sarina fisher - the centre for international economics - rising health spending but who benefits

TRANSCRIPT

Rising health spending but who benefits

Presented by Sarina Fisher

Centre for International Economics

www.TheCIE.com.au

28 July 2015

The ‘up and up’ of health costs

Health costs are consuming a growing proportion of resources…

.. and taking up a growing slice of the tax revenue pie, outcompeting government funds for other public services

www.TheCIE.com.au2

Chart 1: Ratio of health expenditure to GDP

Chart 2: Health spending as a % of taxation revenue

Source: AIHW 2014, Health expenditure Australia 2012-13

Dollar spend is rising and source of funds is changing, but little shift in spending profile

www.TheCIE.com.au3

0

20

40

60

80

100

120

140

160

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

$ billion

Capital expenditure Other recurrent Primary care Hospitals

5.3%

5.3%

20.3%

20.3%

36.3%

38.1%

35.9%

38.0%

Very little change in the distribution of total spending by area of expenditure

5.3%

5.3%

20.3%

20.3%

36.3%

38.1%

35.9%

38.0%

Very little change in the distribution of total spending by area of expenditure

$147.4bn in 2012-13

Health spending continued to rise, up

64%over the past decade

Source: AIHW health expenditure database

Chart 3: Total expenditure on health, constant prices

Chart 4: Health spending by source

www.TheCIE.com.au4

0

10

20

30

40

50

60

70

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

$ billion

Australian Government health expenditureState and Territory Government health expenditureNon-Government health expenditure

Average annual growth in spending per person2002-03 − 2007-08

Average annual growth in spending per person2008-09 − 2012-13

3.3 3.9 3.3 4.24.02.3

Consistent increase in non-Govt spending with growth in 2012-13 at a decade high

Source: AIHW health expenditure database

Everyone is spending more on hospitals■ Hospital spending accounts for 38% of health spending, but

takes the lions share of state and territory health budgets (70%), and is increasing as a share of non-government health spending (27%)

■ PHI’s hospital spending budget is increasingly making room for public hospital spending

■ Policy is driving up individual spending on hospitals. Following the 2008 increase in the MLS income threshold, growth in individual spending on hospitals has averaged 25%, compared to 6% for PHI and 4% for government

■ Individual spending on private hospitals has been strongest, averaging 31% p.a. over past 5 years, possibly reflecting the drift to exclusionary and excess/ co-payment products

www.TheCIE.com.au5

Chart 5: Spending on hospitals as a % of total funding by source

www.TheCIE.com.au6

Source: AIHW health expenditure database

37.0%

64.1%

25.2%

32.8%

69.5%

27.4%

AustralianGovernment

State andTerritoryGovernment

Non-Government

Outer rim = 2012-13 Inner rim = 2002-03

Chart 6: PHI’s growing role in public hospital funding

www.TheCIE.com.au7

Source: AIHW health expenditure database

84.0%

85.0%

86.0%

87.0%

88.0%

89.0%

90.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

Shar

e of

tota

l spe

ndin

g

Public hospital (LHS)

Private hospital (RHS)

$3.6bn

$5.7bn$418m

$904m

Key policy drivers impacting on individual health spend■ Medicare pays 75% of scheduled fee for private patients in

public/private hospital, and 85% of scheduled fee for a specialist, patients pay gap plus any above-schedule fee

■ 2010-11 Medicare levy introduced (1.5%). 1 July 2012 new income thresholds introduced with higher rates of the surcharge for high income earners

■ 1 July 2015, general patients pay $5 for each PBS prescription and $145.30 more to reach the safety net for concessional rate (lesser rises for concession card holders)

■ 1 July 2015, patients may pay (optional) $5 towards bulk billed standard GP consults and out-of-hospital pathology and imaging services. States and Territories allowed to introduce contributions for GP equivalent visits to EDwww.TheCIE.com.au8

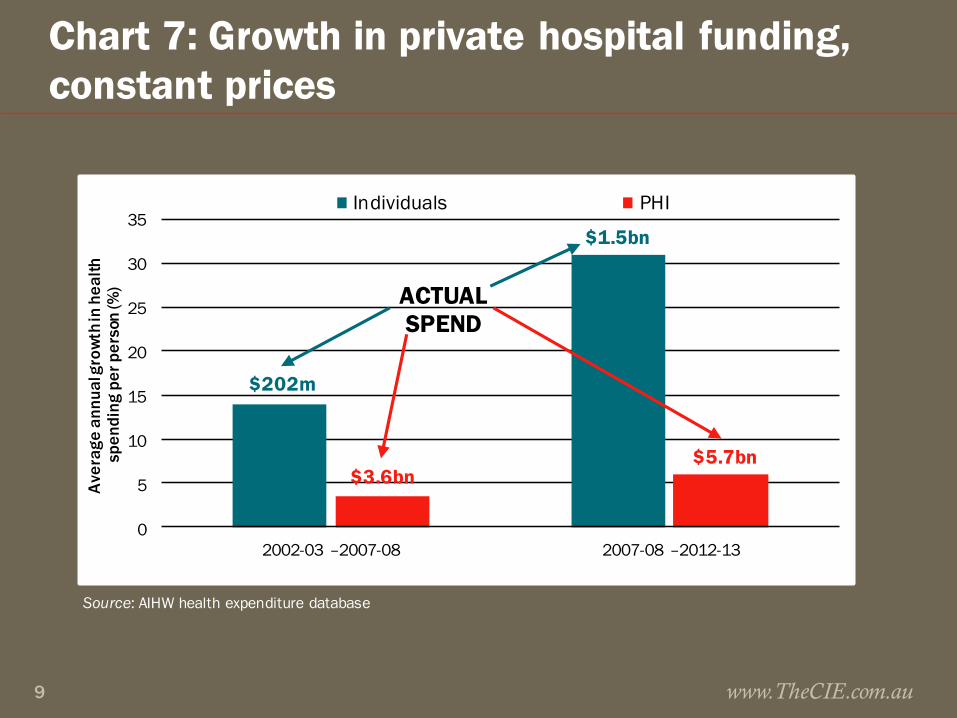

Chart 7: Growth in private hospital funding, constant prices

www.TheCIE.com.au9

Source: AIHW health expenditure database

0

5

10

15

20

25

30

35

2002-03 –2007-08 2007-08 –2012-13

Ave

rage

ann

ual g

row

th in

hea

lth

spen

ding

per

per

son

(%)

Individuals PHI

$202m

$3.6bn$5.7bn

$1.5bn

ACTUALSPEND

PHI premium increases consistently above CPI because of benefits expenditure growth

www.TheCIE.com.au10

Source: Department of Health and ABS

0

1

2

3

4

5

6

7

8

2010 2011 2012 2013 2014 2015*

Annual % change

year to March 2015

Weighted average industry premium increase MBF Bupa CPI

Premium growth well above CPI

Source: Department of Health and ABS

Chart 9: Premium increases across the industry and for the largest PHIs

But as you would expect given growth in benefits expenditure

www.TheCIE.com.au11

Source: PHIAC

6 000

8 000

10 000

12 000

14 000

16 000

18 000

2009 2010 2011 2012 2013 2014

$

Chart 8: Hospital and General Treatment Benefits

Future cost of health care: … up some more

■ Currently >25% of Aust. Government spending is for health, age–related pensions and aged care

■ In GDP terms, Australian Government spending on health is forecast to rise the most in % of GDP terms, widening the spending gap between health and all other areas of Australian Government funding

www.TheCIE.com.au12

Health spending projections foretell ongoing pressure to share the funding burden

www.TheCIE.com.au13

Source: Commonwealth Treasury projections, Intergenerational Report 2015

0

1

2

3

4

5

6

2014-15 2024-25 2034-35 2044-45 2054-55

% of GDP

Health Aged careAge and service persions Other income supportEducation NDISPublic sector superannuation Defence

Health dominates spending growth

Chart 10: Projected Australian Government spending by category

Forecast spending confirms Govt emphasis on primary care, leaving increases in other spending to be met by non-Govt

■ No planned increase in real per person expenditure on the PHI rebate, which will be flat for next 15 years ($280 in 2014-15 to $283 in 2027-28

■ Medicare will growth the most from $855 to $1071 per person

■ Pharma spending to rise from $420 to $474 per person

■ Public hospital spending to rise from $647 to $680 per person

www.TheCIE.com.au14

Commonwealth prioritises primary care for growth spending

www.TheCIE.com.au15

Source: Treasury projections, International Report 2015.

0

200

400

600

800

1 000

1 200

Medicare services Pharmaceuticalspending

Funding for publichospitals

PHI rebate

2014-15 2027-28Strongest growth in

primary care and non-hospital interventions

Low and flat

Chart 11: Projected health spending per person, real terms

This signals wider purposeful shift away from hospital care to early intervention

■ Hospital and PHI funding increase only in line with population and CPI growth (CPI assumed to be < than premium ↑)

■ Medicare and pharmaceutical benefits increase in line with both CPI/population growth and non-demographic factors (in line with age based historical use patterns)

www.TheCIE.com.au16

Why are health costs rising like they are? .. mostly because of the things we do

■ Much talked about population ageing will fuel growth ■ Real health spending on 65+ to rise seven fold

■ Real health spending on 85+ to rise twelve fold

www.TheCIE.com.au17

■ But it is increasing demand for health services that really takes off

Chart 12: Australian Government spending on health: 2009-10 dollars

Source: Treasury projections, Intergenerational Report 2010

Most recent Treasury projections point to non-demographic factors driving health costs

■ Out to 2027-28 Treasury forecasts non-demographic factors will be the largest contributor (80%) to growth in real per person health spending

■ Ageing contributes just 10%■ Projected pharmaceutical benefits spending is four times

higher for 85+ years than the average person across all years

■ Projected public hospital spending is four times higher for 85+ years than the average person across all years

Source: Treasury projections from the 2015 Intergenerational Report www.TheCIE.com.au18

It is our needs, wants and options that are changing

■ Higher incomes bring increased preferences to consume more and/or better health services

■ Technology change increases demand and price (eg. Keyhole surgery is a better/more expensive way of treating same condition

■ Changes in disease rates (esp. chronic disease) increases demand for treatments

■ Wages growth >CPI leads to price growth in labour intensive industries, including hospitals and medical services

www.TheCIE.com.au19

Chart 13: Components of change in health costs 2002-03 to 2032-33 ($bn of 2006-07 dollars)

DiseaseAgeing Population Disease

rateVolume per case

Treatment proportion

Price

Cardiovas. 6.39 3.71 -3.18 4.15 0.68 1.49Respiratory 0.49 -0.03 0.58 12.42 0.00 1.30Injuries 1.19 2.46 -1.66 4.69 0.00 1.03Dental -0.14 2.79 -0.11 6.05 0.00 0.44Mental -0.06 2.20 0.18 4.39 0.00 0.26Digestive 1.55 2.75 0.36 6.75 0.00 0.19Neurolog. 8.09 2.98 0.63 4.28 0.00 0.86

Total 37.75 34.38 -2.29 81.30 1.03 8.84

www.TheCIE.com.au20

■ Almost all of the top 7 diseases driving up costs are most affected by volume per case

■ Volume per case is more than double as costly as any other cost driver

Source: AIHW Disease expenditure projection model

Concluding thoughts..

■ Health spending pressure will make cost sharing inevitable, and price signals will increasingly be used to ration health services: look out for some rebalancing of the access vs quality compromise

■ Arguably unlikely to get additional Government sponsorship of PHI, policy momentum from sector likely to be to preserve the status quo

■ Can more be done to get more market signals into healthcare? Arguably yes, healthcare is very regulated but arguably mature enough to get equitable outcomes from greater market freedoms

www.TheCIE.com.au21