russian defense budget & procurement

DESCRIPTION

Russian defense budget & procurementTRANSCRIPT

Conference on: Russian Decision Making and

Implications for Defense Spending

Lunch Session:

Defense Budget and Procurement

March 2, 2011

by Reed Livergood

Outline

I. Economy

II. Budget

III. Procurement & SAP

IV. Exports

I. Economy

Russia:

• Middle income country– Biggest country outside WTO

• G8 Member

• #1 in: • oil production

• natural gas

(production and reserves)

• #2 in:• Arms exports

• Coal reserves

• Rising:• GDP

• GDP per capita

• Life expectancy

• Education rates

• Hit hard by the financial crisis (2008-2009)

– Stabilization Fund drained• Reserve Fund

• National Welfare Fund

I. Economy

Source: OECD Factbook 2010

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

OECD GDP Canada

Finland

France

Germany

Italy

Netherlands

Norway

Poland

Spain

Sweden

United Kingdom

United States

Russian Federation

in billions

I. Economy

Source: IMF World Economic Outlook 2010

127

266

393433

528 535

355

253327

377417

507

677

843

1,055

1,349

1,669

1,232

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Russian GDP, constant prices (2009)

Gross domestic product, constant prices (2009)

in US billions

I. Economy

Source: IMF World Economic Outlook 2010

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

GDP per capita (PPP)Brazil

Chile

China

India

Kazakhstan

Korea

Poland

Russia

Ukraine

United Kingdom

United States

Venezuela

in US billions

I. Economy

Source: OECD Factbook 2010

Goods• Petroleum-based products

• Natural gas

• Wood-based products

• Metals

• Chemicals

• Medical equipment

• Agricultural products

Services• Financial

• Technology-based

• Information Technology-based

• Academic: mathematics, physics, engineering

• Communication

• Business

58 61 76106

143163 153

201

0

100

200

300

400

500

600

700

800

0

100

200

300

400

500

600

700

800

2001 2002 2003 2004 2005 2006 2007 2008

Russian Trade in goods

Imports of goods Exports of goods Goods trade balance: exports minus imports of goods

in USD Billions in USD Billions

-9.1-9.9

-10.9

-12.7-13.8 -13.6

-19.6

-25.1

-30

-25

-20

-15

-10

-5

0

0

20

40

60

80

100

120

140

2001 2002 2003 2004 2005 2006 2007 2008

Russian Trade in services

Imports of services Exports of services Service trade balance: exports minus imports of services

in USD Billions in USD Billions

I. Economy

Source: OECD Factbook 2010

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2001 2002 2003 2004 2005 2006 2007 2008

Russian Flows of Foreign Direct Investment

Inflows of foreign direct investment Outflows of foreign direct investment

in USD Millions

I. Economy

• 9.6% inflation rate (1-2011)

– Double from summer of 2010

– Biggest problem ahead of alcoholism (BRIC survey)

– Food inflation problematic

– Forecasts of 5.5% through 2015

• 2.7% growth rate

• R28.89 : $1 USD

• Interest rates increase after record low– 7.75% to 8%

Source: OECD Factbook 2010

21.5

15.8

13.7

10.9

12.79.7

9.0

14.1

21.3

12.311.2

10.4

13.7

9.69.0

20.9

0.0

5.0

10.0

15.0

20.0

25.0

2001 2002 2003 2004 2005 2006 2007 2008

Russian Inflation Rates

Inflation rate: all items Inflation rate: food

%

5.1 4.7

7.3 7.26.4

7.7 8.1

5.6

21.5

15.8 13.7

10.912.7

9.7 9.0

14.1

0.0

5.0

10.0

15.0

20.0

25.0

30.0

2001 2002 2003 2004 2005 2006 2007 2008

Russian Real GDP growth compared to inflation

Real GDP growth (%) Inflation rate: all items

%

I. Economy

Source: OECD Factbook 2010

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

19

50

19

52

19

54

19

56

19

58

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

OECD Population Canada

Finland

France

Germany

Italy

Netherlands

Norway

Poland

Spain

Sweden

United Kingdom

United States

Russian Federation

in thousands

II. Budget

Source: Google stock images

II. Budget

• Formulation

• Negotiation

• Implementation

– 5th biggest military budget worldwide• USA, China, United

Kingdom, France, Russia

• Executive Branch

– 8 Ministries• Ministry of Defense

• Ministry of Finance

• Ministry of Economic Development and Trade

• Legislative Branch

– Upper House• Federation Council

– Lower House• Duma

II. Budget

• Basis:

– Oil price• $75/bbl (2011), $78/bbl

(2012), $79 (2013)

– Oil and gas income (% of GDP)

• 8.1% (2011), 7.9% (2012), 9.3% (2013)

– Inflation (%)• 6.5% (2011), 6.0% (2012),

5.5% (2013)

– Defense burden• 2.84% (2010), 3.01% (2011),

2.97% (2012), 3.39% (2013)

$0

$20

$40

$60

$80

$100

$120

$140

$160

Ap

r-1

98

3

Jan

-19

84

Oct

-19

84

Jul-

19

85

Ap

r-1

98

6

Jan

-19

87

Oct

-19

87

Jul-

19

88

Ap

r-1

98

9

Jan

-19

90

Oct

-19

90

Jul-

19

91

Ap

r-1

99

2

Jan

-19

93

Oct

-19

93

Jul-

19

94

Ap

r-1

99

5

Jan

-19

96

Oct

-19

96

Jul-

19

97

Ap

r-1

99

8

Jan

-19

99

Oct

-19

99

Jul-

20

00

Ap

r-2

00

1

Jan

-20

02

Oct

-20

02

Jul-

20

03

Ap

r-2

00

4

Jan

-20

05

Oct

-20

05

Jul-

20

06

Ap

r-2

00

7

Jan

-20

08

Oct

-20

08

Jul-

20

09

Ap

r-2

01

0

Jan

-20

11

Oil Future Contract (Dollars per Barrel)

Oil Price

Key Players

• President = Dmitry Medvedev

• Prime Minister = Vladimir Putin

• Deputy Prime Minister = Sergei Ivanov

• Deputy Prime Minister & Minister of Finance = Aleksey Kudrin

• Deputy Prime Minister & Chairman of Rosneft = Igor Sechin

• Deputy Finance Minister = Anton Siluanov

• Ministry of Industry & Trade = Viktor Khristenko

• Ministry of Economic Development = Elvira Nabiullina

• Minister of Interior = Rashid Nurgaliyev

• Federation Council Chairman = Sergei Mironov

• Fed. Council Defense and Security Committee Chairman = Victor Ozerov

• Duma Chairman = Boris Gryzlov

• Duma Defense and Security Committee Chairman = Victor Zavarzin

• Duma Budget Committee Deputy Chairman = Mikhail Babich

• Auditor of Audit Chamber Nicolai Tabachkov

• Defense Secretary = Anatoly Serdyukov

• 1st Deputy Defense Minister (Acquisitions) = Vladimir Popovkin

• Acting Chief of Armaments (MOD) = Oleg Frolov

• Deputy Defense Minister (Financial-Economic Work) = Lyubov Kudelina

• Chief of General Staff = Nikolai Makarov

• Ministry of Defense's Chief Social Guarantees Department = Anna Kondratyeva

• Defense Ministry Public Council Representative = Igor Korotchenko

• Defense Ministry Public Council Representative = Ruslan Pukhov

• FSMTC General Manager = Alexander Kopetsky

• Federal Service for Defense Contracts (Rosoboronzakaz) = Alexander Sukhorukov

• Federal Service Military-Technical Cooperation Director = Mikhail Arkadievich

• Deputy Director = Konstantin Biryulin

• Director General of Rosoboronexport = Anatoly Isaykin

II. Budget

Defense and Security DraftJane’s & RIA Novosti:

• Income: R8844 tn ($290 bn )– 17.6 (% of GDP)

• Expenditures: R10,658 tn ($329 bn)– 21.2 (% of GDP)

• Deficit = -3.6% (of GDP)– R -1814 bn

• Military: $60 bn

– 13.8% of GDP

Source: Military Balance 2010 (IISS)

II. Budget

Siluanov: (6-3-2010)

• Military:

– 2.6% (2010) of GDP

– Plan was 2.9% (2011), 3.0% (2012), 3.2% (2013)

• Has overseen four-fold increase of military

Medvedev: (11-25-2010)

• Military:

– R574 bn (2011), R726 bn (2012), R1160 bn (2013)

– % of GDP: 2.8% (2011)

Kudrin: (11-30-2010)

• Medvedev’s intention to secure R20 tn was a “new task”

II. Budget

• State Armaments Program (SAP)

– R20,700 tn• R19,040 tn for MOD

• R2.5 – R3.0 tn for other law enforcement agencies

– 1st time in last ten years defense burden is greater than 3%

– 70% to be spent by 2015

– R700 bn allocated for after 2015

• Goal: modernizing and renovation– 30% (by 2015), 70-80% (by 2020)

– R100 bn increase in procurement

– 6.5% raise in personnel pay

– R&D spending will drop • From 22% (2010) to 16% (2013)

Source: Centre for Analysis of Strategies and Technologies

II. Budget

Source: SIPRI Military Expenditure Database 2010

339314

266

66 58 5734 30 33 21 22 30 33 37 39 41 44 48 53 58 61 53

15.8

14.2

12.3

5.5 5.35.9

4.44.1

4.5

3.3 3.43.7

4.14.4 4.3

3.8 3.7 3.6 3.5 3.5

0

2

4

6

8

10

12

14

16

$0

$100

$200

$300

$400

$500

$600

$700

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Russian Military Expenditures ($US bn) and Defense Burden (% of GDP)

Russian Military Expenditures $US bn (constant 2008) % of GDP

II. Budget

Sources: SIPRI, Russia in the 21st Century (Rosefields), Military Balance 2010 (IISS)

15.8

14.2

12.3

5.5 5.35.9

4.4 4.14.5

3.3 3.4 3.74.1 4.4 4.3

3.8 3.7 3.6 3.5 3.54.7 4.4 4.4 4.6

3.0 3.1

2.12.6 2.6 2.9

2.3 2.0 2.52.4 2.5 2.5 2.5 2.5 2.5 2.4

0

2

4

6

8

10

12

14

16

18

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

Russian Defense Burden (% of GDP) SIPRI, Rosefielde, IISS

% of GDP (SIPRI) % of GDP (Rosefielde) % of GDP (IISS)

II. Budget

Source: SIPRI Military Expenditure Database 2010

744716

644

427404 397

361 359 362 350 356 367 368 381 385 387 389 397 403 413 424

339314

266

66 58 5734 30 33 21 22 30 33 37 39 41 44 48 53 58 61

46%44%

41%

15% 14% 14%

9% 8% 9%6% 6%

8% 9% 10% 10% 10% 11% 12% 13% 14% 14%

0%

10%

20%

30%

40%

50%

60%

70%

80%

$0

$100

$200

$300

$400

$500

$600

$700

$800

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

Military Expenditure: Russia to Europe comparison (constant 2008)

Europe Russia Russia as % of Eur Spending

in Billions

II. Budget

• Federal Service Military-Technical Cooperation (FSMTC)

• Military-Industrial Commission (MIC)

(Rosoboronzakaz)

• Kudrin & Serdyukov– 1.5% of GDP spent on army

modernization, military pay, & other

– Called for fair and honest elections to grant authorities mandate for executing difficult economic reforms

– Remains loyal to Putin

– Supported idea to purchase ships (Mistrals) vs. producing domestically

– Has overseen four-fold increase of military industrial complex

III. Procurement & SAP

Source: Centre for Analysis of Strategies and Technologies

III. Procurement & SAP

• Navy: (100+ vessels)

– 20 submarines• 8 Borei-class ballistic

missile submarines

• Yasen-class nuclear attack submarines

• 3 Kilo-class submarines

– 35 corvettes

– 15 frigates• 3 Talwar-class

– Kirov- and Slava-class cruisers

– Mistral assault ships• (2 + 2)

– New Carrier• Design (2011), start

(2015), completed (2020)

– Auxiliary ships

– Service craft

• Kashin-, Sovremennyi-class destroyers likely to be retired soon

• Udaloy will become backbone

III. Procurement & SAP

• Air Force– 1994-2003 = 0 planes

– 2004-2009 = 3 planes

Investigation into 2 crashes (‘08)– 200+ aircraft had fin corrosion

Under SAP 2011-2020

– 600+ planes

– 1,000+ helicopters

• Su-30s

• Su-35s

• Upgrade MiG-29 to MiG-29SMT

• T-50 PAK-FA to be future– Ordered (2015), tested (2015)

• Helicopters– 500 Mi-24 Hind gunships

– Mi-8/Mi-17 transport

• Transport aircraft– Il-112

– An-70

– Il-476

– An-124

III. Procurement & SAP

• Nuclear Forces:

– Procurement, upgrading, maintenance in combat readiness will increase by 50%

– 10 batteries of S-500 anti-missile and anti-aircraft defense missiles

– 56 batteries of S-400 defense missiles

• Other Armaments

– Small batches of drones• UAVs

– Sniper rifles

– Felin (French) infantry combat suits

– T-90s

– AN-94s

Source: Military Balance 2010

III. Procurement & SAP

360,000 35%

35,000 3%142,000

14%

160,000 16%

80,000 8%

250,000 24%

Active Troops (2009)

Army Airborne

Navy Air

Strategic Deterrent Forces Command and Support

III. Procurement & SAP

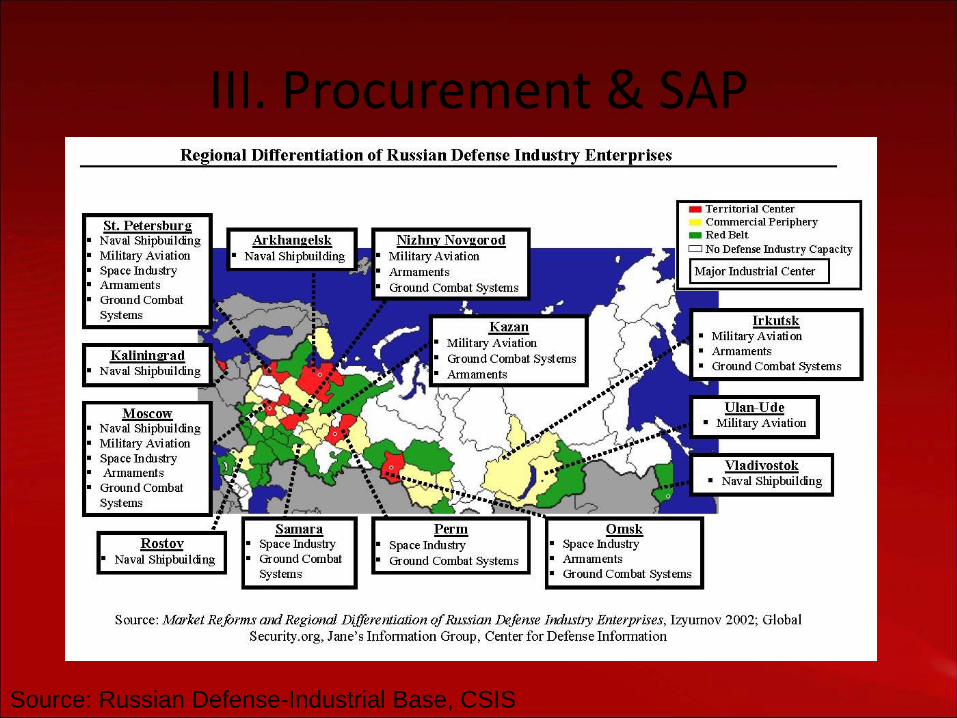

Production in defense– 45% of defense output volume is

dual-use• Oil, gas, transport, energy, household

appliances, electrical engineering sectors

– 70% of scientific output is defense

– Output up 13% while total went down (PM Putin 4-21-2010)

– Production declined 46% (1991-2001)

– Russian government wants to supply 5% of the world’s aircraft by 2015, 10% by 2025

– UAC deal (Jan 2011) with MAG Industrial Automation Systems

• MAG VIPER Fiber Placement System and 2 HyperMachTM Vertical profilers to support aircraft manufacturing

Source: Russian Defense-Industrial Base, CSIS

III. Procurement & SAP

III. Procurement & SAP

Partnerships

• Bridge short- and medium-term gaps

• Not cost free

• France: (STX & DNCS)

– Mistral amphibious assault ships• 1st two to be built in France

– 20%, 40% Russian-built

– $1.9 bn est.

• 2nd two to be built in Russia

– 80%, 80% Russian-built

• Italy: Iveco joint enterprise

– Lynx light multi-purpose armored vehicles (LMVs)

(about 1,000)• BTR-80

• Tiger

III. Procurement & SAP

Investment

• Regulatory changes coming to improve climate, abolish limitations, revise legal investment framework– One of Putin’s last acts as

president was to sign the 50% acquisition law on strategic ventures

• $50 bn worth of bonds to be sold

• $10 bn worth of state assets to be sold until at least 2014

• 1/3rd of defense enterprises are bankrupt, 1/3rd are unstable

• 80% of production plants are obsolete

• Investment is 10-20% it is in developed countries

• Defense is “locomotive” of entire economy

• M&As are creating “industrial kolkhozy”

III. Procurement & SAP

Research & Development• Share of worldwide Russian

research-related products has dropped from 6% (1990), to 1% (2000), to 0.2% (2008)

• Japan spends 4x, Germany 3x, Czech Republic 2x more than Russia on scientific R&D

• Russia faced “stooping to the level of iron supplier”– ROE Director Isaykin

• Russian “Silicon Valley” (Skolkovo)

• Russian “DARPA”– Technological independence

Corruption– 9,000+ corruption-related law

violations• More than R870m in damage

• 950 officials involved

– Almost 10:1 ratio

– Fraud increased by 50%

– Most crimes committed by officials who have regulatory powers

– Mostly found in areas where “hard cash” and material resources are being distributed

IV. Exports

• Worldwide leader in exports (#2)

– USA, Russia, Germany, France, UK

• Total sales (2009) were $8.5 bn (FSMTC) with a 50% growth (2001-6)

• Have played important role domestically

– Arrears, inflation

• “Lifeline” for industry

SIPRI Top 100 Arms-producing companies (2009)

– 9 were Russian• Almaz-Antei (23)

• United Aircraft Corp. (29)

– Sukhoi

– Irkut Corp

– MiG

• TRV Corp (67

• Vertolety Rossii (73)

• Uralvagonzavod (76)

• UEC (90)

IV. Exports

Source: Centre for Analysis of Strategies

and Technologies

IV. Exports

• Exports– Rosoboroneksport (ROE)

• Rosoboronprom (ROP)

• ROE created (2000) and given exclusive right to sell exports (March 2007)– Sales (2009): $7.4 bn (10% increase

from 2008)

– Portfolio: $34 bn ($15 bn from 2009 due to Saudi Arabia, Libya, Venezuela)

– Works with 700+ enterprises and provides R3-4 bn/yr loan guarantees

– Reports to MIC

• ROP created (2005) to officially sign contracts

• 4 others who can export:

– RSK-MiG

– Kolomna Design Bureau

– NPO-Machine-Building

– Tula Instrument Design (KBP)

IV. Exports

(2009)

• S-300 SAM Systems (China)

• 43 Su-30 fighters (Algeria, India, Malaysia)

• Missile weapons for fighters (UAC)

• 120 helicopters

• About 100 T-90 tanks (India)

• M&As Goals

– eliminate problems with skilled personnel shortages

– technology losses

– obsolete production lines

– low labor productivity

– product quality

– duplicative development

– excess capacity issues

IV. Exports

• China

– PLA Commander in Chief (Gen Xu Qiliang) saw “at least five more years of strong co-operation”

– Su-27s (J-11)• J-11B

– Su-33s (J15)

• India

– Uses about 70% Russian-made equipment• T-55s

• T-72s

• T-90s

• Submarines

• MiGs

• Sukhoi fighters

IV. Exports

• Algeria

– 2006 deal ($4.7 bn)• 40 MiGs

– 34 MiG-29s returned

• 20 Su fighters

• 16 Yak trainers

• 8 S-300s

• 40 T-90s

– 2010 deal (about $1 bn)• 16 Su-30s

• Libya

– 2010 deal ($1.8 bn)• Small arms (AKs)

• Light weapons

• Complex weapons

• Venezuela

– 2010 deal ($5 bn)• 92 T-92 tanks

• S-300

• Syria

– Forgiven 75% of debt with purchases

Conclusion

• Key Questions still remain for Russia:

– How will insufficient allocation distribution be addressed and who will assert this effort?

– What role does inflation play in setting budget allocations?

– Will civilian control ever come to pass?

– What are the measureable steps to create a Russian version of “Silicon Valley” or “DARPA”?

– How will the SAP 2011-2020 adapt to the changing nature of military threats?

Conclusion

• Glasnost (transparency) is needed – again

• The nature of the military budget system assists in uncontrolled growth and should have civilian formulation and execution powers

• The nature of oligopoly and secret cost information hurt production and allocation efficiencies

• High Inflation, rampant waste, corruption, and bureaucratic interference have all affected the front-line soldier in detrimental ways