reynolds t. cafferata. you bought it for $40,000 in 1960’s and its worth $4 million in the early...

TRANSCRIPT

Reynolds T. Cafferata

Dusting Off the Old CRT

The Ideal Asset for A CRT?

Yes, if

You bought it for $40,000 in 1960’s and its worth $4 million in the early 1990’s.

Have you done a lot of CRTs in the past ten years?

Low Tax RatesFew appreciated assets

No because …

That’s all changing …

Federal Ordinary Income 39.6%Federal Capital Gains 20%Medicare Surcharge 3.8%California 13.3%

(9.3% base, 1% millionaire tax, 3% Prop. 30)

Rates Are Up

2009 Dow 6627, 2013 Dow 15300Residential House up 10%+ in some Markets

from 2012 to 2013

Assets Are Up

Robert F. Sharpe & Co Research finds peak age for creating a CRT is 68

Next year the first baby boomer turns 68

Demographics Will Favor CRTs

Main benefit of a CRT is not the deductionTax Exempt Status of CRT allows pre-tax

reinvestment of sale proceedsThe greater the appreciation and the greater

the tax rate, the greater the benefit of the CRT

Someone looking to turn an appreciated asset into an income stream will benefit from a CRT

Ideal Circumstances for CRTs

$4,000,000

Sale CRT

$2.8 Million

$4 Million

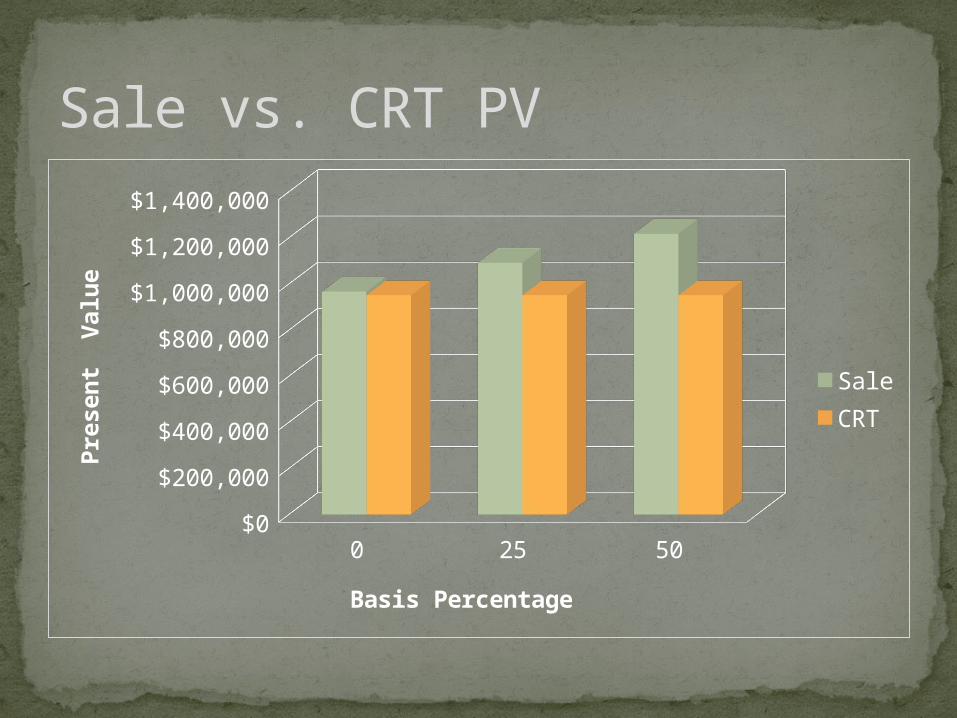

Sale vs. CRT

Unitrust or Annuity TrustLives in Being or Term of years up to 20Assets remaining pass to charity

CRT Review--Structure

10% Remainder Value Payout Term AFR

5% to 50% Payout RateAnnuity Trust must pass Exhaustion Test

CRT Basics--Minimum Requirements

Fixed Dollar AmountNo Additional Contributions AllowedNo Benefit to Beneficiary From Growth of

CRT

CRT Basics—Annuity Trust

Fixed PercentageTrust Revalued AnnuallyFlavors

Standard Net Income (Make-up) Flip (Make Up)

Beneficiary benefits from growth in value

CRT Basics--Unitrust

Payments to Beneficiary Taxed under Four Tier Rule

UBTI Taxed at 100%Cannot Be a Grantor TrustDebt can cause UBTI or Grantor Trust StatusCannot Hold S-Corporation Stock

CRT Basics—Other Rules

Taxes reduce proceeds of sale of highly appreciated asset by 30% to 40%

CRT can reinvest 100% of proceeds of sale of highly appreciated asset

Beneficiary receives unitrust amount from 100% of proceeds of sale of highly appreciated asset

Power of the CRT

Long-term real estate, particularly after 1031 exchanges

Founders stockLong-term stockTangible property like art

Types of Appreciated Assets

Unitrusts that pay net income are limited to cash flow

LLCs, Partnerships and annuities can control cash flow

Flip trusts can have triggers based on a variety of events

Managing Income Flow

Managing CRT Income

0 25 50$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

SaleCRT

Basis Percentage

Pre

sen

t V

alu

eSale vs. CRT PV

2013

2016

2019

2022

2025

2028

2031

2034

2037

2040

2043

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

SaleCRT

Year

Pri

ncip

al

Fixed After Tax Payment