statements comprise the consolidated balance sheet as of 30 september 2011, the consolidated income statement, consolidated statement of comprehensive income, consol-idated statement of cash flows and consolidated statement of changes in equity for the nine-month period then ended, and a summary of significant accounting policies and other explanatory notes.

the management is responsible for the preparation and fair presentation of this interim financial in-formation in accordance with international financial reporting standards (ifrs) as adopted by the eU.

our responsibility is to issue a conclusion on this interim financial information based on our review. our responsibility and liability in connection with the review and with reference to sec. 275 para. 2 of the business code (UGb) towards the company as well as third parties shall be limited to a total of eUr 12 million.

Scope of the audit review

we conducted our review in accordance with the statutory provisions and professional principles applicable in austria and in compliance with the international standard on review engagements 2410 “review of interim financial information Performed by the independent auditor of the entity”. this standard requires that we plan and perform the review to obtain moderate assurance as to whether the financial statements are free of material misstatement. a review is limited primarily to inquiries of company personnel and analytical procedure applied to financial data and thus provides less assurance than an audit. we have not performed an audit and, accordingly, we do not express an audit opinion.

concluSion

based on our review, nothing has come to our attention that causes us to believe that the accompa-nying interim financial information does not give a true and fair view of the financial position of the Group as of 30 september 2011, and of its financial performance and its cash flows for the nine-month period then ended in accordance with the international financial reporting standards (ifrs) as adopted by the eU.

report on the audit review

29palfinger interim report 2011

<< back forward >> search Print

report on the interim conSolidated management report

we are required to perform review procedures to check whether the interim consolidated manage-ment report is consistent with the interim consolidated financial statements and whether the other disclosures made in the interim consolidated management report do not give rise to misconception of the position of the Group.

based on our review, nothing has come to our attention that causes us to believe that the interim consolidated management report for the Group is not consistent with the interim consolidated financial statements.

salzburg, 3 november 2011

ernst & Youngwirtschaftsprüfungsgesellschaft m.b.h.

anna flotzinger m.p. christoph fröhlich m.p.chartered accountant chartered accountant

inveStor relationS

30 palfinger interim report 2011

<< back forward >> search Print

Shareholder information

Q1–Q3 2011

international securities identification number (isin) at0000758305number of shares 35,730,000 of which own shares 328,000Price as of 30 september 2011 eUr 15.91earnings per share (Q1–Q3 2011) eUr 0.92Market capitalization as of 30 september 2011 teUr 568,464.3

Share price development

110%

100%

90%

80%

70%

60%

50%

40%3 Jan 2011 31 March 2011 30 June 2011 30 sep 2011 31 oct 2011

PALFINGER AG

ATX

inveStor relationS

31palfinger interim report 2011

<< back forward >> search Print

inveStor relationS

hannes roitherPhone +43 662 4684-2260, [email protected]

claudia rendlPhone +43 662 4684-2261, [email protected]

fax +43 662 4684-2280www.palfinger.com

financial calendar *

8 february 2012 balance sheet press conference16 february 2012 Publication of annual report 2011 8 March 2012 annual General Meeting12 March 2012 ex-dividend day14 March 2012 dividend payment day10 May 2012 Publication of results for the first quarter of 2012 9 august 2012 Publication of results for the first half of 2012 9 november 2012 Publication of results for the first three quarters of 2012

* Due to the new structure of the financial calendar, no preliminary results will be published in January.

printed onarctic Volume

Minimal arithmetical differences may result from the application of commercial rounding to individual items and percentages in this

interim report. The English translation of this palfINGER report is provided for convenience only. only the German text is binding.

This report contains forward-looking statements made on the basis of all information available at the time of preparation of this report.

forward-looking statements are usually identified by the use of terminology such as “expect”, “plan”, “estimate”, “believe”, etc. actual

outcomes and results may be substantially different from those predicted.

published on 10 November 2011.

No liability is assumed for typographical or printing errors.

www.palfinger.com

palfinger agfranz-wolfram-Scherer-StraSSe 24 5020 SalzburgauStria