review of chapter 14. completed products for sale. materials waiting to be processed. can be direct...

TRANSCRIPT

REVIEW ofChapter 14

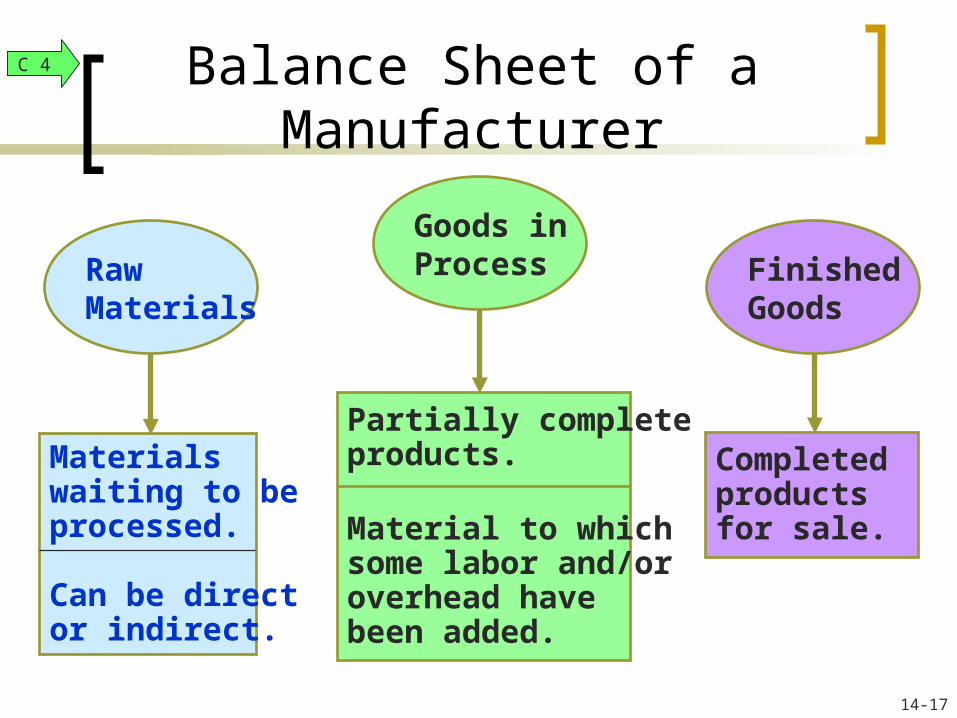

Completedproductsfor sale.

Materialswaiting to beprocessed.

Can be director indirect.

Partially completeproducts.

Material to whichsome labor and/oroverhead havebeen added.

Balance Sheet of a Manufacturer

RawMaterials

FinishedGoods

Goods inProcess

C 4

14-17

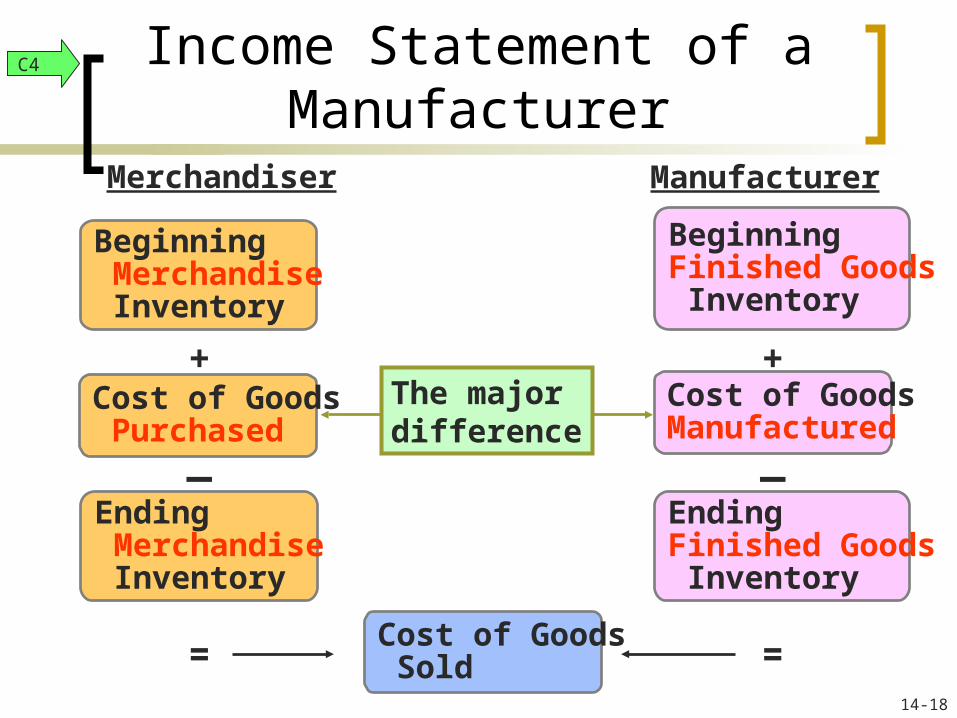

Beginning Merchandise Inventory

BeginningFinished Goods Inventory

Cost of Goods Purchased

Cost of GoodsManufactured

Ending Merchandise Inventory

EndingFinished Goods Inventory

Cost of Goods Sold

Merchandiser Manufacturer

+

_

+

==

_

The major difference

Income Statement of a Manufacturer

C4

14-18

Manufacturing Company

Cost of goods sold: Beg. finished goods inv. $11,200 + Cost of goods manufactured 170,500 = Goods available for sale 181,700 - Ending finished goods inventory (10,300) = Cost of goods sold 171,400$

Merchandising Company

Cost of goods sold: Beg. merchandise inventory 14,200$ + Purchases 234,150 = Goods available for sale 248,350$ - Ending merchandise inventory (12,100) = Cost of goods sold 236,250$

Cost of goods sold for manufacturers differs only slightly from cost of goods sold for merchandisers.

Income Statement of a Manufacturer

P1

14-19

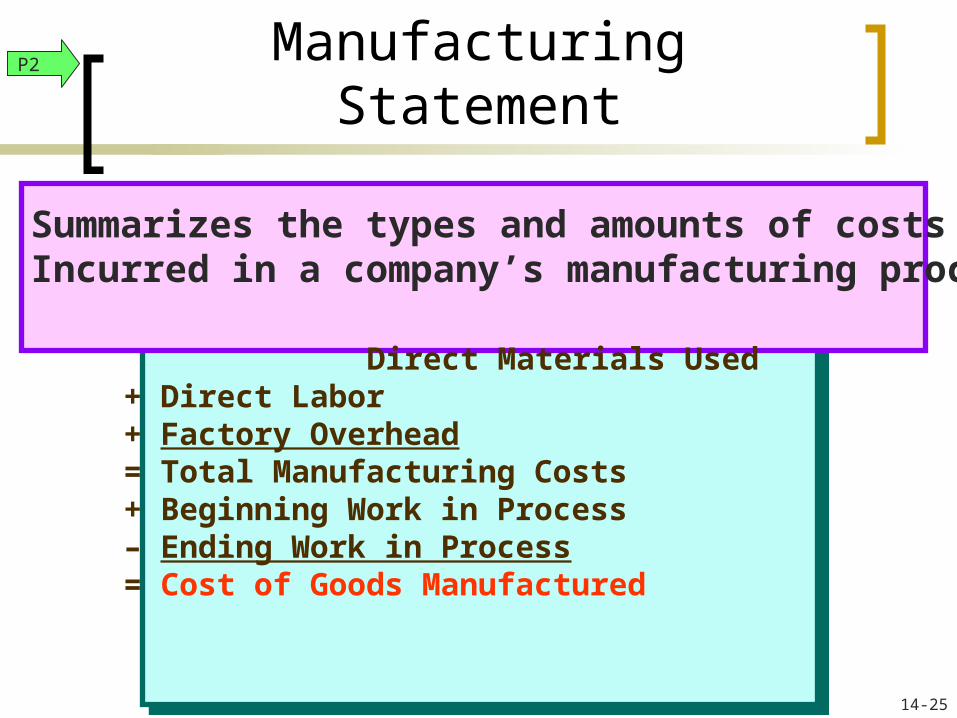

Summarizes the types and amounts of costsIncurred in a company’s manufacturing process.

Direct Materials Used + Direct Labor + Factory Overhead = Total Manufacturing Costs + Beginning Work in Process – Ending Work in Process = Cost of Goods Manufactured

Manufacturing StatementP2

14-25

Chapter 15

Job Order Costing and Analysis

ProcessCosting

JobCosting

Soda

Cereal

Gravel

Cement

Soap

Soda

Cereal

Gravel

Cement

Soap

Chapter 16 Chapter 16

C 1

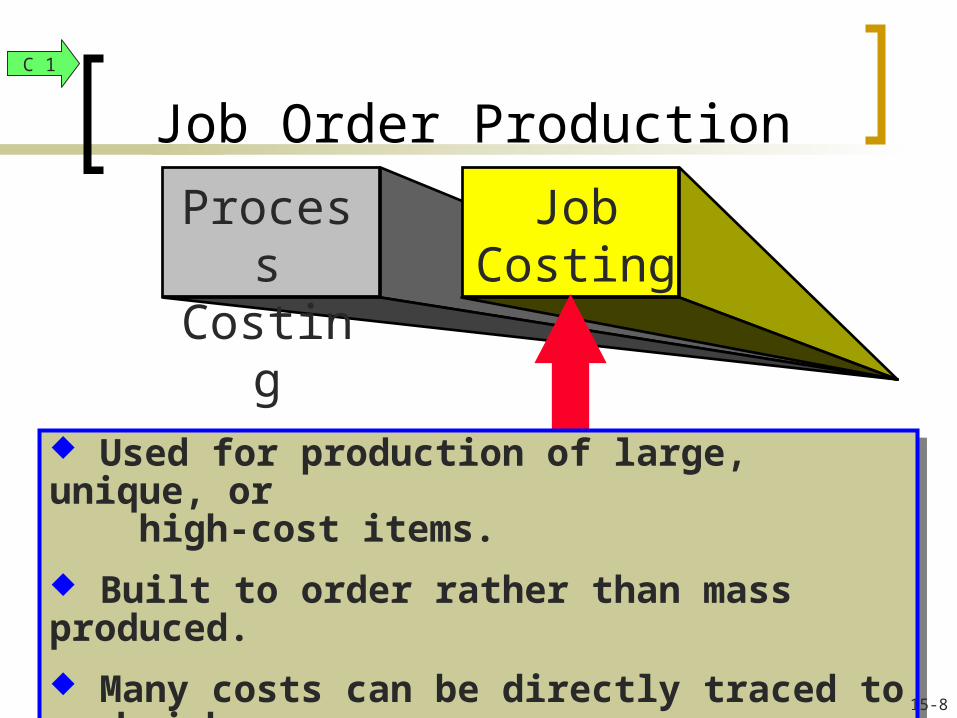

Job Order Manufacturing

15-7

Car repair

Custom home

Custom suit

Home repair

Airplane maker

Car repair

Custom home

Custom suit

Home repair

Airplane maker

ProcessCosting

JobCosting

Used for production of large, unique, or high-cost items.

Built to order rather than mass produced.

Many costs can be directly traced to each job.

Used for production of large, unique, or high-cost items.

Built to order rather than mass produced.

Many costs can be directly traced to each job.

Job Order ProductionC 1

15-8

ProcessCosting

JobCosting

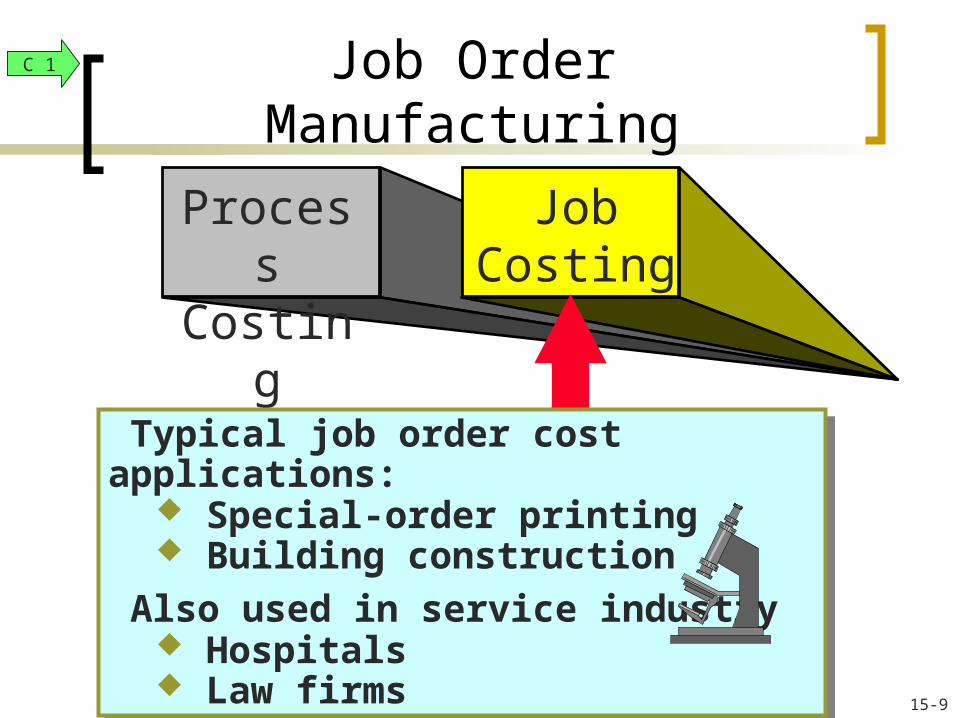

Typical job order cost applications: Special-order printing Building construction

Also used in service industry Hospitals Law firms

Typical job order cost applications: Special-order printing Building construction

Also used in service industry Hospitals Law firms

C 1

Job Order Manufacturing

15-9

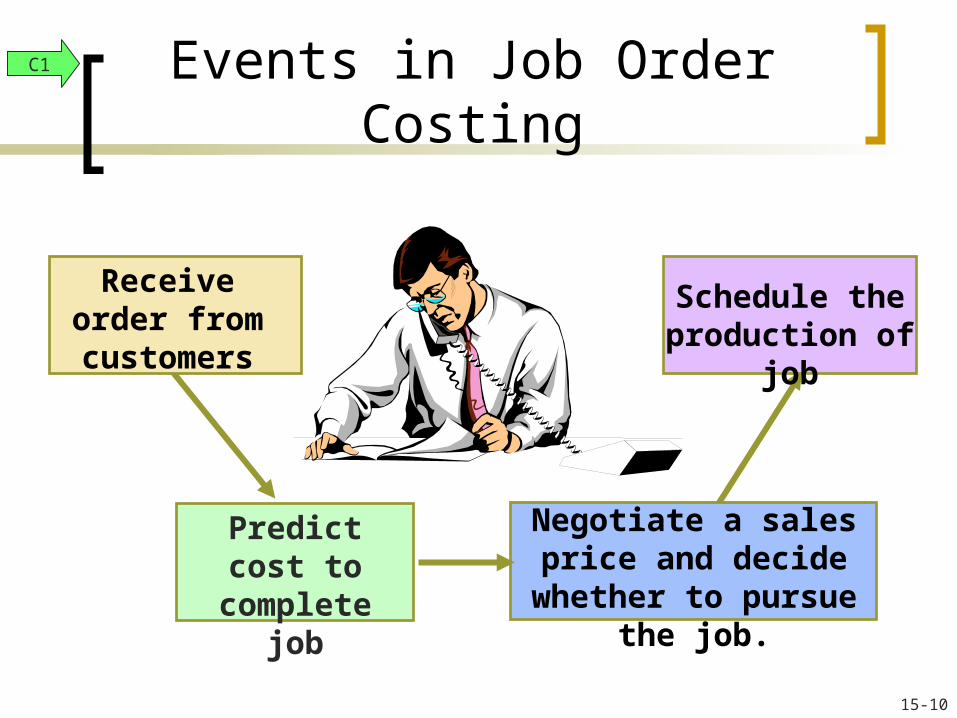

Receive order from

customers

Predict cost to complete

job

Negotiate a sales price and decide whether to

pursue the job.

Schedule the production of job

Events in Job Order CostingC1

15-10

Goods in Process

Cost of GoodsSold

Labor

Materials

Ind

irec

tIn

dir

ect

FinishedGoods

FactoryOverhead

Direct

Direct

Allocate

C 1 Job Order Production Activities

15-11

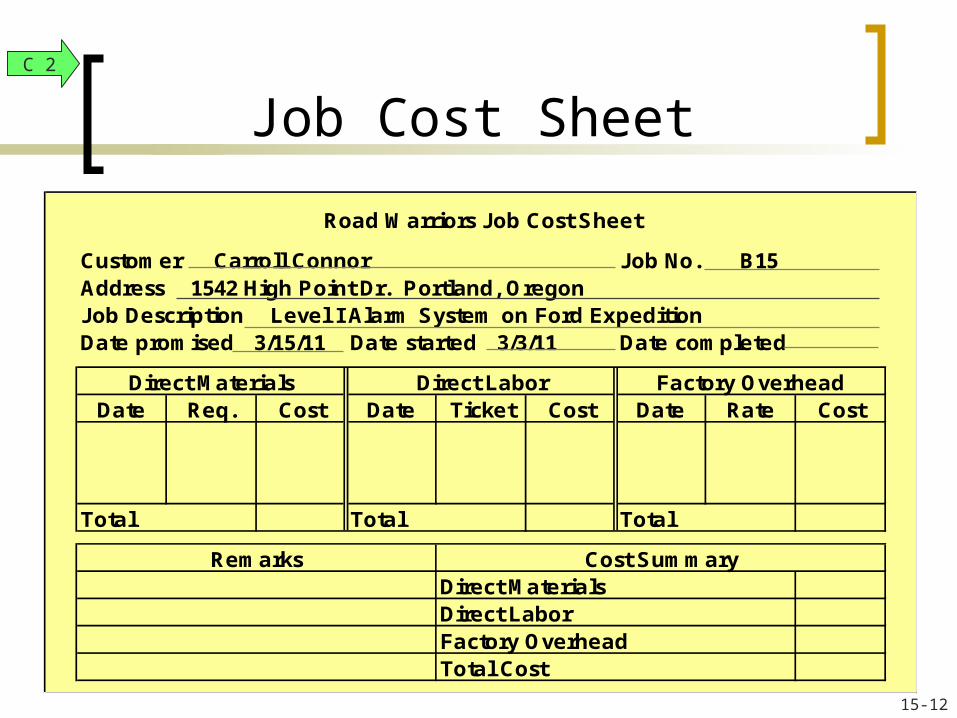

Road Warriors Job Cost Sheet

Customer Carroll Connor Job No. B15Address 1542 High Point Dr. Portland, OregonJob Description Level I Alarm System on Ford Expedition Date promised 3/15/11 Date started 3/3/11 Date completed

Direct Materials Direct Labor Factory OverheadDate Req. Cost Date Ticket Cost Date Rate Cost

Total Total Total

Remarks Cost SummaryDirect MaterialsDirect LaborFactory OverheadTotal Cost

Job Cost SheetC 2

15-12

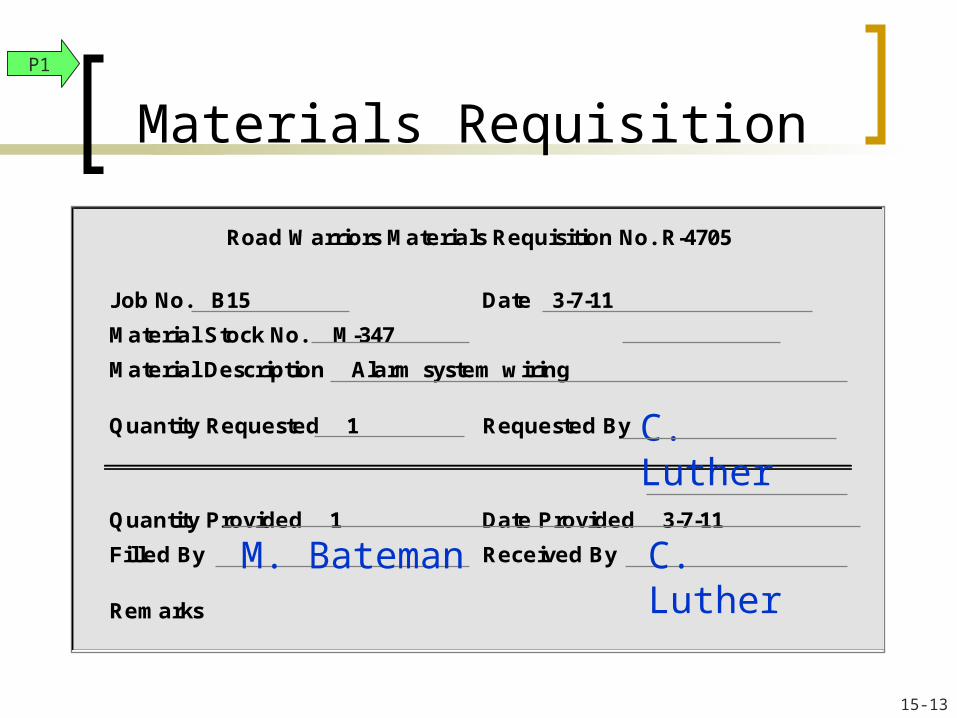

Road Warriors Materials Requisition No. R-4705

Job No. B15 Date 3-7-11

Material Stock No. M-347

Material Description Alarm system wiring

Quantity Requested 1 Requested By

Quantity Provided 1 Date Provided 3-7-11

Filled By Received By

Remarks

C. Luther

C. Luther

M. Bateman

Materials RequisitionP1

15-13

Materials Ledger CardsMaterials

Ledger CardsMaterials Ledger CardsMaterialsRequisition

Direct materials

The materials requisition

indicates the cost of direct materials

to charge tojobs

and the cost of indirect materials

to charge to overhead.

Indirect materials

Job Cost Sheets

Job Cost Sheets

Job Cost Sheets

Job Cost Sheets

Factory Overhead Account

Cost Flows and DocumentsP1

15-14

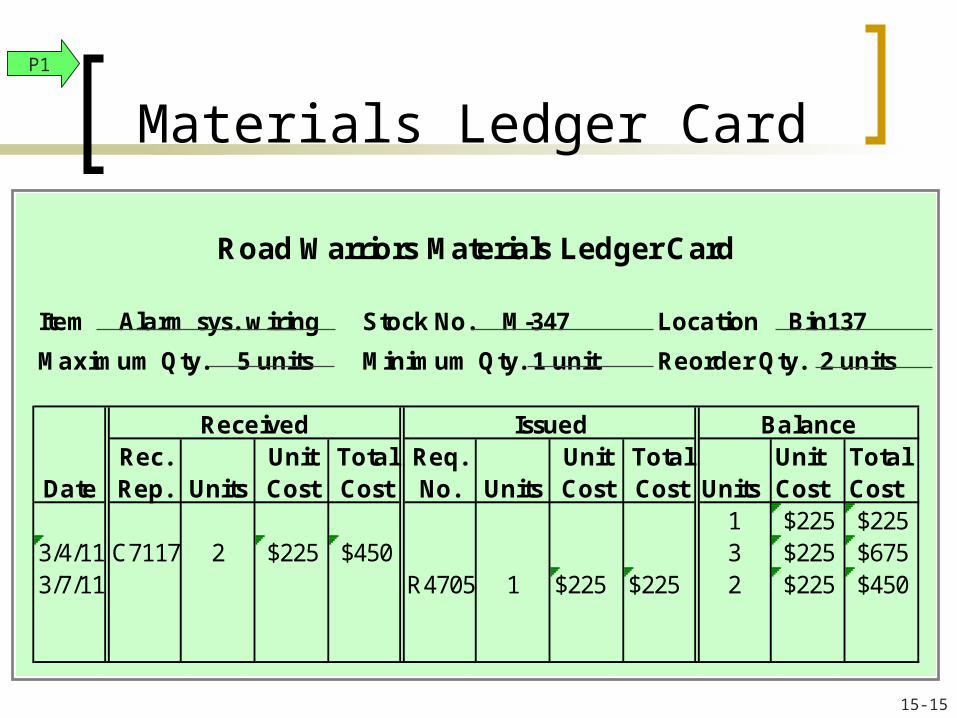

Road Warriors Materials Ledger Card

Item Alarm sys. wiring Stock No. M-347 Location Bin137

Maximum Qty. 5 units Minimum Qty. 1 unit Reorder Qty. 2 units

Received Issued BalanceRec. Unit Total Req. Unit Total Unit Total

Date Rep. Units Cost Cost No. Units Cost Cost Units Cost Cost1 $225 $225

3/4/11 C7117 2 $225 $450 3 $225 $6753/7/11 R4705 1 $225 $225 2 $225 $450

Materials Ledger CardP1

15-15

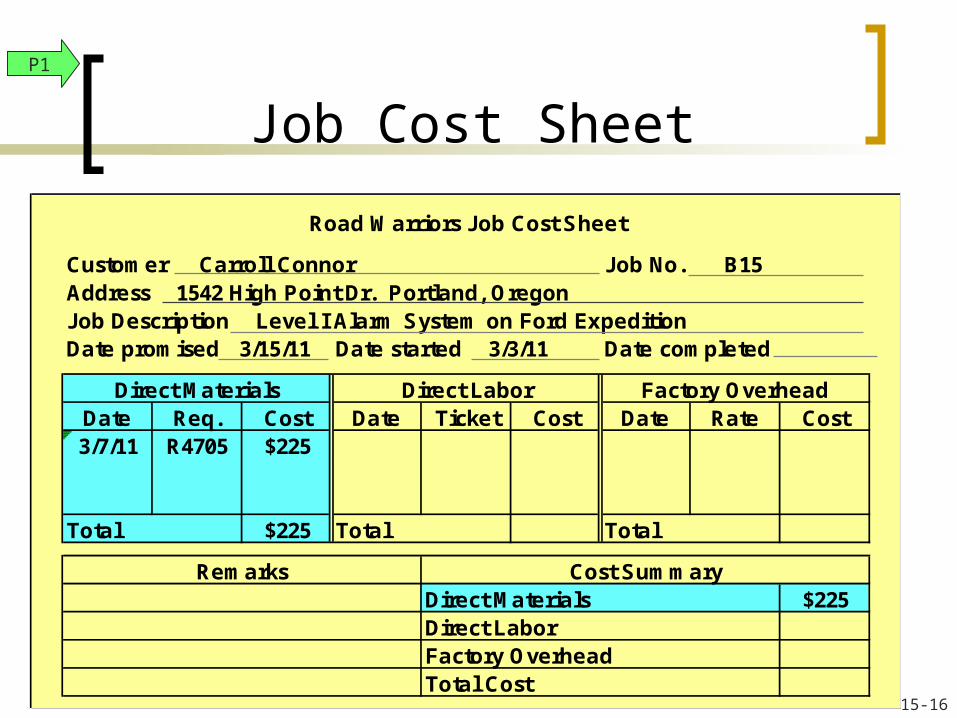

Road Warriors Job Cost Sheet

Customer Carroll Connor Job No. B15Address 1542 High Point Dr. Portland, OregonJob Description Level I Alarm System on Ford Expedition Date promised 3/15/11 Date started 3/3/11 Date completed

Direct Materials Direct Labor Factory OverheadDate Req. Cost Date Ticket Cost Date Rate Cost3/7/11 R4705 $225

Total $225 Total Total

Remarks Cost SummaryDirect Materials $225Direct LaborFactory OverheadTotal Cost

Job Cost SheetP1

15-16

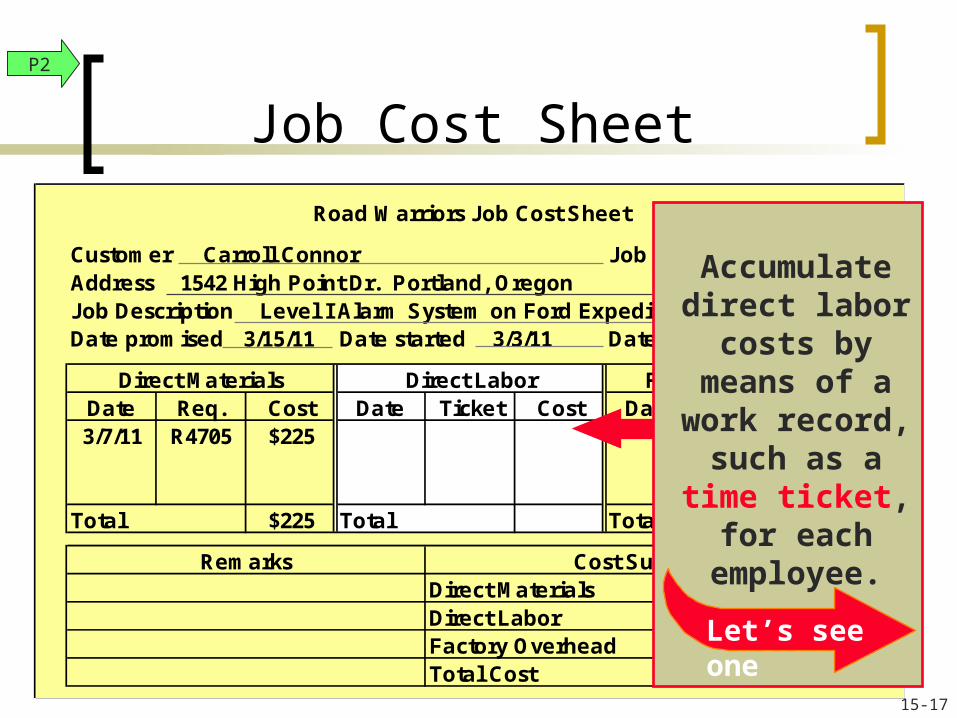

Road Warriors Job Cost Sheet

Customer Carroll Connor Job No. B15Address 1542 High Point Dr. Portland, OregonJob Description Level I Alarm System on Ford Expedition Date promised 3/15/11 Date started 3/3/11 Date completed

Direct Materials Direct Labor Factory OverheadDate Req. Cost Date Ticket Cost Date Rate Cost3/7/11 R4705 $225

Total $225 Total Total

Remarks Cost SummaryDirect Materials $225Direct LaborFactory OverheadTotal Cost

Accumulate direct labor

costs by means of a

work record, such as a time ticket, for each

employee.

Let’s see one

Job Cost SheetP2

15-17

Employee time tickets indicate

the cost of direct laborto charge to

jobsand the cost

of indirect labor to charge to

overhead.

Job Cost Sheets

Factory Overhead Account

Job Cost Sheets

Job Cost Sheets

Job Cost Sheets

Direct Labor

Indirect Labor

Employee Time TicketEmployee Time

TicketEmployee Time TicketEmployee Time

Ticket

P3

Cost Flows and Documents

15-18

Road Warriors Time Ticket No. L-3479

Job No. B15 Date 3/8/11

Employee Name T. Zeller Employee Number 3969

TIME AND RATE INFORMATION:

Start Time 9:00 Finish Time 12:00

Elapsed Time 3.0 Hourly Rate $20.00 Total Cost $60.00

Approved By

RemarksC. Luther

Labor Time TicketP2

15-19

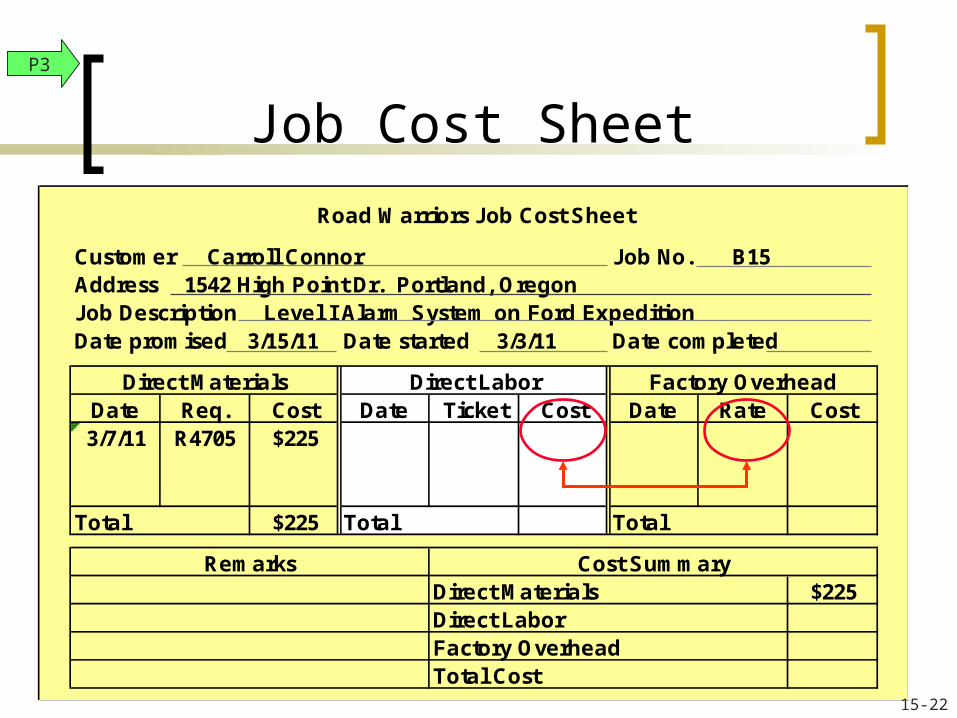

Road Warriors Job Cost Sheet

Customer Carroll Connor Job No. B15Address 1542 High Point Dr. Portland, OregonJob Description Level I Alarm System on Ford Expedition Date promised 3/15/11 Dated started 3/3/11 Date completed

Direct Materials Direct Labor Factory OverheadDate Req. Cost Date Ticket Cost Date Rate Cost3/7/11 R4705 $225 3/8/11 L3479 $60

Total $225 Total $60 Total

Remarks Cost SummaryDirect Materials $225Direct Labor 60Factory OverheadTotal Cost

Job Cost SheetP2

15-20

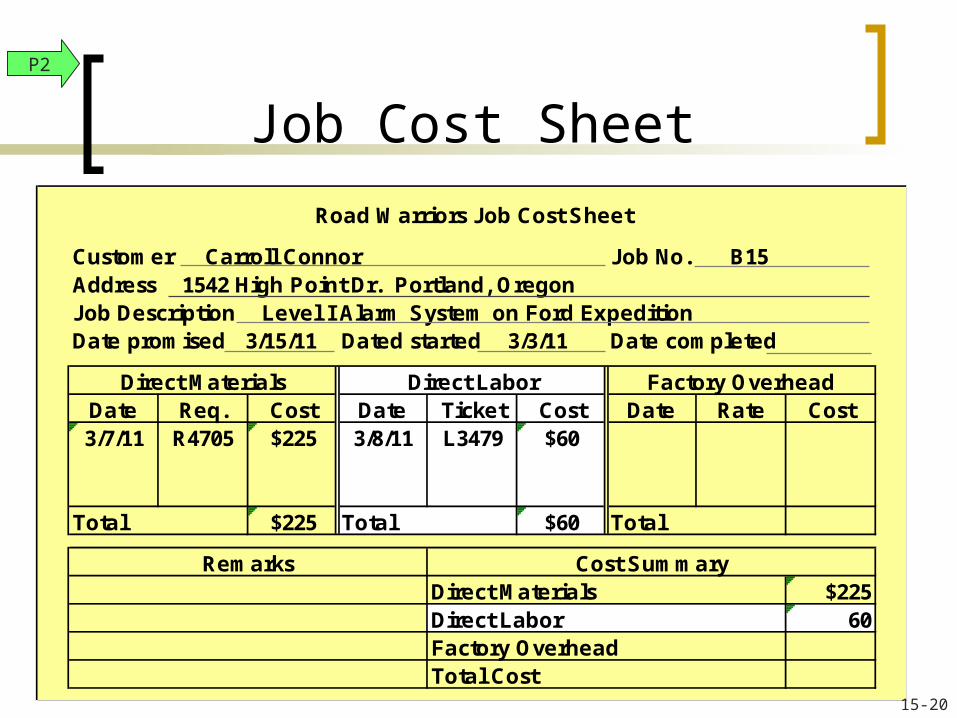

Road Warriors Job Cost Sheet

Customer Carroll Connor Job No. B15Address 1542 High Point Dr. Portland, OregonJob Description Level I Alarm System on Ford Expedition Date promised 3/15/11 Date started 3/3/11 Date completed

Direct Materials Direct Labor Factory OverheadDate Req. Cost Date Ticket Cost Date Rate Cost3/7/11 R4705 $225 3/8/11 L3479 $60

Total $225 Total Total

Remarks Cost SummaryDirect Materials $225Direct Labor 60Factory OverheadTotal Cost

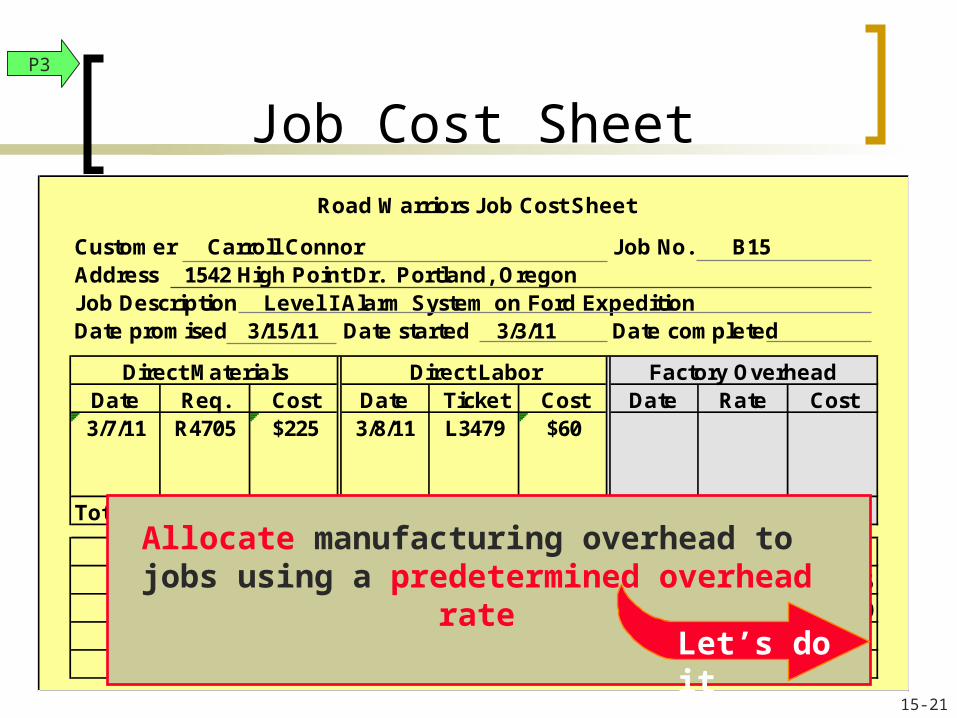

Allocate manufacturing overhead to jobs using a predetermined overhead rate

Let’s do it

Job Cost SheetP3

15-21

Job Cost Sheet

Road Warriors Job Cost Sheet

Customer Carroll Connor Job No. B15Address 1542 High Point Dr. Portland, OregonJob Description Level I Alarm System on Ford Expedition Date promised 3/15/11 Date started 3/3/11 Date completed

Direct Materials Direct Labor Factory OverheadDate Req. Cost Date Ticket Cost Date Rate Cost3/7/11 R4705 $225

Total $225 Total Total

Remarks Cost SummaryDirect Materials $225Direct LaborFactory OverheadTotal Cost

P3

15-22

Road Warriors uses a predetermined overhead rate (POHR) based on direct labor cost to apply overhead to jobs.

Estimated total manufacturingoverhead cost for the coming period

Estimated total direct labor costsfor the coming period

POHR =

POHR = = 160% of direct labor $$200,000

$125,000

Predetermined OverheadAllocation Rate Formula

P3

15-23

MaterialPurchases Direct

MaterialDirect

Material

Raw Materials Goods in Process

Factory Overhead

ActualOverhead

Costs

Indirect Material

P3

Summary of Cost Flows

Dr Cr

Dr Cr Dr Cr

15-24

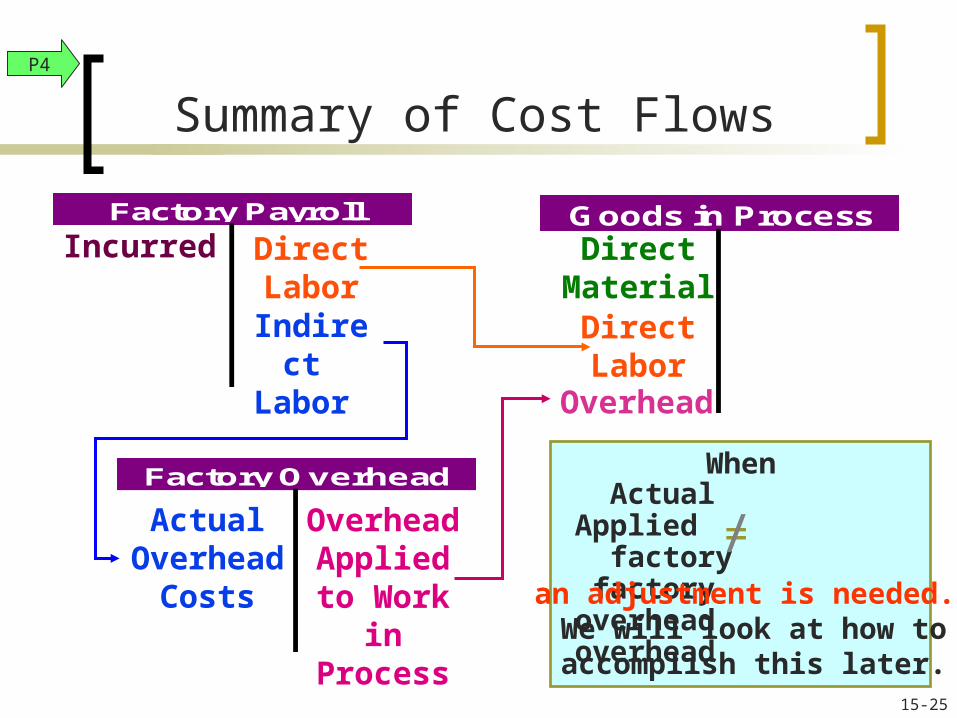

Incurred DirectMaterial

Actual Applied factory factoryoverhead overhead

=/an adjustment is needed.

We will look at how to accomplish this later.

When

Goods in ProcessFactory Payroll

Factory Overhead

DirectLabor

DirectLabor

Indirect Labor

ActualOverhead

Costs

Overhead

OverheadApplied to

Work inProcess

P4

Summary of Cost Flows

15-25

DirectMaterialDirectLabor

Overhead

Cost ofGoodsMfd.

Cost ofGoodsMfd.

Cost ofGoodsSold

Cost ofGoodsSold

Goods in Process Finished Goods

Cost of Goods Sold

P4

Summary of Cost Flows

15-26

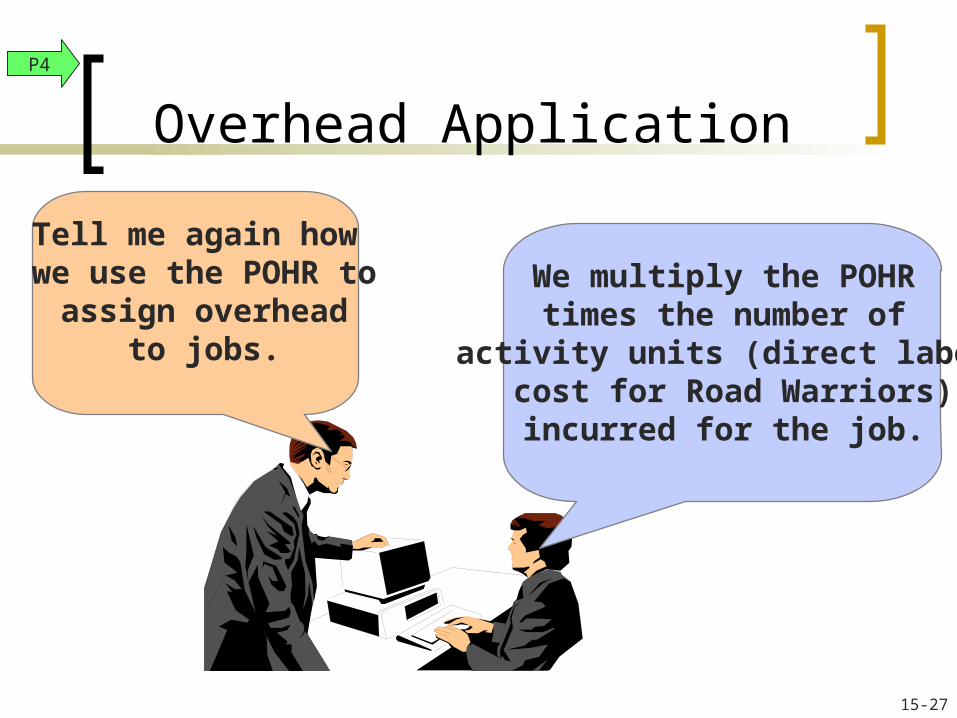

We multiply the POHRtimes the number of

activity units (direct labor cost for Road Warriors)

incurred for the job.

Tell me again how we use the POHR to

assign overhead to jobs.

Overhead ApplicationP4

15-27

Overhead Application

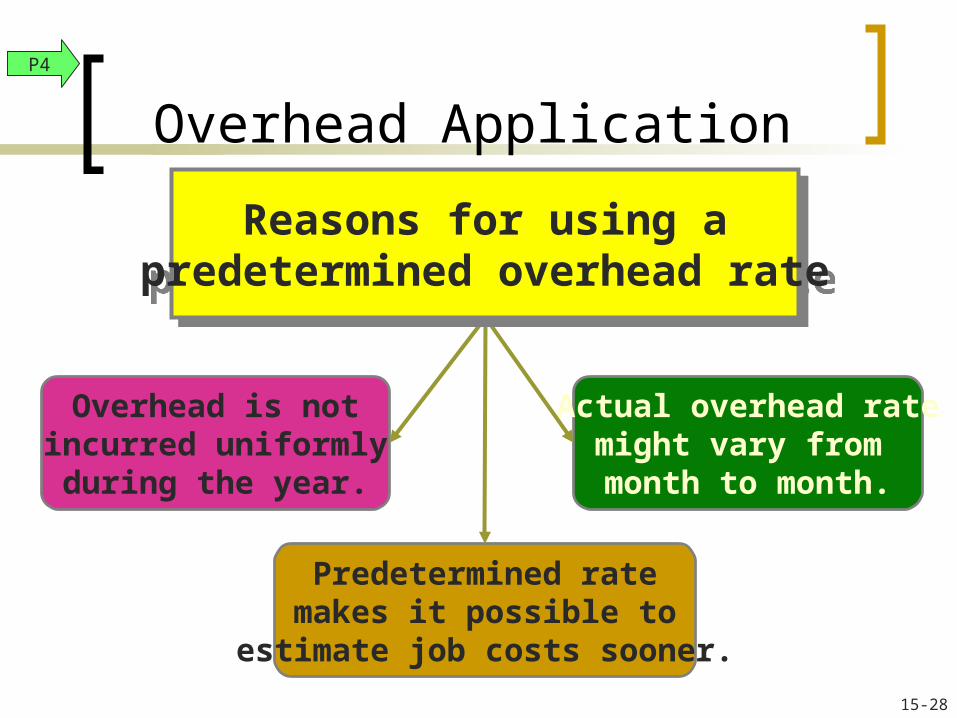

Overhead is notincurred uniformly

during the year.

Actual overhead ratemight vary from month to month.

Predetermined ratemakes it possible to

estimate job costs sooner.

Reasons for using apredetermined overhead rate

Reasons for using apredetermined overhead rate

P4

15-28

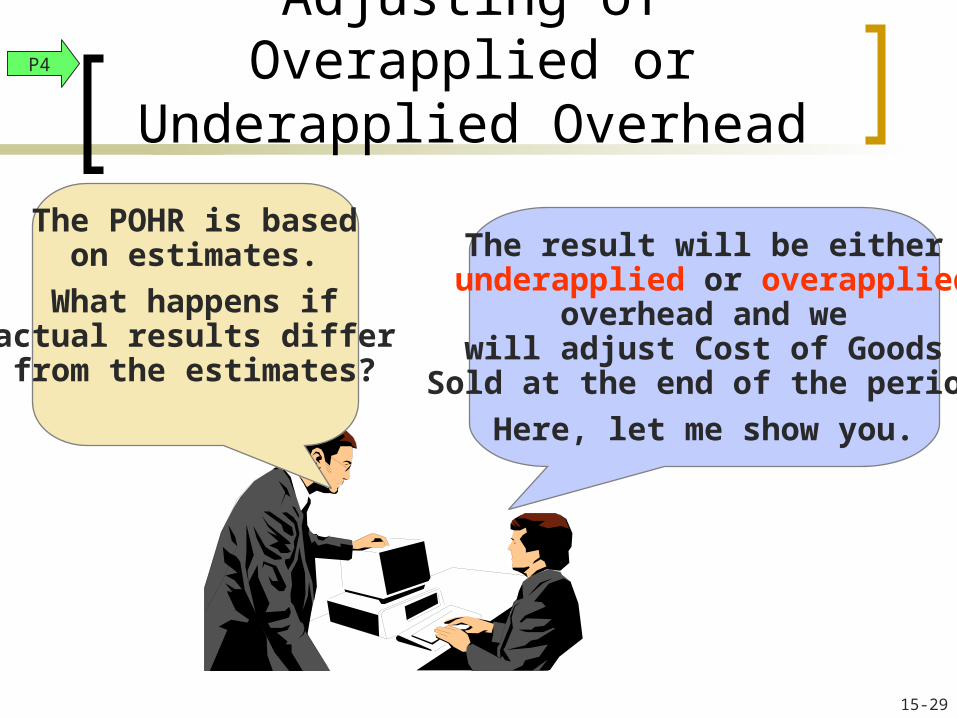

The result will be either underapplied or overapplied

overhead and wewill adjust Cost of Goods

Sold at the end of the period.

Here, let me show you.

The POHR is basedon estimates.

What happens ifactual results differfrom the estimates?

Adjusting of Overapplied or Underapplied Overhead

P4

15-29

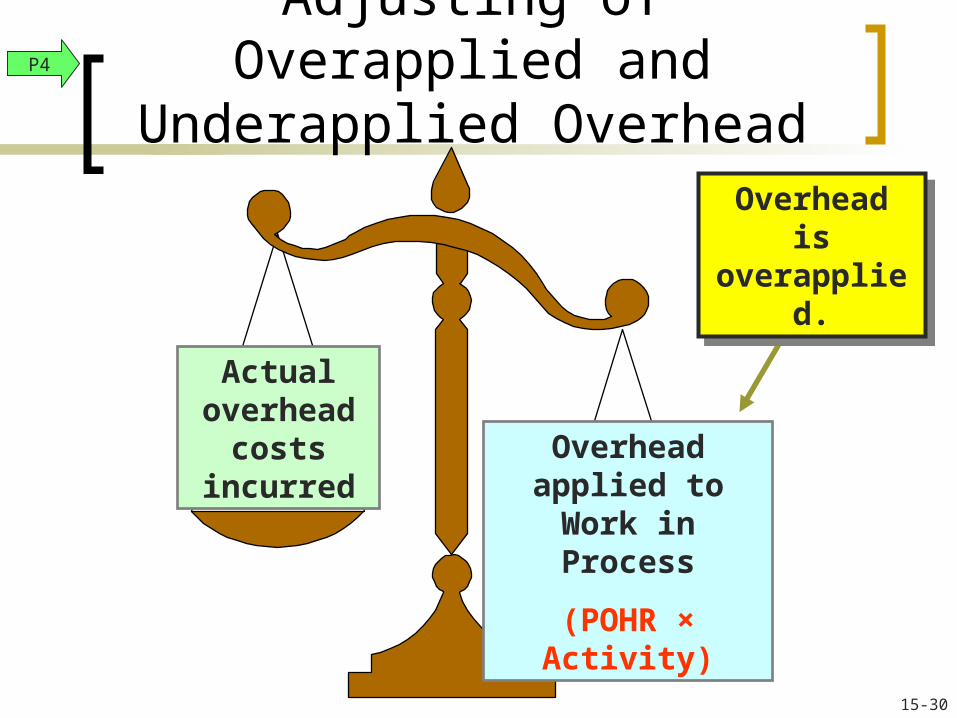

Overhead is overapplied.

Overhead is overapplied.

Overheadapplied to

Work in Process

(POHR × Activity)

Actualoverhead

costsincurred

Adjusting of Overapplied and Underapplied Overhead

P4

15-30

Overhead is underapplied.

Overhead is underapplied.

Actualoverhead

costsincurred

Overheadapplied to

Work in Process

(POHR × Activity)

Adjusting of Overapplied and Underapplied Overhead

P4

15-31

Overhead is: Sold is: Adjustment will:

Actual overhead > applied overhead

Underapplied (Dr. Balance)

Too lowDebit to COGS (Credit FOH)

Actual overhead < applied overhead

Overapplied (Cr. Balance)

Too highDebit to FOH

(Credit to COGS)

Adjusting Cost of Goods Sold for underapplied or overapplied overhead

Adjusting of Overapplied and Underapplied Overhead

P4

15-32

Apply Job Order Costing toPricing Services

Estimate the cost of any supplies (shampoo/conditioner)

Estimate the cost of the labor (stylist’s rate X time of service)

Estimate the amount of overhead to be allocated to all customers

Add a mark up

A typical haircut

15-33