sa credit ratings overview - nedbank · jp morgan global aggregate bond index • em external debt...

TRANSCRIPT

1

SA CREDIT RATINGS OVERVIEW

OCTOBER 2016

Reezwana Sumad

+2711 294 1753

www.nedbank.co.za

Mohammed Yaseen Nalla, CFA

+2711 295 5430

www.nedbank.co.za

2

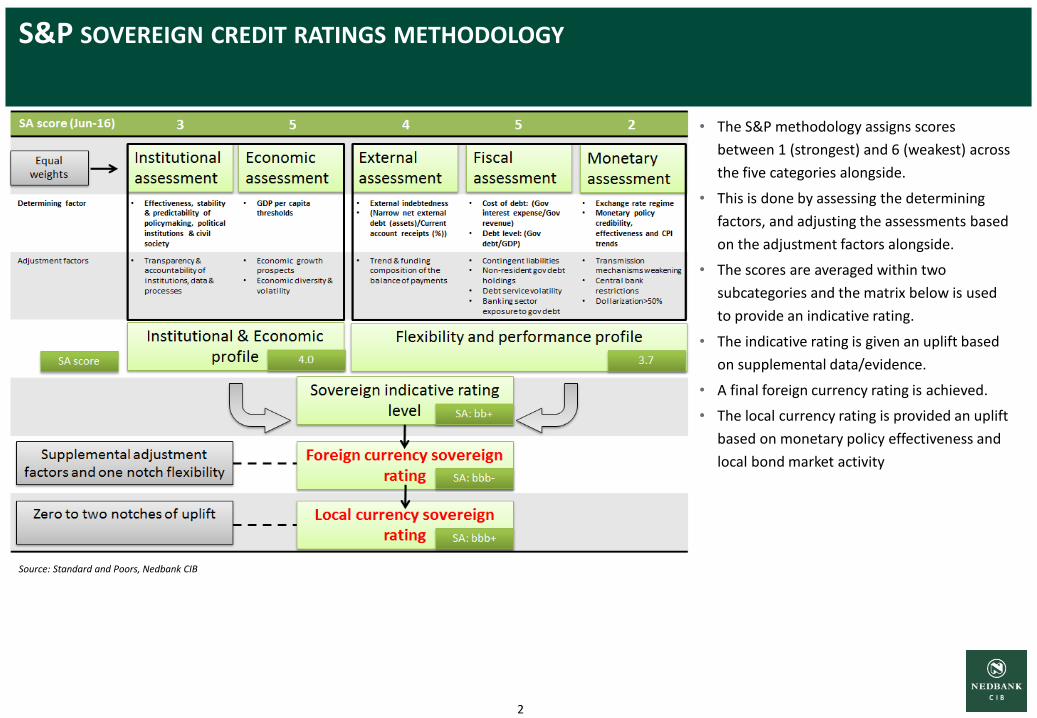

• The S&P methodology assigns scores

between 1 (strongest) and 6 (weakest) across

the five categories alongside.

• This is done by assessing the determining

factors, and adjusting the assessments based

on the adjustment factors alongside.

• The scores are averaged within two

subcategories and the matrix below is used

to provide an indicative rating.

• The indicative rating is given an uplift based

on supplemental data/evidence.

• A final foreign currency rating is achieved.

• The local currency rating is provided an uplift

based on monetary policy effectiveness and

local bond market activity

Source: Standard and Poors, Nedbank CIB

S&P SOVEREIGN CREDIT RATINGS METHODOLOGY

3

Sources: Standard and Poors, Nedbank CIB

S&P SOVEREIGN CREDIT RATINGS METHODOLOGY

• Based on the S&P criteria, and both the

qualitative and quantitative assessment

thereof, a foreign currency rating is derived

from the matrix alongside.

• There remains some latitude in terms of

potential uplift to the above mentioned

rating in the event that qualitative factors

suggest that such an uplift is warranted.

4

Our assessment of key risk flags (since June to date)

indicates that performance has been mixed across the

board.

While there has been progress on some metrics, this is

marginal at times and may not yet indicate a sustained

shift.

Certain macroeconomic indicators have improved but this

improvement is seen as cyclical in some respects, and as

such, insufficient to inform trend changes.

Any potential deferral in a credit downgrade should not be

construed as an incentive to ease off the prioritisation of

structural reforms

EVOLUTION OF KEY RISKS – JUNE 2016 TO PRESENT

Source: Nedbank CIB

5

There is much concern over what a downgrade may entail.

At present, the exclusion criteria for the major bond

indices implies some buffer on the S&P ratings, given the

fact that local currency (LC) ratings are two notches above

foreign currency (FC ratings).

JP Morgan Global Aggregate Bond Index

• EM external debt instrument eligibility is determined by

the HIGHER rating of either S&P or Moody's.

• Currently Moody's is one notch above S&P, implying a

low risk of exclusion

CITI World Government Bond Index

• Remain above BBB- (S&P) or Baa3 (Moody's) for

sovereign LC ratings.

BOND INDEX EXCLUSION (RATINGS) CRITERIA

Source: Nedbank CIB, S&P, Moody's, Fitch, JP Morgan, Citi

6

Nedbank view:

• Institutional - Generally effective policymaking and public finances, but potentially destabilising socioeconomic

challenges remain.

• Economic: SA is currently on the cusp for a lower GDP-per-capita score. Although improvements would have

been noted on the back of a strong rand recently, this will likely be viewed as cyclical. Economic conditions

remain vulnerable to external shocks, while potential growth remains low. A structural trend shift will need to

be observed to inform a change in view.

• External: Despite having a large and liquid currency market, external indebtedness remains high. Current

account receipts are unlikely to maintain the recent favourable trend due to sluggish global demand.

• Fiscal: Fiscal performance and flexibility remain weak. Government debt levels have risen by 6% of GDP, on

average, over the last five years. Added to this is the shortfall in basic services like healthcare and education.

On the debt side, even though the government debt level is acceptable (45% of GDP in 2015), interest

expenditures have averaged 12% of total revenues over the past five years.

• Monetary: SA's monetary sector remains a key strength, with the SARB's credibility, effectiveness ,

independence and inflation targeting policies effective.

OUR CURRENT ASSESSMENT INDICATES SOME MARGINAL IMPROVEMENTS

Sources: Nedbank CIB, IIF

7

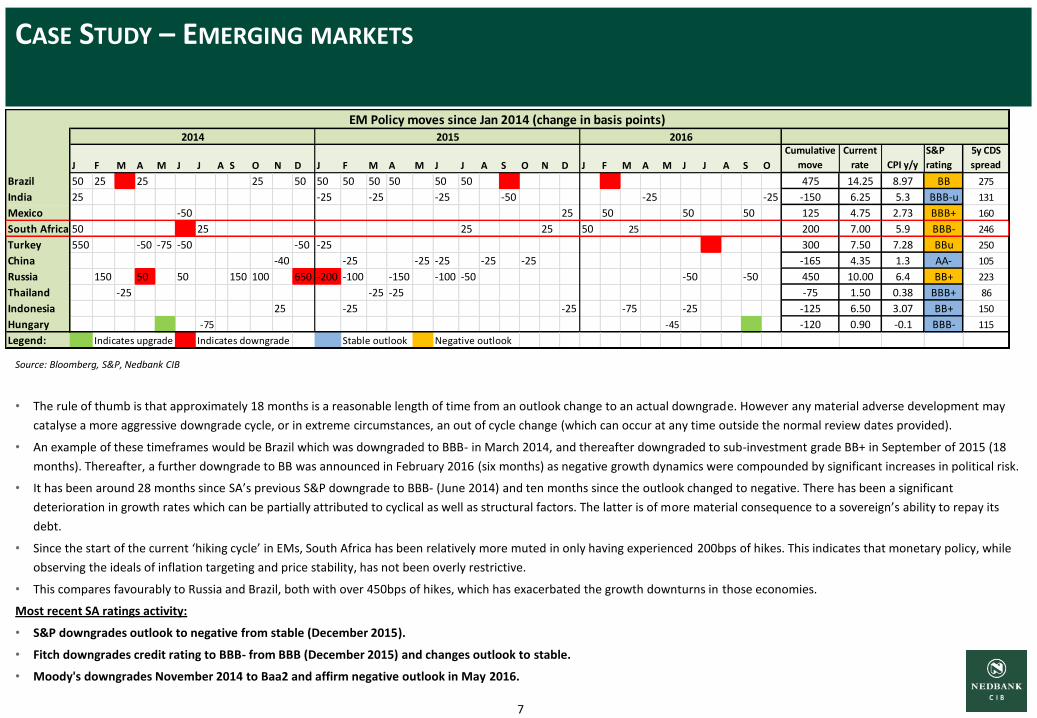

• The rule of thumb is that approximately 18 months is a reasonable length of time from an outlook change to an actual downgrade. However any material adverse development may

catalyse a more aggressive downgrade cycle, or in extreme circumstances, an out of cycle change (which can occur at any time outside the normal review dates provided).

• An example of these timeframes would be Brazil which was downgraded to BBB- in March 2014, and thereafter downgraded to sub-investment grade BB+ in September of 2015 (18

months). Thereafter, a further downgrade to BB was announced in February 2016 (six months) as negative growth dynamics were compounded by significant increases in political risk.

• It has been around 28 months since SA’s previous S&P downgrade to BBB- (June 2014) and ten months since the outlook changed to negative. There has been a significant

deterioration in growth rates which can be partially attributed to cyclical as well as structural factors. The latter is of more material consequence to a sovereign’s ability to repay its

debt.

• Since the start of the current ‘hiking cycle’ in EMs, South Africa has been relatively more muted in only having experienced 200bps of hikes. This indicates that monetary policy, while

observing the ideals of inflation targeting and price stability, has not been overly restrictive.

• This compares favourably to Russia and Brazil, both with over 450bps of hikes, which has exacerbated the growth downturns in those economies.

Most recent SA ratings activity:

• S&P downgrades outlook to negative from stable (December 2015).

• Fitch downgrades credit rating to BBB- from BBB (December 2015) and changes outlook to stable.

• Moody's downgrades November 2014 to Baa2 and affirm negative outlook in May 2016.

Source: Bloomberg, S&P, Nedbank CIB

CASE STUDY – EMERGING MARKETS

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O

Cumulative

move

Current

rate CPI y/y

S&P

rating

5y CDS

spread

Brazil 50 25 25 25 50 50 50 50 50 50 50 475 14.25 8.97 BB 275

India 25 -25 -25 -25 -50 -25 -25 -150 6.25 5.3 BBB-u 131

Mexico -50 25 50 50 50 125 4.75 2.73 BBB+ 160

South Africa 50 25 25 25 50 25 200 7.00 5.9 BBB- 246

Turkey 550 -50 -75 -50 -50 -25 300 7.50 7.28 BBu 250

China -40 -25 -25 -25 -25 -25 -165 4.35 1.3 AA- 105

Russia 150 50 50 150 100 650 -200 -100 -150 -100 -50 -50 -50 450 10.00 6.4 BB+ 223

Thailand -25 -25 -25 -75 1.50 0.38 BBB+ 86

Indonesia 25 -25 -25 -75 -25 -125 6.50 3.07 BB+ 150

Hungary -75 -45 -120 0.90 -0.1 BBB- 115

Legend: Indicates upgrade Indicates downgrade Stable outlook Negative outlook

2014

EM Policy moves since Jan 2014 (change in basis points)2015 2016

8

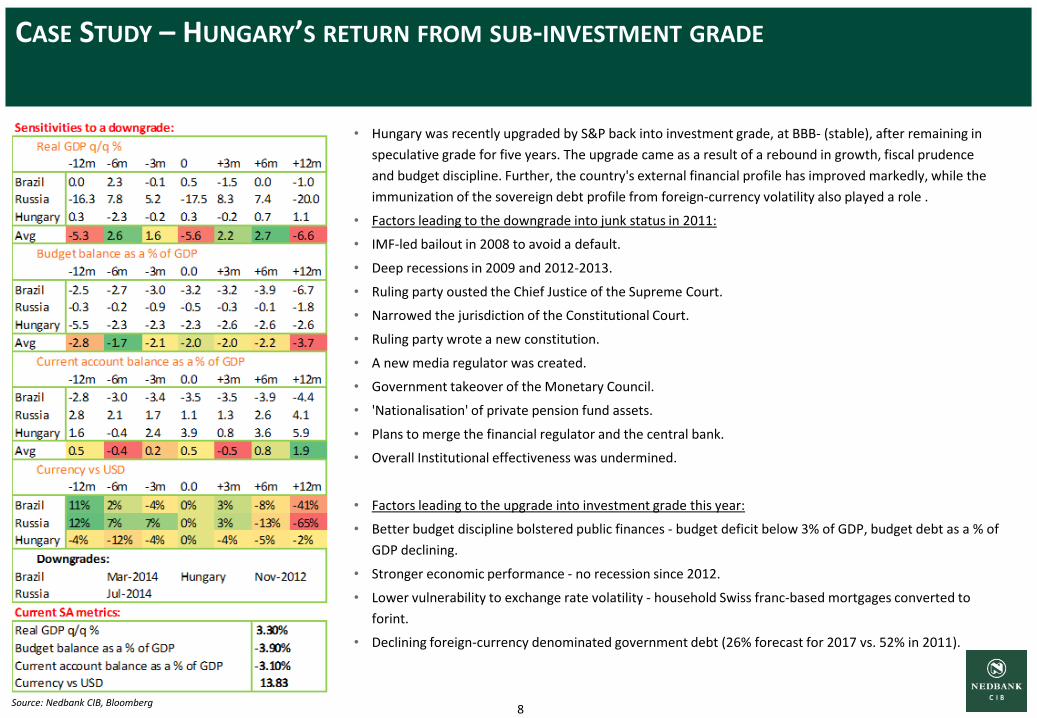

• Hungary was recently upgraded by S&P back into investment grade, at BBB- (stable), after remaining in

speculative grade for five years. The upgrade came as a result of a rebound in growth, fiscal prudence

and budget discipline. Further, the country's external financial profile has improved markedly, while the

immunization of the sovereign debt profile from foreign-currency volatility also played a role .

• Factors leading to the downgrade into junk status in 2011:

• IMF-led bailout in 2008 to avoid a default.

• Deep recessions in 2009 and 2012-2013.

• Ruling party ousted the Chief Justice of the Supreme Court.

• Narrowed the jurisdiction of the Constitutional Court.

• Ruling party wrote a new constitution.

• A new media regulator was created.

• Government takeover of the Monetary Council.

• 'Nationalisation' of private pension fund assets.

• Plans to merge the financial regulator and the central bank.

• Overall Institutional effectiveness was undermined.

• Factors leading to the upgrade into investment grade this year:

• Better budget discipline bolstered public finances - budget deficit below 3% of GDP, budget debt as a % of

GDP declining.

• Stronger economic performance - no recession since 2012.

• Lower vulnerability to exchange rate volatility - household Swiss franc-based mortgages converted to

forint.

• Declining foreign-currency denominated government debt (26% forecast for 2017 vs. 52% in 2011).

CASE STUDY – HUNGARY’S RETURN FROM SUB-INVESTMENT GRADE

Source: Nedbank CIB, Bloomberg

9

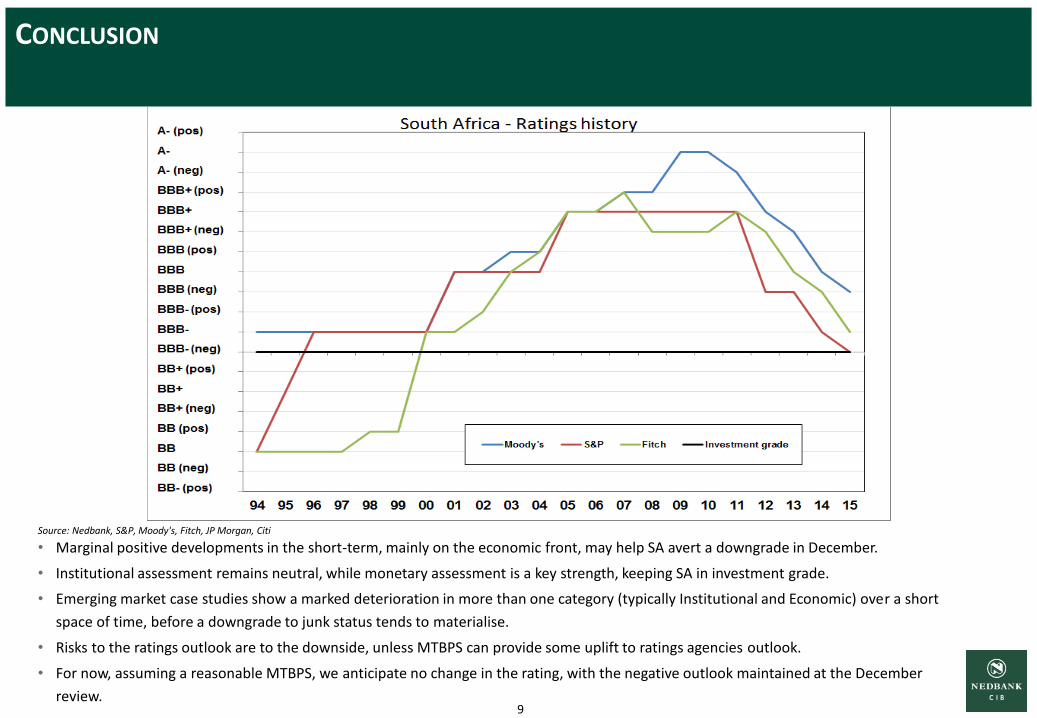

• Marginal positive developments in the short-term, mainly on the economic front, may help SA avert a downgrade in December.

• Institutional assessment remains neutral, while monetary assessment is a key strength, keeping SA in investment grade.

• Emerging market case studies show a marked deterioration in more than one category (typically Institutional and Economic) over a short

space of time, before a downgrade to junk status tends to materialise.

• Risks to the ratings outlook are to the downside, unless MTBPS can provide some uplift to ratings agencies outlook.

• For now, assuming a reasonable MTBPS, we anticipate no change in the rating, with the negative outlook maintained at the December

review.

CONCLUSION

Source: Nedbank, S&P, Moody's, Fitch, JP Morgan, Citi

10

THANK YOU

Disclaimer and Copyright This Report is not directed to, or intended for use by or distribution to, directly or indirectly, in whole or in part, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject any member of the Group to any registration or licensing requirement within such jurisdiction. This Report has been issued or approved for issue by a representative of Nedbank and has been forwarded to you solely for information purposes and for your consideration. The information contained in this Report is confidential and is not intended to be, nor should it be construed as, "advice" as contemplated in the Financial Advisory and Intermediary Services Act, 2002 or otherwise, or a direct or indirect invitation or inducement to any person to engage in investment activity relating to any securities or any derivative instrument or any other rights pertaining thereto of any company mentioned herein (“financial instruments”). Information and opinions presented in this Report were obtained or derived from public sources that Nedbank believes are reliable but makes no representations as to their accuracy or completeness. Any opinions, forecasts or estimates herein constitute a judgement as at the date of this Report and should not be relied upon. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or estimates. Past performance should not be taken as an indication or guarantee of future performance and no representation or warranty, express or implied is made regarding future performance. The price, value of and income from any of the financial instruments mentioned in this Report can fall as well as rise. Certain transactions including those involving futures, options and other derivative instruments can give rise to substantial risk of loss and are not suitable for all investors. Before entering into any transaction, you should independently take advice on and evaluate the risks and potential benefits of the transaction. Opinions, forecasts and estimates expressed in this Report are subject to change without notice and may differ or be contrary to opinions, forecasts and estimates expressed by other business areas in the Group as a result of using different assumptions and criteria. Furthermore, the Group (including each member's directors, employees, representatives and agents) accepts no responsibility or liability (whether in delict, contract or otherwise) for any loss arising from the use of or reliance placed upon the material presented in this Report, except that this exclusion of liability does not apply to the extent that liability arises under specific statutes or regulations applicable to any member of the Group. In addition, members of the Group may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this Report. Those reports reflect the different assumptions, views and analytical methods of the research analysts who prepared them and Nedbank is under no obligation to ensure that such other reports are brought to the attention of any recipient of this Report. Members of the Group may be involved in many businesses that relate to companies and financial instruments mentioned in this Report. Any prices or levels contained herein are preliminary and indicative only and do not represent bids or offers. These indications are provided solely for your information and consideration. The information contained in this Report may include results of analyses from a quantitative model which represent potential future events that may or may not be realized, and is not a complete analysis of every material fact representing any product, company or financial instrument. Any estimates included herein constitute the judgment of the research analyst as of the date hereof and are subject to change without any notice. This Report may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the Report refers to website material of Nedbank, Nedbank has not reviewed the linked site and takes no responsibility for the content contained therein. Such address or hyperlink (including addresses or hyperlinks to Nedbank’s own website material) is provided solely for your convenience and information and the content of the linked site does not in any way form part of this Report. Accessing such website or following such link through this Report or Nedbank’s website is entirely at your own risk. Directors, officers and/or employees of any member of the Group may at any time, to the extent permitted by law, own or have a position in the financial instruments of any company or related company referred to herein, and may add to or dispose of any such position or act as a principal in any transaction in such financial instruments. Nedbank and/or its Affiliates may make a market in these instruments for its customers and for its own account. Accordingly, Nedbank and/or its Affiliates may have a position in any such instrument at any time. Directors, officers and/or employees of Nedbank and/or its Affiliates may also be directors of companies mentioned in this Report. Nedbank and/or its Affiliates may from time to time provide or solicit investment banking, underwriting or other financial services to, for or from any company referred to herein. The financial instruments referred to may not be suitable for the specific investment objectives, financial situation or individual needs of recipients and should not be relied upon in substitution for the exercise of independent judgement. It is recommended that you obtain independent advice if you are in doubt about such investments or investment services. This Report is intended for use by professional and sophisticated business investors only. Structured financial instruments are complex instruments, typically involve a high degree of risk and are intended for sale only to sophisticated investors who are capable of understanding and assuming the risks involved. The market value of any structured financial instrument may be affected by changes in economic, financial and political factors (including, but not limited to, spot and forward interest and exchange rates), time to maturity, market conditions and volatility, and the credit quality of a company or reference company. Any investor interested in purchasing a structured financial instrument/ product should conduct their own investigation and analysis of the product and consult with their own professional advisers as to the risks involved in making such a purchase. Some investments discussed in this Report may have a high level of volatility. High volatility investments may experience sudden and large falls in their value causing losses when that investment is realised. Those losses may equal your original investment. Indeed, in the case of some investments the potential losses may exceed the amount of initial investment and, in such circumstances, you may be required to pay more money to support those losses. Income yields from investments may fluctuate and, in consequence, initial capital paid to make the investment may be used as part of that income yield. Some investments may not be readily realisable and it may be difficult to sell or realise those investments, similarly it may prove difficult for you to obtain reliable information about the value, or risks, to which such an investment is exposed.] To our readers in the United Kingdom, this report has been issued by Nedbank Limited, a firm authorised by the Prudential Regulation Authority and regulated in the United Kingdom by the Financial Conduct Authority and the Prudential Regulation Authority. Nedbank Limited is a member of the Johannesburg Stock Exchange Limited (the ‘JSE”, which is authorised and regulated by the JSE Limited. This Report is not for distribution to private customers. This Report has been issued in the United Kingdom only to persons of a kind described in Article 19 (5), 38, 47 and 49 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (all such persons being referred to as “relevant persons”). Any investment or investment activity to which this Report relates is only available to relevant persons and will be engaged in only with relevant persons. In other EEA countries, this Report has been issued to persons regarded as professional investors (or equivalent) in their home jurisdiction. This Report is not intended for use by, or distribution to, persons in the United States that do not meet the definition of a major US institutional investor under Rule 15a-6 under the US Securities Exchange Act of 1934 (“Rule 15a-6”). The financial instruments described herein may not have been registered under the US Securities Act of 1933 (the “Securities Act”) and may not be offered or sold in the United States unless they have been registered under the Securities Act, or pursuant to an exemption from, or in transactions not subject to, the registration requirements of the Securities Act, and in compliance with any applicable securities laws of any state or other jurisdiction of the United States. Any US persons or recipients of this Report located in the United States that are interested in trading financial instruments referred to in this Report should only effect such transactions through a US-registered broker-dealer. The distribution of this Report in certain jurisdictions may be prohibited or restricted by rules, regulations and/or laws of such jurisdictions and persons into whose possessions this presentation comes should inform themselves about and observe any such restrictions. Any failure to comply with such prohibitions or restrictions may constitute a violation of the laws of such other jurisdictions. All material presented in this Report, unless specifically indicated otherwise, is under copyright to Nedbank. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior written permission of Nedbank. All trademarks, service marks and logos used in this Report are trademarks or service marks or registered trademarks or service marks of Nedbank or its Affiliates.

11

THANK YOU

Disclaimer Continued Nedbank Limited, a firm authorised by the Prudential Regulation Authority ('PRA') and regulated in the United Kingdom by the Financial Conduct Authority ('FCA') and the PRA. Nedbank Limited is a registered bank governed by the South African Reserve Bank ('SARB') in terms of the South African Banks Act, 1990 (as amended) and is also a member of the Johannesburg Stock Exchange Limited (the 'JSE’), which is authorised and regulated by the JSE. is acting exclusively for our directed client and no-one else and will not regard any other person as its client in relation to the subject matter of this presentation and will not be responsible to anyone other than our directed client for providing the protections afforded to their respective clients or for giving advice in relation to the contents of this presentation. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior written permission of Nedbank Limited ('Nedbank'). This presentation may not be released, published or distributed, in whole or in part, directly or indirectly, in or into or from any jurisdiction where such distribution is unlawful including but not limited to the United States, Canada, Japan and Australia. Persons into whose possessions this presentation comes should inform themselves about, and observe, any such restrictions. Any failure to comply with this restriction may constitute a violation of applicable securities laws. For the purposes of this notice, 'presentation' means this document, its contents or any part of it, any oral presentation, any question or answer session and any written or oral material discussed or distributed during the presentation meeting. The information contained in this presentation is confidential and is not intended to be, nor should it be construed as, 'advice' (as contemplated under the South African Financial Advisory and Intermediary Services Act, 2002 (as amended) or otherwise) or a direct or indirect invitation or inducement to any person to engage in investment activity relating to any securities or any derivative instrument or any other rights pertaining thereto ('financial instruments'). This presentation is made available on the express understanding that it does not contain all the information that may be required to evaluate it and will not be used by the recipients in connection with the purchase of or investment in financial instruments. Financial instruments mentioned herein may not be suitable for all investors. Financial instruments of emerging and mid-size growth companies typically involve a higher degree of risk and more volatility then the securities of more established companies. You should seek independent advice (including tax, accounting, legal, regulatory and financial advice) in relation to the content of this document. The information contained in the presentation may constitute 'inside information' in relation to an issuer or its securities within the meaning of Part V of the Criminal Justice Act 1993, as amended from time to time as well as 'inside information' under the South African Financial Markets Act, 2012 (as amended), and disclosure of such information may constitute a criminal offence. Disclosure of such information may also constitute 'market abuse' within the meaning of the United Kingdom Financial Services and Markets Act 2000, as amended ('FSMA') and the South African Financial Markets Act, 2012 (as amended). Nedbank and its ultimate holding companies or any direct or indirect subsidiary undertakings of such holding companies (its 'Affiliates') (and their respective officers, directors, agents, advisors and employees), including persons involved in the preparation or issuance of this document, may from time to time act as manager or co-manager of a public offering or otherwise deal in, hold or act as market-makers or advisors, brokers or commercial and/or investment bankers in relation to the financial instruments which are the subject of this document or any related derivatives. Unless otherwise stated, information and opinions presented in this presentation were obtained or derived from public sources that Nedbank believes are reliable. However, this presentation has not been independently verified and no representation or warranty, express or implied, is made by or on behalf of the Nedbank or its Affiliates or any of their respective directors, officers, employees, agents, or advisers and no reliance should be placed on the adequacy, fairness, accuracy, or completeness of the information or opinions contained in this presentation and no responsibility or liability (whether in tort, contract or otherwise) is assumed or accepted by any such persons in relation to any such information or opinion for any errors or omissions. Nedbank and its Affiliates and their respective directors, officers, employees, agents, or advisers shall have, and to the fullest extent permissible by law such persons disclaim, any responsibility or liability (whether in tort, contract or otherwise) for any loss or damage of whatever description suffered by any persons arising from any use of or reliance placed upon the information or any of the statements, opinions or conclusions set out in this presentation or the comments, written or oral, of any person made in connection with this presentation or otherwise arising in connection with this presentation, except that this exclusion of liability does not apply to the extent that liability arises under specific statutes or regulations applicable to Nedbank or its Affiliates. The information contained in this document may not be construed as advice (including investment, legal, accounting, regulatory or tax advice). All recipients should seek independent advice as to the suitability of any investments described in this document. Past performance is no guarantee of future returns. Any modeling or back-testing data contained in this document should not be construed as a statement or projection as to future performance. Any pricing in this document is indicative only and neither such pricing nor any other part of this document may be construed as an offer or solicitation for the purchase or sale of any financial instrument. Any opinions, forecasts or estimates herein constitute a judgement as at the date of this presentation and should not be relied upon. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or estimates. Past performance should not be taken as an indication or guarantee of future performance and no representation or warranty, express or implied is made regarding future performance. The price, value of and income from any of the financial instruments mentioned in this presentation can fall as well as rise. Certain transactions including those involving futures, options and other derivative instruments can give rise to substantial risk of loss and are not suitable for all investors. Before entering into any transaction, you should independently evaluate the risks and potential benefits of the transaction. Any opinions expressed in this presentation are subject to change without notice This presentation is only addressed to and directed at persons in the Republic of South Africa who have professional experience in, and whom Nedbank believes to be sufficiently knowledgeable to understand, matters relating to investments. Views expressed are those of Nedbank as at the date of this presentation, should not be relied upon and are subject to change without notice.