sameer jain chief economist & managing director [email protected] (646) 861-7726 sameer jain...

TRANSCRIPT

Sameer JainChief Economist & Managing [email protected](646) 861-7726

The Case for Durable Income

REISA USE ONLY. Session 12. 6/10/2013

• Macro Economic Conditions & Investor Sentiment• The Challenge of Fixed Income• Traditional Fixed Income is No Longer Durable Income• Durable Income Improves Traditional Fixed Income Investing• Real Assets - a Source of Durable Income• Appendix – Examples of Durable Income Characteristics of Real Assets

– Private Real Estate– Energy– Timberland– Farmland– Infrastructure

2

Table of Contents

• Abundant liquidity, low interest rates, accommodative monetary stance to keep traditional fixed income returns low

• Market volatility on account of sequester, political impasse, barriers to debt ceiling resolution to create periodic re-pricing shocks and raise risk aversion

• Reduced risk appetite expressed through preference for holding shorter duration assets, higher illiquidity premium and pursuit of interest rate neutral strategies

• Deleveraging in financial, household, corporate sectors well underway. Government deleveraging trajectory remains unclear

• Outperforming efficient traditional fixed income markets without taking excessive credit and interest rate risks increasingly difficult

• Investing risks from spread, interest rate and credit widening and unexpected inflation to continue to rise for next few years

• Investors searching for elusive higher yield, durable fixed income, inflation hedge, less correlated assets, capital growth with lower risk

• Stable consistent income from real assets a viable alternative to traditional fixed income in inevitable rising rate environment

3

Macro Economic Conditions & Investor Sentiment

4

Characteristics of a ‘Perfectly’ Diversified* Fixed Income Portfolio

•Low absolute returns: 40 basis point premium relative to risk free rate for last ten years•No capital appreciation: Returns from only interest income (i.e. driven by interest rates) . No returns from good buy and sell market timing and security selection decisions

•Low risk adjusted returns: Sharpe ratio of just 0.1. Investors not getting compensated for the risks that they take.

•No illiquidity premium

•Significant interest rate risk: For every 1% increase in short term interest rates, the index declines by almost 4.48%•Excludes niche opportunities in credit investing. Excludes bonds with equity-type features , private placements, floating-rate issues, structured notes, as well as illiquid securities with no available internal or third-party price source

* Barclays Capital U.S. Aggregate Bond Index. August’03- August’13

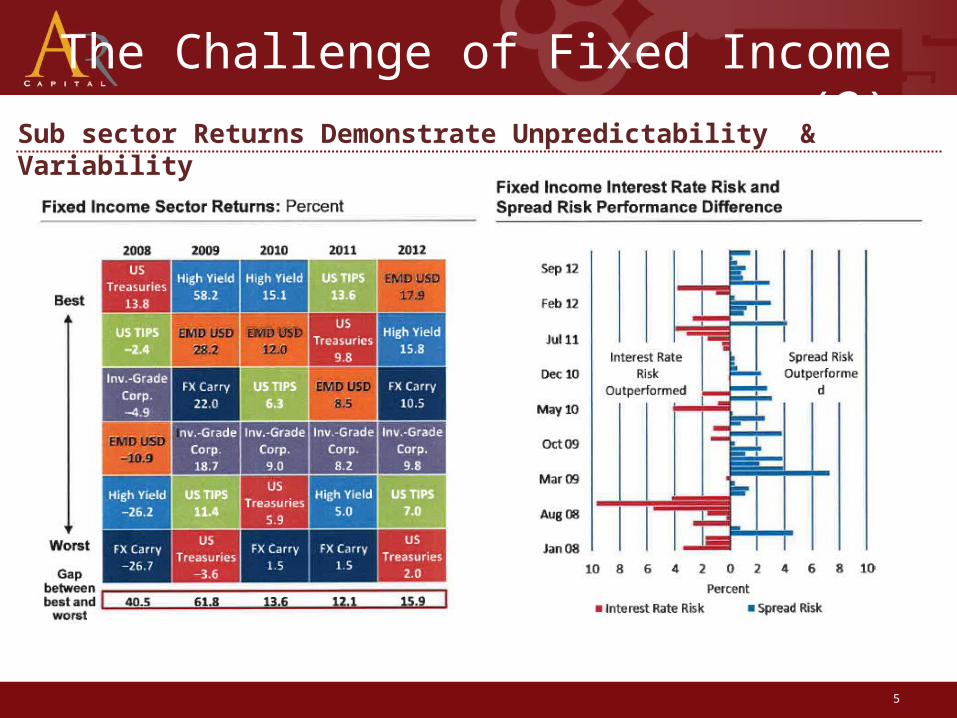

The Challenge of Fixed Income (1)

5

Sub sector Returns Demonstrate Unpredictability & Variability

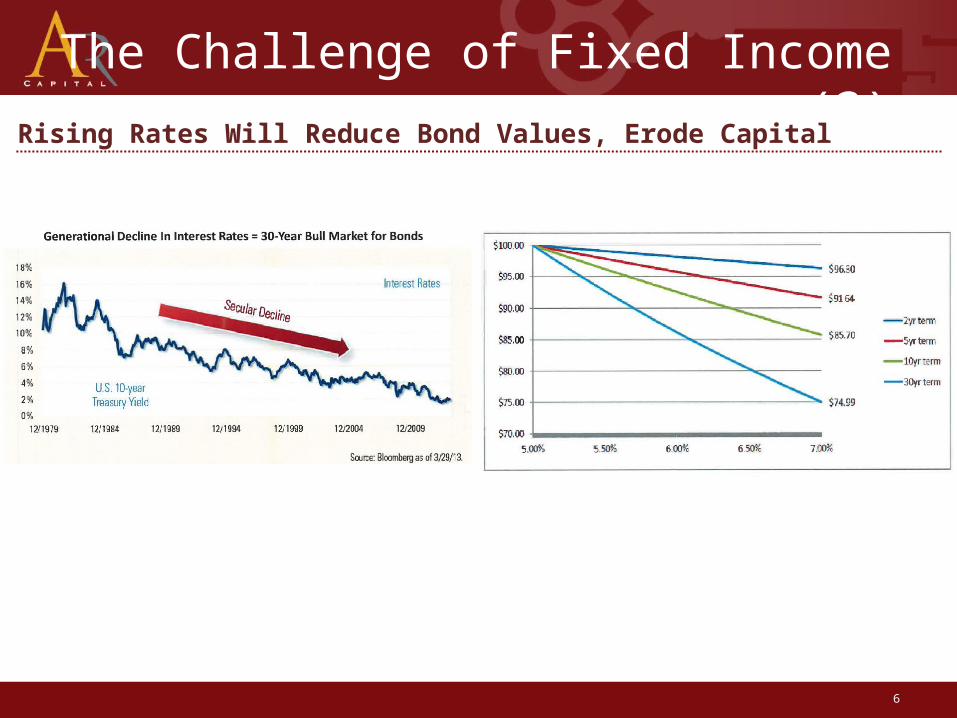

The Challenge of Fixed Income (2)

6

The Challenge of Fixed Income (3)

Rising Rates Will Reduce Bond Values, Erode Capital

7

Short Duration Bonds

FloatingRateSecurity

Diversified Bond Funds

MortgageBackedSecurities

Bank Loans Municipal Bonds

Emerging Market Debt

High Yield

Low sensitivity to interest rates

Coupons reset with increasing interest rates

Professional management and broad diversification

Securitization reduces risks

Stable coupons tied to rising interest rates

Interest income exempt from Fed tax

Multiple drivers of return

Higher returns

Low yield does not meet income objective

Part of High Yield universe

Interim price fluctuations

Opaque underlying mortgage character

Buyer –Seller mismatch during stress periods

Deteriorating financial and local economy conditions

Sensitive to volatility and segment illiquidity

Sensitive to interest rate changes

Credit risk widening

Reduced interest rate risk but does not insulate credit risk

Maturing bonds forcibly liquidated at different dates

High loss severity in challenged properties

Downward pricing pressures, swings and capital loss

Less information transparency in govt. finances

Valuation, fundamental, momentum factors difficult to forecast

Sensitive to credit quality changes

Active management creates little value add after fees

NAV fluctuates daily as driven by changing prices, not value

Convexity, prepayment, extension and model complexity

Market volatility affects funding costs and access

Have experienced significant NAV declines

Challenging growth conditions from developed market spillovers

Borrowing rate increase may diminish liquidity and reduce prices

Fixed Income Subtypes Now Have Increased Embedded Risk

The Challenge of Fixed Income (4)

8 2

Allocation to traditional Fixed Income alone may no longer satisfy long-term investment and income needs

• Low expected returns• No capital appreciation• Low risk adjusted returns• No illiquidity premium• Excludes niches in non traditional credit investing

These problems are exacerbated by Fixed Income’s vulnerability to

• Interest rate risk • Credit spread widening• Unexpected inflation

Summary: Perils of Fixed Income Investing

9 2

Durable Income is product agnostic investing framework with dominant characteristics, including…..

• Generates periodic, stable cash flows• Low volatility• Low correlation to other asset classes• Asset value growth potential• Active management/ skills based returns• Mid to long term investment horizon• Variable liquidity• Inflation hedge• Agnostic to underlying instruments and markets

• May include real assets, natural resource partnerships, oil & gas, infrastructure, timber, real estate

Traditional Fixed Income No Longer Meets Durable Income Criteria

10 2

Durable Income preserves fixed income’s attractive features while mitigating its attendant risks

• Provides steady income and capital appreciation to create higher absolute returns

• Reduces volatility to create higher risk adjusted returns

• Add greater stability to traditionally-constructed portfolios

• Provides long term resilience through reliance on multiple drivers of return

Durable Income Investing Improves Traditional Fixed Income Investing

The more the sources of return, the lesser the dependence on a particular market factor, and the more resilient the investment thesis.

11 2

Reliance on multiple drivers of return

Durable Income is About More Resilient Investing

12 2

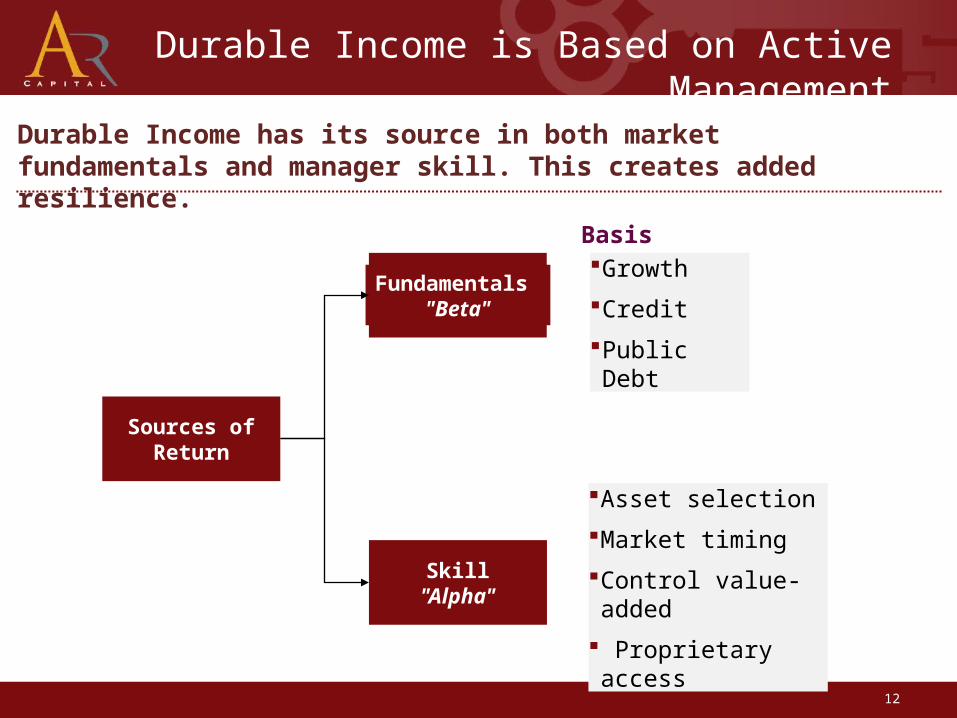

Durable Income has its source in both market fundamentals and manager skill. This creates added resilience.

Sources ofReturn

Fundamentals "Beta"

Skill"Alpha"

Growth

Credit

Public Debt

Basis

Asset selection

Market timing

Control value-added

Proprietary access

Durable Income is Based on Active Management

13 2

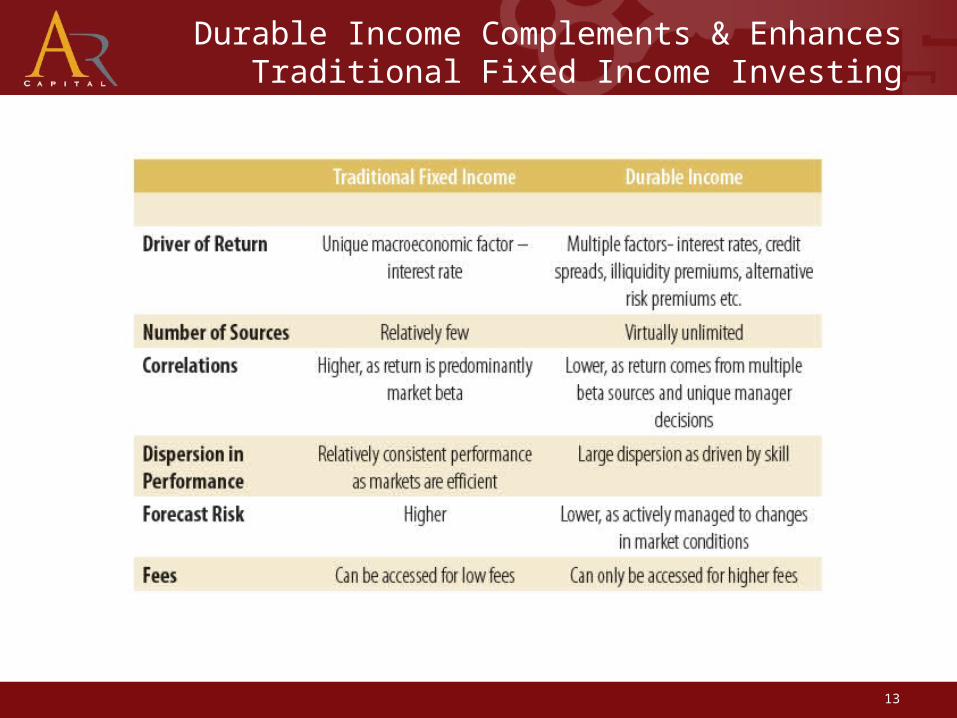

Durable Income Complements & Enhances Traditional Fixed Income Investing

14 2

Durable Income is accretive to Fixed Income portfolios to both meet ongoing income needs as well as match long dated future liabilities.

• Traditional fixed income exposes investors to low returns, unexpected inflation and new risks from interest rate and credit spread widening

• Durable Income has multiple return drivers which provides for resilience

• Durable Income preserves attractive features of fixed income while mitigating its risks. It complements and augments

• Durable income is a product agnostic philosophy and a framework

• Real Assets are a potential source of Durable Income

Durable Income Summary

15

Real assets are generally characterized by high barriers to entry, essential services, relatively inelastic demand, large investment scale, and long duration cash flows

Portfolio benefits include:

• The ability to earn attractive risk-adjusted returns relative to other asset classes

• Low correlation to traditional financial investments, and low correlation between real assets sectors

• Enhanced portfolio diversification and reduced portfolio risk

• Capital preservation

• Current income for investors in advance of capital appreciation

• Inflation hedge

Oil & Gas - Real Estate – Timberland – Farmland - Infrastructure

Real Assets Are a Potential Source of Durable Income

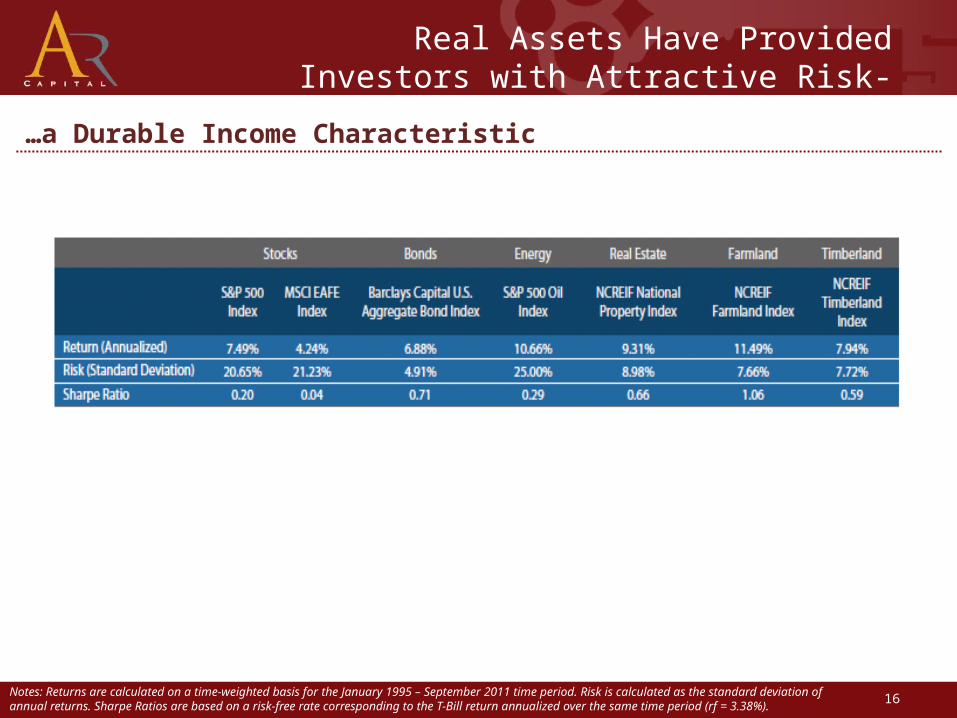

…a Durable Income Characteristic

16Notes: Returns are calculated on a time-weighted basis for the January 1995 – September 2011 time period. Risk is calculated as the standard deviation of annual returns. Sharpe Ratios are based on a risk-free rate corresponding to the T-Bill return annualized over the same time period (rf = 3.38%).

Real Assets Have Provided Investors with Attractive Risk-Adjusted Returns

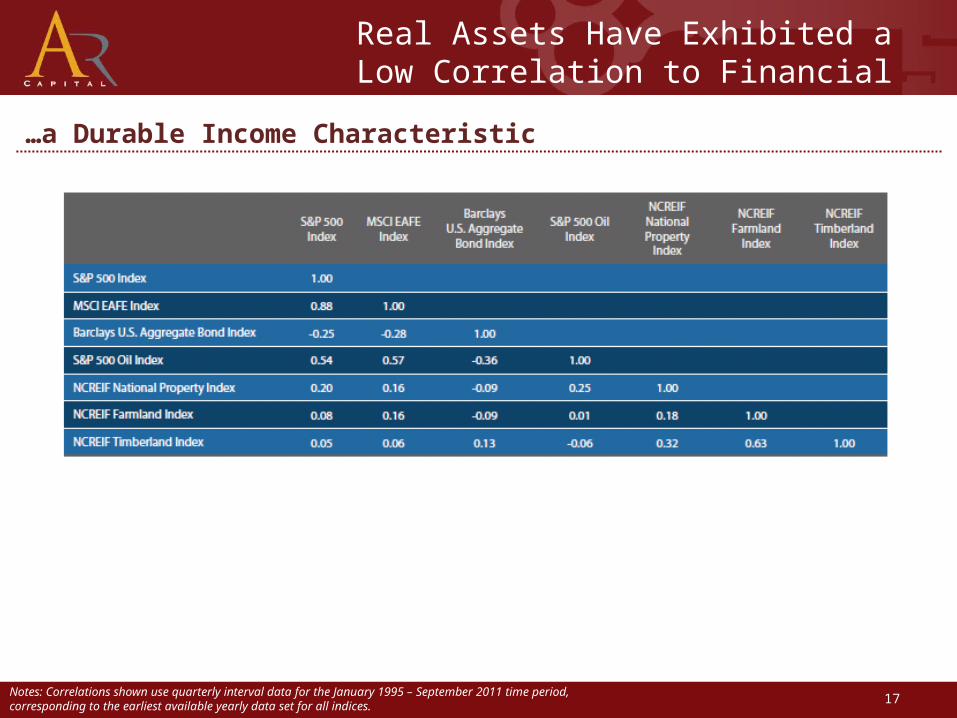

17Notes: Correlations shown use quarterly interval data for the January 1995 – September 2011 time period, corresponding to the earliest available yearly data set for all indices.

Real Assets Have Exhibited a Low Correlation to Financial Assets

…a Durable Income Characteristic

18

Notes: Efficient frontiers constructed based on data spanning the January 1995 – September 2011 time period. Portfolios diversified with Real Assets represent constant allocations of 7% to S&P 500 Oil Index, 7% to NCREIF Townsend Value Added Index, 2% to NCREIF Farmland Index and 4% NCREIF Timberland Index. Highlighted diversified portfolio represents allocations of 50% to S&P 500 and 30% to Barclays U.S. Aggregate Bond Index. Traditional 60/40 portfolio represents allocations of 60% to S&P 500 and 40% to Barclays U.S. Aggregate Bond Index. Sharpe Ratios are based on a risk-free rate corresponding to the T-Bill return annualized over the same time period (rf = 3.38%).

Real Assets Have Provided Investors with Enhanced Portfolio Diversification

…a Durable Income Characteristic

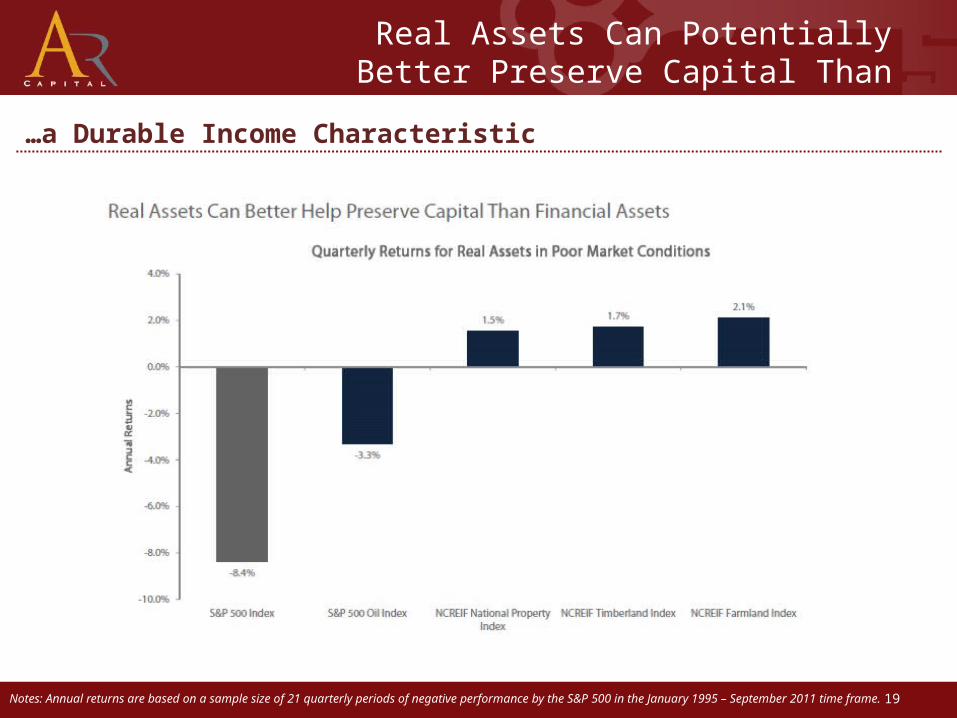

19Notes: Annual returns are based on a sample size of 21 quarterly periods of negative performance by the S&P 500 in the January 1995 – September 2011 time frame.

Real Assets Can Potentially Better Preserve Capital Than Financial Assets

…a Durable Income Characteristic

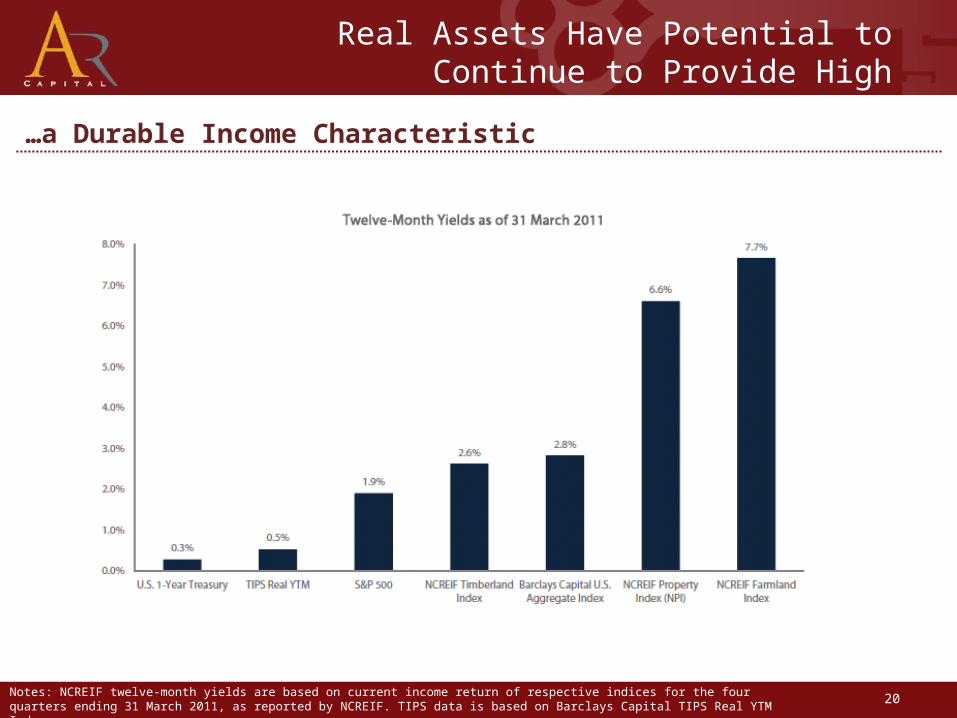

20Notes: NCREIF twelve-month yields are based on current income return of respective indices for the four quarters ending 31 March 2011, as reported by NCREIF. TIPS data is based on Barclays Capital TIPS Real YTM Index.

Real Assets Have Potential to Continue to Provide High Current Income

…a Durable Income Characteristic

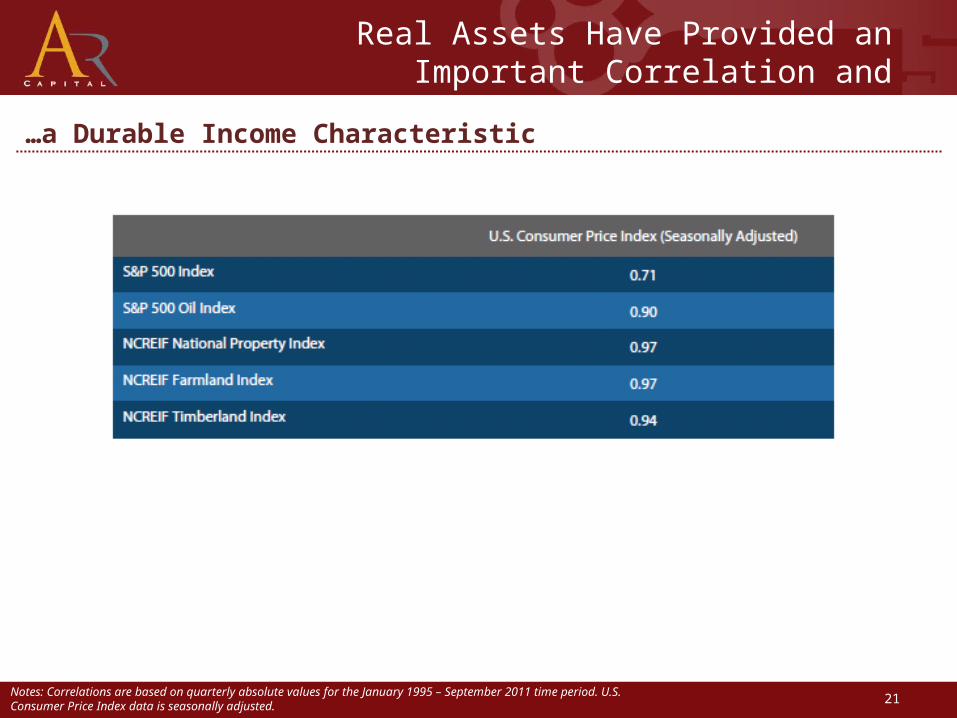

21Notes: Correlations are based on quarterly absolute values for the January 1995 – September 2011 time period. U.S. Consumer Price Index data is seasonally adjusted.

Real Assets Have Provided an Important Correlation and Hedge to Inflation

…a Durable Income Characteristic

22

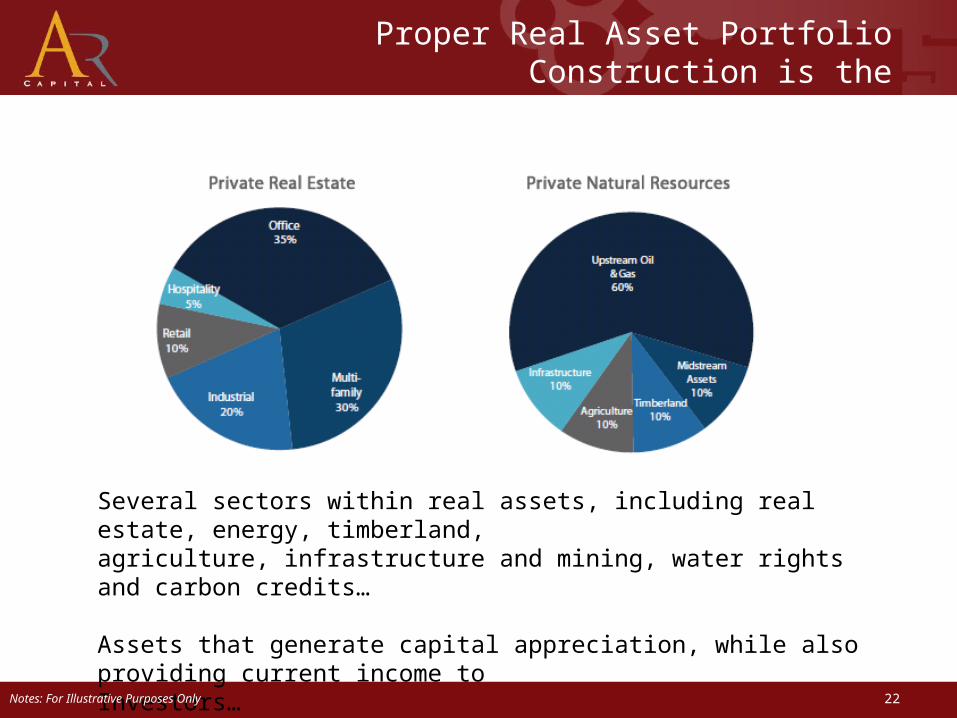

Several sectors within real assets, including real estate, energy, timberland,agriculture, infrastructure and mining, water rights and carbon credits…

Assets that generate capital appreciation, while also providing current income toInvestors…

Notes: For Illustrative Purposes Only

Proper Real Asset Portfolio Construction is the Foundation for Durable Income

Private Real Estate Energy Timberland Farmland Infrastructure

23

Appendix

Examples of Durable Income Characteristics of Real Assets

24

Risks and Disclosures