roadshow asia - le groupe la...

TRANSCRIPT

DIRECTION DE LA COMMUNICATION 1

Roadshow Asia – Investor presentation -

November 2016

• This document has been prepared by La Poste solely for use for general investor presentations. This document is not to be reproduced by any person, nor be distributed to any person other than its original recipient. La Poste takes no responsibility for the use of these materials by any person.

• This document does not constitute or form part of any solicitation, offer or invitation to purchase or subscribe for any Notes.

• The information contained in this document has not been independently verified. No representation or warranty, express or implied, is made as to, and no reliance may be placed for any purposes whatsoever on, the fairness, accuracy, completeness or correctness of the information or opinions contained herein. None of the La Poste, or any of its affiliates, advisers or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with this document.

• Certain statements in this document are forward-looking, including statements concerning La Poste’s plans, objectives, goals, strategies, future events, future revenues or performance, capital expenditures, financing needs, plans or intentions relating to acquisitions, competitive strengths and weaknesses, business strategy and the trends La Poste anticipates in the industries and the political and legal environment in which it operates and other information that is not historical information. By their nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that the predictions, forecasts, projections and other forward-looking statements will not be achieved. La Poste does not make any representation, warranty or prediction that the results anticipated by such forward-looking statements will be achieved, and such forward-looking statements represent, in each case, only one of many possible scenarios and should not be viewed as the most likely or standard scenario. Such forward-looking statements speak only as of the date on which they are made. Any opinions expressed in this document are subject to change without notice and La Poste does not undertake any obligation to update or revise any forward looking statement, whether as a result of new information, future events or otherwise.

Disclaimer

PAGE 2

Group presentation

PAGE 3

Financial information

Business review

Credit profile

Agenda

DIRECTION DE LA COMMUNICATION 4

Group presentation

Supportive, stable and long-term shareholders

Article 1 of Act 2010-123 of 9 February 2010

The share capital shall be held by the State & by other public sector legal entities1

100%

26.32% Employee representatives

Users representative

CDC representatives

Nominated by decree

Nomination proposed by Government and/or CDC

Municipalities representative

State representatives

State representation in the Board of Directors

Government commissioner +

Head of the State's Economic and Financial

Verification Mission

Assisting with no voting right

73.68%

The French government

Chairman & CEO

1) Except for the portion that may be held under employee shareholding arrangements

Nominated by decree

Elected by employees

Active participation of shareholders and public

entities in Group

strategy and business plans

PAGE 5

100% state-owned company

Key role of La Poste in France: 4 public service missions

Public service contract 2013-2017 and specific agreements between the French State and La Poste

• Partial compensation schemes for regional planning, press and banking accessibility

• EU compatible

Universal Postal Service

Press transport and delivery

Banking accessibility

Regional planning and development

Additional missions entrusted by the French State

Distribution of press and periodicals: • 6 days a week • all over the territory • at affordable prices (regulated)

• > 17,000 contact points by law

• Presence in priority areas (rural, underprivileged, mountain areas)

Mail collection and delivery to all points in the territory at affordable prices and at a determined quality

6 days a week

La Banque Postale is required:

• to open a Livret A savings account to any individual

• to operate free of charge cash withdrawals or deposits from €1.50

EU Directive La Poste designated

Universal Postal Service provider

PAGE 6

2000’s 2010’s

Very strong historical link with the State

90’s

2010 2011

In law

Entering the local

authorities financing market

Participation in French “plan

de relance”

Capital increase subscribed

by State & CDC

2012 2005

Creation of La Banque

Postale

From a State administration to an EPIC1

2013 2017 1991

Boosting social home ownership programs

In b

usin

ess

2006

Public

serv

ice

mis

sio

ns

2007 2008 2009 2014

Public service contract 2013-2017

2015 2016

Public limited

company2

Public service contract 2008-2012

Acts

/ D

ecre

es

Postal Act Creation of ARCEP

+ specific agreements covering each mission

Operator of Vital

Importance

Postal Act 4 missions reaffirmed

in law

La Poste, designated provider of the Universal Service for 15 years as from 1 January 2011

New decrees on •Universal Postal Service •Banking accessibility

Status

1) EPIC: public industrial and commercial establishment 2) French legal status of public limited company, i.e. “Société Anonyme”

XVth century

Louis XI

In

vo

lvem

en

t o

f S

tate

PAGE 7

La Poste Network servicing all business units through 17,111 retail outlets

(see appendix)

GeoPost La Banque Postale Services-Mail-Parcels Digital Services

* JV co-owned by La Poste (51%) and SFR (49%), not included in Group revenue following application of IFRS 11 as of 1/1/2014. 1.25m customers, €202m in revenue in 2015 ** Group employees in full time equivalent on average

*

Major multi-business services Group…

€23.045bn

Revenue 2015

€875m

EBIT 2015

A key employer 253,158 employees**

Strong international presence 20.8% revenue – ~23,500 employees** abroad

PAGE 8

Revenue 2

015

Mail and Parcel market, mainly in France

European CEP market

Retail banking in France

€11.5bn €5.7bn €5.7bn

Mark

et

€0.6bn

Internet-based services

48.6% of Group revenue 24.3% of Group revenue 24.9% of Group revenue 2.0% of Group revenue

Retail banking

Insurance

Asset management

4 main brands BtoB Marketing

solutions

Retail products & e-services

BtoB secure & digitised solutions

Logistics International

Services Parcels

Div

isio

ns

~24,000

1) Through partnership with Post Office Ltd 2) Revenue and geographic split based on 9M 2016 financial report, to reflect disposal of €0.4bn logistics subsidiary (trans-o-flex) in Germany early 2016 in business portfolio

Number of outlets/ outsourcing rate1

17,111 ~1,300 ~ 11,5001

46% 100% 97% 0% 100%

~13,200 2,700

50%

~2,200

33%

1,800

72%

Express Mail & Postal parcels Logistics Financial services Other services

9

49% 42%

83% 82%

100% 96%

27%

11%

24%

17%

22%

2%

14%

4%

50%

25%

26%

9%

87%

2%

19% 9%

1%

… with a unique diversification profile

€23bn

21%

€8bn

14%

Revenue 2015 / % international

€13bn

17%

€2bn

16%

€4bn

27%

€59bn €31bn

70% NS

€2bn

17%

Performance Growth

Ensure sustainable cash generation

Accelerate existing activities

Capture new markets

External growth

“La Poste 2020: Conquering the future”

PAGE 10

Strategic plan 2014-2020

Mail prices Public service Social Pact

DIRECTION DE LA COMMUNICATION 11

Business review

€11.5bn

International 5%

Logistics 6%

Parcels 14%

Services <1%

Mail 74%

Employees Revenue EBIT

~142,000 €697m

Presentation of the business unit (2015 figures)

PAGE 12

Services-Mail-Parcels

Unique door-to-door everyday services

Market positions1 Key strengths

Parcels

Logistics

International

1) Source: ARCEP for mail, internal for parcels and cross-border

• ~72,200 postmen, 100%

connected with smartphones

paying daily visits (6

days/7) to 26m households

• Trust capital

• Parcel expertise particularly

during peak periods

#1 addressed mail

#1 unaddressed mail

#1 BtoC parcels

#1 press delivery

Top 2 Europe (through Asendia JV)

Key metrics

12bn addressed mail

10bn unaddressed

~270m parcels

1.2bn press copies shipped

Presence in 15 countries

Market dynamics

Decline in addressed mail volumes - in bn items -

15.8 15.4 14.5 13.7 12.9 12.0

9.0

2010 2015 2020

-24.0%

PAGE 13

Services-Mail-Parcels

Firmly entering the local services market

Strategy

• Remain a key operator in the mail business while activating tariff lever

• Benefit from strongly growing e-commerce parcels: extended delivery possibilities (evening) and sending options (from one’s letterbox)

• Capture growth in new segments: local and in-home services, silver economy, recycling Develo

pm

ent

Perf

orm

ance

• Adapt the number of facilities to mail volume decline

• Continuous rationalization of logistic network

• Productivity

Increasing need for in-home services

E-commerce growth driving parcels market

In €bn

Source : internal for mail volumes (Group delivered mail volumes) ; Source : ICE/Fevad for e-commerce

78% outside France

€5.7bn

Key strengths Market positions**

Employees Revenue EBIT Parcel volume

~28,000 Inc. 22,000

outside France

€367m*

Presentation of the business unit (2015 figures)

PAGE 14

GeoPost European express leader

with strongly differentiating assets

* Published EBIT : €268m, restated €EBIT : 367m restated for provision linked to inquiry of Competition Authority in the French CEP market (appeal currently underway) ; ** CEP: Courier-Express-Parcels - Source: internal study

#1 Russia

Partnerships

Presence of GeoPost

#1 non-postal CEP operator UK

#1 Poland

#1 non-postal CEP operator in France #1 PUDO

#1 Spain

#1 Ireland #2 Germany

#2 (DTDC)

• The most extensive interconnected road network in Europe for deferred parcels <31.5kg

• A hybrid network that addresses BtoB as well as BtoC

• Innovative last-mile solutions (Pickup PUDOs / parcels lockers / Predict interactive delivery option)

• Operational excellence

#2 Europe

2010 2011 2012 2013 2014 2015

781 865

1,006

BtoB ~70%

~30%

BtoC

676 598

724

+100%

BtoC

E-commerce E-commerce BtoC in Western Europe in €bn*

118 161 183 208 233

International

2011 2015e 2014 2013 2012

Market dynamics

PAGE 15

* Source eCommerce Europe

Strategy

• Capture BtoC growth: keep innovating in premium delivery solutions (in-home, out-of home)

• Expand in new markets: fresh food delivery, same-day, medical temperature-controlled logistics

• Selected acquisitions in existing and new countries

Develo

pm

ent

Perf

orm

ance

• Maximize first-time delivery success rate

• Tight control on cost structure

• Monitor profitability of external growth operations

GeoPost Capturing e-commerce growth worldwide

Competition

• Strong liquidity position: L/D ratio 75%, LCR 218%

• Sound capitalization: CET1 13.2%, Tier 1 14.7%, total capital 18.7%

• Quality of assets confirmed by the ECB’s AQR (CET1 phased-in ratio of 7.625% by 1/1/2017)

€5.7bn

Insurance 3%

Asset management 3%

Retail banking 94%

Employees NBI EBIT

~4,000 direct & ~25,000 (1)

through La Poste €851m

Presentation of the business unit (2015 figures)

La Banque Postale Resilient and stable retail banking activities

(1)~15,000 in La Poste Financial Services (Financial centres, IT Division for Financial Services & Network) , ~10,000 advisors in post offices ; (2) Very popular passbook savings account ; (3) Source AFG (French Asset Management Association) 2014

23 12

1620

12 20

24

6992

75 75

Assets Liabilities

219 219

Regulated savings

centralized at CDC

Loans to customers

Customer deposits (excl. regulated savings)

Equity & hybrids Other assets

HTM portfolio

Short term assets

Short term liabilities

AFS portfolio Other liabilities

Regulated savings centralized at CDC

(**) Customer

deposits: €167bn

(**)

Key s

tren

gth

s

• Large domestic franchise (10.8m active customers) with low risk profile

• Significant market shares e.g. on savings outstandings (23.7% on Livret A (2)) and home loans production (6.1%)

• #5 asset management player (€180bn AuM)3

Balance sheet (€bn)

• Strong potential in customer equipment due to progressive authorizations from the regulator:

PAGE 16

2006

Home loans

2007 2009 2011 2012

Consumer loans

Property & casualty

insurance

Corporate loans

Public sector loans

Market dynamics

Low rates

environment

PAGE 17

La Banque Postale Priority on business development

Strategy

• Accelerate business development in the retail banking market (young, high-net-worth clients)

• Become a bank for professionals (dedicated unit in place)

• Enhance the corporate business and become a leading reference bank in the local public sector market

• Develop the asset management and the insurance activities Develo

pm

ent

Perf

orm

ance

• Major transformation programs (IT) underway

• Roll-out an intense training program (70,000 employees of LBP / La Poste Network by 2020)

• Efficiency plan in Financial centers

* Source : SOFIA March 2015

Prudential

regulation

New forms of

competition

Revenue

Presentation of the business unit (2015 figures)

BtoB Marketing Solutions

17%

75% BtoB Secure & Digital

Solutions

Retail Products & E-Services1 8%

€560m

1) Billings to other business units accounted for in 2015 revenue (since 1 January)

PAGE 18

Digital Services A dedicated business unit, lever for

development & internal transformation

Market positions

• 1st e-Health Services Provider in France

• 1st Data Base in France (36 million addresses)

• www.laposte.fr is #11 of the top 100 French e-commerce websites

Market dynamics

Cloud

Growth of online

platforms

Big data

Value / Monetization

of audience and customer data

Digital

Development of hybrid / digital service offers

IoT

Connected objects

Strategy

• Speed up the ongoing digital transformation of La Poste

• Win high-value market segments (e-health, e-administration, IoT)

• Roll-out unique infrastructures supporting all business units

DIRECTION DE LA COMMUNICATION 19

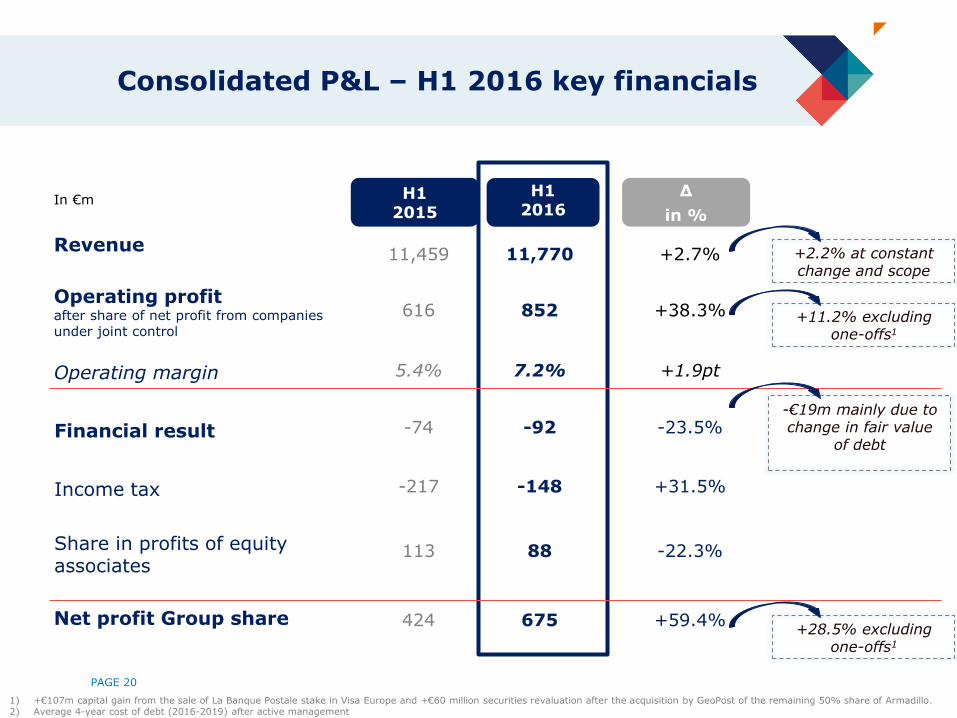

Key financials H1 2016

Revenue

Operating profit after share of net profit from companies under joint control

Operating margin

Financial result

Income tax

Share in profits of equity associates

Net profit Group share

11,770 11,459

H1 2016

H1 2015

852 616

7.2% 5.4%

675 424

-92 -74

-148 -217

88 113

In €m

PAGE 20

Consolidated P&L – H1 2016 key financials

+2.7%

∆

in %

+38.3%

+1.9pt

+59.4%

-23.5%

+31.5%

-22.3%

+2.2% at constant change and scope

+11.2% excluding one-offs1

+28.5% excluding one-offs1

1) +€107m capital gain from the sale of La Banque Postale stake in Visa Europe and +€60 million securities revaluation after the acquisition by GeoPost of the remaining 50% share of Armadillo. 2) Average 4-year cost of debt (2016-2019) after active management

-€19m mainly due to change in fair value

of debt

1) After share of net profit/(loss) of companies under joint control

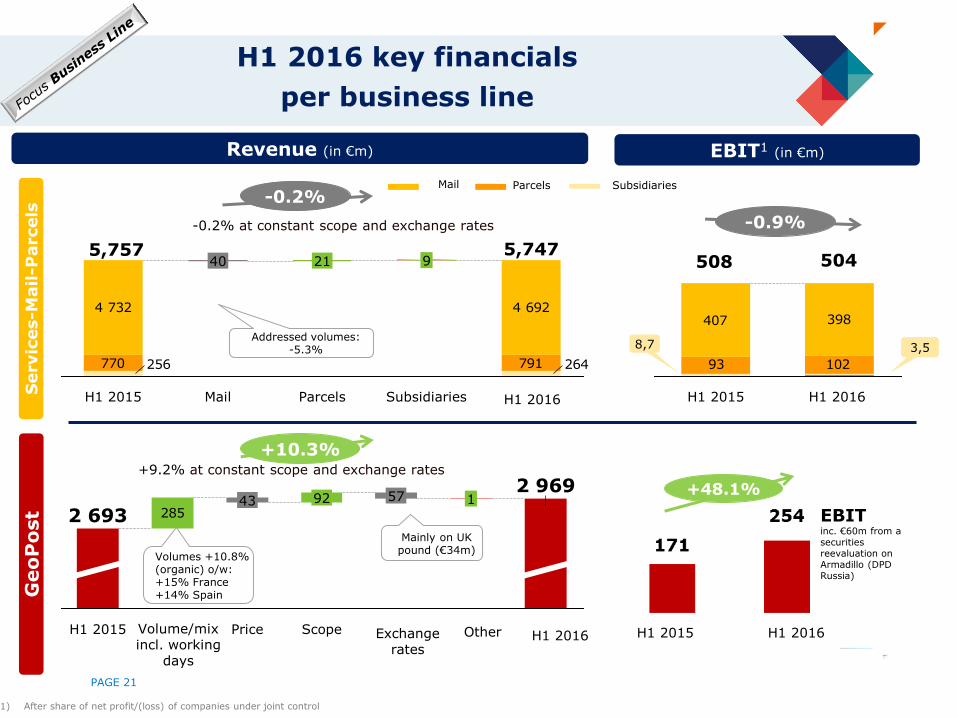

Revenue (in €m) EBIT1 (in €m)

Mail Parcels Subsidiaries

5,757 5,747

Servic

es-M

ail-P

arcels

256 264770 791

4 732 4 692

Subsidiaries

9

Parcels

21

40

H1 2015

-0.2%

-0.2% at constant scope and exchange rates -0.9%

504 508

H1 2016

407

93 102

398

H1 2016 H1 2015

8,7 3,5 Addressed volumes:

-5.3%

H1 2016 key financials

per business line

PAGE 21

Geo

Po

st

Other Exchange rates

H1 2016

+10.3% +9.2% at constant scope and exchange rates

Volume/mix incl. working

days

H1 2016 H1 2015

285

Scope

57 2 969

92

H1 2015

1 43

Price

2 693 EBIT inc. €60m from a securities reevaluation on Armadillo (DPD Russia)

+48.1%

Volumes +10.8% (organic) o/w: +15% France +14% Spain

Mainly on UK pound (€34m)

La B

an

qu

e P

osta

le

1) Including impact of change in home savings provision (€132m in 2014, €63m in 2015, €70m in H1 2015 and €212m in H1 2016) 2) CoR/outstanding relative to credit business (i.e. excl. Insurance and toll)

Net banking income / Revenue (in €m)

22

25

Asset management

6

Retail banking1

H1 2015

2 929

H1 2016

2 975

Scope Insurance

5

+1.6%

Profitability

81.5% 80.7%

(CoR/outstanding)

0.19% 0.19%

EBIT

CoR2

Operating ratio

o/w: - Net interest margin - Commissions

H1 2016 key financials

per business line

PAGE 22

Dig

ital S

ervic

es

H1 2016

289

Interco.

3

Mediapost communication

2

Docapost

9

Digital Services

3

H1 2015

278

+4.0%

+3.1% at constant scope and exchange rates

H1 2016 H1 2015

+€9m

o/w laposte.fr website dvpmt & associated

ad revenue

E-billings, dematerialization

Data management

services

-6.3% at constant scope and excl. home savings provision

PAGE 23

401

-80

173

Net debt change

10

Cash flow from operating activities

662

Others

70

External growth

99

Asset disposals

20

Interest and dividends

29

CAPEX

Services-Mail-Parcels: IT

GeoPost: logistic network (new hubs and depots), IT

Network: modernization/layout of network

Digital Services: IT

Real Estate: modernization and maintenance

Support & Structures: Vehicles, including electric

401

H1 2016 figures - In €m

(1) CFO excluding banking, including dividends from equity associates ; (2) Gross Capex excl. Banking (€401m) net from vehicle disposals (€10m) ; (3) Excluding vehicle disposals; (4) Including acquisition of financial assets

1

2 3 4

Mainly accrued interests

Net debt change H1 2016

DIRECTION DE LA COMMUNICATION 24

Credit profile

Equity1,2 Net debt1

1) 2013, 2014 pro forma data: published data restated for IFRS 10 and 11 impacts; does not take into account the banking activity for which the concept is not relevant 2) Group share

Net debt1 / Equity1,2

1.361.08

0.67 0.46 0.44 0.44 0.380.36

2009 2010 2011 2012 2013 2014 2015 H12016

4,051 4,465

6,7837,47

8,6159,112

9,723 10,293

2009 2010 2011 2012 2013 2014 2015 H12016

5,5174,804 4,544

3,463,805 4,005

3,657 3,737

2009 2010 2011 2012 2013 2014 2015 H12016

(in €m)

(in €m)

PAGE 25

Balance sheet highlights

Real estate

One of the largest real estate portfolio

after the State

~€4bn in 2015

Largest item on the Group balance sheet

High-quality, highly diversified

assets

• 11,362 buildings / facilities

• 6.5 million m², 57% directly owned

From small post offices to very large facilities

(from 9 to 39,000 m2 )

Average maturity

Strong footprint on the bond market

Maturity Issue date Amount

(€m)

Euro Bonds

Jul. 2017 Jul. 2002 600

Jun. 2023 Jun. 2003 1,000

Jul. 2019 Jul. 2004 800

Nov. 2021 Nov. 2006 1,000

Feb. 2018 Feb. 2008 500

Nov. 2024 Nov. 2012 1,000

June 2025 Jun/Sept 2015 750

GBP Bonds

Dec. 2016 Dec. 2000 242

1) 2016-2019 average cost of debt (as at 30/06/2016)

€6.774bn gross debt at 30 June 2016

Mainly euro-denominated bonds

Smooth redemption profile with no refinancing wall

242

600

500

800

1000

2017 2019 2021 2023

1000 1000

Predictability & stability of interest expense

100% foreign currency hedge

€5.892bn nominal value of

bond debt at 30 June 2016 Foreign currency-denominated debt

issues are systematically hedged using currency swaps

€m

2024 2018 2016

750

2025

5.32y

~80%

Cost of debt1 2.66%

% Fixed-rate

Strong ratings

A / A-1 / Stable

A+ / F1 / Stable

Bonds (90.3%)

Savings La Poste (0.9%)

Short term commercial (papers 0%)

Deposits and guarantees (3.7%)

Other (5.2%)

A low risk capital structure given currency, maturity & interest profile

PAGE 26

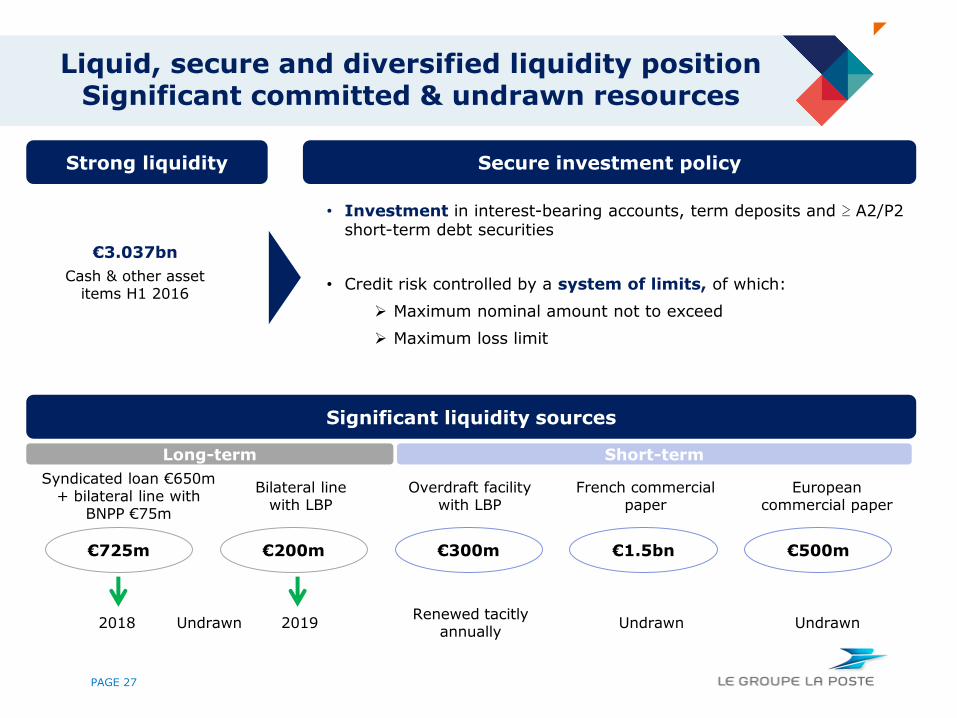

€3.037bn

Strong liquidity

Cash & other asset items H1 2016

€725m €200m

Bilateral line with LBP

2018 2019

€300m

Overdraft facility with LBP

Renewed tacitly annually

French commercial paper

€1.5bn €500m

European commercial paper

Significant liquidity sources

Syndicated loan €650m + bilateral line with

BNPP €75m

PAGE 27

Long-term Short-term

Secure investment policy

• Investment in interest-bearing accounts, term deposits and ≥ A2/P2 short-term debt securities

• Credit risk controlled by a system of limits, of which:

Maximum nominal amount not to exceed

Maximum loss limit

Undrawn Undrawn

Liquid, secure and diversified liquidity position Significant committed & undrawn resources

Undrawn

Le Groupe La Poste’s fundamental strengths

In-depth transformation of the Group underway

Solid balance sheet along with active debt management:

reduced debt leverage

Stable long-standing shareholding structure

(by law), critical role for the French State

Major market-leading businesses with unique assets and positions

Low business risk profile thanks to an unprecedented diversification model and a balanced activities portfolio

Strong credit profile

PAGE 28

DIRECTION DE LA COMMUNICATION 29

Contact details

Financial information available on http://legroupe.laposte.fr/en/Finance

PAGE 30

Yasmina Galle Head of Investor Relations and Financial Communication

[email protected] +33 (0)1 55 44 17 02

DIRECTION DE LA COMMUNICATION 31

Appendices

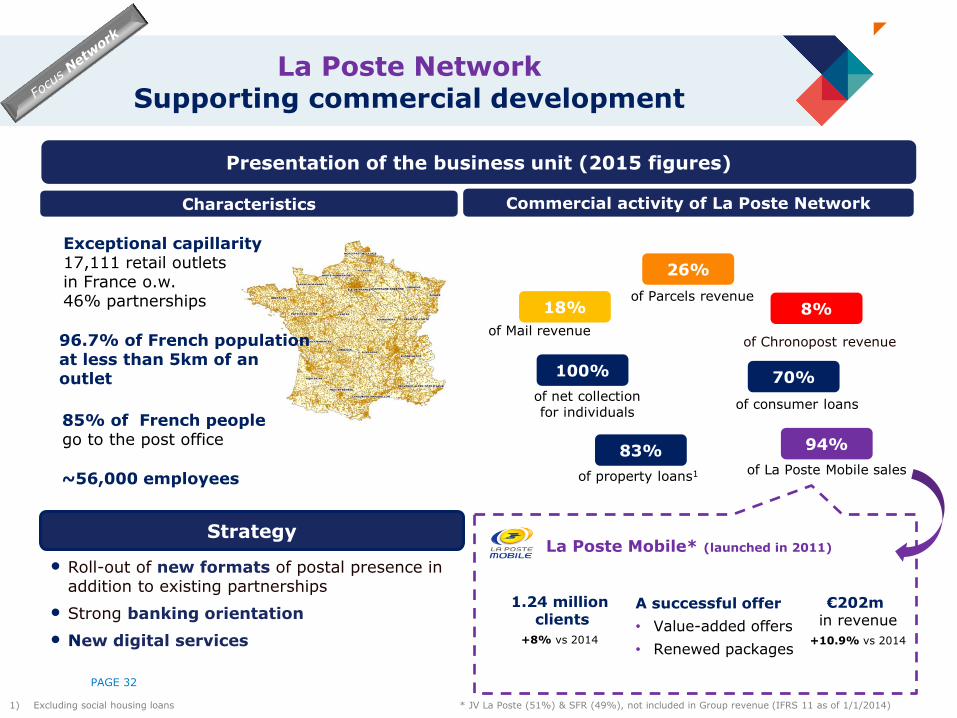

Characteristics

Exceptional capillarity 17,111 retail outlets in France o.w. 46% partnerships

85% of French people go to the post office

~56,000 employees

Presentation of the business unit (2015 figures)

Commercial activity of La Poste Network

18%

of Mail revenue

94%

of La Poste Mobile sales

26%

of Parcels revenue

100%

of net collection for individuals

83%

of property loans1

70%

of consumer loans

of Chronopost revenue

8%

96.7% of French population at less than 5km of an outlet

PAGE 32

La Poste Network Supporting commercial development

La Poste Mobile* (launched in 2011)

1.24 million clients

+8% vs 2014

€202m in revenue

+10.9% vs 2014

A successful offer

• Value-added offers

• Renewed packages

* JV La Poste (51%) & SFR (49%), not included in Group revenue (IFRS 11 as of 1/1/2014) 1) Excluding social housing loans

• Roll-out of new formats of postal presence in addition to existing partnerships

• Strong banking orientation

• New digital services

Strategy

PAGE 33

2010-2015 digitization impact on European postal operators1 (in %)

Services-Mail-Parcels

Volumes (addressed mail, in bn)

15.8 15.4 14.5 13.7 12.9 12.0

9.0

2010 2015 2020

-24.0%

Services-Mail-Parcels Focus on mail volumes

1) Estimated ratio, which takes into account the delegated act published by the European Commission on 10 October 2014 regarding centralized savings at CDC, subject to the European Central

Bank’s authorization.

Solvency: sound capitalization

2015

2014

L/D ratio: 74%

3.4% 3.5%

96

Customer deposits

74

71

Customer loans

(75% in 2014 and 2015)

leverage ratio

Centralized deposits

(not included in L/D ratio calculation)

(in €bn)

Estimated leverage ratio3 5.4% 5.2%

La Banque Postale Solvency and liquidity

PAGE 34

• LCR: 224% at H1 2016

• A strong liquidity buffer with 85% of level 1 assets

H1 2016e

224%

2015

218%

3,1

Level 1

Level 2

H1 2016

€21,2bn

18,1

LCR and liquidity

12,7% 13,2% 13,4%

CET1

14,2% 14,7%

18,7%

14,9%

Tier1

17,0%

+20 bps 19,4%

Total

+20 bps

+70 bps

H1 2016

2015

2014

T2

AT1

CET1

H1 2016

19,4%

4,5%

1,5%

13,4%

Leverage ratio

5,0%

H1 2016

-10 bps

3,4%

2015

5,2%

3,5% Including delegated act*

Without delegated act

Leverage ratio

Ensure safety and responsible change management for the benefit of employees

PAGE 35

Develop services with a positive impact for society

Develop responsible offerings with added value for customers

CSR commitments to 2020 anchored in Group strategy

• Continuous attention to health and quality of life at work

• Focus on professional evolution and training

Cut greenhouse emissions by -15 % over 2013-2020 (already -8% by end 2015)

• Own #1 fleet of electric vehicles worldwide

• Be 100% supplied with renewable electricity by 2020

• Continue to fund its carbon offset programme

Responsibility towards

environment

Responsibility towards society

Responsibility towards

employees

• Provide an environment-friendly transport mode to the 15 major French cities by 2020

• Support public action and be the privileged partner of local authorities

• Increase social and solidarity economy purchases

Responsibility towards clients

• Offer reliable, qualitative and innovative services

• Expand responsible offerings

• Achieve targets set in business contract with State on the 4 public service missions

Develop a more responsible local economy

Anchored CSR policy and strong objectives

DPD Group rated Silver (top 13%)

Rating agency Group ranking Rating and comments

#2

overall rank in transport & logistics sector: #2/29

In the top 10 % of the industry (5% C+ and 5% C)

LBP #1 French and #2 international bank

In the top 6% of the industry

Gold level

• 59 / 100 Overall score in 2015 (+12 vs. 2013)

• 76 / 100 Environmental performance (+26 vs. 2013)

Rating review expected in 2016

• C Overall score in 2014 (vs. C in 2011)

• C- Environmental performance (vs C+ in 2011)

• C for performance (ratings B to C represent only 6% of

the industry group – no A rating)

• 97 for transparency (+16 vs. 2013)

• 70 Overall score (+3 vs. 2014)

• 80 Environmental performance (+10 vs. 2014)

PAGE 36

investo

rs

Bto

B &

Consum

ers

Non-financial rating performance