ryanair holdings plc company report§alves.m_2018.pdf · we are bullish on the stock with a target...

TRANSCRIPT

THIS REPORT WAS PREPARED EXCLUSIVELY FOR ACADEMIC PURPOSES BY MANUEL GONÇALVES, A MASTERS IN FINANCE STUDENT OF

THE NOVA SCHOOL OF BUSINESS AND ECONOMICS. THE REPORT WAS SUPERVISED BY A NOVA SBE FACULTY MEMBER, ACTING IN A

MERE ACADEMIC CAPACITY, WHO REVIEWED THE VALUATION METHODOLOGY AND THE FINANCIAL MODEL. (PLEASE REFER TO THE DISCLOSURES AND DISCLAIMERS AT END OF THE DOCUMENT)

Page 1/28

MASTERS IN FINANCE

▪ Ryanair is our preferred structural play in the European

airline sector. We are bullish on LCCs penetration in Europe to be

50% by the end of the decade.

▪ Recent headwinds related to pilot strikes and flight

cancellations provide an attractive entry point for equity investors.

We disregard brand awareness as long as Ryanair keeps

providing the lowest fares in the market.

▪ Strong economic momentum should boost air travel

demand - strongly related to GDP, according to our findings.

▪ Amid industry consolidation, the company can leverage

market share in countries where its seat overlap with distressed

carriers is high.

▪ By focusing on the digital, the company will boost

ancillary revenues and may bring the case of multiple expansion to

the table.

▪ We are bullish on the stock with a target price of €23.18,

representing a 1-year upside potential of 59%.

Company description

Ryanair Holdings plc is a Low-Cost Carrier (LCC) founded in 1984

by Christopher Ryan, Liam Lonergan and Tony Ryan.

Headquartered in Dublin, Ireland, Ryanair is currently the largest

European airline, carrying over 120 million passengers per year.

RYANAIR HOLDINGS PLC COMPANY REPORT

LOW COST AIRLINES 03 JANUARY 2018

STUDENT: MANUEL GONÇALVES [email protected]

Ryanair still flying high

Getting ahead of labour turbulence

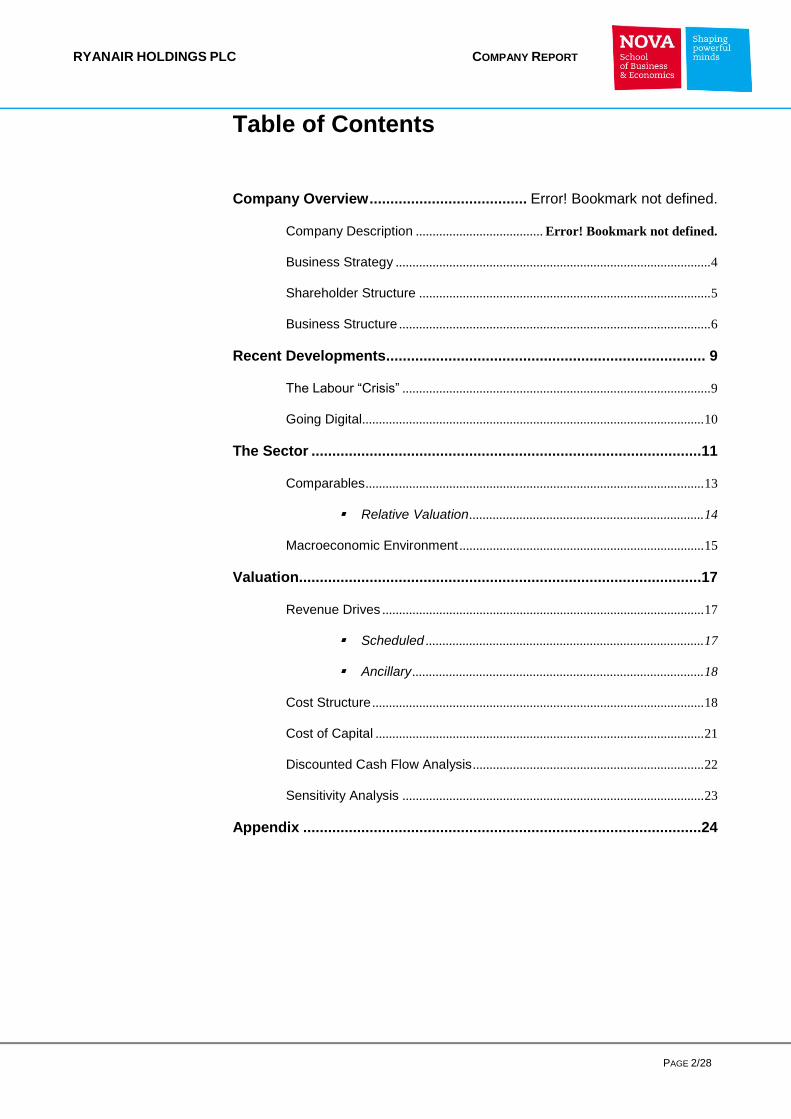

Recommendation: BUY

Price Target FY17: 23.18 €

Price (as of 3-Jan-18) 15.36 €

Reuters: RYA.I, Bloomberg: RYA.ID

52-week range (€) 13.3-19.78

Market Cap (€m) 17,796.14

Outstanding Shares (m) 1,182.86

Other (…)

Source:

Source: Bloomberg

(Values in € millions) 2016 2017E 2018F

Revenues 6647.8 6883.6 7633.1

EBITDA 2030.8 2127.6 2313.4

EBITDA Margin 31% 31% 30%

Net Profit 1315.9 1340.1 1476.9

EPS 1.05 1.07 1.18

P/E 14 15.3 16

ROIC Adj. 28% 24% 26%

Invested Capital Adj. 4290.4 5116.5 5295.1

Profit Pax 12.8 12.2 12.4

Source: Ryanair 2017 Annual Report and Estimates

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 2/28

Table of Contents

Company Overview ...................................... Error! Bookmark not defined.

Company Description ...................................... Error! Bookmark not defined.

Business Strategy .............................................................................................. 4

Shareholder Structure ....................................................................................... 5

Business Structure ............................................................................................. 6

Recent Developments ............................................................................. 9

The Labour “Crisis” ............................................................................................ 9

Going Digital...................................................................................................... 10

The Sector ..............................................................................................11

Comparables ..................................................................................................... 13

▪ Relative Valuation ...................................................................... 14

Macroeconomic Environment ......................................................................... 15

Valuation .................................................................................................17

Revenue Drives ................................................................................................ 17

▪ Scheduled ................................................................................... 17

▪ Ancillary ....................................................................................... 18

Cost Structure ................................................................................................... 18

Cost of Capital .................................................................................................. 21

Discounted Cash Flow Analysis ..................................................................... 22

Sensitivity Analysis .......................................................................................... 23

Appendix ................................................................................................24

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 3/28

Company overview

Ryanair Holdings plc is a Low-Cost Carrier (LCC) founded in 1984 by Christopher

Ryan, Liam Lonergan and Tony Ryan. Headquartered in Dublin, Ireland, Ryanair

is currently the largest European airline, carrying over 120 million passengers per

year.

Company description

The company provides scheduled-airline services in Europe, Morocco and

Israel, which represents 72% of total revenues. It also offers ancillary services,

such as in-flight internet, food & beverage and merchandise. In addition, it sells

bus and rail tickets onboard and through its website, as well as accommodation

services and travel insurance. These two services drive the core-business of the

group.

Ryanair’s first route was launched in July 1985 with daily flights, on a 15-seater

aircraft, linking Waterford in the southeast of Ireland to London Gatwick. Total

staff was 25 and, curiously, first cabin recruits had to be shorter than 1.58m to fit

in the tiny cabin of the aircraft. Ryanair’s disruptive low-cost business model

initiated in 1986 after getting permission from regulatory authorities to challenge

British Airways/Aer Lingus high fare duopoly on the Dublin-London route. An

initial fare of £99, less than half of that of the duopoly, started the first fare war in

Europe: BA/Aer Lingus had to slash their prices in response. With only two routes

in operation, Ryanair carried 82,000 passengers in its first full year in operation.

The beginning of the 1990s would change the company forever and the rest of

the decade would disrupt the entire airlines industry for good. In 1990, Ryanair

had accumulated £20 million in losses after rapid fleet and routes growth and

ferocious price competition with the duopoly. The Ryan family injected new

capital in the company, replaced management and changed the business model

to one very similar to that of Southwest Airlines – the main US low-cost carrier.

Under this strategy, that persists today, Ryanair would offer the lowest fares in

every market, operate a single aircraft type, keep airplanes off the ground by

increasing flight frequency and cease to offer free meals on board.

The year after was the first, and only in the company’s history, in which the

number of employees and passengers decreased. The Gulf War had just broken

out, causing passenger traffic to collapse. Thanks to continuing growth through

the magic formula of low fares and high frequency, Ryanair overtook British

Airways and Aer Lingus in 1995 to become the largest passenger airline on the

biggest international route in Europe: Dublin to London. The scheduled airline

The Gulf War was the second threat to the business...

Ryanair challenged British Airways since the very beginning

Replicating Southwest Airlines

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 4/28

business consummated its disruption in 1996, when the European Union

completed the “Open Skies” deregulation, enabling LCCs to freely compete in

routes and prices with Legacy Carriers.

In 1997, Ryanair goes public for the first time being quoted on the Dublin and

NASDAQ stock exchanges and, in 2000, launches Europe’s largest booking

website. This allowed customers to acquire other services such as low-cost

accommodation and car hire, travel insurance or rail tickets. In just three months,

the company started to register 50,000 online bookings per week.

A second airport base in Continental Europe, after Brussels, was launched in

2002 - in Frankfurt Hahn - bringing an end, after disputes in Germany Courts, to

the high fare monopoly of the Legacy Carrier Lufthansa. Also, the company

announced a long-term partnership with Boeing which would translate into the

acquisition of more than 150 new Boeing 737-800 until 2010.

Passenger growth continued to boom, and Ryanair was named number 1 in

customer service, beating all European airlines for least lost bags, fewer

cancellations and best punctuality. As of today, the company operates a fleet of

over 400 aircrafts used in more than 2,000 daily flights, employs over 13,000

skilled professionals, provides scheduled services to more than 120 million

passengers a year and connects 33 countries. Ryanair has faced some

headwinds recently, related to pilot strikes, who demand a higher pay, and a

decline in customer satisfaction. About 700,000 customers were affected by flight

cancellations.

Business strategy

Ryanair inspired its core strategy on the operational model of the most successful

discounter of all time – the Dallas-based Southwest Airlines. The company has a

strong focus on cost savings and operating efficiencies, and combines it with

aggressive fare promotions and marketing to stimulate demand.

Over the last decade, they have shown great bargaining power over its

stakeholders because of “a self-reinforcing cost advantage” that continuously

fosters lower unit costs. By operating a single aircraft model – Boeing 737-800 –

Ryanair could significantly reduce training costs and achieve speedier repairs,

compared to other airlines. Also, they often ordered aircrafts in bulk from Boeing,

getting huge price discounts. By operating a single class and unassigned seating,

they could accelerate onboarding and through a no-meal policy, the company

could decrease time-consuming clean-up. The strategy, mostly in the beginning,

was also to concentrate on uncongested, secondary airports to enable faster

Going Public

Ryanair Today

Challenging Lufthansa

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 5/28

take-offs and landings. This allowed the negotiation of favourable landing fee

discounts (since most of these airports were desperate for traffic).

This self-perpetuating process continued, as Ryanair recycled the cost savings

into lower passenger fares, getting more traffic and, once again, more bargaining

power over the airports and the aircraft suppliers – Boeing.

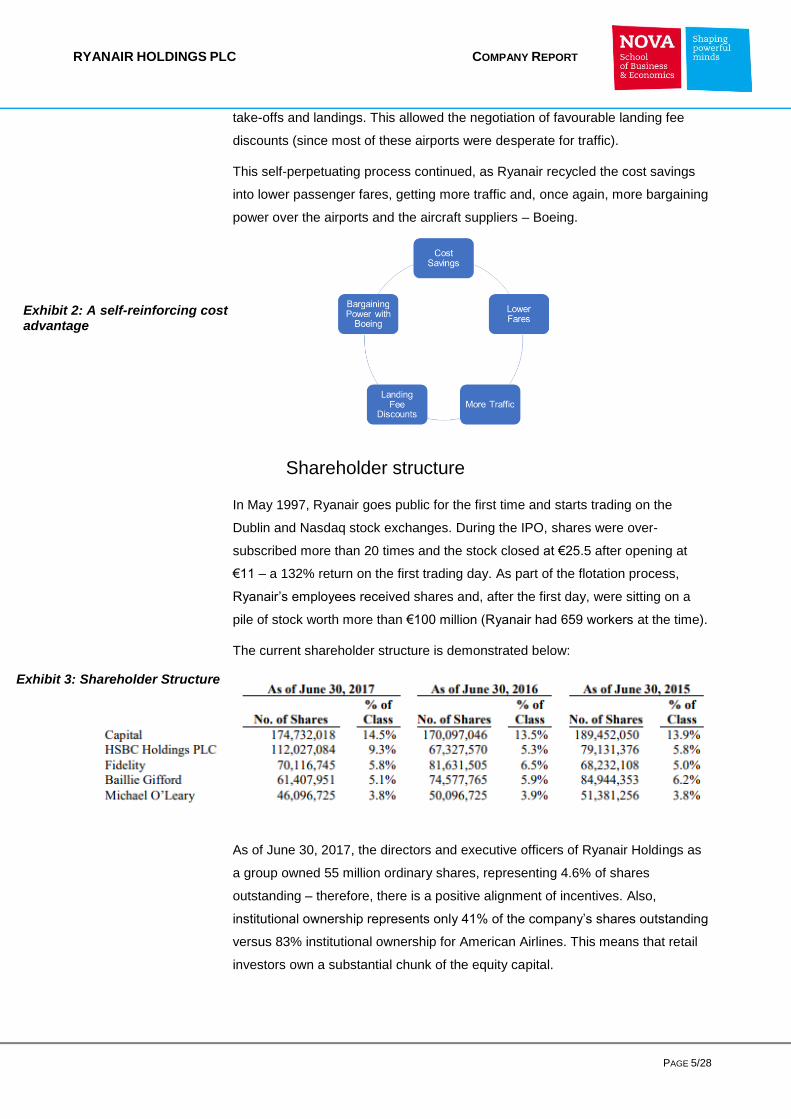

Shareholder structure

In May 1997, Ryanair goes public for the first time and starts trading on the

Dublin and Nasdaq stock exchanges. During the IPO, shares were over-

subscribed more than 20 times and the stock closed at €25.5 after opening at

€11 – a 132% return on the first trading day. As part of the flotation process,

Ryanair’s employees received shares and, after the first day, were sitting on a

pile of stock worth more than €100 million (Ryanair had 659 workers at the time).

The current shareholder structure is demonstrated below:

As of June 30, 2017, the directors and executive officers of Ryanair Holdings as

a group owned 55 million ordinary shares, representing 4.6% of shares

outstanding – therefore, there is a positive alignment of incentives. Also,

institutional ownership represents only 41% of the company’s shares outstanding

versus 83% institutional ownership for American Airlines. This means that retail

investors own a substantial chunk of the equity capital.

Exhibit 2: A self-reinforcing cost advantage

Exhibit 3: Shareholder Structure

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 6/28

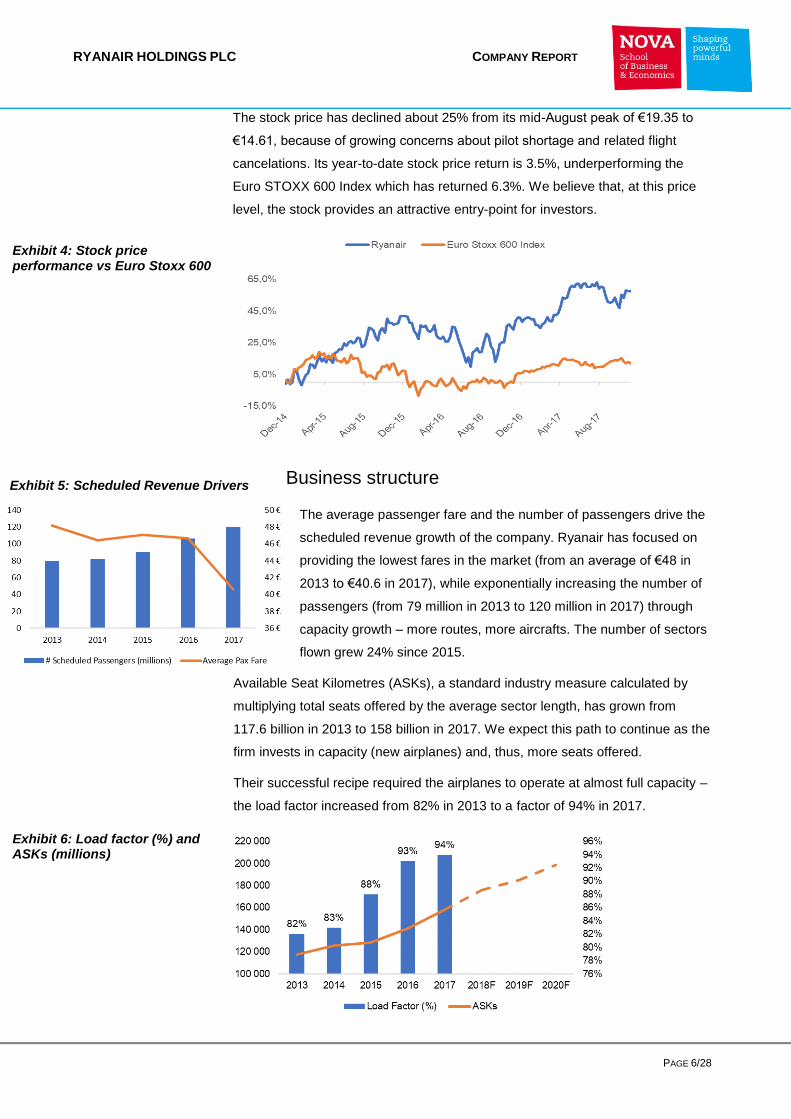

The stock price has declined about 25% from its mid-August peak of €19.35 to

€14.61, because of growing concerns about pilot shortage and related flight

cancelations. Its year-to-date stock price return is 3.5%, underperforming the

Euro STOXX 600 Index which has returned 6.3%. We believe that, at this price

level, the stock provides an attractive entry-point for investors.

Business structure

The average passenger fare and the number of passengers drive the

scheduled revenue growth of the company. Ryanair has focused on

providing the lowest fares in the market (from an average of €48 in

2013 to €40.6 in 2017), while exponentially increasing the number of

passengers (from 79 million in 2013 to 120 million in 2017) through

capacity growth – more routes, more aircrafts. The number of sectors

flown grew 24% since 2015.

Available Seat Kilometres (ASKs), a standard industry measure calculated by

multiplying total seats offered by the average sector length, has grown from

117.6 billion in 2013 to 158 billion in 2017. We expect this path to continue as the

firm invests in capacity (new airplanes) and, thus, more seats offered.

Their successful recipe required the airplanes to operate at almost full capacity –

the load factor increased from 82% in 2013 to a factor of 94% in 2017.

Exhibit 4: Stock price performance vs Euro Stoxx 600

Exhibit 5: Scheduled Revenue Drivers

Exhibit 6: Load factor (%) and ASKs (millions)

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 7/28

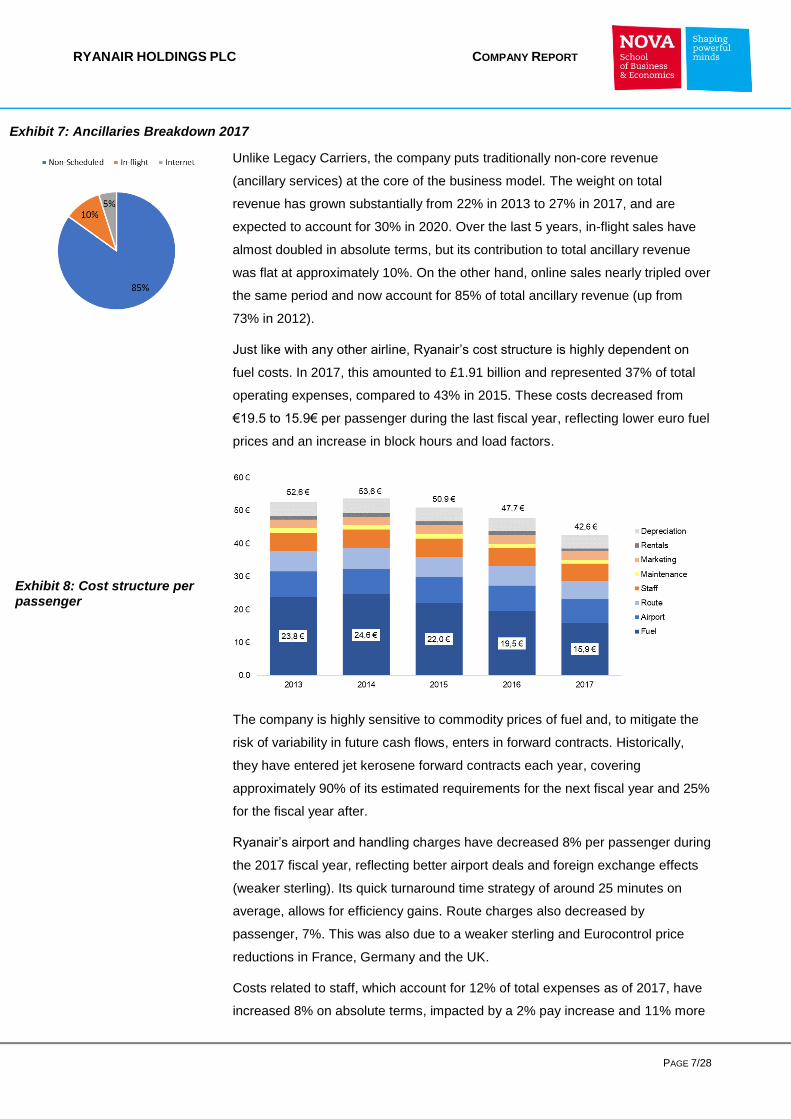

Exhibit 7: Ancillaries Breakdown 2017

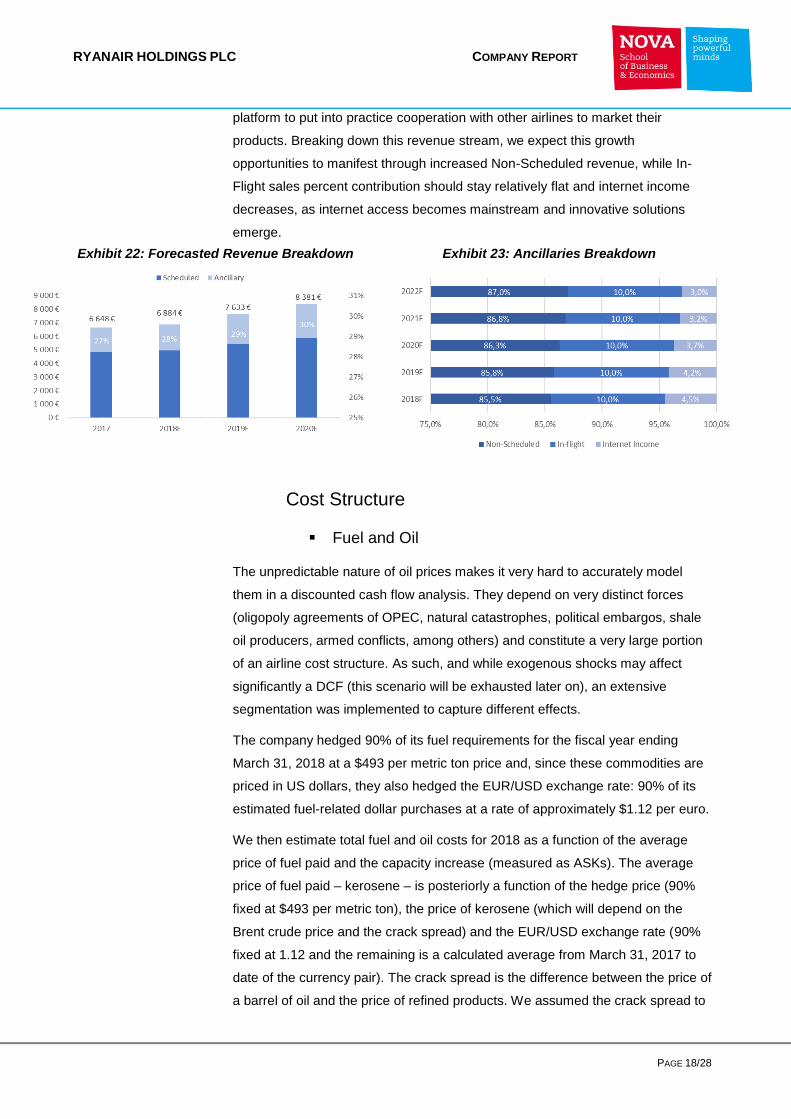

Unlike Legacy Carriers, the company puts traditionally non-core revenue

(ancillary services) at the core of the business model. The weight on total

revenue has grown substantially from 22% in 2013 to 27% in 2017, and are

expected to account for 30% in 2020. Over the last 5 years, in-flight sales have

almost doubled in absolute terms, but its contribution to total ancillary revenue

was flat at approximately 10%. On the other hand, online sales nearly tripled over

the same period and now account for 85% of total ancillary revenue (up from

73% in 2012).

Just like with any other airline, Ryanair’s cost structure is highly dependent on

fuel costs. In 2017, this amounted to £1.91 billion and represented 37% of total

operating expenses, compared to 43% in 2015. These costs decreased from

€19.5 to 15.9€ per passenger during the last fiscal year, reflecting lower euro fuel

prices and an increase in block hours and load factors.

The company is highly sensitive to commodity prices of fuel and, to mitigate the

risk of variability in future cash flows, enters in forward contracts. Historically,

they have entered jet kerosene forward contracts each year, covering

approximately 90% of its estimated requirements for the next fiscal year and 25%

for the fiscal year after.

Ryanair’s airport and handling charges have decreased 8% per passenger during

the 2017 fiscal year, reflecting better airport deals and foreign exchange effects

(weaker sterling). Its quick turnaround time strategy of around 25 minutes on

average, allows for efficiency gains. Route charges also decreased by

passenger, 7%. This was also due to a weaker sterling and Eurocontrol price

reductions in France, Germany and the UK.

Costs related to staff, which account for 12% of total expenses as of 2017, have

increased 8% on absolute terms, impacted by a 2% pay increase and 11% more

Exhibit 8: Cost structure per passenger

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 8/28

sectors flown. However, these costs decreased 4% on a passenger basis. Being

a critical issue for the company at the moment, it will be individually scrutinized in

a Recent Developments section.

The company has grown its EBITDA from €1,421 million in 2015 to

€2,032 million in 2017. EBITDA margin also increased from 25% to

31% in the same period, signalling stronger operating efficiency.

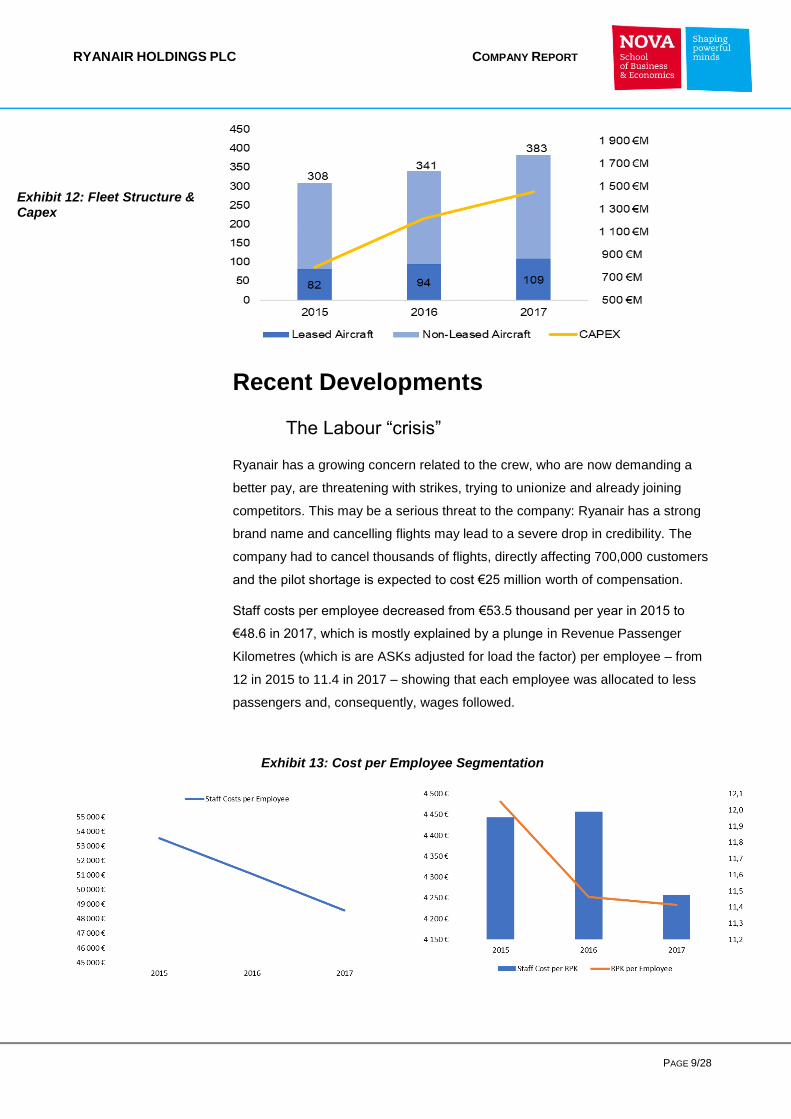

The operating asset structure of the company is composed almost entirely by the

fleet of aircraft. As of March 31, 2017, they operate 383 Boeing 737-800 – up

from 308 in 2015. The acquisitions were funded through borrowings under

facilities provided by international financial institutions on the basis of guarantees

issued by the Export-Import Bank of the United States (174 aircrafts), Japanese

Operating Leases with Call Options (22 aircrafts), commercial debt (6 aircrafts),

operating lease arrangements (33 aircrafts), Ryanair’s own resources (104

aircrafts) and the remaining 44 aircrafts have no remaining debt outstanding.

The Return on Invested Capital (adjusted through an estimation of capitalized

operating leases added to invested capital) grew from 24% in 2015 to 27.5% in

2017, capturing the effects of NOPLAT growth - from €911.5 million in 2015 to

€1,379 million in 2017 – and invested capital growth (from €3,796 million in 2015

to €4,979 million in 2017). New invested capital was mainly the acquisition of

fixed assets, offset by increases in “Unearned Revenue” – cash inflows from

tickets paid upfront.

Ryanair’s net cash outflows for capital expenditures have increased from €789

million in 2015 to €1.45 billion in 2017. The company has been able to generate

sufficient funds from operations to fund non-aircraft acquisition-related working

capital requirements.

Exhibit 9: EBITDA Growth

Exhibit 10: Funding Mix

Exhibit 11: Value Creation Segmentation

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 9/28

Recent Developments

The Labour “crisis”

Ryanair has a growing concern related to the crew, who are now demanding a

better pay, are threatening with strikes, trying to unionize and already joining

competitors. This may be a serious threat to the company: Ryanair has a strong

brand name and cancelling flights may lead to a severe drop in credibility. The

company had to cancel thousands of flights, directly affecting 700,000 customers

and the pilot shortage is expected to cost €25 million worth of compensation.

Staff costs per employee decreased from €53.5 thousand per year in 2015 to

€48.6 in 2017, which is mostly explained by a plunge in Revenue Passenger

Kilometres (which is are ASKs adjusted for load the factor) per employee – from

12 in 2015 to 11.4 in 2017 – showing that each employee was allocated to less

passengers and, consequently, wages followed.

Exhibit 12: Fleet Structure & Capex

Exhibit 13: Cost per Employee Segmentation

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 10/28

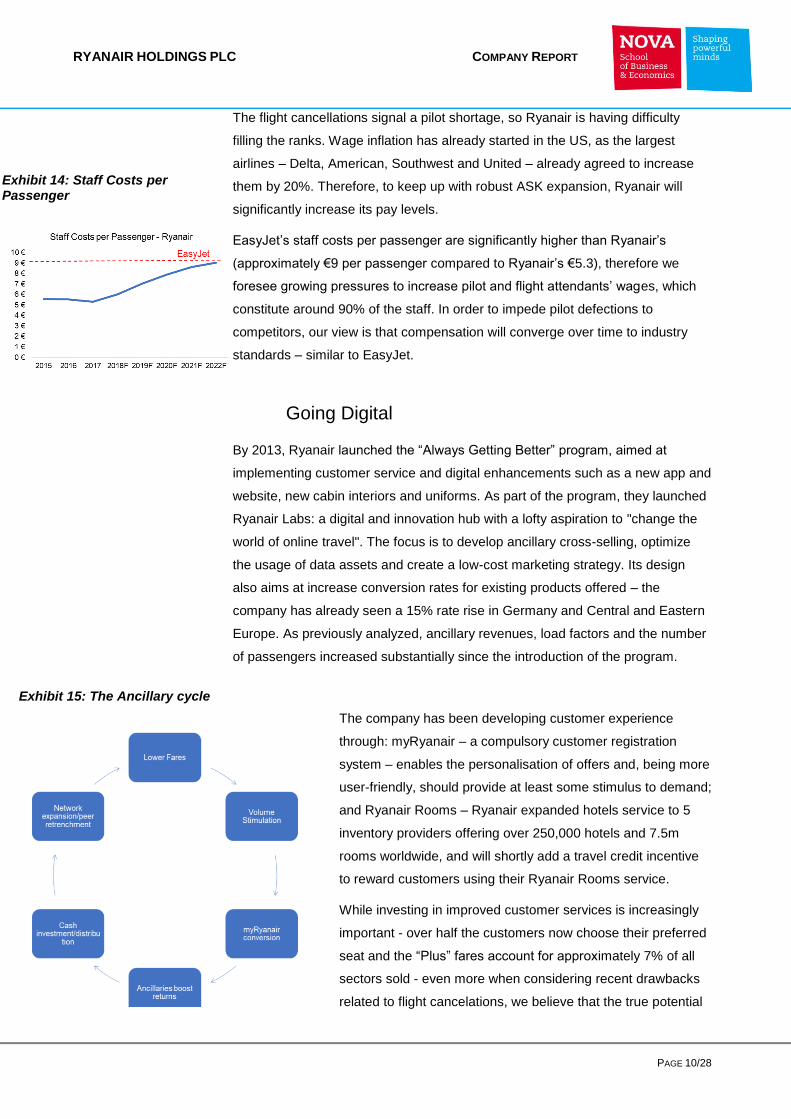

The flight cancellations signal a pilot shortage, so Ryanair is having difficulty

filling the ranks. Wage inflation has already started in the US, as the largest

airlines – Delta, American, Southwest and United – already agreed to increase

them by 20%. Therefore, to keep up with robust ASK expansion, Ryanair will

significantly increase its pay levels.

EasyJet’s staff costs per passenger are significantly higher than Ryanair’s

(approximately €9 per passenger compared to Ryanair’s €5.3), therefore we

foresee growing pressures to increase pilot and flight attendants’ wages, which

constitute around 90% of the staff. In order to impede pilot defections to

competitors, our view is that compensation will converge over time to industry

standards – similar to EasyJet.

Going Digital

By 2013, Ryanair launched the “Always Getting Better” program, aimed at

implementing customer service and digital enhancements such as a new app and

website, new cabin interiors and uniforms. As part of the program, they launched

Ryanair Labs: a digital and innovation hub with a lofty aspiration to "change the

world of online travel". The focus is to develop ancillary cross-selling, optimize

the usage of data assets and create a low-cost marketing strategy. Its design

also aims at increase conversion rates for existing products offered – the

company has already seen a 15% rate rise in Germany and Central and Eastern

Europe. As previously analyzed, ancillary revenues, load factors and the number

of passengers increased substantially since the introduction of the program.

The company has been developing customer experience

through: myRyanair – a compulsory customer registration

system – enables the personalisation of offers and, being more

user-friendly, should provide at least some stimulus to demand;

and Ryanair Rooms – Ryanair expanded hotels service to 5

inventory providers offering over 250,000 hotels and 7.5m

rooms worldwide, and will shortly add a travel credit incentive

to reward customers using their Ryanair Rooms service.

While investing in improved customer services is increasingly

important - over half the customers now choose their preferred

seat and the “Plus” fares account for approximately 7% of all

sectors sold - even more when considering recent drawbacks

related to flight cancelations, we believe that the true potential

Exhibit 14: Staff Costs per Passenger

Exhibit 15: The Ancillary cycle

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 11/28

for the value of the company resides on digital partnerships with other airlines.

At the end of 2016, Ryanair travel platform enjoyed well over half a billion visits

per annum, being the world’s largest airline website with 94% of customers

visiting directly rather than via search engines. Consequently, the company has

been setting a platform to comprise a range of services that will, in our view,

transform the way the aviation sector markets their products.

They started to sell Air Europa flights to South America out of Madrid, have

reached a commercial agreement to market Aer Lingus transatlantic flights

through the platform and a similar deal is in the work with Norwegian Airlines at

Gatwick. Essentially, it is cheaper for other airlines to market their products on

Ryanair.com than using Google or other sources of marketing, given the

website’s number of travel-related visits. And therein lies a major benefit to

Ryanair: if it can capture a growing percentage of not just its own booking on its

digital platform but also of all flights but other airlines in Europe, it will create a

selling and data gathering opportunity.

The Sector

Few industries have exhibited such drastic transformations as the airlines

industry. It has evolved from a system of long-established state-owned carriers to

a dynamic free competitive market in recent years. Unlike other industries,

motivations were rather legal and political than technological. Since 1997, EU air

carriers have been able to provide domestic routes in any EU member state

without restrictions. Before the deregulation, only a few carriers operated

European routes and fares were established by bilateral agreements between

states. The deregulation process and the subsequent privatization, have changed

the structure of the market and gave rise to new business models. Three different

businesses have emerged: Legacy Carriers, Low-cost Carriers and Charter

Carriers.

The industry is cyclical and largely tied to the macroeconomic landscape,

naturally flowing with supply and demand dynamics. It entails different

complexities such as a high fixed cost structure, low barriers to entry but high

barriers to exit due to capital intensity, commodity price movements, the

duopolistic market structure of suppliers and strong unions.

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 12/28

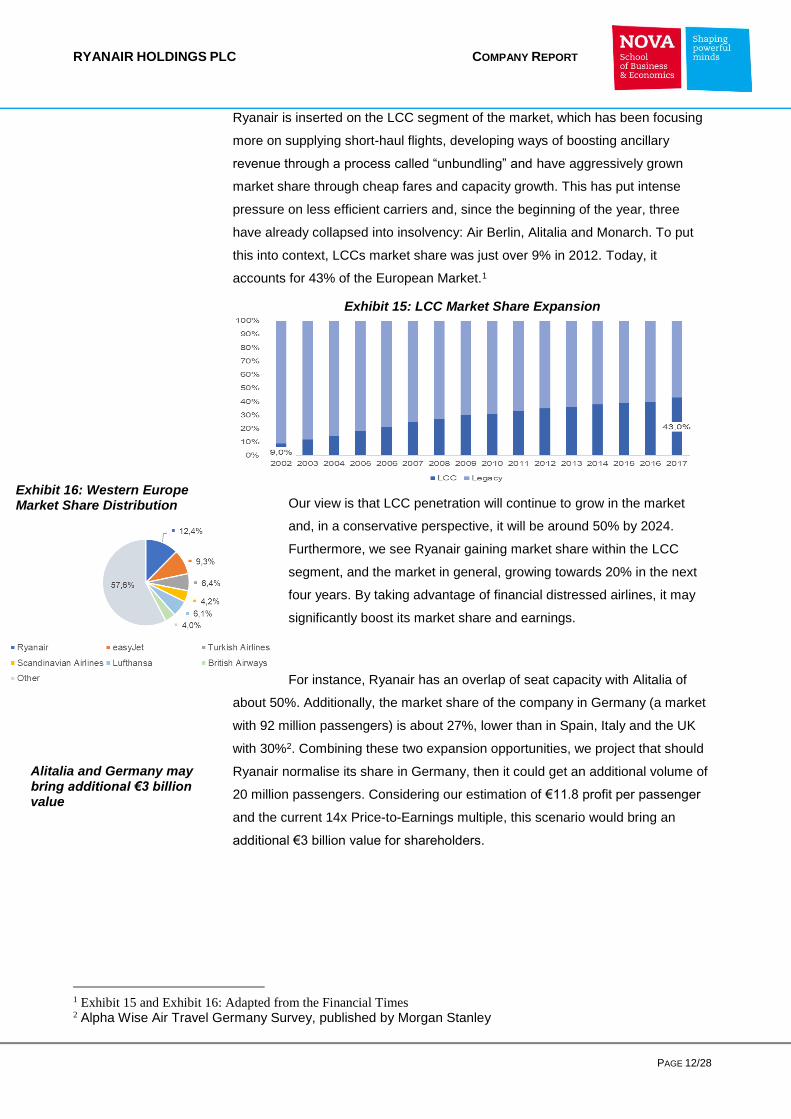

Ryanair is inserted on the LCC segment of the market, which has been focusing

more on supplying short-haul flights, developing ways of boosting ancillary

revenue through a process called “unbundling” and have aggressively grown

market share through cheap fares and capacity growth. This has put intense

pressure on less efficient carriers and, since the beginning of the year, three

have already collapsed into insolvency: Air Berlin, Alitalia and Monarch. To put

this into context, LCCs market share was just over 9% in 2012. Today, it

accounts for 43% of the European Market.1

Our view is that LCC penetration will continue to grow in the market

and, in a conservative perspective, it will be around 50% by 2024.

Furthermore, we see Ryanair gaining market share within the LCC

segment, and the market in general, growing towards 20% in the next

four years. By taking advantage of financial distressed airlines, it may

significantly boost its market share and earnings.

For instance, Ryanair has an overlap of seat capacity with Alitalia of

about 50%. Additionally, the market share of the company in Germany (a market

with 92 million passengers) is about 27%, lower than in Spain, Italy and the UK

with 30%2. Combining these two expansion opportunities, we project that should

Ryanair normalise its share in Germany, then it could get an additional volume of

20 million passengers. Considering our estimation of €11.8 profit per passenger

and the current 14x Price-to-Earnings multiple, this scenario would bring an

additional €3 billion value for shareholders.

1 Exhibit 15 and Exhibit 16: Adapted from the Financial Times 2 Alpha Wise Air Travel Germany Survey, published by Morgan Stanley

Alitalia and Germany may bring additional €3 billion value

Exhibit 15: LCC Market Share Expansion

Exhibit 16: Western Europe Market Share Distribution

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 13/28

Comparables

The European airline sector is very fragmented. Comparing to the US, where the

6 largest airline companies make up 90% of the market, in Europe the top 6

companies account for 43% market share3. According to OAG, an aviation

intelligence company based in the UK, there are 217 airlines operating in Europe.

EasyJet is, by all means, the top direct competitor of

Ryanair. With over 80 million passengers last year and

an average fare of 77€, it is the market leader in several

countries, with the UK among them. They are also held

responsible for the strong LCC penetration with

capacity growth rates ahead of the market’s (7.8% vs

6.9% in the UK, 10.7% vs 4% in France and 7% vs 4%

in Italy and Germany). Their expectation is to invest

over £3 billion in gross CAPEX in the next three years.

Other relevant European LCCs are Wizz Air, Norwegian Airlines, Air Berlin,

Transavia, among others. We highlight Wizz Air, a Hungarian company, as the

most similar (as possible) to Ryanair in terms of cost efficiency. However, it has

currently about 20% of Ryanair’s size with 25 million passengers per year.

As illustrated in the graph above4, no direct competitor can rival, in terms of cost

per passenger, with Ryanair. If we were to consider Legacy Carriers as well, the

gap would widen even more. All these competitors are operating at a cost

structure per passenger above Ryanair’s average fare per passenger of €40.6

(Wizz at €44, easyJet at €51, Norwegian at €73 and Air Berlin at €131). Also, a

study by Credit Suisse Research, found that 40% of European unit costs per seat

are more than 3 times Ryanair’s average fare and 76% more than 2 times

3 Source: “European airlines face more cuts and consolidation”, Financial Times 4 Source: Ryanair Investor Presentation

Exhibit 17: Competitors’ Scheduled Revenue Drivers

Exhibit 18: LCC’s Cost Structure Comparison

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 14/28

Ryanair’s average fare. This, together with recent bankruptcies, represent

opportunities for the company to enter carriers where players, uncapable of

sustaining prices below breakeven, can’t afford to compete.

We expect the company to maintain its ultra-low fare strategy in the medium-term

to continue growing market share, which should translate into higher margins

afterwards.

▪ Relative Valuation

As previously stated, the airlines sector is cyclical and, as such, the stock returns

fluctuate with business cycles. Therefore, we often see trading multiples moving

within ranges.

Two traditional valuation metrics for airlines are the Price-to-Earnings (P/E) and

the EV/EBITDAR multiples. The first is an equity metric that compares the current

market value of equity to the reported Earnings Per Share (EPS). According to

our estimates, Legacy Carriers stock prices have historically traded at the 4-18x

earnings range, while LCC’s at the 7-22x range. Their historical averages are

8.4x and 13.9x respectively, higher than current averages of 7.7x and 13.5x.

This metric is highly influenced by operational leverage, as EPS are easily

manageable by the companies, namely through operating leases. Therefore, we

have to adjust for capital structure issues and normalize for the decision of buy or

lease a plane by adding in capitalized lease payments. The EV/EBITDAR

multiple, for instance, captures this effect.

We estimate that Legacy Carriers have traded in the 3-8x EV/EBITDAR range,

while LCCs in the 4-9x range, historically. Legacy carriers are currently trading at

3.53x, below its historical average of 4.8x, while LCCs are trading at 6.57x,

above the 5.7x historical average.

Inserted in the LCC segment, Ryanair has currently a P/E ratio of 14x and a

EV/EBITDAR of 8.81, both above the industry averages. The premium paid by

investors is explained by its competitive positioning: the company is the most

price competitive and most cost efficient LCC, has a strong balance sheet and is

becoming a digital business.

We added two more metrics to get the full picture of the relative valuation of the

stock – the Price to Book Value of Equity and the EV/EBITDA multiple. The

analysis applies the median industry multiples to Ryanair’s financials to get the

price of the stock should the company be priced at exactly the industry median.

Investors are paying an ownership premium…

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 15/28

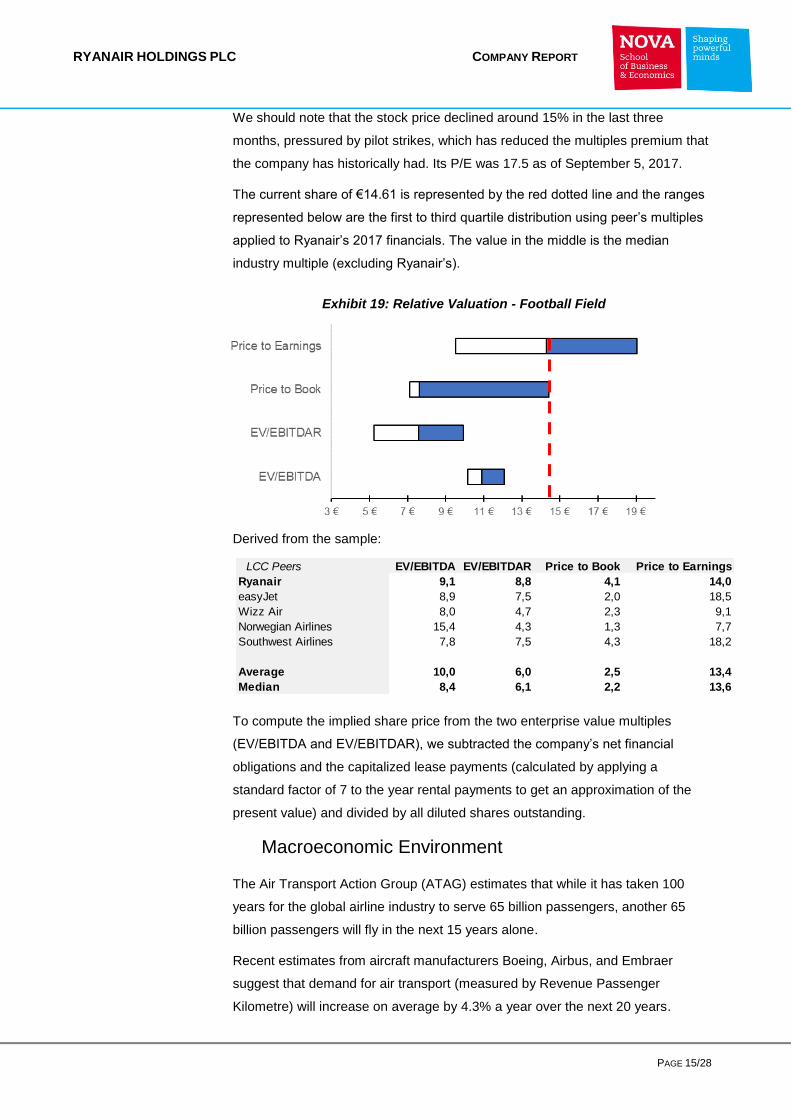

LCC Peers EV/EBITDA EV/EBITDAR Price to Book Price to Earnings

Ryanair 9,1 8,8 4,1 14,0

easyJet 8,9 7,5 2,0 18,5

Wizz Air 8,0 4,7 2,3 9,1

Norwegian Airlines 15,4 4,3 1,3 7,7

Southwest Airlines 7,8 7,5 4,3 18,2

Average 10,0 6,0 2,5 13,4

Median 8,4 6,1 2,2 13,6

We should note that the stock price declined around 15% in the last three

months, pressured by pilot strikes, which has reduced the multiples premium that

the company has historically had. Its P/E was 17.5 as of September 5, 2017.

The current share of €14.61 is represented by the red dotted line and the ranges

represented below are the first to third quartile distribution using peer’s multiples

applied to Ryanair’s 2017 financials. The value in the middle is the median

industry multiple (excluding Ryanair’s).

Derived from the sample:

To compute the implied share price from the two enterprise value multiples

(EV/EBITDA and EV/EBITDAR), we subtracted the company’s net financial

obligations and the capitalized lease payments (calculated by applying a

standard factor of 7 to the year rental payments to get an approximation of the

present value) and divided by all diluted shares outstanding.

Macroeconomic Environment

The Air Transport Action Group (ATAG) estimates that while it has taken 100

years for the global airline industry to serve 65 billion passengers, another 65

billion passengers will fly in the next 15 years alone.

Recent estimates from aircraft manufacturers Boeing, Airbus, and Embraer

suggest that demand for air transport (measured by Revenue Passenger

Kilometre) will increase on average by 4.3% a year over the next 20 years.

Exhibit 19: Relative Valuation - Football Field

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 16/28

The International Air Transport Association (IATA) expects 1% of world GDP to

be spent on air transport in 2018, totalling $861 billion and representing a 9.4%

change from 2017. Passenger departures are also expected to grow by 5.6%, to

4.31 billion a year. They forecast an encouraging near-term economic outlook:

strengthening GDPs and increased passenger and demand should be substantial

enough to offset expected rises in oil prices (they expect an average 2018 price

of $60/b for the Brent crude oil), culminating in the highest global aviation profits

in history – over $35 billion in 2018.

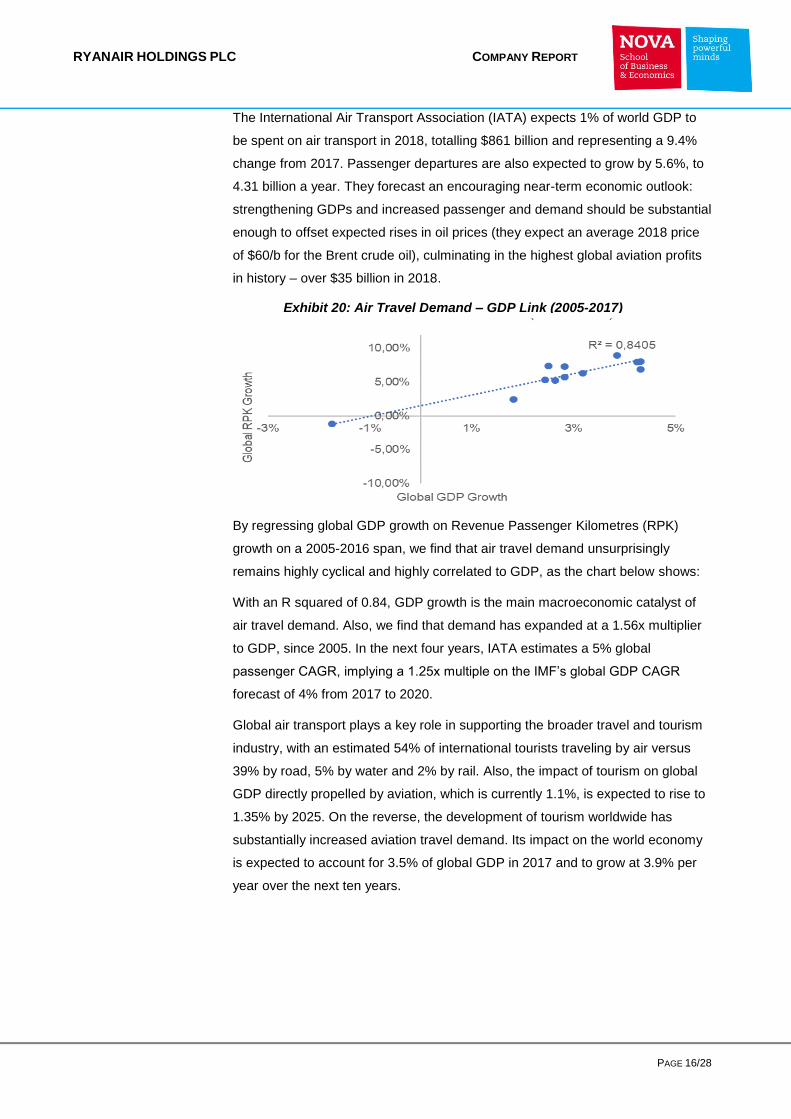

By regressing global GDP growth on Revenue Passenger Kilometres (RPK)

growth on a 2005-2016 span, we find that air travel demand unsurprisingly

remains highly cyclical and highly correlated to GDP, as the chart below shows:

With an R squared of 0.84, GDP growth is the main macroeconomic catalyst of

air travel demand. Also, we find that demand has expanded at a 1.56x multiplier

to GDP, since 2005. In the next four years, IATA estimates a 5% global

passenger CAGR, implying a 1.25x multiple on the IMF’s global GDP CAGR

forecast of 4% from 2017 to 2020.

Global air transport plays a key role in supporting the broader travel and tourism

industry, with an estimated 54% of international tourists traveling by air versus

39% by road, 5% by water and 2% by rail. Also, the impact of tourism on global

GDP directly propelled by aviation, which is currently 1.1%, is expected to rise to

1.35% by 2025. On the reverse, the development of tourism worldwide has

substantially increased aviation travel demand. Its impact on the world economy

is expected to account for 3.5% of global GDP in 2017 and to grow at 3.9% per

year over the next ten years.

Exhibit 20: Air Travel Demand – GDP Link (2005-2017)

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 17/28

Valuation

Revenue drivers

▪ Scheduled

Scheduled revenues are a function of the number of passengers per year and the

average fare charged by the company. We assumed Ryanair will arrive at the

200 million passenger mark by the end of 2024, which yields a CAGR of 7.6%

from 2017 onwards. After allowing for flight cancelations in late 2017, we foresee

the number of passengers to total 129 million by the end of the fiscal year –

March 31, 2018 -, representing a 7.2% increase from the year before.

We expect airfares to come out pressured in 2018, as a result of LCC’s strong

capacity growth. Travel demand has been propelled by lower fares lately amid

lower fuel prices and solid economic conditions, however LCC capacity

expansion seems to be even faster, thus driving fares down. According to our

estimates, ASK’s will grow 11.4% in 2018 units while passenger growth will be

7.2%. As a result, fares are projected to decrease 5% next year, to an average of

€38.5, in line with Ryanair’s guidance of a decrease between 4% and 6%.

Therefore, scheduled revenues will increase 3.5% in 2018 to €4.96 billion.

▪ Ancillary

Our view is that ancillaries will be a growing portion of Ryanair’s revenue stream,

and of LCC’s in general, in the near future. We estimate ancillary expenditure per

passenger to grow 1% in 2018, to €15, and that, by 2020, this stream will

contribute with 30% of total sales. This is a direct effect of the company’s shift to

digital, as it reaps the benefits of the fourth year of the “Always Getting Better”

program. Furthermore, we see more possible value creation as it develops a

Exhibit 21: Forecasted Growth in Tourism facilitated by Aviation

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 18/28

platform to put into practice cooperation with other airlines to market their

products. Breaking down this revenue stream, we expect this growth

opportunities to manifest through increased Non-Scheduled revenue, while In-

Flight sales percent contribution should stay relatively flat and internet income

decreases, as internet access becomes mainstream and innovative solutions

emerge.

Cost Structure

▪ Fuel and Oil

The unpredictable nature of oil prices makes it very hard to accurately model

them in a discounted cash flow analysis. They depend on very distinct forces

(oligopoly agreements of OPEC, natural catastrophes, political embargos, shale

oil producers, armed conflicts, among others) and constitute a very large portion

of an airline cost structure. As such, and while exogenous shocks may affect

significantly a DCF (this scenario will be exhausted later on), an extensive

segmentation was implemented to capture different effects.

The company hedged 90% of its fuel requirements for the fiscal year ending

March 31, 2018 at a $493 per metric ton price and, since these commodities are

priced in US dollars, they also hedged the EUR/USD exchange rate: 90% of its

estimated fuel-related dollar purchases at a rate of approximately $1.12 per euro.

We then estimate total fuel and oil costs for 2018 as a function of the average

price of fuel paid and the capacity increase (measured as ASKs). The average

price of fuel paid – kerosene – is posteriorly a function of the hedge price (90%

fixed at $493 per metric ton), the price of kerosene (which will depend on the

Brent crude price and the crack spread) and the EUR/USD exchange rate (90%

fixed at 1.12 and the remaining is a calculated average from March 31, 2017 to

date of the currency pair). The crack spread is the difference between the price of

a barrel of oil and the price of refined products. We assumed the crack spread to

Exhibit 22: Forecasted Revenue Breakdown Exhibit 23: Ancillaries Breakdown

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 19/28

be equal to the average crack spread of the last 7 years, since it is very hard to

predict its future movements, given its volatility and very few future quotes

outstanding. Also, kerosene is measured in metric tons, while Brent crude is

measured in barrels, so we assumed a factor of 7.9 barrels per metric ton, in line

with the average density of kerosene of 0.81g/cm3.

We forecast a 5.2% decrease in total fuel costs to $1.81 billion in 2018, as a

consequence of a 15% decrease in the average price of fuel paid to €444 (the

hedge price offset the increase in Brent crude prices) and an 11.4% ASK

expansion. On a per passenger basis, these costs reduced from €15.9 in 2017 to

€14.1.

We expect this situation to reverse in March 2019, since the company only

hedged 25% at a price of €484 and the Brent crude futures curve suggests a

$63.3 price, which translates into a €615 price of kerosene. However, this

increase in the price of oil will be offset by an increase in the EUR/USD to 1.24,

as suggested by the futures curve, translating into an average price of fuel paid

of €504.

▪ Airport and Route charges

We forecast airport and route charges to decrease 5% on a per passenger basis

in 2018 to €881 million and €668 million, respectively. Our projection is that the

company will continue to benefit from competitive agreements and landing fees

with airports, using its traffic growth to gain bargaining power, and the trend of

declining Eurocontrol prices in Europe.

▪ Maintenance, Marketing & Other

Marketing and distribution costs are expected to stay relatively constant in the

next two years at €2.7 per passenger. We included a one-off €25 million

provision, as the company addressed the needs of affected passengers to

recover the rostering failure.

Maintenance and repairs costs will stay flat over the years at €390,000 per

aircraft per year. These will be €169 million in 2018, up from €141 million in 2017,

translating into an 11.6% increase per passenger to 1.31€. This reflects a higher

fleet growth and passenger growth.

▪ Aircraft Rentals

Aircraft rentals refer to operating leases: fixed rental payments for aircrafts that

Ryanair operates, but does not own. The arrangement is usually a lessor that

purchases the aircraft and leases it to the company under a 7-year sale-and-

leaseback.

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 20/28

Fiscal year ends in March 2017 2018F 2019F 2020F 2021F 2022F 2023F 2024F

Opening Fleet 341 383 427 448 481 516 540 575

Deliveries under 2013 Boeing Contract 52 50 29

Deliveries under 2014 Boeing Contract 39 19 21 20 11

Option Aircraft under 2014 Boeing Contract 8 25 28 25 14

Planned returns or disposals -10 -6 -8 -14 -9 -25 -10 -15

Total Fleet 383 427 448 481 516 540 575 585

For the last two years, Ryanair paid around $2.6 million a year, for each

operating leased aircraft under aircraft rentals. It is hard to estimate accurately

the level of operating leases in the future, since the decision is based on very-

short term needs – usually in high seasons during the summer and winter.

With a new accounting standard ‘IFRS 16 Leases’ being launched in January

2019, we believe the level of leases on the airline industry will likely decrease.

This new standard requires companies to report all kinds of leases on the

balance sheet, thus reducing its capacity to have artificially low operating profits

and artificially high return on capital. Therefore, estimate the level of total leased

aircraft to decrease as a percentage of total fleet – from 28% in 2017 to 18% in

2022. Also, we expect operating leases to remain at the same 30% level of total

leased aircraft going forward. Therefore, total aircraft rentals will decrease from

€86 million in 2017 to €76 million in 2020.

▪ Depreciation

Ryanair’s Property, Plant & Equipment (PP&E) is composed by aircrafts, hangar

and buildings, plant & equipment, fixture & fittings and motor vehicles. As of

2017, aircrafts constituted more than 98% of gross PP&E. However, they all

contribute to total depreciation and have different rates of depreciation. Aircrafts

have a useful life of 23 years, hangar and buildings depreciate at 5% per year,

plant & equipment between 20% and 33.3%, fixture & fittings at 20%, while motor

vehicles depreciate at 33%. Total depreciation was 4.87% of gross PP&E in 2017

and we expect this percentage to remain constant overtime with yearly

depreciation growing at the same rate as fixed assets.

▪ Capex e NWC

According to Ryanair’s planned aircraft deliveries under the 2013 and 2014

Boeing contracts, including options to further deliveries under the 2014 contract

and planned disposals, we estimate the fleet to total 585 airplanes by 2024, up

from 385 in 2017. Our forecasted capital expenditure to acquire the aircrafts is

based on our estimated investment in PP&E per additional aircraft of €27,5

million.

We expect capital expenditure to total €1,397.6 billion in 2018, compared to

€1,449.8 in 2017, explained by expected 50 additional aircrafts and 6 disposals.

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 21/28

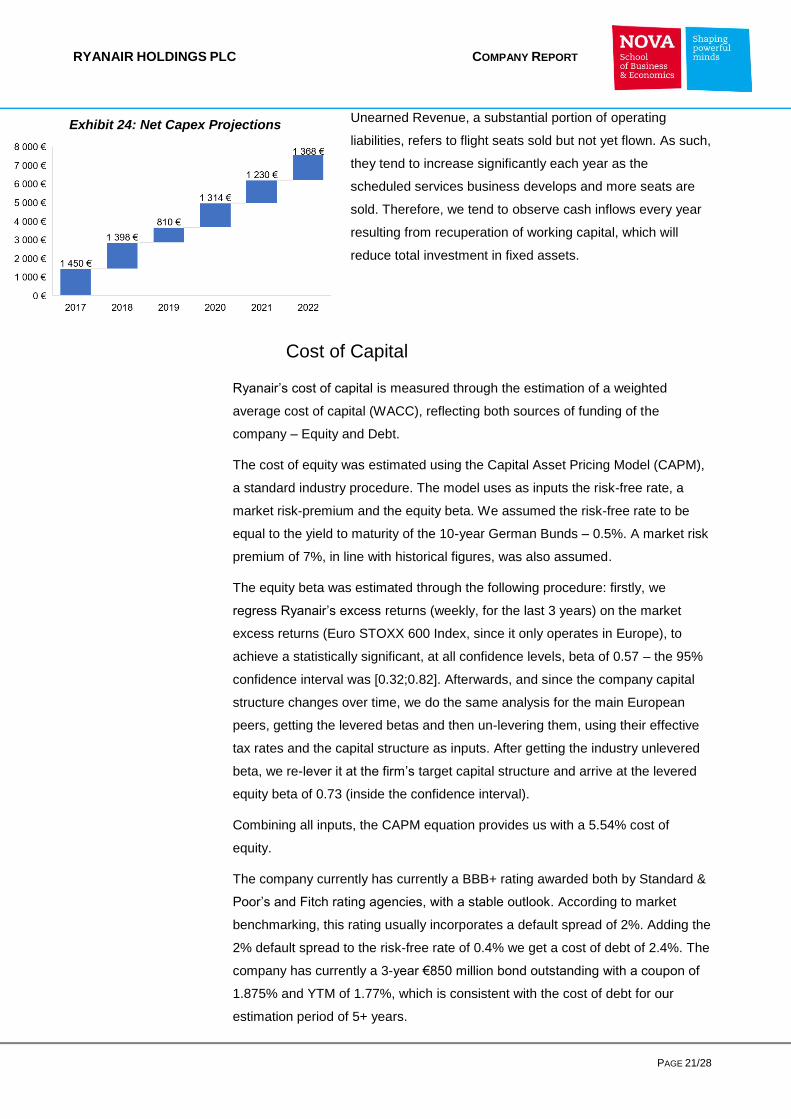

Unearned Revenue, a substantial portion of operating

liabilities, refers to flight seats sold but not yet flown. As such,

they tend to increase significantly each year as the

scheduled services business develops and more seats are

sold. Therefore, we tend to observe cash inflows every year

resulting from recuperation of working capital, which will

reduce total investment in fixed assets.

Cost of Capital

Ryanair’s cost of capital is measured through the estimation of a weighted

average cost of capital (WACC), reflecting both sources of funding of the

company – Equity and Debt.

The cost of equity was estimated using the Capital Asset Pricing Model (CAPM),

a standard industry procedure. The model uses as inputs the risk-free rate, a

market risk-premium and the equity beta. We assumed the risk-free rate to be

equal to the yield to maturity of the 10-year German Bunds – 0.5%. A market risk

premium of 7%, in line with historical figures, was also assumed.

The equity beta was estimated through the following procedure: firstly, we

regress Ryanair’s excess returns (weekly, for the last 3 years) on the market

excess returns (Euro STOXX 600 Index, since it only operates in Europe), to

achieve a statistically significant, at all confidence levels, beta of 0.57 – the 95%

confidence interval was [0.32;0.82]. Afterwards, and since the company capital

structure changes over time, we do the same analysis for the main European

peers, getting the levered betas and then un-levering them, using their effective

tax rates and the capital structure as inputs. After getting the industry unlevered

beta, we re-lever it at the firm’s target capital structure and arrive at the levered

equity beta of 0.73 (inside the confidence interval).

Combining all inputs, the CAPM equation provides us with a 5.54% cost of

equity.

The company currently has currently a BBB+ rating awarded both by Standard &

Poor’s and Fitch rating agencies, with a stable outlook. According to market

benchmarking, this rating usually incorporates a default spread of 2%. Adding the

2% default spread to the risk-free rate of 0.4% we get a cost of debt of 2.4%. The

company has currently a 3-year €850 million bond outstanding with a coupon of

1.875% and YTM of 1.77%, which is consistent with the cost of debt for our

estimation period of 5+ years.

Exhibit 24: Net Capex Projections

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 22/28

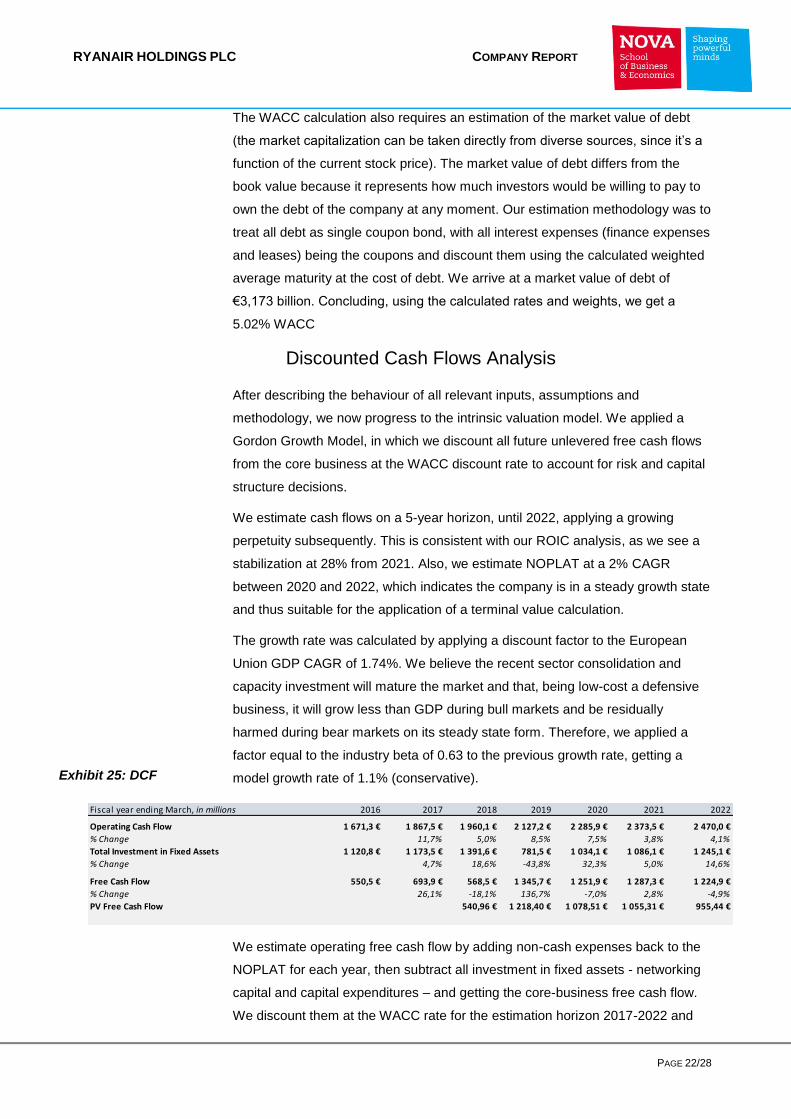

Fiscal year ending March, in millions 2016 2017 2018 2019 2020 2021 2022

Operating Cash Flow 1 671,3 € 1 867,5 € 1 960,1 € 2 127,2 € 2 285,9 € 2 373,5 € 2 470,0 €

% Change 11,7% 5,0% 8,5% 7,5% 3,8% 4,1%

Total Investment in Fixed Assets 1 120,8 € 1 173,5 € 1 391,6 € 781,5 € 1 034,1 € 1 086,1 € 1 245,1 €

% Change 4,7% 18,6% -43,8% 32,3% 5,0% 14,6%

Free Cash Flow 550,5 € 693,9 € 568,5 € 1 345,7 € 1 251,9 € 1 287,3 € 1 224,9 €

% Change 26,1% -18,1% 136,7% -7,0% 2,8% -4,9%

PV Free Cash Flow 540,96 € 1 218,40 € 1 078,51 € 1 055,31 € 955,44 €

The WACC calculation also requires an estimation of the market value of debt

(the market capitalization can be taken directly from diverse sources, since it’s a

function of the current stock price). The market value of debt differs from the

book value because it represents how much investors would be willing to pay to

own the debt of the company at any moment. Our estimation methodology was to

treat all debt as single coupon bond, with all interest expenses (finance expenses

and leases) being the coupons and discount them using the calculated weighted

average maturity at the cost of debt. We arrive at a market value of debt of

€3,173 billion. Concluding, using the calculated rates and weights, we get a

5.02% WACC

Discounted Cash Flows Analysis

After describing the behaviour of all relevant inputs, assumptions and

methodology, we now progress to the intrinsic valuation model. We applied a

Gordon Growth Model, in which we discount all future unlevered free cash flows

from the core business at the WACC discount rate to account for risk and capital

structure decisions.

We estimate cash flows on a 5-year horizon, until 2022, applying a growing

perpetuity subsequently. This is consistent with our ROIC analysis, as we see a

stabilization at 28% from 2021. Also, we estimate NOPLAT at a 2% CAGR

between 2020 and 2022, which indicates the company is in a steady growth state

and thus suitable for the application of a terminal value calculation.

The growth rate was calculated by applying a discount factor to the European

Union GDP CAGR of 1.74%. We believe the recent sector consolidation and

capacity investment will mature the market and that, being low-cost a defensive

business, it will grow less than GDP during bull markets and be residually

harmed during bear markets on its steady state form. Therefore, we applied a

factor equal to the industry beta of 0.63 to the previous growth rate, getting a

model growth rate of 1.1% (conservative).

We estimate operating free cash flow by adding non-cash expenses back to the

NOPLAT for each year, then subtract all investment in fixed assets - networking

capital and capital expenditures – and getting the core-business free cash flow.

We discount them at the WACC rate for the estimation horizon 2017-2022 and

Exhibit 25: DCF

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 23/28

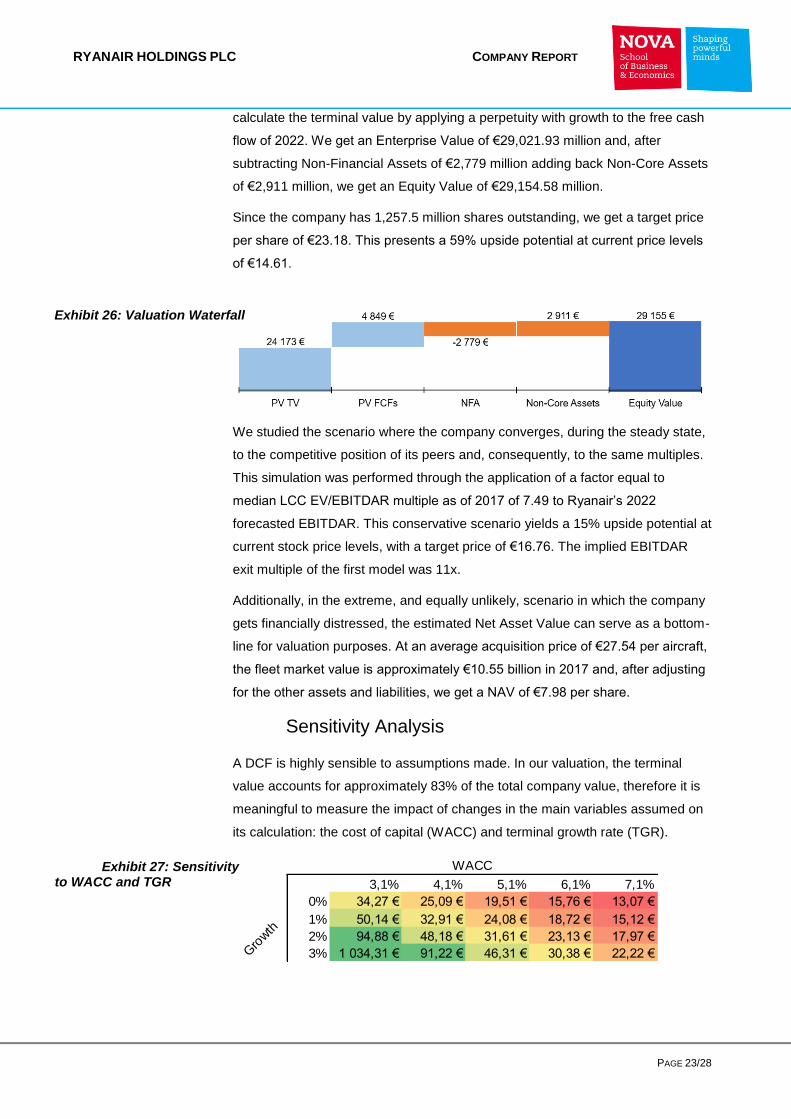

calculate the terminal value by applying a perpetuity with growth to the free cash

flow of 2022. We get an Enterprise Value of €29,021.93 million and, after

subtracting Non-Financial Assets of €2,779 million adding back Non-Core Assets

of €2,911 million, we get an Equity Value of €29,154.58 million.

Since the company has 1,257.5 million shares outstanding, we get a target price

per share of €23.18. This presents a 59% upside potential at current price levels

of €14.61.

We studied the scenario where the company converges, during the steady state,

to the competitive position of its peers and, consequently, to the same multiples.

This simulation was performed through the application of a factor equal to

median LCC EV/EBITDAR multiple as of 2017 of 7.49 to Ryanair’s 2022

forecasted EBITDAR. This conservative scenario yields a 15% upside potential at

current stock price levels, with a target price of €16.76. The implied EBITDAR

exit multiple of the first model was 11x.

Additionally, in the extreme, and equally unlikely, scenario in which the company

gets financially distressed, the estimated Net Asset Value can serve as a bottom-

line for valuation purposes. At an average acquisition price of €27.54 per aircraft,

the fleet market value is approximately €10.55 billion in 2017 and, after adjusting

for the other assets and liabilities, we get a NAV of €7.98 per share.

Sensitivity Analysis

A DCF is highly sensible to assumptions made. In our valuation, the terminal

value accounts for approximately 83% of the total company value, therefore it is

meaningful to measure the impact of changes in the main variables assumed on

its calculation: the cost of capital (WACC) and terminal growth rate (TGR).

WACC

##### 3,1% 4,1% 5,1% 6,1% 7,1%

0% 34,27 € 25,09 € 19,51 € 15,76 € 13,07 €

1% 50,14 € 32,91 € 24,08 € 18,72 € 15,12 €

2% 94,88 € 48,18 € 31,61 € 23,13 € 17,97 €

3% 1 034,31 € 91,22 € 46,31 € 30,38 € 22,22 €Gro

wth

Exhibit 26: Valuation Waterfall

Exhibit 27: Sensitivity to WACC and TGR

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 24/28

Share Price

0,0% 27,85 €

0,5% 24,12 €

1,0% 21,19 €

1,5% 18,83 €

2,0% 16,89 €Risk-

free

March 31, 2017 March 31, 2018 March 31, 2019 March 31, 2020 March 31, 2021 March 31, 2022

Operating revenues

Scheduled revenues 4 868,20 € 4 957,06 € 5 419,47 € 5 866,92 € 6 288,43 € 6 740,23 €

Ancillary revenues 1 779,60 € 1 926,53 € 2 213,59 € 2 514,40 € 2 695,04 € 2 888,67 €

Total operating revenues – continuing operations 6 647,80 € 6 883,59 € 7 633,05 € 8 381,32 € 8 983,48 € 9 628,90 €

Operating expenses

Fuel and oil -1 913,40 € -1 813,56 € -2 050,56 € -2 209,54 € -2 298,30 € -2 441,28 €

Airport and handling charges -864,80 € -880,59 € -953,29 € -1 032,00 € -1 117,20 € -1 209,44 €

Route charges -655,70 € -667,67 € -722,79 € -782,47 € -847,08 € -917,01 €

Staff costs -633,00 € -771,60 € -964,88 € -1 167,17 € -1 361,87 € -1 527,61 €

Depreciation -497,50 € -565,40 € -602,87 € -663,35 € -721,04 € -781,33 €

Marketing, distribution and other -322,30 € -370,46 € -370,28 € -436,57 € -500,69 € -563,49 €

Maintenance, materials and repairs -141,00 € -168,66 € -176,95 € -189,98 € -203,81 € -213,29 €

Aircraft rentals -86,10 € -83,49 € -80,88 € -78,27 € -75,66 € -75,66 €

Total operating expenses -5 113,80 € -5 321,42 € -5 922,50 € -6 559,34 € -7 125,65 € -7 729,11 €

Operating profit – continuing operations 1 534,00 € 1 562,17 € 1 710,55 € 1 821,97 € 1 857,83 € 1 899,79 €

Other income/(expense):

Gain on disposal of available for sale financial asset 0,00 € 0,00 € 0,00 € 0,00 € 0,00 € 0,00 €

Finance expense -67,20 € -67,69 € -75,65 € -87,49 € -90,51 € -95,03 €

Finance income 4,20 € 4,16 € 16,71 € 21,55 € 30,99 € 36,30 €

Foreign exchange (loss) -0,70 € 0,00 € 0,00 € 0,00 € 0,00 € 0,00 €

Total other income/(expenses) -63,70 € -63,53 € -58,94 € -65,94 € -59,51 € -58,73 €

Profit before tax 1 470,30 € 1 498,65 € 1 651,61 € 1 756,03 € 1 798,32 € 1 841,06 €

Tax expense on profit on ordinary activities -154,40 € -158,52 € -174,70 € -185,75 € -190,22 € -194,74 €

Profit for the year – all attributable to equity holders of parent 1 315,90 € 1 340,13 € 1 476,91 € 1 570,28 € 1 608,10 € 1 646,31 €

Basic earnings per ordinary share (euro cent) 105,30 € 107,24 € 118,18 € 125,65 € 128,68 € 131,74 €

Diluted earnings per ordinary share (euro cent) 104,64 € 106,57 € 117,45 € 124,87 € 127,88 € 130,92 €

Number of ordinary shares (in Ms) 1249,70 1249,70 1249,70 1249,70 1249,70 1249,70

Number of diluted shares (in Ms) 1257,50 1257,50 1257,50 1257,50 1257,50 1257,50

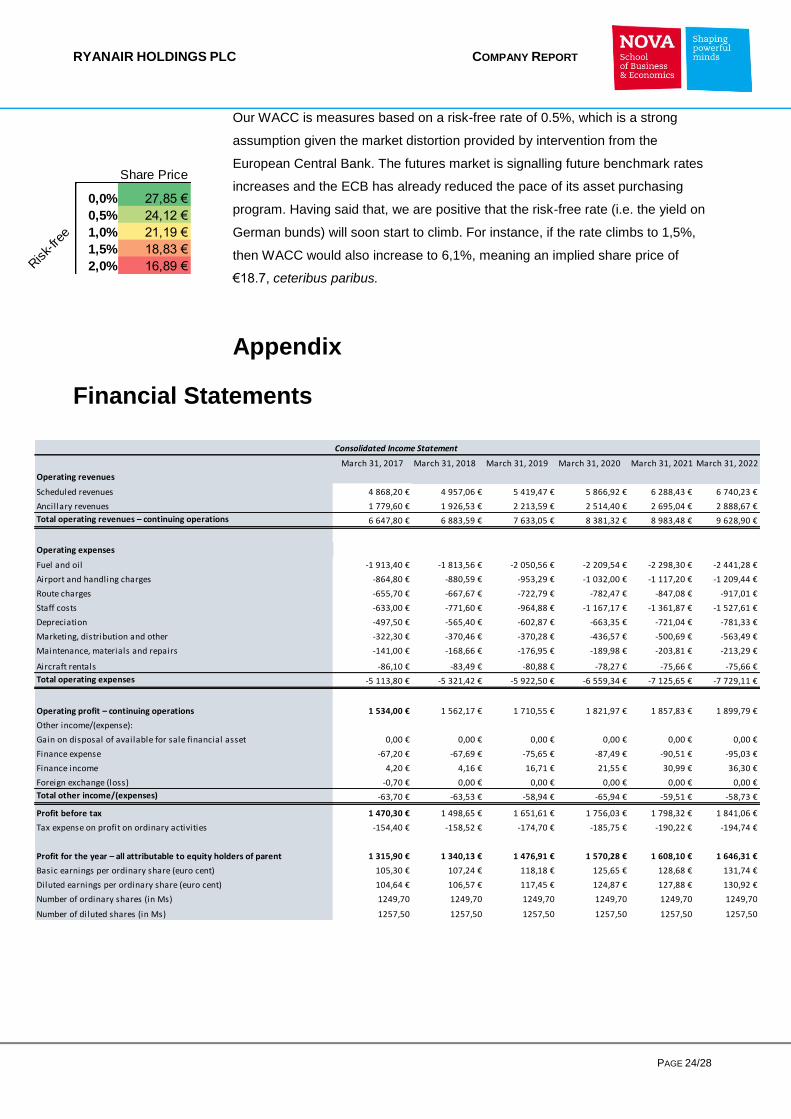

Consolidated Income Statement

Our WACC is measures based on a risk-free rate of 0.5%, which is a strong

assumption given the market distortion provided by intervention from the

European Central Bank. The futures market is signalling future benchmark rates

increases and the ECB has already reduced the pace of its asset purchasing

program. Having said that, we are positive that the risk-free rate (i.e. the yield on

German bunds) will soon start to climb. For instance, if the rate climbs to 1,5%,

then WACC would also increase to 6,1%, meaning an implied share price of

€18.7, ceteribus paribus.

Appendix

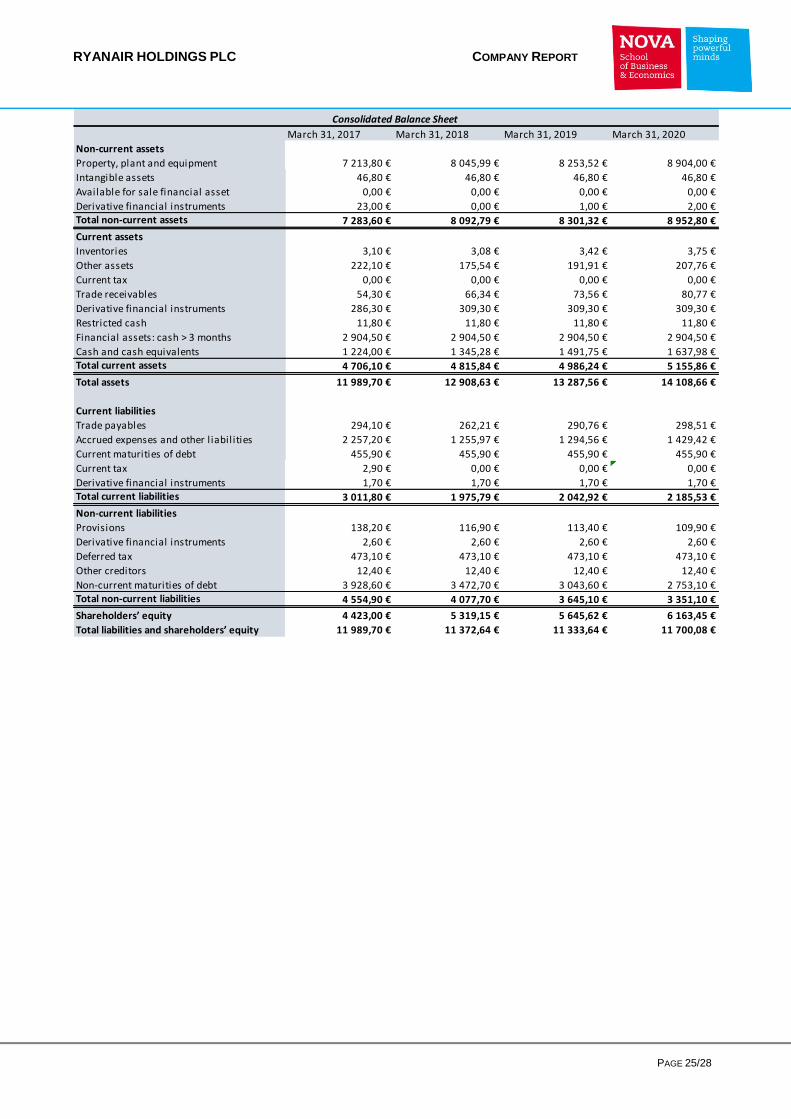

Financial Statements

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 25/28

March 31, 2017 March 31, 2018 March 31, 2019 March 31, 2020

Non-current assets

Property, plant and equipment 7 213,80 € 8 045,99 € 8 253,52 € 8 904,00 €

Intangible assets 46,80 € 46,80 € 46,80 € 46,80 €

Available for sale financial asset 0,00 € 0,00 € 0,00 € 0,00 €

Derivative financial instruments 23,00 € 0,00 € 1,00 € 2,00 €Total non-current assets 7 283,60 € 8 092,79 € 8 301,32 € 8 952,80 €

Current assets

Inventories 3,10 € 3,08 € 3,42 € 3,75 €

Other assets 222,10 € 175,54 € 191,91 € 207,76 €

Current tax 0,00 € 0,00 € 0,00 € 0,00 €

Trade receivables 54,30 € 66,34 € 73,56 € 80,77 €

Derivative financial instruments 286,30 € 309,30 € 309,30 € 309,30 €

Restricted cash 11,80 € 11,80 € 11,80 € 11,80 €

Financial assets: cash > 3 months 2 904,50 € 2 904,50 € 2 904,50 € 2 904,50 €

Cash and cash equivalents 1 224,00 € 1 345,28 € 1 491,75 € 1 637,98 €Total current assets 4 706,10 € 4 815,84 € 4 986,24 € 5 155,86 €

Total assets 11 989,70 € 12 908,63 € 13 287,56 € 14 108,66 €

Current liabilities

Trade payables 294,10 € 262,21 € 290,76 € 298,51 €

Accrued expenses and other l iabilities 2 257,20 € 1 255,97 € 1 294,56 € 1 429,42 €

Current maturities of debt 455,90 € 455,90 € 455,90 € 455,90 €

Current tax 2,90 € 0,00 € 0,00 € 0,00 €

Derivative financial instruments 1,70 € 1,70 € 1,70 € 1,70 €Total current liabilities 3 011,80 € 1 975,79 € 2 042,92 € 2 185,53 €

Non-current liabilities

Provisions 138,20 € 116,90 € 113,40 € 109,90 €

Derivative financial instruments 2,60 € 2,60 € 2,60 € 2,60 €

Deferred tax 473,10 € 473,10 € 473,10 € 473,10 €

Other creditors 12,40 € 12,40 € 12,40 € 12,40 €

Non-current maturities of debt 3 928,60 € 3 472,70 € 3 043,60 € 2 753,10 €Total non-current liabilities 4 554,90 € 4 077,70 € 3 645,10 € 3 351,10 €

Shareholders’ equity 4 423,00 € 5 319,15 € 5 645,62 € 6 163,45 €

Total liabilities and shareholders’ equity 11 989,70 € 11 372,64 € 11 333,64 € 11 700,08 €

Consolidated Balance Sheet

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 26/28

Disclosures and Disclaimers

Report Recommendations

Buy Expected total return (including expected capital gains and expected dividend yield)

of more than 10% over a 12-month period.

Hold Expected total return (including expected capital gains and expected dividend yield)

between 0% and 10% over a 12-month period.

Sell Expected negative total return (including expected capital gains and expected

dividend yield) over a 12-month period.

This report was prepared by [insert student’s name], a Master in Finance’s student of Nova School of

Business & Economics (“Nova SBE”), within the context of the Field Lab – Equity Research.

This report is issued and published exclusively for academic purposes, namely for academic evaluation and

masters graduation purposes, within the context of said Field Lab – Equity Research. It is not to be construed

as an offer or a solicitation of an offer to buy or sell any security or financial instrument.

This report was supervised by a Nova SBE faculty member, acting merely in an academic capacity, who

revised the valuation methodology and the financial model.

Given the exclusive academic purpose of the reports produced by Nova SBE students, it is Nova SBE

understanding that Nova SBE, the author, the present report and its publishing, are excluded from the

persons and activities requiring previous registration from local regulatory authorities. As such, Nova SBE, its

faculty and the author of this report have not sought or obtained registration with or certification as financial

analyst by any local regulator, in any jurisdiction. In Portugal, the author of this report is not registered with or

qualified under COMISSÃO DO MERCADO DE VALORES MOBILIÁRIOS (“CMVM”, the Portuguese Securities Market

Authority) as a financial analyst. Rosário André - as the academic supervisor of the author - is registered as a

financial analyst with CMVM. No approval for publication or distribution of this report was required and/or

obtained from any local authority, given the exclusive academic nature of the report.

The additional disclaimers also apply:

USA: Pursuant to Section 202 (a) (11) of the Investment Advisers Act of 1940, neither Nova SBE nor the

author of this report are to be qualified as an investment adviser and, thus, registration with the Securities and

Exchange Commission (“SEC”, United States of America’s securities market authority) is not necessary.

Neither the Author nor Nova SBE receive any compensation of any kind for the preparation of the Reports.

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 27/28

Germany: Pursuant to §34c of the WpHG (Wertpapierhandelsgesetz, i.e., the German Securities Trading

Act), this entity is not required to register with or otherwise notify the Bundesanstalt für

Finanzdienstleistungsaufsicht (“BaFin”, the German Federal Financial Supervisory Authority). It should be

noted that Nova SBE is a fully-owned state university and there is no relation between the student’s equity

reports and any fund raising programme.

UK: Pursuant to section 22 of the Financial Services and Markets Act 2000 (the “FSMA”), for an activity to be

a regulated activity, it must be carried on “by way of business”. All regulated activities are subject to prior

authorization by the Financial Conduct Authority (“FCA”). However, this Report serves an exclusively

academic purpose and, as such, was not prepared by way of business.The author - a Masters’ student - is

the sole and exclusive responsible for the information, estimates and forecasts contained herein, and for

the opinions expressed, which exclusively reflect his/her own judgment at the date of the report. Nova SBE

and its faculty have no single and formal position in relation to the most appropriate valuation method,

estimates or projections used in the report and may not be held liable by the author’s choice of the latter.

The information contained in this report was compiled by students from public sources believed to be reliable,

but Nova SBE, its faculty, or the students make no representation that it is accurate or complete, and accept

no liability whatsoever for any direct or indirect loss resulting from the use of this report or of its content.

Students are free to choose the target companies of the reports. Therefore, Nova SBE may start covering

and/or suspend the coverage of any listed company, at any time, without prior notice. The students or Nova

SBE are not responsible for updating this report, and the opinions and recommendations expressed herein

may change without further notice.

The target company or security of this report may be simultaneously covered by more than one student.

Because each student is free to choose the valuation method, and make his/her own assumptions and

estimates, the resulting projections, price target and recommendations may differ widely, even when referring

to the same security. Moreover, changing market conditions and/or changing subjective opinions may lead to

significantly different valuation results. Other students’ opinions, estimates and recommendations, as well as

the advisor and other faculty members’ opinions may be inconsistent with the views expressed in this report.

Any recipient of this report should understand that statements regarding future prospects and performance

are, by nature, subjective, and may be fallible.

This report does not necessarily mention and/or analyze all possible risks arising from the investment in the

target company and/or security, namely the possible exchange rate risk resulting from the security being

denominated in a currency either than the investor’s currency, among many other risks.

The purpose of publishing this report is merely academic and it is not intended for distribution among private

investors. The information and opinions expressed in this report are not intended to be available to any

person other than Portuguese natural or legal persons or persons domiciled in Portugal. While preparing this

report, students did not have in consideration the specific investment objectives, financial situation or

particular needs of any specific person. Investors should seek financial advice regarding the appropriateness

of investing in any security, namely in the security covered by this report.

RYANAIR HOLDINGS PLC COMPANY REPORT

PAGE 28/28

The author hereby certifies that the views expressed in this report accurately reflect his/her personal opinion

about the target company and its securities. He/ She has not received or been promised any direct or indirect

compensation for expressing the opinions or recommendation included in this report.

[If applicable, it shall be added: “While preparing the report, the author may have performed an internship

(remunerated or not) in [insert the Company’s name]. This Company may have or have had an interest in the

covered company or security” and/ or “A draft of the reports have been shown to the covered company’s

officials (Investors Relations Officer or other), mainly for the purpose of correcting inaccuracies, and later

modified, prior to its publication.”]

The content of each report have been shown or made public to restricted parties prior to its publication in

Nova SBE’s website or in Bloomberg Professional, for academic purposes such as its distribution among

faculty members for students’ academic evaluation.

Nova SBE is a state-owned university, mainly financed by state subsidies, students tuition fees and

companies, through donations, or indirectly by hiring educational programs, among other possibilities. Thus,

Nova SBE may have received compensation from the target company during the last 12 months, related to its

fund raising programs, or indirectly through the sale of educational, consulting or research services.

Nevertheless, no compensation eventually received by Nova SBE is in any way related to or dependent on

the opinions expressed in this report. The Nova School of Business & Economics does not deal for or

otherwise offer any investment or intermediation services to market counterparties, private or intermediate

customers.

This report may not be reproduced, distributed or published, in whole or in part, without the explicit previous

consent of its author, unless when used by Nova SBE for academic purposes only. At any time, Nova SBE

may decide to suspend this report reproduction or distribution without further notice. Neither this document

nor any copy of it may be taken, transmitted or distributed, directly or indirectly, in any country either than

Portugal or to any resident outside this country. The dissemination of this document other than in Portugal or

to Portuguese citizens is therefore prohibited and unlawful.