russian securities 4pp cover 19/01/2017 17:43 page 2 ... · pdf filejpmorgan russian...

TRANSCRIPT

JPMorgan Russian Securities plcAnnual Report & Accounts for the year ended 31st October 2016

Russian Securities 4pp cover 19/01/2017 17:43 Page 2

Investment Objective To provide shareholders with capital growth

Investment PoliciesTo maintain a diversified portfolio of investments primarily inquoted Russian securities or other companies which operateprincipally in Russia.

The Company may also invest up to 10% of its gross assets incompanies that operate or are located in former Soviet UnionRepublics.

Investment Limits and RestrictionsThe Board seeks to manage some of the Company’s risks byimposing various investment limits and restrictions.

- No more than 10% of the Company’s gross assets are to beinvested in companies that operate or are located in formerSoviet Union Republics.

- The Company will not normally invest in unlisted securities.

- At the time of purchase, the maximum permitted exposure toeach individual company is 15% of the Company’s grossassets.

- The Company will not normally invest in derivatives.

- The Company will utilise liquidity and borrowings in a range of10% net cash to 15% geared in typical market conditions.

- No more than 15% of gross assets are to be invested in otherUK listed investment companies (including investment trusts).

Further details on investment policies and risk managementare given in the Strategic Report on pages 16 to 20.

Benchmark The MSCI Russian 10/40 Equity Indices Index in sterling terms.Effective from 1st November 2016, the Company’s benchmark isthe RTS Index in sterling terms (RTS).

Capital Structure UK domiciled. Full listing on the London Stock Exchange.

At 31st October 2016, the Company’s share capital comprised52,337,112 ordinary shares of 1p each.

Continuation VoteA resolution that the Company continue as an investment trustwill be put to Shareholders at the Annual General Meeting in2017 and every five years thereafter. See page 24 for furtherdetails.

Management Company and Company SecretaryThe Company employs JPMorgan Funds Limited (‘JPMF’ or the‘Manager’) as its Alternative Investment Fund Manager. JPMFdelegates the management of the Company’s portfolio toJPMorgan Asset Management (UK) Limited (‘JPMAM’).

FCA regulation of ‘non-mainstream pooledinvestments’The Company currently conducts its affairs so that the sharesissued by JPMorgan Russian Investment Trust plc can berecommended by independent financial advisers to ordinaryretail investors in accordance with the Financial ConductAuthority (FCA) rules in relation to non-mainstream investmentproducts and intends to continue to do so for the foreseeablefuture.

The shares are excluded from the FCA’s restrictions which applyto non-mainstream investment products because they areshares in an investment trust.

Association of Investment Companies (AIC)The Company is a member of the AIC. www.theaic.co.uk

WebsiteThe Company’s website, which can be found atwww.jpmrussian.co.uk, includes useful information on theCompany, such as daily prices, factsheets, current and historichalf year and annual reports and how to buy shares in thisCompany.

Features

Russian Securities 4pp cover 19/01/2017 17:43 Page 3

1

Contents

FINANCIAL RESULTS

STRATEGIC REPORT

3 Chairman’s Statement

7 Investment Manager’s Report

10 Summary of Results

11 Performance

12 Ten Year Financial Record

13 Ten Largest Investments

14 Sector Analysis

15 List of Investments

16 Business Review

GOVERNANCE

21 Board of Directors

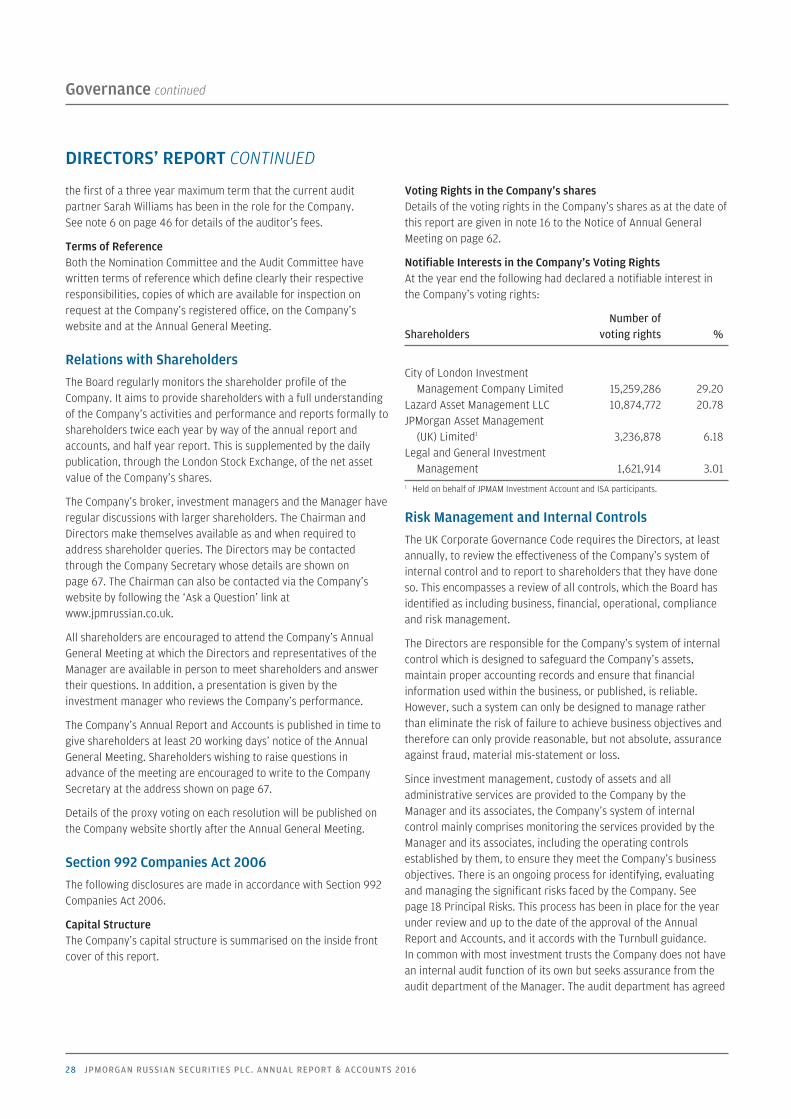

23 Directors’ Report

25 Corporate Governance Statement

30 Directors’ Remuneration Report

33 Statement of Directors’ Responsibilities

34 INDEPENDENT AUDITOR’S REPORT

FINANCIAL STATEMENTS

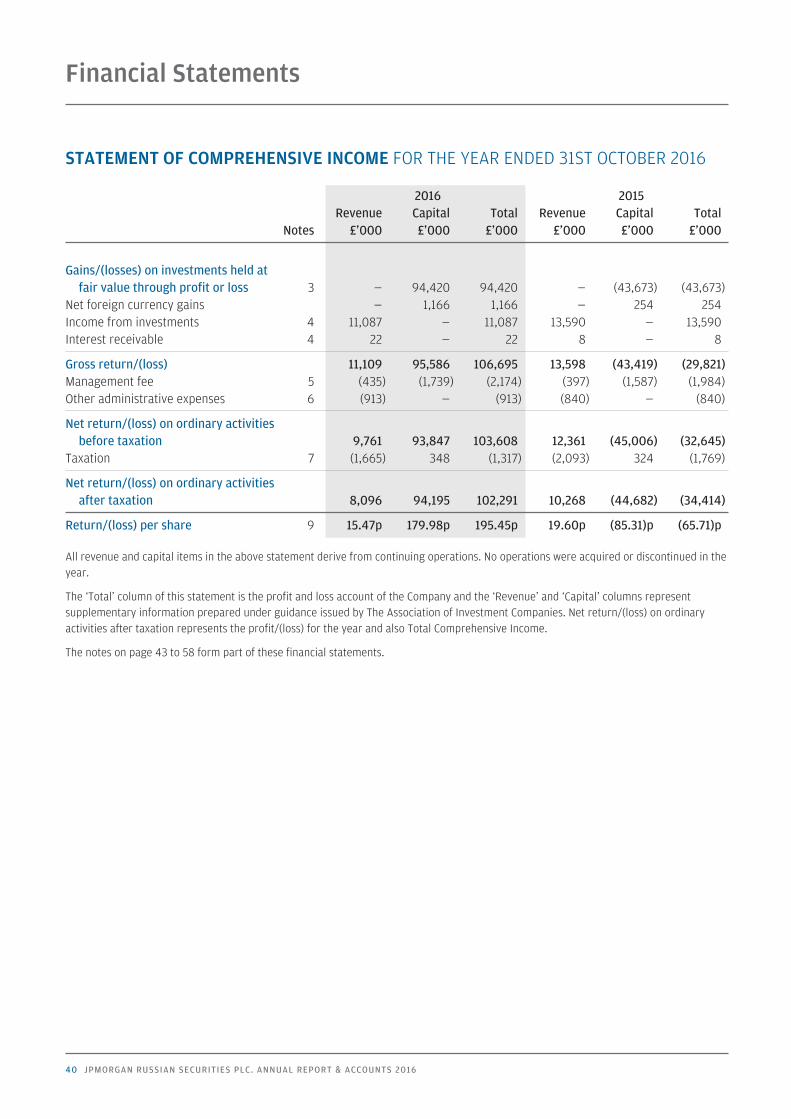

40 Statement of Comprehensive Income

41 Statement of Changes in Equity

42 Statement of Financial Position

43 Notes to the Financial Statements

REGULATORY DISCLOSURES

59 Alternative Investment Fund Managers Directive (‘AIFMD’)Disclosures (Unaudited)

SHAREHOLDER INFORMATION

60 Notice of Annual General Meeting

63 Glossary of Terms and Definitions

64 Where to buy J.P. Morgan Investment Trusts

67 Information about the Company

Russian Securities_pp01_20 19/01/2017 17:40 Page 1

2 JPMORGAN RUSSIAN SECURITIES PLC. ANNUAL REPORT & ACCOUNTS 2016

Financial Results

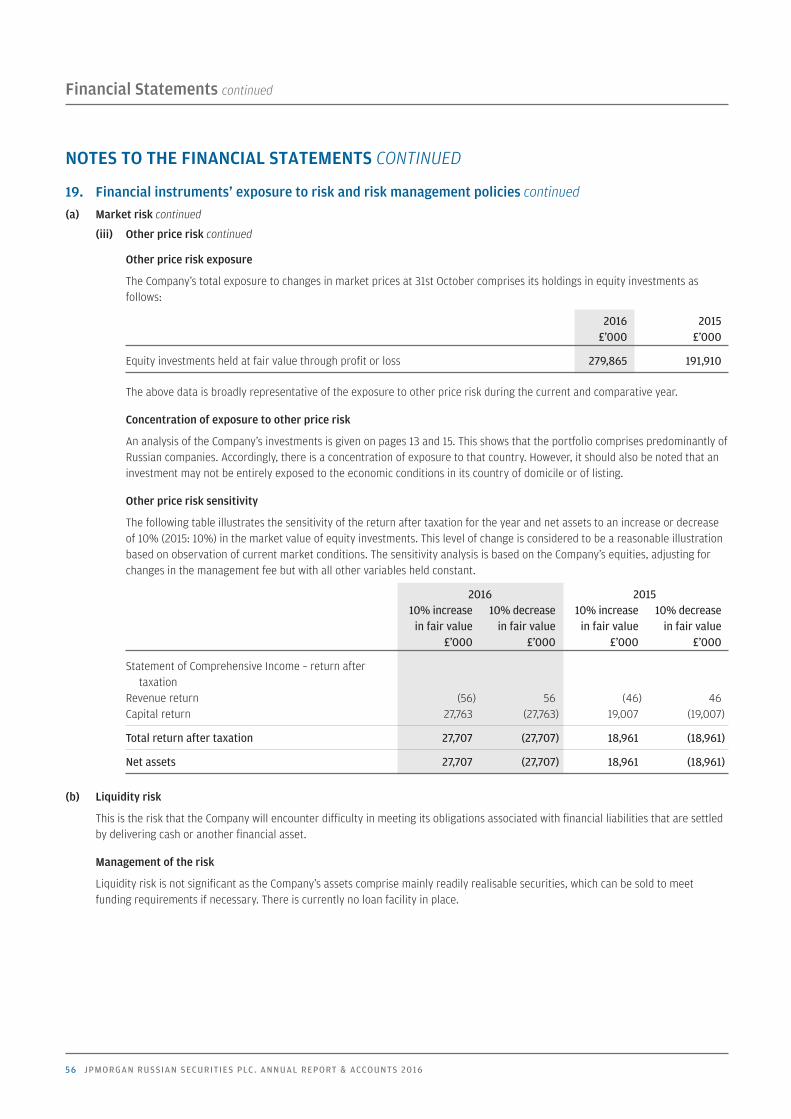

TOTAL RETURNS (INCLUDES DIVIDENDS REINVESTED)

+50.8%Benchmark3

(2015: –13.4%)

Long Term PerformanceFOR PERIODS ENDED 31ST OCTOBER 2016

3 year 5 year 10 year performance performance performance

Return to shareholders1 –5.8% –0.6% +20.8%Return on net assets2 –1.8% –9.8% +28.8%Benchmark return3 +3.2% +4.2% +55.5%

1 Source: Morningstar. 2 Source: J.P. Morgan. 3 Source: MSCI. The Benchmark is the MSCI Russian 10/40 Equity Indices Index in sterling terms. Effective from 1st November 2016, the Company’s benchmark is the RTS Index in

sterling terms (RTS).4 8.0p of the 14.0p is payable subject to the passing of a resolution at the 2017 AGM. 6.0p of the 14.0p was paid as an interim dividend on 28th October 2016.

A glossary of terms and definitions is provided on page 63

+53.1%Return to shareholders1

(2015: –13.5%)

+56.2%Return on net assets2

(2015: –14.2%)

14.0pProposed ordinary dividend4

(2015: 13.0p ordinary4.0p special)

Russian Securities_pp01_20 19/01/2017 17:40 Page 2

3

Performance and overviewThe Company’s positive performance continued into the second half of the year reflectingthe general improvements in the Russian market following the rise in the price of oil.

It is pleasing to report that the Company’s return on a net assets basis outperformed thebenchmark by 5.4% returning 56.2%. The return to shareholders also outperformed thebenchmark, with a rise of 53.1%. The Company’s benchmark during the period under reviewwas the MSCI Russia 10/40 Equity Indices Index and gained 50.8%.

Despite these positive movements, the discount at which the Company’s shares traderelative to its net asset value widened to 16.4% at the year end. Factors that led to thewidening of the discount over the year included the perceived increased political riskassociated with investment in Russia and also the general widening of discounts in emergingmarkets as they fell out of favour.

As at 17th January 2017 the discount stood at 11.2%. Since the year end to 17th January 2017the benchmark index rose 15.1% and the Company’s return to shareholders rose 21.5%.

During the Company’s financial year under review Russia’s economy recorded someimproving data with the increase in oil prices helping the Ruble to appreciate. The CentralBank of Russia interest rate reductions helped bring some feeling of stabilisation. Althoughcorporate earnings in Russia have been under pressure in 2016 and the Company’s dividendincome declined, the longer term outlook for dividend income remains positive.

Russia’s external politics with Western powers continued to be tense as its involvement inSyria proved controversial, and relations with Turkey remained fragile. However, althoughfar too early to comment with any certainty, the impact of the Trump presidential victory inthe US may lead to some thawing of relations.

The United States and European Union economic sanctions due to Russia’s involvement inthe conflict in Ukraine remain in force with an extension to March 2017 signed by PresidentObama in spring 2016. JPMorgan Asset Management’s compliance & investment functionsmonitor investments and the Company is assured by J.P. Morgan that processes are in placeto ensure that the Company remains compliant with the current sanctions regime. Inaddition, the political and economic developments and risks in the region are closelymonitored. The Board carried out regular reviews of the Company’s risk profile during theyear and you will see details of what we judge to be the key risks set out on page 18. TheCompany’s Manager maintains a diversified portfolio which adheres to the Company’sinvestment and risk control guidelines.

Objective and Strategy of the CompanyThe Board holds a strategy day each year during which it reviews the external environmentin which the Company operates and other major factors affecting the Company. This year wepaid particular attention to the political and economic environment, the Company’supcoming continuation vote and feedback from major shareholders.

As referred to in the Investment Manager’s Report, at the Company’s AGM, the shareholdersapproved a resolution to widen the Company’s Investment Objectives. Later in the year, afterconsulting with major shareholders, on 28th October 2016 the Company also announcedthat the benchmark would be changed to the RTS Index from 1st November 2016. This was

Strategic Report

CHAIRMAN’S STATEMENT

Russian Securities_pp01_20 20/01/2017 11:27 Page 3

4 JPMORGAN RUSSIAN SECURITIES PLC. ANNUAL REPORT & ACCOUNTS 2016

because the RTS Index is a more appropriate benchmark for the Company as it includesa wider range of stocks, more accurately reflecting the universe in which the Companyinvests. This is particularly relevant as the previous benchmark, MSCI Russia 10/40 EquityIndices Index in sterling terms, consists of a significantly narrower range of companies thanthat offered by the market in Russia and its former states.

Continuation VoteAt the Company’s General Meeting on 27th January 2012, a resolution was passed requiringthe Company to put a continuation vote to shareholders every five years. Therefore,a continuation vote will be put to shareholders as an ordinary resolution at the forthcomingAnnual General Meeting (AGM) to be held on 7th March 2017. Given the positive performancereturns highlighted above, and after considering the risks associated with investments inRussia your Board recommends to shareholders that they vote in favour of the Companycontinuing as an investment trust for a further five year period.

On the 4th January 2017 the Board of the Company announced that, following consultationwith the Company’s large shareholders and its advisers, it plans to introduce, subject to thepassing of a resolution in favour of the Company’s continuation as an investment trust at theCompany’s AGM on 7th March 2017, a measure to oblige the Board to make a tender offer toshareholders for up to 20% of the outstanding share capital at NAV less costs and less adiscount of 2% if, over the next five years (from the start of the current financial year being1st November 2016), the Company’s net asset value total return in sterling on a cum incomebasis is below the total return of the benchmark in sterling terms over the 5-year period.

Any tender offer will also be conditional on shareholders approving the continuation vote in2022. The Board believes this measure is in shareholders’ interests as it further incentivisesthe manager to focus on long-term investment performance.

The Board also considered whether to include a discount related condition when proposinga tender offer but felt that the higher levels of volatility in Russia, both political and marketrelated, meant that this measure was inappropriate. Given the current reliance that theRussian economy has on the oil price, the Board believes it would be hard to influence thediscount if there was a global commodities slump, or significant geopolitical pressuresaffecting Russia and political sentiment. As the Board has stated in the past, the Boardmonitors discount movements closely and, subject to market conditions, the sharerepurchase authority will be used to assist in managing the imbalance between supply anddemand when the discount widens for Company-specific reasons.

DividendsRevenue for the year, after taxation, was £8,096,000 (2015: £10,268,000) and the revenuereturn per share, calculated on the average number of shares in issue, was 15.47 pence(2015: 19.60 pence). Based upon the revenue generated by the portfolio, an interim dividendof 6.0 pence per share in respect of the year ended 31st October 2016 was paid on28th October 2016. Also in respect of the year ended 31st October 2016, the Board proposesa final dividend of 8.0 pence making a total of 14.0 pence per share for the year (2015:13.0 pence per share, excluding special dividends of 4.0 pence per share). The final dividendis proposed to be paid on 10th March 2017 to ordinary shareholders on the register at theclose of business on 10th February 2017, if approved by shareholders the final dividend willamount to £4,187,000 (2015: £6,804,000). The Company’s objective remains that of capitalgrowth, and the payment of dividends to investors is dependent on the level of dividend

Strategic Report continued

CHAIRMAN’S STATEMENT CONTINUED

Russian Securities_pp01_20 20/01/2017 11:27 Page 4

5

distributions from the companies in the portfolio. The Board reviews income expectationsthroughout the year. Should income receipts permit the Board will continue to makepayment of an interim dividend as well as a final dividend in 2017.

Discount ControlThe Board’s objective remains to use the share repurchase authority to assist in managingany imbalance between supply and demand for the Company’s shares, thereby reducing thevolatility of the discount. During the period the discount ranged from 13.8% to 18.2%. Earlierthis year the Board reviewed the Company’s discount control policy in light of the highmarket volatility. It concluded that buybacks of shares should be considered when theCompany’s discount was above 10% (previously 8%) and the absolute level of the Company’sdiscount should be taken into account, together with the relative level of discount amongstpeers investing in emerging markets. After regular and careful consideration during thecourse of the year the Board decided against the buying back of shares. It concluded thatbuybacks would be ineffective in reducing the discount, given the particular uncertaintiesaround prospects for the Russian market and the generally widening discounts for emergingmarkets.

The Board will seek authority to renew the Company’s share issuance and buyback powers atthe forthcoming AGM.

Board of DirectorsAs referred to in my Chairman’s Statement in the Company’s Half Year Report and Accountsto 30th April 2016, following Lysander Tennant’s retirement as a Director at the Company’sAGM in March 2016, a search for a new director to join the Board was conducted by anindependent non-executive search consultancy. On the 27th July 2016 we were delighted toannounce the appointment of Tamara Sakovska as a new Director of the Company, effectivefrom 1st August 2016. You can see the details of Tamara‘s experience on page 22.In compliance with corporate governance best practice, all Directors will be standing forreappointment at the forthcoming AGM. Following the Company’s annual evaluation of theDirectors, the Chairman, the Board and its Committees, the Board recommends toshareholders that all Directors be reappointed.

The Company’s Directors fees were last increased with effect from 1st November 2013. TheBoard has agreed that, bearing in mind the time since the last increase and the extra burdenplaced by new regulations and developments it was appropriate to increase directors feeseffective from 1st November 2016 as follows: Board Chairman’s fee increased by £2,500(from £35,000 to £37,500), Audit Committee Chairman by £3,000 (from £27,000 to £30,000),Directors by £2,000 per annum (from £23,000 to £25,000).

Investment ManagerThe Board pays particular attention to the way in which the Trust is run and the cost of sodoing. As part of the Board’s scrutiny of the management of the Trust the InvestmentManager is subject to an annual review including performance record managementprocesses, investment style, resources and risk control mechanisms. After a careful reviewthe Board feeds back to the Manager any areas where it feels changes are needed orimprovements could be made.

Russian Securities_pp01_20 20/01/2017 11:27 Page 5

6 JPMORGAN RUSSIAN SECURITIES PLC. ANNUAL REPORT & ACCOUNTS 2016

Strategic Report continued

CHAIRMAN’S STATEMENT CONTINUED

Annual General MeetingThe Company’s AGM will be held on Tuesday, 7th March 2017 at 12.00 noon, at TheHonourable Society of the Inner Temple, Treasury Office, Inner Temple, London EC4Y 7HL.In addition to the formal part of the meeting, there will be a presentation from OlegBiryulyov, who will be available to answer questions on the portfolio and performance.There will also be an opportunity to meet the Board, the Investment Manager andrepresentatives of JPMF and JPMAM. I look forward to seeing as many of you as possible atthis meeting. Shareholders are asked to submit in writing any detailed or technical questionsthat they wish to raise at the AGM in advance to the Company Secretary at 60 VictoriaEmbankment, London EC4Y 0JP. Alternatively you can lodge questions on the Company’swebsite at www.jpmrussian.co.uk.

OutlookThe price of oil is a major determining factor for the Russian economy and if recentincreases continue it seems likely that this will have a positive economic impact on theRussian economy and stock market in 2017. The Investment Manager has maintained hisconsistent approach of investing in well managed companies with strong balance sheets.He continues to believe that the equity market in Russia provides a good long terminvestment opportunity if the right stocks are selected. However, economic sanctions againstRussia remain and the political outlook is uncertain on many fronts, including theMiddle-East, USA and Europe. These significant geopolitical and economic issues willcontinue to impact the Russian market. There are some signs of improvement in thedomestic economy with a stable outlook for fiscal policy and expected growth in Russia’sGDP. Thus, the outlook remains uncertain but with some potential for upside if the oil pricecontinues to strengthen and economic and political stability are maintained.

Gill NottChairman 20th January 2017

Russian Securities_pp01_20 20/01/2017 11:27 Page 6

7

Market Review and PerformanceThe Company delivered strong returns to shareholders in the financial reporting yearto 31st October 2016, as the market benefited from a degree of normalisation of trade.The Company’s net asset value (NAV) was up 56.2% on a total return basis, and the returnto shareholders was 53.1% in sterling terms. This resulted in the Company outperformingits benchmark, the MSCI Russian 10/40 Equity Indices Index by 5.4% on a net asset basis.As referred to in the Chairman’s Statement, effective from the 1st November 2016the Company’s benchmark was changed to the RTS Index (sterling).

In the market, the start of the period under review was much like the beginning of theprevious year, with a global risk sell-off and oil price weakness leading to a slide for Russianequities. The turnaround for the Russian market came with a 90% jump in the oil price(Brent crude) from the lows of February 2016 to the middle of June 2016. At the same time,sentiment was lifted by positive newsflow as economic conditions stabilised: The Rubleappreciated by 10%; the Central Bank of Russia cut rates by 1 percentage point; the currentaccount balance stayed positive and domestic consumption showed signs of bottoming out.Earnings revisions have been mixed so far, but an increase in payout ratios has helped toimprove the dividend yield of the market. The exceptionally large dividends the Companyreceived from Surgutneftegaz in the prior year, were not repeated in 2016.

Asset allocation and stock selection added 3.5% and 2.7% respectively to performance. Theunderweight positions in telecommunications and utilities were contributors to the positivestock selection performance. In the portfolio, the companies that contributed to returns overthe period were broad-based. In the financials sector, our longstanding exposure toSberbank, the dominant banking franchise in Russia and a clear market leader, was positive,as was our avoidance of VTB, the second-largest bank, which has state involvement.Similarly, we benefited from an underweight to telecoms giant Rostelecom, Russia’s leadinglong-distance telephony company, which reflected our concerns around the economics andgovernance of the business, which are not expected to change fundamentally yet. Other keypositions, in Magnit, Russia’s largest retailer, and Ros Agro, an industry leader in agriculturalcommodities and food, also contributed positively.

Detractors were also spread across companies we hold and like, and those where we wereunderweight. In the energy space, we were underweight Lukoil for most of the year givenour preference for other companies, and in materials, we held low exposure to diamondmining company Alrosa. Both of these positions hurt us when the prices moved sharply up.Another energy company, Surgutneftegas, paid a large dividend during the year, but failedto keep up with the market rally. The consumer food producer Cherkizovo was adisappointment, with its earnings outlook deteriorating over the period. Finally, internetstock Qiwi was a stock selection mistake, as we realised the company did not offer thequality and prospects we had believed.

Portfolio positioningThe widening of the Company’s Investment Policy agreed by shareholders at the Company’sAGM in March 2016 provides a broader investment universe, allowing the Company to investup to 10% of its gross assets in companies that operate or are located in former SovietRepublics. This has allowed the manager to establish positions in new names, includingtechnology companies EPAM and Luxoft, and Georgia’s TBC Bank. At the Company’s year endthese companies represented 3.71% of the portfolio value. Further acquisitions will beconsidered subject to availability and the Company’s Investment Regulations Guidelines.

Oleg I. Biryulyov

INVESTMENT MANAGER’S REPORT

Russian Securities_pp01_20 19/01/2017 17:40 Page 7

8 JPMORGAN RUSSIAN SECURITIES PLC. ANNUAL REPORT & ACCOUNTS 2016

Strategic Report continued

INVESTMENT MANAGER’S REPORT CONTINUED

The Company has reduced exposure to Surgutneftegaz, a long-held position in the portfolio,due to the weak outlook for earnings and dividend payments.

Energy holdings are high relative to the history of the Company. Large holdings in Gazprom,Rosneft and Lukoil reflect the Manager’s view that these companies are attractively valuedwith a good outlook for dividends while a position in Novatek reflects the Manager’sexpectations of superior production growth and cash flow generation.

Investment Management Team The Company’s Investment Management Team is part of J.P. Morgan Asset Management’sEmerging Markets and Asia Pacific Equities team (EMAP). The EMAP team is headed byRichard Titherington and consists of around 100 investment professionals withapproximately USD 90 billion under management. As referred to in the Chairman’sStatement of the Company’s Half Year Report and Accounts to 30th April 2016, Sonal Tannatransferred into another area of EMAP and is no longer involved as an Investment Managerof the Company. A team of Investment professionals within EMAP are available to supportme in managing the Company’ s portfolio. In addition a succession plan helps ensurea process for the continuity of Investment Management services to the Company.

PERFORMANCE ATTRIBUTION FOR THE YEAR ENDED 31ST OCTOBER 2016

% %

Contributions to total returns

Benchmark return 50.8

Asset allocation 3.5

Stock selection 2.7

Gearing/(net cash) 0.6

Investment Manager contribution 6.8

Portfolio return 57.6

Management fee/other expenses –1.4

Return on net assets 56.2

Effect of movement in discount over the year –3.1

Return to shareholders 53.1

Source: FactSet, JPMAM and Morningstar. All figures are on a total return basis.

Performance attribution analyses how the Company achieved its recorded performancerelative to its benchmark index.

A glossary of terms and definitions is provided on page 63.

Russian Securities_pp01_20 19/01/2017 17:40 Page 8

9

OutlookWe believe that economic stabilisation is underway in Russia, with positive implications forRussian equities. At the same time, we anticipate reduced volatility in the oil price over thenext 12-18 months as lower investment over the last three years starts to cap globalproduction growth. Greater stability of the oil price will help to improve the outlook for theRuble and for earnings growth, particularly in US dollar and sterling terms.

Two years on from the introduction of the sanctions, we have started to see early signs ofa recovery in domestic demand. The real estate sector was the early indicator, with demandimproving for mortgage products. The market for cars has also steadied and we expectgrowth in 2017. An increase in consumer demand should ultimately feed through intoa resumption of corporate long-term investment plans, in consumer sectors and thenbeyond, supported by falling interest rates.

We continue to see scope for reforms and hope that slowly but surely further liberalizationand restructuring of the Russian economy will take place. Privatization can be useful tool forGovernment to address budget constraints and we would anticipate a number of suchtransactions in the coming year.

On the dividend front, Russia is beginning to deliver on its promise of becoming ahigher-yielding market, and with the payout ratio less than 50% at the market level there isfurther scope for improvement. It is important to highlight that the state is becoming moreactive as a shareholder, so that state-controlled companies are now willing to commit tohigher payout ratios.

The domestic political outlook currently looks stable in Russia. Although we would expect tosee some rotation of specialists in the government and presidential administration, we thinkthe senior leadership in the country will remain unchanged for the foreseeable future.Parliament elections in September ran smoothly as expected, although surprisingly, UnitedRussia won a landslide victory despite the difficult economic environment. This should allowthe implementation of tougher reforms in the next couple of years prior to the Presidentialelections in 2018 and supports our view of a stable outlook for fiscal policy. The globalpolitical outlook would appear to be improving somewhat for Russia, although there are stillmany uncertainties whilst western sanctions continue, and the conflict in Syria heightenstensions generally.

Based on the comments above we hope that slowly but surely further liberalisation andrestructuring of the Russian economy will take place. For investors willing to accept thecurrent level of country risk, we believe that current equity valuations are attractive.

Oleg I. BiryulyovInvestment Manager 20th January 2017

Russian Securities_pp01_20 19/01/2017 17:40 Page 9

10 JPMORGAN RUSSIAN SECURITIES PLC. ANNUAL REPORT & ACCOUNTS 2016

2016 2015

Total returns for the year ended 31st October

Return to shareholders1 +53.1% –13.5%Return on net assets2 +56.2% –14.2%Benchmark3 +50.8% –13.4%

Net asset value, share price and discount at 31st October % change

Shareholders’ funds (£’000) 284,894 194,640 +46.4Net asset value per share 544.3p 371.9p +46.4Share price 455.0p 320.5p +42.0Exchange rate (US$ : £1) 1.22 1.54 –20.8Exchange rate (Ruble : £1) 77.27 98.60 –21.6Share price discount to net asset value per share 16.4% 13.8%Shares in issue 52,337,112 52,337,112

Revenue for the year ended 31st October

Gross revenue return (£’000) 11,109 13,598 –18.3Net revenue return on ordinary activities after taxation (£’000) 8,096 10,268 –21.2Revenue return per share 15.47p 19.60p –21.1Proposed ordinary dividend per share4 14.0p 13.0pProposed special dividend per share4 0.0p 4.0p

Net cash at 31st October5 (1.8)% (1.4)%

Ongoing Charges 1.40% 1.43%

1 Source: Morningstar.2 Source: J.P. Morgan.3 Source: MSCI. The benchmark is the MSCI Russian 10/40 Equity Indices Index in sterling terms. Effective from 1st November 2016, the Company’s benchmark is the RTS Index insterling terms (RTS).

4 2016: Dividend proposed is subject to Shareholder approval of Resolution 14 at the 2017 Annual General Meeting.5 The methodology to calculate gearing has been amended during the year therefore the comparative figure has been recalculated for comparative purposes. Please refer to theglossary of items and definitions on page 63 for the revised calculation.

A glossary of terms and definitions is provided on page 63.

Strategic Report continued

SUMMARY OF RESULTS

Russian Securities_pp01_20 20/01/2017 11:27 Page 10

11

PERFORMANCE

Ten Year PerformanceFIGURES HAVE BEEN REBASED TO 100 AT 31ST OCTOBER 2006

Source: Morningstar/MSCI.

JPMorgan Russian Securities – share price. JPMorgan Russian Securities – net asset value per share. Benchmark.

0

50

100

150

200

250

20162015201420132012201120102009200820072006

Performance Relative to BenchmarkFIGURES HAVE BEEN REBASED TO 100 AT 31ST OCTOBER 2006

Source: Morningstar/MSCI.

JPMorgan Russian Securities – share price. JPMorgan Russian Securities – net asset value per share. Benchmark.

60

70

80

90

100

110

120

20162015201420132012201120102009200820072006

Russian Securities_pp01_20 19/01/2017 17:40 Page 11

12 JPMORGAN RUSSIAN SECURITIES PLC. ANNUAL REPORT & ACCOUNTS 2016

At 31st October 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Net assets (£’m) 265.0 403.5 142.7 260.0 376.1 311.1 298.8 332.4 236.4 194.6 284.9

Net asset value per share (p) 473.1 721.4 255.1 464.9 680.3 564.4 555.2 631.1 450.0 371.9 544.3Share price (p) 436.8 665.5 257.0 416.0 637.5 531.0 498.0 560.0 386.8 320.5 455.0

(Discount)/premium (%) (7.7) (7.7) 0.7 (10.5) (6.3) (5.9) (10.3) (11.3) (14.0) (13.8) (16.4)Gearing/(net cash) (%)1 2.8 5.1 (7.0) 0.5 (3.0) (2.1) (2.1) (2.3) (1.0) (1.4) (1.8)

Ongoing Charges (%) 1.89 1.78 2.53 1.85 1.71 1.82 1.51 1.44 1.50 1.43 1.40

Year ended 31st October

Gross revenue (£’000) 4,388 7,469 9,632 950 6,034 7,550 8,589 12,902 9,383 13,598 11,109

Revenue (loss)/returnper share (p) (1.34) (1.32) 0.95 (4.11) (0.69) (0.63) 5.03 18.14 13.38 19.60 15.47

Ordinary dividends per share (p)2 — — — — — — — 15.3 13.0 13.0 14.0

Special dividends per share (p)2 — — — — — — — — — 4.0 —

Returns rebased to 100 at 31st October 2006

Return to shareholders3 100.0 152.4 58.8 95.2 145.9 121.5 114.0 128.2 91.2 78.9 120.8

Return on net assets3 100.0 152.5 53.7 98.2 143.8 119.3 117.3 133.4 97.7 84.0 131.2

Benchmark return4 100.0 147.6 70.9 120.6 153.7 149.3 140.7 150.7 119.0 103.1 155.5

1 The methodology to calculate gearing has been amended during the year therefore the 2015 comparative figure has been recalculated for comparative purposes. Please refer tothe glossary of items and definitions on page 63 for the revised calculation.

2 2016: Dividend proposed is subject to Shareholder approval of Resolution 14 at the 2017 Annual General Meeting.3 Source: Morningstar/JPMorgan.4 Source: MSCI. The benchmark is the MSCI Russian 10/40 Equity Indices Index in sterling terms. Effective from 1st November 2016, the Company’s benchmark is the RTS Index in

sterling terms (RTS).

A glossary of terms and definitions is provided on page 63.

Strategic Report continued

TEN YEAR FINANCIAL RECORD

Russian Securities_pp01_20 19/01/2017 17:40 Page 12

13

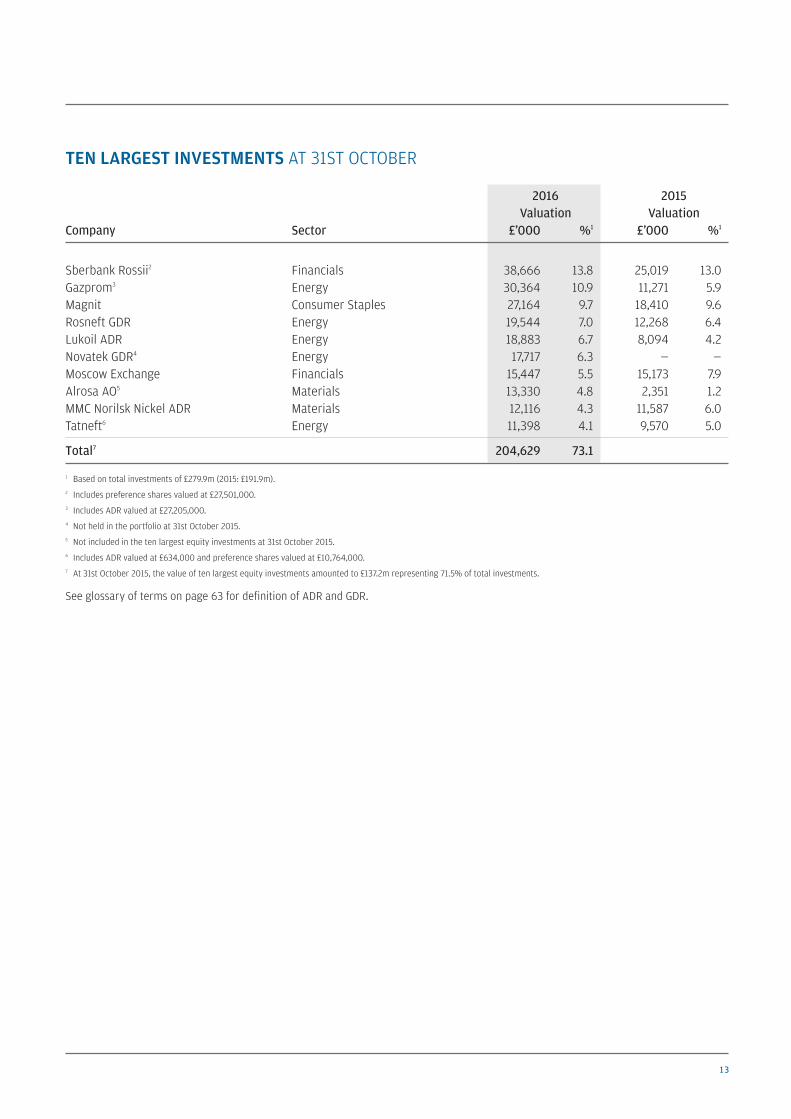

2016 2015 Valuation ValuationCompany Sector £’000 %1 £’000 %1

Sberbank Rossii2 Financials 38,666 13.8 25,019 13.0 Gazprom3 Energy 30,364 10.9 11,271 5.9 Magnit Consumer Staples 27,164 9.7 18,410 9.6 Rosneft GDR Energy 19,544 7.0 12,268 6.4 Lukoil ADR Energy 18,883 6.7 8,094 4.2 Novatek GDR4 Energy 17,717 6.3 — —Moscow Exchange Financials 15,447 5.5 15,173 7.9 Alrosa AO5 Materials 13,330 4.8 2,351 1.2 MMC Norilsk Nickel ADR Materials 12,116 4.3 11,587 6.0 Tatneft6 Energy 11,398 4.1 9,570 5.0

Total7 204,629 73.1

1 Based on total investments of £279.9m (2015: £191.9m).2 Includes preference shares valued at £27,501,000.3 Includes ADR valued at £27,205,000.4 Not held in the portfolio at 31st October 2015.5 Not included in the ten largest equity investments at 31st October 2015.6 Includes ADR valued at £634,000 and preference shares valued at £10,764,000.7 At 31st October 2015, the value of ten largest equity investments amounted to £137.2m representing 71.5% of total investments.

See glossary of terms on page 63 for definition of ADR and GDR.

TEN LARGEST INVESTMENTS AT 31ST OCTOBER

Russian Securities_pp01_20 20/01/2017 12:09 Page 13

14 JPMORGAN RUSSIAN SECURITIES PLC. ANNUAL REPORT & ACCOUNTS 2016

31st October 2016 31st October 2015 Portfolio Benchmark Portfolio Benchmark %1 % %1 %

Energy 36.5 40.1 31.3 41.1Financials 20.7 17.5 20.9 18.4Materials 15.3 17.8 18.7 13.6Consumer Staples 14.9 8.5 18.3 8.7Real Estate2 3.5 — — —Telecommunication Services 2.6 11.3 1.7 13.8Information Technology 2.4 — 4.3 —Consumer Discretionary2 2.2 — 3.4 —Health Care 1.6 — 0.9 —Industrials 0.3 — 0.5 —Utilities — 4.8 — 4.4

Total 100.0 100.0 100.0 100.0

1 Based on total investments of £279.9m (2015: £191.9m).2 Etalon GDR was reclassified to Real Estate from Consumer Discretionary as at 31st October 2016.

Strategic Report continued

SECTOR ANALYSIS

Russian Securities_pp01_20 19/01/2017 17:40 Page 14

15

ValuationCompany £’000

ValuationCompany £’000

EnergyGazprom1 30,364Rosneft GDR 19,544Lukoil ADR 18,883Novatek GDR 17,717Tatneft2 11,398Nostrum Oil & Gas 2,901Volga Gas 1,256Total Energy 102,063

FinancialsSberbank Rossii3 38,666Moscow Exchange 15,447TBC Bank 3,806Total Financials 57,919

MaterialsAlrosa AO 13,330MMC Norilsk Nickel ADR 12,116OAO Severstal GDR 10,253Phosagro GDR 4,132Acron 3,067Total Materials 42,898

Consumer StaplesMagnit 27,164Ros Agro GDR 8,483X5 Retail GDR 5,934Total Consumer Staples 41,581

Real EstateEtalon GDR 6,025LSR GDR 3,695Total Real Estate 9,720

Telecommunication ServicesMegafon GDR 7,423Total Telecommunication Services 7,423

Information TechnologyLuxoft 3,476EPAM systems 3,282Total Information Technology 6,758

Consumer DiscretionarySollers 3,482M Video 2,662Total Consumer Discretionary 6,144

Health CareMD Medical GDR 4,359Total Health Care 4,359

IndustrialsGlobal Ports Investments GDR 1,000Total Industrials 1,000Total Investment Portfolio 279,865

See Glossary for definition of ADR/GDR.1 Includes ADR valued at £27,205,000.2 Includes ADR valued at £634,000 and preference shares valued at £10,764,000.3 Includes preference shares valued at £27,501,000.

LIST OF INVESTMENTS AT 31ST OCTOBER 2016

Russian Securities_pp01_20 19/01/2017 17:40 Page 15

16 JPMORGAN RUSSIAN SECURITIES PLC. ANNUAL REPORT & ACCOUNTS 2016

The aim of the Strategic Report is to provide shareholders with theability to assess how the Directors have performed their duty topromote the success of the Company during the year under review.To assist shareholders with this assessment, the Strategic Reportsets out the structure and objective of the Company, its investmentpolicies and risk management, investment limits and restrictions,performance and key performance indicators, share capital,principal risks and how the Company seeks to manage those risks,the Company’s environmental, social and ethical policy, futuredevelopments and long term viability.

Business ModelJPMorgan Russian Securities plc is an investment trust and hasa premium listing on the London Stock Exchange. Its objective is toprovide shareholders with capital growth, primarily from investingin quoted Russian securities. In seeking to achieve this objective theCompany employs J.P. Morgan Funds Limited (‘JPMF’ or the‘Manager’) which in turn delegates portfolio management toJPMorgan Asset Management (UK) Limited (‘JPMAM’) to activelymanage the Company’s assets. The Board has determinedinvestment policies and related guidelines and limits, as describedbelow. It aims to outperform the MSCI Russian 10/40 Equity IndicesIndex in sterling terms, in the long term with net dividendsreinvested, expressed in sterling terms. The Company changed itsbenchmark to the RTS Index in sterling terms effective from1st November 2016.

The Company is an investment company within the meaning ofSection 833 of the Companies Act 2006 and has been approved byHMRC as an investment trust (for the purposes of Sections 1158 and1159 of the Corporation Tax Act 2010). As a result the Company isnot liable to taxation on capital gains. The Directors have no reasonto believe that approval will not continue to be retained.

A review of the Company’s activities and prospects is given in theChairman’s Statement on pages 3 to 6, and in the InvestmentManager’s Report on pages 7 to 9.

Investment Policies and Risk Management In order to achieve its objective and manage risk, the Companyinvests in a diversified portfolio of investments primarily in quotedRussian securities or other companies which operate principally inRussia. The Company may also invest up to 10% of its gross assets incompanies that operate or are located in former Soviet UnionRepublics. The number of investments in the portfolio will normallyrange between 20 and 50. The investment portfolio is managed bya Russian fund manager, currently based in London, and fullysupported by a global emerging markets team, including sectorspecialists. The Board also discusses the economy and politicaldevelopments of Russia in depth at Board meetings and considersthe possible implications for the investment portfolio.

Investment Limits and Restrictions The Board seeks to manage some of the Company’s risks byimposing various investment limits and restrictions.

• No more than 10% of the Company’s gross assets are to beinvested in companies that operate or are located in formerSoviet Union Republics.

• The Company will not normally invest in unlisted securities.

• At the time of purchase, the maximum permitted exposure toeach individual company is 15% of the Company’s gross assets.

• The Company will not normally invest in derivatives.

• The Company will utilise liquidity and borrowings in a range of10% net cash to 15% geared in typical market conditions.

• No more than 15% of gross assets are to be invested in otherUK listed investment companies (including investment trusts).

Compliance with the Board’s investment restrictions and guidelinesis monitored continuously by the Manager and is reported to theBoard on a monthly basis.

These limits and restrictions may be varied by the Board at any timeat its discretion.

The economic sanctions introduced by the USA and European Unionagainst Russia and Crimea in 2014 continue and were furtherextended in 2016. The Manager undertakes regular checks of holdingsto ensure compliance and reports to the Board. The Board has alsoimplemented a rapid response communication process with theManager, which allows the Board to receive immediate updates fromthe Manager and take decisions as quickly as possible.

Active Fund Management RationaleJPMAM believes that the Russian market is inefficient and that thisis demonstrated by the high and variable volatility of many marketsectors and individual companies. Although corporate disclosureand transparency is improving, there still remain areas where theinefficiencies in this region can be exploited offering opportunitiesto experienced, well-informed investors.

JPMAM’s investment process has been specifically designed foremerging markets and has been refined over 20 years of activemanagement experience in the region.

Highlights of the investment strategy are:

• Inefficient, immature emerging markets reward active investmentmanagement not indexation.

• Identifying growth companies that are well managed to maximiseshareholder returns brings outperformance through fundamentalbottom-up research.

• Valuation disciplines avoid overpaying for growth.

Strategic Report continued

BUSINESS REVIEW

Russian Securities_pp01_20 19/01/2017 17:40 Page 16

17

• JPMAM believes that assets are best managed by specialists fromthe markets and regions in which they have expertise and theyhave therefore established a strong presence around the region.Company visits and local knowledge are also key.

JPMAM has managed money in Russia since 1994. JPMAM’sEmerging Markets and Asia Pacific Group is responsible formanaging all emerging market equity. The approximately 90 teammembers are located in four offices, managing US$50 billion forclients globally.

PerformanceIn the year ended 31st October 2016, the Company produced a totalreturn to shareholders of +53.1% and a total return on net assets of+56.2%. This compares with the return on the Company’sbenchmark of +50.8%. As at 31st October 2016, the value of theCompany’s investment portfolio was £279,865,000. The InvestmentManager’s Report on pages 7 to 9 includes a review ofdevelopments during the year.

The results of the investment strategy, as detailed above, and theperformance of the Company against its benchmark, as identified onpage 2 are regularly reviewed by the Board together with datarelating to the performance of the Company’s Peers and feedbackfrom some of the major shareholders. The Board also considersfactors likely to affect the future performance of the Company.

Total Return, Revenue and DividendGross return for the year totalled £106,695,000 (2015: £29,821,000loss) and net return after deducting management fee, administrativeexpenses, and taxation, amounted to £102,291,000 (2015:£34,414,000 loss). Net revenue after taxation for the year amountedto £8,096,000 (2015: £10,268,000).

The Directors recommend a final ordinary dividend of 8.0 pence pershare as detailed in the Chairman’s Statement on page 4.

Key Performance Indicators (‘KPIs’) The Board uses a number of financial KPIs to monitor and assess theperformance of the Company. The principal KPIs are:

• Performance against the benchmark The principal objective is to achieve capital growth. However, theBoard also monitors performance against a benchmark index.Please refer to page 12 for details of the Company’s performanceagainst the MSCI Russian 10/40 Equity Indices in sterling terms.The Company’s benchmark is the RTS index effective from1st November 2016 as detailed in the Chairman’s Statementon page 3.

• Performance against the Company’s peers The Board also monitors the performance relative to a broadrange of competitor funds. The Company’s performance for thecurrent period is comparable to those of its peers.

• Performance attributionThe purpose of performance attribution analysis is to assess howthe Company achieved its performance relative to its benchmarkindex, i.e. to understand the impact on the Company’s relativeperformance of the various components such as asset allocationand stock selection. Please refer to page 8 for the Company’sperformance attribution for the year ended 31st October 2016.

• Share price (discount)/premium to net asset value (‘NAV’) per shareThe Board has adopted a share repurchase policy which seeks toaddress imbalances in the supply of and demand for theCompany’s shares in the market and thereby reduce the volatilityand absolute level of the discount to NAV per share at which theCompany’s shares trade. The Boards implementation of the policyis subject to market conditions. In the year ended 31st October2016, the shares traded at a discount between 13.8% and 18.2%based on month end data. See the Discount Control section ofChairman’s statement for further detail see page 5.

(Discount)/Premium Performance

Source: Datastream.

JPMorgan Russian Securities – share price discount/premium to NAV (monthend data points).

• Ongoing ChargesThe Ongoing Charges represent the Company’s management feeand all other operating expenses excluding finance costs,expressed as a percentage of the average daily net assets duringthe year. The Ongoing Charges for the year ended 31st October2016 were 1.40% (2015: 1.43%). The Board reviews each year ananalysis which shows a comparison of the Company’s OngoingCharges and its main expenses with those of its peers.

Share CapitalDuring the year, the Company did not make any market purchases ofits own shares. Since the year end the Company has notrepurchased any ordinary shares. Further details regarding theCompany’s purchase of its own shares can be seen in the Chairman’sreport on page 5.

A resolution to renew the authority to repurchase shares at adiscount to NAV is due to be put to shareholders at the forthcomingAnnual General Meeting.

The Company did not issue any new shares during the year.

–20

–15

–10

–5

0

5

20162015201420132012201120102009200820072006

Russian Securities_pp01_20 20/01/2017 10:02 Page 17

18 JPMORGAN RUSSIAN SECURITIES PLC. ANNUAL REPORT & ACCOUNTS 2016

The Modern Slavery Act 2015 (the ‘MSA’)The MSA requires companies to prepare a slavery and humantrafficking statement for each financial year of the organisation.As the Company has no employees and does not supply goodsand services, the MSA does not apply directly to it. The MSArequirements more appropriately relate to JPMF and JPMAM.JPMorgan’s statement on Human Rights can be found on thefollowing website: www.jpmorganchase.com/corporate/About-JPMC/ab-human-rights.htm

Principal RisksThe Directors confirm that they have carried out an assessment ofthe principal risks facing the Company, including those that wouldthreaten its business model, future performance, solvency orliquidity. The risks identified and the ways in which they aremanaged or mitigated are summarised as follows:

With the assistance of the Manager, the Board has drawn up a riskmatrix, which identifies the key risks to the Company and theCompany’s actions to manage the risks.

In the year under review the Board monitored the risks arising whichincluded continuing sanctions against Russia and the significant fallsin the price of oil and valuation of the Ruble which have impactedmarket sentiment.

These key risks fall broadly under the following categories:

• Investing in Russia: Investors should note that there aresignificant risks inherent in investing in Russian securities nottypically associated with investing in securities of companies inmore developed countries. In terms of gauging the economic andpolitical risk of investing in Russia, it frequently appears in thehigher risk categories when compared with most Westerncountries. The value of Russian securities, and therefore the netasset value of the Company, may be affected by uncertaintiessuch as economic, political or diplomatic developments, socialand religious instability, taxation and interest rates, currencyrepatriation restrictions, crime and corruption and developmentsin the law or regulations in Russia and, in particular, the risks ofexpropriation, nationalisation and confiscation of assets andchanges in legislation relating to the level of foreign ownership.

The Board, with the assistance of the Manager, monitors theCompany’s activities to ensure that they remain compliant withthe current sanctions regime including the specific requirementsapplicable to the Manager as a company subject to the laws of theUnited States of America. The Board acknowledges the negativeimpact of sanctions on the wider market although the currentsanctions regime has not prevented the Company from operatingwithin its investment guidelines.

• Share Price Discount to Net Asset Value (‘NAV’) per Share: If theshare price of an investment trust is lower than the NAV pershare, the shares are said to be trading at a discount. Thewidening of the discount can be seen as a disadvantage ofinvestment trusts which could discourage investors. Although it iscommon for an investment trust’s shares to trade at a discount,the current sanctions regime and recent large falls in the price ofoil and value of the Ruble have negatively impacted marketsentiment. The Board monitors the Company’s discount level andseeks, where deemed prudent, to address imbalances in thesupply and demand of the Company’s shares through aprogramme of share buybacks.

• Investment Under Performance and Strategy: An inappropriateinvestment strategy, for example asset allocation or the level ofgearing, may lead to underperformance against the Company’sbenchmark index and peer companies. The Board manages theserisks by diversification of investments through its investmentrestrictions and guidelines, which are monitored and reported onby the Manager. The Manager provides the Directors with timelyand accurate management information, including performancedata and attribution analyses, revenue estimates, liquidity reportsand shareholder analyses. The Board monitors the implementationand results of the investment process with the investmentmanagers, who attend all Board meetings, and reviews data whichshow statistical measures of the Company’s risk profile.

Possible actions include changing the portfolio manager orselecting another manager.

• Failure of Investment Process: A failure of process could lead tolosses. The Manager mitigates this risk through internal controlsand monitoring. Fraud requires immediate notification to theBoard and regular reports are provided on control processes.

• Loss of Investment Team or Investment Manager: The suddendeparture of the investment manager or several members of thewider investment management team could result in a short termdeterioration in investment performance. The Manager takessteps to reduce the likelihood of such an event by ensuringappropriate succession planning and the adoption of a teambased approach, as well as special efforts to retain key personnel.

• Operational and Cyber Crime: Disruption to, or failure of, theManager’s accounting, dealing or payments systems or theDepositary or custodian’s records could prevent accurate reportingand monitoring of the Company’s financial position. Under theterms of its agreement, the Depositary has strict liability for theloss or misappropriation of assets held in custody. See note 19(c)for further details on the responsibilities of the Depositary. Details

Strategic Report continued

BUSINESS REVIEW CONTINUED

Russian Securities_pp01_20 19/01/2017 17:40 Page 18

19

of how the Board monitors the services provided by JPMF and itsassociates and the key elements designed to provide effectiveinternal control are included within the Internal Control section ofthe Corporate Governance report on pages 28 and 29. The threatof Cyber attack is increasing and regarded as having the ability tocause equivalent disruption to the Company’s business as moretraditional business continuity and security threats. The Companybenefits from JPMorgan’s Cyber Security Programme. Theinformation technology controls around the physical security ofJPMorgan’s data centres, security of its networks and security of itstrading applications are tested by Deloitte and reported every sixmonths against the AAF standard.

• Board Relationship with Shareholders: The risk that theCompany’s strategy and performance does not align withshareholders expectations is addressed by the Manager andincludes the organisation of a programme of visits to majorshareholders, and the provision of an extensive range of investorinformation including nationwide presentations by sales teams.Feedback from shareholders is received directly and via brokerswhich is fed back to the Board regularly.

• Political and Economic: Changes in financial or tax legislation,including in the European Union, may adversely affect theCompany. The Manager makes recommendations to the Board onaccounting, dividend and tax policies and the Board seeks externaladvice where appropriate. In addition, the Company is subject toadministrative risks, such as the imposition of restrictions on thefree movement of capital. A widening of the capital controlsrecently introduced by the Russian Government could negativelyimpact the Company. The introduction of limitations on the abilityof Russian companies to distribute dividends to foreign companiescould materially reduce the Company’s revenue and amountavailable for distribution to shareholders.

• Regulatory and Legal: Breach of regulatory rules could lead tosuspension of the Company’s Stock Exchange listing, financialpenalties, or a qualified audit report. Loss of investment truststatus could lead to the Company being subject to tax on capitalgains. The Directors seek to comply with all relevant regulationand legislation and rely on the services of its Company Secretary,the Manager, and its professional advisors to monitor compliancewith all relevant requirements.

• Market and Financial: The Company’s assets consist of listedsecurities and it is therefore exposed to movements in the pricesof individual securities and the market generally. The Boardconsiders asset allocation and stock selection on a regular basisand has set investment restrictions and guidelines, which aremonitored and reported on by the Manager. The recent significant

falls in the price of oil and devaluation of the Ruble have hada negative impact on the Company’s NAV. The financial risks facedby the Company include market price risk, interest rate risk,foreign currency risk, liquidity risk and credit risk. Further detailsare disclosed in note 19 on pages 53 to 57. The Manager regularlymonitors the liquidity of the portfolio including determining themarket valuation of securities held, the average daily volume andnumber of days to liquidate a holding. As can be seen in Note 18on page 52, all the Company’s assets are categorised as Level 1 asthey have quoted prices in an active market.

Board DiversityWhen recruiting a new Director, the Board’s policy is to appointindividuals on merit. Diversity is important in bringing anappropriate range of skills and experience to the Board.

At 31st October 2016, there were three male Directors and twofemale Directors on the Board. The Company has no employees andtherefore there is nothing further to report in respect of diversitywithin the Company.

Employees, Social, Community and Human Rights IssuesThe Company is managed by JPMF, has no employees and all of itsDirectors are non-executive, the day to day activities being carriedout by third parties. There are therefore no disclosures to be madein respect of employees. The Board notes the JPMAM policystatements in respect of Social, Community, Environmental andHuman Rights issues, as outlined below.

Social, Community, Environmental and Human RightsJPMAM believes that companies should act in a socially responsiblemanner. Although our priority at all times is the best economic interestsof our clients, we recognise that, increasingly, non-financial issues suchas social and environmental factors have the potential to impact theshare price, as well as the reputation of companies. Specialists withinJPMAM’s environmental, social and governance (‘ESG’) team are taskedwith assessing how companies deal with and report on social andenvironmental risks and issues specific to their industry.

JPMAM is also a signatory to the United Nations Principles of ResponsibleInvestment, which commits participants to six principles, with the aimof incorporating ESG criteria into their processes when making stockselection decisions and promoting ESG disclosure. Our detailed approachto how we implement the principles is available on request.

Future Developments The future development of the Company is much dependent uponthe success of the Company’s investment strategy in the light ofeconomic and equity market developments. The Chairman andInvestment Manager discusses the outlook in their respectivereports on pages 3 and 7.

Russian Securities_pp01_20 19/01/2017 17:40 Page 19

20 JPMORGAN RUSSIAN SECURITIES PLC. ANNUAL REPORT & ACCOUNTS 2016

Long Term ViabilityTaking account of the Company’s current position, the principalrisks that it faces and their potential impact on its futuredevelopment and prospects, the Directors have assessed theprospects of the Company, to the extent that they are able to do so,over the next five years. They have made that assessment byconsidering those principal risks, the Company’s investmentobjective and strategy, the investment capabilities of the Managerand the current outlook for the Russian economy and equitymarket. It has also taken into account the fact that the Companyhas a continuation vote at the 2017 AGM and, with input from theCompany’s major shareholders and its brokers, the likelihood ofshareholders voting in favour of continuation. Based on thatinformation the Directors do not think that the continuation votewill impact on the Company’s long term viability. In determining theappropriate period of assessment the Directors had regard to their

view that, given the Company’s objective of achieving long termcapital growth, shareholders should consider the Company as along term investment proposition. This is consistent with adviceprovided by independent financial advisers and wealth managers,that investors should consider investing in equities for a minimumof five years. Thus the Directors consider five years to be anappropriate time horizon to assess the Company’s viability. TheDirectors confirm that they have a reasonable expectation that theCompany will be able to continue in operation and meet itsliabilities as they fall due over the five year period of assessment.

By order of the Board Paul Winship, ACIS for and on behalf of JPMorgan Funds Limited, Secretary

20th January 2017

Strategic Report continued

BUSINESS REVIEW CONTINUED

Russian Securities_pp01_20 19/01/2017 17:40 Page 20

21

Governance

BOARD OF DIRECTORS

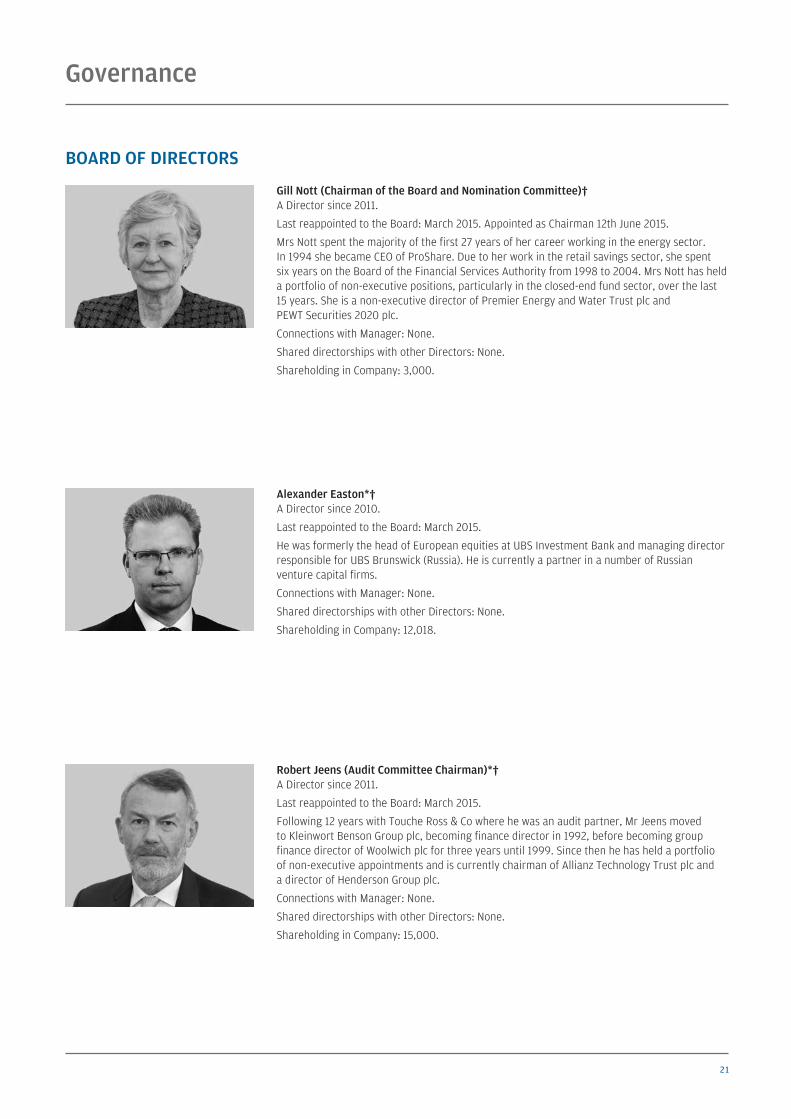

Robert Jeens (Audit Committee Chairman)*†A Director since 2011.

Last reappointed to the Board: March 2015.

Following 12 years with Touche Ross & Co where he was an audit partner, Mr Jeens movedto Kleinwort Benson Group plc, becoming finance director in 1992, before becoming groupfinance director of Woolwich plc for three years until 1999. Since then he has held a portfolioof non-executive appointments and is currently chairman of Allianz Technology Trust plc anda director of Henderson Group plc.

Connections with Manager: None.

Shared directorships with other Directors: None.

Shareholding in Company: 15,000.

Alexander Easton*†A Director since 2010.

Last reappointed to the Board: March 2015.

He was formerly the head of European equities at UBS Investment Bank and managing directorresponsible for UBS Brunswick (Russia). He is currently a partner in a number of Russianventure capital firms.

Connections with Manager: None.

Shared directorships with other Directors: None.

Shareholding in Company: 12,018.

Gill Nott (Chairman of the Board and Nomination Committee)†A Director since 2011.

Last reappointed to the Board: March 2015. Appointed as Chairman 12th June 2015.

Mrs Nott spent the majority of the first 27 years of her career working in the energy sector.In 1994 she became CEO of ProShare. Due to her work in the retail savings sector, she spentsix years on the Board of the Financial Services Authority from 1998 to 2004. Mrs Nott has helda portfolio of non-executive positions, particularly in the closed-end fund sector, over the last15 years. She is a non-executive director of Premier Energy and Water Trust plc andPEWT Securities 2020 plc.

Connections with Manager: None.

Shared directorships with other Directors: None.

Shareholding in Company: 3,000.

Russian Securities_pp21_33 19/01/2017 17:40 Page 21

22 JPMORGAN RUSSIAN SECURITIES PLC. ANNUAL REPORT & ACCOUNTS 2016

Governance continued

BOARD OF DIRECTORS CONTINUED

George Nianias*† A Director since 2008.

Last reappointed to the Board: March 2015.

He is the founder and group chairman of Denholm Hall Group. George has a close associationwith Russia and has also been financial adviser to several eastern European cities includingKrakow, St. Petersburg and Moscow.

Connections with Manager: None.

Shared directorships with other Directors: None.

Shareholding in Company: Nil.

* Member of the Audit Committee.

† Member of the Nomination Committee.

Tamara Sakovska*†Appointed 1st August 2016.

Tamara is an investment professional with significant experience in developed and emergingmarkets. She is currently an investment partner at Global Family Partners in London.Her previous role was Head of Origination, Europe in the private equity team at Eton ParkInternational LLP. Before joining Eton Park, Tamara worked at Permira in London and atGoldman, Sachs & Co. in New York. Tamara is a native Russian speaker.

Connections with Manager: None.

Shared directorships with other Directors: None.

Shareholding in Company: Nil.

Russian Securities_pp21_33 19/01/2017 17:40 Page 22

23

The Directors present their report and the audited financialstatements for the year ended 31st October 2016.

Management of the CompanyThe Manager and Company Secretary to the Company is JPMorganFunds Limited (‘JPMF’). Portfolio Management is delegated toJPMorgan Asset Management UK Limited (JPMAM).

JPMF and JPMAM are wholly-owned subsidiary of JPMorgan Chase& Co which, through other subsidiaries, also provides accounting,banking, dealing and custodian services to the Company.

The Board conducts a formal evaluation of the performance of, andcontractual relationship with, the Manager on an annual basis. Partof this evaluation includes a consideration of the management feesand whether the service received is value for money forshareholders. No separate management engagement committee hasbeen established because all Directors are considered to beindependent of the Manager and, given the nature of the Company’sbusiness, it is felt that all Directors should take part in the reviewprocess.

The Board has thoroughly reviewed the performance of theManager in the course of the year. The review covered theperformance of the Manager, its management processes,investment style, resources and risk controls and the quality ofsupport that the Company receives from the Manager including themarketing support provided. The Board is of the opinion that thecontinuing appointment of the Manager is in the best interests ofshareholders as a whole. Such a review is carried out on an annualbasis.

Management Agreement The current Management Agreement was entered into with effectfrom 1st July 2014 following implementations of the AlternativeFund Manager Directive.

JPMF is employed under a contract which can be terminated on90 days’ notice, without penalty. The Manager may also terminatethe contract on 90 days’ notice if in its sole opinion there has beena loss of confidence between the Manager and the Company so as tomake the relationship unworkable. If the Company wishes toterminate the contract on less than 90 days’ notice, the balance ofthe 90 days’ remuneration is payable by way of compensation.

The Manager is remunerated at a rate of 1.0% per annum of theCompany’s net assets, payable monthly in arrears.

Investments on which the Manager earns a separate managementfee are excluded from the Company’s net assets for the purpose ofcalculating the management fee. No performance fee is payable.

The Alternative Investment Fund Managers Directive(‘AIFMD’)JPMF, an affiliate of JPMAM, has been appointed as the Company’salternative investment fund manager (‘AIFM’). JPMF has beenapproved as an AIFM by the Financial Conduct Authority (‘FCA’).For the purposes of the AIFMD the Company is an alternativeinvestment fund (‘AIF’).

JPMF has delegated responsibility for the day to day management ofthe Company’s portfolio to JPMAM. JPMF is required to ensure thata depositary is appointed to the Company. The Company thereforehas appointed BNY Mellon Trust and Depositary (UK) Limited (‘BNY’)as its depositary. BNY has delegated its safekeeping function to thecustodian, JPMorgan Chase Bank, N.A., however, BNY remainsresponsible for the oversight of the custody of the Company’s assetsand for monitoring its cash flows.

The AIFMD requires certain information to be made available toinvestors in AIFs before they invest and requires that materialchanges to this information be disclosed in the annual report ofeach AIF. Investor Disclosure Documents, which set out informationon the Company’s investment strategy and policies, leverage, risk,liquidity, administration, management, fees, conflicts of interest andother shareholder information are available on the Company’swebsite at www.jpmrussian.co.uk

There have been no material changes (other than those reflected inthese financial statements) to this information requiring disclosure.Any information requiring immediate disclosure pursuant to theAIFMD will be disclosed to the London Stock Exchange througha primary information provider. As an authorised AIFM, JPMF willmake the requisite disclosures on remuneration levels and policiesto the FCA at the appropriate time.

Going Concern In assessing the Company’s ability to continue as a going concernthe Directors have considered the Company’s investment objective(see page 16), risk management policies (see pages 53 to 57), capitalmanagement (see note 20), the nature of the portfolio andexpenditure projections, and believe that the Company hasadequate resources, an appropriate financial structure and suitablemanagement arrangements in place to continue in operationalexistence for the foreseeable future. For these reasons, theDirectors believe that it is appropriate to continue to adopt thegoing concern basis in preparing the accounts. The Directorsconsidered the current political environment in Russia and theimpact of sanctions in making its assessment.

A resolution that the Company continue as an investment trust willbe put to shareholders at the Annual General Meeting in 2017 andevery five years thereafter. See the Chairman’s Statement forfurther details of the Continuation vote, page 4.

DIRECTORS’ REPORT

Russian Securities_pp21_33 19/01/2017 17:40 Page 23

24 JPMORGAN RUSSIAN SECURITIES PLC. ANNUAL REPORT & ACCOUNTS 2016

Directors The Directors of the Company who held office at the end of the yearare detailed on pages 21 and 22.

Details of Directors’ beneficial shareholdings may be found in theDirectors’ Remuneration Report on page 31. No changes have beenreported to the Directors’ shareholdings since the year end.

In accordance with corporate governance best practice, all Directorswill retire by rotation at the forthcoming Annual General Meetingand, being eligible, will offer themselves for reappointment. Havingbeen appointed to the Board on 1st August 2016 Tamara Sakovskawill be standing for appointment for the first time. The NominationCommittee, having considered their qualifications, performance andcontribution to the Board and its committees, confirms that eachDirector continues to be effective and demonstrates commitment tothe role and the Board recommends to shareholders that they beappointed/reappointed.

Director Indemnification and InsuranceAs permitted by the Company’s Articles of Association, the Directorshave the benefit of a deed of indemnity which is a qualifying thirdparty indemnity, as defined by Section 234 of the Companies Act2006. The deeds of indemnity were executed on 21st January 2011and are currently in force.

An insurance policy is maintained by the Company whichindemnifies the Directors of the Company against certain liabilitiesarising in the conduct of their duties. There is no cover againstfraudulent or dishonest actions.

Disclosure of information to Auditors In the case of each of the persons who are Directors of the Companyat the time when this report was approved:

(a) so far as each of the Directors is aware, there is no relevantaudit information (as defined in the Companies Act) of whichthe Company’s auditors are unaware, and

(b) each of the Directors has taken all the steps that he/sheought to have taken as a Director in order to make himself/herself aware of any relevant audit information and toestablish that the Company’s auditors are aware of thatinformation.

The above confirmation is given and should be interpretedin accordance with the provision of Section 418(2) of the CompaniesAct 2006.

Independent AuditorErnst & Young LLP have expressed their willingness to continue inoffice as auditor to the Company, and resolutions proposing their

reappointment and authorising the Directors to determine theirremuneration for the ensuing year will be put to shareholders at theAnnual General Meeting.

Annual General MeetingNOTE: THIS SECTION IS IMPORTANT AND REQUIRES YOURIMMEDIATE ATTENTION. If you are in any doubt as to theaction you should take, you should seek your own personalfinancial advice from your stockbroker, bank manager,solicitor or other financial adviser authorised under theFinancial Services and Markets Act 2000.

Resolutions relating to the following items of special business will beproposed at the forthcoming Annual General Meeting:

(i) Authority to allot relevant securities and disapplypre-emption rights (resolutions 11 & 12)

The Directors will seek renewal of the authority to issue up to2,616,856 new shares or shares held in Treasury other than by a prorata issue to existing shareholders up to an aggregate nominalamount of £26,169, such amount being equivalent to approximately5% of the current issued share capital. The full text of theresolutions is set out in the Notice of Meeting on pages 60 to 61.

It is advantageous for the Company to be able to issue new sharesto investors purchasing shares through the JPMAM savings productsand also to other investors when the Directors consider that it is inthe best interest of shareholders to do so. Any such issues wouldonly be made at prices greater than the NAV, thereby increasing theassets underlying each share.

(ii) Authority to repurchase the Company’s shares forcancellation (resolution 13)

The authority to repurchase up to 14.99% of the Company’s issuedshare capital, granted by shareholders at the 2016 Annual GeneralMeeting, will expire on 3rd March 2017 unless renewed at the 2017Annual General Meeting. The Directors consider that the renewal ofthe authority is in the interests of shareholders as a whole, as therepurchase of shares at a discount to the underlying NAV enhancesthe NAV of the remaining shares.

The full text of the resolution is set out in the Notice of AnnualGeneral Meeting on pages 60 to 61. Repurchases will be made at thediscretion of the Board and will only be made in the market at pricesbelow the prevailing NAV per share as and when market conditionsare appropriate.

(iii) Continuation resolution – Ordinary Resolution(resolution 14)

The Directors seek the shareholders approval to the ordinaryresolution for the Company to continue as an investment trust fora further five years.

Governance continued

DIRECTORS’ REPORT CONTINUED

Russian Securities_pp21_33 19/01/2017 17:40 Page 24

25

RecommendationThe Board considers that resolutions 11 to 14 are likely to promotethe success of the Company and are in the best interests of theCompany and its shareholders as a whole. The Directorsunanimously recommend that you vote in favour of the resolutionsas they intend to do in respect of their own beneficial holdingswhich amount in aggregate to 30,018 shares representingapproximately 0.1% of the voting rights in the Company.

Corporate Governance Statement

Compliance The Company is committed to high standards of corporategovernance. This statement, together with the Statement ofDirectors’ Responsibilities in respect of the Accounts on page 33,indicates how the Company has applied the principles of goodgovernance of the Financial Reporting Council’s UK CorporateGovernance Code (the ‘UK Corporate Governance Code’) and theAIC’s Code of Corporate Governance, (the ‘AIC Code’), whichcomplements the UK Corporate Governance Code and providesa framework of best practice for investment trusts.

The Board is responsible for ensuring the appropriate level ofcorporate governance and considers that, apart from certainmatters noted below, the Company has complied with the bestpractice provisions of the UK Corporate Governance Code, insofaras they are relevant to the Company’s business, and the AIC Codethroughout the year under review, except for the following areas:

— Role of the CEO, as the Company does not appoint a CEO;

— Executive Director remuneration as the Company does notappoint executive directors;

— Internal audit function as the Company relies on the internalaudit department of the manager; and

— Nomination of a Senior Independent Director. The Board hasconsidered whether a senior independent director should beappointed and has concluded that, as the Board consists entirelyof non-executive directors, this is unnecessary at present.

Role of the Board A management agreement between the Company and JPMorganFunds Limited (‘JPMF’) (the Manager), sets out the matters overwhich the Manager has authority. This includes management of theCompany’s assets and the provision of accounting, companysecretarial, administration, and some marketing services. All othermatters are reserved for the approval of the Board. A formalschedule of matters reserved to the Board for decision haspreviously been approved. This includes determination andmonitoring of the Company’s investment objectives and policy andits future strategic direction, gearing policy, management of the

capital structure, appointment and removal of third party serviceproviders, review of key investment and financial data and theCompany’s corporate governance and risk control arrangements.The Board conducts a formal evaluation of the Manager every year.

At each Board meeting, Directors’ interests are considered. Theseare reviewed carefully, taking into account the circumstancessurrounding them, and, if considered appropriate, are approved.It was resolved that there were no actual or indirect interests ofa Director which conflicted with the interests of the Company, whicharose during the year.

Following the introduction of The Bribery Act 2010, the Board hasadopted appropriate procedures designed to prevent bribery.It confirms that the procedures have operated effectively during theyear under review.

The Board meets at least quarterly during the year and additionalmeetings are arranged as necessary. Full and timely information isprovided to the Board to enable it to function effectively and toallow Directors to discharge their responsibilities.

There is an agreed procedure for Directors to take independentprofessional advice if necessary and at the Company’s expense. Thisis in addition to the access that every Director has to the advice andservices of the Company Secretary, JPMF, which is responsible tothe Board for ensuring that the Board procedures are followed andthat applicable rules and regulations are complied with.

Board Composition Following Lysander Tennant’s retirement as a Director at theCompany’s AGM in March 2016, an independent non-executivesearch consultancy (Nurole) identified Tamara Sakovska as asuitably qualified replacement and she was appointed as a newDirector of the Company effective from 1st August 2016.

The Board currently consists of five non-executive Directors, all ofwhom are regarded by the Board as independent. The Chairman’sindependence was assessed upon her appointment and annuallythereafter. The Directors have a breadth of investment knowledge,business and financial skills and experience relevant to the Company’sbusiness and brief biographical details of each Director are set out onpages 21 and 22. There have been no changes to the Chairman’s othersignificant commitments during the year under review.

A review of Board composition and balance is included as part of theannual performance evaluation of the Board, details of which maybe found below.

Tenure Directors are initially appointed until the following Annual GeneralMeeting when, under the Company’s Articles of Association, it isrequired that they be elected by shareholders. Thereafter, Directorsstand for annual re-election, following the Board’s adoption ofcorporate governance best practice. Subject to the performance

Russian Securities_pp21_33 19/01/2017 17:40 Page 25

26 JPMORGAN RUSSIAN SECURITIES PLC. ANNUAL REPORT & ACCOUNTS 2016

evaluation carried out each year, the Board will agree whether it isappropriate for the Director to seek an additional term. The Boarddoes not believe that length of service in itself necessarilydisqualifies a Director from seeking re-election but, when makinga recommendation, the Board will take into account therequirements of the UK Corporate Governance Code, including theneed to periodically refresh the Board and its sub-Committees.Notwithstanding the fact that George Nianias will have served asa director for nine years at the date of the 2017 AGM, theNomination Committee agreed that he continued to remainindependent in character and judgement. Accordingly, due to hissignificantly positive contribution to the Company arising from hisbase in Moscow and knowledge of the market, the NominationCommittee agreed that it would be in the Company’s best interestsif George Nianias’ appointment as a director continued.

The Nomination Committee, having considered their qualifications,performance and contribution to the Board and its Committees,confirms that Mrs Nott, Ms Sakovska and Messrs Easton, Jeens andNianias continue to be effective and demonstrate commitment tothe role. The Board recommends to shareholders that all the aboveDirectors be elected/re-elected.

The terms and conditions of Directors’ appointments are set out informal letters of appointment, copies of which are available forinspection on request at the Company’s registered office and atthe AGM.

Meetings and Committees The Board delegates certain responsibilities and functions tocommittees. Details of membership of committees are shown withthe Directors’ profiles on pages 21 and 22.