savings b ank 1850 1980 - institute for american...

TRANSCRIPT

y HFR utlandSavings B an k

1850 1980Our First 1301fears

! '= 'r r j ? 1

_ T h eR utlandSavings B an k

M e ? ? ® F

i jsi ■ij ±MLal I 1 s

■ d f e - h f PAW^KS_ ^ 4 J 'IJr*,£

cottage ST.

ggmi*

B ____ L

ST.

SUA4 a?i f

a

Diitjijt^ . J ’ 'j|« 1 ?

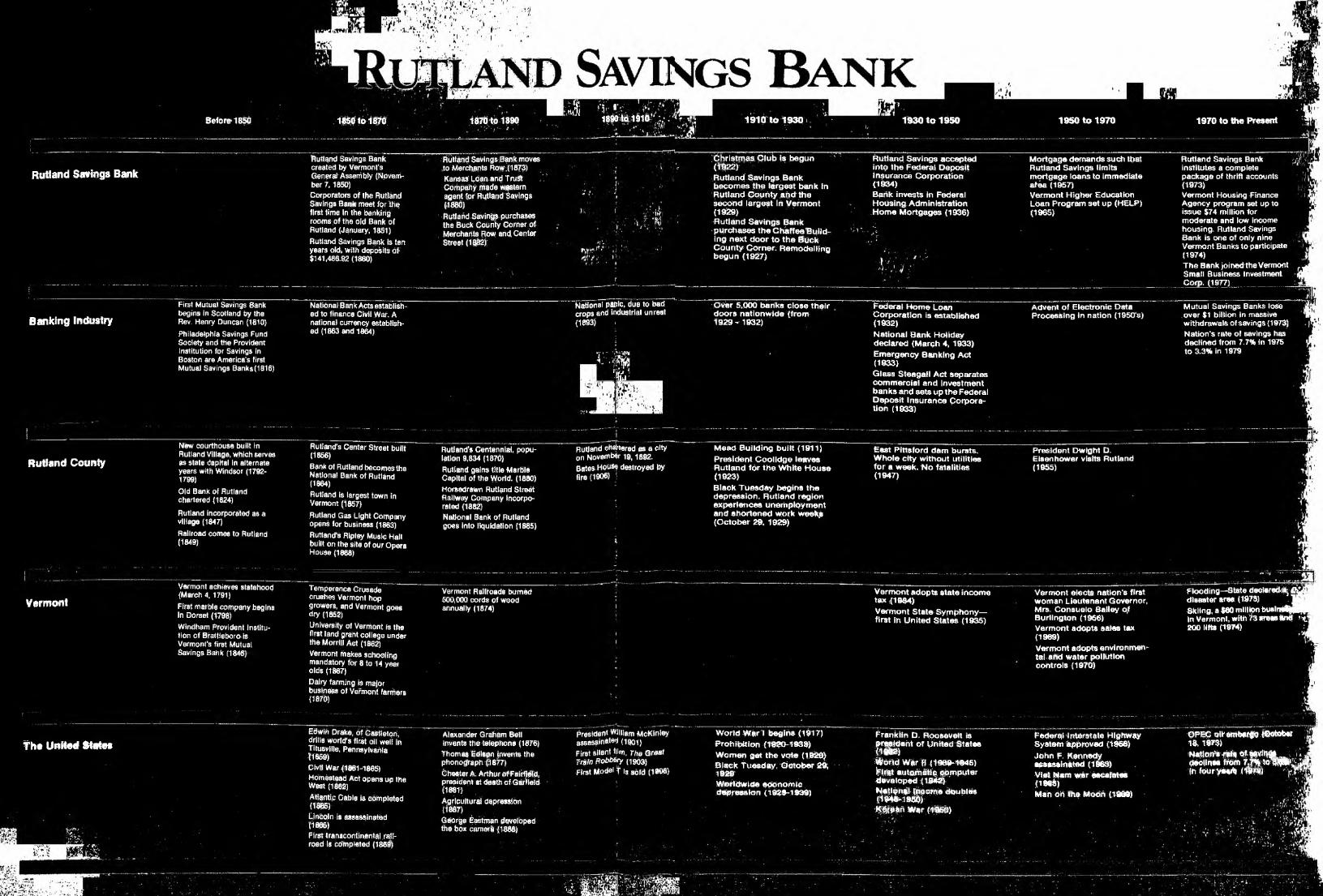

Before 1B50 1850 to 1870 1870 to 1890A 41890 to 1910 , . .....- , -** ' -i.'flr v/1,* m 191016 1930 1930 to 1950 1950 to 1970 1970 to the Present

Rutland Savings BankRutland Savings Bank created by Vermont's General Assembly (November 7. 1850)Corporators of the Rutland Savings Sank meet for the first time in the banking rooms of the old Bank of Rutland (January, 1851)

Rutland Savings Bank Is ten years old, with deposits of $141,486.92 (1860)

Rutland Savings Bank moves to Merchants Row.(1B73) Kansas' Loan and T rust . Company made western agent for Rutland Savings (1880)Rutland Savings purchases the Buck County Corner of Merchants Row arid Center Street (1882)

- . v- *fc-t

Christmas Club is begun ' (1922)Rutland Savings Bank becomes the largest bank in Rutland County and the second largest In Vermont (1929)Rutland Savings Bank purchases the Chaffee Building next door to the Buck County Corner. Remodelling begun (1927)

Rutland Savings accepted into the Federal Deposit Insurance Corporation (1934)Bank invests In Federal Housing Administration Home Mortgages (1336)

Mortgage demands such that Rutland Savings limits mortgage loans to Immediate afea (1957)Vermont Higher Education Loan Program set up (HELP) (1965)

Rutland Savings Bank institutes a complete package of thrift accounts (1973)Vermont Housing Finance Agency program set up to issue $74 million for moderate and low income housing. Rutland Savings Bank is one of only nine Vermont Banks to participate (1874)T h e Bank joined the Vermont Small Business investment Corp. (1977)_________________

Banking IndustryFirst Mutual Savings Sank begins in Scotland by the Rev. Henry Duncan (1810)

Philadelphia Savings Fund Society and the Provident Institution tor Savings In Boston are America's first Mutual Savings Banks(1816)

National Ban k Acts established to finance Civil War. A national currency established (1863 and 1864)

National panic, due to bad crops and industrial unrest (1893) i

■7 ' '

L a i

Over 5,000 banks close their doors nationwide (from 1929- 1932)

Federal Home Loan Corporation is established(1932)National Bank Holiday declared (March 4, 1933) Emergency Banking Act(1933)Glass Steagall Act separates commercial and Investment banks and sets up the Federal Deposit Insurance Corporation (1033)

Advent of E lectronic Data Processing in nation (1950’s )

Mutual Savings Banks lose over $1 billion in massive withdrawals of savings (1973) Nation's rate of savings has declined from 7.7% in 1975 to 3.3% in 1979

Rutland County

New courthouse built in Rutland Village, which serves as state Capital in alternate years with Windsor (17921798)

Old Bank of Rutland chartered (1824)

Rutland incorporated as a village (1847)

Railroad comes to Rutland (1849)

Rutland's Center Street built (1856)

Bank ot Rutland becomes the National Bank of Rutland (1864)

Rutland is largest town in Vermont (1857)

Rutland Gas Light Company opens for business (1863)

Rutland's Ripley Music Hall built on the site of our Opera House (1868)

Rutland's Centennial, population 9,834 (1870)

Rutland gains title Marble Capital of the World. (1880) Horsedrawn Rutland Street Railway Company incorporated (1882)National Bank of Rutland goes Into liquidation (1885)

Rutland chaptered as a city on November 19, 1B02.

Bates destroyed by fire (1906) !

Meat) Building built (1911) President Coolidge leaves Rutland for the White House (1923)Black Tuesday begins the depression. Rutland region experiences unemployment and shortened work weekp (October 29. 1929)

East Pittsford dam bursts. Whole city without utilities for a week. No fatalities (1947)

President Dwight D. Eisenhower visits Rutland (1955)

VermontVermont achieves statehood (March 4, 1791)

First marble company begins in Dorset (1798)

Windham Provident Institution of Brattleboro is Vermont's first Mutual Savings Bank (1846)

Temperance Crusade crushes Vermont hop growers, and Vermont goes dry (1852)

University o( Vermont is the first land grant college under the Morrill Aet (1882)

Vermont makes schooling mandatory for 8 to 14 year olds (1867)

Dairy farming is major business of Vermont farmers (1870)

Vermont Railroads burned 500,000 cords of wood annually (1874)

Vermont adopts state income tax (1984)Vermont State Symphony— first in United States (1935)

Vermont elects nation’s first woman Lieutenant Governor, Mrs. Consuelo Bailey of Burlington (1966)Vermont adopts sales tax (1969)Vermont adopts environmental and water pollution controls (1970)

Flooding— State declared^ f lU B disaster area (1973) . 1 0 9 Skiing, a W0 million b U * ln i$ p H In Vermont, with 73 areas and ' O 200 lifts [1974) 1

f h * U n ite d S tates

Edwin Drake, of Gaitleton, drills world's first oil well In Titusville, Pennsylvania (1959)

Civil War (1861-1865) Homestead Act opens up the West (1862)

Atlantic Cable is completed(1865)Lincoln is assassinated(1866)First transcontinental ralt- roed Is completed (1889)

Alexander Graham Bell Invents the telephone (1876) Thomas Edison Invents the phonograph (1877)

Chester A. Arthur of Fairfield, president at death afQsrtleid (1681)Agricultural depression (1887) ,George Eastman developed the box camera (1888)

president William McKinley assassinated ( 1901)First silent film. The Great Train Robtery (1903)First Model T l3 sold (1908)

World War I begins (1917) Prohibition (f8?0-!t93») Women get the vote (1920) Black Tuesday, dctober 29, 1929 'Worldwide eoonomic depression (1929-1999)

Franklin D. Roosevelt is prggtdaht of united Statee

% orld War H (1969-1946) ifirtrt automatic Qpmputer dBvaloped (194af) ' N«ti<?n*] (noome doubles<1«a-1980j V ’

War(t96Q)

Federal Interstate Highway System improved (.1966)John F. Kennedy assassinated (1969) . Viet Mam war escalates . JiMt)Man oh the Moon (1809)

O P E C QlKetTrfww<©otatoer , 18.1973) •Nation's ratt '*a]deolinM Worn * 7 * toljpl‘;-jJU| fft touryew* fWW

Savings B a n k

1850 1980Our First 130 "fears

A Mutual Savings Bank having no stockholders; organized, and conducted solely to receive and safely invest the savings of its

depositors to whom all the profits belong.

The Years Before 1 7 7 0 -1 8 5 0 3

Becoming Established 1 8 5 0 -1 8 9 9 5

A Bright New Century 1 9 0 0 -1 9 2 9 12

Exploring the Dark Years 1 9 3 0 -1 9 5 0 18

The Prosperous Years 1 9 5 0 -1 9 8 0 22

^ Letter from the Chairman of the BoardA Letter from the PresidentTrusteesPast Presidents

A Letter from the Chairman of the Board

On this one hundred-thirtieth anniversary year o f the founding of the Rutland Savings Bank in 1850, as well as the completion of major expansion and renovation o f its head office banking facilities, it seemed to be a fitting and opportune time to prepare a written record o f the highlights o f the bank’s history.

Since 1850 there have been great changes in the social, political and economic life o f our country as well as in the world. The Rutland Savings Bank has witnessed and survived the many periods of prosperity, depression and recession that have come and gone and has had to adapt itself to many new conditions. The ability and dedication o f the bank’s many trustees and officers over these past 130 years have successfully guided the bank through the Civil W ar period, the depressions of 1893 and 1907, two world wars, the Great Depression of the 1930’s, and the several recessions since W orld W ar II. The devotion of these past generations for the welfare and growth of the bank can well be an inspiration to those who will be responsible for managing the affairs o f the bank in years to come.

Over its first seventy-eight years up to 1929, the bank had a steady growth in assets to a total of $ 1 4 ,9 8 5 ,8 0 0 .0 0 as o f June 30, 1929, but during the depression years, assets dropped to a low of $8 ,486 ,089 .00 by June 30, 1942. However, since that time, there has again been growth every year to the present $212,937 ,169 .00 as o f June 30, 1980. In the last several years, increased competition with commercial banks for the saver’s dollar has forced the Rutland Savings Bank, along with the mutual savings bank industry as a whole, to offer the public more diversified financial services, not merely passbook savings accounts and real estate mortgage loans. The recent spectacular growth o f the bank can certainly be attributed in part to this broadening of banking services. In addition to its long-time primary purpose of promoting thrift and specializing in real estate mortgage loans for home ownership, the bank now offers checking and NOW accounts, a variety o f new types of savings certificates, consumer loans and has four full-service branches as well as free-standing twenty-four hour teller machines in five other towns to better serve southwestern Vermont.

It is hoped that this narrative will be more than just an interesting documentary review o f the long history o f the Rutland Savings Bank, and that it can be o f some help in planning the bank’s future activities, since there are many lessons to be learned from past experience. W e certainly trust and believe that the Rutland Savings Bank will continue to provide the finest possible banking services available With its very fine and capable staff and will also continue to play a vital role in the development and prosperity of the Rutland area and of southwestern Vermont.

Stetson C . Edm unds C h airm an , Board of T ru stees

THE YEARS BEFORE

comparatively short but active period of settlement prefaced the formation of the Rutland Savings Bank. Scarcely eighty years had passed

since the first permanent settlers had arrived in the wilderness that was to become Rutland. Colonel James and Mercy Mead, with their large family, made the grueling three-day journey from Manchester to the Little Falls on Otter Creek in March of 1770. It is said they were met by a discouraging sight, for the cabin that Colonel Mead had built on a previous trip was roofless and uninhabitable. A hunting party o f Coughnawaga Indians camping nearby offered shelter to the Meads until the cabin could be repaired. The Meads accepted, and Rutland’s first housing loan was made.

Our early settlers were subsistence farmers. They formed the nucleus o f communities as later settlers gravitated to them. By 1773, there were over thirty-five families in Rutland. Bartering, for labor as well as for produce, was common practice. Neighbors helped one another to build their barns and houses and exchanged, for example, a wheel of cheese for enough wool to make a coat. Gradually, various craftsmen, merchants and manufacturers — those who provided a specialized service — became established, and the role of money as a tool o f exchange grew more significant.

Industry, by and for those first Vermonters, developed in the form of sawmills, grist mills and carding mills. Potash, used in making soap, powder and glass, was the first cash crop. Merino sheep were imported from Spain, and by 1820 they outnumbered humans six to one. Tourism was a factor from the very beginning. In 1798, Clarendon was doing a brisk business in mineral waters. By 1835, many towns were operating mineral springs and building lavish hotels to accommodate their visitors. The first marble company began in Dorset in 1798. In 1830, Francis Slason, who would be one of the first corporators of the Bank, joined William Barnes to form the Standard Marble Company in West Rutland. In 1844, the Sheldon and Slason quarries had a contract worth $864,000 to provide two hundred and forty-five thousand lettered headstones for

soldiers’ graves in national cemeteries. In 1850, the Sheldon, Morgan and Slason quarry was worth $30,000, rising to $130,000 by 1860.

The gathering momentum of the Industrial Revolution swept inhabitants from the countryside into developing commercial and industrial centers, confronting them with drastic changes in their way o f living. Rewarded with sums of money to which they were unaccustomed, by industries which neither operated consistently, nor were designed to care for the worker in times of closed shops, these people found it difficult to care for their needs and those of their families.

When the phenomenon of industrialization was new, one of the most apparent problems was the relationship between workers and their wages. Solutions were experimental. Some of the earliest thrift institutions were begun by factories. They offered advice and rudimentary banking benefits in an attempt to see that workers did not become wards of the town in times of unemployment. For many, the consequences of unemployment or improvidence were most severe. Imprisonment lay in wait for unwary debtors in those times. The commercial centers of many towns developed around the jailyard, where prisoners worked off their debts.

A plan for a jailyard in Rutland encompassed an area whose center was the intersection of *'The Main Road and The Road to Castleton,” now the intersection of West and North Main Streets. The jailyard looked west across Main Street Park, down over the lowlands to the foothills and west to the mountains. This area became the center o f commerce in early Rutland.

Eventually, word reached the area of the successful experiment begun by the Reverend Henry Duncan. In 1810, Duncan started the world’s first mutual savings bank in a cottage in Ruthwell, Scotland. In 1816, the Philadelphia Savings Fund Society and the Provident Institution for Savings in the Town of Boston became the first American thrift institutions. In Vermont, which remained an agrarian state until the coming

3

of the railroad, the first savings institution was the Windham Provident Institution of Brattleboro, founded in 1846.

The earnings were then distributed prop ortion ately to the original depositors.

Commercial banks at that time fulfilled the needs of a few, comparatively wealthy individuals and were regarded with some suspicion because of the unreliability of paper money. The Reverend Duncan’s fledgling concept was philanthropic in nature, and that of mutual savings banks remains so to this day. It was thought that the combined funds of many small depositors would constitute an amount large enough to invest.

The corporators o f the Rutland Savings Bank held their first annual meeting in January of 1851. They met in the banking rooms of the old Bank o f Rutland, which had become Rutland’s first, and Vermont’s fourth, bank in 1824. As the present home of the Rutland Historical Society, it faces south on Center Street. It was built in 1825 to face north over Main Street Park— its intended view, the bustle o f commerce in early Rutland village.

R u tland H istorica l Society

4

O ne hundred thirty years ago, on November 7 , 18 5 0 , A n A ct to Incorporate T he Rutland Savings Bank was passed by the General Assembly o f the State of Vermont " ...for the purpose of enabling industrious persons o f all classes to invest such part o f their earnings as they can conveniently spare in a safe and profitable m anner. .

BECOMING ESTABLISHED

T H he Rutland Savings Bank was founded inanticipation of the changing banking needs of the working man and woman in Rutland as Vermont

entered the industrial age. The founders were veterans, of the professional and business community serving the rural frontier and hard workers in building the growing village of Rutland.

Luther Daniels was the first president of the Bank. He had settled in Rutland at "the age of his majority,” establishing a mercantile partnership in the old Cheney block with Daniel P. Bell, who was also a founder of the Bank. It was said that Daniels and Bell were known favorably throughout the county, and that they did the largest business in the place. During his lifetime, Daniels represented the town in the state legislature and the county in the senate.

Judge Robert Pier point was elected vice-president. He was one of the most eminent members of the Rutland County Bar. During his lifetime, Pierpoint held various municipal offices, served in the house and the senate, and was lieutenant governor.

John Boardman Page was treasurer. He was a man of great energies, who performed inestimable service to Rutlanders and to all o f Vermont. He was instrumental in returning Howe Scale from Brandon to Rutland in 1877, was president of the Rutland Railroad Company, and held office as state treasurer, representative and governor.

The men who completed the list of founders were: Silas H. Hodges and Charles L. Williams, lawyers; James Porter, doctor; George T. Hodges and James Barrett, merchants; Francis Slason, marble entrepreneur; and Martin G. Everts, municipal judge.

After the initial organization, banking was not a full-time occupation for those first corporators. The function of the president and the board o f trustees, in addition to contributing their business acumen to the undertaking, was to maintain the integrity of the Bank’s dealings. The treasurer, John Page, kept

the books, took in deposits on Monday and Friday of each week from two until four p.m., and kept the board informed of progress. He was required to post a $10,000 bond for himself and was paid $50 that first year. At the end of the year, one hundred-ten people had deposited $19,840. Loans were made in the amount of $12,675, earning interest of $451.16, and expenses totaled $129.88. Two dividends were declared, one of $48.89 in July and one of $232.43 in January. It was a substantial beginning.

Rutland Historical Society* 7.

The first home of the Rutland Savings Bank, now housing the Rutland Historical Society.

John Page held positions in both the Rutland Savings Bank and the Bank of Rutland until the 1858 legislature forced him to choose between the two institutions. So, in March, he resigned as treasurer of Rutland Savings, with many regrets.

President Luther Daniels then took over the duties of treasurer as well. Page went on to become the President of the Bank of Rutland, where he had started as a seventeen year-old cashier under his father’s tutelage.

By January of 1860, the growth of bank business over the past ten years reflected the influence of over fifty manufacturing concerns in Rutland, the largest being the marble industry, which employed over 600 people. Deposits had risen to $161,486.92, and the Bank had invested$121,676.96 in loans.

The advent of the railroad in Rutland in 1849 had changed the village as significantly as it had changed America. Rutland in the 1850’s was the largest town in the state and well on its way to becoming the world’s largest marble producer. An Albany newspaper reported in 1852, "Land in Rutland that was in the market six years ago at $60 an acre is now held at $2,500 and $3,000. ” The reason? "Eight years ago Vermont was without a railroad; now Rutland is a central railroad point. No less than six lines enter Rutland, over which run 45 trains a day. ”

Rutland Historical Society

An early view of the Rutland Railroad depot, machine shop and enginehouse.

Rutland H istorical Society

The Page home, which later became known as the Sycamore Inn.

John Boardm an Page

John Page began his banking career at the age of seventeen, assisting his father at the old Bank of Rutland. He rose in his profession, helping to gain the charter for the Rutland Savings Bank in 1850 and serving as its treasurer for eight years. He became president of the Bank of Rutland in 1866 and held that office for eighteen years.

His effectiveness was felt in other areas of progress and development. He became a trustee of the Rutland and Burlington Railroad in 1860, a time when the rolling stock was in no condition to roll, and the cracks were "only a streak of rust and a right of way." Ten years later, it was a well-built and well- equipped railroad. Page served as president of the Rutland Railroad and of the Howe Scale Company, which he moved from Brandon to Rutland in 1877-

In the meantime, the village received his attention. He was instrumental in establishing a public school system, a fire department — he was foreman of che Nickwacketts — and a system of water supply. In 1882 he was almost unanimously elected village president.

Carrying Rutland's cause to the state, Page represented the village in the legislature in 1852, 1853, and 1854. In 1860 to 1866, years through which the Civil War raged, he was state treasurer, working "all under novel circumstances, where no light could be gained by the experience of the past.” In recognition of his success, he was elected governor in 1867. The following year, at the age of forty-one , he was re-elected by a large majority. In 1880, he again represented Rutland in the legislature, and his emphasis on tax reform became the founda

tion of corporation law in the state.

Page was a long-standing member of the east parish Congregational Church. He served as chairman of its building committee in 1860 and deacon in 1881. Toward the end of his life, he was active in establishing a Christian college in Japan and in 1877 pledged $5,000 toward this goal.

Page traveled to Europe four times in his life. His first wife of twenty-four years, Mary Ann Reynolds, died there in 1872. He

married Harriet Ellen Smith in 1875, " I f inordinate adventure and enterprise seemed to have characterized at times his business career, it was nowhere corroded with the alloy of personal greed . . . ” Indeed, in 1885, at the age of fifty-nine, Page died of bronchial pneumonia and left his wife and family penniless.

Harrier Page converted the family home into an inn and began to take in paying guests, The Sycamore Inn, located on Main Street, is, today, part of the city’s proud history.

Rutland Historical Society

(i

The Bardwell Hotel opened its doors to serve railroad patrons in 1852. In 1856, Center Street connected the village with the tracks. Shortly thereafter, the Bank of Rutland moved into their new building—now the Lawrence Recreation Center—at the comer of Center and Court streets. The move allowed the Rutland Savings Bank to utilize the entire little brick building facing the park.

Vermont had been a staunch abolitionist state, with an extensive Underground Railway system used to smuggle fleeing blacks to the Canadian border. Within a month of the beginning o f the Civil W ar in 1861, Rutland sent off its own regiment, one of sixteen regiments o f Vermonters.

The National Bank Acts of 1863 and 1864 were established to finance that war. Banks were required to invest one-third of their capital in government bonds, on which they earned an attractive interest. In return, they were allowed to loan up to 90% of the value of the bonds. The Acts also instituted a tax on the printing of money by private banks, and thereby helped to unify a national currency. Prior to their passage, there had been more than seven thousand different kinds of bank notes circulating in the nation. Many local commercial banks adopted national charters, and the Bank of Rutland became the National Bank of Rutland.

Victory brought the North a buoyant sense of confidence and prosperity. An 1870 census showed that the per capita income had doubled in that ten years, four of which had been spent at war. This prosperity placed the North in an admirable position to aid western settlement. The Homestead Act in 1862 had offered 160 acres of land to any settler who would work it for at least five years. Inventions flooded the patent office; mechanized farm implements made possible the domestication of the wide western plains; railroads were flung across the continent.

Left These money proofs were printed for the Bank of Rutland and dated July 4, 1863. Be[<w A Rutland Savings Bank treasurer’s check.

> ^

*; to tile ‘f& y .; 'o rd er o f /

TREASURER.

During the winter months, when local business was slow, the Rutland Savings Bank joined other eastern banks in financing the settlement of the West. By 1870, the savings banks of New Hampshire and Vermont had invested 40% of their funds in western mortgages.

In its second decade, the Rutland Savings Bank showed a steady growth, declaring an extra dividend of VA% in 1861, and another of 2% in 1866. The treasurer’s annual salary rose from $700 in 1862 to $1,000, $1,500, and finally to $2,000 in 1870. William M. Field was elected to the board in 1865, beginning a long record of service to the Bank by the Field family, which continues to the present day. Newton Kellogg was elected trustee in 1862, and William Gilmore in 1868. Luther Daniels and James Barrett were the only founding trustees left on the board when, in 1869, the Bank's assets totaled $359,860.32.

Rutland celebrated its centennial in 1870 with a population of almost 10,000. Many trustees are listed as celebrants and organizers of the centennial. Henry Hall, a former trustee, spoke on "The Early History of Rutland” to an overflowing crowd at the Ripley Music Hall, the forerunner of the Opera House on Merchants Row.

In 1871, the treasurer’s salary was increased to $2,500 per year, and he was authorized to hire extra help for the Bank. An extra 2% dividend was declared on deposits that year, another

1 % in 1876 and another 2Vi% in 1879. In 1877, Newton Kellogg was appointed assistant treasurer at the salary of $750. He furnished a $10,000 bond, and Daniels provided one of $20,000. In 1879, the Bank’s assets totaled $639,586.23. The next year, it was decided to elect nine trustees. They were: Luther Daniels, William M. Field, William Gilmore, Edwin Martindale, Newton Kellogg, William B. Mussey, Aldace F. Walker, John Sheldon and Jacob Edgerton.

Although the trustees of the Rutland Savings Bank had the old bank building to themselves, they too were gazing down the hill to the tracks and discussing the subject of "removing the Bank downtown for the better accommodation of our depositors.” In 1865, a committee had been appointed to negotiate with the National Bank of Rutland for space in the new building they were constructing across from the railroad depot. In August of 1872, Luther Daniels and Newton Kellogg were instructed to sell the old building. The Bank then moved just south of Center Street on Merchants Row, sharing, once again, the banking rooms of the National Bank of Rutland. The Bank had arrived downtown, close to the much-celebrated railroad.

In 1880, Rutland had a population of 12,149. The town boasted seventy industries and six banks. W ith 1,500 men working in the marble industry, Rutland became known as "The Marble Capital o f the W orld.”

A lithograph of the Morse block prior to 1882. K i i t h u u l I h s t i i r i k ; i l

Vermont had made the transition to dairy farming, with secondary interests in apple growing and maple syrup production. Vermont education ranked sixth in the nation, although schools were crude and instruction simple. The school year consisted of two three-month terms, starting in November and June. A schoolmaster was considered competent if he possessed physical strength and endurance great enough, and a disposition foul enough, to handle his "cabined, cribbed, confined, juvenile republicans.”

In February of 1880, Luther Daniels resigned from the Rutland Savings Bank. He dramatized his intent at a meeting by seating himself a little to the side, opening up the space he had occupied for so long to whomever would succeed him. The trustees resolved to accept his resignation as treasurer but begged that he "most kindly cease” to insist upon his resignation as president and trustee. Daniels had been the Bank’s guiding force for thirty years, but now he was determined that his usefulness had come to an end. He did not attend another meeting. In January of 1885, the names of Luther Daniels as well as John Boardman Page no longer appeared on the list of corporators of the Rutland Savings Bank. William M. Field was elected president, with an annual salary of $500, increased to $1,000 in 1883. Newton Kellogg was elected treasurer and asked to provide a $40,000 bond.

In December, 1880, the board of trustees voted

unaminously to make the Kansas Loan and Trust Company of Topeka agent to make loans on real estate in the state of Kansas, not to exceed $25,000. In the auditor’s report at that meeting, there were "loans on First Mortgages or Real Estate: Vermont - $181,219.38, Iowa - $42,500, and Kansas-$15,200. ”In 1885, while still supplying the funding needs of prospective area landowners, the Bank had $611,116.70 invested in first mortgages outside the state. The agenda of a meeting in July dealt with eleven items relating to mortgages, three of which concerned Iowa, six Kansas, and two Vermont. It was thought that western mortgages were the safest that could be made, and the practice was to continue in varying intensity for over fifty years.

In 1882, President Field was authorized to "purchase ofE.A. Morse his Buck County Corner of Merchants Row and Center Street in the village of Rutland on the most favorable terms possible, not exceeding $35 ,000 .” The Buck County Comer consisted of half the present main banking room, in width as well as in length. In April of 1885, a committee was appointed to make a contract with a builder and superintendent for "the fitting up” of the new banking rooms.

A bookkeeper was hired in 1887, at the salary of $1,000. The assets of the Bank had tripled to $1,953,749,06 in the ten years preceding 1888. In 1890, William M. Field retired, to be succeeded by William Gilmore. Gilmore held the office for

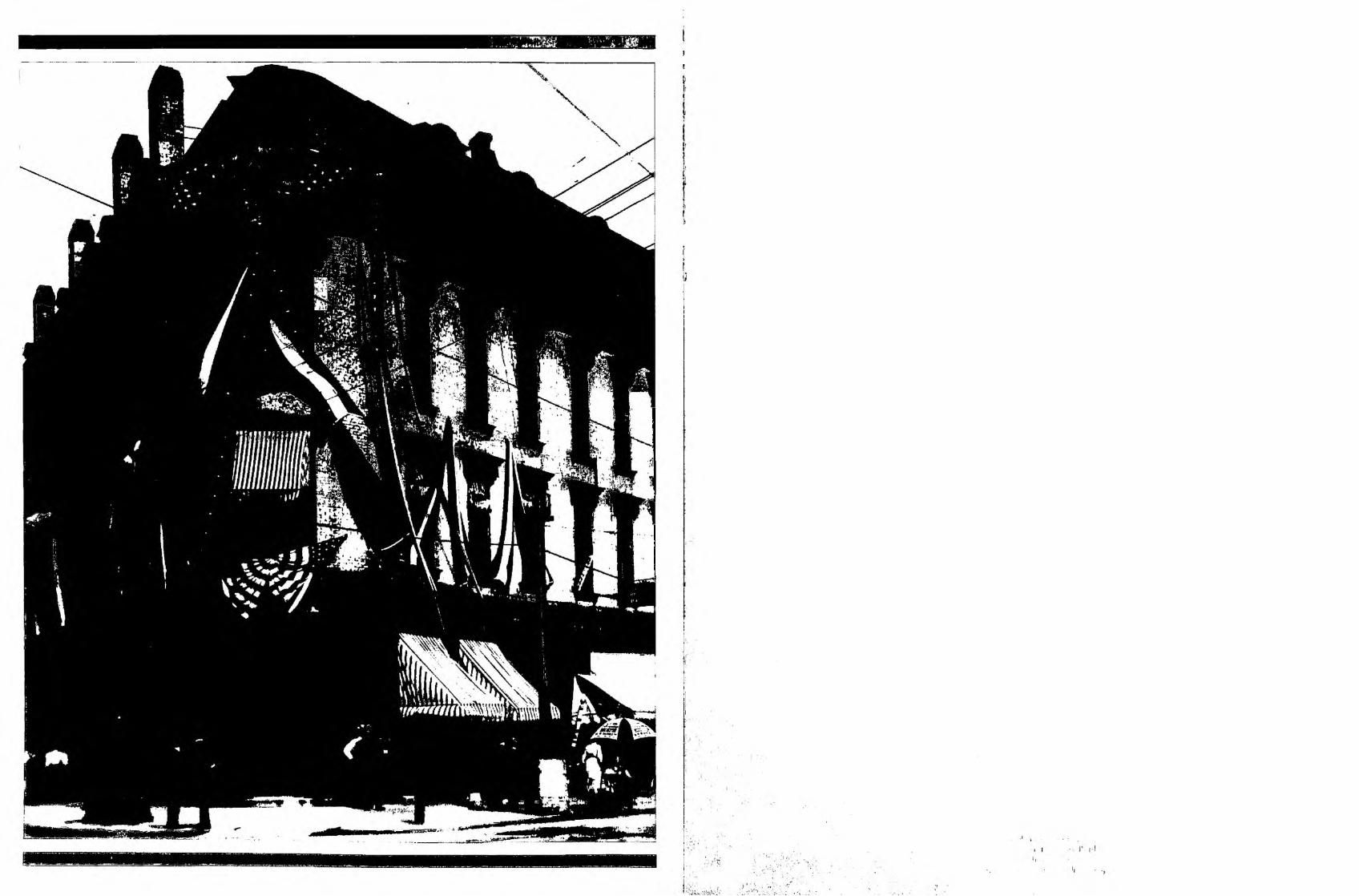

An etching of the Bank used on checks. Below The oldest photograph of The Rutland Savings Bank at its present location. This photograph, taken by Nichols Portrait and Landscape Photographers of 21lA Center Street, was taken sometime after 1887, but before 1891.

10

Stubborn Fire

"The Worst in Rutland for Many Years.1’ Rutland Savings Bank building badly damaged—many narroujiy escape with their lives and lose everything.”

Rutland Herald January 17, 1891

In the early morning of January 16, a fire started in the second floor of the Rutland Savings Bank building, in Dr. Kilburn's dental offices. It was discovered by Schuyler Cook, who shared a sleeping room on the fourth floor with Ed Jenks. Cook gave the alarm at 5 a.m., and "in a minute” the Washington Hose Cart was spraying water through the burning ceiling of the Combination Cash Store, which was located in the Center Street portion of the building. The fire was under control by 9 a.m., and the firemen were gone by noon. Most of the second, third and fourth floors of the Bank building were gutted. The banking rooms suffered slight water damage, and the Bank was closed for the day.

The article, written in a state of feverish excitement—the

Herald office was only two doors south of the burning building— provides a wealth of detail.

All of Rutland turned out, "many in negligee toilets, shivering in the bitter cold as they watched the splendid work of the Rutland firemen,” who, incidentally, looked like "Esquimaux.” Why, it was so cold that one fireman’s rubber boots froze to the rung of the ladder, and another’s felt hat had to be thawed from his head by the practical application of a by-stander’s hot coffee. A sign of the times was an icy banner, flying, with the accompaniment of leaping flames, from a high window, and proclaiming its cold message, "Tremble, King Alcohol.”

Personal and household belongings were stacked in depot park, looking like "frozen bric- a-brac,” and "one young man, who tripped over a rocking chair before he knew anything was in his way, used language more forceful then elegant.”

The loss was estimated at $35,000 to $45,000, all covered by insurance.

Scenes after the fire.

The two gentlemen in the center of this 1887 photograph are William Field, President of the Bank, and to his left, the Bank’s treasurer, Newton Kellogg-

one year, at which time 8,170 people had deposited $2,335,618.13. William B. Mussey was elected president in 1892, with George Briggs as vice-president. The following year, Wayne Bailey became vice-president and, after Mussey retired in 1894, president. H.O. Carpenter served as Bailey’s vice-president.

The expansion of the economy after the war was followed by an agricultural depression in 1887- Industrial unrest resulted in striking workers and impaired business confidence. These, and other associated factors, contributed to the panic of 1893, the effects of which would last to the turn of the century. However, in 1897, President Bailey was able to tell the trustees that the Bank had weathered the storm. "The year just past has been one of unusual business depression,” he told them. It had been a year o f failure for many well-established businesses and banks. He added, "In view of these facts, it seems to me that we have the greater reason to feel well pleased with the showing made by this bank during the year ending December 3 1 ,1 8 9 6 ." Due to 9,670 depositors was $2,781,723.65. Newton Kellogg resigned as treasurer in 1897, and Fred W , Lease was elected in his place. Lease held office for two years, yielding it to Charles A. Simpson in 1899.

In 1900, the Rutland Savings Bank was half a century old, celebrating with resources of $3,629,302.21.

D ecem b er__________________Assets___________Deposits1851 $ 16,874.66 $ 16,704.821859 137,985.51 134,993.551869 359,860.32 320,908.271879 639,586.23 593,541.621888 1,953,749.06 1,874,602.211899 3,629,202.21 3,487,777.04

" I t would be easy to speak o f the twelve months just passed as the banner year were we not already confident that the distinction o f highest records must presently pass to the year ig o o .”

New York Times editorial,January 1, 1 9 0 0

A BRIGHT NEW CENTURY

At the turn of the century, the Rutland Savings Bank could look back over fifty years of progress.

^ Every indication pointed to an even more productive future.

The Rutland of 1900 took on a new look. No longer did its people and buildings circle Main Street Park. Instead, they had come down the hills to the railroad tracks. The buildings were substantial, and the Street Railway gave the city a modern air. The Railway had been in operation since 1893, first horsedrawn and later electrified. There were still no paved roads, no suburbs and no combustion engines. The first automobile garage would not appear until 1906. The sounds of horses’ hooves and the creak and rub of the harness were to be familiar sounds a while longer.

From the railway yards across Merchants Row roared the Colonel Merrill, the J. Burdett, or perhaps the Rockingham. The explosive hiss of steam, the belching of embers from tall, black stacks, and the screeching whistles and brakes of the steam engines were the source of endless fascination to the townspeople.

Bicycles were a popular means of transport and recreation. Food was cooled in iceboxes and consisted of what was in season or had been preserved from the previous one. The few telephones in existence were found mostly in business offices. There would be no radio for another twenty years and no television for forty. Media was scattered and regional, reflecting the ideology and interests of isolated communities. Building materials and labor were inexpensive, allowing people of modest means to build large homes which could contain extended families comfortably. Rutlanders stayed, for the most part, in Rutland, paying attention to area concerns. They had time for nothing else, for the work week consisted of six, ten-hour days.

Wayne Bailey was president of the Rutland Savings Bank from 1894 until 1907, when he was succeeded by Henry O.

Carpenter. Frederick Farrington became Carpenter’s vice- president, and Charles Simpson continued as treasurer. Trustees were: H.H. Brown, Henry O. Carpenter, Newman K. Chaffee, Edward Dana, Frederick Farrington, Fred A. Field, W .R. Kinsman and E.C. Tuttle. By 1913, $6.5 million was due 15,341 depositors.

The mechanical age of banking was appearing. All records were painstakingly transcribed in longhand until 1902, when the typewriter came into use. Bookkeeping machines appeared soon after. The first departure from traditional savings and loan services was the Christmas Club, introduced in 1922.It proved a resounding success, accumulating $27,000 by the following year.

On President W ilson’s paradoxical premise that the only way to avoid war was to fight the one in Europe, the United States declared war on Germany on April6, 1917. Vermonters, echoing the mood of the nation as a whole, dutifully sent off their own contingent of 16,000 fighting men. The Armistice was signed a year and a half later, and our soldiers came home to a changing America.

Rutland Historical Society

The boyhood home of one of Rutland Savings Bank’s most illustrious depositors, Calvin Coolidge.

Rutland Historical Society 1

■ r

iiiiiiii fj_ finiiibMiIs

Panorama of downtown Rutland, probably taken during the summer of 1905.Rutland Historical Society

The Rutland Savings Bank celebrates the 1914 Rutland Carnival and Fair. A penny postcard o f the Rutland Savings Bank.

The main banking room as it appeared on July 12, 1912. From left to right are Charles A. Simpson, treasurer; Louis Campbell, assistant treasurer; Alvin Graves, clerk; F. Finn, Julia Buxton Granger and Agnes Sedileau.

This photograph of Newton Kellogg was found in a glassine envelope containing the following inscription:

"For Mr. H. Carpenter, Vice President of the Rutland Savings Bank.

I, Newton Kellogg came to Rutland from Pittsford in 1844 and worked for Luther Daniels in the building standing on the corner of Main and Tyrell Street from 1894 three years* and for the Old Bank of Rutland from 1849 to 1860 as Teller.

I assisted Mr. Luther Daniels, Treasurer of the Rutland Savings Bank, during his term of service most everytime in making his Reports until his term of service January 1880 and was then appointed Treasurer to take his place whitch* 1 held until sickness compelled my retirement in May 1894. I am now mutch* improved as to attend to the cultivation of my wifes* little garden.

(signed) Newton Kellogg 81st yearDecember 20th 1900.”*As it appeared in original text.

Below President Theodore Roosevelt addresses a crowd of 8 ,000 people on Labor Day, September 1, 1902. A year earlier, to the week, while Roosevelt addressed another Rutland audience, President McKinley was shot. Word reached Roosevelt while visiting with Senator Redfield Proctor and ex-Governor Nelson W. Fisk at the Vermont Fish and Game League luncheon on Isle La Motte.

Rutland Historical Society

Mr. Egbert C. Tuttle, a trustee of the Rutland Savings Bank, standing on the stairs of "his” new building, which replaced the one destroyed in the Bates House fire o f 1906.

Rutland Historical Society

The Rutland railroad yard in the winter of 1900.

A 1904 photograph of the Burditt Brothers Feed & Grain Store. The store was started by the father of the Savings Bank’s President, Dan Burditt. The woman on the right is Agnes Sedileau, who was to become secretary to the Bank's treasurer, Mr. Simpson, and in the late 1940’s, secretary to Mr. Stetson Edmunds.

When Calvin Coolidge became President, the rootless and extravagant post-war populace vicariously embraced his hometown qualities. Coolidge was frugal, thorough and taciturn. He became, in spite of himself, one of the more popular presidents.

His presidency was not without special significance to Rutlanders. Coolidge was a native son. He was also a depositor of the Rutland Savings Bank, and, after taking the oath of office at his home in Plymouth, Coolidge journeyed from Rutland to Washington, D.C., in a Rutland Railroad Company pullman.

Fred A. Field, Jr. was elected trustee in 1927, when the assets of the Bank stood at $13,200,950. That year, the Bank took over the Chaffee Building, the next building south on Merchants Row, and combined it with the Buck County Corner into one large banking room. Major remodelling, including a new vault, furniture and ceilings, exterior marble cornices and bronze doors, was completed in 1929. In May of 1929, Henry O. Carpenter resigned as president. He had been elected corporator in 1890 and served for forty-six years, twenty-two of them as president. Under his administration, deposits had increased from $3.5 million to $13.5 million. In its seventy- nine years, the Bank had only six presidents — Luther Daniels, William M. Field, William Gilmore, William B. Mussey, Wayne Bailey, H.O. Carpenter, and now Fred A. Field, Jr.

Field’s family had made its mark on the Bank, beginning with William M. Field, his grandfather, who had been elected corporator and trustee in 1865, and president from 1881 to 1890. His father, Fred A. Field, Sr., served on the board of trustees from 1890 to 1935, and his uncle, Henry F. Field, was corporator for fifty-eight years. When Fred A. Field, Jr. was elected president, he was "a man in the prime of life, able, strong, aggressive." And well he might be, for he was to be president of the Rutland Savings Bank during a most troubling time, 1929 - 1936.

Dan D. Burditt, Jr. became a trustee in 1929. The Bank had over 16,000 depositors, with deposits o f $13,428,286.It was the largest bank in Rutland County and the second largest in Vermont.

D ecem ber 3 1 Assets1899190919191929

3,629,202.215,679,663.988,349,312.51

13,851,055.25

Deposits3,487,777.045,288,193.407,528,037.94

12,569,302.41

Overleaf Merchants Row on a summer day in 1905. The Nichols and Barney clothing store, next to the Bank, occupied space on the side and the back of the Bank, with another entrance on Center Street.

" W e in America are nearer to the final triumph over poverty than ever before in the history o f any land . . . we shall soon, with the help o f God, be in sight of the day when poverty will be banished from this nation

Herbert Hoover - campaign speech, 19 28

EXPLORING THE DARK YEARS

A t the height o f the nation’s overwhelmingly rapid industrialization, Hoover’s confidence was proven misplaced, and the depression of the 1930’s began. Low wages prevented workers from buying the same goods that they were obliged to produce. Five percent

of the population enjoyed one third of the country’s wealth. This golden age of unfettered American capitalism died on October 29, 1929, Black Tuesday. Factories decreased production to a minimum, construction was shut down altogether, and from 1929 to 1932, over 5,000 banks closed their doors.

The depression continued despite a myriad of federal measures to improve the economy. In 1931, Congress established the Reconstruction Finance Corporation (RFC) to lend money to banks, railroads and other faltering institutions. In the following year, the Federal Home Loan Bank was established to discount mortgages. These methods were not immediately effective and did not stop the country from sinking deeper into misery. The Rutland region had its own share of the unemployed and shorter working hours, as well as suffering local industries.

Roosevelt took the oath of office on March 4, 1933. On March 5, he declared a national bank holiday. When the banks reopened, deposits exceeded withdrawals at many banks, including the Rutland Savings Bank. On March 9, the Emergency Banking Act was passed as the first step in rehabilitating the nation’s banks. Also created was the Farm Credit Administration, which would refinance a fifth of all farm mortgages in the next two years. In June, a Home Owner’s Loan Corporation was established, as well as the Glass-Steagall Act, which separated commercial and investment banking. The Federal Reserve System was expanded and the Federal Deposit Insurance Corporation set up. Bank failures became practically nonexistent.

In May, Congress had passed the Agricultural Adjustment Act to raise commodity prices. The Act paid the farmer for

decreased production, and this, in turn, stimulated the laws of supply and demand.

In 1932, the Rutland Savings Bank had a surplus of nearly $ 1.2 million and a bond list which compared favorably with that of any bank in the state. Railway bonds, decreasing in value as a result of investors’ overspeculation and the increasing competition of the trucking industry, were conspicuously absent from the Bank’s list. Vermont was one of only three states where there had been no banking failures. Nevertheless, the situation was serious. The Bank was cutting expenses — there had been a 10% across-the-board pay cut, and there would be no more luncheons after the annual meetings.

The western loan situation had not improved and was occupying the Bank almost full time. In 1933, the farmer took home only 7% of the GNP, as compared to 30% in 1860. Farmers wrote letters describing their land and buildings, their crops and livestock in an attempt to explain why they were unable to make mortgage payments. An Iowa farmer wrote:

' . . . I shall be delinquent for a short time on interest on my loan.I have on feed some hogs and sheep, expecting them to be ready for market about the 20th. I am enclosing you a statement o f my expenses on tRis farm. I feed yearly about 7 5 0 lambs and am expecting to raise tfus season 1,0 0 0 hogs. I find the only solution to the farm problem is a large volume at low prices. There will be more farmers defaulting on interest in lou/a this season than ever in the history o f the state and I have lived here for sixty-five, years. The Reason: High taxes and interest rates. Hoping you may not have any apprehension over this delay . . . 11

Requests for extensions of terms were being sent to Field. The Bank was dealing with every facet of farming, either directly or through an intermediary. An agent for the Rutland Savings Bank wrote:

" . , ./ have gone over the matter in m;y mind, and 1 believe this dwelling could be put in good condition for between $200

and $250. This would put on a new roof o f asbestos shingles, fix the flues, do what plastering is necessary, and what inside papering and painting..

This letter was written in 1931. In 1934, the farmer succeeded in keeping his farm with the aid of the Federal Farm Mortgage Corporation and the patient problem-solving efforts o f all concerned.

The Bank was torn, during those years, between its basic philosophy and the impersonality of banking laws. Newman K. Chaffee presented the paradox to the Vermont Commissioner o f Banking and Insurance in 1937:

. . . Among the iruinj problems that have confronted the banker having to do with farm loans during this depression is the question o f hou' to handle a farmer who, though delinquent, is lrub desirous o f keeping his farm and paying his debts but who, temporarily at least, cannot meet his payments and is on the point o f throwing up his hands and letting everything go. It has been the theory o f this bank, a theory we think is fully justified by experience, that the more we can do to keep up the courage ° f such a farmer in the face o f tremendous adverse circumstances the better we are serving the interest o f our depositors. Such a farmer can get more out o f the land and pay the Bank more than it could get by owning the land. When such a situation has arisen we have considered it a case comparable to owning the farm ourselves and have taken such measures as were necessary to get out o f the situation as best we cou ld ..

A sense o f humor rated high on the list of qualities needed to see the Bank through the depression. In 1934, President Field told the trustees that, . .My four and one half years of banking experience has certainly been some experience, and you will remember that February 22 last I was elected president of the Vermont Banker’s Association, and just ten days later every bank in the country was closed.”

Vermont’s economy was at its lowest ebb, but the western mortgage situation had improved. President Field had spent some time in Washington with the Federal Farm Credit Administration in an effort to get the Federal Land Banks to be more liberal in their appraisals of property, enabling more delinquent loans to be refinanced and the property saved for the owners. Vermont mortgages had given very little trouble, and those which might have had been refinanced through the Home Owner's Loan Corporation. The Bank had been accepted into the F.D.I.C. As a condition o f membership, it had to sell $850 ,000 in debentures to the Reconstruction Finance Corporation. The money was invested in government bonds as an additional guarantee to the depositors.

President Field felt the Bank was fulfilling its purpose as the founders had envisioned it — that of receiving the savings of the working man or woman to be held in trust for them until the time of need arose. "That time is here, and we are glad to be performing a real service for our depositors.” The Bank was able to perform that service, with $ 1.2 million in government bonds, over $400,00 cash on hand and in banks, and a bond list of over $3 million without one defaulted bond on the list.

The Bank’s assets declined over these years from $13.8 million in 1929 to $9 million in 1939, only to recoup by the early fifties. Guideposts to economic history can be seen clearly in hindsight, but they were erected by hands which groped through the darkness. Listening to President Field’s words, the trustees had reason to feel justified by the route taken by the Bank. They felt renewed vigor to press forward to a destination of economic well-being.

Stetson C. Edmunds, grand-nephew of former president, H.O. Carpenter, was elected clerk in 1935, and in 1936 was appointed assistant treasurer. Mr, Edmunds had graduated from the Wharton School at the University of Pennsylvania, where he had specialized in banking. From there he went to Chase National Bank in New York City for five years, rotating from one department to another on an intensive training basis. He was a Rutland boy, and it was thought that, in addition to his experience, his wide acquaintance among the younger set o f the city would be of benefit to the Bank.

( In 1936, President Fred A. Field, Jr. died, bringing to a close the seventy-one years of continuous service to the Bank by the Field family. He was succeeded by Newman K. Chaffee, who offered this tribute:

" . . .Fred A. Field, Jr., o f the third generation, was elected trustee in ig27 and president in 1929. With experience o f but little over two years on the Board, and no other banking training it seemed a big load to place on his shoulders, but he not only met all the hopes and expectations o f his friends, but carried the Bank through the hardest and most trying period of its history with a dogged persistence and skill that cannot be too highly commended. His was a short but splendid record."

The general condition of the Bank and the economy was improving. The Bank was gradually emerging from the depression and was beginning to see some positive results of its exploration through that dark time. Interest in buying farms was increasing. One major change in the investment policy was the decision to carry fewer bonds and to buy, instead, Federal Housing Administration home mortgages, which were insured by the federal government. Improvement, however, was slow, and setbacks many. From September of 1937 to June of 1938, there had been another national decline. In 1938, President Chaffee was forced to say that progress had continued, but not nearly to the extent he had expected. During those years, the reserves o f the Bank were being shrunk by the sale of western farms. "For a long time we had hoped and expected to see farm values come back to somewhere near the prices they formerly commanded, but after years of waiting for this it is very evident that it is folly to wait longer.” In the three years ending December 31, 1938, the Bank sold one hundred eighty-one farms or parts of farms, a total book value of $950,055. These sales were accomplished by accepting low prices, reducing reserves to an uncomfortably low point. It was thought best to lay the whole western mortgage situation before the State Banking Department, the F.D.I.C. and the Reconstruction Finance Corporation.

"All parties gave us a full and friendly hearing and advised that we continue seiling regardless o f its effect on debentures,

and if possible at a faster rate chan we had previously been able co reach."

It was a relief for the trustees to know that their chosen course of action had the backing of all concerned. However, the trustees wished to do whatever possible to help the farmers by not foreclosing while there remained an alternative avenue of action. In 1940, they succeeded in putting in excellent standing several loans that had been criticized by the authorities,

. .some of which, however, your officers believe and maintain were perfectly good, as the results have shown.”

On December 7, 1941, the Japanese bombed Pearl Harbor. The escalation of the national economy for the war wiped away the last traces of the depression. The production demands of the armed services and the war industries brought to an end more than a decade of high unemployment. The farmer’s cash income would more than quadruple between 1940 and 1945, and the weekly earnings of industrial workers would rise 70%.

At the beginning of 1942, President Chaffee told the trustees that the most important matter before every bank in the country was how best to assist the government in its effort to preserve the American way of life. Trustee and general counsel, General Leonard F. Wing, was serving in the South Pacific. Captain R. Clarke Smith and Lieutenant Donald Ross, corporators, were to serve the duration of the war in the armed

forces, and Frederick S. Allen, trustee, was giving all his time to local war work. The Bank was extremely successful in its effort to sell Defense Bonds and Stamps; by 1946, it had subscribed to nearly $8 million in U.S. Bonds. The only difficulty lay in getting bonds fast enough to fill the orders. When the government depressed interest rates on bonds, the Bank notified depositors six months in advance. This resulted in losing some deposits but reinforced the Bank’s reputation for fair play.

In 1944, Dan D. Burditt became the president of the Rutland Savings Bank after the death of Newman K. Chaffee. Chaffee had been elected corporator in 1894, and a trustee in 1907. When he became president in 1936, he was convinced of the advisability of liquidating the Bank’s western real estate holdings, and for all intents and purposes, he accomplished that task. Nineteen hundred and forty-seven saw the sale of the last out-of-state property, and President Burditt issued his blessing: "May the lessons and experiences of the past serve well to guide our future policies.” It was the practice to keep the mineral rights on the land for a minimal sum. "There are a few that pay enough to make it worthwhile to look after. I do not recall that we ever got any oil from them, the revenue being for rentals from prospectors.”

In 1948, Stetson Edmunds was appointed assistant vice- president. One year later, Alfred J. Wimett, Jr. was appointed treasurer.

The Bank as it appeared in the 1930's. The store on the far end of Center Street was Louras’ shoe shine and hat-cleaning parlor, which also, according to the canopy above the door, sold popcorn. Next door was Howley Brothers’ Sporting Goods store, where one could buy newspapers, sheet music, bicycles, fishing tackle and other hunting supplies. The next shop was Oiney's chil- dren's clothing store.

Prosperous years followed the war. In five years, national income increased from $181 billion to $241 billion. Rationing was gone, and people were able to buy the components of the good life, of which they had been deprived for so long. America was rebuilding half of Europe, and this, as well as home consumption, demanded frenzied production. The power of government and its inclination to spend heavily had shown a marked increase between the two world wars.

The Bank was involved in the task of easing returning soldiers back into civilian life. "W e will continue to do our best to be of service to veterans in assisting them to purchase homes and readjust themselves to civilian life. With the war over now we hope that home building will be possible at an early date.” H ie Bank had invested heavily in FHA and GI mortgage loans. They were all home loans and guaranteed by the government. Bond investments were restricted to U.S. Government bonds. Savings deposits had increased, but interest rates were low on investment possibilities, thus making the profitable use of deposits a real problem. "However, savers of all types, large or small, are welcome here, since the encouragement of thrift is one of the main objectives of the savings bank.”

On June 3, 1947, the East Pittsford dam broke. Water rushed down East Creek, flooded the low areas of the city and wreaked havoc with the utility, transportation and communications systems of Rutland. It affected, in varying

degrees, forty-three properties on which the Bank held mortgages. All possible assistance was given those borrowers in the form of counsel, as well as additional loans for rehabilitation.

By 1950, banks were finding government restrictions cumbersome, but it was not likely there would be fewer in the future. Rules would be tightened further in order to discourage borrowing and so put a brake on inflation, which had increased every year since the war. Dan D. Burditt called upon the founders for inspiration: "Indeed, their courage in starting a bank from nothing can well give us renewed strength to look forward to the future and the many problems it may have in store.” Luther Daniels, Page and Pierpoint founded the Rutland Savings Bank with confidence in the future and the conviction that there was a need for its services in the community. Since then, a handful of people, feeling that same conviction, had steered the Bank through uncharted times that would have seemed preposterous to those pioneers.

D ecem ber 3 1 Assets Deposits192919391949

13,851,055.258,988,865.00

11,762,421.50

12,569,302.418,661,271.10

10,594,917.57

Rutland Historical Society

This house was carried over a tenth of a mile during the flood of 1947 and deposited in the Post Road

"Perhaps it was worth being poor for a long time to be so rich for just a little while.”

John Kenneth Galbraith

THE PROSPEROUS YEARS

BIndustrial Revolution afforded freedom, mobility and sophistication. Not only did it affect our way of

getting from one place to another, the way we worked and the way we played, but it affected our very way of thinking.

The horse was gone. The heyday of railroading was over. In 1961, the Rutland Railroad ground to a halt. Now the car was king. It changed the face of the nation and created new styles of living and abundance. Vermont would join the rest of the country in the construction of a Federal Interstate Highway System in 1956. It would create three hundred twenty- one miles of highway where, in 1925, there had been less than forty miles of paved roads.

Mass media homogenized the nation’s thought and diluted regional differences. There was a growing informality in dress, relationships — indeed, in all aspects of society. The middle class had grown to immense dimensions, dwarfing rich and poor alike. It was an entirely new world.

In the fifties, after twenty years of depression and war, a generation was now ready to enjoy newfound prosperity. Their children were growing up in an era of McCarthyism, fear of communism, race riots in the South and a supreme belief in promises of a push-button space age. These children swamped the schools, and in the sixties, would voice their protests to the entire world.

The Rutland Savings Bank’s practice of investing in FHA and GI mortgage loans flourished through the fifties. Not only did the loans provide a way of helping returning soldiers and their families, but they were guaranteed by the government. The early fifties found a decline in demand for these mortgages as more and more servicemen became settled. However, by 1957, the national mortgage demand had become so great that it exceeded the available supply of funds and resulted in a rise in the cost o f borrowing. The Rutland Savings Bank, limiting itself to satisfying area demand, was able to meet its

obligations. In 1959, with the interest rate on conventional mortgages at 5V4 to 6%, FHA at 5ZA%, and GI loans at5V4%, mortgage loans constituted 78.8% of the Bank’s total assets, 60% being government guaranteed.

One of the most pressing problems addressed by the Bank in the fifties was the slow drop in deposits. When the trustees raised the interest rate on deposits to 2% in 1953, it was not as high as some banks were paying, but it seemed to check the decline. The Bank was unwilling to compete for the saver’s dollar by offering gimmicks, giveaways, or a higher interest rate than it felt warranted. Nevertheless, the rate had risen to 3Vi% by 1959, and there was a net increase in savings deposits for the year of $960,000.

Nineteen hundred fifty-eight was a landmark year. The $850,000 that the Bank had borrowed from the Reconstruction Finance Corporation in 1934 to gain admittance to the F.D.I.C., and an additional $150,000 RFC loan, had both been paid in full plus interest. The loans had been refinanced in part through the National Life Insurance Company of Montpelier in 1954, and "the total was paid out of income accumulated from sound investments, and by following a conservative policy of modest interest rates on deposits. ”

The sixties were years of turmoil. The assassination of national heroes, the destruction of cities in the heat of civil rights demonstrations, the escalation of a foreign war which lacked the backing of most Americans, caused this nation to reflect on its basic principles and institutions.

On December 3, 1962, Dan D. Burditt resigned as president of the Rutland Savings Bank and was elected to the newly-created office of Chairman of the Board of Trustees. Mr. Burditt had been elected corporator in 1924, trustee in 1929, and vice-president in 1941. In 1944, he succeeded the late Newman K. Chaffee as president. During his tenure as president, deposits had increased from $9,185,000 to $19.5 million, with assets of over $21.5 million. Stetson C. Edmunds

22

I

September, 1953

December, 1953

assumed the presidency from Mr. Burditt.

Despite keen competition from other financial institutions for the saver’s dollar, the Bank was able to reverse the decline in savings deposits in the sixties. Deposits in 1960 increased 15.5% over the previous year. In 1962, the interest rate on savings was raised to 4%, and deposits at the end of 1963 had doubled in six years' time. The balance on the 13,072 savings accounts reached an all-time high of $22,066,000. By the end of the decade, 5% was being paid on deposits of slightly less than $39.5 million.

With the increase in deposits and a decline in mortgage demand in the early sixties, the Bank’s investment policy changed. This was reflected in larger U.S. government bond holdings and higher coupon government bonds. By 1965, the growth of conventional mortgages was beginning to overshadow that of government-insured mortgages. This was caused by loans on commercial properties and vacation homes. The Vermont Higher Education Loan Program, (HELP) was set up by the state to guarantee loans of up to $ 1,000 to worthy students to help finance their college expenses. Though this program started out slowly, by 1969, there were loans to one hundred thirty-four college students.

In 1961, the Bank instituted a retirement pension for its staff. These people, responsible for the day-to-day business of the Bank, are consistently cited by the president and the trustees for their excellence.

The need for more adequate office space was becoming increasingly apparent, and the Bank made plans to utilize the

The changing face of the Rutland Savings Bank. The Mansard roof was removed to add another floor to the Bank’s building. BelouJ The main banking room as it appeared in August, 1951.

two vacant stores in their building on Center Street. There had been no change in the physical layout or modernization of the Bank’s facilities for over thirty-five years — not since the major remodeling and expansion in 1927. The project was completed in 1967. On-line teller machines were put into use the following year, as was the new alarm system which connected the Bank with the police station.

The goals of the Bank were expanding throughout the decade. The Bank was being seen more than ever as a function of the area served, and its efforts went increasingly into building a healthy community. " I like to think of successful operations not alone in terms of profits, and dollar and percentage increases,” President Edmunds said, "but also in terms of rendering essential and desirable service to the community and surrounding area in the best possible manner.”

Rutland merchants saw the development of shopping malls outside cities as a potential threat to their livelihood. When a mall was proposed for the Rutland area, there was a move to keep it downtown, diverting shoppers into the heart of the city rather than to the fringes. The Rutland Shopping Plaza was built in the mid-sixties on the site of the old railway depot. The generous amount of free parking it provided was a bonus.

The mid and late sixties were years of tight money and credit squeeze. The demand for mortgage loans in Vermont, as a whole, exceeded the supply of funds available. Historically, Vermont had been a capital-exporting state, with its money contributing to the settlement of the West in the late nineteenth and early twentieth centuries. Then, starting in the thirties, surplus state funds were invested in FHA, and later, VA loans in other areas of the country where there was a need for home financing. In the sixties, it was thought that Vermont might need to go outside the state to find funds for Vermont mortgages. Rutland Savings limited its mortgage loans to the immediate area’s permanent housing market and was able to keep up with demand.

Treasurer, Alfred J. Wimett, Jr., died in 1968, after serving the Bank for nearly twenty-three years and earning the highest respect- Lloyd M. Hier, who joined the Bank in 1952, was appointed treasurer and secretary in his place. Hier would serve in that position until his death in 1975, when Thomas C. Ryan would take his place.

The decade of the sixties ended with continuing and growing inflation reflected in higher prices and costs for most commodities and services. Interest rates on U.S. government securities and high-grade corporate bonds had soared to unprecedented heights, creating an extremely high interest rate for borrowing. These conditions would continue into the seventies.

The nation was preoccupied with bitter issues in the early seventies. The Vietnam War ended in 1973, and the disclosures of Watergate forced Richard Nixon to resign in 1974. The economy was characterized by inflation, recession, mounting unemployment and a sinking stock market. Environmental

concerns came to the fore nationwide. Vermont adopted far- reaching environmental controls, demonstrating the emphasis on the quality o f life in the state.

For the Rutland Savings Bank, the seventies were a continuation of the trends of the sixties. Interest rates fluctuated, while construction and labor costs rose. From July to October of 1973, depositors made massive withdrawals from savings institutions in order to reinvest the funds in high interest-bearing government securities as well as other types of investment offering a higher rate of interest. Mutual savings banks alone lost over $1 billion in deposits. In an effort to recoup, the Rutland Savings Bank offered a complete package of thrift accounts paying the highest legal level of interest. This action, coupled the following year with a decline in interest rates and yields available in money market obligations, was effective. Over 1975, and due mainly to the increase in deposits, the assets of the Bank increased 17.27%, or over $12 million, for that year alone. The problem of savings withdrawal would reappear, but for the time being, it was held in check.

Inflationary costs of construction had dampened the mortgage market in the mid-seventies. Rutland Savings was one of only nine Vermont financial institutions—and the only one in southwestern Vermont—to participate in the Vermont Housing Finance Agency program. The agency, created by the legislature in 1974, was allowed to issue $74 million in revenue bonds, the object being to make mortgage financing available to moderate and low-income families.

The condition of the Bank continued to improve each year during this unsettled time. In 1976, in what would be his last annual report as president, Stetson C. Edmunds was able to report on the Bank’s astonishing progress:

"This past one hundred twenty-fifth anniversary year, 1975 .

has not only been a milestone for the Bank, but has seen both the largest dollar and percentage growth in many years, if not in history. , .The Bank’s assets increased $12 ,173 ,0 0 0 to $ 8 2,6 5 8 ,00 0 .”

Edmunds went on to speak of the broadening service offerings which would involve the Bank in the immediate future. The Financial Institutions Act of 1975 greatly broadened the lending and investment powers and authorized checking and interest-bearing Negotiable Order of Withdrawal (NOW) Accounts in thrift institutions. Though their basic concern would always be with savings accounts and mortgage lending, the function of savings banks was being redefined and expanded by federal and state laws. The Rutland Savings Bank would need to develop full-service banking to serve their customers’ one-stop banking needs.

Business in the M an ch ester-S tra tto n -L o n d o n d erry area had increased to the p o in t o f ju stify in g the B an k ’s first branch o ffice . A com p lete facility was planned fo r M anch ester Center, to be in op eration the follow ing year.

President Edmunds also noted the increasing influence o f

Electronic Data Processing (EDP) on the workings of the Bank. On-line teller machines had been in use since 1968, the loan bookkeeping system had been converted from ledger cards to computer, and a powerful mini-computer would be installed to care for various complicated banking procedures.

Stetson C. Edmunds had joined the Bank in 1935. He served as president from 1962 to 1976. In those fourteen years the Bank’s assets increased from $21.5 million to $82.5 million. When he retired as president, Edmunds was elected chairman o f die board o f trustees, a trust which he still fulfills.

Thomas C. Ryan was chosen to carry on into the ambitious future outlined by Edmunds. Ryan, a native of Rutland, had extensive banking and real estate experience in the Hartford, Connecticut area. He joined the Bank in April of 1974 as assistant to the president, and in 1976, he became the eleventh president o f the Rutland Savings Bank. In his turn, Ryan asked the question asked by his predecessors: For whose benefit does the Rutland Savings Bank exist?

" If we accept the classic answer, i.e., exclusively for the depositor, our sole objective would be in seeking the maximum in profits and dividends. But, i f we accept that we best serve the depositors by helping to improve the community at large, management has a broader range o f options and obligations "

The Pawlet Office

T he M anchester office

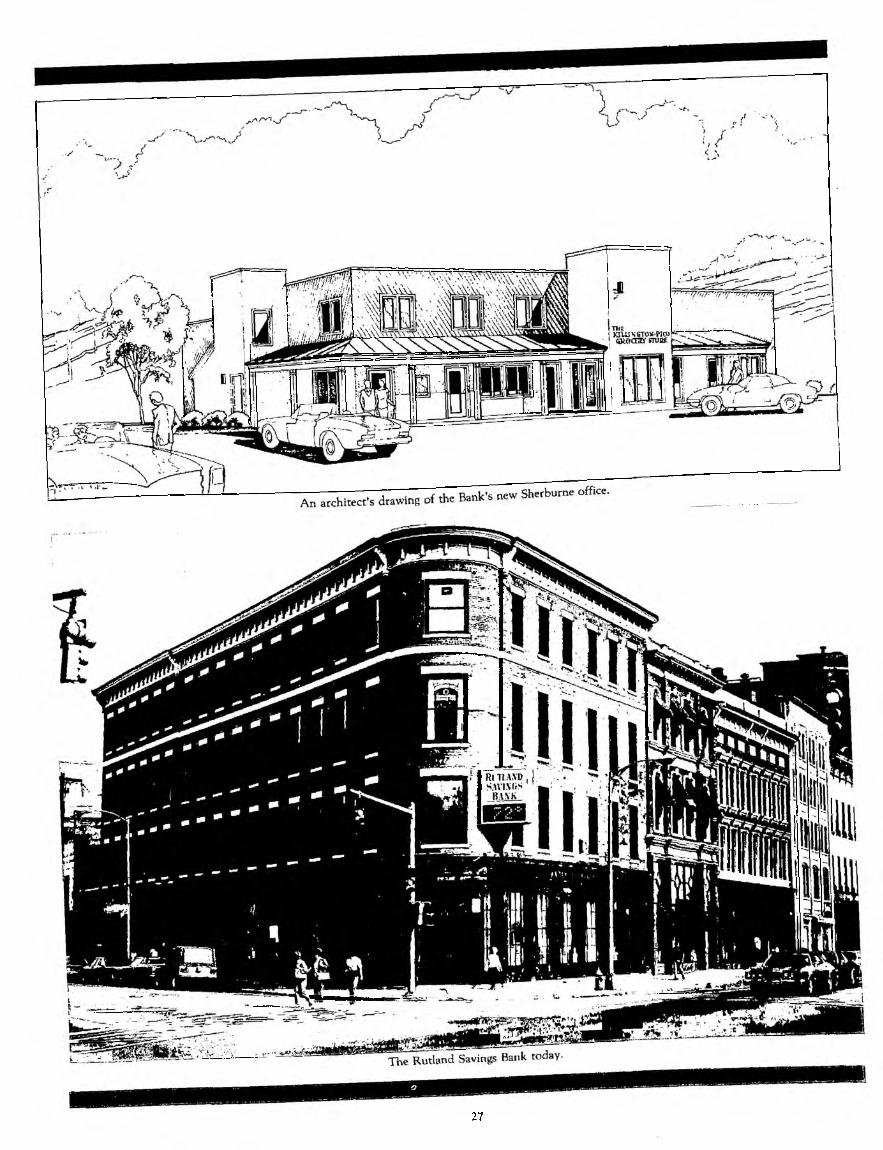

The Bank continued to branch out into the community. The Manchester office opened in March of 1977. At the end of the year, its deposits totaled over $5 million. The Ludlow office opened that December and had accumulated $600,000 by January. Rutland’s second facility opened on Woodstock Avenue in April of 1978, and the Bennington office in May of 1979. In addition to these full-service offices, five Free-Standing, Twenty-Four Hour Automated Teller sites were put into effect — those in Pawlet and Pittsford in 1979, with Wallingford, Bridgewater and Sherburne following in 1980. All offices are now also equipped with the Twenty-Four Hour Automatic Teller machines, which the customer can use to make deposits, mortgage and loan payments, and also to withdraw cash or transfer funds from checking to savings or vice-versa, at anytime of the day or night.

Financial services have grown, and public acceptance of these services has been outstanding. Despite the fact that money has been inordinately tight these last years, and that the nationwide rate of savings had declined (from 7.7% in 1975, to 3.3% in the last quarter of 1979), deposits at the Rutland Savings Bank have increased each year. In each of the last three years, assets have increased 29.4% over the year before. Nineteen seventy-seven was a red-letter year. For the first time, earnings netted over $1 million, and almost one-third of the total mortgage portfolio was put on the books during the year.

The Bennington office

The Pittsford office

The Bridgewater Mill Mall office

Through these years of ever-changing and expanding banking services, Rutland Savings became one of the fastest- growing institutions in the industry. The officers and staff have not lost sight of the fact that the Bank is a function of the community. They have worked with local, state and federal organi2ations to improve the quality of life, the economy of the Rutland region and to attract new money into the area.

In 1977, the Bank joined with several of the state’s commercial banks in sponsoring the Vermont Small Business Investment Corporation, the object being to provide more venture capital to small businesses in the state. In conjunction with that effort, the Bank began to consider mortgage financing of business facilities if their establishment would increase jobs and payroll in the region. In 1979, the Bank employed an Industrial Relations Officer as a liaison between the Bank and local industry. This officer’s job is to foster economic growth by working closely with the Rutland Industrial Development Corporation (RIDC), new business prospects, and federal, state and local developmental agencies.

With these efforts to improve the business and industrial climate, the individual has not been forgotten. Last year, President Ryan appeared before committees o f the Vermont House of Representatives and the United States Senate to urge a continuance of the Vermont Housing Finance Agency bond issuance. The Bank also cooperated with that agency to make low-cost energy conservation loans available to low and moderate-income Vermonters. Both efforts were successful.

In 1977, the Rutland Savings Bank formed a subsidiary to take title to all real estate, property and equipment purchased thereafter. In that same year, the subsidiary, named the Daniels Corporation after its first president and founder, purchased the next two buildings south on Merchants Row, and an extensive renovation program was begun. In the process, the facades of all three adjoining buildings were restored to a reasonable authenticity. The interiors were integrated to provide badly- needed departmental space as well as additional rental offices. The lengthy project reached completion in this one hundred and thirtieth anniversary year.

Shortly after its creation, the Daniels Corporation acquired the old Bennington Mill. It, too, has been restored and converted into offices, while retaining the historic detail of the building.

The subsidiary’s newest acquisition is Rutland’s own Opera House complex. In the mid-seventies, a local development concern bought three badly-dilapidated and unused buildings on Merchants Row in the heart of the city. The graceful facade of the original Opera House was restored and the interiors converted into attractive retail and office space. The Opera House project has been an enormous boon to Rutland, both aesthetically and commercially.

During the last two decades, Vermont, by virtue of its rural charm and its concern with protecting that quality, has attracted numerous out-of-staters who have become permanent

26

27

The Woodstock Avenue office

The Opera House with its newest face.

The G row th

residents. This new and idealistic energy, at work with proud and established Vermonters, has been extremely effective.

In the seventies a massive effort was commenced to wake a slumbering downtown Rutland. The Downtown Development Corporation (DDC), an energetic group composed of downtown business people, was created early in the decade. Through its efforts, an enormous amount of money has been brought into the area, and much has been accomplish' ed to benefit the city. With the aid of grant money, the DDC established the Rutland Area Transit, which serves Rutland and surrounding towns. The construction of a housing complex for the elderly began this year — its downtown location will benefit both the occupants of the project and downtown businesses. The DDC was responsible for writing a Historic Preservation Grant and distributing the money to interested downtown building owners to renovate their buildings. The grant provided $350,000 in seed money and has generated almost $6 million in return from the private sector. The DDC’s latest undertaking, one that has long been in the works, is the renovation of Center Street Alley into a fine arts and crafts- oriented commercial and studio area. Construction, which began this spring, will consist of rejuvenating present utilities, laying new brick paving and providing pedestrian and park amenities. The extension of the project to indoor areas will be left to the individual building owners.

The Rutland Savings Bank not only supported and worked with DDC on these programs but has taken an active part in them when possible. For the recently-finished renovation, the Bank built on $162,000 of the Historic Preservation seed money to generate over $2.6 million to local firms and workers.