safety & economic supervised by: prof. mohamed fahim eng. yusuf ismail presented by hessa...

TRANSCRIPT

Safety & EconomicSafety & Economic

Supervised By:Prof. Mohamed Fahim

Eng. Yusuf Ismail

Presented byHessa Al-sahlawi

Beshayer Al-DihaniLatifah Al-Qabandi

Agenda

. Environmental Consideration.

.Plant Safety.

.Economy.

Environmental Considerations

• Environmental Protection Agency (EPA):Environmental Protection Agency (EPA):

• The role of the EPA is to protect the environmental from the effects of human activity.

• For the chemical processing industries, this role relates to emissions to harmful or potentially harmful materials from the plant site to outside by air or by water.

• There are three classes of such emission: (1). Planned emissions. (2). Fugitive emissions. (3). Emergency emissions.

• In our process syngas production from the steam reforming of natural gas entails the disposal of the following waste effluent streams:

• 1- In stream 8 (Output from Compressor K-102) which is Gaseous flue gas mixture, containing mainly CO2 and H2O, but with traces of CO, SO2 and nitrogen oxides which discharge to the atmosphere.

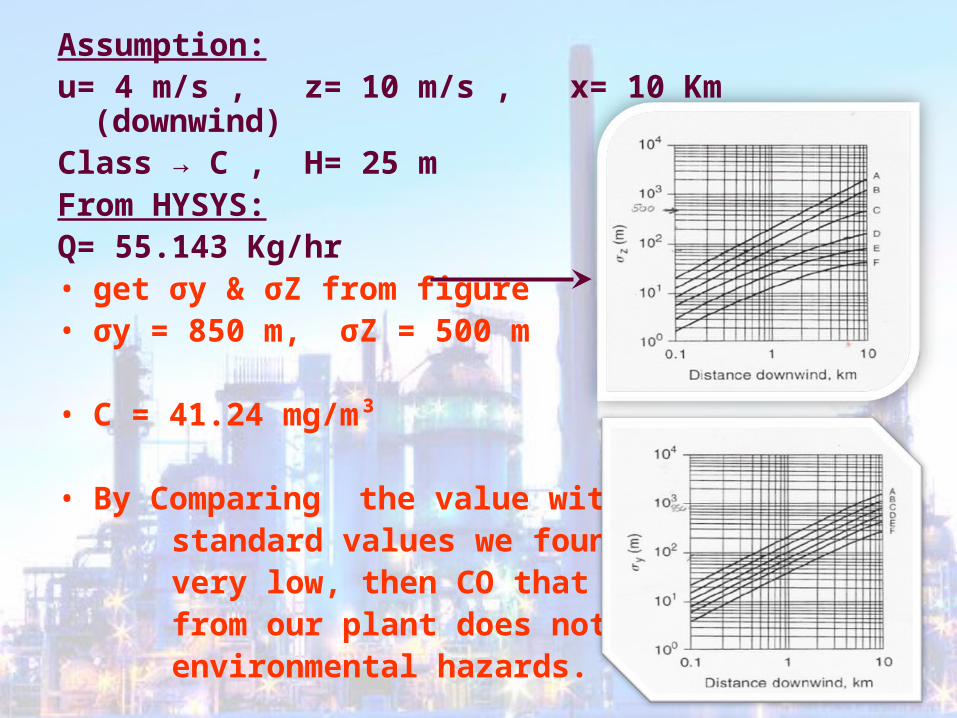

• We study the chance that we have a harmful emission of CO, we found the concentration of CO was 41.24 mg/m³.

• From Gaussian Dispersion Model:

C = Q/(2πσyσZ u)*[ exp(-(z-H)²/2 σZ²)+exp(-(z+H) ²/ 2 σz ²)]

Assumption:u= 4 m/s , z= 10 m/s , x= 10 Km (downwind)Class → C , H= 25 mFrom HYSYS:Q= 55.143 Kg/hr• get σy & σZ from figure • σy = 850 m, σZ = 500 m

• C = 41.24 mg/m³

• By Comparing the value with EPA standard values we found it’s very low, then CO that product from our plant does not cause environmental hazards.

• 2- In stream 12, Gaseous, CO2 Purge stream which discharge to the atmosphere.

• 3- In stream 24, Aqueous, Condensate purge from the

cooled syngas stream. Traces of dissolved H2, with CH4, CO and CO2 send to waste water treatment.

• 4- In absorber [C-101] a zinc oxide system is environmentally desirable. Thus, no H2S is discharge to the atmosphere and the spent zinc oxide adsorbent is returned to the supplier to carry out the regeneration offsite.

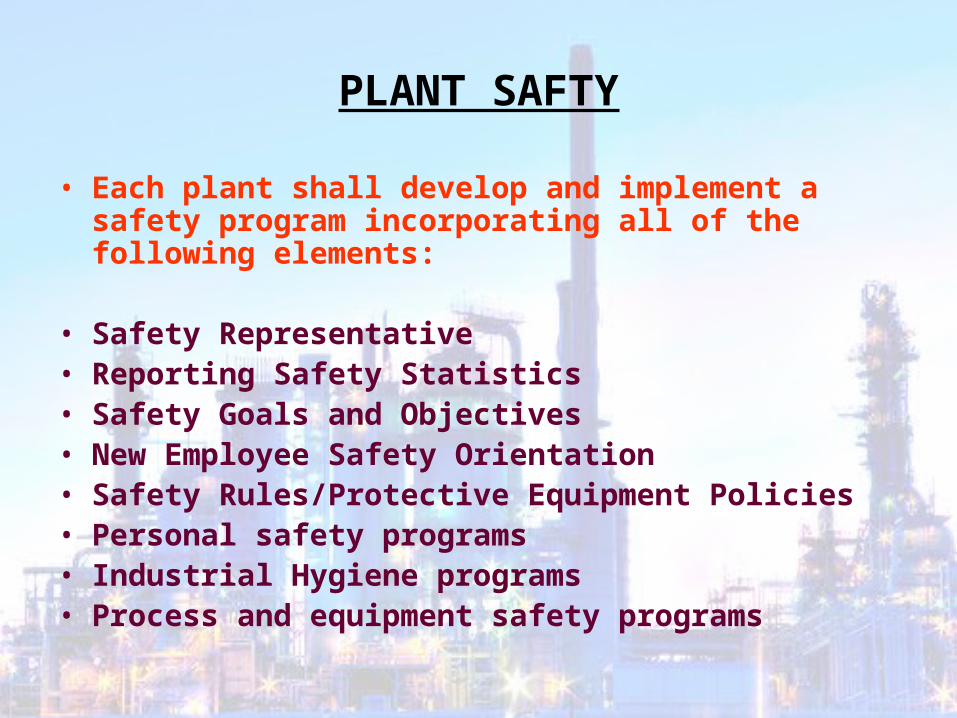

PLANT SAFTY

• Each plant shall develop and implement a safety program incorporating all of the following elements:

• Safety Representative• Reporting Safety Statistics• Safety Goals and Objectives • New Employee Safety Orientation• Safety Rules/Protective Equipment Policies • Personal safety programs • Industrial Hygiene programs • Process and equipment safety programs

What is HAZOP?

A Hazard and Operability (HAZOP) study is a structured and systematic examination of a planned or existing process or operation in order to identify and evaluate problems that may represent risks to personnel or equipment, or prevent efficient operation.

When to perform a HAZOP?

The HAZOP is usually carried out as a final check when the detailed design has been completed.

The following information should be available When study HAZOP:

•Process flow diagrams.

•Piping and instrumentation diagrams (P&IDs).

•Layout diagrams.

•Material safety data sheets.

•Provisional operating instructions.

•Heat and material balances.

•Equipment data sheets

Worksheet entriesWorksheet entries

Guide Word:

No flow – More of – Less of – Part of – As well as –

other than - Reverse.…

1.Deviation

2 .Cause

3 .Consequence

4. Action

Our process : E-101 Heat Exchanger

Intention: To provide feed to tubular reactor at 538˚C

Guide Word

DeviationCauseConsequenceAction

NoNo flow

(stream 4)Blockage in line

Fluid in E-101 overheats

Consider an interlock on fuel gas flow

NoNo flow

Out put StreamHeat tubes burstExplosion

Interlock with sudden pressure drop alarm

and shutdown

More ofMore flow in

(stream 4)Surge of K-103Unstable operationAlarm

More ofHigher pressureDown stream blockageTube failurePressure relief system

on tubes

Loss ofLess pressure in

tubesBurst pipe down stream

Explosion and toxic release

Alarm on low pressure or low flow

Other thanImpurities in Out

put StreamImpurities in feed or overheating in tubes

Impurities in product and/or catalyst

deactivation

Monitor E-101 temperatures

Part ofLow CO2 in

Stream 4K-103 not working

CO:H2 ratio off to R-101

Maintain spare compressor K-101

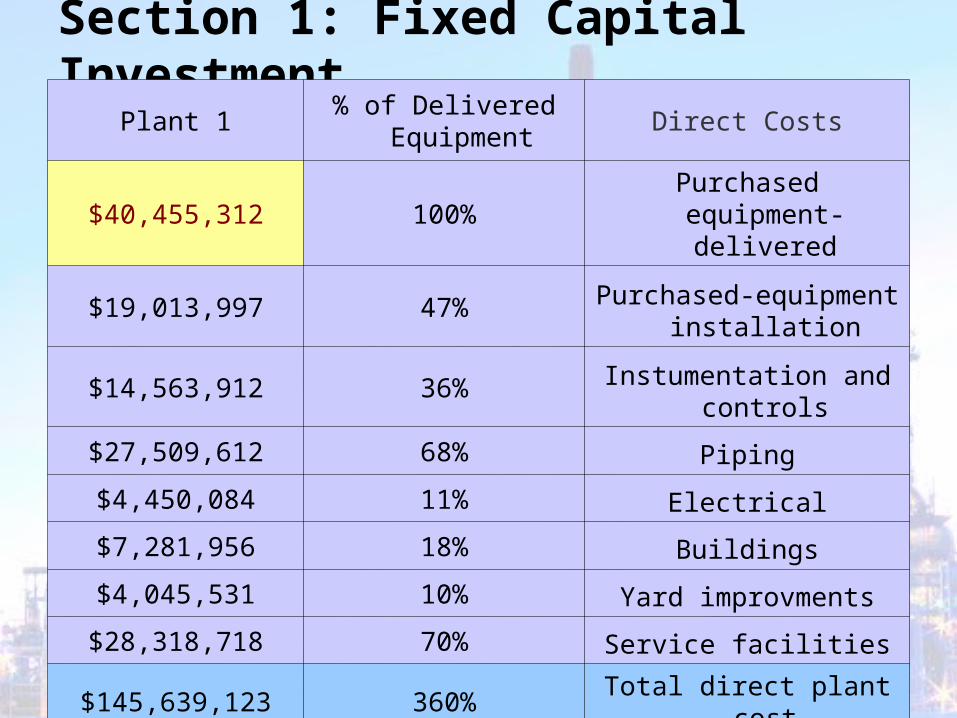

Section 1: Fixed Capital Investment

Direct Costs% of Delivered

EquipmentPlant 1

Purchased equipment-delivered

100%$40,455,312

Purchased-equipment installation

47%$19,013,997

Instumentation and controls

36%$14,563,912

Piping68%$27,509,612

Electrical11%$4,450,084

Buildings18%$7,281,956

Yard improvments10%$4,045,531

Service facilities70%$28,318,718

Total direct plant cost360%$145,639,123

Indirect Costs

Engineering and supevision

33%$13,350,253

Construction expenses

41%$16,586,678

Legal Expences4%$1,618,212

Contractor's fee22%$8,900,169

Contingency44%$17,800,337

Total Indirect Plant Cost

144%$58,255,649

Fixed capital investment

504%$203,894,772

Working capital89%$36,005,228

Total capital investment

593%$239,900,000

Total Fixed Capital Investment for Plant

$239,900,000

Total product cost

IManufacturing cost = Direct production cost + Fixed charges + Plant overhead costs

$84,761,420

ADirect production costs (about 36.5% of total product cost)

$67,807,000

1Raw materials (11% of the total product cost) $20,418,200

2Operating labor (5% of the total product cost) $9,281,000

3Direct supervisory and clerical labor (10% of operating labor)

$928,100

4Utilities (10% of total product cost) $18,562,000

5Maintenance and repairs (6% of fixed capital investment)

$14,394,000

6Operatint supplies (10% of cost of maintenance and repairs)

$1,439,400

7Laboratory charges (10% of operating labor) $928,100

8Patents and royalties (1% of total product cost)

$1,856,200

BFixed charges (2.1% of total product

cost) $3,961,020

1Depreciation (about 4% of fixed capital

investment and 2% of utlities)$1,330,840

2Insurance (0.4% of fixed capital

investment) $959,600

3Rent (9% of utilities) $1,670,580

CPlant overhead cost (7% of total

product cost) $12,993,400

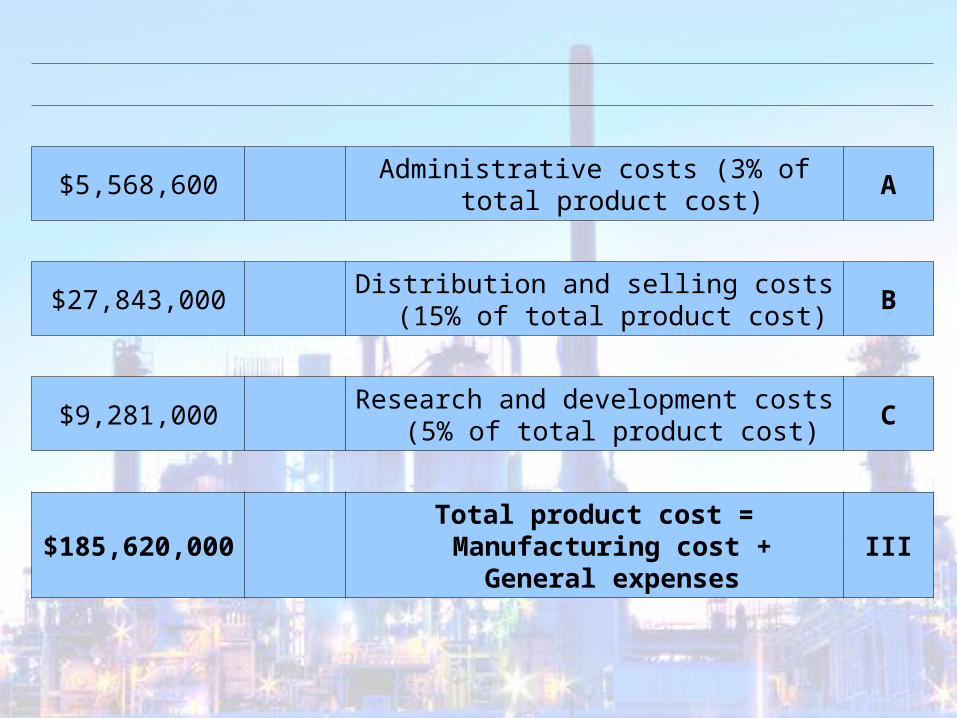

IIGeneral expenses = administrative costs +

distribution and selling costs + research and development costs

$42,692,600

AAdministrative costs (3% of total product

cost) $5,568,600

BDistribution and selling costs (15% of

total product cost) $27,843,000

CResearch and development costs (5%

of total product cost) $9,281,000

IIITotal product cost = Manufacturing

cost + General expenses $185,620,000

Pay Back Period

Fixed Capital Investment =

$239,900,000i = 15%

Total manufacturing cost =$185,620,000.00

Total Product Sales =$271,300,000

Life of Plant =20 yr

YearFixed Capital InvestmentTotal Manufacturing

CostTotal Product

SalesEnd of year

Balance

0$239,900,000$0$0-$239,900,000

1$0$185,620,000$271,300,000-$190,205,000

2$0$185,620,000$271,300,000-$133,055,750

3$0$185,620,000$271,300,000-$67,334,113

4$0$185,620,000$271,300,000$8,245,771

5$0$185,620,000$271,300,000$95,162,636

6$0$185,620,000$271,300,000$195,117,032

7$0$185,620,000$271,300,000$310,064,586

8$0$185,620,000$271,300,000$442,254,274

9$0$185,620,000$271,300,000$594,272,416

10$0$185,620,000$271,300,000$769,093,278

11$0$185,620,000$271,300,000$970,137,270

12$0$185,620,000$271,300,000$1,201,337,860

13$0$185,620,000$271,300,000$1,467,218,539

14$0$185,620,000$271,300,000$1,772,981,320

15$0$185,620,000$271,300,000$2,124,608,518

16$0$185,620,000$271,300,000$2,528,979,795

17$0$185,620,000$271,300,000$2,994,006,765

18$0$185,620,000$271,300,000$3,528,787,779

19$0$185,620,000$271,300,000$4,143,785,946

20$0$185,620,000$271,300,000$4,851,033,838

-$1,000,000,000

$0

$1,000,000,000

$2,000,000,000

$3,000,000,000

$4,000,000,000

$5,000,000,000

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Years

Payback Period

THANK YOU FOR LISTENING