scenario passenger car - information and library...

TRANSCRIPT

Chapter 3

Market Scenario of Passenger Car

Industry in India

CHAPTER 3

PRE CONSOLIDATION PHASE

CONSOLIDATION PHASE

THE COMPETITIVE PHASE

ENTRY OF GLOBAL CAR GIANTS I N INDIA

SALIENT FEATURES OF GLOBAL GIANTS

PRESENT SCENARIO

ERA OF COMPACT AND SMALL CARS

TOTAL PRODUCTION TREND OF PASSENGER CARS I N INDIA

TOTAL SALES TREND OF PASSENGER CARS I N INDIA

MARKET SHARE OF LEADING PASSENGER CAR MANUFACTURERS

INDIAN EXPORTS OF PASSENGER CARS

10. PROSPECTS

Chapter 3 5 8

This chapter deals with the historical background and the

present scenario of passenger car market in India.

1 PRE-CONSOLIDATION PHASE

The Indian car industry has only a century old .The first motorcar

was seen on the streets of India in 1898. Mumbai had its first

taxicabs in the early 1900. Then for the next fifty years, cars were

imported to satisfy domestic demand. Between 1910 and 1920s the

automobile industry made a humble beginning by setting up

assembly plants in Mumbai, Calcutta and Chennai. The

import/assembly of vehicles grew consistently after the 1920s,

crossing the 30,000 mark in 1930. I n 1946, Premier Automobile

Ltd. (PAL) earned the distinction of manufacturing the first car in

the country by assembling 'Dodge DeSoto' and 'Plymouth' cars at its

Kurla plant. Hindustan Motors (HM), which started as a

manufacturer of auto components gradually rose to manufacture

cars in 1949. I n 1952, the Government of India (GOI) setup a tariff

commission to device regulations to develop an indigenous

automobile industry in the country. After the commission submitted

its recommendations, the GO1 asked assembly plants, which did not

have plans to set up manufacturing facilities, to shut operations. As

a result, General Motors, Ford and other assemblers closed

operations in the country. This decision of the government marked

a turning point in the history of the Indian car industry. The GO1

also had a say in what type of vehicle each manufacturer should

make. Therefore, each product was safely cocooned in its own

segment with no fears of any impending competition. Also, no new

entrant was allowed even though they had plants of a full-fledged

manufacturing program. The restrictive set of policies was chiefly

aimed at buillding an indigenous auto industry. However, the

restrictions on foreign collaborations led to limitations on import of

technology through technical collaboration agreements.

The other control imposed on carmakers related to production

capacity and distribution. The GO1 control even extended to fixation

of prices for cars and dealer commissions. This triggered the start of

a protracted legal battle in 1969 between some carmakers and GOI.

Thus, the first three decades of the passenger car industry in India,

proved to be the 'dark ages' for the consumer, as his choice

throughout this period was limited to two models viz. Ambassador

and Padmini,

2.THE CONSOLIDAT1,ON PHASE: (SCENARIO BETWEEN 1980 AND 1990)

The 1980s witnessed the second distinctive phase in car

industry, i.e. consolidation which was marked by the entry and

consolidation of Maruti. The entry of Maruti brought about the first

substantial change in the Indian passenger car industry. Backed by

Suzuki of Japan, Maruti Udyog Ltd., then a public sector unit,

introduced the fuel efficient car, Maruti 800 in the Indian market.

Chapter 3 60

For the first time, technological advancements began to show their

impact on the industry. The production capacity of Maruti Ltd. was

also high, compared to the other car manufacturers operating in the

country at that time. And it was the qualitative-cum-quantitative

thrust of Maruti that brought about a significant change in the

industry. Mainly there was improvement in the quality of vehicles

offered and the standard of customer service. Manufacturers started

bestowing attention on aspects like design, models, styling, etc.

There was also a slight reduction in the 'waiting period', a

phenomenon peculiar to India. The industry structure and market

shares tilted; Maruti, the new entrant secured a high market share.

Hindustan Motors Ltd. (HM) and Premier Auto Ltd. (PAL), the

established players lost their shares to Maruthi heavily. Soon, they

started their defensive operations. HM, the oldest player in the

industry, gave a facelift to its Ambassador and launched the

'Contessa', putting the old Ambassador engine in a new stylish

body. Subsequently, it brought out the 'Contessa Classic' with an

Isuzu engine. PAL launched the 'Premier 118-NE'. By the latter half

of this phase, Telco joined the fray with its diesel Tata mobile.

Though technically a light commercial vehicle, it was used by quite

a few as a passenger car. Tata Sierra, a sturdy and spacious jeep,

Tata Estate and Tata Sumo were also added to the list of Indian

motor cars.

Chapter 3

3. COMPETITIVE PHASE

The industry started witnessing radical changes in 1990s. With

de-licensing and liberalization, the industry entered the competitive

phase. Indian government has now permitted majority ownership

for foreign companies entering the industry through a joint venture.

I n addition to this, there is no problem now in foreign exchange

availability, as the foreign collaborator could now take upto 51%

equity stake. Four major developments marked this phase: (i)

several new players entered the industry, (ii) the existing players

adopted new strategies, (iii) the industry went through a growth

phase, (iv) international car giants entered India and established

their units.

4. GLOBAL CAR GIANTS I N I N D I A

With the opening up of India's economy and the de-licensing of

the passenger car industry, India became a fertile ground for entry

of global car majors. The permission for foreign investment in the

industry and the scope for majority ownership for foreign players in

their Indian car ventures strengthened the interest of global car

giants in the Indian market. Practically all the major car

manufacturers of the world started setting shops in India. With the

establishment of Maruthi, Suzuki has been here for quite some

years now as the partner with GOI. GM struck a joint venture with

HM. Ford floated a joint venture with Mahindra and Mahindra.

Chapter 3 62

Daewoo started in partnership with DCM and later became an

almost cent percent owner. Hyundai unit in Chennai has been

operating as a cent percent subsidiary of the parent company.

Peugeot and Fiat aligned with PAL. Fiat later went alone. Mitsubishi

collaborated with HM. Honda struck an alliance with SIEL. Thus,

nearly a dozen internationall passenger car majors entered the

Indian car industry in the liberalization era. The country could now

boast of the presence of practically all the best-known car

manufactures of the world. Now a whole new range of cars hit the

market, offering wider choice to the Indian consumer.

AT PRESENT THE FOLLOWING GLOBAL CAR GIANTS ARE

OPERATING I N INDIA as shown in the following table.

Global passenger car giants and their partners in Indian ventures

1 Daem' Korea .-,l:::;ndia 1 1 GM, USA GM India Ltd. HM

Global Firm

Suzuki, Japan

Hyundai, Korea

- > --

Honda, Japan

Indian

Venture

Maruti Udyog

Hyundai

Motor India ~. ."- ---

Honda SIEL

Ford, USA

Peugeot, France L

Source: 1. Association of Indian Automobile Manufacturers ( AIAM)

Indian

Partner

GO1

-

No Partner

SIEL Ltd.

Fiat, Italy

Mitsubishi, Japan

Mercedes Benz,

Germany

2. Centre for Industrial and Economic Research

Ma hindra

Ford -

PAL Peugeot

M&M

PAL 4

PAL Fiat

HM

Mitsu bishi

Telco

PAL

HM

Telco

Chapter 3

5. SALIENT FEATURES OF GLOBAL GIANTS

Daewoo Motor Corporation of South Korea, a part of Daewoo

group which is ranked among the world's 50 largest industrial

houses, tied up with the DCM group. The project was to

manufacture modern, fuel efficient, 1500 cc cars, to start with, and

small cars later. Daewoo brought in its latest technology and

created a 'world class' facility in India for producing cars. The idea

was to manufacture 20,000 cars per year by 1996, 70,000 by

1997and 225,000 by the year 2000.

Ford set up a JV with Mahindra and Mahindra (M&M). It

introduced the Escort and Fiesta models in India. The project

involved an outlay of Rs. 2,700 crore. Ford's own investment was in

the range of $ 500-700 million. The project had a manufacturing

capacity of 125,000 cars a year. It was to manufacture 20,000

vehicles initially and gradually increase the capacity. The cars were

to be marketed both in India and abroad. Initially, the company

manufactured vehicles using the production facilities of M&M. Ford

also purchased 5.87 per cent of equity in M&M.

GM set up a joint venture with HM and launched the Opel Astra.

Ope1 is the largest selling brand in Western Europe. The Astra is

Opel's best selling model worldwide. The initial production was to be

25,000 units per annum with a provision to expand to 100,000

later. Astra was positioned in the Indian market as a premium car,

Chapter 3 65

reflecting its heritage as well as quality and reliability. GM India

played up its technological strength. I n addition, it tried to build a

strong dealer network. The idea was to create a nation-wide chain

of dealers ensuring that the customer gets specially trained

mechanics to look after the car and a regular supply of spares and

accessories.

Honda Motor Company of Japan entered the SIEL of the Siddarth

Shriram group as its partner. The project was to manufacture cars

in the 1300-1500 cc range to start with and small car later. The

joint venture was named as Honda-SIEL Cars India Limited. Honda

was to have 60 percent of the equity in the joint venture and SIEL

the rest. The proposal envisaged an investment of Rs. 860 crores

over a seven-year period. The equity base of the company was to

be Rs. 180 crores. The company was to manufacture 10,000 cars in

the first year and gradually increase production to 30,000 cars per

annum by the third year, depending on market conditions. Honda-

SIEL launched Honda City, by the end of 1997 /early 1998. Honda

developed this car specifically for India.

South Korea's Hyundai Motor Corporation, HMC, is the other

global auto major to set up shop in India. HMC, which is the leading

auto company in South Korea and is ranked 13'~ among world car

majors, planned to manufacture cars in India in the 1000-1500 cc

range. It planned to invest a total of $1.1 billion in a fully integrated

Chapter 3 66

automobile manufacturing facility at Sriperumbudur, Chennai.

Hyundai Motor India came up as 100 percent subsidiary of HMC.

The plant had an initial capacity of one lakh cars a year. The

capacity was to go up to produce 120,000 cars per annum later.

Telco had earlier located a niche for its indigenously developed

diesel vehicles, Tata mobile, Tata Sierra, Tata Estate and Tata

Sumo. Tata Safari followed later. Now, Telco came up with two new

projects. First, it forged a tie-up with Daimler Benz, makers of

Mercedes Benz cars. Then it went ahead with its project for small

cars, a 'national car' of 'international quality'. Telco's formula for the

car was that it should be small, affordable, modern, comfortable

and fuel efficient. Telco was trying to build a unique strength; it was

trying to emerge as the only company represented in the top,

middle and lower segments of the Indian car market. It is

interesting to note here that i t is actively considering to introduce a

passenger car costing only one lakh rupees.

6. PRESENT SCENARIO

Maruti Suzuki dominated the Indian passenger car industry in

the mid 1990s with a market share of around 70%. The model

range was limited to the incredibly popular Maruti 800, Maruti Zen,

Maruti Esteem, Maruti Omni, Fiat Uno, Ope1 Astra and of course

Hindustan Motor's Ambassador.

Chapter 3

Maruti Suzuki reigned supreme as the king of the Indian roads. It

was essentially a sellersf market, over which Maruti had a vice-like

grip. This phase was characterized by:

P MUL's near monopoly in the mid 90s

'i. No focus on product design /technology improvement

P No R&D or attempts to expand the market

k Flat market growth rate

Non-availability of Consumer Finance Schemes

b A Sellers' market

There were hardly any product innovations. The technology

prevalent in the market had grown archaic. Foreign car

manufacturers like Ford, General Motors were dumping their decade

old models in the Indian market. The Indian consumer had no

access t o easy consumer finance to fund his purchase, and

customer service was a term heard only in management textbooks.

ow ever, the market situation changed with the entry of

Hyundai Motor India Limited and its maiden offering to the Indian

market - the Hyundai Santro in September 1998. This launch was

followed by other high profile launches like Daewoo Matiz and Tata

Indica. These thlree launches in the compact car segment changed

the entire dynamics of the Indian passenger car market. From a

Chupter 3

sellers' market it overnight transformed into a buyers' market. The

Indian consumers were exposed to the latest international models

with the latest technology. These launches led to a substantial jump

in the market growth after 1998-99.

Sensing the emerging change, the existing players, HM, PAL, and

Maruti have come up with new strategies. With the help of McKinsey

& Co, HM prepared a turnaround plan as well as a new long-term

strategy. It brought in the Ambassador 1800 ISZ model. A tie-up

with GM formed the central piece of HM's new strategy. HM

promoted a joint venture with GM and launched the Opel Astra. HM

also invested Rs. 300 crore on the Lancer car project in

collaboration with Mitsubishi Motor Corporation. The initial capacity

of the Lancer car unit would be 30,000 units per year. The car rolled

out of the assembly line by September 1998.

PAL went in for improvements in the existing models. It also

introduced the diesel version of premier 118 NE, combining the

economy of diesel and the comfort of 118 NE. PAL also went in for

new collaborations with Peugeot and Fiat. The tie up with Peugeot

was for producing cars in the range of 1100-1600 cc, mainly

Peugeot 309. It was targeting a capacity of 60,000 cars per annum

with Peugeot 309 and Premier 118 NE models together. PAL tied up

with Fiat for making Fiat Uno cars in India. The two doors, five-

seated car, with a 1000 cc fully integrated robotized engine, was

targeted to compete with Maruti Zen. The company was planning

for a capacity of 50,000 cars per annum with Uno and Padmini

models together. This project too did not work the way it was

intended. Fiat later decided to go it alone with its own project in the

Indian market, keeping Uno-diesel as its trump card. Maruti

responded with its Zen and a sizeable expansion of overall capacity.

And subsequently, i t introduced the Esteem on the market.

7 . ERA OF COMPACT AND SMALL CARS

With the advent of new compact cars in 1998 - Hyundai Santro,

Daewoo's Matiz, Tata's Indica, and Fiat's Uno diesel - Maruti started

facing real competition. Competition was no longer limited to the

mid-segment. The new entrants were storming straight into Maruti's

exclusive domain, the small car segment. I t was an altogether new

scenario for Maruti. Interestingly, Maruti persisted with its strategy

of intensification and kept on expanding production and market. It

also kept enlarging and utilizing its competitive advantages for

achieving further expansion.

Daewoo launched its small car Matiz, in November 1998. It was a

800 cc vehicle. Daewoo had developed it from its Tico, which had

been based on Suzuki technology. Tico had become popular in the

South Korea and East European markets. Daewoo, however, did not

bring the Tico as it is to the Indian market. For India, it preferred to

supply a car that matched Indian requirements. Second, as per its

Chapter 3 7 0

agreement with Suzuki, Daewoo was restricted from offering the

Tico in the Indian market. Daewoo specially developed a new small

car for India. It was an in-house endeavour. Daewoo's small car for

India was launched simultaneously with the world launch of

Daewoo's small car.

Hyundai launched its small car 'Santro' in September 1998. I t

was a 1000 cc vehicle. Hyundai offered three different variants of

Santro. Like the Matiz, Santro too was specially designed for India.

Hyundai had developed the Santro from the basic Atoz model,

modifying it to suit the Indian conditions. The crucial change was

the upgradation of the 800 cc engine of Atoz to a 1000 cc one in the

case of Santro.

Towards the end of the calendar year 1998, Telco's small car,

Tata Indica too hit the Indian roads. Tata Indica was India's first

indigenously designed and manufactured passenger car. Telco had

designed it with technical help from the Italian car design shop,

IDEA. The Indica had a 1.4 litre engine. It came with an 18-month

mileage warranty. It was available in eight colours. Unlike Daewoo

and Hyundai, Telco offered a diesel version of its small car

simultaneously with the petrol version. And that made the crucial

difference.

Chapter 3

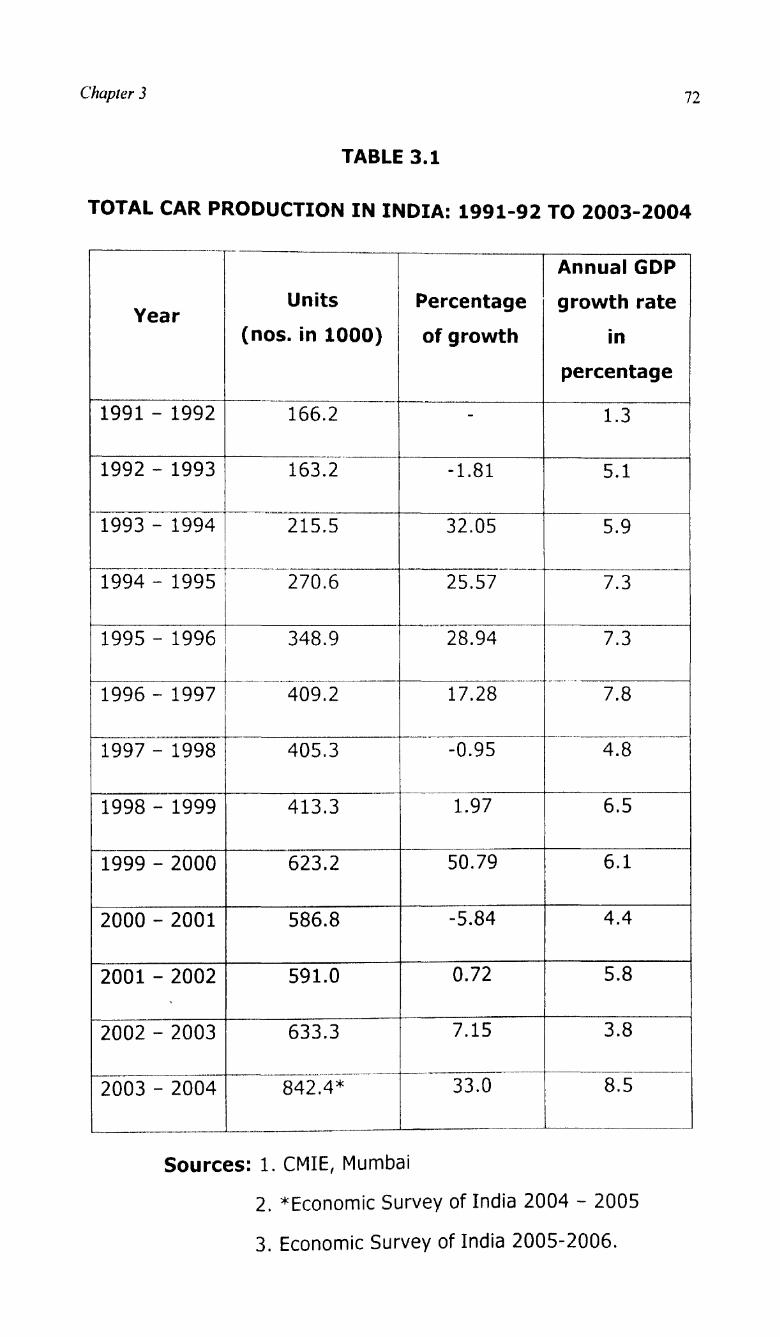

8. TOTAL PRODUCTION TREND OF PASSENGER CARS

The data relating to passenger car production in India since

1991-92 is depicted in Table 3.1. The number of cars produced in

1991-92 stood at 1,16,200 and increased to 4,09,200 in 1996-97.

However, the rate of annual growth gradually declined from 32.05%

in 1993-94 to 17.28 in 1996-97. Thereafter, the production

performance of Indian car industry has not been encouraging,

excepting 1999-2000 in which year there was record growth of

production a t 6,23,000 cars registering a growth rate of about 50%

over the previous year. I n all other years, the growth rate was

either negative or positive marginally. In the year 2002-2003, more

than 6 lakh cars were produced registering a growth rate of around

7% over the previous year. However during the years 2002-2003

and 2003-2004 the production had grown by 7.15 percent and 33

percent over the previous year respectively.

Gross Domestic Product (GDP) growth rates presented in the

last column of the Table 3.1 help us in under standing the relation

ship between car production and economic growth in India.

Chapter 3

TABLE 3.1

TOTAL CAR PRODUCTION I N INDIA: 1991-92 TO 2003-2004

". -

1 1" Annual GDP

Year Units 1 Percentage growth rate

/ (nos. in 1000) 1 of growth I I percentage

Sources: 1. CMIE, Mumlbai

2. *Economic Survey of India 2004 - 2005

3. Economic Survey of India 2005-2006.

Chaprer 3

Production capacities of leading manufacturers in the year

2002 are shown in Table 3.2

TABLE 3.2

PRODUCTION CAPACITY OF LEADING CAR MANUFACTURERS

( I N NUMBERS)

-- ---.- -- --". - --

Maruti Udyog -

2~501000 3,50,000

Car Manufacturing Company

-.. - - " ." - --

Hyundai 1,10,000 1,30,000

Telco 1 1.00.000 1,50,000

FY 2002 2005 (Expected)

Ford India 50,000 70,000

--- - A -- -.- " -- * ""%&.* - m-

Daewoo

General Motors I

72,000

Fiat India

1,30,000

6O,OOO

Honda Siel

Source: MARKET SURVEY FACTS FOR YOU - SEP 2003

60,000

Hindustan Motors

30,000 50,000

30,000 50,000

Chapter 3

9. TOTAL SALES TREND OF PASSENGER CARS I N INDIA

The details of total car sales in value are shown in Table 3.3.

The growth in sales during the period 1993-94 to 2003-04 is not

regular. The growth rate has shown increasing trend up to

1996-97. I n the next two years there was a negative growth rate

followed by substantial growth rate of about 53 percent in

1999-2000. Again there was a negative growth rate in the

succeeding year followed by marginal increase in the next two

years. Only in the latest year i.e. 2003-2004 the growth rate is at

an encouraging level of 29.48 percent.

The above analysis of sales trend reveals that the market for

passenger cars is not stable and regular. I t is highly fluctuating

from year to year. Of all the years there was highest growth rate of

52.94% during the year 1999-2000. It is interesting to note that

there was negative growth in both preceding and succeeding years.

However, it is encouraging to note that the value of car sales which

was rupees 3,845 crores in 1993-94 increased manifold to 22,940

crores in 2003-2004, thus registering a record growth of about 6

times.

Chapter 3

TABLE 3.3

TOTAL CAR SALES I N INDIA ---

~ e a r - p " C r o i F % of growth

Source: CMIE, Mumbai.

10. MARKET SHARES OF LEADING CAR MANUFACTURERS

The particulars of market share of different leading car

manufacturing companies are presented for the period from

1992-93 to 2003-2004 in table 3.4. I t can be easily noticed from

the table that Maruti has the lion share of more than 50 percent in

the Indian car market up to 1999-2000. Thereafter, its market

Chapter 3 76

share has slowly declined. I ts share, which stood at around 70

p e r c e ~ t up to 1998-99, has declined to 46.15 percent in 2003-04.

And H~undai , a latest entry in the Indian car market started its play

with 4.64 Percent share in 1998-1999, increased its market share

to around 24 percent in the recent years. TATAs, a leading Indian

industrial giant has been increasing its share in the Indian car

market from around 3.5 percent in 1992-93 to around 12 percent in

2003-2004. The success of its Indica model can be the single major

factor which contributed greatly for the increase of TATA's market

share. Other car manufacturers like Daewoo, Ford and Honda are

having a share of around 5% each in the Indian car market. Of

these, three players, Daewoo and Honda have been struggling hard

to maintain their share around 5% and the other company i.e., Ford

has been striving hard to improve its share from 2.5% in 1997-98

to around 4 percent in the recent years. One significant change

noticeable from the table is that Premier Company has been

constantly losing its share in the Indian car market from 11.34°/~ in

1992 - 1993 to an insignificant share of 0.0l0/0 in the recent years.

The impact of imports in the Indian car market is insignificant with

less than one per cent share all through the period under study.

To sum up, Hyundai, TATAs, Ford and others are improving

their shares, while Maruti and Premier are losing their shares in the

Indian car market.

Chapter 3

TABLE 3.4

MARKET SHARE OF LEADING PLAYERS I N PASSENGER CAR MARKET

(Percent)

Source: CMIE, Mumbai

-- .

Brand

Name

1.Marut1

2.Hyunda1

3 Tata

4.H M.

5.Daewoo

6. Ford

.- -,

7.Honda

8,Premler

9,Others

0.88 0.52 0.34 0.25 0.25 1.31 0.01

1992-

1993

69 72

-

-

3 53

15.04

-

-

--

11.34

0.07

1993-

1994

65.90

- " -

7 25

-- -

14.11

-----

11.93

0,07

1994-

1995

66.75

---- --

- .

9 84

-

10.50

8.07

4,41

---

1995-

1996

69.56

6 63

8.67

5.61

4.58

-

4.04

- A

1996-

1997

69.63

2.60

.

6.58

8.39

,----

2,80

9.24

1997-

1998

71.37

- ..

~-

1 6 2

5.55

3.08

2.50

2.71

12.29

- ---

1998-

1999

68 48

4.64

1.24

6.33

3,20

2.09

5.66

0.98

6-86

1999-

2000

-

52 47

13 78

- .

9.77

-.,a

7.18

6-32

2.04

3.86

O,11

4.13

--I

2000-

2001

-

48.17

17 02

7.34

-

6 50

----

5.71

5.39

4.03

0.01

5-58

_.+---.m

2003-

2004

46.15

23.93

--".--"----

12.29

2.67

6,61

8034

- 1-1,-1"

2001

2002

47.21

18.45

10.96

4.88

1.38

3.86

4.61

-

8.4

.--..

2002-

2003

47.02

-

21.14

- -"

12.08

4.71

1.35

-

5,21

0,01

7.17

Chapter 3

11. INDIAN EXPORTS OF PASSENGER CARS

As seen from Table 3.5, about 32,000 cars were exported in

1995-96 and in the succeeding year a growth of 13.84O/0 took place.

Thereafter, there is negative growth up to 2000-2001. However, the

export of Indian passenger cars has picked up again from 2001-

2002, in which year there is more than 100% growth. The growth

rate has again declined to 41.33 percent in 2002-2003 and rose to

78.29 percent in 2003-2004. The entry of global giants in car

manufacturing industry in India has lead for the increasing growth

of exports from India in the recent years.

TABLE 3.5

INDIAN EXPORTS OF PASSENGER CARS

Source: 1. *CMIE, Mumbai

2. ECONOMIC SURVEY OF INDIA 2004 - 2005

Chapter 3

CAPACITY UTILIZATION

Except Maruti Udyog Limited (MUL), all the car manufacturing

companies have been found producing much below their installed

capacities. Maruti topped the list for its capacity utilization level of

the order of 135 percent in 1998-99. The passenger car industry's

overall capacity utilization was recorded around 60 percent in the

same year.

12. PROSPECTS

With the up gradation of technologies, the users have

developed liking for efficient, sleek and spacious cars. The growing

popularity of Maruti cars has not only inflated the demand for cars

but also expanded the market for cars with more advanced

technologies. Some of the modern passenger cars with world-class

technologies recently introduced in the Indian panorama are Santro

(Hyundai), Matiz (Daewoo). Ikon (Ford), Fiat Uno (PAL), Zen

(Maruti), Lancer (Mitsubishi), Honda City (Honda), Astra (GM),

Esteem (Maruti), Cielo (Daewoo) and Indica (Tata).

For better prospects of passenger car industry, there should

be competitiveness among the manufactures in the adoption of the

latest technology with low consumption of fuel and more indigenous

components. This would help in reducing the cost of car as well as

the costs on repairs and replacements after sales. Widened and

Chapter 3

CAPACITY UTILIZATION

Except Maruti Udyog Limited (MUL), all the car manufacturing

companies have been found producing much below their installed

capacities. Maruti topped the list for its capacity utilization level of

the order of 135 percent in 1998-99. The passenger car industry's

overall capacity utilization was recorded around 60 percent in the

same year.

12. PROSPECTS

With the up gradation of technologies, the users have

developed liking for efficient, sleek and spacious cars. The growing

popularity of Maruti cars has not only inflated the demand for cars

but also expanded the market for cars with more advanced

technologies. Some of the modern passenger cars with world-class

technologies recently introduced in the Indian panorama are Santro

(Hyundai), Matiz (Daewoo). Ikon (Ford), Fiat Uno (PAL), Zen

(Maruti), Lancer (Mitsubishi), Honda City (Honda), Astra (GM),

Esteem (Maruti), Cielo (Daewoo) and Indica (Tata).

For better prospects of passenger car industry, there should

be competitiveness among the manufactures in the adoption of the

latest technology with low consumption of fuel and more indigenous

components. This would help in reducing the cost of car as well as

the costs on repairs and replacements after sales. Widened and

Chapter 3

smooth metalled roads and removal of traffic hazards are the other

prerequisites. I n this regard, special infrastructural development

programs are currently being implemented in the country.

The tremendous rise (47%) in the sales of domestic

passenger cars in 1999 over 1998 has attracted car manufactures

for significant demand projections in the new millennium. Car

manufacturers predicted a growth of 12 percent in automobile

industry, 8-9 percent in upper mid-size segment, and 8-10 percent,

in the small car segment in the year 2000. The industry sources are

of the view that the lower end of the mid-size segment, comprising

cars like Ford's Ikon, Hyundai's Accent and GM's Corsa, would

witness a 50 percent growth. The next segment that would see

substantial growth is the so-called lower end of the luxury market,

currently dominated by the Esteem. This segment has seen a large

number of new entrants in recent times.

The analysis on the performance of Indian passenger car

industry shows that the Maruti has maintained its lead over all the

established competitors as well as new entrants. It has reportedly

achieved the record sale of nearly 370,000 cars in the calendar year

1999.

As seen in the earlier pages, the Indian car industry is

undergoing a gargantuan change. Vehicle manufacturers are vying

with each other to offer sophisticated and top line features to their

Chapter 3 8 1

customers. They are confronted with an impatient customer who

suddenly has a rich menu of attractive cars to choose from. A

fiercely competitive environment is under way, where customers'

satisfaction rules.

The demand for cars is a function of the increase in the

threshold income in the country. Probity research estimates that to

be able to afford a car, a household should have an annual income

of at least Rs. 1.6 lakh. Only 7.8 million households in India are

identified to fall under this income group. Considering that all these

homes do not have cars yet, demand for cars is expected to

increase. These findings have far reaching and revolutionary

implications for the passenger car market in India. Disposable

household income is no longer the only single most important factor

in determining the demand for vehicles. Other critical factors are

the mobility needs of people and the availability of cheap finance.

Car production capacity has increased substantially in the last

two years. I n fact, it is expected to increase from around 750,000

(1999) to 1,210,000 in 2001, according to probity research. I f this

happens, the industry will witness a gut-wrenching shake out, since

everyone cannot afford to continue operating in low capacity

utilization, losing large sums of money in the name of "long haul"

and dreams of "eventual success".

Chapter 3

The development of the used car market will play a major

role, as the customers will be encouraged to trade in their old cars.

As a firm steps in this direction, Ford Motors introduced "used car"

initiative under "Ford assured" brand dealership.

The lack of adequate public transportation system coupled

with the fact that the electric of hybrid cars are still in the

development stage means that the Indian car industry faces

minimal competition from substitutes.

Although liberalization of the Indian economy has reduced the

impact of government policy as an entry barrier, the car industry

still enjoys high entry barrier due to huge capital costs involved in

setting up efficient plants and numerous cost advantages enjoyed

by Maruti. The pullout of Peugeot is an example that even a global

automobile company could find it extremely difficult to operate in

India if i t faces labour trouble and problems with its joint venture

partner. With so many players in the market the current game in

India is not about stealing market share but increasing the size of

the market on the whole.

The competition between firms in the car industry is expected

to intensify considerably as new companies will start reducing

Ma rut its dominance in the market. The expected over-capaci ty in

the industry, increasing working capital needs, and high exit barrier

coupled with low differentiation between models especially in the

economy segment, will put downward pressure on prices and

profitability of companies.

The entry of the global car manufacturers has transferred the

balance of bargaining power into the hands of the buyer. The Indian

car buyers are not only extremely price-conscious, but also want

the highest value and service. Huge dealerships, member clubs,

mobile squads, and replacement vehicles are just some of the sops

being offered to the customer. The availability of cheap financing

and maturing of the used car market will also increase the choices

for the consumers.

With many new models waiting to be launched, the Indian car

buyer will have more scope to choose and dictate terms to the

dealer. On the whole, car market is changing from sellers to the

buyers market and car companies are becoming more and more

customer-centric. They are coming up with various promotional

activities, attractive investment schemes, etc., to lure the customer.

The orientations of their strategies are shifting from push to pull. No

doubt, the customer is at the driver's seat.

Supplier power in the car industry will diminish greatly in the

coming years due to the larger number of competing suppliers,

threat of cheaper and better quality imports, and an increasing

trend towards reduction of a car company's vendor base. The

diminishing power of the suppliers industry will help the industry in

Chapter 3 84

improving the quality of car components and getting longer

payment periods. The key to succcss in the Indian car market will

be offering good quality cars that offer value for money, run

innovative marketing campaigns to attract potential buyers and

offer excellent after-sales service.

Thus the Indian passenger car market has now passing

through dynamic phase and the economy car segment accounts for

the major share in the passenger car market. Significant

opportunities exist for players to spot gaps in the market and cater

to particular niche markets. Companies, which have a range of

vehicles in all the segments of the market, like Maruti, will have

significant advantage due to their ability to cross-subsidies models.

The key to growth of the future car market is to make

maintenance-free vehicles, to improve the road infrastructure and

to reformulate fuels and lubricants so as to reduce vehicle-operating

costs.

The great Indian car wars have just started and whatever

company wins, the final winner will be THE INDIAN CUSTOMER.