sample chapter tax and family business succession planning,

TRANSCRIPT

Sample Chapter Tax and Family Business Succession Planning, 3rd Edition

Chapter 10: Spinouts

Sample Chapter

Tax and Family Business Succession Planning, 3rd Edition

Chapter 10: Spinouts

The attached sample chapter, which is a work in progress, has been

prepared to illustrate the general form and content of the forthcoming volume,

Tax and Family Business Succession Planning, 3rd Edition. The contents of

the chapter may be subject to change, and may contain grammatical or other

editorial errors or omissions. In any event, it does not purport and is not

intended to be advice on any particular matter. The authors do not accept any

responsibility or liability to any person in respect of anything done or omitted

to be done by any such person in reliance, sole or partial, on the whole or any

part of the contents of this sample. This sample is made available solely for

evaluation purposes.

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 1 Free lead: 260D Next lead: 565D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Chapter 10

¶1000 Spinouts

CONTENTSParagraph

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶1001

General Example of Spinout Transaction . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶1002

Subsection 55(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶1003

Significant Exceptions to Subsection 55(2) . . . . . . . . . . . . . . . . . . . . . . . . . ¶1004

Purifications and Asset Protection Spinouts . . . . . . . . . . . . . . . . . . . . . . . . ¶1005

Series of Transactions or Events . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶1006

Case Law — Series of Transactions/Transactions in

Contemplation of Series . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶1007

U.K. Case Law . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶1008

Canadian Case Law . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶1009

Spinouts to Family Members . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶1010

Paragraph 55(3)(a) and Related Provisions . . . . . . . . . . . . . . . . . . . . . . . . . ¶1011

Examples of Spinouts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶1012

Example 3: Spinout to Family Trust . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶1013

Example 4: Spinout to Children . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶1014

Series of Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶1015

¶1001 Introduction

At various points during the life of a business and a succession plan, itwill be advisable to effect a divisive reorganization whereby the assets of acorporation are spun out into sister corporations or to a holding company. A

413 ¶1001

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 2 Free lead: 83D Next lead: 125D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

414 Tax and Family Business Succession Planning

spinout transaction contemplates the division of a corporation’s assetsamong its shareholders in a series of tax-deferred transfers.

Within the context of succession planning, some of the reasons for sucha spinout are as follows:

(a) Asset Protection. To enhance the protection of particular assetsfrom creditor claims. For example, if real estate or other valuableinvestment assets are held in the same corporation as businessoperations subject to potential creditor risk , it may be advisable tospin these out to a separate sister corporation.

(b) Spinout to Certain Family Members. To divide up the corporation’sassets, e.g., so that specif ic assets will be held by a particular familymember. As will be seen later in the Chapter, this can be diff icult toachieve, short of a true proportional butter f ly. Alternatively, a spi-nout reorganization might be used, for example, to cash-outFreezor so that the children can operate the business.

(c) Small Business Corporation Status. In order to maintain status as asmall business corporation. This status is essential in order toutilize a number of provisions under the Act, including the capitalgains exemption. (For further discussion, reference should be madeto ¶1005.)

(d) Wholesale Division. To split the frozen corporation amongst thechildren, for example, after the death of the Freezor. Unfortunately,one instance in which this may be advisable is if the succession planhas not worked and there are various assets which the children nowwish to split-up amongst themselves and go their separate ways.

A spinout reorganization might also be effected prior to a sale to a thirdparty, e.g., to remove assets not to be sold and/or to ensure that the corpora-tion’s shares qualif y for the capital gains exemption. For some examples ofspinouts in this context, reference should be made to ¶1012.

¶1002 General Example of Spinout Transaction

The objective of a butter f ly-type transaction is to separate the interestsof shareholders and in effect demerge the corporation. For example, anoperating corporation with a number of businesses or properties might beowned by two holding companies, with equal shareholdings, that wish to

¶1002

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 3 Free lead: 626D Next lead: 0D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Ch. 10/Spinouts 415

separate their interests. The operating corporation might wind up and dis-tribute one-half of its assets to each holding company, which would thencontinue as independent operating companies.

This procedure may not be feasible if the assets have appreciated invalue over cost (or have other deferred tax exposure), because of the opera-tion of subsection 69(5). In this case, a butter f ly transaction might beadopted.

Suppose, for example, that two individual shareholders, Mr. Louis andMs. Prasad, each own 50% of the shares of an operating company (‘‘Opco’’)and wish to separate their interests. They might undertake the followingprocedure:

Example 1

(a) Each shareholder would form a holding company (Louis Holdco,and Prasad Holdco, respectively) to which he or she would transfershares of Opco, making an election under subsection 85(1).

(b) As shown in Figure X, Opco would transfer one-half of its assets toeach of these holding companies in consideration for shares (andpossibly a note receivable from the holding companies), makingelections under subsection 85(1). The shares of the holding compa-nies held by Opco would have a paid-up capital which would notexceed the cost amount of the assets of Opco (net of assumedliabilities).1

(c) Louis Holdco and Prasad Holdco would redeem their shares heldby the operating company producing a deemed dividend to theoperating company but no capital gain.

(d) Opco would wind up, distributing its assets (cash or notes of theholding companies) to the holding companies, producing a deemeddividend to the holding companies but not a capital gain.

1 Subsection 85(2.1), which normally restricts paid-up capital to the elected amount, issubject to section 84.1 and section 212.1, neither of which is applicable here.

¶1002

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 4 Free lead: 145D Next lead: 0D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

416 Tax and Family Business Succession Planning

Figure ‘‘X’’

Louis

HoldcoPrasadHoldco

Opco

50% Common

50% Common

PreferredPreferred

Shares

AssetsAssets

Ms. Prasad Mr. Louis

Shares

If structured properly, the entire transaction would take place free oftax. The deemed dividends would not be taxed by virtue of the inter-corporate dividend deduction found in subsection 112(1). As will be seenshortly, the proper structuring of the foregoing transaction involves theavoidance of subsection 55(2), which potentially transmogrif ies the deemeddividends mentioned above into deemed capital gains.

Note: In the foregoing example, it is possible to transfer Opco’s assetsdirectly into Louis Holdco and Prasad Holdco, respectively because neitherof these corporations controls Opco; otherwise, corporate law issues arise,forcing a more complex reorganization.

¶1002

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 5 Free lead: 55D Next lead: 230D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Ch. 10/Spinouts 417

¶1003 Subsection 55(2)

Central to such a divisive reorganization is the potential application ofsubsection 55(2) of the Act. Essentially, subsection 55(2) provides that inter-corporate dividends, which would generally pass free of tax under Part I ofthe Act, pursuant to subsection 112(1), will be treated as capital gains to therecipient if received as part of a transaction or series of transactions, thepurpose of which — or in the case of a dividend pursuant to subsec-tion 84(3), the result of which — was to effect a signif icant reduction in thecapital gain that would have been realized on a sale of shares at fair marketvalue, assuming the dividend had not been paid. It is important to realizethat by virtue of subsection 248(10), a dividend declared in contemplationof a series of steps to effect a reduction in what would otherwise be a capitalgain, may also lead to the tax results described under subsection 55(2).

Safe Income. Subsection 55(2) does allow an inter-corporate taxabledividend to pass tax-free, provided it is wholly paid out of income earned orrealized (per subsection 55(2)), by the payor corporation after 1971, after theacquisition of the shares on which the dividend is paid (or deemed to bepaid) and before safe income determination time, (which is determined withreference to certain transactions within the series of transactions or eventsin question). This income is referred to as ‘‘safe income’’.2 The CRA hasdiscussed the components of safe income and, in general, the application ofsubsection 55(2) in a number of instances. See especially Robertson, ‘‘Cap-ital Gains Strips: A Revenue Canada Perspective on the Provisions ofSection 55’’, Canadian Tax Foundation 1981 Conference Report, 81; Hiltz,‘‘Section 55: An Update’’, 1984 CMTC 40; and Read, ‘‘Section 55: A Reviewof Current Issues’’, Canadian Tax Foundation 1988 Conference Report, 18:1.

The CRA takes the position that any portion of a dividend which isderived from non-safe income will cause the entire dividend to be consid-ered a capital gain. Consequently, it is imperative that a thorough calcula-tion of safe income be done before any dividends are declared where a thirdparty sale might occur.

It is important to realize that safe income does not necessarily equalthe retained earnings of the corporation. In calculating the safe income ofthe corporation or of particular shares of the corporation, the guidelines in

2 Per subsection 55(1), ‘‘safe-income determination time’’ for a transaction or event or aseries of transactions or events means the time that is the earlier of:

(a) the time that is immediately after the earliest disposition or increase in interestdescribed in any of subparagraphs (3)(a)(i) to (v) that resulted from the transaction,event or series, and

(b) the time that is immediately before the earliest time that a dividend is paid as partof the transaction, event or series.

¶1003

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 6 Free lead: 376D Next lead: 0D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

418 Tax and Family Business Succession Planning

the above-noted articles should be followed, as well as the statutory require-ments of subsection 55(5).

Safe income is pro-rated over all shares outstanding at the time thedividend is paid. The f irst dividends paid on a share come from the share’ssafe income. Thus, it is possible to pay a series of dividends in order tominimize the possibilit y that a portion of a dividend comes from unsafeearnings. In the alternative, paragraph 55(5)(f ) allows a dividend to bedesignated as two separate dividends. The CRA has indicated that it wouldaccept multiple paragraph 55(5)(f ) designations if there was reasonabledoubt as to different components of safe income.3 In the case of uncertainty,therefore, where a dividend is paid, it should be designated as a number ofdividends so that as much as possible of the dividend will be considered tobe paid out of safe income.

¶1004 Significant Exceptions to Subsection 55(2)

Apart from dividends paid out of the safe income, subsection 55(3)contains two signif icant exceptions to subsection 55(2):

● Paragraph 55(3)(a) is generally directed at limiting the operation ofsubsection 55(2) in cases where the reorganization is part of a trans-action or event, or a series of transactions or events where there isnot a sale or other disposition of assets on a rollover basis to anunrelated person,4 nor a transaction that increases such a person’spercentage or value of a corporation. The subsection imposes anumber of technical tests pertaining to ‘‘unrelated persons’’ (asdef ined in subsection 55(3.01)), all of which must be met in order forthe exception to subsection 55(2) (which otherwise triggers deemedcapital gains) to be applicable. It should be noted that the paragraph55(3)(a) exemption may not be applicable in a number of situationswhich might normally be considered to be within a related personmilieu.

3 CRA Doc. No. ACC9323, August 14, 1990. This Technical Interpretation adds restrictionsthat were not expressed by Michael Hiltz in his 1984 Corporate Management Tax Conferencepaper ‘‘Section 55: An Update’’, in Selected Income Tax Aspects of the Purchase and Sale of aBusiness, 1984 Corporate Management Tax Conference (Toronto: Canadian Tax Foundation,1984).

4 I.e., a person who is unrelated to the dividend recipient.

¶1004

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 7 Free lead: 254D Next lead: 845D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Ch. 10/Spinouts 419

For a summary of paragraph 55(3)(a) and related provisions, refer-ence should be made to ¶1011.

● Paragraph 55(3)(b) contains the so-called ‘‘butter f ly exception’’. Thisprovision essentially allows a corporation to distribute its assetsamong its shareholders, so long as each shareholder receives itsproportional share of each type of property of the corporation. TheCRA has stated that there are essentially three types of property:cash and near cash, business assets, and investment assets. The intri-cacies of paragraph 55(3)(b) are beyond the scope of this book. Formore information on the butter f ly transaction, see Sider & Ton-That,Understanding Section 55 and Butter f ly Reorganizations (CCH Cana-dian Limited, 1999).

In most situations where family business succession planning isinvolved, a spinout will be accomplished through the paragraph 55(3)(a)exemption if possible. For one thing, while paragraph 55(3)(a) certainly canhave complexities in certain situations (especially where spinouts to familymembers are involved), paragraph 55(3)(b) is even more complex and, asmentioned above, is limited to a proportional division of assets.

The intricacies of the paragraph 55(3)(a) exception come into playwhere there are issues as to whether unrelated persons are involved in atransaction, particularly spinouts to family members. In this respect, itshould be noted that, for the purpose of section 55, siblings are deemed tobe at arm’s length and unrelated to one another so that the spinout of assetsto children could be quite problematic, short of a full-scale proportionalbutter f ly.

Before getting into such intricacies, let us deal with examples where theparties to the reorganization are related. This tends to be the case for capitalgains purif ications (where no third-party sale is contemplated, at least) andasset-protection spinouts, as these may involve that split-up of corporate-level assets where the shareholder is a single individual or spouses.

¶1005 Purifications and Asset Protection Spinouts

If it is desired to keep the operating company in existence and simplypurif y it for the purposes of the small business corporation rules/capitalgains cr ystallization, or spinout assets to achieve a degree of asset

¶1005

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 8 Free lead: 487D Next lead: 0D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

420 Tax and Family Business Succession Planning

protection, as illustrated in Figures ‘‘A’’ and ‘‘B’’, a paragraph 55(3)(a) spi-nout could be implemented as follows.

Example 2

(a) A new holding company (‘‘Newco’’) would be incorporated withboth common shares and a f ixed number of preferred shares, whoseredemption amount would equal the fair market value of the con-sideration received on the f irst issuance of the preferred shares (theNewco Redemption Amount).

(b) The operating corporation’s (‘‘Opco’’) share capital would be reor-ganized pursuant to subsection 86(1) so that the existing issuedcommon shares owned by the shareholder(s) are changed into fornew common shares and preferred shares, whose redemption valuewould equal the fair market value of the assets to be transferred(the ‘‘Opco Redemption Amount’’).

(c) Opco would transfer its investment assets to Newco in exchange forall of Newco’s preferred shares pursuant to subsection 85(1), at anelected amount equaling the cost amount of those assets — i.e., noimmediate tax consequences (see Figure A ).

(d) The preference shares of Opco would be rolled into Newco undersubsection 85(1) in exchange for common shares in Newco for anelected amount equal to the cost base of the preferred shares,usually low (see Figure B).

(e) Newco would redeem its preferred shares held by Opco in consider-ation for a non-interest bearing demand promissory note, the prin-cipal amount of which would be the Newco Redemption Amount(the ‘‘Newco Note’’).

(f ) Opco would redeem its preferred shares held by Newco, inexchange for the cancellation of the Newco Note.

(g) There will be a tax-free inter-corporate dividend under subsec-tion 84(3) to Newco and Opco for the excess of the redemptionproceeds over the paid-up capital of the preferred shares.

¶1005

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 9 Free lead: 120D Next lead: 290D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Ch. 10/Spinouts 421

Figure ‘‘A’’

David

Opco NewcoPreferred Shares

Investment Assets

Common

SharesPreferred Shares

Figure ‘‘B’’

David

Opco

Newco

Investment

Assets

Preferred Shares

Common

Shares

Common

Shares

Preferred Shares

Notes:

When Opco reorganizes its share capital under subsection 86(1), andthere is a signif icant cost base in the pre-existing common shares of Opco, itwould be averaged pro rata as to the fair market value in the course of thesection 86 reorganization. The cost base allocable to the redeem-able/retractable shares would disappear as a result of the rollover of thoseshares by Opco to Newco pursuant to subsection 85(1) (as noted in para-graph (d) above, and their consequent redemption (per paragraph (e)).

¶1005

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 10 Free lead: 80D Next lead: 115D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

422 Tax and Family Business Succession Planning

One way of eliminating this problem would be to issue the preferredshares as a so-called ‘‘high-low’’ stock dividend, so that the cost base of thecommon shares would not average with the preferred shares. The signif i-cance of low stated capital is that this will minimize the deemed dividend byvirtue of the issuance of the preferred shares, since this is based on theincrease in stated capital thereof. In some provinces, e.g., British Columbia,it is clear that a high-low stock dividend can be paid. In others, such asOntario and Alberta, there has in the past been some debate as to whetherthis is permissible under corporate law. Consequently, both provinces haverecently passed legislation which eliminates the uncertainty.

The Newco and Opco redemption amounts are based on the fairmarket value of the non-business assets of Opco. This number is partiallybased on the fair market value of Opco. The value of an operating companyis not a hard and fast science, and any value may be open to dispute by theCRA. Therefore, it is advisable to utilize special shares (as noted in theabove example) rather than common shares so as to be able to have formularedemption and price adjustment clauses in the event that there is a disputein the value of the non-business assets.5

The result of the foregoing transactions would be that the investmentswould be owned by Newco, and the business assets would be owned byOpco. Opco would then meet the def inition of a small business corporationin the event that a cr ystallization of the capital gains exemption is desired.In addition, the removal of investment assets will hopefully result in anadditional degree of asset protection.

It should be noted that, because it does not involve a pro rata distribu-tion of different types of properties, this last example contemplates a para-graph 55(3)(a) situation — e.g., where there is only one owner-manager.Where there is more than one (unrelated) owner-manager, the abilit y toutilize the purif ication process outlined may be restricted, for example, dueto the application of subparagraph 55(3)(a)(ii), which, in essence, knocks outthe paragraph 55(3)(a) exemption when there is a signif icant increase in theinterest in any corporation of persons unrelated to the corporation prior tothe butter f ly. The CRA has taken the position that a signif icant increase in acorporation can be either a proportionate increase or a dollar valueincrease. In the multiple owner-manager situation, the incorporation ofNewco and the transfer of shares to Newco by each owner-manager could beinterpreted as a signif icant increase of each owner-manager in Newco. If this

5 However, as noted at ¶210, it appears that the CRA is not willing to recognize the effectof a price adjustment clause in connection with shares issued pursuant to a stock dividendfreeze on the basis that the stock dividend freeze does not involve a transfer of property in anon-arm’s length transaction (see Doc. No. 2003-0004125, April 1, 2003 (French only)).

¶1005

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 11 Free lead: 100D Next lead: 290D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Ch. 10/Spinouts 423

is the case, the inter-corporate deemed dividends on the cross-redemptionof shares may fall afoul of subsection 55(2), and be deemed to be capitalgains. It should be noted in this regard that siblings are considered to deal atarm’s length and be unrelated to each other by virtue of paragraph 55(5)(e).6

As stated previously, two objectives of the t ype of reorganizationdepicted above could be maintenance of small business corporation statusand asset protection.

Small Business Corporation (‘‘SBC’’): SBC status has become increas-ingly signif icant due to various income tax provisions which depend on thisstatus. Besides being a prerequisite for the small business capital gainsexemption, it is also signif icant with respect to the following:

● the corporate attribution rules;

● allowable business investment losses;

● the 10-year reserve for intergenerational transfers; and

● the capital gains deferral for investments in small business perrecently enacted section 44.1.

A small business corporation (def ined in subsection 248(1)) must, f irstof all, be a Canadian-controlled private corporation. Second (subject tosubsection 110.6(15), which refers to the valuation of life insurance policiesand proceeds and ignoring net income stabilization accounts), all or sub-stantially all of the fair market value of the assets of the corporation must beattributable to assets that are:

● used principally in an active business carried on primarily in Canadaby the corporation or a corporation related to it . The meaning of theterm ‘‘active business’’ as presently found in subsection 125(7) appliesto this paragraph (see section 248(1) ‘‘active business’’ def inition):

● shares or indebtedness of one or more small business corporationsthat are ‘‘connected’’ (see below)7 with the particular corporation; or

● any combination of the assets described above.

6 There was some initial concern as to whether the CRA would apply GA AR to thismethod of purif ication. Paragraph 15 of Information Circular IC 88-2 provides an example of asituation in which a corporation was purif ied. The CRA indicated that GA AR would not beapplied in the particular circumstances described. The example did not mention the use ofsection 85 rollovers to defer taxable gains on appreciated assets in the course of implementingthe purif ication procedures. However, purif ications involving section 85 rollovers have gener-ally become accepted practice.

7 Within the meaning of subsection 186(4) on the assumption that the small businesscorporation is at the time a ‘‘payer corporation’’ within the meaning of that subsection.

¶1005

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 12 Free lead: 5D Next lead: 115D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

424 Tax and Family Business Succession Planning

Basically, a corporation is connected with another corporation if itcontrols that other corporation (within the extended meaning of subsec-tion 186(2) of the Act) or owns more than 10% of the voting issued sharecapital and shares representing a fair market value in excess of 10% of thetotal fair market value of all issued capital of that corporation.

The CRA uses a 90% or more benchmark in respect of the all orsubstantially all test .

(For further discussion, reference should be made to ¶402, Chapter 4,Capital Gains Exemption, Crystallization & Multiplication, et seq.)

Asset Protection. It should be noted that, if asset protection is anobjective of the transaction, certain transfers of property discussed in theforegoing discussion may be subject to the various statutory provisions thatare intended to protect creditors’ interests. In the above discussion, it shouldbe noted that the butter f lies basically involve the spin out of corporateassets through the redemption of shares, i.e., vis-a-vis holding companieswhich may be formed to receive the assets. Accordingly, the solvency testsfound in subsection 32(2) of the OBCA relating to the redemption of shareswould come into play where the shares involved in the butter f ly are redeem-able. If the shares involved are not redeemable, there is also a solvency testunder subsection 30(2) of the OBCA relating to the reacquisition of suchshares by the corporation. If the solvency tests are not met, there could bedirectors’ liabilit y within subsection 130(2) of the OBCA, or the violationcould form the basis of an oppression action by creditors. Even if thesesolvency tests are met, there is also the possibilit y that aggrieved creditorscould bring other actions.

(For further discussion, reference should be made to Chapter 7, AssetProtection; the solvency tests of various provisions of the OBCA are summa-rized at ¶708a.)

Note on Part IV Tax

Where there is a cross-redemption of shares, as shown in the aboveexamples, the effect of refundable tax balances should be considered care-fully. The CRA has taken the position that where the two corporations areconnected, as would typically be the case with a purif ication, a cross-redemption of shares causes a ‘‘cascade effect’’ with respect to Part IV taxand dividend refunds: where a dividend refund is generated on a redemp-tion, there will be corresponding Part IV tax to the recipient corporation.The redemption of the recipient corporation’s shares, in turn, generates adividend refund, based at least in part on such Part IV tax. This in turnenlarges Part IV tax to the f irst corporation, thus enlarging its dividend

¶1005

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 13 Free lead: 130D Next lead: 0D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Ch. 10/Spinouts 425

refund and therefore the amount of Part IV tax to the recipient corporation,and so on. The result — a mathematical iterative (circular) calculationwhereby the dividend refund and Part IV tax cascade appears to generatesignif icant Part IV tax/dividend refund. (A similar calculation was upheldby the Tax Court of Canada in Les Entreprises Michele L’Heureux Inc. v. TheQueen, 94 DTC 1693.)

One possible solution to this Part IV tax problem would be to structurethe transaction so that the cross-redemption of shares could straddle a year-end. One share redemption would happen before the year-end and the otherafter. The ordering of redemptions would depend on where the taxpayerwanted the RDTOH to end up.

In a typical purif ication, the paid-up capital will be lower in the corpo-ration which is being purif ied: the paid-up capital of the recipient corpora-tion will normally ref lect the cost base of assets transferred (see subsec-tion 85(2.1)). Under these circumstances, the corporation with the higherpaid-up capital (t ypically the recipient) will experience a signif icant netliabilit y for Part IV tax, while the payor corporation will enjoy a net dividendrefund. Although it appears that the net result is self-cancelling, it should beremembered that there could be cash f low problems/opportunities, e.g., dueto differing year-ends and so on.

It further appears that if the deemed dividends in respect of bothcorporations are equal, the f inal position (when the reorganization is con-sidered in isolation, at least) may be that each corporation will experience aself-cancelling liabilit y for Part IV tax equal to its dividend refund and thateach corporation will continue to have a balance of RDTOH at the begin-ning of its next f iscal period equal to its opening balance before the but-ter f ly transaction.

In this respect, it may be possible to limit or reduce the recipientcorporation’s paid-up capital under applicable corporate law, such that theamount of the deemed dividend generated by each corporation would beidentical.

Of course, the foregoing is not a problem if there is no refundable taxbalance to begin with. (There may be different effects depending onwhether both corporations are connected with one another, or dividendsare paid other than as a result of the butter f ly.)

For further discussion of the cascade effect see ‘‘Part IV Complicationsin Butter f ly Transactions’’, Christopher J. Potter, 1992 Canadian TaxJournal, Vol. 4, p. 992 et seq.

¶1005

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 14 Free lead: 50D Next lead: 290D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

426 Tax and Family Business Succession Planning

¶1006 Series of Transactions or Events

As stated previously, the so-called paragraph 55(3)(a) exemption may becritical to a spinout. Central to this is the concept of whether the purif ica-tion is part of a series of transactions involving a sale or other disposition ofassets on a rollover basis to an unrelated person, or a transaction thatincreases such a person’s percentage or value of a corporation.

Subsection 248(10) states that a ‘‘series of transactions or events’’ willinclude any ‘‘related transactions or events completed in contemplation ofthe series’’. The CRA appears to take a very wide view of the application ofsubsection 248(10).

The following is CRA’s standard response regarding the issue:

A preliminary transaction will form part of a series determined withreference to subsection 248(10) if, at the time the preliminary transaction iscarried out, the taxpayer intends to implement the subsequent transactionsconstituting the series, and the subsequent transactions are eventuallycarried out. Thus, the preliminary and subsequent transactions will be partof a series even though at the time of the completion of the preliminarytransaction the taxpayer either had not determined all the important ele-ments of the subsequent transactions — including, possibly, the identity ofother taxpayers involved — or had lacked the abilit y to implement thesubsequent transactions.8

The CRA’s views on this and related issues are also discussed in Hiltz,‘‘Section 245 of the Income Tax Act’’, Canadian Tax Foundation 1988 Confer-ence Report, 7:1; Robertson, ‘‘Capital Gains Strips: A Revenue Canada Per-spective on the Provisions of Section 55’’, Canadian Tax Foundation 1981Conference Report, 81; Hiltz, ‘‘Section 55: An Update’’, Canadian Tax Foun-dation 1984 Corporate Management Tax Conference, 40; and Read, ‘‘Section55: A Review of Current Issues’’, Canadian Tax Foundation 1988 ConferenceReport, 18:1.

The CRA has also commented as to the application of subsec-tion 248(10) in a technical interpretation involving three scenarios regardingtax-free inter-corporate div idends included in a series of transactionsdesigned to purif y a corporation.9

1. The shareholders have no intention to sell their shares in the nextthree years.

8 Revenue Canada Round Table, 1992 APFF Conference, Question 39.9 See, for example, Michael Hiltz, ‘‘Section 245 Update’’ in Report of Proceedings of the

Fortieth Tax Conference, 1988; Conference Report (Toronto: Canadian Tax Foundation, 1989)7:1-9, at 7:6; CRA Doc. No. 9237670, December 23, 1992. See also Doc. No. AC57939, June 30,1989, among others.

¶1006

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 15 Free lead: 160D Next lead: 230D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Ch. 10/Spinouts 427

2. The shareholders have not identif ied a purchaser and there is ageneral intention to sell the shares in the next three to f ive years.

3. The shareholders have identif ied a purchaser and it is anticipatedthat the shareholders will sell their shares within the year.

The CRA’s response was as follows:

1. In situation 1, the fact that the shareholders have no intention ofselling their shares within the next three years is not conclusivethat the receipt of the dividends is not part of the series whichincludes an eventual sale of the shares to an arm’s length person.The facts of each particular situation would have to be reviewed todetermine whether subsection 55(2) would apply to the series oftransactions.

2. Where, at the time the dividends are received the shareholdershave an intention to sell their shares, the purif ication and theeventual sale, would generally be considered to be part of the sameseries of transactions determined with reference to subsec-tion 248(10), notwithstanding the fact that the shareholders hadnot identif ied a purchaser and that the eventual sale may not becompleted for several years.

3. The purif ication and the eventual sale, in such a situation, wouldbe considered to be part of the same series of transactions, deter-mined with reference to subsection 248(10), since the shareholdersintend to sell their shares and a purchaser had been identif ied atthe time of the reorganization.

Within the context of purif ication transactions, such expansive viewson the application of subsection 55(2) by virtue of the series of transactionprovisions are premised on the notion that, in most situations, a shareholderwho causes a purif ication reorganization to be carried out does so in orderthat the capital gains exemption will be available upon a disposition of theshares. In such cases, the shareholder would therefore have some intentionat the time of the reorganization of eventually selling the shares.10

With respect to the potential application of the general anti-avoidancerule in subsection 245(2), the CRA referred to paragraph 15 of InformationCircular 88-2, which provides that a transaction entered into to purif y acorporat ion is w ithin the scheme of the Act , and accordingly,

10 See Doc. No. 5-7939, June 30, 1989. See also notes to the introductory portion of ¶414afor further comments on the CRA’s view of the application of subsection 248(10) in the contextof a purif ication.

¶1006

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 16 Free lead: 215D Next lead: 290D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

428 Tax and Family Business Succession Planning

subsection 245(2) would not normally be applied to the claim for the capitalgains exemption.

¶1007 Case Law — Series of Transactions/Transactionsin Contemplation of Series

Besides continually emerging Canadian case law on series of transac-tions and transactions in contemplation of a series, there is considerableU.K . case law on the former issue. In fact, as elaborated below, the Canadianlaw in this area is ver y much inf luenced by U.K . case law.

¶1008 U.K . Case Law

The English courts have considered the concept of a ‘‘pre-ordained’’series of transactions in a series of cases11 which focus on the concept thatthe series must be pre-ordained, in essence, confining a series of transac-tions to a situation where it was practically certain that the other stepswould follow; only then could it be said that the steps were pre-ordained.This would not be the case if the terms on which the subsequent steps are totake place are not settled at the time of the f irst .

The common law interpretation of the phrase ‘‘series of transactions’’in the English cases was adopted by the Federal Court of Appeal in OSFCHoldings Ltd. v. The Queen, 2001 DTC 5471. However, as discussed below,the current state of the law appears to be that subsection 248(10) signif i-cantly extends the common law meaning of this phrase.

¶1009 Canadian Case Law

At time of writing, the Supreme Court of Canada had rendered twosimultaneous decisions that def ined series of transactions in connectionwith the general anti-avoidance rule (subsection 245(2)).12 Both decisionswere substantially consistent with the law as previously decided in the U.K .courts as well as the Court of Appeal in OSFC.13 In fact, the ruling in OSFCremains entrenched in the heart of the Supreme Court’s rulings.

11 Including Furniss v. Dawson, [1984] A .C. 474 (H.L.) and Craven v. White, [1989] A .C. 459(H.L.). These cases are discussed in some detail by John Tiley, in his article, ‘‘Series of Transac-tions’’, Canadian Tax Foundation 1988 Conference Report, 8:1.

12 Canada Trustco Mortgage Co. v. Canada, 2005 DTC 5523 and Mathew v. Canada, 2005DTC 5538. Because of the nature of the transaction in issue, the third Supreme Court ofCanada GA AR case, Lipson et al. v. The Queen, 2009 DTC 5015, said little about series oftransactions and subsection 248(10).

13 I.e., ignoring subsection 248(10).

¶1007

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 17 Free lead: 300D Next lead: 210D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Ch. 10/Spinouts 429

In OSFC, which also considered the concept in connection with thegeneral anti-avoidance rule (subsection 245(2)), the Federal Court of Appealindicated that subsection 248(10) broadened the meaning of series from thatdef ined in the British cases. The OSFC case involved a series of transactionswhereby mortgages in loss positions were transferred to a partnership. Afterthis series was completed, a buyer (OSFC) was found which was not identi-f ied at the time of the series. OSFC became the majority interest partnerand then syndicated its interest in the partnership. The Federal Court ofAppeal held that the introduction of the buyer was in contemplation of theseries of transactions involving the formation of the partnership. In otherwords, the concept of ‘‘contemplation’’ includes a retroactive reference to aprevious series.

In respect of series of transactions, Rothstein, J. stated:

I would, subject to subsection 248(10), adopt the House of Lordsapproach. Thus, for there to be a series of transactions, each transaction inthe series must be pre-ordained to produce a f inal result . Pre-ordinationmeans that when the f irst transaction of the series is implemented, allessential features of the subsequent transaction or transactions are deter-mined by persons who have the f irm intention and abilit y to implementthem. That is, there must be no practical likelihood that the subsequenttransaction or transactions will not take place [paragraph 24].

In respect of subsection 248(10), Rothstein, J. stated:

Subsection 248(10) requires three things: f irst , a series of transactionswithin the common law meaning; second, a transaction related to thatseries; and third, the completion of the related transaction in contempla-tion of that series [paragraph 35].

Thus, before applying subsection 248(10), ‘‘series’’ must be construedaccording to its common law meaning, which I have found to be pre-ordained transactions which are practically certain to occur. To that isadded ‘‘any related transactions or events completed in contemplation ofthe series’’. Subsection 248(10) does not require that the related transactionbe pre-ordained. Nor does it say when the related transaction must becompleted. As long as the transaction has some connection with thecommon law series, it will, if it was completed in contemplation of thecommon law series, be included in the series by reason of the deemingeffect of subsection 248(10). Whether the related transaction is completedin contemplation of the common law series requires an assessment ofwhether the parties to the transaction knew of the common law series, suchthat it could be said that they took it into account when deciding to completethe transaction. If so, the transaction can be said to be completed in

¶1009

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 18 Free lead: 200D Next lead: 230D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

430 Tax and Family Business Succession Planning

contemplation of the common law series [paragraph 36 — emphasisadded].14

The appellant in OSFC had f iled leave to appeal to the Supreme Courtof Canada, however, the Supreme Court declined to grant leave.

The Supreme Court’s decision in Canada Trustco echoed OSFC andsaid:

The meaning of the expression ‘‘series of transactions’’ under s. 245(2)and (3) is not clear on its face. We agree with the majority of the FederalCourt of Appeal in OSFC and endorse the test for a series of transactions asadopted by the House of Lords that a series of transactions involves anumber of transactions that are ‘‘pre-ordained in order to produce a givenresult’’ with ‘‘no practical likelihood that the pre-planned events would nottake place in the order ordained’’: Craven v. White, [1989] A .C. 398, at p. 514,per Lord Oliver; see also W.T. Ramsay Ltd. v. Inland Revenue Commissioners,[1981] 1 All E.R . 865 [paragraph 25].

However, the Supreme Court then expanded on the interpretation of‘‘in contemplation’’ found within the def inition of ‘‘series of transaction’’ insubsection 248(10) and said:

Section 248(10) extends the meaning of ‘‘series of transactions’’ toinclude ‘‘related transactions or events completed in contemplation of theseries’’. The Federal Court of Appeal held, at para. 36 of OSFC, that thisoccurs where the parties to the transaction ‘‘knew of the . . . series, suchthat it could be said that they took it into account when deciding tocomplete the transaction’’. We would elaborate that ‘‘in contemplation’’ isread not in the sense of actual knowledge but in the broader sense of‘‘because of’’ or ‘‘in relation to’’ the series. The phrase can be applied toevents either before or after the basic avoidance transaction found unders. 245(3). As has been noted:

It is highly unlikely that Parliament could have intended toinclude in the statutory def inition of ‘‘series of transactions’’related transactions completed in contemplation of a subsequentseries of transactions, but not related transactions in the contem-plation of which taxpayers completed a prior series of transac-tions [paragraph 26 — emphasis added].

Thus, the ‘‘knew of’’ and ‘‘took it into account’’ language articulated inOFSC were subject to the ‘‘elaboration’’ that ‘‘in contemplation’’ is read notin the sense of actual knowledge but in the ‘‘broader sense of ‘because of’’’

14 In Doc. No. 2002-0173345, December 3, 2002, the CRA indicated that the OFSC deci-sion is consistent with the CRA’s longstanding interpretation, as expressed by the ‘‘standardresponse’’ quoted earlier.

¶1009

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 19 Free lead: 75D Next lead: 115D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Ch. 10/Spinouts 431

or ‘‘in relation to’’ — an articulation of a functional relationship. However,this left ver y little guidance as to the degree of nexus.

In MIL (Investments) S.A . v. Canada, 2006 DTC 3307, Justice Bell triedto clarif y the foregoing by indicating that there must be a ‘‘strong nexus’’between the transactions (paragraph 65); however, as discussed below, thisauthority is now questionable.

As a consequence of the Supreme Court rulings, the current state of thelaw remains that subsection 248(10) expands the scope of the phrase ‘‘seriesof transactions’’ beyond the common law def initions of English cases toinclude ‘‘any related transactions or events completed in contemplation ofthe series’’. However, the Supreme Court of Canada revised the common lawdef inition to allow for ‘‘the event’’ to occur either before or after the transac-tion.

In the wake of the OSFC decision, the CRA issued Income Tax Tech-nical News No. 22 and Technical Interpretation No. 2002-0173345,December 3, 2002, in which it reaff irmed its prior administrative positionsconcerning the meaning of the phrase ‘‘series of transactions’’ for purposesof subsection 248(10) that have been described above. The CRA was also ofthe opinion that the ruling in OSFC was consistent with its position. TheCRA has not elaborated on this issue since the Supreme Court’s decisionswas rendered.

Addendum. In Copthorne Holdings v. The Queen, 2007 DTC 1230(T.C.C.), ‘‘contemplation’’ of a series of transactions for the purposes ofsubsection 248(10) related to a previous series15 involving the preservationof paid-up capital in certain corporate-group reorganizations which, in thejudge’s view, resulted in a ‘‘double count’’ of paid-up capital. The Courtindicated the subsequent redemption of shares which crystallized the ben-ef it of the high paid-up capital (the impetus of which was a subsequentchange to the FAPI rules — unforeseen at the time of the f irst series) had a‘‘strong nexus’’ to the previous series; it was completed in contemplation ofthe previous series, within the meaning of subsection 248(10). By virtue ofthe concept of ‘‘backwards contemplation’’, a series could be extended toinclude a subsequent transaction, even if unforeseen at the time of the priorseries. This concept could adversely affect a variety of tax planning transac-

15 The statement of professor D.G. Duff in ‘‘Judicial Application of the General Anti-Avoidance Rule in Canada: OSFC Holdings Ltd. v. The Queen’’, 57 I.B.F.D. Bulletin 278, at p. 287(as cited at paragraph 26 of Canada Trustco) was noted:

It is highly unlikely that Parliament could have intended to include in the statutorydef inition of ‘‘series of transactions’’ related transactions completed in contemplation ofa subsequent series of transactions, but not related transactions in the contemplation ofwhich taxpayers completed a prior series of transactions.

¶1009

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 20 Free lead: 355D Next lead: 0D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

432 Tax and Family Business Succession Planning

tions, e.g., if designed to preserve/enhance favourable tax attributes in theevent that a transaction which might benef it therefrom might ‘‘come along’’in the future. (The fact that a transaction may have an independent purposeand existence, apart from the series, does not mean that is excluded if it hadbeen intended to achieve a composite result .)16

The Federal Court of Appeal aff irmed the Tax Court of Canada deci-sion.17 The Court effectively expanded the series of transactions concept bydisapproving of the ‘‘strong nexus’’ test between the series of transactionsitself and transactions in contemplation of the series by looking to a ‘‘moti-vating factor’’ test :

In my view, if a series is a motivating factor with respect to thecompletion of a subsequent transaction, the transaction can be said tohave been completed ‘‘in contemplation of the series’’ and a direct causalrelationship between the series and the transaction, as argued by theappellant, need not be established. In my opinion, this standard is reconcil-able with the test as stated in OSFC and as broadened in Canada Trustco[paragraph 46].18

The Court also noted the ‘‘relatively close temporal connection’’between the transactions in question, indicating that:

While I do not wish to suggest that any particular length of timebetween a series and a transaction will be determinative . . ., it is my viewthat an approximately one year gap between the 1993 Share Sale and thecompletion of the 1995 Redemption militates against accepting an asser-tion that there was an ‘‘extreme degree of remoteness’’ that the 1995Redemption would be undertaken, as was urged upon the Court [para-graph 51].

Obviously, the issue of whether a series is a ‘‘motivating factor’’ withrespect of the completion of a subsequent transaction will only increase theuncertainty in respect of the series of transactions issue. One may betempted to conclude that if the prior series of transactions results in apotential tax advantage, this would likely be a ‘‘motivating factor’’ withrespect to the completion of a subsequent transaction.

16 See paragraph 42.17 2009 DTC 5101.18 In the preceding paragraph, the Court approved of the statement in MIL that ‘‘in

contemplation’’, as used in subsection 248(10), does not lead to the conclusion that the merepossibilit y of a connection between a series of transactions and a related transaction issuff icient to include that transaction in the series.

¶1009

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 21 Free lead: 55D Next lead: 230D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Ch. 10/Spinouts 433

¶1010 Spinouts to Family Members

The foregoing discussion assumes that the spinout is between relatedparties, so that the paragraph 55(3)(a) exemption is applicable (assumingthat series of transactions/transactions in contemplation of a series is not inissue). However, the prospect of a spinout reorganization in favour of afamily member raises more signif icant complexities with respect to theapplication of the paragraph 55(3)(a) exemption, without which the onlyalternative may be a full-scale 55(3)(b) proportional butter f ly.

¶1011 Paragraph 55(3)(a) and Related Provisions

The paragraph 55(3)(a) exemption from subsection 55(2) would gener-ally not apply to a purif ication, if it is part of a series of transactions thatincludes a sale or other disposition of assets on a rollover basis to anunrelated person or a transaction that increases such a person’s percentageor value of a corporation. However, as stated previously, for the purpose ofsection 55, siblings are deemed to be at arm’s length and unrelated to oneanother so that the spin out of assets to children could be quite problematic,short of a full-scale proportional butter f ly. Other issues may arise where afamily trust is involved, especially if a distribution from such a trust is part ofthe series of transactions involving a spinout. In such situations, the intrica-cies of paragraph 55(3)(a) and related provisions must be reviewed verycarefully.

More precisely, paragraph 55(3)(a) provides that subsection 55(2)(deemed capital gains) will apply where, as part of a series of transactions orevents as a part of which a dividend was received, there was at any particulartime, any of the following:

(i) Disposition of property to unrelated person — A disposition of prop-erty for proceeds19 that are less than its fair market value to a person(or partnership) that was an unrelated person immediately before theparticular time, other than money disposed of on the payment of adividend or on a reduction of the paid-up capital of a share. (As

19 Under paragraph 55(3.01)(d ), the def inition of ‘‘proceeds of disposition’’ is altered forthe purposes of paragraph 55(3)(a). Proceeds of disposition, in these circumstances, are to bedetermined without reference to paragraph 55(2)(a), as provided for in paragraph (j ) of thedef inition in section 54 of the Act (and section 93, per former Bill C-10). Non-residents aredeemed, for the purposes of paragraph 55(3)(a), to have disposed of property for proceeds ofdisposition less than its fair market value, notwithstanding any other provision of the Act,where the gain or loss from the disposition is not included in computing the person’s taxableincome earned in Canada. The exception to this rule provided for under paragraph 55(3.01)(e),is where, under the laws of the countr y in which the person is resident, the gain or loss iscomputed as if the property were disposed of for proceeds that are not less than its fair marketvalue and the gain or loss so computed is recognized for the purposes of the those laws.

¶1011

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 22 Free lead: 57D Next lead: 118D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

434 Tax and Family Business Succession Planning

observed below, ‘‘unrelated person’’ means a person unrelated to thedividend recipient.)

(ii) Signif icant increase in direct interest in any corporation by unre-lated person — A signif icant increase in the direct interest in anycorporation of any persons (or partnerships) that were unrelatedpersons immediately before the particular time, other than anincrease that arises as a consequence of a disposition of shares of acorporation for proceeds not less than the fair market value of suchshares.

(iii) Disposition of dividend payer to unrelated person — A dispositionto a person (or partnership) who was an unrelated person immedi-ately before the particular time, of either shares of the corporationthat paid the dividend (the dividend payer) or property20 whichderived more than 10% of its value from shares of the dividend payer.

(iv) Disposition of dividend recipient to unrelated person — A disposi-tion, after the time the dividend was received, to a person (or part-nership) who was an unrelated person immediately before the partic-ular time, of either shares of the dividend recipient or property whichderived more than 10% of its value from shares of the dividendrecipient.

(v) Signif icant increase in direct interest of unrelated person in dividendpayer — A signif icant increase in the total of all direct interests in thedividend payer of any persons (or partnerships) who were unrelatedpersons immediately before the particular time.

Unrelated Person. Subsection 55(3.01) def ines ‘‘unrelated person’’immediately before the particular time, to mean a person (other than thedividend recipient) to whom the dividend recipient is not related or apartnership, any member of which (other than the dividend recipient) is notrelated to the dividend recipient.

Signif icant Increase. It will often be diff icult to determine whetherthere has been a signif icant increase in the interest of an unrelated personin any corporation. It is the view of the CRA that a signif icant increase ismeasured in terms of dollar value as well as percentage interest . Also thereference to an ‘‘interest’’ in a corporation may go beyond share ownershipto include ownership of debt of a corporation or any other rights which givethe unrelated person a claim on the corporation’s assets or revenues. TheCRA has consistently taken the position that interest should not be

20 Other than shares of the dividend recipient, per former Bill C-10.

¶1011

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 23 Free lead: 28D Next lead: 118D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Ch. 10/Spinouts 435

restricted to ownership of shares; the term should describe the economicinterest that a person has in the assets held by a corporation and is thereforebroad enough to include an indirect interest .21

Deeming Rules. The rules for determining whether people are relatedare set out in section 251. However, there are several deeming rules inparagraph 55(5)(e):

(i) Siblings not related — Brothers and sisters are deemed to deal atarm’s length and not to be related.

(ii) Trusts — A person who is related to every benef iciar y of a trust(other than a registered charity) who is or may (otherwise than byreason of the death of another benef iciar y of the trust) be entitled toshare in the income or capital of the trust is deemed to be related tothe trust (and if the person is also a benef iciar y, the person isdeemed for these purposes to be related to himself or herself ).

(iii) Trusts and benef iciaries — A benef iciar y of a trust and the trustare deemed not to be related unless the benef iciar y receives a shareowned by the trust in satisfaction of all or part of his or her interest inthe trust, or if the benef iciar y is a corporation controlled by thetrust, or if the benef iciar y and trust are related by virtue of (ii) above.

(iv) Rights/connective relationship not applicable — Persons who arerelated solely by virtue of paragraph 251(5)(b) (rights to acquireshares, etc.), or subsection 251(3) (two corporations are related toone another if they are related to the same corporation) are deemednot to be related to each other.

Anti-Avoidance. Subsection 55(4) contains a further rule that may deempersons not to be related or deem a corporation not to be controlled if it isreasonable to consider that one of the main purposes of one or moretransactions was to cause the persons to be related or a corporation to becontrolled and thus make subsection 55(2) inapplicable.

Interpretative Provisions. Paragraph 55(3.01)(b) provides that for thepurposes of paragraph 55(3)(a), a corporation that is formed by an amalga-mation of two or more predecessor corporations, is deemed to be the same

21 See M. Ton-That & V. Sider, Understanding Section 55 and Butter f ly Reorganizations(1999, CCH Canadian Limited, North York), page 68. See also John Robertson ‘‘Capital GainsStrips; A Revenue Canada Perspective on the Provisions of Section 55’’ in Report of Proceedingsof the Thirty-Third Tax Conference, 1981, Conference Report (Toronto: Canadian Tax Founda-tion, 1982), 81-109, at 105, Question 28; and Peter K . Rogers, CGA, ‘‘Splitting Up and Reorga-nizing the Family Business — Some Tips and Traps’’, 2001 British Columbia Tax Conference(Vancouver : Canadian Tax Foundation, 2001), 8:1-30.

¶1011

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 24 Free lead: 313D Next lead: 0D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

436 Tax and Family Business Succession Planning

corporation as, and a continuation of the predecessor corporations. Simi-larly, paragraph 55(3.01)(c) provides that where a subsidiar y is wound upinto its parent corporation in circumstances to which subsection 88(1) isapplicable, the parent corporation is deemed, for the purposes of para-graph 55(3)(a), to be the same corporation as, and a continuation of thesubsidiar y.

Related Persons. ‘‘Related persons’’ are def ined in subsection 251(2) forthe purposes of the Act, as follows:

(a) indiv iduals connected by blood relat ionship, marr iage orcommon-law partnership or adoption;

(b) a corporation and

(i) a person who controls the corporation, if it is controlled by oneperson,

(ii) a person who is a member of a related group that controls thecorporation, or

(iii) any person related to a person described in subparagraph (i) or(ii);

(c) any two corporations

(i) if they are controlled by the same person or group of persons,

(ii) if each of the corporations is controlled by one person and theperson who controls one of the corporations is related to theperson who controls the other corporation,

(iii) if one of the corporations is controlled by one person and thatperson is related to any member of a related group that controlsthe other corporation,

(iv) if one of the corporations is controlled by one person and thatperson is related to each member of an unrelated group thatcontrols the other corporation,

(v) if any member of a related group that controls one of the corpo-rations is related to each member of an unrelated group thatcontrols the other corporation, or

(vi) if each member of an unrelated group that controls one of thecorporations is related to at least one member of an unrelatedgroup that controls the other corporation.

¶1011

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 25 Free lead: 413D Next lead: 0D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Ch. 10/Spinouts 437

¶1012 Examples of Spinouts

As stated previously, spinouts to family members and the like must bereviewed carefully to ensure that the paragraph 55(3)(a) exemption applies;otherwise the spinout must be effected as a full-scale proportionate but-ter f ly.

¶1013 Example 3: Spinout to Family Trust

Figures C and D illustrate a spinout to a family trust which manypractitioners take for granted. As shown in Figure C, David (father) isassumed to hold f reeze shares of Hoot s-Paw Holding s redeem-able/retractable at $500,000, with common shares held by the Louis FamilyTrust, having a fair market value of $1 million. For convenience, we areassuming that Hoots-Paw Holdings holds $500,000 of investment assets andall of the shares of Subco, which also has a FMV of $1 million. The purposeof this reorganization could be a capital gains exemption purif ication, orasset protection, for example.

Figure ‘‘C’’

Louis

Family

Trust

David

Louis

Hoots-Paw

Holdings

Subco

Freeze Shares

$500,000

Common

SharesFMV $1M

FMV $1M

¶1013

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 26 Free lead: 235D Next lead: 0D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

438 Tax and Family Business Succession Planning

The spinout reorganization is shown in Figure D. The Louis FamilyTrust would roll its common shares of Hoots-Paw Holdings into TrustHoldco pursuant to section 85 of the Act. David would hold thin-votingshares of a Trust Holdco, i.e., to retain control. The idea of the spinout wouldbe for Hoots-Paw Holdings to transfer its shares of Subco into Trust Holdco,in return for redeemable/retractable shares based on the FMV of Subco.The inter-corporate shareholdings as between Hoots-Paw Holdings andTrust Holdco would, of course be redeemed; e.g., the consideration for theredemption would be promissory notes, which would then be set off againstone another. The redemption would involve deemed dividends in bothcorporations. Therefore, both Hoots-Paw Holdings and Trust Holdco wouldbe dividend recipients.

Figure ‘‘D’’

Louis

Family

Trust

David

Louis

Trust HoldcoHoots-Paw

Holdings

Subco

Thin-Voting Shares

Freeze Shares

Common Shares

?

¶1013

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 27 Free lead: 468D Next lead: 248D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Ch. 10/Spinouts 439

Accordingly, the unrelated person tests applies with respect to bothHoots-Paw Holdings and Trust Holdco. Generally, however, a spinout reor-ganization will qualif y if each of the parties are related to one another, sinceall of the provisions of paragraph 55(3)(a) will be satisf ied in such case.

● Louis Family Trust/David. Per paragraph 55(5)(e), the Louis FamilyTrust will be related to David Louis if David Louis is related to eachbenef iciar y (other than a registered charity) under a trust who is ormay (otherwise than by reason of the death of another benef iciar yunder the trust) be entitled to share in the income or capital of theLouis Family Trust . If the benef iciaries of the Louis Family Trust arethe issue of David, or the issue of David and his spouse Mia, thiswould be the case. As noted, it is also possible to include a registeredcharity as a benef iciar y. If, however, the benef iciaries included asibling, niece, or nephew of David, the Louis Family Trust would notbe related to David. There would also be a problem if a charity otherthan a registered charity were named as a benef iciar y. Registeredcharities generally pertain to Canadian-resident institutions, per sub-section 248(1); this means, for example, that a foreign charity wouldthrow the trust offside, unless the charity could only be entitled toincome or capital by virtue of the death of the benef iciaries (thismight be the case if the charity was named the benef iciar y if all ofthe other benef iciaries passed away — i.e., as a default clause).

● Louis Family Trust/Hoots-Paw. The Louis Family Trust is related toHoots-Paw Holdings by virtue of subparagraph 251(2)(b)(iii), since itis related to the person who controls Hoots-Paw Holdings, DavidLouis.

● Louis Family Trust/Trust Holdco. The Louis Family Trust is related toTrust Holdco by virtue of subparagraph 251(2)(b)(iii) since it isrelated to the person who controls Trust Holdco, David Louis.

If, however, subsection 55(4) were to apply, one must determinewhether the Louis Family Trust would otherwise be related to TrustHoldco. Per subparagraph 55(5)(e)(iii), a trust and a person shall bedeemed not to be related unless they are deemed by paragraph55(3.2)(d ) or subparagraph 55(5)(e)(ii) to be related to each other, or

¶1013

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 28 Free lead: 54D Next lead: 124D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

440 Tax and Family Business Succession Planning

the person is a corporation that is controlled by the Trust. It wouldappear that the last part of subparagraph 55(5)(e)(iii) would apply.22

● Hoots-Paw/Trust Holdco. Hoots-Paw Holdings and Trust Holdco arerelated because David controls both corporations. If, however, theanti-avoidance rule in subsection 55(4) applies, and David’s thin-voting shares are ignored, Hoots-Paw Holdings and Trust Holdco arerelated by virtue of subparagraph 251(2)(c)(ii), since each corporationis controlled by one person and the person who controls TrustHoldco (Louis Family Trust) is related to the person who controlsHoots-Paw (David).

● David Louis/Hoots-Paw. David is related to Hoots-Paw because hecontrols this corporation.

● David Louis/Trust Holdco. David is related to Trust Holdco, eitherbecause he controls it , or if subsection 55(4) (anti-avoidance) applies,by virtue of subparagraph 251(2)(b)(iii), since Trust Holdco is con-trolled by the Louis Family Trust and David is related to the LouisFamily Trust .

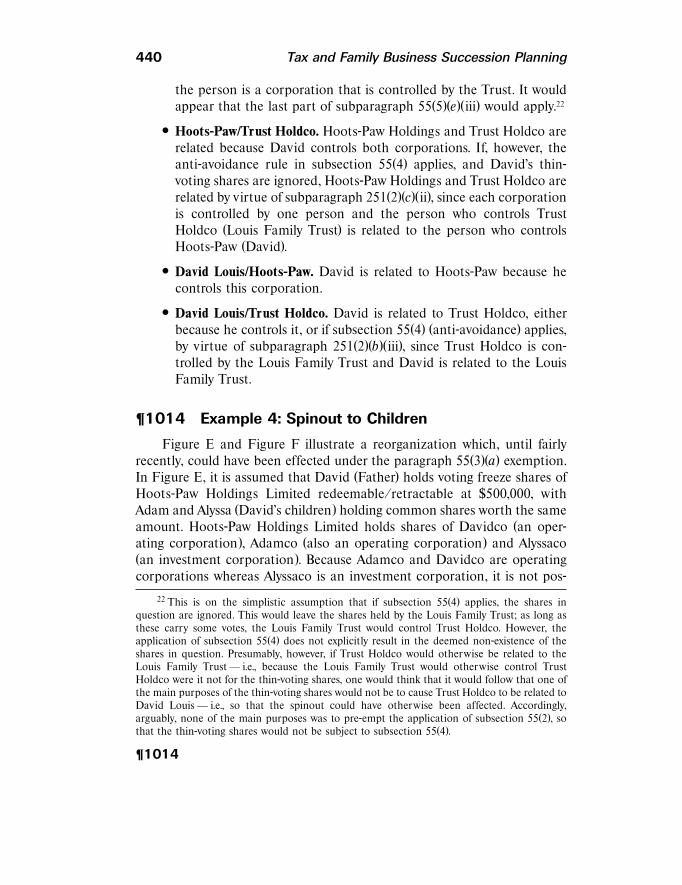

¶1014 Example 4: Spinout to Children

Figure E and Figure F illustrate a reorganization which, until fairlyrecently, could have been effected under the paragraph 55(3)(a) exemption.In Figure E, it is assumed that David (Father) holds voting freeze shares ofHoots-Paw Holdings Limited redeemable/retractable at $500,000, withAdam and Alyssa (David’s children) holding common shares worth the sameamount. Hoots-Paw Holdings Limited holds shares of Davidco (an oper-ating corporation), Adamco (also an operating corporation) and Alyssaco(an investment corporation). Because Adamco and Davidco are operatingcorporations whereas Alyssaco is an investment corporation, it is not pos-

22 This is on the simplistic assumption that if subsection 55(4) applies, the shares inquestion are ignored. This would leave the shares held by the Louis Family Trust; as long asthese carr y some votes, the Louis Family Trust would control Trust Holdco. However, theapplication of subsection 55(4) does not explicitly result in the deemed non-existence of theshares in question. Presumably, however, if Trust Holdco would otherwise be related to theLouis Family Trust — i.e., because the Louis Family Trust would otherwise control TrustHoldco were it not for the thin-voting shares, one would think that it would follow that one ofthe main purposes of the thin-voting shares would not be to cause Trust Holdco to be related toDavid Louis — i.e., so that the spinout could have otherwise been affected. Accordingly,arguably, none of the main purposes was to pre-empt the application of subsection 55(2), sothat the thin-voting shares would not be subject to subsection 55(4).

¶1014

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 29 Free lead: 42D Next lead: 0D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Ch. 10/Spinouts 441

sible to spinout Alyssaco to Alyssa Holdings as a true proportional butter f ly.For convenience, we have assumed that each of Davidco, Adamco, andAlyssaco is worth $500,000, the value of the common shares held by Adamand Alyssa respectively.

Figure ‘‘E’’

David Adam Alyssa

Hoots-Paw

Holdings

Limited

Davidco

(Opco)

Adamco

(Opco)

Alyssaco

(Investco)

Freeze Shares

FMV $500,000

Common Shares

FMV $500,000Common Shares

FMV $500,000

FMV $500,000

FMV $500,000

FMV $500,000

As illustrated in Figure F, the object of the reorganization is for Adamto form Adam Holdings, Alyssa to form Alyssa Holdings, and then spin outthe shares of Adamco and Alyssaco to these holding companies. It should beremembered that, for the purposes of section 55, siblings are deemed to beat arm’s length and unrelated to one another.

¶1014

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 30 Free lead: 0D Next lead: 290D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

442 Tax and Family Business Succession Planning

Figure ‘‘F’’

AlyssaAdamDavid

Hoots-PawHoldings*

AdamHoldings*

AlyssaHoldings*

Davidco Adamco Alyssaco

Freeze Shares Common Shares Common Shares

CommonShares

?Common Shares

?

* Dividend Recipient

Among other things, this reorganization would involve a disposition ofproperty at less than fair market value to both Adam Holdings and AlyssaHoldings. Adam Holdings and Alyssa Holdings are both dividend recipients,as is Hoots-Paw Holdings. The problem is that Adam Holdings and AlyssaHoldings must be related to each other, since this is determined in referenceto the dividend recipient (i.e., per subparagraph 55(3)(a)(i) there is a disposi-tion at less than fair market value to a person — Adam Holdings — which isunrelated to the div idend recipient , Alyssa Holdings, and vice versa).Although Adam Holdings and Alyssa Holdings are related to Hoots-PawHoldings by virtue of subparagraph 251(2)(b)(ii), they are not related to oneanother, since, for the purposes of section 55, each corporation is controlledby an unrelated person, Adam and Alyssa respectively. Until recently, AdamHoldings and Alyssa Holdings would be deemed to be related throughsubsection 251(3) of the Act, a connective provision which deems twocorporations to be related to each other if they are related to the samecor porat ion , i .e . , Hoot s-Paw Holding s. However, per subpara-graph 55(5)(e)(iv), this provision no longer applies to section 55.

¶1014

N CCH CANADIAN LIMITED ♦ NT PAGER Username: aline.kurdian Date: 16-SEP-09 Time: 11:59Filename: D:\books\b212\chap10.dat Style: D:\books\b212\fmt\book.bst Format: $BOOKS/tax_books/fmt/taxbooks.bft (binary)Seq: 31 Free lead: 45D Next lead: 115D Comment: ***** TAX BOOKS * DTD: (taxlib.dtd) *****

Ch. 10/Spinouts 443

As shown in Figure G, however, ignoring subsection 55(4) (discussedbelow), it appears to be possible to effect the spinout if David controlledHoots-Paw Holdings, Adam Holdings and Alyssa Holdings — i.e., if it is a‘‘complete’’ series of transactions — that is, not part of a larger series oftransactions involving an unrelated person (or in contemplation thereof ).23

Figure ‘‘G’’

AlyssaAdamDavid

Hoots-PawHoldings

AdamHoldings

AlyssaHoldings*

Davidco Adamco Alyssaco

Common SharesCommon Shares

CommonShares

?

Common Shares

?

* Dividend Recipient

Freeze Shares(Voting)

Voting Shares

Voting Shares

The foregoing example illustrates that spinout reorganizations can beef fected on a non-proportional basis if a parent controls all of the

23 In this case, since Hoots-Paw Holdings, Adam Holdings and Alyssa Holdings are con-trolled by the same person — David — they would now be related to one another, per subpara-graph 251(2)(c)(i). Further, while Adam/Adam Holdings and Alyssa/Alyssa Holdings would nolonger be related to each other by virtue of being controlled by Adam and Alyssa respectively,they would be related to each other by virtue of subparagraph 251(2)(b)(iii), and Adam andAlyssa would also be related to Hoots-Paw Holdings by virtue of this provision. Thus, whileAdam and Alyssa continue to be unrelated to one another, they are now related to all threecorporations which are the dividend recipients.

¶1014