sbh project

TRANSCRIPT

CHAPTER 3

STATE BANK OF HYDERABAD

COMPANY PROFILE

STATE BANK OF HYDERABAD

CHAPTER

STUDY ON COMPARATIVE STATEMENT

COMPANY PROFILE

STATE BANK OF HYDERABAD PROFILE

State Bank of Hyderabad was constituted as Hyderabad State Bank on

08.08.1941 under Hyderabad State Bank Act, 1941. The Bank started with

the unique distinction of being the central bank of the erstwhile State of

Hyderabad, covering present-day Telangana region of Andhra Pradesh,

Hyderabad – Karnataka of Karnataka state and Marathwada of

Maharashtra state, to manage its currency – Osmania Sikka and public

debt apart from the functions of commercial banking. The first branch of

the bank was opened at Gunfoundry, Hyderabad on 5th April, 1942.

In 1953, the Bank took over the assets and liabilities of the Hyderabad

Mercantile Bank Ltd. In the same year, the Bank started conducting

Government and Treasury business as agent of Reserve Bank of India. In

1956, the Bank was taken over by Reserve Bank of India as its first

INSTITUTE OF MANAGEMENT STUDIES Page 2

COMPANY PROFILE

STUDY ON COMPARATIVE STATEMENT

subsidiary and its name was changed from Hyderabad State Bank to State

Bank of Hyderabad. The Bank became a subsidiary of State Bank of India

on the 1st October 1959 and is now the largest Associate Bank of State

Bank of India.

All the branches of the Bank are totally networked under Core Banking

Solutions,offering a vide range of products to it’s customers. All the

customers of the Bank have access to the latest technologies like Internet

Banking, ATMs etc. The Bank has pan India presence and operates

through more than 1000 Bank branches

About State Bank of Hyderabad / Board of Directors

Shri O. P. BhattChairman

Ex-officio under Section 25(1)(a) of theState Bank of India (Subsidiary Banks) Act,1959

Smt Renu ChalluManaging Director

INSTITUTE OF MANAGEMENT STUDIES Page 3

STUDY ON COMPARATIVE STATEMENT

Shri Kaza SudhakarDirector

Nominated by the Reserve Bank of India

Photo no availableShri R Sridharan

DirectorNominated by the State Bank

of India

Shri B Ramesh BabuDirector

Nominated by the State Bank of India

Shri B S Gopala Krishna Director

Nominated by the State Bank of India

Shri Ramesh DatlaDirector

Nominated by the State Bank of India

Shri V. MuraliDirector

Nominated by the State Bank of India

INSTITUTE OF MANAGEMENT STUDIES Page 4

STUDY ON COMPARATIVE STATEMENT

Shri Gopal Vaidya Director

Nominated by the Govt. of India

Shri P. Narasimha Director

Nominated by the Govt. of India

DirectorNominated by the State

Bank of India

Prof. V. Venkata RamanaDirector

Nominated by the State Bank of India

Shri S Gopal KrishnaDirector

Nominated by the Govt. of India

Organizational Set-up:

INSTITUTE OF MANAGEMENT STUDIES Page 5

STUDY ON COMPARATIVE STATEMENT

INSTITUTE OF MANAGEMENT STUDIES Page 6

Managing Director

MD’s Sectt

C.G.M

CGM’s Sectt

GM (C&IB)

GM

(Ops)

G.M

(PB,Tech&Fin )

GM(MSME,Treasury

GM (AGRI &CRO)

GM &

CVO

STUDY ON COMPARATIVE STATEMENT

SERVICES PROVIDED BY STATE BANK OF

HYDERABAD

Services

Demat/

Depository

Services

Electronic Fund

Transfer System

Safe Deposit

Lockers

ATM Services Internet

Banking

RISET

Information and

Formats

ATM Locations Service Charges Customer

Service

Download

service_charges.

doc

RTGS , NEFT

& GRPT

Frequently

Asked Questions

(FAQ)

Mobile Banking Cash

Management

Products -

Divident

Warrants

NEFT - Contact

Details of

Customer

Facilitation

Centres

New Pension

System

Cheque

Collection Policy

Settlement of

claims in respect

of Deceased

Depositors

INSTITUTE OF MANAGEMENT STUDIES Page 7

STUDY ON COMPARATIVE STATEMENT

Demat/depository services:

We have launched depository participant services with National Securities

Depository Ltd., (NSDL). You can now hold your securities as electronic

book entries and transfer securities without actually handling physical

scripts. Hand in your share certificates with a Demat Request form. When

you want to sell or purchase securities, you only need to give

delivery/instructions to effect a settlement.

Why should I hold securities in dematerialized form?

Because, in the demat form, you do not run the risk of theft, loss,

misplacement, bad deliveries, or damage to scripts. No stamp duties on

transfers of securities.

No bad deliveries

The settlement cycle is faster. You do not lose out on market opportunities

as the securities are available in your account immediately after pay

out(T+2 settlement). There are no cumbersome transfer deeds to be signed

and bonus and rights shares are credited by issuers directly into your

demat account, cash components to your SB/CA accounts maintained at

your branch directly through ECS, eliminating delays.

When you purchase new issues of securities in the primary market, they

are directly credited to your account on allotment. You enjoy preferential

treatment to obtain loans against demat shares. SBH is registered with

NSDL as a Depository Participant, which permits us to perform the

following activities:

Our Depository Participant ID NO. IN 301397 situated at Gunfoundry,

Hyderabad.

INSTITUTE OF MANAGEMENT STUDIES Page 8

STUDY ON COMPARATIVE STATEMENT

• Demat and Remat of securities such as equities, shares and debentures

• Market transfer purchases and sales

• Off-Market transfer purchase and sales

• Noting pledges SCHEDULE OF CHARGES for individuals and

corporate houses

Agreement Charges/Stamp Duty

Rs.100/-

Account Opening None

Account Closing None

Annual Maintenance Charges

Rs.200/- p.a.

Dematerialisation Rs.100/- p.a. for SBH staff and pensioners

Rematerialisation Rs.2/- per certificate Minimum Rs.10/- + Courier charges Rs.25/- per request

Transaction Fee Rs.25/- per certificate or 0.20% of the market value, whichever is higher

Market Purchase Credit

0.04% of value, minimum of Rs.20/- for retail customer Rs.40/- for others per tradeFor CP- Nil

INSTITUTE OF MANAGEMENT STUDIES Page 9

STUDY ON COMPARATIVE STATEMENT

Market Sale 0.04% of value, minimum Rs.20/- for retail customer Rs.40/- for others per trade0.02% of face value for CP, maximum of Rs.500/- per trade

Off-Market Purchase 0.04% of value, minimum of Rs.20/- for retail customers Rs.40/- for others per trade

Off-Market Sale 0.04% of value, minimum of Rs.20/- for retail customers Rs.40/- for others per trade

Inter Depository Transactions

Rs.20/- per transaction

Pledge: Creation /Confirmation / Closure

Rs.100/- per request and Rs.100/- per request or invocation

Custody Charges Equity

None for retail customers0.02%, minimum of Rs.25/- per quarter for companies that have paid one time chargesFor CP- Nil

Custody Charges Government Securities

0.15% of the value of the holdings as on the last Friday of the month

INSTITUTE OF MANAGEMENT STUDIES Page 10

STUDY ON COMPARATIVE STATEMENT

Electronic fund transfer

RBI’s Electronic Funds Transfer (EFT) system facilitates inter-bank and

intra-bank fund transfers among our 15 notified centers. EFT transfers are

soon coming to replace demand drafts because they are faster, less

expensive, and more secure. SBH levies nominal service charges for such

transfers. The funds are transferred to the beneficiary’s account either on

the same day or on the next working day.

You can transfer a maximum of Rs.2 crore in a single transaction. To

make an EFT transfer, you need to fill up and submit an EFT request form.

You can submit the form either online or at the branch where you hold an

account. Provide the following information in the EFT form:

• The name of the beneficiary

• The name of your bank and branch name

• Your account number

• The amount to be remitted

SBH offers the EFT service at the following centers: Mumbai, Chennai,

Kolkata, New Delhi, Ahmedabad, Bangalore, Bhubaneshwar, Chandigarh,

Guwahati, Hyderabad, Jaipur, Kanpur, Nagpur, Patna, and

Thiruvananthapuram.

SAFE CUSTODY LOCKERS

For the safety of your valuables we offer our customers safe deposit vaults

or locker facilities at nominal annual charges depending on the size of the

locker and the branch. Please avail nomination facility. Rentals in rupees

p.a.

INSTITUTE OF MANAGEMENT STUDIES Page 11

STUDY ON COMPARATIVE STATEMENT

ATM SERVICES:

SBH’s ATM Debit card services offer customers easy access to money

anytime from anywhere.

The card is safe and secure and eliminates the need to carry large amounts

of cash. It saves you time and the inconvenience of going to the bank for

cash withdrawals.

You can withdraw from Savings and Current accounts, including overdraft

accounts. You can view the current balance and also a mini statement of

the last five transactions on your account. You are provided a Personal

Identification Number (PIN) when you receive the card. You can change

the PIN later.

ATM cum Debit Cards issued by the Bank can be used at more than 12500

ATMs of Andhra Bank, Bank of India, Corporation Bank, Dena Bank,

HDFC Bank, Indian Bank, IndusInd Bank, Punjab National Bank, UCO

Bank, Union Bank of India , UTI Bank, Canara Bank and Bank of

Rajasthan which are members of bilateral sharing arrangement.

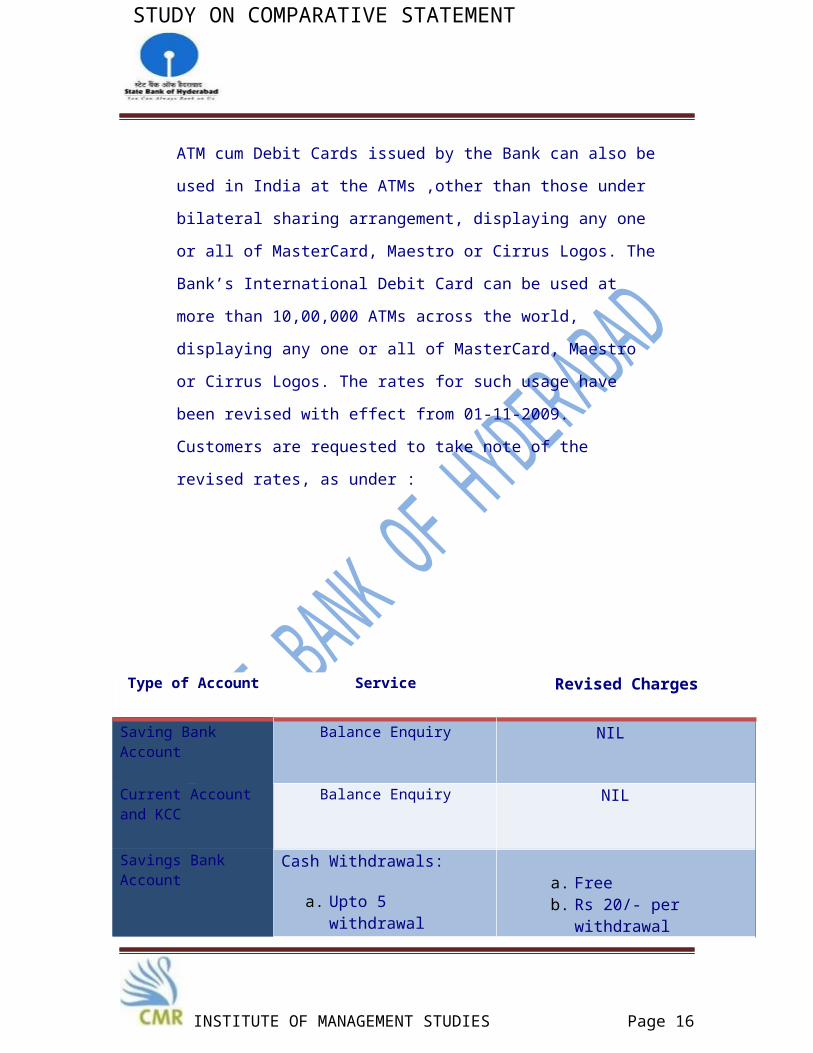

ATM cum Debit Cards issued by the Bank can also be used in India at the

ATMs ,other than those under bilateral sharing arrangement, displaying

any one or all of MasterCard, Maestro or Cirrus Logos. The Bank’s

International Debit Card can be used at more than 10,00,000 ATMs across

the world, displaying any one or all of MasterCard, Maestro or Cirrus

Logos. The rates for such usage have been revised with effect from 01-11-

2009. Customers are requested to take note of the revised rates, as under :

INSTITUTE OF MANAGEMENT STUDIES Page 12

STUDY ON COMPARATIVE STATEMENT

Type of Account Service Revised Charges

Saving Bank Account Balance Enquiry NIL

Current Account and KCC

Balance Enquiry NIL

Savings Bank Account Cash Withdrawals:

a. Upto 5 withdrawal transactions at other Bank ATMs in a month

b. Above 5 withdrawal transactions

a. Freeb. Rs 20/- per

withdrawal transaction

Current Account and KCC

Cash Withdrawals Rs 20/- per withdrawal transaction. (i.e. No free withdrawal transaction permitted)

INTERNET BANKING:

SBH’s Internet banking facility is an online banking facility that can be

accessed from the website. You need to register yourself at the branch

where you hold an account. You will be provided with a customer

identification numbe and an initial password.

You can:

• Browse various types of accounts, such as Savings Bank account and

Current account

• Download account statement

• Communicate with SBH through eMail

• Order new cheque books through eMail

INSTITUTE OF MANAGEMENT STUDIES Page 13

STUDY ON COMPARATIVE STATEMENT

CUSTOMER SERVICES

In terms of Reserve Bank of India directions, an ad-hoc committee on

procedures and performance audit on customer service in banks has been

constituted in our bank, with AGM (DB) as the nodal officer and Senior

Manager level officials as members. The committee would look into

simplification of procedures and practices with a view to safeguarding the

interests of common persons and to improve the customer service in the

areas of foreign exchange transactions, government and public debt

transactions, banking operations and currency management. The

committee would also recommend for modification/rationalization of

existing RBI guidelines that could help in further enhancing the customer

service.

MOBILE BANKING :

SB FreedoM – Your Mobile Your Bank Away from home, bills can be paid or money sent to the loved ones or balance enquiries done anytime 24x7 !!!That is what SBI FreedoM offers -convenience, simple, secure, anytime and anywhere banking.

The service is presently available on java enabled mobile phones over SMS/ GPRS/ WAP as also non java phones with GPRS connection. The service can be availed over the free GPRS facilities offered by various mobile service providers. The services for other non-Java mobile phones are under development and will be offered using Unstructured Supplementary Services Data (USSD).

The following functionalities will be provided in the Phase I :

-Funds transfer (within and outside the bank –using NEFT) -Enquiry services (Balance enquiry/ Mini statement) -Request services (cheque book request)

INSTITUTE OF MANAGEMENT STUDIES Page 14

STUDY ON COMPARATIVE STATEMENT

-Bill Payment (Utility bills, credit cards) -M Commerce (Mobile Top Up, Merchant payment, SBI life insurance

premium)

Business Rules Governing Mobile Banking Services:

The Mobile Banking Service will be available to all the customers having a satisfactory running account (Current/ Savings). The customers will have to register for the services.

Daily transaction limit of Rs.50,000/- for both fund transfer and bill/ merchant payment individually however combined limit for both funds transfer and bill/ merchant payment cannot exceed Rs.50,000/- per customer with an overall calendar month limit of Rs.2,50,000.00

The service will be carrier-agnostic i.e. all customers can avail the mobile banking service with the Bank irrespective of the service provider for their mobiles.

The service is free of charge. However, the cost of SMS / GPRS connectivity will have to be borne by the customer.

INSTITUTE OF MANAGEMENT STUDIES Page 15

STUDY ON COMPARATIVE STATEMENT

CASH MANAGEMENT PRODUCTS:

Features Cash Management Product (CMP)

Eligibility All Companies who wish to pay Dividends to their investors

Scheme details 1. The company enters into an MOU with the Bank, specifying details of terms and conditions

2. It opens Current Account "Dividend Warrant A/c" 3. Deposits total amount of dividend payable into this A/c 4. Co. gives a list of DW containing all details like DW No., amount,

beneficiary name and a/c no. , date of payment of Warrants etc 5. The paying branches pay the DW on presentation through

respective menu option

Benefits of the Scheme

1. DW payable at par at all branches 2. Built in security features, as the system validates DW No. &

amount at the time of payment 3. Manual intervention for reconciliation of account is not required 4. Company can access details of paid Warrants through statement of

account / Corporate Internet Banking facility

INSTITUTE OF MANAGEMENT STUDIES Page 16

STUDY ON COMPARATIVE STATEMENT

GENERAL RISKS

For taking an investment decision the investor must rely on their

examination of the Offeror and the Offer including the risks involved. The

securities have not been recommended or approved by Securities and

Exchange Board of India (SEBI) nor does SEBI guarantee the accuracy or

adequacy of this document .

OFFEROR’S ABSOLUTE RESPONSIBILITY

The Offeror, having made all reasonable inquiries, accepts responsibility

for, and confirms that this Information Memorandum contains all

information with regard to the Offeror and the Offer, which is material in

the context of the Offer, that the information contained in this Information

Memorandum is true and correct in all material aspects and is not

misleading in any material respect, that the opinions and intentions

expressed herein are honestly held and that there are no other facts, the

omission of which makes this document as a whole or any of such

information or the expression of any such opinions or intentions

misleading in any material respect. The Arranger is not required to file this

document with SEBI/ROC as it is on private placement and not an Offer to

the general Public.

CREDIT RATING

CRISIL Ltd. has assigned a ‘AAA/stable’ (pronounced Triple A with

stable outlook) rating

INSTITUTE OF MANAGEMENT STUDIES Page 17

STUDY ON COMPARATIVE STATEMENT

to the captioned debt programme of the Bank. This rating indicates the

highest degree of

safety with regard to timely payment of interest and principal on the

instrument. The rate instrument carries the lowest credit risk.

CARE has assigned a ‘CARE AAA’ (pronounced Triple A) rating to the

captioned debt programme of the Bank. This is the best credit quality

rating assigned by CARE.

Instruments with this rating are considered to be of the best credit quality,

offering highest safety for timely servicing of debt obligations. Such

instruments carry minimal credit risk.

The rating is not a recommendation to buy, sell or hold Securities and

investors should take their own decision. The rating may be subject to

revision or withdrawal at any time by the assigning rating agency and each

rating should be evaluated independently of any other rating. The rating

obtained is subject to revision at any point of time in the uture. The rating

agencies have a right to suspend, withdraw the rating at any time on

the basis of new information, etc.

TRUSTEES FOR THE BOND HOLDERS:

IDBI Trusteeship Services Ltd., have given their consent to the Bank vide

their letter No

2846/ITSL/OPR/CL-2009-10 Dated 28.08.2009, for being appointed as

Bond Trustee for the present private placement.

INSTITUTE OF MANAGEMENT STUDIES Page 18

STUDY ON COMPARATIVE STATEMENT

Lead Arranger tothe PrivatePlacement

Co-Arranger to thePrivate Placement

Co-Arranger tothe PrivatePlacement

REGISTRARS TOTHE ISSUE

Trustee ForTheBondholders

Darashaw & Co. PvtLtd.1205-06Regent Chambers,208 Nariman Point,Mumbai 400 021Tel no:022 6630 6612Fax no:022 2204 0031/40

Standard CharteredBank90, M.G.Road,Mumbai – 400 001.Tel : 022 22617151Fax : 022 22651255

KARVY ComputerShare Private Ltd17-24, Vittal RaoNagar, Madhapur,Hyderabad -500 081Andhra PradeshTel: 040 23420815-28Fax 23420814

IDBITrusteeshipServices Ltd.RegisteredOfficeAsian Building,Ground Floor17, R KamaniMarg, BallardEstateMumbai – 400001Tel: (022)66311771-3Fax: 91-22-66311776E-mail:[email protected]

Brief summary of the business/ activities of the issuer and its line ofbusinessHIGHLIGHTS OF THE BANK

1. Bank with more than 67 years of existence.2. Member of the State Bank Group, the largest banking Group in India.The Group has the biggest network of branches and the highest marketshare of deposits and advances in the country.3. Professionally managed Bank with an uninterrupted record ofprofitability since inception.4. Large Network of 1034 branches and 28 extension counters as on June,30 2009.

INSTITUTE OF MANAGEMENT STUDIES Page 19

STUDY ON COMPARATIVE STATEMENT

5. Low net NPA ratio of 0.64% as on 30th June 2009.6. Capital Adequacy Ratio of the Bank stood at 12.54% as on June 30, 2009Under Basel-I and 13.96% under Basel-II, which is well above thestipulated minimum of 9% prescribed by the Reserve Bank of India.7. Return on Average Assets stood at 0.59% and Return on Average NetLoan Policy:

State Bank of Hyderabad’s Loan Policy (hereinafter referred to as “The LoanPolicy” or “The Policy”) is aimed at accomplishing its mission of all-roundgrowth with maximum profits, achievement of pre-eminence in banking withcommitment to excellence, in rendering customer, shareholder andemployee satisfaction, while continuing to emphasis on its developmentbanking role to be fulfilled through a skilled and committed workforce andtechnological up gradation.The Loan Policy of the Bank has successfully withstood the test of time andwith inbuilt flexibilities, has been able to meet the challenges in the marketplace. The policy is well documented and implemented through circularinstructions and periodic guidelines. The procedural aspects are highlightedin the Bank’s Book of Instructions. The policy, at the holistic level is anembodiment of the Bank’s approach to sanctioning, managing andmonitoring credit risk and aims at making the systems and controls effective.

The basic tenets of State Bank of Hyderabad’s Loan Policy are as follows:

(i)The policy establishes a commonality of approach regarding credit basics,appraisal skills, documentation standards and awareness of institutionalconcerns and strategies, while leaving enough room for flexibility andinnovation.

(ii) Exposure levels are set out in the policy in order to ensure growth of assetsin an orderly manner.

(iii) The policy sets out minimum scores/hurdle rates (in terms of Credit RiskAssessment parameters) for new/additional exposures.

(iv) Bank’s general approach to Export Credit and Priority Sector Advances isset out in the policy.

(v) The policy lays down norms for take over of advances from otherbanks/FIs.

(vi) Bank’s stand on granting credit facilities to companies whose directorsare in the defaulter’s list of RBI is covered in the policy.(vii) The policy aims at continued growth of assets while endeavoring toensure that these remain performing and standard. To this end, as a matter

INSTITUTE OF MANAGEMENT STUDIES Page 20

STUDY ON COMPARATIVE STATEMENT

of policy the Bank does not take over Non-Performing Assets (NPA) fromother banks.

The Board of Director the Bank is the apex authority in formulating all mattersof policy in the bank. The Credit Risk Management Committee (CRMC) dealswith issues relating to credit policy and procedures on a Bank-wide basis. TheCRMC sets broad policies for managing credit risks, sets parameters forgrowth of credit portfolio within the boundaries of exposure limits, andreviews credit appraisal systems.

ASSET CLASSIFICATION, INCOME RECOGNITION & PROVISIONING:

ASSET CLASSIFICATION:

The Bank classifies its assets in compliance with RBI guidelines. Under theseguidelines, an asset is classified as non-performing if any amount of interest /principal remains overdue for more than 90 days in respect of term loans. Inrespect of overdraft / cash credit, an asset is classified as non-performing ifthe account remains out of order for a period of more than 90 days and inrespect of bills, if they remain overdue for more than 90 days. In case of retailassets, the Bank classifies an asset as non-performing where any amount ofinterest / principal remains overdue for more than 90 days in respect of allloans.NPAs are further categorized into three groups i.e. Substandard, Doubtfuland Loss Asset depending upon the period of delinquency and availability oftangible security. The table below gives the criteria for asset classification viz.Standard, Substandard, Doubtful and Loss asset-

INSTITUTE OF MANAGEMENT STUDIES Page 21

STUDY ON COMPARATIVE STATEMENT

Category Classification1. Performing

Standard Assets An asset which has not posed any problem and whichdoes not carry more than the normal business risk.

2. Non-Performing

a)Sub-standardAssets

An asset which has been non-performing for a periodless than or equal to twelve months

b)Doubtful Assets An asset which has been non-performsing for a periodof over 12 months

c)Loss Assets Asset where loss has been identified by the Bank orauditors / RBI and any non-performing asset where thevalue of security is less than 10% of the dues to the bank.

INSTITUTE OF MANAGEMENT STUDIES Page 22