scenario analysis in risk management -...

TRANSCRIPT

Bertrand K. Hassani

Scenario Analysis in Risk ManagementTheory and Practice in Finance

Scenario Analysis in Risk Management

Bertrand K. Hassani

Scenario Analysis in RiskManagementTheory and Practice in Finance

123

Dr. Bertrand K. HassaniGlobal Head of Research and

Innovation - Risk MethodologyGrupo SantanderMadrid, Spain

Associate ResearcherUniversité Paris 1 Panthéon SorbonneLabex ReFiParis, France

The opinions, ideas and approaches expressed or presented are those of the author and donot necessarily reflect Santander’s position. As a result, Santander cannot be held responsiblefor them. The values presented are just illustrations and do not represent Santander losses,exposures or risks.

ISBN 978-3-319-25054-0 ISBN 978-3-319-25056-4 (eBook)DOI 10.1007/978-3-319-25056-4

Library of Congress Control Number: 2016950567

© Springer International Publishing Switzerland 2016This work is subject to copyright. All rights are reserved by the Publisher, whether the whole or part ofthe material is concerned, specifically the rights of translation, reprinting, reuse of illustrations, recitation,broadcasting, reproduction on microfilms or in any other physical way, and transmission or informationstorage and retrieval, electronic adaptation, computer software, or by similar or dissimilar methodologynow known or hereafter developed.The use of general descriptive names, registered names, trademarks, service marks, etc. in this publicationdoes not imply, even in the absence of a specific statement, that such names are exempt from the relevantprotective laws and regulations and therefore free for general use.The publisher, the authors and the editors are safe to assume that the advice and information in this bookare believed to be true and accurate at the date of publication. Neither the publisher nor the authors orthe editors give a warranty, express or implied, with respect to the material contained herein or for anyerrors or omissions that may have been made.

Printed on acid-free paper

This Springer imprint is published by Springer NatureThe registered company is Springer International Publishing AG Switzerland

To my sunshines, Lila, Liam and Jihane

To my parents, my brother, my family, myfriends and my colleagues without whom Iwould not be where I am

To Pr. Dr. Dominique Guégan, who believedin me. . .

Preface

The objective of this book is to show that scenario analysis in financial institutionscan be addressed in various ways depending on what we would like to achieve.There is not one method better than the other; there are just methods moreappropriate in some particular situations.

I heard so many times opinionated people selecting a scenario strategy overanother because everyone was doing it; that is not the appropriate answer andmay lead to selecting an inappropriate methodology and consequently to unusableresults. Even worse, the managers may lose faith in the process and tell everyonethat scenario analysis for risk management is useless.

Therefore, in this book, I am presenting various approaches to perform scenarioanalysis; some are relying on quantitative approaches; others are more qualitative,but once again, none of them are better than another. Each of them has some prosand cons and depends on the maturity of your risk framework, the type of riskthat banks are willing to assess and manage and the information available. I triedto present them in the simplest way possible and to keep only the essence of themethodologies as in any case; eventually, the managers will have to fine-tune them,making them their own approach. I hope this book will inspire them. One of myobjectives was also to make supposedly complicated methodologies accessible toany risk managers. Indeed, these would just need to have a basic understanding ofmathematics.

Note that I implemented all the methodologies I am presenting in this book,and all the figures presented are my own. Most of them have been implementedin professional environments to answer practical issues. Therefore, I am givingsome tools for risk managers to address scenario analysis, I am providing leadsfor researchers to start proposing solutions to address them and I hope that theclear perspective of combining the methodologies will lead to future academic andprofessional developments.

vii

viii Preface

As failures of risk management related to failures of scenario analysis pro-grammes may have disastrous impacts, note that all the proceedings of this bookare going to charities to contribute to the relief of suffering people.

Global Head of Research and Innovation - Bertrand K. HassaniRisk MethodologyGrupo SantanderMadrid, Spain

Associate ResearcherUniversité Paris 1 Panthéon SorbonneLabex ReFiParis, France

Biography

Bertrand is a risk measurement and management specialist (Credit, Market, Oper-ational, Liquidity, Counterparty etc.) for SIFIs. He is also an active associateresearcher at Paris Pantheon-Sorbonne University. He wrote several articles dealingwith Risk Measures, Risk Modelling, and Risk Management. He is still studyingto obtain the D.Sc. degree (French H.D.R.). He spent two years working in theBond/Structure notes market (Eurocorporate), four years in the banking industryin a Risk Management/Modelling department (BPCE) and one year as a SeniorRisk Consultant (Aon-AGRC within Unicredit in Milan). He is currently workingfor Santander where he successively held the Head of Major Risk Managementposition (San UK), the Head of Change and Consolidated Risk Managementposition (San UK), the Global Head of Advanced and Alternative Analyticsposition (Grupo Santander) and is now Global Head of Research and Innovations(Grupo Santander) for the risk division. In this role, Bertrand aims at developingnovel approaches to measure risk (financial and non-financial) and integrating themin the decision-making process of the bank (business orientated convoluted risk

ix

x Biography

management), relying on methodologies coming from the field of data science(data mining, machine learning, frequentist statistics, A.I., etc.).

Contents

1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.1 Is this War? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.2 Scenario Planning: Why, What, Where, How, When. . . . . . . . . . . . . . 21.3 Objectives and Typology .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41.4 Scenario Pre-requirements .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61.5 Scenarios, a Living Organism . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71.6 Risk Culture . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8References .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2 Environment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112.1 The Risk Framework .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112.2 The Risk Taxonomy: A Base for Story Lines . . . . . . . . . . . . . . . . . . . . . . . 122.3 Risk Interactions and Contagion.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142.4 The Regulatory Framework .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17References .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

3 The Information Set: Feeding the Scenarios . . . . . . . . . . . . . . . . . . . . . . . . . . . . 253.1 Characterising Numeric Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

3.1.1 Moments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 283.1.2 Quantiles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 293.1.3 Dependencies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

3.2 Data Sciences . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 303.2.1 Data Mining. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 303.2.2 Machine Learning and Artificial Intelligence . . . . . . . . . . . . . 323.2.3 Common Methodologies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

References .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

4 The Consensus Approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 394.1 The Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 404.2 In Practice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

4.2.1 Pre-workshop . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 444.2.2 The Workshops . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

xi

xii Contents

4.3 For the Manager . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 464.3.1 Sponsorship .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 474.3.2 Buy-In .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 484.3.3 Validation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 484.3.4 Sign-Offs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

4.4 Alternatives and Comparison . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49References .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

5 Tilting Strategy: Using Probability Distribution Properties . . . . . . . . . . . 515.1 Theoretical Basis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

5.1.1 Distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 525.1.2 Risk Measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 565.1.3 Fitting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 585.1.4 Goodness-of-Fit Tests . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

5.2 Application . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 625.3 For the Manager: Pros and Cons . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

5.3.1 Implementation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 655.3.2 Distribution Selection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 665.3.3 Risk Measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

References .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

6 Leveraging Extreme Value Theory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 696.1 Introduction .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 696.2 The Extreme Value Framework.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

6.2.1 Fisher–Tippett Theorem .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 726.2.2 The GEV . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 726.2.3 Building the Data Set . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 746.2.4 How to Apply It? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

6.3 Summary of Results Obtained .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 776.4 Conclusion .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79References .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

7 Fault Trees and Variations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 817.1 Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 827.2 In Practice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

7.2.1 Symbols . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 837.2.2 Construction Steps . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 867.2.3 Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 887.2.4 For the Manager . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 897.2.5 Calculations: An Example . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89

7.3 Alternatives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 907.3.1 Failure Mode and Effects Analysis . . . . . . . . . . . . . . . . . . . . . . . . 917.3.2 Root Cause Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 917.3.3 Why-Because Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 927.3.4 Ishikawa’s Fishbone Diagrams. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 937.3.5 Fuzzy Logic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

References .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95

Contents xiii

8 Bayesian Networks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 978.1 Introduction .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 978.2 Theory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100

8.2.1 A Practical Focus on the Gaussian Case. . . . . . . . . . . . . . . . . . . 1038.2.2 Moving Towards an Integrated System: Learning . . . . . . . . 104

8.3 For the Managers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106References .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 108

9 Artificial Neural Network to Serve Scenario Analysis Purposes . . . . . . 1119.1 Origins . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1129.2 In Theory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1139.3 Learning Algorithms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1149.4 Application . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1169.5 For the Manager: Pros and Cons . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119References .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120

10 Forward-Looking Underlying Information: Working withTime Series . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12310.1 Introduction .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12310.2 Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124

10.2.1 Theoretical Aspects. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12510.2.2 The Models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

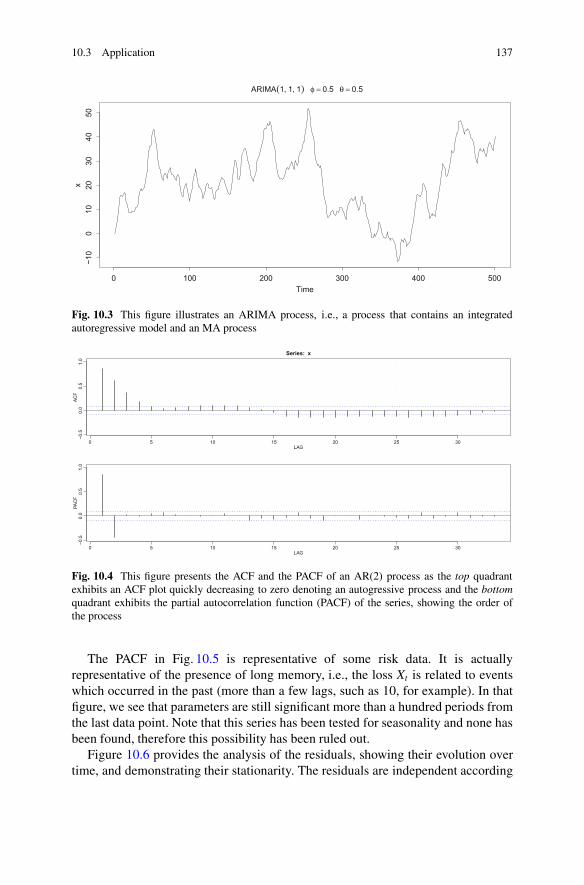

10.3 Application . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 135References .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139

11 Dependencies and Relationships Between Variables . . . . . . . . . . . . . . . . . . . 14111.1 Dependencies, Correlations and Copulas . . . . . . . . . . . . . . . . . . . . . . . . . . . 142

11.1.1 Correlations Measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14211.1.2 Regression . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14411.1.3 Copula .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 151

11.2 For the Manager . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 155References .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 157

Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 159

Chapter 1Introduction

1.1 Is this War?

Scenarios have been used for years in many areas (economics, military, aeronautics,public health, etc.) and are far from being limited to the financial industry. Scenariosare a postulated sequence or development of events, a summary of the plot of a play,including information about its stakeholders, characters, locations, scenes, weather,etc., i.e., anything that could contribute to make it more realistic. One of the keyaspects of scenario analysis is the fact that starting from one set of assumptionsit is possible to evaluate and map various outcome of a particular situation. Whilein this book we will limit ourselves to the financial industry for our applicationsand examples, it would be an extreme prejudice not to inspire ourselves fromwhat we could use from other industries in terms of methodologies, procedures orregulations.

Indeed, to illustrate the importance of scenario analysis in our world, let’sstart with famous historical examples combining geopolitics and military strategy.The greatest leaders in the history of mankind based their decisions on theoutcome of scenarios, Pearl Harbor attack was one of the outcomes of the scenarioanalysed by Commanders Mitsuo Fuchida and Minoru Genda considering thattheir objective was to make US naval forces inoperative for 6 months at least(Burbeck, 2013). Sir Winston Churchill analysed the possibility of attacking theSoviet Union with Americans and West Germans as allied after World War II(Operation Unthinkable—Lewis 2008). Scenarios are a very useful and powerfultool to analyse all potential future outcomes and prepare ourselves for them. Froma counter terrorism point of view, the protection scheme of nuclear plants fromterrorist attacks is clearly the result of a scenario analysis, for example, in Francesquadron of fighter pilots are ready to take off and intercept an airborne potentialthreat in less than 15 min. It is also really important to understand that the riskassessment resulting from a scenario analysis may result in the acceptance of thisrisk. The nuclear plant located in Fessenheim, next to the Switzerland border has

© Springer International Publishing Switzerland 2016B.K. Hassani, Scenario Analysis in Risk Management,DOI 10.1007/978-3-319-25056-4_1

1

2 1 Introduction

been built in a seismic area, but the authorities came to the conclusion that the riskwas acceptable, besides it is one of the oldest nuclear plants in France and one maythink the likelihood of a failure and age are correlated.1

In the military, most equipments are the results of either field experience orscenarios or past failure, but in many industries, contrary to the financial sector,we may not have the opportunity to wait for a failure to be able to identify an issueand fix it, and therefore learn from it as in other industries such as aeronautics orpharmaceutical if a failure occurs or a faulty product is released, people’s lives areat risk.

Now, focusing on scenario analysis within financial institutions, this one hasusually one of the following forms. The first form is stress testing (Rebonato,2010). Stress testing aims at assessing multiple outcomes resulting from adversestories of different magnitude, for instance, likely, mild and worse case scenariorelying on macroeconomic variables. Indeed, it is quite frequent to analyse aparticular situation with respect to how would macroeconomic variables evolve.The second form relates to operational risk management as prescribed in the currentregulation,2 where scenarios are required for capital calculations (Pillar I and PillarII—Rippel and Teply 2011). The recent crisis taught us that banks failing dueto extreme incidents may dramatically impact the real economy, indeed, SociétéGénérale rogue tading, a massive operational risk resulted in a massive marketrisk materialisation as all the prices went down simultaneously, in a huge lackof liquidity as the interbanking market was failing (banks were not funding eachothers) and consequently in the well-known credit crunch as banks were not fundingthe real economy, the whole occurring within the context of the subprime crisis.Impacted companies were suffering and some relatively healthy went even bankrupt.The last use of scenarios is related to general risk management. It is probably themost useful use of scenario analysis as it is not necessary a regulatory demand and assuch would only be used by risk managers to improve their risk framework removingthe pressure of a potential higher capital charge.

1.2 Scenario Planning: Why, What, Where, How, When. . .

Presenting scenario analysis in its globality and not only in the financial industry,the following paragraph presents a military scenario planning. In this book, wedraw a parallel between the scenario process in the Army and in a financialinstitution. The scenario planning as suggested in Aepli et al. (2010) is summarisedbelow. It can be broken down in 12 successive steps of equal importance and we

1The idea behind these example is neither to generate any controversy nor to feed any conspiracytheory but to refer to examples which should talk to the largest number of readers.2Note that though the regulation might change, scenarios should still be required for riskmanagement purposes.

1.2 Scenario Planning: Why, What, Where, How, When. . . 3

would recommend risk managers to keep them in mind undertaking such a process(International Institute for Environment and Development (IIED) 2009; GregoryStone and Redmer, 2006).

1. Decide on the key question to be answered by the analysis. This allows creatingthe framework for the analysis and condition the next points.

2. Set both time and scope of the analysis, i.e. place the scenario in a period oftime, define the environment and precise the condition.

3. Identify and select major stakeholders to be engaged, i.e. people at theorigination of the risk, responsible or accountable, or impacted by it.

4. Map basic trends and driving forces such as industry, economic, political,technological, legal and societal trends. Evaluate to what extent these trendsaffect the issues to be analysed.

5. Find key uncertainties, assess the presence of relationships between the drivingforces and rule out any inappropriate scenarios.

6. Group the linked forces and try to operate a reduction of the forces to the mostrelevant.

7. Identify the extreme outcomes of the driving forces. Check the consistency andthe plausibility of these ones with respect of the time frame, the scope and theenvironment of the scenario and stakeholders behaviours.

8. Define and write out the scenarios. The narrative is very important as it will bea reference for all the stakeholders, i.e., a common ground for analysis.

9. Identify research needs (e.g. data, information, elements supporting the stories,etc.).

10. Develop quantitative methods. Depending on the objectives, methodologiesmay have to be refined or developed. This is the book main focus and it providesmultiple examples, but these are not exhaustive.

11. Assess the scenarios implementing for example one of the strategies presentedin this book, such as the consensus approach.

12. Transform the outcome of the scenario analysis into key management actionsto prevent, control or mitigate the risks.

These steps are almost applicable as such to perform a reliable scenario analysis ina financial institution. None of the questions should be a priori left aside.

Remark 1.2.1 An issue to bear in mind during the scenario planning phase of theprocess which may impact the model selection and the selection of the stakeholdersis what we would refer to as the seniority bias. This is something we observedfacilitating the workshops, even if you have the best experts of a topic in theroom, the presence of a more senior person might lead to a self-censorship. Peoplemay censor themselves due to threats against them or their interests from theirline manager, shareholders, etc. Self-censor occurs when employees deliberatelydistort their contributions either to please the more senior manager or by fear of himwithout any other pressure than their own perception of the situation.

4 1 Introduction

1.3 Objectives and Typology

Now that we have presented examples of scenarios, a fundamental question needto be raised: up to what extent the scenario should be real? Indeed what afinancial institution should focus on? A science fiction type of scenario such as ameteor striking the building, except a reliable business continuity plan is not reallymanageable. Another example relates to something that already happened, and theinstitution has now good controls in place to prevent or mitigate the issue andtherefore did not suffer any incident in the past 20 years. Should it have a scenario?Obviously, these questions are both rhetorical and provocative. What is the point ofa scenario if the outcome is not manageable or is already fully controlled, we do notlearn anything from the process, it might be considered a waste of time. Indeed, it isimportant that in its scenario selection process a bank identify its immediate largestexposures, those which could have a tremendous impact in the short term, even ifthe event is assessed in the longer term, and prioritise those requiring an immediateattention.

Remark 1.3.1 The usual denomination “1 in 100 years” scenario characterises a tailevent, but there is no information about when the event may occur. Indeed, contraryto the common mistake, 1 in 100 years refers to a large magnitude not to the datethe scenario may materialise itself. Indeed, this one may occur the next day.

Scenario analysis may have a high impact on regulatory capital calculations(operational risks) but this is not the focal point of this books, scenario analysisshould be used for management thoroughly anyway. We would argue that scenarioanalysis is the purest risk management tool as if a risk materialises it is not a riskany more, in the best case, it is an incident. Consequently, contrary to people mainlydealing with the aftermath (accountant, for instance, except for what relates toprovisions), risk managers deal with exposures, i.e., a position which may ultimatelyresult in some damages for financial institutions. These may be financial losses (butnot necessarily if the risk is insured), reputational impact, etc. The most importantis that actually, a risk may never materialise in an incident. We may draw a parallelbetween the risk and a volcano. Indeed, an incident is the crystallisation of a risk, sometaphorically, it is the eruption of the volcano (especially is this one is consideredasleep). But this eruption may not engender any damages or losses if the lava is onlycoming on one side and nothing is on its path, it may even generate some positivethings as it may provide some good fertiliser. However, if the eruption results in aglowing cloud which destroys everything on its path, the impact might be dramatic.

The ultimate objective of the scenario analysis is to prevent and/or mitigate risksand losses, therefore, in a first stage, it is important to identify the risks, to makesure that controls are in place to prevent incidents, and if they still materialise,mitigate the losses. At the risk of sounding overly dramatic, it is really importantthat financial institutions follow a rigorous process as eventually, we are discussingthe protection of the consumer, the competitiveness of the bank and the security ofthe financial system.

1.3 Objectives and Typology 5

To make this book more readable and to help risk managers sorting issuesin a simple scenario taxonomy, we propose the following classification. Themost destructive risks a financial institution has to bear are those we will labelConventional Warfare, Over Confident, Black Swans, Dinosaurs and Chimera.By “conventional warfare”, we are talking about the traditional risk, those youwould face on a “Business as Usual” basis, such as credit risk and market risk.Taken independently, they are not usually leading to dramatic issues and thebank address then permanently, but when an event transforms their non-correlatedbehaviour into highly correlated one, i.e., each and every individual component failssimultaneously, they might be dramatic (and may fall in the last category). The OverConfident label refers to types of incidents which have already materialised but themagnitude was really low, or it led to a near miss therefore practitioners assumedthat their framework was functioning until we have a similar but larger incident.The Black Swan is as reference to Nassim Taleb’s book, entitled the Black Swan(Taleb, 2010). The allegory of the Black Swan was, no one could ever believe thatBlack Swans existed until someone saw one. For a financial institution it is “therisk that can never materialise in a target entity” type of scenario, but only purelack of experience made us make that judgment. The Dinosaur is the risk that theinstitution thought did not exist anymore but suddenly “comes back to life” andstomps on the financial institution. This is typically the exposure to the back bookfinancial institutions are experiencing. The last one is the Chimera, the mythologicalbeast, the one which is not supposed to exist, it is the impossible, the things that donot make sense a priori. Here, we know it can happen, we just do not believe it willsuch as the Fessenheim nuclear plant example before, a meteor striking the buildingor a rogue wave which until the middle of the twentieth century was consider asnonexistent by scientist, despite having been reported by multiple witnesses. Thedifference between the Black Swan and the Chimera types of scenarios is that theBlack Swan did exist we just did not know it, we did not even think about thepossible existence of a Black Swan, while the Chimera is not supposed to exist,we do not want to believe it can happen even if we could imagine it, as it ismythological, and we have not been able to understand the underlying phenomenonyet.

Scenarios can both find their roots in endogenous and exogenous issues. Exam-ples of endogenous risk are those due to the intrinsic way of doing business, ofcrating value, of dealing with customers, etc. Exogenous risks are those havingexternal roots such as terrorist attacks and earthquakes. The main problem withendogenous risk is that we may be able to point fingers at people if we experiencesome failures and therefore, we may have an adverse incentive as these peoplemay not want anyone to discover that there is a potential issue in their area. Whileexogenous risk, we may experience another problem, in the sense that sometimenot much can be done to control it, though awareness is still important. The humanaspect of scenario analysis briefly discussed here is really important and shouldalways be bore in mind. As if the process is not clearly explained and the peopleworking in the financial institution do not buy in then we will face a major issue, thescenarios will not be reliable as they will not be performed properly, they would do

6 1 Introduction

them because it is compulsory, but they will never try to obtain any usable outcomeas for them it is a waste of time. The first step of a good scenario process is to teachand train people on why scenarios are useful, how to deal with them, in other wordsto market the process. The objective is to embedded the process. The best evidenceof an embedded process is the transformation of a demanded “tick the box” kind ofprocess to scenarios analysis performed by business unit themselves without beingrequested to do so as it became part of their culture.

Another question which is worth addressing in the process is the moment whenwe should capture the controls already in place. Indeed, facilitating a scenarioanalysis, you will often hear the following answer to the question “do you havea risk?”, “no, we have controls in place”. To what, the manager should reply, youhave controls because you have a risk. This comes from the confusion made betweeninherent and residual risk. Indeed, the inherent risk is the one the entity faces, theone it has before putting any controls or mitigants in place. The residual risk isthe one the financial institution faces after the controls. The one that will faceeven if the mitigants are functioning. Performing a scenario analysis, it is reallyimportant working with inherent risk in a first step, otherwise our perception of therisk might be biased. Indeed, let’s assume we would rather work with the residualrisk, then your control is failing, you would never have captured the real exposure,and therefore would have assumed you were safe when you were not. Therefore,we would recommend working with the inherent risk in the first place and capturingthe impact of the control in a second stage. The inherent risk will also support theinternal process of prioritisation.

Another question arise, should scenarios be analysed independently one fromthe other or should we adopt a holistic methodology? Obviously here it not onlydepends on the quality and the availability of the information, inputs, experts, timingand feasibility, but also on the type of scenario you are interested in analysing.Indeed, if your scenario is for stress testing purposes and a contagion channel hasbeen identified between various risks, you would need to capture this phenomenonotherwise the full exposure will not be taken into account and your scenario willnot be representative of the threat. Now, if you are only working on a limited scopekind of scenarios and you only have a few weeks to do the analysis you may want toadopt an alternative strategy. Note that holistic approaches are usually highly inputconsuming.

1.4 Scenario Pre-requirements

One of the key success factors of scenario analysis is the analysis of the underlyinginputs, for instance, the data. These are analysed prior to the scenario analysis,this is the starting point to evaluate the extreme exposure. No one should everunderestimate the importance of data in scenario analysis, in both what it bringsand the limitations associated. Indeed, the information used for scenario analysis,obtained internally (losses, customer data, etc.) or externally (macroeconomicvariables, external LGD, etc.) are key to the reliability of the scenario analysis,

1.5 Scenarios, a Living Organism 7

but some major challenges may arise that could limit the use of these data andworse may mislead people owning the scenarios, i.e., responsible for evaluating theexposures and dealing with the outcomes. Some of the main issues we would needto discuss are

• Data security: It is the issue of individual privacy. While using the data we haveto be careful not to threaten the character confidential of most data.

• Data integrity: Clearly, data analysis can only be as good as the data relying upon.A key implementation challenge is integrating conflicting or redundant data fromdifferent sources. A data validation process should be undertaken. This is theprocess of ensuring that a program operates on clean, correct and useful data,checking the correctness, the meaningfulness and the security of data used asinput into the system.

• Stationarity analysis: In mathematics and statistics, a stationary process is astochastic process whose joint probability distribution does not change whenshifted in time. Consequently, moments such as mean and variance, if they exist,do not change over time and do not follow any trends. In other words, we canrely on past data to predict the future (up to certain extent).

• Technical obsolescence: The requirement we all have to store large quantity ofdata drives technological innovation in storage. This results in fast advances instorage technology. However, the technologies that used to be the best not solong ago are rapidly discarded by both suppliers and customers. Proper migrationstrategies have to be anticipated at the risk of not being able to access the dataanymore.

• Data relevance: How old should be the data? Can we assume a single horizonof analysis for all the data or depending on the question we are interested inanswering, should we use different horizons? This question is almost rhetoricalas obviously we need to use the data that are appropriate and consistent with whatwe would be interested in analysing. It also means that the quantity of data andtheir reliability depends on the possibility to use outdated data.

1.5 Scenarios, a Living Organism

It is extremely important to understand that scenario analysis is like a livingorganism. It is alive, self feeding, evolving and may become something completelydifferent from what we originally intended to achieve. It is possible to draw aparallel between a recurring scenario analysis process in a company and the theoryof evolution of Charles Darwin (up to a certain extent). Darwin’s general theorypresumes the development of life from non-life and stresses a purely naturalistic(undirected) descent with modification (Darwin, 1859). Complex creatures evolvefrom more simplistic ancestors naturally over time. These mutations are passed onto the next generation. Over time, beneficial mutations accumulate and the result isan entirely different organism. In a bank, it is the same, the mutation is embedded

8 1 Introduction

in the genetic code, as in the savana, the bank that is going to survive the longer isnot the biggest or the strongest, but the one the most likely to adapt, and scenarioallows adaptation through understanding of the environment.

Darwin’s theory of evolution is a slow gradual process. Darwin wrote, “Naturalselection acts only by taking advantage of slight successive variations; she can nevertake a great and sudden leap, but must advance by short and sure, though slowsteps” formed by numerous, successive, slight modifications. The transcription ofthe evolution into a financial institution tells us that scenarios may evolve slowly,but they will evolve as long as practices. A scenario to be plausible should capturethe largest number of impacts and interactions. As for Darwin’s theoretical startingpoint for evolution, the starting point of a scenario analysis process is always quitegross, but by digging more and more every time, learning from experience, thisheuristic process would lead to better ways of assessing the risk, better outcomes,better controls, etc.

Indeed, we usually observe that the scenario analysis process in a financialinstitution mature in parallel of the framework. The first time the process isundertaken, this one is never based on the most advanced strategy, the latestmethodologies and does not necessarily provide the most precise results. But thisphase is really important and necessary as it is the ignition phase, i.e., the onethat triggers a cultural change in terms of risk management procedure. The processwill constantly evolve towards the most appropriate strategy for the target financialinstitution as the stakeholders will own the process.

Scenario is not a box ticking process.

1.6 Risk Culture

It is widely agreed that failures of culture (Ashby et al., 2013), which permittedexcessive and uncontrolled risk-taking and a loss of focus on end customer, wereat the heart of the financial crisis. The cultural dimensions of risk-taking andcontrol in financial organisations have been widely discussed, arguing that, forall the many formal frameworks and technical modelling expertise of modernfinancial risk management, risk-taking behaviour and a questionable ethics weremisunderstood by individuals, companies and regulators. The growing interest infinancial institution risk culture since 2008 has been symptomatic of a desire toreconnect risk-taking, related management and appropriate return. The couple risk-return which somehow has been forgotten came back not as a couple but as a singlepolymorphic organism in which risk and return are indivisible elements.

When risk culture change programs were being led by risk functions the reshap-ing of the organisational risk management was at the centre of these programs. Riskculture is a way of framing and perceiving risk issues in an organisation. In addition,risk culture is itself a composite of a number of interrelated factors involving manytrade-offs. Risk culture is not static but dynamic, a continuous process which repeatsand renews itself constantly. The risk culture is permanently subject to shocks that

1.6 Risk Culture 9

lead to permanent questioning. The informal aspect is probably the most important,i.e., small behaviours and habits which in the aggregate constitute the state ofrisk culture. Note that risk culture can be taken in a more general sense, as riskculture is what makes us fasten our seat-belts in our cars. Risk culture is usuallytransorganisational, and different risk cultures may be found within organisations oracross the financial industry.

The most fundamental issue at stake in the risk culture debate is an organisationsself-awareness of its balance between risk-taking and control. It is clear thatmany organisational actors prior to the financial crisis were either unaware of,or indifferent to, the risk profile of the organisation as a whole as soon as thereturn generated was appropriate or sufficient according to their own standard.Indeed, inefficient control functions and revenue-generating functions consideredmore important created an unbalanced relationship leading to the disaster we know.The risk appetite framework now helps articulating these relationships with moreclarity.

The risk culture discussion shows the desire to make risk and risk management amore prominent feature of organisational decision-making and governance, withthe embedded idea to move towards a more convoluted risk framework, i.e., aframework in which the risk department is engaged before rather than after abusiness decision is made. The usual structure of the risk management frameworkcurrently relies on

• a three Lines of Defence backbone• risk oversight units and capabilities and• increased attention to risk information consolidation and aggregation.

Risk representatives engage directly with the businesses, acting as trusted advisors;they usually propose risk training programs and general awareness-raising activities.Naturally this is only possible if the risk function is credible. The former approachinvolves acting on the capabilities of the risk function and in developing greaterbusiness fluency and credibility. Combining the independence of the second lineof defence and the construction of partnerships might be perceived as inconsistent,though one may argue that an effective supervision requires proper explanations andclear statements of the expectations to the supervisee. Consequently, they need tohave good relationships and regular interactions (structured or ad-hoc).

According to Ashby et al. (2013), two kinds of attitude have been observedtowards interactions: enthusiastic and realistic. The former are developing toolson their own, and are investing time and resource in building informal internalnetworks. Realists have a tendency to think that too much interaction can inhibitdecision-making. Realists have more respect for the lines of defense models thanenthusiasts who continually work across first and second lines. Limits and relatedrisk management policies and rules unintentionally become a system in their ownright. The impact of history and collective memory of past incidents should not beunderestimated as this is a constituting part of the culture of the company and maydrive future risk management behaviours.

10 1 Introduction

Regulation has undoubtedly been a big driver of risk culture change programmes.Though a lot of organisations were frustrated about the weigh of the regulatorydemand, they had no choice but to cooperate and most of them sooner or latteraccepted the new regulatory climate and worked with it more actively; however, itis still unclear if the extent of the regulatory footprint on the business has been fullyunderstood.

Behaviour alteration related to cultural change requires repositioning customerservice at the centre of financial institutions activities, and good behaviour shouldbe incentivised for faster changes. Martial artists say that it requires 1000 repetitionsof a single move to make it a reflex, and 10,000 thousands to change it. Therefore itis critical to adjust behaviours before it becomes a reflex.

Scenario analysis will impact the risk culture within a financial institution as itwill change the perception of some risks and will consequently lead to the creation,the amendment or enhancement of controls, leading themselves to the reinforcementof the risk culture. As mentioned previously, scenarios will evolve and the riskculture will evolve simultaneously. We believe that the current three line of defencemodel will slowly fade away as the empowerment of the first line will grow.

References

Aepli, P., Summerfield, E., & Ribaux, O. (2010). Decision making in policing: Operations andmanagement. Lausanne: EPFL Press.

Ashby, S., Palermo, T., & Power, M. (2013). Risk culture in financial organisations - a researchreport. London: London School of Economics.

Burbeck, J. (2013). Pearl Harbor - a World War II summary. http://www.wtj.com/articles/pearl_harbor/.

Darwin, C. (1859). On the origin of species by means of natural selection, or the preservation offavoured races in the struggle for life (1st ed.). London: John Murray.

Gregory Stone, A., & Redmer, T. A. O. (2006). The case study approach to scenario planning.Journal of Practical Consulting, 1(1), 7–18.

International Institute for Environment and Development (IIED). (2009). In Profiles of tools andtactics for environmental mainstreaming. Scenario planning, No. 9.

Lewis, J. (2008). Changing direction: British military planning for post-war strategic defence (2nded.). London: Routledge.

Rebonato, R. (2010). Coherent stress testing: A Bayesian approach to the analysis of financialstress. London: Wiley.

Rippel, M., & Teply, P. (2011). Operational risk - scenario analysis. Prague Economic Paper, 1,23–39.

Taleb, N. (2010). The black swan: The impact of highly improbable (2nd ed.). New York: RandomHouse and Penguin.

Chapter 2Environment

2.1 The Risk Framework

As introduced in the previous chapter, risk management is a central element ofbanking—integrating risk management practices into processes, systems and cultureis key. As a proactive partner to senior management, risk management value lies insupporting and challenging them to align the business control environment with thebank’s strategy by measuring and mitigating risk exposure and therefore contribut-ing to optimal return for stakeholders. For instance, some banks invested heavilyin understanding customer behaviour through new systems initially designed forfraud detection, which is now being leveraged beyond compliance to address moreeffective customer service.

The risk department of an organisation keeps its people up-to-date on problemsthat have happened to other financial institutions, allowing it to take a more proactiveapproach. As mentioned previously, the risk framework of a financial institution isusually split into three layers, usually referred to as three lines of defense. The firstline which is in the business is supposed to manage the risks, the second line issupposed to control the risks and the third line characterised by the audit departmentis supposed to oversee. The target is to embed the risk framework, i.e., empower thefirst line of defence to identify, assess, manage, report, etc. Ultimately, each andevery person working in the bank is a risk manager, and any piece of data is a riskdata.

Contrary to what the latest regulatory documents suggest, there is no one-size-fits-all approach to risk management—as every company has a framework specificto its own internal operating environment. A bank should aim for integrated riskframeworks and models supporting behavioural improvements. Understanding therisks should mechanically lead to a better decision-making process and to betterperformance, i.e., better or more efficient returns (in the portfolio theory sense—Markowitz 1952).

© Springer International Publishing Switzerland 2016B.K. Hassani, Scenario Analysis in Risk Management,DOI 10.1007/978-3-319-25056-4_2

11

12 2 Environment

Banks’ risk strategy drives the management framework as it sets the tone forrisk appetite, policies, controls and “business as usual” risk management processes.Policies should be efficiently and effectively cascaded at all levels as long as acrossthe entity to ensure a homogeneous risk management.

The risk governance is the process by which the Board of Directors setsobjectives, oversees the framework and the management execution. A successfulrisk strategy is equivalent to the risk being embedded at every level of a financialinstitution. Governance sets the precedence for strategy, structure and execution. Anideal risk management process ensures that organisational behaviour is consistentwith its risk appetite or tolerance, i.e., the risk an institution is willing to take togenerate a particular return. In other words, the risk appetite has two components:risk and return. Through the risk appetite process, we see that risk managementclearly informs business decisions.

In financial institutions, it is necessary to evaluate the risk management effective-ness regularly to ensure its quality in the long term, and to test stressed situationsto ensure its reliability when extreme incidents materialise. Here, we realise thatscenario analysis is inherent to risk management as we are talking about situationswhich never materialised.

The appropriate risk management execution requires risk measurement toolsrelying on the information obtained through risk control self-assessments, datacollection, etc., to better replicate the company risk profile. Indeed, appropriate riskmitigation and internal control procedures are established in the first line such thatthe risk is mitigated. “Key Risk Indicators” are established to ensure timely warningis received prior to the occurrence of an event (COSO, 2004).

2.2 The Risk Taxonomy: A Base for Story Lines

In this section we present the main risks to which scenario analysis is usually or canbe applied in financial institutions. This list is non-exhaustive but gives a good ideaof the task to be accomplished.

Starting with credit risk, this one is defined as the risk of default on a debtthat may arise from a borrower failing to make contractual payments, such as theprincipal and/ or the interests. The loss may be total or partial. Credit risk can itselfbe split as follows:

• Credit default risk is the risk of loss arising from a debtor being unable to pay itsdebt. For example, if the debtor is more than 90 days past due on any materialcredit obligation. A potential story line would be an increase in the probability ofdefault of a signature due to a decrease in the profit generated.

• Concentration risk is the risk associated with a single type of counterparty(signature or industry) having the potential to produce losses large enough tolead to the failure of the financial institution. An example of story line would be

2.2 The Risk Taxonomy: A Base for Story Lines 13

a breach in concentration appetite due to a position taken by the target entity forthe sake of another entity of the same group.

• Country risk is the risk of loss arising from a sovereign state freezing foreigncurrency payments or defaulting on its obligations. The relationship betweenthis risk, macroeconomics and countries stability is non-negligible. Political riskanalysis lies at the intersection between politics and business, and it deals withthe probability that political decisions, events or conditions significantly affectthe profitability of a business actor or the expected value of a given economicaction. An acceptable story line would be the bank has invested in a country inwhich the government has changed and has nationalised some of the companies.

Market risk is the risk of a loss in positions arising from movements in marketprices. This one can be split between,

• Equity risk: the risk associated with changes in stock or stock index prices.• Interest rate risk: the risk associated with changes in interest rates.• Currency risk: the risk associated with changes in foreign exchange rates.• Commodity risk: the risk associated with changes in commodity prices.• Margining risk results from uncertain future cash outflows due to margin calls

covering adverse value changes of a given position.

A potential story line would be a simultaneous drop in all indexes, rates and currencyof a country due to a sudden decrease of GDP.

Liquidity risk is the risk that given a certain period of time, a particular financialasset cannot be traded quickly enough without impacting the market price. Astory line could be a portfolio of structured notes that was performing correctlyis suddenly crashing as the index on which they have been built is dropping, butthe structured notes have no market and therefore the products can only be sold at ahuge loss. It might make more sense to analyse the liquidity risk at the micro level(portfolio level). Regarding this risk of illiquidity at the macro level, considering thata bank is transforming the money with a short duration such as savings into moneywith a longer one through lending, a bank is operating a maturity transformation.This ends up in banks having an unfavourable liquidity position as they do nothave access to the money they lent while the money they owe to customer can bewithdrawn at any time on demand. Through “asset and liability management”, banksare managing this mismatch, however, and we cannot emphasise enough this point,this implies that banks are structurally illiquid (Guégan and Hassani, 2015).

Operational risk is defined as the risk of loss resulting from inadequate or failedinternal processes, people and systems or from external events. This definitionincludes legal risk, but excludes strategic and reputational risk (BCBS, 2004). Italso includes other classes of risk, such as fraud, security, privacy protection, cyberrisks, physical, environmental risks and currently one of the most dramatic, conductrisk. Contrary to other risks such as those related to credit or market, operationalrisks are usually not willingly incurred nor are they revenue driven (i.e. they arenot resulting from a voluntary position), they are not necessarily diversifiable, butthey are manageable. An example of story line would be the occurrence of a roguetrading on the “delta one” desk on which a trader took an illegal position. Note that

14 2 Environment

for some bank this might not be a scenario as it happened, but for others it might bean interesting case to test their resilience.

Financial institutions misconduct or perception of misconduct leads to con-duct risk. Indeed, the terminology “conduct risk” gathers various processes andbehaviours which fall into operational risk Basel category 4 (Clients, Productsand Business Practices), but goes beyond as it generally implies a non-negligiblereputational risk. Conduct risk can lead to huge losses, usually resulting fromcompensations, fines or remediation costs and the reputational impact (see below)might non negligible. Contrary to other operational risks, conduct risk is connectedto the activity of the financial institution, i.e. the way the business is driven.

Legal risk is a component of operational risk. It is the risk of loss which isprimarily caused by a defective transaction, a claim, a change in law, an inadequatemanagement of non-contractual rights, a failure to meet non-contractual obligationsamong other things (McCormick, 2011). Some may define it as any incidentimplying a litigation.

Model risk is the risk of loss resulting from using models to make decisions(Hassani, 2015). Understanding this risk partly as probability and partly as impactprovides insight into other risk measured. A potential story line would be amodel not properly adjusted due to a paradigm shift in the market leading to aninappropriate hedge of some positions.

Reputational risk is a risk of loss resulting from damages to a firm’s reputationin terms of revenue, operating costs, capital or regulatory costs, or destruction ofshareholder value, resulting from an adverse or potentially criminal event even if thecompany is not found guilty. In that case, a good reputational risk scenario would bea loss of income due to the discovery that the target entity is funding illegal activitiesin a banned country. Once again, for some banks this might not be as scenario as theincident already materialised, but the lesson learnt might be useful for others.

The systemic risk defines itself as the risk of collapse of an entire financialsystem, as opposed to the risk associated with the failure of one of its componentwithout jeopardising the entire system. The financial system instability engenderedpotentially caused or exacerbated by idiosyncratic events or conditions in financialintermediaries may lead to the destruction of the system (Piatetsky-Shapiro, 2011).The materialisation of a systemic risk implies the presence of interdependenciesin the financial system, i.e. the failure of a single entity may trigger a cascadingfailure, which could potentially bankrupt or bring down the entire system or market(Schwarcz, 2008).

2.3 Risk Interactions and Contagion

It is not possible to discuss scenario analysis without addressing contagion effects.Indeed, it is not always possible or appropriate to deal with a particular risk andanalysing it in silo. It is important to capture the impact of a risk over another, i.e.,a spread or a spillover effect.

2.3 Risk Interactions and Contagion 15

In fact this aspect is too often left aside when it should be at the centre of thetopic. Combined effect due to contagion can lead to larger losses than the sum of theimpact of each components taken separately. Consequently, capturing the contagioneffect between the risks may be a first way of tackling systemic risks.

Originally, financial contagion referred to the spread of market disturbances fromone country to the other. Financial contagion is a natural risk for countries whosefinancial systems are integrated in international financial markets as obviously whatoccurs in a country would mechanically impact the other in a way or another. Theimpact is usually proportional to the incident, in other words, the larger the issue,the larger the impact on the other countries belonging to the same system unlesssome mitigants are in place to at least confine the smaller exposures. The contagionphenomenon is usually one of the main components explaining that a crisis is notcontained and may pass across borders and affect an entire region of the globe.

Financial contagion may occur at any level of a particular economy and may betriggered by various things. Note that lately, banks have been at the conjunction of adramatic contagion process (subprime crisis), but inappropriate political decisionmay lead to even larger issues. At the domestic level, usually the failure of adomestic bank or financial intermediary triggers a transmission when it defaults oninterbank liabilities and sells assets in a fire sale, thereby undermining confidencein similar banks. International financial contagion, which happens in both advancedand developing economies, is the transmission of a financial crisis across financialmarkets to directly and indirectly connected economies. However, in today’sfinancial system, due to both cross-regional and cross-border operations of banks,financial contagion usually happens simultaneously at the domestic level and acrossborders.

Financial contagion usually generates financial volatility and may damage theeconomy of countries. There are several branches of classifications that explainthe mechanism of financial contagion, which are spillover effects and financialcrisis that are caused by the influence of the four agents’ behaviour. These aregovernments, financial institutions, investors and borrowers (Dornbusch et al., 2000)

The first branch, spillover effects, can be seen as a negative externality. Spillovereffects are also known as fundamental-based contagion. These effects can occurglobally, i.e., affecting several countries simultaneously, or regionally, only impact-ing adjacent countries. The larger the countries, the more global the effect is thegeneral rule. Conversely, the smaller countries are those triggering regional effects.Though some debates arose regarding the difference between co-movements andcontagion, here we will state that if what happen in a particular location directly orindirectly impact the situation in another geographical region, with a time lag1 then,we should refer to it as contagion.

At the micro level, from a risk management perspective, contagion should beconsidered when the materialisation of a first risk (say operational risk) triggers thematerialisation of subsequent risk (for instance, market or credit). This is typically

1This one might be extremely short.

16 2 Environment

what happened in Société Générale rogue trading issue as briefly discussed in theprevious chapter.

From a macroeconomic point of view, contagion effects have repercussions onan international scale transmitted through channels such as trade links, competitivedevaluations and financial links. “A financial crisis in one country can lead to directfinancial effects, including reductions in trade credits, foreign direct investment, andother capital flows abroad”. Financial links come from globalisation since countriestry to be more economically integrated with global financial markets. Many authorshave analysed financial contagions. Allen and Gale (2000) and Lagunoff andSchreft (2001) analyse financial contagion as a result of linkages among financialintermediaries.

Trade links are another type of shock that has its similarities to common shocksand financial links. These types of shocks are more focused on its integrationcausing local impacts. Kaminsky and Reinhart (2000) document the evidence thattrade links in goods and services and exposure to a common creditor can explainearlier crises clusters, not only the debt crisis of the early 1980s and 1990s, but alsothe observed historical pattern of contagion.

Irrational phenomenon might also cause financial contagion. Co-movementsare considered irrational when there is no global shock triggering and interde-pendence channeling. The cause is related to one of the four agents’ behaviourspresented earlier. Contagion causes are increased risk aversion, lack of confidenceand financial fears. Transmission channel can be through typical correlations orliquidation processes (i.e. sell in one country to fund a position in another) (Kingand Wadhwani, 1990; Calvo, 2004).

Remark 2.3.1 Investor’s behaviour seems to be one of the biggest issues that canimpact a country’s financial system.

So to summarise, a contagion may be caused by:

1. Irrational co-movements related to crowed psychology (Shiller, 1984; Kirman,1993)

2. Rational but excessive co-movements3. Liquidity problems4. Information asymmetry and coordination problems5. Shift of equilibrium6. Change in the international financial system, or in the rules of the game7. Geographic factors or neighbourhood effect (De Gregorio and Valdes, 2001)8. The developments of sophisticated financial products, such as credit default

swaps and collateralised debt obligations which spread the exposure across theworld (sub-prime crisis).

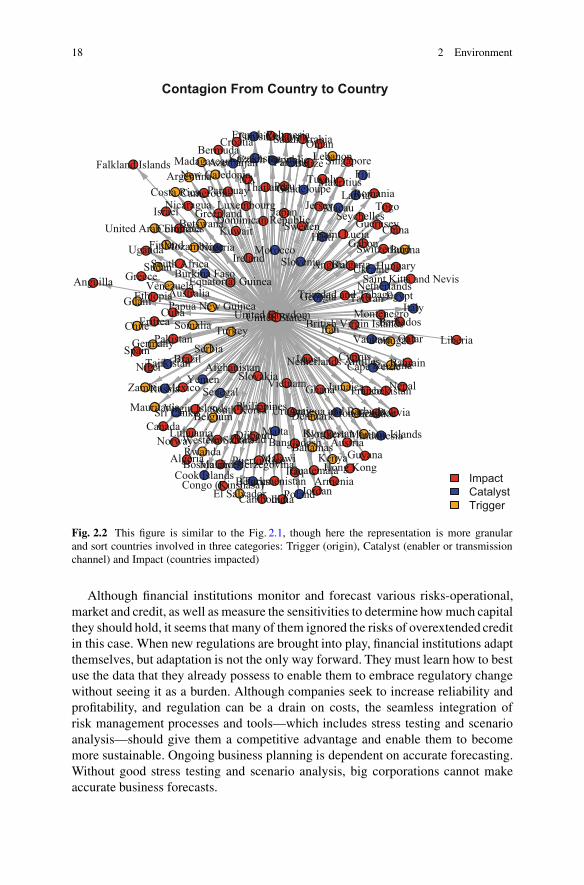

Capturing interactions and contagion effects leads to analysing financial crises.The term financial crisis refers to a variety of situations resulting in a loss ofpaper wealth, which may ultimately affect the real economy. An interesting wayof representing financial contagion can be done extending models used to representepidemics as illustrated by Figs. 2.1 and 2.2.

2.4 The Regulatory Framework 17

Financial Crisis: Contagion From A Country To Another

ll

ll ll

ll

llllll

ll

ll

ll

llllllll

llllll

ll

ll

ll

ll

ll

ll

ll

ll

ll

llll

ll

ll

ll

ll

ll

llll

ll

ll

llll

ll

llll

ll

ll

ll

ll

ll

ll

ll

llllll

ll

ll

llllll

ll

ll

ll

llll

llll

ll

ll

llll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

llll ll

ll

ll

ll

ll

ll

llll

llll

ll

ll

llll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

llll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

llll

ll

ll

ll

ll

ll

llll

ll

ll

ll

ll

ll

ll

ll

llll

llll

ll

ll

llll

ll

ll

ll

llll

ll

llll ll

llll

ll

ll

ll

llll

ll

ll

ll

ll

ll

ll

ll

ll

ll ll

ll

ll llll

llll

ll

ll

ll llll

ll

ll

llllll

ll

ll

ll

ll

ll ll

llll

ll ll

ll

ll

ll

llllllll

llll

ll

llll

ll

ll

llll

ll

USAUKFranceChinaBrazil

Fig. 2.1 In order to graphically represent a financial contagion, I inspired myself from a modelcreated to represent the way epidemies move from a specific geographic region to another(Oganisian, 2015)

2.4 The Regulatory Framework

In this section, we will briefly discuss the regulatory framework surroundingscenario analysis. Indeed, scenario analysis can be found in multiple regulatoryprocesses, such as stress testing and operational risk management and not only fromthe financial industry. As it has been introduced in the previous sections, we believethat some precision regarding stress testing might be useful to understand the scopeof the pieces of regulations below.

The stress-testing term generally refers to examining how a company’s financesrespond to an extreme scenario. The stress-testing process is important for prudentbusiness management, as it looks at the “what if” scenarios companies needto explore to determine their vulnerabilities. Since the early 1990s, catastrophemodelling, which is a form of scenario analysis for providing insight into themagnitude and probabilities of potential business disasters, has become increasinglysophisticated. Regulators globally are increasingly encouraging the use of stresstesting to evaluate capital adequacy (Quagliariello, 2009).

18 2 Environment

Contagion From Country to Country

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

llll

ll

ll

ll

ll

ll

llll

ll

ll

ll

ll

ll

ll

llll

llll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

llll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

llll

ll

ll

ll

ll

ll

ll

ll

ll

ll

llll

ll

ll

ll

ll

ll ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

ll

llll

ll

ll

ll

Afghanistan

Algeria

Angola

Antigua and Barbuda

Argentina

Armenia

Australia

Austria

Azerbaijan

Bahamas

Bahrain

Bangladesh

Barbados

Belarus

Belgium

Belize

Bermuda

Bolivia

Bosnia and Herzegovina

Botswana

Brazil

British Virgin Islands

BulgariaBurkina Faso

Burma

Cambodia

Cameroon

Canada

Cape Verde

Chile

ChinaColombia

Congo (Kinshasa)

Cook Islands

Costa Rica

Croatia

Cuba

Cyprus

Czech Republic

Denmark

Djibouti

Dominican Republic

Ecuador

Egypt

El Salvador

Equatorial Guinea

Eritrea

Ethiopia

Fiji

Finland

France

French Polynesia

Gabon

Georgia

Germany

Ghana

Greece

Greenland

Guadeloupe

Guam

Guatemala

Guernsey

Guyana

Haiti

Honduras

Hong Kong

Hungary

India

Indonesia

Iran

Iraq

Ireland

Israel

Italy

Jamaica

JapanJersey

Jordan

Kazakhstan

Kenya

Kuwait

Kyrgyzstan

Laos

Latvia

Lebanon

Liberia

Lithuania

Luxembourg Macau

Madagascar

Malawi

Malaysia

Maldives

Malta

Mauritania

Mauritius

Mexico

Montenegro

MoroccoMozambique

NA

Nepal

Netherlands Antilles

Netherlands

New Caledonia

New Zealand

Nicaragua

Niger

Nigeria

Northern Mariana IslandsNorway

Oman

Pakistan

Panama

Papua New Guinea

ParaguayPeru

Philippines

Poland

Portugal

Puerto Rico

Qatar

Romania

Russia

Rwanda

Saint Kitts and Nevis

Saint Lucia

Saudi Arabia

Senegal

Serbia

Seychelles

Singapore

Slovakia

Slovenia

Somalia

South Africa

South Korea

Spain

Sri Lanka

Sudan

Sweden

Switzerland

Taiwan

Tajikistan Tanzania

Thailand

Togo

Trinidad and Tobago

Tunisia

Turkey

Turkmenistan

Tuvalu

Uganda

Ukraine

United Arab Emirates

United Kingdom

Uruguay

Uzbekistan

Vanuatu

Venezuela

Vietnam

Virgin Islands

Western Sahara

YemenZambia

United States

Anguilla

Falkland Islands

ImpactCatalystTrigger

Fig. 2.2 This figure is similar to the Fig. 2.1, though here the representation is more granularand sort countries involved in three categories: Trigger (origin), Catalyst (enabler or transmissionchannel) and Impact (countries impacted)

Although financial institutions monitor and forecast various risks-operational,market and credit, as well as measure the sensitivities to determine how much capitalthey should hold, it seems that many of them ignored the risks of overextended creditin this case. When new regulations are brought into play, financial institutions adaptthemselves, but adaptation is not the only way forward. They must learn how to bestuse the data that they already possess to enable them to embrace regulatory changewithout seeing it as a burden. Although companies seek to increase reliability andprofitability, and regulation can be a drain on costs, the seamless integration ofrisk management processes and tools—which includes stress testing and scenarioanalysis—should give them a competitive advantage and enable them to becomemore sustainable. Ongoing business planning is dependent on accurate forecasting.Without good stress testing and scenario analysis, big corporations cannot makeaccurate business forecasts.

2.4 The Regulatory Framework 19

One approach is to view the business from a portfolio perspective, with capitalmanagement, liquidity management and financial performance integrated into theprocess. Comprehensive stress testing and scenario analysis must take into accountall risk factors, including credit, market, liquidity, operational, funding, interest,foreign exchange and trading risks. To these must be added operational risks due toinadequate systems and controls, insurance risk (including catastrophes), businessrisk factors (including interest rate, securitisation and residual risks), concentrationrisk, high impact low-probability events, cyclicality and capital planning.

In the following paragraphs, we extract quotes from multiple regulatory docu-ments or international associations discussing scenario analysis requests to empha-sise how important the process is considered. We analysed documents from multiplecountries and multiple industries. These documents are also used to give someperspectives and illustrate the relationships between scenario analysis, stress testingand risk management.

In IAA (2013), the International Actuarial Association points out the differencesbetween scenario analysis and stress testing: “A scenario is a possible futureenvironment, either at a point in time or over a period of time. A projection ofthe effects of a scenario over the time period studied can either address a particularfirm or an entire industry or national economy. To determine the relevant aspects ofthis situation to consider, one or more events or changes in circumstances may beforecast, possibly through identification or simulation of several risk factors, oftenover multiple time periods. The effect of these events or changes in circumstancesin a scenario can be generated from a shock to the system resulting from a suddenchange in a single variable or risk factor. Scenarios can also be complex, involvingchanges to and interactions among many factors over time, perhaps generated by aset of cascading events. It can be helpful in scenario analysis to provide a narrative(story) behind the scenario, including the risks (events) that generated the scenario.Because the future is uncertain, there are many possible scenarios. In additionthere may be a range of financial effects on a firm arising from each scenario. Theprojection of the financial effects during a selected scenario will likely differ fromthose seen using the modeler’s best expectation of the way the current state of theworld is most likely to evolve. Nevertheless, an analysis of alternative scenarios canprovide useful information to involved stakeholders. While the study of the effectof likely scenarios is useful for business planning and for the estimation of expectedprofits or losses, it is not useful for assessing the impact of rare and/or catastrophicfuture events, or even moderately adverse scenarios. A scenario with significant orunexpected adverse consequences is referred to as a stress scenario.”

“A stress test is a projection of the financial condition of a firm or economyunder a specific set of severely adverse conditions that may be the result of severalrisk factors over several time periods with severe consequences that can extendover months or years. Alternatively, it might be just one risk factor and be shortin duration. The likelihood of the scenario underlying a stress test has been referredto as extreme but plausible.”

20 2 Environment