salient features of gst - pajpbm · 2014-08-19 · 4 什么是销售税what is sales tax? •...

TRANSCRIPT

消费税的特征

SALIENT FEATURES

OF GST

1

2

3

4

简介 INTRODUCTION

了解消费税 WHAT IS GST?

消费税的模式PROPOSED MALAYSIAN GST MODEL

消费税注册 REGISTRATION FOR GST

讲座内容 Agenda

1

3

4

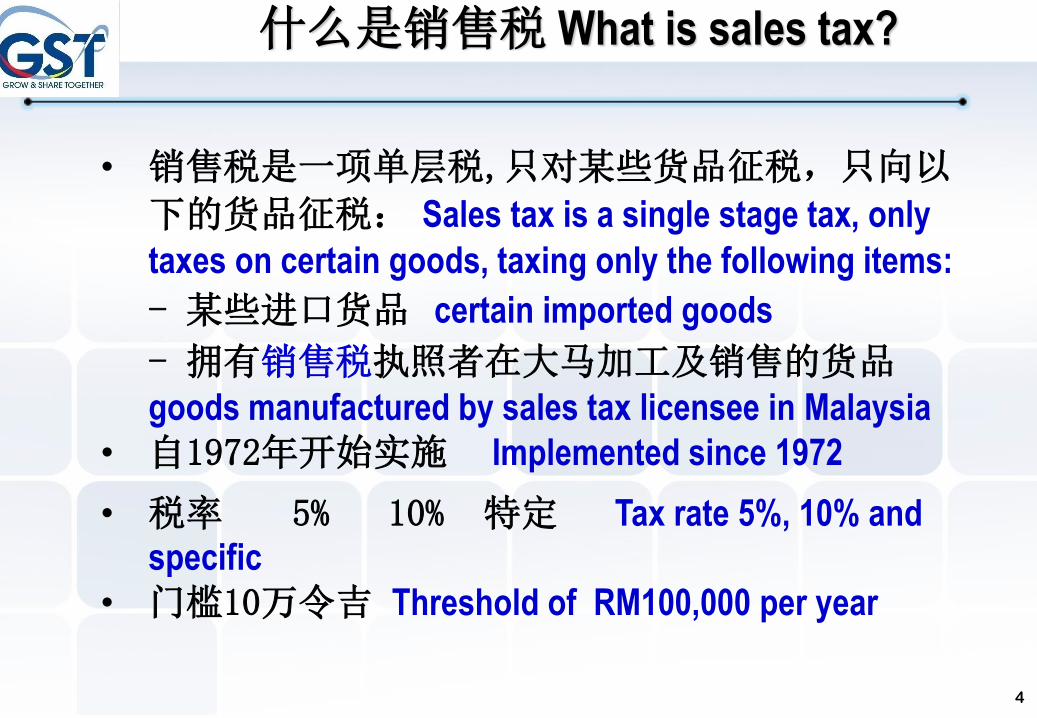

什么是销售税 What is sales tax?

• 销售税是一项单层税,只对某些货品征税,只向以

下的货品征税: Sales tax is a single stage tax, only

taxes on certain goods, taxing only the following items:

- 某些进口货品 certain imported goods

- 拥有销售税执照者在大马加工及销售的货品goods manufactured by sales tax licensee in Malaysia

• 自1972年开始实施 Implemented since 1972

• 税率 5% 10% 特定 Tax rate 5%, 10% and

specific

• 门槛10万令吉 Threshold of RM100,000 per year

消费者支付的货物价格中已含有销售税

element of sales tax embedded in

the price paid by consumer

征收销售税sales tax is collected at

the manufacturer level

什么是销售税 What is sales tax?

制造商

Manufacturer

批发商Wholesaler

零售商Retailer

消费者Consumer

5% 销售税货品例子Examples – Goods subject to 5% Sales Tax

7

10% 销售税货品例子Examples – Goods subject to 10% Sales Tax

8

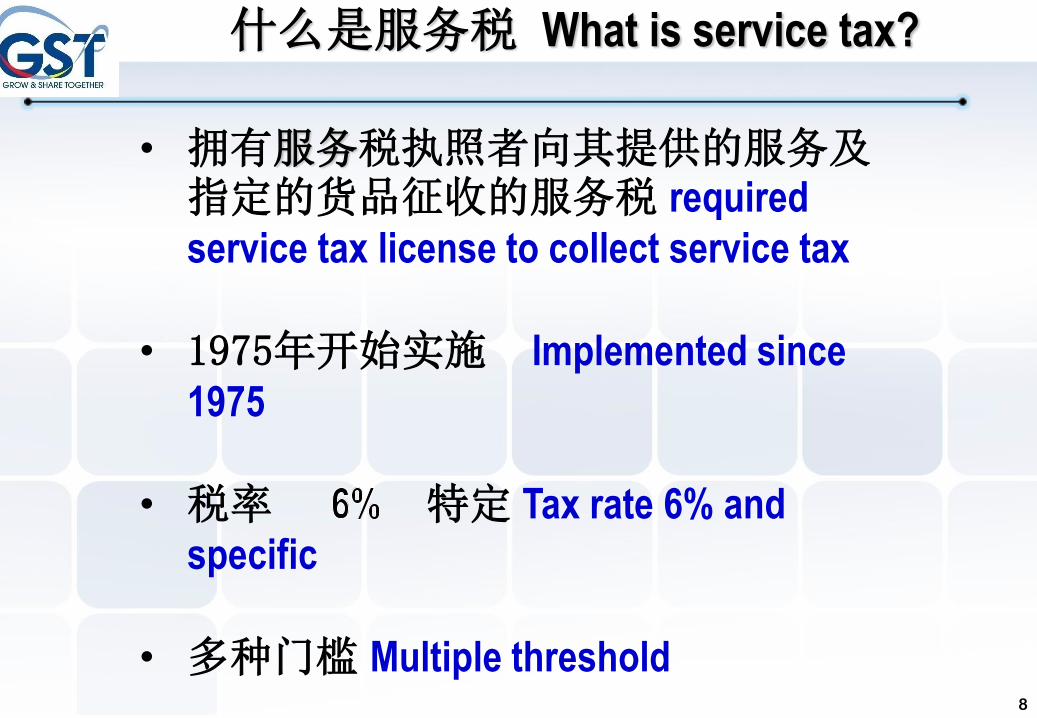

什么是服务税 What is service tax?

• 拥有服务税执照者向其提供的服务及指定的货品征收的服务税 required

service tax license to collect service tax

• 1975年开始实施 Implemented since

1975

• 税率 特定 Tax rate 6% and

specific

• 多种门槛 Multiple threshold

9

保安服务

Security Services

停车场

Parking Lots

专业服务Professional Services

维修中心

Car Service Centres

酒店 Hotel

6%

服务税例子Current Consumption Tax - Service Tax

餐馆 Restaurant

服务供应商Services provider

商业business

消费者consumer

服务提供予商业时

政府征税

服务提供予消费者时政府征税

消费者知道自己支付服务税

服务税6%

service tax

6% imposed

when

service

provided

什么是服务税 What is service tax?

11

制造商

Manufacturer

批发商Wholesaler

零售商Retailer

消费者Consumer

Cost RM 100

+ 10% tax

(RM10)

+ 20% Margin

(RM 22)RM110

Govt

collects:

Tax

RM10

Tax

Nil

RM132 + 30% Margin

(RM 39.60) RM171.60

Final price paid by

Consumer

Tax

Nil

RM10.00

Total tax

collected by

Govt

RM 5.60

Total tax loss/

uncollected

Businessmen

“free ride”

RM10 x 20%

= RM2.00

(10 + 2) x 30%

= RM3.60

RM10.00 *Tax ballooned to RM15.60

(10 + 2 + 3.60)

销售与服务税 SST is ineffective 双重征税 Compounding effect

Assume SST at 10%

12

Cost RM 100 + 20% Margin

on RM100 w/oTax

(RM 20)

RM100

Govt

collects:

Tax

RM 10

Tax

RM 2

RM120 + 30% Margin

on RM120 w/o Tax

(RM 36)

RM171.60

Tax

RM3.60

+ 10% tax

on RM20

(RM 2.00)

+ 10% tax

(RM10) RM10 RM12.00 + 10% tax

on RM36

(RM 3.60)

RM156

RM15.60Final price

paid by

Consumer

RM15.60

RM 0 (Zero)

Total tax loss/

uncollected

Total GST

collected

消费税是多层次的增值税 GST is an effective tax because it is

captured at every stage (Assume GST at 10%)

制造商

Manufacturer

批发商Wholesaler

零售商Retailer

消费者Consumer

13

Cost RM 100 + 20% Margin

on RM100 w/oTax

(RM 20)

RM100

Govt

collects:

Tax

RM 6

Tax

RM 1.20

RM120 + 30% Margin

on RM120 w/o Tax

(RM 36)

RM165.36

Tax

RM2.16

+ 6% tax

on RM20

(RM 1.20)

+ 6% tax

(RM6) RM6 RM7.20 + 6% tax

on RM36

(RM 2.16)

RM156

RM9.36Final price

paid by

Consumer

RM9.36

RM 0 (Zero)

Total tax loss/

uncollected

Total GST

collected

消费税是多层次的增值税 GST is an effective tax because

it is captured at every stage (GST at 6%)

制造商

Manufacturer

批发商Wholesaler

零售商Retailer

消费者Consumer

OCEANIANo. of countries = 7

Highest tax rate = 15%

Lowest tax rate = 5%

ASIANo. of countries = 19

Highest tax rate = 20%

Lowest tax rate = 5%

ASEANNo. of countries = 7

Highest tax rate = 12%

Lowest tax rate = 7%

AFRICANo. of countries = 44

Highest tax rate = 20%

Lowest tax rate = 5%

EUROPENo. of countries = 53

Highest tax rate = 27%

Lowest tax rate = 5%

SOUTH AMERICANo. of countries = 11

Highest tax rate = 22%

Lowest tax rate = 10%

CARIBBEAN, CENTRAL &

NORTH AMERICA

No. of countries = 19

Highest tax rate = 17.5%

Lowest tax rate = 5%

160个国家落实消费税160 countries implementing GST/VAT

2

15

消费税的基本原则 Basic principles of GST• 基于消费的增值税务 A consumption tax in the form of value added

tax→ each stage of business transaction up to the retail stage of distribution

• Also known as Value Added Tax (VAT)

• 商业进项税可获回扣 GST incurred on inputs is allowed as a credit to

the registrant→ offset against output tax

业务Business

进项税INPUT

销项税OUTPUT

Raw materials, rents,

electricity, furniture,

professional services

etc.

Goods

Services

索回进项税Claimed input tax

GST on inputs

= Input taxGST on output

= Output tax

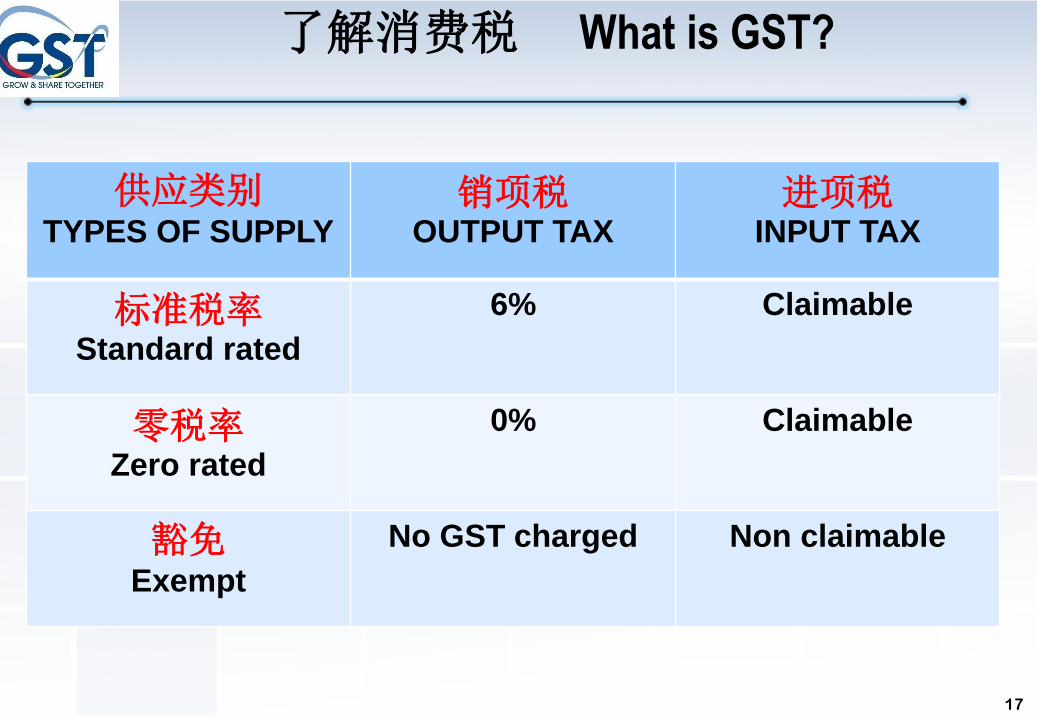

了解消费税 What is GST?

供应类别TYPES OF SUPPLY

销项税OUTPUT TAX

进项税INPUT TAX

标准税率Standard rated

6% Claimable

零税率Zero rated

0% Claimable

豁免Exempt

No GST charged Non claimable

17

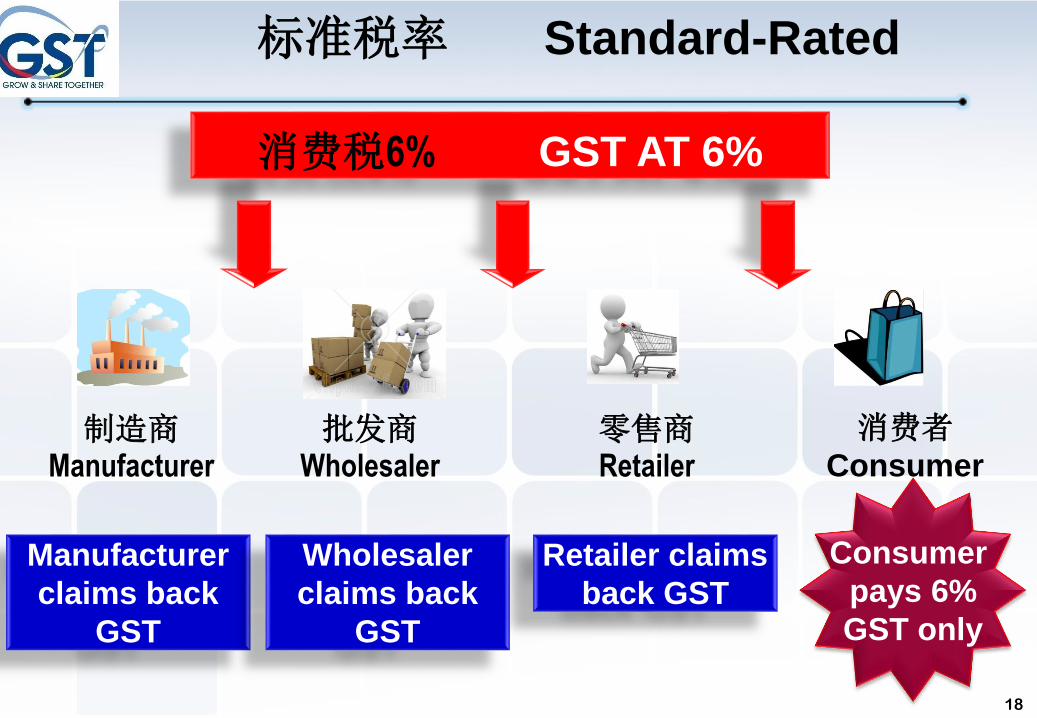

了解消费税 What is GST?

18

消费税6% GST AT 6%

制造商Manufacturer

批发商Wholesaler

零售商Retailer

消费者Consumer

Consumer

pays 6%

GST only

Manufacturer

claims back

GST

标准税率 Standard-Rated

Wholesaler

claims back

GST

Retailer claims

back GST

19

增值活动VALUE ADDED

ACTIVITY

供应链Supply

Chain

Purchase cost : RM100

GST* 6% : RM6

Purchase Price : RM106

*Note : claim input tax

Selling price : RM125

GST* 6% : RM7.50

Total selling price: RM132.50Added value : RM25

(Add GST : RM1.50)

标准税率 Standard-Rated

制造商Manufacturer

批发商Wholesaler

零售商Retailer

消费者Consumer

20

GST AT 0%

Consumer

does not pay

any GST

Manufacturer

claims back

GST

Wholesaler

claims back

GST

Retailer

claims back

GST

零税率 Zero-Rated

制造商Manufacturer

批发商Wholesaler

零售商Retailer

消费者Consumer

21

Purchase cost : RM100

GST* 0%

Purchase Price : RM100

*Note : claim input tax

Selling price : RM125

GST* 0% : RM0

Total selling price: RM125Added value : RM25

零税率 Zero-Rated

供应链Supply

Chain

增值活动VALUE ADDED

ACTIVITY

制造商Manufacturer

批发商Wholesaler

零售商Retailer

消费者Consumer

22

GST 6%

Private hospital

cannot claim GST on

inputs

NO GST

供应商Medical supplier

私人医院private hospital

消费者consumer

Private Hospital

does not charge

GST – consumer does

not pay any GST

Supplier claims tax

paid on inputs

豁免 Exempt

3

23

2424

范围及推行 Scope and charged

• 消费税施于: GST is charged on:

须征税货品和服务 the taxable supply of goods and services

须缴税人执行 made by a taxable person

正在进行或继续营业的公司 in the course or furtherance of

business

在马来西亚 in Malaysia

• 进口货品或服务将征收消费税 注册消费税 GST is charged on the imported goods/services

• 必须注册者 (征税营业额> RM500K) Mandatory register (taxable turnover> RM500K)

• 自愿注册者 (征税营业额< RM500K) Voluntary registrant (taxable turnover <RM500K)

消费税的模式PROPOSED MALAYSIAN GST MODEL

25

Sales Tax &

Service Tax (SST)

Goods and Services

Tax (GST)

5%, 6%, 10% & specific rate

Various threshold

Rate = 6 %

Threshold = RM500,000

• To replace current tax system2015年4月1日消费税(GST)6 %将取代现有的销售税与服务税

• GST is charged on goods and services that

are 消费税的范围

supplied in Malaysia大马供应货物和服务的税务

imported into Malaysia进口的货物和服务均需支付消费税

消费税的模式PROPOSED MALAYSIAN GST MODEL

BRIEFING AGENDA

零税率

26

首300單位家庭電供300 units a month-domestic use

出口货物服务exported goods and services

–

家庭自來水供應water domestic use only

婴儿奶粉infant milk 谷米

rice

糖sugar

食油cooking oil

海鲜及鱼类seafood and fish

蛋eggs

青菜vegetable

家畜/产品肉类raw meat

零税率 Zero-Rated

27

Rail Transporation Bus/Taxi/Hire Car Water Transportation

Toll Highway Residential Property Land for Agriculture

& General Use

Financial ServicesEducation

GST

Health

豁免 Exempt

28

Standard Rate

标准税率 Standard-Rated

29

不在征税范围Out of Scope

提供的服务供应All supplies by Federal &

State government

提供的服务供应Supplies made in the regulatory

and enforcement (R&E) functions

eg. Assessment rate collection, issuance

of licenses, penalty

有消费税Subject to

GST

Supplies that have been

directed by Minister in the

GST (Government Taxable

Supply) Order

eg. Supply made by RTM, Prison

Department

业务活动Non R&E functions

ie. Business activities for example rental

facilities and etc.

中央政府、州政府Federal &

State Government

地方市政局/市议会Local Authority &

Statutory Body

消费税的模式-政府服务PROPOSED MALAYSIAN GST MODEL-Supply by Government

4

30

31www.gst.customs.gov.my

消费税注册 Registration in GST

Common error: Please don’t key in www

32

消费税注册 Registration in GST

10 user-friendly screens

1

33

消费税注册 Registration in GST

2

34

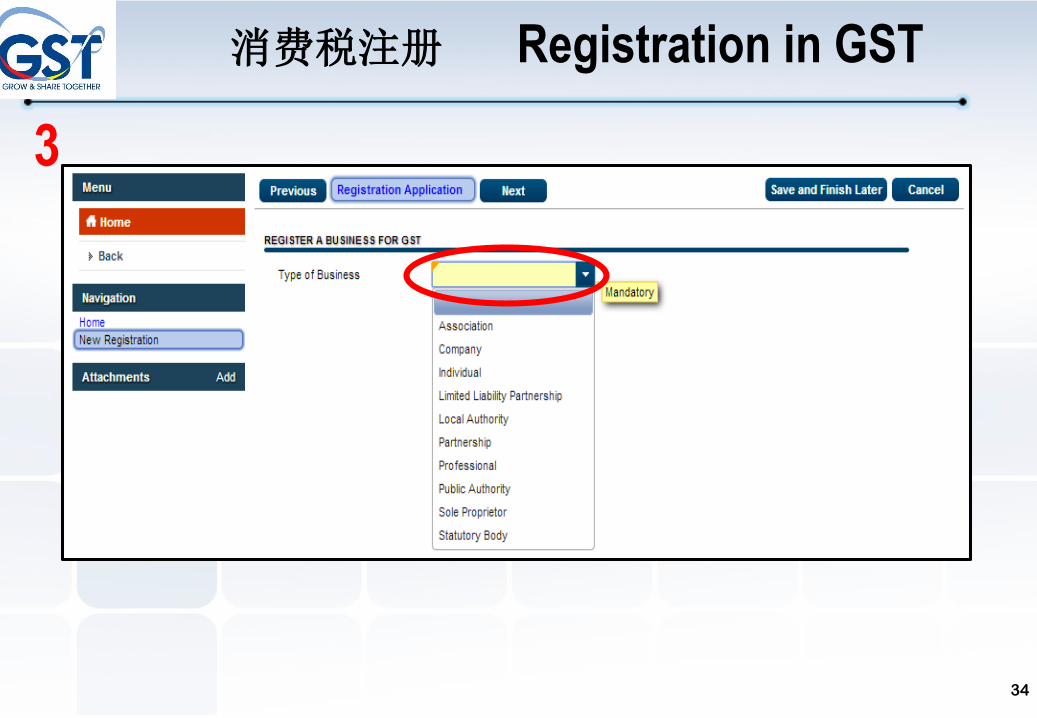

消费税注册 Registration in GST

3

35

消费税注册 Registration in GST

yellow text boxes indicate

mandatory fields

green text boxes indicate

optional fields

The Country defaults to

MALAYSIA”. white box means

taxpayers cannot change this

value.

The state and city details are automatically

filled in when a zip code is entered. It is

possible for multiple states/cities to share the

same zip code. In this case, the taxpayer will

be given the option to choose from a list of

states/cities when applicable

3

36

消费税注册 Registration in GST

4

37

消费税注册 Registration in GST

5

38

消费税注册 Registration in GST

Refer Business Code of LHDN Form C, Part A

OR

http://msic.stats.gov.my

6

39

消费税注册 Registration in GST

7

40

消费税注册 Registration in GST

8

41

消费税注册 Registration in GST

9

42

消费税注册 Registration in GST

10

43

Sekian,

Terima Kasih

谢谢

44

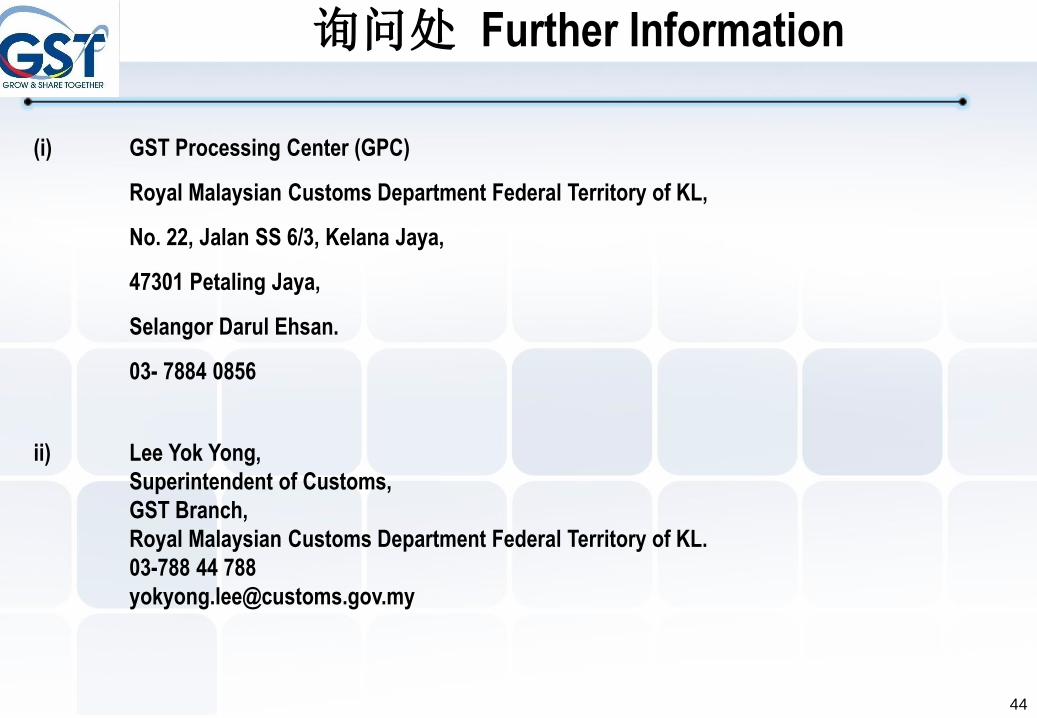

(i) GST Processing Center (GPC)

Royal Malaysian Customs Department Federal Territory of KL,

No. 22, Jalan SS 6/3, Kelana Jaya,

47301 Petaling Jaya,

Selangor Darul Ehsan.

03- 7884 0856

ii) Lee Yok Yong,

Superintendent of Customs,

GST Branch,

Royal Malaysian Customs Department Federal Territory of KL.

03-788 44 788

询问处 Further Information