review of varsity football game ticket sales and cash ... · pdf filecall the executive...

TRANSCRIPT

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures

September and October 2012

To be presented to the:

Audit Committee On March 7, 2013

School Board of Broward County, Florida On April 9, 2013

The Nation’s Sixth-Largest School District

The School Board of Broward County, Florida Laurie Rich Levinson, Chair

Patricia Good, Vice Chair

Robin Bartleman Abby M. Freedman

Donna P. Korn Katherine M. Leach

Ann Murray Dr. Rosalind Osgood

Nora Rupert

Robert W. Runcie Superintendent of Schools

The School Board of Broward County, Florida, prohibits any policy or procedure, which results in discrimination on the basis of age, color, disability,

gender, national origin, marital status, race, religion or sexual orientation. Individuals who wish to file a discrimination and/or harassment complaint may call the Executive Director, Benefits & EEO Compliance at 754-321-2150 or

Teletype Machine (TTY) 754-321-2158.

Individuals with disabilities requesting accommodations under the Americans with Disabilities Act (ADA) may call Equal Educational Opportunities (EEO) at

754-321-2150 or Teletype Machine (TTY) 754-321-2158.

www.browardschools.com

Table of Contents

Table of Contents

EXECUTIVE SUMMARY

Pages

Scope, Methodology and Background ............................................................................................. 1-3

Opinion, Summary of Results and Recommendations ........................................................................ 3

OBSERVATIONS

1. Tickets were not torn in half at three schools … ....................................................................... 4-5 2. Lack of accountability for tickets and money ............................................................................ 6-7 3. Security of money / Safety Issues ............................................................................................. 8-9 4. Concession stands / Safety Issues .......................................................................................... 10-11 5. Parking Revenues .................................................................................................................. 12-13 6. Athletic workers / Supplements ............................................................................................. 14-16

EXHIBITS Exhibit A - Summary of Observations. ............................................................................................. 17 Exhibit B - Athletic Directors’ Responsibilities, workshop presentation August 2011 ............... 18-37 Exhibit C - Independent School Related Organization, Letter of Agreement (SPB I-101) ............... 38 Exhibit D - Memo—Booster Clubs/School Allied Organizations and Concessions .................... 39-40 Exhibit E - Department of Athletics and Student Activities Booster Club Guidelines ................ 41-45 Exhibit F - Memo—Supplemental Positions ................................................................................ 46-60 Exhibit G - Photos illustrating safety issues at one football game ............................................... 61-63

FULL TEXT OF ADMINISTRATIVE RESPONSES ............................................................ 64-67

The School Board of Broward County, Florida

Office of the Chief Auditor

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures

September and October 2012

EXECUTIVE SUMMARY

1

EXECUTIVE SUMMARY

Scope and Methodology

In accordance with the 2012-2013 Audit Plan, the Office of the Chief Auditor has performed a Review of Varsity Football Game Ticket Sales and Cash Collection Procedures, for September and October 2012. The objectives of this review were to determine:

Whether current operations and related internal controls have been established and are adequate, pursuant to sound business practice, and are in compliance with applicable laws, regulations, and School Board policies.

To determine whether adequate safeguards exist and are in place for cash collections at District athletic events.

To provide management with recommendations to improve operations, as deemed necessary. This office previously conducted a similar review in 2003, with a follow-up in 2004. Our audit was conducted in accordance with generally accepted auditing standards and Government Auditing Standards, issued by the Comptroller General of the United States. These standards require that we plan and perform the audit to afford a reasonable basis for our judgments and conclusions regarding the function under audit. An audit includes assessments of applicable controls and compliance with the requirements of laws, rules and regulations when necessary to satisfy the audit objectives.

It is our responsibility to perform the review under generally accepted auditing standards and Government Auditing Standards, as well as report on recommendations to improve operations, strengthen internal controls and ensure compliance with the requirements of laws, rules and regulations in matters selected for review. It is administration’s responsibility to implement recommendations, to maintain an internal control environment conducive to the safeguarding of District assets and to preserve the District’s resources, as well as comply with applicable laws, regulations and School Board policies.

The procedures used to satisfy our objectives in this audit were to:

Attend a sample of Athletic varsity football games and perform audit procedures. Interview involved parties associated with Athletic activities. Review Standard Practice Bulletins, School Board Policies and Athletic Directors’

Responsibilities Guidelines. Perform other auditing procedures as deemed necessary.

Background

Office of the Chief Auditor staff members attended and observed fifteen varsity football games in September and October, 2012, and performed cash counts at the close of ticket sales at ten of the games. This required us to observe ticket selling and ticket taking practices; count the unused tickets, ticket sales revenues, and change fund in each ticket seller’s cash box; and reconcile tickets sold with monies collected. We also obtained ticket sales reports, and traced the ticket revenues to a receipt in the school’s

School Board of Broward County, Florida Office of the Chief Auditor

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures September and October 2012

2

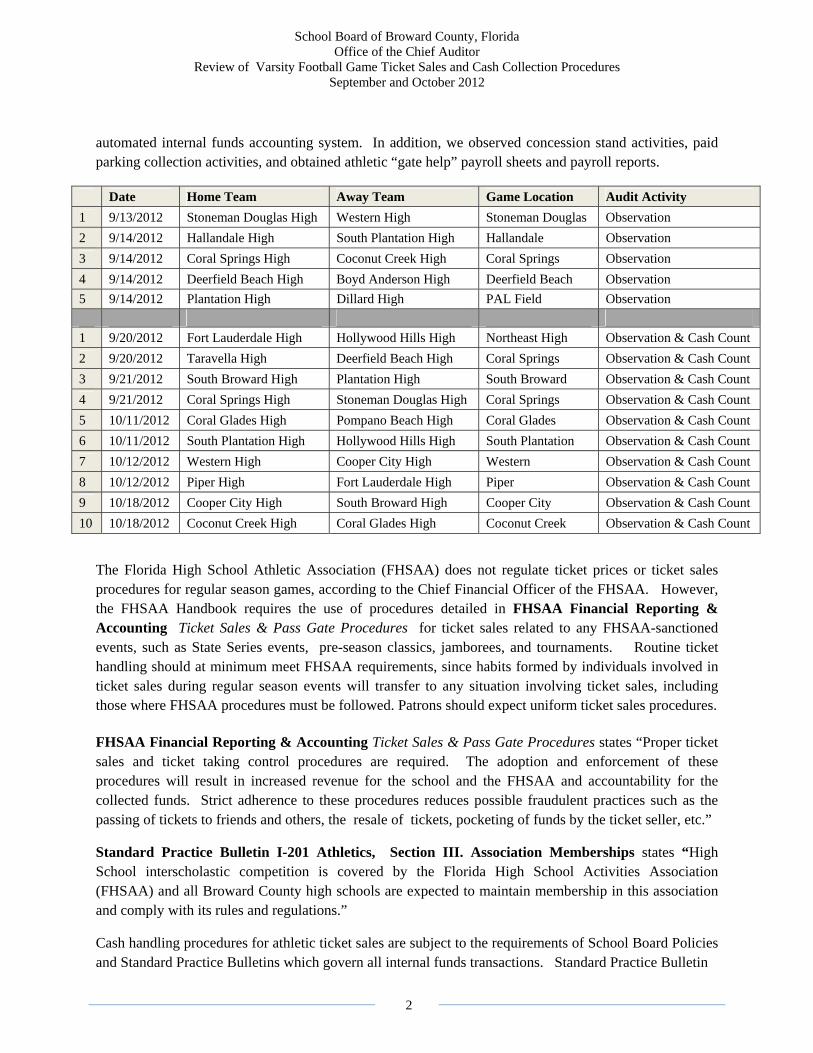

automated internal funds accounting system. In addition, we observed concession stand activities, paid parking collection activities, and obtained athletic “gate help” payroll sheets and payroll reports.

Date Home Team Away Team Game Location Audit Activity

1 9/13/2012 Stoneman Douglas High Western High Stoneman Douglas Observation

2 9/14/2012 Hallandale High South Plantation High Hallandale Observation

3 9/14/2012 Coral Springs High Coconut Creek High Coral Springs Observation

4 9/14/2012 Deerfield Beach High Boyd Anderson High Deerfield Beach Observation

5 9/14/2012 Plantation High Dillard High PAL Field Observation

1 9/20/2012 Fort Lauderdale High Hollywood Hills High Northeast High Observation & Cash Count

2 9/20/2012 Taravella High Deerfield Beach High Coral Springs Observation & Cash Count

3 9/21/2012 South Broward High Plantation High South Broward Observation & Cash Count

4 9/21/2012 Coral Springs High Stoneman Douglas High Coral Springs Observation & Cash Count

5 10/11/2012 Coral Glades High Pompano Beach High Coral Glades Observation & Cash Count

6 10/11/2012 South Plantation High Hollywood Hills High South Plantation Observation & Cash Count

7 10/12/2012 Western High Cooper City High Western Observation & Cash Count

8 10/12/2012 Piper High Fort Lauderdale High Piper Observation & Cash Count

9 10/18/2012 Cooper City High South Broward High Cooper City Observation & Cash Count

10 10/18/2012 Coconut Creek High Coral Glades High Coconut Creek Observation & Cash Count

The Florida High School Athletic Association (FHSAA) does not regulate ticket prices or ticket sales procedures for regular season games, according to the Chief Financial Officer of the FHSAA. However, the FHSAA Handbook requires the use of procedures detailed in FHSAA Financial Reporting & Accounting Ticket Sales & Pass Gate Procedures for ticket sales related to any FHSAA-sanctioned events, such as State Series events, pre-season classics, jamborees, and tournaments. Routine ticket handling should at minimum meet FHSAA requirements, since habits formed by individuals involved in ticket sales during regular season events will transfer to any situation involving ticket sales, including those where FHSAA procedures must be followed. Patrons should expect uniform ticket sales procedures.

FHSAA Financial Reporting & Accounting Ticket Sales & Pass Gate Procedures states “Proper ticket sales and ticket taking control procedures are required. The adoption and enforcement of these procedures will result in increased revenue for the school and the FHSAA and accountability for the collected funds. Strict adherence to these procedures reduces possible fraudulent practices such as the passing of tickets to friends and others, the resale of tickets, pocketing of funds by the ticket seller, etc.”

Standard Practice Bulletin I-201 Athletics, Section III. Association Memberships states “High School interscholastic competition is covered by the Florida High School Activities Association (FHSAA) and all Broward County high schools are expected to maintain membership in this association and comply with its rules and regulations.”

Cash handling procedures for athletic ticket sales are subject to the requirements of School Board Policies and Standard Practice Bulletins which govern all internal funds transactions. Standard Practice Bulletin

OBSERVATIONS

School Board of Broward County, Florida Office of the Chief Auditor

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures September and October 2012

4

OBSERVATION 1. TICKETS WERE NOT TORN IN HALF AT THREE SCHOOLS

a) Tickets were not torn in half by ticket takers at four football games, but were placed whole in collection bags. Patrons consequently did not receive a ticket stub. This practice creates the potential for re-sale of unaccountable tickets.

b) At one of these schools, thirty-five $5 tickets, which had been listed on a ticket report as previously used on August 31, 2012, were found in the ticket takers’ gate entry collection bags at a football game on October 12, 2012. One of the possible causes of such an occurrence might be the re-sale of unaccounted tickets, which could result in sales revenues not being recorded.

BACKGROUND

Standard Practice Bulletin I-201 Athletics, Section II. Athletic Director’s Responsibilities, states “All tickets presented for admission to an athletic event must be torn in half upon presentation at the event entry area. Under no circumstances may a used ticket be resold!” Standard Practice Bulletin I-403 Admission Tickets/Ticket Report, Section II. Ticket Usage, A. Athletic Tickets states “All tickets presented for admission to an event must be torn in half upon presentation for entry to the event.”

FHSAA Financial Reporting & Accounting Ticket Sales & Pass Gate Procedures states “Ticket takers should take the ticket and tear it in half and give one half to the person entering the event and keep the other half. The half that is retained by the school should be kept secure and remain with the documentation from the event. This ensures that the tickets cannot be resold or used by another person for entrance. No one should ever pay and enter one of these events without receiving a ticket from the ticket seller and their half of the torn ticket from the ticket taker… No one should be allowed to leave the event and re-enter with a ticket stub… This cuts down on the passing of ticket stubs to others for entrance to the event.”

RECOMMENDATION

We recommend that tickets always be torn in half, with one half returned to the patron. Bags of collected ticket stubs should be retained by the school’s bookkeeper for audit. This control procedure enhances accountability for ticket sales and prevents the re-sale of used tickets.

School Board of Broward County, Florida Office of the Chief Auditor

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures September and October 2012

5

MANAGEMENT RESPONSE

We concur with this recommendation. Game tickets shall always be torn in half with one half returned to the patron. Also, accountability for ticket sales and inventory of tickets will be strengthened. A comprehensive review of audit recommendations will be held with high school athletic directors on April 5, 2013 at Pompano Beach High. Representatives from the Audit Department will be on hand to assist with this review. The training will be facilitated by the Department of Athletics and Student Activities.

The Director of Athletics and Student Activities will further meet with all high school Principals on March 21, 2013 at McArthur High to review all the observations and recommendations of the audit report.

.

School Board of Broward County, Florida Office of the Chief Auditor

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures September and October 2012

6

OBSERVATION 2. LACK OF ACCOUNTABILITY FOR TICKETS AND MONEY

a) At two football games, we noted staff, including an Athletic Director (AD) and Assistant Athletic Director, walking around selling tickets outside the stadium entrance gates. This practice defeats the accountability for tickets and money created by assigning a cash box containing known tickets and an established change fund to an individual ticket seller.

1. Additionally, since the Athletic Director has the responsibility of reconciling the tickets sold and the money deposited, proper segregation of duties requires that the AD not be a ticket seller. 2. It is also inadvisable to accustom patrons to the idea of purchasing tickets from individuals who are not official ticket sellers selling from a marked location.

b) Two official, paid ticket sellers were selling out of a single assigned cash box at one school. This

practice eliminates responsibility and accountability for tickets and cash.

c) Amounts of money contained in cash boxes and ticket numbers being distributed were generally not being recorded, verified, nor signed for receipt, when money and tickets changed hands. We did not observe a manifest or transmittal form detailing the contents of the cash boxes and ticket numbers being conveyed, with signatures indicating verification, when the cash and tickets changed hands, at nine of the ten cash counts conducted. In one case, the ticket sellers had completed and signed a form listing the cash and ticket numbers being turned in after the game, however there was no verification at the time the cash boxes and tickets changed hands. Verification and signing for receipt should occur when the Athletic Director distributes the change fund and tickets to each ticket seller, and again after the game when the ticket sellers return the cash boxes, with money collected for ticket sales and unsold tickets, to the Athletic Director. Without following verification and documentation procedures, it is impossible to fix accountability for the money and tickets distributed to ticket sellers. In cases where the ticket sellers do not independently verify and document their ticket sales, the Athletic Director completely controls the amount of ticket revenue reported. Lack of accountability greatly increases the risk that all money collected will not be deposited into the school’s internal accounts.

d) We were informed by five Athletic Directors that money collected and tickets returned were not normally being counted immediately following each game.

e) At three schools, the Athletic Director could not remember how much money had been placed in the cash boxes as a change fund before the boxes were handed over to the ticket sellers. Since no verification of cash or tickets had occurred or been recorded when the cash and tickets changed hands, there was no evidence documenting how much money should have been in the cash boxes. A $45 shortage in ticket revenues was subsequently documented by the Athletic Director.

School Board of Broward County, Florida Office of the Chief Auditor

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures September and October 2012

7

BACKGROUND

FHSAA Financial Reporting & Accounting Ticket Sales & Pass Gate Procedures states “A reconciliation should be conducted at the finish of each event or shift to ensure that the funds were properly handled and that no funds are missing for the number of tickets sold.”

RECOMMENDATION

We recommend that a standard cash box manifest form (see page 23 of Exhibit B) be created by the Internal Accounts Department and attached to Standard Practice Bulletin I-201 as an exhibit. The form should contain spaces for the Athletic Director to note the numbers of the tickets being assigned to the ticket seller, and the composition of the change fund being delivered to the ticket seller with the cash box. It should also have spaces for the ticket seller to record the cash and tickets being returned to the Athletic Director after the game, with spaces for the ticket seller and Athletic Director to sign in confirmation that they have verified the tickets and cash together, before and after the game.

Standard Practice Bulletin I-201 should be revised to include a requirement that each ticket seller be assigned a separate cash box, change fund, and tickets, accessible to no one other than the assigned ticket seller. Standard Practice Bulletin I-201 should also be revised to forbid the selling of tickets by anyone other than designated ticket sellers who have been assigned documented cash and specific documented tickets and who are selling tickets in a fixed official location. Specifically, Athletic Directors should not be selling tickets at athletic events.

Athletic Directors should review and follow Standard Practice Bulletins I-101, 1-201, 1-302, and 1-403 and Athletic Directors’ Responsibilities guidelines, and strengthen internal controls over ticket sales and cash collections procedures.

MANAGEMENT RESPONSE

We concur with this recommendation. Athletic directors should not be selling tickets the day of the game at athletic events. Since the athletic director has the responsibility of reconciling the tickets sold and the money deposited, proper segregation of duties should be followed. In addition, athletic directors may be involved in the presale of tickets for games where large crowds are expected. All pre-sale monies and remaining tickets will be turned in to the Bookkeeper prior to the game.

The Director of Athletics and Student Activities will confer with the Director of the Business Support Center to revise Standard Practice Bulletin I-201 to strengthen internal controls over ticket sales and cash collection procedures.

School Board of Broward County, Florida Office of the Chief Auditor

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures September and October 2012

8

OBSERVATION 3. SECURITY OF MONEY / SAFETY ISSUES

a) In at least one instance, we observed that the Athletic Director did not have access to a reliable safe to secure the cash receipts.

b) We also noted in one instance, when the Athletic Director stored the cash collected in the bookkeeper’s vault, there was no separate secure locker inside the vault where the Athletic Director could store the money until such time as it could be counted with the bookkeeper. Leaving unreceipted money in a vault where more than one person has access to it eliminates accountability for the money.

c) At one school where money was routinely not counted immediately after each game, we noticed the Athletic Director had some difficulty opening the bookkeeper’s vault, and there was no separate locker for the Athletic Director’s use inside the vault. During this school’s routine internal funds audit, we could not trace approximately $6,000 recorded on a ticket report in the fall of 2010 to a receipt or a deposit on the school’s bank statements.

d) We also noted in two cases, money was moved around the school building and parking lot after the football game without the accompaniment of a police officer. Personal safety requires a security escort when money is being handled under such circumstances.

BACKGROUND Standard Practice Bulletin I-201 Athletics, Section II. Athletic Director’s Responsibilities, F. Gate Receipts states “All monies generated from the sale of pre-numbered tickets for athletic events must be kept in a secured area until presented to the bookkeeper for receipting and depositing. It is strongly advised if access cannot be obtained to the school vault, then a safe be obtained for the Athletic Director’s office for the safekeeping of the collections until deposited with the bookkeeper…If an athletic event is held at a location other than the host school’s location, then arrangements have to be made to transport the collections back to the host school’s location for safekeeping in a safe (immediately after reconciling the money to the Report of Tickets sold) or arrangements made with the host school’s bank for a night deposit. Under no circumstances are collections to be safe kept in an individual’s possession at their home or in their car.” RECOMMENDATIONS

We recommend that secure storage arrangements be implemented for handling money received when the school’s bookkeeper is not available, such as a reliable safe in the Athletic Director’s office and/or a separate locker, with an operating lock, installed inside the bookkeeper’s vault. In this way accountability for money rests with the Athletic Director until such time as the funds are presented to the school’s Bookkeeper for receipting. As a matter of personal safety, we also recommend that a police officer be enlisted to attend movement of cash boxes, counting and verification of money and tickets, and securing of money in a safe after each game.

School Board of Broward County, Florida Office of the Chief Auditor

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures September and October 2012

9

MANAGEMENT RESPONSE

We concur with this recommendation. The district provides funding for the deployment of police officers at high school football games. As a matter of personal safety, a police officer will be enlisted to attend movement of cash boxes, counting and verification of money and tickets and securing of money in a safe after each game.

School Board of Broward County, Florida Office of the Chief Auditor

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures September and October 2012

10

OBSERVATION 4. CONCESSION STANDS / SAFETY ISSUES

a) The Florida Department of Health requires inspection and permitting of school concession stands. Food handling and food hygiene practices may also be subject to inspection by the Broward County Department of Public Health. According to County Health Department officials, only one school concession stand has been inspected by the Broward County Department of Public Health to date.

b) We also noted grills, positioned in locations of heavy foot traffic, being used to cook chicken or hamburgers at four schools. At one of these schools, we observed containers of lighter fluid in use, and kettles full of hot oil being used to cook French fries over open flames.

c) In schools where booster clubs were running a concession stand, we found that no school was able to provide us with an adequate agreement with the booster club which required the booster club to report the amount of money collected to the school, or which detailed the booster club’s proposed use of the funds collected.

BACKGROUND

The Florida Department of Health has published Florida Administrative Code 64E-11 detailing regulations on Food Hygiene and requirements for food handling. This regulation specifically includes “small, seasonally operated concession stands at schools” within its scope.

Standard Practice Bulletin A-429 Rental of School Board Facilities states “All food received and used by students must be prepared or purchased from services approved by the Broward County Health Department. Food prepared in a private home cannot be used or offered for sale to students.”

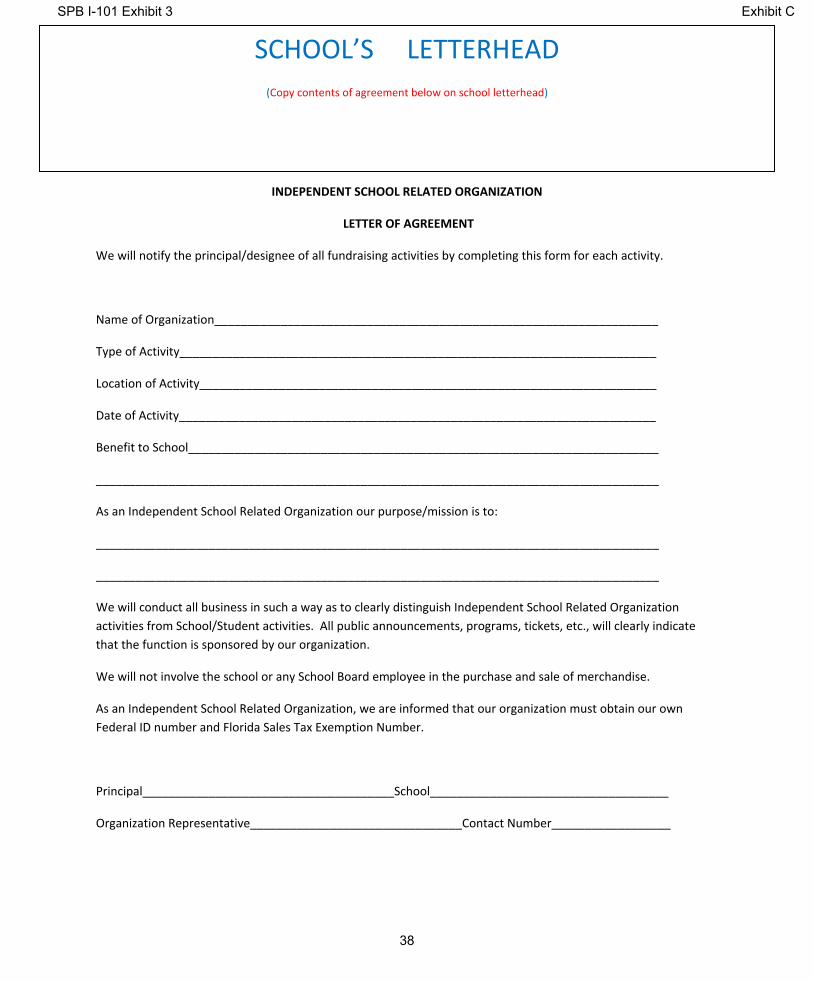

Standard Practice Bulletin I-101 General Policy states “All school-related activities must be approved by the Principal and be beneficial to students…If the school-related activity is sponsored by the ISRO (Independent School-Related Organization) and a share of the proceeds is to be disbursed to the school, a Letter of Agreement must be executed prior to the start of the activity.” (See Exhibit C.)

Department of Athletics and Student Activities Booster Club Guidelines states “If a booster club utilizes a school facility for fundraising purposes, and elects to charge students or parents, the booster club must provide the affected principal a projection of revenues prior to the scheduled event and a statement of actual revenues after the event. At the end of each school year, the booster club must provide the affected principal a written summary statement regarding fundraisers conducted on/in school grounds/facilities. The statement shall include how the funds were raised, accumulated revenue minus expenditures, and how the funds raised were expended to support public school activities. Failure to provide this information may result in the school principal refusing to allow the booster club use of School Board facilities.” Booster Club Guidelines also states “The booster club shall keep financial records of all concession expenditures, sales, purchases, and revenue. The concession financial records shall be made available to the principal upon request. The booster club shall provide written documentation that concession revenue is directly spent to support student activities.”

School Board of Broward County, Florida Office of the Chief Auditor

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures September and October 2012

11

A memo from the Director, Athletics and Student Activities, dated October 25, 2004, titled Booster Clubs/School Allied Organizations and Concessions states “A letter of understanding on school stationery, signed by the school’s Principal and the President of the Booster/Band organization must outline how the concession revenue will be spent. Specifically, all revenue must be spent to directly benefit and support students. The letter of understanding must address the general categories that revenue will be spent on. For example, if the band organization is running the concession stand, the letter of understanding may reflect that concession revenue will be spent on uniforms, uniform cleaning, transportation for band competitions, etc….it is recommended that all booster clubs/band organizations that operate concession stands on school property, submit, in a timely fashion during the school year, a full written account of revenues and expenditures on students.”

RECOMMENDATIONS

We recommend that the Director of Athletics and Student Activities ensure that administrators of each school with a concession stand contact the Broward County Health Department and the Florida Department of Health for an evaluation of the need for an inspection and permit at each location, to include assessment of any special food handling requirements. We also recommend that safety parameters be established for the use of grills on school property, if their continued use is allowed.

We also recommend that booster clubs complete a letter of understanding, approved by the school’s Principal prior to engaging in fundraising activities. Such a letter of understanding should require the booster club to report the amount of money collected to the school, and detail the booster club’s proposed use of the funds collected.

MANAGEMENT RESPONSE

We concur with the recommendation that booster clubs complete a letter of understanding approved by the school’s principal listing their fundraising activities. The letter of understanding shall be provided prior to engaging in fundraising activities.

We concur with the recommendation that safety parameters be established for the use of grills on school property. The Safety Department has developed a list of guidelines for the operation of BBQ’s at athletic events. The guidelines will be shared and reviewed with the high school athletic directors at the April 5, 2013 training. Further, an e-mail was sent to all high school athletic directors on September 19, 2012 regarding the prohibition of using boiling oil for cooking french fries (see attached safety guidelines on grilling and boiling oil).

The Department of Safety is conducting a follow-up meeting March 19, 2013 with appropriate staff on concession stands at Broward County schools. The Broward County Health Department and the Florida Department of Health have the authority to inspect and permit all football concession stands at any time.

School Board of Broward County, Florida Office of the Chief Auditor

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures September and October 2012

12

OBSERVATION 5. PARKING REVENUES

Money was collected for parking on school property, at every football game visited.

a) In six instances, the organization and/or individual collecting parking money was not identified to patrons at all.

b) Cash handling was largely uncontrolled, and tickets or other receipting measures were not used at nine locations.

c) In one case, two different individuals approached our vehicles asking for different amounts of money.

d) Most schools were unable to provide us with an adequate agreement with a booster club collecting parking money which required the booster club to report the amount of money collected to the school, or which detailed the booster club’s proposed use of the funds collected.

The absence of controls and receipting procedures in most cases means that the amount of cash that is collected for parking cannot be reliably determined by either the school’s administration or the organization collecting the money.

We note that the FHSAA bylaws assign extensive responsibility for Booster Clubs’ compliance with the rules, regulations, and bylaws of the FHSAA to the school’s Principal.

BACKGROUND

Standard Practice Bulletin I-101 General Policy, Section IV. Employee Restrictions states “School Board employees are NOT allowed to collect or handle money for ISRO (Independent School Related Organization) sponsored activities and Non-School Board employees are not allowed to handle money of school sponsored activities….

Standard Practice Bulletin I-101 General Policy, Section VI. Independent School Related Organizations states “To avoid violations of School Board Policy, activities sponsored by Independent School Related Organizations should be conducted in such a way that they are clearly distinguished from student activities...These organizations:… Must reflect the organization’s name on all programs, flyers, or other promotional material for activities sponsored by the organization…All public announcements, programs, tickets, etc., should clearly designate the activity as an activity of the independent organization.” Standard Practice Bulletin I-201 Athletics, Section III. Association Memberships states “High School interscholastic competition is covered by the Florida High School Activities Association (FHSAA) and all Broward County high schools are expected to maintain membership in this association and comply with its rules and regulations.”

School Board of Broward County, Florida Office of the Chief Auditor

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures September and October 2012

13

2012-2013 Florida High School Athletic Association Handbook, Bylaws, Article 3.5—Obligations of Membership states:

3.5.1 Administrative Control. A member school must control its interscholastic athletic programs in accordance with the regulations of the Association. Responsibility for this control rests with the principal, who is responsible for the administration of all aspects of the school’s interscholastic programs.

3.5.1.1 Scope of Responsibility. Responsibility for control of a school’s interscholastic athletic programs extends to and includes the education of, responsibility for and control over the actions of the school’s administration, faculty, athletic staff, student-athletes, student body, and any other individual or group engaged in activities representing, supporting or promoting the athletic interests of the school.

3.5.2 Compliance with rules. A member school must comply with all bylaws and other rules of the Association. The school must monitor its athletic programs to assure compliance with all bylaws and regulations, must identify and report to the FHSAA Office instances in which compliance has not been achieved, and must take appropriate corrective actions regarding such instances of non-compliance. Staff members, student-athletes and other individuals and groups representing, supporting or promoting the school’s athletic interests must comply with all applicable bylaws and rules. The school is responsible for such compliance.

RECOMMENDATION

Parking revenues are generated using taxpayer-funded school property, with no “cost of goods sold” or inventory to maintain, and minimal labor required. Parking collections should be regulated by school personnel, using proper receipting and other control procedures, such as using prenumbered parking tickets, accounting for parking tickets on ticket reports, maintaining ticket issuance log and parking ticket inventory. Proceeds should be deposited directly into the school’s athletic internal funds account, to be expended under the supervision of each school’s Principal.

MANAGEMENT RESPONSE

We concur with the recommendation that parking should be regulated by school personnel; however, it is understood that high schools may also use booster clubs for parking fundraisers. As a best practice, schools should collect fees as a school fundraising activity, with parking revenues deposited into the schools’ internal funds. When school personnel are utilized, all proceeds are deposited into the school’s internal funds. When school booster clubs perform parking duties, funds may be deposited in the booster account. The booster club will notify the athletic director or school principal in writing the amount of funds collected and provide a ticket report.

School Board of Broward County, Florida Office of the Chief Auditor

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures September and October 2012

14

OBSERVATION 6. ATHLETIC WORKERS / SUPPLEMENTS

a) At one school, the wife of the Athletic Director was paid $940 as an athletic event worker between July 1, 2011 and June 30, 2012. The Athletic Director also paid himself $510 as an Athletic Event Worker during the same period of time (this does not include $200 he was paid as an Event Supervisor, which is permitted as stated on the School Activities Unit Price Salary Schedule.)

b) The Athletic Director paid her son $905 as an athletic event worker between July 1, 2011 and June 30, 2012, at another school.

c) At a third school, the assistant Athletic Director, who is in charge of athletic event workers and their payroll, paid his daughter $545 as an athletic event worker between July 1, 2011 and June 30, 2012.

d) The wife of the Athletic Director was paid $230 as an athletic event worker during the 2011-2012 school year, at a fourth school.

e) In one instance, two persons paid as ticket takers did not sign in on the athletic payroll signature sheet on the night of the game, making it difficult to substantiate whether they were there.

f) We noted a Head Football Coach also received the Assistant Athletic Director supplement for the 2011-2012 school year and the Athletic Director supplement for the 2012-2013 school year.

BACKGROUND

School Board Policy 6210 Supplements states “No person shall receive more than one supplement for duties performed simultaneously with the duties for which another supplement is paid, i.e., an employee cannot receive pay for two supplements for the same hour(s) of work.”

Supplement Guidelines 12/18/2012 states “An employee cannot receive compensation for two supplemental positions for the same hours of work or performed at the same time (i.e. it is not permissible to compensate someone as Athletic Director and a football coach).” Supplement Guidelines also states “Athletic Directors must relinquish their supplement during the season if they wish to receive a supplement for coaching.”

School Board Policy 4002.10 Nepotism/Employment and Assignment of Relatives states “It is the intent of this policy to avoid any situation or occurrence that creates or gives the appearance of a conflict of interest either on the part of a School Board Member or an employee of the school district. The purpose of this policy is to provide guidelines to maintain an equitable work environment and to prevent and address conflict of interest situations of active or potential employees relating to employment, job assignment, promotion, supervision, and evaluation of employees… The terms "related" or "relative" shall refer to father, mother, son, daughter, brother, sister, uncle, aunt, first cousin, nephew, niece, husband, wife, father-in-law, mother-in-law, son-in-law, daughter-in-law, brother-in-law, sister-in-law,

School Board of Broward County, Florida Office of the Chief Auditor

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures September and October 2012

15

stepfather, stepmother, stepson, stepdaughter, stepbrother, stepsister, half-brother, half-sister, grandfather, grandmother, grandchild, court-appointed legal guardian, ward of employee, or domestic partner or any persons who reside at the same residence as the School Board member or School District employee… The term "directly supervise" shall relate to those situations in which a School Board member or School District employee is directly responsible for another full-time, part-time or temporary employee’s appointment, employment, promotion, demotion, job assignments, overtime/ payroll authorization or job performance evaluation…A School Board member or School District employee shall not advance, advocate for or participate in any personnel action, including recommendation for appointment, employment, promotion, demotion, advancement or evaluation concerning an applicant or employee to whom s/he is related or a relative. A School Board member or School District employee shall not directly supervise or be directly supervised by an employee to whom that person is related or a relative. This Policy applies to all personnel assignments (full-time, part-time and temporary) including substitute assignments.” Standard Practice Bulletin I-201 Athletics, Section I. states “Each Principal shall appoint an Athletic Director who will be responsible for administering the interscholastic athletic program and shall be responsible for the management of all business transactions pertaining to the athletic program.” Section II. Athletic Director’s Responsibilities states “The Athletic Director shall provide the bookkeeper with the proper paperwork required in order to issue payments for Athletic payrolls... The next morning following a game, the Athletic Director will provide the school bookkeeper with the completed Athletic Payroll Reports and ensure that the Payroll Reports have been filled out completely. In addition to approving the Athletic Payroll Reports, the Athletic Director is responsible for completing the Report of Tickets Sold or Split Gate Report when hosting another team.” Section V. Bookkeeper/Budgetkeeper’s Payroll Contact Responsibilities- Athletic Payroll states “The School Bookkeeper/Budgetkeeper is required to perform the following tasks in processing the Athletic Payroll Payments… Receive the Athletic Worker- Athletic Game Report form approved by the Athletic Director...” The Athletic Director is required to sign the Athletic Payroll Report, as indicated on the report form. Additionally, the job descriptions for athletic event workers, such as Ticket Sellers, provide for accountability to the Athletic Director, and the Athletic Director’s job description states that the Athletic Director is to “…assist the Principal in securing competent personnel for the athletic staff…secure all needed personnel for the operation of the athletic program…serve as treasurer of the school athletic fund…” among other duties. Clearly the Athletic Director is the supervisor of athletic event workers, from hiring them for the job, to authorizing the accompanying payment. To avoid exploiting his or her position for unwarranted personal gain, the Athletic Director should not employ and pay himself or herself or any relative as “gate help”.

RECOMMENDATIONS

We recommend District staff refrain from collecting duplicate compensation and/or employing relatives, in accordance with School Board Policies 4002.10 and 6210, and Supplement Guidelines 12/18/2012. We also recommend promulgation of guidelines and further training of District personnel by the Athletic and Student Activities Department.

School Board of Broward County, Florida Office of the Chief Auditor

Review of Varsity Football Game Ticket Sales and Cash Collection Procedures September and October 2012

16

MANAGEMENT RESPONSE

We concur with this recommendation that the athletic director is not entitled to receive additional compensation for supervising event workers at regular season games, nor should they receive additional compensation as gate help at athletic events. In addition, athletic directors must relinquish their supplement during the season if they wish to receive a supplement for coaching. Athletic directors will be subject to further training on April 5, 2013 and August 8, 2013.

EXHIBITS

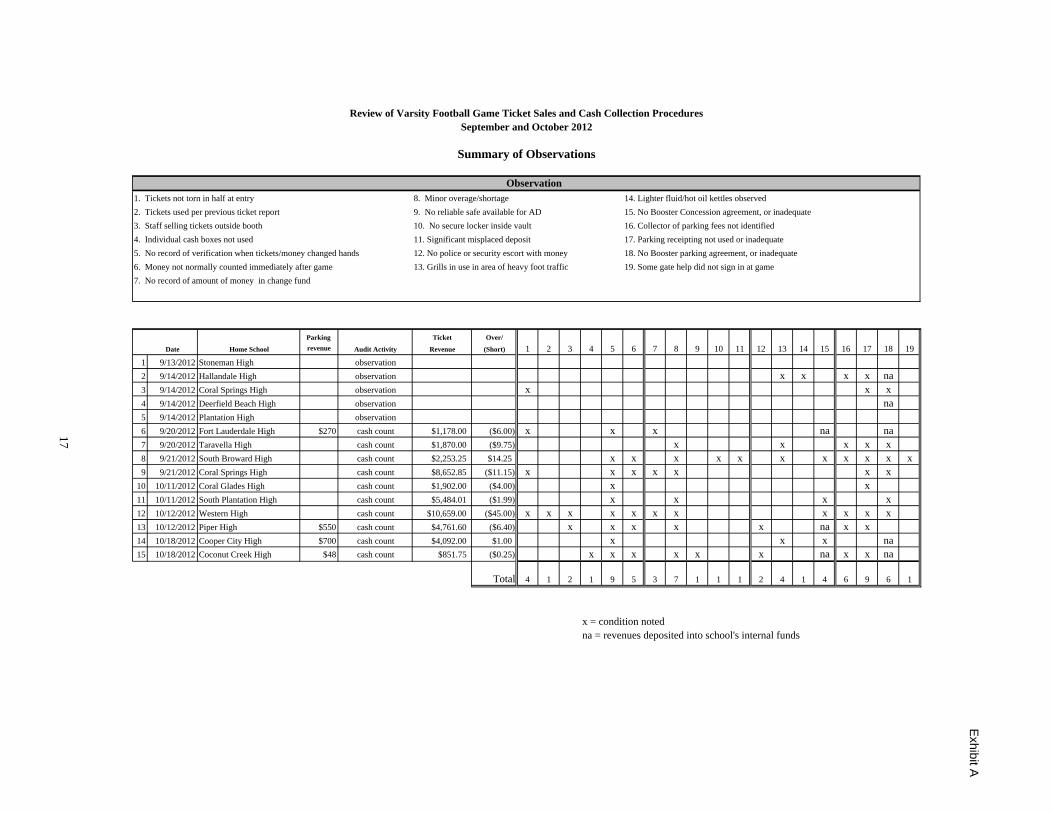

Observation1. Tickets not torn in half at entry 8. Minor overage/shortage 14. Lighter fluid/hot oil kettles observed

2. Tickets used per previous ticket report 9. No reliable safe available for AD 15. No Booster Concession agreement, or inadequate

3. Staff selling tickets outside booth 10. No secure locker inside vault 16. Collector of parking fees not identified

4. Individual cash boxes not used 11. Significant misplaced deposit 17. Parking receipting not used or inadequate

5. No record of verification when tickets/money changed hands 12. No police or security escort with money 18. No Booster parking agreement, or inadequate

6. Money not normally counted immediately after game 13. Grills in use in area of heavy foot traffic 19. Some gate help did not sign in at game

7. No record of amount of money in change fund

Parking Ticket Over/

Date Home School revenue Audit Activity Revenue (Short) 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19

1 9/13/2012 Stoneman High observation

2 9/14/2012 Hallandale High observation x x x x na3 9/14/2012 Coral Springs High observation x x x4 9/14/2012 Deerfield Beach High observation na5 9/14/2012 Plantation High observation

6 9/20/2012 Fort Lauderdale High $270 cash count $1,178.00 ($6.00) x x x na na7 9/20/2012 Taravella High cash count $1,870.00 ($9.75) x x x x x8 9/21/2012 South Broward High cash count $2,253.25 $14.25 x x x x x x x x x x x9 9/21/2012 Coral Springs High cash count $8,652.85 ($11.15) x x x x x x x

10 10/11/2012 Coral Glades High cash count $1,902.00 ($4.00) x x11 10/11/2012 South Plantation High cash count $5,484.01 ($1.99) x x x x12 10/12/2012 Western High cash count $10,659.00 ($45.00) x x x x x x x x x x x13 10/12/2012 Piper High $550 cash count $4,761.60 ($6.40) x x x x x na x x 14 10/18/2012 Cooper City High $700 cash count $4,092.00 $1.00 x x x na15 10/18/2012 Coconut Creek High $48 cash count $851.75 ($0.25) x x x x x x na x x na

Total 4 1 2 1 9 5 3 7 1 1 1 2 4 1 4 6 9 6 1

x = condition notedna = revenues deposited into school's internal funds

Exhibit A

17

Review of Varsity Football Game Ticket Sales and Cash Collection ProceduresSeptember and October 2012

Summary of Observations

1

Athletic Directors’ Responsibilities

Presented by

The Office of the Chief Auditor754‐321‐2400

A. RECEIPTS

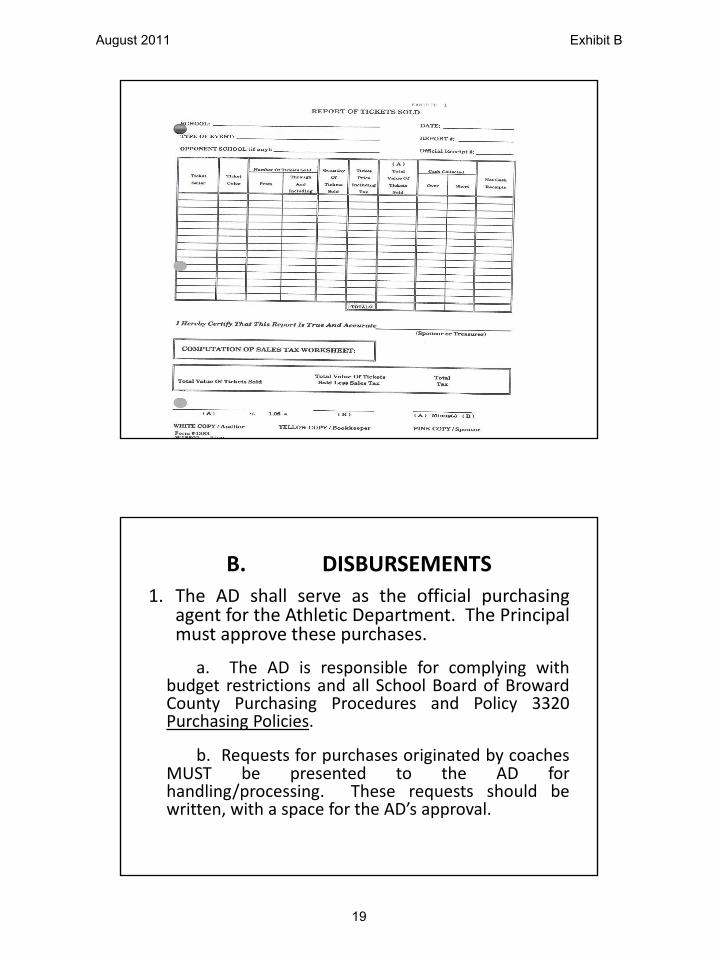

1. All monies from any source MUST be depositedwith the school’s bookkeeper by the AthleticDirector (AD) or designee immediately followingthe athletic event (next business day).

2. When presenting deposits to the bookkeeper,the AD or designee will support the depositswith a properly documented Report of TicketsSold Form (Exhibit 1) and an Athletic GameReport.

August 2011 Exhibit B

18

2

B. DISBURSEMENTS

1. The AD shall serve as the official purchasingagent for the Athletic Department. The Principalmust approve these purchases.

a. The AD is responsible for complying withbudget restrictions and all School Board of BrowardCounty Purchasing Procedures and Policy 3320Purchasing Policies.

b. Requests for purchases originated by coachesMUST be presented to the AD forhandling/processing. These requests should bewritten, with a space for the AD’s approval.

August 2011 Exhibit B

19

3

c. To initiate a disbursement, the AD will sign off on allvendor invoices to be paid through internal accounts.

2. The AD shall provide the bookkeeper/payroll processorwith the proper paperwork (see section C below)required in order to issue payments for Athletic payrolls.

C. ATHLETIC PAYROLL

NO CASH PAYMENTS WILL BE ISSUED TO ANY ATHLETICWORKERS OR OFFICIALS. Payments to athletic workerswill be in accordance with the SCHOOL ACTIVITIES UNITPRICE SALARY SCHEDULE (current salary schedule can beobtained by contacting the Athletic Department). Theserates are established by the School Board of BrowardCounty and NO OTHER rate of pay is to be used.

D. GAME REPORTS

In addition to approving the AthleticPayroll Reports, the AD is responsible forcompleting the REPORT OF TICKETS SOLD(Exhibit 1) and SPLIT GATE REPORT (Exhibit6) when hosting another team. Copies ofgame guarantees and split gateagreements executed between the ADsmust be filed with the accounting records.

August 2011 Exhibit B

20

4

Split Gate Report‐ Exhibit 6

Reporting School__________________

Nature of Event___________________ Location __________

1. Income from Ticket Sales

Number Sold X Selling Price = Total Sales

Advance Sales

Students _________ $________ $_________

Adults __________ $________ $________

Gate Sales

Students __________ $________ $________

Adults __________ $________ $________

2. Total Receipts $________

Split Gate Report‐ Exhibit 6 (cont.)

3. EXPENSESGuarantees $_________

Officials __________

Field Help __________

Gate Help _________

Announcer __________

Police __________

Ticket Manager __________

Custodial Help __________

Ambulance __________

Facility Rental __________

State Sales Tax (when applicable) __________

Other __________

Total $___________

August 2011 Exhibit B

21

5

Split Gate Report‐ Exhibit 6 (cont.)

4. Subtract Total Expenses $________

5. Net Receipts $ ________

6. Split Gate

Participating Schools % of Line 5 Amount

__________________ _________ $_______

_________________ __________ $ ________

7. Total Split Gate (Same as line 5 above) $ _______

Prepared by :____________________ Date _________

Certified Correct by : _______________________

Athletic Director

Ticket Sales and Cash Collections

Each of the Ticket Sellers should be assigned his/her own cash box with

assigned tickets and cash.

August 2011 Exhibit B

22

6

Sample ManifestFor __________________________________

(Opponent Name & Game Date)

TICKET SELLER: PLEASE COMPLETE. Name _____________________Print Name

(BEFORE GAME) I received the following roll of ticket(s) from

_____________________

_______ tickets with numbers starting with _______ through ________(color)

__________ tickets with numbers starting with ____________ through(color)

I also received a Change Fund in the amount of $______________

_____________________.Signature

Sample ManifestFor BRADFORD HIGH SCHOOL September 4, 2009

(Opponent Name & Game Date)•

TICKET SELLER: PLEASE COMPLETE. Name Janet SmithPrint Name

(BEFORE GAME) I received the following roll of ticket(s) from

Ann Murray

Blue $5 tickets with numbers starting with _10 through _2000(color & $ value)

Yellow $4 tickets with numbers starting with __500 through 2000(color)

I also received a Change Fund in the amount of $___200.00____ __

_Janet Smith____Signature

August 2011 Exhibit B

23

7

NOT ACCEPTABLE

• Two people should not share the same cash box as this eliminates accountability of each ticket seller.

Conflict of Interest

• The bookkeeper cannot be employed as a

– Ticket Seller

– Ticket Taker

– Money Counter

August 2011 Exhibit B

24

8

Counterfeit Pens

• Ticket Sellers must use “counterfeit” pens for bills larger than $20.

Note: If you start having a problem with $20s, then use the pen for all $20s.

TICKETS

• All attendees must be issued an admissionticket when admission is paid.

• Collecting cash at the gate without tickets is aviolation of School Board Policy # 6301Collection of Monies.

• There is no accountability for

money changing hands, without

tickets.

August 2011 Exhibit B

25

9

Complimentary Tickets

• Only specially printed pre‐numberedcomplimentary tickets are to be used.

• The visiting school may secure these ticketsfrom the home school.

We recommend the receiving AD sign for thetickets.

• Complimentary tickets are to be included onthe Report of Tickets Sold form.

Sign‐In Sheets

• School’s faculty members do not need to beissued complimentary tickets.

• A sign‐in sheet for faculty and guests is a goodcontrol instrument.

August 2011 Exhibit B

26

10

Ticket Seller requires Ticket Taker

• Every event which has a Ticket Seller must have a Ticket Taker.

• Either or both people may be volunteers, but they must be recorded on the Cash Payroll Sheet and listed as volunteers.

• = requires

• Ticket Seller Ticket Taker

Ticket Taker• The ticket taker will collect each ticket and tear the ticket in half.

• One half is kept for auditing.Keep the deadwood tickets in a

secured place.

• The second half is given to the patron or deposited into a receptacle, if there is no re‐admission through the gate.

• We recommend a sign be posted stating“No re admittance”.

August 2011 Exhibit B

27

11

CLOSING OUT CASH BOX

• Each ticket seller must count the cash andbalance his/her cash with the ticket sales.

• Any cash overages/shortages should beidentified.

• The Ticket Closeout Report is given to theAthletic Director or Appointee/AssistantPrincipal.

Sample ManifestFor BRADFORD HIGH SCHOOL September 4, 2009

(Opponent Name & Game Date)

TICKET SELLER: PLEASE COMPLETE. Name Janet SmithPrint Name

(BEFORE GAME) I received the following roll of ticket(s) from

Ann Murray

Blue $5 tickets with numbers starting with _10 through _2000(color & $ value)

Yellow $4 tickets with numbers starting with __500 through 2000(color)

I also received a Change Fund in the amount of $___200.00____ __

_Janet Smith____Signature

August 2011 Exhibit B

28

12

Ticket Closeout ‐ After the Game

Ticket ReconciliationBlue $5

Ending Number of tickets sold 1749Less Beginning Number ‐10Plus One +1Total $5 Tickets Sold 1740A (1,740 X $5 = $8,700)

Yellow $4 Ending Number of tickets sold 999Less Beginning Number ‐ 500Plus One +1Total $4 Tickets Sold 500B (500 X $4 = $2,000)

A + B = $8,700 + $2,000 = $10,700

Returned TicketsBlue $5 1750 to 2000Yellow $4 1000 to 2000

Cash Reconciliation

Change Fund Returned $ 200.00

Potential Total Ticket Sales $ 10,700.00

TOTAL CASH $ 10,900.00

Difference over/under $ 0.00

I HEREBY CERTIFY THAT THIS REPORT IS TRUE AND ACCURATE

_Janet Jones_______________ (Ticket Seller)

Robert Rogers

AD/Designee Signature

Cash Count Sheet

Quantity $ Value• __________ .01 ___________• ___5______ .05 __.25______• __________ .10 ___________• __________ .25 ___________• __________ .50 ___________• __________ 1.00 ___________• __________ 5.00 ___________• __________ 10.00 ___________• __________ 20.00 ___________• __________ 50.00 ___________• __________ 100.00 ___________

August 2011 Exhibit B

29

13

Report of Tickets Sold Exhibit 1

Number of Tickets Sold Total Value Cash Collected

Ticket Ticket Through and Quantity Sold Ticket of Over Short Net Cash

Seller Color From Including Price Tickets sold Receipts

J. Smith Blue 10 1749 1740 $5 $8,700 0 0 $8,700

Yellow 500 999 500 $4 $2,000 0 0 2,000

TOTALS $10,700 0 0 $10,700

Safeguarding of CASH

• The AD or designee will confirm each ticket seller’s report and secure the funds in the school’s vault. The AD should be the only one having access to this safe.

• All revenues must be deposited with the school’s bookkeeper immediately following the athletic event (next business day).

August 2011 Exhibit B

30

14

Athletic Director’s Responsibility

• As soon as possible after the event, the AD ordesignee will count the funds, and verify thefunds with the school’s bookkeeper.

• Prepare the Report of Tickets Sold form.

• Attach the Athletic Game Report.

• Return unused tickets to the bookkeeper.

• Receive a computerized receipt from theBookkeeper.

Who Are You Working For?

• Every person collecting money in or near thestadium should be clearly identified, so thatpatrons know whether they are supporting aschool’s club or a booster club.

• If donations are collected for parking, ticketsshould be issued to the patrons and a reportof tickets sold should be maintained, even if itis a Booster Club. This is something thatshould be a part of the Booster Agreement.

August 2011 Exhibit B

31

15

Booster Clubs Finding‐‐the school did not have writtenagreements with any booster clubs concerningthe operation of various booster clubs’concession stands on school grounds, within theconfines of the school building and in the athleticstadium. The agreement must be approved bythe Principal.

• Boosters should not be paying coaches. This maycause problems with the IRS, and jeopardize thenon‐profit status.

School Year 2006 Case

Auditors attended a varsity football home game onNovember 2, 2006, to perform a cash count of the gatereceipts and observe the ticket taking procedures. At thegame, and during our follow‐up review of the school’scurrent ticket use, we noted:

• No admission tickets were used, and it appeared that $5admission was being collected from most of the patrons.Hands were stamped by the ticket sellers to allow re‐entry.We later observed rolls of $5 athletic tickets stored in thecash boxes.

• One of the cash boxes also contained an intact strip of 18$4 athletic tickets, which had previously been reported on aticket report as sold at a volleyball game.

August 2011 Exhibit B

32

16

• No sign‐in sheets were used to record gate helppresent at the game. The sign in sheets used to justifypayments were created the day after the event. This isthe habitual practice according to the AD.

• When we later obtained copies of the subsequently‐produced gate help pay sheets, the AD had not signedthe pay sheets. Instead, a signature stamp facsimilehad been applied.

• The cash box manifest sheets listing the change fundand numbers of the tickets given to each ticket sellerwere not signed by the ticket sellers inacknowledgment of verification and receipt of thechange fund and the tickets listed. The ticket numberslisted on these sheets were also not accurate.

• The ticket sellers did not count the money and tickets with the AthleticDirector at the end of the game, nor did the ticket sellers and AthleticDirector sign off on any receipt enumerating the money and tickets beingreturned to the AD.

• We noted for the current school year athletic ticket sales revenues werereceipted more than a week after the event. A ticket collection of $1,015was receipted 5 weeks after the event. We also noted where a ticketcollection of $428 was receipted 3 weeks after the event, and fourinstances where ticket collections of $228, $1,005, $264, and $60 werereceipted 2 weeks after the event.

• Also, in Fiscal Year 2005‐2006 we noted collections for three athleticevents in January 2006 totaling $539 were receipted and deposited inJuly 2006. When the bookkeeper was on leave, the funds were put inthe vault and the bookkeeper discovered them while filing year endrecords.

Note: The AD should receive an official receipt and request a copy of theAthletic account to ensure timely deposit to the correct account.

August 2011 Exhibit B

33

17

• The money counted by auditors after the game onThursday, November 2, 2006 was brought in to theBookkeeper on November 3 by the AD at the auditor’srequest, yet it was not receipted until the followingMonday, November 6.

• The AD did not lock the two cash boxes containing atotal of $4,923.88 in the bookkeeper’s vault or anysafe after the game, which was played on the schoolgrounds.

• Ticket reports are frequently not being completedpromptly on the correct form. As of November 3,2006, no ticket reports had been completed at all fortwo volleyball games which had taken place over amonth previously, and seventy five $4 tickets hadbeen used in fiscal year 2007 which were notaccounted for on any ticket report presented foraudit.

• Overages and shortages in gate receipts werenot noted on any of the ticket reportscompleted to date, including the six ticketreports which had been completed for varsityfootball ticket sales.

• As of November 3, 2006, complimentary ticketshad not been accounted for on a Ticket Report.

• The bookkeeper is currently not updating theticket log to reflect ticket usage in a timelyfashion.

• Two rolls of unused tickets observed ininventory are identical as to color,denomination and ticket numbers.

August 2011 Exhibit B

34

18

School Year 2007 CaseOur analysis of the ticket reports and the pre‐numbered ticketinventory revealed the following discrepancies, whichcontributed to our inability to determine the accuracy of theaccounting for all sales and deposits to the internal accounts.

• The former Athletic Director (AD) kept all athletic tickets in hisoffice;

• Over 100 ticket reports were reviewed and none had anoverage or shortage simply due to the AD matching monies totickets, rather than depositing actual monies collected intactto the bookkeeper.

• Tickets were not always given to payees during entries togames, because 67 tickets were reused.

• Another 819 tickets from various rolls were missing.

In December 2007, the prior AD resigned from this position.

School Year 2009 caseAuditors attended a varsity football game on October 10, 2008 to observethe use of athletic tickets and to perform a cash count of gate receipts.During our observation of ticket sales and cash count we noted thefollowing:

• None of the ticket sellers were selling individually assignedpre‐numbered tickets. Two ticket sellers were collectingfunds, issuing tickets and admitting patrons. The ticket takerswere not ripping the tickets and returning half to thepurchaser.

• A third seller at another entrance gate was taking cashwithout issuing tickets.

• Funds totaling $5,873.61 were counted by the AD and verifiedby the auditors after the game. According to our analysis,collections were $291.61 more than the tickets documentedas sold on the ticket report. The Athletic Director did not havean explanation for the overage.

August 2011 Exhibit B

35

19

SY 2009‐‐School B• September 2008, the auditor found a total of forty‐one (41) torn $5

tickets totaling $205 were not included in the sellers’ ticket inventory.These tickets were not included as part of the school’s ticket inventoryon August 7, 2008, when the auditor verified the ticket inventory. Ofthe total, $200 was not included in cash revenue. The ticket sellerstated that he had one ticket from this roll which was ticket #23420.The auditors could not account for the additional forty (40) tickets.This $200 was not documented on the Ticket Report or remitted to thebookkeeper for deposit.

• The ticket sellers did not sign the manifest sheetsacknowledging receipt or verification of their change funds orticket rolls. Accurate completion and verification of manifestsheets are essential to maintaining accountability for thetickets and money in the cash boxes.

• In November 2009, staff discovered numerous unauthorizedtickets in the Athletic Director’s office. The SpecialInvestigative Unit (SIU) is conducting an investigation of thismatter.

Workers Data Info Exhibit 2

Exhibit 2

Broward County Public Schools

Athletic Workers Data Information

Vendor Name Social Number First Last Address City State Zip Security Number

August 2011 Exhibit B

36

20

Resources/References

• Standard Practice Bulletin I‐201, Athletics.

• A workshop for Athletic Department Operations and Procedures. This can be found on the Office of the Chief Auditor’s website.

Office of the Chief Auditor’s Staff

• Patrick Reilly, Chief Auditor

• Delores Y. McKinley, Director

• Rupert Jairam, Auditor III

Chief Auditor’s August 2011 presentation to Athletic Directors

Office of the Chief Auditor Website > Staff Development > Workshops

http://www.broward.k12.fl.us/auditdept/staffdevelopment/Athletic_Workshop_2011.pdf

August 2011 Exhibit B

37

EXHIBIT 3

INDEPENDENT SCHOOL RELATED ORGANIZATION

LETTER OF AGREEMENT

We will notify the principal/designee of all fundraising activities by completing this form for each activity.

Name of Organization___________________________________________________________________

Type of Activity________________________________________________________________________

Location of Activity_____________________________________________________________________

Date of Activity________________________________________________________________________

Benefit to School_______________________________________________________________________

_____________________________________________________________________________________

As an Independent School Related Organization our purpose/mission is to:

_____________________________________________________________________________________

_____________________________________________________________________________________

We will conduct all business in such a way as to clearly distinguish Independent School Related Organization

activities from School/Student activities. All public announcements, programs, tickets, etc., will clearly indicate

that the function is sponsored by our organization.

We will not involve the school or any School Board employee in the purchase and sale of merchandise.

As an Independent School Related Organization, we are informed that our organization must obtain our own

Federal ID number and Florida Sales Tax Exemption Number.

Principal______________________________________School____________________________________

Organization Representative________________________________Contact Number__________________

SCHOOL’S LETTERHEAD

(Copy contents of agreement below on school letterhead)

SPB I-101 Exhibit 3 Exhibit C

38

Exhibit D

39

Exhibit D

40

DEPARTMENT OF ATHLETICS & STUDENT ACTIVITIES

BOOSTER CLUB GUIDELINES The School Board of Broward County recognizes that athletic booster clubs have a valued role in supporting and supplementing educational programs. Athletic booster clubs are independent organizations designated to support, encourage and advance educational extracurricular programming. The School Board of Broward County recognizes athletic booster clubs as a school-allied group through School Board Policy #1341. This policy specifically accords school-allied groups certain rights and privileges regarding the use and or rental of Broward County facilities. In addition, School Board of Broward County Standard Practice Bulletins, Internal Fund Accounting, recognizes that school allied groups including athletic booster clubs have a legitimate role in raising funds for student activities programs. The purpose of this document is to address specific issues and answer frequently asked questions regarding the role and relationship of athletic booster organizations with schools and the School Board of Broward County.

Mission and Purpose of Athletic Booster Organizations Booster clubs exist as independent organizations comprised of parents and interested community persons. Booster clubs serve two general purposes: To promote the education, general welfare and morale of students, and To assist in financing the legitimate extracurricular activities of the athletic student

body in order to augment, but not conflict with, the educational programs provided by the School Board.

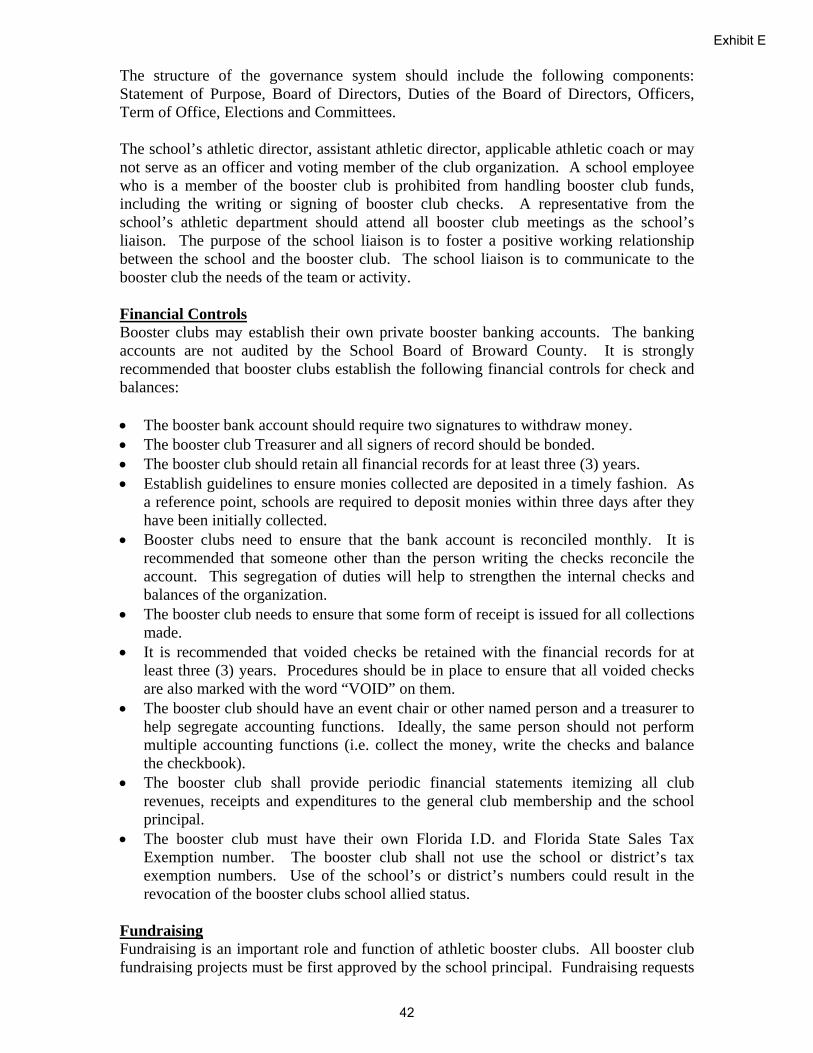

Booster clubs are responsible and expected to promote school spirit, sportsmanship and advancement of the School Board of Broward County’s adopted eight character education traits: Responsibility, Citizenship, Kindness, Respect, Honesty, Self-Control, Tolerance and Cooperation. Booster clubs are organized to help promote, support and improve the extracurricular activities at schools. Although booster clubs are independent organizations, school principals reserve the right to recognize and sanction the booster clubs involvement in school extracurricular activities including fundraising. The school principal is not obligated or required to accept funds from the booster club or recognize the booster club as a school allied organization. Further, only the school principal shall allow a booster club to incorporate the school’s name into the booster club. The school principal has final authority on the existence of and all activities of a booster club. Booster Club Governance Booster clubs are a separate legal entity from the School Board of Broward County. All booster clubs shall operate according to a written constitution and a set of by-laws. The booster clubs shall be open to all parents and community members. The constitution of Booster clubs should include a nondiscrimination clause which states, “The Booster Club of _________________________ shall not discriminate against any participant or deny club membership because of race, age, religion, color, gender, national origin, marital status, disability, or sexual orientation.”

Exhibit E

41

The structure of the governance system should include the following components: Statement of Purpose, Board of Directors, Duties of the Board of Directors, Officers, Term of Office, Elections and Committees. The school’s athletic director, assistant athletic director, applicable athletic coach or may not serve as an officer and voting member of the club organization. A school employee who is a member of the booster club is prohibited from handling booster club funds, including the writing or signing of booster club checks. A representative from the school’s athletic department should attend all booster club meetings as the school’s liaison. The purpose of the school liaison is to foster a positive working relationship between the school and the booster club. The school liaison is to communicate to the booster club the needs of the team or activity. Financial Controls Booster clubs may establish their own private booster banking accounts. The banking accounts are not audited by the School Board of Broward County. It is strongly recommended that booster clubs establish the following financial controls for check and balances: The booster bank account should require two signatures to withdraw money. The booster club Treasurer and all signers of record should be bonded. The booster club should retain all financial records for at least three (3) years. Establish guidelines to ensure monies collected are deposited in a timely fashion. As

a reference point, schools are required to deposit monies within three days after they have been initially collected.

Booster clubs need to ensure that the bank account is reconciled monthly. It is recommended that someone other than the person writing the checks reconcile the account. This segregation of duties will help to strengthen the internal checks and balances of the organization.

The booster club needs to ensure that some form of receipt is issued for all collections made.

It is recommended that voided checks be retained with the financial records for at least three (3) years. Procedures should be in place to ensure that all voided checks are also marked with the word “VOID” on them.

The booster club should have an event chair or other named person and a treasurer to help segregate accounting functions. Ideally, the same person should not perform multiple accounting functions (i.e. collect the money, write the checks and balance the checkbook).

The booster club shall provide periodic financial statements itemizing all club revenues, receipts and expenditures to the general club membership and the school principal.

The booster club must have their own Florida I.D. and Florida State Sales Tax Exemption number. The booster club shall not use the school or district’s tax exemption numbers. Use of the school’s or district’s numbers could result in the revocation of the booster clubs school allied status.

Fundraising Fundraising is an important role and function of athletic booster clubs. All booster club fundraising projects must be first approved by the school principal. Fundraising requests

Exhibit E

42

submitted to the principal should state the type of activity, duration and intended purpose of the fundraising. Revenue from fundraising events that directly involve students and employees handling money must be deposited in the school’s internal booster club account. Fundraising revenue exclusively raised and handled by the booster club may be deposited in the club’s private bank account or school’s internal club account. The following guidelines are intended to ensure that booster clubs are aware of School Board policies and procedures regarding fundraising: Flyers and advertisements for fundraising activities conducted by booster clubs must

state that the activity is being sponsored by the booster club and not the school. All fundraising activities conducted by booster clubs should be summarized in

writing and reflected in the booster club minutes. Booster clubs may deposit fundraising revenue in their club bank account for

fundraising projects/activities that do not involve the handling of money or checks by students or employees. Examples include: Barbecues, dinners, and similar activities conducted entirely by the booster

organization and not involving any school employee(s) or student(s) in the handling of money.

Benefit shows or performances by non-school groups such as college or professional music groups, when arrangements are made by the booster organization and not involving any employee(s) or student(s) in the handling of funds.

Merchandising sales including but not limited to memorabilia, booster club items like pom-poms, cheer-stiks, etc.. where the booster club operates the sales activity and handles the receipts and money exchanges without involving employee(s) or student(s).

Transfer of Funds from Booster Club to School Booster clubs may elect to make gifts or donations to the school. All donations made to a school should be supported by an official school receipt. If the organization does not receive an official school receipt in a timely manner, the Principal of the school should be contacted. The donation/gift should be accompanied with a letter of purpose from the booster club. The letter should reflect the specific purpose the gift/donation is intended for. A booster club may make undesignated gifts to benefit students in a specific activity (i.e. undesignated gift for football). Funds collected in connection with gifts, donations and contributions from an athletic booster club shall be deposited in the school’s internal funds account. The responsibility for Internal Fund accounts is established by State Law, State Board Rules, Section 6A-1.85, which states in part, “Monies collected and expended within a school shall be used for financing the normal program of school activities not otherwise financed, for providing necessary and proper services and materials for school activities and for other purposes consistent with the school program as established and approved by the School Board. Such funds are the responsibility of the School Board and it shall be the duty of the School Board to see the funds are properly accounted for through the use of generally recognized accounting procedures and effectively administered through adherence to internal funds policies of the School Board and applicable Florida Statutes.”

Exhibit E

43

School internal accounts are audited annually by the School Board’s Office of Management/Facility Audits Department. Purchasing The school is responsible for the purchasing of all athletic equipment associated with the specific athletic activity. This procedure ensures that the products purchased meet Florida High School Athletic Association, National High School Federation, and school system standards. Further, School Board purchasing ensures quality control as well as protection during warranty periods. The school may also obtain the best pricing from authorized vendors through district’s catalog purchasing system. The booster club should donate funds to the school, accompanied with a letter detailing the purpose of the gift. The school is eligible to purchase all equipment and goods tax exempt. The school principal must ensure that all gifts or donations support and follow the gender equity requirements provided through Title IX and the Florida Gender Equity Act. Use of School Facilities Pursuant to School Board Policy #1341, Use of Broward County School Facilities for Non-School Purposes, athletic booster clubs are not required to pay rental fees, provide certificates of insurance, nor submit an application for use of facilities agreement when using School Board facilities. For example, a booster club may conduct their booster club meetings at the school free of charge. Booster clubs will be required to pay personnel costs as incurred and shall pay custodial operational costs for fundraising events or for use of school facilities required on non-school days at the rate specified in the established policy fee schedule. Booster clubs may charge for fundraising events such as dinner, dances, car washes, etc.. and not be required to pay rental fees to the school district or provide a certificate of insurance to the School Board as long as all of the funds raised are spent to support public school activities. If a booster club utilizes a school facility for fundraising purposes, and elects to charge students or parents, the booster club must provide the affected principal a projection of revenues prior to the scheduled event and a statement of actual revenues after the event. At the end of each school year, the booster club must provide the affected principal a written summary statement regarding fundraisers conducted on/in school grounds/facilities. The statement shall include how the funds were raised, accumulated revenue minus expenditures, and how the funds raised were expended to support public school activities. Failure to provide this information may result in the school principal refusing to allow the booster club use of School Board facilities. Booster Club Restrictions Athletic booster clubs are prohibited from establishing rules that require parents to

fundraise as a pre-condition of a student’s athletic participation on a school district sanctioned team. The booster club shall not charge student fees as a condition for membership on a school/district sanctioned team. The school principal, athletic director and coach/sponsor determine eligibility to participate in a school sponsored team or activity.

Booster clubs are not allowed to issue personal checks or cash to coaches or athletes for any purpose. Booster clubs shall adhere to and follow the Florida High School Athletic Association (FHSAA) rules pertaining to student athlete amateurism.

Booster clubs are not authorized to sponsor athletic team field trips. All field trips involving students and staff must be sponsored and authorized by the school in

Exhibit E

44

accordance with School Board Policy 6303. Booster clubs may fundraise and donate funds to underwrite expenses associated with a field trip.

Booster clubs shall not make cash disbursements from fundraising cash collections. Failure to adopt financial control procedures will hinder review of fundraising activities and the profit that the activity generated.