riocans1.q4cdn.com/.../2015/q3/q3-2015-vfinal_web.pdffinancial highlights • riocan's...

TRANSCRIPT

RIOCAN PRESENTATION 2015 February 25, 2015

RioCan Investor Presentation Third Quarter 2015 November 24, 2015

2

Non-GAAP Measures RioCan’s consolidated financial statements are prepared in accordance with IFRS. Consistent with RioCan’s management framework, management uses certain financial measures to assess RioCan’s financial performance, which are not generally accepted accounting principles (GAAP) under IFRS. The following measures, RioCan’s Interest, Funds From Operations (“FFO”), Adjusted FFO, Operating FFO, Net Operating Income (“NOI”), Adjusted Earnings before interest, taxes, depreciation and amortization (“Adjusted EBITDA”), Operating EBITDA, Net Consolidated Debt to Adjusted EBITDA, Net Operating Debt to Operating EBITDA, Adjusted Unitholders Equity, Same Store NOI, and Same Property NOI, and Total Enterprise Value as well as other measures discussed elsewhere in this presentation, do not have a standardized definition prescribed by IFRS and are, therefore, unlikely to be comparable to similar measures presented by other reporting issuers. Non-GAAP measures should not be considered as alternatives to net earnings or comparable metrics determined in accordance with IFRS as indicators of RioCan’s performance, liquidity, cash flow, and profitability. For a full definition of these measures, please refer to the “Non-GAAP Measures” in RioCan’s Management’s Discussion and Analysis for the period ended September 30, 2015. RioCan uses these measures to better assess the Trust’s underlying performance and provides these additional measures so that investors may do the same.

Forward Looking Statements

3

Certain information included in this presentation contains forward-looking statements within the meaning of applicable securities laws including, among others, statements concerning our objectives, our strategies to achieve those objectives, as well as statements with respect to management's beliefs, plans, estimates, and intentions, and similar statements concerning anticipated future events, results, circumstances, performance or expectations that are not historical facts. Certain material factors, estimates or assumptions were applied in drawing a conclusion or making a forecast or projection as reflected in these statements and actual results could differ materially from such conclusions, forecasts or projections. Additional information on the material risks that could cause our actual results to differ materially from the conclusions, forecast or projections in these statements and the material factors, estimates or assumptions that were applied in drawing a conclusion or making a forecast or projection as reflected in the forward-looking information can be found in our annual information form and annual report that are available on our website and at www.sedar.com. Except as required by applicable law, RioCan undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

3

One of North America’s Largest Retail REITS

4

354 properties in Canada & U.S.

78 million sqft total portfolio

$8.2 billion market cap

53 million sqft owned

$15.1 billion enterprise value

~84% revenue generated by national and anchor tenants

~7,500 tenancies

This slide contains references to non-GAAP Measures. For a definition of such measures please refer to RioCan’s Sept. 30, 2015 MD&A.

Core Strengths

5

Strong, reliable distribution yield provided to investors

Stable, diversified portfolio of national retail tenants

Disciplined growth strategy in Canada and U.S.

Positioned to benefit from robust development pipeline and acquisitions

Experienced, performance driven management team

Dominant platform, geographically diversified

Conservative balance sheet / financial strength

QC

PA

VA

Property Portfolio

As at Sept. 30, 2015 at RioCan’s interest

CT MA

BC

AB

ON

SA MB

NB

NFLD

305 properties

43 million sqft

81.7% annualized rental revenue

TX

49 properties

10 million sqft

18.3% annualized rental revenue

6

Ontario 56%

Quebec 8%

Western Canada 16%

Eastern Canada 2%

United States 18%

Annualized Rental Revenue by Region

Property Portfolio – Canada

7

Calgary

Edmonton

Vancouver

Toronto

Montreal Ottawa

BC

AB

ON

QC

Annualized Rental Revenue by Major Market

11.2%

Major markets

combined, 74.4%

Rest of Canada, 25.6%

6.8%

3.9% 4.0%

6.5%

42.0%

7

Strong Tenant Relationships

8 8

Strong Tenant Relationships

9

Top 10 Canada & US Combined

Top 10 Tenant Name Annualized

Rental Revenue

Number Of Locations

NLA (Sq. Ft. In

000s)

Weighted Avg Remaining Lease Term

(Yrs)

1 Loblaws/Shoppers Drug Mart (i) 4.0% 82 2,002 7.3

2 Walmart 3.9% 35 4,231 11.2

3 Canadian Tire Corporation (ii) 3.7% 90 2,176 7.8

4 Cineplex/Galaxy Cinemas 3.2% 29 1,336 8.6

5 Metro/Super C/Loeb/Food Basics 2.9% 54 1,955 5.9

6 Winners/HomeSense/Marshalls/TJ Maxx 2.7% 73 1,621 7.2

7 Staples/Business Depot 1.7% 53 1,027 4.8

8 Giant Food Stores/Stop & Shop (Royal Ahold) 1.7% 24 1,113 10.6

9 Sobeys Inc./Safeway 1.6% 33 970 7.6

10 Cara/Prime Restaurants 1.5% 107 466 6.1

(i) Loblaws/Shoppers Drug Mart includes No Frills, Fortinos, Zehrs and Maxi. (ii) Canadian Tire Corporation includes Canadian Tire/PartSource/Mark’s/Sport Mart/ Sport Chek/Sports Experts/National Sports/Atmosphere.

As at Sept. 30, 2015

9

Lease Rollover Profile Broadly Distributed Lease Expiries

10

1,279

3,464 3,883 4,466 4,698

2015(remaining)

2016 2017 2018 2019

356 515 712 1,079

1,525

2015(remaining)

2016 2017 2018 2019

% Square Feet expiring / portfolio NLA Canadian Portfolio As at Sept. 30, 2015

U.S. Portfolio As at Sept. 30, 2015

’000s Square Feet

’000s Square Feet

3.3% 8.8% 9.9% 11.4% 12.0%

5.1% 7.1% 10.8% 15.2% 3.5%

Occupancy since 1996 Historical Committed Occupancy Rates 1996 to Q3 2015

96.9% 95.0% 95.0% 95.4% 96.1% 95.6% 95.8% 96.3% 96.3% 97.1% 97.7% 97.6% 96.9% 97.4% 97.4% 97.6% 97.4% 96.9% 97.0%

94.0%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Q32015*

11

* RioCan’s committed occupancy rate as at Sept. 30, 2015 reflects 18 disclaimed leases by Target Canada in properties owned by RioCan.

Corporate Developments • RioCan announced with its second quarter results that the Trust has engaged

advisors to conduct a strategic review of its U.S. Operations

• RioCan began acquiring assets in the U.S. in the fourth quarter of 2009 and since has seen strong gains in the value of the portfolio from cap rate compression and appreciation of the U.S. dollar

• With an abundance of capital and greater number of investors it has become increasingly difficult to continue to grow through acquisition and the Trust does not have the infrastructure to support development activities in the U.S.

• Review is in early stages and will consider a wide range of options, which include but are not limited to:

– Status quo – continue to operate the U.S. Portfolio – Sale of some or all of the Trust’s U.S. Assets – Other strategic joint venture alternatives

• Review is progressing along anticipated timelines and the expectation is to update the market in late 2015

12

Property Portfolio – U.S. High quality assets with a focus towards grocery anchored centres

13

Riverpark, Houston Alamo Ranch, San Antonio

Stop N Shop Plaza, Bridgeport, CT

Town Square Plaza, Reading, PA

Shaw’s Plaza, Raynham, MA

Loyal Plaza, Williamsport, PA

U.S. Property Portfolio – Key Facts Focused in two geographic regions, Northeastern United States and Texas

14 This slide contains references to non-GAAP Measures. For a definition of such measures please refer to RioCan’s Sept. 30, 2015 MD&A.

# Properties NLA (millions sf) %NLA % annualized

rental revenue

Northeastern United States 28 4.7 46.9% 44.4%

Texas 21 5.3 53.1% 55.6%

Rank Tenant name Annualized

rental revenue

Number of locations

NLA (‘000s sf)

Weighted average

remaining lease term

(years) 1 Giant Food Stores/Stop&Shop 10.0% 24 1,113 10.6 2 Best Buy 3.5% 10 329 5.1 3 Staples/Business Depot 3.0% 17 335 4.6 4 PetSmart 2.8% 13 280 4.2 5 Walmart 2.7% 5 880 13.3 6 Michaels 2.3% 13 278 3.6 7 Ross Dress for Less 1.8% 8 242 3.7 8 Bed Bath & Beyond 1.7% 9 237 5.0 9 Lowe's 1.6% 3 476 11.4 10 Market Street 1.4% 3 193 8.3 30.8% 105 4,363 7.8

Portfolio Statistics • 49 Properties • 10.0 million SF at RioCan’s Interest • 13.2 million SF including Partners

and Shadow anchors • 97.1% Occupied as at Sept. 30, 2015 • 85.8% - annualized rental revenue

generated by national and anchor tenants

• 61.5% - portfolio NLA anchored or shadow anchored by grocers

• 18.3% - total annualized rental revenue as at Sept. 30, 2015

Top Ten Tenants

Financial Highlights (at RioCan’s interest in millions of $ except per unit amounts)

Revenues

758 882

988 1,114

1,195 1,240

2009 2010 2011 2012 2013 2014

Operating FFO*

280 329

380 440

492

2009 2010 2011 2012 2013 2014

517

Operating FFO* Per Unit

1.22 1.33

1.43 1.52

1.63 1.68

2009 2010 2011 2012 2013 2014

15

Years ended December 31st

* Note: FFO reported under IFRS for 2010 onwards, excludes trading gain income

13.0% CAGR

6.6% CAGR

10.3% CAGR

This slide contains references to non-GAAP Measures. For a definition of such measures please refer to RioCan’s Sept. 30, 2015 MD&A.

Financial Highlights

• RioCan's Operating FFO for the three months ended September 30, 2015 ("Third Quarter") was $140.2 million or $0.44 per Unit compared to $133.6 million or $0.43 per Unit for the third quarter in 2014, representing an increase of $6.6 million or 5.0%. On a per Unit basis, Operating FFO increased by $0.01 per Unit;

• RioCan's Operating FFO increased 6.9% to $414.6 million for the nine months ended September 30, 2015 compared to $387.9 million for the same period in 2014. On a per unit basis, Operating FFO increased by $0.03 or 2.8% to $1.30 compared to $1.27 for 2014;

• In the Third Quarter, RioCan achieved an AFFO payout ratio of less than 90% at 89.7% as compared to 90.3% for the same period in 2014. RioCan's AFFO payout ratio for the nine months ended September 30, 2015 also improved to 90.5% as compared to 92.8% for the same period in 2014;

16 This slide contains references to non-GAAP Measures. For a definition of such measures please refer to RioCan’s Sept. 30, 2015 MD&A.

Financial Highlights • RioCan and Hudson's Bay Company ("HBC") completed the first tranche in a strategic joint

venture focused on retail real estate growth opportunities in Canada. The joint venture will enable RioCan and HBC to build on the strength of existing real estate assets through potential future redevelopment, as well as identify retail and enclosed mall acquisitions;

• Subsequent to the quarter end, RioCan and Kimco Realty Corporation ("Kimco") completed the first tranche of the previously announced agreement for RioCan to acquire Kimco's interest in 22 properties in Canada that were previously owned jointly;

• Subsequent to the quarter end, in anticipation of completing the first tranche of the acquisition from Kimco, RioCan added $200 million in capacity to an existing credit facility thereby increasing the Trust's financial flexibility; and

• On November 23, 2015 RioCan announced that it had reached a settlement with Target Corporation in the amount of $132 million of which $91.8 million belongs to RioCan.

17

Q3 Financial Highlights

$ per unit Payout Ratio $ per unit Payout Ratio

Quarter % Change Q3 2015 Q3 2014 Q3 2015 Q3 2014 % Change Nine

Months 2015

Nine Months

2014

Nine Months

2015

Nine Months

2014

Distribution 0.0% 0.3525 0.3525 n/a n/a 0.0% 1.0575 1.0575 n/a n/a

FFO 2.7% 0.44 0.42 80.1% 83.9% 1.4% 1.26 1.24 83.9% 85.3%

OFFO 1.0% 0.44 0.43 80.1% 82.0% 2.8% 1.30 1.27 81.3% 83.3%

AFFO nm 0.39 0.39 89.7% 90.3% 0.8% 1.17 1.14 90.5% 92.8%

Canada United States

Q3 2015 Q3 2014 Q3 2015 Q3 2014

Same Store NOI Growth (1.3%) 1.9% 0.6% 3.7%

Same Property NOI Growth (2.4%) 1.5% 0.2% 3.7%

18 This slide contains references to non-GAAP Measures. For a definition of such measures please refer to RioCan’s Sept. 30, 2015 MD&A.

($ millions) % Change Q3 2015 Q3 2014 % Change Nine Months

2015 Nine Months

2014

Total Revenue 4.5% 320.6 306.9 6.2% 974.0 917.5

FFO 6.7% 139.7 130.9 5.4% 401.4 380.7

OFFO 4.9% 140.2 133.6 6.9% 414.6 387.9

AFFO 4.7% 126.0 120.3 6.6% 372.4 349.5

Financial Highlights (in millions)

Distributions to Unitholders

228 261 281 285 293 316 315 307

297 318 343 367 401

426 434 450

0.99 1.04 1.13 1.14 1.07 1.01 1.04 1.02 1.03

1.3275 1.36 1.38 1.38 1.38 1.38 1.41 1.41 1.41

2007 2008 2009 2010 2011 2012 2013 2014 Q32015

Rolling12

mos.

Distributions to Unitholders per Unit

19

Distributions to Unitholders net of DRIP Distributions per Unit net of DRIP

Organic Growth

20

Occupancy and Leasing Profile – Last eight quarters

2015 2014 2013

Third Quarter

Second Quarter

First Quarter

Fourth Quarter

Third Quarter

Second Quarter

First Quarter

Fourth Quarter

Committed occupancy 94.0% 93.9% 96.7% 97.0% 97.0% 96.9% 96.8% 96.9%

Economic occupancy 92.6% 92.8% 95.5% 96.0% 96.0% 95.9% 95.7% 95.8%

NLA leased but not paying rent (thousands of square feet) 685 544 623 512 488 520 519 542

Annualized rental impact (thousands) $17,657 $16,763 $17,580 $15,696 $15,588 $15,336 $12,912 $14,004

Retention rate – Canada 89.8% 87.7% 83.5% 85.0% 91.7% 88.8% 91.2% 97.0%

% increase in average net rent per sq ft –Canada 8.6% 9.8% 9.8% 11.8% 12.9% 13.9% 7.0% 8.8%

Retention rate – US 80.5% 91.7% 58.9% 78.3% 92.2% 97.3% 86.4% 98.2%

% increase in average net rent per sq ft – US 9.8% 10.6% 8.3% 7.8% 9.3% 7.0% 8.3% 4.8%

This slide contains references to non-GAAP Measures. For a definition of such measures please refer to RioCan’s Sept. 30, 2015 MD&A.

Target’s Departure from Canada

• On January 15, 2015, Target Corporation (Target) announced plans to discontinue its Canadian operations through its indirect wholly-owned subsidiary, Target Canada, and that it was utilizing the Companies’ Creditors Arrangement Act (Canada) (“CCAA”) to wind down its operations.

• Pursuant to IFRS, effective July 1, 2015 RioCan is no longer recognizing rental revenue on the leases that were disclaimed by Target Canada.

• On November 23, 2015 RioCan announced that it had reached a settlement with Target Corporation in the amount of $132 million of which $91.8 million belongs to RioCan.

• RioCan is actively in discussion with potential retailers to backfill the vacant premises.

• Estimated 18 to 24 months to break-up the former Target spaces and a new tenant to commence paying rent in these reconfigured spaces taking into consideration lease negotiations, construction approvals, construction time and fitting out of such space.

• When complete re-tenanting will result in a more diversified revenue stream and potentially a better draw for consumers.

21

Target’s Departure from Canada

22

As at September 30, 2015, Target Canada had disclaimed 18 leases in properties owned by RioCan with annualized net rental revenue of approximately $11 million, estimated common area maintenance costs and taxes of $7.5 million and NLA of 1,602,000 square feet at an average lease rate of $6.67 per square foot (all figures at RioCan's interest). One of the disclaimed locations has reverted to Walmart Canada through a pre-existing covenant and Walmart Canada has presently assumed payment of the annual rent obligation. In August 2015, one additional lease was disclaimed by Target Canada representing approximately 61,000 square feet and annualized net rental revenue and estimated maintenance costs and taxes of $0.3 million at RioCan's interest

Site City Province

RioCan % ownership GLA (100%)

GLA (RioCan %)

Burlington Mall Burlington Ontario 50% 121,523 60,762 Charlottetown Mall Charlottetown PEI 50% 107,806 53,903 County Fair Mall Smiths Falls Ontario 100% 92,989 92,989 Desserte Ouest Laval Quebec 50% 116,147 58,074 Five Points Mall Oshawa Ontario 100% 102,444 102,444 Flamborough Power Centre Flamborough Ontario 100% 116,493 116,493 Gates of Fergus Fergus Ontario 50% 95,978 47,989 Lawrence Square Toronto Ontario 100% 89,432 89,432 Mill Woods Town Centre Edmonton Alberta 40% 122,804 49,539 Millcroft Shopping Centre Burlington Ontario 50% 115,566 57,783 Orillia Square Mall Orillia Ontario 100% 91,440 91,440 RioCan Durham Centre Ajax Ontario 100% 121,280 121,280 RioCan Niagara Falls Niagara Falls Ontario 100% 106,103 106,103 RioCan Scarborough Centre Scarborough Ontario 100% 116,241 116,241 Shopper's World Brampton Brampton Ontario 100% 121,490 121,490 South Hamilton Square Hamilton Ontario 100% 93,125 93,125 Stratford Centre Stratford Ontario 100% 88,935 88,935 The Stockyards Toronto Ontario 50% 153,456 76,728 Trinity Common Brampton Brampton Ontario 100% 118,228 118,228 TOTAL 2,091,480 1,662,978

Update on Backfill Progress

23

RioCan currently 32 leases that are committed, conditional, or in advanced stages of negotiations that represent approximately $10.3 million at RioCan’s interest, or 94% of the total rental revenue lost through Target’s departure. These new leases will have a stronger growth profile than the previous Target Canada leases, which were assumed from Zellers and had little, if any, rent growth through the remaining lease terms and renewal options. In addition, the new leases are more market based, providing for a full pro-rata share of operating cost recoveries, utilities, and realty taxes, which were capped under the former Target Canada leases.

Deal Count

Square Feet at 100%

Square Feet at RioCan's Interest

Annual Base Rental Revenue at RioCan’s Interest

(millions)

Former Target Canada Space 19 2,091,480 1,662,977 $10.9

Backfill Progress

Committed Space 14 448,130 343,669 $5.2

Conditional Agreements 2 49,906 49,906 $0.6

Advanced Discussions 16 669,544 533,321 $4.5

Total Leased or in discussions 32 1,167,580 926,896 $10.3

Space Currently Marketed 568,625 411,121 TBD Total NLA upon completion of redevelopment 1,736,205 1,338,016

GLA converted for landlord uses (common area, loading docks, etc.) 186,155 188,841 n/a

Space for demolition/potential redevelopment 195,433 195,433 TBD

Total* 2,117,793 1,689,290 .

* Expansion space at RioCan Niagara Falls will result in an additional 26,313sf. of net leaseable area at this property.

Conservative Debt Profile

• Debt-to-Total Assets of 43.6% at Sept. 30, 2015. • Total operating lines $731 million, $582 available as at Sept. 30, 2015 • Unencumbered pool has a fair value of $3.3 billion • Floating rate debt 9.0% of aggregate debt • Strong coverage ratios (based on rolling 12 months to Sept. 30, 2015):

• EBITDA interest coverage of 3.0x • Debt service coverage of 2.3x and • Fixed charge coverage of 1.1x

24 * At RioCan’s interest This slide contains references to non-GAAP Measures. For a definition of such measures please refer to RioCan’s Sept. 30, 2015 MD&A.

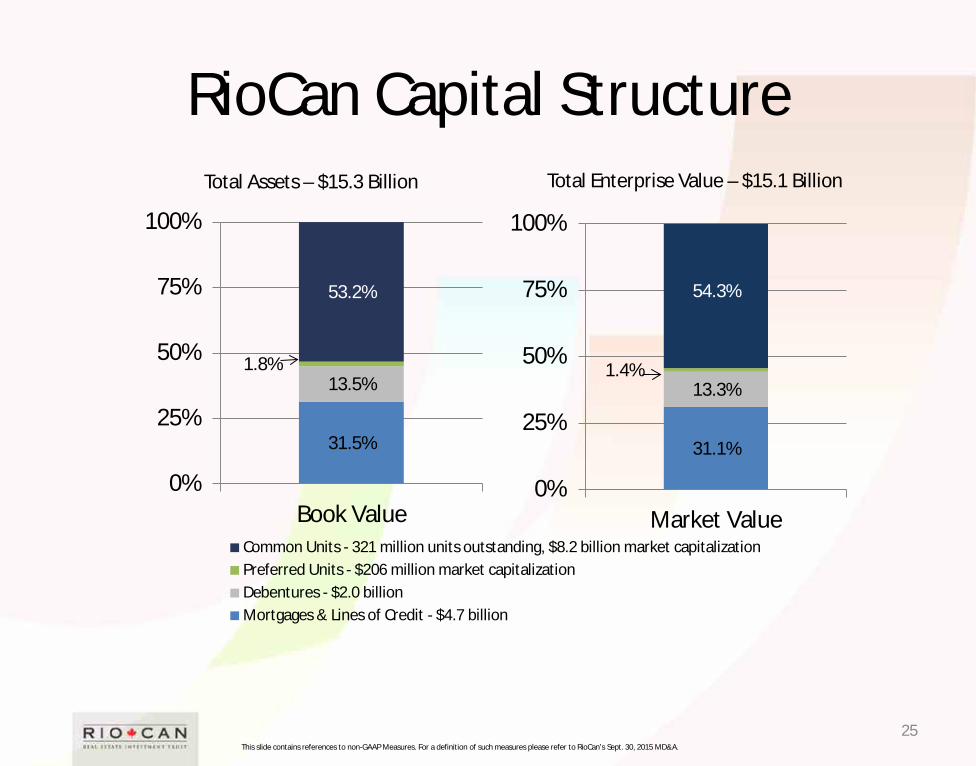

RioCan Capital Structure

31.5%

13.5% 1.8%

53.2%

0%

25%

50%

75%

100%

Book ValueCommon Units - 321 million units outstanding, $8.2 billion market capitalizationPreferred Units - $206 million market capitalizationDebentures - $2.0 billionMortgages & Lines of Credit - $4.7 billion

25

31.1%

13.3% 1.4%

54.3%

0%

25%

50%

75%

100%

Market Value

Total Assets – $15.3 Billion Total Enterprise Value – $15.1 Billion

This slide contains references to non-GAAP Measures. For a definition of such measures please refer to RioCan’s Sept. 30, 2015 MD&A.

Conservative Debt Structure Growth in Asset vs Debt

26

In millions Debt

Assets

20082009

2010

2011

2012

2013

2014

Q3 2015

3,260

6,667

5,338

15,255

Debt

Assets

CAGR – 16.8%

CAGR – 11.2%

This slide contains references to non-GAAP Measures. For a definition of such measures please refer to RioCan’s Sept.30, 2015 MD&A.

Modest Leverage, Strong Interest Coverage

• RioCan has consistently adhered to a conservative debt policy even through periods of considerable growth

• 60% max permitted under covenant • Interest coverage well in excess of the 1.65x maintenance covenant

47.3% 48.2% 51.9% 53.1% 53.8% 53.9% 56.6% 56.3% 54.9% 55.6% 49.1% 46.4% 43.6% 44.0% 43.8% 43.8%

2.9x 2.9x 2.6x 2.6x 2.7x 2.8x 2.9x

2.7x 2.6x 2.2x

2.5x 2.5x 2.7x 2.8x 2.9x 3.0x

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Q3 2015

Leverage Interest Coverage

27

* At RioCan’s interest

This slide contains references to non-GAAP Measures. For a definition of such measures please refer to RioCan’s Sept. 30, 2015 MD&A.

Debt Maturity Schedule

28

• Long-term, staggered debt maturity profile. • RioCan has successfully lowered overall borrowing costs and extended the weighted average term to maturity on

its debt since Dec. 31, 2014. The weighted average interest rate at Sept. 30, 2015 was 3.87% with a 4.24 year weighted avg. term to maturity at RioCan’s interest as compared to 4.12% and 3.95 years at Dec. 31, 2014.

• Low floating rate debt exposure (9.0% of total debt).

1.64%

4.35% 4.03%

3.65% 3.26%

4.12%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2015 (remaining) 2016 2017 2018 2019 Thereafter

Scheduled principal amortization Mortgages payable

Floating Rate Mortgages and Lines of Credit Debentures payable

Weighted average interest rate

$ Millions

Weighted Avg. Interest Rate on M

aturing Debt

211 702

948 811 1,004

2,985

29

Leverage and Coverage Ratios & Targets

Rolling 12 Months Ended

At RioCan’s interest

Sept. 30/15

Dec. 31/14

Interest coverage ratio 3.00x 2.89x

Debt service coverage ratio 2.31x 2.20x

Fixed charge coverage ratio 1.09x 1.08x

Net operating debt to operating EBITDA ratio 7.87x 7.67x

Distributions as a percentage of AFFO 91.6% 94.5%

Unencumbered Assets to Unsecured Debt 165% 149%

This slide contains references to non-GAAP Measures. For a definition of such measures please refer to RioCan’s Sept. 30, 2015 MD&A.

Targeted Ratios

>3.00X

>2.25X

>1.10X

<6.50X

<90%

>200%

Future Growth Drivers

30

Organic Growth

Development

Institutional Relationships

Acquisitions

Land Use Intensification

Organic Growth Canadian Portfolio

31

Lease Expiries

(thousands except psf and % amounts) Portfolio NLA 2015 remaining 2016 2017 2018 2019

Total 39,282 1,279 3,464 3,883 4,466 4,698

Square Feet expiring/portfolio NLA 3.3% 8.8% 9.9% 11.4% 12.0%

Total average net rent psf $17.02 $17.92 $18.35 $18.77 $17.97 $18.10

Ability to add growth through rental renewals with 45% of leases renewing over next five years. • In Q3 2015 achieved renewal rent increases of 8.6% or $1.41 psf with an average renewal rate of $17.75 psf. YTD achieved renewal rent increases of 9.4% or

$1.57 psf with an average renewal rate of $18.29 psf. • Retention rate of 89.8% in Q3 2015 (87.0% YTD).

$10

$11

$12

$13

$14

$15

$16

$17

$18

$19

$20

0

1,000

2,000

3,000

4,000

5,000

6,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Rent

PSF

Squa

re fe

et ('

000s

)

RioCan Lease Maturity Schedule and Renewal History

Square feet expiring (left axis) Square feet renewed (left axis) Achieved Renewal Rent PSF Expired Rent PSF Expiring Rent PSF

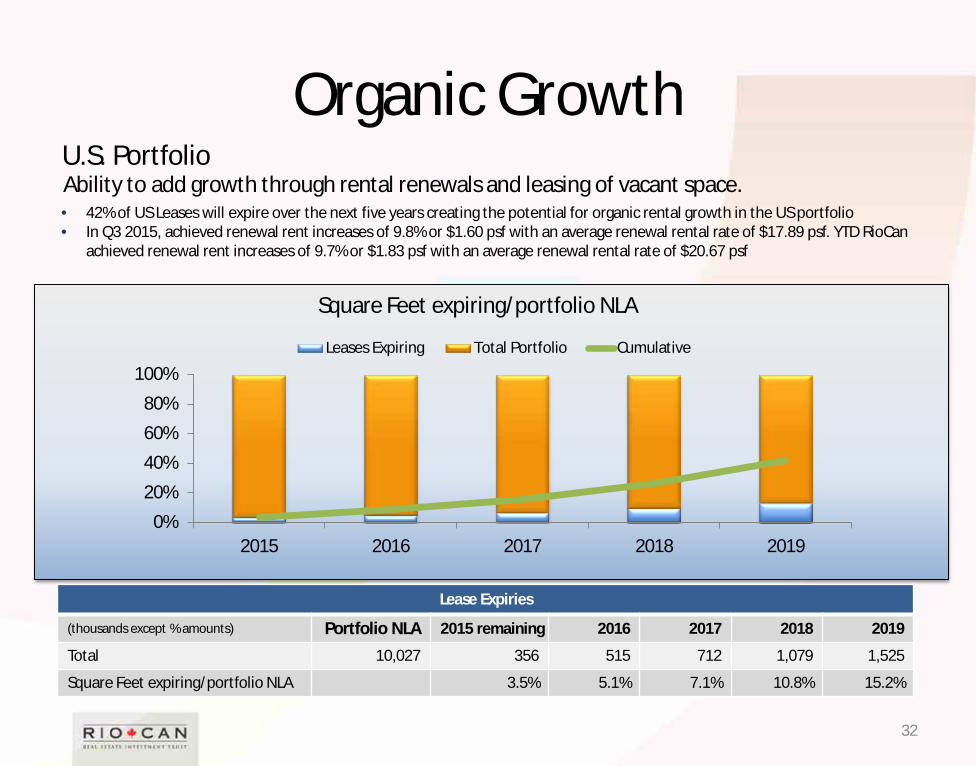

Organic Growth U.S. Portfolio

32

Lease Expiries

(thousands except % amounts) Portfolio NLA 2015 remaining 2016 2017 2018 2019

Total 10,027 356 515 712 1,079 1,525

Square Feet expiring/portfolio NLA 3.5% 5.1% 7.1% 10.8% 15.2%

0%

20%

40%

60%

80%

100%

2015 2016 2017 2018 2019

Leases Expiring Total Portfolio Cumulative

Square Feet expiring/portfolio NLA

Ability to add growth through rental renewals and leasing of vacant space. • 42% of US Leases will expire over the next five years creating the potential for organic rental growth in the US portfolio • In Q3 2015, achieved renewal rent increases of 9.8% or $1.60 psf with an average renewal rental rate of $17.89 psf. YTD RioCan

achieved renewal rent increases of 9.7% or $1.83 psf with an average renewal rental rate of $20.67 psf

Organic Growth

33

Occupancy Sept. 30, 2015 Sept. 30, 2014

Canada US Total Canada US Total

Majors (>10,000 sf) 94.0% 99.9% 95.3% 98.9% 99.9% 99.1%

Small Shop (<10,000 sf) 91.9% 88.9% 91.4% 93.2% 88.2% 92.4%

Blended 93.2% 97.1% 94.0% 97.0% 96.9% 97.0%

Leasing Activity Canada US

Quarter ended Sept. 30, (per square foot) 2015 2014 2015 2014

New Leasing $16.23 $20.65 $21.32 $24.39

Renewal Leasing $17.75 $17.57 $20.67 $20.11

% increase in average net rent psf 8.6% 12.9% 9.8% 9.3%

During the third quarter of 2015, new deals in Canada were completed at lower average net rents per square foot of $16.23 compared to $20.65 in the prior year quarter. Average rents this quarter were lower due to an increased number of new leases over 10,000 square feet compared to the third quarter of 2014.

Joint Venture Agreement to purchase Kimco’s interest in 22 Canadian properties

34

• On September 24, 2015, RioCan announced that after fifteen successful years as partners, RioCan and Kimco have agreed to unwind their Canadian joint venture. The portfolio of 35 jointly owned properties ("RioKim Portfolio") will be divided into three groups:

• the first group is a collection of 22 properties selected by RioCan that will be acquired in two stages: 19 properties were acquired on Oct. 6, 2015 at a purchase price of $477 million. RioCan assumed Kimco's share of the existing in-place debt of $127 million, and three properties to be acquired by January 2016;

• the second group consists of ten institutional-quality retail assets which the partners have agreed to market for sale, one of which is currently under a conditional contract to be sold; and

• the third group of assets includes three transitional properties (Charlottetown Mall, Desserte Ouest, and that were previously occupied by Target, which will be dealt with at a future date.

• The acquisition will be immediately accretive, and upon completion of the second phase of the transaction the portfolio is expected to generate additional annualized net operating income of approximately $45 million and will require no additional resources by management. RioCan's cash commitment of approximately $485 million needed to complete the overall transaction will be funded from a combination of internal resources and credit facilities.

34

Joint Venture Agreement with Hudson’s Bay Company

35

• On February 25, 2015, RioCan announced that it has agreed to form a joint venture (“JV Entity”) focused on real estate growth opportunities in Canada with Hudson’s Bay Company (“HBC”).

• The joint venture will enable RioCan and HBC to build on the strength of existing real estate assets through potential future redevelopment, as well as identify new real estate acquisition and redevelopment opportunities.

• The transaction is structured to facilitate an IPO or other monetization of the joint venture at a yet to be determined future date.

• On July 9, 2015, the parties completed the first tranche of the joint venture: • RioCan contributed a 50% interest in two mall properties in Ontario (Oakville Place and Georgian Mall), resulting

in an initial equity stake of $147 million or 13.4% in the joint venture entity. HBC contributed 7 owned or ground-leased properties (including Hudson's Bay flagship properties in downtown Vancouver, Calgary, Ottawa, and Montreal) with approximately 2.6 million square feet.

• RioCan has committed to contribute a total of $325 million to the JV for an eventual pro forma equity stake of approximately 25% based on the first tranche closing to be made by the third anniversary of the closing date.

• The balance of RioCan’s contributions will consist of $53 million in tenant allowances, and $125 million in cash to be used to fund future property acquisitions to increase the value and diversify the tenant base of the JV.

35

Extracting Value by Recycling Capital • RioCan continues to evaluate its portfolio in order to selectively dispose of assets as a means of recycling

capital, and also to increase the portfolio weighting to the six major markets in Canada. • Since the start of 2013 to Sept. 30, 2015, the Trust disposed of $818 million (excluding assets sold into HBC

Joint venture) of properties in Canada. • These asset sales will further enhance RioCan’s strategy to shift the portfolio’s geographic allocation away

from low growth markets to Canada’s high population, high growth markets;

– RioCan’s concentration in Canada’s six high growth markets is 74.4% (Year end 2004 - 57.7%) and will increase as the result of the Kimco asset acquisition.

– Capital from asset sales redeployed into acquisitions and development activities. – Markets with highest population growth will outperform smaller markets with little growth or negative population statistics.

36

RioCan’s plan to recycle capital into higher growth assets will provide for enhanced returns to unitholders and a reduced need for access to public equity markets to raise capital.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Q32015

57.7%

74.4%

Development Activity - Current Portfolio

37

Alberta 16%

Suburban GTA 27%

Toronto 50%

Other Ontario 7%

Development Portfolio by Geographic Diversification

(thousands of square feet) NLA - 100% NLA - RioCan%

Greenfield Development 2,872 1,833

Urban Intensification 4,213 2,135

Sub-total 7,085 3,968

Expansion & Redevelopment 2,804 1,922

Total 9,889 5,890

(thousands of dollars) 2015 remainder 2016 2017+ Future

Development Total

Greenfield Development 12,263 29,224 28,937 207,811 278,235

Urban Intensification 6,211 95,831 170,600 702,030 974,672

Expansion & Redevelopment 11,951 111,588 154,796 97,622 375,957

Total RioCan Share of Construction Expenditures 30,325 236,643 354,333 1,007,463 1,628,864

(i) Includes project costs funded by RioCan construction lines. (ii) Credits reflect proceeds from potential land parcel sale.

Toronto Development Projects and Recent Completions

Key Development Projects Eglinton & Warden (completed) The Stockyards (completed) 1860 Bayview Ave Bathurst & College Yonge & Eglinton Northeast Corner College and Manning Dupont Street The Well King & Portland

Properties not mapped: Westney Road and Taunton, RioCan Centre Vaughan, Windfield Farms

38

Calgary Development Projects Greenfield Developments

East Hills Sage Hill

Urban Intensification Calgary East village (CPA Lands)

39

Ottawa Development Projects and Recent Completions

Key Development Projects Grant Crossing (completed) Herongate Mall (completed) Tanger Outlets – Kanata (Phase I completed)

40

Land Use Intensification – Residential Potential Transit Oriented Development

• RioCan’s Urban Platform holds a number of sites where the possibility for additional density through residential exist: – Properties with the greatest potential for residential intensification are located on or near transit lines

• Capitalize on trend in Canada’s six high growth markets towards “densifying” existing urban locations, driven by: – Prohibitive costs of expanding infrastructure beyond urban boundaries – Maximizing use of mass transit – Generate higher yields as land is already owned

• RioCan has a number of potential sites located in other major markets such as, Tillicum Centre in Victoria, BC and Brentwood Village Mall in Calgary Alberta

41

Toronto

Development Activities - Residential Intensification Investment Rationale

• Demand for professionally managed, quality apartment units in Canada remains high.

• Rental rates in key major markets, like Toronto, have reached a level where the economics are attractive for redeveloping certain centres in urban, transit oriented locations. RioCan owns the underlying land, often at irreplaceable locations, thus giving it the unique opportunity to create a tremendous amount of value.

Market CMHC Reported Vacancy Rate October 2015

Toronto, Ontario 1.6%

Ottawa, Ontario 2.6%

Calgary, Alberta 5.3%

Edmonton, Alberta

4.2%

Vancouver, BC 0.8%

• The addition of a residential component will enhance the value of the underlying retail element of RioCan’s property.

• It is a sector that allows a steady and continuous income stream with a growth profile that will serve as a hedge against inflation. The residential rental sector serves as a healthy diversification to RioCan’s retail portfolio.

42

Favourable demographic trends

• Demand for rental residential spaces has strengthened as home prices have increased dramatically. Average price of a detached home in Toronto now exceeds $1 million

Land Use Intensification – Residential Potential Transit Oriented Development

17% 14%

4%

16%

1991-2006 2006-2011 1991-2006 2006-2011

Gro

wth

%

Population Growth Rates Suburban GTA Downtown Toronto

43

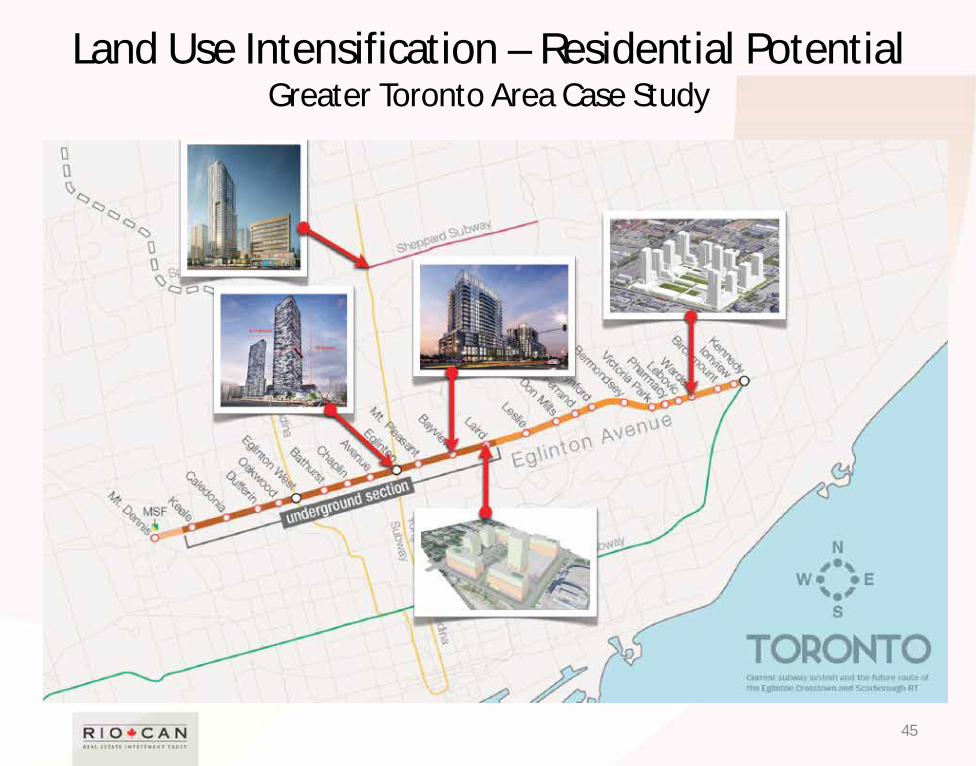

Land Use Intensification – Residential Potential Greater Toronto Area Case Study

44

N

12 1. 2955 Bloor Street 2. 740 Dupont Ave 3. College & Manning 4. 491 College Street 5. Dufferin Plaza 6. King & Portland 7. Lawrence Square 8. Markington Square 9. Queensway Cineplex 10. RioCan Hall 11. RioCan Leaside 12. RioCan Marketplace 13. RioCan Scarborough 14. Yonge Sheppard Centre 15. Sunnybrook Plaza 16. The Well 17. Northeast Yonge & Eglinton

Favourable barriers to entry: – Land is already owned aiding overall project yields – Intensification replaces old stock with dynamic retail. High demand space that attracts the

highest class of tenants and attracts the highest rents

Land Use Intensification – Residential Potential Greater Toronto Area Case Study

45

Land Use Intensification – Residential Potential

• RioCan’s Residential development plans include amenities that meet or exceed offerings in current condominium developments providing a competitive advantage over that of existing residential stock.

• Given the extent of this initiative, RioCan will possess a scale that will result in numerous efficiencies going forward. Residential rental properties will typically attract favourable financing terms based on the availability of CMHC insurance.

• RioCan is committed to ensuring that the individual properties in its portfolio are utilized to their highest and best use. RioCan has focused on mixed use projects containing predominantly multi-residential rental buildings. RioCan has identified 46 properties that it deems to be strong intensification opportunities all located in Canada’s six major markets.

46

Development Activities Residential Intensification

Potential GLA (square feet at 100%)

Property Location

Application Submission

Date RioCan Ownership %

(Partner) Commercial Residential Rental (i) Condominium Total

Residential Rental Units

Yonge Eglinton Northeast Corner Toronto, ON Jan-12 50% (Metropia/Bazis) 57,000 377,000 491,000 925,000 461 Sunnybrook Plaza Toronto, ON Dec-14 100% 25,000 384,000 — 409,000 426 College & Manning Toronto, ON Sep-13 50% (Allied) 6,000 57,000 — 63,000 77 740 Dupont Street Toronto, ON Jul-14 100% 85,000 103,000 — 188,000 122 Sheppard Centre Toronto, ON May-13 50% (Kingsett) 108,000 327,000 — 435,000 369 King & Portland Toronto, ON Aug-13 50% (Allied) 267,000 118,000 — 385,000 116 The Well Toronto, ON Feb-14 40% (Allied / Diamondcorp) 1,611,000 1,003,000 482,000 3,096,000 1,143 Tillicum Victoria, BC Feb-09 50% (Kimco) — 122,000 — 122,000 169 2955 Bloor Street West Toronto, ON Aug-15 100% 8,000 67,000 — 75,000 86 Markington Square Toronto, ON Oct-15 100% — 267,000 — 267,000 288 RioCan Grand Park GTA, ON Aug-15 100% 9,000 259,000 — 268,000 321 Brentwood Village Calgary, AB Oct-15 100% 13,000 184,000 — 197,000 224 TOTAL 2,189,000 3,268,000 973,000 6,430,000 3,802

RioCan has filed applications for rezoning 12 projects which, upon completion, should comprise a total of 6.4 million square feet, of which 3.3 million square feet will be residential rental units held for long-term rental income, 1.0 million square feet will be condominiums for sale and 2.2 million square feet will be incremental commercial gross leasable area. This would permit RioCan to have an interest in approximately 3,802 residential units.

RioCan intends to file applications to rezone 15 additional properties by the second half of 2016. These proposed redevelopments are expected to produce approximately 6.7 million square feet, of which 7.2 million square feet is expected to be residential. This would permit RioCan to have an interest in an additional 8,500 residential units. As these projects are in preliminary stages, there can be no assurance that any of these developments will be undertaken and if so, on what terms.

47

48

Location: Toronto, Ontario

Intersection: Yonge & Eglinton

Total Proposed Retail GLA: 57,000 square feet*

Proposed Rental Residential Units: 461 Units

Design Concept: Urban Retail

Anticipated Completion: 2018

RioCan Interest 50%

Yonge & Eglinton Northeast Corner - Toronto, Ontario

• Located across the street from RioCan’s head office

• 1.1 acre site has been approved for redevelopment by the city of Toronto with a 58 storey tower at corner of Yonge and Eglinton and a 36 storey tower fronting Roehampton Avenue (first street north of Eglinton).

• Condominium portion of the project is 100% pre-sold.

• North tower to be developed as rental residential. Current plans are for a 461 unit residential apartment building.

• Construction commenced in Q2 2014.

* RioCan will purchase 100% of the retail space at a 7% capitalization rate upon completion of the project.

Investing for the Future Creating New Cash Flow Sources

Residential Intensification

• Located at the busy intersection of Bayview Avenue and Eglinton Avenue in midtown Toronto.

• The site benefits from excellent demographics and is a probable location for a stop along the proposed Eglinton subway line.

• RioCan has filed for rezoning to permit a 409,000 sf mixed use, retail/residential redevelopment project including 25,000 sf of retail and 384,000 sf of residential including 426 units.

49

RioCan has a number of Urban Intensification opportunities in the GTA market

Sunnybrook Plaza, Toronto, ON

Today

Proposed

Investing for the Future Creating New Cash Flow Sources

Residential Intensification

50

The Sheppard Centre, Toronto Location: Toronto, Ontario Intersection: Yonge & Sheppard Total Commercial GLA: 108,000 square feet Proposed Rental Units: 369 Design Concept: Urban Retail Expected Construction Start: 2015 Anticipated Completion: 2017 RioCan Interest 50%

• Plans include substantial renovation of retail space including a new four storey retail addition fronting Sheppard Avenue and substantial upgrade to the interior retail space.

• When complete will includes 108,000 square feet of retail space.

• Plans also contemplate the addition of a new 39 storey residential tower containing 327,000 square feet including approximately 369 rental units.

• In June 2015, RioCan and its partner received zoning approval

• Anchored by Shoppers Drug Mart, Winners, and three major banks • Agreements in place with Longo’s and LA Fitness

Potential Design

Investing for the Future Creating New Cash Flow Sources

Residential Intensification

Development Pipeline

51

• RioCan, Allied Properties and Diamond Corp entered into a joint venture arrangement to acquire the Globe and Mail site in downtown The site is approximately 7.7 acres.

• During the quarter, RioCan and its partners received an Official Plan Amendment from The City of Toronto for approximately 3.1 million square feet of Gross Floor Area.

• Project is expected to be approximately 3.1 million square feet of mixed use space including approximately 1.6 million sf of retail and office space and 1.5 million sf of residential space (1.0 million sf rental and 0.5 million sf as condominium space) that will be built out in phases.

• The joint venture is structured on a 40/40/20 basis between RioCan, Allied and Diamond. RioCan and Allied will act as joint development and construction managers. Upon completion of any projects RioCan will act as property manager for any retail portion of the property and Allied will act as property manager for any office portion.

RioCan, Allied Properties REIT, & Diamond Corporation Joint Venture

Development Pipeline

52

RioCan, Allied Properties REIT, & Diamond Corporation Joint Venture

THE WELL – Potential Layout and Vision

Current vision for the site includes a mixed use of office, retail and residential uses with inspiration drawn from other open air mixed retail properties in Europe.

Development Pipeline

53

• RioCan and Allied Properties announced in July 2012 that they had entered into a joint venture arrangement on a non exclusive basis to acquire sites in the urban areas of major Canadian cities that are suitable for mixed use intensification.

• The joint venture is structured on a 50/50 basis between RioCan and Allied. Upon completion of any projects RioCan will act as property manager for any retail portion of the property and Allied will act as property manager for any office portion.

• First two sites to be developed are: – King and Portland which will be developed into a mixed use

complex with approx. 385,000 square feet including 116 residential units in Toronto, Ontario. RioCan and its partner received zoning approval in July 2015 for this project.

– College and Manning will be developed into a mixed use complex with approx. 63,000 square feet. The site, which received zoning approval in the third quarter of 2014, will include 6,000 square feet of retail and 77 residential units in an eight-storey mixed-use building.

RioCan & Allied Properties REIT Joint Venture King & Portland

College and Manning

Development Pipeline

• 2.8 acre site located in the East Village area of downtown Calgary, Alberta. One of Calgary’s few remaining privately owned blocks.

• The site was acquired on a 50/50 joint venture basis with KingSett Capital. RioCan purchased KingSett’s 50% interest in the property in Q2 2015, resulting in a 100% interest in the property.

• The site is zoned for the proposed development and RioCan has submitted for a development permit, which the Trust expects to be approved by the Calgary Planning Commission in Q3 2015.

• The intention is for two residential towers to be erected upon the retail podium that will be anchored by Loblaws.

• RioCan and KingSett, have entered into an agreement with developer, Embassy BOSA Inc., to sell up to $30 million in air rights (representing 600,000 square feet) above the site, along with approximately $40 million in cost reimbursement for infrastructure works.

• Development is anticipated to commence in 2016.

54

Calgary East Village Potential Design

Current Site

Development Pipeline Greenfield Development

55

Sage Hill, Calgary

• Sage Hill Crossing, a 32 acre greenfield development site in Northwest Calgary.

• RioCan owns the development on a 50/50 basis with KingSett Capital.

• Development commenced in 2013.

• Once completed, the anticipated gross leasable area is 394,000 square feet of retail use.

• The property is 80% preleased with Walmart and Loblaws as anchor tenants. Walmart commenced operations in January 2015.

• Other major tenants include, RBC, Scotiabank, McDonalds, Liquor Depot and London Drugs.

• Loblaws is slated to open in Q1 2016 with the remainder of the tenants opening over the course of 2016.

• RioCan is responsible for the development, management and leasing of the property.

“Densifying” existing urban locations

56

RioCan Yonge Eglinton Centre –The Cube

Location: Toronto, Ontario Intersection: Yonge & Eglinton Total Proposed GLA: 45,000 square feet Design Concept: Urban Retail Construction Start: Q2 2013 Completion: 2015 RioCan Interest: 100% RioCan has leased the media screens to CBS Outdoor Canada, which will generate additional revenue at the site.

Before After

Urban Intensification

57

420 Bathurst Street, Toronto

Location: Toronto, Ontario

Intersection: Bathurst & College

Total Proposed GLA: 145,000 square feet

Design Concept: Urban Retail/Office

Anticipated Completion: 2018

Urban Intensification – Completed Projects

58

Queen & Portland, Toronto, ON

Before

After

Location: Toronto, Ontario

Intersection: Portland & Queen

Total GLA: 91,000 square feet

Design Concept: Mixed-use facility Construction Completed: 2011

Urban Intensification – Completed Projects

59

1717 Avenue Road, Toronto, ON

Location: Toronto, Ontario

Intersection: 1717 Avenue Road

Total GLA: 91,000 square feet

Design Concept: Mixed-use facility Construction Completed: 2011

• 52.5 acre site, approximately 20 kilometres west of Ottawa • Construction was completed on the initial phase comprising 299,000 square foot in Q4 2014. • The site is performing well since the grand opening on October 17, 2014. • Saks Off Fifth, part of the phase two development on the site, is currently under construction and anticipates commencing operations in

the second quarter of 2016. The third phase featuring 51,000 square feet will commence construction in 2016.

60

Tanger Outlets - Kanata

Outlet Centre Development