royal exchange · 2019-08-27 · annual report & accounts 2016 8 royal exchange plc results at...

TRANSCRIPT

ROYAL EXCHANGE

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 3

Corporate Information 5

Corporate Profile 6

Results at a Glance 7-8

The Notice of Annual General Meeting 9-10

Proxy/Authority to Admit Form 11-12

Important Notice 13-14

Mandate for E-Dividend Payment 15-16

Chairman’s Statement and Reports 18-21

Group Managing Director’s Statement and Reports 22-25

Report of Corporate Governance 26-32

Risk Management Statement 33-37

Board of Directors 39

Brief Particulars of our Directors 40-42

Executive Management Team 43

Executive Management Team’s Profile 44-47

Directors & Regional Directors 48

Report of the Directors 49-54

Statement of Directors’ Responsibilities in relation to the Financial Statements 55

Report of Audit Committee 56

Independent Auditor’s Report 58-61

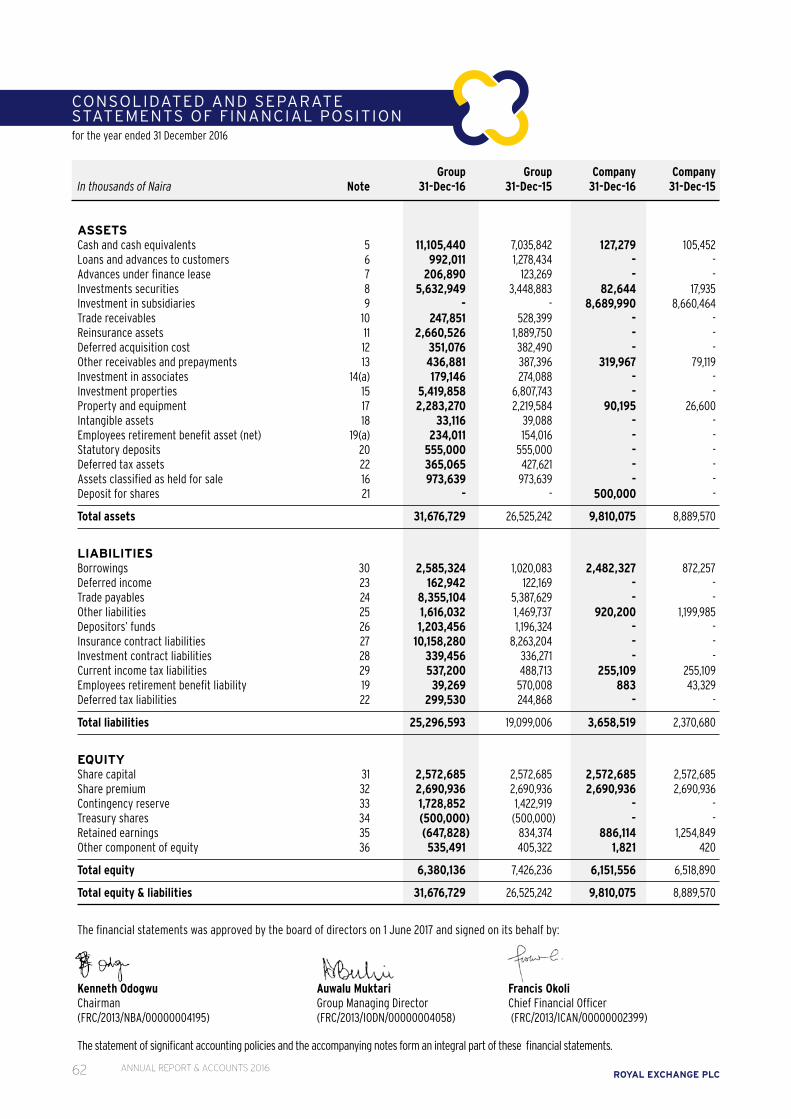

Consolidated and Separate Statement of Financial Position 62

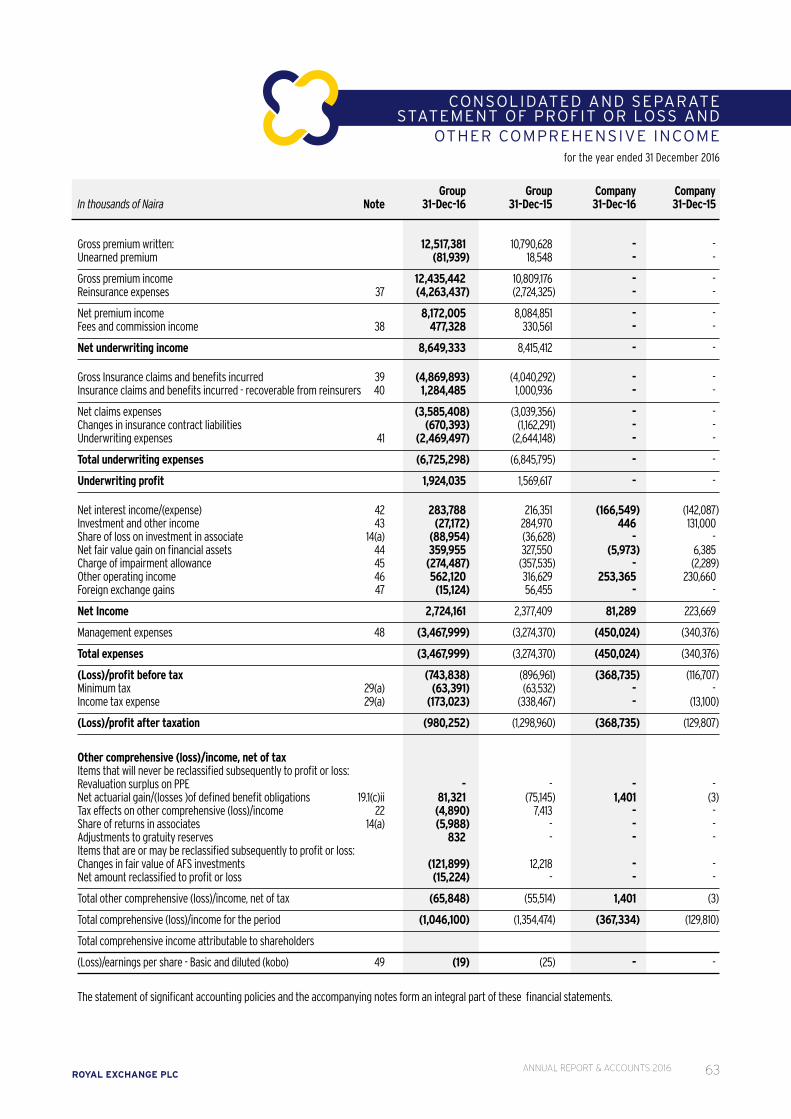

Consolidated and Separate Statement of Profit or Loss and Other Comprehensive Income 63

Statement of Change in Equity - Group 64

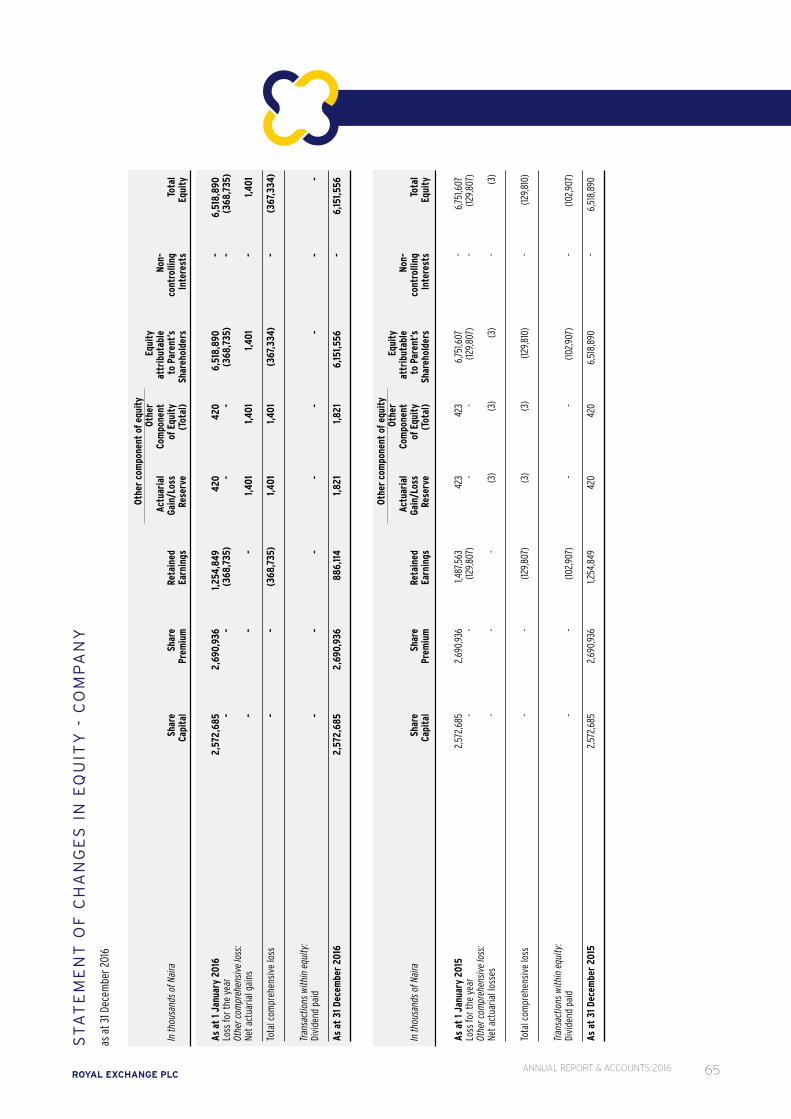

Statement of Change in Equity - Company 65

Consolidated Statement of Cash Flows . 66

Notes to the Consolidated Financial Statements 68-186

Statement of Value Added 188

Financial Summary - Group 189

Financial Summary - Company 190

Management (Group and Subsidiaries) 192-197

Branch/Office Network cum Directory 198

Friendship Centre Network 199

Corporate Events 200-201

Notes 202

CONTENTS

ROYAL EXCHANGE PLC4 ANNUAL REPORT & ACCOUNTS 2016

WHO WE ARE

OUR VALUES

C - Customer orientationC - CreativityI - IntegrityL - Learning organisationP - ProfessionalismT - Teamwork

VISION STATEMENT

“To responsibly and efficiently mobilize and utilize human, financial and technological capital to exceed stakeholders expectations”.

MISSION STATEMENT

“To attain leadership in the financial sector and provide the highest quality services in accordance with ethical practices and norms to our clients, while ensuring adequate returns to our stakeholders”.

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 5

DIRECTORSChairman - Mr. Kenny Ezenwani Odogwu

Non-Executive Directors - Chief Anthony Ikemefuna Idigbe (SAN) Mr. Daniel Maegerle (Swiss) Chief Uwadi Okpa-Obaji Alhaji Ahmed Rufa’i Mohammed Alhaji Rabiu Muhammad Gwarzo, OON Mr. Adeyinka Ojora

Group Managing Director - Alhaji Auwalu Muktari

Group Company Secretary - Ms. Sheila Ezeuko

REGISTERED OFFICE - 31, Marina, Lagos

AUDITORS - KPMG Professional Services

BANKERS - Access Bank Plc Diamond Bank Plc Ecobank Plc FCMB Plc First Bank of Nigeria Plc Guaranty Trust Bank Plc Heritage Bank Plc Stanbic IBTC Bank Plc Keystone Bank Ltd Mainstreet Bank Ltd (Now Skye Bank Plc) Sterling Bank Plc UBA Plc UBN Plc Wema Bank Plc Zenith Bank Plc

REGISTRARS - CardinalStone (Registrars) Limited, 358, Herbert Macauley Street, Yaba, Lagos.

RC NUMBER. - 6752

CORPORATE INFORMATION

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC6

In 1918, our company started operations in Nigeria represented by Barclays Bank DCO and on February 28, 1921 converted to a full branch of its then parent company, Royal Exchange Assurance, London.

Royal Exchange Assurance, London was originally founded in 1720 and was one of the first two insurance companies in Britain to receive legal status via Royal Charter. Originally established for marine business, it expanded within a year to include fire and life insurance as well, thereby becoming Britain’s first composite insurer. The establishment of its branch in Nigeria was the result of an overseas expansion drive in the early 20th century.

Some notable figures in the local insurance industry have headed our company, which was, for over twenty years, the only insurance company operating in Nigeria. Thus, our company can be said to be the beginning of insurance in Nigeria and today, has one of the largest branch networks in its sector, with thirty-three branches, two friendship centers and ten sales outlets.

Pursuant to Section 396(2) of then companies Act of 1968, our company was on December 29, 1969, reconstituted and incorporated as a private limited liability company, Royal Exchange Assurance (Nigeria) Limited. The company went public July 18, 1989 and was duly listed on the Nigerian Stock Exchange on December 3, 1990.

In June 2007, our company entered into a merger with African Prudential Insurance Company and Phoenix of Nigeria Assurance Company Plc. The merger brought about a significantly stronger company, better positioned to serve the needs of its clientele in the financial services sector.

In June 2008, our company was re-organized into a Group Structure, whereby it assumed the role of a group holding and asset management company to execute its strategic vision for financial services, namely insurances, funds management, finance and banking, through its six wholly owned subsidiaries namely:• Royal Exchange General Insurance Company Limited

established in January 2008, to carry on the non-life insurance business of the group;

• Royal Exchange Prudential Life Plc, established in February 2007 to carry on life assurance business of the group;

• Royal Exchange Finance & Asset Management Limited (previouly called Royal Exchange Finance & Investment Ltd) was incorporated as a wholly-owned subsidiary of Royal Exchange Plc in October 2004 and licensed in April 2005 by Central Bank of Nigeria, to carry on the finance and assets management functions of the group;

• Royal Exchange Healthcare Limited, established in May 2006 to provide health management services and healthcare insurance;

• Royal Exchange Microfinance Bank Limited, established in July 2009 and licensed to carry on the business of assisting all enterprises engaged in small scale industries, micro economic activities and co-operative related endeavors;

All subsidiaries are properly licensed by their respective regulators and are structured to fully exploit the significant opportunities available in the Nigerian economy.

The Royal Exchange brand is a notable brand in Nigeria especially in the field of insurance. The company will ensure its continued relevance in the environment in which it operates by continuously re-inventing its products and services.

OUR DIRECTORS:

ROYAL EXCHANGE PLC 1. Mr. Kenny Ezenwani Odogwu - Chairman2. Chief Anthony Ikemefuna Idigbe (SAN) - Director 3. Mr. Daniel Maegerle (Swiss) - Director4. Chief Uwadi Okpa-Obaji - Director5. Alhaji Ahmed Rufa’i Mohammed - Director6. Alhaji Rabi’u Muhammad Gwarzo, OON - Director 7. Mr. Adeyinka Ojora - Director 8. Alhaji Auwalu Muktari - Group Managing Director

ROYAL EXCHANGE GENERAL INSURANCE COMPANY LIMITED (REGIC)1. Alhaji Auwalu Muktari - Chairman2. Mr. Benjamin Agili - Managing Director 3. Mr. Donald Nosiri - Director4. Mr. Nelson Akerele - Director 5. Mr. Austin Nwankwo - Director6. Mr. Ejike Osisioma - Director

ROYAL EXCHANGE PRUDENTIAL LIFE PLC (REPRU)1. Alhaji Auwalu Muktari - Chairman2. Mr. Olawale Banmore - Managing Director3. Mr. Adekunle Kasim - Director4. Mr. Nelson Akerele - Director5. Dr. Pius Ofulue - Director6. Mr. Ben Azi - Independent Director

ROYAL EXCHANGE HEALTHCARE LIMITED (REHL)1. Alhaji M. S. Hammid (fwc) - Chairman2. Dr. Pius Ofulue - Managing Director3. Alhaji Auwalu Muktari - Director4. Mr. Olawale Banmore - Director5. Mr. Nnamdi Melie - Director6. Mrs. Jane Ekomwereren - Director7. Mr. Ben Azi - Independent Director

ROYAL EXCHANGE FINANCE AND ASSET MANAGEMENT LIMITED (REFAM)1. Alhaji Auwalu Muktari - Chairman2. Mr. Abiola Sanni - Managing Director3. Mr. Benjamin Agili - Director4. Mr. Olawale Banmore - Director

ROYAL EXCHANGE MICROFINANCE BANK LIMITED (REMFB)1. Alhaji Auwalu Muktari - Chairman2. Mrs. Elizabeth Elghoche - Managing Director3. Mr. Abiola Sanni - Director4. Mr. Ben Azi - Independent Director

CORPORATE PROFILE

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 7

Group Parent 2016 2015 % 2016 2015 % =N=’000 =N=’000 Growth =N=’000 =N=’000 Growth

MAJOR STATEMENT OF COMPREHENSIVE INCOME ITEMS Gross Premium Written 12,517,381 10,790,628 16.00 - - Gross Premium Income 12,435,442 10,809,176 15.05 - - Net Premium Income 8,172,005 8,084,851 1.08 - - Investment and Other Income 800,126 807,792 (0.95) 81,289 223,669 (63.66)Loss Before Tax (743,838) (896,961) 17.07 (368,735) (116,707) (215.95)

Loss for the period (980,252) (1,298,960) 24.54 (368,735) (129,807) (184.06)

2016 2015 2016 2015 =N=’000 =N=’000 =N=’000 =N=’000

MAJOR STATEMENT OF FINANCIAL POSITION ITEMS Total Assets 31,676,729 26,525,242 19.42 9,810,075 8,889,570 10.35Insurance Contract Liabilities 10,158,280 8,263,204 22.93 - - - Investment Contract Liabilities 339,456 336,271 0.95 - - -

RESULTS AT A GLANCE

(2,000,000)

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

GrossPremiumWri6en

GrossPremiumEarned

NetPremiumIncomeInvestmentandOtherIncome

ProfitBeforeTax Profit/Lossfortheperiod

Thou

sand

sofN

aira

Group-MajorStatementofComprehensiveIncomeItems

2016₦'000

2015₦'000

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

TotalAssets InsuranceContractLiabili:es InvestmentContractLiabili:es

Thou

sand

sofN

aira

Group-MajorStatementofFinancialPosi;onItems

2016₦'000

2015₦'000

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC8

RESULTS AT A GLANCE

-400,000

-300,000

-200,000

-100,000

-

100,000

200,000

300,000

InvestmentandOtherIncome ProfitBeforeTax Profit/Lossfortheperiod

Parent-MajorStatementOfComprehensiveIncomeItems

2016₦'000

2015₦'000

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

TotalAssets

Thou

sand

sofN

aira

PARENT-MajorStatementofFinancialPosi<onItems

2016₦'000

2015₦'000

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 9

NOTICE OF AGM

ORDINARY BUSINESS:

1. To lay before the meeting, the Consolidated Financial Statements of the Group for the year ended December 31, 2016 together with the Reports of the Directors, the Audit Committee and the Auditors thereon.

2. To re-elect directors.

3. To approve the remuneration of the directors.

4. To authorize the directors to fix the remuneration of the auditors.

5. To elect shareholders as members of the Statutory Audit Committee.

BY ORDER OF THE BOARD

SHEILA EZEUKO COMPANY SECRETARY/GM (LEGAL SERVICES)FRC/2013/NBA/00000004059

New Africa House31, Marina, Lagos.

September 25, 2017

NOTICE is hereby given that the Forty-Eighth Annual General Meeting of Royal Exchange Plc will be held at the Al’Murjan Hall, Bristol Palace Hotel Ltd., 54/56 Guda Abdullahi Street, Farm Center, Kano, Kano State on Thursday, 19th October, 2017 at 11.00 o’clock in the forenoon to transact the following business:

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC10

NOTES

• Proxy

A member of the company entitled to attend and vote is allowed to appoint a proxy to attend and vote in his/her stead. A proxy need not be a member of the company. A proxy form is contained in the Annual Report and Accounts. If it is to be valid for the purpose of the meeting, it must be completed, detached, duly stamped at the office of the Commissioner for Stamp Duties and deposited at the office of the Registrars, CardinalStone (Registrars) Limited, 358, Herbert Macauley Street, Yaba, Lagos, not later than 48 hours before the time appointed for holding the meeting.

• Dividend Warrants

The company will not recommend any dividend for the year ended December 31, 2016.

• Closure of Register of Members and Transfer Books

The Register of Members and the Transfer Books will be closed from 5 October, 2017 to 11 October, 2017, both dates inclusive.

• Appointment of Members of the Audit Committee

Any member may nominate a shareholder as a member of the Audit Committee of the company, by giving notice in writing of such nomination to the Company Secretary, at least 21 (Twenty-One) days before the Annual General Meeting.

• Unclaimed Share Certificates and Dividend Warrants

The company notes that some share certificates have been returned, marked “unclaimed”. The company notes further that some dividend warrants sent to shareholders are yet to be presented for payment.

Therefore, all shareholders with unclaimed share certificates should write to The Registrars, CardinalStone (Registrars) Limited, the Company Secretary or call at the registered office of the company during normal working hours.

Furthermore, all shareholders with unclaimed dividend warrants Nos. 1 – 12 should address their claims to the Company Secretary or call at the registered office of the company during normal working hours for processing of their claims or assistance. Shareholders, with unclaimed dividend warrants Nos. 13 – 17 should address their claims to The Registrars, CardinalStone (Registrars) Limited.

Members are urged to advise the Registrars or the Company Secretary of any change of address or situation particularly as it relates to share certificates and dividend warrants.

• Right of Securities’ Holders to ask Questions

Securities’ Holders have a right to ask questions not only at the Meeting, but also in writing prior to the Meeting, and such questions must be submitted to the company on or before 14th day of October, 2017.

NOTICE OF AGM

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 11

Tear off from here

The Annual General Meeting of Royal Exchange Plc to be held at the Al’Murjan Hall, Bristol Palace Hotel Ltd., 54/56 Guda Abdullahi Street, Farm Center, Kano, Kano State, on Thursday, 19th October, 2017 at 11.00 am in the forenoon.

I/We………………………………. being a member/members of Royal Exchange Plc hereby appoint …….…….………...................………………………………………or failing him, the chairman of the meeting as my/our proxy to vote for me/us and on my/our behalf at the 48th Annual General Meeting of the Company to be held on Thursday, 19th October, 2017 and at every adjournment thereof.

Dated this 25th day of September, 2017.

NOTES:

1. Please indicate with an ‘X’ in the appropriate squares how you wish your votes to be cast on the resolutions set out above.

2. A member (shareholder) who is unable to attend the Annual General Meeting is allowed to vote by proxy. The above proxy form has been prepared to enable you to exercise your right to vote in case you cannot personally attend the meeting. Members wishing to vote by proxy should please ensure that the appropriate stamp duties due on the proxy form are paid. The proxy must produce the “Authority to Admit”, attached to this form to gain entrance to the Meeting.

3. Provision has been made on this form for the Chairman of the meeting to act as your proxy. However, if you so wish, you may insert in the space provided on the form, the name of any person whether a member of the company or not who will attend the Meeting and vote on your behalf.

4. Please sign the above proxy form and post it so as to reach The Registrars, CardinalStone (Registrars) Limited, 358, Herbert Macauley Street, Yaba Lagos, not later than 48 hours before the appointed time for holding the meeting. If executed by a corporation, the proxy form must bear the common seal of such corporation.

Nos. RESOLUTIONS FOR AGAINST

1. To re-elect Chief Anthony Idigbe (SAN)

2. To re-elect Mr. Daniel Maegerle

3. To fix the remuneration of directors 4. To authorize the directors to fix the remuneration of auditors 5. To elect members of the Audit Committee

AUTHORITY TO ADMIT

Please admit …………………………………………………………. at the 48th Annual General Meeting of Royal Exchange Plc to be held at the Al’Murjan Hall, Bristol Palace Hotel Ltd., 54/56 Guda Abdullahi Street, Farm Center, Kano, Kano State on Thursday, 19th October, 2017, 11.00 am in the forenoon.

SHEILA EZEUKOCOMPANY SECRETARY/GM (LEGAL SERVICES)FRC/2013/NBA/00000004059

NOTES:

1. This authority to admit must be produced by the shareholder or his/her proxy in order to gain entry to the venue of the Annual General Meeting

2. Shareholders or their proxies must sign this authority for admission before attending the Meeting.

………………………………….............…Signature of person attending

FOR REGISTRAR/COMPANY USE ONLY

NAME OF SHAREHOLDER:

NUMBER OF SHARES:

CAUTION: TO BE VALID THIS FORM MUST BE STAMPED ACCORDINGLY

BEFORE POSTING THE ABOVE CARD PLEASE TEAR OFF THIS PART AND RETAIN IT.

PROXY FORM

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC12

Tear off from here

Please AffixPostage Stamp

Here

The Registrar,CardinalStone (Registrars) Limited,358, Herbert Macauley Street, Yaba, Lagos.

PROXY/AUTHORITY TO ADMIT

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 13

To:

The Registrar, CardinalStone (Registrars) Limited, 358, Herbert Macauley StreetYaba, Lagos.

ROYAL EXCHANGE PLCREQUEST FOR E-BONUS

I/We hereby request that henceforth, all bonuses due to me/us with respect to my/our shareholding in Royal Exchange Plc be paid directly to my CSCS/stock broker account stated below:

Account Details:

Shareholder Account No: (Please look on the left hand corner of our certificate for your shareholder account number)

Name of Shareholder:

Address of Shareholder:

Investor’s Account No:

CSCS Account No. (CHN):

GSM No:

E-mail Address:

Yours faithfully,

Signature: ) Corporate shareholders ) should please affix sealName: ) here and state RC No. For Joint Shareholders

Signature: ) Name: ) ) of Shareholder

Signature: ) Name: ) ) of Shareholder

Signature: ) Name: ) ) of Shareholder

Official stamp and authorized signatures of stockbroker

1. Signatory: Seal of stockbroker

2. Signatory:

IMPORTANT NOTICE

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC14

Please AffixPostage Stamp

Here

The Registrar,CardinalStone (Registrars) Limited,358, Herbert Macauley Street, Yaba, Lagos.

IMPORTANT NOTICE

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 15

MANDATE FOR E-DIVIDEND PAYMENT

NAME OF COMPANYACORN PET. PLCAFRIK PHARMACEUTICALS PLCAG HOMES SAVINGS & LOANSAG LEVENTISARBICO PLCASHAKACEM PLCBANKERS WAREHOUSEBETA GLASSCAPITAL HOTEL PLCELLAH LAKESEVANS MED PLCFCMB BONDFCMB GROUP PLCFIDSON BONDG. CAPPA PLCGUINEA PLCIMB ENERGY MASTER FUNDJOS INT. BREWERIES PLCKOGI SAVINGS & LOAN LTDLAFARGE AFRICA PLCLAFARGE BONDLAW UNION & ROCK PLCLEGACY FUNDLIVESTOCK FEEDS PLCMORISON PLCMRS OIL PLCNAHCO BONDNAHCO PLCNEWPAK PLCN.G.C PLCNGC STERILENPF MICROFINANCE BANKNULEC INDUSTRIES PLCOKOMU OIL PALM PLCPREMIER PAINT PLCREAN PLCSKYE BANK PLCTOTAL NIG. PLCTRANEX PLCWOMEN INVESTMENT FUND

TICK ACCOUNT NO.SHAREHOLDER’S

S L

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC16

Please AffixPostage Stamp

Here

The Registrar,CardinalStone (Registrars) Limited,358, Herbert Macauley Street, Yaba, Lagos.

MANDATE FOR E-DIVIDEND PAYMENT

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 17

STATEMENTS & REPORTS

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC18

Distinguished fellow shareholders, members of the board of directors, ladies and gentlemen.

It is my pleasure to welcome you to the 48th Annual General Meeting of our company, taking place this 19th Day of October, 2017 here in Kano. I am pleased to present an overview of the 2016 macroeconomic environment, a review of our operating results for the year and synopsis of our expectations for 2017, all for your consideration, and in accordance with the mandate of my office as Chairman.

MACROECONOMIC REVIEWThe global economy decelerated in the final quarter of 2016 due to a combination of improved conditions in emerging market countries and stronger growth in developed economies. It expanded 2.7% year-on-year in Q4, above the 2.5% rise in Q3 and the strongest print in the full year. Q4’s strong reading brought total growth for 2016 to 2.6%, a notch above the 2.5% previously forecast but well below 2015’s 3.0%. Despite the deceleration in 2016, the global economy managed to navigate its way through troubled waters and perform at a still decent rate. Geopolitical risks remained high in 2016 as a result of the Brexit vote, a still-inflamed Middle East, the impeachment of Dilma Rousseff in Brazil and the election of Donald Trump in the U.S. presidential elections, among others. Challenging weather conditions, led by a severe El Niño weather effect, seriously damaged the agricultural sector in some countries, particularly in emerging markets.

This year, many developed economies are still benefiting from accommodative monetary policies due to the low global inflation environment. While cheap money is buttressing business and consumer confidence, ultra-low interest rates cannot last forever. This situation is raising doubts about how authorities will stimulate these economies once inflation starts to take off. The main exception is the United States, where an already well-performing economy could receive a further boost if a new stimulus plan is approved by President Trump. This situation could force the Federal Government to accelerate the pace of its monetary policy tightening, which would reverberate across the world mostly via rising volatility in the financial and exchange rate markets.

Economic dynamics among developing economies are gradually improving following some quarters of sluggish growth. The increase in commodity prices that started in the final quarter of 2016 is good news for the majority of emerging market nations. That said, the recovery in raw material costs is expected to be limited, thereby hampering the possibility of a sharp and sustained recovery. Against this backdrop, many governments will have to continue dealing with tough fiscal positions and the need for structural reforms appears inevitable.

CHAIRMAN’S STATEMENT & REPORT

MR. KENNY EZENWANI ODOGWU - Chairman

Despite the daunting challenges posed by the hostile operating environment, Royal Exchange Group was able to deliver a mixed result in 2016 through cost optimization initiatives, innovation in key categories and extensive retail market expansion, all of which helped to offset further deterioration of margins during the year.

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 19

CHAIRMAN’S STATEMENT & REPORT

Across Sub-Saharan Africa, growth slowed markedly in 2016 to 1.5%, and is projected to recover moderately in 2017 to 2.6%. However, the recovery remains fragile with most of the uplift coming from Africa’s three largest economies – Angola, Nigeria and South Africa – as they rebound from a sharp slowdown in 2016.

With rising debt levels and an environment of tighter and more volatile financial conditions, many African countries face the challenge of undertaking their much-needed development spending without jeopardizing their hard-won debt sustainability.

Nigeria’s economy continued to weaken in the third quarter. GDP contracted 2.24% year-on-year in Q3, marking a sharper drop than the 2.06% decline observed in the previous quarter.

The third quarter reading was underpinned by a contraction in the oil sector, largely due to militant attacks on oil infrastructure. Oil output in Q3 slid to 1.63 million barrels per day (mbpd) from 1.69 mbpd in Q2, which marks the fourth quarterly decline. Compared to the same quarter of the previous year, oil output declined 24.9% (Q3 2015: 2.17 mbpd) and the oil industry has contracted 22.01%.

From an average 9.0% in 2015, inflation averaged 15.66% over the year 2016, rising from 9.6% in January to 18.55% at the latest print in December. Much of this has been structural rather than demand driven, with hikes to energy tariffs, the removal of fuel subsidies and the depreciation of the naira on the black market being principally responsible.

In its final Monetary Policy Committee meeting for 2016, the Central Bank of Nigeria (CBN) held its main interest rate, the Monetary Policy Rate (MPR), at 14% in November, retaining its tighter monetary stance, which began with a two percentage point rate hike at its July meeting.

Nigeria’s unemployment situation deteriorated in Q3 2016, with unemployment rate rising to 13.9% from 13.3% as at Q2 2016. This represents the eight consecutive rise in unemployment rate since Q4, 2014.

Gross official external reserves as at December 2016 stood at $25.84 billion compared with opening levels of $29.07 billion. The depletion was triggered by market interventions made by the CBN in a bid to stabilize the naira exchange rate. This left the country’s external reserves vulnerable to absorbing less than six months of imports.

The local currency was under persistent pressure both at the interbank and parallel foreign exchange markets throughout 2016 owing to acute shortage of the dollar.

Over the year, the naira has seen a drastic depreciation in value, moving from =N=197/$ to =N=282/$ at the launch of the current “floating” foreign exchange rate policy in June 2016.

As at December 31st 2016, the interbank exchange rate closed at =N=305/$, about 8% weaker than in June. At the parallel market, the exchange rate weakened significantly to around =N=490/$ on December 30th compared to around =N=278/$ and =N=352/$ respectively at the beginning of the year and June. The weakening of the local unit at the parallel market took the spread or premium between the two market rates to a high of =N=185 at the end of 2016 compared to about =N=110 at the beginning of the year.

The socio-political scene witnessed several developments The 2016 budget passage was delayed after the two arms of the National Assembly (the Senate and House of Representatives) discovered it was full of inaccuracies. The budget titled ‘Budget of Change’ was eventually signed by President Muhammadu Buhari on May 6 after the Senate had passed it earlier on March 23. The delay was caused by accusations and counter-accusations by both the Legislature and Executive that the budget contained inaccurate figures.

In May, the Federal Government announced that a litre of petrol would be sold for =N=145 from the previous price of =N=98. Nigerians reacted to the hike with mixed feelings which led to a failed attempt by the Nigerian Labour Congress (NLC) to organise a nationwide strike.

The anti-corruption drive of the administration gained further traction in 2016. In what it described as a sting operation, the Department of State Services raided the houses of some judges in different parts of the country between October 7 and 8, 2016. The operation saw four serving judges, including two Justices of the Supreme Court, arrested for alleged corruption allegations.

The insurance sectorThe insurance sector, like other sectors of the economy shared in the negative effects of the economic recession which left many businesses stagnant in 2016. However, industry also reaped the fruit of improved awareness of insurance by Nigerians.

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC20

CHAIRMAN’S STATEMENT & REPORT

The insurance industry’s activities were also slowed down by the effects of the recession as operators lamented that given its usual position as the last in the scale of preference of an average Nigerian, patronage of the industry was at a very low ebb during the year while premium payment suffered major setback in spite of the ‘no premium no cover’ regime in the country.

Apparently, the industry’s abysmal performance had its root cause from the overall poor performance of the economy due to the recession.

The National Insurance Commission (NAICOM) in 2016 made repeated attempts to increase awareness of insurance, in order to deepen insurance penetration, however, the much desired insurance inclusiveness and insurance penetration to the grass root with the proposed introduction of micro-insurance, was not totally achieved even though the Commission introduced guidelines for the operation of “Takaful”, a model of micro-insurance based on Islamic principles.

Towards the end of the year, NAICOM introduced the use of alternative channels of distribution tagged Referral/Partners/agents, while it suspended previously existing alternative channels for security reasons.

Though insurers in 2015 celebrated timely premium payment by the Federal Government for its workers’ group Life Insurance, 2016 contrarily witnessed delay in payment of Group life insurance by government as up till date, the Federal Government is yet to fulfill its annual insurance (group life insurance) obligations to the federal civil servants as well as the renewal of insurance of its assets located in various parts of the country.

A plan to increase the capital base of underwriters was mooted in 2016 and we strongly believe that NAICOM will follow up this plan in 2017 in order to increase the competitiveness of insurance companies and make them to underwrite bigger projects. Meanwhile, as the directive for recapitalization of insurance companies is still being awaited, NAICOM, however, has recorded a pass mark in instilling good corporate governance on the operators.

The Commission also took a major step in its bid to place Nigeria insurance industry on the global best practices pedestal through the introduction of the Risk Base Supervision (RBS) model. NAICOM, has released a blue print document for the implementation of the model for the insurance industry.

The clamour for greater government’s participation and enforcement of compulsory insurance regulations as provided by the Market Development and Restructuring Initiative (MDRI) will be most likely one of the top agenda items and policy thrust for NAICOM in 2017.

OPERATING RESULTSDespite the daunting challenges posed by the hostile operating environment, Royal Exchange Group was able to deliver a mixed result in 2016 through cost optimization initiatives, innovation in key categories and extensive retail market expansion, all of which helped to offset further deterioration of margins during the year.

During the period under review, your company generated gross written premium of =N=12.52billion, while that of the preceding year was =N=10.79billion, an increase of 16%. Claims expense for the year amounted to =N=3.59billion in comparison with =N=3.04billion reported in 2015; signaling an increase of 18%. Underwriting expenses decreased by 7% from =N=2.64 billion in 2015 to =N=2.47 billion in 2016. Provisions of =N=670million were made to cater mainly for our Life insurance contract liabilities during the year against the sum of =N=1.16billion, provided in the previous year of 2015. These translated into net income before overhead expenses of =N=2.72billion, an increase of 14% when compared with 2015 value of =N=2.38billion.

Management expenses were =N=3.47billion in 2016 in comparison with =N=3.27billion in 2015 showing an increment of 6%. The increase is largely due to cost of doing business which spiked during the year.

EXPECTATIONS FOR 2017The outlook for 2017 will depend, largely, on the quality of policy and on the effective implementation of various reform initiatives of the Federal Government of Nigeria. Ability of Government to curb or substantially reduce militancy activities in Niger Delta in 2017 would go a long way in boosting oil production and improving foreign exchange earnings and Government’s revenues.

Another important area of emphasis in 2017 is the diversification of the non-oil sector. The 2017 budget will seek to encourage local production, by optimizing the use of local content and empowering local businesses. Related to this are the ongoing efforts to upgrade Nigeria’s infrastructure, in order to enhance long-term growth, capital flows and development.

During 2017, most economic variables, real growth, inflation and exchange rate, can be expected to improve towards conditions prevalent in 2015 when inflation was a single digit while real growth was just below three percent, and the naira exchange rate was about =N=200/US$.

Worthy of mention is the Economic Recovery and Growth Plan that was recently launched by the Federal Government. Effective implementation of this this plan will help to tackle the constraints to growth and improve the overall business environment.

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 21

CHAIRMAN’S STATEMENT & REPORT

Ultimately, rebuilding Nigeria’s external reserves, improving the liquidity of the foreign exchange market, strengthening the Naira, managing interest rates and inflation, developing vital infrastructure and the growth of the non-oil sector will remain critical success factors for 2017. The bright outlook could be threatened by any adverse shock to oil price or oil production.

Focusing more specifically on your Company, Royal Exchange in 2017 we will be consolidating the initiatives that we started in 2016, support growth and working capital and restructuring across the group.

As always, Royal Exchange stays abreast with many of the initiatives mentioned above in our quest to grow market share and attain market leadership position. The group is presently streamlining major components of her businesses, service delivery, processes and operations to deliver superior returns in the short-term to our shareholders. This we believe will reposition our great Company as not only a major industry player but as a potential game changer.

To sum it up, your board is confident about the future of our company.

DIVIDENDSThe Board of Directors do not recommend the payment of a dividend for the year ended December 31, 2016.

CONCLUSION

Future OutlookDistinguished shareholders, I am confident that your company is already on the path of sustainable growth and profitability. As we look forward to improved performance in the years ahead, I seek your understanding and cooperation with the Board and management in their concerted efforts to further improve the fortunes of the Company.

The management and staff of the Company are highly commended for their deep sense and display of loyalty, commitment, honesty and dedication to duty during the year under review. The Board assures you of its continued commitment to the delivery of optimal returns whilst keeping the company a responsible corporate citizen of our great nation, Nigeria.

Finally, I must also appreciate our esteemed clients, agents and brokers for their patronage and shareholders for the trust bestowed upon the Board. We assure you of our commitment to you always and continue to solicit your support now and always.

The future of our company and our plans for 2017 are well on course notwithstanding the vulnerabilities imminent in our domestic economy.

Thank you.

Kenny Ezeanwani OdogwuChairman

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC22

AUWALU MUKTARI- Group Managing Director

GROUP MANAGING DIRECTOR’S

STATEMENT

GROUP MANAGING DIRECTOR’S BUSINESS REVIEWDistinguished Shareholders, members of the Board of Directors and Colleagues, it is my pleasure to present to you the report of our stewardship for the financial year ended 2016. The Nigerian economy continues to be dominated by a range of structural problems, specifically volatile oil production, lack of optimal FX liquidity, weak fiscal policy and governance issues for the major part of 2016.

Nigeria major source of revenue, oil production stabilized somewhat at around 1.7mn b/d, having dropped significantly to 1.4mn b/d mid-year, from an estimated 2.17mn b/d in February 2016.

At current level, oil production remains below the 2016 budget projection of 2.2mn b/d owing to spate of attacks by militants (Niger Delta Avengers) after initial talks for a ceasefire failed.

The Nigerian economy entered economic recession in 2016 and the insurance sector, like other sectors of the economy shared in the negative effects of the economic recession which left many businesses stagnant during the year under review. A delay in the passage of the National Budget resulted in delayed payment of insurance premium, as the government are the major buyers of insurance in Nigeria. This led to attendant challenges for insurance companies and businesses operating in the country. However, industry also reaped the fruit of improved awareness of insurance by Nigerians, while National Insurance Commission (NAICOM) was equal to the task in ensuring improvement in corporate governance and the introduction of Risk Based Supervision in 2016 shows the seriousness of the regulator to ensure business sustainability within the insurance sector of the economy.

For the group, the board and management of Royal Exchange remained resolute in accomplishing its long term strategic objectives. Our Company continued through the year 2016 with her Strategic Plan aimed at steering the company towards market leadership. We shall continue to proactively take measures to mitigate the impact of the

During the year, Royal Exchange kept to its promise of being a socially responsible corporate citizen by engaging in insurance education and advocacy. In future, we intend to be more active in promoting Micro insurance to bridge insurance needs of the yearning public.

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 23

GROUP MANAGING DIRECTOR’S

STATEMENT

adverse business environment by continuing to drive change in our business processes and strategies. Having said all these, our loss position for the year is not reflective of a poor performance, but rather the need to accommodate mandatory provisioning in respect of our Life insurance business as recommended and in accordance with global best practices.

Our performance for the year 2016 at Royal Exchange was a good show of spirit and tenacity. At the Group level, business retention levels were solid giving room for us to focus on our new business areas. Our revenue diversification, away from traditional markets, might still be at its preliminary stages but we are recording good progress in deepening our tentacles in some frontier markets; most especially retail business. Looking at the figures, our top line rose 16% year-on-year from =N=10.79 billion in 2015 to =N=12.52 billion in 2016. Results from core operating activities grew with underwriting profit increasing by 22% from =N=1.57 billion in the corresponding year to =N=1.92 billion in 2016. However, management expenses was tamed, only able to rise by 6% year-on-year to =N=3.47 billion in 2016 despite unexpected surge in the cost of doing business during the year.

A Loss before tax of =N=743.84 million was reported in 2016. As pointed out above, the occurrence of this loss is traceable to a =N=0.670 billion provisions made to Insurance contract liabilities during the year as well as impairment charges recognized. Our Healthcare, Microfinance bank and Royal Exchange Prudential Life posted negative figures due to hostile business environment during the year.

Moving ahead, we reassure our shareholders of more stringent cost monitoring measures in place in the forthcoming year to improve our efficiency levels. The Group is investing in products and driving new product launches. We have also gone far in setting up another micro-insurance subsidiary called Royal Exchange Takaful Insurance Ltd. This we believe will improve our margin considerably. Regulatory approval is almost concluded. These self-help actions are progressing to plan and some further actions are being taken to drive profitable medium-term growth despite uncertain market conditions. The management remains confident about the Company’s future as it is stable and looks promising.

At subsidiary level, our objectives were clear and precise; continue to expand the market share for our core insurance subsidiaries and ensure a sustained increase in the contributions of our non-core insurance businesses i.e. asset management and microfinance banking divisions to the pool. On our insurance businesses, growth was extended through our retail footprint with on-going creation of new alliances and engagement in key strategic partnerships.

Generally, bottom-line performances were down in some of our subsidiaries due to a very volatile business operating environment. Notwithstanding, the board and management are determined to reverse this trend especially for our life business, Royal Exchange Prudential Life Plc, which was a major drag on our profitability for the year. OPERATING RESULTS

GROUPThe company’s wholly owned subsidiaries at the end of 2016 were:(a) Royal Exchange General Insurance Company Ltd(b) Royal Exchange Prudential Life Plc(c) Royal Exchange Healthcare Ltd(d) Royal Exchange Finance & Asset Management Ltd(e) Royal Exchange Microfinance Bank Ltd

Royal Exchange General Insurance Company LimitedRoyal Exchange General Insurance Company Limited (REGIC) being the major income earner of the group contributed about 70% of the gross earning of the group.

Gross Premium Income (GPI) at =N=8.76 billion rose 26% above 2015 results of =N=6.97 billion. Without the considerable cutbacks by government on its annual insurance spend, the premium collected would have surpassed the amount recorded. Reinsurance cost year –on-year rose by 72% impacting negatively on net premium earned. Net premium income of =N=4.78 billion was recorded in the year; 3% higher than that of 2015.

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC24

GROUP MANAGING DIRECTOR’S

STATEMENT

Net Claims incurred (excluding reinsurance recoverable) was =N=1.72 billion as against =N=1.48 billion recorded in 2015 displaying an increase of 16%. The company’s claims ratio also dropped marginally from 21% in 2015 to 20% in 2016.Underwriting expenses at =N=1.88 billion declined by 12% over 2015 levels. Hence, we recorded an underwriting profit of =N=1.61 billion in 2016, as against =N=1.32 billion in 2015.

Management expenses at =N=1.89 billion increased marginally by 16% against 2015 levels.

Consequently, a profit before tax of =N=285.40 million is reported for the company in 2016.

Royal Exchange Prudential Life PlcDespite the challenges of 2016 especially for Life underwriters, Royal Exchange Prudential Life was able to maintain her growth potential within the group.

Gross Premium Income at =N=3.47 billion dropped marginally by 3% in comparison with 2015. However, underwriting profit spiked from =N=225 million in 2015 to =N=464 million in 2016 even with the provisions of =N=0. 706 billion made in respect of life insurance contract liabilities.

Management expenses at =N=1.11 billion was 11% lower than =N=1.24 billion recorded in 2015. The reduction in management expenses was attributed to operational efficiency and cost optimization during the year. Consequently, the company realized a Loss before tax of =N=616 million in 2016.

Royal Exchange Healthcare LtdGross written premium dipped by 31% to =N=288 million in 2016 from =N=419.8 million in 2015.

Gross Underwriting expenses rose slightly by 9% to =N=348 million in 2016 as against =N=319 million in 2015 as a result of large medical claims incurred during the period. Operating expenses declined by 13% from =N=130 million in 2016 to =N=150 million in 2015.

A loss before tax of =N=103.7 million is reported for 2016.

Royal Exchange Finance & Asset Management LtdThe Company achieved total income of =N=229 million as against =N=162 million in 2015, an increase of 41%.

The Company re-energized its credit creation business during the year 2016 and this resulted in an improved bottom line for the Company.

A profit before tax of =N=51.0 million is reported for 2016 as against =N=9 million in 2015.

Royal Exchange Microfinance Bank LtdThe audited account shows a total income of =N=73 million in 2016, within close proximity of its 2015 level at =N=77million with a dip of 5%.

Operating expense increased from =N=67 million in 2015 to =N=84 million in 2016. Loss before tax of =N=11 million is reported for 2016 as against a profit of =N=9 million in 2015.

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 25

GROUP MANAGING DIRECTOR’S

STATEMENT

CORPORATE SOCIAL RESPONSIBILITYDuring the year, Royal Exchange kept to its promise of being a socially responsible corporate citizen by engaging in insurance education and advocacy. In future, we intend to be more active in promoting Micro insurance to bridge insurance needs of the yearning public.

CONCLUSIONFor the future that we behold, our goal is to continuously redefine, reinvent and differentiate ourselves in the marketplace. The focus would be on achieving long-term sustainable growth for our company through the deepening of our revenue base, improving service delivery support systems and at same time keeping a lid on our group-wide costs.

Once again, I use this medium to appreciate the firm commitments of our executive and senior management team as well as staff who put in their best during the year. I am indeed grateful for the trust, contributions and sacrifices made by all in the course of this journey.

Thank you

Auwalu MuktariGroup Managing Director

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC26

INTRODUCTIONRoyal Exchange, with the understanding that corporate governance stands for responsible and transparent management and is essential to achieving its vision, consistently developed corporate policies, standards and governance framework to avoid potential conflicts of interest between all stakeholders with a view to earning and retaining the confidence and trust of its stakeholders. Royal Exchange understands that good corporate governance goes beyond just adhering to rules and policies of the regulators; but also consistently creating value through going the extra mile, hence the Company continually strives to carry out its business operations based on its core values and pledges to safeguard and increase investor value through transparent corporate governance practices.

To ensure consistency in its practice of good corporate governance, Royal Exchange continuously reviews its practice to align with the various applicable Codes of Corporate Governance, such as the Securities and Exchange Commission (SEC) Code and the National Insurance Commission (NAICOM) Code with particular reference to compliance, disclosures and structure and complies with all other requirements.

GOVERNANCE STRUCTURE

The Board Having the right people with an appropriate balance of skills, knowledge and experience is an important aspect of corporate governance. The Board’s size thus provides for sufficient diversity among its members to enable them exercise their business judgment in the best interest of Royal Exchange’s shareholders, while facilitating substantial discussions in which each director can participate meaningfully.

The Board membership comprises eight (8) members, including the Chairman, six (6) Non-Executive Directors, and one (1) Executive Director. The Company is presently in consultation for the appointment of an Independent Director to replace the erstwhile Independent Director. The Independent Director is not expected to have any significant shareholding interest or any special business relationship with the Company.

The Board of DirectorsThe Board of Directors through the Chairman directs the strategic affairs of Royal Exchange and is responsible for the governance of the Company and also accountable to the shareholders for creating and delivering sustainable value through the management of the company’s business. All the current Non-Executive Directors served on the Board throughout 2016. Members of the Board of Directors of the subsidiaries are appointed from the Group Executive Management as well as an independent director for each subsidiary.

In addition to the Board’s direct oversight, the Board exercises its oversight responsibilities through six (6) Committees, namely, Risk Management, Board Investment, Board Strategy, Establishment and Governance, Finance and General Purpose, and the Board Audit.

The Board is required to meet at least four times each year. The Board met seven (7) times in 2016 and the average attendance was 92%.

REPORT OF CORPORATE GOVERNANCE

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 27

Internal OrganizationThere is an effective structure for cooperation amongst the members of the Board, Management and Internal Control functions in Royal Exchange. These structures define the powers and responsibilities of its corporate bodies and employees and are reviewed periodically to ensure proper organization.

The Board is headed by the Chairman. Board members are also subject to standards of business conduct policies, rules and regulations to avoid conflict of interest and use of insider information. The Board appoints committees to help carry out its duties. Given the separation of roles of the chairman and the CEO, the Board appoints Non-Executive Directors as chairmen of Board committees. Board committees work on key issues in greater details than would be possible at full Board meetings, which helps to ensure more effective full Board meetings. Each Board committee reviews the results of its meeting with the full Board.

Board Code of EthicsTo avoid unethical and unwholesome practice and conflict of interest in any business relationship with the Company, the board has established a Code of Business Ethics to provide guidance for the board and staff to maintain strong ethical standards.

Board Performance Evaluation In compliance with the provisions of the Securities and Exchange Commission (SEC) Code of Corporate Governance, the performance of the Board, its committees, the chairman and individual directors was appraised by an independent consultant. Furthermore, an annual board appraisal is also conducted by an Independent Consultant appointed by the Company.

Board Meetings Attendance

Directors Status Designation Attendance % Attendance

Expected Meetings 4

Actual Meetings 7

Mr. K. E. Odogwu Non-Executive Director Chairman 7 100%

Chief A. I. Idigbe (SAN) Non-Executive Director Member 7 100%

Mr. D. Maegerle Non-Executive Director Member 6 86%

Chief U. Okpa-Obaji Non-Executive Director Member 6 86%

Alhaji A. R. Mohammed Non-Executive Director Member 7 100%

Alhaji R. M. Gwarzo, OON Non-Executive Director Member 7 100%

Mr. A. A. Ojora Non-Executive Director Member 7 100%

Alhaji A. Muktari Group Managing Director Member 7 100%

Average Attendance 92%

REPORT OF CORPORATE GOVERNANCE

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC28

CODE OF CORPORATE GOVERNANCE

Board CommitteesIn order to increase the efficiency of its work and enable a more detailed analysis of certain issues, the Board appointed Committees for specific areas from among its members and established terms of reference and rules with respect to delegated authority and reporting to the Board. The primary objective of the Committees is to provide preparatory and administrative support to the Board. The issues considered at Committee meetings are recorded in minutes and reported at the subsequent Board meetings.

The Board has the following standing committees which regularly report to the Board, as well as submit proposals for discussions and decision making.

Establishment and Governance CommitteeThe Committee comprises five (5) members (Four Non-Executives and One Executive) and oversees the Group’s governance and measures its governance program against best practice to ensure that the rights of the shareholders are fully protected. It is also responsible for determining the remuneration of the executive and non-executive members of the Board, nominations for approval of the Board candidates to fill Board vacancies, and for the continuous review of senior management succession plans. To assist in the review of the compensation structures and practices, the Committee has retained its own independent advisor – Leading Edge Consultants.

The Committee met four (4) times with average attendance of 90%.

Audit CommitteeThe Committee comprises of six (6) members made up of three Non-Executives, and three shareholder representatives. The Committee serves as a focal point for the communication and oversight regarding Financial Accounting Reporting, Internal Control and Compliance among Management, as stated in section 359 (6) of the Companies and Allied Matters Act. The Audit Committee, at least annually, reviews the standards of internal control, including the activities, plans, organization and quality of Internal Audit and Group Compliance.

The Committee met five (5) times in 2016 with an average attendance of 88%.

Risk Management CommitteeThe Committee oversees the Group-wide risk governance framework, including risk management and control, risk policies and their implementation as well as the risk strategy and monitoring of operational risks. It reviews the business management and group risk management function, the Group’s general policies and procedures and satisfies itself that the effective systems of risk management are established and maintained. It oversees the Group’s risk appetite statements to ensure alignments with the Group’s strategic objectives.

The Committee comprises of five (5) members. The Committee met four (4) times in 2016 with average attendance of 64%.

Finance and General Purpose CommitteeThe Committee assists the board in fulfilling its financial oversight responsibilities with specific reference to corporate finance, resources and assets utilization, capital structure, cash management, equity and debt financing, financial planning and reporting, as well as the overall financial performance of the Group.

The Committee comprises of six (6) members. The Committee met four (4) times in 2016 with attendance of 68%.

REPORT OF CORPORATE GOVERNANCE

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 29

Investment CommitteeThe Committee assists the Board in its oversight functions with respect to investment strategies, investment portfolio performance, investment mix and the overall investment performance of the Group.

The Committee consists of five (5) members and met four times in 2016 with attendance of 67%.

Strategy CommitteeThe committee’s responsibilities includes but not limited to advising and assisting the board in carrying out:i) the development, articulation and execution of the Group’s long term strategic plan, andii) it’s advisory oversight responsibilities relating to potential mergers, acquisitions and other key strategic

transactions outside the ordinary course of the Group’s business.

The Committee comprises of four (4) members and met four times in 2016 with the average attendance of 58%.

REPORT OF CORPORATE GOVERNANCE

Board Committee Meetings Attendance

LegendBIC - Board Investment CommitteeF & GP - Finance and General Purpose CommitteeRMC - Risk Management CommitteeAC - Audit CommitteeBSC - Board Strategy CommitteeE & GC - Establishment and Governance Committee

Directors BIC E&GC F&GP RMS AC BSC

Expected Meetings 4 4 4 4 4 4

Actual Meetings 4 4 4 4 5 4

Mr. K. E. Odogwu N/A N/A N/A N/A N/A N/A

Chief A. I. Idigbe (SAN) 4 2 2 2 N/A 3

Mr. D. Magerle 1 4 1 2 N/A 2

Chief U. Okpa–Obaji 2 4 4 4 5 N/A

Alhaji A. R. Mohammed 4 N/A 4 2 3 2

Alhaji R. M. Gwarzo (OON) N/A 4 2 2 2 2

Mr. A. Ojora 2 N/A 2 2 5 1

Alhaji A. Muktari 4 4 4 4 5 4

Alhaja A. S. Kudaisi N/A N/A N/A N/A 5 N/A

Mr. T. Olawuyi N/A N/A N/A N/A 5 N/A

Mr. A. Benkunmi N/A N/A N/A N/A 5 N/A

Average Attendance 67% 90% 68% 64% 88% 58%

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC30

GROUP STRUCTURE AND SHAREHOLDERS

Operational Group StructureTo effectively manage the complexity associated with group structure both in operations and governance, Royal Exchange Plc manages its exposure to group governance on a matrix depicting lines of business and functionalities which reflect in the areas of responsibility.

The Executive Committee (EXCO)The Executive Committee (EXCO) is headed by the Group Managing Director and includes the Group General Manager and the Group Heads of Finance and Accounts, Human Resources, Strategy and Business Improvement, and the Managing Directors of all the subsidiaries.

This management structure leads to the reporting of the Group based on the following primary business segments:

• General insurance serves the property and casualty insurance (inclusive of oil and gas business) need of a wide range of customers, from individual to small and medium sized businesses, commercial enterprises and multinational corporations.

• Prudential Life pursues a strategy with market-leading proposition in investment linked and protection products through global distribution and proposition pillars to develop leadership position in its chosen segment.

• Healthcare provides qualitative healthcare services to individuals and organizations. Their major strategy is to pursue blue chip companies that have large number of staff. The main benefits of the service is that, apart from the easy access to healthcare delivery system, the enormous cash outlay needed by the organizations to settle medical bills of staff is significantly reduced.

• Finance and Asset Management provides financial services to the Group and the public. It pursues a strategy of generating income in the course of garnering borrowings from the public, disbursing credits to individuals and corporate entities, as well as asset management for individuals and corporate entities.

• Microfinance Bank provides services to the less privileged public, having a total production assets of not exceeding =N=500,000.00 and monthly income not exceeding twice the monthly per capita income in Nigeria or minimum wage.

The Group Management Executive Committee (GMEC)The GMEC is headed by the Group Managing Director and includes the Group General Manager, Managing Directors of the subsidiaries and Group Heads of Departments.

The GMEC is responsible for:• The day-to-day running of the Group on behalf of the Board• The development and implementation of all Board - approved initiatives • The achievement of all business and operational plans, targets, strategies and objectives within the company’s risk

management framework; and • The development of advanced reporting procedures to ensure the Board is fully informed at all times.

The GMEC also ensures that the processes, policies, procedures and controls within the Group are effective and regularly reviewed to deliver financial and operational accountability and success.

SUBSIDIARY GOVERNANCE Subsidiary governance is a vital ingredient of Royal Exchange Risk management framework. Royal Exchange’s governance strategy is implemented through the establishment of systems and processes which assures the Board that the subsidiaries reflect the same values, ethics, control and processes as that of the parent, while remaining independent in the conduct of their business. It provides the structure through which performance objectives of the subsidiaries are set, the means through which the set objectives are achieved and how performance monitoring is conducted.

REPORT OF CORPORATE GOVERNANCE

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 31

Monthly subsidiaries business activities and operating environment are discussed at the Executive Committee (EXCO) level where strategic directions are set. The reports cover the subsidiaries’ financial performance, risk assessment and regulatory activities among others. To ensure an effective and consistent compliance culture across all entities, the Group Compliance function oversee compliance risk and promotes training and best practice implementation across the subsidiaries, therefore affirming the Group’s commitment to zero tolerance for regulatory breaches.

INFORMATION TO SHAREHOLDERS Shareholders have the opportunity to express their opinions on the company’s financial results and other issues affecting the Company. Royal Exchange Plc is thus committed to continually disclose all material information in a timely and transparent manner to its shareholders. To ensure the shareholders’ are adequately informed and their interest protected, the Company has an Investors Relations Unit domiciled in the company secretariat to deal directly with enquiries from shareholders and ensure that shareholders’ views are escalated to Management and the Board. Information relating to the goings on in the Company are periodically released to the investing public on quarterly, half-yearly and annual basis in widely read national newspapers.

Annual General MeetingIn compliance with statutory and regulatory requirements, the Annual General Meeting of the Company is annually held and provides the shareholders of the Company or their proxies with the opportunity and direct access to senior and executive Management to deliberate and take decisions on the issues affecting the Company. The Annual General Meetings are attended by representatives of regulators such as the Securities and Exchange Commission (SEC), the Nigerian Stock Exchange (NSE), Corporate Affairs Commission (CAC), as well as members of Shareholders’ Associations.

Cross shareholding The Company has no interest in any other company exceeding 5% of the voting rights of that other company, where that other company has an interest in Royal Exchange Plc exceeding 5% of the voting rights in Royal Exchange Plc.

Communication PolicyThe Company ensures that communication and information dissemination regarding the company’s operations to stakeholders and the general public is timely, accurate and continuous. Such information is available on the company’s website, http://www.royalexchangeplc.com.

Whistle Blowing proceduresRoyal Exchange is committed to the highest standards of ethical, moral and legal business conduct. In line with this commitment and Royal Exchange’s philosophy of open dialogue and communications, the Company has established a whistleblowing procedure that ensures and provides an avenue for employees to raise concerns and be assured that they will be protected from reprisals or victimization for whistleblowing. This whistleblower policy is intended to provide protection for any whistleblower that raises concerns in good faith regarding Royal Exchange Plc, relating to:• Incorrect or inappropriate financial reporting;• A violation of a law or regulation;• Possible fraud and corruption;• Activities which otherwise amount to serious improper conduct;• Health and safety risks including risks to the public, as well as other staff;

The Company Secretary The Company Secretary provides reference and support for all Directors. She also consults regularly with Directors to ensure that they receive required information promptly. The Company Secretary is also responsible for assisting the Board and Management in the implementation of the Code of Corporate Governance, coordinating the orientation and training of new Directors and the continuous education of Non-Executive Directors.

REPORT OF CORPORATE GOVERNANCE

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC32

Complaints Management Royal Exchange views complaints as any expression of dissatisfaction, resentment or grievance, whether justified or not, made by a person or corporate body about any aspect of Royal Exchange operations, services, personnel, policies, shares or dividends. We are thus committed to resolving customer’s complaints if and when they arise. Our complaints and feedback structure ensures the prompt resolution of customers’ complaints. There is a dedicated Complaints Unit responsible for receiving, ensuring prompt investigation and resolution of customers’ complaints.

Anti-Money laundering and combating the Financing of Terrorism (AML/CFT) frameworkRoyal Exchange is committed to ensuring that its products and services are not used for Money Laundering and Financing of Terrorism and Proliferation of Weapons of Mass Destruction; and that its processes and procedures are in compliance with all applicable laws and regulations on Money Laundering. In view of this, Royal Exchange annually exposes its Board, Management and staff across the nation to money laundering techniques and how to combat it.

NOTES:

1. It is the policy of the Group that any director, who will be absent from any meeting shall send his alternate to attend the meeting. In compliance with the above, every director ab-initio has named and presented his permanent alternates details with the board. The directors with asterisks were represented by their alternates on the dates they were absent.

2. The Company has an approved Share Dealing Policy and the Directors adhere to the policy in their dealings with the Company’s shares.

3. The Company has an approved Complaints Management Policy Framework in compliance with the rules and regulations of Securities and Exchange Commission.

SHEILA IFEYINWA EZEUKO COMPANY SECRETARY/GM (LEGAL SERVICES)FRC/2013/NBA/00000004059LAGOS, NIGERIA1 JUNE, 2017

REPORT OF CORPORATE GOVERNANCE

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 33

The Royal Exchange Group is committed to continually embrace best practice in its enterprise risk management by aligning strategy, people, processes, technology and business intelligence with a view to minimizing the potential threats of risk events and maximizing potential business and growth opportunities for sustainable stakeholders’ value.

The Group, recognizing its major risk areas as Insurance, Credit, Operational, Information Technology, Market and Liquidity Risks has adopted risk management principles and processes which support, promote and embed its risk management and business objectives to sustain its risk management culture.

The risk management infrastructure encompasses a comprehensive and integrated approach to identifying, managing, monitoring and reporting risks with focus on the following inherent risk groups – Insurance, Liquidity, Credit, Market, Operation, and Technology.

In compliance with best global practices and in pro-activeness to National Insurance Commission (NAICOM) Risk-based Supervision guidelines, the Group has begun the strategic framework for efficient measurement and management of the insurance sector risks and capital.

Our key Enterprise Risk Management (ERM) objectives:

• Aligning risk appetite and corporate strategy• Protect the Group’s capital base by monitoring and ensuring that risks are not taken beyond the Group’s tolerance

limit• Enhance value creation and contribute to an optimal risk return profile by providing the basis for efficient capital

deployment• Support the Group’s decision-making processes by providing consistent, reliable and timely risk information• Protect our reputation and brand by promoting a sound culture of risk awareness, discipline and informed risk-

taking.

Our key Enterprise Risk Management (ERM) framework:

Risk management has been effectively embedded into the system through clearly articulated roles for the Board of Directors, Chief Executive Officer, business and functional areas. Our risk management framework is centered around a robust risk governance process with assigned responsibilities for identifying, managing, monitoring and reporting risk within the Group.

The Board of Directors has the overall responsibility for the establishment of the Group’s Risk Management framework and exercises its oversight function over all the Group’s prevalent risks via its various committees; Board Risk Management Committee (BRMC); Board Investment Committee (BIC); Board Strategy Committee (BSC); Board Finance and General Purpose Committee (BF & GPC); Board Establishment and Governance Committee (BE&GC) and Audit Committee (AC). These committees are responsible for developing and monitoring risk policies in their specific areas and report regularly to the Board of Directors.

To ensure adherence to and support the governance process, the Group relies on documented policies and guidelines, regular reporting of the Group risk profile and current risk issues. These are generated by the various business units such as Audit, Control, Risk and Compliance for Management’s decision-making. These reports include:

• Monthly Key Risk Indicator (KRI) Report • Monthly Internal Control Report• Quarterly Actuarial Valuation Report (AVR)• Quarterly Risk Assessment Report • Quarterly Compliance and Governance Report • Quarterly Internal Audit Report

RISK MANAGEMENT STATEMENT

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC34

The Board Risk Management Committee charter and the Enterprise Risk Management policy are the Group’s main risk governance documents. They specify authorities, reporting requirements, procedure to approve any exceptions and methods of referring any risk issues to senior management and the Board of Directors.

Risk CultureThe Board of Directors and management ensures that the long-term survival and reputation of the Company are not at risk by sustaining the promotion of risk awareness across the Group to manage products, market, portfolio, liquidity, credit and interest rate risks where the associated risks are deemed unacceptable and may affect the strategic vision of the Company. In addition, the Company continually exposes staff to training on principles and practice of ERM which has enhanced the skill level of staff members.

Risk AppetiteThe Board of Directors established the Group risk appetite statement to guide the Group to effectively discharge its functions. The management is thus guided to take decisions on managing different categories of risk within the purview of the risk appetite statements. Also, the risk appetite levels, such as prudential limits were set by the Board of Directors to guide the management’s decision on the amount of risk they are prepared to accept, when decisions are taken to manage any mitigating measures. In line with the Group appetite statements, the subsidiaries’ risk appetites were scaled down from that of the Group to reflect the respective subsidiary’s need.

Risk Governance The primary objective of the Company’s risk and financial management framework is to protect the Company’s stakeholders from events that hinder the sustainable achievement of financial performance objectives, including failing to exploit opportunities.

The Company’s strategy for managing risk exposures is to establish and maintain a robust Enterprise Risk Management (ERM) programme, that is embedded in all processes and driven by technology with emphasis on protection from unwanted risk while maintaining stakeholders’ value.

To this end, the Board established the Group’s corporate risk management framework. The ERM programme helps to structure and coordinate all direct and indirect risk management activities within the Company, while eliminating redundancies and ensuring consistency in the risk management process.

The risk management committee of the Board serves as the focal point for oversight regarding risk management. It reviews the risk management methodologies, policies, models, reporting and risk strategies.

Capital Management ApproachThe Group’s operations are subject to regulatory requirements of the National Insurance Commission (NAICOM), Central Bank of Nigeria (CBN), the Nigerian Stock Exchange (NSE) and the Securities and Exchange Commission (SEC). Such regulations not only prescribe approval and monitoring of activities, but also impose certain restrictive provisions (e.g., capital adequacy) to minimize the risk of default and insolvency on the part of the financial service companies and to meet unforeseen liabilities as these arise.

The Group’s capital management policy is therefore to hold sufficient capital to cover the statutory requirements based on regulators’ directives, including any additional amounts required by the regulators.

RISK MANAGEMENT STATEMENT

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC 35

The Group has established the following capital management objectives, policies and approach to managing the risks that affect its capital position:

• Maintain the required level of stability of the Group thereby providing a degree of security to policyholders;• Allocate capital efficiently and support the development of business by ensuring that returns on capital employed

meet the requirements of its capital providers and of its shareholders;• Retain financial flexibility by maintaining strong liquidity and access to a range of capital markets;• Align the profile of assets and liabilities, taking account of risks inherent in the business; and• Maintain financial strength to support new business growth and satisfy the requirements of the policyholders,

regulators and other stakeholders;

In reporting financial strength, capital and solvency are measured using the rules prescribed by NAICOM. These regulatory tests are based upon required levels of solvency, capital and a series of prudent assumptions in respect of the type of assets held.

The capital management process is governed by the Board of Directors who has the ultimate responsibility for the capital management process. The Board of Directors is supported by the Board Risk Management Committee and the Board Credit Committee, all of whom have various inputs into the capital management process.

Regulatory FrameworkRegulators are primarily interested in protecting the rights of policyholders and depositors’ funds and monitoring them closely to ensure that the Company is satisfactorily managing affairs for their benefit. At the same time, regulators are also interested in ensuring that the Company maintains an appropriate solvency position to meet unforeseen liabilities arising from economic shocks or natural disasters.

The operations of the Company are thus subject to regulatory requirements. Such regulations not only prescribe approval and monitoring of activities, but also impose certain restrictive reserves (e.g., contingency reserve, limits on recognition of revaluation reserves for solvency purposes, limit of investment in fixed assets, permissible level of portfolio at risk and distribution to shareholders of actuarial surpluses) to minimize the risk of default and insolvency on the part of the companies to meet unforeseen liabilities as these arise.

Asset and Liability Management FrameworkThe Assets and Liability Management framework is integrated in the overall risk management policy of the Company be it directly or indirectly associated with insurance and investment liabilities. Our insurance risk management policy is to ensure, in each period, sufficient cash flow is available to meet liabilities arising from insurance and investment contracts.

Risk Management The Group operations cut across the financial sector thus, the Group operations is exposed to varied forms of risks, such as, Operational Risk, Insurance Risk, Credit Risk, Liquidity Risk, and Market Risk. To mitigate all of these risks, the Company has put in place approved policies, procedures and guidelines to identifying, measuring and controlling of these risks.

Operational RiskThe Group, recognizing it cannot completely eliminate the Group operational risk, such as human error, system failure fraud and external events, has put in place adequate controls to ensure that the impact does not lead to damage to the reputation of the Company, financial loss or legal and regulatory implication.

Controls such as segregation of duties, access control, authorization and reconciliation procedures, staff education and assessment processes including the use of internal audit have been put in place. Business risks such as changes in environment, technology and industry are monitored through the Company strategic planning and budgeting process.

RISK MANAGEMENT STATEMENT

ANNUAL REPORT & ACCOUNTS 2016ROYAL EXCHANGE PLC36

Insurance Risk Insurance business being the central part of the Group’s business exposes the Company to the risk of timing and expectations of claims and benefit payments. This is influenced by the frequency of claims, severity of claims, actual benefits paid and subsequent development of long-term claims.

The risk exposure is mitigated by diversification across a large portfolio of insurance contracts and ensuring that sufficient reserves are available to cover these liabilities. The variability of risks is also improved by careful selection and implementation of underwriting strategy guidelines, as well as the use of reinsurance arrangements.

Underwriting risk appetite is defined based on underwriting objectives, business acceptance guidelines, retention guidelines, net retention capacity, annual treaty capacity, regulatory guidelines, other operational considerations and the judgment of the Board and executive management.

Credit Risk The Group’s credit risk appetite is in line with the Company’s strategic objectives, available resources and the provisions of the regulators’ operational guidelines. The Group credit risk policy is to ensure that an appropriate, adequate and effective system of risk management and internal control which addresses credit control is established and maintained.

The Group thus ensures the establishment of principles, policies and processes and structure for the management of risk exposure arising from direct default, counter party and concentration risks to ensure that these risks are properly managed within the Group’s risk appetite.

In setting these appetite limits, the corporate solvency level, risk capital and liquidity level, level of investments, reinsurance and co-insurance arrangements, nature and categories of its clients, are taken into consideration.

The following risk mitigation and control activities are in place to effectively manage exposures to default risk: client evaluation, credit analysis, credit limit setting, credit approval, security management, and provision for impairments.