risk management adequacy

TRANSCRIPT

RISK MANAGEMENTAND CAPITALADEQUACY

Gallati_fm_1p_j.qxd 2/27/03 9:15 AM Page i

This page intentionally left blank.

RISK MANAGEMENTAND CAPITALADEQUACY

RETO R. GALLATI

McGraw-HillNew York / Chicago / San Francisco / Lisbon

London / Madrid / Mexico City / Milan / New Delhi

San Juan / Singapore / Sydney / Toronto

Gallati_fm_1p_j.qxd 2/27/03 9:15 AM Page iii

Copyright © 2003 by The McGraw-Hill Companies, Inc. All rights reserved. Manufactured in theUnited States of America. Except as permitted under the United States Copyright Act of 1976, no partof this publication may be reproduced or distributed in any form or by any means, or stored in a data-base or retrieval system, without the prior written permission of the publisher.

0-07-142558-6

The material in this eBook also appears in the print version of this title: 0-07-140763-4.

All trademarks are trademarks of their respective owners. Rather than put a trademark symbol afterevery occurrence of a trademarked name, we use names in an editorial fashion only, and to the benefitof the trademark owner, with no intention of infringement of the trademark. Where such designationsappear in this book, they have been printed with initial caps.

McGraw-Hill eBooks are available at special quantity discounts to use as premiums and sales pro-motions, or for use in corporate training programs. For more information, please contact GeorgeHoare, Special Sales, at [email protected] or (212) 904-4069.

TERMS OF USEThis is a copyrighted work and The McGraw-Hill Companies, Inc. (“McGraw-Hill”) and its licensorsreserve all rights in and to the work. Use of this work is subject to these terms. Except as permittedunder the Copyright Act of 1976 and the right to store and retrieve one copy of the work, you may notdecompile, disassemble, reverse engineer, reproduce, modify, create derivative works based upon,transmit, distribute, disseminate, sell, publish or sublicense the work or any part of it withoutMcGraw-Hill’s prior consent. You may use the work for your own noncommercial and personal use;any other use of the work is strictly prohibited. Your right to use the work may be terminated if youfail to comply with these terms.

THE WORK IS PROVIDED “AS IS”. McGRAW-HILL AND ITS LICENSORS MAKE NO GUAR-ANTEES OR WARRANTIES AS TO THE ACCURACY, ADEQUACY OR COMPLETENESS OFOR RESULTS TO BE OBTAINED FROM USING THE WORK, INCLUDING ANY INFORMA-TION THAT CAN BE ACCESSED THROUGH THE WORK VIA HYPERLINK OR OTHERWISE,AND EXPRESSLY DISCLAIM ANY WARRANTY, EXPRESS OR IMPLIED, INCLUDING BUTNOT LIMITED TO IMPLIED WARRANTIES OF MERCHANTABILITY OR FITNESS FOR APARTICULAR PURPOSE. McGraw-Hill and its licensors do not warrant or guarantee that the func-tions contained in the work will meet your requirements or that its operation will be uninterrupted orerror free. Neither McGraw-Hill nor its licensors shall be liable to you or anyone else for any inac-curacy, error or omission, regardless of cause, in the work or for any damages resulting therefrom.McGraw-Hill has no responsibility for the content of any information accessed through the work.Under no circumstances shall McGraw-Hill and/or its licensors be liable for any indirect, incidental,special, punitive, consequential or similar damages that result from the use of or inability to use thework, even if any of them has been advised of the possibility of such damages. This limitation of lia-bility shall apply to any claim or cause whatsoever whether such claim or cause arises in contract, tortor otherwise.

DOI: 10.1036/0071425586

ebook_copyright 7x9.qxd 7/23/03 10:53 AM Page 1

When I was young, people called me a gambler. As thescale of my operations increased I became known as aspeculator. Now I am called a banker. But I have beendoing the same thing all the time.

—Sir Ernest CassellBanker to Edward VII

Gallati_fm_1p_j.qxd 2/27/03 9:15 AM Page v

This page intentionally left blank.

To my parents with love and gratitude

Gallati_fm_1p_j.qxd 2/27/03 9:15 AM Page vii

A C K N O W L E D G M E N T S

The suggestion that I write a book about risk came from the late FischerBlack, while I was working at Goldman Sachs. The vastness of the projectis daunting. The topic touches on the most profound depths of statistics,mathematics, psychology, and economics. I would like to thank the editorsand reviewers and those who provided comments, especially M.R. Careyand Jean Eske, who carefully read the entire manuscript and providedvaluable comments, corrections, and advice.

I end with a note of thanks to my family, my friends, and my facultycolleagues at Sloan, who inspired much of the enthusiasm that went intothe creation of this book and endured me with patience.

RETO R. GALLATI

Cambridge, MassachusettsFebruary 2003

Gallati_fm_1p_j.qxd 2/28/03 2:10 PM Page viii

Copyright 2003 by The McGraw-Hill Companies, Inc. Click Here for Terms of Use.

C O N T E N T S

ACKNOWLEDGMENTS viii

INTRODUCTION xvii

Chapter 1

Risk Management: A Maturing Discipline 1

1.1 Background 11.2 Risks: A View of the Past Decades 51.3 Definition of Risk 71.4 Related Terms and Differentiation 81.5 Degree of Risk 101.6 Risk Management: A Multilayered Term 11

1.6.1 Background 111.6.2 History of Modern Risk Management 111.6.3 Related Approaches 131.6.4 Approach and Risk Maps 22

1.7 Systemic Risk 221.7.1 Definition 221.7.2 Causes of Systemic Risk 261.7.3 Factors That Support Systemic Risk 261.7.4 Regulatory Mechanisms for Risk Management 27

1.8 Summary 281.9 Notes 30

Chapter 2

Market Risk 33

2.1 Background 332.2 Definition of Market Risk 342.3 Conceptual Approaches for Modeling Market Risk 372.4 Modern Portfolio Theory 39

2.4.1 The Capital Asset Pricing Model 412.4.2 The Security Market Line 43

ix

Gallati_fm_1p_j.qxd 2/28/03 2:10 PM Page ix

For more information about this title, click here.

Copyright 2003 by The McGraw-Hill Companies, Inc. Click Here for Terms of Use.

2.4.3 Modified Form of CAPM by Black, Jensen, and Scholes 452.4.4 Arbitrage Pricing Theory 462.4.5 Approaches to Option Pricing 47

2.5 Regulatory Initiatives for Market Risks and Value at Risk 542.5.1 Development of an International Framework

for Risk Regulation 562.5.2 Framework of the 1988 BIS Capital Adequacy Calculation 562.5.3 Criticisms of the 1988 Approach 582.5.4 Evolution of the 1996 Amendment on Market Risks 58

2.6 Amendment to the Capital Accord to Incorporate Market Risks 602.6.1 Scope and Coverage of Capital Charges 602.6.2 Countable Capital Components 612.6.3 The de Minimis Rule 62

2.7 The Standardized Measurement Method 622.7.1 General and Specific Risks for Equity- and

Interest-Rate-Sensitive Instruments 652.7.2 Interest-Rate Risks 662.7.3 Equity Position Risk 792.7.4 Foreign-Exchange Risk 832.7.5 Commodities Risk 842.7.6 Treatment of Options 882.7.7 Criticisms of the Standard Approach 94

2.8 The Internal Model Approach 952.8.1 Conditions for and Process of Granting Approval 952.8.2 VaR-Based Components and Multiplication Factor 972.8.3 Requirement for Specific Risks 982.8.4 Combination of Model-Based and Standard Approaches 982.8.5 Specification of Market Risk Factors to Be Captured 992.8.6 Minimum Quantitative Requirements 1012.8.7 Minimum Qualitative Requirements 102

2.9 The Precommitment Model 1072.10 Comparison of Approaches 1082.11 Revision and Modification of the Basel Accord

on Market Risks 1092.11.1 The E.U. Capital Adequacy Directive 1092.11.2 New Capital Adequacy Framework to Replace

the 1988 Accord 110

x Contents

Gallati_fm_1p_j.qxd 2/27/03 9:15 AM Page x

2.12 Regulation of Nonbanks 1102.12.1 Pension Funds 1112.12.2 Insurance Companies 1112.12.3 Securities Firms 1122.12.4 The Trend Toward Risk-Based Disclosures 1132.12.5 Disclosure Requirements 1132.12.6 Encouraged Disclosures 114

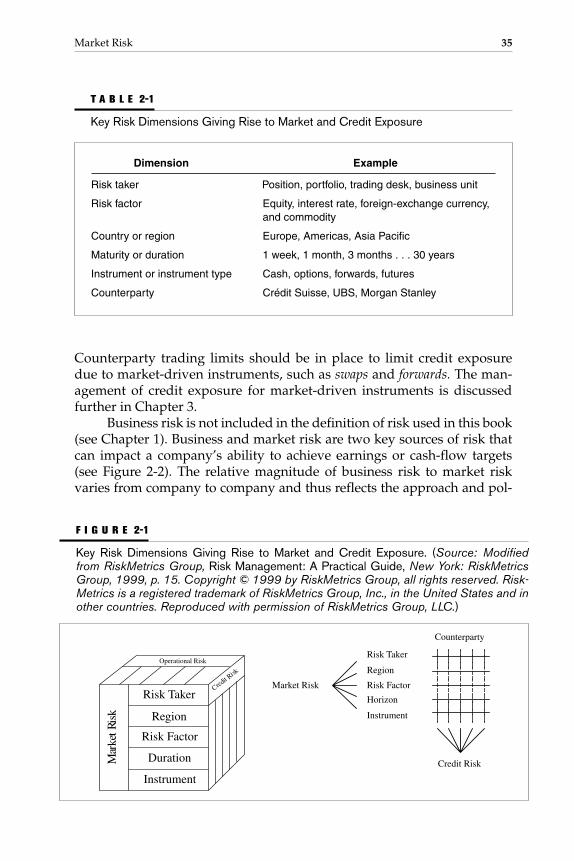

2.13 Market Instruments and Credit Risks 1142.14 Summary 1162.15 Notes 117

Chapter 3

Credit Risk 129

3.1 Background 1293.2 Definition 1303.3 Current Credit Risk Regulations 1303.4 Deficiencies of the Current Regulations 1313.5 Deficiencies of the Current Conceptual Approaches

for Modeling Credit Risk 1333.6 Conceptual Approaches for Modeling Credit Risk 135

3.6.1 Transaction and Portfolio Management 1363.6.2 Measuring Transaction Risk–Adjusted Profitability 140

3.7 Measuring Credit Risk for Credit Portfolios 1403.7.1 Economic Capital Allocation 1413.7.2 Choice of Time Horizon 1463.7.3 Credit Loss Measurement Definition 1463.7.4 Risk Aggregation 149

3.8 Development of New Approaches to Credit Risk Management 1503.8.1 Background 1513.8.2 BIS Risk-Based Capital Requirement Framework 1523.8.3 Traditional Credit Risk Management Approaches 1543.8.4 Option Theory, Credit Risk, and the KMV Model 1593.8.5 J. P. Morgan’s CreditMetrics and Other VaR

Approaches 1673.8.6 The McKinsey Model and Other

Macrosimulation Models 178

Contents xi

Gallati_fm_1p_j.qxd 2/27/03 9:15 AM Page xi

3.8.7 KPMG’s Loan Analysis System and Other Risk-Neutral Valuation Approaches 183

3.8.8 The CSFB CreditRisk+ Model 1903.8.9 CSFB’s CreditRisk+ Approach 1933.8.10 Summary and Comparison of New Internal

Model Approaches 1973.9 Modern Portfolio Theory and Its Application

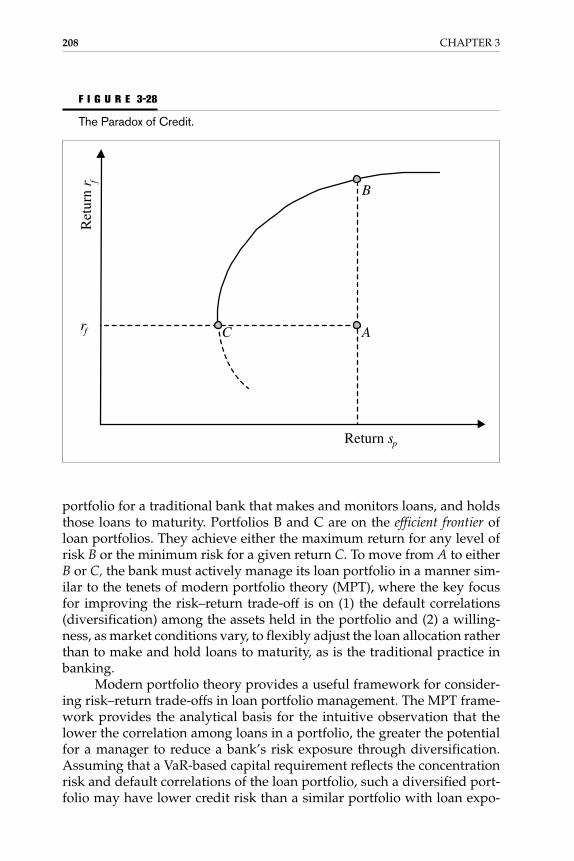

to Loan Portfolios 2053.9.1 Background 2053.9.2 Application to Nontraded Bonds and Credits 2083.9.3 Nonnormal Returns 2093.9.4 Unobservable Returns 2093.9.5 Unobservable Correlations 2093.9.6 Modeling Risk–Return Trade-off of Loans

and Loan Portfolios 2093.9.7 Differences in Credit Versus Market Risk Models 225

3.10 Backtesting and Stress Testing Credit Risk Models 2263.10.1 Background 2263.10.2 Credit Risk Models and Backtesting 2273.10.3 Stress Testing Based on Time-Series Versus

Cross-Sectional Approaches 2283.11 Products with Inherent Credit Risks 229

3.11.1 Credit Lines 2293.11.2 Secured Loans 2313.11.3 Money Market Instruments 2333.11.4 Futures Contracts 2373.11.5 Options 2403.11.6 Forward Rate Agreements 2433.11.7 Asset-Backed Securities 2453.11.8 Interest-Rate Swaps 247

3.12 Proposal for a Modern Capital Accord for Credit Risk 2503.12.1 Institute of International Finance 2513.12.2 International Swaps and Derivatives Association 2523.12.3 Basel Committee on Banking Supervision

and the New Capital Accord 2533.13 Summary 2633.14 Notes 265

xii Contents

Gallati_fm_1p_j.qxd 2/27/03 9:15 AM Page xii

Chapter 4

Operational Risk 283

4.1 Background 2834.2 Increasing Focus on Operational Risk 285

4.2.1 Drivers of Operational Risk Management 2864.2.2 Operational Risk and Shareholder Value 288

4.3 Definition of Operational Risk 2894.4 Regulatory Understanding of Operational Risk Definition 2934.5 Enforcement of Operational Risk Management 2964.6 Evolution of Operational Risk Initiatives 2994.7 Measurement of Operational Risk 3024.8 Core Elements of an Operational Risk Management Process 3034.9 Alternative Operational Risk Management Approaches 304

4.9.1 Top-Down Approaches 3054.9.2 Bottom-Up Approaches 3144.9.3 Top-Down vs. Bottom-Up Approaches 3194.9.4 The Emerging Operational Risk Discussion 321

4.10 Capital Issues from the Regulatory Perspective 3214.11 Capital Adequacy Issues from an Industry Perspective 324

4.11.1 Measurement Techniques and Progress in the Industry Today 327

4.11.2 Regulatory Framework for Operational Risk Overview Under the New Capital Accord 330

4.11.3 Operational Risk Standards 3354.11.4 Possible Role of Bank Supervisors 336

4.12 Summary and Conclusion 3374.13 Notes 338

Chapter 5

Building Blocks for Integration of Risk Categories 341

5.1 Background 3415.2 The New Basel Capital Accord 342

5.2.1 Background 3425.2.2 Existing Framework 3435.2.3 Impact of the 1988 Accord 3455.2.4 The June 1999 Proposal 3465.2.5 Potential Modifications to the Committee’s Proposals 348

Contents xiii

Gallati_fm_1p_j.qxd 2/27/03 9:15 AM Page xiii

5.3 Structure of the New Accord and Impact on Risk Management 3525.3.1 Pillar I: Minimum Capital Requirement 3525.3.2 Pillar II: Supervisory Review Process 3535.3.3 Pillar III: Market Discipline and General

Disclosure Requirements 3545.4 Value at Risk and Regulatory Capital Requirement 356

5.4.1 Background 3565.4.2 Historical Development of VaR 3575.4.3 VaR and Modern Financial Management 3595.4.4 Definition of VaR 364

5.5 Conceptual Overview of Risk Methodologies 3665.6 Limitations of VaR 368

5.6.1 Parameters for VaR Analysis 3685.6.2 Different Approaches to Measuring VaR 3735.6.3 Historical Simulation Method 3805.6.4 Stress Testing 3825.6.5 Summary of Stress Tests 389

5.7 Portfolio Risk 3895.7.1 Portfolio VaR 3905.7.2 Incremental VaR 3935.7.3 Alternative Covariance Matrix Approaches 395

5.8 Pitfalls in the Application and Interpretation of VaR 4045.8.1 Event and Stability Risks 4055.8.2 Transition Risk 4065.8.3 Changing Holdings 4065.8.4 Problem Positions 4065.8.5 Model Risks 4075.8.6 Strategic Risks 4095.8.7 Time Aggregation 4095.8.8 Predicting Volatility and Correlations 4145.8.9 Modeling Time-Varying Risk 4155.8.10 The RiskMetrics Approach 4235.8.11 Modeling Correlations 427

5.9 Liquidity Risk 4315.10 Summary 4365.11 Notes 437

xiv Contents

Gallati_fm_1p_j.qxd 2/27/03 9:15 AM Page xiv

Chapter 6

Case Studies 441

6.1 Structure of Studies 4416.2 Overview of Cases 4416.3 Metallgesellschaft 445

6.3.1 Background 4456.3.2 Cause 4486.3.3 Risk Areas Affected 457

6.4 Sumitomo 4616.4.1 Background 4616.4.2 Cause 4616.4.3 Effect 4646.4.4 Risk Areas Affected 464

6.5 LTCM 4666.5.1 Background 4666.5.2 Cause 4686.5.3 Effect 4726.5.4 Risk Areas Affected 473

6.6 Barings 4796.6.1 Background 4796.6.2 Cause 4806.6.3 Effect 4856.6.4 Risk Areas Affected 486

6.7 Notes 490

GLOSSARY 495

BIBLIOGRAPHY 519

INDEX 539

Contents xv

Gallati_fm_1p_j.qxd 2/27/03 9:15 AM Page xv

This page intentionally left blank.

I N T R O D U C T I O N

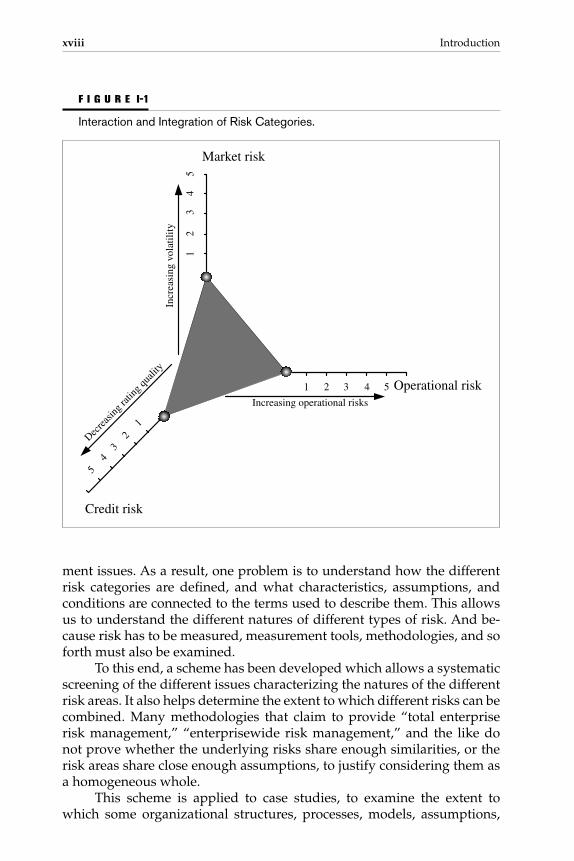

Over the past decades, investors, regulators, and industry self-regulatorybodies have forced banks, other financial institutions, and insurance com-panies to develop organizational structures and processes for the manage-ment of credit, market, and operational risk. Risk management became a hottopic for many institutions, as a means of increasing shareholder value anddemonstrating the willingness and capability of top management to handlethis issue. In most financial organizations, risk management is mainly un-derstood as the job area of the chief risk officer and is limited, for the mostpart, to market risks. The credit risk officer usually takes care of credit riskissues. Both areas are supervised at the board level by separate competenceand reporting lines and separate directives. More and more instruments,strategies, and structured services have combined the profile characteristicsof credit and market risk, but most management concepts treat the differentparts of risk management separately. Only a few institutions have started todevelop an overall risk management approach, with the aim of quantifyingthe overall risk exposures of the company (Figure I-1).

This book presents an inventory of the different approaches to market,credit and, operational risk. The following chapters provide an in-depthanalysis of how the different risk areas diverge regarding methodologies,assumptions, and conditions. The book also discusses how the different ap-proaches can be identified and measured, and how their various parts con-tribute to the discipline of risk management as a whole. The closing chapterprovides case studies showing the relevance of the different risk categoriesand discusses the “crash-testing” of regulatory rules through their applica-tion to various crises and accidents.

The objective of this book is to demonstrate the extent to which theserisk areas can be combined from a management standpoint, and to whichsome of the methodologies and approaches are or are not reasonable foreconomic, regulatory, or other purposes.

PROBLEMS AND OBJECTIVES

Most institutions treat market, credit, operational, and systemic risk asseparate management issues, which are therefore managed through sepa-rate competence directives and reporting lines. With the increased com-plexity and speed of events, regulators have implemented more and moreregulations regarding how to measure, report, and disclose risk manage-

xvii

Gallati_fm_1p_j.qxd 2/27/03 9:15 AM Page xvii

Copyright 2003 by The McGraw-Hill Companies, Inc. Click Here for Terms of Use.

ment issues. As a result, one problem is to understand how the differentrisk categories are defined, and what characteristics, assumptions, andconditions are connected to the terms used to describe them. This allowsus to understand the different natures of different types of risk. And be-cause risk has to be measured, measurement tools, methodologies, and soforth must also be examined.

To this end, a scheme has been developed which allows a systematicscreening of the different issues characterizing the natures of the differentrisk areas. It also helps determine the extent to which different risks can becombined. Many methodologies that claim to provide “total enterpriserisk management,” “enterprisewide risk management,” and the like donot prove whether the underlying risks share enough similarities, or therisk areas share close enough assumptions, to justify considering them asa homogeneous whole.

This scheme is applied to case studies, to examine the extent towhich some organizational structures, processes, models, assumptions,

xviii Introduction

5

4

3

2

1

1

2

3

4

5

1 2 3 4 5

Credit risk

Market risk

Operational risk

Decrea

sing r

ating

quali

ty

Incr

easi

ng v

olat

ility

Increasing operational risks

F I G U R E I-1

Interaction and Integration of Risk Categories.

Gallati_fm_1p_j.qxd 2/27/03 9:15 AM Page xviii

methodologies, and so forth have proved applicable, and the extent of theserious financial, reputational, and sometimes existential damages thathave resulted when they have not.

APPROACH

This work focuses on the level above the financial instruments and is in-tended to add value at the organization, transaction, and process levels soas to increase the store of knowledge already accumulated. The pricing ofinstruments and the valuation of portfolios are not the primary objects ofthis book. Substantial knowledge has already been developed in this areaand is in continuous development. Risk management at the instrumentlevel is an essential basis for understanding how to make an institution’srisk management structures, processes, and organizations efficient and effective.

This book aims to develop a scheme or structure to screen and com-pare the different risk areas. This scheme must be structured in such a way that it considers the appropriateness and usefulness of the differentmethodologies, assumptions, and conditions for economic and regulatorypurposes.

The objectives of this book are as follows:• Define the main terms used for the setup of the scheme, such as

systemic, market, credit, and operational risk.• Review the methodologies, assumptions, and conditions

connected to these terms.• Structure the characteristics of the different risk areas in such a

way that the screening of these risk areas allows comparison ofthe different risk areas for economic and regulatory purposes.

In a subsequent step, this scheme is applied to a selection of casestudies. These are mainly publicized banking failures from the past decadeor so. The structured analysis of these relevant case studies should demon-strate the major causes and effects of each loss and the extent to which riskcontrol measures were or were not appropriate and effective.

The objectives of the case study analyses are as follows:• Highlight past loss experiences.• Detail previous losses in terms of systemic, market, credit, and

operational risks.• Highlight the impact of the losses.• Provide practical assistance in the development of improved risk

management through knowledge transfer and managementinformation.

• Generate future risk management indicators to mitigate thepotential likelihood of such disasters.

Introduction xix

Gallati_fm_1p_j.qxd 2/27/03 9:15 AM Page xix

This page intentionally left blank.

C H A P T E R 1

Risk Management: A Maturing Discipline

1.1 BACKGROUND

The entire history of human society is a chronology of exposure to risksof all kinds and human efforts to deal with those risks. From the firstemergence of the species Homo sapiens, our ancestors practiced risk man-agement in order to survive, not only as individuals but as a species. Thesurvival instinct drove humans to avoid the risks that threatened extinc-tion and strive for security. Our actual physical existence is proof of ourancestors’ success in applying risk management strategies.

Originally, our ancestors faced the same risks as other animals: thehazardous environment, weather, starvation, and the threat of beinghunted by predators that were stronger and faster than humans. The en-vironment was one of continuous peril, with chronic hunger and danger,and we can only speculate how hard it must have been to achieve a sem-blance of security in such a threatening world.

In response to risk, our early ancestors learned to avoid dangerousareas and situations. However, their instinctive reactions to risk and theiradaptive behavior do not adequately answer our questions about how theysuccessfully managed the different risks they faced. Other hominids did notattain the ultimate goal of survival—including H. sapiens neanderthalensis,despite the fact that they were larger and stronger than modern humans.The modern humans, H. sapiens sapiens, not only survived all their relativesbut proved more resilient and excelled in adaptation and risk management.

Figure 1-1 shows the threats that humans have been exposed to overthe ages, and which probably will continue in the next century, as well. Itis obvious that these threats have shifted from the individual to society

1

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 1

Copyright 2003 by The McGraw-Hill Companies, Inc. Click Here for Terms of Use.

2

1800 1900 20001700Middle Ages0Stone Age

Indi

vidu

alG

roup

Nat

ion

Wor

ld

Slavery, violations of human rights

Robbery, tyranny

Hunger

Diseases, epidemics

Local wars

Life at subsistence level

Lack of work

Threats to social security

Economic underdevelopment

Wars on national level

Atomic threat

Overpopulation

Exhaustion of nonrenewable energy

Environmental destruction

F I G U R E 1-1

Development of the Threats to Individuals, Groups, Nations, and the World.

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 2

and the global community. Thousands of years ago, humans first learnedto cultivate the wild herbs, grasses, grains, and roots that they had tradi-tionally gathered. Concurrently, humans were creating the first settle-ments and domesticating wild animals. Next, humans began to grow,harvest, and stockpile grain, which helped to form the concept of owner-ship. Over time, humans learned to defend their possessions and their in-terests, to accumulate foodstuffs and other goods for the future, and tolive together in tribal and other communal settings. As wealth accumu-lated in modest increments, rules about how to live together were needed,and the first laws to govern human interaction were developed. Thus, thebeginning of civilization was launched. Walled cities, fortifications, andother measures to protect property and communities demonstrate thatwith increases in wealth came increased risk in a new form. Old forms,which had threatened humans for generations, were replaced by newthreats. Famine and pestilence were frequent crises, and the perils of na-ture destroyed what communities and individuals had built. Warfare andplundering increased the threats. As a result, our ancestors created tech-nologies, war strategies, and social and legal rules to survive.

The evolution of business risks coincides with the start of trading andcommerce. We do not know exactly when trading and commerce began,but their rise is clearly connected with the fact that society took advantageof specialization, which increased the capacity to produce and stockpilegoods for future use. Stockpiling goods acts as a cushion against misfor-tune, the perils of nature, and the ravages of war. It is very probable thatbusiness, in the form of trading and commerce, was one of the first activeefforts of society to deal with risk. Artifacts unearthed by archaeologistsprove that those early businesspeople developed techniques for dealingwith risk. Two major techniques are noteworthy and should be mentioned.

First, in 3000 B.C., the Babylonian civilization, with its extensive traderelations, exhibited a highly developed bureaucracy and trading sectorwith a monetary and legal system.

One consequence of the concept of private property was the evolu-tion of a market economy, but until the innovation of money was intro-duced, commerce was on a barter basis. There is some debate regardingthe exact moment when money was first used, but its use revolutionizedcommerce, private property, and the accumulation of wealth. It pro-vided a new means of stockpiling resources, and thus had an importantimpact on risk management. With the introduction of money as a storagemedium, wealth could be held in the form of tangible property or as anasset that could be exchanged for tangible properties. Physical assetscould be acquired even by those who did not have financial assets, pro-vided someone was willing to lend the money, which was the innovationof credit. This created risk for the lender, who was compensated bycharging interest for loans.

Risk Management: A Maturing Discipline 3

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 3

The legal system was the second innovation that revolutionized soci-ety. Laws or rules originated as tribal conventions, which became more for-malized over time. One of the first formal legal codes was established byHammurabi between 1792 and 1750 B.C. There were no other major legal sys-tem innovations until the beginning of the Industrial Revolution, so we canfly over the periods of the Egyptian, Greek, and Roman empires, feudalism,the rise of the merchant class, and mercantilism. The beginning of the In-dustrial Revolution was characterized by two major events. Modern capital-ism emerged after a transition period over several centuries, during whichthe conditions needed for a capitalistic market society were created. Amongthese conditions were formalized private ownership of the means of pro-duction, profit orientation, and the mechanisms of a market economy. Withexpanding industrial and economic activity, new organizational forms wereneeded to raise large amounts of capital and build production capacity. Thecorporation limited individual risk and leveraged production, distribution,and capital resources. The earliest form of shareholder organization, the jointstock company, appeared at the end of the seventeenth century. The investorspooled their funds, allowing multiple investors to share in both the profitsand risks of the enterprise. This feature was equivalent to partnerships andother joint forms and was not an innovation. But the corporation addressedrisk in a different way, by limiting the liability of the investors based on theamount invested. From a legal standpoint, a corporation is an artificial con-struct or artificial person, whose competencies and responsibilities are sepa-rate from those of the investor-owners (with exceptions).

The Industrial Revolution created new sources of risks. The applica-tion of steam power to the production process and transportation replacedold threats with the new risks that accompany advancing technologies.With the emergence of the age of information technology, inherent risksinclude business system problems, fraud, and privacy issues, which canall interrupt the day-to-day operations of a business.

Although the term risk management originated in the 1950s, HenryFayol recognized its significance earlier.1 Fayol, a leading managementauthority, was influenced by growing mass production in the UnitedStates, and the existence of giant corporations and their managementchallenges. In 1916, he structured industrial activities into six functions,including one called security, which sounds surprisingly like the conceptof risk management:

The purpose of this function is to safeguard property and persons againsttheft, fire and flood, to ward off strikes and felonies and broadly all socialdisturbances or natural disturbances liable to endanger the progress andeven the life of the business. It is the master’s eye, the watchdog of the one-man business, the police or the army in the case of the state. It is generallyspeaking all measures conferring security upon the undertaking and requi-site peace of mind upon the personnel.2

4 CHAPTER 1

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 4

Centuries ago, bandits and pirates threatened traders. Now hackersare engaged in vandalism and commit electronic larceny.

The media are full of news about the perils of human-made and nat-ural hazards. The nuclear power plant accidents at the Three Mile Islandfacility in Pennsylvania in 1979 and at Chernobyl in Ukraine in 1987 showthe new risks posed by human-made hazards and the seriousness of thesethreats. Destructive natural hazards exist as well. Hurricane Andrewcaused damages of around $22 billion; and the floods in the midwesternUnited States in 1993 and the earthquakes in California in 1993 and inKobe, Japan, in 1994 had devastating effects. In addition, terrorist activi-ties have become more dangerous over the years, as demonstrated by the1993 and 2001 bombings of the World Trade Center in New York, and the1995 bombing of the Murrah Federal Building in Oklahoma City.

A review of the past along with an assessment of the growing arrayof risks shows that the impact of risks (in terms of financial losses) has in-creased. This is not only a consequence of the increased numbers of riskswe are confronted with; the severity and frequency of disasters has in-creased as well. The financial losses from natural perils, such as floods,forest fires, and earthquakes, are not only a function of the number ofevents, as natural disasters occur with a certain average frequency as inthe past. However, each catastrophe seems to be worse than the one thatcame before it. The ultimate reason is obvious: as more and more peoplelive close together, business has become more capital intensive, and ourinfrastructure is more vulnerable and capital intensive as well. With theincreased growth of capital investment in infrastructure, manufacturingcapacity, and private ownership of real estate and other goods, the risk offinancial losses increased substantially.

1.2 RISKS: A VIEW OF THE PAST DECADES

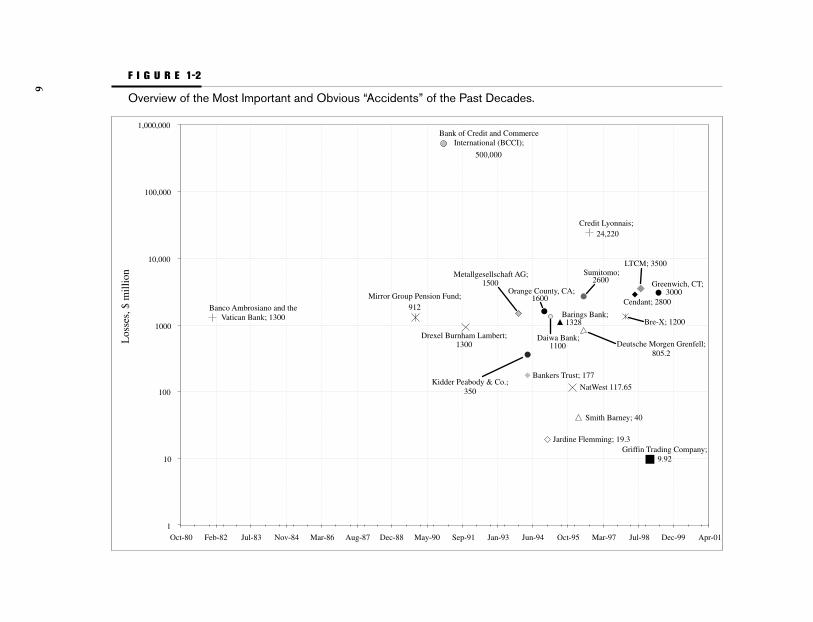

Recently, there have been a number of massive financial losses due to in-adequate risk management procedures and processes (Figure 1-2). The fail-ures of risk management in the world of finance were not primarily due tothe incorrect pricing of derivative instruments. Rather, the necessary su-pervisory oversight was inadequate. The decision makers in control of or-ganizations left them exposed to risks from derivative transactions andinstitutional money. Risk management does not primarily involve the cor-rect pricing of derivative instruments—rather, it involves the supervision,management, and control of organizational structures and processes that dealwith derivatives and other instruments.

Many cases in which managers focused on the correct pricing of financial instruments and neglected the other dimensions show the dramatic consequences of this one-dimensional understanding of riskmanagement. In Switzerland, the pension fund scheme of Landis & Gyr

Risk Management: A Maturing Discipline 5

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 5

6

Bankers Trust; 177

Jardine Flemming; 19.3

NatWest 117.65

Smith Barney; 40

24,220

3000

Griffin Trading Company;9.92

1300

500,000

912

1500

Kidder Peabody & Co.;350

Orange County, CA;

Bank of Credit and CommerceInternational (BCCI);

Banco Ambrosiano and theVatican Bank; 1300

Los

ses,

$ m

illio

n

Mirror Group Pension Fund;

Drexel Burnham Lambert;

Credit Lyonnais;

Metallgesellschaft AG;

1600

Barings Bank;1328

Daiwa Bank; 1100

Sumitomo;LTCM; 3500

2600

Deutsche Morgen Grenfell;805.2

Bre-X; 1200

Cendant; 2800

Greenwich, CT;

1

10

100

1000

10,000

100,000

1,000,000

Oct-80 Feb-82 Jul-83 Nov-84 Mar-86 Aug-87 Dec-88 May-90 Sep-91 Jan-93 Jun-94 Oct-95 Mar-97 Jul-98 Dec-99 Apr-01

F I G U R E 1-2

Overview of the Most Important and Obvious “Accidents” of the Past Decades.

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 6

resulted in the loss of a substantial part of the fund’s assets. RobertMaxwell swindled the Mirror Group’s pension fund for £480 million.Daiwa lost more than $1 billion. Barings lost £850 million. KidderPeabody lost more than $300 million. Orange County, California, lostmore than $1 billion. This list of accidents, frauds, and willful swindlesin the world of finance is never-ending. The reasons include behavioralrisk, pricing risk, an incorrect understanding of products and services,and simple credit and market risks. Risk is not a one-dimensional, well-defined concept. Rather, it is a shifting concept whose meaning variesaccording to the environment in which it is used. Thus far, the term riskhas been used in this discussion to mean “exposure to adversity.” In thisloose sense, the term risk has been adequate for the explanation of thehistory of risk. Now, risk and its associated terms have to be analyzedand defined more precisely, and the context in which these terms areused must be outlined. Each activity or area of knowledge has its ownindividual concept and terms. The terminology of risk, like many simpleterms in everyday usage, takes on different meanings in specializedfields. The term risk shimmers with all the colors of the rainbow; it de-pends on how we define it. Risk is often linked with uncertainty and in-security. Statisticians, economists, bankers, and academicians try and tryagain to develop a common understanding and definition of the termrisk. But at present there is no agreed definition that can be applied to allareas; the concept of risk that is suitable for the economist can not beused by the social psychologist or the insurance mathematician. Thisbook does not attempt to develop a concept for all areas of knowledge.The discussion is limited to economics and finance. However, there aresome concepts that are shared with the fields of insurance, mathematics,and statistics, as many products and services in the economic and finan-cial field are based on calculations that include risk. In the insurance in-dustry, risk means either a peril insured against (e.g., flood damage) or aperson or property protected by insurance (e.g., a driver and vehicleprotected against financial damages from personal injury or collision bycar insurance). For the moment, however, the term risk will be appliedhere in an abstract way, to indicate a situation in which a certain expo-sure exists. Therefore, risk is not strictly related to loss for present pur-poses, as this again would be one-dimensional and would unnecessarilyrestrict the discussion.

1.3 DEFINITION OF RISK

For the purposes of this discussion, risk is defined as “a condition in whichthere exists an exposure to adversity.” In addition, there is an expectationof what the outcome should look like. Therefore, risk is defined here asfollows:

Risk Management: A Maturing Discipline 7

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 7

risk A condition in which there exists a possibility of deviation from a desiredoutcome that is expected or hoped for.

Other definitions include the restriction that risk is based on real-world events, including a combination of circumstances in the external en-vironment. We do not agree with this limitation. Potential risks that mightoccur in the future are excluded. In addition, we do not limit the range ofrisk to circumstances in the external environment. Many crises in theeconomy and the financial services industry happen because of problemswithin organizations. These often have to do with problems in the humanresource area, which belong in the realm of the behavioral sciences.

The term risk is linked to the possibility of deviation. This means thatthe possibility of risk can be expressed as a probability, ranging from 0 to100 percent. Therefore, the probability is neither impossible nor definite.This definition does not require that the probability be quantified, onlythat it must exist. The degree of risk may not be measurable, for whateverreason, but the probability of the adverse outcome must be between 0 and100 percent.

Another key element of the definition is the “deviation from a de-sired outcome that is expected or hoped for.” The definition does not sayhow such an undesirable deviation is defined. There are many ways ofbuilding expectations. By projecting historical data into the future, webuild expectations. This pattern of behavior can be observed in our every-day lives. Another way of building expectations is to forecast by using in-formation directed toward the future, not by looking back. The definitionof expectations is absolutely key in the concept of risk, as it is used to definethe benchmark. Any misconception of the expectations will distort themeasurement of risk substantially. This issue is discussed in full in the au-diting and consulting literature, which analyzes the problem of risk andcontrol in great depth.3

Many definitions of risk include the term adverse deviation to expressthe negative dimension of the expected or hoped-for outcome. We do notagree with this limitation, which implies that risk exists only with adversedeviations, which must be negative and thus are linked to losses. Such arestriction would implicitly exclude any positive connotations from theconcept of risk. We believe that risk has two sides, which both have to beincluded in the definition, and that risk itself has no dimension, negativeor positive.

1.4 RELATED TERMS AND DIFFERENTIATION

Frequently, terms such as peril, hazard, danger, and jeopardy are used inter-changeably with each other and with the term risk. But to be more preciseabout risk, it is useful to distinguish these terms:

8 CHAPTER 1

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 8

• Peril. A peril creates the potential for loss. Perils include floods,fire, hail, and so forth. Peril is a common term to define a dangerresulting from a natural phenomenon. Each of the eventsmentioned is a potential cause of loss.

• Hazard. A hazard is a condition that may create or increase thechance of a loss arising from a given peril. It is possible forsomething to be both a peril and a hazard at the same time. Forinstance, a damaged brake rotor on a car is a peril that causes aneconomic loss (the brake has to be repaired, causing financialloss). It is also a hazard that increases the likelihood of loss fromthe peril of a car accident that causes premature death.

Hazards can be classified into the following four main categories:

• Physical hazard. This type of hazard involves the physicalproperties that influence the chances of loss from various perils.

• Moral hazard. This type of hazard involves the character ofpersons involved in the situation, which might increase thelikelihood of a loss. One example of a moral hazard is the dishonestbehavior of a person who commits fraud by intentionallydamaging property in order to collect an insurance payment. Thisdishonest behavior results in a loss to the insurance company.

• Morale hazard. This type of hazard involves a careless attitudetoward the occurrence of losses. An insured person ororganization, knowing that the insurance company will bear thebrunt of any loss, may exercise less care than if forced to bear anyloss alone, and may thereby cause a condition of morale hazard,resulting in a loss to the insurance company. This hazard shouldnot be confused with moral hazard, as it requires neitherintentional behavior nor criminal tendencies.

• Legal hazard. This type of hazard involves an increase in theseverity and frequency of losses (legal costs, compensationpayments, etc.) that arises from regulatory and legal requirementsenacted by legislatures and self-regulating bodies and interpretedand enforced by the courts. Legal hazards flourish in jurisdictionsin which legal doctrines favor a plaintiff, because this represents ahazard to persons or organizations that may be sued. The Americanand European systems of jurisprudence are quite different. In theAmerican system, it is much easier to go to court, and producers ofgoods and services thus face an almost unlimited legal exposure topotential lawsuits. The European courts have placed higher hurdlesin the path of those who might take legal action against anotherparty. In addition, “commonsense” standards of what is actionableare different in Europe and the United States.

Risk Management: A Maturing Discipline 9

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 9

For a risk manager, the legal and criminal hazards are especially im-portant. Legal and regulatory hazards arise out of statutes and court deci-sions. The hazard varies from one jurisdiction to another, which meansglobal companies must watch legal and regulatory developments carefully.

1.5 DEGREE OF RISK

Risk itself does not say anything about the dimension of measurement.How can we express that a certain event or condition carries more or lessrisk than another? Most definitions link the degree of risk with the likeli-hood of occurrence. We intuitively consider events with a higher likeli-hood of occurrence to be riskier than those with a lower likelihood. Thisintuitive perception fits well with our definition of the term risk. Most def-initions regard a higher likelihood of loss to be riskier than a lower likeli-hood. We do not agree, as this view is already affected by the insuranceindustry’s definition of risk. If risk is defined as the possibility of a devia-tion from a desired outcome that is expected or hoped for, the degree ofrisk is expressed by the likelihood of deviation from the desired outcome.

Thus far we have not included the size of potential loss or profit inour analysis. We say that a situation carries more or less risk, and mean aswell the value impact of the deviation. The expected value of a loss orprofit in a given situation is the likelihood of the deviation multiplied bythe amount of the potential loss or profit. If the money at risk is $100 andthe likelihood of a loss is 10 percent, the expected value of the loss is $10.If the money at risk is $50 and the likelihood of a loss is 20 percent, the ex-pected value of the loss is still $10. The same calculation applies to a profitsituation. This separation of likelihood and value impact is very impor-tant, but we do not always consider this when we talk about more or lessrisk. Later we will see how the separation of likelihood and impact canhelp us analyze processes, structures, and instruments to create an overallview of organizational risk.

Frequently, persons who sit on supervisory committees (e.g., boardmembers and trustees of endowment institutions and other organiza-tions) have to make decisions with long-ranging financial impact but haveinadequate backgrounds and training to do so. Organizational structuresand processes are rarely set up to support risk management, as thesestructures are usually adopted from the operational areas. But with in-creased staff turnover, higher production volumes, expansion into newmarkets, and so forth, the control structures and processes are rarelyadapted and developed to match the changing situation.

New problems challenge management, as the existing controlprocesses and reporting lines no longer provide alerts and appropriate in-formation to protect the firm from serious damage or bankruptcy, as wasthe case with Barings or Yamaichy.

10 CHAPTER 1

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 10

Banks and other regulated financial institutions have been forced bygovernment regulations and industry self-regulating bodies to developthe culture, infrastructure, and organizational processes and structures foradequate risk management. Risk management has become a nondelegablepart of top management’s function and thus a nondelegable responsibilityand liability. Driven by law, the financial sector has developed over thepast years strategies, culture, and considerable technical and managementknow-how relating to risk management, which represents a competitiveadvantage against the manufacturing and insurance sectors.

1.6 RISK MANAGEMENT: A MULTILAYERED TERM

1.6.1 Background

As previously discussed, risk management is a shifting concept that hashad different definitions and interpretations. Risk management is basi-cally a scientific approach to the problem of managing the pure risks facedby individuals and institutions. The concept of risk management evolvedfrom corporate insurance management and has as its focal point the pos-sibility of accidental losses to the assets and income of the organization.Those who carry the responsibility for risk management (among whomthe insurance case is only one example) are called risk managers. The termrisk management is a recent creation, but the actual practice of risk man-agement is as old as civilization itself. The following is the definition ofrisk management as used used throughout this work:

risk management In a broad sense, the process of protecting one’s person or or-ganization intact in terms of assets and income. In the narrow sense, it is the mana-gerial function of business, using a scientific approach to dealing with risk. As such,it is based on a distinct philosophy and follows a well-defined sequence of steps.

1.6.2 History of Modern Risk Management

Risk management is an evolving concept and has been used in the sense de-fined here since the dawn of human society. As previously mentioned, riskmanagement has its roots in the corporate insurance industry. The earliestinsurance managers were employed at the turn of the twentieth century bythe first giant companies, the railroads and steel manufacturers. As capitalinvestment in other industries grew, insurance contracts became an increas-ingly significant line item in the budgets of firms in those industries, as well.

It would be mistaken to say that risk management evolved naturallyfrom the purchase of insurance by corporations. The emergence of riskmanagement as an independent approach signaled a dramatic, revolu-

Risk Management: A Maturing Discipline 11

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 11

tionary shift in philosophy and methodology, occurring when attitudestoward various insurance approaches shifted. One of the earliest refer-ences to the risk management concept in literature appeared in 1956 in theHarvard Business Review.4 In this article, Russell Gallagher proposed a rev-olutionary idea, for the time, that someone within the organization shouldbe responsible for managing the organization’s pure risk:

The aim of this article is to outline the most important principles of a work-able program for “risk management”—so far so it must be conceived, evento the extent of putting it under one executive, who in a large companymight be a full-time “risk manager.”

Within the insurance industry, managers had always considered in-surance to be the standard approach to dealing with risk. Though insurancemanagement included approaches and techniques other than insurance(such as noninsurance, retention, and loss prevention and control), these ap-proaches had been considered primarily as alternatives to insurance.

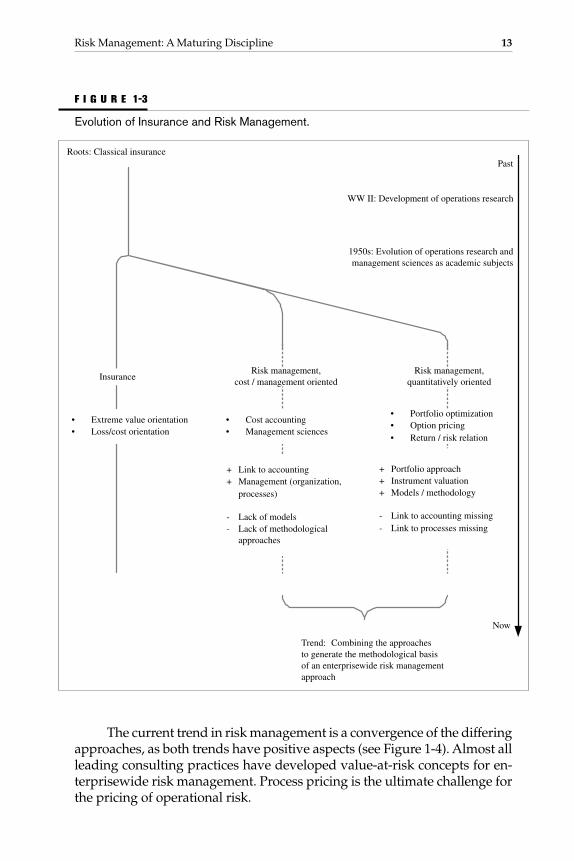

But in the current understanding, risk management began in the early1950s. The change in attitude and philosophy and the shift to the risk man-agement philosophy had to await management science, with its emphasis oncost-benefit analysis, expected value, and a scientific approach to decisionmaking under uncertainty. The development from insurance managementto risk management occurred over a period of time and paralleled the evolu-tion of the academic discipline of risk management (Figure 1-3). Operationsresearch seems to have originated during World War II, when scientists wereengaged in solving logistical problems, developing methodologies for deci-phering unknown codes, and assisting in other aspects of military opera-tions. It appears that in the industry and in the academic discipline thedevelopment happened simultaneously, but without question the academicdiscipline produced valuable approaches, methodologies, and models thatsupported the further development of risk management in the industry.New courses such as operations research and management science empha-size the shift in focus from a descriptive to a normative decision theory.

Markowitz was the first financial theorist to explicitly include risk inthe portfolio and diversification discussion.5 He linked terms such as returnand utility with the concept of risk. Combining approaches from operationsresearch and mathematics with his new portfolio theory, he built the basisfor later developments in finance. This approach became the modern portfo-lio theory, and was followed by other developments, such as Fischer Black’soption-pricing theory, which is considered the foundation of the deriva-tives industry. In the early 1970s, Black and Scholes made a breakthroughby deriving a differential equation which must be satisfied by the price ofany derivative instrument dependent on a nondividend stock.6 This ap-proach has been developed further and is one of the driving factors for theactual financial engineering of structured products.

12 CHAPTER 1

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 12

The current trend in risk management is a convergence of the differingapproaches, as both trends have positive aspects (see Figure 1-4). Almost allleading consulting practices have developed value-at-risk concepts for en-terprisewide risk management. Process pricing is the ultimate challenge forthe pricing of operational risk.

Risk Management: A Maturing Discipline 13

Risk management,cost / management oriented

• Portfolio optimization• Option pricing• Return / risk relation

+ Portfolio approach+ Instrument valuation+ Models / methodology

- Link to accounting missing- Link to processes missing

+ Link to accounting+ Management (organization,

processes)

- Lack of models- Lack of methodological

approaches

• Cost accounting• Management sciences

• Extreme value orientation• Loss/cost orientation

Insurance

Trend: Combining the approachesto generate the methodological basisof an enterprisewide risk managementapproach

Roots: Classical insurancePast

Now

WW II: Development of operations research

1950s: Evolution of operations research andmanagement sciences as academic subjects

Risk management,quantitatively oriented

F I G U R E 1-3

Evolution of Insurance and Risk Management.

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 13

14

Iden

tific

atio

nof

ris

k

Mea

sure

men

tof

ris

k

Con

trol

of

risk

Lin

king

ris

kan

d re

turn

Cap

ital

allo

catio

npr

oces

s

Cap

ital

allo

catio

nte

chni

ques

Val

ue-b

ased

stra

tegy

Max

imiz

edea

rnin

gspo

tent

ial

Ear

ning

sst

abili

ty

Prot

ectio

nag

ains

tun

fors

een

loss

es

Stra

tegi

c ad

vant

age

Cre

dit r

isk

Mar

ket r

isk

Shareholder value objective

Ris

k m

anag

emen

t so

phis

tica

tion

Ope

ratio

nal r

isk

FI

GU

RE

1-4

Dev

elop

men

t Lev

els

of D

iffer

ent R

isk

Cat

egor

ies.

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 14

1.6.3 Related Approaches

1.6.3.1 Total Risk ManagementTotal risk management, enterprisewide risk management, integrated risk man-agement, and other terms are used for approaches that implementfirmwide concepts including measurement and aggregation techniquesfor market, credit, and operational risks. This book uses the following def-inition for total risk management, based on the understanding in the mar-ket regarding the concept:

total risk management The development and implementation of an enter-prisewide risk management system that spans markets, products, and processesand requires the successful integration of analytics, management, and technology.

The following paragraphs highlight some concepts developed byconsulting and auditing companies. Enterprise risk management, as devel-oped by Ernst & Young, emphasizes corporate governance as a key elementof a firmwide risk management solution. Boards that implement leading-edge corporate governance practices stimulate chief executives to sponsorimplementation of risk management programs that align with their busi-nesses. In fulfilling their risk oversight duties, board members request reg-ular updates regarding the key risks across the organization and theprocesses in place to manage them. Given these new practices, boards areincreasingly turning to the discipline of enterprise risk management as ameans of meeting their fiduciary obligations. As a result, pioneering or-ganizations and their boards are initiating enterprisewide risk manage-ment programs designed to provide collective risk knowledge for effectivedecision making and advocating the alignment of management processeswith these risks. These organizations have recognized the advantages of:

• Achieving strategic objectives and improving financialperformance by managing risks that have the largest potentialimpact

• Assessing risk in the aggregate to minimize surprises and reduceearnings fluctuations

• Fostering better decision making by establishing a commonunderstanding of accepted risk levels and consistent monitoringof risks across business units

• Improving corporate governance with better risk managementand reporting processes, thereby fulfilling stakeholderresponsibilities and ensuring compliance with regulatoryrequirements

At present, many risk management programs attempt to provide alevel of assurance that the most significant risks are identified and man-

Risk Management: A Maturing Discipline 15

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 15

aged. However, they frequently fall short in aggregating and evaluatingthose risks across the enterprise from a strategic perspective. Effective en-terprise risk management represents a sophisticated, full-fledged man-agement discipline that links risk to shareholder value and correlates withthe complexity of the organization and the dynamic environments inwhich it operates (Figure 1-5).

Once an organization has transformed its risk management capabil-ities, it will be in a position to promote its success through an effective, in-tegrated risk management process. Ernst & Young’s point of view is thateffective enterprise risk management includes the following points (seeFigure 1-6):7

• A culture that embraces a common understanding and vision ofenterprise risk management

• A risk strategy that formalizes enterprise risk management andstrategically embeds risk thinking within the enterprise

16 CHAPTER 1

F I G U R E 1-5

Evolving Trends and the Development of an Integrated Risk Framework to Supportthe Increasing Gap Between Business Opportunities and Risk Management Capa-bilities. (Source: Ernst & Young, Enterprise Risk Management, Ernst & Young LLP,2000. Copyright © 2000 by Ernst & Young LLP; reprinted with permission of Ernst& Young LLP.)

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 16

• An evolved governance practice that champions an effectiveenterprisewide risk management system

• Competent and integrated risk management capabilities foreffective risk identification, assessment, and management

Coopers & Lybrand has developed its own version of an enter-prisewide risk management solution in the form of generally accepted riskprinciples (GARP).8 The GARP approach seeks to distil and codify majorprinciples for managing and controlling risk from the guidance issued todate by practitioners, regulators, and other advisors. The framework usesthe experience and expertise of all parties involved in its development toexpand these principles so as to establish a comprehensive frameworkwithin which each firm can manage its risks and through which regulatorscan assess the adequacy of risk management in place. It presents a set ofprinciples for the management of risk by firms, and for the maintenance ofa proper internal control framework, going further than the mere assess-ment of the algorithms within risk management models. It covers such

Risk Management: A Maturing Discipline 17

assuredsupported

and

stakeholder

communications

functio

ns

technology

risk management

capabilityriskmana

gement

process

riskstrategy

cultureand

governance

embedded

valu

eba

sed

shar

ehol

der

reviewed

F I G U R E 1-6

Enterprise Risk Management Point of View. (Source: Ernst & Young LLP, a mem-ber of Ernst & Young Global. Copyright © 2002 by Ernst & Young LLP; reprintedwith permission of Ernst & Young LLP.)

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 17

matters as the organization of the firm, the operation of its overall controlframework, the means and principles of risk measurement and reporting,and the systems themselves. The approach is based around principles, eachof which is supported by relevant details. The extent of the detail variesdepending on the principle concerned. In all cases, the guidance providedis based on the assumption that the level of trading in a firm is likely togive rise to material risks. In certain cases an indication of alternative ac-ceptable practices is given.

KPMG has developed a risk management approach based on theshareholder value concept, in which the value of an organization is notsolely dependent on market risks, such as interest or exchange rate fluc-tuations. It is much more important to study all types of risks. Thismeans that macroeconomic or microeconomic risks, on both the strategicand operational levels, have to be analyzed and considered in relation toevery single decision. An organization can seize a chance for lasting andlong-term success only if all risks are defined and considered in its overalldecision-making process as well as in that of its individual businessunits. KPMG assumes (as do other leading companies) that the key fac-tor for a total risk management approach is the phase of risk identifica-tion, which forms the basis for risk evaluation, risk management, andcontrol. Figure 1-7 shows the Risk Reference Matrix, KPMG’s systematicand integrated approach to the identification of risk across all areas ofthe business.9 This is a high-level overview, which can be further brokendown into details.

Many other approaches from leading consulting and auditing prac-tices could be mentioned. They all assume that they have a frameworkthat contains all the risks that must be identified and measured to get theoverall risk management.

Figure 1-8 shows a risk map that covers many different risk areas,from a high-level to low-level view. From an analytical standpoint, it looksconsistent and comprehensive, covering all risks in an extended frame-work. The allocation of individual risks may be arbitrary, depending onwhat concept is used. But the combination and complexity of all risks,their conditions and assumptions, might make it difficult to identify andmeasure the risk for an enterprisewide setup.

In practice, significant problems often occur at this stage. A system-atic and consistent procedure to identify risk across all areas of the busi-ness, adhering to an integrated concept, is essential to this first sequenceof the risk management process. But this integrated concept is, in certainregards, a matter of wishful thinking. The definition of certain individualrisks—for example, development, distribution, and technology risks—isnot overly problematic. The concepts span the complete range of riskterms. But in many cases the categorization and definition of some termsare ambiguous. One example is the term liquidity. Liquidity can be seen as

18 CHAPTER 1

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 18

part of market and credit risks, but it also affects systemic risk. The totalrisk management concept appears to be complete, consistent, and ade-quate. But this interpretation is too optimistic, as some of the concepts stilllack major elements and assumptions.

In an overall approach, the interaction between individual risks, aswell as the definition of the weighting factors between the risk trees thatmust be attached to this correlation, creates serious difficulties. Portfoliotheory tells us that correlation between the individual risk elements rep-

Risk Management: A Maturing Discipline 19

TOTAL

RISK

BusinessEnvironment Risk

Activity Risk

MacroeconomicRisk Factors

MicroeconomicRisk Factors

Cultural-LevelRisks

Strategic-LevelRisks

Operational-LevelRisks

InternationalStability Risk

National StabilityRisk

Outside RiskFactors

Financial MarketRisks

Development &Production Risks

Customer-FacingRisks

OrganizationalPolicy Risks

General Industry-Related Risks

Business PolicyRisks

Business ValueRisks

Ethical ValueRisks

Local IndustrialSector Risks

Support ServiceRisks

F I G U R E 1-7

KPMG Risk Reference Matrix. (Source: Cristoph Auckenthaler and Jürg Gabathuler,Gedanken zum Konzept eines Total Enterprise Wide Risk Management (TERM), Zurich:University of Zurich, 1997, 9, fig. 2.)

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 19

20

Market risk

Legal

Compliance

Regulatory

Human resources

Management direction anddecision making

Accounting Taxation

External physicalevents

Product / servicedevelopment

Controlframework

Suppliers

Communication / relationshipmanagement

Corporate strategy /direction

SupportServices

Internal physicalevents

Processmanagement /

design

Productselling /

distribution

Systemic risk

Credit risk

Strategic / management risk

Financial riskOperational riskSystemic risk

F I G U R E 1-8

Risk Map of a Total Risk Management Approach. (Source: Modified from KPMG.)

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 20

resents a central role in the establishment of risk definitions and strate-gies, and therefore in the risk management and hedging process (pro-vided hedging is feasible). The same is also true for the risk managementof a business (with elements such as new product risks, model risks,counterparty risks, etc.). From a practical standpoint, it is often not possi-ble to get data and calculate risk coefficients if the overall scheme of atotal risk management concept represents a widely branching system,because the number of interactions (correlations) and the required dataincrease substantially as the number of elements increases. Such ap-proaches require the combined and well-orchestrated use of question-naires, checklists, flowcharts, organization charts, analyses of yearlyfinancial statements and transactions, and inspections of the individualbusiness locations. This requires substantial expenditures and commit-ment from management.

As can be seen from the preceding descriptions of the different en-terprise risk management solutions, the major consulting firms approachthe same issues from different perspectives. Whereas KPMG and Ernst &Young have a more holistic approach, Coopers & Lybrand takes a morenormative, trading-oriented, and regulatory approach. Regardless of thedifferent approaches offered by the various auditing and consulting com-panies, a company has to adapt the approach it selects based on its ownneeds, its understanding of risk management, and the extent to which riskmanagement is an integrated part of upper management’s responsibilitiesor an independent control and oversight function.

1.6.3.2 Total Quality ManagementVirtually every activity within an organization changes the organiza-tion’s exposure to risk. It is part of a risk manager’s responsibility to ed-ucate others on the risk-creating and risk-reducing aspects of theiractivities. The recognition that risk control is everyone’s responsibilityclosely links risk control to principles of quality improvement, an ap-proach to management that has been employed with considerable suc-cess in Japan and the United States. The movement toward qualityimprovement often is known by code names and acronyms such as totalquality management (TQM) and total quality improvement (TQI). TQM wasdeveloped in Japan after World War II, with important contributionsfrom American experts. Ultimately, Japanese companies recognized thatproduction volume itself does not create competitive advantage, onlyquality and product differentiation can do so. In the context of TQM,quality is here defined as follows:10

quality The fulfillment of the agreed-upon requirements communicated by thecustomer regarding products, services, and delivery performance. Quality ismeasured by customer satisfaction.

Risk Management: A Maturing Discipline 21

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 21

TQM has five approaches, reflecting the different dimensions ofquality:11

• Transcendent approach. Quality is universally recognizable and isa synonym for high standards for the functionality of a product.The problem is that quality cannot be measured precisely underthis approach.

• Product-oriented approach. Differences in quality are observablecharacteristics linked to specific products. Thus, quality isprecisely measurable.

• User-oriented approach. Quality is defined by the user, dependingon the utility value.

• Process-oriented approach. The production process is the focus ofquality efforts. Quality results when product specifications andstandards are met through the use of the proper productionprocess.

• Value-oriented approach. Quality is defined through the price-product-service relationship. A quality product or service isidentified as one that provides the defined utility at an acceptableprice.

The TQM approach has four characteristics:

• Zero-error principle. Only impeccable components and perfectprocesses may be used in the production process to ensuresystematic error avoidance in the quality circle.

• Method of “why.” This is a rule of thumb: the basis of a problemcan be evaluated by asking why five times. This avoids taking thesymptoms of a problem to be the problem itself.

• Kaizen. Kaizen is a continuous process of improvement throughsystematic learning. This means turning away from the traditionaltayloristic division of labor and returning to an integratedorganization of different tasks that includes continuous training todevelop personnel’s technical and human relations skills.

• Simultaneous engineering. Simultaneous engineering demandsfeedback loops between different organizational units anddifferent processes. This requires overlapping teams and processorientation.12

Table 1-1 highlights the profiles of the total quality management andtotal risk management approaches.

Total quality management has its own very distinct terms and defi-nitions, which make it a different approach from total risk management. Itis a multidimensional client-oriented approach, in which managementtakes preventive measures to ensure that all processes, organizational en-

22 CHAPTER 1

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 22

tities, and employees focus on quality assurance and continuous improve-ment throughout the organization.

1.6.4 Approach and Risk Maps

Figures 1-9 and 1-10 present the approach and risk maps used in this book.

1.7 SYSTEMIC RISK

1.7.1 Definition

There is no uniform accepted definition of systemic risk. This book usesthe definition contained in a 1992 report of the Bank for International Set-tlement (BIS):13

Risk Management: A Maturing Discipline 23

T A B L E 1-1

Differences and Similarities Between Total Quality Management and Total Risk Management

Total Quality Management (TQM) Total Risk Management (TRM)

Extended, multidimensional, client- Integrated, multidimensional enterprise-oriented quality term. oriented term.

Extended client definition: clients are Internal client definition: clients areinternal and external. internal.

Preventive quality assurance policy. Preventive and product-oriented riskmanagement policy.

Quality assurance is the duty of all TRM assurance is the duty of speciallyemployees. assigned and responsible persons.

Enterprisewide quality assurance. TRM assurance within the limits and forthe risk factors to be measured accordingto the risk policy.

Systematic quality improvement with Systematic risk control within thezero-error target. defined limits.

Quality assurance is a strategic job. TRM is a strategic job.

Quality is a fundamental goal of the TRM is a fundamental goal of theenterprise. enterprise.

Productivity through quality. TRM to ensure ongoing production.

SOURCE: Hans-Jörg Bullinger, “Customer Focus: Neue Trends für eine zukunftsorientierte Unternehmungsführung,” inHans-Jörg Bullinger (ed.), “Neue Impulse für eine erfolgreiche Unternehmungsführung, 13. IAO-Arbeitstagung,” Forschungund Praxis, Band 43, Heidelberg u.a., 1994.

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 23

24 CHAPTER 1

Model Risk

Market Risk

Credit Risk

Operational Risk

Systemic Risk

Current Exposure

Potential Exposure

Cumulation Risk

Counterparty Risk

Direct Credit Risk

Credit EquivalentExposure

Diversification Risk

Credit Risk Exposure

RegulatoryMechanisms

Capital Adequacy

Risk Disclosure

Regulatory Constraints

Model Risk

Equity Risk

Interest Rate Risk

Currency Risk

Capital Adequacy

Risk Disclosure

Regulatory Constraints

Model Risk

Commodity Risk

Model Risk

Equity Price Risk

Model Risk

Yield Curve Risk Basis / Spread Risk

Product Risk

Product Risk

"Greeks"

Dividends

"Greeks"

Prepayment

Model Risk

Commodity CurveRisk

Basis / Spread Risk

"Greeks"

Model Risk

Fx Curve Risk Basis / Spread Risk

"Greeks"

Liquidity Risk Model Risk

Rating

Customer / TransactionRisks

Marketing Risks

Sales Risks

Disclosures

Product / MarketCombination

Distribution

Order Capture &Confirmation

Controlling

Internal Audit

Legal & Compliance

Business Control

Logistics

Support Service Risks

Accounting

HR

IT / Technology

RegulatoryMechanisms

Risk Disclosure

Regulatory Constraints

Market EfficiencyMarket Liquidity

InformationTransparency

Market Access /Hurdles

International / NationalStability Risks Economy

Legal System

Political Stability

Market Risk Factors

RegulatoryMechanisms

F I G U R E 1-9

Risk Categorization Used as an Integrative Framework in This Book.

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 24

25

PortfolioManagement

Resarch Compliance Trade ManagementTools

Order Routing Trade ExecutionTrade

ConfirmationSettlement andReconciliation

Custody orSecurities Lending Compliance

PortfolioAccounting

Market Risk Market Risk

Credit Risk Credit Risk

Legal /Regulatory

OperationalRisk

Market Risk

OperationalRisk

OperationalRisk

Systemic Risk

OperationalRisk

OperationalRisk

OperationalRisk

OperationalRisk

Legal /Regulatory

Pretrade Trade Posttrade

Market Risk

Credit Risk

During the phases of research, tactical or strategic asset allocation, and selection of instruments, there is an inherent risk of misjudgment or faulty estimation. Therefore, timing, instrument selection, and rating considerations have a market and credit component.

Compliance has to take into account all client restrictions, internal directives, and regulatory constraints affected by the intended transaction. Capital adequacy, suitability to the client's account, and so forth, also must be considered.

From the moment the trade is entered into the system until the final transaction is entered in the portfolio accounting and custody or securities lending systems, systems are crucial and have inherent risks.

During the trade execution phase, the trading desk has directed exposure to system risk. Until final settlement, the trade amount is exposed to disruption in the system, which could disturb correct trade confirmation and settlement.

From the moment of execution until settlement, the books are exposed to changes in the market risk factors. They are also exposed to changes in spread risk (i.e., credit risk).

Market risk during the trade execution is especially high, as the market price or model pricing might give the wrong information (e.g., the market could be illiquid, or the models might not fit the instruments).

Compliance can be considered the last stop before the transaction is complete. There is the opportunity to review whether the transaction has been executed and settled correctly.

F I G U R E 1-10

Example of Transaction Breakdown, Process-Oriented Flow of Different Risk Categories Involved.

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 25

systemic risk The risk that a disruption (at a firm, in a market segment, to a set-tlement system, etc.) causes widespread difficulties at other firms, in other marketsegments, or in the financial system as a whole.

In this definition, systemic risk is based on a shock or disruption originatingeither within or outside the financial system that triggers disruptions toother market participants and mechanisms. Such a risk thereby substan-tially impairs credit allocation, payments, or the pricing of financial assets.While many would argue that no shock would be sufficient to cause a totalbreakdown of the financial system, there is little doubt that shocks of sub-stantial magnitude could occur, and that their rapid propagation throughthe system could cause a serious system disruption, sufficient to threaten thecontinued operation of major financial institutions, exchanges, or settlementsystems, or result in the need for supervisory agencies to step in rapidly.

1.7.2 Causes of Systemic Risk

Under the BIS definition, one should consider not only the steps takenwithin the institution to guard against a major internal breakdown. Oneshould also consider those features of the global financial marketplaceand current approaches to risk management and supervision that couldadversely affect the institution’s ability to react quickly and appropriatelyto a shock or disturbance elsewhere.

Recent developments in the financial market have produced a broadrange of highly developed pricing models. Shareholder value, which is oftenmistakenly thought of as the generation of higher return on equity, leads fi-nancial institutions to reduce the proprietary capital used for activities that in-crease the profitability of equity capital. The financial institution reduces theequity capital to the bare regulatory minimum with the result that less and lesscapital supports the expanded trading activities, because the shareholdervalue concept has nothing to do with capital support. This trend is quitedangerous, as less and less capital serves as security capital in the return-generationprocessformoreandmorerisk,withoutgeneratingcommensuratereturns, and this trend alone promotes systemic risks. The development of aninternationally linked settlement system has progressed significantly; never-theless, there are still other factors that create systemic risk.

1.7.3 Factors That Support Systemic Risk

The following factors support systemic risk, based on empirical experi-ence from previous crises or near-misses in the market:

• Economic implications. Our understanding of the relationshipbetween the financial markets and the real state of the economy is

26 CHAPTER 1

Gallati_01_1p_j.qxd 2/27/03 9:11 AM Page 26

questionable. The pricing of individual positions or positions for aportfolio can be done with any desired precision. The economicimplications of the created models are often overlooked. It is notalways a simple matter to understand the basic economicassumptions and parameters of complex mathematical models.This is one of the biggest systemic risks and a possible reason forthe irritating, erratic movements of the markets. The participants—especially the “rocket scientists,” highly intelligent but with anarrow horizon—do not understand the impact of coordinationand feedback loops among the many individual decisions on thefinancial markets, especially concerning derivative constructs.