sba 32 unit-1 type: 20% theory 80% problem...

TRANSCRIPT

ACADEMIC YEAR: 2015 – 2016 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/IYR /II Sem/UBA 32/FIN. ACC/UNIT-1 QB/VER1.0Unit – 1 Answers Page 1 of 13

SBA 32 – FINANCIAL ACCOUNTINGUnit-1 – ACCOUNTING CONCEPTS

Type: 20% Theory – 80% ProblemQuestion & Answers

PART – A ANSWERS

1. Define Subsidiary Books.(2015)A subsidiary account is an account that is kept within a subsidiary ledger, whichin turn summarizes into a control account in the general ledger.Subsidiary account is used to track information at a very detailed level for certaintypes of transactions, such as accounts receivable and accounts payable.

2. Define Accounting? (April 2012)According to the American Institute of Certified Public Accountants (AICPA)“Accounting is the art of recording, classifying and summarizing in a significantmanner and in terms of money transactions and events which are of a financialcharacter and interpreting the results thereof”.

3. Write short note on Accounting concepts? (Nov/Dec. 2013)The generally accepted principles were evolved from common experience ofaccountants, historical precedents, regulations of government agencies andstatements from professional bodies.

4. Write short note on ledger? (Nov/Dec. 2013)Ledger is the second important stage in the accounting cycle or process. In thisstage of a accounting cycle, all recorded business transactions or entries aregrouped on a predetermined basis. Ledger is the main book of accounts in abusiness. Ledger and the accounts contains are the core of accounting process.

5. What do you mean by subsidiary books? (Apr./May 2014)Maintaining a single Journal book in which journal entries are written for eachtransaction and posting them to ledger is practicable in small business where asingle accountant can maintain accounts or the owner himself can do the accountswork.

6. State any two accounting rules? (Apr./May 2014)1. To maintain accounting records2. To ascertain the financial position.

ACADEMIC YEAR: 2015 – 2016 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/IYR /II Sem/UBA 32/FIN. ACC/UNIT-1 QB/VER1.0Unit – 1 Answers Page 2 of 13

7. What is Double Entry System? (Apr./May 2013)The double entry system of accounting or bookkeeping means that every businesstransaction will involve two accounts (or more). Double entry also allows for theaccounting equation (assets = liabilities + owner's equity) to always be in balance.

8. What is meant by Dual Aspect Concept? (April 2012)This state that there are two aspects of accounting, one represented by the assets ofthe business and the other by the claims against them. The concept states that thesetwo aspect are always equal to each other. In other words, this is the alternate formAssets=Liabilities+CapitalDual aspect concept is known as "Double Entry Book Keeping System".

9. Define Journal?Recording is the first step which usually accomplished through journal orsubsidiary books. Classifying is achieved through ledger. Summarising isaccomplished by preparation of trial balance. Finalising is through preparation oftrading account, profit and loss account and balance sheet. It is essential tounderstand the objective of each stage and the books and records maintained toachieve the objective.

10. What are the objectives of accounting?1. To maintain accounting records.2. To calculate the result of operations.3. To ascertain the financial position.4. To communicate the information to users.

11. What is purchase book?Purchase book is also known as bought book, purchase day book, invoice book andpurchase journal. All credit purchases of goods are recorded in this book.Periodical total of this book provides total credit purchase of goods made by thefirm. Inward invoices received from suppliers, duly verified, form the basis forentries in purchase book.

12. What is Sales Book?Sales book is also known as day book, sales day book, sold book, sales journal etc.All credit sales of goods are recorded in this book. Periodical totals of this bookprovide the total credit sales of goods by the firm. Outward invoices form the basisfor making entries in the sales book.

ACADEMIC YEAR: 2015 – 2016 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/IYR /II Sem/UBA 32/FIN. ACC/UNIT-1 QB/VER1.0Unit – 1 Answers Page 3 of 13

13. What is Purchase Return Book?It is also called Return outward book and Purchase returns journal. Goods returnedto suppliers which were originally purchased on credit are recorded in this book.Periodical totals of this book provide data on purchase returns by the firm.

14. What is Sales Return Book?This book is also called Return inward book and sales return journal. Goodsreturned by customers who were originally sold on credit are recorded in this book.Monthly total of this book provide data on sales returns.

15. What is cash book?Cash book plays a dual role by serving as a subsidiary book and also as a ledgeraccount. It is the book of original entry because receipts and payments arerecorded in the cash book and they are posted to the different accounts in theledger.

16. Give Journal Entries for the following:a) Purchased goods from kumar for cash Rs. 6000b) Paid Interest Rs. 1500.

a) Purchase a/c 6000To Cash a/c 6000

(Purchased goods for cash)

b) Interest a/c 1500To Cash a/c 1500

(Paid interest)

17. What is debit note?Debit note means sent by the firm to the suppliers when goods are returned formthe basis for entries in this book.

18. What is credit note?Credit note sent to the customers after receiving the goods returned by them formthe basis for entries in this book.

ACADEMIC YEAR: 2015 – 2016 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/IYR /II Sem/UBA 32/FIN. ACC/UNIT-1 QB/VER1.0Unit – 1 Answers Page 4 of 13

19. Mention the different types of cash book?1. Simple cash book or single column cash book2. Two column cash book with cash and discount columns3. Two column cash book with bank and discount columns and4. Three column cash book with cash, bank and discount columns.

20. What is a “Three columnar cash book”?This cash book is of maximum utility because it minimizes work relating toaccounts and presents a summarized picture of the liquidity position of a business.

21. What are the basic documents needed for subsidiary books?Inward invoice, Outward invoice, Debit note, Credit note, Cash receipts andvouchers.

22. What are the benefits of subsidiary books?1. Reduction in work2. Permits group work3. Accuracy4. Better information5. Cash book

23. What is a contra entry?When cash is deposited into bank, it is debited in bank column on debit side andcredited in cash column on the credit side. Similarly, when cash is withdrawn forbusiness use, cash column is debited on the receipts side and bank column iscredited on the payment side. Thus, both debit and credit aspects of ‘contraentries” are completed in cash book itself.

24. What is Inward invoice?It is received from suppliers, duly verified, form the basis for entries in purchasebook.

25. What is Outward invoice?Outward invoice form the basis for making entries in the sales book. The invoicesmust be properly authenticated.

ACADEMIC YEAR: 2015 – 2016 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/IYR /II Sem/UBA 32/FIN. ACC/UNIT-1 QB/VER1.0Unit – 1 Answers Page 5 of 13

26. What are the methods of recording the purchase return book?As per the dates of returns made, entries are recorded in purchase returns book.Name of supplier, with details of goods returned and the relevant debit notenumber are shown along with the net amount.

PART – B ANSWERS

1. Give journal entries to the following transactions.(Apr/May 2015)Mar 1 sold goods to Ragavan for cash Rs. 9,500

2 Sold goods to Mugunthan Rs. 7,0003 Cash sales Rs.12,0004 Goods bought by Murthy Rs. 3,5005 Sold old Machinery Rs. 14,000

2. Prepare Double Column cash book from the following information.2000 cash balance Rs.6900 (Apr/May 2015)Mar 1

6 Paid to sundar Rs. 1,428 and received discount Rs. 729 Paid salary Rs.5,025

20 cash sales Rs, 11,37029 Cash withdraw for personal use Rs.1, 02030 Getting compensation from railway officer Rs. 4,38031 Cash received from santhi Rs.3, 975 and allowed discount Rs.75

3. Journalise the following(April 2012)(i) Sold goods to Mani for cash Rs 25,000(ii) Paid wages by cheque Rs. 10,000(iii) Old furniture sold to Ram for cash Rs 3,000

4. Journalise the following transactions in the books of Sri T.N of Coimbatore:(April/May 2013)

Oct 1 commenced business with Rs 50,0003 Purchased goods for cash Rs.10,000 at 5% trade discount.4 Paid Carriage Rs 508 Purchased machinery for Rs. 20,000

10 Sold goods to Madan on account for Rs.15,000

5. Why we are preparing subsidiary books? What are subsidiary books?Subsidiary Book:

Maintaining a single Journal book in which journal entries are written for eachtransaction and posting them to ledger is practicable in small business where asingle accountant can maintain accounts or the owner himself can do the accounts

ACADEMIC YEAR: 2015 – 2016 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/IYR /II Sem/UBA 32/FIN. ACC/UNIT-1 QB/VER1.0Unit – 1 Answers Page 6 of 13

work. In bigger transactions are so numerous and varied that a single journal bookis absolutely inadequate and cumbersome.Need for preparing subsidiary books:(a) Reduction in work: Overall work reduces in this system compared to a singlejournal because one posting alone is made on the date of the transactions.Consolidated monthly posting is made for the second aspect.(b)Permits group work: Single journal can be written by one personal alone.Work on subsidiary books can be carried on by many accountants.(c) Accuracy: Accounts will be more accurate because of specialized work andmonthly summarized postings.(d) Better information: A lot of useful data like total credit sales, creditpurchases, returns, etc., is made available which is not possible in journal system.(e) Cash book: Cash book itself takes the place of journal as well as ledgeraccount. Thus, separate cash account in not needed. In case of three column cashbook, even bank a/c is not needed in the ledger.

6. Enter the following transactions in the purchases book and sales Book ofMr.Pandian 2012 (April/May 2013)

Jan 1 Purchased goods from Balu 30,0002 Sold goods to swamy 15,0004 Bought goods from gown 13,500

12 Sold goods to Thenali 10,50019 Sold goods to jayaraman 75021 Bought goods from Rajesh 9,00030 Sold goods to shanthi 900

7. Explain types of accounts and state the rules for it? (Nov/Dec.2013)Types of Accounts:1. Personal Accounts2. Impersonal Accounts

Impersonal accounts can be further divided into real and nominal accounts. Thus,there

areThree kinds of accounts maintained by a business.

a) Personal Accounts: Accounts of persons with whom the business has dealingsare known as personal accounts. It takes the following forms:(i) Natural Accounts: The name of an individual – customers or suppliers.

ACADEMIC YEAR: 2015 – 2016 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/IYR /II Sem/UBA 32/FIN. ACC/UNIT-1 QB/VER1.0Unit – 1 Answers Page 7 of 13

(ii) Artificial persons or legal bodies: Firms’ accounts, limited companies’accounts, educational institutions’ accounts, bank account, co-operative societyaccount etc., are known as artificial persons, accounts.(iii) Representative personal accounts: All accounts representing outstandingexpenses and accrued or prepaid incomes are personal accounts.b) Real Accounts: Accounts in which the business records the real things ownedby it. i.e., assets of the business are known as real accounts. Real accounts are oftwo types i.e., tangible real accounts and intangible real accounts. There are someintangible real accounts, which cannot be toughed because they have no physicalshape such as trademark, goodwill, patents and copyright etc.c) Nominal Accounts: It relates to the items which exist in name only. Expenses,incomes etc., are there in business activities. Accounts which record expenses,losses, incomes and gains of the business are known as nominal accounts.

8. Describe any two accounting concepts? (Nov/Dec) 2013.There are the necessary assumptions or conditions upon which accounting isbased. Accounting concepts are postulates, assumptions or conditions upon whichaccounting records and statement are based. The various accounting concepts areas follows:Money measurement concept: As per this concept, in accounting everything isrecorded in terms of money. Events or transactions which cannot be expressed interms of money are not recorded in the books of accounts, even if they are veryimportant or useful for the business. Purchase and sale of goods, payment ofexpenses and receipt of income are monetary transactions which are recorded inthe accounting books however events like death of an executive, resignation of amanager are such events which cannot be expressed in money.Cost Concept (Objectivity Concept): This concept does not recognize therealizable value, the replacement value or the real worth of an asset. Thus, as perthe cost concept(a) As asset is ordinarily recorded at the price paid to acquire it i.e. at its cost, and(b) This cost is the basis for all subsequent accounting for the asset. For example,if a machine is purchased for Rs. 10,000/- it is recorded in the books at Rs.10,000/- and even if its market value at the time of the preparation of the finalaccount is Rs. 20,000/- or Rs. 60,000/- the same will not considered.

9. Prepare a three column cash book from the following( April 2012)

2011 RsMarch 1 Cash balance 20,000

Bank balance 23,000

ACADEMIC YEAR: 2015 – 2016 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/IYR /II Sem/UBA 32/FIN. ACC/UNIT-1 QB/VER1.0Unit – 1 Answers Page 8 of 13

3 Paid rent by cheque 5,0004 cash received on a/c of sales 6,0005 deposited into bank 8,0009 Bought goods by cheque 7,000

11 withdrew from bank for office use 5,00020 Paid into bank 3,00030 Paid salaries 10,000

10. Journalise the following transactions (Nov/Dec 2013)March 1 2011 sold goods to Ragavan for cash 9,500

2 Sold goods to Mukundan 7,0003 Cash sales 12,0004 Murthy bought goods 3,500

11. Record the following transactions in the Personal account of Kapil:2000 RsApr 1 sold goods to kapil 6,000

5 Cash received from kapil 5,800And allowed him discount 200

18 Kapil puchased goods 8,00030 received cash from kapil on account 4,500

May 1 balance from last month b/d 3,50012 sold goods to kapil 12,00022 received cash from kapil 4,850

And allowed him account 15031 Received cash in full settlement of

Kapil’s account 10,250

PART – C ANSWERS

1. Explain the difference between Journal with ledger? (April/May) 2014.1. Primary: Journal is the book of original entry; ledger is dependent on journalfor data.2. Recording: In the journal, recording is in chronological order – as and whentransactions take place. In ledger recording is analytical. Transactions relating toparticular accounts are entered in those accounts. No specific order is followed.3. Evidence Value: As book of primary entry, journal has better ‘evidence value’is case of legal problems. However, ledger is the primary source for assessingbusiness results.

ACADEMIC YEAR: 2015 – 2016 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/IYR /II Sem/UBA 32/FIN. ACC/UNIT-1 QB/VER1.0Unit – 1 Answers Page 9 of 13

4. Focus: In journal the focus is on ‘transaction’. Both aspects – debit and credit –of a transaction are to be recorded. In ledger, the focus is on account. All dealingsrelating to an account must be recorded in the account.5. Terminology: Recording in journal is called ‘journalising’. Recording ledger iscalled ‘posting’.6. Importance: Ledger is the main book of accounts. Journal is ‘subsidiary’which means secondary.7. Timing: Journalising is a continuous process. It has to be done day after day, asand when transactions take place. Ledger can be intermittent. It can be done anytime – either daily or once in a while, according to need convenience.

2. Briefly explain the various accounting concepts? (April/May) 2014.There are the necessary assumptions or conditions upon which accounting isbased. Accounting concepts are postulates, assumptions or conditions upon whichaccounting records and statement are based. The various accounting concepts areas follows:

1. Entity Concept: For accounting purpose the “business” is treated as a separateentity from the proprietor(s). One can sell goods to himself, but all thetransactions are recorded in the book of the business. This concept helps inkeeping private affairs of the proprietor away from the business affairs. E.g. If aproprietor invests Rs. 1,00,000/- in the business, it is deemed that the proprietorhas given Rs. 1,00,000/- to the “business” and it is shown as a “liability” in thebooks of the business. Similarly, if the proprietor withdraws Rs. 10,000/- from thebusiness, it is charged to them.

2. Dual Aspect Concept: As per this concept, every business transaction has adual affect. For example, if Ram starts business with cash Rs. 1, 00,000/- there aretwo aspects of the transaction: “Asset Account” and “Capital Account”. Thebusiness gets asset (cash) of Rs. 1, 00,000/- and on the other hand the businessowes Rs. 1, 00,000/- to Ram.

3. Going Business Concept (Continuity of Activity): It is assumed that thebusiness concern will continue for a fairly long time, unless and until has enteredinto a state of liquidation. It is as per this assumption, that the accountant does nottake into account the forced sale values of assets while valuing them.

4. Money measurement concept: As per this concept, in accounting everythingis recorded in terms of money. Events or transactions which cannot be expressed

ACADEMIC YEAR: 2015 – 2016 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/IYR /II Sem/UBA 32/FIN. ACC/UNIT-1 QB/VER1.0Unit – 1 Answers Page 10 of 13

in terms of money are not recorded in the books of accounts, even if they are veryimportant or useful for the business. Purchase and sale of goods, payment ofexpenses and receipt of income are monetary transactions which are recorded inthe accounting books however events like death of an executive, resignation of amanager are such events which cannot be expressed in money.

5. Cost Concept (Objectivity Concept): This concept does not recognize therealizable value, the replacement value or the real worth of an asset. Thus, as perthe cost concept as asset is ordinarily recorded at the price paid to acquire it i.e. atits cost, and this cost is the basis for all subsequent accounting for the asset. Forexample, if a machine is purchased for Rs. 10,000/- it is recorded in the books atRs. 10,000/- and even if its market value at the time of the preparation of the finalaccount is Rs. 20,000/- or Rs. 60,000/- the same will not considered.

6. Cost-Attach Concept: This concept is also known as “cost-merge” concept.When a finished good is produced from the raw material there are certain processand costs which are involved like labor cost, power and other overhead expenses.These costs have a capacity to “merge” or “attach” when they are broughttogether.

7. Accounting Period Concept: An accounting period is the interval of time atthe end of which the income statement and financial position statement (balancesheet) are prepared to know the results and resources of the business.

8. Accrual Concept: The accrual system is a method whereby revenue andexpenses are identified with specific periods of time like a month, half year or ayear. It implies recording of revenues and expenses of a particular accountingperiod, whether they are received/paid in cash or not.

9. Period Matching of Cost and Revenue Concept: This concept is based on theperiod concept. Making profit is the most important objective that keeps theproprietor engaged in business activities. That is why most of the accountant’stime is spent in evolving techniques for measuring the profit/profitability of theconcern. To ascertain the profit made during a period, it is necessary to match“revenues” of the period with the “expenses” of that period. Income (profit)earned by the business during a period is compared with the expenditureincurred to earn the revenue.

10. Realization Concept: According to this concept profit, should be accountedfor only when it is actually realized. Revenue is recognized only when sale is

ACADEMIC YEAR: 2015 – 2016 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/IYR /II Sem/UBA 32/FIN. ACC/UNIT-1 QB/VER1.0Unit – 1 Answers Page 11 of 13

affected or the services are rendered. However, in order to recognize revenue,receipt of cash us not essential. Even credit sale results in realization as it createsa definite asset called “Account Receivable”. However there are certain exceptionto the concept like in case of contract accounts, hire purchase etc. Similarlyincomes like commission interest rent etc. are shown in Profit and Loss A/c onaccrual basis though they may not be realized in cash on the date of preparingaccounts.

11. Verifiable Objective Evidence Concept: According to this concept allaccounting transactions should be evidenced and supported by objectivedocuments. These documents include invoices, contract, correspondence,vouchers, bills, passbooks, cheque etc.

3. Prepare purchase returns book sales returns book from the following data (April2012)

2010 RsDec 1 purchased goods returned to Arun 410

3 received goods returned by Ram 6005 goods returned to Kumar 1,6007 Sales returns of Rs.2520 by mohan

15 Returned defective goods to Ravi 2,56018 Damaged goods returned by Mani 2,24023 Outward returns to Kumar 55029 Inward returns by samy 1,50030 Returned inferior goods to sasi 1,78031 Sekar returned goods to us 2,660

4. What is single entry system? Distinguish between single entry system and doubleentry system? (April 2012)Single Entry System:There is no system of accounts called ‘Single Entry System’. The term singleentry is vaguely used to refer to any method of maintain accounts which does notconform to strict principles of double entry. Single entry does not mean that thereis only one entry for each transaction. In fact, single entry is a combination of (a)Double entry for some transactions like cash collected from debtors (b) single

ACADEMIC YEAR: 2015 – 2016 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/IYR /II Sem/UBA 32/FIN. ACC/UNIT-1 QB/VER1.0Unit – 1 Answers Page 12 of 13

entry for transactions like cash sales and (c) No entry for transactions likedepreciation.Difference between single entry and double entry system

Sl.No.

Basis of Difference Double Entry System Single Entry System

1. Recording oftransactions

Both aspects of alltransactions are recorded.

In some cases, bothaspects, in someothers a single aspector no aspect isrecorded.

2. Opening of Accounts All personal, real andnominal accounts areopened.

Only personalaccounts and cashaccount are opened.

3. Preparation of TrialBalance

Trial Balance can beprepared.

Trial Balance cannotbe prepared

4. Ascertaining profit andloss

Accurate profit or losscan be found, throughtrading and profit andloss a/c.

Profit or loss cannotbe found normally, inthe absence of tradingand profit and lossa/c.

5. Revealing financialposition

Reliable financialposition can be foundthrough balance sheet.

Balance sheet cannotbe prepared. So,financial position isdifficult to ascertain.

6. Acceptability Acceptable for Incometax and other taxpurposes, for raising ofbank loans etc.

Not acceptable fortaxation, claims,raising of loans. etc.

7. Acceptable evidence In case of disputes,accounting records can beproduced in courts of

The accountingrecords are notacceptable as

ACADEMIC YEAR: 2015 – 2016 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/IYR /II Sem/UBA 32/FIN. ACC/UNIT-1 QB/VER1.0Unit – 1 Answers Page 13 of 13

law. evidence.

8. Utility Suitable for any type ofbusiness of any size.

It can be followed bysmall business menwho can exercisepersonal control overthe business.

9. Internal check Internal check is possible. Internal check is notpossible.

5. Enter the following transactions in Rehan’s cash book with discount and cashcolumns1999 RsJan 1 cash balance 18,500

3 Cash sales 33,0007 Paid dravid 15,850

Discount allowed by him 15013 sold goods to manohar on credit 19,20015 cash withdrawn for personal expenses 2,40016 Purchased goods from Charles on credit 14,30022 Paid into bank 22,75025 Cash received from Monohar 19,000

Allowed him discount 20026 Drew a cheque for office use 17,50027 Paid cash to saravanan 2,950

Discount received from him 5028 Paid cash to Charles less discount 14,20029 Cash purchases 13,50030 Paid for advertising 60031 Paid salaries 12,000

-----

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/I YEAR/VI Sem/UBA 32/FIN. ACC/UNIT-2QB/VER 2.0Unit – 2Answer Page 1 of 13

UBA 32 – FINANCIAL ACCOUNTINGUnit-2 – TRAIL BALANCE AND DEPRECIATION

Type:20% Theory – 80% ProblemQuestion Bank

Syllabus: [Regulation: 2012]UNIT II: Trial balance-depreciation-need for depreciation-straight line andWDV methods of charging depreciation only.

PART – A QUESTIONS

1. Short Note on Trial Balance? (Nov/Dec.2013)A trial balance is a list of all the General ledger accounts (both revenue andcapital) contained in the ledger of a business. This list will contain the name of thenominal ledger account and the value of that nominal ledger account. The value ofthe nominal ledger will hold either a debit balance value or a credit balance value.The debit balance values will be listed in the debit column of the trial balance andthe credit value balance will be listed in the credit column. The profit and lossstatement and balance sheet and other financial reports can then be producedusing the ledger accounts listed on the trial balance.

2. Define Trial Balance?According to Carter “Trial balance is the list or debit and credit balances, takenout from ledger; it also includes the balances of cash and bank taken from cashbook”.

3. What are the methods of preparation of Trial Balance?A trial balance may be prepared according to either of the following two methods:Total method: If the total of debit sides of all accounts in the ledger is placed inone column of the list and similarly total of credit sides of all the accounts in theledger is placed in another column of the list then list of total will be known tohave been prepared with the total methods.Balances method: According to this system a trial balance is prepared on thebasis of balances of accounts. It is based on the mathematical maxim that if equalsare taken away from equals, results are equal. This method is simple and requiresless work.

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/I YEAR/VI Sem/UBA 32/FIN. ACC/UNIT-2QB/VER 2.0Unit – 2Answer Page 2 of 13

4. Is trial balance a conclusive proof of the accuracy of books of accounts?No, Trial balance is not being the conclusive proof of the accuracy of books ofaccounts, because there are certain errors which are not disclosed by the trialbalance even if it tallies.1. Errors not disclosed by trial balance.2. Errors disclosed by trial balance.

5. How do you compute depreciation rate under straight line method? (April2012)

In straight line depreciation method, depreciation is charged uniformly over thelife of an asset. We first subtract residual value of the asset from its cost to obtainthe depreciable amount. The depreciable amount is then divided by the useful lifeof the asset in number of accounting periods to obtain depreciation expense peraccounting period. Due to the simplicity of the straight line method ofdepreciation, it is the most commonly used depreciation method.FormulaThe formula to calculate the straight-line depreciation of an asset for a fullaccounting period is:

Depreciation =Cost − Salvage ValueLife in Number of Periods

6. What is written down value method of depreciation? (Apr/May 2013)

In Written downvalue method, the rate of depreciation is predetermined. This isdone by deducting the amount of depreciation charged before from the balance ofcost of asset (Cost of Asset-Estimated Scrap Value). In simple words, in the firstyear the amount of depreciation charged is high and it gradually starts decreasingduring the subsequent years.

7. Explain fixed instalment method of depreciation? (Apr/May 2014)

According to the fixed instalment method or cost price method, a fixed amount ofdepreciation is written off annually (therefore the amount of depreciation will besame every year.) It is calculated according to the life span of a fixed asset.

8. What is depreciation?Depreciation is a permanent decline in the value of an asset. The gradualdecrease, both in the value and usefulness, of an asset due to its nature and usageis termed as depreciation.

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/I YEAR/VI Sem/UBA 32/FIN. ACC/UNIT-2QB/VER 2.0Unit – 2Answer Page 3 of 13

9. What is the need for depreciation?Ascertainment of true profit or lossAscertainment of true cost of productionTrue valuation of assetsReplacement of assetsKeeping capital intact

10. What are the types of depreciation?1. Straight Line Method or Fixed Instalment Method or Original Cost Method2. Diminishing Balance Method or Reducing Instalment Method or Written Downvalue method.3. Annuity Method4. Depreciation Fund or Sinking Fund Method5. Insurance Policy Method6. Revaluation Method7. Depletion or Output Method8. Machine Hour Rate Method

11. What is Error of Principle?An accounting mistake in which an entry is recorded in the incorrect account,violating the fundamental principles of accounting. An error of principle is aprocedural error, meaning that the value recorded was the correct value but placedincorrectly.

12. What is Error of Complete Omission?When no entry is made for a transaction in journal or in the subsidiary books, trialbalance will tally. Such errors are known as errors of omission, which are notdisclosed by trial balance.

13. What is Error of Duplication?Such errors arise when an entry in a book of original entry has been made twiceand has also been posted twice.

14. What is Error of Commission?Posting of correct amount but to a wrong side of the proper accountPosting of wrong amount to the correct side of proper accountPosting to the correct side of the proper account but twiceA customer’s account may be debited twice for a sale of goods

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/I YEAR/VI Sem/UBA 32/FIN. ACC/UNIT-2QB/VER 2.0Unit – 2Answer Page 4 of 13

15. What is Error of Partial Omission?While posting from journal to ledger, omission of posting to some account ismade, e.g., furniture purchased for cash Rs. 1000. In this case Rs. 1000 may berecorded in the debit side of furniture account but not recorded in the credit sideof cash account.

16. What is Error of Casting?This type of mistake may occur in the subsidiary books. While totaling purchasesbook or sales book or sales returns book or purchase returns book, higher or loweramount maybe written.

17. What is Error in Balancing?While balancing the ledger accounts, this type of error may occur. The balanceshown in an account may be more or less than the correct figure.

18. Define Depreciation?According to International Accounting Standards Committee “Depreciation is theallocation of the depreciable amount of an asset over its estimated usefullife.Depreciation for the accounting period is charged to income either directly orindirectly”.

19. Mention any three causes for depreciation?(i) Use(ii) Lapse of time(iii) Obsolescence

20. Mention the various methods of providing for depreciation?(a) When a provision for Depreciation Account is not maintained(b) When a provision for depreciation Account is maintained.

21. What is Revaluation Method?A method of calculating the depreciation of assets, by which the asset isdepreciated by the difference in its value at the end of the year over its value atthe beginning of the year.

22. Explain the meaning of (a) Obsolescence (b) Amortisation?(a)Amortisation: Refers to the expensing of intangible capital assets (intellectualproperty: patents, trademarks, copyrights, etc.) in order to show their decrease in

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/I YEAR/VI Sem/UBA 32/FIN. ACC/UNIT-2QB/VER 2.0Unit – 2Answer Page 5 of 13

value as a result of use or passage of time. This could be because of consumption,expiration or(b) Obsolescence:Loss of usefulness occasioned by improved productionmethods is known as obsolescence.

23. What are the merits of Annuity Method?Advantages:Useful method to use in respect to long-term lease which generally involveconsiderable capital outlay.Interest on capital investment is taken into account. This method is perceived tothe most exact, precise and scientific form from the point of view of calculations.

24. What is Machine Hour Rate Method?Machine hour rate is useful for calculating the value of different overheadsfastly.Because depreciation is one of main overhead of the business, so, we can usemachine hour rate method for calculating the value of depreciation.As per machine hour rate method of depreciation, we calculate the total life of anyfixed asset on the basis of its working hour’s life. After this, we divide actual costof fixed assets with life of fixed assets in hours. After dividing, we will obtain thedepreciation rate per hour.

25. A company purchased a plant for Rs. 50000. The useful life of the plant is 10years and the residual value is Rs. 10000. Find out the rate of depreciation underthe straight line method.Solution:

Cost – Estimated Scrap ValueAmount of Depreciation = ________________________

No. of years of expected life= 50,000 – 10,000

------------------- = Rs. 4,00010 YearsDepreciation

Rate of Depreciation = ------------------------- x100Original cost of plant

= 4,000-------- X 10050,000

= 8 %

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/I YEAR/VI Sem/UBA 32/FIN. ACC/UNIT-2QB/VER 2.0Unit – 2Answer Page 6 of 13

PART – B QUESTIONS

1. An asset is purchased for Rs. 25,000.Depreciation is to be provided annuallyaccording to the straight line method. The useful life of the asset is 10 years andthe residual value is Rs.5, 000. Your are required to find out rate of depreciationand prepare the Asset A/C for the first three years.(April/May 2013)

2. Prepare Trial Balance:(April/May 2013)RsOpening stock 10,600Wages 2,200Carriage 200Commission (Dr) 300Purchases 12,000Return inward 440Trade expenses 580Rent 200Plant 2,600Repairs to plant 460Cash in hand 200Cash at Bank 1,000Debtors 3,000Income tax 500

3. Prepare trial balance from the following data of Nathan year ended 31.12.2012(Nov/Dec 2013)Capital 40,000Sales 25,000Creditors 1,000Purchases 15,000Salaries 2,000Rent 1,500Insurance 300Machineries 28,000Drawings 5,000

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/I YEAR/VI Sem/UBA 32/FIN. ACC/UNIT-2QB/VER 2.0Unit – 2Answer Page 7 of 13

Bank 4,500Cash 2,000Opening Stock 5,200Debtors 2,500

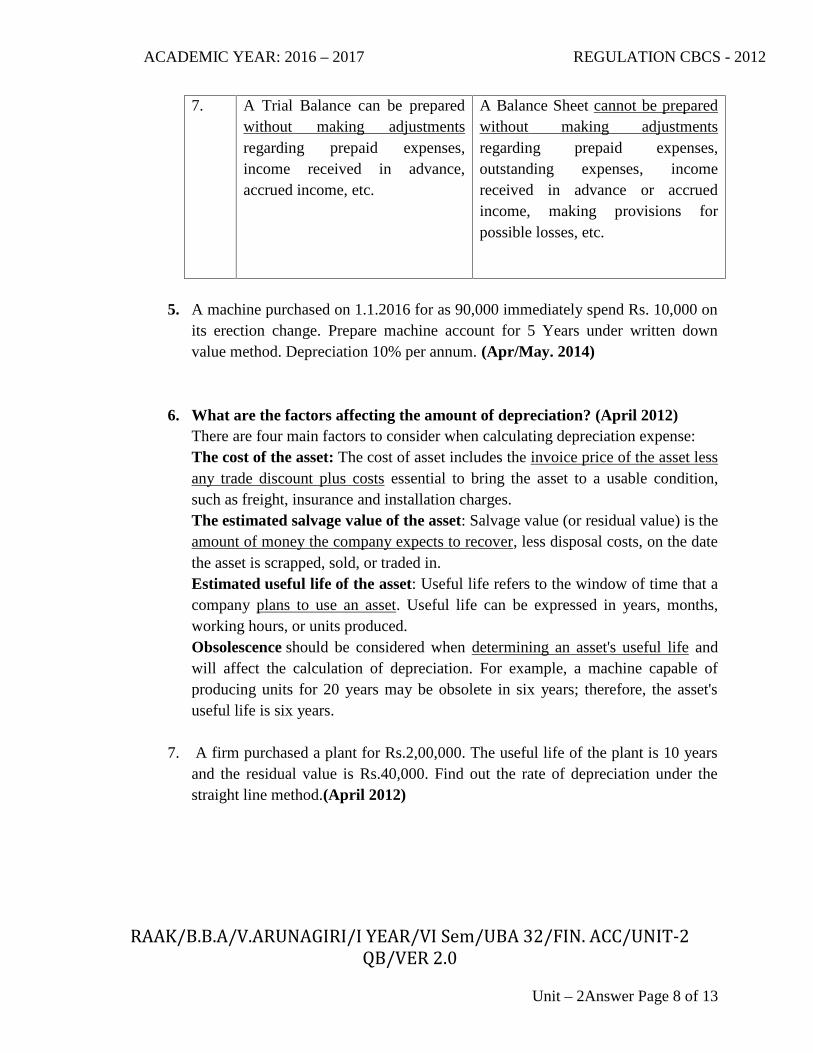

4. Explain the difference between Trial Balance and Balance Sheet? (Nov/Dec.2013)

S.No. Trial Balance Balance Sheet

1. A Trial Balance is prepared tocheck the arithmetical accuracy ofthe books of accounts.

A Balance Sheet is prepared to knowthe financial position of the businessenterprise on a given date.

2. A Trial Balance can be preparedfrequently. It may be prepared atthe end of a month or a quarter.

A Balance Sheet is generallyprepared at the end of the accountingperiod.

3. The heading of the two columnsare “Debit Balances” and “CreditBalances”.

The headings of the two sides are“Liabilities” and “Assets”.

4. All types of accounts find theirplace in the Trial Balance.

In a Balance Sheet, accounts ofassets, liabilities, capital and thoseaccounts which are remained openafter the preparation of Trading andProfit and Loss account.

5. Generally, the opening stockappears in the Trial Balance,whereas the closing stock doesnot.

In a Balance Sheet, only the closingstock appears on the assets side.

6. In a Trial Balance, it is notpossible to have information aboutnet profit or net loss.

In the Balance Sheet, informationabout net profit earned or net lossincurred is provided.

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/I YEAR/VI Sem/UBA 32/FIN. ACC/UNIT-2QB/VER 2.0Unit – 2Answer Page 8 of 13

7. A Trial Balance can be preparedwithout making adjustmentsregarding prepaid expenses,income received in advance,accrued income, etc.

A Balance Sheet cannot be preparedwithout making adjustmentsregarding prepaid expenses,outstanding expenses, incomereceived in advance or accruedincome, making provisions forpossible losses, etc.

5. A machine purchased on 1.1.2016 for as 90,000 immediately spend Rs. 10,000 onits erection change. Prepare machine account for 5 Years under written downvalue method. Depreciation 10% per annum. (Apr/May. 2014)

6. What are the factors affecting the amount of depreciation? (April 2012)There are four main factors to consider when calculating depreciation expense:The cost of the asset: The cost of asset includes the invoice price of the asset lessany trade discount plus costs essential to bring the asset to a usable condition,such as freight, insurance and installation charges.The estimated salvage value of the asset: Salvage value (or residual value) is theamount of money the company expects to recover, less disposal costs, on the datethe asset is scrapped, sold, or traded in.Estimated useful life of the asset: Useful life refers to the window of time that acompany plans to use an asset. Useful life can be expressed in years, months,working hours, or units produced.Obsolescence should be considered when determining an asset's useful life andwill affect the calculation of depreciation. For example, a machine capable ofproducing units for 20 years may be obsolete in six years; therefore, the asset'suseful life is six years.

7. A firm purchased a plant for Rs.2,00,000. The useful life of the plant is 10 yearsand the residual value is Rs.40,000. Find out the rate of depreciation under thestraight line method.(April 2012)

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/I YEAR/VI Sem/UBA 32/FIN. ACC/UNIT-2QB/VER 2.0Unit – 2Answer Page 9 of 13

8. What are the causes for depreciation?

The following are the main causes of depreciation:

(i) Use: Wear and tear is an important cause of depreciation in the case of atangible fixed asset. It is due to use of the asset.

(ii) Lapse of time: Assets such as, lease, copyright, patent etc. have a fixednumber of years of legal life, after the expiry of which, they are rendered useless.As such, their cost is written off over their legal life and the amount chargedagainst revenue every year is known as depreciation. This is true of acquiredgoodwill also. In these cases, depreciation is known as “amortization”.

(iii) Obsolescence:Loss of usefulness occasioned by improved productionmethods is known as obsolescence.

(iv) Accidents: An asset may reduce in value because of an accident. Accidentalloss may be permanent but it is not continuing and gradual.

(v)Disuse: A machine remaining continuously idle becomes potentially less andless useful with the passage of time. In fact, certain machines life farmimplements and machinery used in farming kept in the open, may depreciate morerapidly from disuse than from use.

(v) Inadequacy: It refers to the termination of the use of an asset because ofgrowth and changes in the size of the firm.

(vii) Depletion: An asset may get exhausted through working as in the case ofmines, quarries, oil fields and forests etc. The natural resources such as minerals,granite, oil and timber get exhausted because of extraction and exploitation, andthe asset becomes useless.

9. Explain the errors which are disclosed by the Trial balance?

A trial balance may not tally because of the following errors:

1. Errors of Commission: There are clerical errors committed by the staff in theaccounting department. Such mistakes arise in the following ways:

(a) Posting of correct amount but to a wrong side of the proper account. Forexample, instead of crediting a supplier who has supplied goods on credit, hisaccount might have been debited.

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/I YEAR/VI Sem/UBA 32/FIN. ACC/UNIT-2QB/VER 2.0Unit – 2Answer Page 10 of 13

(b) Posting of wrong amount to the correct side of proper account: Instead ofdebiting Rs. 200 in customer’s account, he may be debited with Rs. 2,000.(c) Posting to the correct side of the proper account but twice.A customer’s account may be debited twice for a sale of goods.(ii) Errors of partial omission: While posting from journal to ledger, omissionof posting to some account is made, e.g., furniture purchased for cash Rs. 1,000.In this case Rs. 1,000 may be recorded in the debit side of furniture account butnot recorded in the credit side of cash account.(iii) Errors in Casting: This type of mistake may occur in the subsidiary books.While totaling purchases book or sales book or sales returns book or purchasereturns book, higher or lower amount may be written. For example, if the actualtotal of purchases book if Rs. 2,000, it may wrongly be totaled as Rs. 2,200. Thisis known as over casting. If the amount is wrongly totaled as Rs. 1,800, it isknown as under casting. Such mistakes will get transferred to ledger andultimately to the trial balance. As result, trial balance will not tally.(iv) Errors in carrying or bringing forward: While transferring the totalamount from one page to another, this type of error may occur. For example, thetotal of the sales book Rs. 698 on page 15 may be taken to page 16 as Rs. 968.(v) Error in balancing: While balancing the ledger accounts, this type of errormay occur. The balance shown in an account may be more or less than the correctfigure.

10. Messrs.SarojiniBalu& Co purchased a machine for Rs. 22,000 on January 1 1992.The estimated life4 of the machine is 10 years after which its break – up valuewill be Rs.2000.Depreciation has to be charged at 21 % on the diminishingbalance. There was an addition to the original plant on January 1 1994 to thevalue of Rs.4000. You are required to prepare machinery account for the firstthree years.

11. A Company purchased a plant for Rs. 1, 00,000.The useful life of the plant forRs.1,00.000. The useful life of the plant is 5 years and the residual value is Rs.10,000. Find out the rate of depreciation under this straight linemethod.(Apr/May2015)

12. Prepare Trial Balance from the following: (Apr/May 2015)Capital 1,00,000Debtors 50,000Creditors 60,000Purchase 60,000

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/I YEAR/VI Sem/UBA 32/FIN. ACC/UNIT-2QB/VER 2.0Unit – 2Answer Page 11 of 13

Sales 1,20,000Opening stock 70,000Land and Buildings 1,00,000

PART – C QUESTIONS

1. Prepare trail balance for the year ended 31.3. 2011 (Nov/Dec 2013)Capital 1,24,000Land and Building 84,000Purchases 81,350Stock(1.4.2010) 11,520Debtors 29,000Machinery 40,000Furniture 15,000Sales 1,97,500Sales returns 1,350Creditors 30,660

2. A machine was purchased for Rs. 90,000 and spend installation expenses of Rs.15,000. The machine size is 5 years with the scrap realizable worth Rs.5,000 atthe end of the year. The depreciation is calculated on straight line method.Calculate (a) Amount of depreciation

(b) Rate of Depreciation (Apr/May 2014).(c)

3. A machine was bought on 1.1.2008 for Rs.60,000 and installation expensesamount to Rs. 15,000.Depreciation was provided at 10% on the reducing balancemethod . It was sold on 30.6.2010 for 36,250. Show the machine account (April2012)

4. On 1.1. 2001, Machinery was purchase for 30,000. Depreciation at the rate of10% on the original cost was written off during the first two years. For the nexttwo years, 15% was written off the diminishing balance method. The machinerywas sold for Rs.15, 000. Write up the machinery account for four years and givejournal entries. (Apr/May 2015)

5. What are the guidelines to locate the errors when trial balance is not tallied?When the trial balance disagrees, it is necessary to find out immediately where themistake lies. A routine procedure for this may be stated as under.

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/I YEAR/VI Sem/UBA 32/FIN. ACC/UNIT-2QB/VER 2.0Unit – 2Answer Page 12 of 13

(i) Total thedebit and credit sides of the trial balance once again.(ii) Find out whether there is any item in thetrial balance with an amount equal tohalf of the difference and if there is any;check up whether the amount is written inthe correct column. e.g., if sales returns amount say Rs, 200 is entered in thecredit column, the difference in the trial balance would be Rs, 400 excess credit.(iii) See whether any ledger balance is left out of the trial balance.(iv) Check up the ledger balances in the accounts with the balances shown in thetrial balance.(v) If totals of different ledger accounts are taken collectively in the trial balance,as in case of sundry creditors account, see whether the total of the balances of allthe individual ledger accounts tallies with the collective total taken in the trialbalance.(vi) Compare the present trial balance with that of a previous year to ascertainwhether the name of some ledger account appeared therein is inadvertentlyomitted from the present trial balance.(vii) If the error remains still undetected, check all the subsidiary books withparticular attention to the posting to ledger accounts.(viii) Check all carry forwards, particularly where accounts have openingbalances. Check them with the help of previous balance sheet and other schedules.(ix) Recast all the ledgers, taking utmost care to see that the correct balances havebeen carried down and that the accounts are accurately balanced.

6. Explain straight line method of providing for depreciation and its merits anddemerits?In straight line depreciation method, depreciation is charged uniformly over thelife of an asset. We first subtract residual value of the asset from its cost to obtainthe depreciable amount. The depreciable amount is then divided by the useful lifeof the asset in number of accounting periods to obtain depreciation expense peraccounting period. Due to the simplicity of the straight line method ofdepreciation, it is the most commonly used depreciation method.

Formula

The formula to calculate the straight-line depreciation of an asset for a fullaccounting period is:

Depreciation =Cost − Salvage ValueLife in Number of Periods

Merits:

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/I YEAR/VI Sem/UBA 32/FIN. ACC/UNIT-2QB/VER 2.0Unit – 2Answer Page 13 of 13

1. This method is very simple and easy to calculate.2. The value of asset can be reduced to zero (or its scrap value) under this method.3. This method is suitable, for these assets whole working life can easily beestimated.4. It is recognized by the Companies Amendment Act of 1988.

Demerits:1. The same amount of depreciation is charged every year irrespective of the useof the asset. Thus, it does not take into account the effective utilization of theasset.2. In this method, it becomes difficult to calculate the depreciation on additionsmade during the particular year.3. It does not make any provision for the interest on capital invested in fixed asset.4. As the amount of depreciation remains fixed even during the inflation period,maintenance of capital becomes difficult.5. This method tends to report an increasing rate of return on investment in theasset on account of the fat that net balance of the asset account is taken.

-----

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/II Sem/UBA21/FIN. ACC/UNIT-III ANS/VER 2.0Unit – 3 Answer Page 1 of 8

UBA21 – FINANCIAL ACCOUNTINGUnit-III – FINAL ACCOUNTS

Type: 20% Theory – 80% ProblemQuestion & Answer Bank

Syllabus: [Regulation: 2012]UNIT III: Preparation of trading, profit and loss account and balance sheet.

PART – A

1. What is profit and loss account? (Apr. /May 2013 May 2015 ,2016)Profit and Loss account is an account into which all gains and losses are

collected in order to ascertain the excess of gains over the losses or vice versa.Profit and loss account is prepared in order to calculate the net profit and net lossof the business.

2. “Balance Sheet”? (Nov. /Dec. 2013)According to R.N. Antony “Balance sheet is a screen picture of the

financial position of a going business at a certain moment”.

3. ‘Net Loss”? (Nov. /Dec. 2013)When total of all the expenses is more than gross profit and other income,

there remains a deficit and this is called net loss.

4. “Drawings”? (Nov. /Dec. 2013)Drawing means any amount withdraws from business for personal use.

Not only cash but if we withdraw any product from business or any asset ofbusiness for personal use that will be drawing. It surely reduces the capital of anybusiness. It is shown on the liability side of the balance sheet and it is reducedfrom the capital.

5. What do you understand by final accounts? (April 2012)The manner in which the amount of profit or loss has been arrived at is

disclosed in the statement of accounts, prepared at the end of the accountingperiod.

6. What is gross profit? (April 2012)Gross profit is the difference between actual sale proceeds and the cost of

goods sold. [Gross profit = Excess of sale proceeds over cost of goods sold].

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/II Sem/UBA21/FIN. ACC/UNIT-III ANS/VER 2.0Unit – 3 Answer Page 2 of 8

7. What are Non-Operating expenses?These expenses are not related to the operation of the business and

include capital losses as loss on the sale of furniture etc., writing off fictitiousassets as preliminary expenses, underwriting commission etc., writing offintangible assets as goodwill, copyright, patents etc.

8. What are Operating expenses?It refers to those expenses which are incurred in order to operate the

business efficiently and smoothly. These include administration, selling,distribution, finance and maintenance expenses.

9. When do you prepare a ‘Manufacturing Account’?Those concerns which convert raw materials into finished goods and then

sell the finished goods are required to prepare manufacturing account. Thisaccount is prepared to calculate the cost of goods manufactured, which istransferred to the trading account.

10. Pass necessary adjusting entries in Mr. X’s journal on 31st December1988:

(i) Rs. 20,000 for wages was outstanding.(ii) Write off depreciation on machinery Rs. 50,000.(iii) Rs. 15,000 was received in advance as interest.

Ans:S.N. Particulars Debit Credit(i) Wages a/c Dr

To Outstanding Wages a/c(Being wages outstanding)

20,00020,000

(ii) Depreciation a/c DrTo Machinery a/c

(Being depreciation on machinery)

50,00050,000

(iii) Interest a/c DrTo Interest received in advance a/c

(Being interest received in advance)

15,00015,000

11. What is a final account?In short, the businessman wants to know the profitability and the financial

soundness of the business. The final accounts are prepared at the end of the yearfrom the trial balance. These two statements i.e., trading and profit and lossaccount and balance sheet are prepared to give the final results of the business.

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/II Sem/UBA21/FIN. ACC/UNIT-III ANS/VER 2.0Unit – 3 Answer Page 3 of 8

12. What do you understand by provision for bad and doubtful debts? (Apr./May. 2013)

As there is a possibility of anticipated losses and in order to provide for suchloss in the accounts, a provision for doubtful debts is required to be made.

13. What are the distinct stages in final accounts?There are three distinct stages in final accounts they are trading, profit and

loss account and balance sheet.

14. What is the result of each such stage in final accounts?Trading a/c – the expenses relating to factory is shown in this a/c.Profit & Loss a/c – to calculate the net profit or net loss of the business.Balance sheet – to measure the correct financial position of a business.

15. Are adjustments necessary for the preparation of final accounts? If yes,why?

Yes, there are certain necessary adjustments needed for the preparation offinal accounts, they are closing stock, outstanding expenses, prepaid expenses,accrued income, income received in advance, depreciation of assets, etc.,

16. What are the situations in which purchase account is credited?The purchase returns is a credit balance shown the return of goods to thesuppliers. It should be subtracted from the total purchases to get the net purchases.

17. What are all items added to and reduced from the capital of a sole traderin balance sheet?

In balance sheet, first add the net profit or subtract the net loss and addinterest on capital to the capital. Then subtract drawings and interest on drawingsto the capital.

18. What is the purpose of preparation of profit and loss account?Profit and loss account is prepared in order to calculate the net profit or net

loss of the business. Since the profit and loss account is prepared to show the netprofit earned or net loss incurred during a particular period.

19. What are fictitious assets?As the name implies such “assets” are not really assets. No amount can be

realised or further benefit derived from the expenditure concerned. These assetsare shown on the assets side of the balance sheet till they are fully written off.

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/II Sem/UBA21/FIN. ACC/UNIT-III ANS/VER 2.0Unit – 3 Answer Page 4 of 8

20. What are contingent assets?Contingent asset is one, the existence of which depends upon the happening

of a certain event which may or may not take place. For example: claim forincome tax refund, uncalled share capital of a public limited company, claim bythe firm for infringement of trademarks or patent copy right etc.

21. What are contingent liabilities?Contingent liability will become an actual liability only on the happening of

a certain event which may or may not happen. For example bills discounted andendorsed which may be dishonoured, claim by others, unpaid call amount oninvestments.

22. What are outstanding expenses? (2015 May 2015) (Nov/ Dec 2016)These are certain expenses which relate to a particular accounting period but

they are not paid in that accounting period due to certain reasons. It is added tothe respective account in the trading or profit and loss a/c and also shown on theliabilities side of the balance sheet.

23. What are prepaid expenses?Prepaid expenses are those expenses which have been paid in advance but

relating to the future accounting period. These are also called the unexpiredexpenses. It is deducted from the respective account of trading and profit & lossa/c and also shown on the asset side of the balance sheet.

24. What is accrued income?Outstanding or accrued income is the income which has been earned but not

received during the accounting period. It is shown on the asset side of balancesheet and it is added to the respective income account in P & L a/c credit side.

25. What is income received in advance?Without rendering any service the trader receive income. Such an income is

known as income received in advance, i.e, the income received but not earnedduring the accounting period. It is shown as deduction from the respective incomein P & L a/c and is shown on the liabilities side of balance sheet.

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/II Sem/UBA21/FIN. ACC/UNIT-III ANS/VER 2.0Unit – 3 Answer Page 5 of 8

PART – B

1. Question and Answer in Hard copy (Nov. /Dec. 2013)2. Question and Answer in Hard copy (Apr. /May 2013)3. Question and Answer in Hard copy (Apr. /May 2013)4. What are the items appearing on debit side of profit & loss a/c?

The business expenses are divided into two types. Direct expenses which arerecorded in the trading a/c and indirect expenses which are recorded in the debitside of profit & loss a/c. Indirect expenses can be further divided into twovarieties:(i) Operating expenses and (ii) Non-operating expenses(i) Operating expenses: It refers to those expenses which are incurred in order tooperate the business efficiently and smoothly. These include administration,selling, distribution, finance and maintenance expenses.(ii) Non-operating expenses: These expenses are not related to the operation ofthe business and include capital losses as loss on the sale of furniture etc., writingoff fictitious assets as preliminary expenses, underwriting commission etc.,writing of intangible assets as goodwill, copyright, patents etc.

5. Question and Answer in Hard copy.6. Question and Answer in Hard copy. (Apr. /May 2014)7. How do you treat accrued incomes and incomes received in advance when

they are given in trial balance and in adjustments?Accrued income: Accrued income is shown on the asset side of balance sheetand it is added to the respective income account in P & L a/c credit side. Noadjustment is required in the P & L a/c if accrued income a/c appears in the trialbalance, but such an account must be shown as an asset in balance sheet.Income received in advance: Income received in advance is shown as deductionfrom the respective income in P & L a/c and is shown on the liabilities side of thebalance sheet. No treatment is required in the P & L a/c if income received inadvance account appears in the trial balance. But such account must be shown asa liability in the balance sheet.

8. How do you treat stock when it is given in trial balance and in adjustments?The stock on hand at the beginning of the year is called opening stock. This itemis usually shown as the first item on the debit side of the trading account. Thefigure is available from the trial balance. It may include raw materials, work-in-progress and finished goods.Closing stock refers to the unsold goods which is lying in the godown at the endof the accounting year. Generally, the closing stock does not appear in the trial

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/II Sem/UBA21/FIN. ACC/UNIT-III ANS/VER 2.0Unit – 3 Answer Page 6 of 8

balance. It appears outside the trial balance. The value of closing stock willappear on the assets side of balance sheet and on the credit side of tradingaccount. In trial balance opening stock is shown on the debit side.

9. What are the items appearing on the debit and credit side of trading a/c?Item appearing on the debit side of trading a/c:1. Opening stock: Stock on hand at the beginning of the year is called openingstock.2. Purchases: It shows the gross amount of purchases made of the materials andsaleable goods.3. Purchase returns or Returns outwards: The purchase returns is a creditbalance showing the return of goods to the suppliers. It should be subtracted fromthe total purchases.4. Direct expenses: It refers to those expenses which are incurred for making thegoods saleable. Factory rent, wages, octroi, freight on purchases, manufacturingexpenses, import duty, carriage inward, customs duty, dock dues, clearing chargesetc.Item appearing on the credit side of trading a/c:1. Sales: It is a credit balance indicating the total sales of goods made during theyear. It includes both cash and credit sale of goods.2. Sales return: This is a debit balance, showing the total amount of goodsreturned by the customers. It should be subtracted from the total sales.3. Closing stock: It refers to the unsold goods, which is lying in the godown atthe end of the accounting year. If it is given outside the trial balance, it will beshown on the credit side of the trading a/c and also in the assets side of thebalance sheet.

10. Mention some classification of assets and liabilities of balance sheet?Classification of assets and liabilities:Assets:1. Fixed Assets: It refers to those assets which held by way of equipment and notfor the purpose of resale. For e.g., Plant & machinery, buildings, furniture,fixtures and motor vehicles etc. The asset may be further sub-divided into (a)tangible assets and (b) intangible assets.(a) Tangible assets: It refers to those assets which can be seen, touched and hasvolume.(b) Intangible assets: These assets do not have physical existence. Goodwill,patents, trademarks and copyright are examples of intangible assets.

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/II Sem/UBA21/FIN. ACC/UNIT-III ANS/VER 2.0Unit – 3 Answer Page 7 of 8

2. Current assets: Current assets are those assets which are to be converted intocash within one year or during the normal operating cycle of the business. E.g.,Cash, bank, marketable securities, debtors, bills receivable and inventory.3. Liquid assets: Liquid assets are readily convertible into cash at short noticewith little or no risk of loss. E.g., Cash, Bank, Marketable securities, debtors andbills receivable.Liabilities:1. Proprietor’s Capital or Networth: Proprietor’s capital is the original fundwith which he entered a business Networth means the amount of capitaloutstanding on the particular date plus any profits retained in the business.2. Long-term liabilities: The liabilities which are repayable after a long period oftime are known as fixed liabilities. E.g., long-term loans and debentures.3. Current liabilities: It refers to those liabilities which are repayable within oneyear or during the normal operating cycle of the business. E.g., Trade creditors,bills payable, accrued expenses, bank overdraft, proposed dividend etc.

PART – C

1. Question and Answer in Hard copy. (Apr. 2012)2. Question and Answer in Hard copy. (Nov. /Dec. 2013)3. Question and Answer in Hard copy. (Apr. /May. 2013)4. Difference between Trial balance and Balance sheet?

S.No. Trial Balance Balance Sheet

1. A Trial Balance is prepared tocheck the arithmetical accuracyof the books of accounts.

A Balance Sheet is prepared toknow the financial position of thebusiness enterprise on a givendate.

2. A Trial Balance can be preparedfrequently. It may be prepared atthe end of a month or a quarter.

A Balance Sheet is generallyprepared at the end of theaccounting period.

3. The heading of the two columnsare “Debit Balances” and “CreditBalances”.

The headings of the two sides are“Liabilities” and “Assets”.

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/II Sem/UBA21/FIN. ACC/UNIT-III ANS/VER 2.0Unit – 3 Answer Page 8 of 8

4. All types of accounts find theirplace in the Trial Balance.

In a Balance Sheet, accounts ofassets, liabilities, capital and thoseaccounts which are remained openafter the preparation of Tradingand Profit and Loss account.

5. Generally, the opening stockappears in the Trial Balance,whereas the closing stock doesnot.

In a Balance Sheet, only theclosing stock appears on the assetsside.

6. In a Trial Balance, it is notpossible to have informationabout net profit or net loss.

In the Balance Sheet, informationabout net profit earned or net lossincurred is provided.

7. A Trial Balance can be preparedwithout making adjustmentsregarding prepaid expenses,income received in advance,accrued income, etc.

A Balance Sheet cannot beprepared without makingadjustments regarding prepaidexpenses, outstanding expenses,income received in advance oraccrued income, makingprovisions for possible losses, etc.

5. What is ‘Grouping and Marshalling’ of assets and liabilities? How is it done?A balance sheet is usually prepared in the form of statement, with assets on theright-hand side and liabilities and capital on the left-hand side. The componentitems of a balance sheet should be arranged in an orderly manner and in asequence that should be adhered to year by year. Such an arrangement of theitems in a balance sheet is known as ‘Marshalling’. There are two ways in whichthe assets and liabilities can be arranged in balance sheet. They are:(a) Order of permanence; (b) Order of liquidity.The first method commonly used by companies whereas the second one is popularamong sole traders and partnership firms. However, in case of certain concerns,such as banking companies, insurance companies, railway companies, other jointstock companies etc., form of balance sheet is prescribed by the law.

____________

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/II Sem/UBA21/FIN. ACC/UNIT-III QB/VER 1.0Unit – 3 Question Bank Page 1 of 8

UBA21 – FINANCIAL ACCOUNTINGUnit-IV – FINAL ACCOUNTSType: 20% Theory – 80% Problem

Question & Answer Bank

Syllabus: [Regulation: 2012]UNIT III: Preparation of trading, profit and loss account and balance sheet.

PART – A

1. What is profit and loss account? (Apr. /May 2013 May 2015 ,2016)Profit and Loss account is an account into which all gains and losses are

collected in order to ascertain the excess of gains over the losses or vice versa.Profit and loss account is prepared in order to calculate the net profit and net lossof the business.

2. “Balance Sheet”? (Nov. /Dec. 2013)According to R.N. Antony “Balance sheet is a screen picture of the

financial position of a going business at a certain moment”.

3. ‘Net Loss”? (Nov. /Dec. 2013)When total of all the expenses is more than gross profit and other income,

there remains a deficit and this is called net loss.

4. “Drawings”? (Nov. /Dec. 2013)Drawing means any amount withdraws from business for personal use.

Not only cash but if we withdraw any product from business or any asset ofbusiness for personal use that will be drawing. It surely reduces the capital of anybusiness. It is shown on the liability side of the balance sheet and it is reducedfrom the capital.

5. What do you understand by final accounts? (April 2012)The manner in which the amount of profit or loss has been arrived at is

disclosed in the statement of accounts, prepared at the end of the accountingperiod.

6. What is gross profit? (April 2012)

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/II Sem/UBA21/FIN. ACC/UNIT-III QB/VER 1.0Unit – 3 Question Bank Page 2 of 8

Gross profit is the difference between actual sale proceeds and the cost ofgoods sold. [Gross profit = Excess of sale proceeds over cost of goods sold].

7. What are Non-Operating expenses?These expenses are not related to the operation of the business and

include capital losses as loss on the sale of furniture etc., writing off fictitiousassets as preliminary expenses, underwriting commission etc., writing offintangible assets as goodwill, copyright, patents etc.

8. What are Operating expenses?It refers to those expenses which are incurred in order to operate the

business efficiently and smoothly. These include administration, selling,distribution, finance and maintenance expenses.

9. When do you prepare a ‘Manufacturing Account’?Those concerns which convert raw materials into finished goods and then

sell the finished goods are required to prepare manufacturing account. Thisaccount is prepared to calculate the cost of goods manufactured, which istransferred to the trading account.

10. Pass necessary adjusting entries in Mr. X’s journal on 31st December1988:

(i) Rs. 20,000 for wages was outstanding.(ii) Write off depreciation on machinery Rs. 50,000.(iii) Rs. 15,000 was received in advance as interest.

Ans:S.N. Particulars Debit Credit(i) Wages a/c Dr

To Outstanding Wages a/c(Being wages outstanding)

20,00020,000

(ii) Depreciation a/c DrTo Machinery a/c

(Being depreciation on machinery)

50,00050,000

(iii) Interest a/c DrTo Interest received in advance a/c

(Being interest received in advance)

15,00015,000

11. What is a final account?

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/II Sem/UBA21/FIN. ACC/UNIT-III QB/VER 1.0Unit – 3 Question Bank Page 3 of 8

In short, the businessman wants to know the profitability and the financialsoundness of the business. The final accounts are prepared at the end of the yearfrom the trial balance. These two statements i.e., trading and profit and lossaccount and balance sheet are prepared to give the final results of the business.

12. What do you understand by provision for bad and doubtful debts? (Apr./May. 2013)

As there is a possibility of anticipated losses and in order to provide for suchloss in the accounts, a provision for doubtful debts is required to be made.

13. What are the distinct stages in final accounts?There are three distinct stages in final accounts they are trading, profit and

loss account and balance sheet.

14. What is the result of each such stage in final accounts?Trading a/c – the expenses relating to factory is shown in this a/c.Profit & Loss a/c – to calculate the net profit or net loss of the business.Balance sheet – to measure the correct financial position of a business.

15. Are adjustments necessary for the preparation of final accounts? If yes,why?

Yes, there are certain necessary adjustments needed for the preparation offinal accounts, they are closing stock, outstanding expenses, prepaid expenses,accrued income, income received in advance, depreciation of assets, etc.,

16. What are the situations in which purchase account is credited?The purchase returns is a credit balance shown the return of goods to thesuppliers. It should be subtracted from the total purchases to get the net purchases.

17. What are all items added to and reduced from the capital of a sole traderin balance sheet?

In balance sheet, first add the net profit or subtract the net loss and addinterest on capital to the capital. Then subtract drawings and interest on drawingsto the capital.

18. What is the purpose of preparation of profit and loss account?Profit and loss account is prepared in order to calculate the net profit or net

loss of the business. Since the profit and loss account is prepared to show the netprofit earned or net loss incurred during a particular period.

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/II Sem/UBA21/FIN. ACC/UNIT-III QB/VER 1.0Unit – 3 Question Bank Page 4 of 8

19. What are fictitious assets?As the name implies such “assets” are not really assets. No amount can be

realised or further benefit derived from the expenditure concerned. These assetsare shown on the assets side of the balance sheet till they are fully written off.

20. What are contingent assets?Contingent asset is one, the existence of which depends upon the happening

of a certain event which may or may not take place. For example: claim forincome tax refund, uncalled share capital of a public limited company, claim bythe firm for infringement of trademarks or patent copy right etc.

21. What are contingent liabilities?Contingent liability will become an actual liability only on the happening of

a certain event which may or may not happen. For example bills discounted andendorsed which may be dishonoured, claim by others, unpaid call amount oninvestments.

22. What are outstanding expenses? (2015 May 2015) (Nov/ Dec 2016)These are certain expenses which relate to a particular accounting period but

they are not paid in that accounting period due to certain reasons. It is added tothe respective account in the trading or profit and loss a/c and also shown on theliabilities side of the balance sheet.

23. What are prepaid expenses?Prepaid expenses are those expenses which have been paid in advance but

relating to the future accounting period. These are also called the unexpiredexpenses. It is deducted from the respective account of trading and profit & lossa/c and also shown on the asset side of the balance sheet.

24. What is accrued income?Outstanding or accrued income is the income which has been earned but not

received during the accounting period. It is shown on the asset side of balancesheet and it is added to the respective income account in P & L a/c credit side.

25. What is income received in advance?Without rendering any service the trader receive income. Such an income is

known as income received in advance, i.e, the income received but not earnedduring the accounting period. It is shown as deduction from the respective incomein P & L a/c and is shown on the liabilities side of balance sheet.

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/II Sem/UBA21/FIN. ACC/UNIT-III QB/VER 1.0Unit – 3 Question Bank Page 5 of 8

PART – B

1. Question and Answer in Hard copy (Nov. /Dec. 2013)2. Question and Answer in Hard copy (Apr. /May 2013)3. Question and Answer in Hard copy (Apr. /May 2013)4. What are the items appearing on debit side of profit & loss a/c?

The business expenses are divided into two types. Direct expenses which arerecorded in the trading a/c and indirect expenses which are recorded in the debitside of profit & loss a/c. Indirect expenses can be further divided into twovarieties:(i) Operating expenses and (ii) Non-operating expenses(i) Operating expenses: It refers to those expenses which are incurred in order tooperate the business efficiently and smoothly. These include administration,selling, distribution, finance and maintenance expenses.(ii) Non-operating expenses: These expenses are not related to the operation ofthe business and include capital losses as loss on the sale of furniture etc., writingoff fictitious assets as preliminary expenses, underwriting commission etc.,writing of intangible assets as goodwill, copyright, patents etc.

5. Question and Answer in Hard copy.6. Question and Answer in Hard copy. (Apr. /May 2014)7. How do you treat accrued incomes and incomes received in advance when

they are given in trial balance and in adjustments?Accrued income: Accrued income is shown on the asset side of balance sheetand it is added to the respective income account in P & L a/c credit side. Noadjustment is required in the P & L a/c if accrued income a/c appears in the trialbalance, but such an account must be shown as an asset in balance sheet.Income received in advance: Income received in advance is shown as deductionfrom the respective income in P & L a/c and is shown on the liabilities side of thebalance sheet. No treatment is required in the P & L a/c if income received inadvance account appears in the trial balance. But such account must be shown asa liability in the balance sheet.

8. How do you treat stock when it is given in trial balance and in adjustments?The stock on hand at the beginning of the year is called opening stock. This itemis usually shown as the first item on the debit side of the trading account. Thefigure is available from the trial balance. It may include raw materials, work-in-progress and finished goods.Closing stock refers to the unsold goods which is lying in the godown at the endof the accounting year. Generally, the closing stock does not appear in the trial

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/II Sem/UBA21/FIN. ACC/UNIT-III QB/VER 1.0Unit – 3 Question Bank Page 6 of 8

balance. It appears outside the trial balance. The value of closing stock willappear on the assets side of balance sheet and on the credit side of tradingaccount. In trial balance opening stock is shown on the debit side.

9. What are the items appearing on the debit and credit side of trading a/c?Item appearing on the debit side of trading a/c:1. Opening stock: Stock on hand at the beginning of the year is called openingstock.2. Purchases: It shows the gross amount of purchases made of the materials andsaleable goods.3. Purchase returns or Returns outwards: The purchase returns is a creditbalance showing the return of goods to the suppliers. It should be subtracted fromthe total purchases.4. Direct expenses: It refers to those expenses which are incurred for making thegoods saleable. Factory rent, wages, octroi, freight on purchases, manufacturingexpenses, import duty, carriage inward, customs duty, dock dues, clearing chargesetc.Item appearing on the credit side of trading a/c:1. Sales: It is a credit balance indicating the total sales of goods made during theyear. It includes both cash and credit sale of goods.2. Sales return: This is a debit balance, showing the total amount of goodsreturned by the customers. It should be subtracted from the total sales.3. Closing stock: It refers to the unsold goods, which is lying in the godown atthe end of the accounting year. If it is given outside the trial balance, it will beshown on the credit side of the trading a/c and also in the assets side of thebalance sheet.

10. Mention some classification of assets and liabilities of balance sheet?Classification of assets and liabilities:Assets:1. Fixed Assets: It refers to those assets which held by way of equipment and notfor the purpose of resale. For e.g., Plant & machinery, buildings, furniture,fixtures and motor vehicles etc. The asset may be further sub-divided into (a)tangible assets and (b) intangible assets.(a) Tangible assets: It refers to those assets which can be seen, touched and hasvolume.(b) Intangible assets: These assets do not have physical existence. Goodwill,patents, trademarks and copyright are examples of intangible assets.

ACADEMIC YEAR: 2016 – 2017 REGULATION CBCS - 2012

RAAK/B.B.A/V.ARUNAGIRI/II Sem/UBA21/FIN. ACC/UNIT-III QB/VER 1.0Unit – 3 Question Bank Page 7 of 8