scenario models and sensitivity analysis in operational risk

TRANSCRIPT

COMPG007:OperationalRiskMeasurementforFinancialInstitutions

Coursework

ScenarioModelsandSensitivityAnalysisinOperationalRisk

Lecturer:DrArianeChapelle

TeamMember:RuixinBao,YangLi,HanlinYue

2016.12

2

Content1.Introduction...........................................................................................................3

1.1ResearchObjective.........................................................................................31.2LiteratureReview...........................................................................................41.3ResearchProcedure.......................................................................................4

2.ScenariosGeneration.............................................................................................52.1ScenarioI–AssetMisappropriation...............................................................52.2ScenarioII–DatalossbyCyberAttack..........................................................92.3AggregatedScenario....................................................................................11

3.SensitivityAnalysis...............................................................................................143.1SensitivityanalysisforScenarioI..................................................................143.2SensitivityanalysisforScenarioII.................................................................213.3SensitivityAnalysisforAggregatedScenario................................................25

4.AlternativeAdjustmentonLossMeasureQuantile.............................................264.1IntroductiontoClusterAnalysis...................................................................264.2ApplicationonAdjustmentofScenarioResult.............................................274.3ImportantMeaningtoLossMeasureQuantile............................................27

5.Conclusion............................................................................................................285.1Discussionofstrategicoptions.....................................................................285.2LimitationandImprovement........................................................................29

6.Reference.............................................................................................................297.Appendix..............................................................................................................30

3

1.Introduction

Thepurposeofthispaperistocreate,analyseandgeneratereliablescenariodataforoperationalrisk(OR) events in a bank and to provide efficient strategies regarding the improvement ofoperationalriskmanagementinordertoassistinthepreventionoffuturerisks.Sincethescarceof the essential data in these eventswith ‘high severity and low frequency’when aggregatingbank’slosses,scenarioapproachismostappropriatemethodtobeabletofillthegapsofourtotallosses distribution, especially in the tail. Effective scenario modelling could help the financialinstitutionstounderstandhowaparticularoperationalriskeventhappened,whatcauseit,andwhat’sthepossibleimpactsofit.Scenariosensitivityanalysiscouldalsohelpthedecisionmakertofindthekeyfactorswhenthelossoccursandinspirethemtogeneratemostefficientcontrolstopreventtheirinstitutionsfromfuturelosses.

At this paper, we focus on modelling and sensitivity testing of two cases including assetmisappropriation and cyber-attack since these two events donate huge contributions in lossdistributionsinabank.Bothofthemhavecharacteristicslikehighseveritylowfrequency,whichare obviously main targets of scenario analysis. Moreover, sensitivity analysis for these twoscenarios and combined scenario also be used as the method to explore most sensitive andessential riskdrivers.Next, clustermethod isapplied toadjustquantilesbygroupingdata intosubsetsofdataregardingtheseverityofORlosses.Basedontheresultwehaveobtained;strategicoptionscanbeprovidedtomanagersinthefutureoperationalriskmanagementasforthesetwoORevents.

1.1ResearchObjective

Asfarasweknow,thereisstillnostandardmethodforscenariogenerationandaggregationsincetheexistenceofdifferencesinvariousOReventsandbusinessenvironment.Hence,it’smeaningfultoexplorethemoreefficientprocessandmethodologyatthissectionaimingtosupportdecisionmakers by showing the sensitive factors at scenario cases and estimating the sufficient andappropriatecapitalrequirementforpreventingthebankfromfuturerisks.Here,thisresearchistoapplyacademicconceptsandmethodologiesofoperationalriskmanagementandassessmentespeciallyscenarioapproachintotherealisticcaseinabank.Theresultofthisresearchcanbedirectly used in banks as the models to analyse their operational losses from assetmisappropriation and cyber-attack. Based on scenario approach and cluster method, theappropriatecapitalrequirementcanbecalculatedasoperationallossesinthefollowingyears.Ofcourse, some additional conditions should be considered every year regarding the changes ofexternalfinancialenvironmentandinternalbusinessstructure.Wedobelievethatthisresearchisapplicable in current global financial circumstance and it could contribute on robustness ofscenariomodelling throughsolidconsiderationsofdetails in thiseventandtargetorganisationconstruction.

4

1.2LiteratureReview

Academics and practitioners have proposed various multiple-scenario analyses to treatuncertaintiesinthefutureofbusinessorganizationssincethe1970s[14].Sincetheexternallocalandglobalenvironmentareladenwithuncertainchanges,itisdifficulttodetectpotentialtrends.Hence scenario analysis is worth by advocating the generations of alternative pictures of theexternal environment’s future[2]. There is no doubt that scenario analysis has increasingattractiveness tomanagers [3][4].Generatingscenarioshasvariousmethodologieswhichcanbefoundinliterature[4-10].

Forinstance,Ringland[10]illustratesthatmajorityofcompaniesshehassurveyedapplyapproachnamedasPierreWackIntuitiveLogics,whichcreatedbyformerShellgroupplannerPierreWack.This approach focuses on constructing a comprehensible and credible set of situations of theforthcomingtotestbusinessplansorprojectsasa‘windtunnel’bytheencouragementofpublicdebateorimprovementofcoherence.Duringthepastfewdecades,thethinkingthatShellusedtodealwithscenarioshasspreadouttootherorganizationsandinstitutionssuchasSRIandGBN[10].Later,thisShellapproachandGodet’sapproacharecomparedbyBarbieriMasiniandMedinaVasquez[13].

Ringland[10] also introduces other organizations and their methods constructing scenariosincluding ‘Battelle Institute (BASICS), the Copenhagen Institute for Future Studies (the futuresgame),theEuropeanCommission(theShapingFactors–ShapingActors),theFrenchSchool(Godetapproach:MICMAC), the Futures Group (the Fundamental PlanningMethod), Global BusinessNetwork (scenariodevelopmentbyusingPeterSchwartz’smethodology),NortheastConsultingResources(theFutureMappingMethod)andStanfordResearchInstitute(Scenario-BasedStrategyDevelopment)’.Inthispaper,scenarioprocessisadjustedbasedonbankstructure,targetevents,andallabovethepreviousscenarioapproachesexperiences.

1.3ResearchProcedureTheresearchprocessisbasedonthebasicscenarioprocessasfollowingsteps[2][11][12]:Step1:IdentifyfocalissuesforourbankStep2:Mainforcesinthelocalcircumstanceandinternalandexternalbusinessenvironment Step3:DrivingkeyriskdriversandforcesStep4:Rankingfactorsbyuncertaintyandimportance Step5:DrawingscenariosflowchartinreasonableandlogicalwayStep6:MaterializingthescenariosandaggregatingscenariosStep7:Sensitivityanalysis Step8:ClustermethodtogenerateStep9:ImplicationsforstrategyStep10:DiscussthestrategicoptionsStep11:Settletheimplementationplan

5

The objective is to observe and analyse sensitivities of scenario cases based on suitableassumptionssummarizedfromempiricalevidence.TheSwissCheeseModelcanbeusedtobuildscenario modelling after finding each events’ exposures, occurrences, and impacts. ThroughMontoCarlomethod,thelossdistributionscanbegeneratedduringayear,andcombinedscenariolossdistributioncanbeobtainedthroughaggregationtechniqueasthebenchmarkingofcapitalrequirement.

Inthispaper,twoindividualscenariosandonecombinedscenariodistributionsaregeneratedforOReventsassetmisappropriationanddatalossfromcyber-attack.Afterinputtingthenecessaryparametersbasedonbank’sinformationandexperts’opinions,MonteCarlossimulationisusedtogeneratetheVaRineachscenario.Next,VaRquantilescanbecorrectbyclustermethodologytoproducemoresuitableVaRquantilesbasedontheseverityofORlosses.Decisionmakerscancitethisresearchresultasreliableandessentialsuggestionsforoperationalriskmanagementfortheirbank.

2.ScenariosGeneration

2.1ScenarioI–AssetMisappropriation

2.1.1AssetMisappropriationdefinitionAssetmisappropriationfraudistheassetlostifpeoplewhoareentrustedtomanagetheassetsoforganizationstealfromit.Thisfraudbehaviorusuallyhappensduetothirdpartiesoremployeesin an organization abuse their position to obtain access for stealing cash, cash equivalents,companydataor intellectualproperty,whicharevital forbusinessrunningforanorganization.Hence,thistypeoperationalriskshouldbemodelledandanalysedappropriately,especiallyunderthecasethatextremelyscarceofrealdataduetoprivacyofthisissueandstigmaoforganizationandnegativeimpactofpublicimage.Thistypeofinternalfraudcanattributetocompanydirectors,or itsemployees,oranyoneelseentrusted toholdandmanage theassetsand interestsofanorganization.Modelling,analysing,anddiscoveringthemostefficientscenariomethodologyisthemainpurposeofthispaperinordertoobtainadeeperunderstandingofthiskindoffraudandproviderealisticsolvingmethodstoavoid,stopandremedythiskindofissues.

2.1.2ScenarioExplanationandAssumptions

Normally,assetmisappropriationfraudcanbethefraudulentbehaviorincluding: i. Embezzlementwhereaccountshavebeenfalsifiedorfakeinvoiceshavebeenmade.ii. Deceptionbyemployeesinsidebank,falseexpensestatementsiii. Payment frauds where payrolls have been fictive or diverted, or inexistent clients or

employeeshavebeencreated.iv. Datatheftv. Intellectualpropertystealing

6

Inthisscenario,thetargetobjectistheassetmisappropriationwithinamediumsizebankbranch.Basedonbank’sbasicinformationandstructure,somereasonableassumptionscanbeproposedatthisstageasfollows.

• Themostpossibleassetstypes inthisbankcanbestolencovercreditnotes,vouchers,companydataandintellectualproperty.

• Bankhas2000employees,andwecouldsimplifierallstaffinto5differenttypespositionsincludingheadofabankandvice-presidents(20)with10%,managersanddirectors(180)with10%,senioranalyst(600)with5%,junioranalyst(1200)with5%accordingtovalueofaccesstheyholdinabank.

• Generally, the average probability of internal fraud happens inside bankwhich is 5%.Basedonthe levelofprocessesand internalsystemsandcontrols, thisprobabilitycanmoveonordown.Itisslightlydifferentforcriminalprobabilityindifferentlevelssuchasthe head of a bank and vice-presidents with 10% criminal probability, managers anddirectorswith10%,senioranalystwith5%,junioranalystwith5%accordingtovalueofaccesstheyholdinabank.

• The amount of asset can be stolen are different with various positions and it can bemeasuredasarandomprocesswhichfollowsnormaldistributionswithdifferentmeanand(variance).Forinstance,headofabankandvice-presidentsstealaround1000-unitasset with variance (300), managers and directors may access about 100-unit withvariance(30),seniorassociatescancontrolnearly20-unitwithvariance (6),and junioranalystonlycouldobtainnear10-unititemswithvariance(3).

• If employees what to misappropriate bank’s asset under their authority, they coulddirectlyaccesscertainvolumesuchasheadofabankandvice-presidents(level4)couldaccess100%amountofasset,managersanddirectors(level3)cancontrol90%,senioranalyst(level2)couldapproach75%,andjunioranalyst(level1)canaccess50%accordingtonumberofentrancestheyholdinabank.

• ifanemployeewantstoembezzlebankassets,thisemployeeneedspermissionfromhisorhersuperiorstocompletethisfraudulentbehaviour.Accordingtoexpertswithinthisbank, thepossibilities that superiors are cheated successfully through fakedocumentswithprobability50%thatjunioranalystobtainspermitfromtheirmanagers,similarlywithprobability25%managersanddirectorscouldfraudsuccessfully,andwithprobability10%thatheadandvice-presidentsstealassetsfrombank.

• Regardingtothe levelofemployees,theseverityofthis issuecanbemeasuredwithabankandvice-presidents ×1,728,managersanddirectors ×1.44,senioranalyst ×1.2,andjunioranalyst ×1.

Oncethishappens,banksshouldadaptimmediatereactionsandreportitintoactionfraud.Sinceiffraudstersarenottackled,theseopportunisticone-offfraudscanbecomesystemicandspreadoutwithinbankandfraudstersmaythinktheirbehaviorsareacceptable,whichformsanegativecompanycultureoftheftandfraud.

2.1.3AssetMisappropriationFlowchart

7

Inthisscenario,themostpossiblemissedatourbankunderassetmisappropriationcanbedivideinto four types such as credit notes, vouchers, bank data and intellectual property. All assetmisappropriationcanattribute to two isolatedcases involvingexpense fiddlingoranemployeelyingabouthisorherqualificationstogetajob.Inthiscase,differenttypesofemployees’positionsareconsideredasdifferentoccurrenceswhichareeasytocalculatethetotallossbasedontheirlevelofaccessandvalueofassetstheycouldobtain.Attheend,theimpactcanbeusedtocalculatethetotallossasthefollowingformula.Here,wemeasurereputationlossbasedonseverityofthisevent.

𝑳𝒐𝒔𝒔 = 𝑽𝒍𝒐𝒔𝒔 ∗ 𝑽𝒂𝒎𝒐𝒖𝒏𝒕 ∗ 𝑺𝒆𝒗𝒆𝒓𝒊𝒕𝒚

Afteranalysingexposure,occurrenceandimpactofassetmisappropriation,wecouldusetheSwissCheeseModel(CumulativeActEffect)toapplypreventative(P),detective(D),andcorrective(C)controls to reduce the possibility of this issue happens, control the effect of this event, andmitigatetheconsequencesofthisevent. Here, different controls can be initialized as the quantitative values according to the expert’ssuggestionsandhistoricaldataasfollowing:

• P1:VetemployeesbyCVandreferencescouldreduceinitialcriminalprobability• P2-Implementawhistleblowingpolicy• P3-Imposeclearsegregationofduties• P4-Controlaccesstobuildingsandsystems• D1-Checkinginvoicesandrelateddocuments• D2:Internalauditcoulddetectthiseventwithprobability98%.• C1:Theinsuranceproportionsaredifferentforvariouslevelofemployeessuchasabank

andvice-presidents 0%,managersanddirectors 70%,senioranalyst 50%,andjunioranalyst 0%.

• C2:Tacklerelevantemployeescouldreducetheseverityofthisissue

Expusure

CreditNotes

Vouchers

BankData

Intellectualproperty

Occurrence

HeadandVice-

presidents

ManagersandDirectors

SeniorAssociate

JuniorAnalyst

Impact

Valueofloss

Amountofloss

Reputationloss

8

2.1.4Result

Let’sapplyMonteCarlotosimulatethisscenarioinordertoobtainreliabledatatoanalysethisevent.Formakingsuretheaccuracyoftheresult,thisprocessisrepeatedfor10000times,whichshowsmorereasonableandrealisticresultscomparedwith2000timesand5000times.InputtingalltheparametrisesandusingtheabovearithmetictogetthefollowingresultofVaR($):

Plot1:SimulationResultofScenarioI–AssetMisappropriation

Bytryingtoapplydifferentdistributiontypestofitourdata,wefindthatGeneralizedExtremeValuefitsdataverywell,anditmakessensessinceassetmisappropriationcanbetreatedastheextremeevents.ByExtremeValueTheorem(EVT),GeneralizedExtremeValue(GEV)distribution

P1:VetemployeesbyCVandreferences

P2:Implementawhistleblowing

policy

P3:Controlaccessto

buildingsandsystems

P4:Imposeclearsegregationof

duties

Scenario:AssetMisappropriation

D1:Checkinginvoicesand

relateddocuments

D2:InternalAudit

C1:Insuranceandbackup

C2:Tacklerelevant

employees

25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

13783.10 22268.45 41949.64 118382.76 210907.22 302527.28

9

isanormalwaytomeasuretailloss,especiallyforscenariocase.Fromthesimulationresult,wecanfindthattheoverallVaRdistributionisroughlyalognormaldistribution,whichmightfitreality.Wecantreatitasanacceptableresult.

EstimatevaluesforGEVdistribution’sparameters,mean,andvarianceasfollows:

Loglikelihood Mean Variance k sigma mu

-112685 44682.1 Inf 0.657664 11172.5 17407.7

Fromabovefigure,oneimportantcharacteristicofassetmisappropriationisthatonceithappensandwillcourselargelossforabank.Althoughthetrustbetweenbankandemployeesisessential,somestrategiesoughttobeadaptedtostopthiskindofissuesattheverybeginningtomakesureitwon’tmakeahugeimpactforbank.GeneralizedExtremeValueFittingisthemostappropriatefittingmethodinthiscase.Obviously,thisfigurescanbetreatedasLognormaldistribution,whichmakessenseinreallife.

2.2ScenarioII–DatalossbyCyberAttack

2.2.1Significanceofexploringdatalossbycyberattack

Cyber-attacksareadvancedpersistentmenaces,whichtargetcompanysecretsinordertocancostcompaniesahugeamountofmoneylossandcouldevenputthemoutofbusiness.Therefore,it’svaluabletomodelandanalysethe losscausedbycyber-attacks.Normally,hackers infiltrateaninstitution’ssystemoutofoneoftwoaims:cyberespionageordatasabotage. Inthisscenario,datasabotageishighlightedespeciallydatalosscausedbyhacker’sinfiltrateatbank.Theemphasisof this scenario is to simulate how hackers insinuate into bank’s network system and destroyessentialdata,andwhatdetectionsabankcouldapplytoprotecttheirdataandminimizelosses.

2.2.2scenarioanalysisflowchart

Assumptions:• Thetotalvolumeofdataatthisbankis10000units• Therearethreefirewallsatthisbankwithdifferentsecuritylevels,dataallocations,anddata

significance.• There are only two types of data including client’s information (50%) and management

information(50%).Usually,bankhasbackupforallclients’information,butsometimestheymayforgettorecordsomeclients’informationbecauseofomittingoffulfillinbackupstorageor negligence of related staff.Majority ofmanagement informationmay not be copied atbackup.

• Networkengineerscheckthewholesystemonceanhour,however,frequencyofcheckingcanberecognizedastheabilityofengineers,whichmeansthatmorefrequentofcheckingmorestrongcapabilityofanengineeris.Athere,itcanbesupposedthathackersalmostsurelycanbefoundiftheyinfiltrateatthesametimethatengineerschecksystem.

10

2.2.3Scenarioprocess

Basedonassumptionsofthisscenario,MonteCarlotechniqueisappliedtosimulatecyber-attacksduringayearandgeneratedatainordertocomputeVaR(ValueatRisk)andfindthedistributionofloss.Formakingsuretheaccuracyofthismodel,MonteCarlowasrepeated10000times.

Let’sstartwithahackertriestoinfiltratebank’ssystemandhackerneedstopassthreefirewallswithdifferentsecuritylevels,datavalue,anddatadistributionsasfollows.

a. Hackersneedtospend5minutestoinfiltratethefirstfirewallandobtain5%datavalued10dollarsperunits,however,eachhackerscouldpassfirstfirewallwithprobability50%.

b. Hackersneedtospend15minutestoinfiltratethesecondfirewallandobtain10%datavalued20dollarsperunits,andeachhackercouldpassthesecondfirewallwithprobability25%.

c. Hackersneedtospend45minutestoinfiltratethethirdfirewallandobtain85%datavalued50dollarsperunits,howevereachhackercouldpassfirstfirewallwithprobability5%.

After passing three firewalls, a hacker could obtain 5%data perminute for downloading it ordestroying it. Once engineers check the system, hacker stops destroying data immediately.However,thedatahasbeendestroyedwhichcan’trecoverimmediately,whichwillcausedirectlossofbank.Hence,thelosscanbecalculatedbytimingtimetodetect(Time),datavalue(Vadata),anddatavolume(Voldata).

𝑳𝒐𝒔𝒔 = 𝑻𝒊𝒎𝒆×𝑽𝒂𝒅𝒂𝒕𝒂×𝑽𝒐𝒍𝒅𝒂𝒕𝒂

2.2.4Result

DatalossunderCyber-attacks

ExposureClient’sInformation

Managementinformation

Impact

PC.1Fire

wall1:5

0%

pass,5%datavol

Scenario:Cyber-attacks

D.C.1Engineers

Valueofdata

Volumeofdata

Timetodetect

PC.2Fire

wall2:2

5%

pass,10%

datavol

PC.3Fire

wall3:

5%pass,85%

data

D.C.2Backup

11

ByrunningMonteCarlomethodthroughMatLab,VaRvaluesarecomputedfordifferentquantiles,whichismeaningfultoprovidescenariodatainordertocombineitwithinternallossdata,externallossdatafordifferentbusinesslinesatbank.Thenbroadoperationallossatbankcanbecalculated.

Plot2:SimulationResultofScenarioII–datalossbycyberattack

After trying Lognormal, Generalized Lognormal, and Generalized Extreme Value (GEV)distributionstofitourdata,GEVperformswellinthiscyber-attackscenario.ThefollowingresultshowsthefittingofGEVdistributionforourscenario.

Fromthesimulationresult,wecanfindthattheoverallVaRdistributionisroughlya lognormaldistribution,whichmightfitreality.Wecantreatitasanacceptableresult.

FollowingsarethevalueforparametersforfittingGEVdistributions:Loglikelihood Mean Variance k sigma mu

-103520 32427.5 6.81508e+07 -0.0122104 6538.51 28731.5

2.3AggregatedScenario

2.3.1MeaningofCombinationofTwoScenarios

Applyingourscenariodatawithanaimatincorporationintocapital,aggregatinglossesofthesedifferentscenariosisthekeypartforobtainingbank’stotaloperationallosses.Ingeneral,all80(10eventtypesX8businesslines)operationalriskcategorieswouldbemeasured.Thefirststepistoconsiderdifferentcombinationsofvariousscenariosbyusingdependencygraphorscenariocorrelationmatrix.Atthispaper,theaggregationofthesetwoscenarios isconsideredbyusingvar-covmatrixmethodsinceassetmisappropriationandcyber-attackarethekeyoperationalrisk

25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

26932.00 31143.42 36216.00 48334.67 59349.45 76068.35

12

events. The objective is to explore the relationship between total loss distribution and twoindividual lossdistribution throughapplyingscenarioaggregationmethodology.By focusingonkeyriskexposuresandassessingthedependenciesbetweenscenarios,theregulatorycapitalofbotheventscanbecalculatedtomeetrequirementofpreventingourbankfromoperationalrisklosses.

2.3.2Dependencyanalysis

Theinteractionpartofthesetwoscenariosisthesameobjectbankdata.Consideringbankdatalostbycyber-attack,thismaybecausedbythebothexternalandinternalfraudsters.Forinstance,someinternalemployeesmaysellinternalaccessofessentialdatatoexternalfraudsterstostealcompany assets. As for specifically interacted terms, two pairs are found as highly includingdependentpotentialCriminalinScenario1withcheckingfrequencyinscenario2,andinsuranceandbackupinscenario1withbackupinscenario2.Asforotherelementsinbothscenarios,theycanbedealtasidenticallyindependent,sincethecorrelationsbetweenthemcanbeignoredoutoflowdependentorindependentrelationships.

Forouraggregatedscenario,theconnectionoftheindividualscenarioisthecorrelatedparameters.From the previous parameters discussed above, it shows that the correlated parameter isfollowing.

Scenario1 Scenario2 Correlation

A ProbabilityofPotential“Criminal”inP1 CheckingFrequency High

B InsuranceandbackupproportioninC1 BackupProportion Median

ForpairA,theprobabilityofpotentialcriminalreflectstheoverallqualityleveloftheemployees,whilecheckingfrequencyreflectsthetechnologyleveloftheengineer.Bothofthesereflectthequalityofinstitution’semployee.

ForpairB,theproportionofinsuranceandbackupinscenario1includethebackupofdata.Dataalsocouldbeimportantassetwhichneedstobeprotected.Sothebackupofdataisincludedinboth scenarios. Once the data in scenario 2 recover, part of C1 also should be recovered (orinsured).

2.3.3AggregationMethod

Fromaboveanalysis,twoscenarioscanbedealtwithcorrelationmatrixsincetheyhavesomemainfactorswhicharecorrelatedwitheachother.However,consideringtheseveralparametersusedintwoscenarios,onlyafewofthemarecorrelated.Thecorrelatedrelationshipisnotthatobvious.Herethecorrelatedparameteroftwoscenarioscanbesimplysettledas0.3.

Byvar-covmatrixmethod,thefollowingformulaisusedtocalculatetheaggregatedloss.

𝑋L ∙ Σ ∙ 𝑋

Where 𝑋 is the vector of the loss, Σ is the correlatedmatrix. Then, we adjust this for two-scenariossituation.Theformulaisintheformoffollowing.

13

𝐿PQPRS =𝑆U𝑆V

𝜌UU 𝜌UV𝜌VU 𝜌VV

𝑆U 𝑆V

UV

This formula is given in the ‘’MillimanResearchReport:AggregationofRisks andAllocationofCapital”.[15]

Where 𝑆U and 𝑆V arethelossfromScenario1andScenario2respectively,

and 𝜌UV = 𝜌VU = 0.3 resultingfromexperts’opinionsorhistoricallossdistributions.

𝜌UU = 𝜌VV = 1 whichisbecauseeveryrandomvariableiscompletelycorrelatedtoitself.

2.3.4Results

ApplyingMonteCarlomethodology forabove-aggregatedscenario,VaRcanbegeneratedafterrunning10000timesM-Cmethods.Thealgorithmissimilartoscenario1;similarly,GEVfitsourdatawellinthissectionsinceit’sstillthecombinationofextremeeventlosses.

Plot3:SimulationResultofCombinedScenarios

Also,GEVperformswellinthisscenario.Parameters,mean,andvarianceforGEVdistributionareestimatedasfollows:

Loglikelihood Mean Variance k sigma mu

-114376 57520.1 4.59793e+09 0.423088 14972.3 38246.2

Our finding is the following. Comparing three histogram plot, to get the distribution ofaggregatedscenario,thedistributionofscenario1shifttorightalittlebybeingaffectedbythedistributionofscenario2.

25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

33734.71 43380.94 63110.38 140655.30 235615.27 333344.57

14

3.SensitivityAnalysisSomechangeonthenecessarycontrolanddifferentparametriccanbechangedtoobservetheimpactonVaR.ThentheimportanceofthesecontrolmethodsandparametriccanbeprioritiseddependingonassortedVaR,whichmighthelpthemanagertohaveagoodcontrolontheriskofrelativescenarios.Inordertohaveagoodversiontotherealsituationofloss,herewerecalculate25%VaR, 50%VaR, 75%VaR, 95%VaR, 99%VaR and 99.9%VaR to compare andmainly focus on50%VaR and 99.9%VaR This could help decision makers to understand the expected andunexpectedlosslevel.Ineachtable,thegraylinewouldbetheoriginalvaluessetting.

3.1SensitivityanalysisforScenarioI

3.1.1P1-VetemployeesbyCVandreferences

The“VetemployeesbyCVandreferences” isacontrolmethodduringtherecruitmentprocessandemployeetraining.Herewesetaprobabilitytorepresenttheprobabilityofeveryemployeemightwanttohavesuch“criminal”behavior.Combinedwiththeoverallstaffnumber,thenumberofpotential“criminal”arebinomialdistribution.Throughstrictrecruitmentandcareertraining,thepossibilityofpotential‘theft’coulddecrease.Hereweadjustthisvalueandgetthefollowingtable.

ProbabilityofPotential“Criminal” VaR

Analyst Associate DirectorsVice-

presidents25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

0.05 0.05 0.025 0.025 5331.20 9679.31 22463.20 74212.06 187905.30 251974.99

0.1 0.1 0.05 0.05 13783.10 22268.45 41949.64 118382.76 210907.22 302527.28

0.2 0.2 0.1 0.1 31358.74 47146.27 75410.93 182585.70 268775.28 432655.92

0.3 0.3 0.15 0.15 49975.73 73195.94 108119.85 227406.16 317244.38 432344.15

0.1 0.1 0.05 0.05 13783.10 22268.45 41949.64 118382.76 210907.22 302527.28

0.05 0.1 0.05 0.05 11915.89 20135.48 40328.27 124702.50 205327.38 267028.34

0.1 0.05 0.05 0.05 12742.31 21427.96 41775.47 117471.95 216375.04 288731.09

0.1 0.1 0.025 0.05 11695.91 19724.78 40345.43 122966.52 204077.74 347431.20

0.1 0.1 0.05 0.025 10769.72 15193.14 26137.63 72223.46 185688.72 272214.32

Fromthefirstsetof thetable,itcanbedetectedthathigherprobabilityofpotential“criminal”shouldleadtomoreloss.Forthesecondsetofthetable,followingplotcanillustratethechanges.

15

Ifonlyonelevelisstrictlycontrolled,thelossdecreasesinthedifferentdegree.Bothonexpectedlossandextremelosspointofview,theconclusionisobvious.Strictlycontrolthe“HeadandVice-presidents”levelfromassetmisappropriationisthemostefficientwaytocontroltheloss.

3.1.2P2-Implementawhistleblowingpolicy

In“Implementawhistleblowingpolicy”control,itcanbeassumedthatifthereisawhistleblowingpolicy,thewhistleblowingcouldonlyhappenwhentheemployeehasaccesstotherelativeasset.Thisshouldmakesensebecauseonlyotheremployeewhohavethesameaccesslevelcandisclosethe“criminal”.Tomakethemodelclear,settingthepossibilityofbeingdisclosedbythesamelevelemployee is 0.5. Once being disclosed, the loss should be 0. Then the loss can be comparedbetweenwithandwithoutthiscontrol.

Disclosed

probability25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

NoControl 19619.21 29618.54 53995.88 178867.91 246059.11 371722.37

0.25 16779.74 25913.66 47422.27 157204.22 231346.46 338667.38

0.5 13783.10 22268.45 41949.64 118382.76 210907.22 302527.28

0.75 10991.09 18582.81 36765.00 82775.73 179818.56 256146.46

Fromthetable,itisobviousthatthecorrelationbetweendisclosedprobabilityandlossisnegative.Thisalsomakessenseinmanagement,whichiswhistleblowingmore,losslower.

3.1.3P3-Imposeclearsegregationofduties

Incorporationmanagement,segregationofdutiesisalwaysnecessary.Consideringsecurityfactor,theemployeeinthecertaindepartmentshouldhavenoaccesstotheassetwhichhavenorelationtohisduty.Inthismodel,ifthis“Imposeclearsegregationofduties”exist,everyemployeeonlyhasaccessto80%ofalltheassetathisaccesslevel.However,thetoplevelisnotaffectedbythis

controlcondition.

NoLevelControl

ControlJuniorAnalyst

ControlSenior

Associate

ControlManagers&Directors

ControlHead&Vice-

presidents

99.9%VaR 302527.28 267028.34 288731.09 347431.20 272214.32

50%VaR 22268.45 20135.48 21427.96 19724.78 15193.14

0.00

80000.00

160000.00

240000.00

320000.00

400000.00

10000.00

13000.00

16000.00

19000.00

22000.00

25000.00

16

Trans-departmentAsset 25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

0.4 12908.76 21278.66 41080.52 117088.34 210221.36 301523.66

0.6 13351.52 21782.61 41466.08 117592.98 210578.02 302022.50

0.8 13783.10 22268.45 41949.64 118382.76 210907.22 302527.28

No Control 14222.78 22704.57 42397.68 118984.80 211220.30 302998.81

Fromtheplot,havingcontrolontrans-departmentaccessisnotaneffectivewayforpreventhugeloss.Andithassomeeffectsoncontrollingtheexpectedloss.

3.1.4P4-Controlaccesstobuildingsandsystems

Controllingaccess isacommonwaybothforcorporationmanagementandsecurity inmodernbusinessmanagement.Inthismodel,allemployeescanbeseparatedinto4level.Thehigherlevelstaffhavemoreaccessandthevalueoftheassetheaccessestoishigher.High-levelstaff’saccesscoverslow-levelstaff’s.However,ifthepotential“criminal”stafftargetonthehigherlevelassetswhichhehasnoaccessto.Forexample,todothis,thestaffneedtogetthepermitorsignaturefromhigherlevel.Thereiscertainpossibilitytogethigheraccess.Consideringtheuniversalityofthiscontrol,here it is treatedasanecessaryway forprotectingassetandwillnotassumethiscontroldisappear.However,thepossibilitiesofgettinghigheraccessareadjustedtoseetheVaRchanging.

LowerAccessProbability VaR1->2 2->3 3->4 25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

0.5 0.25 0.1 13783.10 22268.45 41949.64 118382.76 210907.22 302527.28

0.25 0.25 0.1 12751.61 21241.60 40958.12 117211.00 209653.17 301148.42

0.5 0.125 0.1 13332.93 21823.25 41435.27 117963.40 210747.79 302040.43

0.5 0.25 0.05 13672.26 22050.67 41792.86 118314.18 210907.22 302527.28

0.4 0.6 0.8 NoControl

99.9%VaR 301523.66 302022.50 302527.28 302998.81

50%VaR 21278.66 21782.61 22268.45 22704.57

300500.00

301000.00

301500.00

302000.00

302500.00

303000.00

303500.00

20500.00

21000.00

21500.00

22000.00

22500.00

23000.00

17

Fromtheplot,it iseasytoobservethatpartwhichshouldstrictlycontrolisbottomcross-level.Strictlycontrollingthiscouldbringdownthelosseffectively.Inotherwords,theprocessofcross-levelauthorizationshouldbedesignedwell,especiallyonthebottomlevel.Besides,authorizationtothetoplevelisnotthatimportantwhichcouldnotreducetoomuchloss.

2.1.5D1-Checkinginvoicesandrelateddocuments

Once asset misappropriation happens, checking invoices and related documents also couldprevent loss.Forexample,thedailyormomentaryreviewcouldfindouttheunusualsituation.Oncediscovery,therelativeaccountcanbelockedtopreventloss.Theassumptionismadethatassetmisappropriationforallcross-levelmisappropriationmightbechecked.Theprobabilityissetas 0.5 if assetmisappropriation could notbepreventeddue to “checking invoices and relateddocuments”control.Ifthiscontrolisnotbeingusedorfailure,theincreasingofVaRcanbeshowedinthiscase.

Prevent

probability25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

0.25 9323.02 14158.38 23769.44 100787.35 199441.42 293501.83

0.5 13783.10 22268.45 41949.64 118382.76 210907.22 302527.28

0.75 18213.83 30380.83 60060.16 144409.18 225844.52 323583.66

NoControl 22558.54 38510.17 78060.97 170365.08 250599.46 343463.46

Thepreventprobabilityhigher,thelosshigher.Itcanbedescribedashighersupervision, lowerloss.

Or,iflightercontrolistaken,whichmeansthatonlycheckcross-levelmisappropriationischecked,whichisfromhigherleveltolowerlevel,orfromlowertohigher.Tworesultscanbecomparedasfollows.

Base Control1->2 Control2->3 Control3->4

99.9%VaR 302527.28 301148.42 302040.43 302527.28

50%VaR 22268.45 21241.60 21823.25 22050.67

300000.00

300500.00

301000.00

301500.00

302000.00

302500.00

303000.00

20600.00

20800.00

21000.00

21200.00

21400.00

21600.00

21800.00

22000.00

22200.00

22400.00

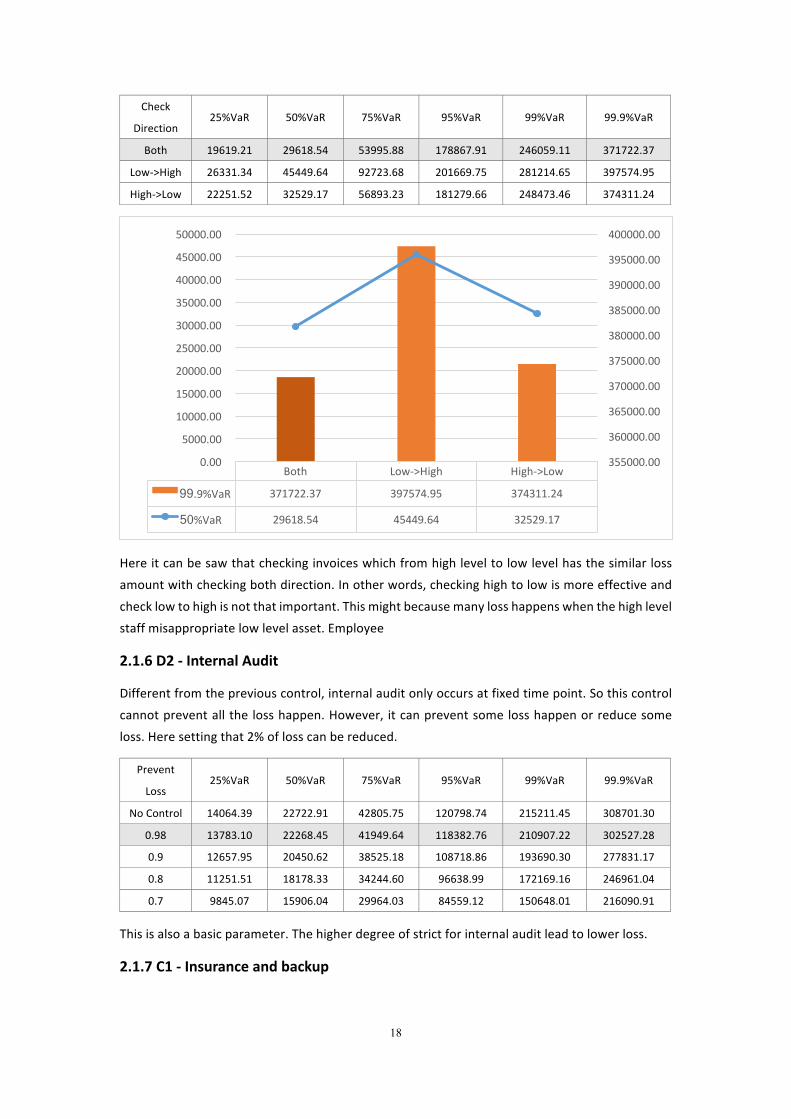

18

Check

Direction25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

Both 19619.21 29618.54 53995.88 178867.91 246059.11 371722.37

Low->High 26331.34 45449.64 92723.68 201669.75 281214.65 397574.95

High->Low 22251.52 32529.17 56893.23 181279.66 248473.46 374311.24

Hereitcanbesawthatcheckinginvoiceswhichfromhighleveltolowlevelhasthesimilarlossamountwithcheckingbothdirection.Inotherwords,checkinghightolowismoreeffectiveandchecklowtohighisnotthatimportant.Thismightbecausemanylosshappenswhenthehighlevelstaffmisappropriatelowlevelasset.Employee

2.1.6D2-InternalAudit

Differentfromthepreviouscontrol,internalauditonlyoccursatfixedtimepoint.Sothiscontrolcannotpreventallthelosshappen.However, itcanpreventsomelosshappenorreducesomeloss.Heresettingthat2%oflosscanbereduced.

Prevent

Loss25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

NoControl 14064.39 22722.91 42805.75 120798.74 215211.45 308701.30

0.98 13783.10 22268.45 41949.64 118382.76 210907.22 302527.28

0.9 12657.95 20450.62 38525.18 108718.86 193690.30 277831.17

0.8 11251.51 18178.33 34244.60 96638.99 172169.16 246961.04

0.7 9845.07 15906.04 29964.03 84559.12 150648.01 216090.91

Thisisalsoabasicparameter.Thehigherdegreeofstrictforinternalauditleadtolowerloss.

2.1.7C1-Insuranceandbackup

Both Low->High High->Low

99.9%VaR 371722.37 397574.95 374311.24

50%VaR 29618.54 45449.64 32529.17

355000.00

360000.00

365000.00

370000.00

375000.00

380000.00

385000.00

390000.00

395000.00

400000.00

0.00

5000.00

10000.00

15000.00

20000.00

25000.00

30000.00

35000.00

40000.00

45000.00

50000.00

19

Oncelossfrommisappropriationhappens,insurancecouldbeagoodwaytocontroltheloss.Or,someassetsuchasimportantdatacanberecoveredifhavingbackup.Hereitcanbesettledthatonlyasset inthesecondandthird levelhave insurance intheproportionof70%and50%.Thebottom level asset has low value and are cost-efficient for insurance. The top level asset onlyassesses to top level staff and have high level of security. So still no insurance for this level.However,theproportionofinsurancecanbealteredtofindabetterwayforreducingVaR.

InsuranceProportion VaRLevel1 Level2 Level3 Level4 25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

NoControl 23247.35 33175.01 52407.24 127692.78 221607.36 315079.68

0 0 0.7 0.5 15482.45 19981.17 29676.13 67843.51 114056.54 160163.33

0 0.7 0.5 0 13783.10 22268.45 41949.64 118382.76 210907.22 302527.28

0.7 0.5 0 0 16836.87 26886.46 46009.92 121173.33 215548.58 308304.32

0.3 0.3 0.3 0.3 16273.14 23222.51 36685.07 89384.95 155125.15 220555.78

Itoughttobeassumedthattheoverallpercentageofinsuranceisfixed.Bycomparingthedifferentfocuspointfortheinsurance,itshowsthattheexpectedlossislowwheninsurancefocusonthetoplevelasset.Thismakesensebecausetoplevelhasthehighestvalue.Andputtinginsuranceonaverageindifferentlevelshouldalsoeffectivelyreduceloss.

2.1.8C2-Tacklerelevantemployees

Afterassetmisappropriationoccurs,tacklerelevantemployees.Dismissalorfiringbillsmightbethemostcommonwaytodealwiththese.Onceneedtotacklerelevantemployeesanddismissalhim,thelossshouldsurpasstheonlyassetlosing.Plus,higherlevel’sdismissalshouldhavelargerimpact.Therefore,theseverityindexcanbesetfordifferentleveltoshowtheextraloss,suchaslossofvaluableemployees.

SeverityIndex VaR

NoControl InsureHigh InsureMedian InsureLow Average

Insure

99.9%VaR 315079.68 160163.33 302527.28 308304.32 220555.78

50%VaR 33175.01 19981.17 22268.45 26886.46 23222.51

0.00

50000.00

100000.00

150000.00

200000.00

250000.00

300000.00

350000.00

0.00

5000.00

10000.00

15000.00

20000.00

25000.00

30000.00

35000.00

20

Level1 Level2 Level3 Level4 25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

1 1 1 1 10801.93 15835.07 27158.07 71314.39 125321.62 178246.62

1 1.2 1.44 1.728 13783.10 22268.45 41949.64 118382.76 210907.22 302527.28

1 1.4 1.96 2.744 17555.94 30718.59 62141.51 183129.61 330894.30 475413.99

1 1.6 2.56 4.096 22116.06 41355.50 88486.15 269109.48 489831.22 704930.20

Thisisalsocommonparameter.Moreimportantthestaffis,thehigherlossis.

2.1.9Whichisthebestcontrol?

Pickpartlydatafromallabovetables,wecanonlycomparetheVaRwithorwithoutcertaincontrol.Inthisway,thecontrolmethodcanbeconsideredasthebestefficiency.Astheessentialpartofourmodel,controlP1,P4andC2areretained,whicharealsounrealisticifdeleting.Hereisourresultofremovingcontrol.

Control 25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

Origin 13783.10 22268.45 41949.64 118382.76 210907.22 302527.28

NoP2 19619.21 29618.54 53995.88 178867.91 246059.11 371722.37

NoP3 14222.78 22704.57 42397.68 118984.80 211220.30 302998.81

NoD1 22558.54 38510.17 78060.97 170365.08 250599.46 343463.46

NoD2 14064.39 22722.91 42805.75 120798.74 215211.45 308701.30

NoC1 23247.35 33175.01 52407.24 127692.78 221607.36 315079.68

Onceremovingcertaincontrol,itindicatesthatsuchloss’increaseislarge.Thismeansthatsuchcontrol is effectively. From this plot, ’Checking invoices and related documents’ (D1) and‘Insuranceandbackup’(C1)arethemosteffectivecontroltoreducetheexpectedloss.‘Implementawhistleblowingpolicy’(P2)and‘Checkinginvoicesandrelateddocuments’(D1)areeffectivetoreducethemassloss.‘InternalAudit’(D2)and‘Imposeclearsegregationofduties’(P3)functionisnotthatobviousifanothercontrolisset.

Origin NoP2 NoP3 NoD1 NoD2 NoC1

99.9%VaR 302527.28 371722.37 302998.81 343463.46 308701.30 315079.68

50%VaR 22268.45 29618.54 22704.57 38510.17 22722.91 33175.01

80000.00

130000.00

180000.00

230000.00

280000.00

330000.00

380000.00

430000.00

10000.00

15000.00

20000.00

25000.00

30000.00

35000.00

40000.00

21

3.2SensitivityanalysisforScenarioIIIt’simportanttoexploreandanalysehowdifferentmethodscouldreduceandprotectbank’sdatafromcyber-attacks.Atthisscenario,threemainfactorscanberecognizedtoprotectourdataandrecoverlossdatasuchastheabilityofengineers,solidityofeachfirewalls,andbackupofdata.Thepurpose is to compareanddrawa reliable conclusion to seewhich is themost significantfactor,whichstrategycouldbeusedasmostefficientwaytoreactandpreventdatasabotage.

3.2.1Analyzingimportanceofabilityofengineers

Asstatedabove,frequencyofcheckingsystemisthewaywemeasurethecapabilityofengineersat this scenario. Since increasing frequency of checking could reduce average time to detectinfiltrating. Therefore,different resultsofVaRbyadjustingdifferent valuesof frequency couldshowushowsensitivebetweenabilityofengineersandfinallossdollars.

CheckFreq 25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

once70mins 27820.00 32642.00 38692.00 57662.00 70757.35 88987.40

once60mins 26932.00 31143.42 36216.00 48334.67 59349.45 76068.35

once50mins 25376.00 29248.00 33388.00 39912.00 44763.71 50326.59

once40mins 23306.00 26910.00 30740.00 36652.00 40856.00 46206.00

once30mins 20182.00 23512.00 27060.00 32304.00 36158.00 40582.00

Fromtheresultsshowedinthegraphabove,wefindthereisapositiverelationshipbetweenabilityof engineers and data loss. Especial, improving capability of engineers is more efficient byconsideringmorequantilesofvalueatrisk.Thereisbigchangebetweenonce70mins,once60minsandonce50mins,it’sefficientandworthytoimprovethelevelofnetworkengineersfromlevel(once60mins)tolevel(once50mins)byconsideringcostsofnetworkengineers.Ofcoursebankcouldchoosemostprofessionalengineerstoprotecttheirimportantdataiftheythinkit’s

10000.00

20000.00

30000.00

40000.00

50000.00

60000.00

70000.00

80000.00

90000.00

100000.00

20% 30% 40% 50% 60% 70% 80% 90% 100%

ImapctofTimetodetectonVaR

once70mins once60mins once50mins once40mins once30mins

22

necessary based on the importance of their data. The largest change is 70081.88 by changingfrequencyfromonce60minstoonce30mins.

3.2.2Analyzingsolidityofeachfirewall

Firewalls are most significant and usual method to prevent bank’s data from majority datasabotagebehaviors.Atthispart,wewanttoshowhowessentialofeachfirewallbydecreasingprobabilityofpassingeachfirewallasthestandardofimprovingitssecuritylevels.

50%VaR Firewall1 Firewall2 Firewall3

(50%,25%,5%) 31143.42 31143.42 31143.42

reducedby10% 27972.00 29394.00 31058.00

reducedby20% 24786.00 27640.00 30978.00

reducedby30% 21704.00 25772.00 30916.00

99.9%VaR Firewall1 Firewall2 Firewall3

(50%,25%,5%) 76068.35 76068.35 76068.35

reducedby10% 69854.40 74094.82 74053.13

reducedby20% 65736.68 70948.92 73887.35

reducedby30% 61185.86 65778.22 69987.35

10000.00

15000.00

20000.00

25000.00

30000.00

35000.00

(50%, 25% , 5%) reducedby10% reducedby20% reducedby30%

Improvingsecurityofeachfirewallswith50%VaR

Firewall1 Firewall2 Firewall3

23

Fromgraphsabove,itillustratesthatthesecuritylevelisverysensitivefortheresultofVaR,thelargestchangeis69987.35byimprovingsecurityleveloffirewall1.Therefore,conclusionismadethatfirewallsareessentialtoprotectbank’sdata.

3.2.3ImpactofpercentageoftotaldatainbackuponVaR

Normally,bankcouldrecovertheirlossdatafromtheirbackup,howevertheycouldn’tobtainalldatafromtheirdatabasebackupbasedonsomestaffmissoperations.Therefore,it’simportanttoensureabankhaveallessentialdatabackupinordertomakesurebusinessworkwellevenintheworstcasethattheylosesomeessentialdata.Atthispart,thepercentagesofdatainbackuparechangedinordertoshowchangesofVaRandfindamostefficientwaytorecoverourdataafterdatasabotage.

%ofdatainbackup 25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

80% 26932.00 31143.42 36216.00 48334.67 59349.45 76068.35

85% 25785.00 29853.25 34705.25 46282.36 56996.67 73124.86

90% 24662.00 28537.00 33178.50 44241.33 54723.11 70181.37

95% 23544.25 27252.50 31671.00 42219.02 52339.19 67237.88

50000.00

55000.00

60000.00

65000.00

70000.00

75000.00

80000.00

(50%, 25% , 5%) reducedby10% reducedby20% reducedby30%

Improvingsecurityofeachfirewallswith99.9%VaR

Firewall1 Firewall2 Firewall3

24

From above chart, it shows a large changing if increasing percentage of backup of client’sinformation.Eventhoughonlythehalfofclient’sinformationcanbecopied,anditnormallycan’tmakebackupofmanagementinformationontime,itstillmakeshugeimpactonreducingVaRatdifferentquantilelevels.

3.2.4Impactofdifferentfirewalls

Changingthenumberoffirewallscanbeusedtofindabetterwayofbuildingfirewall.Aboveall,‘3firewalls’istheinitialconditionofbank.Whatifbankreducethenumberoffirewallsto2?Atthesametime,adjustingsomeparametersisnecessarytofitthedata.Comparingtheresultstofindstrategicoptionsforbank’snetworksystem.

Beforechanging 3FirewallsStructure Afterchanging 2FirewallsStructure

Timeofbreakthe

firework(min)

1stfirewall 5 1stfirewall 15

2ndfirewall 15 2ndfirewall 50

3rdfirewall 45

Probabilityof

breakthefirework

1stfirewall 0.5 1stfirewall 0.2

2ndfirewall 0.25 2ndfirewall 0.04

3rdfirewall 0.05

Datavolume

proportionbehind

thefirework

1stfirewall 0.05 1stfirewall 0.2

2ndfirewall 0.15 2ndfirewall 0.8

3rdfirewall 0.8

Datavaluebehind

thefirework(unit

value)($)

1stfirewall 10 1stfirewall 17.5

2ndfirewall 20 2ndfirewall 50

3rdfirewall 50

Afterusingthesamealgorithm,followingresultcanbeshowed.

25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

20000.00

30000.00

40000.00

50000.00

60000.00

70000.00

80000.00

20% 30% 40% 50% 60% 70% 80% 90% 100%

ImpactofPercentageofdatainbackuponVaR

80%Backup 85%Backup 90%Backup 95%Backup

25

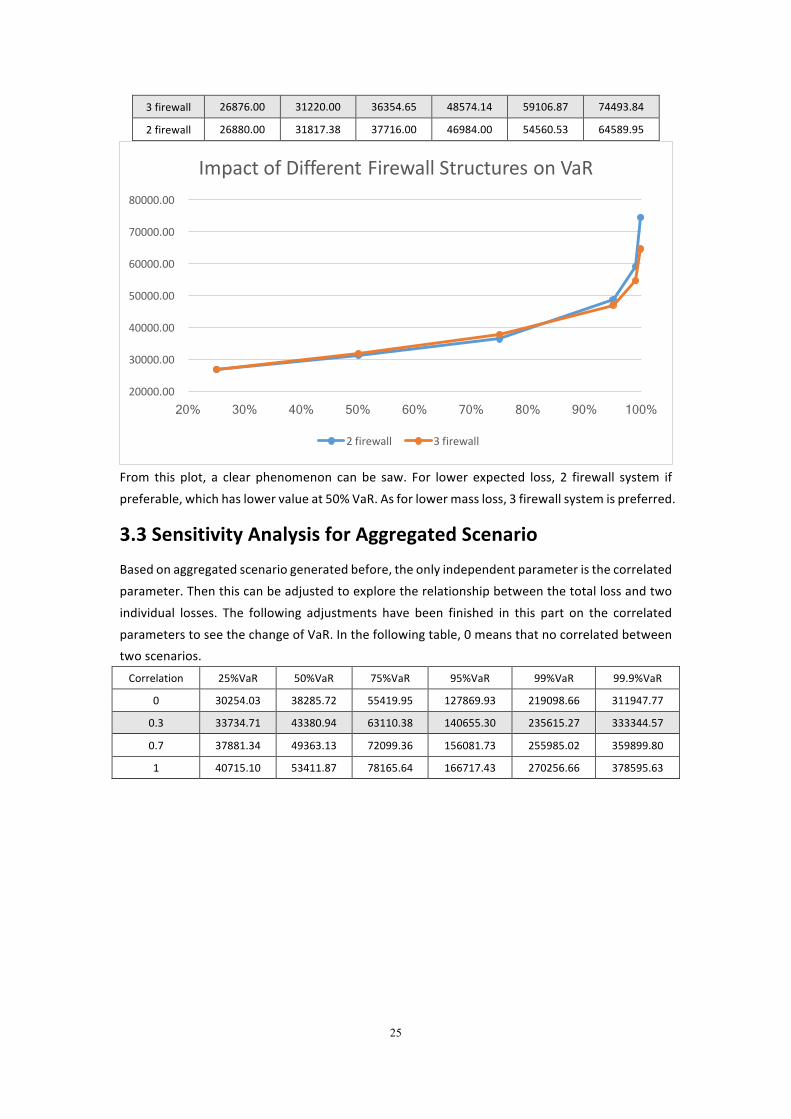

3firewall 26876.00 31220.00 36354.65 48574.14 59106.87 74493.84

2firewall 26880.00 31817.38 37716.00 46984.00 54560.53 64589.95

From this plot, a clear phenomenon can be saw. For lower expected loss, 2 firewall system ifpreferable,whichhaslowervalueat50%VaR.Asforlowermassloss,3firewallsystemispreferred.

3.3SensitivityAnalysisforAggregatedScenarioBasedonaggregatedscenariogeneratedbefore,theonlyindependentparameteristhecorrelatedparameter.Thenthiscanbeadjustedtoexploretherelationshipbetweenthetotallossandtwoindividual losses. The following adjustments have been finished in this part on the correlatedparameterstoseethechangeofVaR.Inthefollowingtable,0meansthatnocorrelatedbetweentwoscenarios.Correlation 25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

0 30254.03 38285.72 55419.95 127869.93 219098.66 311947.77

0.3 33734.71 43380.94 63110.38 140655.30 235615.27 333344.57

0.7 37881.34 49363.13 72099.36 156081.73 255985.02 359899.80

1 40715.10 53411.87 78165.64 166717.43 270256.66 378595.63

20000.00

30000.00

40000.00

50000.00

60000.00

70000.00

80000.00

20% 30% 40% 50% 60% 70% 80% 90% 100%

ImpactofDifferentFirewallStructuresonVaR

2firewall 3firewall

26

Fromtheplot,itshowsthathigherstrongercorrelationgetshigherVaRbothinaspectofexpectedlossandextremeloss.Theexplanationmightbethis–onceoneofthescenariolosshappen,itmeans that the probability of risk factor is relatively high. In this way, as the existence ofcorrelation,higherriskfactoralsocausescauselossonanotherscenario.

4.AlternativeAdjustmentonLossMeasureQuantile

HNext,introducingclustermethodaimstoimprovetheresultofVaR,andthisapproachisworthyforgeneratingnewVaRquantilesbasedonseverity,whichenablesonetocombineexpertopinionscenarioswithquantitativeoperational riskdata.Thismethodologywas firstlyproposedbyDr.SovanMitrain2013byusingthekeyideafrommachinelearning.[12]

4.1IntroductiontoClusterAnalysis

Toachievescenarioadjustment,clusteringanalysiscanbeappliedtomatchseveritymagnitude.Clustering isamethodofgroupingdata intosubsetsofdata,whicharealsoknownasclusters.Moreover,K-meansclustersanalysisisonekindofunsupervisedlearning,whichisonesubjectofmachine learning.Unsupervised learning isaway toexplore thecommon featureofdatabyaparticularalgorithm.K-meansalgorithmisasimpleiterativeclusteringalgorithm.Itusesdistance(e.g.Euclideandistance)asthesimilarityindextofindagivendatasetofKclasses.Eachcentreofclassisobtainedbythemeanofallthevalueinsuchclass.Eachclassisdescribedastheclusteringcentre.

0.00

50000.00

100000.00

150000.00

200000.00

250000.00

300000.00

350000.00

400000.00

20% 30% 40% 50% 60% 70% 80% 90% 100%

0 0.3 0.7 1

27

4.2ApplicationonAdjustmentofScenarioResult

ThefollowingisthebasicstepsofK-meanclustersalgorithm.

Step1:SelectKobjects in thedataspaceas the initialcentre.Eachobjectrepresentsaclustercentre.

Step2:Foreverydataobjectsinthesample,wecalculatetheEuclideandistancebetweenitandtheclustercentres.Thendifferentdataaregroupedaccordingtothenearestcriterionandaredividedintothecorrespondingclassesofnearestclustercentres.

Step3:Updatetheclustercentre-themeanvaluesofalltheobjectsineachcategoryaredealtastheclustercentreoftheclass.Thenthevalueoftheobjectivefunctioncanbecomputed.

Step4:Determiningwethertheclustercentreandthevalueofobjectivefunctionarechangedornot.Iftheybothstaythesame,outputtheresults;ifchanged,thenturnbacktostep2.

Usingtheabovealgorithm,theMCsimulationresultisusedasthesampleclass.TheVaRs’intervalsoftheclustercentreofeachintervalaremodified.Theresultsareshowedasfollowing.

Forscenario1-assetmisappropriation

Forscenario2-cyberattack

4.3ImportantMeaningtoLossMeasureQuantile

TheintervalpointofVaR(25%,50%,75%,95%,99%,99.5%)isbasedontheempiricaljudgement.In common situation, these quantiles are fixed as a standard for operational risk modelling.However,settingtheseintervalpointscannotclearlyreflectthefeatureofadifferentdistribution.Clustermethodintroducesaneffectivewaytoreflectthefeatureofdistributioninseveralintervalsandtheloss leveloneachintervalatthesametime.This isveryimportanttoimprovethelossmeasure quantile. In our result, although the fixed interval points have change, themodifiedoutcome can reflect average VaR level in 6 different intervals. It can also reflect relativerelationshipofindividualintervalamongtheoveralldistributionofloss.

Unmodified25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

13783.10 22268.45 41949.64 118382.76 210907.22 302527.28

Modified48.1% 76.3% 92.4% 96.5% 99.8% 100.0%

21335.32 43380.22 84397.50 151063.49 257611.43 429427.17

Unmodified25%VaR 50%VaR 75%VaR 95%VaR 99%VaR 99.9%VaR

26932.00 31143.42 36216.00 48334.67 59349.45 76068.35

Modified31.6% 66.6% 88.7% 97.1% 99.7% 100.0%

28136.00 34181.89 41909.31 52582.55 66845.03 90931.40

28

5.ConclusionInconclusion, the lossdistributionscanbegenerated for scenariosassetmisappropriationandcyber-attackandcombinedscenariosofbothofthem;basedonourscenariosanalysis,sensitivityanalysisofscenariosisusefultoassistustoderivemostessentialfactorsforoperationalrisksasthebasisofstrategicsuggestionstomanagers.

5.1Discussionofstrategicoptions

Atthispart,thespecificstrategiesarediscussedseparatelyforassetmisappropriation(scenario1)andcyber-attack(scenario2)forourbank.

In scenario 1, firstly, it illuminates that internal fraudsters within bank regarding assetmisappropriationarefromtoptwolevelsemployeeswithinbankcoveringtheheadofabankandvice-presidents,managersordirectors.Outoftheabuseoftheirauthority,theycouldeasilyaccessandoccupybank’s assetwithout supervision.Once this events happened, it almost surelywillcausehugelossesforbank.Therefore,westronglysuggestourbanktoinvokethirdpartyasspecialfair assetmanagementplatform to recordandcheck thehigh-levelemployees’ applicationsoftheirauthorityespeciallyforassetsofbank.Next,whistleblowingisalsoahighlyefficientcontroltoreduceORlossesinscenario1.Basedonourscenariodata, itshowswhistleblowingschemewithinsamelevelemployeesorbetweendifferentlevelsemployeesdonateshugecontributionofoperational risk management under this circumstance compared with other controls. Hence,whistleblowingshouldbespreadoutwithcertainbonustohelpbanktocreatethisschemeandformemployeewhistleblowingawareness.

Inscenario2,cyber-attackisnormallycausedbyexternalintendedattacktobank’sinformationnetworksystem.Hence,wecanthinkthisasthebattlebetweenourinformationsecurityengineersandhackers.It’sefficientifwedecreasedetectiongaptimeofengineersfromonce70minutestoonce50minutes;however,ithasloweffectifwetrytoreducefurtherfrom50minuteswithhighexpenses. It may be caused ability of engineers from 50minutes has exceeded the ability ofmajority hackers. As for firewalls, more firewalls can reduce the data losses of essentialinformationandcausemorelossesofnonessentialdata.Sincewemeasurethesamelevelofourfirewalls,weassumethatfirewallswillhavestrongerabilitytopreventournetworkfromhackers’attacks.Then,resultsshowthatwemaylosemorecoreinformationinourbankandlesslossofnormaldataunderlessnumberoffirewallscomparedwithmulti-complexfirewalls.Basedthetypeof informationthatbankwanttoprotect,managerscanchangetheirstrategiesandadjust it ifnecessary.

From dependency analysis in our combined scenario, the result proves that the quality ofemployeesiskeyriskdriversofbothscenarios;hence,it’snecessarytoimprovebank’srecruitmentprocedureandvetCVaswellasreferences.

29

5.2LimitationandImprovementInthispaper,someessentialparametersofourscenarios,wesimplyusetheexpert’sopinionsandhistorical loss distributions which may result in cognition biases from the real market andpredictionscausedbytheuncertaintiesoffuturebusinessenvironment.Hence,theparametersinourscenariosshouldbeassumedbasedonbothinternalandexternalexpertsaswellasreasonableassumptionsoffuturechangesforlocalandglobalcircumstances.Ifnecessarily,weoughttobeconservative on parameter assumptions for some sensitive factors.Moreover, it can bemoreflexible on changes of parameters; for instances, hackers’ ability should be adjusted morerandomlyandmoreunpredictedforsimulatingrealisticcases.Theadvanceddependencystructurecanbeappliedheretoattributedifferentriskdriverstoscenarios.Inthisway,moreappropriatecorrelationandvariancematrixcanbegeneratedtocombinetwoscenarios.

6.Reference[1] K.vanderHeijden,Scenarios:TheArtofStrategicConversation,Wiley,Chichester,1996.

[2] T.J.PostmaandF.Liebl,Howtoimprovescenarioanalysisasastrategicmanagementtool,TechnologicalForecasting&SocialChange72(2005)161–173

[3] P.J.H.Schoemaker,C.A.J.M.vanderHeijden,IntegratingscenariosintostrategicplanningatRoyalDutch/Shell,Plann. Rev.20(3)(1992)41–48.

[4] K.vanderHeijden,Scenarios:TheArtofStrategicConversation,Wiley,Chichester,1996.

[5] M.Godet,ScenariosandStrategicManagement,Butterworth,London,1987.

[6] W.R.Huss,Amovetowardscenarioanalysis,Int.J.Forecast.4(1988)377–388.

[7] M.E. Porter, Competitive Advantage—Creating and Sustaining Superior Performance,FreePress,NewYork,1985.

[8] P.Schwartz,TheArtof theLongView:Planning for theFuture inanUncertainWorld,DoubledayCurrency,NewYork, 1991.

[9] U.vonReibnitz,ScenarioTechniques,McGraw-Hill,Hamburg,1988.

[10] G.Ringland,ScenarioPlanning:ManagingfortheFuture,Wiley,Chichester,1998.

[11] R.P.Bood,Th.J.B.M.Postma,Strategiclearningwithscenarios,Eur.Manag.J.15(6)(1997)633–647.

[12] S. Mitar, Scenario Generation for Operational Risk,Intelligent Systems In Accounting,FinanceAndManagement,20(2013),163–187.

30

[13] E. Barbieri Masini, J. Medina Vasquez, Scenarios as seen from a human and socialperspective,Technol.Forecast.Soc.Change65(1)(2000)49–66.

[14] K.vanderHeijden,R.Bradfield,G.Burt,G.Cairns,G.Wright,TheSixthSense:AcceleratingOrganizationalLearningwithScenarios,Wiley,Chichester,2002.

[15] J.Corriganetal,MillimanReserchReport:AggregationofRisksandAllocationofCapital,2009.

7.Appendix1. CodesforScenarioIbasedonMatlabclear;close all;clc

rand('state',0); % fix random number, good for sensitivity randn('seed',0); % fix random number H=2000; % total employees Hlevel=[1200 600 180 20]; % employees level number ptheft=[.1 .1 .05 .05]; % criminal probability muthe=[10 20 100 1000]; % asset mu sigmathe=[3 6 30 300]; % asset sigma percentage=[.5 .75 .9]; % volume of asset in different level itemrange=[15 35 65 100]; % level setting whithe=0.5; % whistleblowing probability segthe=0.2; % cross-deppartment probability minuamou=0.8; % proportion of access to cross-asset pplevel=[.5 .25 .1]; % cross-level probability severi=[1 1.2 1.44 1.728]; % severity Sevinteadu=0.98; % internal audit insran=[0 .7 .5 0]; % insurance proportion N=10000; for i=1:N % P1 - Vet employees by CV and references ntheft(1)=binornd(Hlevel(1),ptheft(1),1,1); ntheft(2)=binornd(Hlevel(2),ptheft(2),1,1); ntheft(3)=binornd(Hlevel(3),ptheft(3),1,1); ntheft(4)=binornd(Hlevel(4),ptheft(4),1,1); for ii=1:4 sumtiWU(ii)=0;sumtiP2(ii)=0;sumtiD1(ii)=0;sumtiQU(ii)=0; if ntheft(ii)==0 % amou(ii)=0; jthe(ii)=0; sxx(ii)=0;

ppp(ii)=0;

break;

31

end for j=1:ntheft(ii) % decide amount amou(ii)=ceil(normrnd(muthe(ii),sigmathe(ii))); % decide values xx=rand(); if xx<=percentage(1) sxx(ii)=rand()*10; elseif xx<=percentage(2) sxx(ii)=rand()*20+10; elseif xx<=percentage(3) sxx(ii)=rand()*30+30; else sxx(ii)=rand()*40+60; end % decide levels if sxx(ii)<=itemrange(1) jthe(ii)=1; elseif sxx(ii)<=itemrange(2) jthe(ii)=2; elseif sxx(ii)<=itemrange(3) jthe(ii)=3; else jthe(ii)=4; end QUQU=1; % P2 - Implement a whistleblowing policy if (ii==jthe(ii)) && (rand()<=whithe) QUQU=0; end % P3 - Impose clear segregation of duties if (ii~=4)&&(rand()<=segthe)

amou(ii)=ceil(amou(ii)*minuamou); end % P4 - Control access to buildings and systems if sxx(ii)<=itemrange(1) ppp(ii)=1; elseif sxx(ii)<=itemrange(2)

ppp(ii)=1*(ii>=2)+(ii==1)*(rand()<pplevel(1)); elseif sxx(ii)<=itemrange(3)

ppp(ii)=1*(ii>=3)+(ii==1)*(rand()<pplevel(1))*(rand()<pplevel(2))+(

ii==2)*(rand()<pplevel(2)); else

ppp(ii)=(ii==4)+(ii==1)*(rand()<pplevel(1))*(rand()<pplevel(2))*(ra

nd()<pplevel(3))+(ii==2)*(rand()<pplevel(2))*(rand()<pplevel(3))+(i

i==3)*(rand()<pplevel(3)); end DDD=1; % D1 - Checking invoices and related documents if ii~=jthe(ii) DDD=0.5; end % C1 - Insurance + C2 - Tackle relevant employees

sumtiQU(ii)=sumtiQU(ii)+amou(ii)*sxx(ii)*ppp(ii)*severi(ii)*(1-

insran(ii))*DDD*QUQU;

32

end %D2 - Internal Audit sumtheQU(i)=sum(sumtiQU)*Sevinteadu; end end hist(sumtheQU,1000); % percentile selection of the convoluted distributions VARQU=prctile(sumtheQU,[25, 50, 75, 95, 99, 99.9]2. CodesforScenarioIIbasedonMatlabrand('state',0); randn('seed',0); H=100; % possible attack Efrequency=60; % Engineers check system once an hour amoutdata=10000; % assume there are 10000 nits of data fiwotime=[5 15 45]; % time used by hackers to pass each firewalls probattk=[.5 .25 .05];% probability of hackers pass each firewalls perdata=[.05 .1 .85]; % percentage of data hackers pass each firewall valdata=[10 20 50]; % dollars per unit of data percentpermin=.05; % data loss rate when hackers pass third firewall percentdata=.5; %the proportion of clients’ data backupdata=.8; % back up 80% of clients' data percentage=[.6 .9 .95 .975 .99]; N=10000; % times that Monte Carlo runs for ii=1:N vnlost(ii)=0; for i=1:H restime=rand()*Efrequency; if restime<fiwotime(1) srr=0;svv=0; elseif restime<fiwotime(2)

srr=(rand()<probattk(1))*perdata(1); svv=srr*valdata(1); elseif restime<fiwotime(3)

srr=(rand()<probattk(1))*(perdata(1)+(rand()<probattk(2))*perdata(2

)); svv=srr*valdata(1)+(srr>perdata(1))*(srr-

perdata(1))*(valdata(2)-valdata(1)); else

srr=(rand()<probattk(1))*(perdata(1)+(rand()<probattk(2))*(perdata(

2)+(rand()<probattk(3))*(restime-fiwotime(3))*percentpermin)); svv=srr*valdata(1)+(srr>perdata(1))*(srr-

perdata(1))*(valdata(2)-

33

valdata(1))+(srr>(perdata(1)+perdata(2)))*(srr-perdata(1)-

perdata(2))*(valdata(3)-valdata(2)); end vlost(i)=svv*amoutdata; %backup of loss data in clients information %vlosta are divided into 100 units, 50% client 50% management

client's infor with 80%back up veachlost(i)=vlost(i)/100; for j=1:100 vback(j)=(rand()<percentdata)*backupdata*veachlost(i); vlost(i)=vlost(i)-vback(j); end vnlost(ii)=vnlost(ii)+vlost(i); end end hist(vlost,1000);

% plot of the results VAR=prctile(vlost,[25, 50, 75, 95, 99, 99.9]) % percentile selection of the convoluted distributions3. CodesforAggregatedScenariobasedonMatlabX1=sort(vnlost); X2=sort(sumtheQU); corr=[0 .3 .7 1]; % correlation output=[] for j=1:4 ROU=[1 corr(j);corr(j) 1]; % correlation matrix for i=1:N X=[X1(i) X2(i)]; XBOTH(i)=sqrt(X*ROU*X'); end

VARboth=prctile(XBOTH,[25, 50, 75, 95, 99, 99.9])

plot([25, 50, 75, 95, 99, 99.9],VARboth)

output=[output;VARboth]

hold on, end

output

4. K-meanclusteralgorithmbasedonMatlab

34

Q=VARQU; %VAR n=X2; % LOSS PEC=[25 50 75 95 99 99.9]; % PERCENTAGE k=[0 0 0 0 0 0]; % LOCATION SUI1=[0 0 0 0 0 0]; % AMOUNT OF EACH GROUP SUM1=Q; SUM2=Q; %n=gamrnd(2,20000,10000,1); subplot(1,2,1) hist(n,1000); subplot(1,2,2); %plot([25, 50, 75, 95, 99, 99.9],SUM1,'-O'); while 1 SUM1=[0 0 0 0 0 0]; % grouping for j=1:10000 for i=1:6 k(i)=abs(SUM2(i)-n(j)); end m=min(k); [xx]=find(k==m); SUM1(xx)=SUM1(xx)+n(j); SUI1(xx)=SUI1(xx)+1; end % K-means K=6 SUL(1)=0; for i=1:6 SUM1(i)=SUM1(i)/SUI1(i); SUL(i+1)=SUL(i)+SUI1(i); end for i=1:6 SULL(i)=SUL(i+1); SSS(i)=n(SULL(i)); end %disp(SULL); %disp(SUM1); SUI1=[0 0 0 0 0 0]; % convergence condition

35

if max(abs(SUM1-SUM2)./SUM2)<=0.05 break; end SDASSDA=6; SUM2=SUM1; hold on, plot(SULL(1:SDASSDA)/100,SSS(1:SDASSDA)); end hhhh=[SULL;SSS;PEC*100;Q] hold on, plot(SULL(1:SDASSDA)/100,SSS(1:SDASSDA),'LineWidth',3); hold on, plot(PEC(1:SDASSDA),Q(1:SDASSDA),'-O');