sbn holdings limited annual report 2016 - standard bank us... · 2018-09-27 · namibia. our...

TRANSCRIPT

SBN Holdings Limited Annual report

2016

1915–2016

Celebrating 101 years of moving Namibia forward

Our success and growth over the long term is built on making a difference in the communities in which we operate. We are commercially and morally bound to serve Namibia and her people, in return for the long-term profitable growth we envisage as the leading financial services group on the continent. We are committed to moving Namibia forward.

Standard Bank’s first branch opened in 1915 in Lüderitz. Standard Bank is one of Namibia’s oldest companies. The bank’s original vision was to understand its customers better, have people with strong knowledge of local business conditions and to do a better job of connecting borrowers with lenders. This vision created the platform for the kind of bank it would become and the qualities on which its customers and clients would come to rely.

Over its history, Standard Bank has grown from a mere few staff members to over 1 700 today, and extended its roots deep into the fabric of Namibian society. We have evolved and adapted along with our customers and clients, growing a rich heritage while nurturing and protecting our reputation. We uphold high standards of corporate governance and are committed to advancing the principles and practices of sustainable development. We are inspired to advance national development objectives.

Standard Bank currently has a strong presence in Namibia. These points constitute:

Branches

58ATMs

266Standard Bank has always lived up to the promise of bringing banking to the nation and we have succeeded in doing so by having a wide ATM network of ATMs in Namibia.

1915 1919 1920 1927 1928 1929 1935 1950

LüderitzSwakopmund

Windhoek

GrootfonteinOkahandjaOmaruru

Otjiwarongo

TsumebWalvis Bay

KeetmanshoopOutjo

Mariental Gobabis Otavi Bethanie

1954 1956 1974 1978 1979 1980 1983 1994

Aranos Maltahohe Ausspannplatz Oshakati Khorixas Katutura Gustav Voigts Centre

Henties Bay

1996 1997 1998 1999 2002 2003 2007 2008

GameWernhill Service

Centre

Arandis OndangwaNorthern

Industrial Area Oshakati South

Oshikango RehobothRosh Pinah

RunduAussenkehr

Omuthiya

EenhanaKatima MuliloMaerua Mall

Kuisebmund

2009 2010 2011 2012 2013 2014 2015 2016

Klein Windhoek Okalongo

Okahao Nkurenkuru Otjinene

OpuwoWalvis Bay

OngwediwaOutapi

(ombalantu)

Khomasdal Oshana

The GroveMondesa

Okahandja

OkuryangavaOkongo Agency

RuacanaSwakopmund

(Waterfront)

SBN Holdings Limited Annual report 2016 1

About Standard Bank Namibia 2Our integrated pillars of operation 3

Our value creation story 4

What we do 6

Group strategy 8

Strategic objectives 9 In, for and across Africa 10

Measuring our strategic progress 12

Our material issues 14

Responding to our stakeholders 16

Our socioeconomic impact 18

Chairman’s report 20Chief executive’s review 24Financial review 28Corporate governance report 32Board of directors 40

Executive committee 42

Annual financial statements 44Directors’ responsibilities and approval 46

Independent auditors’ report 47

Directors’ report 49

Statements of financial position 50

Statements of profit or loss 51

Statements of other comprehensive income 52

Statements of changes in equity 54

Statements of cash flows 55

Accounting policy elections 56

Key management assumptions 57

Notes to the annual financial statements 59

Annexure A – Subsidiaries 98

Annexure B – Joint ventures 99

Annexure C – Risk and capital management 100

Annexure D – Emoluments of directors 136

Annexure E – Detailed group accounting policies 137

OversightThe board audit subcommittee is responsible for providing oversight of the financial reporting process. The committee recommended the report for approval to the SBN Holdings board of directors, which was obtained on 23 March 2017.

FeedbackWe welcome the views of our stakeholders on this report. Please contact Sigrid Tjijorokisa: Group company secretary at [email protected] with your feedback.

Reporting suiteTo meet the information needs of our diverse stakeholders, we produce the following reports:

The Annual Report (this report)Our primary report to stakeholders which provides an assessment of our ability to create value over time.

The Corporate Social Investment ReportSets out our corporate social investment initiatives for 2016.

AIRThe Sustainability ReportThis report covers our operations and covers the material focus areas in relation to our strategy.

SDCSI

www.standardbank.com.na/namibia/about-us/company-overview/Annual-reports

Contents

Standard Bank Corporate social

investment report 2016

SBN Holdings Limited Annual report

2016

2

ABOUT STANDARD BANK NAMIBIA

About Standard Bank Namibia

Our listings and shareholdersHeadquartered in Windhoek, SBN Holdings is 90% owned by

Standard Bank Group and 10% owned by Purros Investments Trust, our staff empowerment scheme.

Over the years, our customers and clients have come to rely on us to understand their needs, employ people with strong knowledge of local business conditions and connect borrowers with lenders. We are proud to be part of Standard Bank Group, a large financial services organisation rooted in Africa and with operations in 22 countries.

From humble beginnings of three branches, today, Standard Bank Namibia operates a distribution network of 58 branches and 266 ATMs across Namibia. Our workforce has grown to over 1 700 employees and our roots have extended deep into the fabric of Namibian society.

Standard Bank is committed to making banking available to all Namibians.

Standard Bank opened its first commercial branch in August 1915 in Lüderitz, making it one of Namibia’s oldest companies today.

Our company structure

90%

10%

100%

Stanfin (Namibia)

Standard Insurance Brokers (Namibia)

Purros Investments Trust

Standard Bank Group

SBN Holdings

100% Standard Bank Namibia Nominees

Standard Bank Namibia

NAMIBIA IS OUR HOME

– we drive her growth

To this end we have evolved and adapted together with our customers and clients, developing a rich heritage while nurturing and protecting our reputation. We uphold high standards of corporate governance, are committed to advancing the principles and practices of sustainable development and are inspired to advance national development objectives.

Our success and growth over the long term is built on making a difference in the communities in which we operate. We are commercially and morally bound to serve Namibia and her people, in return for the long-term profitable growth we envisage as a leading financial services group on the continent.

SBN Holdings Limited Annual report 2016 3

Our integrated pillars of operation

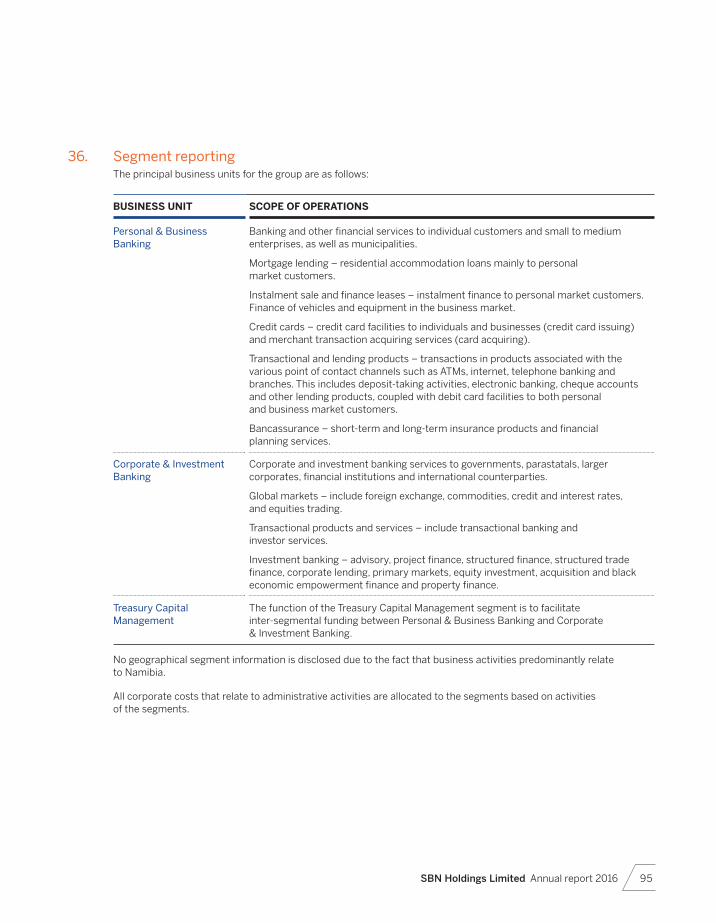

Our third business area includes the results of centralised support functions (back office), including those functions that were previously embedded in the business segments. The direct costs of support functions are recharged to the business segments.

Mortgage lending Instalment sale and finance

leases Card products Transactional products Lending products Bancassurance

PBB provides banking and other financial services to individual customers and to small- to medium-sized enterprises.

CIB offers corporate and investment banking services to its clients, which include governments, parastatals, larger corporates, financial institutions and international counterparties.

Global markets Transactional products and

services Investment banking

Personal & Business Banking (PBB)

Corporate & Investment Banking (CIB) Other

OUR OFFERING

CONTRIBUTIONS TO SBN HOLDINGS PAT

PROFIT AFTER TAX (PAT) PROFIT AFTER TAX (PAT)

N$310 million2015: N$356 million

N$218 million2015: N$171 million

N$11 million2015: N$2 million (loss)

57% 41% 2%

4

Our value creation story

Governance approach to value creation over time

Our governance approach promotes strategic decision making that combines long-term and shorter-term outcomes, to reconcile the interests of the group and society in our pursuit of sustainable value.

Our material issues synthesise the interests of the group and those of its stakeholders. They are linked to our value drivers, direct the focus of our strategic planning and management priorities, and inform our reporting to stakeholders.

Managing economic headwinds

Acting on our material issues

Group strategy

Bus

iness

units and corporate functions

Risk appetiteOperating contextOur group strategy is focused on

creating shared value, and represents our commitment to the shared future we intend to create for our clients, our people and our other stakeholders.

Our clients are at the centre of everything we do. This is the central organising principle in the work we are doing to build a digital bank, redesign our operating models, and to develop our people and change our culture – which together will create long-term sustainable competitive advantage.

Our business units and corporate functions have aligned their operating strategies to the group strategy, to ensure effective and coordinated execution within and across our operations for the benefit of our clients.

Our strategy is achieved within the parameters of our risk appetite, which implies conscious risk taking. To enable regular changes to our risk appetite in response to challenges in our operating context, we are instilling a risk-aware culture throughout the group and continually enhancing our risk management capabilities.

Our strategy represents an effective approach to the structural shifts in our industry. Global megatrends such as the technological revolution, increasing stakeholder pressure, and socioeconomic and environmental challenges are imposing the need for wide-reaching transformation in the way we do business.

We remain flexible in our strategic responses to the cyclical pressures in our markets. We identify pockets of opportunity for revenue generation, and employ well-developed risk models to anticipate and manage the impact of risks that are heightened during times of economic stress.

Our clients

Responding to our stakeholders

Our stakeholders are the providers of the capital we need to create value. Stakeholder inclusivity and responsiveness enables us to secure and maintain these inputs, and to identify opportunities and challenges.

Clients

Performance linked to value creationWe are embedding a high-performance culture and creating an environment in which our people are empowered and motivated to deliver exceptional client experiences, and are rewarded for their contribution towards realising our purpose and vision.

Remuneration that drives value over timeOur reward philosophy is being evolved to reflect the group strategy. We combine reward elements that link directly to strategic and financial performance criteria and thresholds. These awards are made on a discretionary basis to avoid penalising executives for factors outside of their control that impact on value creation.

ABOUT STANDARD BANK NAMIBIA

SBN Holdings Limited Annual report 2016 5

Ethical and effective leadershipEthical and effective leadership relates to uniting purpose and performance. Embedding an ethical culture recognises that the trust of our stakeholders is the basis on which we compete and win.

Corporate citizenshipCorporate citizenship relates to the integral role we play in the socioeconomic wellbeing of Namibia. It commits us to using our resources responsibly as inputs to our business model, and balances our needs with those of society.

Sustainable developmentSustainable development commits us to enhance the resources and relationships we rely on today, for the future. Our plans to measure social, environmental and economic returns, will enable us to account for the total returns we deliver in line with our purpose.

Our strategic value drivers are outlined starting on page 9. The chief executive’s review on page 24, assesses our strategic performance for the year.

Driving Namibia’s growth over the

long term

Our multi-generational purpose recognises the

mutual interdependency of Namibia’s wellbeing and

that of the group. It is the ultimate expression of our

commitment to Namibian growth that is inclusive

and sustainable, and in turn secures viable

markets for our long-term profitability and value

creation.

Creating value for society

Social relevance is fundamental to our survival

and success, and is implied in our purpose and vision.

We are moving towards measuring our social return,

and to obtain a truer picture of our broader value

outcomes. This involves identifying the social,

economic and environmental risks and opportunities that

Namibia presents and how our business activities can

respond to these.

Creating value for the group

Our strategic value drivers align our allocation of

resources to our strategy. We have identified five key

value drivers, shown below, and continue to work on

selecting the appropriate metrics for each, which are

supporting more effective resource allocation and

appropriate trade-off decisions.

• Client focus • Employee engagement

• Risk and conduct • Financial outcome

• Social, economic and environmental

outcome

The chairman’s report on page 20 discusses key governance

developments and substantiates our commitment to corporate citizenship and sustainability.

The governance and remuneration report discusses how our governance framework and processes, and our board and committees, support the creation and protection of value.

Embracing innovation

Shareholders and investment analysts

Putting our clients’ best interests at the

centre of our business

Employees and their representatives

Leveraging our investments in IT

Communities and civil society

Motivating our people

Suppliers

What we do on page 6 links our business activities to socially beneficial outcomes.

Managing regulatory

change

Governments and regulators

6

What we do

Net profit

Retained equity which is reinvested to sustain and

grow our business

Income after credit impairments

Expenses

Dividends to our shareholders

Direct and indirect taxes to governments and other

related regulators

Credit risk Interest rate risk Insurance risk Business and reputational risk

Liquidity risk Market risk Operational risk, including compliance, environmental and/or social risk

As a financial services organisation with a broad offering of products and services, our goal is for all of our business units and corporate functions to work together in an integrated manner to seamlessly deliver on our clients’ financial needs.

ABOUT STANDARD BANK NAMIBIA

INCOME

EXPENSES

Interest expense

Net fee and commission

revenue

Trading revenue

Other revenue

Other operating costs

Interest income and credit

impairments

Source funding from client

deposits and other funders.

Provide transactional

banking facilities and knowledge-based

services to clients.

Market access and risk mitigation

products to businesses.

Revenue from other sources linked to

core business, as well as strategic

investments.

Invest in our operations.

Lend money to our

clients.

Invest in our people.

Staff costs

bankin

g activities

BU

SIN

ES

S A

CT

IVIT

IES

Inco

me

sta

tem

en

t im

pa

ct

Our clients are at the cen

tre of everything we do

banking and insurance activ

ities

Net interest income

1

2

3

4

5

6

7

SBN Holdings Limited Annual report 2016 7

1 Creates assets from which we derive interest income over time.

Lending enables individual clients to create wealth and generate income, helps business clients remain sustainable and supports employment and inclusive economic growth in Namibia.

2 Enables lending, creating liabilities that generate interest expense.

Funding provides our depositors with long-term returns, while mitigating against the erosion of their capital due to inflation.

3 Generates income through fee and commission revenue.

Transactional banking facilitates the movement of wealth, providing clients with convenient access to their funds. Our knowledge-based services, which include corporate advisory and loan structuring services, allow our clients to benefit from our experience and track record on the continent, and enables us to connect them to global pools of capital.

4 Creates trading revenue through participation in foreign exchange, commodity, credit, interest rate and equity instruments.

Market access enables businesses to grow, provides a conduit for investment into Namibia and helps economies monetise resources and diversify. Risk mitigation products enable financial protection and diversification through risk transfer.

5 Creates other sources of revenue, including insurance-related revenue and income from strategic investments.

Strategic investments support inclusive economic activity and enable wealth creation, while also contributing to investments that drive the socioeconomic development of Namibia. Short-term insurance activities offer protection of the value of assets against unforeseen loss.

6 Enables the group to invest in strategic information technology (IT) infrastructure, to enhance our capabilities and improve efficiency, and to deliver relevant products and services that meet our clients’ needs.

Investing in our operations enables us to develop innovative products and to continue meeting our clients’ needs, which supports our social relevance and legitimacy, maintains our positive contribution to the Namibian economy and strengthens our competitive position.

7 We invest in our people to align them to our strategic objective of consistently delivering excellent client experiences.

We hire locally wherever possible and through our activities, sustain other jobs in local economies. Training and development enhances the level of financial services and related skills in Namibia.

What this means for society

What this means for the group

8

ABOUT STANDARD BANK NAMIBIA

Why we can confidently deliver on our purpose

Legitimacy

Great

PEOPLE

PIONEERING

Passionate about

Namibia

The reason we exist Purpose

Group strategy Our strategy is centred on our commitment to Africa and directs our growth and evolution to the shared benefit of our clients, our people and all our stakeholders. It allows us to lead with purpose, to build a better business, and to position our footprint and platform for the future.

OU

R G

RO

UP

ST

RA

TE

GY

Risk Finance IT Operations Human capital Marketing and

communications

Compliance Legal Internal audit Group real

estate services

CORPORATE FUNCTIONS

BUSINESS UNITS

Corporate & Investment Banking

Personal & Business Banking

Liberty

Sta

nd

ard

B

an

k W

ealt

h

*Brand Finance: Africa’s most valuable banking brand, September 2016.

Technology andclient offerings(blue wallet blue voucher)

54 348 people

Brand*

1 20countries of operation in sub-Saharan Africa

What we aspire to be

Vision

directs and guides our business units and corporate functions

who leverage our presence and diverse capabilities to deliver on our group strategy

The behaviours and qualities that define us at our best

Values

Africa is our home, we drive her growth.

To be Africa’s (Namibia’s) agile provider of innovative financial solutions

Our values support our legitimacy, and are the basis on which we earn the trust

of our stakeholders:

Being proactive

Constantly raising the bar

Delivering to our shareholders

Serving our customers

Growing our people

Working in teams

Respecting each other

Upholding the highest levels of integrity

Heritage and brand >150 years

Commercial pragmatism

Brave long-term decisions

Present in AFRICA AND BEYOND

Committed to our clients & the trust they have in us

SBN Holdings Limited Annual report 2016 9

Strategic objectives

In 2015, the SBN Holdings leadership team commenced with the implementation of our 2015 – 2017 strategy, founded on a strong sense of team work and common purpose as evidenced by the collaboration and coordination of activities and plans across the bank.

The 2015 – 2017 strategic plan is underpinned by our values and the following themes:

Client centricityThis strategic objective aims to provide an excellent customer experience to everyone that engages with us. In doing this, we aim to employ a culture of continuous improvements to our systems, processes, products and people, as well as commit to a deep understanding of our customers’ needs and requirements in order to customise our propositions.

We want to position the bank as the employer of choice in Namibia. To this end, we have reviewed our staff engagement and recognition programmes, and have strengthened our training programmes given the business requirements. We cannot achieve the change and progress we are planning without a strong, motivated, skilled and engaged workforce.

Employer of choice

Given the journey that the bank has travelled in the implementation of the new core banking system, it is imperative that we prioritise the need to review and update our processes, products and services to optimise the new core banking system. In order to make this possible, we are creating an enabling environment for harvesting new ideas and look for opportunities for change and continuous improvement.

Continuous innovation

This pillar of our strategy is aimed at making the bank the preferred bank in our chosen market segments, supported by products and services that are solution driven, in line with our customers’ needs. This pillar looks at the refreshing of our value propositions to our customers for our key products and focus segments to ensure ongoing relevance and preference.

Trusted & preferred bank

All the above initiatives are geared toward the bank realising accelerated growth over the coming years. The management team has set itself ambitious but achievable targets for growth over the three-year strategy period.

Accelerated growth

The state-of-the-art systems and technologies that the bank has invested in and implemented over the last three years provide a foundation for system optimisation, efficiencies and cutting edge innovation in the years ahead.

Technology optimisation

10

ABOUT STANDARD BANK NAMIBIA

Tanzania

AngolaZambia

Namibia

Botswana

Zimbabwe

South Africa Lesotho

Swaziland

Mauritius

Malawi

EthiopiaSouth SudanNigeria

GhanaCôte

d’Ivoire

Kenya

Uganda

DRC

Mozambique

In, for and across Africa

Our diverse portfolio of operations has demonstrated resilience in withstanding cyclical pressures of generally slower economic growth and low commodity prices, and the spill-over effects of currency dislocation, regulatory reactivity and socio-political instability. Our contribution to driving more inclusive growth and promoting policy reform that supports economic diversification and development over the long term, will assist in extending Africa’s structural growth path notwithstanding the immediate economic challenges.

Our purpose-led strategy is designed to realise the opportunities presented by Africa’s longer-term structural trends.

Standard Bank

Representative office

Africa’s relative underdevelopment enables the implementation of the latest technologies, leapfrogging older technologies such as fixed-line communications with mobile networks, and coal-fired power with renewable energy.

50% of Africans will live in cities by 20301

Africa’s rapid rate of urbanisation is expected to continue rising from 36% in 2010 to 50% in 2030. This conglomeration of people provides governments and businesses with an opportunity to lower the cost of providing products and services.

200 million Africans aged 15 to 24 by 20504

Africa’s population is expected to double by 2050. With an estimated median age of 20, Africa’s youthful population will place increasing pressure on governments and businesses to drive employment growth as a greater number of Africans reach working age.

1.5 billion Africans of working age (15 to 64) by 20503

Africa’s working population is currently 659 million people, expected to grow to 861 million by 2020 and 1.5 billion by 2050.

28.7% of Africans are

online2

5.4% average GDP growth in sub-Saharan Africa from 2005 to 20156

GDP growth in Africa as a whole for the same period was slightly lower at 4.0%. This compares to the global average of 3.8% and 1.5% growth in developed economies over the same period.

136% increase in inter-Africa trade from 2005 to 20155

Inter-Africa trade increased from USD28,8 billion in 2005 to USD68 billion in 2015.

We are well positioned to facilitate the growing interregional trade and investment flows across the continent, to assist the economic growth of African countries and the expansion of multinationals into Africa.

Facilitating Africa’s growth

AFRICA

SBN Holdings Limited Annual report 2016 11

47.8% growth in China-Africa foreign direct investment (FDI)7

FDI into Africa from China is shifting from extraction to manufacturing industries.

Connecting Africa to developed world economic centres Our presence in, and connection with, global financial centres enables us to facilitate investment and development flows into Africa, and to access international capital to facilitate growth, diversification and development in Africa.

USD929 billion in world trade with Africa in 20157

This represents a 178% increase from USD334 billion a decade ago. About 70% of Africa’s exports are metals and minerals, indicating the need for economic diversification.31% of capital flowing into Africa is from worker

remittances8

Remittances replaced foreign aid as the largest external inflow to Africa in 2009, as Africa’s dependence on official development assistance eased by 18.7% to USD83,7 billion in 2015, from USD103 billion in 2014.

One third of the world’s mineral reserves are in Africa11

The continent also has 10% of world oil reserves and the largest cobalt and diamond reserves in the world, and 95% of the world’s platinum reserves are located in South Africa. Commodities remain fundamental to modern economies, and Africa’s resources remain largely either undiscovered or underexploited.

38.4% less Africans living below the international poverty line over the last decade10

Africans living below USD1,9 a day has fallen to 39.1% compared to 63.5% a decade ago.

60% of the world’s arable land is in Africa9

The underutilisation of arable land across the continent holds vast potential for increased commercial agriculture and production of agricultural goods. Mitigating the impact of climate change will be an essential part of realising this potential.

Facilitating China-Africa trade and investmentChina remains Africa’s largest trading partner and an increasingly important source of foreign investment across Africa. Our strategic partnership with ICBC provides us with a unique opportunity to provide financial services to clients operating in the China-Africa corridor.

1 African Development Bank – Urbanization in Africa (2012).

2 Internet World Stats (June 2016) – www.internetworldstats.com.

3 UN Population Statistics.

4 Africa Economic Outlook – Promoting Youth Employment in Africa (2012).

5 International Trade Centre.

6 International Monetary Fund; Standard Bank Research.

7 Annualised compound growth Overseas Development Institute (ODI, 2016).

8 African Development Bank – Organisation for Economic Co-operation and Development.

9 World Bank.

10 African Development Bank.

11 Economics Intelligence Unit – African Development Bank.

12

ABOUT STANDARD BANK NAMIBIA

Measuring our strategic progress

During 2016, we embarked on a journey across the group to develop clearly defined strategic value drivers. These drivers provide the group and its stakeholders with transparent and consolidated information that we believe is of most relevance in measuring the group’s sustainability lead strategy and performance in delivering value to the group’s stakeholders.

Strategic value drivers*

CLIENT FOCUS EMPLOYEE ENGAGEMENT

What this means

Placing clients at the centre of everything we do

Making Standard Bank a great place to work

How the driver aligns with our strategy

Clients are at the heart of our business and by focusing on our clients we will achieve a profitable and sustainable business.

Our focus is to consistently create excellent client experiences, by understanding our clients and by offering the products, services and solutions that our clients need.

We strive to create a great place to work where our people feel deeply connected with our purpose and our clients, are empowered and recognised for delivering against our strategic objectives, and have made the most of every opportunity to achieve their full potential. How our people think and feel about work directly correlates with our client satisfaction levels and our ability to deliver our strategy.

How we measure our progress and performance

To understand our clients better we measure their satisfaction in terms of:

Net Promoter Score (NPS) for PBB

Client satisfaction index (CSI) for CIB.

These scores are determined from client surveys conducted in phases throughout the year to obtain an annual result.

To determine engagement levels, we consider the following:

Deloitte Best Company to Work for Survey.

What we are working toward

Over and above these existing measures, the group is looking to develop a holistic client experience measure across segments, business units and geographies. This will provide more detail on accessibility, ease of doing business, personalised offerings, staff engagement, brand value and reputation, executional excellence and value for money.

The employee survey will be conducted annually across the group.

Our performance to delivering on our strategy

The results of our client surveys indicate that we have met expectations in servicing our clients. We will continue to explore ways to better our results.

Deloitte Best Company to Work for Survey has shown improvements on the rating from 3.55 to 3.62 in 2016.

SBN Holdings Limited Annual report 2016 13

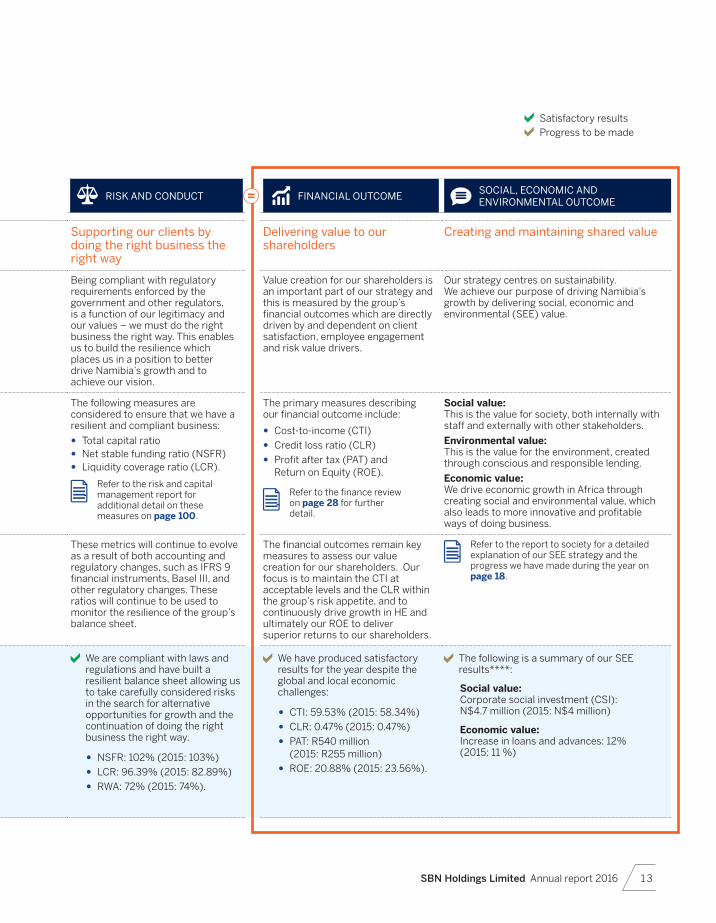

RISK AND CONDUCT FINANCIAL OUTCOMESOCIAL, ECONOMIC AND ENVIRONMENTAL OUTCOME

Supporting our clients by doing the right business the right way

Delivering value to our shareholders

Creating and maintaining shared value

Being compliant with regulatory requirements enforced by the government and other regulators, is a function of our legitimacy and our values – we must do the right business the right way. This enables us to build the resilience which places us in a position to better drive Namibia’s growth and to achieve our vision.

Value creation for our shareholders is an important part of our strategy and this is measured by the group’s financial outcomes which are directly driven by and dependent on client satisfaction, employee engagement and risk value drivers.

Our strategy centres on sustainability. We achieve our purpose of driving Namibia’s growth by delivering social, economic and environmental (SEE) value.

The following measures are considered to ensure that we have a resilient and compliant business:

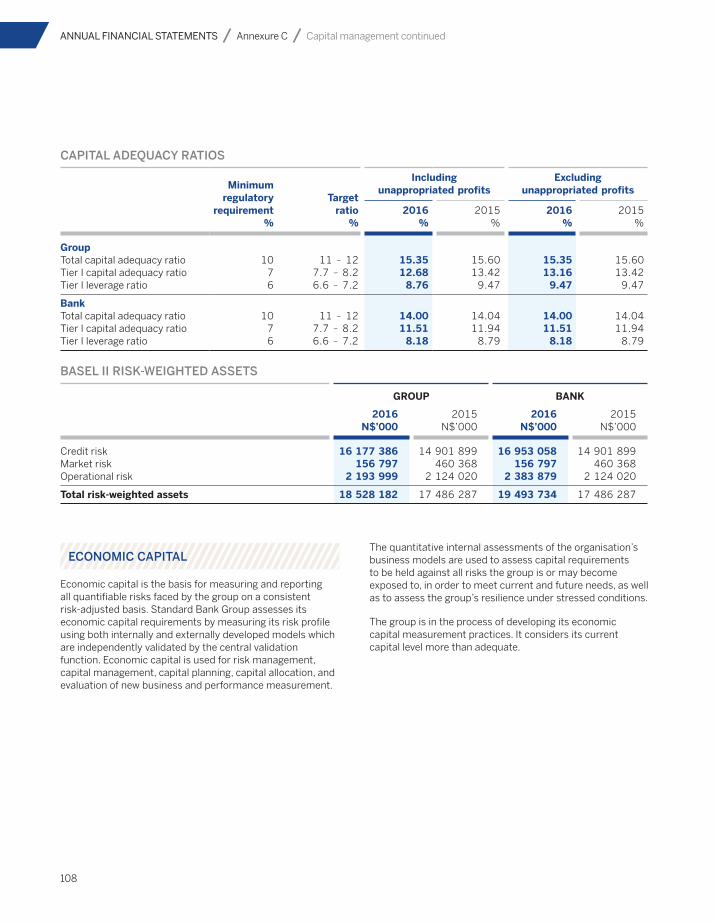

Total capital ratio Net stable funding ratio (NSFR) Liquidity coverage ratio (LCR).

Refer to the risk and capital management report for additional detail on these measures on page 100.

The primary measures describing our financial outcome include:

Cost-to-income (CTI)

Credit loss ratio (CLR)

Profit after tax (PAT) and Return on Equity (ROE).

Refer to the finance review on page 28 for further detail.

Social value:This is the value for society, both internally with staff and externally with other stakeholders.

Environmental value: This is the value for the environment, created through conscious and responsible lending.

Economic value: We drive economic growth in Africa through creating social and environmental value, which also leads to more innovative and profitable ways of doing business.

These metrics will continue to evolve as a result of both accounting and regulatory changes, such as IFRS 9 financial instruments, Basel III, and other regulatory changes. These ratios will continue to be used to monitor the resilience of the group’s balance sheet.

The financial outcomes remain key measures to assess our value creation for our shareholders. Our focus is to maintain the CTI at acceptable levels and the CLR within the group’s risk appetite, and to continuously drive growth in HE and ultimately our ROE to deliver superior returns to our shareholders.

Refer to the report to society for a detailed explanation of our SEE strategy and the progress we have made during the year on page 18.

We are compliant with laws and regulations and have built a resilient balance sheet allowing us to take carefully considered risks in the search for alternative opportunities for growth and the continuation of doing the right business the right way.

NSFR: 102% (2015: 103%)

LCR: 96.39% (2015: 82.89%)

RWA: 72% (2015: 74%).

We have produced satisfactory results for the year despite the global and local economic challenges:

CTI: 59.53% (2015: 58.34%)

CLR: 0.47% (2015: 0.47%)

PAT: R540 million (2015: R255 million)

ROE: 20.88% (2015: 23.56%).

The following is a summary of our SEE results****:

Social value: Corporate social investment (CSI):

N$4.7 million (2015: N$4 million)

Economic value: Increase in loans and advances: 12%

(2015: 11 %)

Satisfactory results

Progress to be made

14

INPUTS

INTERNAL

EXTERNAL

ABOUT STANDARD BANK NAMIBIA

Our material issues

We view the materiality determination process as a business tool that facilitates integrated thinking. The process draws on our ongoing stakeholder engagements, for instance with clients and regulators, and the work we are doing to revise the measures that underpin our strategic value drivers –

We consider an issue to be material if it has the potential to substantially impact on our commercial viability, our social relevance and our relationships with our stakeholders. Our material issues are informed by the expectations and concerns of our stakeholders, and the social, economic and environmental context in which we operate.

How we determine our material issues

Based on this review, we identify the themes and issues that appear to be of greatest interest and concern to our stakeholders, and summarise, consolidate and align these as a list of material issues. In 2016, we undertook a fresh assessment of the issues and concerns raised by our stakeholders, which confirmed that the themes identified in 2015, remain pertinent. The board risk committee examined and confirmed our material issues in 2016.

The identified concerns of our stakeholders and how we are responding are discussed on page 16.

specifically our assessments of client and employee satisfaction. It also considers the views of key social and political stakeholders, obtained through specific engagements undertaken to assess the quality of our relationships with them.

Information gathered within the organisation from thefollowing sources:

Ongoing scanning of external sources of information to identify statements, concerns andperceptions raised by our stakeholders in relation to the banking sector in general and the

group in particular. This includes:

• Shareholders at the annual general meeting.• Requests, memos and complaints received from clients, political parties, civil society bodies and others.

• Media coverage.• Research and risk reports issued by institutions such as the World Economic Forum and the International Institute of Finance.

• Issues raised in parliamentary committees and government speeches, statements and policy documents.• Reports and statements by trade associations, business organisations and think tanks.

• Reports and articles by industry analysts and investors. • Global and regional development concerns such as the Sustainable Development Goals, Namibia’s National Development Plan and the government Harambee Prosperity Plan.

• Leadership.• Public events such as investor conferences and/or business summits.

• Internal events such as our annual Leadership Conference.• Social corporate investment, board risk committee.

• Stakeholder engagement undertaken by the group at various levels.• Group risk reports prepared by the integrated operational risk function and based on a consultative process run throughout the group.

• Reports prepared by the group’s research and investor relations functions.• Group internal audit.

• Employee engagement surveys.

SBN Holdings Limited Annual report 2016 15

1Our customers and clients are the reason we are in business.

Our intentHow we design our products, deliver our services, conduct ourselves and make strategic decisions should all be done in the best interests of our clients.

What we will do to realise the opportunities presented by our strategy Instil a culture that values excellent client experiences, ethical and fair conduct and market

integrity among all our people. Constantly leverage new technologies to meet changing client expectations and enter

partnerships for innovation. Ensure appropriate technical capability and skill to prevent our clients from being exploited. Keep client information private and ensure the veracity of client data.

2Our employees enable our ability to meet our objectives, provide a positive client experience, comply with our regulatory obligations and create shareholder value.

Our intentWe are committed to embedding a culture that encourages and rewards excellence and ensures adherence to our values.

What we will do to realise the opportunities presented by our strategy Ensure we have the right skills and capabilities to successfully execute our strategy, manage

differing expectations of a multi-generational workforce and comply with local transformation legislation.

Build an ethical and risk-aware culture that mitigates the risk of internal fraud, client exploitation and unethical conduct.

Capacitate our people to perform in a technology-led environment.

3Namibia is our home and we are committed to the expansion and deepening of our business across the country.

Our intentWe will work with our clients to support economic growth and diversification and counterbalance the slowdown in emerging markets and the related decline in commodity prices.

What we will do to realise the opportunities presented by our strategy Maintain profitability within our risk appetite while navigating challenging economic and

regulatory environments, meeting client expectations and competing effectively. Invest in innovative products and services. Ensure robust monitoring of strategy implementation and harmonise strategies across the

business. Maintain a forward-looking view of potential socio-political landscape and put appropriate

business continuity measures in place.

4Continual innovation.

Our intentWe will continue to innovate so that we are able to constantly improve the value and experience we provide for our clients and to stay ahead of our competitors.

What we will do to realise the opportunities presented by our strategy Deliver new products and services to market quickly without compromising system stability. Develop a culture that encourages innovation and challenges established processes, with a view

to delivering excellent client experiences to differentiate us in a commoditised and low-cost competitive environment.

Develop the capacity of our people to ensure they are resilient and supportive of business changes. Ensure third parties maintain the security of client information, where it is necessary to share

such information to develop innovative solutions. Address social challenges through innovation.

5The regulatory frameworks governing financial services providers, at national and global level, are continually evolving with supervisory powers of certain regulatory bodies having significantly increased.

Our intentWe will continue to work closely with all our regulators to ensure that we manage regulatory developments effectively, while minimising as far as possible negative impacts on clients, employees and areas of business.

What we will do to realise the opportunities presented by our strategy Adhere to associated regulations when processing data shared across third-party networks and

monitor service providers to ensure compliance with privacy controls. Maintain and enhance our ability to comply with changing regulation across jurisdictions and

comply with capital requirements at all times, in a way that does not compromise client experience. Instil a compliance mindset across the group.

6Our IT systems and functionality is essential to our ability to provide our clients with uninterrupted access to safe, secure and reliable products and services, and to mitigate risk.

Our intentWe will strive to improve the stability and technical sophistication of our IT systems and functionality to improve the services we provide to our clients.

What we will do to realise the opportunities presented by our strategy Balance client expectation for innovation against maintaining system stability. Constantly monitor and anticipate criminal exploitation of our systems and cyber-attacks on our

services, and deploy prevention and mitigation measures. Ensure that our systems maintain the privacy of client information and put additional measures in

place to protect our data stores.

16

ABOUT STANDARD BANK NAMIBIA

To protect our legitimacy, which is necessary to compete effectively and create value, we work hard to build and maintain relationships of trust with our stakeholders based on open and proactive engagement.

Our stakeholders are those individuals or organisations that have an interest in our success or failure and whose opinions and actions can impact on our ability to execute our strategy and conduct our business activities. Outlined below are the top issues raised by our key stakeholders and our strategic initiatives that respond to these concerns.

Concern Our strategic initiatives Material issue

Clients

Improving client service levels and providing cheaper, more convenient banking options.

Groupwide focus on enhancing client experience through: IT platform modernisation programme. Innovative digital services that provide relevant banking and wealth solutions

per client segment. Empowering client-facing staff to make decisions. Changing organisational structures and ways of working.

2 5 6

Increasing process efficiency and automation of payments to reduce delays, errors and complexity.

Managing the impact of compliance requirements on client experience.

Technologically-enabled compliance and risk solutions. Digital services that meet regulatory requirements.

2 4 5 6

Preserving multi-generational wealth and delivering solutions for younger high net worth individuals.

Integrated multi-generational wealth solutions. Leadership Academies to guide this client segment.

2

Higher expectations of personalised, relevant advice from financial advisers.

New client-focused operating model in Wealth. Goals-based investment philosophy where product and advisory services are

aligned to the principles of the pending Retail Distribution Review.

2 4

Concerns with respect to cybercrime and fraud.

Sophisticated fraud detection and mitigation tools. Regular client and staff awareness campaigns.

2 5 6

Suppliers

Aligning the group’s procurement practices to support transformation in Namibia.

Proactive and deliberate approach, including targets, to ensure the equitable participation of black-owned businesses in Standard Bank’s supply chain.

Redirecting goods and services previously procured from foreign suppliers to local black suppliers, where feasible.

Supplier development programmes for small businesses, including access to financing, where relevant.

1 4

Employees and their representatives

The need to develop new skills in a changing operating environment due to the rise of digitisation and automation.

Wide range of continuous learning programmes. Leadership, youth and specialised skills development programmes. University partnerships to develop IT curricula. Initiatives such as upskilling, retraining and redeployment to assist

employees affected by changes to business operating models and the introduction of new ways of working.

3 6

Driving diversity and inclusion to create a workforce that is locally relevant.

Diversity and inclusion framework. Employment equity targets in Namibia. Accelerate the development of local talent pipelines in operating countries,

and the advancement of black employees in Namibia.

1 3 4

Responding to our stakeholders

SBN Holdings Limited Annual report 2016 17

Our ongoing stakeholder engagement initiatives and those specifically related to determining the group’s material issues are outlined on page 14, and discussed comprehensively in the report to society.

Concern Our strategic initiatives Material issue

Governments and regulators

Rebuilding trust and maintaining stability in the financial sector, and compliance with various legislative changes.

Adoption of global best practice in financial standards. Strong relationships with local banking regulators and central bank officials. Standardised groupwide compliance model. Cooperation between compliance teams at group and country level. Skills sharing through cross-jurisdictional secondments. Automated compliance monitoring and reporting. Standardisation of the methodology to assess and prepare for the impact of

new regulation.

1 4 6

Improving the control environment in the Africa Regions.

Embedding compliance and risk-aware behaviour.

Strong focus on employee conduct and values. Regulatory awareness initiatives and compulsory compliance training.

1 3 4

Shareholders and investment analysts

The group’s resilience to challenging economic conditions, globally and in South Africa.

Leverage our diversified portfolio at sector, regional and client levels, by allocating capital to select growth opportunities.

Regular risk assessments and adjustment of risk appetite. Retain quality client segments and grow select client segments in PBB. Increase CIB’s exposure to growth sectors and economies, offsetting

declines in commodity sectors. Support clients facing difficulties through appropriate debt restructuring.

1 2

Maintaining asset quality.

Managing costs and improving the cost-to-income ratio.

Maintain disciplined cost management. Achieve global benchmarks for IT expenditure from 2018.

2 4

Improving the performance of ICBCS.

The strategic cooperation agreement with ICBC remains an important element in both our Africa strategy and in the future of the group’s other banking interests.

1 2

Unclear executive pay and long and short-term incentive structures.

Review the current remuneration policy and how it links to the group’s strategic value drivers to provide stakeholders with a better understanding of executive remuneration structures.

3 4

Communities and civil society

Contributing to alleviating societal challenges across the continent.

Business activities facilitate financial inclusion, infrastructure investment, entrepreneurship, enterprise development and job creation.

Initiatives and digital solutions that support small businesses to become sustainable.

Support for civil society organisations. Learnership programmes that provide on-the-job experience for matriculants

and graduates. Standard Bank Namibia Buy a Brick campaign. CE outreach

1 2 5

Contributing to initiatives that address macroeconomic and socio-political challenges.

Funding for higher education. Standard Bank bursary programmes. Work with government, corporates and universities to develop sustainable

tertiary education funding solutions. Fawena

1 3

The group’s efforts to mitigate the impact of climate change.

Managing environmental and social risk related to financing activities. Standard Bank-financed renewable energy projects. Adoption of green building principles and measures to reduce the direct

environmental impact of activities.

1 2

18

ABOUT STANDARD BANK NAMIBIA

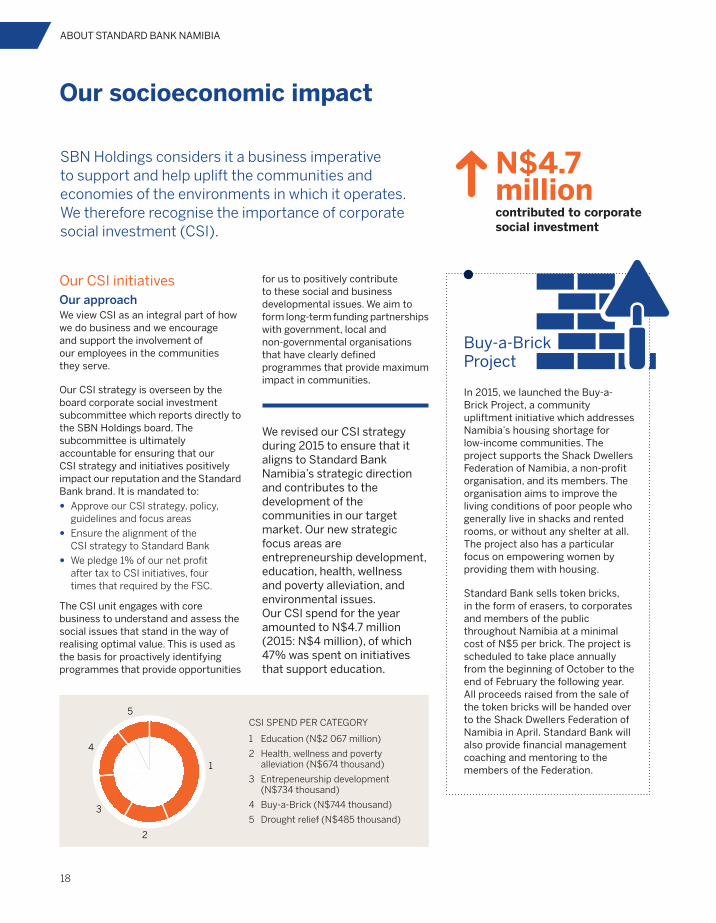

SBN Holdings considers it a business imperative to support and help uplift the communities and economies of the environments in which it operates. We therefore recognise the importance of corporate social investment (CSI).

Our socioeconomic impact

Our CSI initiativesOur approachWe view CSI as an integral part of how we do business and we encourage and support the involvement of our employees in the communities they serve.

Our CSI strategy is overseen by the board corporate social investment subcommittee which reports directly to the SBN Holdings board. The subcommittee is ultimately accountable for ensuring that our CSI strategy and initiatives positively impact our reputation and the Standard Bank brand. It is mandated to:

Approve our CSI strategy, policy, guidelines and focus areas

Ensure the alignment of the CSI strategy to Standard Bank

We pledge 1% of our net profit after tax to CSI initiatives, four times that required by the FSC.

The CSI unit engages with core business to understand and assess the social issues that stand in the way of realising optimal value. This is used as the basis for proactively identifying programmes that provide opportunities

We revised our CSI strategy during 2015 to ensure that it aligns to Standard Bank Namibia’s strategic direction and contributes to the development of the communities in our target market. Our new strategic focus areas are entrepreneurship development, education, health, wellness and poverty alleviation, and environmental issues. Our CSI spend for the year amounted to N$4.7 million (2015: N$4 million), of which 47% was spent on initiatives that support education.

In 2015, we launched the Buy-a-Brick Project, a community upliftment initiative which addresses Namibia’s housing shortage for low-income communities. The project supports the Shack Dwellers Federation of Namibia, a non-profit organisation, and its members. The organisation aims to improve the living conditions of poor people who generally live in shacks and rented rooms, or without any shelter at all. The project also has a particular focus on empowering women by providing them with housing.

Standard Bank sells token bricks, in the form of erasers, to corporates and members of the public throughout Namibia at a minimal cost of N$5 per brick. The project is scheduled to take place annually from the beginning of October to the end of February the following year. All proceeds raised from the sale of the token bricks will be handed over to the Shack Dwellers Federation of Namibia in April. Standard Bank will also provide financial management coaching and mentoring to the members of the Federation.

CSI SPEND PER CATEGORY

1 Education (N$2 067 million)

2 Health, wellness and poverty alleviation (N$674 thousand)

3 Entrepeneurship development (N$734 thousand)

4 Buy-a-Brick (N$744 thousand)

5 Drought relief (N$485 thousand)

N$4.7 millioncontributed to corporate social investment

for us to positively contribute to these social and business developmental issues. We aim to form long-term funding partnerships with government, local and non-governmental organisations that have clearly defined programmes that provide maximum impact in communities.

1

4

5

2

3

Buy-a-Brick Project

SBN Holdings Limited Annual report 2016 19

Our footprint

Lüderitz

Rosh Pinah

Keetmanshoop

Maltahohe Mariental

Aranos

Rehoboth

WindhoekWalvis Bay

SwakopmundArandis

OmaruruOkahandja

Gobabis

Otjinene

OtjiwarongoKhorixas

Outjo

Tsumeb

RunduOndangwaOngwediva

Eenhana

OpuwoOkahao

OkalongoOshikango

OutapiRuacana Nkurenkuru

Katima Mulilo

Grootfontein

Standard Bank was the first commercial

bank to open its doors in Lüderitz in 1915.

The credo of the bank is simple, the approach direct, and the

results are positive. We offer a complete range of financial

services, be it Corporate, Commercial, Personal or

Business Banking. We have an extensive branch network

and ATMs all over Namibia, with specialist support divisions

such as Standard Insurance Brokers, Vehicle and Asset

Finance and our Home Loans Department.

Omuthiya

Bethanie

Aussenkehr

Otavi

Henties Bay

Oshakati

20

Chairman’s report

Overview2016 was a tumultuous year. Globally, two key events stole the limelight – the UK’s “Brexit” vote and the US election. The ambiguity in the run-up to these events, as well as the contrarian outcomes drove uncertainty and volatility. Overall, global growth is expected to have been in line with the International Monetary Fund’s (IMF) expectations, i.e. at 3.1% for the year. In Namibia, the threat of a sovereign downgrade by rating agencies to sub-investment grade persisted and emerged towards the end of 2016. This in turn negatively impacted the already weak business and consumer confidence and further delayed much needed domestic investment and job creation opportunities. Inflationary pressures brought about by the drought and the weak exchange rate placed

additional pressure on already constrained consumers. Demand for credit was weaker year-on-year and displayed a decelerating trend over the year, with household demand broadly flat, compounded by policy changes seeking to stem the demand for credit on motor vehicles and reduce speculation within the property market.

Overall GDP growth for 2016 is expected to have been around 1%, down from 5.3% in 2015. In certain sectors, such as agriculture and mining, growth oscillated between expansion and contraction over the year, while other sectors, such as finance, real estate business and personal services, continued to report growth quarter-on-quarter despite the difficult conditions. In 2H16, on the back of positive global sentiment, firmer commodity prices and some recovery in the currency,

Namibia’s economic outlook improved. This momentum, combined with the fiscal decisiveness by the Minister of Finance on certain of the areas of concern raised by the rating agencies, aided the country in maintaining an investment grade rating. There remains a broad recognition that there is still considerable work to be done, not only to avoid a downgrade in 2017, but more importantly, to deliver the inclusive growth required to tackle poverty and unemployment and transform the economy into one in which everyone can share in its benefits.

Against this backdrop, the group showed resilience in its financial performance for 2016 with profit after tax increasing by 3% compared to 2015. Furthermore, our capital position and liquidity remained strong, with a total capital adequacy ratio of 15.35% for

“The group showed resilience in its financial performance for 2016 with profit after tax increasing by 3% compared to 2015.”

CHAIRMAN'S REPORT

SBN Holdings Limited Annual report 2016 21

SBNH and liquid assets well in excess of prudential requirements.

The “Tuyende” journey has the board’s full support, specifically the emphasis given to defining the factors that underpin the bank’s legitimacy and the trust our stakeholders have in us. Our results for 2016 are testimony to the challenges we face on this journey – more work is required to ensure that we are in a position to fully realise the potential inherent in the bank’s brand and that the market offers.

Our people are the custodians of the customer experience and the overall strength of our brand, and are therefore the ultimate determinant of success and competitive advantage. Attracting and retaining the skills we need, and creating a desirable and differentiated workplace culture is a complex undertaking in a

highly competitive environment where the ability to attract top talent is critical. As such, “Tuyende” emphasises the importance of empowering our people and developing great leaders. During 2016, we reviewed our employee value propositions and looked to embed our values and culture, which together will differentiate us as an employer.

Compliance with Basel II has been at the forefront of the central bank’s policy for monitoring capital adequacy. The bank remains well capitalised on both Tier I

and total capital ratios, as well as maintaining conservative buffers for both liquidity and other risk positions. At the end of 2016, the Bank of Namibia communicated the draft requirements of Basel III for consultation. The group has already begun to monitor the internal compliance established by Basel III so as to be well-prepared for any proposed adoption date and transitional arrangements. Where possible, we contribute actively and constructively to the development of national policy, legislation and regulation

Herbert Maier

N$540 millionPROFIT AFTER TAX2015: N$525 million +3%

“During 2016, we reviewed our employee value propositions and looked to embed our values and culture, which together will differentiate us as an employer.”

22

CHAIRMAN'S REPORT continued

the agriculture sectors. Commodity exporters will welcome higher prices. Namibia’s forecast growth is expected to improve to 2.9% in 2017, but remains subject to government commitment to reduce consumptive expenditure, and event risk such as rating agency decision points during the year. Lastly, BON has indicated that it expects rates to remain on hold, subject to inflation and exchange rate developments, which is likely to continue to constrain household consumptions and fixed investment.

With these dynamics in mind, we look to our clients, to the challenges and opportunities they may face, and seek ways to partner with them on their journeys in 2017 and beyond. As we focus on delivering market-leading client experiences, we continue to invest in our client-facing digital capabilities to enable our clients to transact independently and safely anytime anywhere. We recognise and value the trust that our clients place in us and remain vigilant in our efforts to protect our clients’ resources and data.

Accordingly, we continue to monitor developments and potential threats, engage with industry bodies and invest

through formal submissions and regular engagement with policymakers, law-makers and regulatory authorities. Our approach is guided by our aim to promote regulatory frameworks that are unambiguous, cohesive and practical, and that minimise unintended consequences.

ProspectsThe economic growth momentum that built towards the end of 2016, driven by China and the US, has continued into the start of 2017. The IMF is forecasting an uptick in global growth from 3.1% in 2016 to 3.4% and 3.6% in 2017 and 2018 respectively. Global trade activity should pick up on the back of policy stimulus and a gradual normalisation of large economies, such as Brazil and Russia. However, uncertainty surrounding US policy direction under the new administration, Brexit negotiations and the broader European macro outlook may pose downside risks to global growth prospects.

Sub-Saharan Africa’s GDP growth is expected to be 2.8%, buoyed by global trade, resource demand and improved economic prospects generally. Rains in late 2016 and early 2017 bode well for

in our defences to enhance our resilience. The businesses we operate are complex and we rely on our people across our network to navigate the challenges each business faces and make appropriate decisions in line with strategic priorities and our values. To this end, we continue to invest and equip our people with the skills required, empower them to make decisions, hold them accountable and celebrate their successes. Furthermore, we are seeking opportunities to use technology to leverage our data to inform decisions, deliver client-specific solutions and drive process efficiency and productivity gains.

AppreciationThe board and I would like to express our appreciation to our customers and other stakeholders, including the bank’s shareholders, for their continued support. We extend our appreciation to the entire staff of Standard Bank for their commitment to service and excellence in managing the business.

I wish to express my utmost appreciation to Martha Namundjebo- Tilahun who, after a period of ten (10) years on the Board, retired in July 2016. I also want to welcome Bryan Mandy

“The businesses we operate are complex and we rely on our people across our network to navigate the challenges each business faces and make appropriate decisions in line with strategic priorities and our values.”

SBN Holdings Limited Annual report 2016 23

(chief financial officer) to the board from December 2016 as an executive director.

As we look to the year ahead, we remain steadfast in our commitment to doing the right business the right way. In this context, we continue to embed a culture of responsible business practices. We remain committed to delivering through-the-cycle headline earnings growth and ROE within our target range of 20.88% to 25% over the medium term. In order to do so, we recognise the need to balance prudent capital management with appropriate return-based resource allocation and leverage.

I wish to highlight that banks play an important role in society which is

“We recognise the need to balance prudent capital management with appropriate return-based resource allocation and leverage.”

broader than creating shareholder value. We seek to create value for all our stakeholders – clients, employees, shareholders, government and communities alike. In doing so, we continue to contribute meaningfully to the social, economic and environmental prosperity and wellbeing in the markets in which we operate.

Finally, a well-earned word of thanks to my fellow board members for their valued input, productive participation, excellent teamwork and sound guidance throughout 2016. Our purpose as an organisation remains – Namibia is our home and we support her growth.

24

Chief executive’s review

“2016 was, therefore, a year of stagnation for business, and despite these challenges, Standard Bank posted satisfactory results and made great strides in transforming our operational environment, operational processes, products and operational structures.”

OverviewThe slowdown in the mining, agriculture and construction industries, compounded by the regional drought and government consolidation efforts constrained the performance of the domestic economic activities. It is estimated that the domestic economy grew at an overall GDP growth of 1%, which is significantly below the GDP of between 5% to 7% seen in the preceding three years.

The year was further characterised by heightened liquidity constraints and increasing costs of liquidity in the domestic market which negatively impacted interest margins.

2016 was, therefore, a year of stagnation for business, and despite these challenges, Standard Bank posted

satisfactory results and made great strides in transforming our operational environment, operational processes, products and operational structures.

Strategic prioritiesDuring 2016, we not only reaffirmed our commitment to understanding and meeting our customers’ needs, but we started to implement a revolutionary programme aimed at changing the culture and ways of work in the bank with the objective of improving our processes and products from a customer’s perspective. The programme has been implemented at three pilot Proofs of Concept and the early feedback is very encouraging.

The programme is expected to be extended to the rest of the bank’s operations by the end of 2017, and we

believe these will significantly revolutionise our processes and approach to servicing our customers.

Customer centricity We continued the review of our products, processes and structures to enhance customer service and deliver solutions efficiently and effectively. The results are visible in the key products such as Home Loans and Vehicle and Asset Finance which saw improvements as evidenced by the reduction in turnaround times for Home Loans from 170 days in 2014 to 51 days in 2016 and an increase in market share for Vehicle and Asset Finance to over 27% from below 25% in 2015.

Technology optimisationWe have seen a continual stabilisation of our Information Technology systems

CHIEF EXECUTIVE'S REVIEW

SBN Holdings Limited Annual report 2016 25

and channels during the course of the year following focused initiatives and actions implemented during the year.

In our quest to be relevant to the Namibian market and our drive to becoming the most preferred bank, technology optimisation and innovation remained a high priority which saw the launch of the BlueWallet, refreshed Online Banking platform, SmartApp and EMV debit cards.

Trusted & preferred bankWe are pleased that we have, during 2016, completed the review and refreshing of our Customer Value Propositions for key segments of our customer base. This process will be continued into 2017 with the continual review of these value propositions as informed by our customers’ needs and requirements.

We continued with investments in the expansions of our points of representation in our quest to bring our services closer to our customers. We opened four new points of representation across the country in Ruacana, Okuryangava, the Waterfront in Swakopmund and Okongo. We upgraded the Keetmanshoop, Nkurenkuru, Otjinene and Game Shopping Centre branches to enhance customer experience. We further relocated a number of our points of

representation into new refurbished facilities in Gobabis, Eenhana and Aussenkehr signifying our commitment and trust in the future of these towns.

We are honoured and pleased by the number of prestigious awards received during the year. Standard Bank was awarded as the best investment bank in the country for 2016, Best Emerging Markets Bank in Namibia and Best Sub-Custodian Bank in Namibia.

Vetumbuavi Mungunda

“In our quest to bring our services closer to our customers – we opened four new points of representation across the country.”

Vet

“The Standard Bank Employee Shares Ownership Scheme is unique in Namibia given the scale and number of beneficiaries, being over 1 300 staff members participating in the over N$300 million Shares Scheme.”

26

CHIEF EXECUTIVE'S REVIEW continued

Employer of choiceWe reviewed our staff value propositions, accompanied by transitions to a new medical aid provider and the conclusion of the final phase of the Employee Shares Ownership Scheme. The Standard Bank Employee Shares Ownership Scheme is unique in Namibia given the scale and number of beneficiaries, being over 1 300 staff members participating in the over N$300 million shares scheme. This is probably one of the most broad-based and inclusive shares schemes implemented in Namibia.

We continued our participation in the Deloitte Best Company to Work for Survey which saw the bank improve its overall score from 3.55 in 2015 to 3.62 in 2016. We are most pleased with the feedback we receive from our employees through this participation on how they experience Standard Bank and the levers available to us to improve our offerings and their experience.

The development of our people has remained a key focus during 2016, with the following people development initiatives executed during the year:

Intensive executive mentorship programme for 25 senior management personnel of the bank

Graduate development programme which exposes selected top graduates to all the functions of the bank

Learning Academy where entry staff members are exposed to the activities of the bank for three months before being deployed into the bank.

Sustainable growthOur profits for the year amounting to N$540 million and representing a growth of 3% above the prior year is satisfactory in the current macro-economic environment. The current year results were impacted by interest expense growth of 21%, which was significantly higher than the 12% growth in interest income. The increase in interest expense was driven by the increasing costs of funds and liquidity holdings, as well as divergence in the correlation between local prime interest rates and JIBAR rates from which most of the local liquidity costs are derived from.

The results were further impacted by once-off systems implementation- related costs amounting to N$54 million written-off during the current year. Normalised earnings, excluding these once-off written-off costs would show a growth of 14.3% on the 2015 earnings.

We are pleased to report that our results for 2016 were supported by growth in quality assets at 12% over the prior year. The growth in loans and advances to customers of 11% is pleasing when compared to the industry growth of 8.9% for the year.

Our capital position continues to exceed regulatory capital thresholds at 15.35% capital adequacy and 8.76% leverage ratios respectively.

LeadershipKey positions were filled during 2016, including the key position of head of Personal & Business Banking (Mercia Geises) following the departure of the previous incumbent.

Corporate & Investment Banking (CIB) highlightsCIB profits for the year at N$218 million represent a growth of 28% on the 2015 results. These results were supported by a number of landmark transactions concluded during the year. The business has shown significant resilience given the complexity and scale of regulatory projects it is tasked with, including PSD7 and the localisation of corporate accounts.

Personal & Business Banking (PBB) highlightsThe business launched a number of innovation products, including BlueWallet which has been well-embraced by the market. The regulatory environment has continued to impact the business profitability, firstly through the greater liquidity requirements and secondly the scale and complexity of regulatory projects hit the income statements as they impair the business ability to focus on business growth and the resultant higher costs of compliance which need to be absorbed by the business.

Credit managementStandard Bank continues to show improvements in credit impairments, seeing a reduction in our non-performing loans ratio to 1.94% from 2.68% in 2015. This is due to the robust and stringent application process which protects both the customer and our bank.

“We are pleased to report that our results for 2016 were supported by growth in quality assets at 12% over the prior year.”

SBN Holdings Limited Annual report 2016 27

We continue to review our credit processes and risk appetite with respect to our key products.

Corporate social investment highlightsStandard Bank considers it a business imperative to support and help uplift the communities and economies of the environments in which it operates. We therefore recognise the importance of Corporate social investment (CSI).

We pledge 1% of net profit generated to CSI initiatives. The strategic focus of our CSI programme is entrepreneurship development, the environment, education and health and wellness. In 2016, we committed N$5 million to corporate social investment programmes for 2017.

We are pleased with the contribution we have made through the launch of our flagship project, Buy-a-Brick, which is aimed at mobilising individual Namibians to buy token bricks where proceeds are handed over to the Shack Dwellers Federation of Namibia in April of every year.

Contributions collected in 2016 through the Buy-a-Brick Initiative of N$1.4 million realised the construction of 44 houses in Rehoboth. The other significant objective of this project, which we believe is being achieved, is to create awareness about the acute housing shortage in the country and establish the need for housing for the no-and-low-income communities and the quest for solutions in the national discourse.

New head officeThe board at its meeting in December 2016, approved the location and construction of a new head office for the bank. This move signifies not only our long-term commitment to Namibia, but also demonstrates our trust and belief in the long-term future of our country.

It is expected that the ground excavation work on the new head office should start in April 2017 and construction work is expected to commence in June 2017.

Outlook for 2017The macro-economic environment in the country started to deteriorate in 2016, notably as a result of a combination of several factors that have come together to diminish growth and drive imbalances within the local economy. These factors are the low level of government spending, weak commodity prices, drought, water supply constraints, inflation and lower retail tourists.

The challenging environment has continued into the early months of 2017 and has been compounded by increased liquidity constraints in the local market, reduction in economic activities such as motor vehicle and house sales and increasing inflation. The steep increase in inflation heightens the risk of an increase in interest rates which may add to the already increasing costs of funds in the local market and further erodes margins in the local banking sector.

The recent good rains, and the increase in water levels at major storage dams across the country should point to improvements in the outlook for the

agricultural sector, as well as other water-dependent sectors such as manufacturing. Marginal improvements in the fortunes of the mining sector driven by improving commodity prices should assist the economy to grow at 4% during 2017.

However, the high government debt at over 40% to GDP will see government continuing to cut down on spending. We are of the view that the deep spending cuts are necessary given the national debt levels and the significant reduction in the revenue outlook. We are, however, worried that the cuts, instead of targeting consumptive non-productive expenditures with limited multiplier effects, may impact infrastructure and capacity building priorities.

AcknowledgementsWe are grateful to have the continued support of Standard Bank Group to guide us on best practice and to allow us to leverage off their innovations in the banking world.

A great deal of our success relies on the interactions with our staff and our customers. We thank our customers for their support and promise to strive for excellence in customer service and to tailor our banking offering to meet the ever-changing requirements of the market through innovative products.

28

HEADING HEADING Sub heading heading continued

Financial review

The results

The SBN Holdings group profit after tax increased by 3% in 2016 to N$540 million. Loans and advances increased by 12%. The group’s return on equity decreased to 20.88% from 23.56%. The group experienced a negative JAWS ratio of 2%, partly due to significant investments in staff. This is also reflected in the cost-to-income ratio which increased from 58.34% to 59.53%.

Bryan Mandy

FINANCIAL RESULTS AND RATIOS

Change

% 2016 2015

ROE (%) (17) 20.88 23.56 Profit for the year

(N$000) 3 539 686 524 531 Tier I capital

adequacy ratio1 (6) 12.68 13.42 Total assets

(N$000) 13 27 213 048 23 992 115 Non-interest

revenue to total income 2 43.57 42.76

Credit loss ratio (4) 0.49 0.51 Cost-to-income

ratio 2 59.53 58.34

1 Excluding unappropriated profits.

SBN Holdings Limited Annual report 2016 29

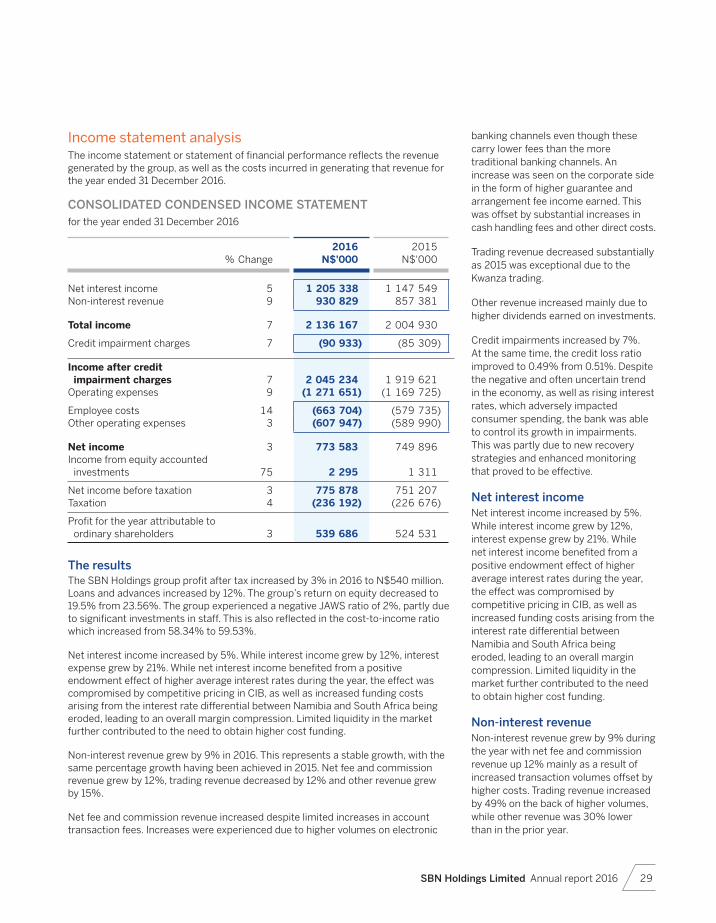

Income statement analysisThe income statement or statement of financial performance reflects the revenue generated by the group, as well as the costs incurred in generating that revenue for the year ended 31 December 2016.

CONSOLIDATED CONDENSED INCOME STATEMENT

for the year ended 31 December 2016

% Change2016

N$'0002015

N$'000

Net interest income 5 1 205 338 1 147 549Non-interest revenue 9 930 829 857 381

Total income 7 2 136 167 2 004 930

Credit impairment charges 7 (90 933) (85 309)

Income after credit impairment charges 7 2 045 234 1 919 621

Operating expenses 9 (1 271 651) (1 169 725)

Employee costs 14 (663 704) (579 735)Other operating expenses 3 (607 947) (589 990)