s & s news letter for 2010 october part 2

DESCRIPTION

S & S NEWS LETTER FOR 2010 OCTOBER Part 2. VAS IN COMPARISON With IAS/IFRS. NON-ISSUED VIETNAMESE ACCOUNTING STANDARDS. VAS "First time Adoption of IFRS ” VAS "Share-based payment VAS "Non-current assets held for sale and discontinued operations" - PowerPoint PPT PresentationTRANSCRIPT

S & S NEWS LETTER FOR 2010 OCTOBER

Part 2

S & S Auditing and Consulting Co.,Ltd

VAS

IN COMPARISON With

IAS/IFRS

S & S Auditing and Consulting Co.,Ltd

NON-ISSUED VIETNAMESE ACCOUNTING STANDARDS

VAS "First time Adoption of IFRS”

VAS "Share-based payment VAS "Non-current assets held for sale and

discontinued operations" VAS "Exploration for and evaluation of mineral

resources” VAS "Financial instruments: Recognition and

Measurement VAS "Financial instruments: Presentation VAS "Financial instruments: Disclosures

S & S Auditing and Consulting Co.,Ltd

NON-ISSUED VIETNAMESE ACCOUNTING STANDARDS

VAS "Employee benefits" VAS "Accounting for Government grants disclosure of

Government assistance” VAS "Accounting and reporting by retirement benefit plans" VAS "Financial reporting in hyperinflationary economies" VAS "Impairment of assets" ._ VAS "Agriculture"

S & S Auditing and Consulting Co.,Ltd

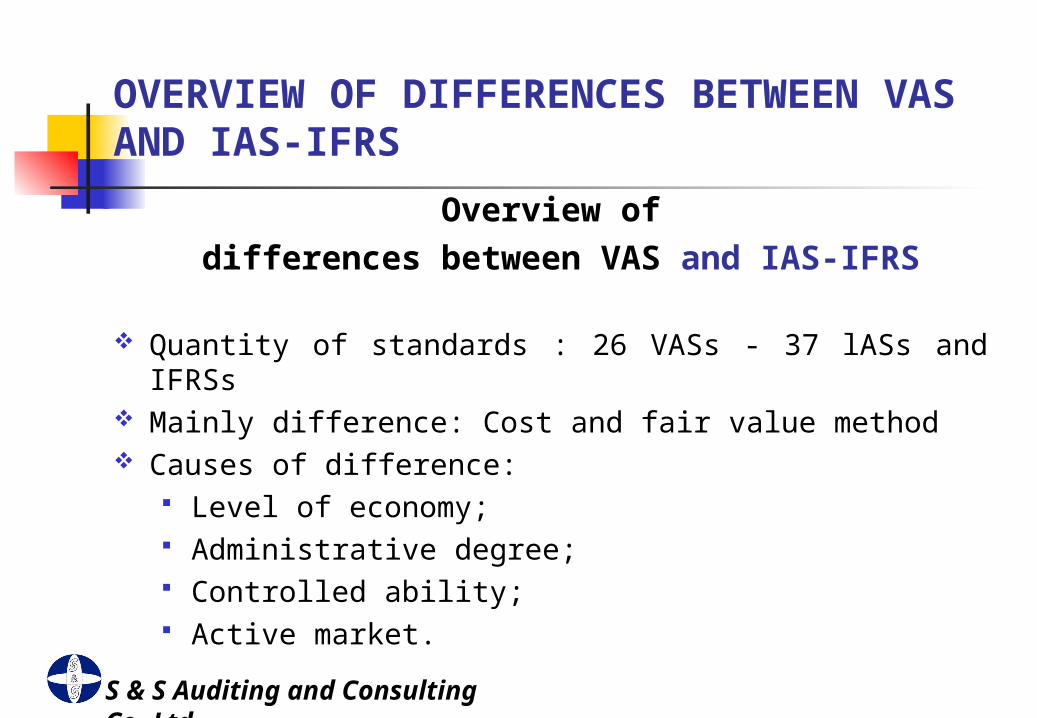

OVERVIEW OF DIFFERENCES BETWEEN VAS AND IAS-IFRS

Overview of

differences between VAS and IAS-IFRS

Quantity of standards : 26 VASs - 37 lASs and IFRSs Mainly difference: Cost and fair value method Causes of difference:

Level of economy; Administrative degree; Controlled ability; Active market.

S & S Auditing and Consulting Co.,Ltd

INSIGNIFICANT DIFFERENT VAS IN COMPARISON WITH IAS/IFRS

Insignificant different Standards Standard "Provisions, contingent liabilities and contingent

assets" Standard "Insurance contract" Standard "Events after the reporting period" Standard "Interim financial reporting" Standard "Earnings per share" Standard "Operating segments" Standard "Related party disclosures“ Standard "Accounting policies, changes in accounting

estimates and errors"

S & S Auditing and Consulting Co.,Ltd

VAS 01: GENERAL STANDARD - FRAMEWORK

Main differences

Accounting Principles and underlying assumptions Cost and other methods Accrual basis, going concern and substance over form

Measurement of the elements of financial statements

Historical and current cost, present and realizable values Concepts of capital and capital maintenance

S & S Auditing and Consulting Co.,Ltd

INVENTORY (VAS 02 - IAS 02)

Main differences Scope Cost of inventory

Cost method Retail method

Cost formulas of inventory Specific identification cost First-in, first-out(FIFO) Weighted average cost

Net realizable value

S & S Auditing and Consulting Co.,Ltd

PROPERTY, PLANT AND EQUIPMENT (VAS 03 - IAS 16)

Main differences

Scope Initial recognition - Elements of cost:

The initial estimate of the costs of dismantling and removing the asset and restoring to the site on which it is located should be include in the cost of fixed assets

Measurement after recognition

Cost and Revaluation models

S & S Auditing and Consulting Co.,Ltd

INTANGIBLE ASSETS (VAS 04 - 1AS 38)

Main differences

Scope Definitions:

Impairment loss Initial Recognition and measurement:

Land use right Measurement after recognition:

Cost and revaluation models Disclosure

S & S Auditing and Consulting Co.,Ltd

INVESTMENT PROPERTY (VAS 05 - IAS 40)

Main differences Initial recognition Measurement after initial recognition

Cost model Fair value model

Transfers Disposals Disclosure

Cost model Fair value model

S & S Auditing and Consulting Co.,Ltd

LEASES (VAS 06 - IAS 17)

Main differences

Accounting treatment in the financial statement of lessees - financial leases

Accounting treatment in the financial statements of lessees - operating leases

Accounting treatment in the financial statements of lessons - financial leases

S & S Auditing and Consulting Co.,Ltd

INVESTMENT IN ASSOCIATES (VAS 07 - IAS 28)

Main differences Scope Separate and consolidate financial statements

Cost method or in accordance with IAS 39 Equity method

Discontinue the use of the equity method Transactions between an investor and an associate Initial recognition Allocation of differences between Net book value and fair value

of net identified assets

S & S Auditing and Consulting Co.,Ltd

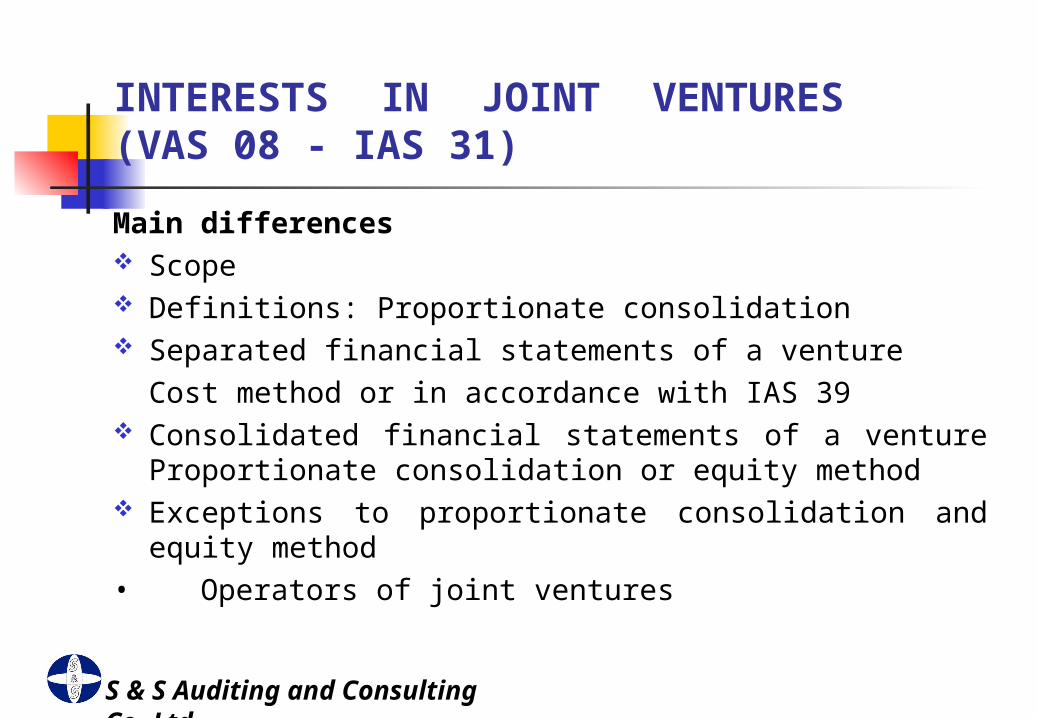

INTERESTS IN JOINT VENTURES (VAS 08 - IAS 31)

Main differences Scope Definitions: Proportionate consolidation Separated financial statements of a venture

Cost method or in accordance with IAS 39 Consolidated financial statements of a venture Proportionate

consolidation or equity method Exceptions to proportionate consolidation and equity method

• Operators of joint ventures

S & S Auditing and Consulting Co.,Ltd

THE EFFECTS OF CHANGES IN FOREIGN EXCHANGE RATES (VAS 10 – IAS 21)

Main differences Scope

Except to the extent that relates to IAS 39 Arising from applying proportionate consolidation

Functional currency Functional currency and accounting currency Change in functional currency Reporting foreign currency transactions in the fictional

currency (recognition of exchange difference) Tax effects of all exchange differences

S & S Auditing and Consulting Co.,Ltd

BUSINESS COMBINATION (VAS 11 - IFRS 03)

Main differences

Structure of standard Exceptions to both recognition and measurement principles

Income taxes; Employee benefits; Indemnification assets Exceptions to both recognition and measurement principles

Reacquired rights; Share-based payment awards; Assets held for sale

Accounting for goodwill

Impairment test of goodwill or Amortization of goodwill

S & S Auditing and Consulting Co.,Ltd

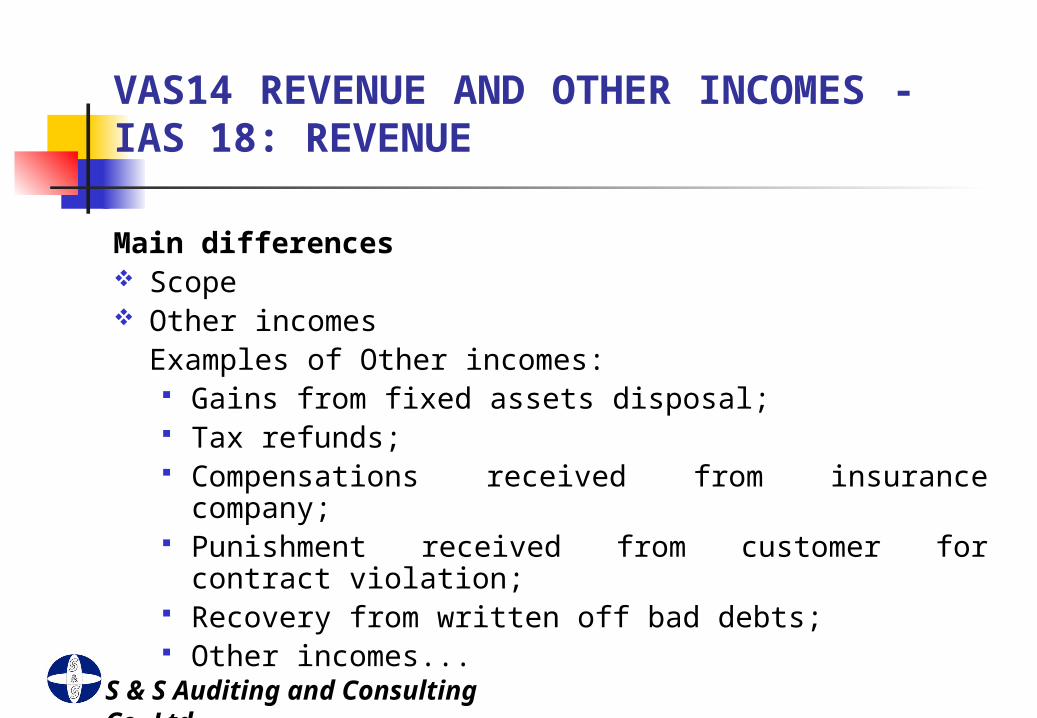

VAS14 REVENUE AND OTHER INCOMES - IAS 18: REVENUE

Main differences Scope Other incomes

Examples of Other incomes: Gains from fixed assets disposal; Tax refunds; Compensations received from insurance company; Punishment received from customer for contract violation; Recovery from written off bad debts; Other incomes...

S & S Auditing and Consulting Co.,Ltd

CONSTRUCTION CONTRACT (VAS 15 - IAS 11)

Main differences

Recognition of contract revenue and expenses Stage of completion method Progress payments method Amount of work completed method

Recognition of expected losses

S & S Auditing and Consulting Co.,Ltd

BORROWING COSTS (VAS 16 - IAS 23)

Main differences

Scope Definitions: Elements of Borrowing costs

The borrowing costs may include the exchange differences arising from foreign currency borrowings to the extent that they are regarded as an adjustment to interest costs

S & S Auditing and Consulting Co.,Ltd

INCOME TAXES (VAS17 - IAS12)

Main differences Tax base Recognition of deferred tax liabilities and assets Business combinations Assets carried at fair value Goodwill Initial recognition of an asset or liability Measurement Deferred tax arising from a business combination Current and deferred tax arising from share-based payment

transactions Presentation

S & S Auditing and Consulting Co.,Ltd

PRESENTATION OF FINANCIAL STATEMENTS (VAS21 - IAS01)

Main differences Complete set of financial statements

Form of statement of comprehensive income for the period Statement of changes in equity for the period Statement of financial position as at the beginning of the

earliest comparative period when an entity applies an accounting policies retrospectively or makes a retrospective restatement of items in its F/S or when it reclassifies items in its F/S

Reporting period Maturity date of assets and liabilities

S & S Auditing and Consulting Co.,Ltd

STATEMENT OF CASH FLOWS (VAS 24 - IAS 07)

Main differences

Investing activities

Cash flows from derivatives

Taxes on income Investments in subsidiaries, associates and joint ventures

S & S Auditing and Consulting Co.,Ltd

CONSOLIDATED AND SEPARATE FINANCIAL STATEMENTS S 25 - IAS 27)

Main differences

• Presentation of consolidated financial state!

• Scope of consolidated financial statements

• Consolidation procedures

• Loss of control

• Accounting for investments in subsidiaries, jointly controlled entities and associates in separate financial statements

+ Cost method

+ In accordance with IAS 32