saudi arabia - thaihalalfoods.com · saudi arabia food industry swot strengths saudi arabia boasts...

TRANSCRIPT

Q3 2012www.businessmonitor.com

food & drink report

iSSn 1749-2920published by Business Monitor international Ltd.

SAUdi ArABiAINCLUDES BMI'S FORECASTS

Business Monitor International 85 Queen Victoria Street London, EC4V 4AB UK Tel: +44 (0) 20 7248 0468 Fax: +44 (0) 20 7248 0467 Email: [email protected] Web: www.businessmonitor.com

© 2012 Business Monitor International. All rights reserved. All information contained in this publication is copyrighted in the name of Business Monitor International, and as such no part of this publication may be reproduced, repackaged, redistributed, resold in whole or in any part, or used in any form or by any means graphic, electronic or mechanical, including photocopying, recording, taping, or by information storage or retrieval, or by any other means, without the express written consent of the publisher.

DISCLAIMER All information contained in this publication has been researched and compiled from sources believed to be accurate and reliable at the time of publishing. However, in view of the natural scope for human and/or mechanical error, either at source or during production, Business Monitor International accepts no liability whatsoever for any loss or damage resulting from errors, inaccuracies or omissions affecting any part of the publication. All information is provided without warranty, and Business Monitor International makes no representation of warranty of any kind as to the accuracy or completeness of any information hereto contained.

SAUDI ARABIA FOOD & DRINK REPORT Q3 2012 INCLUDES 5-YEAR FORECASTS TO 2016

Part of BMI’s Industry Survey & Forecasts Series

Published by: Business Monitor International

Copy deadline: May 2012

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 2

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 3

CONTENTS

BMI Industry View ............................................................................................................................................ 5

SWOT Analysis ................................................................................................................................................ 7

Saudi Arabia Food Industry SWOT........................................................................................................................................................................ 7 Saudi Arabia Drink Industry SWOT ....................................................................................................................................................................... 8 Saudi Arabia Mass Grocery Retail Industry SWOT ............................................................................................................................................... 9

Business Environment .................................................................................................................................. 10

BMI’s Core Global Industry Views ........................................................................................................................................................................... 10 Table: BMI’s Core Views ..................................................................................................................................................................................... 20

Middle East Food & Drink Risk/Reward Ratings ..................................................................................................................................................... 21 Table: MENA Risk/Reward Ratings Subcategories, Q312 (scores out of 10) ....................................................................................................... 21 Table: MENA Food & Drink Risk/Reward Ratings, Q312 ................................................................................................................................... 25

Saudi Arabia Food & Drink Business Environment Rating ...................................................................................................................................... 26 Macroeconomic Outlook ........................................................................................................................................................................................... 27

Table: Saudi Arabia – Economic Activity ............................................................................................................................................................ 33

Industry Forecast Scenario .......................................................................................................................... 34

Consumer Outlook .................................................................................................................................................................................................... 34 Food .......................................................................................................................................................................................................................... 36

Food Consumption ............................................................................................................................................................................................... 36 Table: Food Consumption Indicators – Historical Data & Forecasts ................................................................................................................. 37 Confectionery ....................................................................................................................................................................................................... 37 Table: Confectionery Value Sales – Historical Data & Forecasts ....................................................................................................................... 38

Drinks ....................................................................................................................................................................................................................... 38 Soft Drinks ........................................................................................................................................................................................................... 38 Table: Soft Drinks Value Sales – Historical Data & Forecasts ........................................................................................................................... 39 Alcoholic Drinks .................................................................................................................................................................................................. 40 Hot Drinks ........................................................................................................................................................................................................... 40 Table: Hot Drinks Value Sales – Historical Data & Forecasts ............................................................................................................................ 41

Mass Grocery Retail ................................................................................................................................................................................................. 42 Table: Mass Grocery Retail Sales – Historical Data & Forecasts ....................................................................................................................... 43 Table: Mass Grocery Retail Sales By Format ...................................................................................................................................................... 43

Trade ......................................................................................................................................................................................................................... 44 Table: Trade Indicators – Historical Data & Forecasts ...................................................................................................................................... 44

Food ................................................................................................................................................................ 45

Key Gulf Region Industry Trends And Developments ............................................................................................................................................... 45 Almarai Investing In Diversification .................................................................................................................................................................... 45 New Products And Frontier Markets ................................................................................................................................................................... 46 Growing Investment Interest From Multinational Corporations .......................................................................................................................... 46 Growing Popularity Of Eating Out ...................................................................................................................................................................... 47

Market Overview ....................................................................................................................................................................................................... 48 Food Processing .................................................................................................................................................................................................. 48 Dairy Processing ................................................................................................................................................................................................. 49 Agriculture ........................................................................................................................................................................................................... 50 Halal .................................................................................................................................................................................................................... 51

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 4

Drink ................................................................................................................................................................ 52

Key Gulf Region Industry Trends And Developments ............................................................................................................................................... 52 Bottled Water Sector Growing in Importance ...................................................................................................................................................... 52 Frontier Market Investment Strengthening .......................................................................................................................................................... 52 Carbonates Shake-Up .......................................................................................................................................................................................... 53 Diversifying Away From Carbonates ................................................................................................................................................................... 53

Market Overview ....................................................................................................................................................................................................... 54 Soft Drinks ........................................................................................................................................................................................................... 54 Hot Drinks ........................................................................................................................................................................................................... 55 Alcoholic Drinks .................................................................................................................................................................................................. 55

Mass Grocery Retail ...................................................................................................................................... 56

Key Gulf Region Industry Trends And Developments ............................................................................................................................................... 56 Foreign Retailers Looking At Saudi Arabia ......................................................................................................................................................... 56 Frontier Market Investment ................................................................................................................................................................................. 56 Growing Investment Into Modern Convenience Retailing .................................................................................................................................... 57

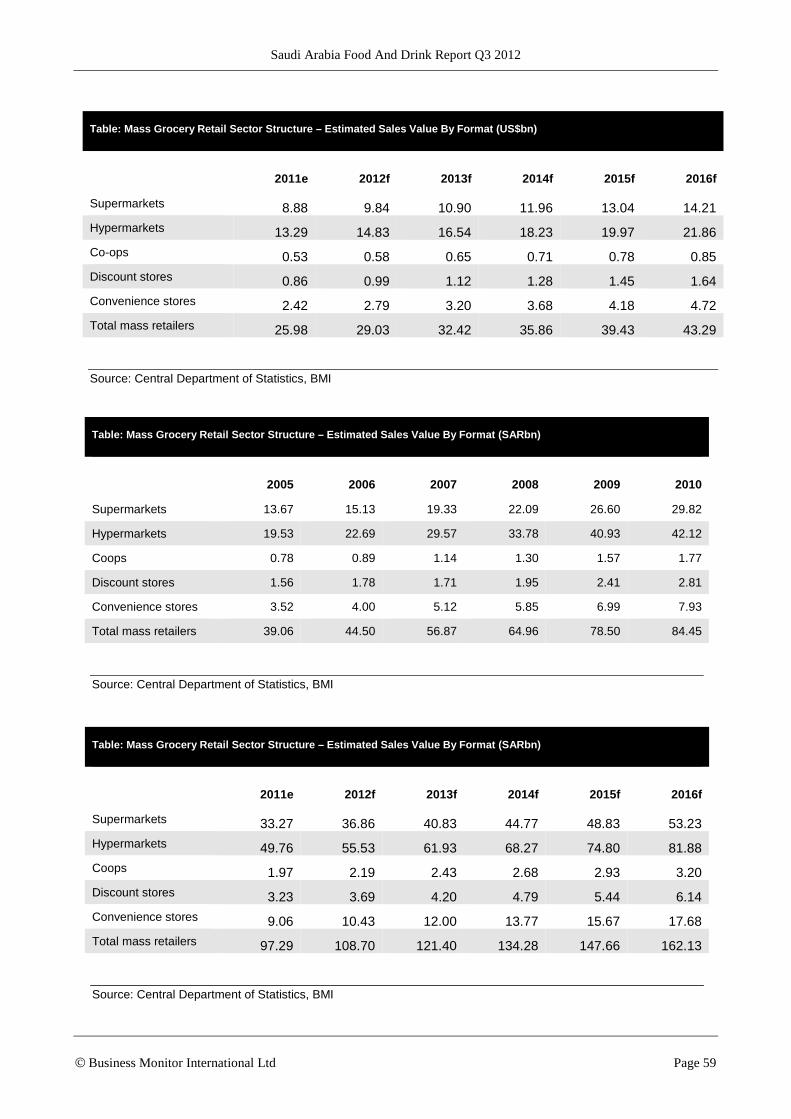

Market Overview ....................................................................................................................................................................................................... 58 Table: Mass Grocery Retail Sector Structure – Estimated Sales Value By Format (US$bn) ............................................................................... 58 Table: Mass Grocery Retail Sector Structure – Estimated Sales Value By Format (US$bn) ............................................................................... 59 Table: Mass Grocery Retail Sector Structure – Estimated Sales Value By Format (SARbn) ............................................................................... 59 Table: Mass Grocery Retail Sector Structure – Estimated Sales Value By Format (SARbn) ............................................................................... 59

Competitive Landscape ................................................................................................................................ 60

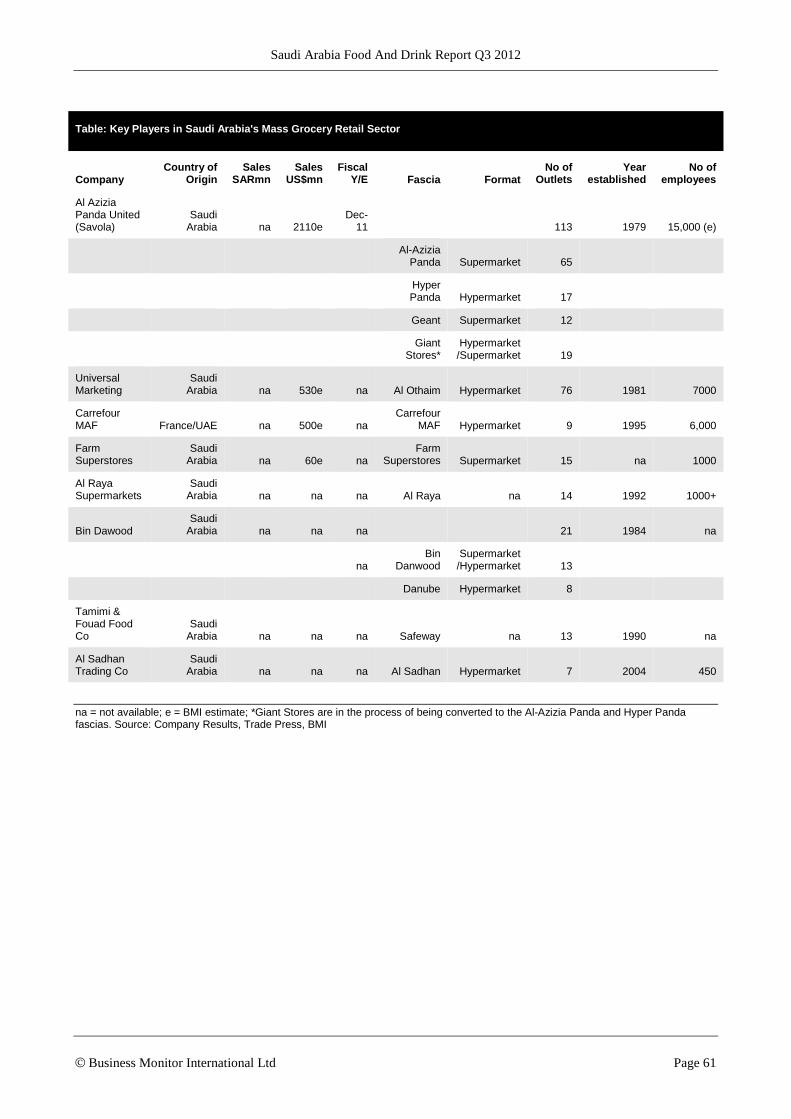

Table: Key Players in Saudi Arabia's Food & Drink Sector ................................................................................................................................ 60 Table: Key Players in Saudi Arabia's Mass Grocery Retail Sector ...................................................................................................................... 61

Company Monitor .......................................................................................................................................... 62

Food .......................................................................................................................................................................................................................... 62 Al Safi-Danone ..................................................................................................................................................................................................... 62 Saudi Dairy & Foodstuff Company (SADAFCO) ................................................................................................................................................. 64 Almarai ................................................................................................................................................................................................................ 65 Al Rabie Saudi Foods ........................................................................................................................................................................................... 66

Drink ......................................................................................................................................................................................................................... 67 Aujan.................................................................................................................................................................................................................... 67

Mass Grocery Retail ................................................................................................................................................................................................. 69 Savola Group – Al Azizia Panda .......................................................................................................................................................................... 69 Carrefour MAF – Saudi Arabia ........................................................................................................................................................................... 71

BMI Methodology ........................................................................................................................................... 72

Risk/Reward Ratings Methodology ............................................................................................................. 72

Table: Rewards .................................................................................................................................................................................................... 72 Table: Risks ......................................................................................................................................................................................................... 73

Weighting .................................................................................................................................................................................................................. 73 Table: Weighting.................................................................................................................................................................................................. 73

BMI Food & Drink Industry Glossary ........................................................................................................... 74

Food & Drink............................................................................................................................................................................................................ 74 Mass Grocery Retail ................................................................................................................................................................................................. 74

BMI Food & Drink Forecasting & Sourcing ................................................................................................. 76

How We Generate Our Industry Forecasts ............................................................................................................................................................... 76 Sourcing ............................................................................................................................................................................................................... 77

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 5

BMI Industry View

Our outlook for the Saudi Arabian consumer sector remains bright, in line with the latest economic

indicators. The Saudi Arabian economy is currently firing on all cylinders, as high oil prices, heavy

government spending and buoyant consumer confidence continue to drive growth. Consumers in Saudi

Arabia are benefitting from heavy government spending and easy monetary policy, and our outlook for

household consumption remains upbeat. Across the board, consumption-related data paint a positive

picture. Moreover, leading indicator data also remain broadly encouraging. The YouGov consumer

confidence index is close to four-year highs. Government consumption will also remain a major driver

throughout the year. It has long been our view that the political tension stirred up by the Arab Spring

would lead to a sustained increase in public spending on healthcare, education and other social services,

as a means placating the population. We have revised up our forecast for real GDP growth in 2012 from

4.6% to 5.3%, though we still expect growth to slow next year as the impact of government spending

begins to fade.

Headline Industry Data

2012 per capita food consumption growth in local currency = 9.0%; forecast growth 2011-2016

= 40.0%

2012 confectionary value sales growth = 12.0%; forecast growth to 2016 = 46.5%

2012 mass grocery retail sales growth = 11.7%; forecast growth to 2016 = 66.6%

Key Company Trends

Fast Food Attracting More Investments: The fast food sector in Saudi Arabia is continuing to grow in

importance and is forecast to be worth around US$4.5bn by 2015. In May 2012 American burger chain

Burger King opened their 65th and largest-yet Saudi restaurant in Riyadh. The Burger King brand is

managed by HANA International, a subsidiary of Olayan Financing Company in the Middle East and

North Africa. The company has said that Saudi Arabia is a key growth market, and that it will continue to

be a focal point for their investment strategy in the Middle East.

Drinks Tax Ahead?

In May 2012 it was reported that the GCC states are considering a 50% tax on beverages and cigarettes to

control consumption. At a meeting of health ministers held in Saudi Arabia, the tax was discussed,

pointing out that soft drinks prices in the region are far lower than in most other parts of the world, and

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 6

that the consumption of these drinks is a key factor in the spread of diabetes among children. If such a tax

were to be implemented, it would have a major impact on the sale of soft drinks throughout the region.

Key Risks To Outlook

Given the extent to which our forecasts rely on heavy government spending, and by extension elevated oil

prices, a sharper-than-expected downturn in the global economy, if it was to translate into a substantial

decline in oil prices, would pose significant downside risks to our forecasts for Saudi Arabia's fiscal and

current account position, though it remains highly unlikely that either account will fall into the red in the

near term.

A more pressing concern is the potential for a sharp acceleration of inflation. With the economy

experiencing a prolonged period of robust growth amid loose monetary and fiscal policy, there is a

significant risk that upside price pressures could pick up rapidly in the medium term, putting pressure on

consumer spending. While we expect consumer price inflation to remain relatively subdued in 2012 as

global commodity prices moderate and spending on subsidies stays high, over the medium term inflation

is a problem that is likely to come increasingly into focus.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 7

SWOT Analysis

Saudi Arabia Food Industry SWOT

Strengths Saudi Arabia boasts the Gulf region’s largest dairy industry.

With a youthful population of more than 28mn, which is increasingly susceptible to Western consumer trends, Saudi Arabia is a good regional point of entry for investors seeking long-term volume growth.

Like the rest of its Gulf peers, Saudi Arabia is home to a vast expatriate population able to consume high-value packaged and processed foods.

Saudi Arabia is a member of the Gulf Cooperation Council common market and provides a lower-cost export base than some neighbouring countries.

The Middle East and North Africa political crisis has possibly made Saudi Arabia seem more secure as an investment destination relative to some other countries in the region.

Weaknesses Saudi consumers are more price conscious than those in the UAE, Kuwait or Qatar.

Saudi Arabia has a saturated dairy industry with little room for new dairy manufacturers to enter.

The private sector’s dependence on expatriate labour is a burden for potential investors.

Food manufacturers are highly dependent on imports for ingredients due to the country’s severe agricultural shortcomings.

Opportunities Demand for processed and packaged goods among Saudi consumers is set to continue increasing as tastes and preferences evolve and lifestyles become busier.

Long-term opportunities for premiumisation remain across all segments of the food industry.

Rising health consciousness has significantly increased opportunities for food producers that are able to introduce ‘healthy’ or ‘light’ options.

Demand for organic foods is steadily increasing.

Threats Demand for higher-value foods fell in 2009, and, despite recent improvements, consumer confidence remains way off pre-2009 highs.

Poverty levels remain quite high despite the country’s oil wealth and generous government handouts.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 8

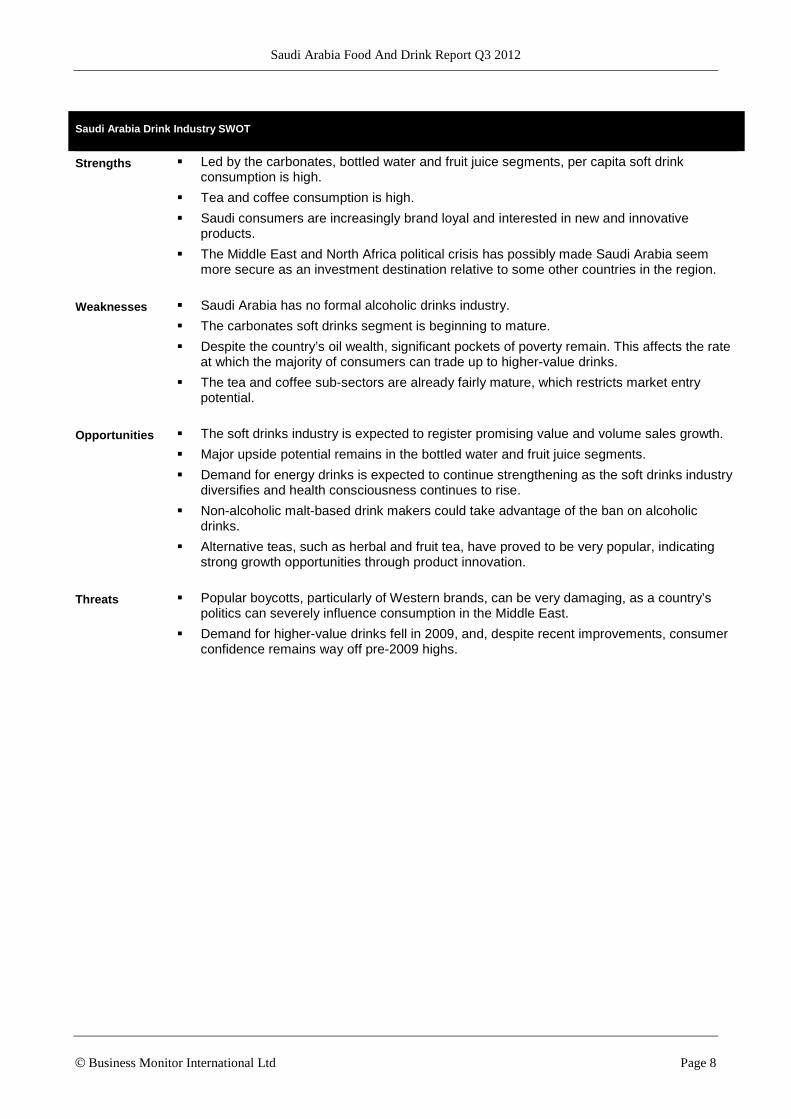

Saudi Arabia Drink Industry SWOT

Strengths Led by the carbonates, bottled water and fruit juice segments, per capita soft drink consumption is high.

Tea and coffee consumption is high.

Saudi consumers are increasingly brand loyal and interested in new and innovative products.

The Middle East and North Africa political crisis has possibly made Saudi Arabia seem more secure as an investment destination relative to some other countries in the region.

Weaknesses Saudi Arabia has no formal alcoholic drinks industry.

The carbonates soft drinks segment is beginning to mature.

Despite the country’s oil wealth, significant pockets of poverty remain. This affects the rate at which the majority of consumers can trade up to higher-value drinks.

The tea and coffee sub-sectors are already fairly mature, which restricts market entry potential.

Opportunities The soft drinks industry is expected to register promising value and volume sales growth.

Major upside potential remains in the bottled water and fruit juice segments.

Demand for energy drinks is expected to continue strengthening as the soft drinks industry diversifies and health consciousness continues to rise.

Non-alcoholic malt-based drink makers could take advantage of the ban on alcoholic drinks.

Alternative teas, such as herbal and fruit tea, have proved to be very popular, indicating strong growth opportunities through product innovation.

Threats Popular boycotts, particularly of Western brands, can be very damaging, as a country’s politics can severely influence consumption in the Middle East.

Demand for higher-value drinks fell in 2009, and, despite recent improvements, consumer confidence remains way off pre-2009 highs.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 9

Saudi Arabia Mass Grocery Retail Industry SWOT

Strengths Saudi Arabia’s organised grocery retail sector is the Gulf region’s largest by value.

The hypermarket segment is particularly well established.

Saudi Arabia has the Gulf region’s largest population.

High disposable incomes among a proportion of the population have created an aspirational consumer base interested in premium products.

The Middle East and North Africa political crisis has possibly made Saudi Arabia seem even more secure as an investment destination relative to some other countries in the region.

Weaknesses The entry of hard discounters is highly unlikely as consumers continue to associate discounted goods with poor quality.

The convenience segment remains underdeveloped.

The severe constraints on women’s public participation inhibit their ability as a demographic to maximise their consumer spending power.

With women being prevented from driving, out-of-town hypermarkets and malls are beyond their reach unless they have access to a driver.

Opportunities Non-organised retail and independent outlets still account for nearly half of total sales, which is strong evidence that significant scope remains for the penetration of organised grocery retailing.

Room for store launches across both the high-value hypermarket and supermarket segments still exists.

Mass grocery retail outlets are clustered around major cities, and a number of secondary towns remain underserviced.

Over the longer term, the underdeveloped convenience store segment could be boosted by the development of community stores, which would allow retailers to target more specific geographical locations.

More effective marketing by retailers could boost demand for private label goods, which are currently restricted by misplaced concerns over quality.

Threats Demand for higher-value goods fell in 2009, and, despite recent improvements, consumer confidence remains way off pre-2009 highs.

Poverty levels remain quite high despite the country’s oil wealth and generous government handouts.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 10

Business Environment

BMI’s Core Global Industry Views

The global food and drink (F&D) markets are facing mixed headwinds in the short term. A continued

moderation in food price pressure, as well as an improving demand climate in the US, should provide a

much-needed reprieve to global F&D producers and exporters. However, we continue to see domestic

demand uncertainties in the majority of developed F&D markets such as Japan, Australia and Europe,

which will present a host of demand challenges to local consumer-facing firms.

Over the longer term, the key themes of geographical and product diversification, such as diversification

away from emerging markets to frontier markets, will continue to feature strongly in the growth strategies

of global F&D companies.

Food Inflation Less Of An Issue In 2012

Food Price Pressure To Wane In 2012

Commodity Prices

f = BMI forecast. Source: Bloomberg, BMI

Food inflation was a major theme that largely dictated the earnings performances of F&D companies in

2011. The latest results from US food producers Conagra and General Mills continue to point to the

difficulty that firms are having in passing on increased commodity costs at a time when the consumer

sector remains weak. For the six months through to November 27, Conagra registered an 8.8% increase in

revenue but net income was down by 26% and operating incomes fell by 2.2%, with profits at its

consumer food business off by 6.9%. For the same period, General Mills registered a 13.7% increase in

sales but a 21.5% drop in its net income and a 14.4% decline in its operating profit. Both firms partly

attributed the drop in operating income to rising commodity costs.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 11

However, in line with one of BMI’s short-term core views that commodity prices will continue to

moderate and pose less of a threat to consumer goods producers and retailers, there have already been

gradual improvements in the earnings performances of some of the major F&D players. Both Conagra

and General Mills registered an improvement in their second quarter ending on November 27. Conagra’s

operating profit for this period was up by 2.8%, thanks to the strength of its commercial food business,

while General Mills’ operating profit fell by a slightly less rapid rate, coming in 12.9% lower.

We think this pattern of gradual improvement is set to continue over the coming months. Our

Commodities team forecasts additional relief for producers. Fundamentally, the global agriculture market

remains better supplied than it was during the 2008 food crisis, implying lower risks of food price

inflation occurring as a result of supply shortages. Secondly, government policies aimed at protecting the

end consumer from food price appreciation, such as releasing government stocks, will continue to

mitigate the impact of higher food prices. Lastly, a global economic slowdown is likely to depress

demand and taken together these factors mean we forecast lower average prices for most agricultural

commodities during 2012 (see table).

Domestic Demand Uncertainties Abound In Developed Markets

US Consumer Improving, Demand Sluggish In Australia And Japan

US, Japan And Australia Private Consumption Growth In Local Currency, % chg y-o-y

f = BMI forecast. Source: Australian Bureau of Statistics, Japanese Cabinet Office, US Bureau of Economic Analysis

We maintain our expectation of a subdued demand environment in developed markets such as Australia

and Japan. The Australian consumer will continue to face troubles that will hamper its consumption and

we expect growth in private consumption to slow, coming in at 1.5% in 2012 and 1.7% in 2013 (see

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 12

chart). As interest rates rise and debt repayments grow, a larger proportion of disposable income will be

used to repay debt, forcing households to cut back on the consumption of goods. With the announcement

of job cuts by a number of financial institutions and manufacturers, a poor employment outlook is likely

to put a further drag on private consumption activity as consumers look to save more for the uncertain

times ahead.

In Japan, the temporary boost to private consumption in the aftermath of the Tōhoku earthquake and

tsunami has already given way to structural weakness. Faced with domestic demand pressure, Asahi

experienced a decline of 4.7% in its domestic alcoholic drinks sales in FY2011. Similarly, Sapporo and

Kirin reported declines of 4.0% and 9.5% respectively in their domestic alcoholic drinks sales for the 12

months ending in December 2011. With weak asset prices putting pressure on consumer purchasing

power, we believe the Japanese consumer will maintain a conservative stance over the coming quarters,

though factors such as a strong currency and low unemployment should provide some support to domestic

demand.

While consumer goods producers will continue to face demand headwinds in Australia and Japan in the

coming quarters, the short-term future for the US consumer is looking brighter. Although a full recovery

of the US housing market could take several years to play out and will be marred by volatility, we believe

the recovery could start to accelerate over the coming months from extremely depressed levels. With

unemployment edging down towards 8% and initial jobless claims continuing to decline, the trend in

labour market metrics is slowly improving. These dynamics are typically positive for sentiment and

purchasing power.

Improving Demand Climate In US Prompts Loosening Of Purse Strings

While the value theme will remain well entrenched across the developed world in the near future,

particularly in markets such as Japan and Australia, there are signs that an improvement in consumer

confidence is fuelling a gradual shift of consumption away from the private label and discount retail

sectors in the US. US private label specialist TreeHouse Foods has been forced to issue a profit warning

after registering a drop in volumes during the fourth quarter of 2011. The firm reported that its volumes in

December fell by 8% and this major sales decline during the important festive period potentially points to

a wider movement away from the private label sector amid improving domestic demand conditions. The

latest results posted by US discount retailer Family Dollar also fit with our view that the discount retail

format’s rate of growth could be set to gradually decline as the US economic situation improves. Family

Dollar registered total sales growth of 7.6% for its fiscal first quarter (ending November 26 2011), but

comparable-store sales growth came in at a more muted 4.1%, which compares unfavourably with its

Q110 like-for-like sales growth of 6.9%.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 13

EM-Oriented Companies To Perform Strongly

Casino Outperforming Tesco And Carrefour

Selected MGR Companies Share Prices (rebased 14/3/2011)

Source: Bloomberg

Bearing out one of our core views that companies with a strong emerging markets (EMs) profile will

continue to outperform, France-based retailer Casino posted solid results for 2011, when rivals Tesco,

Carrefour and Walmart struggled to make much headway. Of the major retailers based in developed

markets, it is Casino rather than Walmart or Tesco that has greatest exposure to EMs. For 2011, Casino

registered an 18.2% year-on-year (y-o-y) increase in sales, while net income increased by 6.6%. This

robust sales showing was thanks to changes in its consolidation scope, with the company buying up

Carrefour’s operations in Thailand, upping its stake in Brazil’s CBD and benefiting from the merger of

CBD with local electronics good specialist Casas Bahia. Casino’s well-balanced portfolio has helped its

share price outperform most of its global rivals since the beginning of 2009 and its strong EM base,

combined with a steady domestic operation, suggests that this outperformance could be set to continue

(see chart above).

The importance of building a strong EM business, particularly when demand in the developed world

remains sluggish, is further underlined by the underperformance of US food firms compared to their

European counterparts. US food firms are generally less exposed to EMs than their European peers (see

chart below). This has meant that on average they have underperformed over the last five years in terms

of organic revenue growth.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 14

However, the major US food

producers are already looking to

address their weakness in this

regard and have been largely

ramping up their expansions in

the EMs through mergers and

acquisitions (M&A). Kellogg

announced the purchase of

Pringles from Proctor &

Gamble (P&G) for US$2.7bn.

Kellogg has always been in a bit

of a tricky situation because

cereal is not a common option in

key EMs such as China and

India, while future growth is also

hampered by high levels of

lactose intolerance in many

major EMs. On this front,

Kellogg’s acquisition of popular snack brand Pringles should allow it to circumnavigate the unique

consumer preferences in the EMs, facilitating its expansionary ambitions. A second move is General

Mills’ reported acquisition of Brazil-based Yoki in a deal worth US$1.2bn. We estimate that General

Mills only derives 10% of its revenues from EMs, but with this acquisition, which has yet to be officially

confirmed, this would rise to 13.5%, showing how quickly things can change if firms are willing to

invest. Other US companies that are keen to be making these types of acquisitions are Heinz, Campbell

Soup, Hershey and Sara Lee. All will be anxious to increase their EM exposure and will be sizing up

which markets and categories offer the best opportunities.

For Heinz and Hershey, the route to international growth looks relatively straightforward. Heinz has

already found success for its core condiment portfolio in markets such as Russia and Mexico, and looks

like it has a portfolio that is well suited to EM expansion. In contrast, Campbell Soup has struggled in

EMs, with packaged soup having failed to find a receptive market in countries where homemade soup is

often a cheap staple. The firm may therefore need to copy Kellogg’s example and branch out into a new

category if it is to benefit from the EM opportunity.

The opportunities on offer in EMs may be difficult to exploit for some consumer-facing companies.

Global consumer goods players Nestlé and Danone are overhauling their business models in China amid

intensifying domestic competition. Chinese dairy companies Mengniu and Yili, for example, are looking

to capture a greater market among the country’s middle classes by innovating and introducing more

upmarket products. While better product quality and stronger brand appeal were typically viewed as the

European Firms In Front

Revenues From Emerging Markets (%)

Source: Nestlé, investor relations, BMI

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 15

competitive strengths of foreign consumer players such as Danone, domestic companies are quickly

catching up.

Faced with the rapid emergence of competition from domestic players, Nestlé plans to shut down one of

its three ice cream factories in China so it can channel more resources into building a stronger foothold in

the higher-end market segments. Nestlé aims to boost sales through distribution channels such as hotels

and restaurants. Danone, meanwhile, is suspending production at its Shanghai yogurt plant as part of its

restructuring strategy to focus on its premium brands in China.

In the retail space, Walmart is facing a tough predicament in China as well. The loss of valuable brand

control and the risk of having brands mismanaged under a franchising model have been cited as some of

the major drawbacks of expanding through this operating model, and these problems have caught up with

Walmart. Walmart has been punished 21 times in Chongqing since 2006 for alleged violations such as

mislabelling products, false advertising and selling products that were already past their expiry dates.

Although Walmart prides itself on offering quality grocery products at low prices, it has struggled to

achieve price leadership against the more cost-effective traditional retailers and has arguably not lived up

to its assurance of providing quality products. Moreover, by positioning itself as a low-end retailer,

Walmart is seemingly striking the wrong chord with its main clientele, which is middle class.

Therefore, we stress the importance for consumer-facing companies to get their strategies and positioning

right in order to really enjoy success in the developing world. For Nestlé and Danone, we believe it would

make strategic sense for them to focus on improving their product quality and further leverage on their

global brand appeal in China, particularly amid dampened consumer confidence in domestically produced

goods. For Walmart, it would probably do better by positioning itself at the higher-end of the Chinese

retail market, as well as providing sales-related incentives to keep its objectives aligned with its

franchisees.

From Emerging To Frontier

While EMs will continue to hold immense appeal to the global F&D players, the flurry of expansionary

activity across the frontier markets is likely to heat up over the coming years as well. Netherlands-based

brewer Heineken boosted its stake in Haitian brewer Brasserie Nationale D’Haiti (Brana) from 22.5%

to 95%, which fits with our core view that major multinationals will increasingly look for frontier market

investments as the opportunities in traditional EMs become scarcer as competition increases. As another

case in point, confectionery producer Mars has started construction of a chocolate facility in Saudi

Arabia. This reflects growing demand for confectionery products in the Middle East, where Mars already

operates a facility in Dubai producing Mars, Galaxy and Snickers bars. Cereal Partners Worldwide, a

joint venture between Nestlé and General Mills, has opened a new factory in Turkey.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 16

The facility required investment of TRY85mn and will supply cereal products to the Turkish market and

14 other countries in the Middle East and North Africa (MENA). The decision to use the country as a

launch pad to the wider region fits with Turkey’s rapidly improving business environment and private

sector mentality. We expect more companies to use the country as a base to expand their reach into the

high-potential markets across MENA.

Pursuing Innovation To Improve Differentiation

Another of BMI’s longer-term core views is the ramping up of product innovation among F&D

companies as they seek differentiation and further market share gains. US coffee giant Starbucks looks

set to roll out its new coffee capsule products across Europe, which have already been launched in the

US, to attempt to gain market share from Nestlé. However, BMI believes this may take a while to make a

meaningful contribution to Starbucks’ results, with the firm facing an uphill battle in tempting consumers

away from Nestlé’s ubiquitous Nespresso format. The company also plans to increase customers’

exposure to Starbucks products in Europe, with the Financial Times reporting that the firm is exploring

ways to sell Starbucks coffee through vending machines and on trains and aeroplanes.

In the US, ruling out the prospect of stronger growth through store expansions, the ramping up of its

product offerings is arguably the most viable strategic option available for Starbucks to secure its

domestic growth prospects. Starbucks’ plans to move into the US alcoholic drinks sector underscore the

importance of product diversification in its growth strategy. However, we are only cautiously optimistic

about this strategy. On the one hand, expansion into alcoholic drinks should support higher margins for

Starbucks. On the other, given that the positioning of Starbucks as a premium coffee giant is already well

entrenched among local consumers, it could potentially lose some of its core customers who are looking

for the ‘Starbucks coffee experience’.

Trans-Asian soft drinks manufacturer Fraser and Neave (F&N) is also looking to get on the innovation

bandwagon to lock in its future prospects. F&N plans to invest more heavily in research and development

to create new products such as its recently launched carbonated soft drink Clearly Citrus to compensate

the potential loss of revenue as a result of the termination of its bottling agreement with The Coca-Cola

Company.

Burgeoning Global Appetite For Functional Foods

Fuelled by growing health awareness and rising consumer affluence, consumers across the global markets

are quickly developing a bigger appetite for functional food products. In a bid to tap into the functional

food potential, Nestlé and Danone are reportedly looking to acquire baby formula producer Wyeth, which

is valued at around US$10bn. The acquisition of Wyeth would present a chance to gain control of a

number of well-known infant formula brands that could expedite their expansion in the fast-growing baby

formula market.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 17

While PepsiCo is gradually calibrating its portfolio away from soft drinks and salty snacks, we have

questioned whether PepsiCo’s starting position puts it in a strong place to capture the opportunities in

healthy categories. It is PepsiCo’s move into the dairy sector that is perhaps the most transformational for

the group. The company’s ambitions in this sector were underlined by the purchase of Russia’s Wimm-

Bill-Dann (WBD) and setting up a joint venture in 2009 with Saudi Arabia’s Almarai.

The response to PepsiCo’s strategy of expanding in the diary sector has been less than enthusiastic among

investors, which fits with our analysis. Consumers worldwide are sometimes willing to put health

concerns aside and indulge themselves. In emerging markets these types of purchases are likely to rise in

line with increased affluence and offset downward pressure from increased health-consciousness.

PepsiCo’s existing portfolio is well tailored to meet this growing demand and an attempt to reshape its

business is likely to require significant funds that could be better spent ensuring it is capable of meeting

the growing demand for ‘fun-for-you’ products in emerging markets. PepsiCo seems to want to transform

itself into Danone and the fear that it is steaming off in a new direction and not playing to its strengths

may be partly behind its recent underperformance.

Coca-Cola And PepsiCo Spearheading Diversification Away From Carbonates

A notable trend in global F&D is the continued diversification among beverage producers away from

carbonated drinks. Over the past quarter, Coca-Cola and PepsiCo were some of the bigger names

spearheading this trend, particularly in EMs. Coca-Cola India is forming an independent business

division to raise its stake in the expanding non-carbonates market, which will be responsible for the

innovation, sale and distribution of juices, energy drinks and powdered drinks. With their sights set firmly

on the opportunities provided by a growing health awareness trend in India, PepsiCo and domestic drinks

producer Tata Global Beverages plan to increase their product portfolio of functional beverages through

their joint venture NourishCo. NourishCo will introduce a new range of functional drinks over the next

18-24 months and it aims to generate overall revenue of INR7bn (US$141.8mn).

Although the low purchasing power of Indian consumers means that the lower-value carbonates are likely

to remain the beverage of choice for most consumers, rising income and an emerging health awareness

trend are fuelling demand for non-carbonates such as fruit juices and energy drinks. Companies such as

Coca-Cola and PepsiCo are likely to accelerate their portfolio expansion initiatives to capitalise on this

opportunity.

Consolidation To Drive M&A Activity

Consolidation will continue rapidly in the global F&D space as companies seek greater efficiencies by

improving their domestic scale. Interestingly, this trend has been largely fuelled by M&A rather than

organic growth, which can be linked to the benefits of achieving immediate scale through inorganic

expansion.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 18

Russian-based vodka producer Russian Standard made an offer to Poland-based Central European

Distribution Corp (CEDC) that could see it take a 32.99% stake in the business. A combination between

Russian Standard and CEDC would create a regional spirits giant, combining Russian Standard’s strength

at the premium end of the market with CEDC’s strength in the economy and mid-price sectors.

Coca-Cola FEMSA continues to drive consolidation in Mexico’s soft drink sector, with the purchase the

drinks arm of Mexican group Fomento Queretano. The deal is worth MXN6.6bn (including MXN1.2bn

of Queretano’s debt) and was FEMSA’s third major acquisition in Mexico’s soft drink sector in 2011.

FEMSA said its acquisitions in Mexico will increase its volumes and revenues by 30%, a substantial

increase in the firm’s exposure to the market. As Mexico’s largest bottler, FEMSA cannot take its eye off

the ball here and we see this consolidation as a sensible strategy given the weakness of the market.

However, over the longer term we think FEMSA will remain primarily focused on international growth;

the structure of the acquisition (based on shares rather than cash) supports our view that the firm is

preparing for major acquisitions outside its domestic market.

Further bearing out the consolidation trend in the global F&D markets, Swedish confectionery producers

Cloetta and Leaf International have announced plans to merge their operations. The combined portfolio

will see Cloetta’s strength in chocolate confectionery complemented by Leaf’s strong position in the

pastilles, gum and sugar confectionery categories, with brands including Cloetta, Läkerol, Malaco, Red

Band and Chewits. We believe it will be in the sugar confectionery area that the combined firm will seek

to drive expansion, with the popular Cloetta brand used to back a number of sugar confectionery products

in the Leaf stable. The merger will also create a firm with the scale to expand internationally, with the

business already having a sizeable base in both Netherlands and Italy.

AB InBev And SABMiller Have Massive Financial Power

Selected Brewers Market Capitalisation, US$mn (LHS) And Debt-To-EBITDA Ratios (RHS)

Y= last financial year, Y-1 = the previous financial year, etc. Source: Bloomberg, investor relations

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 19

More recently, the sale of Chinese brewer Kingway Brewery’s beer assets, which represents an exciting

opportunity for multinational and domestic brewers to consolidate a stronger presence in the Chinese beer

market, has unsurprisingly stirred massive interest among domestic and foreign brewers. China

Resources Snow Breweries (CR Snow), Beijing Yanjing Brewery and Anheuser-Busch InBev (AB

InBev) are reportedly among the frontrunners to make the acquisition. While AB InBev’s massive

financial scale could give it a slight edge over CR Snow, we believe the latter has a good chance of

success in acquiring Kingway’s brewery assets. Through the sale of its non-core assets, as well as fiscal

prudence and strong earnings growth on the back of cost cutting at the acquired Anheuser-Busch

business, AB InBev’s total debt-to-EBITDA ratio has been cut from a five-year high of 7.8 to 3.2 in its

last financial year, implying that it now has a stronger financial capacity for deals (see chart). However,

CR Snow has the backing of its parent company SABMiller, which is also a financial colossus and

certainly has plenty of scope to carry out the acquisition. While Beijing Yanjing Brewery is also in the

running, we believe its smaller financial clout probably places it in a weaker position against the

financially powerful AB InBev and CR Snow.

Private Equity Companies Attracted To Unfashionable Categories

We have introduced a new core view this quarter: private equity (PE) firms will develop a stronger

interest in unfashionable F&D categories. Two deals have highlighted PE’s attraction to relatively

unfashionable parts of the food sector. In the US, Centre Partners announced the acquisition of frozen

food manufacturer Bellisio Foods, while in Europe Manfield Partners acquired two canned food units

from Japanese conglomerate Mitsui & Co. BMI has previously highlighted the sector’s interest in parts

of the industry that are largely stagnant, or even in decline, with the PE industry attracted by the relatively

low valuations and the potential for restoring growth through investment in marketing and innovation.

These PE firms saw a chance to reinvigorate categories that had declined, partly due to a lack of

investment, while being able to pick up major brands for relatively affordable prices. Innovations in the

frozen food sector have since been stepped up, with improvements in taste and convenience filtering

through the sector. Canned food is also a sector in decline in many developed markets but looks

increasingly like an industry in demand by PE firms. The canned food units acquired by Manfield

Partners include seafood, fruit and vegetables in the UK and the Netherlands, with combined revenues of

around GBP75mn. Another canned food producer in the hands of PE owners is US-based Bumble Bee

Foods, formerly owned by Centre Partners but now owned by Lion Capital.

The PE firms investing in these categories will of course be thinking of their eventual exit strategies.

Given the lack of interest from major brand builders, these exits have been primarily through the sale to

another PE fund in the past. However, we expect more deals to take the form of IPOs. A well-run,

steadily expanding food business will always attract defensive investors and the international scale of

companies such Birds Eye Iglo and Findus will certainly make them suitable for a wide variety of

European funds. However, nobody wants to invest in a shrinking category and to ensure that they

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 20

generate a return on the investment these firms will have to continue investing in innovation to win back

consumers that have moved away from the frozen and canned sectors.

Table: BMI’s Core Views

Short-term outlook

Raw material prices will trend lower in 2012 and become less of a threat to producers and retailers.

Developed markets still feeling the pinch with economic weakness and political uncertainty weighing on spending. Tentative signs of improvement in US consumer market.

The value theme is still very important across the developed world, with price consciousness inherent.

Long-term outlook

Companies with strong EM exposure will continue to outperform.

Multinationals will increasingly pursue frontier market investments.

Investment in innovation will increase as producers seek differentiation. Emphasis will be placed on protecting innovations.

Some consumer goods manufacturers will continue to leave sectors under threat from private labels, while others will calibrate their portfolios toward private labels to capitalise on their growing demand.

Government legislation will play an increasing role in marginalising unhealthy food and drink products.

Premiumisation will re-emerge as a key driving force behind revenue growth.

Demand for convenience in retail and food will continue to grow.

Functional foods will provide considerable opportunities in developed markets in particular.

Consolidation will continue as producers seek greater efficiencies.

Beverage companies will continue to invest in diversification away from carbonated beverages and into healthier subsectors.

PE companies will continue to be attracted to unfashionable categories.

Source: BMI

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 21

Middle East Food & Drink Risk/Reward Ratings

BMI’s Risk/Reward Ratings Highlight Most Attractive MENA Food & Drink Markets

BMI’s Middle East and North Africa (MENA) Risk/Reward Ratings (RRRs) assess a market’s

attractiveness to industry investors in comparison with its peers. The rewards part of the rating takes into

account market size, current consumption levels, future industry growth prospects (based on our five-year

industry forecasts), market fragmentation (with greater fragmentation indicating higher opportunities) and

the size of the youth population. The risks part takes into account the legislative environment, the level of

development of the organised retail sector (with higher development leading to lower risks), as well as

relevant aspects of the economic and political environment.

The table below outlines the subcategories that make up each rating and the scores for each market in the

MENA region. The six factors that make up the rewards rating are food consumption per capita, market

fragmentation, per capita food consumption (five-year compound annual growth), population size, GDP

per capita and youth population.

Table: MENA Risk/Reward Ratings Subcategories, Q312 (scores out of 10)

Saudi

Arabia Israel Egypt UAE Qatar Kuwait Oman Bahrain Libya Tunisia Morocco

Rewards

Food consumption per capita 10 10 4 8 9 8 10 9 9 4 2

Market fragmentation 7 1 9 5 4 4 7 2 8 7 7

Per capita food consumption five-year CAGR 4 4 9 3 3 2 3 4 4 5 3

Population size 4 2 7 2 1 1 1 1 2 3 4

GDP per capita, US$ 7 8 2 10 10 10 7 6 5 2 2

Youth population % 6 6 7 3 3 5 5 3 6 4 5

Risks

MGR penetration 5 7 2 6 5 5 3 5 1 1 2

Regulatory environment 6 8 2 7 6 5 4 7 1 5 5

Short term economic risk rating 8 8 5 6 7 7 7 6 5 4 6

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 22

Table: MENA Risk/Reward Ratings Subcategories, Q312 (scores out of 10)

Saudi

Arabia Israel Egypt UAE Qatar Kuwait Oman Bahrain Libya Tunisia Morocco

Income distribution 7 9 7 1 7 7 7 7 7 7 7

Lack of bureaucracy 6 6 4 6 7 6 6 7 4 5 4

Market orientation 6 7 4 6 6 7 4 7 2 5 5

Physical infrastructure 3 7 5 7 5 3 2 5 3 5 3

The Food & Drink Risk/Reward Rating is the principal rating. It comprises two sub-ratings, rewards and risks, which have 60% and 40% weightings respectively. Source: BMI

MENA encompasses a wide range of disparate markets and the table shows there is wide disparity in the

first of these factors, food consumption per capita, with spending very high across most of the Middle

East but low across most of North Africa. Oil wealth means consumers across the Middle East already

spend a significant amount on food. However, this also means the potential for growth is perhaps lower

than in lower-spending countries.

For the second factor, market fragmentation, scores are generally fairly high across the region, indicating

low levels of concentration and the relative ease for a new entrant to come in and quickly capture market

share. On this factor Israel and Bahrain are viewed less favourably, with high levels of concentration in

certain sectors. The North African countries, Oman and Saudi Arabia are viewed more favourably as

these markets are less developed and have significant room for new players in a large number of sectors.

Third, the scores for per capita food consumption (five-year compound annual growth) in MENA are

relatively muted in comparison with the global average. In most Middle Eastern markets spending is

already high, leaving limited room for growth. In many North African countries, while spending is low,

relatively muted economic forecasts mean spending is not expected to increase at the rapid rates seen in

some other emerging markets. The major standout country in the region is Egypt, which is perhaps the

most interesting economy in our RRRs, with the prospect of very strong growth as long as the transition

towards multi-party democracy is successful.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 23

For the fourth factor, population

size, Egypt is again the standout

market, followed by Saudi

Arabia, Morocco and Tunisia.

The rewards scores of other

markets in the region are

hampered by the limited size of

the overall market due to their

smaller populations.

The fifth category, GDP per

capita, is again quite variable,

with a close correlation to the

food consumption per capita. It

is the Middle Eastern countries

that score well in this area,

although Libya’s relatively high

GDP per capita is also a boost to

its rewards rating and to some

extent sets it apart from other North African countries.

This can be attributed to oil wealth and is perhaps a sign of the consumer potential on offer if the

transition towards democracy is successful and the country’s significant natural resources are divided

more equitably. The final factor in the rewards part of the table is youth population. Egypt is yet again

seen most favourably, followed by Saudi Arabia, Libya and Israel. In contrast, the UAE, Qatar and

Bahrain score relatively poorly.

The seven factors that make up the risks rating are MGR penetration, regulatory environment, short-term

economic risk rating, income distribution, lack of bureaucracy, market orientation and physical

infrastructure.

MGR penetration measures the extent to which food retailing is controlled by large, organised retailers.

High penetration is seen as positive from a risk perspective as it eases the distribution of goods and

simplifies the supply process. On a regional basis, MGR penetration is low, with only Israel boasting a

very well developed MGR network. In the Middle East there has been some level of development, with

Saudi Arabia, the UAE, Qatar, Kuwait and Bahrain all attracting some investment in this sector.

However, in North Africa the industry is still in the very early stages of development, with only a handful

of MGR outlets present in each country, which is an impediment to the development of an advanced food

and drink sector.

Saudi Arabia First, Morocco Last

MENA Food & Drink RRRs, Q312

Scores out of 100, with 100 highest. The Food & Drink Risk/Reward Rating is the principal rating. It comprises two sub-ratings, rewards and risks, which have 60% and 40% weightings respectively. Source: BMI

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 24

Regulatory environment evaluates the complexity of factors such as labelling and nutrition requirements.

There is limited regional differentiation and all markets in MENA are viewed relatively favourably from

this perspective. Israel is viewed as the easiest market to navigate in this respect, while Libya is seen as

the most challenging, though much of this can be attributed to hangover from the Qadhafi regime and

could quickly change over the coming months and years.

The third category, short-term economic risk rating, assesses the degree to which the country

approximates the ideal of non-inflationary growth with falling unemployment, contained fiscal and

external deficits and manageable debt ratios. Most Middle Eastern countries score well in this rating,

thanks to a stable track record of growth and a positive growth outlook. Across North Africa the picture is

more mixed, with significant risks inherent in the economies of Egypt, Libya and Tunisia, where the

economic policies of current and future administrations are harder to predict.

The fourth factor, income distribution, is measured by the proportion of private consumption accounted

for by the middle 60% of earners and scores across the region are fairly high, despite the inherent

inequality in many of the economies that are highly dependent on oil. The administrations in each of these

markets recognise that wealth must be distributed to prevent social unrest and they have been fairly

successful in ensuring that the population benefits from the country’s natural oil wealth.

Fifthly, lack of bureaucracy, is a measure of the hurdles that a producer is likely to face in areas such as

starting and closing businesses, paying taxes, dealing with licences and registering property. Scores are

generally average across MENA, with Qatar and Bahrain viewed most favourably and Egypt, Libya and

Morocco still having much to do to be easy places for new entrants to set up shop and for existing players

to expand.

The sixth factor, market orientation, is a measure of how business orientated an economy is, and measures

the level of foreign direct investment protectionism, tax rates and the level of government intervention.

Israel, Kuwait and Bahrain score the highest, while the markets of North Africa are again seen as having

work to do. Libya has the lowest score for the market orientation component, though this could also

change following the overthrow of the Qadhafi regime and the election of an administration that is more

open to foreign investment.

The final risk category, physical infrastructure, measures the ease and cost of operating in a market from

an infrastructure perspective. Infrastructure in Israel and the UAE is seen as relatively well advanced,

though in the rest of the Middle East it is only moderately developed. In North Africa and a number of

Middle Eastern markets, including Kuwait, Oman and Saudi Arabia, the level of infrastructure is seen as a

major additional risk factor and these countries would benefit enormously from increased investment in

this area. This would help to reduce costs for incumbent operators and ease access to more remote areas,

helping to realise the potential of the region’s consumer sector.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 25

Table: MENA Food & Drink Risk/Reward Ratings, Q312

Rewards Risks

Rewards Industry Rewards

Country Rewards Risks

Industry Risks

Country Risks

Food & Drink RRR Rank

Saudi Arabia 59.7 64.0 55.3 57.8 55.0 60.6 58.9 1

Israel 45.3 40.0 50.7 74.2 75.0 73.4 56.9 2

Egypt 68.3 80.0 56.7 36.1 20.0 52.2 55.4 3

UAE 46.5 48.0 45.0 58.7 65.0 52.4 51.4 4

Qatar 43.7 46.0 41.3 58.6 55.0 62.3 49.7 5

Kuwait 44.3 40.0 48.7 54.5 50.0 59.0 48.4 6

Oman 50.3 60.0 40.7 42.6 35.0 50.2 47.2 7

Bahrain 36.3 42.0 30.7 61.9 60.0 63.8 46.6 8

Libya 54.3 66.0 42.7 25.4 10.0 40.8 42.8 9=

Tunisia 43.5 56.0 31.0 41.8 30.0 53.6 42.8 9=

Morocco 41.2 44.0 38.3 42.9 35.0 50.7 41.8 11

Scores out of 100, with 100 highest. The Food & Drink RRR is the principal rating. It comprises two sub-ratings, rewards and risks, which have 60% and 40% weightings respectively. Source: BMI

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 26

Saudi Arabia Food & Drink Business Environment Rating

Saudi Arabia remains at the top of our risk/rewards ratings for the Middle East and North Africa region.

The country’s main competitive edge continues to be its relatively huge population, which accounts for

around two-thirds of the overall Gulf population. The current ratings system places a greater emphasis on

which markets offer the best growth opportunities, rather than which is the most developed. While Saudi

consumers are currently not as high-spending as their Gulf peers in the UAE or Qatar, the market

nevertheless offers better long-term growth, with a decent score for food consumption growth.

Furthermore, not only is the population large, but it is also young, with around half of the population

younger than 25, according to UN estimates.

Saudi Arabia also benefits from a fairly good business environment, even if it is a riskier place to do

business than countries such as the UAE or Bahrain. The new ratings also give greater weight to market

fragmentation, a subjective indicator that assesses how relatively developed a market is. Here Saudi

Arabia receives a score of 7 out of 10, reflecting a fairly developed consumer market. The country’s mass

grocery retail industry is also fairly well developed, allowing companies to get their goods to consumers

more efficiently than in other regional markets. Add to all of this the country’s strong short-term

economic outlook and it’s easy to see why Saudi Arabia has maintained its lead position in our ratings.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 27

Macroeconomic Outlook

Loose Policy Driving Growth

BMI View: We retain our sanguine outlook on Saudi Arabia's growth prospects in 2012. Heavy

government spending, coupled with loose monetary policy, will keep domestic consumption and fixed

investment growing healthily through the year, though we expect the net export position to worsen as oil

production slows.

Macro Strategy: Saudi Arabia's growth outlook remains broadly positive. Throughout 2011, robust

growth was spurred by loose fiscal and monetary policy, and we expect these conditions to persist this

year. With memories of the Arab Spring still lingering, the government is unlikely to risk stirring up

domestic discontent by tightening policy, while still-elevated global oil prices will leave Riyadh with

plenty of room to manoeuvre on the fiscal front. Although oil production is likely to slow as supply from

Libya and Iraq comes back on line, leading to a moderate decline in the net export position, overall we

expect the healthy outlook for domestic consumption and fixed investment to continue driving strong

growth in the medium term.

We forecast real GDP growth of 4.6% in 2012 and 4.1% in 2013, down from an estimated 6.8% last year.

Our projection leaves us above Bloomberg consensus – a survey of research houses and investment

banks – which sees growth coming in at 3.8%. Moreover, we highlight that the risks to our outlook are

relatively minimal, with the potential for a sharp uptick in inflation representing the most substantial

threat to the economy in 2012.

Expenditure Breakdown

Private Expenditure Outlook: We see household consumption holding up well in 2012, pencilling in

real growth of 5.0% through the year. The main driver of this expansion will continue to be government

spending, with public sector wages, social benefits and food and fuel subsidies all having been hiked

substantially in the past year, and unlikely to be reined in while the Arab Spring continues to occupy the

minds of policymakers. Loose fiscal policy has spurred consumer spending, an effect that has been

reflected in a host of leading indicator data showing a strong performance by the domestic private sector.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 28

A Downtick, But Confidence Still High Saudi Arabia – Dun & Bradstreet Business Optimism Index

Source: BMI, Dun & Bradstreet

The HSBC/SABB Purchasing Managers' Index stood at 60.0 in January (a reading above 50 signals

growth in the non-oil sector), a six-month high. In addition, while the non-hydrocarbon component of the

Dun & Bradsteet Business Optimism Index – a survey of confidence among local businesses – took a

slight leg down in Q112, coming in at 54 (against 60 in Q411), but remains the highest reading among the

countries surveyed in the Gulf.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 29

Recovery Well Underway Saudi Arabia – Commercial Bank Lending & Broad Money Supply (M2), % ch. y-o-y

Source: BMI, SAMA

This robust outlook will be further bolstered by loose monetary conditions. Given the riyal's peg to the

dollar, dovish policy at the US Federal Reserve – which has made clear its intention to keep rates low

until 2014 – has forced the Saudi Arabian Monetary Agency to keep its benchmark rate on hold at 2.00%

or risk an inflow of 'hot money'. Easy credit has led to a rapid expansion of the money supply – broad

money supply growth came in at 15.4% y-o-y in December, compared with 9.3% in December 2010 – as

well as a sharp pickup up in commercial bank lending, which grew by 10.2% y-o-y in December, up from

6.0% the previous year. While these conditions pose a medium-term inflation risk, in the nearer term they

are likely to act as a further stimulus for consumer spending and domestic business activity.

Public Expenditure Outlook: For largely the same reason as we expect government spending on wages

and benefits to remain elevated, we see Riyadh keeping public consumption high in 2012. Heavy

spending on social services is part of a strategy to shore up public support (see our online service,

January 4, 'No Let-Up In Spending In 2012'), and we have pencilled in growth of 6.0% in public

consumption accordingly.

Saudi Arabia Food And Drink Report Q3 2012

© Business Monitor International Ltd Page 30

No Secret To Their Success Saudi Arabia – Components of GDP By Output, 2011

Source: BMI, SAMA

The recently-announced 2012 budget is instructive in this regard. The budget outlined plans for a

substantial nominal increase in social spending, including a 13.0% increase on the allocation for

'education and training', a 26.0% rise for 'health and social affairs' and a 19.0% increase for 'municipality

services'. Though not disclosed in the budget, we also anticipate a further ramping up of spending on

defence and security, with several large contracts having been signed in recent years. It is important to

bear in mind that these figures are measured against the budgeted allocations in 2011 rather than actual

spending (which was considerably higher), and there is generally a wide disparity between budgeted and

actual expenditure. Nevertheless, Riyadh's intention to keep fiscal policy expansionary is clear, and will

serve to further stimulate the economy throughout the year.

Fixed Investment Outlook: Our view on the prospects for fixed investment in 2012 is similarly bullish.

Riyadh's 2012 budget has a heavy focus on capital spending, signalling the government's intention to

persist with its ongoing drive to improve the country's transport, energy and social services infrastructure.