revenue recognition webinar-may 19th, 2015

TRANSCRIPT

Compliance Made Simple ™

Revenue Recognition

Internal Control Considerations

2015

Presented by:

Sonia Luna, CPA, CIA

2Compliance Made Simple ™

House Keeping Items

• GREEN BUTTON – CPE CREDIT• Q&A = Chat box• Polling Questions MUST = CPE CREDIT• COSO Implementation MEMBERS = MUST

FOR CPE– See LinkedIN invitation today/tomorrow

• Recording will be available in 2 weeks

3Compliance Made Simple ™

Today’s Presenters

Sonia Luna, CEO, Aviva Spectrum– CONNECT: www.linkedin.com/in/sonialuna– EMAIL: [email protected] – PHONE: (213) 250-5700

Larry Stewart, VP, Information Security / IT Compliance at PennyMac

– CONNECT: www.linkedin.com/in/larrystewart– EMAIL: [email protected]– PHONE: (805) 358-0016

Luis Puncel, President, Puncel Consulting Associates– CONNECT: www.linkedin.com/in/luispuncel – EMAIL: [email protected] – PHONE: (949) 466-1368

Revenue Recognition Controls

4Compliance Made Simple ™

Agenda

• Revenue Rec. internal control updates– Overview– SEC/PCAOB Point of views

• IT CONTROL Considerations

• Revenue Rec. the basics of adoption

5Compliance Made Simple ™

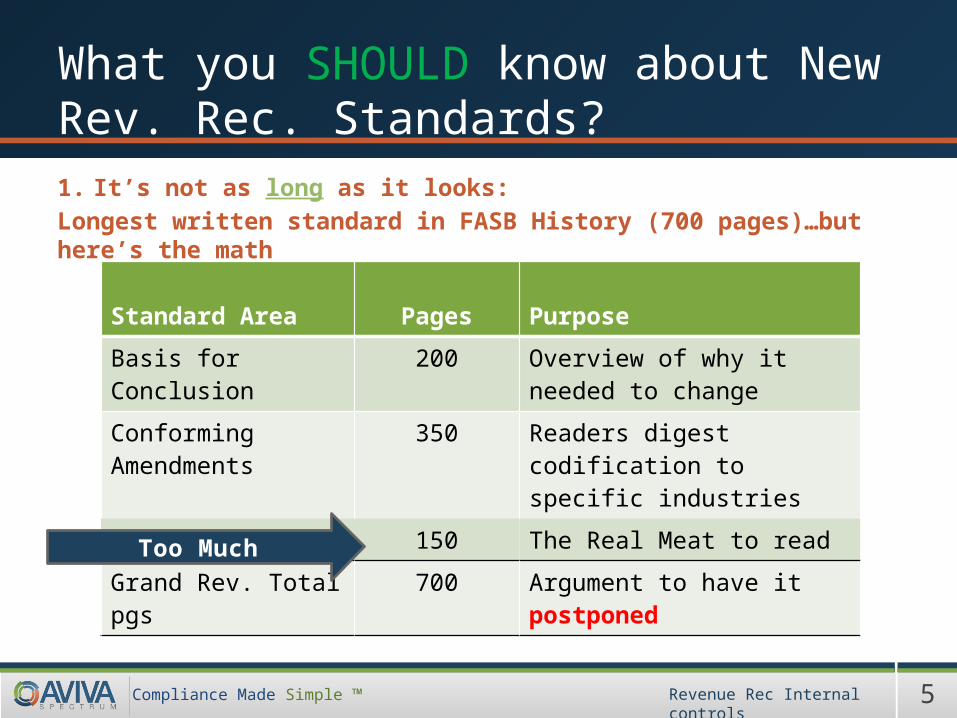

What you SHOULD know about New Rev. Rec. Standards?1. It’s not as long as it looks: Longest written standard in FASB History (700 pages)…but here’s the math

Revenue Rec Internal controls

Standard Area Pages Purpose

Basis for Conclusion 200 Overview of why it needed to change

Conforming Amendments

350 Readers digest codification to specific industries

Actual Guidance 150 The Real Meat to read

Grand Rev. Total pgs 700 Argument to have it postponedToo Much

6Compliance Made Simple ™

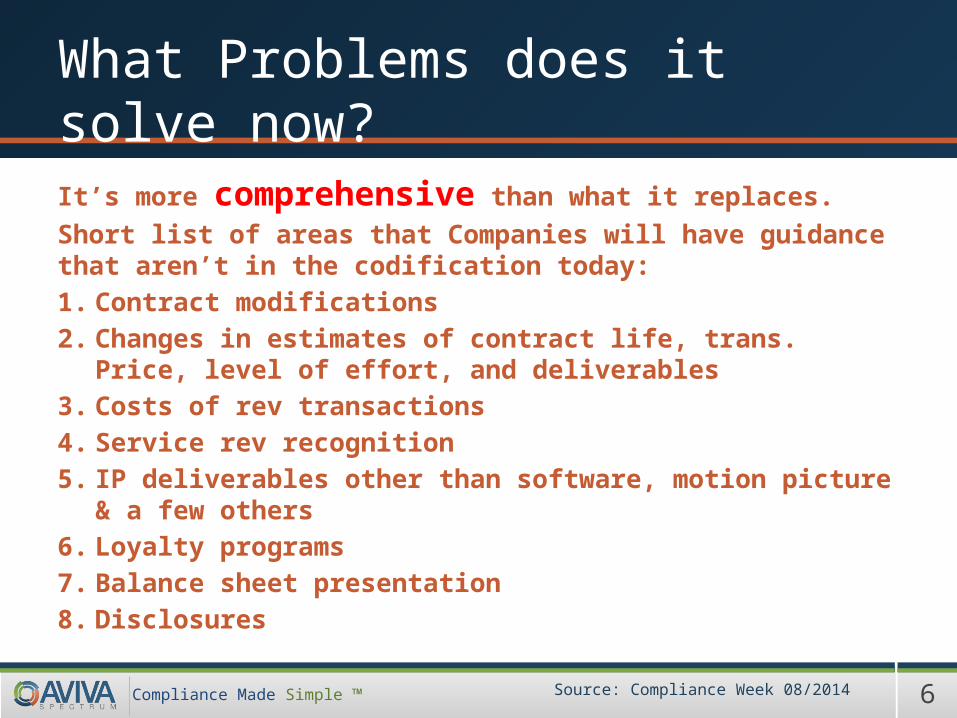

What Problems does it solve now?It’s more comprehensive than what it replaces.Short list of areas that Companies will have guidance that aren’t in the codification today:1. Contract modifications2. Changes in estimates of contract life, trans. Price,

level of effort, and deliverables3. Costs of rev transactions4. Service rev recognition5. IP deliverables other than software, motion picture

& a few others6. Loyalty programs7. Balance sheet presentation8. Disclosures

Source: Compliance Week 08/2014

7Compliance Made Simple ™

Polling: Disclosure Change Question

How many are implementing new revenue rec footnotes this 2016?

Revenue Rec Internal Controls

8Compliance Made Simple ™

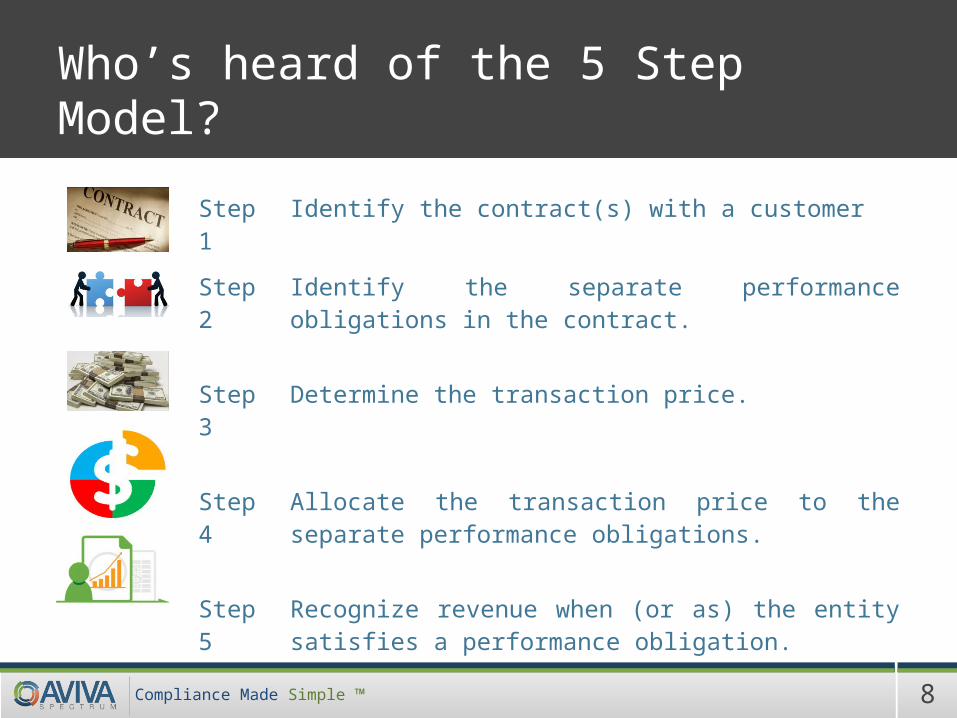

Who’s heard of the 5 Step Model?

Step 1

Identify the contract(s) with a customer

Step 2

Identify the separate performance obligations in the contract.

Step 3

Determine the transaction price.

Step 4

Allocate the transaction price to the separate performance obligations.

Step 5

Recognize revenue when (or as) the entity satisfies a performance obligation.

9Compliance Made Simple ™

Polling Question?

Who’s on Step 1 = Contract Identification (Yes/No)?

Revenue Rec Internal Controls

10Compliance Made Simple ™

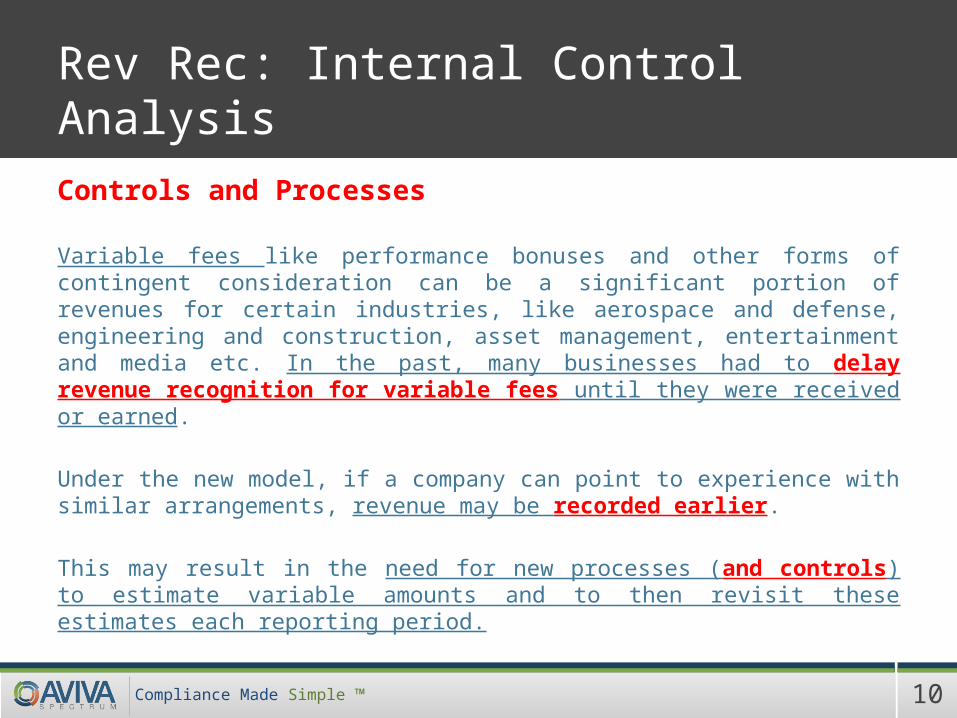

Rev Rec: Internal Control Analysis

Controls and Processes

Variable fees like performance bonuses and other forms of contingent consideration can be a significant portion of revenues for certain industries, like aerospace and defense, engineering and construction, asset management, entertainment and media etc. In the past, many businesses had to delay revenue recognition for variable fees until they were received or earned.

Under the new model, if a company can point to experience with similar arrangements, revenue may be recorded earlier.

This may result in the need for new processes (and controls) to estimate variable amounts and to then revisit these estimates each reporting period.

11Compliance Made Simple ™

Footnote Options: Internal Controls

Revenue Rec Internal Controls

Who’s Retro?Who’s Modified?

12Compliance Made Simple ™

Case of wrong footnotes

Kenote Systems• Initial IMPACT Year = FYE: 09/30/2011• Keynote offers service for planning, testing and monitoring

the functionality, usability, performance and availability of mobile apps and websites.

13Compliance Made Simple ™

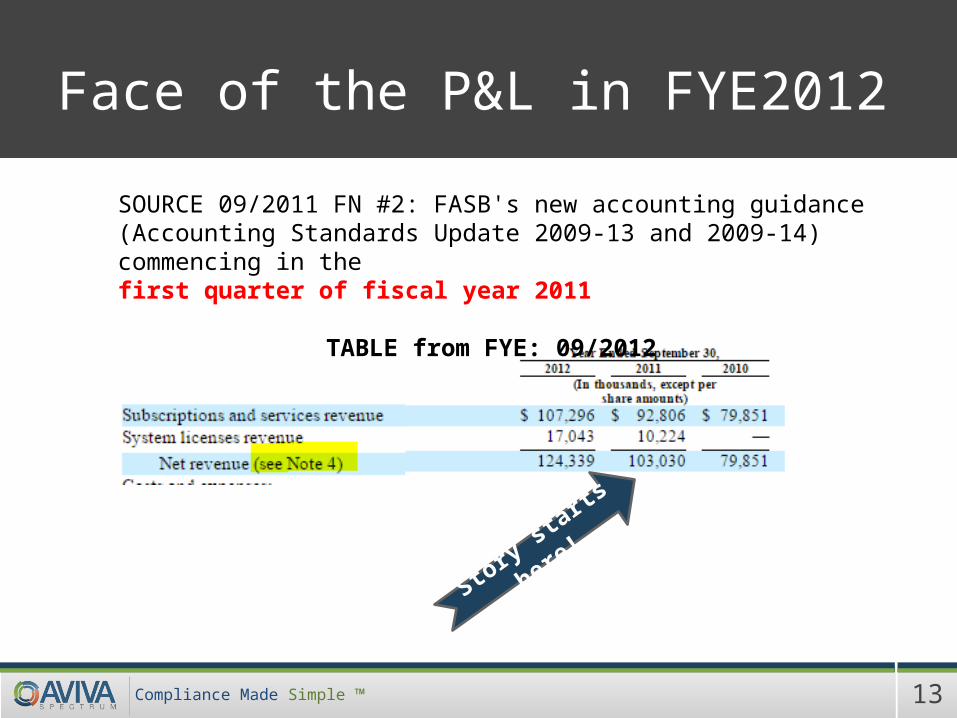

Face of the P&L in FYE2012

SOURCE 09/2011 FN #2: FASB's new accounting guidance (Accounting Standards Update 2009-13 and 2009-14) commencing in thefirst quarter of fiscal year 2011

TABLE from FYE: 09/2012

Story starts

here!

14Compliance Made Simple ™

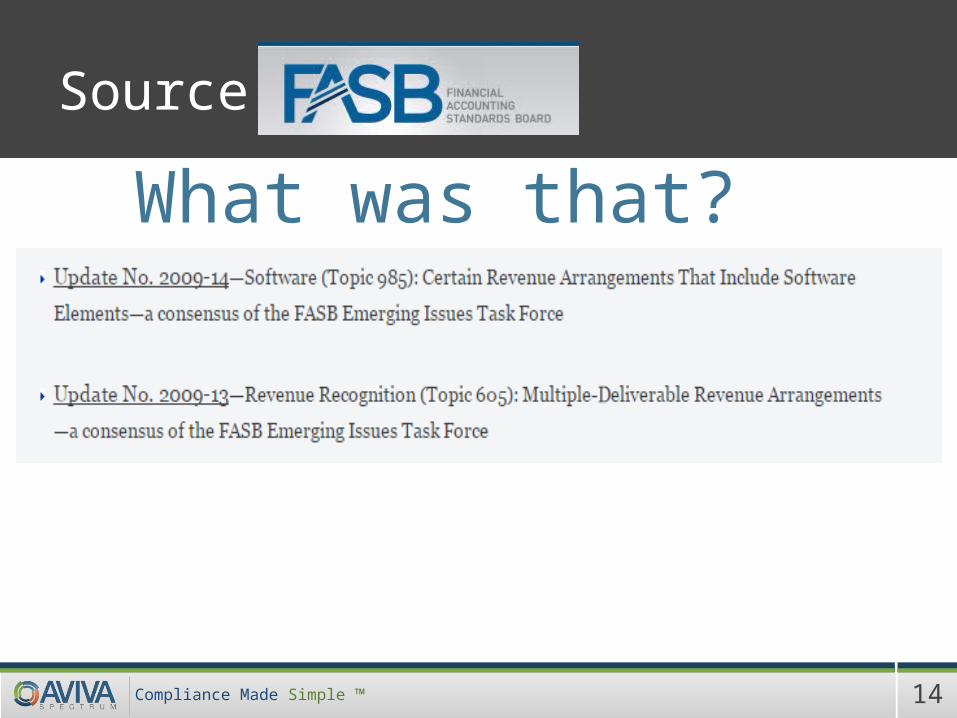

Source: FASB

What was that?

15Compliance Made Simple ™

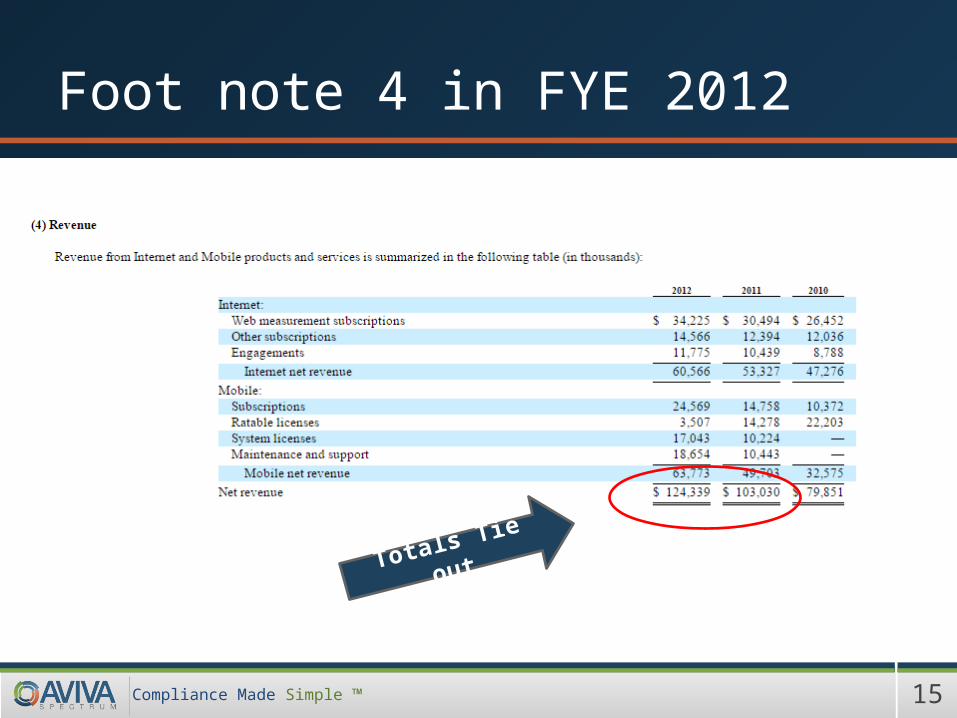

Foot note 4 in FYE 2012

Totals Tie out

16Compliance Made Simple ™

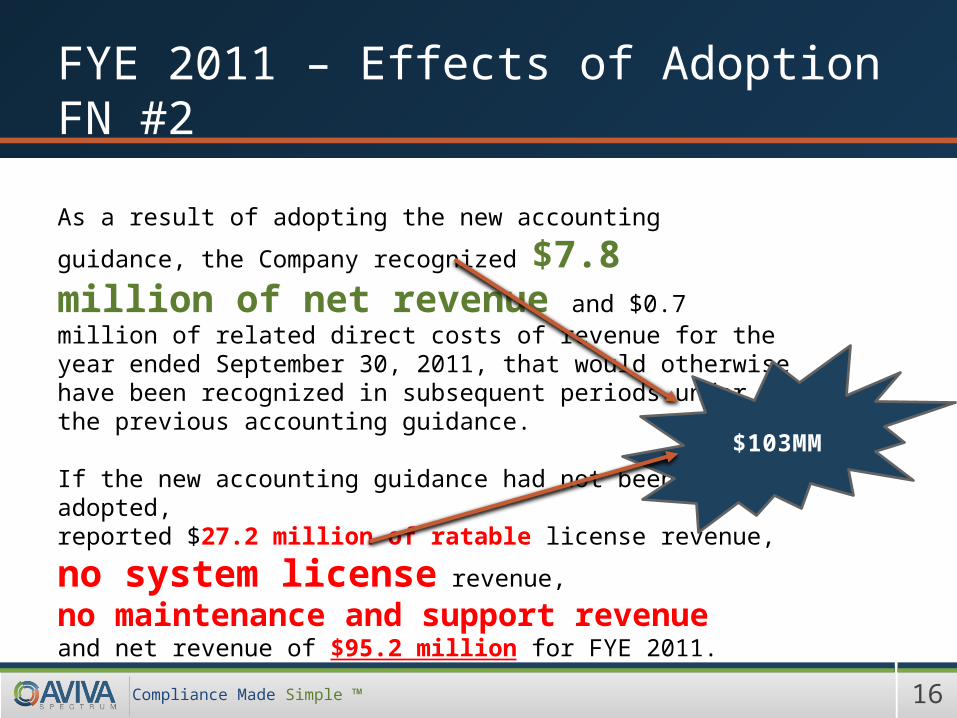

FYE 2011 – Effects of Adoption FN #2

As a result of adopting the new accounting guidance, the Company

recognized $7.8 million of net revenue and $0.7 million of related direct costs of revenue for the year ended September 30, 2011, that would otherwise have been recognized in subsequent periods under the previous accounting guidance.

If the new accounting guidance had not been adopted, reported $27.2 million of ratable license revenue,

no system license revenue,

no maintenance and support revenue and net revenue of $95.2 million for FYE 2011.

$103MM

17Compliance Made Simple ™

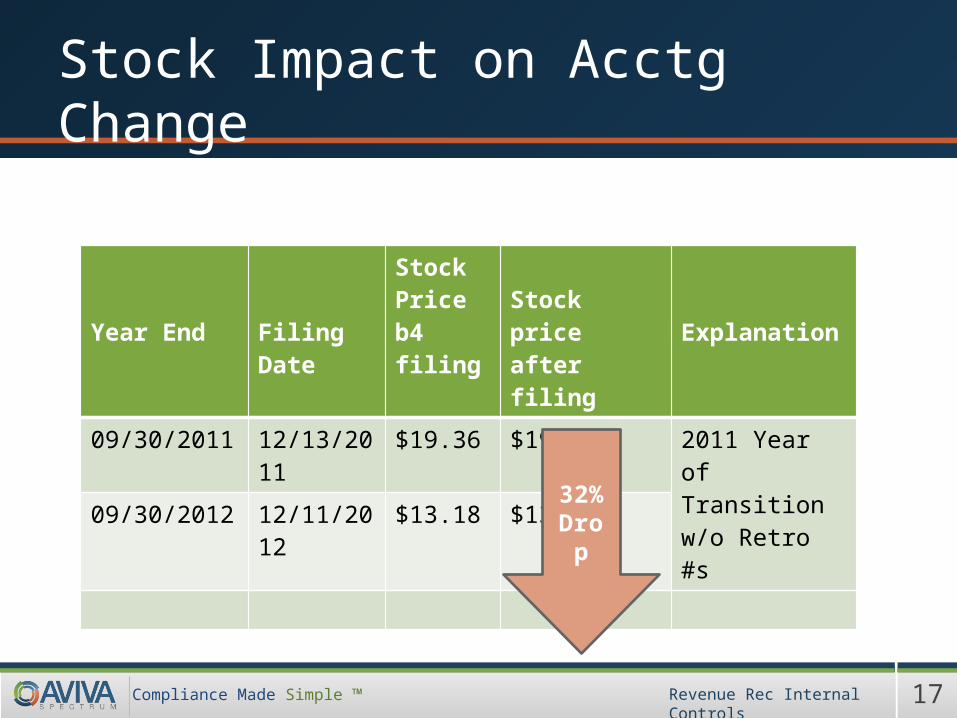

Stock Impact on Acctg Change

Revenue Rec Internal Controls

Year End Filing Date

Stock Price b4 filing

Stock price after filing Explanation

09/30/2011 12/13/2011 $19.36 $19.54 2011 Year of Transition w/o Retro #s 09/30/2012 12/11/2012 $13.18 $13.34

32%Drop

18Compliance Made Simple ™

Stock Price – graph AFTER 10K 2011

Pop is GONE!

19Compliance Made Simple ™

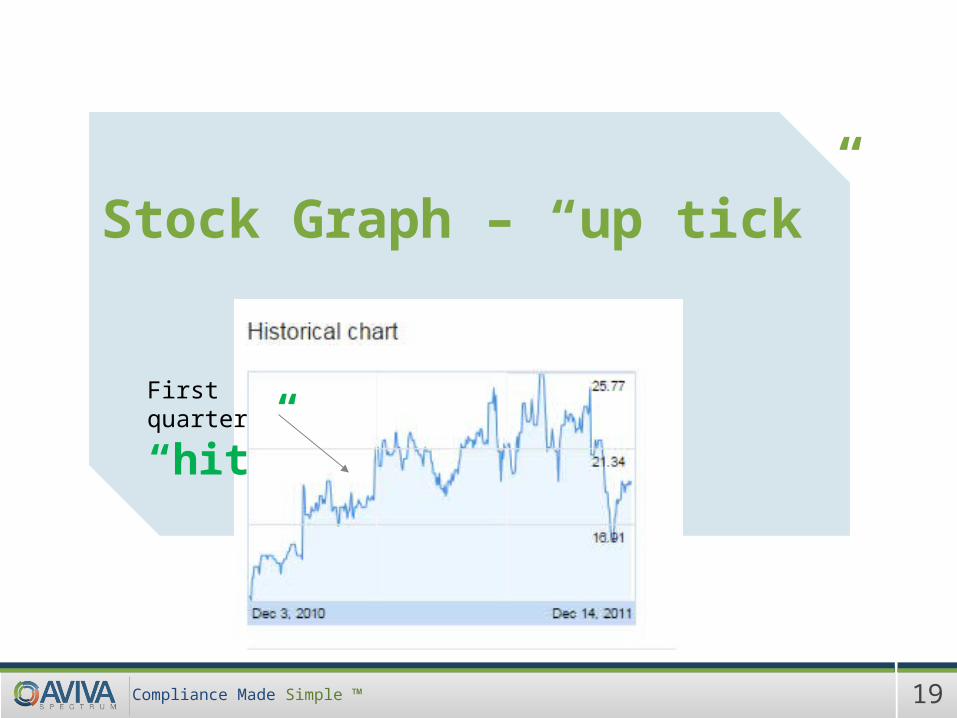

Stock Graph – “up tick”

First quarter

“hit”

20Compliance Made Simple ™

• Analysts didn’t read and understand 2011 FN!

• Analysts are people too, sometimes VERY YOUNG people

• Other factors came to play!

Market Reactions

21Compliance Made Simple ™

What Caused Keynote’s Stock Drop?

Polling Question

Revenue Rec Internal Controls

22Compliance Made Simple ™

REGULATORS

23Compliance Made Simple ™

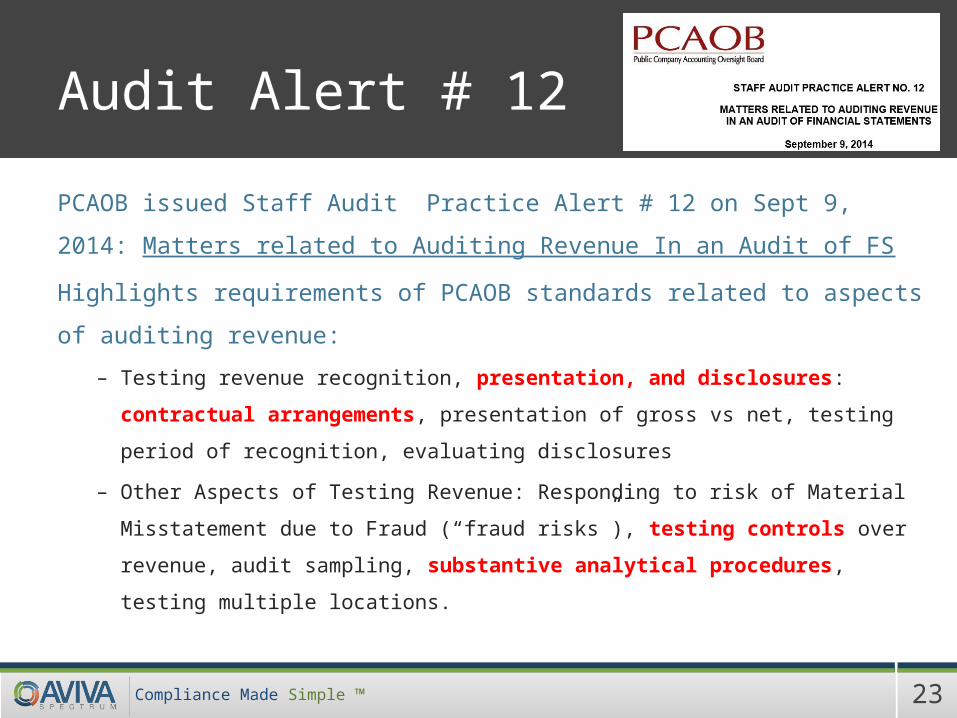

Audit Alert # 12

PCAOB issued Staff Audit Practice Alert # 12 on Sept 9, 2014: Matters

related to Auditing Revenue In an Audit of FS

Highlights requirements of PCAOB standards related to aspects of

auditing revenue:

– Testing revenue recognition, presentation, and disclosures:

contractual arrangements, presentation of gross vs net, testing period

of recognition, evaluating disclosures

– Other Aspects of Testing Revenue: Responding to risk of Material

Misstatement due to Fraud (“fraud risks”), testing controls over

revenue, audit sampling, substantive analytical procedures, testing

multiple locations.

24Compliance Made Simple ™

PCAOB’s Revenue Concerns

• Examples–DATA–Key CONTROL TESTING on COMPLETENESS of arrangements

25Compliance Made Simple ™

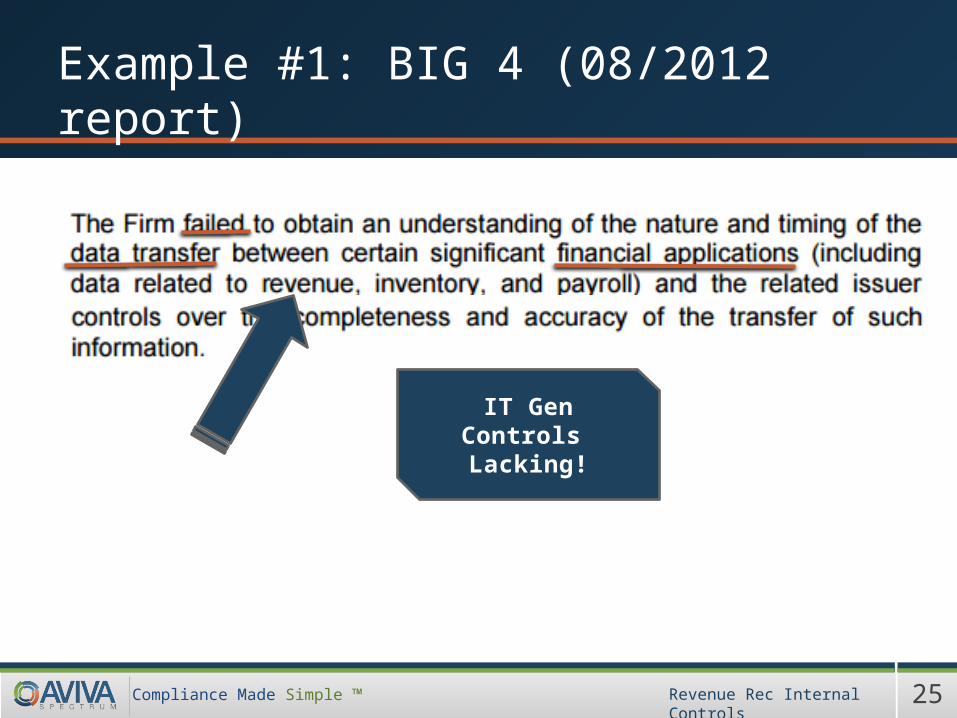

Example #1: BIG 4 (08/2012 report)

Revenue Rec Internal Controls

IT Gen Controls Lacking!

26Compliance Made Simple ™

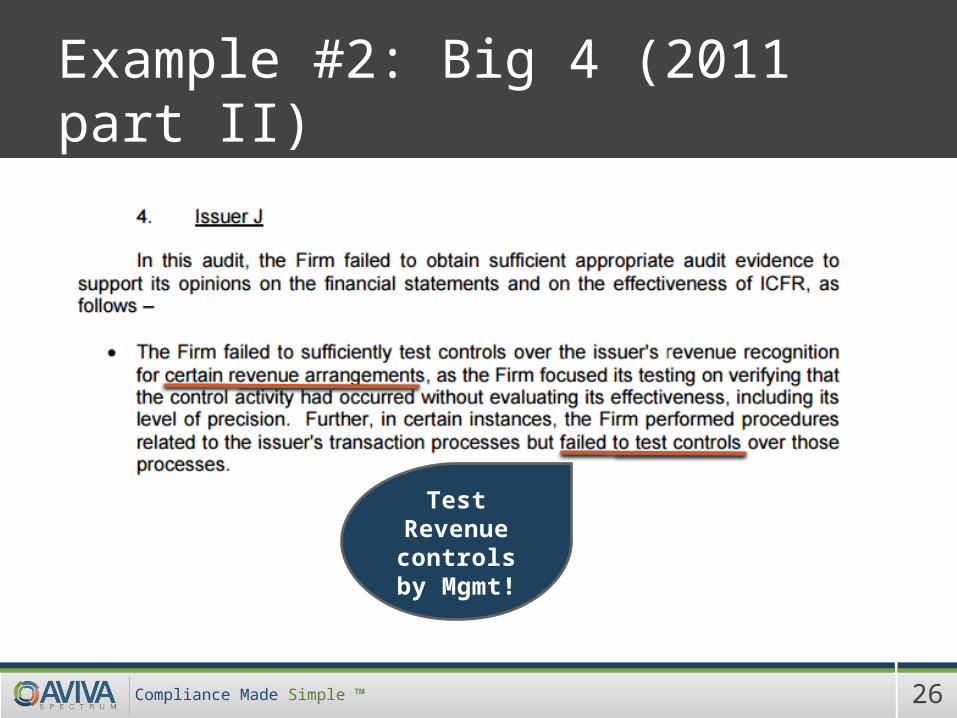

Example #2: Big 4 (2011 part II)

Test Revenue controls by

Mgmt!

27Compliance Made Simple ™

COSO Implementation MEMBERS ONLY!

5 Steps

5 Questions

RiskScore

25 minutes

28Compliance Made Simple ™

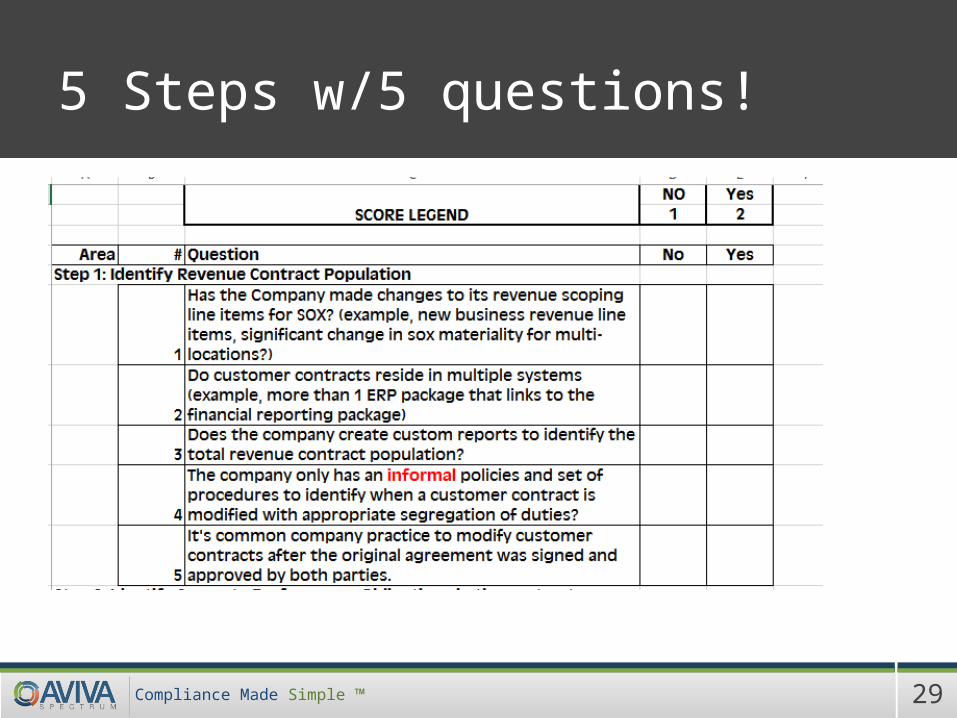

Internal Control Revenue RISKS!

29Compliance Made Simple ™

5 Steps w/5 questions!

30Compliance Made Simple ™

Control Compliance Analysis

Revenue Rec Internal Controls

REVENUE IC RISK STANDARDS

1. Top Transition Failures (Restatement Issues)2. Audit Evidence required3. Priority Driven by the 5 Steps 4. Latest PCAOB Internal Control Standards

[email protected]: CCA Reservation 2

31Compliance Made Simple ™

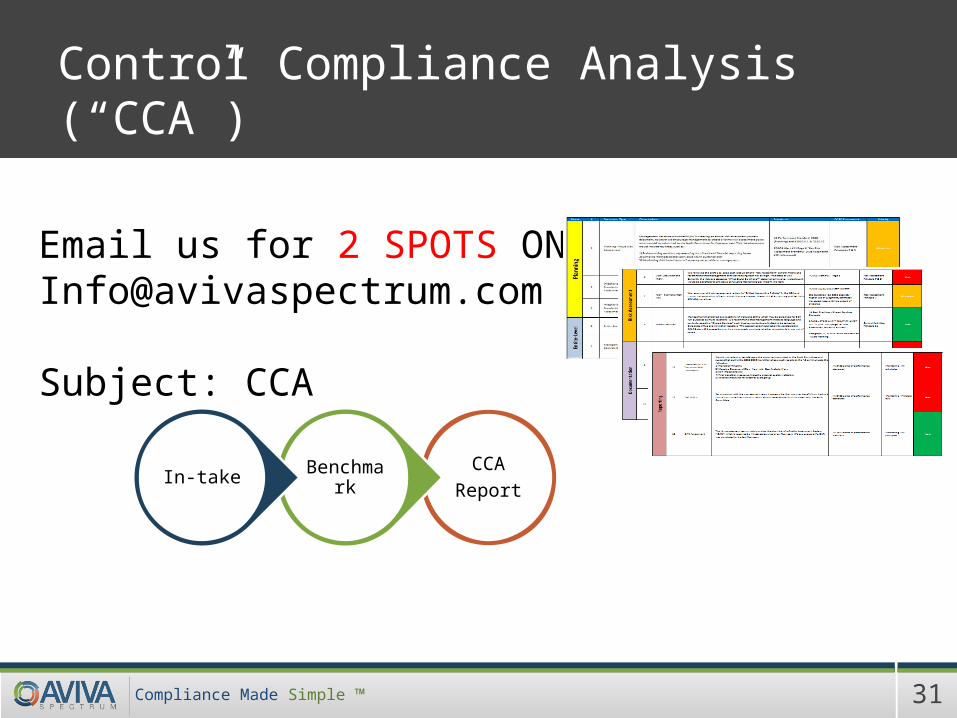

Control Compliance Analysis (“CCA”)

Email us for 2 SPOTS ONLY: [email protected]

Subject: CCA

CCAReport

BenchmarkIn-take

32Compliance Made Simple ™

Q & A session (5 – 8 Min)

CONNECT: www.linkedin.com/in/sonialunaSLIDES: www.slideshare.net/soxppt VIDEOS: http://avivaspectrum.com/webcasts

Compliance Made Simple

What IT auditors and Finance folks keep missing?

Presented By:

Larry Stewart

IT Control Considerations

TM

34Compliance Made Simple ™ Revenue Recognition and Internal Controls

Presenter:

Larry Stewart

TM

35Compliance Made Simple ™ Revenue Recognition and Internal Controls

What are the IT control considerations for the New Revenue

Recognition Standard

TM

36Compliance Made Simple ™ Revenue Recognition and Internal Controls

What is the core principle of the new standard

Recognized revenue to detect the transfer of promised goods or services to customers in an amount that reflects the consideration to

which the entity expects to be entitled in exchange for those goods or services.

TM

37Compliance Made Simple ™

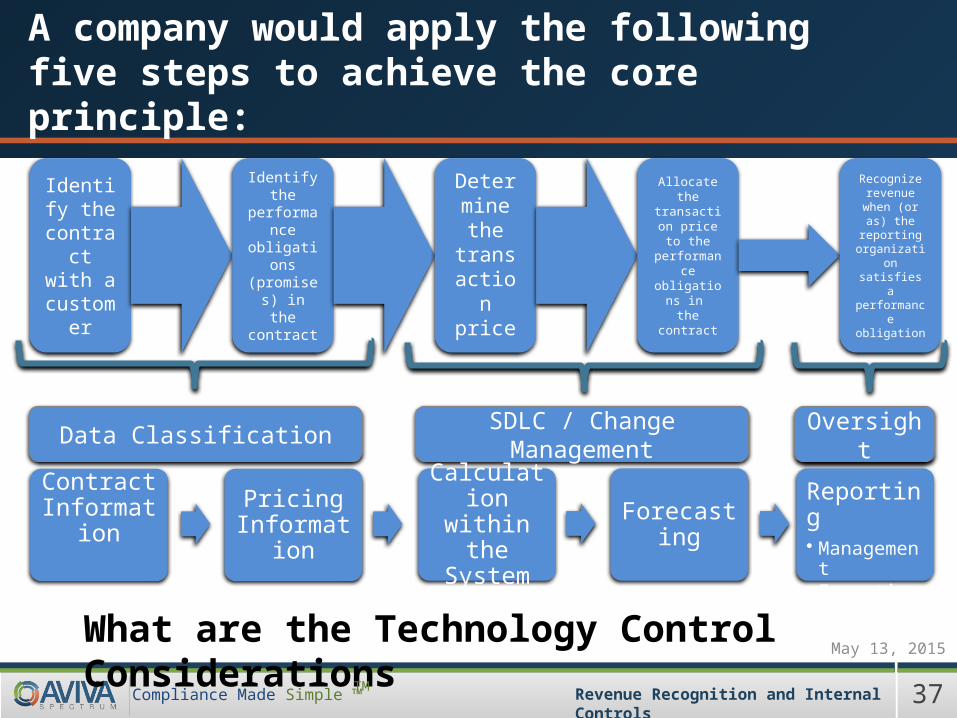

A company would apply the following five steps to achieve the core principle:

Revenue Recognition and Internal Controls

Identify the

contract with a custom

er

Identify the

performance

obligations

(promises) in the

contract

Determine the

transaction price

Allocate the

transaction price to the performan

ce obligations

in the contract

Recognize revenue when (or

as) the reporting

organization satisfies a performance obligation

Data Classification

Contract Information Pricing

Information

SDLC / Change Management

Calculation within the

SystemForecasting

Oversight

Reporting• Management• Exception

What are the Technology Control ConsiderationsMay 13, 2015

TM

38Compliance Made Simple ™ Revenue Recognition and Internal Controls

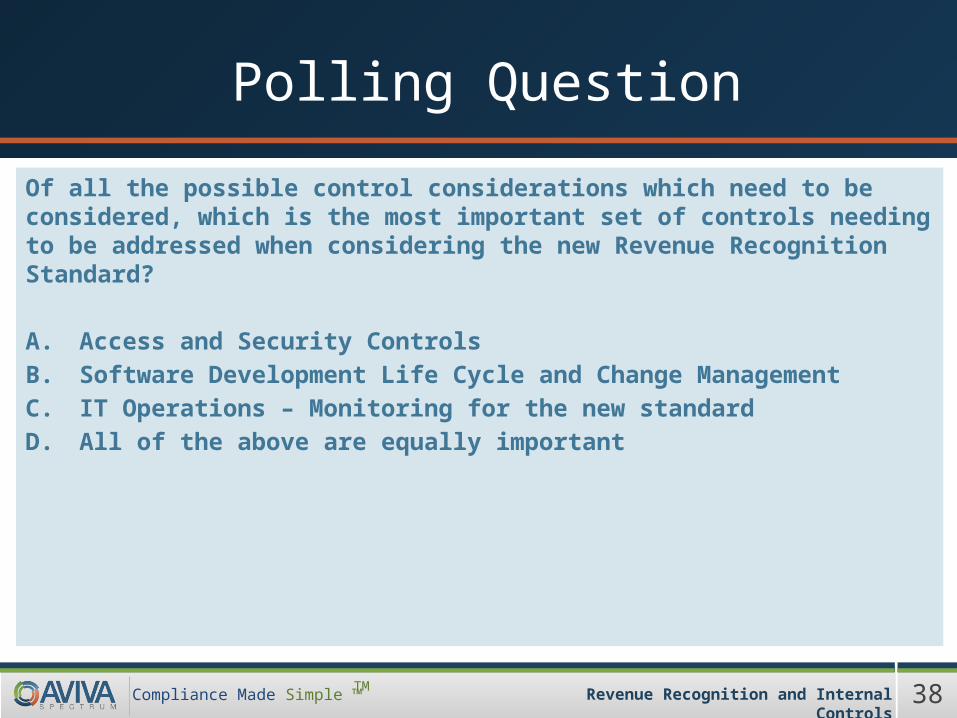

Polling Question

Of all the possible control considerations which need to be considered, which is the most important set of controls needing to be addressed when considering the new Revenue Recognition Standard?

A. Access and Security ControlsB. Software Development Life Cycle and Change ManagementC. IT Operations – Monitoring for the new standardD. All of the above are equally important

TM

39Compliance Made Simple ™ Revenue Recognition and Internal Controls

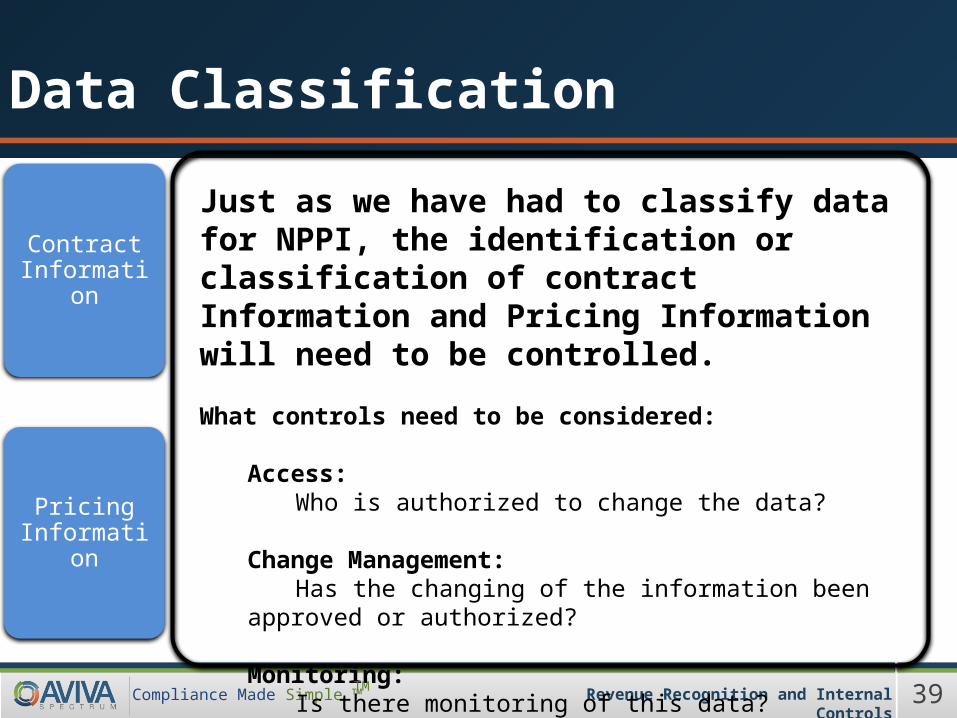

Data Classification

Just as we have had to classify data for NPPI, the identification or classification of contract Information and Pricing Information will need to be controlled.

What controls need to be considered:

Access:Who is authorized to change the data?

Change Management:Has the changing of the information been approved or

authorized?

Monitoring:Is there monitoring of this data?

Contract Information

Pricing Information

TM

40Compliance Made Simple ™ Revenue Recognition and Internal Controls

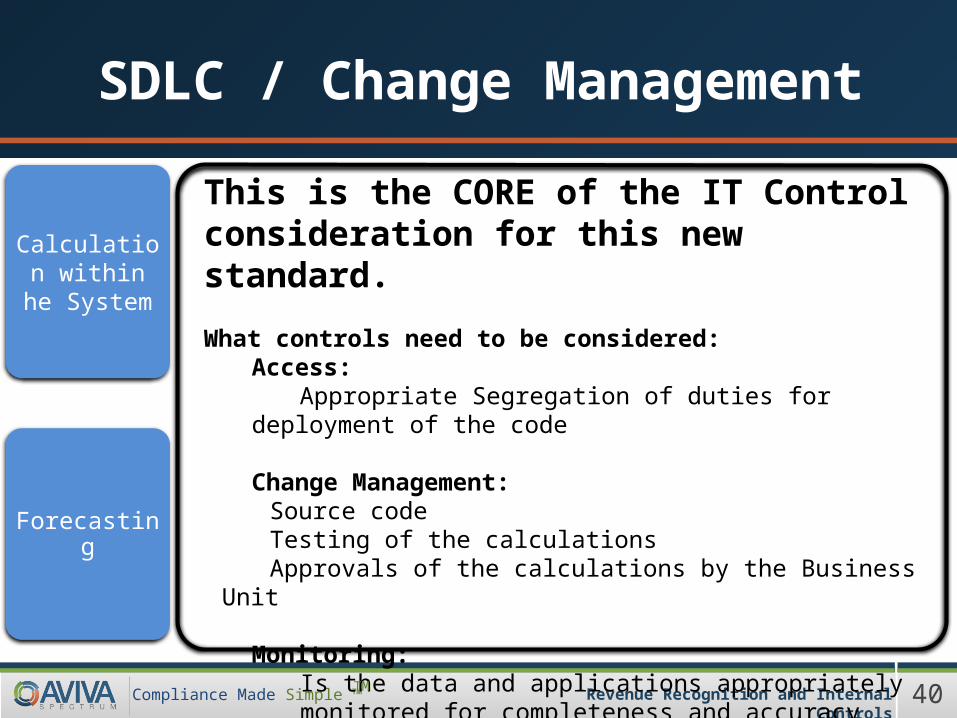

SDLC / Change Management

This is the CORE of the IT Control consideration for this new standard.

What controls need to be considered:Access:

Appropriate Segregation of duties for deployment of the code

Change Management:Source codeTesting of the calculationsApprovals of the calculations by the Business Unit

Monitoring:Is the data and applications appropriately monitored for completeness and accuracy

Calculation within he System

Forecasting

TM

41Compliance Made Simple ™ Revenue Recognition and Internal Controls

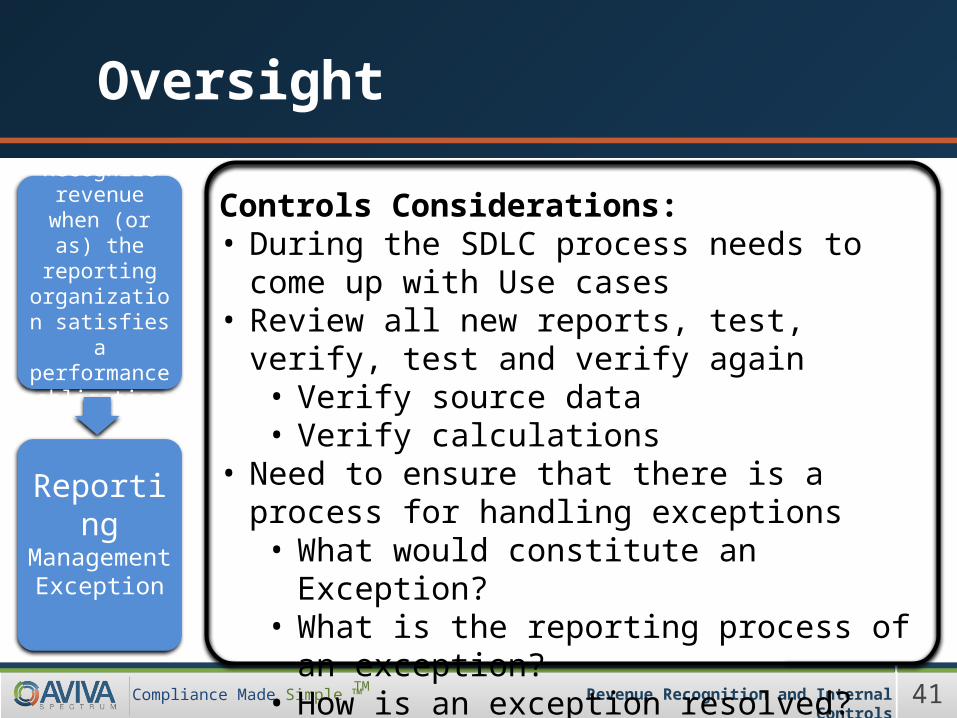

Oversight

Controls Considerations:• During the SDLC process needs to come up with Use

cases• Review all new reports, test, verify, test and verify

again• Verify source data• Verify calculations

• Need to ensure that there is a process for handling exceptions

• What would constitute an Exception?• What is the reporting process of an exception?• How is an exception resolved?

Recognize revenue when

(or as) the reporting

organization satisfies a

performance obligation

ReportingManagement

Exception

TM

42Compliance Made Simple ™ Revenue Recognition and Internal Controls

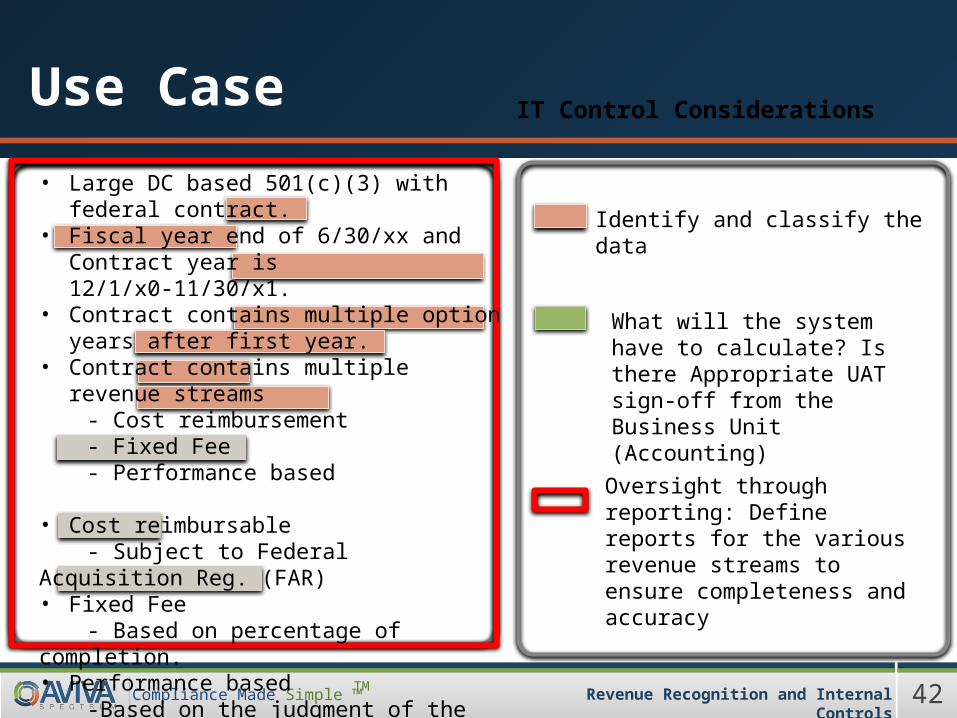

Use Case IT Control Considerations

Identify and classify the data

What will the system have to calculate? Is there Appropriate UAT sign-off from the Business Unit (Accounting)

Oversight through reporting: Define reports for the various revenue streams to ensure completeness and accuracy

• Large DC based 501(c)(3) with federal contract.• Fiscal year end of 6/30/xx and Contract year is

12/1/x0-11/30/x1.• Contract contains multiple option years after first

year.• Contract contains multiple revenue streams

- Cost reimbursement- Fixed Fee- Performance based

• Cost reimbursable- Subject to Federal Acquisition Reg. (FAR)

• Fixed Fee- Based on percentage of completion.

• Performance based-Based on the judgment of the agency.

TM

43Compliance Made Simple ™ Revenue Recognition and Internal Controls

Conclusion

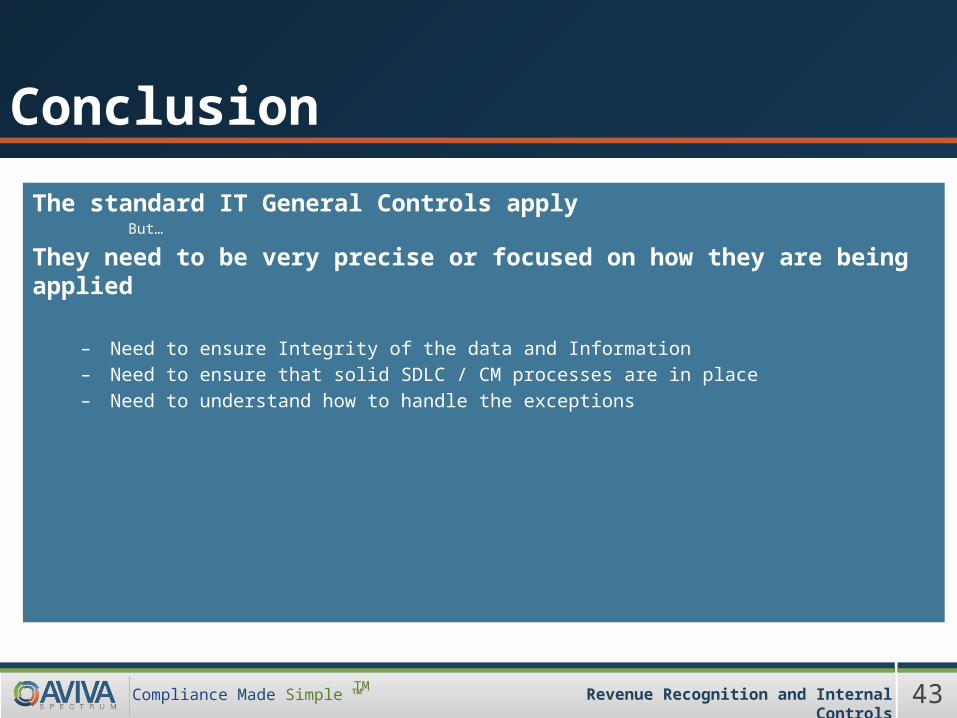

The standard IT General Controls applyBut…

They need to be very precise or focused on how they are being applied

– Need to ensure Integrity of the data and Information– Need to ensure that solid SDLC / CM processes are in place– Need to understand how to handle the exceptions

TM

44Compliance Made Simple ™ Revenue Recognition and Internal Controls

Interim Questions?

• IT Control considerations Q&A

TM

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Challenges in Adoption of the New Revenue

Recognition StandardMay 19, 2015

Luis Puncel, CPAPuncel Consulting Associates

Illuminating GAAP and Financial Reporting

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

About The Presenter

Luis Puncel, President of Puncel Consulting Associates, is a former PwC audit partner with more than 30 years’ experience in consulting on accounting and financial reporting matters, auditing, and business advisory services to public and private companies ranging from early stage to Fortune 500 in a number of industries, such as manufacturing, technology, software, web services, manufacturing, medical device, and others.Luis assists company management, audit committees, CPA firms and others in interpreting and applying generally accepted accounting principles to complex transactions. His specialties are performing technical accounting research and analysis of complex GAAP and SEC financial reporting issues of all types, audit preparation, and providing training programs.He worked with PricewaterhouseCoopers for 21 years, including 10 years as an audit partner heading private and public company audit engagements. Subsequently he was the partner in charge and ‐ ‐technical consulting partner for another international accounting firm. Also, he worked for an international public company, where he managed the successful first year implementation of Section ‐404 of the Sarbanes Oxley Act.‐Luis graduated from the University of Southern California with a degree in Business Administration. He is a licensed CPA in California, a member of the American Institute of Certified Public Accountants, and is a nationally recognized author of the 2008 through 2011 editions of Knowledge Based Audit™ Procedures ‐and Knowledge Based Audits™ of Public Entities: A Guide to PCAOB Standards and SEC Rules published ‐by CCH. He also authored editions of the Knowledge Based Audit™ (KBA) Tools for audits of commercial ‐entities, which are currently in use by accounting firms across the U.S. He is a frequent speaker, panelist, and trainer on topics related to accounting, auditing and SEC matters.

46

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

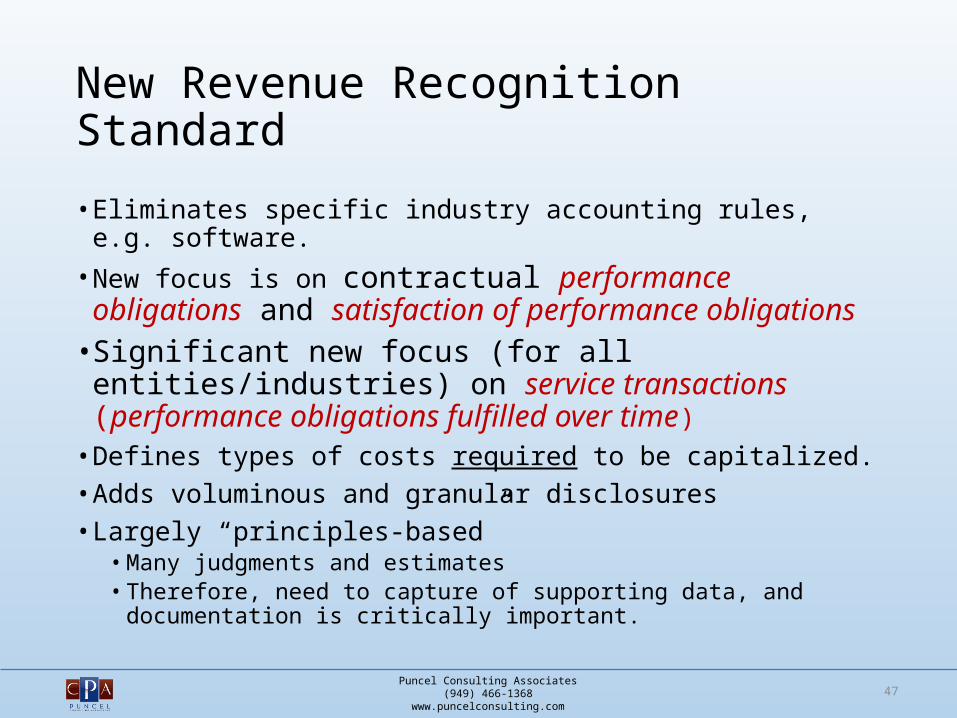

New Revenue Recognition Standard

• Eliminates specific industry accounting rules, e.g. software.• New focus is on contractual performance obligations and

satisfaction of performance obligations• Significant new focus (for all entities/industries) on service

transactions (performance obligations fulfilled over time)• Defines types of costs required to be capitalized. • Adds voluminous and granular disclosures• Largely “principles-based”

• Many judgments and estimates• Therefore, need to capture of supporting data, and documentation is

critically important.

47

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Core Principle of New Model

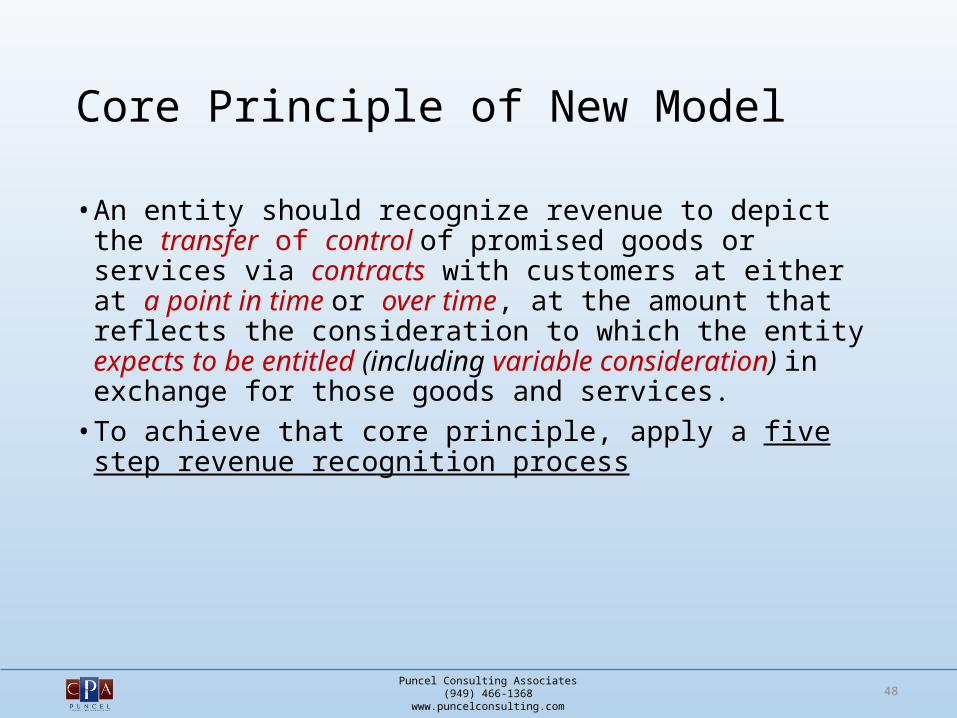

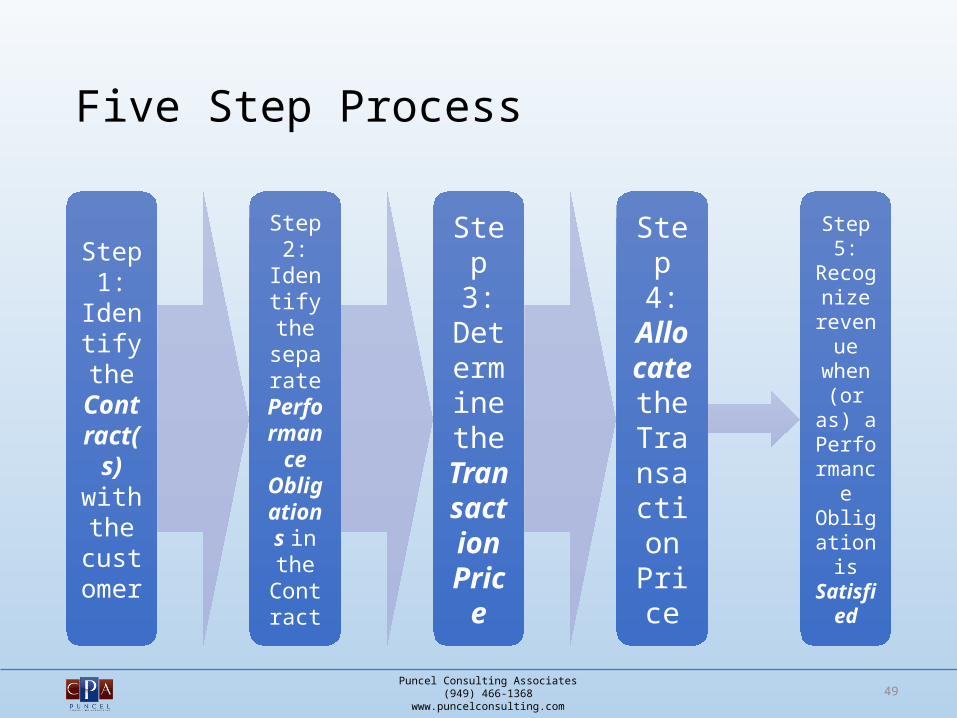

• An entity should recognize revenue to depict the transfer of control of promised goods or services via contracts with customers at either at a point in time or over time, at the amount that reflects the consideration to which the entity expects to be entitled (including variable consideration) in exchange for those goods and services.

• To achieve that core principle, apply a five step revenue recognition process

48

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Five Step Process

Step 1:

Identify the

Contract(

s) with the

customer

Step 2:

Identify the separ

ate Performanc

e Obligations in the Contr

act

Step 3:

Determine the

Transaction

Price

Step 4: Allocate the Transaction Pric

e

Step 5:

Recognize

revenue

when (or as)

a Performanc

e Obligation is Satisfi

ed

49

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Step 1: Identify the Contract(s) With a Customer

50

Step 1:

Identify the

Contract(

s) with the

customer

Step 2:

Identify the separ

ate Performanc

e Obligations in the Contr

act

Step 3:

Determine the

Transaction

Price

Step 4: Allocate the Transaction Pric

e

Step 5:

Recognize

revenue

when (or as)

a Performanc

e Obligation is Satisfi

ed

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

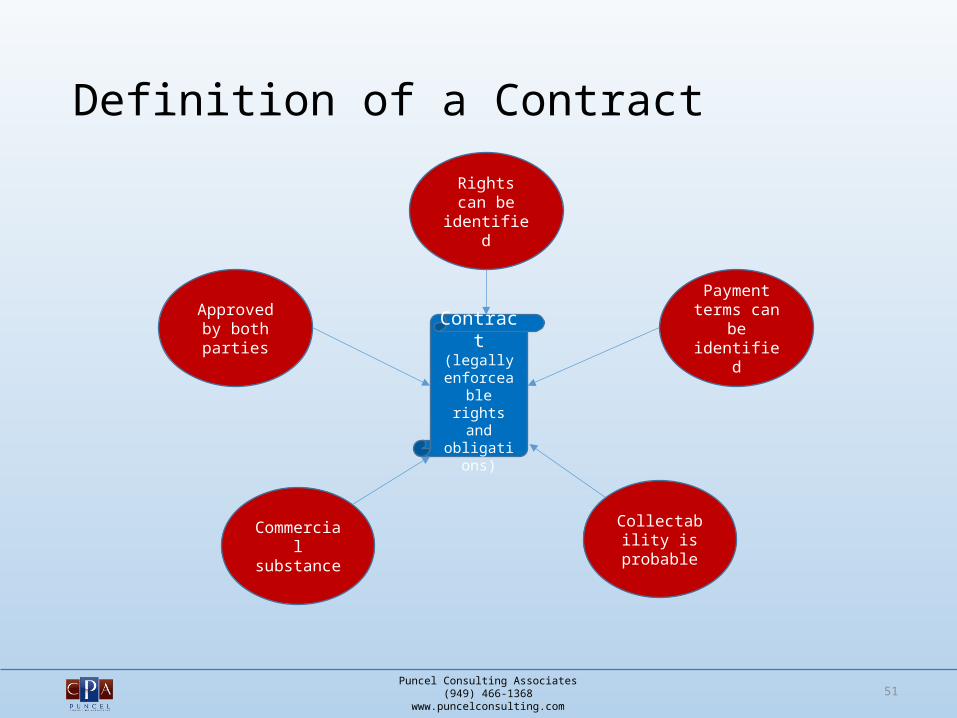

Definition of a Contract

51

Payment terms can be

identified

Approved by both parties

Rights can be identified

Commercial substance

Collectability is probable

Contract (legally

enforceable rights and

obligations)

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Expected Impact

• No more specific requirement to have both signatures on a contract• Legally enforceable is the standard• Contracts may be written, oral or implied by an entity’s customer’s

business practice• May require legal team involvement to document specific point when a

contract becomes enforceable• If an entity enters into non-standard contracts, this will be a bigger

challenge• There may be cross-border considerations• Entities may assess collectability using a portfolio approach if the result is

expected not to vary from a case-by-case review, but must have processes/controls to identify outliers

• An entity may want to consider changes to standard contracts to better document when they become enforceable

52

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

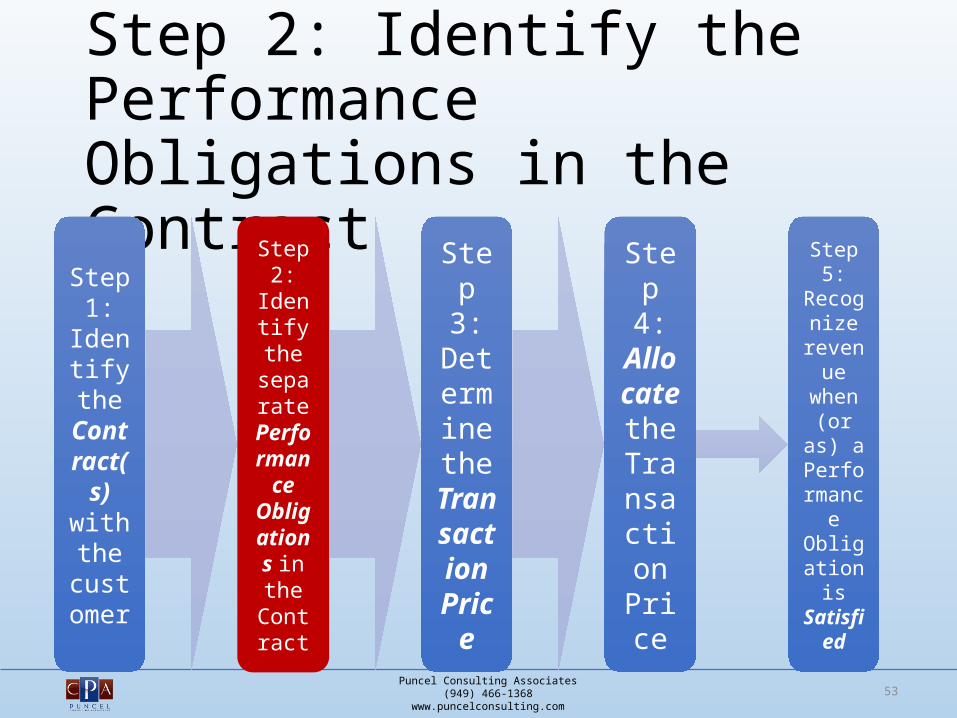

Step 2: Identify the Performance Obligations in the Contract

53

Step 1:

Identify the

Contract(

s) with the

customer

Step 2:

Identify the separ

ate Performanc

e Obligations in the Contr

act

Step 3:

Determine the

Transaction

Price

Step 4: Allocate the Transaction Pric

e

Step 5:

Recognize

revenue

when (or as)

a Performanc

e Obligation is Satisfi

ed

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

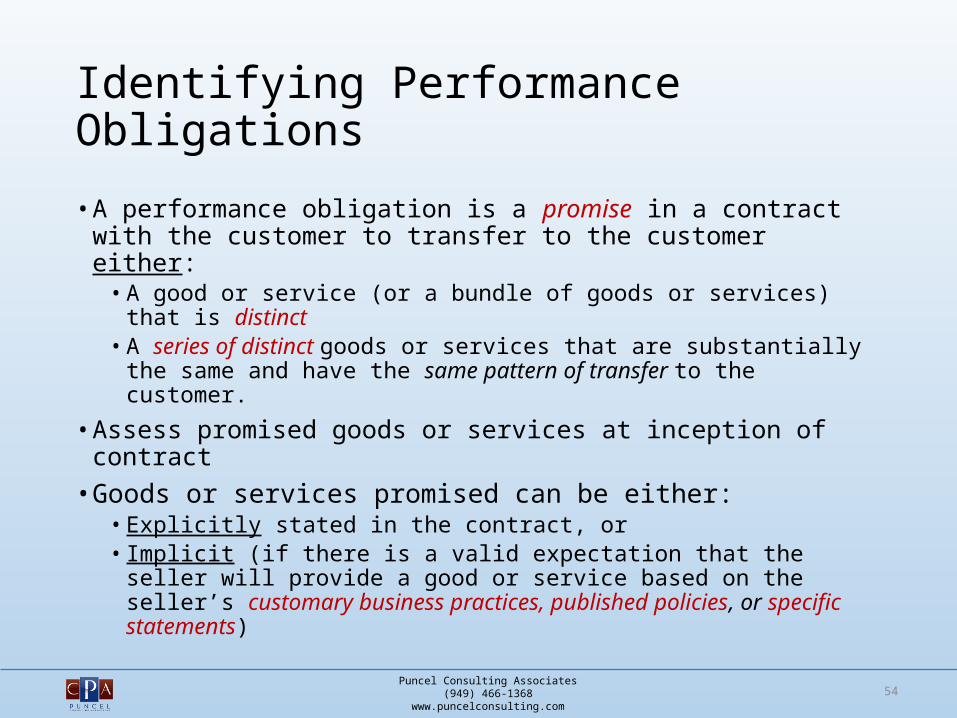

Identifying Performance Obligations

• A performance obligation is a promise in a contract with the customer to transfer to the customer either:

• A good or service (or a bundle of goods or services) that is distinct• A series of distinct goods or services that are substantially the same and have

the same pattern of transfer to the customer.

• Assess promised goods or services at inception of contract• Goods or services promised can be either:

• Explicitly stated in the contract, or• Implicit (if there is a valid expectation that the seller will provide a good or

service based on the seller’s customary business practices, published policies, or specific statements)

54

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

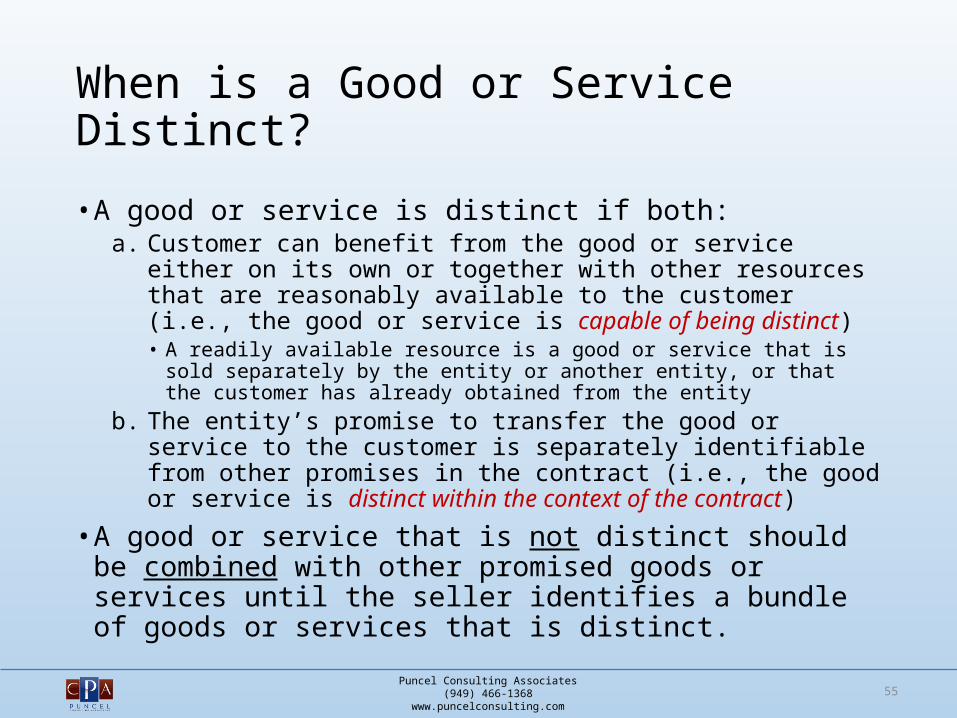

When is a Good or Service Distinct?

• A good or service is distinct if both:a. Customer can benefit from the good or service either on its own or

together with other resources that are reasonably available to the customer (i.e., the good or service is capable of being distinct)• A readily available resource is a good or service that is sold separately by the entity or

another entity, or that the customer has already obtained from the entityb. The entity’s promise to transfer the good or service to the customer is

separately identifiable from other promises in the contract (i.e., the good or service is distinct within the context of the contract)

• A good or service that is not distinct should be combined with other promised goods or services until the seller identifies a bundle of goods or services that is distinct.

55

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Expected Impact

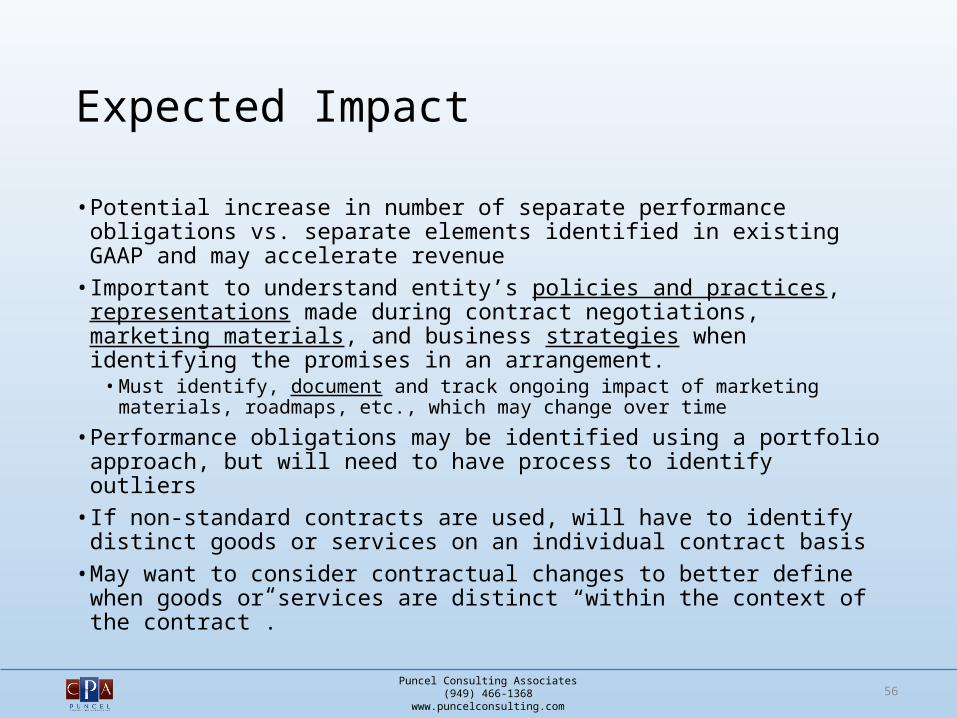

• Potential increase in number of separate performance obligations vs. separate elements identified in existing GAAP and may accelerate revenue

• Important to understand entity’s policies and practices, representations made during contract negotiations, marketing materials, and business strategies when identifying the promises in an arrangement.

• Must identify, document and track ongoing impact of marketing materials, roadmaps, etc., which may change over time

• Performance obligations may be identified using a portfolio approach, but will need to have process to identify outliers

• If non-standard contracts are used, will have to identify distinct goods or services on an individual contract basis

• May want to consider contractual changes to better define when goods or services are distinct “within the context of the contract”.

56

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

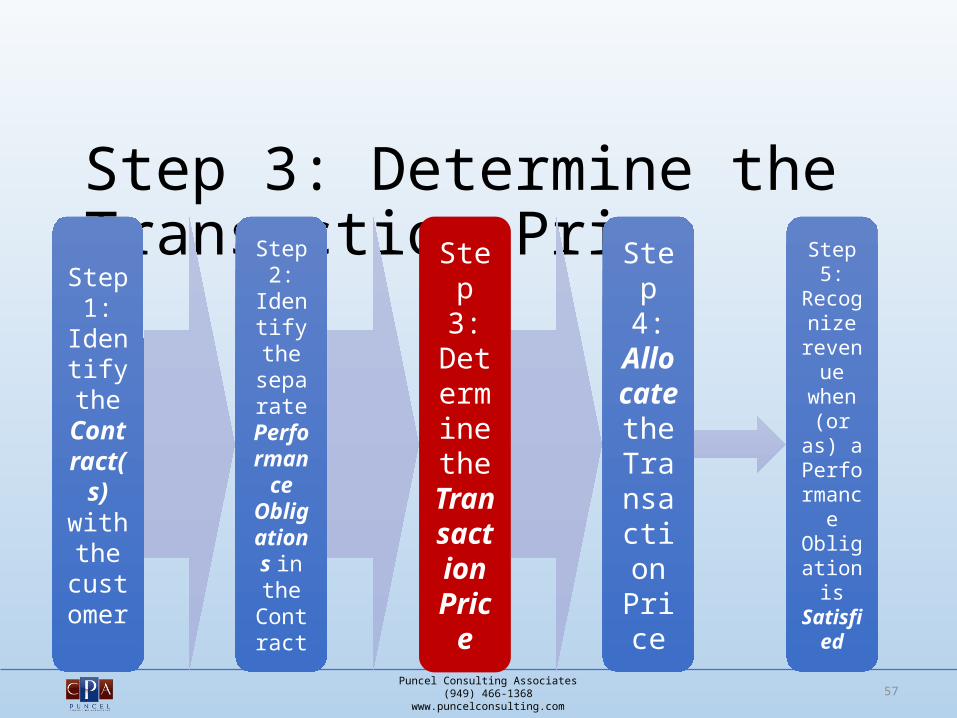

Step 3: Determine the Transaction Price

57

Step 1:

Identify the

Contract(

s) with the

customer

Step 2:

Identify the separ

ate Performanc

e Obligations in the Contr

act

Step 3:

Determine the

Transaction

Price

Step 4: Allocate the Transaction Pric

e

Step 5:

Recognize

revenue

when (or as)

a Performanc

e Obligation is Satisfi

ed

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

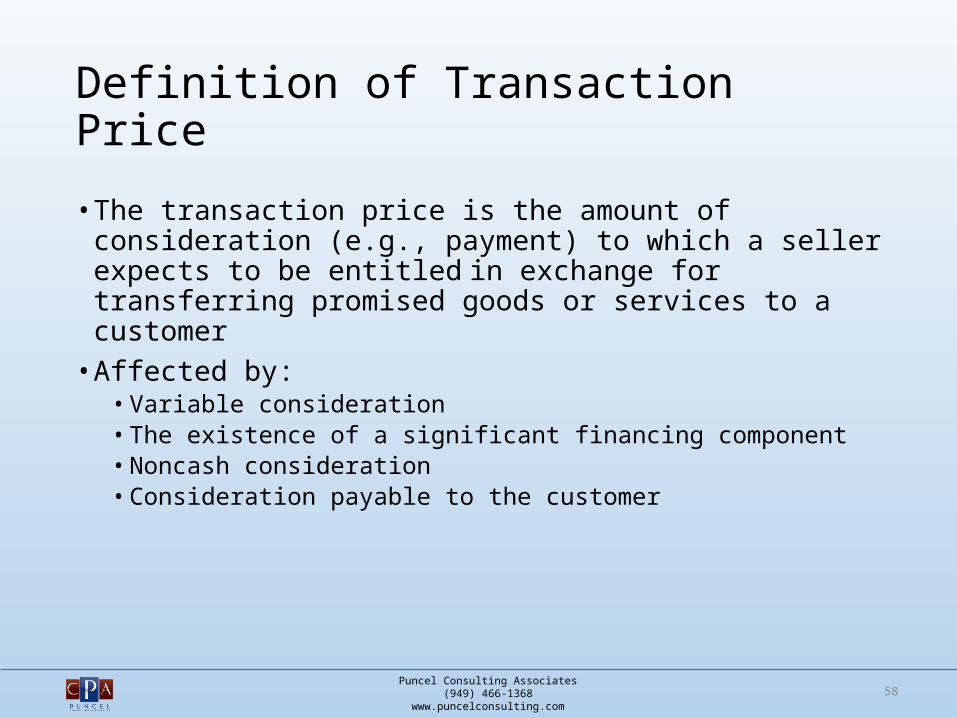

Definition of Transaction Price

• The transaction price is the amount of consideration (e.g., payment) to which a seller expects to be entitled in exchange for transferring promised goods or services to a customer

• Affected by:• Variable consideration• The existence of a significant financing component• Noncash consideration• Consideration payable to the customer

58

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

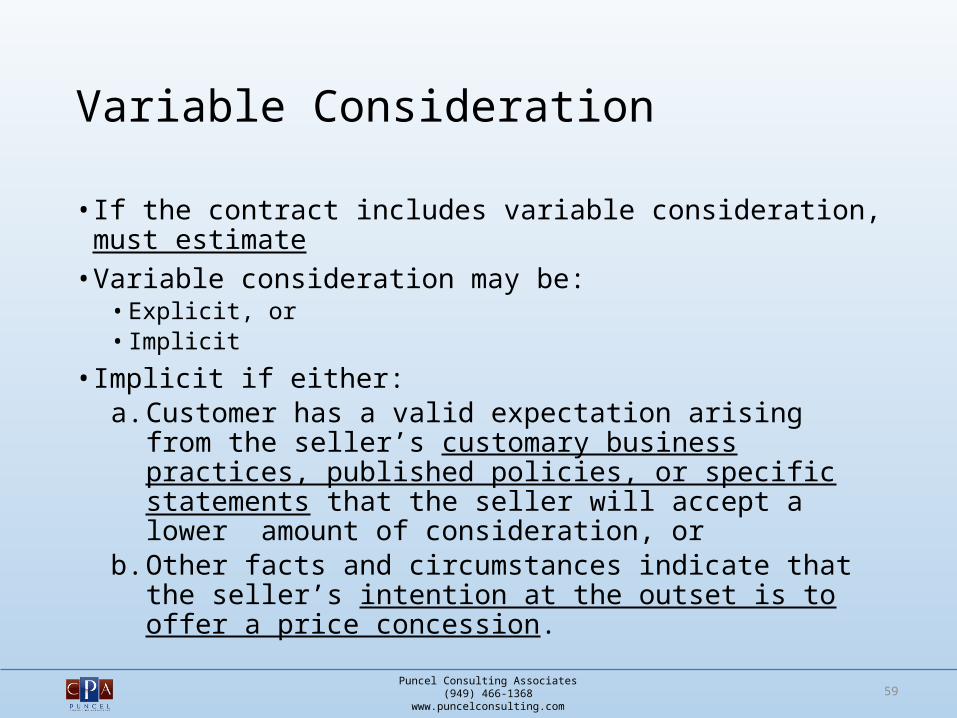

Variable Consideration

• If the contract includes variable consideration, must estimate• Variable consideration may be:

• Explicit, or• Implicit

• Implicit if either:a. Customer has a valid expectation arising from the seller’s

customary business practices, published policies, or specific statements that the seller will accept a lower amount of consideration, or

b. Other facts and circumstances indicate that the seller’s intention at the outset is to offer a price concession.

59

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Variable Consideration

60

Common types of variable consideration

Bonuses Incentive payments Penalties

Refunds Money-back guarantees Volume discounts

Rights of return Price concessions Volume rebates

Credits Performance bonuses Royalties

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

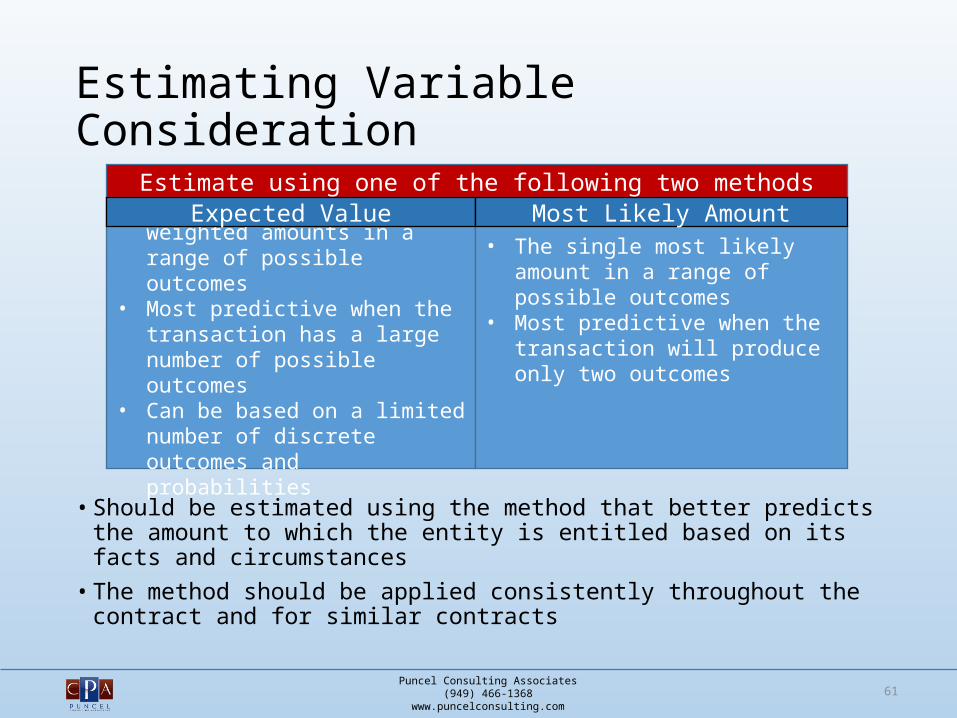

Estimating Variable Consideration

• Should be estimated using the method that better predicts the amount to which the entity is entitled based on its facts and circumstances

• The method should be applied consistently throughout the contract and for similar contracts

61

• Sum of the probability-weighted amounts in a range of possible outcomes

• Most predictive when the transaction has a large number of possible outcomes

• Can be based on a limited number of discrete outcomes and probabilities

• The single most likely amount in a range of possible outcomes

• Most predictive when the transaction will produce only two outcomes

Estimate using one of the following two methodsExpected Value Most Likely Amount

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

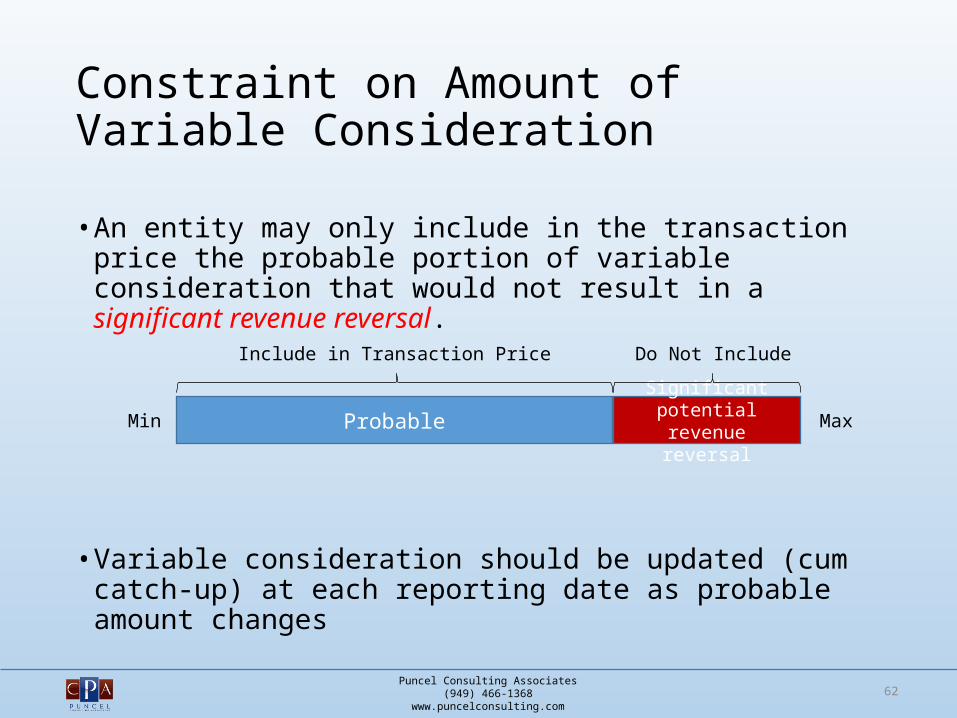

Constraint on Amount of Variable Consideration

• An entity may only include in the transaction price the probable portion of variable consideration that would not result in a significant revenue reversal.

• Variable consideration should be updated (cum catch-up) at each reporting date as probable amount changes

62

Probable Significant potential revenue reversal

Min Max

Include in Transaction Price Do Not Include

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Expected Impact

• Recording estimated variable consideration may significantly affect the timing of recognition compared to today.

• Significant judgment will be required to estimate the amount of variable consideration that should be included in the transaction price.

• If there are standard arrangements and performance obligations, this may require significant effort, although entities may assess by class of customer, products or services, distribution channel, etc. if it is expected to provide the same result. However, there will have to have processes/controls to identify any outliers.

• Must identify and document customary business practices, published policies, specific statements and/or intent to offer a price concession

• Must track over time to incorporate changes in customary practices

• May be more of a challenge if there are non-standard practices by product, location, etc.

63

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

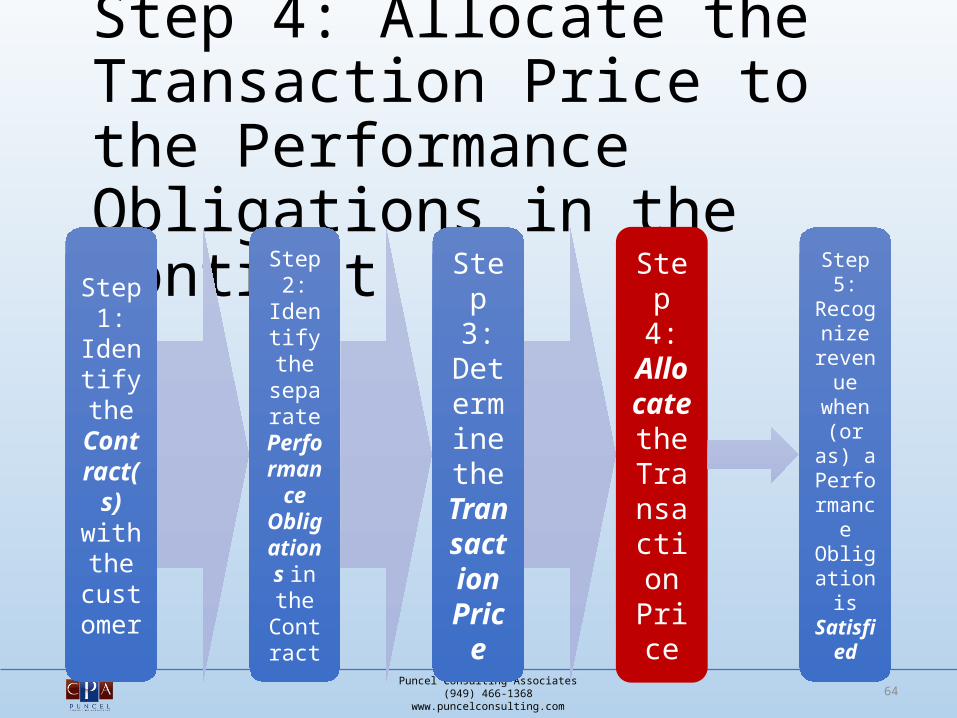

Step 4: Allocate the Transaction Price to the Performance Obligations in the Contract

64

Step 1:

Identify the

Contract(

s) with the

customer

Step 2:

Identify the separ

ate Performanc

e Obligations in the Contr

act

Step 3:

Determine the

Transaction

Price

Step 4: Allocate the Transaction Pric

e

Step 5:

Recognize

revenue

when (or as)

a Performanc

e Obligation is Satisfi

ed

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

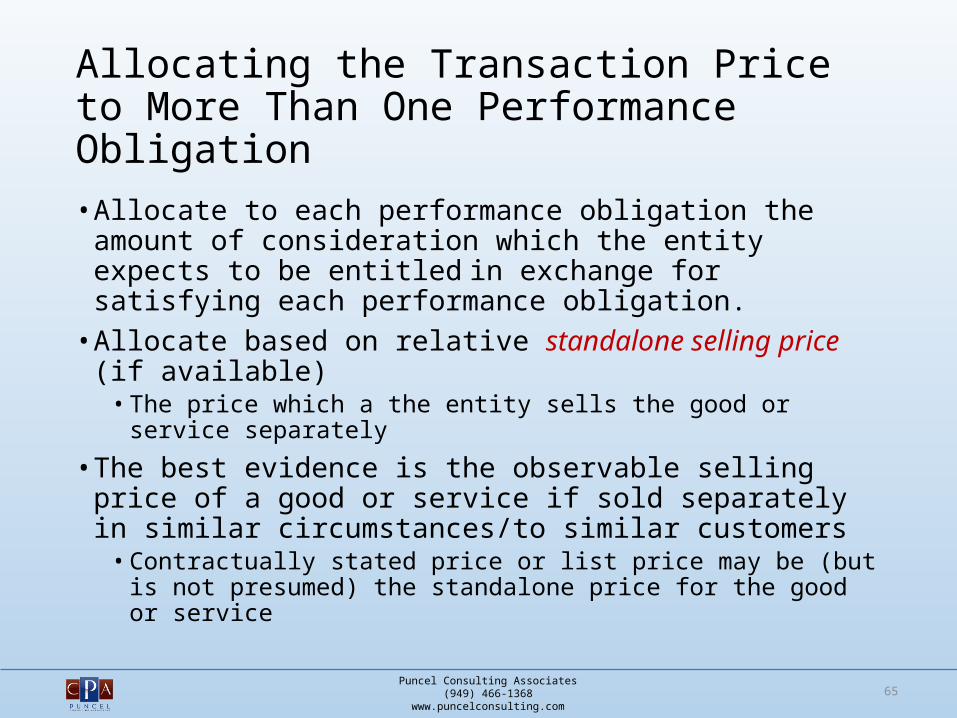

Allocating the Transaction Price to More Than One Performance Obligation• Allocate to each performance obligation the amount of consideration

which the entity expects to be entitled in exchange for satisfying each performance obligation.

• Allocate based on relative standalone selling price (if available) • The price which a the entity sells the good or service separately

• The best evidence is the observable selling price of a good or service if sold separately in similar circumstances/to similar customers

• Contractually stated price or list price may be (but is not presumed) the standalone price for the good or service

65

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

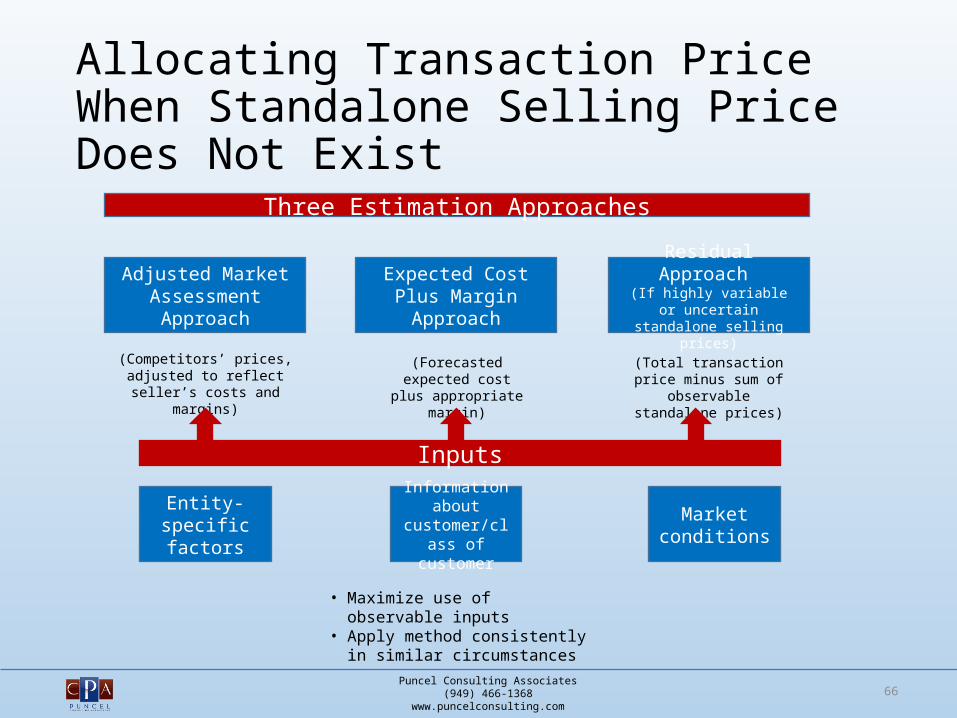

Allocating Transaction Price When Standalone Selling Price Does Not Exist

66

Market conditions

Residual Approach (If highly variable or uncertain

standalone selling prices)

Expected Cost Plus Margin Approach

Adjusted Market Assessment Approach

Entity-specific factors

Information about

customer/class of customer

• Maximize use of observable inputs• Apply method consistently in similar

circumstances

(Competitors’ prices, adjusted to reflect seller’s costs and

margins)

(Total transaction price minus sum of observable

standalone prices)

Inputs

(Forecasted expected cost plus appropriate

margin)

Three Estimation Approaches

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

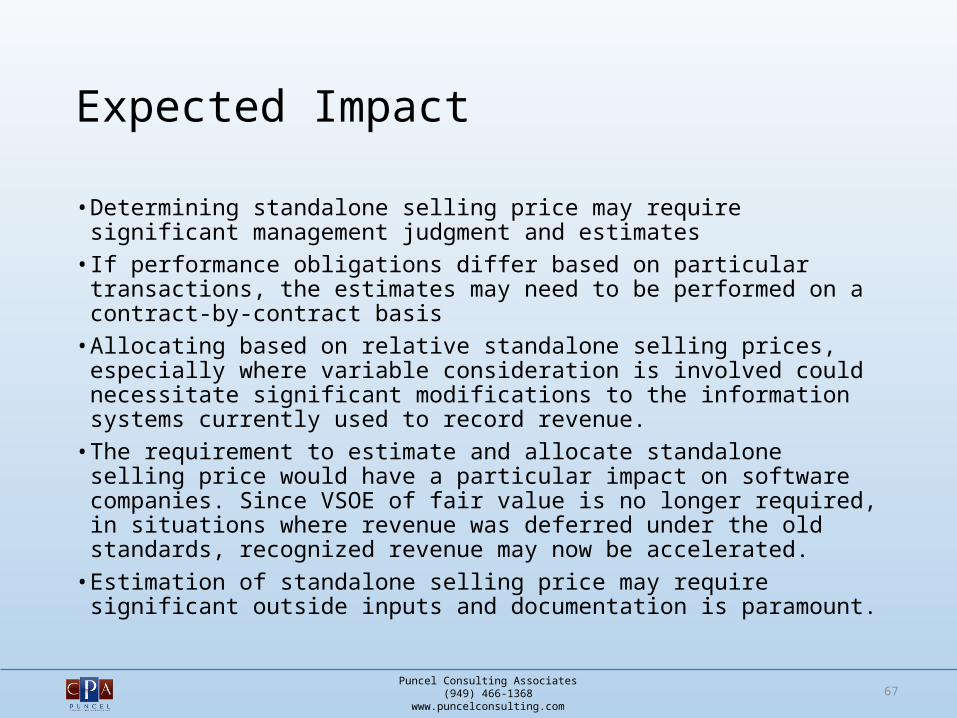

Expected Impact

• Determining standalone selling price may require significant management judgment and estimates

• If performance obligations differ based on particular transactions, the estimates may need to be performed on a contract-by-contract basis

• Allocating based on relative standalone selling prices, especially where variable consideration is involved could necessitate significant modifications to the information systems currently used to record revenue.

• The requirement to estimate and allocate standalone selling price would have a particular impact on software companies. Since VSOE of fair value is no longer required, in situations where revenue was deferred under the old standards, recognized revenue may now be accelerated.

• Estimation of standalone selling price may require significant outside inputs and documentation is paramount.

67

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

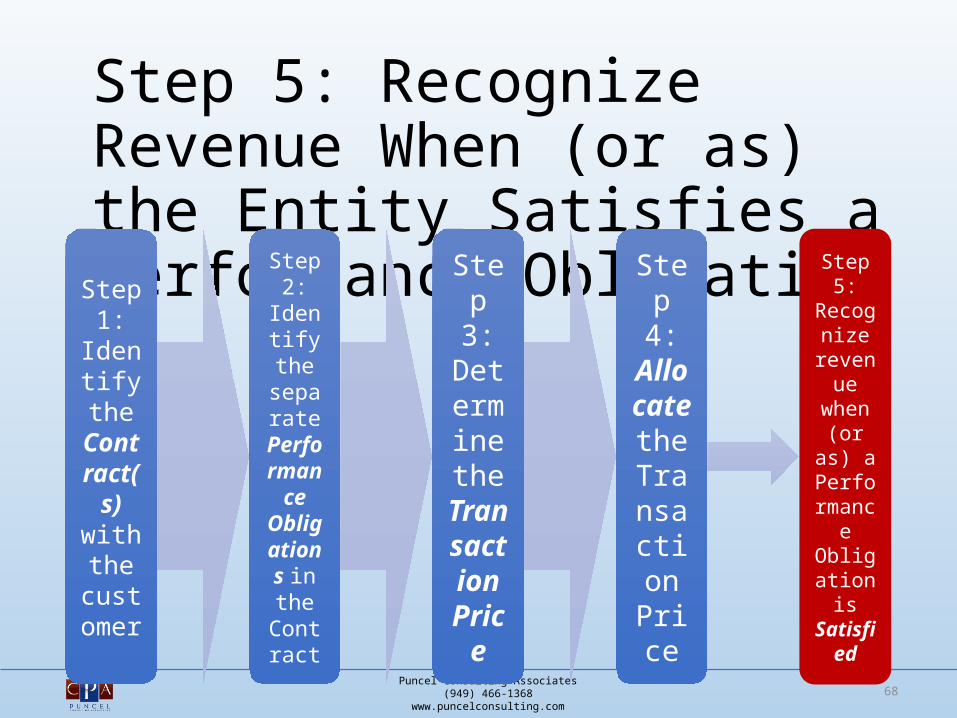

Step 5: Recognize Revenue When (or as) the Entity Satisfies a Performance Obligation

68

Step 1:

Identify the

Contract(

s) with the

customer

Step 2:

Identify the separ

ate Performanc

e Obligations in the Contr

act

Step 3:

Determine the

Transaction

Price

Step 4: Allocate the Transaction Pric

e

Step 5:

Recognize

revenue

when (or as)

a Performanc

e Obligation is Satisfi

ed

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

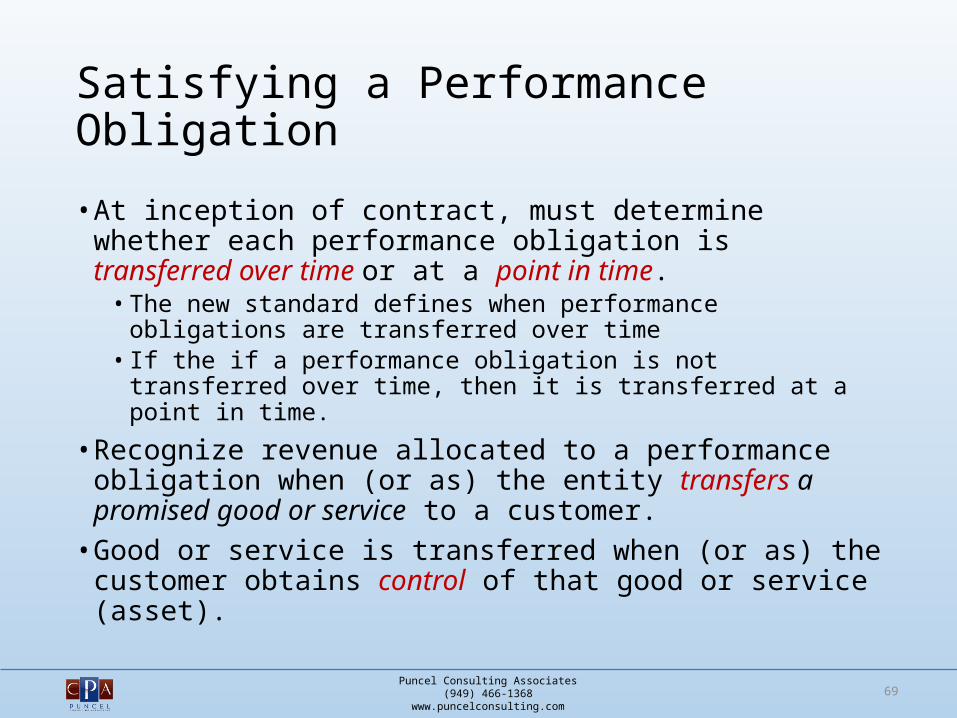

Satisfying a Performance Obligation

• At inception of contract, must determine whether each performance obligation is transferred over time or at a point in time.

• The new standard defines when performance obligations are transferred over time

• If the if a performance obligation is not transferred over time, then it is transferred at a point in time.

• Recognize revenue allocated to a performance obligation when (or as) the entity transfers a promised good or service to a customer.

• Good or service is transferred when (or as) the customer obtains control of that good or service (asset).

69

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

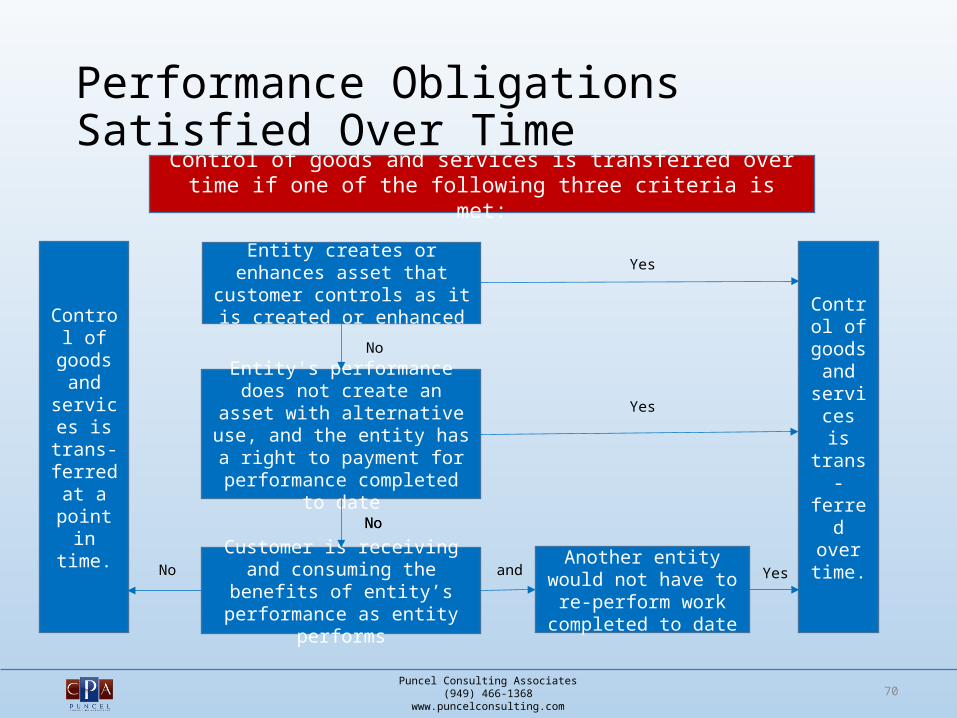

Performance Obligations Satisfied Over Time

70

Entity creates or enhances asset that customer controls as it is

created or enhanced

Entity's performance does not create an asset with alternative use, and the entity has a right to

payment for performance completed to date

Customer is receiving and consuming the benefits of entity’s performance as entity performs

Another entity would not have to re-perform work

completed to date

Control of

goods and

services is trans-ferred over time.

and

Control of goods and services is transferred over time if one of the following three criteria is met:

Control of goods

and services is trans-ferred at a point in time. No

No

No

No Yes

Yes

Yes

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

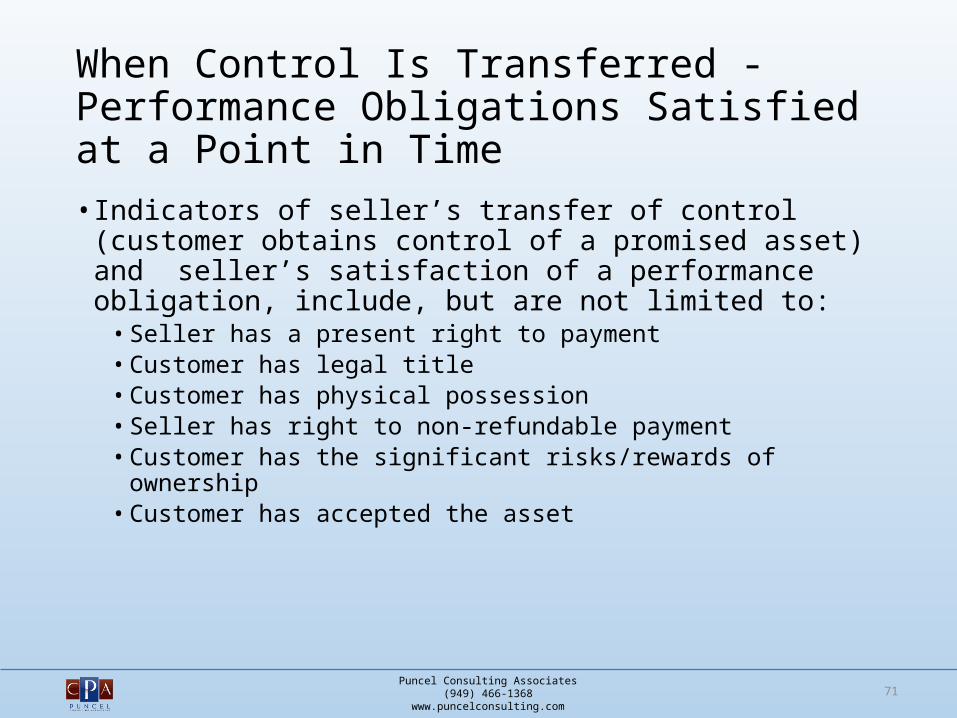

When Control Is Transferred - Performance Obligations Satisfied at a Point in Time• Indicators of seller’s transfer of control (customer obtains control of a

promised asset) and seller’s satisfaction of a performance obligation, include, but are not limited to:

• Seller has a present right to payment• Customer has legal title• Customer has physical possession• Seller has right to non-refundable payment• Customer has the significant risks/rewards of ownership• Customer has accepted the asset

71

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Measuring Progress Towards Completion – Performance Obligations Transferred Over Time• Measure the progress toward control transfer by one of the two

methods:• Output (hourly billings, milestones)• Input (costs, labor hours, time) methods

72

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Expected Impact

• The concept of transfer of control may require more judgment.• It may change revenue timing, because it is no longer focused

narrowly on transfer of title (FOB terms) and risks and rewards of ownership.

• Determining when control transferred may involve legal considerations that vary across jurisdictions, performance obligations, distribution channels, etc.

• The transfer of control concept may change revenue recognition pattern for companies who currently use “sell-through” policy.

• The new guidance on service transactions may represent a significant change to entities outside of the construction/contracting industry who use various methods to recognize services revenue.

73

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Disclosures

74

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Disclosures

• Objective: to provide sufficient information to enable users of financial statements to understand the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers

• Requires numerous qualitative and quantitative disclosures• Required for each period for which an income statement and balance

sheet are presented

75

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Examples of Qualitative Disclosures

• How estimates are made for:• Determination of transaction price• Determination of variable consideration, with separate discussion of each

significant type and how potential for reversal is evaluated• Allocation of transaction price to performance obligations• Returns, refunds and similar items

• Significant judgments and changes in judgments in determining the timing of satisfaction of performance obligations (over time or at a point in time), and determining the transaction price and amounts allocated to performance obligations

• The methods used to recognize revenue for performance obligations satisfied over time and an explanation of why the methods used provide a faithful depiction of how control is transferred

76

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Examples of Quantitative Disclosures

• Amount of transaction price allocated to remaining performance obligations at end of the period

• When amounts will be recognized• Variable consideration not yet included

• Revenue disaggregated into categories (by reportable segment and other categories) that reflect different responses to economic factors

• Roll-forward of contract assets and liabilities• Assets recognized from the costs to obtain or fulfill a contract• Revenue and impairments recognized• Information about contract balances (assets and liabilities)

77

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Disaggregated Revenues

• Principle: disaggregate revenue into categories that depict how the nature, amount, timing, and uncertainty of revenues and cash flows are affected by economic factors.

• In addition, an entity should disclose sufficient information to enable users of the financial statements to understand the relationship between the disclosure of disaggregated revenue and revenue information that is disclosed for each reportable segment.

• Categories are based on entity’s specific facts and circumstances• To decide categories, must consider how revenue disclosures:

a. Have been provided outside the financial statements, e.g., earnings releases,

b. Are reviewed by the chief operating decision maker, andc. In other information similar to that in (a) and (b) is used by the entity or

external users to evaluate financial performance and resource allocation.

78

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Disaggregated Revenues

• Example categories include (but are not limited to):• Type of good or service (e.g., major product line)• Geographical region (e.g., country or region)• Market or type of customer (e.g., government and nongovernment)• Type of contract (e.g., fixed-price and time-and-materials contracts)• Contract duration (e.g., short-term and long-term)• Timing of transfer of goods or services (e.g., point in time and over time)• Sales channels (e.g., direct to consumers and sold through intermediaries)

• Judgment required regarding level of aggregation or disaggregation (well in advance of adoption)

• Categorization may necessitate changes in information systems• Private companies may elect not to present certain types of

disaggregated disclosure

79

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

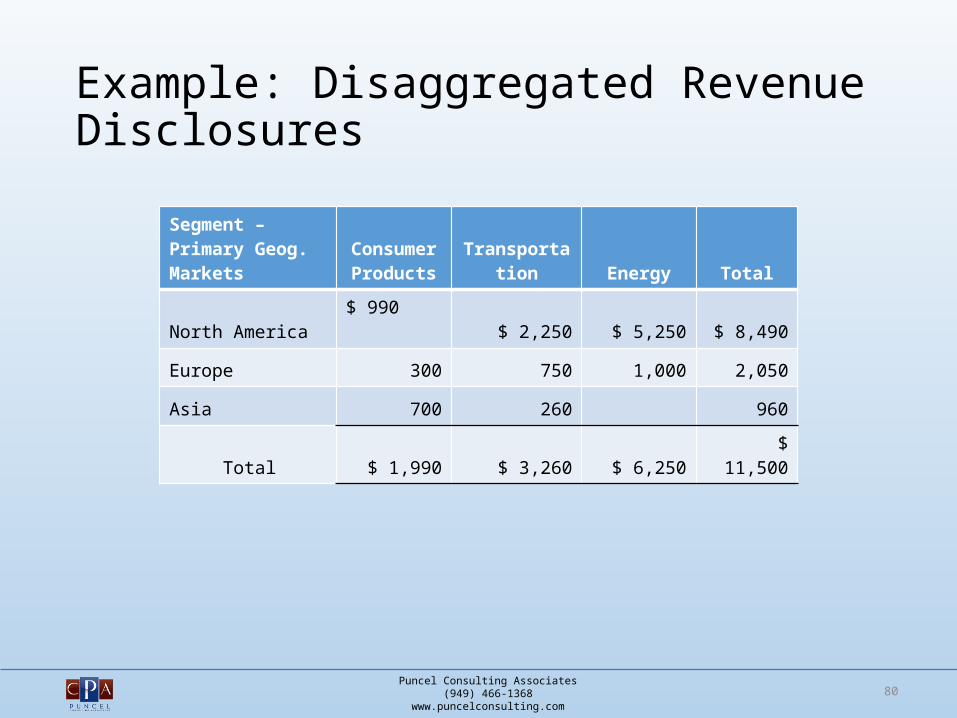

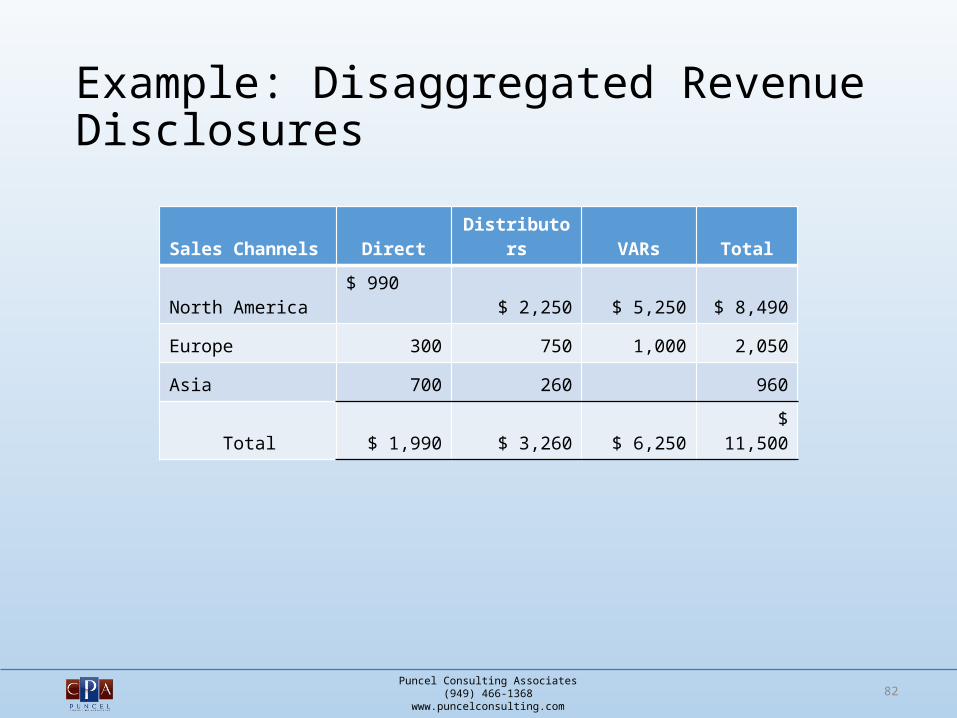

Example: Disaggregated Revenue Disclosures

80

Segment – Primary Geog. Markets

Consumer Products Transportation Energy Total

North America $ 990 $ 2,250 $ 5,250 $ 8,490

Europe 300 750 1,000 2,050

Asia 700 260 960

Total $ 1,990 $ 3,260 $ 6,250 $ 11,500

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

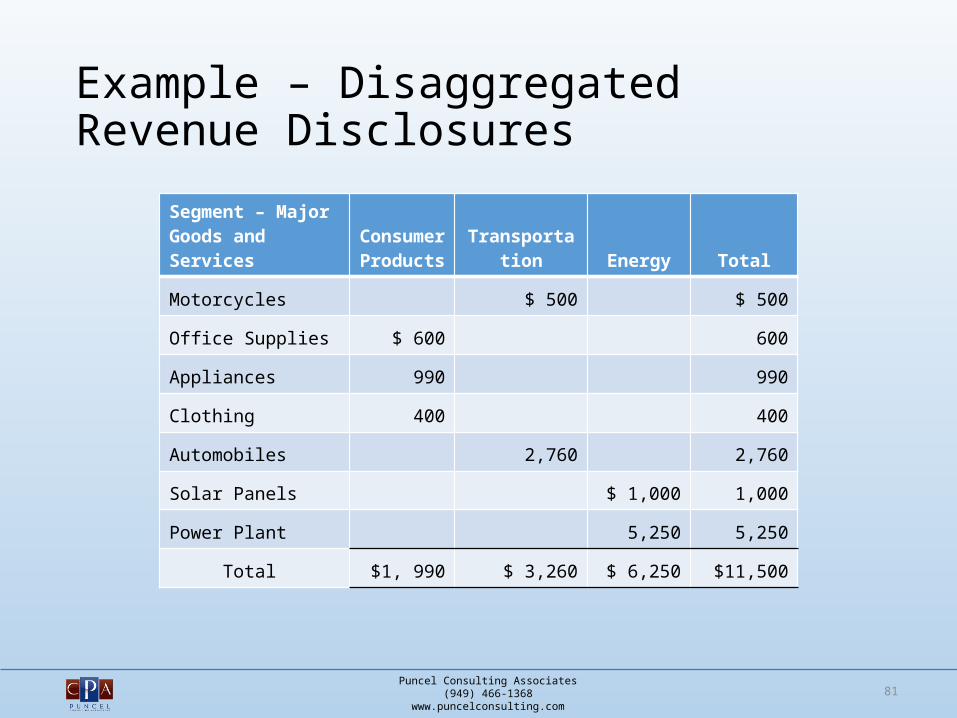

Example – Disaggregated Revenue Disclosures

81

Segment – Major Goods and Services

Consumer Products Transportation Energy Total

Motorcycles $ 500 $ 500

Office Supplies $ 600 600

Appliances 990 990

Clothing 400 400

Automobiles 2,760 2,760

Solar Panels $ 1,000 1,000

Power Plant 5,250 5,250

Total $1, 990 $ 3,260 $ 6,250 $11,500

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Example: Disaggregated Revenue Disclosures

82

Sales Channels Direct Distributors VARs Total

North America $ 990 $ 2,250 $ 5,250 $ 8,490

Europe 300 750 1,000 2,050

Asia 700 260 960

Total $ 1,990 $ 3,260 $ 6,250 $ 11,500

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Example – Disaggregated Revenue Disclosures

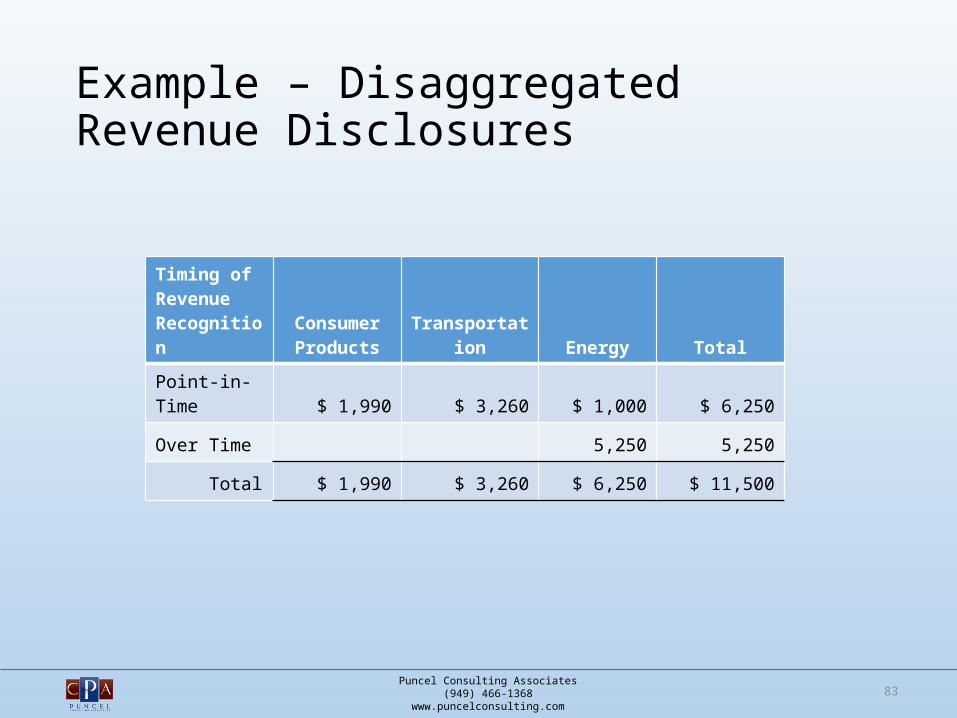

83

Timing of Revenue Recognition

Consumer Products Transportation Energy Total

Point-in-Time $ 1,990 $ 3,260 $ 1,000 $ 6,250

Over Time 5,250 5,250

Total $ 1,990 $ 3,260 $ 6,250 $ 11,500

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Expected Impact

• Significant management judgment required to decide categories of disaggregated revenue disclosures

• Current information systems may not capture data to provide disaggregated revenue disclosures. Therefore, consideration of the proper categories needs to be done early during the planning phase.

• The process of disaggregating revenue may require entities to rethink segment reporting categories

• Internal and external information considered in determining the categories will need to be well supported and documented.

84

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Effective Date and Transition

85

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

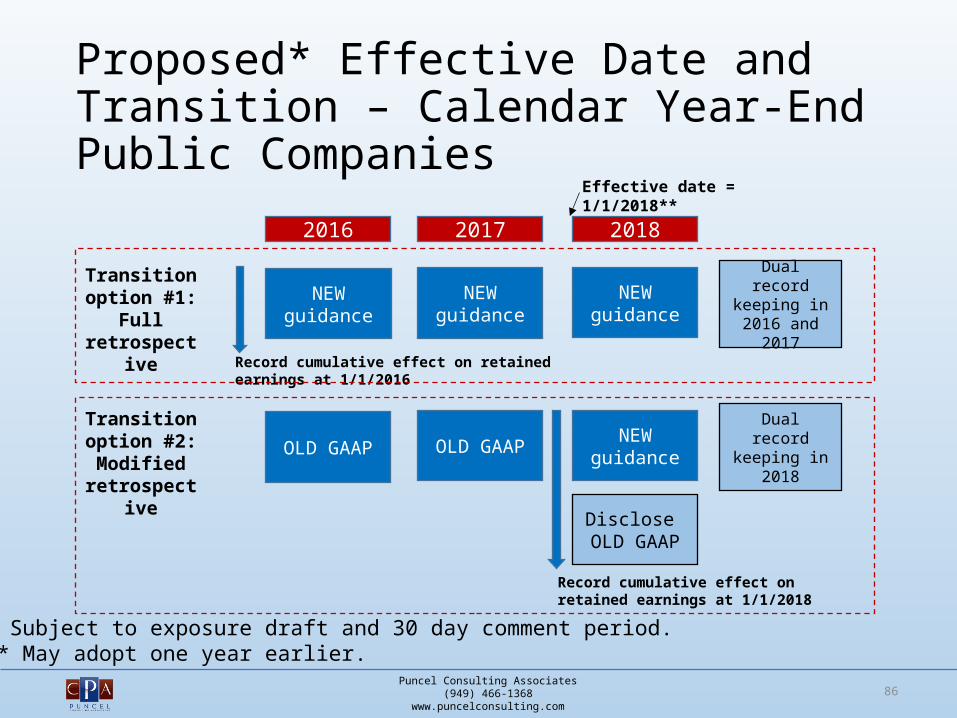

Proposed* Effective Date and Transition – Calendar Year-End Public Companies

86

2016

NEW guidance

2017 2018

NEW guidance

NEW guidance

Transition option #1:

Full retrospective

Transition option #2: Modified

retrospective

Record cumulative effect on retained earnings at 1/1/2016

OLD GAAP OLD GAAP NEW guidance

Record cumulative effect on retained earnings at 1/1/2018

Disclose OLD GAAP

Dual record keeping in

2016 and 2017

Dual record keeping in

2018

Effective date = 1/1/2018**

* Subject to exposure draft and 30 day comment period.** May adopt one year earlier.

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Takeaways

87

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Why is This a Big Deal Right Now?

• The transition choice has big effect on systems, processes and controls, so the decision as to which method will be adopted should be made as soon as possible

• Critical decisions and judgments required throughout the standard necessitate careful consideration and adequate time

• Time will be need to compile and document historical data which may require changes to information systems

• Determining and documenting the entity’s customary business practices could require a lot of work.

• The new standard will significantly affect internal controls and SOX compliance• An entity will need management, audit committee and auditor buy-in, which should

not be left to the last minute• There is the potential need for contractual changes, e.g., revenue contracts,

compensation structures, loan covenants, and may be others.• Information systems may (likely) need to be changed• Training and preparation will be needed throughout the organization• Will affect multiple departments, functions and geographic regions.

88

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

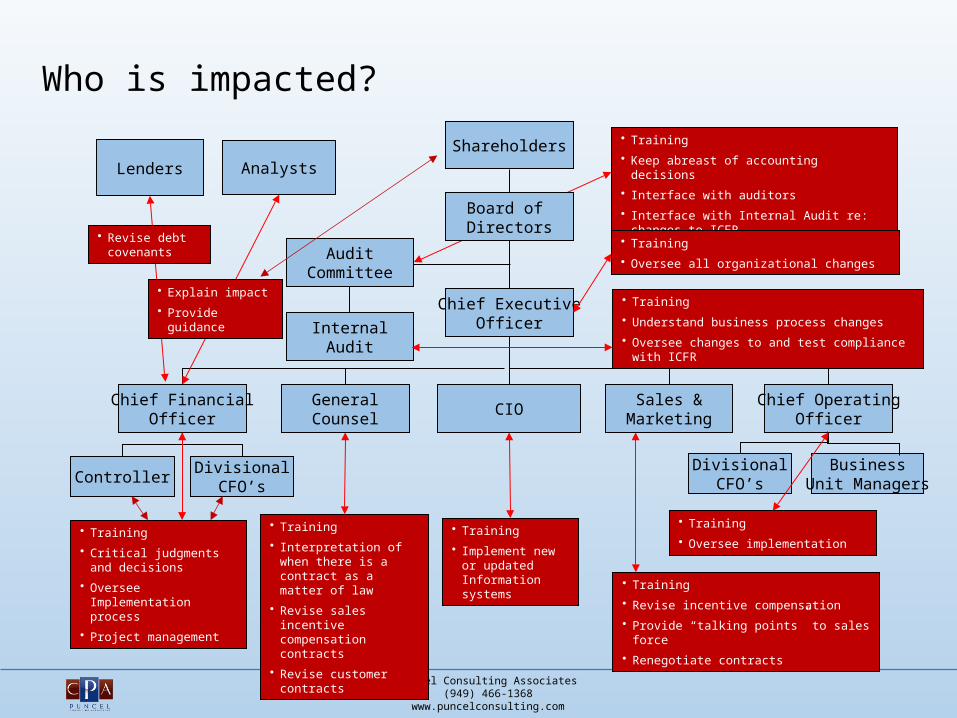

Who is impacted?

Shareholders

Chief ExecutiveOfficer

Sales &Marketing

GeneralCounsel

CIOChief Operating

OfficerChief Financial

Officer

InternalAudit

Controller

• Training

• Critical judgments and decisions

• Oversee Implementation process

• Project management

AuditCommittee

• Training

• Keep abreast of accounting decisions

• Interface with auditors

• Interface with Internal Audit re: changes to ICFR

• Training

• Interpretation of when there is a contract as a matter of law

• Revise sales incentive compensation contracts

• Revise customer contracts

• Training

• Implement new or updated Information systems

• Training

• Oversee implementation

DivisionalCFO’s

DivisionalCFO’s

BusinessUnit Managers

• Training

• Oversee all organizational changes

Board of Directors

Lenders Analysts

• Training

• Understand business process changes

• Oversee changes to and test compliance with ICFR

• Revise debt covenants

• Explain impact

• Provide guidance

• Training

• Revise incentive compensation

• Provide “talking points” to sales force

• Renegotiate contracts

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

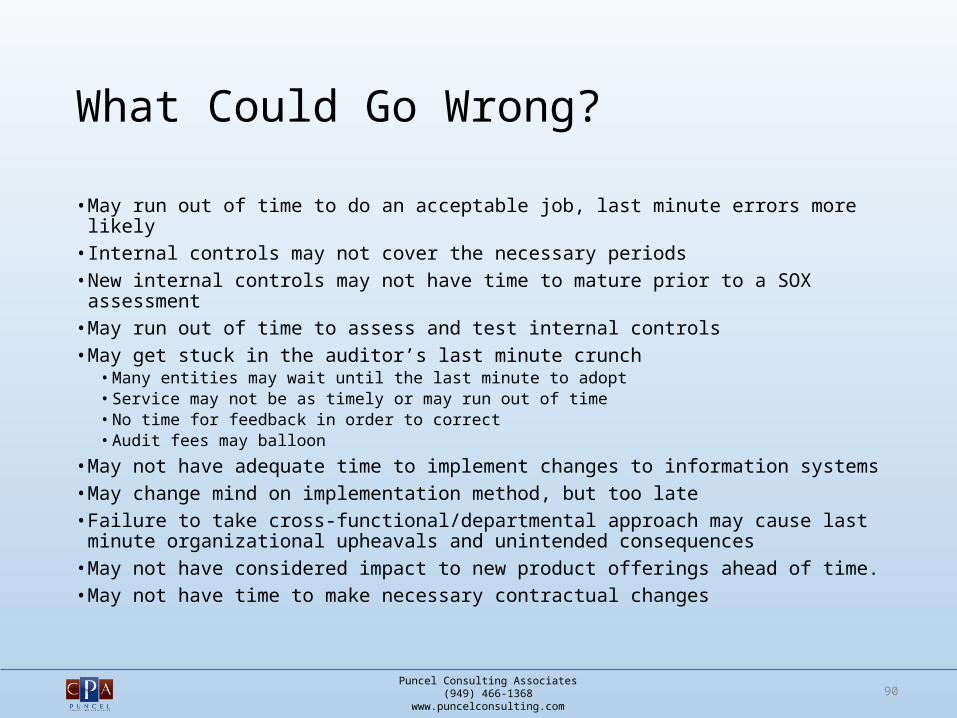

What Could Go Wrong?

• May run out of time to do an acceptable job, last minute errors more likely• Internal controls may not cover the necessary periods• New internal controls may not have time to mature prior to a SOX assessment• May run out of time to assess and test internal controls• May get stuck in the auditor’s last minute crunch

• Many entities may wait until the last minute to adopt• Service may not be as timely or may run out of time• No time for feedback in order to correct• Audit fees may balloon

• May not have adequate time to implement changes to information systems• May change mind on implementation method, but too late• Failure to take cross-functional/departmental approach may cause last minute

organizational upheavals and unintended consequences• May not have considered impact to new product offerings ahead of time.• May not have time to make necessary contractual changes

90

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

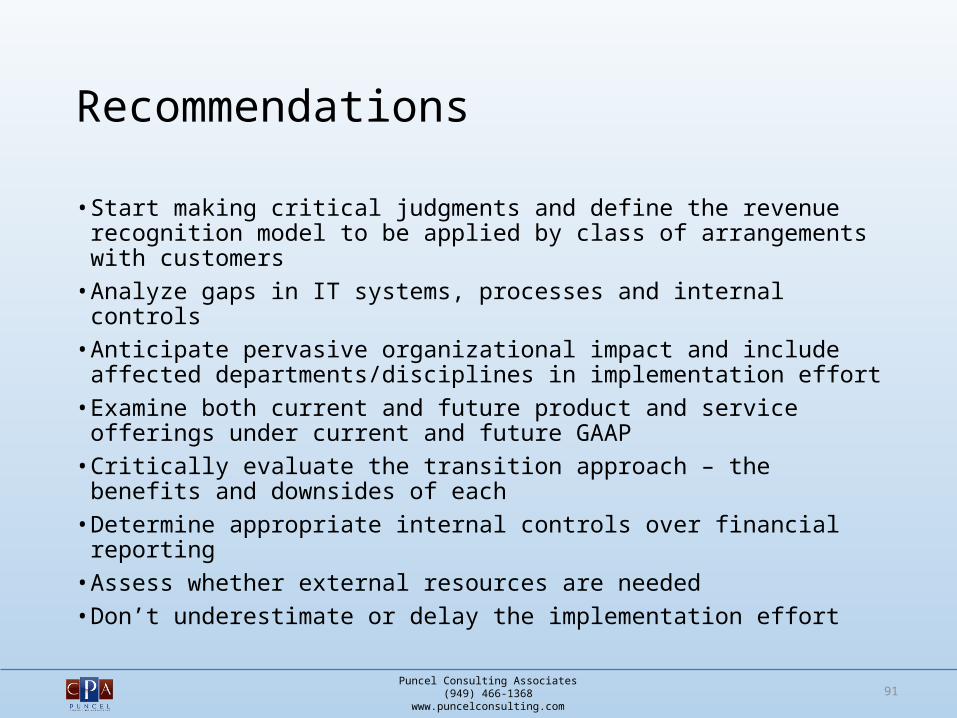

Recommendations

• Start making critical judgments and define the revenue recognition model to be applied by class of arrangements with customers

• Analyze gaps in IT systems, processes and internal controls• Anticipate pervasive organizational impact and include affected

departments/disciplines in implementation effort• Examine both current and future product and service offerings under

current and future GAAP• Critically evaluate the transition approach – the benefits and

downsides of each• Determine appropriate internal controls over financial reporting• Assess whether external resources are needed• Don’t underestimate or delay the implementation effort

91

Puncel Consulting Associates(949) 466-1368

www.puncelconsulting.com

Questions?

92

93Compliance Made Simple ™

Community & Sharing

Risk Assessments

Join Our LinkedIn GroupCOSO Framework Discussion &

Webinars

https://www.linkedin.com/groups/COSO-Implementation-4888186/about

Technical Community sharing Ideas ,Templates, WEBINARS, Advise and Learn from others implementing new framework.

Share your latest templates here!

94Compliance Made Simple ™

Control Compliance Analysis (“CCA”)

Email us for 2 SPOTS ONLY: [email protected]

Subject: CCA

CCAReportBenchmarkIn-take

95Compliance Made Simple ™

Aviva Spectrum is HIRING

1. SOX 404 – Senior Internal Auditors2. IT auditors3. SEC Reporting Managers4. Cyber security consultants

Email:

96Compliance Made Simple ™

Contact Information

Sonia Luna, CEO, Aviva Spectrum– CONNECT: www.linkedin.com/in/sonialuna– EMAIL: [email protected] – PHONE: (213) 250-5700

Larry Stewart, VP, Information Security / IT Compliance at PennyMac

– CONNECT: www.linkedin.com/in/larrystewart– EMAIL: [email protected]– PHONE: (805) 358-0016

Luis Puncel, President, Puncel Consulting Associates– CONNECT: www.linkedin.com/in/luispuncel – EMAIL: [email protected] – PHONE: (949) 466-1368

Revenue Recognition Controls