rice: global competitiveness of the u.s. rice industry 1 rice: global competitiveness of the u.s....

TRANSCRIPT

10/7/2015

1

Rice: Global Competitiveness of the U.S. Rice Industry

October 7, 2015

The views expressed here are those of the presenters, and do not necessarily represent those

of any individual Commissioner or of the Commission as a whole.

Disclaimer:

10/7/2015

2

Agenda

3

Overview of the Global Rice Market

Competitiveness: Cross‐country Comparison

Competitiveness: Country‐specific Findings

Competition in Export Markets

Assessment of the Impact of Government Programs

Overview: Global Rice Market

10/7/2015

3

Global White Rice Production

Asia90%

South America3.6%

Africa3.5%

North America1.5%

RoW1.6%All other

10%

All other: 46 million mtAsia: 409 million mt

Source: USDA, PSD Online (average for 2007/08‐13/14)

Most Rice is Consumed Locally

6Source: USDA, PSD Online (average for 2007/08‐13/14)

Exports7%

Domestic Consumption and Residual

92%

Annual addition to Stocks 1%

10/7/2015

4

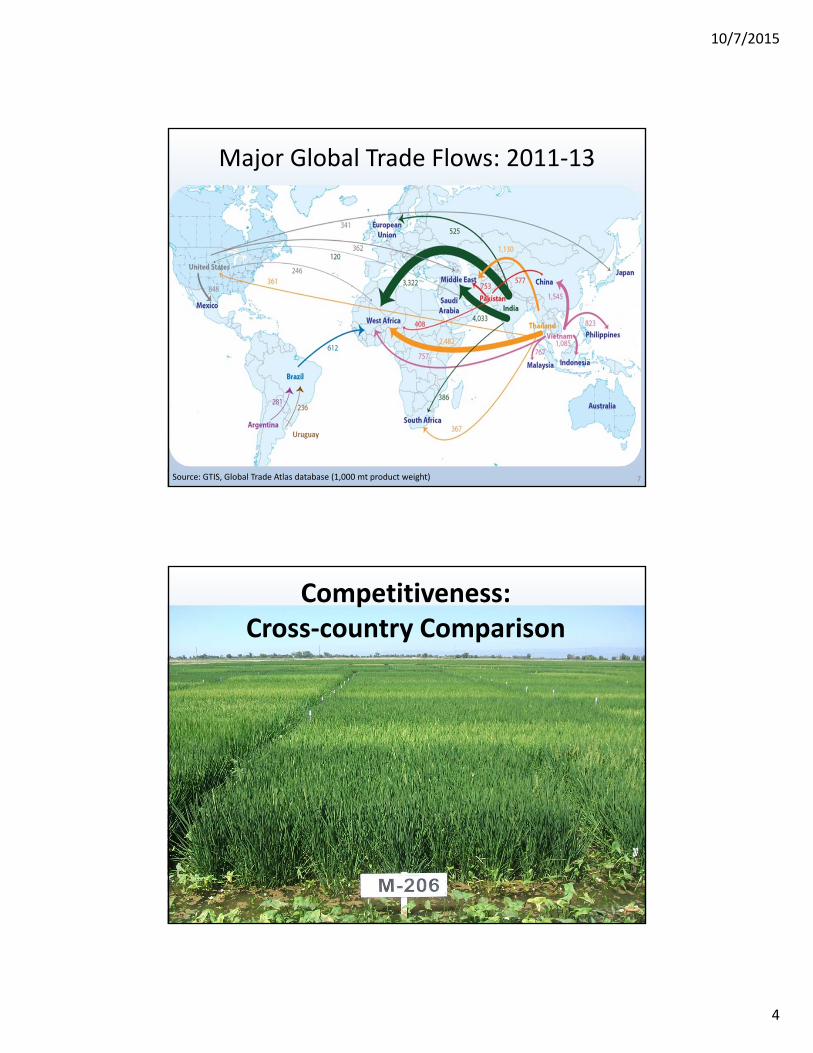

Major Global Trade Flows: 2011‐13

•

7Source: GTIS, Global Trade Atlas database (1,000 mt product weight)

Competitiveness: Cross‐country Comparison

10/7/2015

5

Highlighted Countries Country

Export Import Consumption Production

Global ranking

India 1 ‐‐ 2 2

Thailand 2 17 7 6

Vietnam 3 50 5 5

Pakistan* 4 ‐‐ 22 11

USA 5 16 14 12

Burma* 6 ‐‐ 8 7

Cambodia* 7 104 15 13

Brazil 8 14 10 9

Uruguay 9 ‐‐ 96 32

China 14 1 1 1

Indonesia ‐‐ 5 3 3

Philippines* ‐‐ 3 6 8

* Additions to the countries listed in request letter

Source: USDA, PSD Online (rankings based on 2013/14 data).

Highlighted Country GroupingsCountry

Export Import Consumption Production

Global ranking

China 14 1 1 1

Indonesia ‐‐ 5 3 3

Philippines* ‐‐ 3 6 8

India 1 ‐‐ 2 2

Thailand 2 17 7 6

Vietnam 3 50 5 5

Burma* 6 ‐‐ 8 7

Cambodia* 7 104 15 13

Brazil 8 14 10 9

Uruguay 9 ‐‐ 96 32

Pakistan* 4 ‐‐ 22 11

USA 5 16 14 12

10Source: USDA, PSD Online (based on 2013/14 data).

* Additions to the countries listed in request letter

10/7/2015

6

Country Delivered cost Product differentiation (quality)

Reliability of supply

Domestic Export Domestic Export

Brazil High Medium Medium Medium Low

Burma Low Low Low High Low

Cambodia Low Low Low High Low

China High Low N/A Medium N/A

India Low Medium Low High Low

Indonesia High Low N/A Low N/A

Pakistan Low Medium Low High Medium

Philippines Medium Low N/A Low N/A

Thailand Medium Medium High High Medium

Uruguay Low High High High High

United States Medium High High High High

Vietnam Low Low Low High Medium

Comparison of Factors of Competitiveness

Competitiveness: Country‐specific Findings

Rice ExportingCountries

10/7/2015

7

Factors Affecting Competitiveness:India

• Low cost of production

• Supportive government policies

• Innovation benefits Indian rice farmers

• Poor storage and milling infrastructure

13

Factors Affecting Competitiveness:Pakistan

• Government assistance for inputs lowers production costs

• Investment in processing facilities improves quality

• Lack of innovation keeps crop yields low

• Water– Extensive resources create favorable growing conditions

– . . . but poor water management raises delivered costs and reduces supply

• Road infrastructure also hinders competiveness

14

10/7/2015

8

Factors Affecting Competitiveness: Thailand

• Regionally high cost of production

• Reputation for premium quality

• Reliability of supply

– Historically highly reliable…

– … but recent problems with reliability

15

Factors Affecting Competitiveness: Vietnam

• Low cost of production

• Natural resource endowments

• Better seed varieties and crop management increase yields and quality

16

• Poor government data & lack of market information

10/7/2015

9

Factors Affecting Competitiveness:Burma

• Low cost of production

• Abundant natural resources favor rice production

• Inefficient milling infrastructure and poor quality

• Poor road and port infrastructure

17

Factors Affecting Competitiveness:Cambodia

• Low cost of production

• Poor irrigation, utility, and transportation infrastructure

• The inefficient milling sector reduces quality and reliability of supply

• Efforts to improve quality and reliability

• Tariff preferences benefit the export sector

18

10/7/2015

10

Factors Affecting Competitiveness:Brazil

• High cost of production

• Improved yields

• Participation in paddy rice market

• Competition from other crops

19

Factors Affecting Competitiveness:Uruguay

• Cost competitive producer

• High quality

• Product well suited to certain export markets

• Constraints on expanding capacity

20

10/7/2015

11

Factors Affecting Competitiveness: USA

• Production costs limit U.S. exports in price‐sensitive markets

• Ability to supply various rice types and forms

• Developments in long grain rice breeding research

• Reputation for high quality

• Inability to meet certain customer specifications

21

Competition in Export Markets

10/7/2015

12

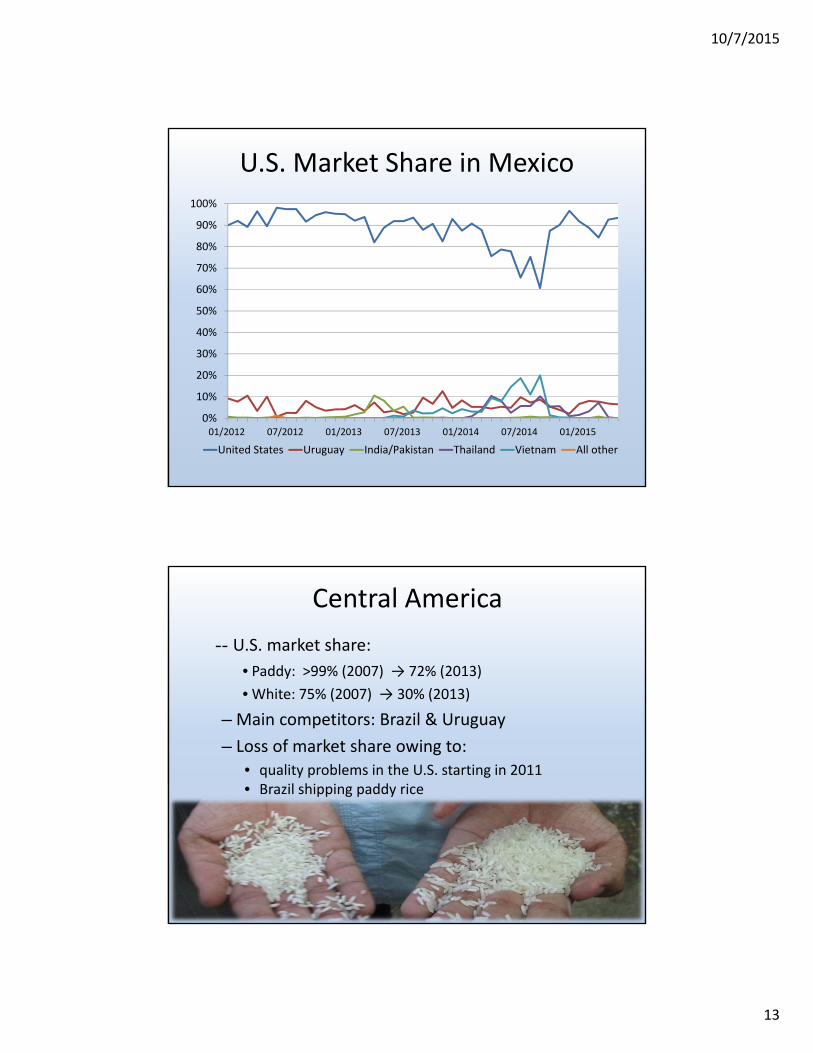

U.S. Competition in Long Grain Exports

23

Traditional U.S. markets Nontraditional U.S. markets

Declin

ing U.S.

competitiven

ess Box A

Mexico Central America European Union Haiti Ghana

Box B

China

NigeriaU.S. p

oten

tially competitive

U.S. competitive,

open

trade

Box C

CanadaJordanSaudi Arabia

Box D

IranIraqVenezuela

U.S. o

ccasionally

competitive

U.S. competitive,

restricted

trade Box E

JapanSouth KoreaTaiwan

Box F

Senegal PhilippinesMalaysia South Africa

U.S. lim

ited

competitiven

ess

Mexico

– U.S. market share: 98% (2007) → 55% (2013)

– Main competitors: Vietnam, Pakistan*, Uruguay

– Loss of market share owing to:• extension of (temporary) tariff preferences • quality problems in the U.S. starting in 2011• lower‐cost, reasonable quality, alternative supplies

10/7/2015

13

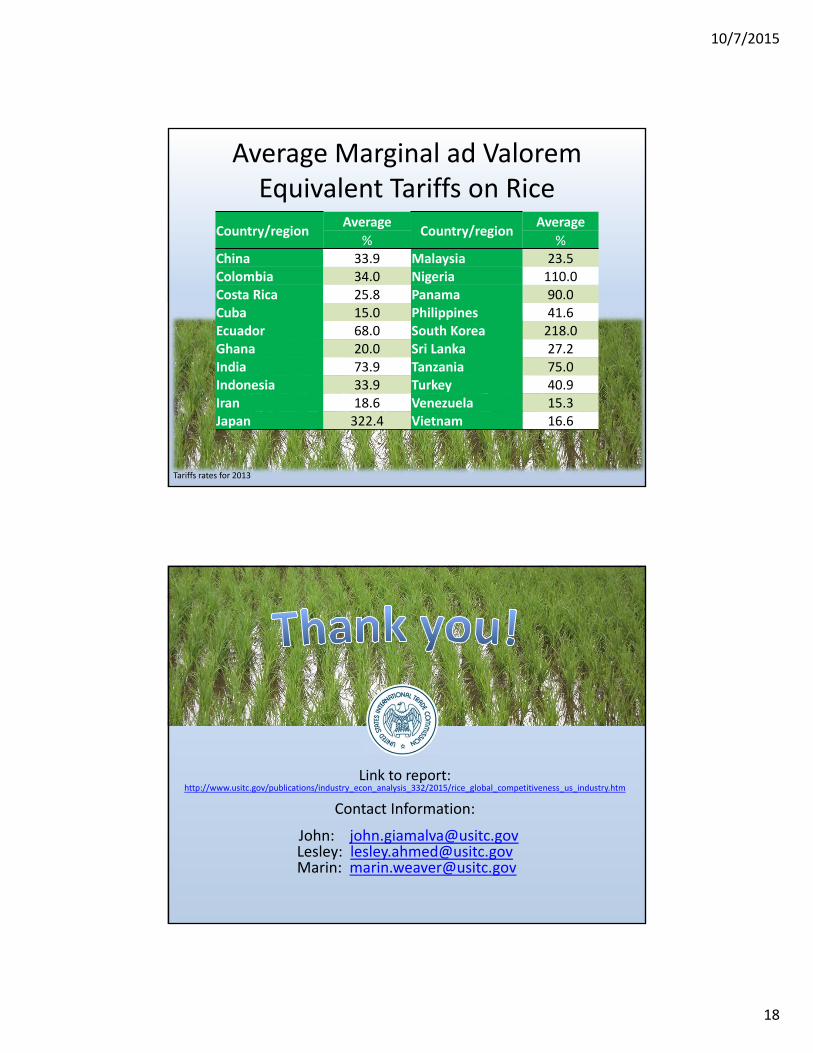

U.S. Market Share in Mexico

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

01/2012 07/2012 01/2013 07/2013 01/2014 07/2014 01/2015

United States Uruguay India/Pakistan Thailand Vietnam All other

Central America

‐‐ U.S. market share:

• Paddy: >99% (2007) → 72% (2013)

• White: 75% (2007) → 30% (2013)

– Main competitors: Brazil & Uruguay

– Loss of market share owing to:• quality problems in the U.S. starting in 2011• Brazil shipping paddy rice

10/7/2015

14

European Union

– U.S. market share: 24% (2005) → 4% (2013)

– Main competitors: India, Cambodia, Thailand, and Pakistan

– Owing to:

• Discovery of GE traits in U.S. rice in 2006

• EU tariff rate quotas

• EBA preferences for Cambodia

Haiti

– U.S. market share: near 100%

– Main competitor: Vietnam (2013)

– Loss of market share owing to:

• shipping delays ↑ US price and delivery mes, 2012

• G2G contract with Vietnam 2012/13

10/7/2015

15

Ghana

–U.S. market share: peaked in 2012 at 23%

–Fell to 16.5% in 2013

– Main competitors: Vietnam, Thailand

– Loss of market share owing to:

• lower priced aromatic rice from Vietnam

U.S. Competition in Long Grain Exports

30

Traditional U.S. markets Nontraditional U.S. markets

Declin

ing U.S.

competitiven

ess Box A

Mexico Central America European Union Haiti Ghana

Box B

China Nigeria

U.S. p

oten

tially competitive

U.S. competitive,

open

trade

Box C

CanadaJordanSaudi Arabia

Box D

IranIraqVenezuela

U.S. o

ccasionally

competitive

U.S. competitive,

restricted

trade Box E

JapanSouth KoreaTaiwan

Box F

Senegal PhilippinesMalaysia South Africa

U.S. lim

ited

competitiven

ess

10/7/2015

16

Impact of Government Programs: Modeling Results

Measurable Policies & ProgramsAffecting Rice

Price Support

Production Support

Consumer Support

Tariffs/Export Taxes

10/7/2015

17

Other Policies &Programs Affecting Rice

33

Seed Research

Infrastructure Projects

Extension Services

Export Market Development

Global Simulations Modeling Results

Policy Instrument United States Global total

Removal of Production Consumption Exports Imports Production Consumption

1,000 mt

Producer price support 105 <0.5 107 1 ‐329 ‐329

Factor input support 44 <0.5 46 1 ‐523 ‐523

Intermediate input support 51 <0.5 47 ‐4 ‐3,098 ‐3,098

Consumption support ‐14 <0.5 ‐12 2 ‐6,066 ‐6,066

Tariffs 1,269 ‐7 1,349 75 2,190 2,189

Export tax ‐2 <0.5 ‐2 <0.5 14 14

All except tariffs 182 ‐1 182 ‐1 ‐9,950 ‐9,950

All including tariffs 1,359 ‐7 1,435 69 ‐7,650 ‐7,651

10/7/2015

18

Average Marginal ad Valorem Equivalent Tariffs on Rice

Country/regionAverage

Country/regionAverage

% %China 33.9 Malaysia 23.5Colombia 34.0 Nigeria 110.0Costa Rica 25.8 Panama 90.0Cuba 15.0 Philippines 41.6Ecuador 68.0 South Korea 218.0Ghana 20.0 Sri Lanka 27.2India 73.9 Tanzania 75.0Indonesia 33.9 Turkey 40.9Iran 18.6 Venezuela 15.3Japan 322.4 Vietnam 16.6

Tariffs rates for 2013

Link to report: http://www.usitc.gov/publications/industry_econ_analysis_332/2015/rice_global_competitiveness_us_industry.htm

Contact Information:

John: [email protected]: [email protected]: [email protected]