revised schedule vi, companies bill

TRANSCRIPT

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 1/43

Name ……………………………..

Membership No. …….…………..

Background Material

Sem inar on

Revised Sch edule VI , Com panies Bi l l

&

Survey , Searc h & Seizure

03rd March 2012

Hote l Le Mer id ien

Windsor Plac e, J anpat h, New Delh i

Organised by

Nort hern Ind ia Regional Counc i l of

The Inst i t u te o f Char tered Acc ountants o f Ind ia

1

1

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 2/43

ENROLMENT FORM FOR ALL STUDY GROUP OF NIRC (2012-2013)

1. Membership fee is applicable from 1st April 2012 to 31st March 20132. Please √ you want information of Seminars (Please tick only one option) (i) Through Email (ii)Through

hard copy of Letter

3. Please send above Form with photograph & Fee at NIRC of ICAI, ICAI Bhawan, 4th Floor, Annexe

Building, I.P. Marg, N.Delhi- 02. Cheque/DD in favour of `NIRC of ICAI’ and Payable at New Delhi. 1. Rs. 7500/- For ACA 2. Rs. 9,000/- For FCA

3. Rs.12,000/- For Firm with three partners- (one out of up to Three partners may participate)

4. Rs.16,000/- For Firm with five partners- (Two out of up to Five partners may participate)

5 Rs.20,000/- For Firm with eight partners- (Three out of Eight Partners may participate )

6 Rs. 25000/- Corporate Membership (Any Two out of Five Participate) E n r o l l m e n t

F e e

7 Rs.40,000/ Corporate Membership (Any Four out of Eight Participate)

Mode of Enrolment:(Enrolment as an Individual/ a Firm/ a Company) (Please fill in Full & Block letters)

1. As a Firm/Company _________ 2. As an Individual _________________

a. Name of Individual/Firm/Company: ___________________________________________________________________

b. Address of Individual/ firm/company: __________________________________________________________________

__________________________________________________________________

c. Telephone No(s) 1. __________________ 2. ________________________ 3._____________________

d. E-mail ID: _____________________________________ [Members Detail:

A] 1. Membership No. :__________________

2. Name : ____________________________________________

3. Mobile No. _____________4. Email.Id__________________

Signature of Member______________________________

B] 1. Membership No. :____________________

2. Name : ___________________________________________

3. Mobile No. ___________4. Email.Id__________________

Signature of Member ______________________________

C] 1. Membership No. :_________________

2. Name : ___________________________________________

3. Mobile No. _____________4. Email.Id__________________

Signature of Member ________________________

D] 1. Membership No. :_________________

2. Name : ___________________________________________

3. Mobile No. ______________4. Email.Id__________________

Signature of Member ________________________

E] 1 Membership No. :_________________

2. Name : ___________________________________________

3. Mobile No. _______________4. Email.Id__________________

Signature of Member ________________________

---------------------------------------------------------------------------------------------------------------------------------------FOR OFFICE USE ONLY

FASG No/CASG No.____________ IASG No.: __________________ Receipt No.: __________________

Cheque/DD No. ________________Date: ______________________ Amount: (Rs.) _________________

Photo

Photo

Photo

Photo

Photo

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 3/43

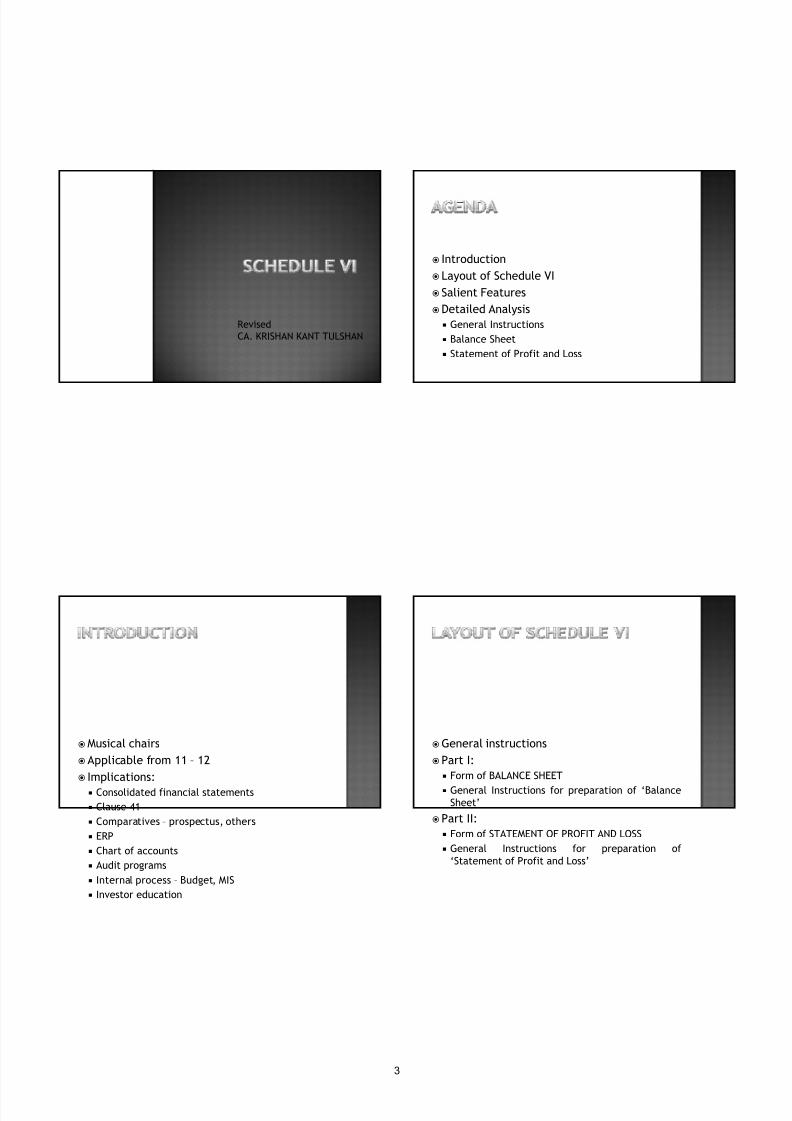

RevisedCA. KRISHAN KANT TULSHAN

Introduction Layout of Schedule VI Salient FeaturesDetailed Analysis General Instructions Balance Sheet Statement of Profit and Loss

Musical chairsApplicable from 11 – 12 Implications: Consolidated financial statements Clause 41 Comparatives – prospectus, others ERP Chart of accounts Audit programs

Internal process – Budget, MIS Investor education

General instructionsPart I: Form of BALANCE SHEET General Instructions for preparation of ‘Balance

Sheet’

Part II: Form of STATEMENT OF PROFIT AND LOSS General Instructions for preparation of

‘Statement of Profit and Loss’

3

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 4/43

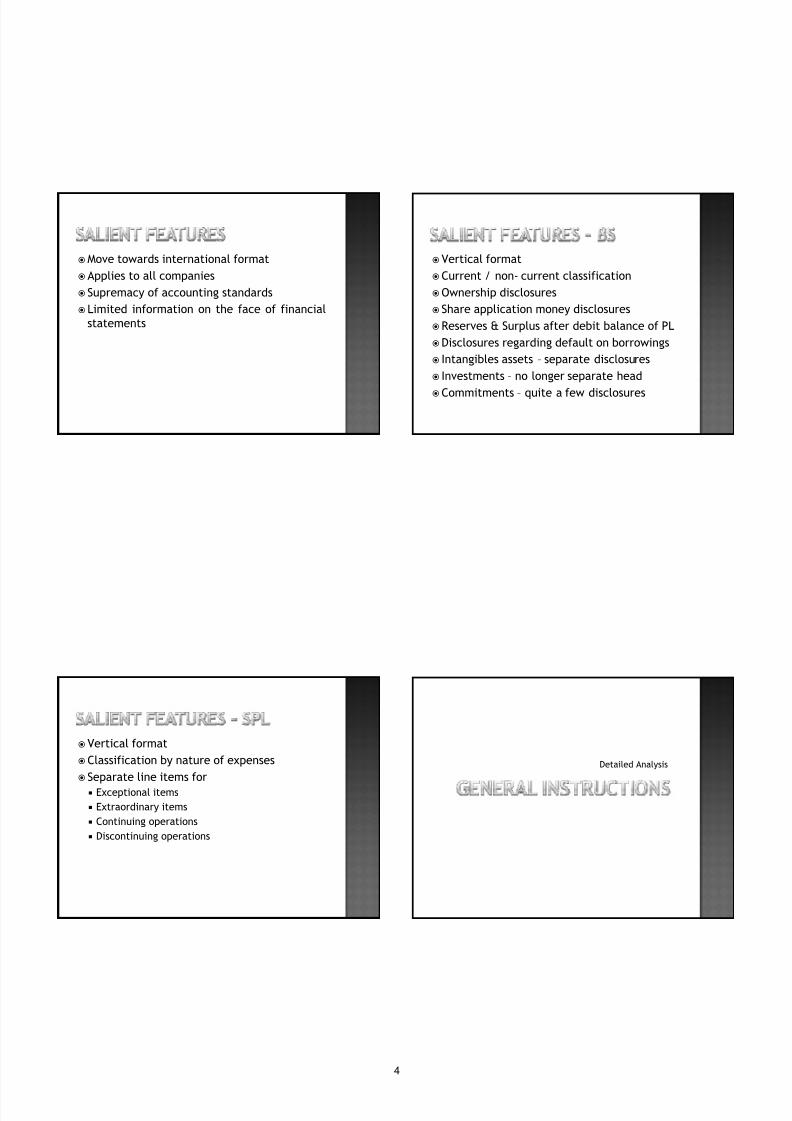

Move towards international formatApplies to all companies Supremacy of accounting standards Limited information on the face of financial

statements

Vertical formatCurrent / non- current classificationOwnership disclosures Share application money disclosuresReserves & Surplus after debit balance of PLDisclosures regarding default on borrowings Intangibles assets – separate disclosures

Investments – no longer separate head

Commitments – quite a few disclosures

Vertical formatClassification by nature of expenses Separate line items for Exceptional items Extraordinary items Continuing operations Discontinuing operations

Detailed Analysis

4

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 5/43

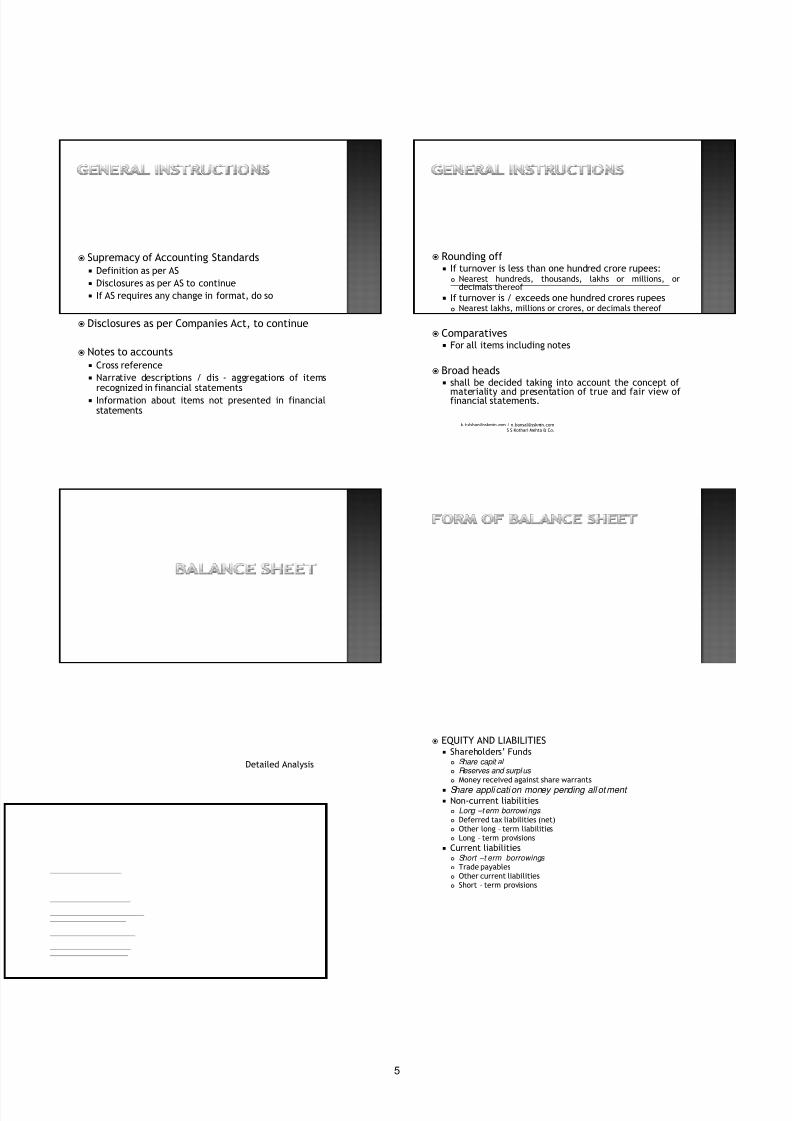

Supremacy of Accounting Standards Definition as per AS Disclosures as per AS to continue If AS requires any change in format, do so

Disclosures as per Companies Act, to continue

Notes to accounts Cross reference Narrative descriptions / dis - aggregations of items

recognized in financial statements Information about items not presented in financialstatements

Rounding off If turnover is less than one hundred crore rupees: Nearest hundreds, thousands, lakhs or millions, or

decimals thereof If turnover is / exceeds one hundred crores rupees Nearest lakhs, millions or crores, or decimals thereof

Comparatives For all items including notes

Broad heads shall be decided taking into account the concept of

materiality and presentation of true and fair view offinancial statements.

[email protected] / [email protected] S Kothari Mehta & Co.

Detailed Analysis

EQUITY AND LIABILITIES Shareholders’ Funds

Share capit al Reserves and surpl us Money received against share warrants

Share appli cation money pending allotment Non-current liabilities

Long –term borrowings Deferred tax liabilities (net) Other long – term liabilities Long – term provisions

Current liabilities Short –t erm borrowings Trade payables Other current liabilities Short – term provisions

5

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 6/43

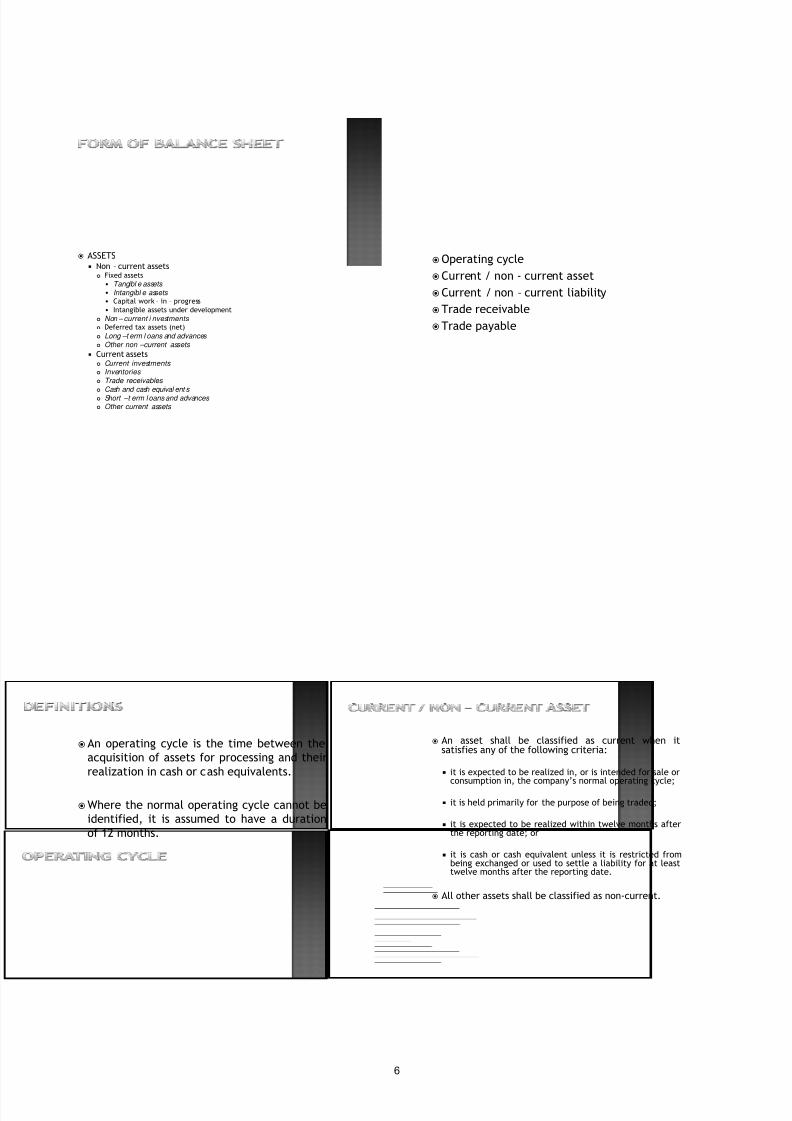

ASSETS Non – current assets

Fixed assets Tangibl e assets Intangibl e assets Capital work – in – progress Intangible assets under development

Non – current i nvestments Deferred tax assets (net) Long –t erm l oans and advances

Other non –current assets

Current assets Current investments Inventories

Trade receivables

Cash and cash equival ent s Short –t erm l oans and advances Other current assets

Operating cycleCurrent / non - current assetCurrent / non – current liabilityTrade receivableTrade payable

An operating cycle is the time between theacquisition of assets for processing and theirrealization in cash or cash equivalents.

Where the normal operating cycle cannot beidentified, it is assumed to have a durationof 12 months.

An asset shall be classified as current when itsatisfies any of the following criteria:

it is expected to be realized in, or is intended for sale orconsumption in, the company’s normal operating cycle;

it is held primarily for the purpose of being traded;

it is expected to be realized within twelve months afterthe reporting date; or

it is cash or cash equivalent unless it is restricted frombeing exchanged or used to settle a liability for at leasttwelve months after the reporting date.

All other assets shall be classified as non-current.

6

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 7/43

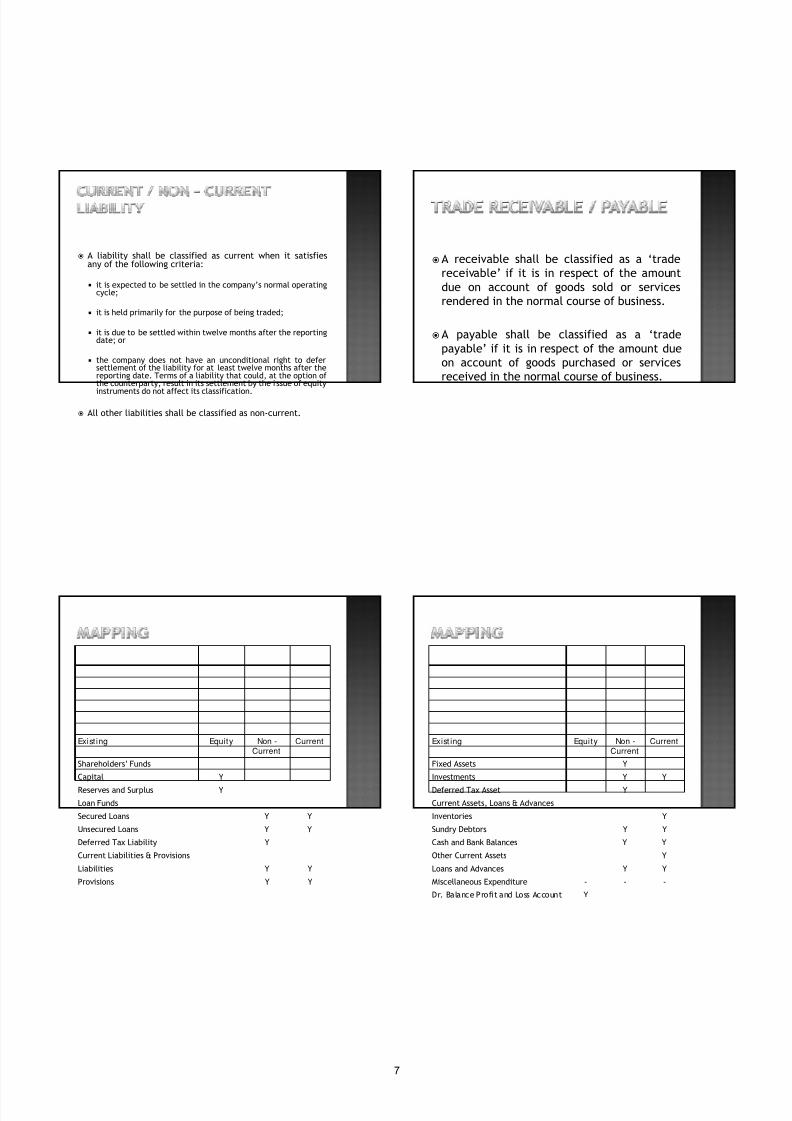

A liability shall be classified as current when it satisfiesany of the following criteria:

it is expected to be settled in the company’s normal operatingcycle;

it is held primarily for the purpose of being traded;

it is due to be settled within twelve months after the reportingdate; or

the company does not have an unconditional right to defersettlement of the liability for at least twelve months after thereporting date. Terms of a liability that could, at the option ofthe counterparty, result in its settlement by the i ssue of equity

instruments do not affect its classification.

All other liabilities shall be classified as non-current.

A receivable shall be classified as a ‘tradereceivable’ if it is in respect of the amountdue on account of goods sold or servicesrendered in the normal course of business.

A payable shall be classified as a ‘tradepayable’ if it is in respect of the amount dueon account of goods purchased or servicesreceived in the normal course of business.

Exist ing Equity Non -Current

Current

Shareholders’ Funds

Capital Y

Reserves and Surplus Y

Loan Funds

Secured Loans Y Y

Unsecured Loans Y Y

Deferred Tax Liability Y

Current Liabilities & Provisions

Liabilities Y Y

Provisions Y Y

Exist ing Equity Non -Current

Current

Fixed Assets Y

Investments Y Y

Deferred Tax Asset Y

Current Assets, Loans & Advances

Inventories Y

Sundry Debtors Y Y

Cash and Bank Balances Y Y

Other Current Assets Y

Loans and Advances Y Y

Miscellaneous Expenditure - - -

Dr. Balance Profit and Loss Account Y

7

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 8/43

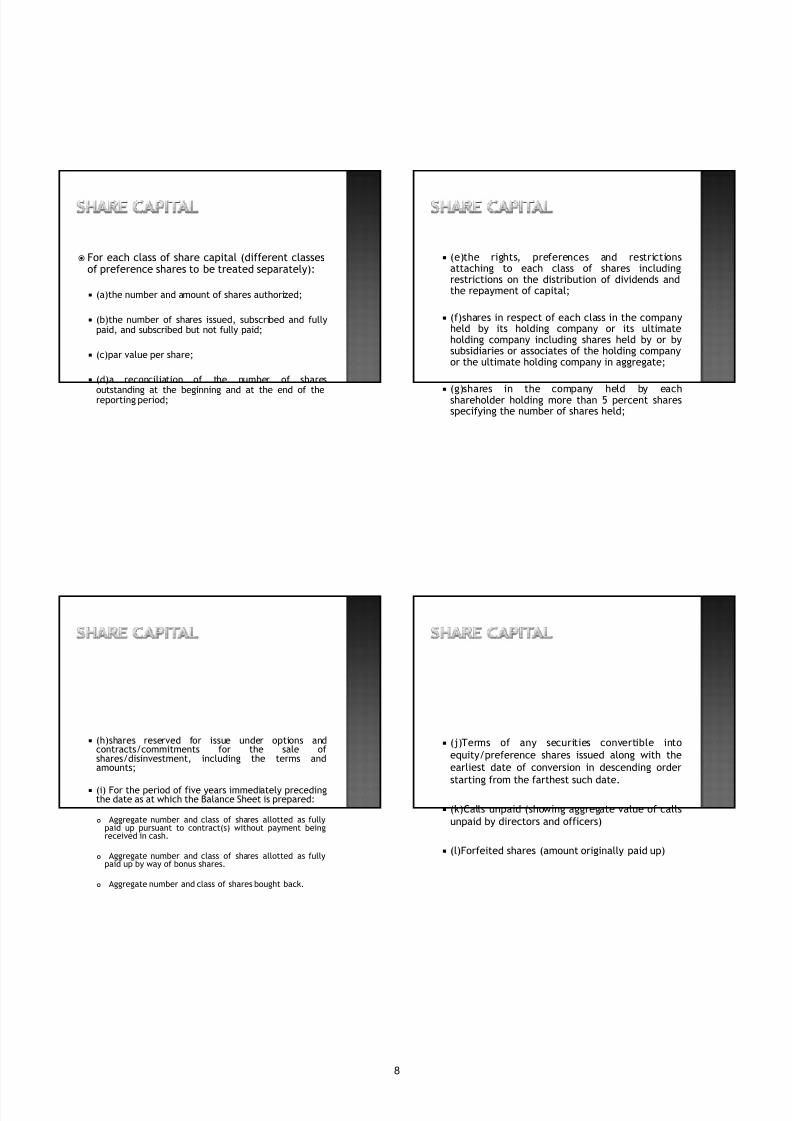

For each class of share capital (different classesof preference shares to be treated separately):

(a)the number and amount of shares authorized;

(b)the number of shares issued, subscribed and fullypaid, and subscribed but not fully paid;

(c)par value per share;

(d)a reconciliation of the number of shares

outstanding at the beginning and at the end of thereporting period;

(e)the rights, preferences and restrictionsattaching to each class of shares includingrestrictions on the distribution of dividends andthe repayment of capital;

(f)shares in respect of each class in the companyheld by its holding company or its ultimateholding company including shares held by or bysubsidiaries or associates of the holding companyor the ultimate holding company in aggregate;

(g)shares in the company held by eachshareholder holding more than 5 percent sharesspecifying the number of shares held;

(h)shares reserved for issue under options andcontracts/commitments for the sale ofshares/disinvestment, including the terms andamounts;

(i) For the period of five years immediately precedingthe date as at which the Balance Sheet is prepared:

Aggregate number and class of shares allotted as fullypaid up pursuant to contract(s) without payment beingreceived in cash.

Aggregate number and class of shares allotted as fullypaid up by way of bonus shares.

Aggregate number and class of shares bought back.

(j)Terms of any securities convertible intoequity/preference shares issued along with theearliest date of conversion in descending orderstarting from the farthest such date.

(k)Calls unpaid (showing aggregate value of callsunpaid by directors and officers)

(l)Forfeited shares (amount originally paid up)

8

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 9/43

Reserves and Surplus shall be classified as: (a)Capital Reserves ; (b)Capital Redemption Reserve; (c)Securities Premium Reserve; (d)Debenture Redemption Reserve; (e)Revaluation Reserve; (f)Share Options Outstanding Account; (g)Other Reserves – (specify the nature and purpose

of each reserve and the amount in respect thereof); (h)Surplus i.e. balance in Statement of Profit & Loss

disclosing allocations and appropriations such asdividend, bonus shares and transfer to/from reservesetc.

Other requirements:

Additions and deductions since last balance sheet tobe shown under each of the specified heads

A reserve specifically represented by earmarkedinvestments shall be termed as a ‘fund’.

Debit balance of statement of profit and loss shall beshown as a negative figure under the head ‘Surplus’.

Similarly, the balance of ‘Reserves and Surplus’, afteradjusting negative balance of surplus, if any, shall beshown under the head ‘Reserves and Surplus’ even ifthe resulting figure is in the negative.

Share application money includes advancestowards allotment of share capital.

Share application money not exceeding theissued capital and to the extent not refundableshall be shown under the head Equity and

Share application money to the extentrefundable i.e., the amount in excess ofsubscription or in case the requirements ofminimum subscription are not met, shall beseparately shown under ‘Óther currentliabilities’

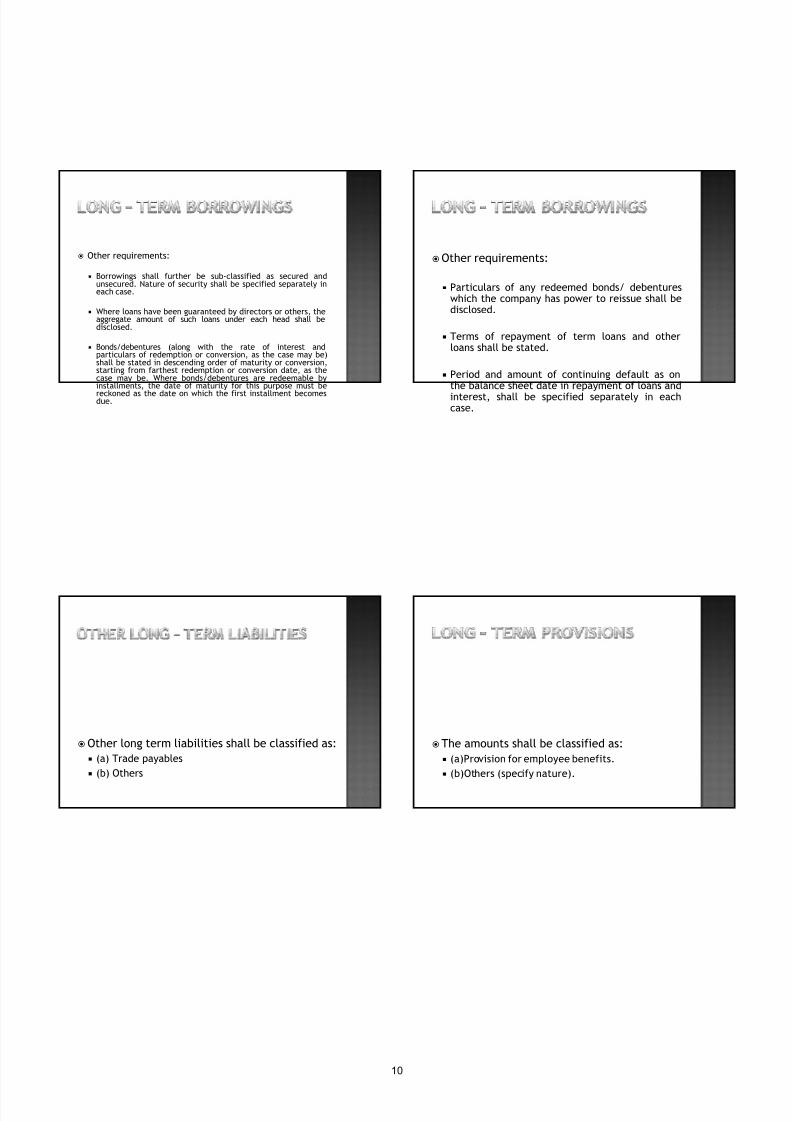

Long-term borrowings shall be classified as: (a)Bonds/debentures. (b)Term loans from banks. from other parties.

(c)Deferred payment liabilities. (d)Deposits. (e)Loans and advances from related parties. (f)Long term maturities of finance lease

obligations (g)Other loans and advances (specify nature).

9

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 10/43

Other requirements:

Borrowings shall further be sub-classified as secured andunsecured. Nature of security shall be specified separately ineach case.

Where loans have been guaranteed by directors or others, theaggregate amount of such loans under each head shall bedisclosed.

Bonds/debentures (along with the rate of interest andparticulars of redemption or conversion, as the case may be)shall be stated in descending order of maturity or conversion,starting from farthest redemption or conversion date, as thecase may be. Where bonds/debentures are redeemable byinstallments, the date of maturity for this purpose must be

reckoned as the date on which the first installment becomesdue.

Other requirements:

Particulars of any redeemed bonds/ debentureswhich the company has power to reissue shall bedisclosed.

Terms of repayment of term loans and otherloans shall be stated.

Period and amount of continuing default as onthe balance sheet date in repayment of loans andinterest, shall be specified separately in eachcase.

Other long term liabilities shall be classified as: (a) Trade payables (b) Others

The amounts shall be classified as: (a)Provision for employee benefits. (b)Others (specify nature).

10

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 11/43

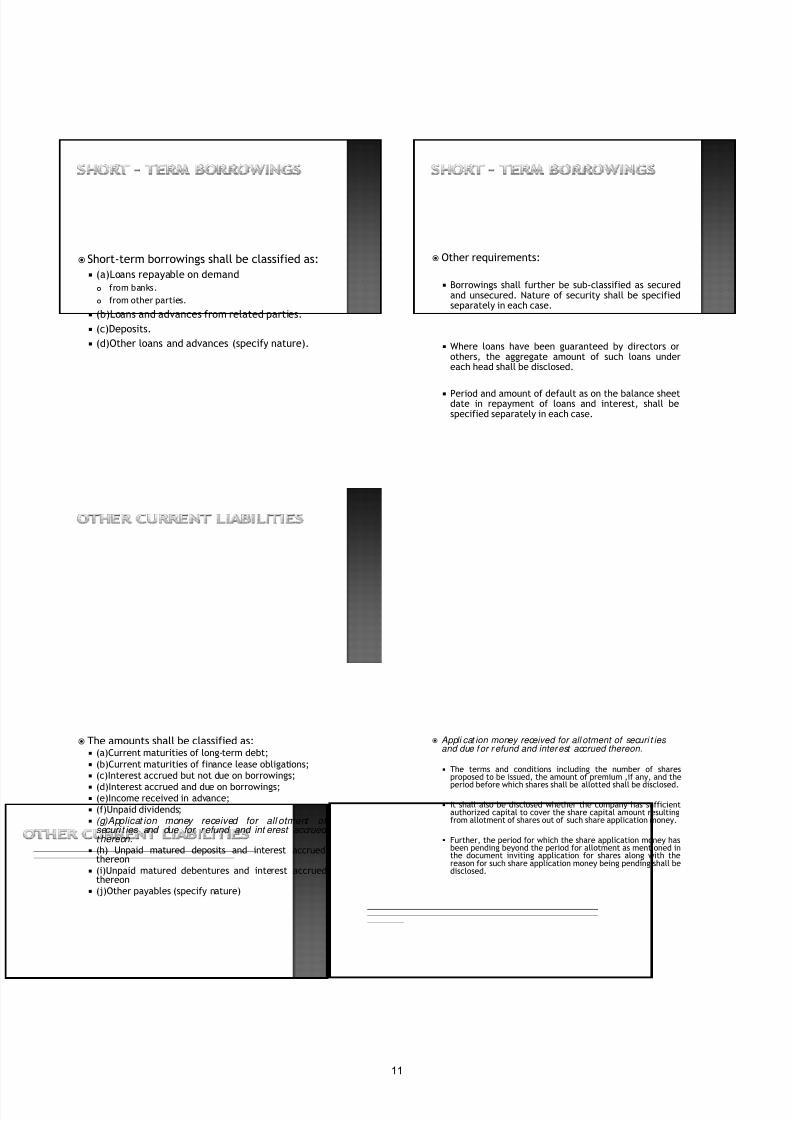

Short-term borrowings shall be classified as: (a)Loans repayable on demand from banks. from other parties.

(b)Loans and advances from related parties. (c)Deposits. (d)Other loans and advances (specify nature).

Other requirements:

Borrowings shall further be sub-classified as securedand unsecured. Nature of security shall be specifiedseparately in each case.

Where loans have been guaranteed by directors orothers, the aggregate amount of such loans undereach head shall be disclosed.

Period and amount of default as on the balance sheetdate in repayment of loans and interest, shall bespecified separately in each case.

The amounts shall be classified as: (a)Current maturities of long-term debt; (b)Current maturities of finance lease obligations; (c)Interest accrued but not due on borrowings; (d)Interest accrued and due on borrowings; (e)Income received in advance; (f)Unpaid dividends; (g)Applicat ion money received for all otment of

securi t ies and due for refund and int erest accrued t hereon.

(h) Unpaid matured deposits and interest accruedthereon

(i)Unpaid matured debentures and interest accruedthereon

(j)Other payables (specify nature)

Appli cat ion money received for all otment of securi t ies and due for r efund and interest accrued thereon.

The terms and conditions including the number of sharesproposed to be issued, the amount of premium ,if any, and the

period before which shares shall be allotted shall be disclosed.

It shall also be disclosed whether the company has sufficientauthorized capital to cover the share capital amount resultingfrom allotment of shares out of such share application money.

Further, the period for which the share application money hasbeen pending beyond the period for allotment as mentioned inthe document inviting application for shares along with thereason for such share application money being pending shall bedisclosed.

11

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 12/43

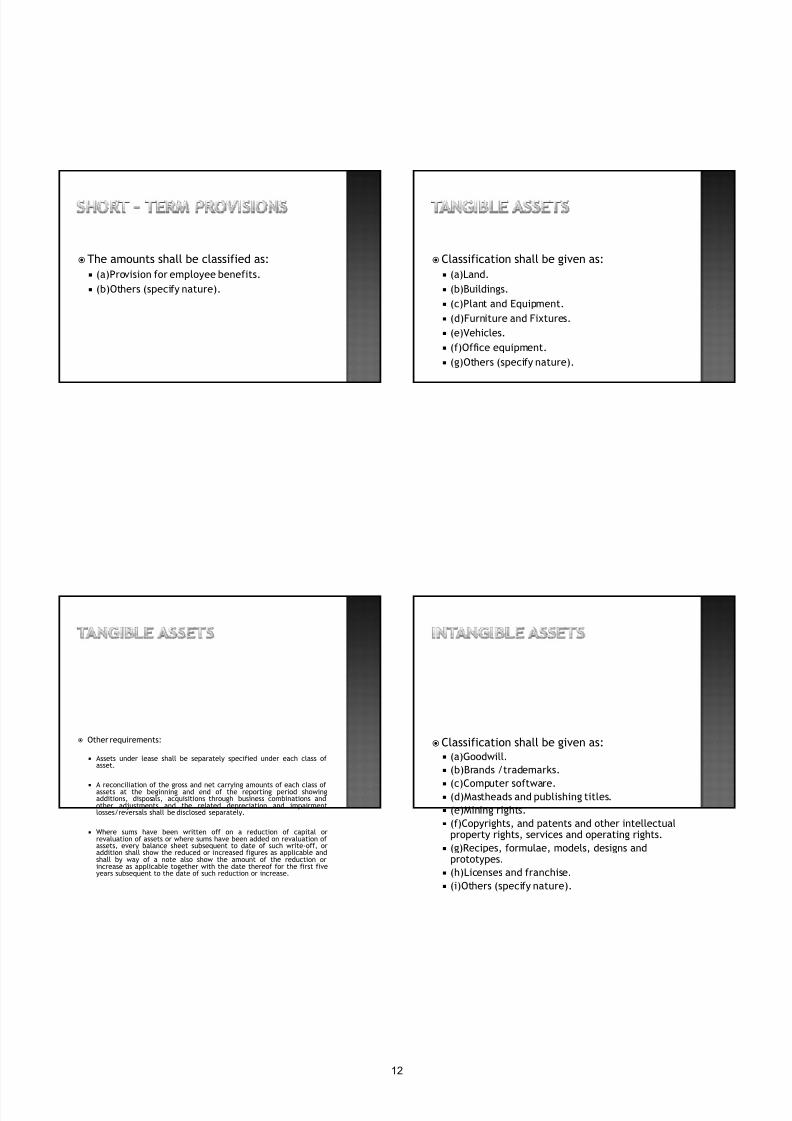

The amounts shall be classified as: (a)Provision for employee benefits. (b)Others (specify nature).

Classification shall be given as: (a)Land. (b)Buildings. (c)Plant and Equipment. (d)Furniture and Fixtures. (e)Vehicles. (f)Office equipment. (g)Others (specify nature).

Other requirements:

Assets under lease shall be separately specified under each class ofasset.

A reconciliation of the gross and net carrying amounts of each class ofassets at the beginning and end of the reporting period showingadditions, disposals, acquisitions through business combinations andother adjustments and the related depreciation and impairmentlosses/reversals shall be disclosed separately.

Where sums have been written off on a reduction of capital orrevaluation of assets or where sums have been added on revaluation ofassets, every balance sheet subsequent to date of such write-off, oraddition shall show the reduced or increased figures as applicable andshall by way of a note also show the amount of the reduction orincrease as applicable together with the date thereof for the first fiveyears subsequent to the date of such reduction or increase.

Classification shall be given as: (a)Goodwill. (b)Brands /trademarks.

(c)Computer software. (d)Mastheads and publishing titles. (e)Mining rights. (f)Copyrights, and patents and other intellectual

property rights, services and operating rights. (g)Recipes, formulae, models, designs and

prototypes. (h)Licenses and franchise. (i)Others (specify nature).

12

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 13/43

Other requirements:

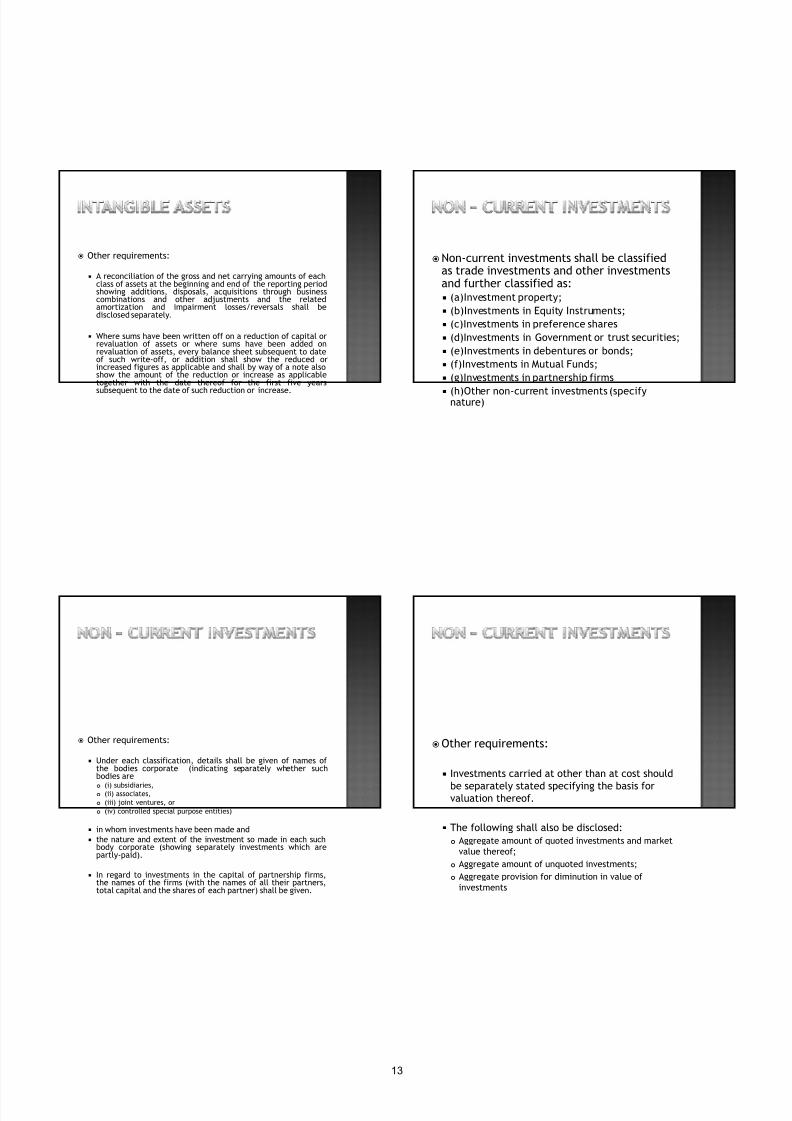

A reconciliation of the gross and net carrying amounts of eachclass of assets at the beginning and end of the reporting periodshowing additions, disposals, acquisitions through businesscombinations and other adjustments and the relatedamortization and impairment losses/reversals shall bedisclosed separately.

Where sums have been written off on a reduction of capital orrevaluation of assets or where sums have been added onrevaluation of assets, every balance sheet subsequent to dateof such write-off, or addition shall show the reduced orincreased figures as applicable and shall by way of a note alsoshow the amount of the reduction or increase as applicabletogether with the date thereof for the first five years

subsequent to the date of such reduction or increase.

Non-current investments shall be classifiedas trade investments and other investmentsand further classified as: (a)Investment property; (b)Investments in Equity Instruments; (c)Investments in preference shares (d)Investments in Government or trust securities; (e)Investments in debentures or bonds; (f)Investments in Mutual Funds; (g)Investments in partnership firms

(h)Other non-current investments (specifynature)

Other requirements:

Under each classification, details shall be given of names ofthe bodies corporate (indicating separately whether suchbodies are (i) subsidiaries, (ii) associates, (iii) joint ventures, or (iv) controlled special purpose entities)

in whom investments have been made and the nature and extent of the investment so made in each such

body corporate (showing separately investments which arepartly-paid).

In regard to investments in the capital of partnership firms,the names of the firms (with the names of all their partners,total capital and the shares of each partner) shall be given.

Other requirements:

Investments carried at other than at cost should

be separately stated specifying the basis forvaluation thereof.

The following shall also be disclosed: Aggregate amount of quoted investments and market

value thereof; Aggregate amount of unquoted investments; Aggregate provision for diminution in value of

investments

13

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 14/43

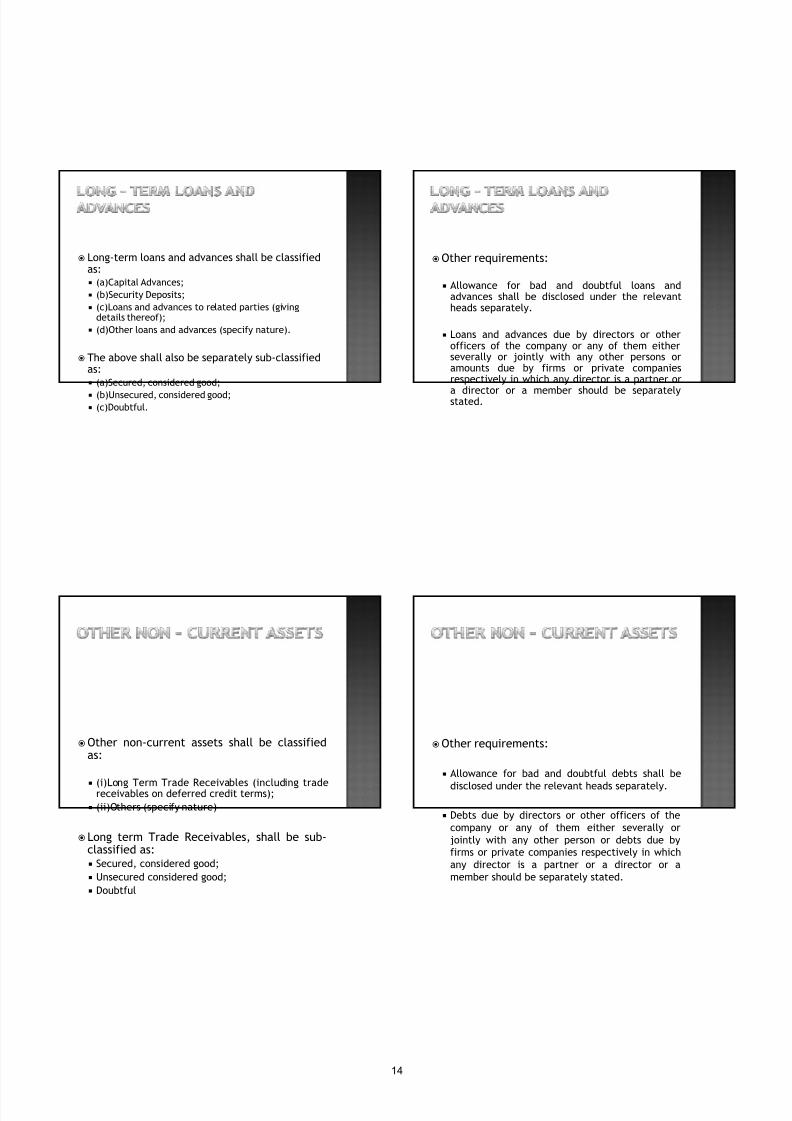

Long-term loans and advances shall be classifiedas: (a)Capital Advances; (b)Security Deposits; (c)Loans and advances to related parties (giving

details thereof); (d)Other loans and advances (specify nature).

The above shall also be separately sub-classifiedas: (a)Secured, considered good; (b)Unsecured, considered good; (c)Doubtful.

Other requirements:

Allowance for bad and doubtful loans andadvances shall be disclosed under the relevantheads separately.

Loans and advances due by directors or otherofficers of the company or any of them eitherseverally or jointly with any other persons oramounts due by firms or private companiesrespectively in which any director is a partner or

a director or a member should be separatelystated.

Other non-current assets shall be classifiedas:

(i)Long Term Trade Receivables (including tradereceivables on deferred credit terms); (ii)Others (specify nature)

Long term Trade Receivables, shall be sub-classified as: Secured, considered good; Unsecured considered good; Doubtful

Other requirements:

Allowance for bad and doubtful debts shall be

disclosed under the relevant heads separately.

Debts due by directors or other officers of thecompany or any of them either severally orjointly with any other person or debts due byfirms or private companies respectively in whichany director is a partner or a director or amember should be separately stated.

14

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 15/43

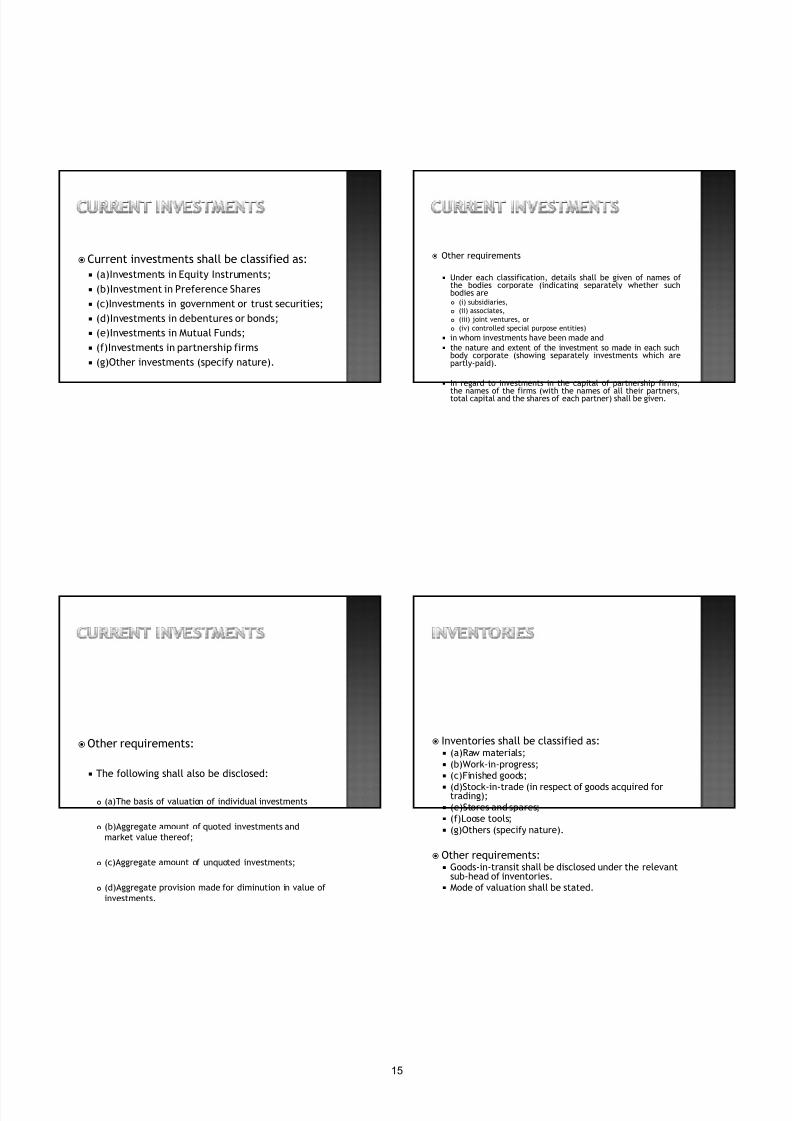

Current investments shall be classified as: (a)Investments in Equity Instruments; (b)Investment in Preference Shares (c)Investments in government or trust securities; (d)Investments in debentures or bonds; (e)Investments in Mutual Funds; (f)Investments in partnership firms (g)Other investments (specify nature).

Other requirements

Under each classification, details shall be given of names ofthe bodies corporate (indicating separately whether suchbodies are (i) subsidiaries, (ii) associates, (iii) joint ventures, or (iv) controlled special purpose entities)

in whom investments have been made and the nature and extent of the investment so made in each such

body corporate (showing separately investments which arepartly-paid).

In regard to investments in the capital of partnership firms,

the names of the firms (with the names of all their partners,total capital and the shares of each partner) shall be given.

Other requirements:

The following shall also be disclosed:

(a)The basis of valuation of individual investments

(b)Aggregate amount of quoted investments andmarket value thereof;

(c)Aggregate amount of unquoted investments;

(d)Aggregate provision made for diminution in value ofinvestments.

Inventories shall be classified as: (a)Raw materials; (b)Work-in-progress; (c)Finished goods; (d)Stock-in-trade (in respect of goods acquired fortrading); (e)Stores and spares; (f)Loose tools; (g)Others (specify nature).

Other requirements: Goods-in-transit shall be disclosed under the relevant

sub-head of inventories. Mode of valuation shall be stated.

15

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 16/43

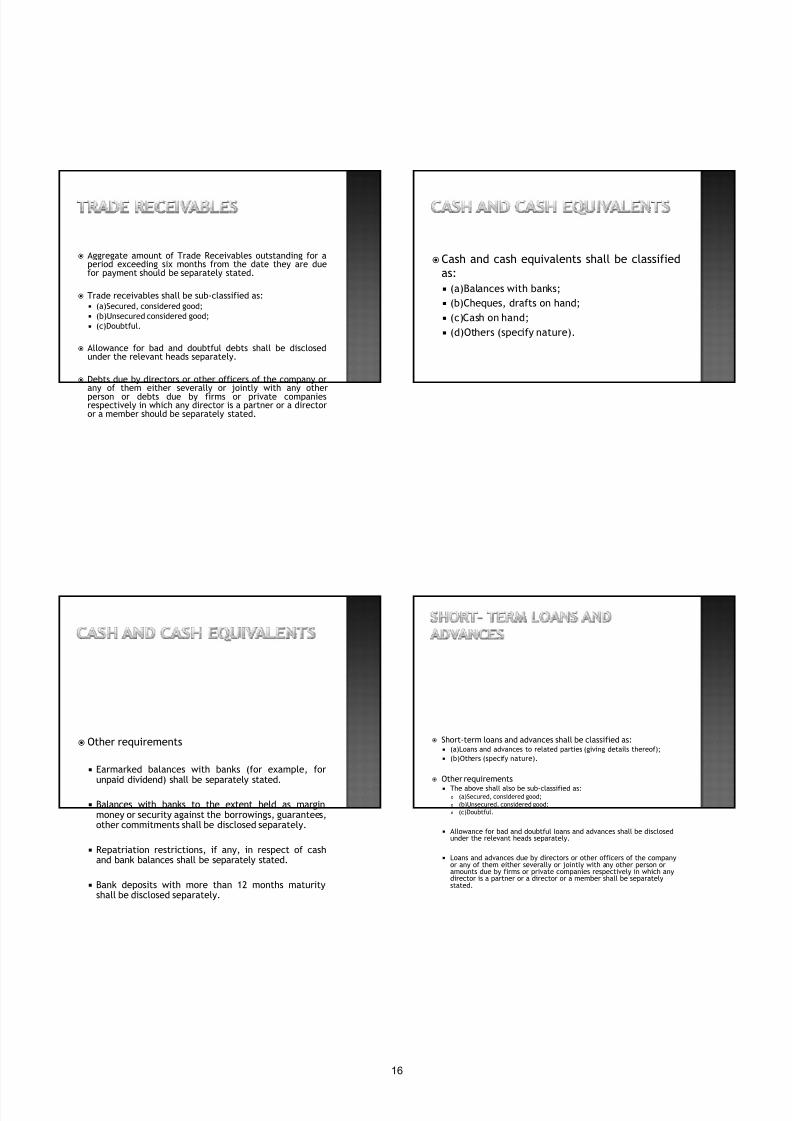

Aggregate amount of Trade Receivables outstanding for aperiod exceeding six months from the date they are duefor payment should be separately stated.

Trade receivables shall be sub-classified as: (a)Secured, considered good; (b)Unsecured considered good; (c)Doubtful.

Allowance for bad and doubtful debts shall be disclosedunder the relevant heads separately.

Debts due by directors or other officers of the company orany of them either severally or jointly with any otherperson or debts due by firms or private companiesrespectively in which any director is a partner or a directoror a member should be separately stated.

Cash and cash equivalents shall be classifiedas: (a)Balances with banks; (b)Cheques, drafts on hand; (c)Cash on hand; (d)Others (specify nature).

Other requirements

Earmarked balances with banks (for example, forunpaid dividend) shall be separately stated.

Balances with banks to the extent held as marginmoney or security against the borrowings, guarantees,other commitments shall be disclosed separately.

Repatriation restrictions, if any, in respect of cashand bank balances shall be separately stated.

Bank deposits with more than 12 months maturityshall be disclosed separately.

Short-term loans and advances shall be classified as: (a)Loans and advances to related parties (giving details thereof); (b)Others (specify nature).

Other requirements The above shall also be sub-classified as:

(a)Secured, considered good; (b)Unsecured, considered good; (c)Doubtful.

Allowance for bad and doubtful loans and advances shall be disclosedunder the relevant heads separately.

Loans and advances due by directors or other officers of the companyor any of them either severally or jointly with any other person oramounts due by firms or private companies respectively in which anydirector is a partner or a director or a member shall be separatelystated.

16

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 17/43

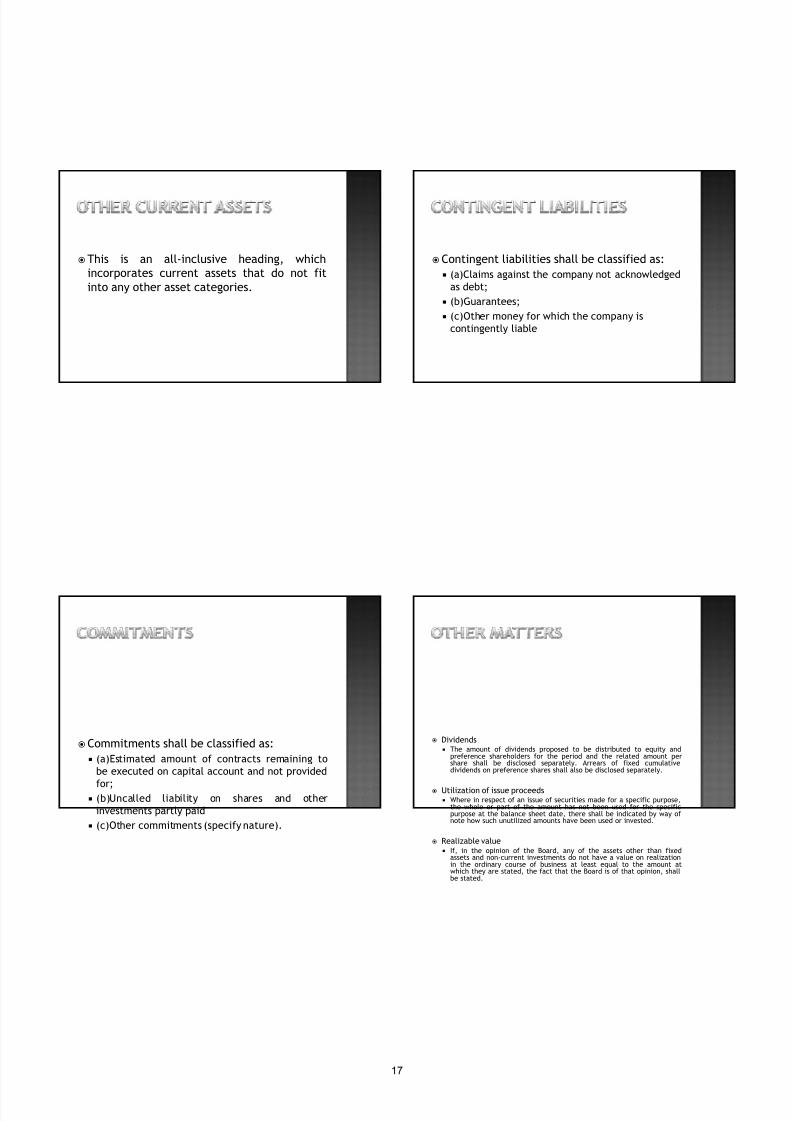

This is an all-inclusive heading, whichincorporates current assets that do not fitinto any other asset categories.

Contingent liabilities shall be classified as: (a)Claims against the company not acknowledged

as debt; (b)Guarantees; (c)Other money for which the company is

contingently liable

Commitments shall be classified as: (a)Estimated amount of contracts remaining to

be executed on capital account and not provided

for; (b)Uncalled liability on shares and other

investments partly paid (c)Other commitments (specify nature).

Dividends The amount of dividends proposed to be distributed to equity and

preference shareholders for the period and the related amount pershare shall be disclosed separately. Arrears of fixed cumulativedividends on preference shares shall also be disclosed separately.

Utilization of issue proceeds Where in respect of an issue of securities made for a specific purpose,

the whole or part of the amount has not been used for the specificpurpose at the balance sheet date, there shall be indicated by way ofnote how such unutilized amounts have been used or invested.

Realizable value If, in the opinion of the Board, any of the assets other than fixed

assets and non-current investments do not have a value on realizationin the ordinary course of business at least equal to the amount atwhich they are stated, the fact that the Board is of that opinion, shallbe stated.

17

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 18/43

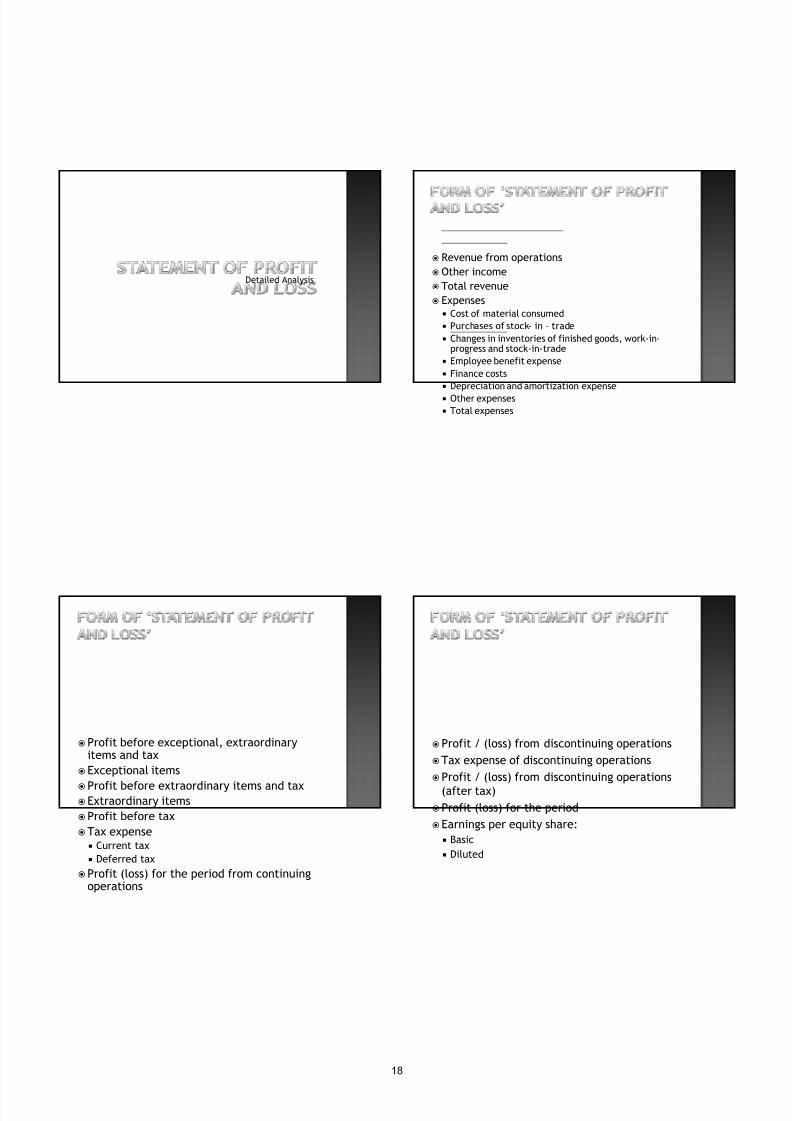

Detailed Analysis

Revenue from operations Other income Total revenue Expenses

Cost of material consumed Purchases of stock- in – trade Changes in inventories of finished goods, work-in-

progress and stock-in-trade Employee benefit expense Finance costs Depreciation and amortization expense Other expenses Total expenses

Profit before exceptional, extraordinaryitems and tax

Exceptional items

Profit before extraordinary items and taxExtraordinary itemsProfit before taxTax expense Current tax Deferred tax

Profit (loss) for the period from continuingoperations

Profit / (loss) from discontinuing operationsTax expense of discontinuing operationsProfit / (loss) from discontinuing operations

(after tax)Profit (loss) for the periodEarnings per equity share: Basic Diluted

18

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 19/43

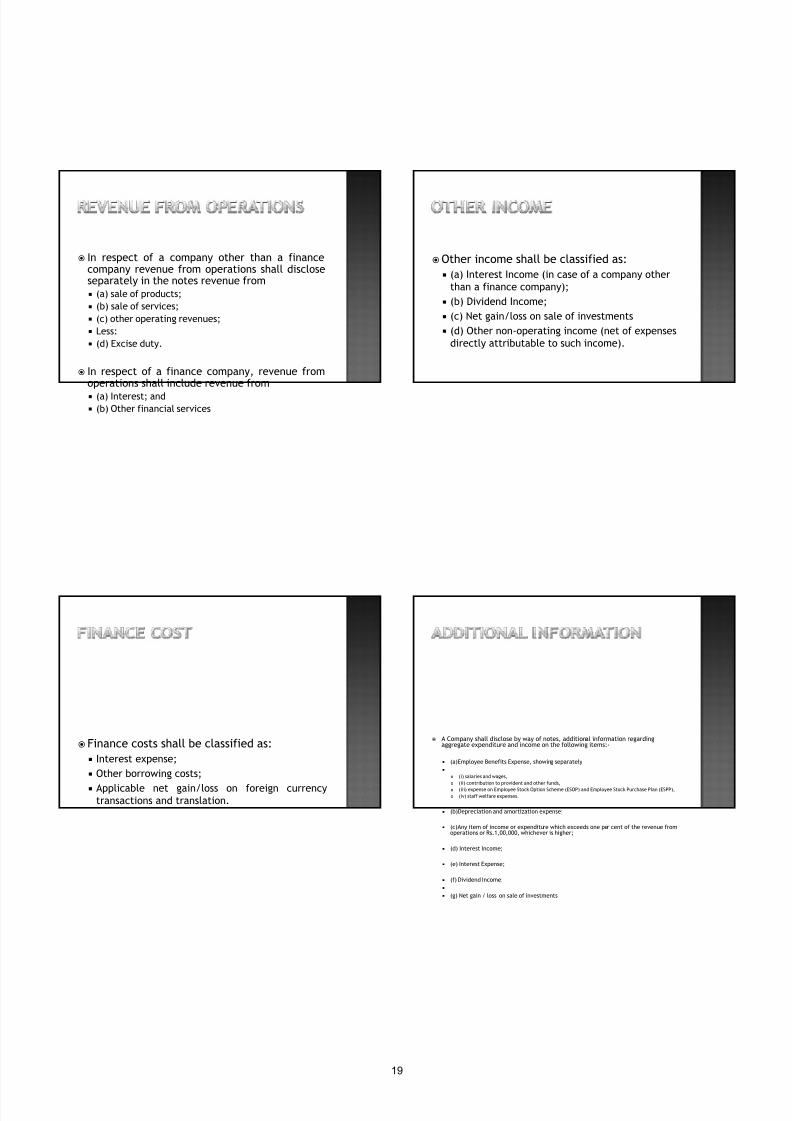

In respect of a company other than a financecompany revenue from operations shall discloseseparately in the notes revenue from (a) sale of products; (b) sale of services; (c) other operating revenues; Less: (d) Excise duty.

In respect of a finance company, revenue fromoperations shall include revenue from (a) Interest; and (b) Other financial services

Other income shall be classified as: (a) Interest Income (in case of a company other

than a finance company); (b) Dividend Income; (c) Net gain/loss on sale of investments (d) Other non-operating income (net of expenses

directly attributable to such income).

Finance costs shall be classified as: Interest expense; Other borrowing costs; Applicable net gain/loss on foreign currency

transactions and translation.

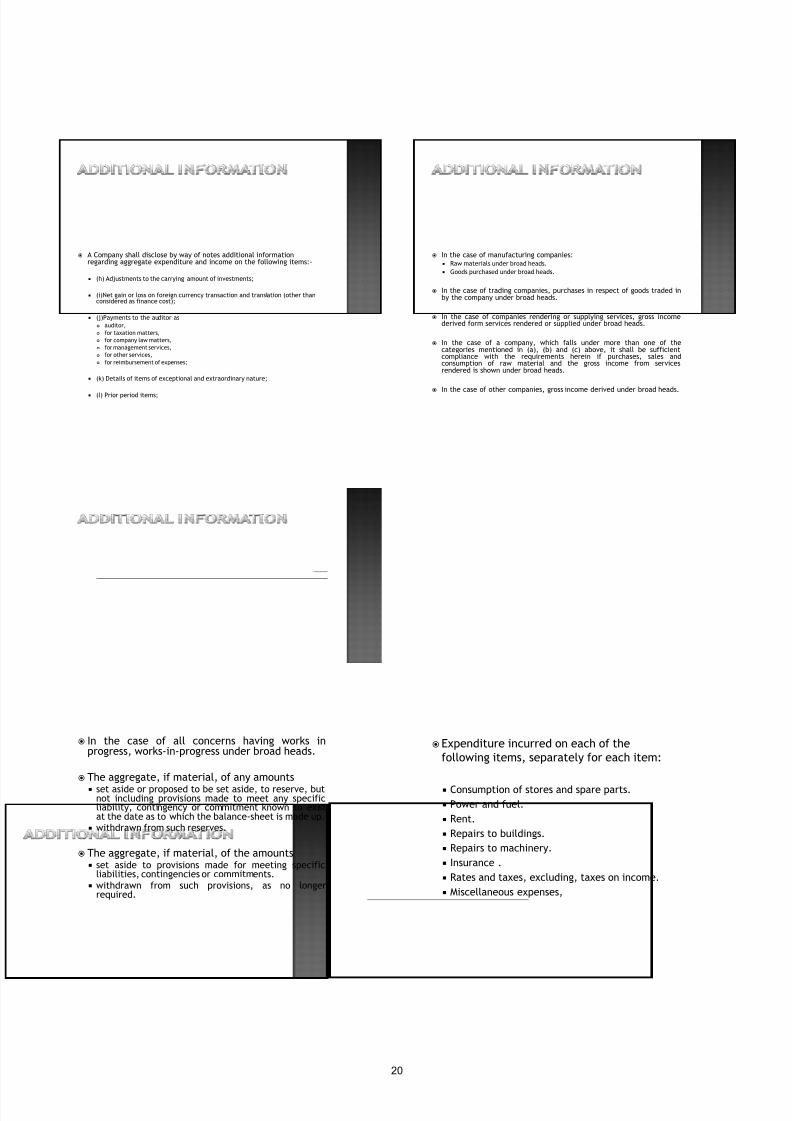

A Company shall disclose by way of notes, additional information regardingaggregate expenditure and income on the following items:-

(a)Employee Benefits Expense, showing separately

(i) salaries and wages, (ii) contribution to provident and other funds, (iii) expense on Employee Stock Option Scheme (ESOP) and Employee Stock Purchase Plan (ESPP), (iv) staff welfare expenses.

(b)Depreciation and amortization expense;

(c)Any item of income or expenditure which exceeds one per cent of the revenue fromoperations or Rs.1,00,000, whichever is higher;

(d) Interest Income;

(e) Interest Expense;

(f) Dividend Income;

(g) Net gain / loss on sale of investments

19

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 20/43

A Company shall disclose by way of notes additional informationregarding aggregate expenditure and income on the following items:-

(h) Adjustments to the carrying amount of investments;

(i)Net gain or loss on foreign currency transaction and translation (other thanconsidered as finance cost);

(j)Payments to the auditor as auditor, for taxation matters, for company law matters, for management services, for other services, for reimbursement of expenses;

(k) Details of items of exceptional and extraordinary nature;

(l) Prior period items;

In the case of manufacturing companies: Raw materials under broad heads. Goods purchased under broad heads.

In the case of trading companies, purchases in respect of goods traded inby the company under broad heads.

In the case of companies rendering or supplying services, gross incomederived form services rendered or supplied under broad heads.

In the case of a company, which falls under more than one of thecategories mentioned in (a), (b) and (c) above, it shall be sufficientcompliance with the requirements herein if purchases, sales andconsumption of raw material and the gross income from servicesrendered is shown under broad heads.

In the case of other companies, gross income derived under broad heads.

In the case of all concerns having works inprogress, works-in-progress under broad heads.

The aggregate, if material, of any amounts set aside or proposed to be set aside, to reserve, but

not including provisions made to meet any specificliability, contingency or commitment known to existat the date as to which the balance-sheet is made up.

withdrawn from such reserves.

The aggregate, if material, of the amounts set aside to provisions made for meeting specific

liabilities, contingencies or commitments. withdrawn from such provisions, as no longer

required.

Expenditure incurred on each of thefollowing items, separately for each item:

Consumption of stores and spare parts. Power and fuel. Rent. Repairs to buildings. Repairs to machinery. Insurance . Rates and taxes, excluding, taxes on income. Miscellaneous expenses,

20

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 21/43

A Company shall disclose by way of notesadditional information regarding aggregateexpenditure and income on the followingitems:- Dividends from subsidiary companies. Provisions for losses of subsidiary companies.

Value of imports calculated on C.I.F basis by thecompany during the financial year in respect of – Raw materials; Components and spare parts; Capital goods;

Expenditure in foreign currency during the financialyear on account of royalty, know-how, professionaland consultation fees, interest, and other matters;

Total value if all imported raw materials, spare partsand components consumed during the financial yearand the total value of all indigenous raw materials,spare parts and components similarly consumed andthe percentage of each to the total consumption.

The amount remitted during the year in foreigncurrencies on account of dividends with aspecific mention of the total number of non-

resident shareholders, the total number ofshares held by them on which the dividends weredue and the year to which the dividends related;

Earnings in foreign exchange classified under thefollowing heads, namely:- Export of goods calculated on F.O.B. basis; Royalty, know-how ,professional and consultation

fees; Interest and dividend; Other income, indicating the nature thereof

No longer required: In case of interest / dividend income – tds details Details / computation of managerial

remuneration AND QUANTITATIVE DETAILS, BUT FOR THE COST

ACCOUNTING RECORD AND REPORT RULES

21

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 22/43

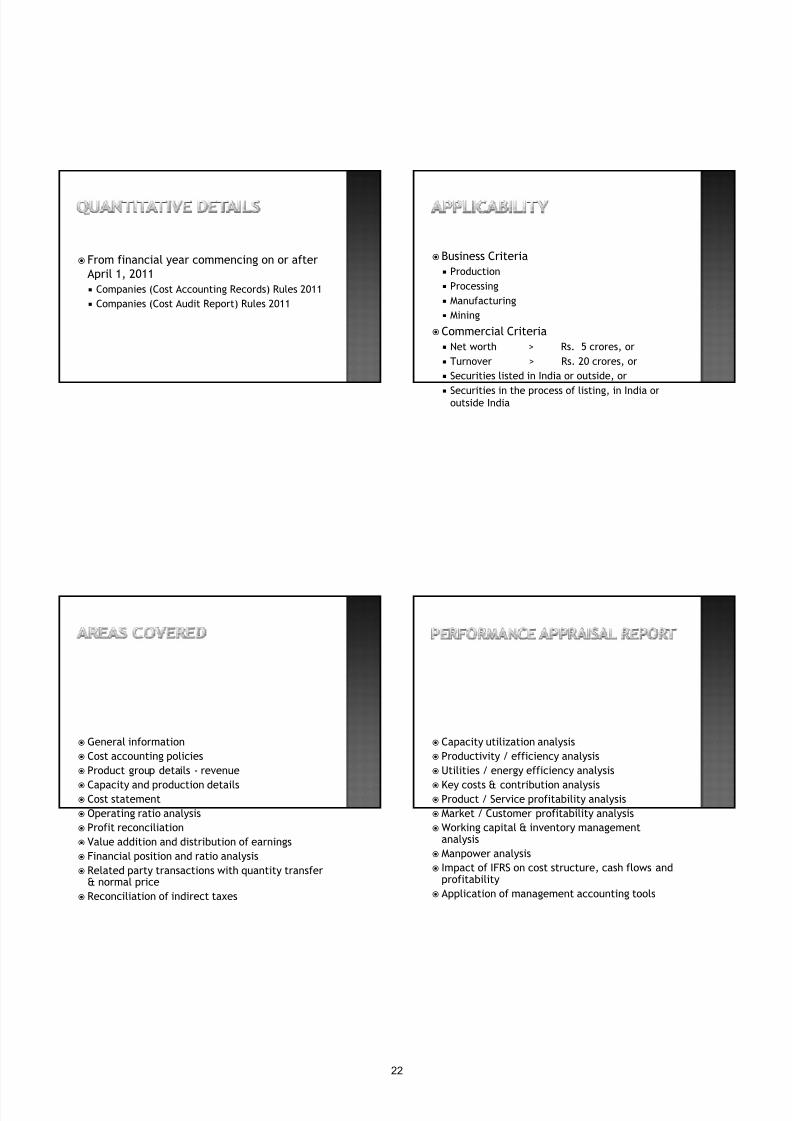

From financial year commencing on or afterApril 1, 2011 Companies (Cost Accounting Records) Rules 2011 Companies (Cost Audit Report) Rules 2011

Business Criteria Production Processing Manufacturing Mining

Commercial Criteria Net worth > Rs. 5 crores, or Turnover > Rs. 20 crores, or Securities listed in India or outside, or

Securities in the process of listing, in India oroutside India

General information Cost accounting policies Product group details - revenue

Capacity and production details Cost statement Operating ratio analysis Profit reconciliation Value addition and distribution of earnings Financial position and ratio analysis Related party transactions with quantity transfer

& normal price Reconciliation of indirect taxes

Capacity utilization analysis Productivity / efficiency analysis Utilities / energy efficiency analysis

Key costs & contribution analysis Product / Service profitability analysis Market / Customer profitability analysis Working capital & inventory management

analysis Manpower analysis Impact of IFRS on cost structure, cash flows and

profitability Application of management accounting tools

22

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 23/43

Companies Bill 2011 - Changing Face of Indian Company Law

Ashish Makhija*

B.Com (Hons.), LLB, FCA, FICWA

The much-awaited Companies Bill 2011 was introduced in Lok Sabha on 15

December 2011. The Indian administration has made several attempts to bring

out a complete code replacing the existing Companies Act, 1956 since 1993 but

without success. The Ministry of Corporate Affairs is hopeful that the latest

version of the comprehensive new bill will see the light of the day during the

forthcoming Budget Session in March 2012.

The Companies Bill 2011 attempts to meet the changing dynamics of business,

governance and accountability. From a broader perspective, one thing is quite

discernible and that is to reduce the substantive portion of the Act. Statistically

speaking, the Bill contains 470 sections and 7 schedules as against nearly 900

sections (including sections numbered as A, B, C and so on) and 16 schedules –

seemingly a sizable reduction. The 1956 Act has notified 34 rules and

regulations. In the new Bill, the phrase ‘as may be prescribed’ appears as many as346 times. The bulk of the procedural provisions have, therefore, been relegated

to the Rules. This marks a paradigm shift, as after the passing of the Bill, the

Central Government will possess more delegated power than it has at present.

What lies behind the mysterious phrase ‘as may be prescribed’ is a subject matter

of another discussion. Watch this space for the dangers that this phrase may

hold.

Right now, changes in governance system that are likely to be brought about are

discussed in a series of this article. The governance provisions relating to

directors, board of directors etc have been critically analysed in the paper and

the question as to what’s new in the bill is answered.

* The author is a freelance writer on Corporate Law. He is an Advocate headingAMC Law Firm in Delhi and is also the standing counsel for the office of Official

Liquidator, Ministry of Corporate Affairs attached to Delhi High Court.

23

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 24/43

Composition and Size of Board of Directors

The Bill proposes to increase the maximum number of directors in any company

from 12 to 15. Presently, any increase beyond 12, necessitates Central

Government approval. In the Bill, the number of directors beyond proposed

maximum limit of 15 can be increased by a special resolution. Women power is

at the fore and the Central Government has retained power to specify the class of

companies, which may have at least one woman director. Presently all directors

can be stationed out of India and still controlling and managing the company.

The Bill, however, proposes to change this with a stringent condition that at least

one director must have stayed in India for not less than 182 days during the

previous calendar year. The reason behind this provision is unclear. On the one

hand, the bill claims that it is a step towards globalization and on the other, it

wears down the globalization path. The condition of 182 days’ stay in India

during previous calendar year is self-defeating.

Independent Directors - Qualifications

The Bill defines independent director, who should not be a managing director or

whole-time director or nominee director. The definition has some ingredients

borrowed from clause 49. It encompasses three limbs, for the satisfaction of

which the independent director has to submit a declaration withthe company –

(a) Integrity:Independent Director must be a person of integrity having

relevant experience and expertise. This issue has been left to the wisdom

of the Board. The other board members need not pass the test of integrity,

experience or expertise but the independent director has to.

(b) Disqualifications: The Independent Director must not have

disqualifications attached to him. The disqualifications lie in being a

promoter of holding, subsidiary or associate company or related to

24

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 25/43

promoters etc. or having pecuniary relationship and being an auditor,

legal consultant etc.

(c) Qualifications: The independent director must possess qualifications, asmay be prescribed by the Central Government. This is highly debatable

and subjective. The Central Government needs to discharge this

responsibility in a careful manner.

Term of Independent Director

The term of independent term is now proposed to be fixed for 5 years at a time,

which can be extended for another 5-year term by the members by passing a

special resolution. After two terms of 5 years each, there is a provision of cooling

off period of 3 years during which he should not have any direct or indirect

association with the company. The fixing of tenure of independent director is a

welcome step, as it will ensure independence of director in a true sense –

without any fear not being re-elected in general meeting upon retirement by

rotation. It will shieldhim from pressures of management.

Insulation from liability

After Satyam fiasco, most of the professional independent directors refused to

accept appointments as such. The question of liability in case of scams and

frauds led them to reject proposals of becoming independent directors. The

purpose of appointment of an independent director was thought to be coming to

a standstill with such overhang of liability. This is proposed to be corrected with

making the independent directors liability proof unless the fraudulent act is

done with consent, knowledge and connivance of the independent director. The

bill seeks to achieve a balance between accountability and freedom of

independent directors. This will encourage the independent directors to accept

such positions sans any fright of being hauled up unnecessarily.

25

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 26/43

Selection of Independent Directors

Who selects independent directors and how, is the question that remains largely

unanswered. The freedom to the management to select independent directorsled to their favourites being selected and elected. The process of selection was

not transparent leading to deficit in governance. The bill seeks to remedy this

situation with creation of panel or data bank by authorized institutions and

bodies. The manner and procedure of selection will be notified by the Central

Government.

Disqualifications for appointment as director

The disqualifications of directors have been stretched a bit. Presently, any

person who has been convicted by a Court of any offence involving moral

turpitude and sentenced to imprisonment for not less than 6 months is ineligible

to be appointed as a director of any company. The bill proposes to cover all

offences without restricting to ‘offences involving moral turpitude’. However, the

use of words ‘whether involving moral turpitude or otherwise’ seem to be

superfluous. The bill has propounded a stricter approach in respect of persons

sentenced for 7 years or more. Such persons are ineligible for appointment as

director in any company.

A disqualification will get attached to a person if he is or has beena director of

any company which has defaulted in filing its financial statements and annual

return for 3 continuous years or has defaulted in repayment of deposit or

interest or redemption of debentures or payment of any dividend for a period of

one year. Such a person shall not be eligible for appointment as director in any

company. This disqualification has been remodeled in a stringent form.

Presently, such a disqualification relates to default by any public company and

the person becomes ineligible to become a director of any other public company.

The proposed clause extends the default to any company and also extends

ineligibility to become a director in any company. The proposed clause covers

26

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 27/43

past appointments also. This is a major shift from the present provisions and the

directors will do good to select and choose the companies diligently.

Number of directorships

Presently a person cannot be a director in more than 15 companies excluding

private companies. This is proposed to be extended to 20 companies but

including private companies. The sub-limit for directorship in public companies

is proposed at 10.

Duties of Directors

The duties of directors have evolved over time and through plethora of cases.

The directors have to act diligently, in good faith and in best interest of the

company. The directors need to avoid conflict of interest with the company. The

position of directorship cannot be assigned. All these duties hitherto evolved and

finding place in text books and judgments, are now forming part of the Bill. An

extremely welcome step in the Bill lists out duties of directors for the first time

and makes it punishable, if the director contravenes it. The duties forming part of

the Bill include –

a. To act in accordance with the Articles of the company;

b. To actin good faith and in best interest of the company;

c. To act with reasonable care, skill and diligence;

d. To avoid conflict of interest with the company;

e. Not to achieve any undue gain or advantage; and

f. Not to assign the office of director.

27

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 28/43

Vacation of office of director

The Bill proposes to relax the provision relating to abstention from the board

meetings. The present Act provides that the office of director becomes vacant if the director absents himself from 3 consecutive meetings of the Board of

Directors or from all meetings of the Board for a continuous period of 3 months,

whichever is longer, without obtaining leave of absence from the Board. The bill

proposes to extend the period to 12 months.

Resignation of director

The subject of resignation of director has always been contentious. The present

Act is silent on the subject leading to controversies as to the date from which

resignation is effective and whether the resignation requires approval of the

Board. The Courts had settled the controversy to a larger extent. The new Bill

seeks to set at rest any controversy by providing that the resignation takes effect

from later of the date of receipt of notice by the company or the date stated in

the resignation letter. In the event of all directors resigning together, the Central

Government gets the power to appoint directors till the directors are appointed

in the general meeting. Under the proposed provisions, no approval/acceptance

of the Board is necessary. The resigning director will be required to intimate the

Registrar of Companies about his resignation by forwarding a copy of resignation

with detailed reasons. The responsibility for filing the form relating to the

resignation of the director rests on the company, as is the present case. The Bill

does not address the concern of the resigning directors that what happens if the

company fails to inform the Registrar. Unless the records of the Registrar are

corrected, the resigning director’s name will continue to be reflected. This makes

the resigning director vulnerable as the general public continues to believe that

he continues to be a director. It is hoped that law makers will correct the

position in the Bill.

28

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 29/43

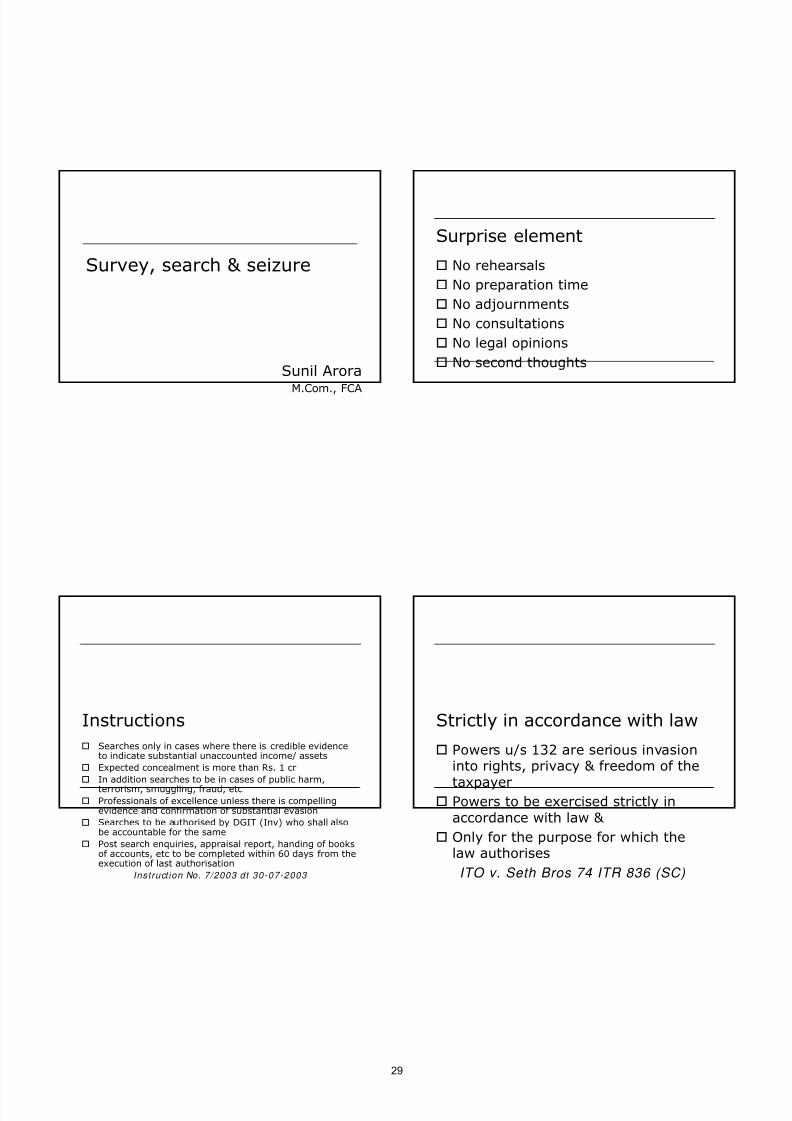

Survey, search & seizure

Sunil Arora

M.Com., FCA

Surprise element

No rehearsals

No preparation time

No adjournments

No consultations

No legal opinions

No second thoughts

Instructions

Searches only in cases where there is credible evidenceto indicate substantial unaccounted income/ assets

Expected concealment is more than Rs. 1 cr

In addition searches to be in cases of public harm,terrorism, smuggling, fraud, etc

Professionals of excellence unless there is compellingevidence and confirmation of substantial evasion

Searches to be authorised by DGIT (Inv) who shall alsobe accountable for the same

Post search enquiries, appraisal report, handing of booksof accounts, etc to be completed within 60 days from theexecution of last authorisation

Instruction No. 7/2003 dt 30-07-2003

Strictly in accordance with law

Powers u/s 132 are serious invasioninto rights, privacy & freedom of the

taxpayer Powers to be exercised strictly in

accordance with law &

Only for the purpose for which thelaw authorises

ITO v. Seth Bros 74 ITR 836 (SC)

29

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 30/43

Survey u/s 133A

Action u/s 133A: Range where being assessed Investigation wing Connected surveys

TDS

Issues: Properties Assets Nature of transactions

Size & type of operations Informal information

General observations

Statutory provisions

Section 132 : Search & seizure

Section 133A: Survey

Section 132

DG or Dir, CCIT or CIT or

Addl Dir or Comm or Jt Dir or Jt Commw.r.e.f. 01-06-1994 by The Finance (No.) Act,2009

in consequence to information in hispossession

has reason to believe

Section 132

That any person; has omitted or failed to produce books of

accounts or other documents in compliance

with section 131(1) or 142(1) would not produce such books/ documents

Section 131(1A)

in possession of money, bullion, jewellery, orother valuable article or thing;

Represents either wholly or partly income orproperty Which has not been disclosed or

Would not be disclosed

30

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 31/43

Section 132; Authorised Officer

DG or Dir, CCIT or CIT may authorise:

Addl/ Jt/ Deputy/ Asst Dir or

Addl/ Jt/ Deputy/ Asst Commissioner or

ITO

Addl Dir/ Comm or Jt Dir/ Jt Comm

Asst/ Deputy Dir or

Asst/ Deputy Commissioner or

ITO

Jt Dir/ Comm includes Addl Dir/ Comm (Section 2(28C) & (28D)

Expansion of the authority base

Addl Dir cannot authorise himself

Information

Phone tapping?

Rumour, gossip, intuition or otherirrelevant information cannot betermed as ‘information’ for formationof ‘reasons to believe’

Information should be definite andnot imaginary

Information should be in the

possession of the authority

Information

HL Sibal v. CIT 101 ITR 112 (P&H)

Subba Associates v. UoI 276 ITR 456

(Sikkim)MS Associates v. UoI 275 ITR 502

(Gauhati)

Reasons to believe

The expression reasons to believe does notmean purely subjective satisfaction on thepart of the AO. The belief must be in goodfaith and cannot be merely a pretence. Thebelief must have rational connection orrelevant bearing and are not extraneous orirrelevant for the purpose.

S. Narayanappa v. CIT 63 I TR 219 ( SC)

31

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 32/43

Judicial principles

Authority must apply his mind to the information toform opinion

Opinion must be based on material available and noton the basis of extraneous or irrelevant material

Belief must be bona fide and based on cogentmaterial

There should be a rational connection betweeninformation possessed and opinion

Court not to examine sufficiency of the material

Prabhubhai Vastabhai Patel v. R.P.Meena 226 ITR 781(Guj)

Judicial principles

Authority must be in possession of the information

Authority must form an opinion that there is reason tobelieve

That the article or property has not been or would notbe disclosed

Information must be something more than mererumor or gossip

Information must exist before opinion is formed

Reasons to believe is different from reason to suspect

But the sufficiency of the reason is not open for judicial review.

CIT v. Vindhya Metal Corpn 224 ITR 614 (SC)

Consequences of an illegal search

Money, bullion, jewellery or other valuablearticle or things to be returned

Information collected during the course of search can still be used against theassessee

Damages awarded against the revenue forwrongful seizure of assets

DGIT v. Diamondstar Exports ltd 293 ITR 438 (SC)

Powers u/s 132(1)

Enter and search

Any building, place, vessel, vehicle or

aircaft, where he has reason to suspect Books of account, other documents

Money, bullion, jewellery or other valuablearticle or thing are kept

Break open lock of door, almirah, safe, etcwhere key is not available

Personal search of any person who isentering or leaving such premises

32

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 33/43

Powers u/s 132(1)

To seek facility to inspect any books of accounts or otherdocuments maintained in the form of electronic record

RI for 2 yrs u/s 275B in case of non compliance

Inventory of money, bullion, jewellery or other valuablearticle or thing

Seize any such:

Books of accounts, documents

Money, bullion, jewellery or other valuable article or thing

Make inventory of stock in trade

No seizure of stock in trade

Seizure without physical possession of valuable article or

thing where not possible or practical

Powers u/s 132(3)

Restrain to remove, part with orotherwise deal with except withprevious permission in case seizurenot practicable

Such order shall not be in force for aperiod exceeding 60 days from thedate of the order (Section 132(8A))

Retention of seized record

Books of account or other documents not tobe retained beyond 30 days from the dateof the assessment orders

Retention beyond 30 days:

Reasons to be recorded in writing

Approval of the CCIT/ CIT/ DG/ Dir

No retention beyond 30 days after allproceedings in respect of the relevant yearare completed

Place of search

CCIT/ CIT may authorise the said officers totake action in respect of places notspecified in the original authorisation incase it is suspected that books of accounts,other documents, money, bullion, jewelleryor other valuable article or thing is kept inany such building, place, vessel, vehicle oraircraft.

Authorisation to be in Form No 45B

Section 132(1A)

33

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 34/43

Survey u/s 133A

An IT authority may enter:

Any place within the area assigned to him

Any place occupied by person under his jurisdiction

Any place authorised by the jurisdictional authority

At which business or profession is carried on or

any place where it is stated that books of account orother documents, cash or stock is kept

Authority may enter a place:

Where business is carried on; during the hours whichsuch place is open for conducting business orprofession

Any other place; only after sunrise and before sunset

Survey u/s 133A

IT authority may require anyproprietor, employee or any otherperson attending to the business toprovide facility to: Inspect books of account or other

documents

Verify cash stock or other valuable articleor thing

Furnish such information as he may

require

Powers of authorities u/s 133A

Place marks of identification on books or otherdocuments

Make extracts or copies there from Impound books of account or other documents

After recording reasons For not exceeding 10 days without approval of CCIT

or DG

Make inventory of: Cash

Stock

Other valuable articles or things

Record the statement of any person which may beuseful or relevant

Survey u/s 133A

No power to remove or seize cash, stock orother valuable article or thing

Power u/s 133A(1) to be exercised after

obtaining approval of the Jt. Commissioner / Jt. Director

Section 2(28C): Jt Commissioner includesAddl. Commissioner as well

Authority only by the jurisdictional JCIT

Enforce compliance u/s 131(1) in case of refusal / evasive

34

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 35/43

Survey u/s 133A

Inventory stock taking

Physical cash verification

Updation of books and ascertainingcash & inventory as per accountingrecords

Surrender of addl income based onthe difference books & physical cash/

inventory

Section 133A(5)

Expenditure incurred in connectionwith any function, ceremony or event

After the function

Income tax authority may require

Assessee or any other person to: Furnish such information

Record statement

Statement may be used as evidence

in any proceedings under the Act

Survey v. Search

Section 133A/ section 132

Reasons for initiation

Different authorities Place only where business or profession is

carried on

No seizure during survey

Impounding of books of accounts or otherdocuments only

Conversion of survey into search

Charter of Rights

To see the warrant of authorisation

Verify identity of each member of the

search party Personal search of the party

35

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 36/43

Warrant of authorisation

Warrant of authorisation in Form No 45,45A or 45B

Not entitled to copy, only to see

Issues in authorisation:

Name of the person

Particulars of the building/ place/ vessel/vehicle/ aircraft

Names of the authorised officers

Striking off inapplicable portion

Signed & sealed by the issuing authority

Panchnama

Two or more respectable inhabitantsof the locality to be witnesses of thesearch

Search to be made in the presence of such witnesses

List of all things seized to be preparedand to be signed by such witnesses

Rule 112(6) & (7)

Rights of female members

Right to withdraw before beginning of the search, if she does not appear in

public To be searched only by a lady with

strict regard to decency

Duties of the person

To allow free and unhindered ingress intothe premises

To sign the warrant after seeing To identify all receptacles:

Where assets / books of accounts, etc are kept

Hand over keys of such receptacles

To identify and explain ownership of theassets, books of accounts and documents

36

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 37/43

Charter of rights

To call a medical practitioner in caseof emergency

To allow children to go to school afterchecking their bags

Facility of having meals, at thenormal times

Inspect the seals

Duties

To disclose correct identity of every personin the premises and his relationship

Impersonation is an offence punishable u/s416 of the Indian Penal Code

Not to remove any article from its place ordestroy any document

Punishable u/s 204 of the Indian PenalCode

Not to allow or encourage entry of

unauthorised persons

Counsel

Survey u/s 133A: yes

Search u/s 132 : Generally NO,

unless the assessee takes a standbefore making a surrender

Only the record of the relevantassessee to be provided by thecounsel

DIT (I nv) v. SR Batliboi & Co. 227 CTR 238 (SC)

Recording of statement

AO may during the course of the searchexamine on oath any person

Person who is found to be in possession or

control of: Books of accounts, documents Money, bullion, jewellery or other valuable

article or thing

Statement may not be restricted to suchbooks, documents, assets, etc

Statement may be used as evidence

Ensure that the statement is correctlyrecorded

37

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 38/43

Recording of the statement

To answer all queries truthfully and tothe best of his knowledge

Third party not allowed to interfere orprompt

Consultation; depending upon natureof query:

May be permitted

May not be permitted

Recording of the statement

Refusal to answer a question: Offenceu/s 179 of the IPC

False statement: Offence u/s 181 of the IPC

Providing of false evidence: Offenceu/s 191 of IPC

Any person

Term any person in 132(4) has verywide connotation.

The person may be an employee,relative, etc

Person should be in the possession orcontrol of: Any books of accounts, documents,

money, bullion, jewellery or othervaluable article or thing.

Confessional statement

MD of a company not in possession of anyunaccounted money, bullion, etc. nor anyincriminating documents from the premises

of the company or the residence of the MD Question of examining u/s 132 (4) does notarise and such statement does not haveany evidentiary value

Merely confessional statement withoutdocumentary evidence cannot be usedagainst the assessee

CIT v. Ramdass Motor Transport 238 ITR 177 (AP)Decision still open due to SC directions in t his case

38

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 39/43

Statement u/s 132(4)

Surrender of income?

Two objectives: Buy peace with the department

Avoid penalty

Explanation 5 to section 271(1)(c) notapplicable for search initiated after 01-06-2007

Explanation 5A inserted by the Finance Bill(No. 2), 2009 w.r.e.f. 01-06-2007

Waiver of penalty u/s 271AAA

Explanation 5A

Search initiated after 01-06-2007

Income on the basis of:

Money, bullion, jewellery or other valuable article orthing or

Entry in any books of accounts or other documents ortransactions

For any PY which has ended before the date of searchand,-

Where ITR furnished before the said date but suchincome has not been declared therein or

Due date has expired but ITR not filed

Penalty leviable even if the income included in the ITRfurnished subsequently

Surrender in statement u/s 132(4)

Penalty @ 10% of undisclosed income u/s271AAA(1) applicable to: AY for which time for 139(1) has not expired &

the assessee has not furnished ITR before thedate of search

Year in which search is conducted

No penalty: Undisclosed income admitted u/s 132(4) along

with manner of deriving Substantiation of the manner of deriving

undisclosed income Payment of tax along with interest in respect of

undisclosed income

Surrender u/s 133A(3)

Two objectives: Buy peace with the department

Avoid penalty

Penalty for the years for which ITRs have been filed

ITRs not yet filed

Nature of asset/ income may alsodetermine whether penalty leviable ornot

39

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 40/43

Retraction of surrender

Once surrender made in statementrecorded u/s 132(4) has beenwithdrawn or retracted it loses itsevidentiary value and cognizance of the same cannot be taken.

CIT v. Dr N. Thippa Setty 322 ITR 525 (Kar.)

Retraction of surrender/ statement

Retraction to be on the first possibleopportunity instead of an after thought

Depending upon the nature of surrender

Undue influence

Addition of income surrendered as well asthe value of assets based on whichsurrender made.

AO not accepting surrender in totality

What can be seized

Section 132 (1) (iii):

Seize any such,

books of accounts, other documents,

money, bullion, jewellery or

other valuable article or thing

What can be seized

‘Such’ occurring in 132(1)(iii) refers to

undisclosed assets, as mentioned in clause

(c)Sriram Jaiswal v. UOI 176 ITR 261 (All)

Money, bullion, jewellery, or other valuable

article or thing; representing either whollyor partly income or property

Which has not been disclosed or

Would not be disclosed

40

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 41/43

What can be seized

Relevancy or usefulness of every document cannot be

made out conclusively at the time of search

Sri Venkateswara Lodge v. CIT 71 I TR 629 ( AP)

Stock in trade of the business being bullion, jewellery,

other valuable article or thing not to be seized

But the AO shall make a note or inventory of such stock

Proviso to section 132(1)(iii)

Computers / Laptops / Mobile phones

Money in the bank a/c

Cash in bank is conceptually differentfrom cash in hand…………. Under thelaw true relationship between banker& costumer is of a debtor andcreditor.Shanti Prasad Jain v. Director of Enforcement

(1963) 2 SCR 297

KCC Software Ltd v. DI ( Inv .) 29 8 I TR 1 (SC)

Jewellery

Quantum of jewellery

Old jewellery

Prior to 6 years Other

Source of acquisition:

Explained

unexplained

CBDT Guidelines

Wealth tax assessees: Gross weightdeclared in the wealth tax returns

Not assessed to wealth tax: 500 grms per married lady

250 grms per unmarried lady

100 grms per male member

Other factors: Status of the family

Custom & practices

Community to which family belongs

Hindu dt 30-06- 1994

41

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 42/43

Jewellery

Consequences of Jewellery not as pervaluation report

Evidence to substantiate date of acquisition of jewellery

Not pertaining to the assessee

Cash found during search

Seizure of cash: Explained Unexplained

Explained: Withdrawals Old withdrawals Subsequent withdrawals Imprest accounts IOU

Repres en t s ei t he r w ho l l y o r pa r t l y i nc ome o r p r o p e r t y w h i ch h a s n o t b e e n o r

w ou ld no t be d i s cl os ed

Documents found

Parallel books of accounts

Incriminating documents

Property agreements

Settlement of accounts Books of accounts: not tallying with FS

Dairies

Loose papers / Notings, etc

CBI v. V.C. Shukla & others ( 1998) 1 SCR 1153

MIS reports

Correspondence

E-mails

SMS

Presumption

Books of account, other documents, money, bullion, jewellery or other valuable article or thing is found inpossession or control of any person

Presumption:

Belong to such person

Contents are true

Person’s handwriting or signatures

Section 132(4A)

Presumption only for the purpose of 132 and thesame not available at the time of assessmentproceedings.

PR Metrani v. CIT 287 ITR 209 (SC)

42

8/2/2019 Revised Schedule VI, Companies Bill

http://slidepdf.com/reader/full/revised-schedule-vi-companies-bill 43/43

Rights of the tax authorities

Whether any building of the assessee can be searched

Specified in search warrant in Form 45

Addl places in Form 45B

No power to arrest under the I.Tax Act

Breaking open locks, etc

Damage to the property:

Rule 112 (4) : break open any outer or inner door orwindow to effect an entrance

Rule 112 (4B) : break open box, locker, safe, almirahor other receptacle where key is not available

Requisiton service of any police officer or any otherCG officer or both

Rights of the assessee

Copy of list of things seized to beprovided (Rule 112(8) )

Bullion, jewellery and other valuablearticles or things seized to be placedin packages which shall be sealed andbear identification marks. Assesseemay also place his own seal on them

Documents

Panchnama together with all theannexures

Copy of statement that is usedagainst him by the department

Inspection of the seized books of accounts or other documents and tomake copies or take extracts therefrom (Section 132(9) )

Personal availability

Warrant of authorisation

Any person

in charge of or

in any

Building, place, vessel, vehicle or aircraft Relative

Authorised representative

Knowing your

Facts with conviction

Transactions in books

Details in ITRs

Strengths

House keeping

Weaknesses

Implications

Worst scenario

Psychological warfare

Be in command Maintain composure Retain presence of mind Remain cool Do not loose temper

Do not get ruffled By loose talk Aggressive behavior Sweet talk Misbehavior by the officers

Do not get tired No need to be docile or aggressive Enjoy the drama in lighter vein Handle intelligently Not to come under pressure for:

Surrender or fabricate documents