risi international containerboard conference| 2018...industrial bags (global) based on sales vo lume...

TRANSCRIPT

Florian StockertNovember 2018

The European Containerboard Market

RISIInternational Containerboard Conference| 2018

Mondi is a global leader in packaging and paper

1

More than 100,000 solutions for our customersThe image part with relationship ID rId10 was not found in the file.

Group offices in Johannesburg, London and ViennaThe image part with relationship ID rId13 was not found in the file.

FTSE4Good Index Series JSE’s Socially Responsible Investment Index

26,000 employees

Over 100 operations across more than 30 countries

2.4M hectares of forest managed

Primary listing on the JSE Limited for Mondi Limited

Premium listing on the London Stock Exchange for Mondi plc

2

Mondi at a glance

2017revenue1

& underlying

EBITDA margin3

Products

22.3% 13.5% 25.3%

€3,735m €1,646m €1,832m

52%

1 Segment revenues, before elimination of inter-segment revenues2 Packaging Paper and Fibre Packaging were replaced by a single business unit called Fibre Packaging effective from 1 August 20183 The Group early adopted the new 'Leases' accounting standard, IFRS 16. All 2017 comparative figures in this presentation have been restated where applicable.

Consumer Packaging Uncoated Fine Paper Fibre Packaging2

23%

25%

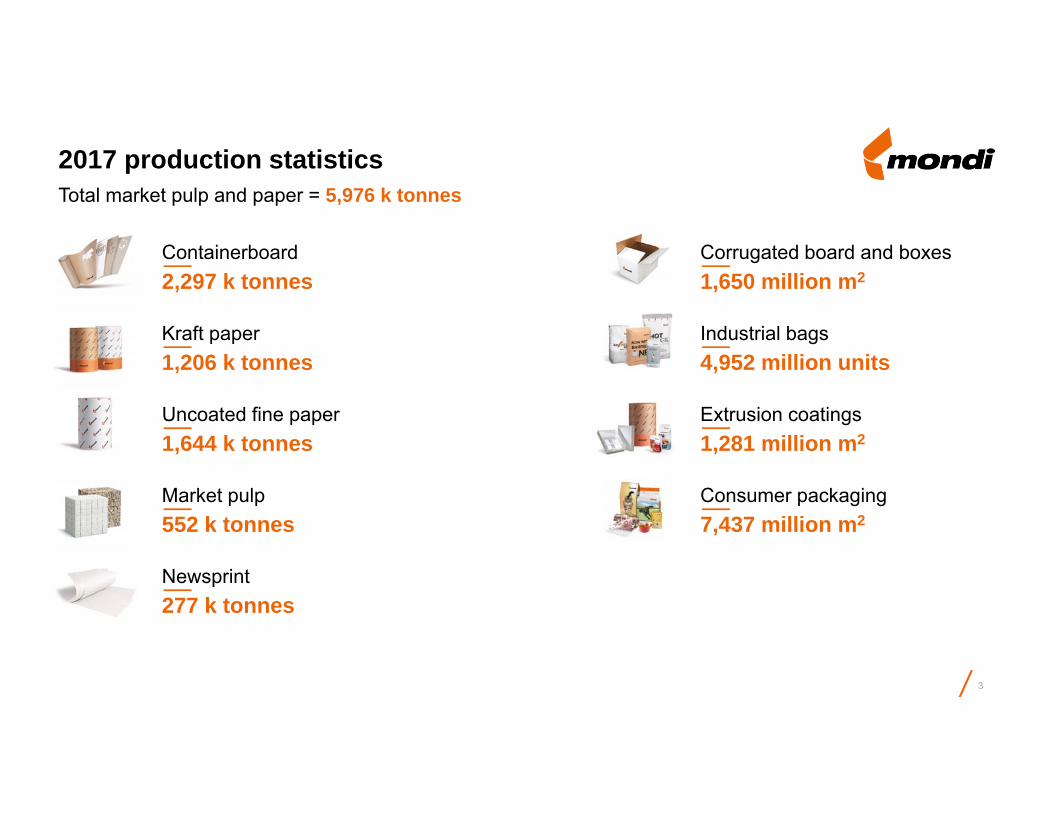

2017 production statistics

Kraft paper1,206 k tonnes

Uncoated fine paper1,644 k tonnes

Market pulp552 k tonnes

Newsprint277 k tonnes

Corrugated board and boxes1,650 million m2

Industrial bags4,952 million units

Extrusion coatings1,281 million m2

Consumer packaging7,437 million m2

Containerboard2,297 k tonnes

Total market pulp and paper = 5,976 k tonnes

3

4

Leading market positions

Consumer flexible packaging

Kraft paper

Industrialbags

#3

Corrugated packaging

Virgin containerboard

Containerboard

Commercial release liner

GlobalUncoated fine paper

Please see sources and definitions at the end of this document

Europe Emerging Europe South AfricaUncoated fine paper

#1

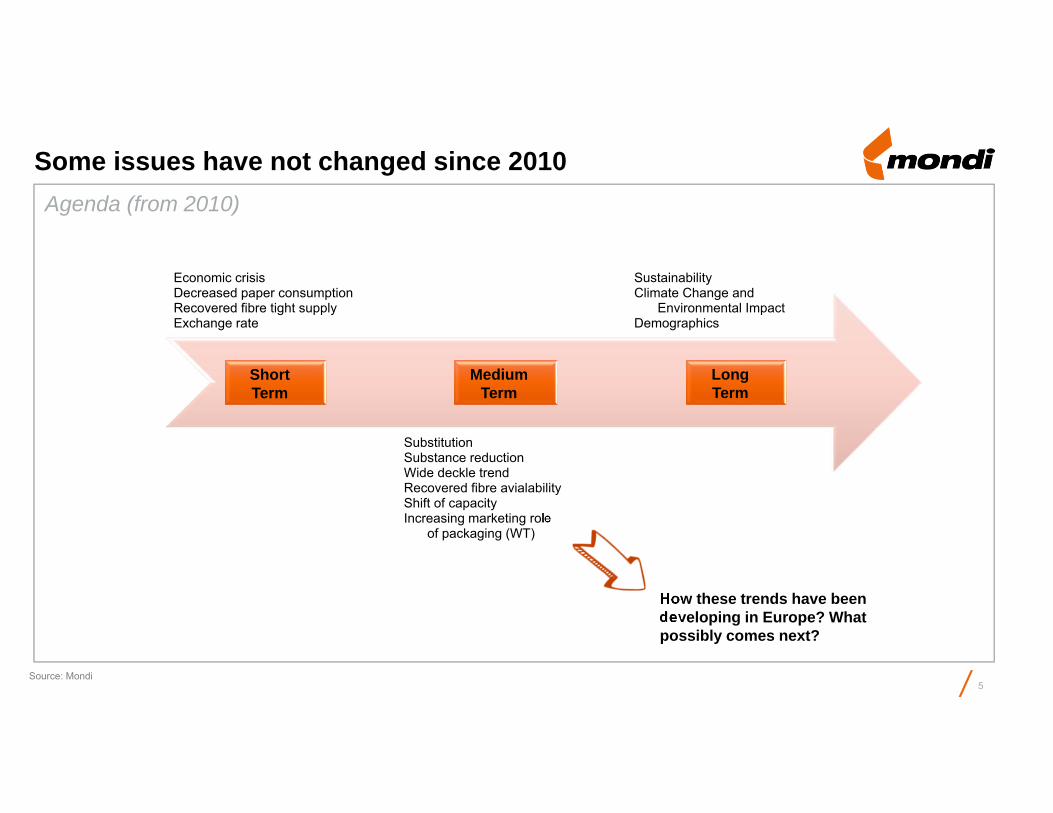

Some issues have not changed since 2010

Economic crisisDecreased paper consumptionRecovered fibre tight supplyExchange rate

SubstitutionSubstance reductionWide deckle trendRecovered fibre avialabilityShift of capacityIncreasing marketing role

of packaging (WT)

SustainabilityClimate Change and

Environmental ImpactDemographics

ShortTerm

MediumTerm

LongTerm

How these trends have beendeveloping in Europe? Whatpossibly comes next?

Agenda (from 2010)

5Source: Mondi

6

Drivers for containerboard growth 2013-2018

Containerboard market overview

Recycled containerboard

Kraft Top Liner

Kraftliner

White liners

Semi-chemical Fluting

Strong fundamentals driving containerboard consumption in Europe

Source: Numera Analytics 7

2013 20132017 20172010 2012

4.3%

2.5%3.2%

1.4%2.4%

9.9%

0%

5%

10%

15%

Demand Real GDP Manufacturing ConsumerSpending

Retail Sales E-commerce

EU containerboard demand and its drivers

E-commerce growth is pulling corrugated

Source: Eurostat, Numera Analytics, Mondi corrugated e-commerce study 8

81%

15%

4% 1%0%

15%

30%

45%

60%

75%

90%

Corrugated Flexibles Protectivepackaging

Protective mailers

Global e-commerce packaging by type(2017)

80% of packaging in e-commerce is corrugated

e-commerce growth needs corrugated to grow with it

0

40

80

120

160

200

08 09 10 11 12 13 14 15 16 17

EU e-commerce retail sales

Index, 2010 = 100

This one exceptionally strong increase is partly due to change in reporting standards of Amazon in 2016

0

10

20

30

40

50

60

70

80

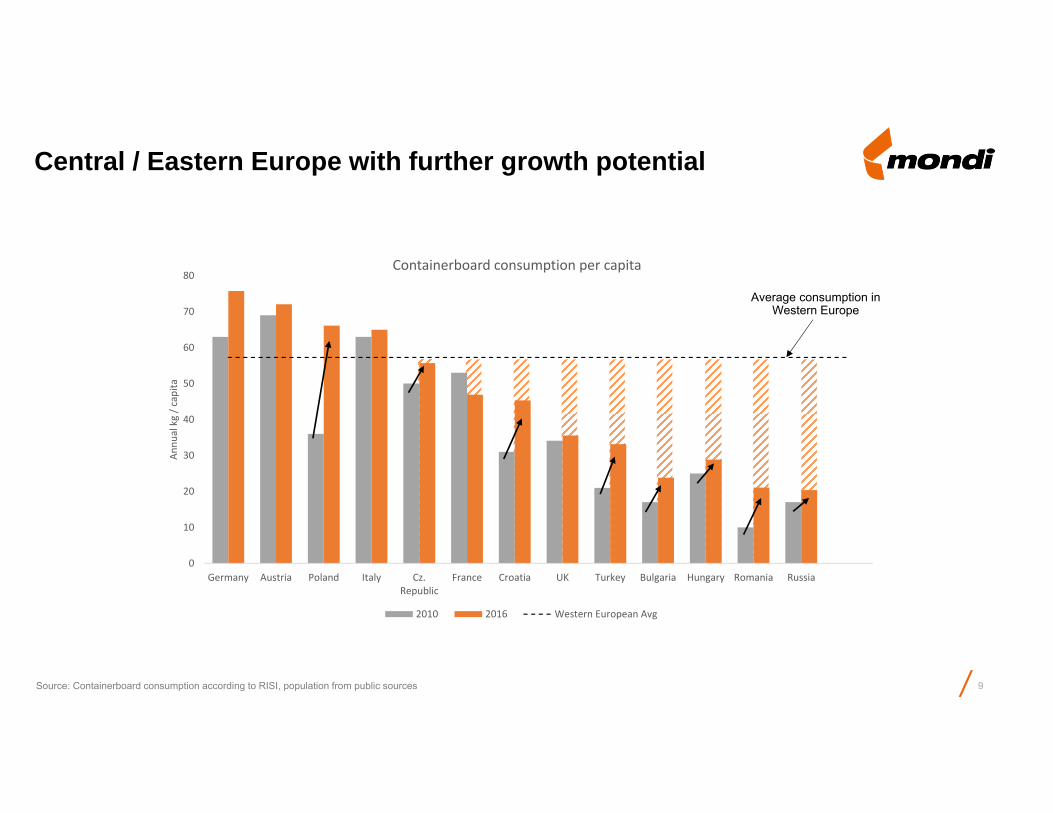

Germany Austria Poland Italy Cz.Republic

France Croatia UK Turkey Bulgaria Hungary Romania Russia

Annu

al kg / c

apita

Containerboard consumption per capita

2010 2016 Western European Avg

Central / Eastern Europe with further growth potential

Source: Containerboard consumption according to RISI, population from public sources

Average consumption inWestern Europe

9

10

Drivers for containerboard growth 2013-2018

Containerboard market overview

Recycled containerboard

Kraft Top Liner

Kraftliner

White liners

Semi-chemical Fluting

In the last five years, RCB growth in Europe has exceeded new capacity

Source: RISI (2013), CEPI (2014-2018). 2018 based on extrapolated H1 2018 growth. Based on current available information.1. Europe excluding Russia 11

4.4%

2.3%

3.9%

1.6%

5.9%

3.9%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

5,000

10,000

15,000

20,000

25,000

30,000

2013 2014 2015 2016 2017 2018Aug YTD

Mar

ket d

eman

d (k

t)

Growth rate RCB Europe

● Europe growth according to CEPI / RISI:

○ 2017 RCB consumption: 26-27 mt

○ Average market growth for 2013 – 2018:

- 3.5-4% per annum

- ~4.5mt (~900ktpa)

● New RCB capacity in Europe absorbed due to strong

domestic demand, especially in 2017

● Over the last 5 years (2013-2018), demand has

outstripped new capacity by 1.1mt:

4.83.7

0.0

1.0

2.0

3.0

4.0

5.0

Mill

ion

tonn

es

Demand Capacity

RCB demand growth in Europe 1 (CEPI)

Strong increase in average containerboard prices since January 2017

Source: FOEX PIX 12

TL3 PIX

Kraftliner PIX

0

100

200

300

400

500

600

700

800

1/1/2010 7/1/2010 1/1/2011 7/1/2011 1/1/2012 7/1/2012 1/1/2013 7/1/2013 1/1/2014 7/1/2014 1/1/2015 7/1/2015 1/1/2016 7/1/2016 1/1/2017 7/1/2017 1/1/2018 7/1/2018

EU

R /t

Looking ahead…

13

1.82.7

3.5 3.1

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Base -1% Base Base +1% Capacity

Mill

ion

tonn

es

Demand

2018 – 2020

2.02.9

4.0

2.8

1.2

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Base -1% Base Base +1% Capacity

Mill

ion

tonn

es

Demand

● We expect European recycled containerboard to grow at ~3% per annum in the medium term

● We expect demand to be in line supply over the next couple of years

● Post 2020, variables:

○ European demand growth and structural drivers (e-commerce, exports)

○ Execution of new capacity. Projects may be further delayed or cancelled

○ China OCC ban will affect global tradeflows - underpin for net exports from Europe

2021 – 20234.0

Range of possible outcomes depending on timing capacities materialise

14

Drivers for containerboard growth 2013-2018

Containerboard market overview

Recycled containerboard

Kraft Top Liner

Kraftliner

White liners

Semi-chemical Fluting

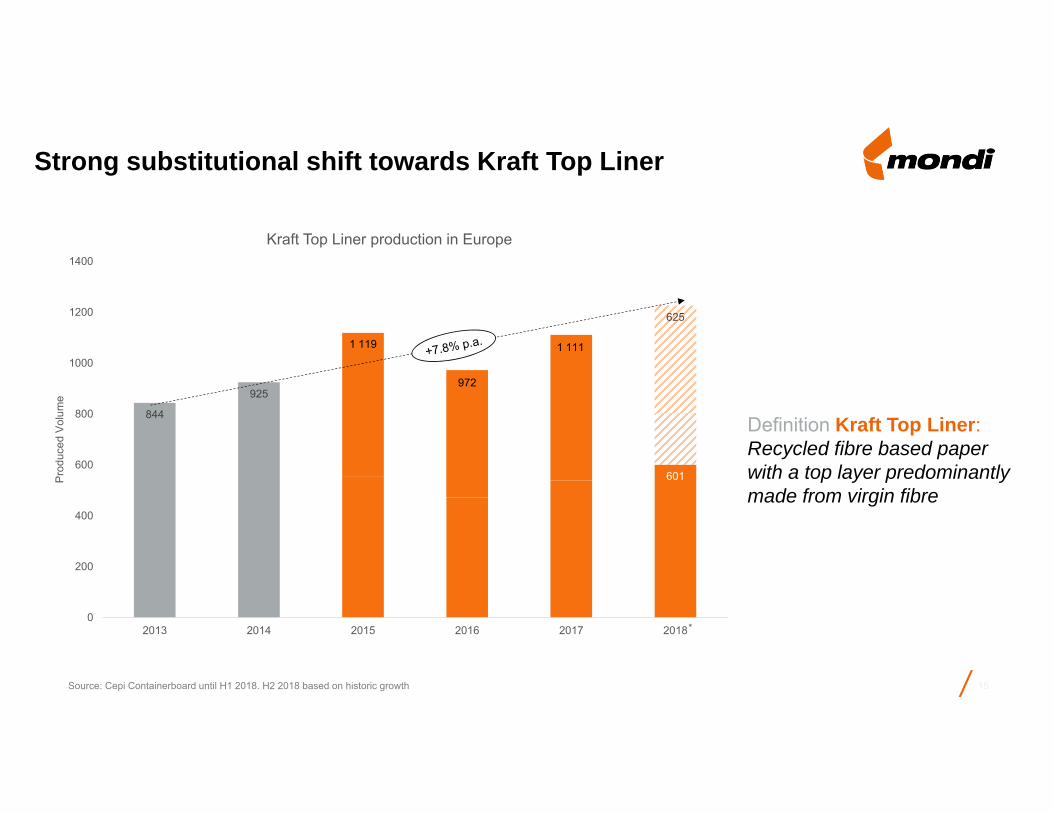

Strong substitutional shift towards Kraft Top Liner

Source: Cepi Containerboard until H1 2018. H2 2018 based on historic growth 15

601

625

844

925

0

200

400

600

800

1000

1200

1400

2013 2014 2015 2016 2017 2018

Pro

duce

d V

olum

e

Kraft Top Liner production in Europe

Definition Kraft Top Liner:Recycled fibre based paper with a top layer predominantly made from virgin fibre

*

1 119

972

1 111

Strength, printability, appearance: Kraft Top White

16

17

Drivers for containerboard growth 2013-2018

Containerboard market overview

Recycled containerboard

Kraft Top Liner

Kraftliner

White liners

Semi-chemical Fluting

-0.5%

2.5%

4.7%4.0%

1.6%

-2.3%

-4%

-2%

0%

2%

4%

6%

8%

10%

0

1,000

2,000

3,000

4,000

5,000

2013 2014 2015 2016 2017 2018Aug YTD

Mar

ket d

eman

d (k

t)

Growth rate KL Europe

Kraftliner historic demand growth in Europe and new capacity

Source: CEPI (2015-2018) and RISI (2013-2014). 2018 based on extrapolated H1 2018 growth. Based on current available information.1. Kraftliner includes all kraftliner including white but excludes kraft top liner2. Europe excludes Russia

18

● Europe growth according to CEPI / RISI:

○ 2017 kraftliner consumption: 5.2mt

○ Average market growth for 2013 – 2018:

- 2.1-2.7% per annum

- 500-650 kt (~120ktpa)

● There is no new significant capacity expected in

Europe over the next 2-3 years with 3 potential new

machines that could come on stream from 2021 on:

○ SCA Obbola (400kt)

○ Stora Enso Oulu (400kt)

○ Ilim Ust Ilimsk (400kt) – mostly destined for Chinese

market

Kraftliner1 deliveries to Europe2 (CEPI)

Stora Varkausstartup

Supply limitations

643695

776

844

1,053

921

642584

493446

387 375405

380

535

655602

867

953

837

732

803 801 811777

514

0.920.90

0.94

1.13

1.24 1.25 1.26

1.37

1.47

1.391.33

1.39

1.291.33 1.33

1.11 1.11 1.131.19

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

0

200

400

600

800

1,000

1,200

1,400

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018AugYTD

EUR/USD

'000

TONNES

Historical development of US unbleached KL exports to Europe

Europe is a importer of unbleached kraftliner, predominantly from the US

Source: US Census, FX rates publicly available 19

- 4.2% (34 kt)

2017 US imports were lower than 2016, but in the range of recent years

1% of European demand

20

Drivers for containerboard growth 2013-2018

Containerboard market overview

Recycled containerboard

Kraft Top Liner

Kraftliner

White liners

Semi-chemical Fluting

White liners continue to grow in Europe

Source: CEPI Containerboard 21

+5.1%

+2.5%

+1.9%

+5.3%

+4.5%

+5.1%

White Rec. Liners WT Kraftliners Total Brown Grades

European white liners growth

2016 2017

White top kraftliner

5% White Recycled

Liners11%

Brown kraftliner

9%

Recycled containerboard

72%

Semi-chemical fluting

4%

European production per containerboard grade

Coated grades represent 10% of white top testliners and 23% of white top kraftliners.

22

Drivers for containerboard growth 2013-2018

Containerboard market overview

Recycled containerboard

Kraft Top Liner

Kraftliner

White liners

Semi-chemical Fluting

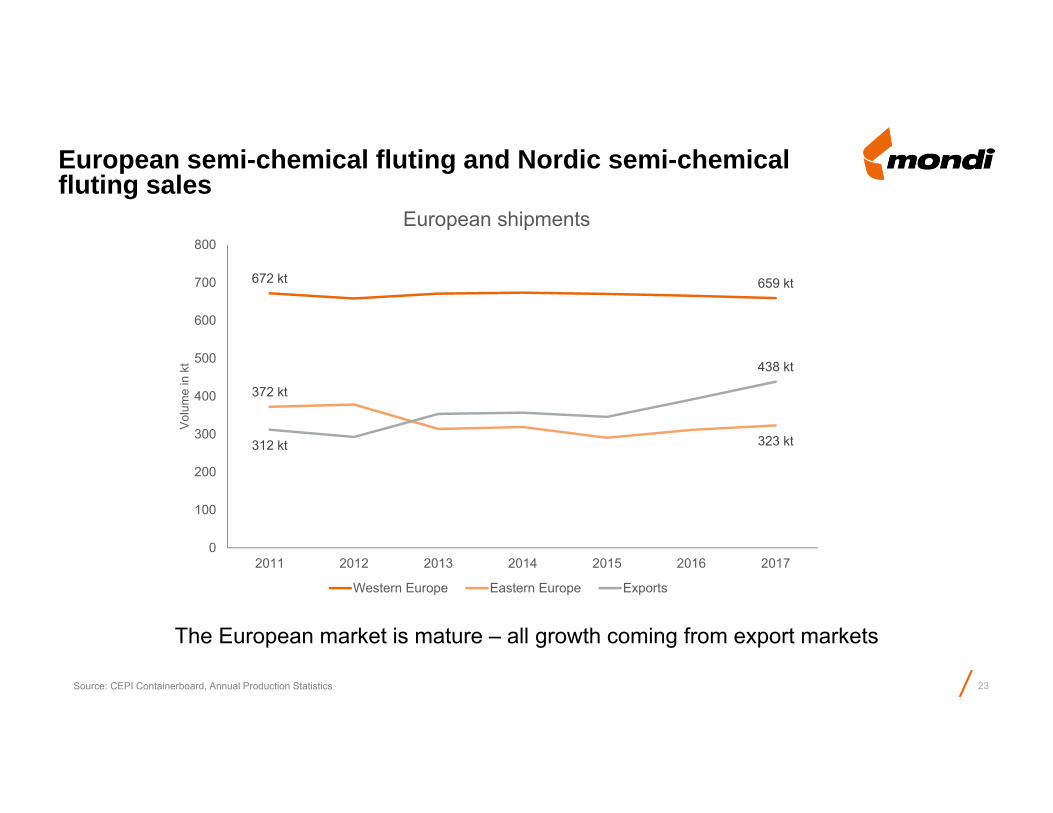

The European market is mature – all growth coming from export markets

European semi-chemical fluting and Nordic semi-chemical fluting sales

23Source: CEPI Containerboard, Annual Production Statistics

672 kt 659 kt

372 kt

323 kt312 kt

438 kt

0

100

200

300

400

500

600

700

800

2011 2012 2013 2014 2015 2016 2017

Vol

ume

in k

t

European shipments

Western Europe Eastern Europe Exports

Wrap Up

24

Recycled● Strong demand growth● Capacity in line with demand in med. term

Kraftliner● Smaller growth, no significant capacity in mid-term● Some meaningful projects under investigation

Trends and Demand Drivers

White Top linersSemi-chemical Fluting

● Growing market for white liners in Europe ● Stable market for semi-chemical fluting in Europe● Continuous potential for exports globally based on high

quality

● Strong economy● Strong growth in Eastern Europe● E-commerce● China ● Plastic ban and demand for paper based solutions

25

Market position sources and definitions

Europe – Europe including Russia and Turkey

Emerging Europe – Albania, Armenia, Azerbaijan, Belarus, Bosnia and Herzegovina, Bulgaria, Croatia, Cyprus, Czech Republic, Estonia, Georgia, Hungary, Latvia, Lithuania, Macedonia, Malta, Moldova, Montenegro, Poland, Romania, Serbia, Slovakia, Slovenia, Turkey, Ukraine

North America – Canada, Mexico, USA

Virgin containerboard (Europe) and Containerboard (emerging Europe) based on capacity (including kraft top liner) – Source: RISI European Paper Packaging Capacity Report and Mondi estimates

Kraft paper (Global) based on capacity – Source: RISI European Paper Packaging Capacity Report, RISI Mill Asset Database, Pöyry Smart Terminal Service and Mondi estimates

Corrugated packaging (emerging Europe) based on production – Source: Henry Poole Consulting and Mondi estimates

Industrial bags (Global) based on sales volume – Source: Eurosac, Freedonia World Industrial Bags 2016 study and Mondi estimates

Consumer flexible packaging (Europe) based on sales – Source: PCI Wood Mackenzie – Flexible Packaging, European Supply/Demand report, 2017

Commercial release liner (Europe) based on sales volumes – Source: AWA European Release Liner Market Study and Mondi estimates

Uncoated Fine Paper (Europe) based on sales volumes (Ilim JV considered separate from IP) – Source: Euro-Graph delivery statistics, EMGE WoodfreeForecast, EMGE World Graphic Papers, RISI Mill Asset Database, Eastconsult and Mondi estimates

Uncoated Fine Paper (South Africa) based on Mondi estimates

Mondi region definitions

Sources for market position estimates

Forward-looking statements disclaimer

This document includes forward-looking statements. All statements other than statements of historical facts included herein, including, without limitation, those regarding Mondi’s financial position, business strategy, market growth and developments, expectations of growth and profitability and plans and objectives of management for future operations, are forward-looking statements. Forward-looking statements are sometimes identified by the use of forward-looking terminology such as ‘believe’, ‘expects’, ‘may’, ‘will’, ‘could’, ‘should’, ‘shall’, ‘risk’, ‘intends’, ‘estimates’, ‘aims’, ‘plans’, ‘predicts’, ‘continues’, ‘assumes’, ‘positioned’ or ‘anticipates’ or the negative thereof, other variations thereon or comparable terminology. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Mondi, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements and other statements contained in this document regarding matters that are not historical facts involve predictions and are based on numerous assumptions regarding Mondi’s present and future business strategies and the environment in which Mondi will operate in the future. These forward-looking statements speak only as of the date on which they are made.

No assurance can be given that such future results will be achieved; various factors could cause actual future results, performance or events to differ materially from those described in these statements. Such factors include in particular but without any limitation: (1) operating factors, such as continued success of manufacturing activities and the achievement of efficiencies therein, continued success of product development plans and targets, changes in the degree of protection created by Mondi’s patents and other intellectual property rights and the availability of capital on acceptable terms; (2) industry conditions, such as strength of product demand, intensity of competition, prevailing and future global market prices for Mondi’s products and raw materials and the pricing pressures thereto, financial condition of the customers, suppliers and the competitors of Mondi and potential introduction of competing products and technologies by competitors; and (3) general economic conditions, such as rates of economic growth in Mondi’s principal geographical markets or fluctuations of exchange rates and interest rates.

Mondi expressly disclaims

a) any warranty or liability as to accuracy or completeness of the information provided herein; and

b) any obligation or undertaking to review or confirm analysts’ expectations or estimates or to update any forward-looking statements to reflect any change in Mondi’s expectations or any events that occur or circumstances that arise after the date of making any forward-looking statements,

unless required to do so by applicable law or any regulatory body applicable to Mondi, including the JSE Limited and the LSE.

26