reviewing the structure and capacity of the nigerian

TRANSCRIPT

Reviewing the structure and capacity of

the Nigerian economy for improving

Government Revenue

Dr. Yemi Kale

Statistician General of the Federation/ CEO

National Bureau of Statistics

08/05/2015

BudgIT Symposium: Options and possibilities for government revenue growth and efficiency- Options, Opportunities and Possibilities

OUTLINE…

i. Introduction

ii. What is GDP?

iii. What GDP is not

iv. Structure of the

Economy: Output

approach

vii. Structure of

government

revenue

viii. Conclusions

v. Structure of the

Economy:

Expenditure

approach

vi. Opportunities for

further growth

A

A

A

A

INTRODUCTION

SECTION A

UEFA CHAMPIONS LEAGUE AND NIGERIA’S GDP

Q1: From these

statistics, can we tell

which team (left or

right) won the

match?

Q2: Does having a

higher ball possession

rate, or covering

more distance mean

that a team would

ALWAYS win the

match?

ENGLISH PREMIER LEAGUE AND NIGERIA’S GDP

Q1: From these

statistics, can we tell

which team (left or

right) won the

match?

B

B

B

B

What is GDP?

SECTION B

“Very few people indeed trully understand how the

regularly published GDP figures are constructed” Diane

Coyle

Domestic private savings

GDP Defined

Rest of world

Firms Households

Product

Markets

Factor

Markets

Government Save/Invest

Factor

cost

Sales

revenues

Wages

& rents

Private

cons.

Gov’t

exp.

Invest.

exp.

Transfers

Import payments

Export receipts Foreign savings

Taxes Gov’t savings

Domestic demand for final goods

Intermediate

demand Leakages and

withdrawals

Injections

Budget deficit

Current account

balance

Absorption

= C + I + G

GDP (market price)

= C + I + G + X – M

GDP (factor cost)

= L+K

Circular Flow of Income

The Gross Domestic Product (GDP) is the market value of all officially recognized final goods and services produced within

a country in a given period

Output/Production approach

Value of Sales of goods and services – Intermediate Consumption in producing those goods and services.

Expenditure Approach

GDP = C + I + G + (EX – IM)

Income Approach

Wages+Rent+Interests+ profits+ adjustments

What is GDP?

Methodology

Four major methodological pillars

The System of National Accounts (SNA 2008 version),

The International Standard Industrial Classification

(ISIC Revision 4),

The Central Product Classification (CPC version 2)

The development of a Supply and Use Table/matrix

(SUT)

Then NBS conducts sector surveys

Formal sector from company audited reports from FIrS,

SEC etc

Informal sector from HH surveys.

Data also collected from various MDAs, Federal

and States

9

Measuring GDP

Background and Key Milestones The SNA 2008: The SUTISIC 3.1 to 4

10

ISIC Rev.3.1

A Agriculture, hunting and forestry

B Fishing

C Mining and quarrying

D Manufacturing

E Electricity, gas and water supply

F Construction

G Wholesale and retail trade; …

H Hotels and restaurants

I Transport, storage and communications

J Financial intermediation

K Real estate, renting and business …

L Public administration …

M Education

N Health and social work

O Other community, social, personal …

P Activities of private households

Q Extraterritorial organizations and bodies

ISIC Rev.4

A Agriculture, forestry and fishing

B Mining and quarrying

C Manufacturing

D Electricity, gas, steam …

E Water supply; sewerage, waste …

F Construction

G Wholesale and retail trade; …

H Transportation and storage

I Accommodation and food service activities

J Information and communication

K Financial and insurance activities

L Real estate activities

M Professional, scientific and technical activities

N Administrative and support service activities

O Public administration …

P Education

Q Human health and social work activities

R Arts, entertainment and recreation

S Other service activities

T Activities of households …

U Activities of extraterritorial organizations …

10

C

C

C

C

What GDP is Not

SECTION C

UEFA CHAMPIONS LEAGUE AND NIGERIA’S GDP

Q1: From these

statistics, can we tell

which team (left or

right) won the

match?

Q2: Does having a

higher ball possession

rate, or covering

more distance mean

that a team would

ALWAYS win the

match?

UEFA CHAMPIONS LEAGUE AND NIGERIA’S GDP

Real Madrid qualified

for the Finals by

beating Bayern

Munich 4-0

Nearly all the stats

would indicate the

opposite

...the problem with

aggregates

...knowing what each

statistic measures

...focusing on data

not ideology!

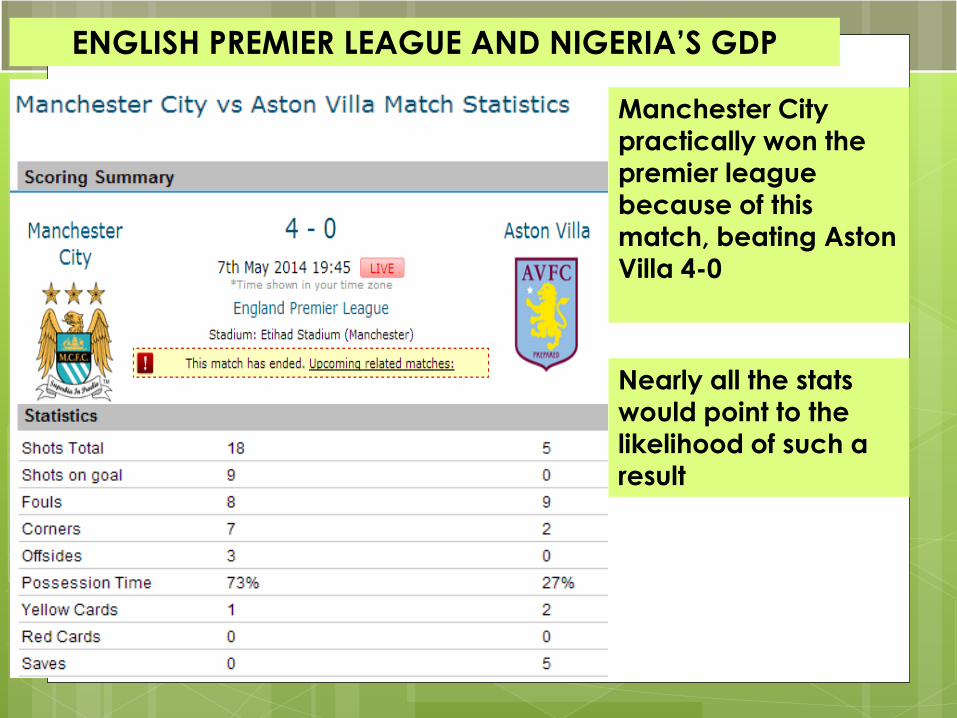

ENGLISH PREMIER LEAGUE AND NIGERIA’S GDP

Q1: From these

statistics, can we tell

which team (left or

right) won the

match?

ENGLISH PREMIER LEAGUE AND NIGERIA’S GDP

Manchester City

practically won the premier league

because of this

match, beating Aston

Villa 4-0

Nearly all the stats

would point to the

likelihood of such a

result

GDP growth isn't synonymous with development

…but is required for Development

Rising output Increase in tax revenue development infrastructure (public goods) higher output

GDP not necessarily Significantly job creating Either

What is the nature of the growth?

In what sectors and are they high labor intensive sectors?

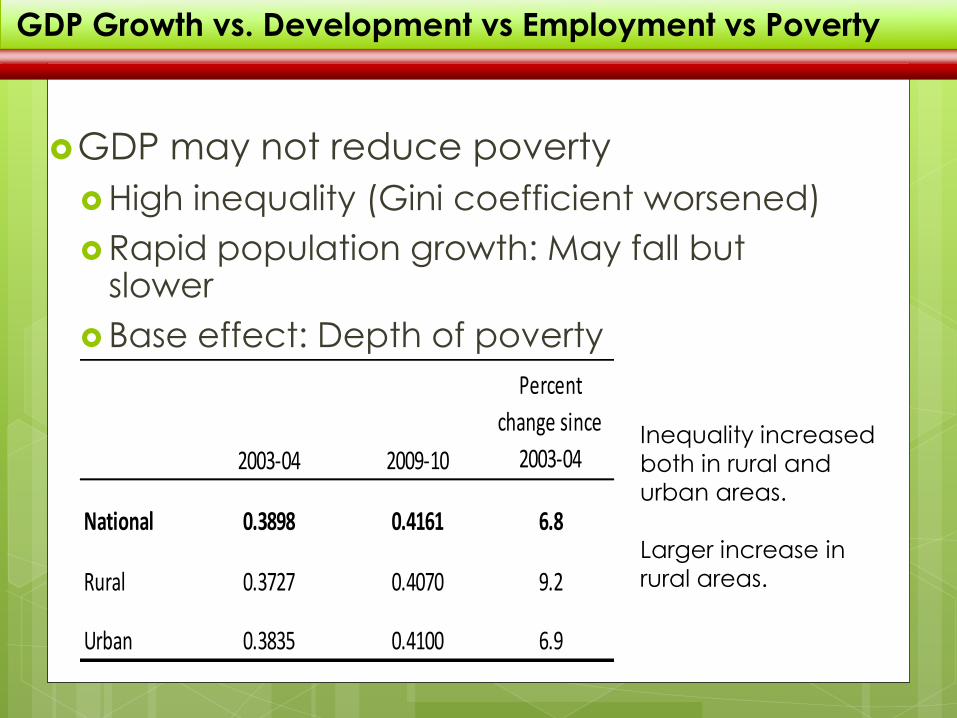

GDP Growth vs. Development vs Employment vs Poverty

GDP may not reduce poverty

High inequality (Gini coefficient worsened)

Rapid population growth: May fall but slower

Base effect: Depth of poverty

2003-04 2009-10

Percent

change since

2003-04

National 0.3898 0.4161 6.8

Rural 0.3727 0.4070 9.2

Urban 0.3835 0.4100 6.9

Inequality increased

both in rural and

urban areas.

Larger increase in

rural areas.

GDP Growth vs. Development vs Employment vs Poverty

Socio Economic Ratios

5/9/2015 18

1419.54 1479.07 1517.41 1539.39

2281.14

2490.05

2683.98

2908.08

3,128

2010 2011 2012 2013 2014

Income per capita (US$)

Old Series (%) New Series (%)

19

Rebasing/Re-benchmarking of GDP

GDP and GDP per caita of top 10 economies, 2013, IMF

Rank Country GDP USD trn$ Rank Country GDP US$

1 United States 16.79 1 Qatar 98,814

2 China 9.18 2 Luxumbourg 78,670

3 Japan 4.9 3 Singaporre 64,584

4 Germany 3.63 4 Norway 54,947

5 France 2.73 5 Brunei 53,431

6 United Kingdom 2.53 6 Unites States 53,101

7 Brazil 2.24 7 Switzerland 46,430

8 Russia 2.11 8 Canada 43,472

9 Italy 2.07 9 Australia 43,073

10 India 1.87 10 Austria 42,597

26 Nigeria 0.5 121 Nigeria 2,689

Countries with the highest GDP are

not necessarily the same countries

with the highest per capita GDP ...Except for the US

D

D

D

D

Structure of the

Economy: Output

Approach

SECTION D

Macro Economic Summary

Real GDP Growth: Slower yet

strong

5/9/2015 21

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

2011 2012 2013 2014

Real GDP Growth (%)

Old Series (%)

New Series (%)

Old Series (N, Million, Current Prices) 2010 2011 2012 2013F

Agriculture 10,310,655.64 11,593,434.13 13,413,842.46 14,709,104.92

Industry 15,659,521.00 16,569,291.58 16,456,457.10 15,374,554.67

Services 8,014,577.50 9,247,134.90 10,673,800.38 12,313,106.11

TOTAL 33,984,754.13 37,409,860.61 40,544,099.94 42,396,765.71

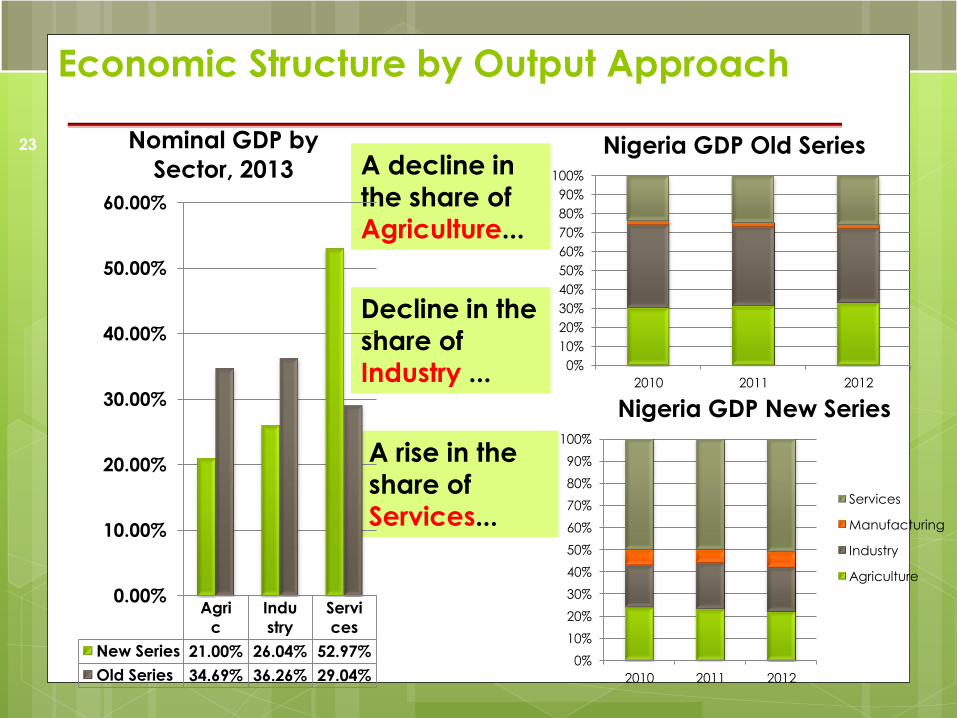

Economic Structure by Output Approach

New Series (N, Million, Current Prices) 2010 2011 2012 2013

Agriculture 13,048,892.80 14,037,825.84 15,815,997.51 16,816,553.01

Industry 13,826,433.90 17,853,113.99 19,587,721.32 20,853,845.33

Services 27,736,937.48 31,089,457.4 36,310,216.23 42,422,165.04

TOTAL 54,612,264.18 62,980,397.22 71,713,935.06 80,092,563.38

Percentage change between Old and New Estimates (%)

2010 2011 2012 2013

Agriculture 27% 21% 18% 14%

Industry -12% 8% 19% 36%

Services 246% 236% 240% 245%

TOTAL 61% 68% 77% 89%

Largest

economy in

Africa;

26th largest in

the world

This

translates to

US$509.2

billion

Nominal GDP

(2013) est.:

N80.1trillion

23

A decline in

the share of

Agriculture...

A rise in the

share of

Services...

Decline in the

share of

Industry ...

Agri

c

Indu

stry

Servi

ces

New Series 21.00% 26.04% 52.97%

Old Series 34.69% 36.26% 29.04%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

Nominal GDP by

Sector, 2013

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012

Nigeria GDP Old Series

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012

Nigeria GDP New Series

Services

Manufacturing

Industry

Agriculture

Economic Structure by Output Approach

24

Nigeria’s service sector (grey section) compares well to that of BRICS

countries, although agriculture (green section) remains larger than all

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Brazil Russia India China South

Africa

Nigeria

GDP by Sector: BRICS Comparison (2012)

Services

Manufacturing

Industry

Agriculture

Comparison with BRICS...

Sourc WDI

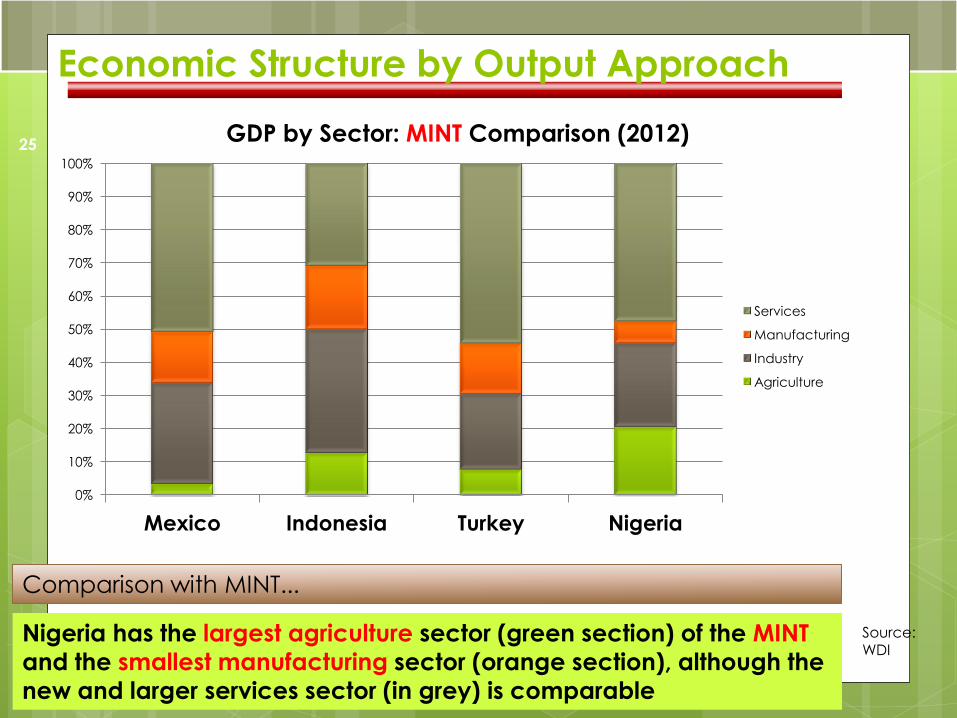

Economic Structure by Output Approach

25

Comparison with MINT...

Nigeria has the largest agriculture sector (green section) of the MINT

and the smallest manufacturing sector (orange section), although the

new and larger services sector (in grey) is comparable

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Mexico Indonesia Turkey Nigeria

GDP by Sector: MINT Comparison (2012)

Services

Manufacturing

Industry

Agriculture

Source: WDI

Economic Structure by Output Approach

-6 -4 -2 0 2 4 6 8

Crude Petroleum and Natural Gas

Fishing

Rail Transport & Pipelines

Metal Ores

Water Transport

Coal Mining

ARTS, ENTERTAINMENT AND RECREATION

CONSTRUCTION

PUBLIC ADMINISTRATION

Crop Production

PROFESSIONAL, SCIENTIFIC AND TECHNICAL …

REAL ESTATE

MANUFACTURING

TRADE

Telecommunications and Information Services

Naira, Trillions

Change in GDP between old and new series for selected

Activities, 2010 Current Prices 26

Two activities

recorded

downward

revisions

Telecommunications

sector recorded the

largest positive

revisions

Economic Structure by Output Approach

27

...compared to only 3

activities in the old series

The number of economic activities that

constitute 70% of nominal GDP is now 6...

13.25

10.51

7.11

5.83

5.42

4.90

2.94

2.27

2.27

1.83

1.59

1.55

1.28

1.10

1.03

0.74

0.62

0.61

0.54

0.43

0.38

Crop …

Trade

Crude …

Manufacturi…

Telecommu…

Real Estate

Food, …

Construction

Professional, …

Public …

Financial …

Other Services

Education

Textile, …

Livestock

Broadcasting

Road …

Accommod…

Human …

Cement

New real GDP: 2013

Rebased Series, (N,

Trillion)

20.96%

16.62%

11.24%

9.22%

8.57%

7.76%

4.65%

3.59%

3.58%

2.89%

2.52%

2.45%

2.02%

1.73%

1.63%

1.17%

0.97%

0.97%

0.86%

0.68%

0.60%

Crop Production

Trade

Crude Petroleum …

Manufacturing

Telecommunicat…

Real Estate

Food, Beverage …

Construction

Professional, …

Public …

Financial …

Other Services

Education

Textile, Apparel …

Livestock

Broadcasting

Road Transport

Accommodation …

Human Health …

Cement

% of real GDP, 2013

Rebased 34.13%

20.33%

12.82%

8.10%

4.00%

3.12%

2.69%

2.52%

2.41%

2.35%

1.92%

1.30%

0.86%

0.61%

0.58%

0.50%

0.40%

0.22%

0.16%

0.16%

0.14%

Crop Production

Wholesale and Retail …

Crude Petroleum & …

Telecommunications

Other Manufacturing

Financial Institutions

Electricity

Livestock

Road Transport

Building & Construction

Real Estate

Fishing

Other Services

Public Administration

Hotel and Restaurants

Forestry

Quarrying & Other …

Education

Water

Insurance

Transport Services

% GDP 2013F, at 1990 prices

Economic Structure by Output Approach

GDP Activity

Average

Growth (2012-2014)

Average

Contributi

on to GDP

(2012-2014)

1 Chemical and Pharmaceutical Products 48.85% 0.15%

2 Textile, Apparel and Footwear 36.08% 1.75%

3 Accommodation and Food Services 36.01% 0.78%

4 Plastic and Rubber products 33.40% 0.22%

5 Other Manufacturing 31.49% 0.45%

6 Motor vehicles & assembly 28.55% 0.07%

7 Cement 27.48% 0.59%

8 Non-Metallic Products 26.55% 0.24%

9 Other Services 26.11% 2.50%

10

Water Supply, Sewerage,

Waste Management and Remediation 24.17% 0.10%

• All Activities but Three

(Accommodation and

Food Services, Other

Services and Water

Supply, Sewerage,

Waste Management

and Remediation) are

under the

Manufacturing Sector

• Many fast growing

sectors have small

contributions to GDP

• More potential for

investment and taxation

Economic Structure by Output Approach: Fastest growing

E

E

E

E

Structure of the

Economy:

Expenditure Approach

SECTION E

The Expenditure Approach Specifically, GDP is equal to the sum of the four

categories of expenditures.

GDP = C + I + G + (X - M)

C = Private consumption expenditure

I = Investment Expenditure

G= Government Consumption Expenditure

X = Value of Exports

M = Value of Imports

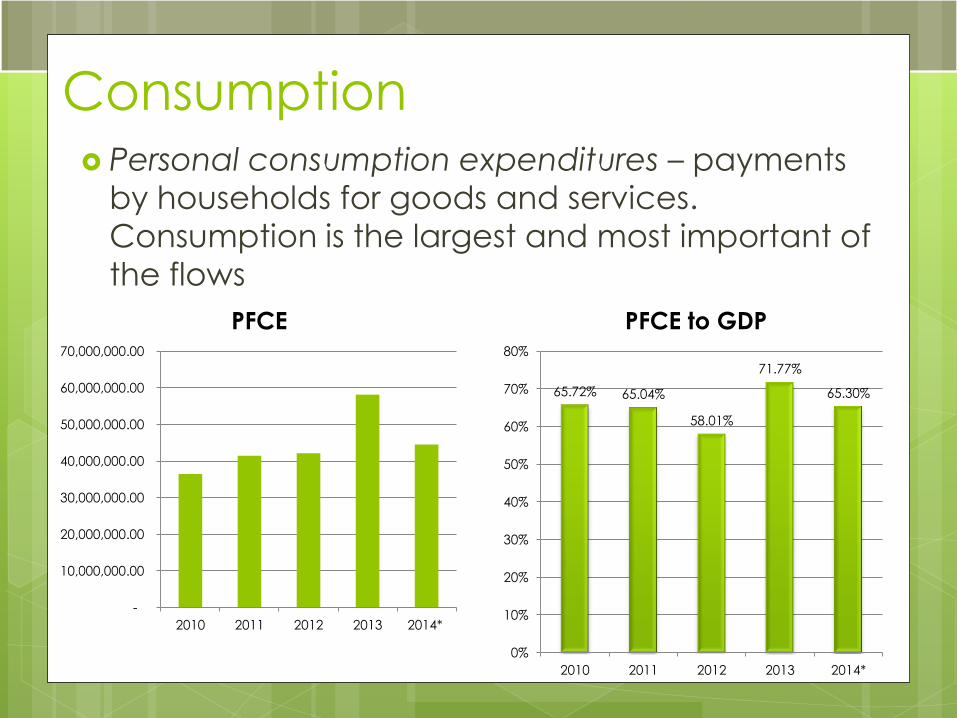

Consumption Personal consumption expenditures – payments

by households for goods and services.

Consumption is the largest and most important of

the flows

-

10,000,000.00

20,000,000.00

30,000,000.00

40,000,000.00

50,000,000.00

60,000,000.00

70,000,000.00

2010 2011 2012 2013 2014*

PFCE

65.72% 65.04%

58.01%

71.77%

65.30%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2010 2011 2012 2013 2014*

PFCE to GDP

Investment This is business spending on equipment, structures, and

inventories.

16.99%

15.98%

14.63% 14.47%

15.38%

11.63%

10.28%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2010 2011 2012 2013 2014*

INVESTMENT TO GDP (%)

GFCF New Series

GFCF Old Series

-

2,000,000.00

4,000,000.00

6,000,000.00

8,000,000.00

10,000,000.00

12,000,000.00

14,000,000.00

2010 2011 2012 2013 2014*

GROSS FIXED CAPITAL

FORMATION

Financial and Monetary Ratios 5/9/2015 33

29.2 25.9

36.5

45.0

18.2 15.4

20.6 23.8

2010 2011 2012 2013

Market Capitalisation to GDP (%) NGR before

and after

Old Series New Series

0

50

100

150

200 Market Capitalisation as a percentage

of GDP various countries

Nigeria

South

Africa Brazil

Mexico

No of Firms

in NBS

Frame

No of

NSE-

Listed

firms

(equities)

Share of

nominal

GDP

(2013)

AGRICULTURE 1,116 6 21.97% MINING AND QUARRYING 971 21 14.50%

MANUFACTURING 76,656 67 6.83%

CONSTRUCTION 53,507 16 3.12%

TRADE 502,085 1 17.02% TRANSPORTATION AND STORAGE 5,902 4 1.24%

INFORMATION AND COMMUNICATION 1,719 22 10.94%

ARTS, ENTERTAINMENT AND RECREATION 805 0 0.08%

PROFESSIONAL, SCIENTIFIC AND TECHNICAL SERVICES 125,482 0 3.19%

ADMINISTRATIVE & SUPPORT SERVICES 2,048 0 0.02%

EDUCATION 34,974 0 1.65%

HUMAN HEALTH AND SOCIAL SERVICES 13,083 14 1.02%

Financial and Monetary Ratios

5/9/2015 34

32.47 32.54

34.27

35.76

0.00

20.21 19.33 19.38 18.93 18.63

2010 2011 2012 2013 2014

Financial Deepening (M2/GDP)

Old Series

New Series

29.89 28.50

36.13 37.22

23.96

16.93

20.43 19.70 19.28

2010 2011 2012 2013 2014

Credit to Private Sector as

% of GDP

Government Expenditures Government expenditures – government payments

for goods and services

-

2,000,000.00

4,000,000.00

6,000,000.00

8,000,000.00

2010 2011 2012 2013 2014*

FINAL CONSUMPTION EXPENDITURE OF GENERAL

GOVERNMENT

0.00

1.00

2.00

3.00

2010 2011 2012 2013 2014

FGN Budgeted Capital

Expenditure to GDP

FGN Budgeted

Capital Expenditure

to GDP

7.50

8.00

8.50

9.00

2010 2011 2012 2013 2014*

Government Expenditure (%) OF

GDP

SHARE OF GDP

Net Exports NX= Domestic Exports of goods + Re-exports of

goods + Exports of Services - Imports of Goods -

Imports of Services

-

5,000,000.00

10,000,000.00

15,000,000.00

20,000,000.00

25,000,000.00

2010 2011 2012 2013 2014*

NET EXPORTS

EXPORTS OF GOODS AND SERVICES

IMPORTS OF GOODS AND SERVICES

NET EXPORTS

External Sector Ratios

5/9/2015 37

38.28

51.97

55.36

33.60

23.82

30.87 31.30

17.79 19.30

2010 2011 2012 2013 2014*

Annual Exports to GDP

*Estimated Q4, 2014 Oil exports

5.80%

4.39%

6.75% 7.07%

-

3.61%

2.61%

3.82% 3.74%

0.23%

2010 2011 2012 2013 2014*

Current Account Surplus to

GDP (%)

Old Series

New Series

*Preliminary Estimate

Source: CBN

F

F

F

F

Opportunities for further

Growth

SECTION F

Growth and Job Opportunities - Fastest Growing Sectors

• Accommodation &

Food Services

• 74% Growth rate

(2013)

• Population is a huge

advantage

• Tourism potentials

• High propensity to

consume

Cement 39% growth rate (2013)

Nigeria is now a net exporter of

cement

huge housing deficit presents an

opportunity for growth

growing interest in investment in

public works towards NV20:2020

• Textile, apparel & footwear 34% growth rate (2013)

slowly re-emerging textile mills in

the Kano and Kaduna

rising number of prominent

Nigerian designers

World Fashion University to be

named after President Jonathan!

Growth and Job Opportunities - Fastest Growing Sectors

• Motion picture

24% growth rate

Sector evolved largely without any

intervention/support

Nollywood is 2nd largest film industry

in the world

ahead of US, behind India

Average cost per movie in Nigeria is

considerably lower

<$0.1million compared to Hollywood

($20million )

Significant opportunity for value

added

Challenges of piracy, informality

and non-registration with regulators

• Arts, entertainment and recreation

15% growth rate (2013)

Includes creative art, entertainment,

libraries, museum, sports and

amusement activities

Like Nollywood, high value-added

Challenge of piracy and non-formality

CIA WFB

Growth and Job Opportunities - Fastest Growing Sectors

Real estate - Contribution: 8%

- Growth: 12% - Estimated housing deficit of 17m,

mainly affordable housing

- Potential constraints: Financial (access to mortgages), cheap building supplies, skilled labour.

Food, beverage, tobacco - Contribution : 5%

- Growth: 12% - Great domestic demand

- Growing consumer market. Some of the biggest companies are investing more money into Nigeria - Nestle, Diageo (Guinness) and Dufil

Prima (Indomie)

36,000

26,000

50,000

South Africa India Nigeria

Average Cost of Building a House

(US$)

Source: World Bank

Growth and Job Opportunities - Fastest Growing Sectors

Telecomms and

information services - Contribution: 8%

- Market greater than at first glance Internet: 62million

devices connected, yet

many consumers own

multiple devices (phone,

laptop, ipad etc).

- Mobile Phones: Only 67

phones per 100 people,

again multiple devices

- Youthful population; largest

consumers of internet

83

114

67

127

125

70

131

Mexico

Indonesia

Nigeria

Thailand

Brazil

India

South Africa

Cell Phone subscriptions per 100

people

Source: WDI

Growth and Job Opportunities - Fastest Growing Sectors

G

G

G

G

Structure of Government

Revenue

SECTION G

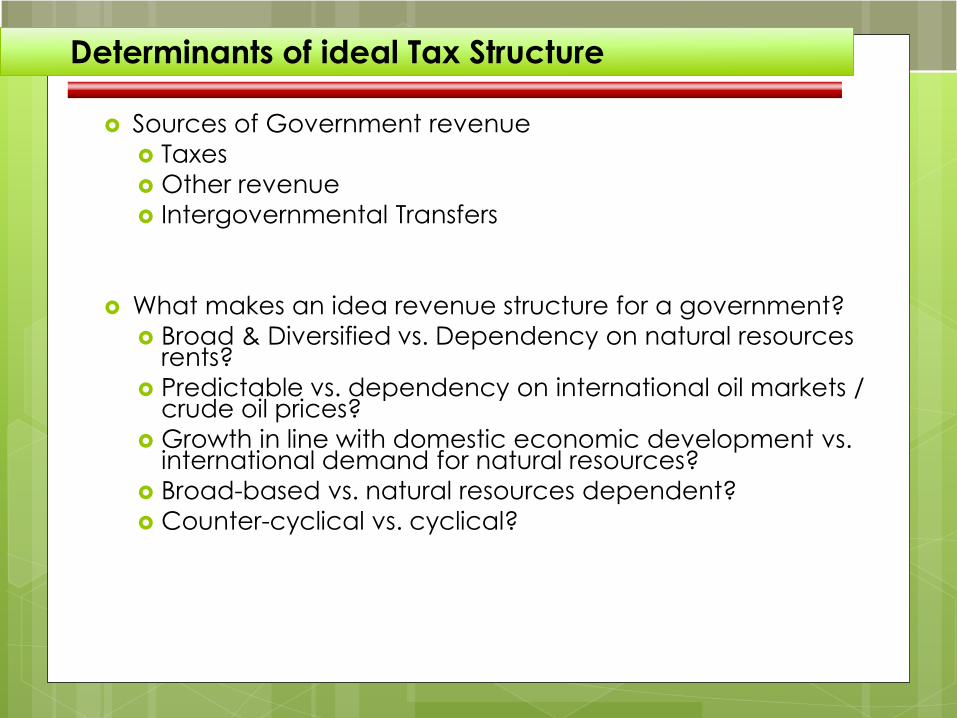

Sources of Government revenue

Taxes

Other revenue

Intergovernmental Transfers

What makes an idea revenue structure for a government?

Broad & Diversified vs. Dependency on natural resources rents?

Predictable vs. dependency on international oil markets / crude oil prices?

Growth in line with domestic economic development vs. international demand for natural resources?

Broad-based vs. natural resources dependent?

Counter-cyclical vs. cyclical?

Determinants of ideal Tax Structure

Government Revenue made up of

GOVERNMENT

REVENUE

OIL:

Crude oil/gas

exports, PPT

etc

Custom

duties/le

vies etc

NON OIL;

Corporate

tax, VAT

Nigeria revenue structure

Nigeria Revenue structure

0

10

20

30

40

50

60

70

80

90

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1998 2000 2002 2004 2006 2008 2010 2012

Contribution of oil and Non Oil revenue 1970-2013

Non Oil revenue % of total Oil revene % of total

Oil Revenue (Gross)

Crude Oil / Gas Exports

PPT and Royalties etc.

Domestic Crude Oil Sales

Other Oil Revenue

Less:

Deductions/

OIL Revenue

Oil Revenue & Distribution

5/9/2015 49

0.00 10.00 20.00 30.00 40.00 50.00 60.00

Distribution of Oil Revenues

2011

2012

2013

2014

-

1,000

2,000

3,000

4,000

5,000

6,000

Billio

ns

FGN OIL REVENUES

2011

2012

2013

2014

Crude Oil, Gas and PPT: a closer

look

5/9/2015 50

-

1,000,000,000,000.00

2,000,000,000,000.00

3,000,000,000,000.00

4,000,000,000,000.00

5,000,000,000,000.00

6,000,000,000,000.00

2011 2012 2013 2014

Crude Oil and Gas Revenue and PPT

Crude Oil And Gas Revenue Petroleum Profit Tax (PPT) Gas Revenue

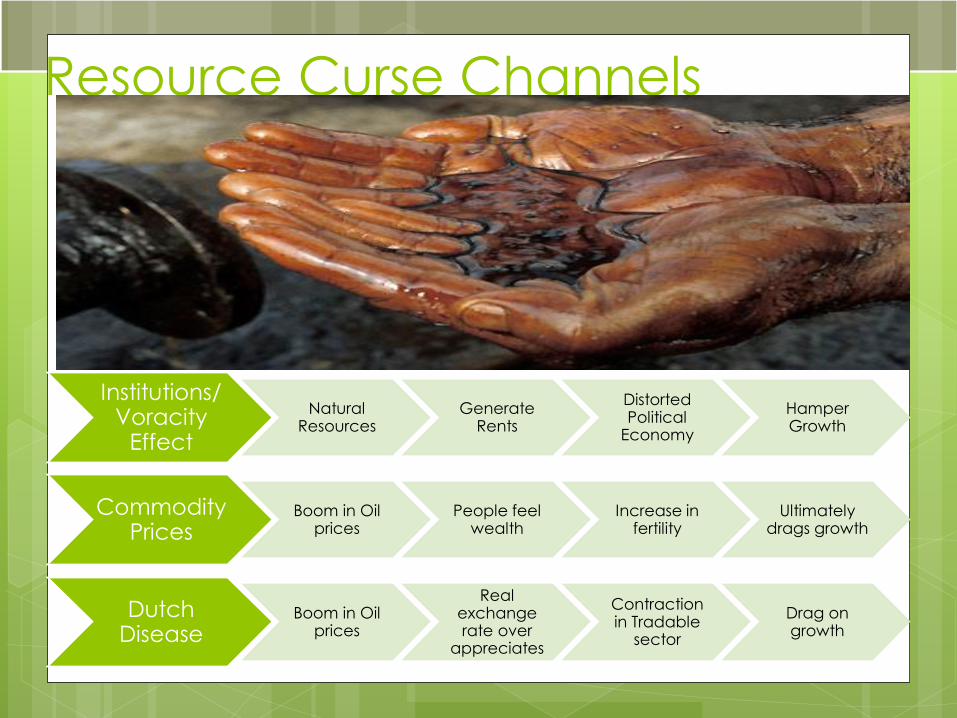

Resource Curse

The Voracity Effect/ Institutional

Impact

Volatility in Commodity Prices

Dutch Disease

Hausman and Rigobon (2002) summarise what we know now: “The

concern that natural resource wealth may somehow be immiserating is

a recurring theme in both policy discussions and in empirical analysis.

The empirical regularity seems to be in the data but understanding its

causes has been a much harder task.”

Challenges of dependency on oil revenue

Resource Curse Channels

Institutions/ Voracity

Effect

Natural Resources

Generate Rents

Distorted Political

Economy

Hamper Growth

Commodity Prices

Boom in Oil prices

People feel wealth

Increase in fertility

Ultimately drags growth

Dutch Disease

Boom in Oil prices

Real exchange rate over

appreciates

Contraction in Tradable

sector

Drag on growth

Beyond Oil- What is the Hitch?

Its all about Incentives: Yes, Democracy Now, but :

balance of power between citizens and public officials, including those at state and local government levels, is inordinately skewed in favor of the latter by virtue of their easy access to oil revenues. This perpetuates politics, even democratic politics, as patronage

Thus there are no right incentives for governance, incentives that are now sorely missing, and would contribute to reduce corruption and the rest of the problems that affect the Nigerian institutions today.

For 2014, Oil Revenues accounted for Roughly 67.12% of all FGN revenues

As such, the government has little incentive to provide services efficiently because the discipline exerted by the need to tax the public is largely absent: oil revenues are manna from heaven and keep flowing regardless of what the public sector delivers.

The Nigerian experience provides telling confirmation of this aspect of natural resources. Waste and

corruption from oil rather than Dutch disease has been responsible for its poor long run economic

performance.

Beyond Oil- There is hope!

Natural resources appear to have negative

effect on growth by impairing institutional

quality.

But it could be Managed:

Once institutions are properly controlled, the

effect can even be positive!.

In particular, it is fuel and minerals—that typically

generate rents.

This effect is quantitatively significant, amounting

to lower growth of about 0.36 percent per year.

Other resources do not seem to adversely affect

institutional quality.

FGN Non-Oil Revenues & Distribution

5/9/2015 55

- 200 400 600 800

1,000 1,200 1,400 1,600 1,800

Billio

ns

FGN NON-OIL REVENUE

2011

2012

2013

2014

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

Company

Income

Tax

Import

Duty

Excise Duty Value

Added Tax

(VAT)

Fees Custom

Levies

2008-2012

CET

Education

Tax

PAYE NITDF

DISTRIBUTION OF FGN NON-OIL REVENUES

2011

2012

2013

2014

Tariffs on Imported Goods: Impact

of government revenue

• Customs Revenue has been

increasing, peaking at N342,808.52

million in 2012

• Growth in revenue greatest in 2011

at 36.13%

• Share of imports highest in 2012,

increasing by 2.94% points to 6.09%

of total imports for that year

Source: NCS

228,567.60

311,149.38

342,808.52

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

2010 2011 2012

Na

ira

, M

illio

ns

Total Customs Revenue

N ‘000,000 2010 2011 2012

% Growth in Revenue 36.13% 10.17%

Total Import 6,648,525.9 9,892,644.1 5,624,870.4

% Imports 3.44% 3.15% 6.09%

Sources of Customs Revenue

2011 7% Port Levy

20%

Sugar Levy 5% VAT 1% CISS 0.5% ETLS

20%

Rice Levy

10%

Steel Levy

20%

Wine Levy NESS

20%

Ceme

nt Levy

100%

Cigarette

2% NAC

9.26% 0.33% 53.56% 13.96% 7.96% 11.07% 0.14% 0.00% 0.19% 2.36% 1.16% 0.00%

2012

7%

Port Levy

20%

Sugar Levy

Wheat

Flour Levy

Wheat

Grain Levy 5% VAT

1% CISS

0.5% ETLS

Brown Rice

40%

Rice Levy

10%

Steel Levy

20%

Wine Levy

30%

Textil

e Levy NESS

20%

Cement Levy

100%

Cigarette

8.89% 0.39% 0.00% 0.93% 48.33% 12.43% 7.28% 1.09% 18.90%

0.32%

0.01% 0.04% 0.16% 0.59% 0.65%

2010:

- VAT is the largest source of revenue at 55.98%

- 15.02% for Comprehensive Import Scheme (CISS)

followed

- Third greatest was the Port Levy at 9.62%

2011:

- Textile levy removed

- VAT is the largest source of Revenue at 55.56%

- CISS follows at 12.96%

- 20% Rice Levy third at 11.07%

Source: NCS

2010 7% Port Levy

Sugar Levy 5% VAT 1% CISS

0.5% ETLS

20%

Rice Levy

10%

Steel Levy

Wine Levy NESS

Ceme

nt Levy

100%

Cigarette

2% NAC

30%

Textile Levy

9.62% 0.38% 55.98% 15.02% 8.68% 7.62% 0.49% 0.00% 0.20% 0.55% 1.47% 0.00% 0.00%

2012:

- Three new levies were added (circled)

- Rice levy was increased to 40%, which

increased revenue by N30,334.61 million and

% contribution by 7.83% points

- 2% NAC levy was dropped

- Largest contributor remained 5% VAT, now

followed by Rice

Major Non-Oil Revenues: a closer

look

5/9/2015 58

-

200,000,000,000.00

400,000,000,000.00

600,000,000,000.00

800,000,000,000.00

1,000,000,000,000.00

1,200,000,000,000.00

1,400,000,000,000.00

1,600,000,000,000.00

1,800,000,000,000.00

2011 2012 2013 2014

Evolution of CIT and VAT

Company Income Tax Value Added Tax (VAT)

Tax Revenue Agriculture collects the

lowest VAT relative to its economic contribution, contributing 0.11% to total VAT, yet 18.45% to GDP

Professional Services contributes the highest VAT relative to GDP, with 13.69% of total VAT, and 3.69 of total GDP

Hotel and Catering, Mining, publishing, automobile assembly and pharmaceutical production are taxed almost equally to their contributions to GDP

Higher VAT

collected relative

to GDP

Lower VAT

collected relative

to GDP

-15% -10% -5% 0% 5% 10% 15% 20%

Professionl Services

Transport and Haulage …

Banks and Financial Institutions

Breweries. Bottling and …

Pharmaceutical, soaps and …

Automobiles and Assemblies

Publishing,Printing,Paper …

Hotel and Catering

Mining

Building and construction

Textile and Garment industry

Properties and investments

Commercial and Trading

Agricultural and Plantations

Percentage point difference in % contribution

to GDP and % contribution to VAT, 2013

Fiscal Ratios

5/9/2015 60

22.31 22.69 22.02

13.88 13.47

12.45

2010 2011 2012

Government Revenue to GDP

(%)

Old Series New Series

8.35

12.37 12.35 11.33

5.20

7.35 6.98 6.00

2010 2011 2012 2013

Federal Tax Revenue to

GDP

Old Series New Series

Analysis of PFCE and VAT Receipts

0.00

5.00

10.00

15.00

20.00

5% of PFCE= N1.8 Trillion

VAT RECEIPTS BY FIRS CLASIFICATION 2010= N465 BILLION

2010

0.00 2.00 4.00 6.00 8.00

10.00 12.00 14.00 16.00 18.00 20.00

5% of PFCE = 2.9Trillion VAT RECEIPTS BY FIRS

CLASSIFICATION 2013 (N481.6B) - H1 2014 (N248.5B)

2013

h1 2014

Jobs and Income Tax

Job creation survey started in 2012

Jobs are divided into three categories:

Informal: Fewer than 10 employees

Formal: 10 or more employees and registered

professional services

Public Sector

Policy relevance:

• Employment is important for growth and social

wellbeing

• Taxation of income can only be achieved in the

formal sector

Jobs Created

- 369,585 jobs in Q4 2014, with 138,026 (37.36%) formal

- In all quarters informal jobs were greatest, reaching 67.78% of all new jobs in Q3, 2013

- Formal jobs followed, whilst jobs created in public sector were fewer

- Jobs created has been growing in 2014, yet has not reached 2012 levels

Policy Implication: need to both encourage growth of the formal sector, ( higher skilled and paying jobs)as well as formalize the existing informal sector in order that incomes can be taxed and regulated

0

50

100

150

200

250

300

350

400

450

500

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014

Jo

bs

cre

ate

d,

Tho

usa

nd

s

PUBLIC INSTITUTIONS

INFORMAL (Less than 10 employees)

FORMAL (10 persons above & Professional Services

employing less than 10)

Employee Compensation Vs Firm

Profitability

N’000,000 2010 2011 2012 2013 2014 Q1

COMPENSATION OF EMPLOYEES 14,626,616.12 16,068,305.93 16,630,297.15 17,124,049.41 4,266,455.09

OPERATING SURPLUS 37,238,661.09 38,237,852.10 39,484,104.24 42,344,736.11 10,213,241.91

GROSS DOMESTIC PRODUCT AT MARKET PRICES 55,469,350.31 58,180,351.90 60,670,050.46 63,942,845.56 15,601,048.05

Employee compensation depends on many factors. For instance:

- Composition of the firm (capital/labour/skills intensive)

- The size of the firm (economies of scale)

- Length of time in operation (learning effects)

- Among others

Tells policy makers about the condition of the labour market and the ability of

workers to bargain for higher compensation

Growth in COE: 5.44%

Growth in OS: 4.40%

Sources of Government revenue

Taxes

Other revenue

Intergovernmental Transfers

What makes an idea revenue structure for a government?

Broad & Diversified vs. Dependency on natural resources rents?

Predictable vs. dependency on international oil markets / crude oil prices?

Growth in line with domestic economic development vs. international demand for natural resources?

Broad-based vs. natural resources dependent?

Counter-cyclical vs. cyclical?

Determinants of ideal Tax Structure

Large Firm Case Studies

Compensation of Employees The Employee compensation component of value added:

- Varies from as low as 6.02% in Dangote Cement in 2013

- As high as 32.16% in Nestle in 2012

- Increasing in all firms, perhaps indicating increased bargaining power of employees

Corporate Profitability: Operating profit to value added:

- Ratios are generally high, reaching 77.29% in Dangote Cement Group in 2013

- Lowest proportion in Guinness in 2013 at 51.52%

- It is declining through time in all companies, perhaps indicating a squeezed profit margin

Guinness Nestle Dangote Cement Group

(N '000) 2012 2013 2012 2013 2013 2014

% Employee component of value added to value added 21.48% 23.04% 30.16% 32.16% 6.02% 7.38%

% operating Profit to Value added 56.40% 51.52% 59.17% 57.45% 77.29% 68.25%

H

H

H

H

CONCLUSION

SECTION H

Conclusion Nigeria is going through hard times Like the economists say…Never let a crisis go

to waste What we have been clamoring for since

1970s and 80s, we now have the opportunity to do…further diversify our economy

Government needs funding to do this, and this CAN be done, by expanding our tax base via incorporation of the informal sector and increasing the VAT (its is very low)

So use GDP which shows structure of the economy to compare with current tax receipts and bridge the gap by formalizing the sector

Companies currently paying taxes to pay more not by increasing tax rates but encouraging

them to expand output to meet local demand as well as export.

Intra African trade

Those outside tax system informal or formal

evading taxes or underreporting output

incentives to pay and disincentive not to pay(severe penalties).

FGN Share of VAT

FGN Independent Revenue

FGN Share of Fed. Acct. (Net)

-

50.000

100.000

150.000

200.000

250.000

300.000

350.000

JanuaryFebruary

MarchApril

MayJune

July

August

SeptemberOctober

November

December

FGN Share of VAT FGN Independent Revenue FGN Share of Fed. Acct. (Net)

Dependency on FAAC allocations vs. indirect taxes / IGR

Plot 762, Independence Avenue,

Central Business District, Abuja.

Email: [email protected]

Website :www.nigerianstat.gov.ng

5/9/2015 69

“@nigerianstat”

www.facebook.com/nigerianstatistics

THANK YOU FOR YOUR ATTENTION!

“@sgyemikale”