scaling up agricultural finance - … · some factors affecting agricultural ... farm productivity...

TRANSCRIPT

SCALING UP AGRICULTURAL FINANCE

Can Small Scale farmers be financed on commercial basis by a Financial Institution?

The Case of KCB BANK RWANDA LTD

Presentation profile

1. Rwanda’s Agricultural scene

2. Agricultural Lending

3. Value Chains as a business approach to finance

4. Addressing farmer issues

5. Success stories

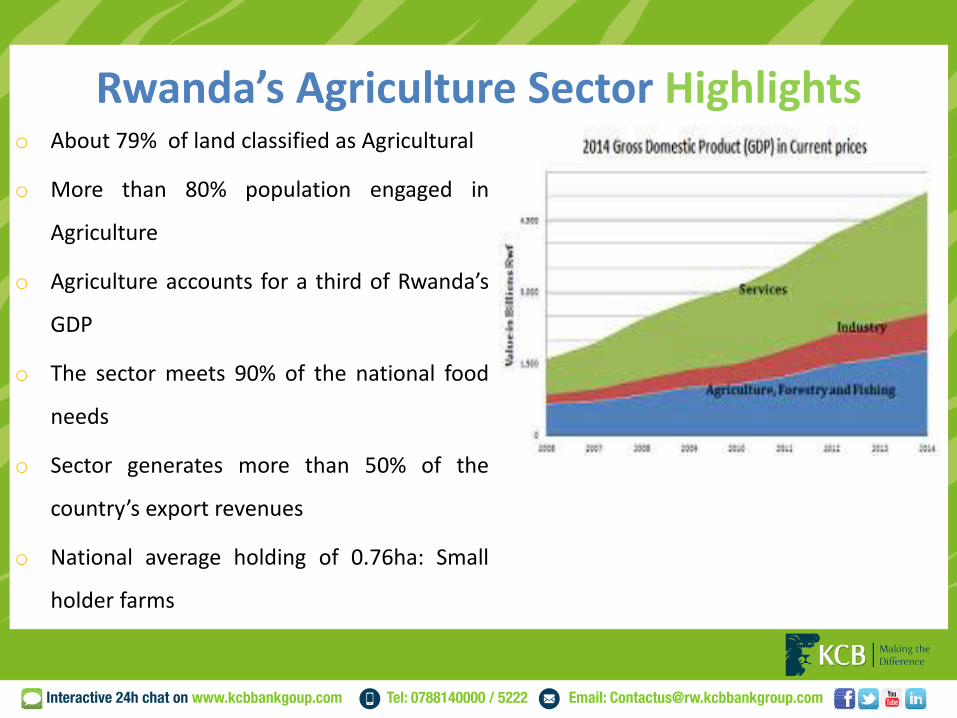

Rwanda’s Agriculture Sector Highlightso About 79% of land classified as Agricultural

o More than 80% population engaged in

Agriculture

o Agriculture accounts for a third of Rwanda’s

GDP

o The sector meets 90% of the national food

needs

o Sector generates more than 50% of the

country’s export revenues

o National average holding of 0.76ha: Small

holder farms

Sector Highlights: The future• Agriculture is expected to

grow from 5.8% to 8.5% p.a. by 2018.

• People living under primarily agriculture sector expected to reduce from 34% to 25% with focus on agro processing

• Agricultural exports expected to increase in average from 19.2% to 28% p.a. and imports to be maintained at 17% average growth

Sector Highlights: Government InitiativesAgricultural Policy: Strategic Plan for Agricultural Transformation

Currently at Phase III (2013-2017) with 4 programs.

Agriculture and Animal Resource Intensification

• Soil Erosion Control

• Irrigation and Water Management

• Agricultural Mechanization

• Soil Fertility and Management

• Agricultural Inputs Development

• Nutrition and Household Vulnerability

Research and Technology Transfer, Advisory Services

and professionalism of farming

• Research and Technology Transfer in Agricultural sector

• Extension and Proximity Services for Producers

• Farmer Cooperatives and Organizations

Institutional Development & Agricultural Cross-Cutting

Issues

• Institutional Capacity Building

• Agricultural Communication, Statistical Systems, M&E and Management Information Systems

Value Chain Development and Private Sector

Investment

• Private Sector Investment Promotion

• Development of Priority Value Chains

• Agriculture finance

• Market oriented infrastructure

Some factors favoring agricultural lending in Rwanda

o Government initiatives:

Policy and Strategy on Agricultural Finance

Agricultural Guarantee Funds

Post Harvest Infrastructures

Irrigation and Mechanization Initiatives

o New markets to explore

Large % of population in Agriculture Sector

Some factors favoring agricultural lending in Rwanda (contd.)

• Private ownership of land

• Large % of Agricultural Land to total land

• Two seasons (A & B) per year for food crops and season

C on irrigated land

Some factors affecting agricultural lending in Rwanda

o Smallholder farmers implying

low scale of production

o Weather related risks

o Quality constraints

o High transaction costs

o Lack of strong collateral for

smallholder farmers

o Lack of succession plans

o Side selling culture

o Lack of storage facilities

o Lack of Technology for small

scale farmers (Irrigation system)

o Price fluctuations

o Lack of records (Management

issues): lack of financial

information, no credit history

KCB Business Model : Agricultural value chain financing

o Partnering with different actors

within the value chain:

Agricultural inputs suppliers,

Agricultural Insurance Providers,

Technical Support Providers (technical

assistance, quality assessment),

Processors and buyers among others

KCB Business Model : Agricultural value chain financing (cont’d)

o Promoting Innovation in Agricultural Finance:

Agricultural Insurance Cover, Inventory Credit

Facility among others

o Reducing Agribusiness loan applications Turn

Around Time (TAT) to 24 hours decision.

o Applying Banking Standards: KYC, Credit files,

reporting to Credit Reference Bureau (CRB),

among others

KCB Business Model : Agricultural value chain financing (cont’d)

o Putting in place an Agribusiness

Unit and recruiting staff with

Agribusiness expertise

o Training of all staff involved in

lending on Agricultural Lending

model

Agricultural Lending to small farmers – KCB Business Model workflow

Agriculture financial need

assessment

Risk assessment and mitigation

measures

Partnership formation

Product development

The key is to identify the supply chains & integration with a large number of producers

o Agricultural inputs suppliers: work with companies which supply

seeds, fertilizers pesticides to farmers: the loan for purchasing

these inputs are directly paid to the suppliers

o Identifying farmers under cooperatives : based on the level of

management, crops, season, infrastructures available, experience

The key is to identify the supply chains & integration with a large number of producers

o Identifying services providers: Insurance companies, technical

support provider, quality assessor, among others

o Identifying the buyers of the produce: Specialized buyers at local

level (Government, Private Processors, World Food Program

among others)

Solving the small scale farmer’s issues

Solving farmers’ issues (contd.)

Client Assessment

Legally registered;

Farm Management and/ or Cooperative Management;

Experience in Agricultural operations (minimum 2 seasons)

Experience in banking and lending

Clean CRB report

Improved and certified agricultural inputs use

Market availability and price fluctuation consideration

Competitive advantage of the value chain and cooperative

Client Assessment (cont.)

Operating margins and cash flow consideration;

Agricultural knowledge capacity of management and technical

team;

Farm productivity compared to the national average within the

value chain;

Postharvest handling and storage knowledge and availability of

the storage infrastructures;

Collateral and second source of repayment;

Loan approval and monitoring process

Loan approval process:

Collection of required documents from client (Done by branch)

Loan analysis by agribusiness banker and recommendation by

branch manager

Risk assessment by credit analyst and recommendation for

approval

Approval of the facility at different level depending on the loan

limit

Loan approval and monitoring process (Cont.)

Post approval process:

Legal documentation (offer letter/ loan contract drafting)

Security Registration process;

Disbursement of the loan by disbursement unit;

Monitoring process :

Dairy monitoring of loan performance by RM;

Monthly reporting on loan portfolio performance;

Post disbursement regular visit of the farm/ business;

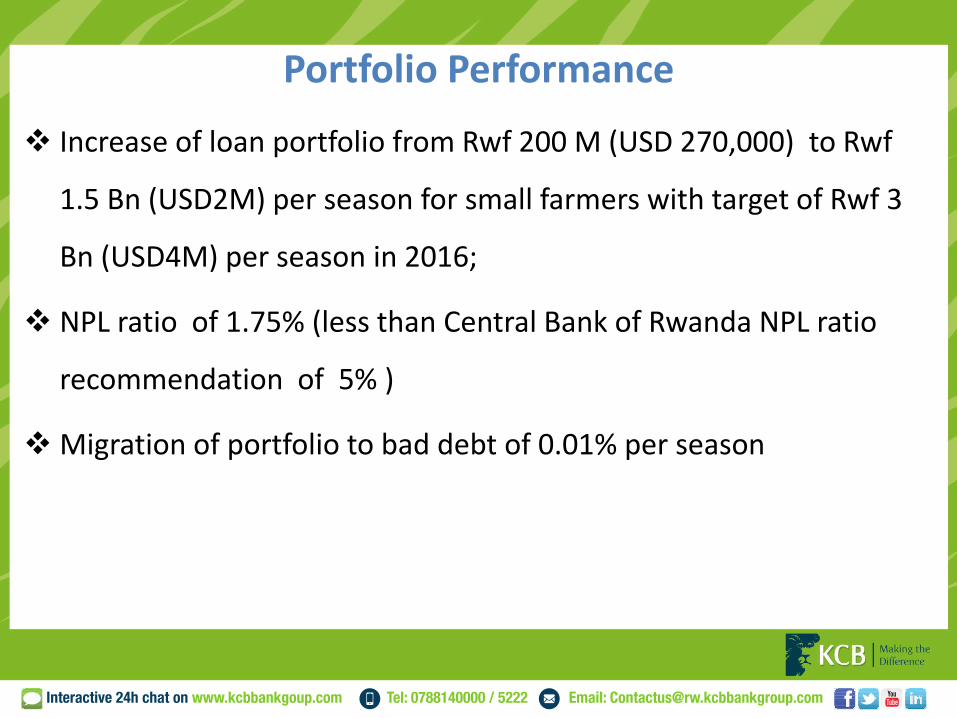

Portfolio Performance

Increase of loan portfolio from Rwf 200 M (USD 270,000) to Rwf

1.5 Bn (USD2M) per season for small farmers with target of Rwf 3

Bn (USD4M) per season in 2016;

NPL ratio of 1.75% (less than Central Bank of Rwanda NPL ratio

recommendation of 5% )

Migration of portfolio to bad debt of 0.01% per season

KCB Bank Rwanda success stories

o 28,263 smallholder farmers have received loans from KCB under

the model in Maize, beans, rice, soybeans, Irish potatoes value

chains.

o 10 partnerships in place: IFC, AFR, IFDC, RDO, BDF, RWARRI,

SPARK RWANDA, CHAI, MINAGRI, UAP Insurance.

o 5 Loans products designed: agricultural inputs financing,

Inventory credit facility, Contract finance, Invoice discounting

and investment loan facility

KCB Bank Rwanda success stories

o KCBR is the first commercial bank to introduce Inventory credit

facility in Rwandan market.

o KCBR is the first commercial bank to introduce agricultural

insurance on the Rwandan market

The Model creates value to all stakeholderso KCBR smallholder farmers loans increased from Rwf 200 M to Rwf

1.5 Bn per season in 2014 (1 USD / 750 Rwf).

o The side selling has reduced and farmers are now supplying

harvest to cooperatives.

o 61 Cooperatives have been linked to the formal markets

o Cooperatives started building their own storage facilities due to

the increase of sales and profit.

The Model creates value to all stakeholders(contd.)

o Farmers are assured of access to markets: MINAGRI, WFP, local

specialized buyers

o Farmers start doing agriculture as business on commercial basis

o Farmers gained more knowledge from service providers:

Quality of harvest improved, post harvest losses reduced

o The financial records are available to the users

o Farmers are now insured

Summary of key lessons learned Developing new products and services that better meet farmers

needs is important:

The Bank needs to have specific products targeting agricultural value chain operators as agriculture related businesses have their own specificity

Having services and products for agricultural clients is important, but not sufficient to acquire new clients:

Adequate training of staff is critical to enable them to sell loan products to agricultural clients effectively

Address issues quickly to meet customer expectation (dealing with seasonal business)

Summary of key lessons learned Lending to smallholder farmers needs intervention and support from

different stakeholders

The bank does not enough technical and financial capacity to mitigate allinvolved risks in smallholders farmers financing and the support fromstakeholders as risk mitigation service providers are critical.

Bank senior level commitment is key of agricultural finance success

Having agricultural lending strategy, policy and budget allocation is key foragricultural lending initiative success;

Government intervention and commitment to support agricultural sector is veryimportant

Government willing to promote agricultural value chain finance and theinvestments done in agricultural somehow reduced the risks to lend tothe farmers

28

Selected 11 Farmer

Cooperatives

KCB Rwanda

Partner Bank

IFC Portfolio Client

Off-taker Final Buyers

Government of Rwanda

Rwanda Development Organization

5. Technical Assistance

Advisory Services

Sponsor

UAP Rwanda

Crop Insurance

IFC Portfolio Client

3. Direct Payment

3. Direct Payment

Input Suppliers

4. Input (Seeds,

Fertilizer)

6. Maize, Soy Beans8. Payment to

Collection Account

3. Loans

8. Payment

7. Maize, Soy Beans

2. Risk Sharing Facility

Credit Line

1. Origination

Advisory Services

Rwanda Agricultural Board

Rwanda

Cooperative Agency

9. Repayment

SHOWCASE: RWANDA FARMER FINANCING FACILITY

Farmer financing facility with KCB Rwanda in

support of local farmer cooperatives that will

supply maize and soybeans to the DSM plant

through Off-take arrangements.

YES! Small Scale farmers can be

financed on commercial basis

by a financial institution?

George Odhiambo

Head of Business Development & Client Services

KCB BANK RWANDA LTD

A subsidiary of KCB BANK GROUP

www.kcbbankgroup.com

THANK YOU