· pdf filescores highest among gcc on ... as can also be seen in the fall in dubai property...

TRANSCRIPT

Mashreq

INVESTOR PRESENTATION

December 2017

2

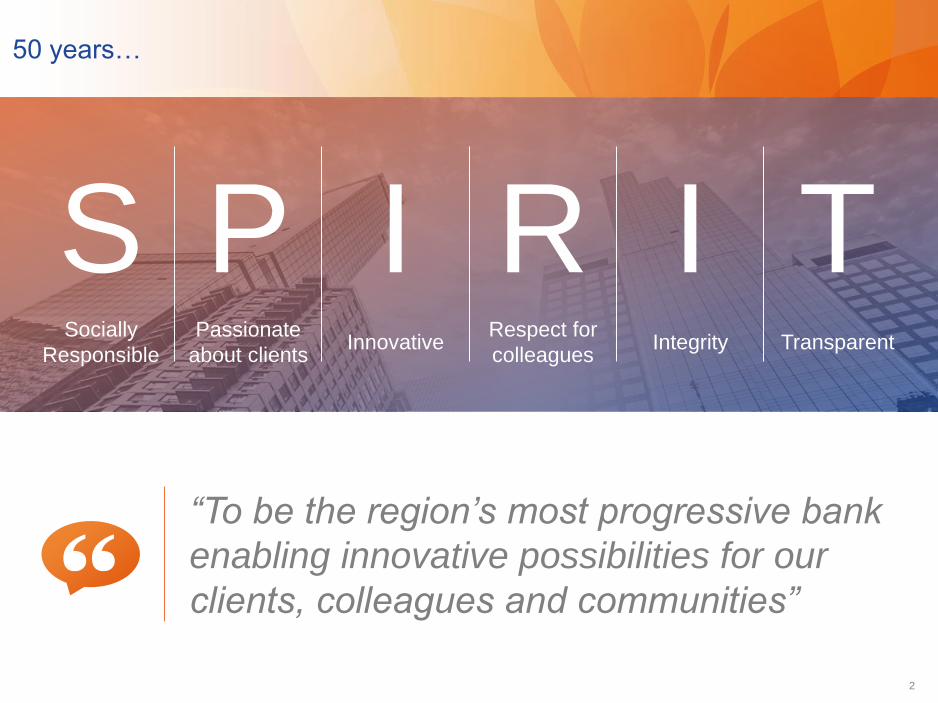

50 years…

S P I R I TSocially

Responsible

Passionate

about clientsInnovative

Respect for

colleaguesIntegrity Transparent

“To be the region’s most progressive bank

enabling innovative possibilities for our

clients, colleagues and communities”

3

Mashreq

Investor

Presentation

UAE economy

Mashreq heritage

Structure and Leadership

Strategy

Financial track record

Trading history, rating and dividends

Corporate governance

Accolades

4

3.53.23.0

2.62.0

1.7

KSA Bahrain Oman Qatar UAE Kuwait

UAE is the 2nd largest economy in the GCC, with promising economic growth

prospects

UAE - The second largest economy in the GCC Real GDP Growth Potential

– 2017-22F (%)

A1 B1 Baa2 Aa3 Aa2 Aa2

Sovereign Rating

by Moody’s

72 679 34 118 379 166

Nominal GDP per Capita – 2017

(USD thousand)

GDP Breakdown by Sector – 2016

(%)Nominal GDP

2017 (USD billion)

Source: IMF WEO October 2017,CIA & OPEC, Moody‘s Ratings, National Bureau of Statistics

UAE ECONOMY – MACROECONOMIC OUTLOOK

▪ Second largest economy in the GCC with nominal GDP of

USD 379bn in 2017

▪ Well diversified economy with oil & gas contributing only

~21% of the total GDP

▪ Despite fall in oil prices, UAE economy remained strong

with current account surplus at 2.1% of GDP in 2017

▪ Holds 8.0% of the proven OPEC crude oil reserves,

primarily concentrated in Abu Dhabi

▪ Young population with ~61.1% aged between 25-54 years

and a literacy rate of ~94%

60.8

37.3

21.017.425.2 27.2

KSAOman UAEKuwaitBahrain Qatar

9%10%

10%

7%

13%

15%

7%

7%

1%

21%Construction

Government Services

Wholesale Retail Trade

Other

Transport, Storage & Communication

Real Estate

Financial Corporations

Manufacturing

Crude Oil and Natural Gas

Agriculture

5

1 Rank out of 137 economies

UAE ECONOMY – MACROECONOMIC OUTLOOK

Current Account Balance to GDP – 2017

(%)

Govt. Net Borrowing to GDP – 2017

(%)

Global Competitiveness Index – 2017-18 Ranking1 Inflation to Remain Stable Over the Medium Term

(%)

One of the best ranked economies on global competitive index among the

GCC nations

Source: IMF WEO October 2017, World Economics Forum-Global Competitiveness Index 2017

1.5

-1.0-3.7

-8.6-13.0-13.2

Bahrain Oman KSA UAE Qatar Kuwait

2517

30

UAE Qatar

44

KSA

52

Bahrain

62

Kuwait Oman

2.32.10.6

-0.6-4.6

-14.3

Kuwait KSA QatarUAEOman Bahrain

1.9

2.32.42.3

2.9

2.1

2018E2017E 2019E 2021E 2022E2020E

6

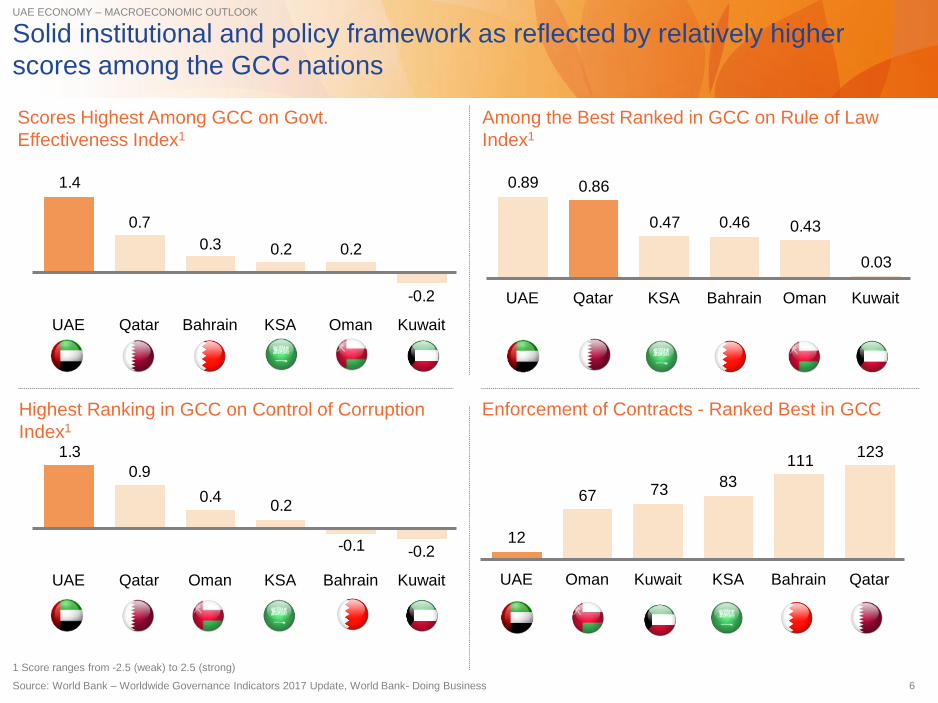

UAE ECONOMY – MACROECONOMIC OUTLOOK

Scores Highest Among GCC on Govt.

Effectiveness Index1

Among the Best Ranked in GCC on Rule of Law

Index1

Highest Ranking in GCC on Control of Corruption

Index1

Enforcement of Contracts - Ranked Best in GCC

Solid institutional and policy framework as reflected by relatively higher

scores among the GCC nations

0.03

0.430.460.47

0.860.89

KuwaitUAE Qatar KSA Bahrain Oman

-0.2-0.1

0.20.4

0.9

1.3

KSAOman KuwaitBahrainUAE Qatar

-0.2

0.20.20.3

0.7

1.4

BahrainQatarUAE KSA Oman Kuwait

123111

837367

12

OmanUAE QatarBahrainKuwait KSA

1 Score ranges from -2.5 (weak) to 2.5 (strong)

Source: World Bank – Worldwide Governance Indicators 2017 Update, World Bank- Doing Business

7

Non-oil growth is supported by strong hospitality and logistics sectors

UAE ECONOMY – MICROECONOMIC OUTLOOK

Non-oil growth continues to be steady with PMI remaining

above 50

Emirates NBD UAE PMI index

Increasing rate of growth

The hospitality sector, especially in Dubai, is one of the major

growth drivers …

Hotel guests (million) Air passengers (million)

50 – no change on previous month

Increasing rate of contraction

15.814.9

14.213.2

11.010.0

4.94.44.13.52.82.4

201720162015201420132012

8884

7870

6658

252523201715

201720162015201420132012

Abu DhabiDubai

2.3 2.4 2.4 2.5 2.6 2.7

2017

3.5

0.8

2016

3.4

0.8

2015

3.3

0.8

2014

3.2

0.8

2013

3.1

0.7

2012

2.9

0.6

Abu DhabiDubai

21.020.421.220.218.618.0

668 685 696952 969

170

185 195219 232 244

419 400

944

185

433

1,563

1,057

1,5641,556

1,072

132

1,065

148

20162013 20152012 2014 2017

… along with the logistic sector

UAE container volumes (TEU million)

UAE air freight (million tonnes)

Non-oil direct trade flows have witnessed steady growth over the

last few years

UAE non-oil direct trade flows (AED billion)

CAGR

’12-’17

7.2%

1.8%

14.6%

Source: Emirates NBD, Federal Customs Authority, Hotel and Airport authorities of UAE, World Bank, Khaleej Times, National

40

45

50

55

60

65

585756

55

585656

55565756

5555

Dec-

16

SepAugJulJunMayAprMarFebJan Oct Nov Dec-

17

ImportsExportsRe-exports

8

40

45

50

55

60

65

Consumer borrowing has slowed due to flat employment levels

Source: JLL, UAE Central Bank, Emirates NBD

UAE ECONOMY – MICROECONOMIC OUTLOOK

… due to flat employment levels

Emirates NBD Employment index (#)

Increasing rate of growth

50 – no change on previous month

338326311283

265

+6%

20172016201520142013

5151515152515051

5251515252

SepAugJulJun NovOct Dec-17

MayAprMarFebJanDec-

16

Increasing rate of contraction

… as can also be seen in the fall in Dubai property prices over the

year

Mashreq Property Price Index (%)

Domestic credit to Individuals (AED Bn)

Consumer borrowing growth has slowed…

Rents continue to be falling …

Dubai 4Q ‘17 Abu Dhabi 4Q ‘17

Residential Office Retail Hotel

Rent

falling

Rent

bottoming

out

Rent

growth

slowing

Rent

growth

acceler-

ating

Rent

falling

Rent

bottoming

out

Rent

growth

slowing

Rent

growth

acceler-

ating

0.0-0.1-0.1-0.2-0.2-0.2-0.2-0.2-0.2-0.2-0.2-0.5-0.2

13.713.713.813.914.014.314.414.714.815.015.315.515.9

-5

0

5

10

15

20

Oct-

17

Sep-1

7

Aug-1

7

Jul-

17

Jun-1

7

May-1

7

Apr-

17

Mar-

17

Feb-1

7

Jan-1

7

De

c-1

6

Dec-1

7

Nov-1

7

Avg MPPI inc (%) Cum MPPI inc (%)

9

UAE ECONOMY – BANKING SECTOR OVERVIEW

Diversified and Well Regulated Banking Sector GCC Banking Assets1 – 2017 (AED billion)

UAE – Gross Credit & Deposits (AED billion) UAE – Loans by Sector – 9M 2017 (%)

Total Banking Assets to GDP Ratio

Regulated & Diversified Banking Environment

194% 91% 226% 178% 101% 173%

215267774

1,378

2,2602,695

BahrainKSA Qatar KuwaitUAE Oman

▪ As of December 2017, UAE banking sector comprised 49

banks

– 22 National Banks with 771 branches and

– 27 Foreign Banks with 82 branches

▪ Diversified loan portfolio - Real Estate and Construction

sector accounted for only ~20% of loan book in 9M 2017

▪ Well regulated banking system, in line with internationally

followed best practices

▪ UAE Banking sector has a long-standing track record of

Government support during crisis situations

Deposit

Gross credit

1,5811,5741,485

1,2761,378

1,6271,5631,472

1,2791,168

1,421

2012 20152013 2014

1,184

20172016

CAGR 2012- 2017: 6.0%

Source: UAE Central Bank, Central Bank of other respective countries, IMF WEO October 2017, Khaleej Times

6%

5%

10%

11%

1%

20%

9%

22%

0%1%

4%

9%

Electricity, Gas and Water

Transport, Storage & Comm

Personal Loans for Business

Manufacturing

Trade

Government

Others2

Mining and Quarrying

Construction and Real Estate

Financial Institutions (Ex. Banks)

Personal Loans for Consumption

AgricultureCAGR 2012- 2017: 6.9%

1Data for Bahrain relates to Nov 2017

10

Mashreq

Investor

Presentation

UAE economy

Mashreq heritage

Structure and Leadership

Strategy

Financial track record

Trading history, rating and dividends

Corporate governance

Accolades

11

Mashreq is one of UAE's leading financial institutions

Established in 1967 by the Al-Ghurair Group

51 years in UAE banking and financial services marketHeritage

Oldest regional bank based out of UAE

Combines the entrepreneurial spirit of Dubai with enduring trade banking relationships across the region

Listed on the DFM on creation of local stock exchange

Publicly listed

Prominent Regional bank with presence in most GCC countries and leading international network with

24 branches / rep-offices in MENA, Asia, Europe and United States

Well positioned to finance regional trade flows

Strong

regional /

international

presence

Universal bank offering a comprehensive suite of products and services to individuals and corporates

across all lines of business

Most diversified revenue streams with fee and other income contributing over 40% of total income; high

degree of geographic diversification with 21% of revenue coming from outside UAE

Diversified

business case

Long serving senior executives along with international management expertise delivering a robust

growth model

Led by Abdul Aziz Abdulla Al-Ghurair, Chief Executive Officer for 28 years

Strong

management

team

Al-Ghurair Group, the main shareholders of the bank, are a leading conglomerate in the UAE with

numerous business interests

Featured in the Forbes billionaire list for the last 10 years

Mashreq is the flagship business for the family for over 50 years

Strong and

supportive

ownership

structure

MASHREQ HERITAGE

12

Ownership – Al-Ghurair flagship brand

Key shareholders (December 2017)

Stable and supportive ownership structure

MASHREQ HERITAGE

Mashreq’s Leadership

Mr. Abdulla Bin Ahmad Al-Ghurair

Chairman

H.E. Abdul Aziz Abdulla Al-Ghurair

Chief Executive Officer & Director

9.6%

3.5%

3.6%

12.7%

31.1%

39.5%

Other shareholders

National Cement Company

Majid Capital

Masar Investments

Abdulla Ahmed Al Ghurair Inv. Co.

Saif Al Ghurair Investment LLC

▪ One of the most prominent businessmen and

industrialists in the UAE

▪ Former Chairman of the UAE Banks Association

▪ Chairman of UAE Banks Federation

▪ Vice Chairman of the higher board of DIFC

▪ Chairman of Masafi

▪ Chairman of Oman Insurance

▪ Board Member of Emirates Foundation

▪ Former Speaker of the Federal National Council

▪ Al-Ghurair families holds the majority stake in

Mashreq (approximately 87%) and are the

founders of the Bank

▪ Al-Ghurair family has a strong commitment to

the continued growth and financial solidity of

Mashreq

▪ Al-Ghurair family is one of the oldest and

wealthiest families in the UAE

– Featured in Forbes billionaire list for over

10 years

– Business interests include shopping

malls, real estate, cement manufacturing,

food industries, Masafi (mineral) water,

contracting, trading, retailing, shipping,

printing & packaging, aluminium

extrusion, building materials, oil refinery,

manufacturing, steel and canning

▪ Mashreq’s shares are listed and traded on

the Dubai Financial Market

13

Strong distribution network in the UAE with 26 branches in Dubai

MASHREQ HERITAGE

Umm Al Quwain

1 branch

Abu Dhabi

12 branches

Ajman

1 branch

Ras Al Khaimah

1 branch

Fujairah

1 branch

Sharjah

8 branches

Dubai

26 branches

Alternate Channels

▪ 50 branches (out of which Mashreq Gold has

presence in 29 branches and SME Banking has

presence in 24 branches) and a Retail Customer

Service Center in UAE serving ~500K customers

▪ ATMs and CCDMs increased coverage to 343 units

in UAE

▪ 35,000 POS machines spread 14,000 merchant

location in the UAE. Second Largest Merchant

acquirer in the UAE with close to 30% market share

▪ Internet Banking through Mashreq Online (Retail incl.

Brokerage), Mashreq Business online (Corporate),

Mashreq-FI online (Correspondent Banking); 306,662

active users are registered with online banking

▪ Mobile banking services: Snapp registration has

grown up by 29% year on year and financial

transactions has grown by 21% as compared to last

year figures. Snapp has been recently upgraded with

unique new features such as transfer your credit card

balance from other banks card control, Quick remit to

Pakistan, Mashreq Pay and Samsung Pay.

▪ Fully integrated electronic platform for transaction

banking (GTS)

▪ State of the art Polaris System (mashreqMATRIX) to

provide online services to corporate customers

▪ 24 x 7 Direct Banking Call Centre

14

Regional and international banking presence with 21% of revenues from

outside of UAE

International

branches

Financial Institution

branches

New York

London

Representative

Offices

Hong KongIndia

Bangladesh

NepalPakistan

EgyptKuwait

Bahrain

Qatar

MASHREQ HERITAGE

15

Strong track record in International expansion

972

1967

1971

1980

1984

2009

1978

1981

2001

2010

UAEEgypt, London,

Pakistan, Hong Kong Nepal

Qatar India Kuwait

10

11

12

Presence in number of countries

Bahrain

New York

Bangladesh

MASHREQ HERITAGE

16

Mashreq

Investor

Presentation

UAE economy

Mashreq heritage

Structure and Leadership

Strategy

Financial track record

Trading history, rating and dividends

Corporate governance

Accolades

17

Mashreq organization chart

STRUCTURE AND LEADERSHIP

Note: Financials as of 30 December 2017

Board of Directors

Chief Executive Officer

Corporate Banking

Group (CBG)(23% of revenue)

Treasury & Capital

Markets (TCM)(10% of revenue)

Retail Banking

Group (RBG) (26% of revenue)

International Banking

Group (IBG)(21% of revenue)

Corporate Affairs

(CA)

Audit , Fraud &

Compliance Group

(AFCG)

Risk

Management (RM)

Operations &

Technology (O&T)

18

Mashreq is a well diversified universal bank that covers significant lines of

business with a full product and channel suite

Corporate Banking

Group (CBG)

Energy, Services &

Manufacturing

Trading

Contracting Finance

Real Estate

NBFI

Emerging Corporates

Division

Global Transaction

Services

Corporate Finance

Islamic Banking products

Offers wholesale banking

Treasury & Capital

Markets (TCM)

FX and Investments

Rates & Structured

Solutions

Mashreq Capital

Islamic banking products

Equity Derivatives &

Institutional Sales

Mashreq Securities

Investments

Offers treasury &

investment products

Retail Banking Group

(RBG)

Personal Banking

SME

Mashreq Gold

Private Banking

Payments

Islamic banking products

Distribution

Alternate Channels

Direct Sales

Direct Banking Centre

Offers personal banking

International Banking

Group (IBG)

Wholesale and

investment banking

Treasury and investment

products

Personal banking

Financial Institutions

globally

Islamic banking products

Offers banking services

outside UAE

Note: Islamic banking and Insurance segments contributes the remaining revenue

STRUCTURE AND LEADERSHIP

19

Oman Insurance is the largest subsidiary of Mashreq

Mashreqbank Psc

Note: Figures are based on draft audited statements

Mashreq Al Islami Finance (99.8%)

▪ Islamic Finance Company

▪ Provides full range of Islamic Products & Services

▪ Dec ’17 Equity: AED 832 Mn

▪ FY 2017 profit: AED 37 Mn

Mashreq Securities (99.98%)

▪ Securities brokerage Company registered at Dubai

Financial Market

▪ One of the leading brokerage in the UAE

▪ Dec ’17 Equity: AED 79 Mn

▪ FY 2017 Profit: AED 3 Mn

Oman Insurance Company (63.94%)

▪ Largest insurance company in the UAE

▪ Provides full range of Insurance Products &

Services

▪ Dec ’17 Equity: AED 2,039 Mn

▪ FY 2017 profit: AED 105 Mn

Mashreq Capital (100%)

▪ Registered in DIFC for Brokerage, Asset

Management and Fund Management services

▪ One of the largest asset management in UAE with

USD 800 mn in asset under management

▪ Funds rated highest in the market

▪ Dec ’17 Equity: AED 26 Mn

▪ FY 2017 profit: AED 4 Mn

STRUCTURE AND LEADERSHIP

20

Corporate Banking (CIBG) business

STRUCTURE AND LEADERSHIP

1,3611,3191,324

+3%

2017

0%

20162015

CIBG Revenues (AED million)Business highlights

CIBG Assets (AED million)

▪ Corporate banking is the biggest segment in Mashreq in

terms of assets (26% of total assets) & liabilities (31% of

total liabilities)

▪ Corporate Banking Group provides financing solutions to

corporate and commercial customers in the UAE

▪ Major products offered include trade finance, contracting

finance, project finance, corporate finance advisory and

cash management

▪ Corporate Banking has moved to a best-in-class, expertise-

led coverage model for clients. The relationship teams have

been realigned into industry verticals that best serve the

corporate financial needs. Our diverse industry coverage

includes among others: Contracting Finance, Services &

Manufacturing, Government, Multinational Corporates, Real

Estate, Trading Companies, Non-Banking financial

Institutions and Emerging Corporates – including DXB NE &

Abu Dhabi.

▪ The Corporate Finance team has retained its position

amongst the premier institutions for debt capital raising in

the region. Mashreq was amongst the top 5 loan

Bookrunners in the GCC per Bloomberg

▪ Mashreq’s Global Transaction Services team maintained its

regional dominance in the transaction banking space by

winning 8 awards in 2017 for Trade finance, Factoring and

Cash Management.

▪ In line with its Mission Mashreq continued to lead

innovation, GTS won the innovators award 2017 by Global

Finance for providing cardless cash to its corporate clients,

a first in the region solution. Mashreq was also the first bank

to go live in the region with SWIFT ‘s Global Payment

Initiative.

32,79830,91129,501

+5%+6%

Dec-17Dec-16Dec-15

21

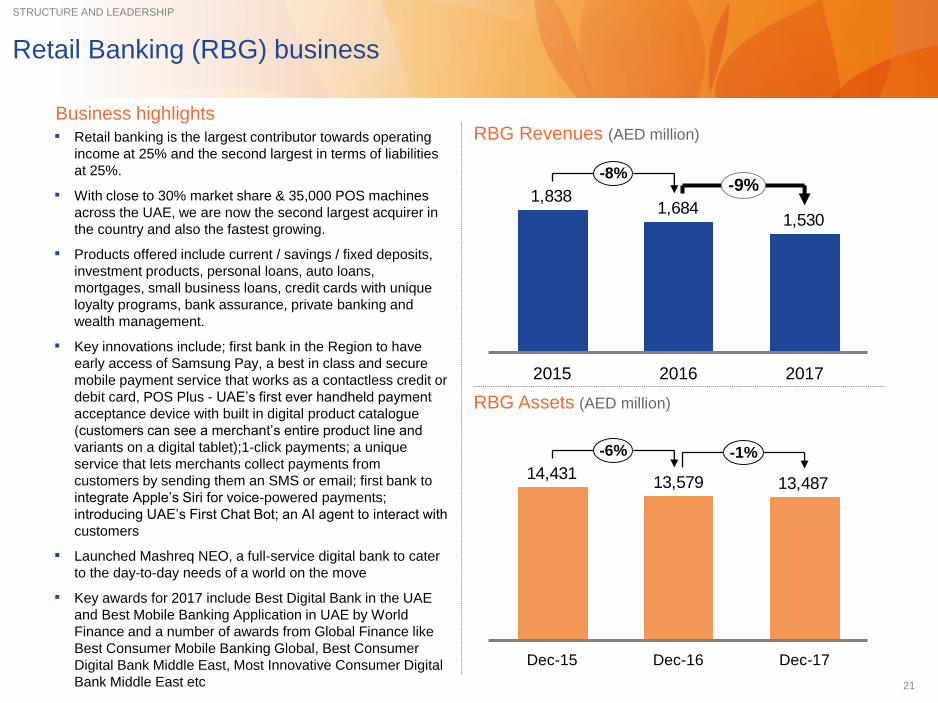

Retail Banking (RBG) business

13,48713,57914,431

-6% -1%

Dec-17Dec-16Dec-15

STRUCTURE AND LEADERSHIP

1,5301,684

1,838

2017

-8%

20162015

-9%

Business highlights

▪ Retail banking is the largest contributor towards operating

income at 25% and the second largest in terms of liabilities

at 25%.

▪ With close to 30% market share & 35,000 POS machines

across the UAE, we are now the second largest acquirer in

the country and also the fastest growing.

▪ Products offered include current / savings / fixed deposits,

investment products, personal loans, auto loans,

mortgages, small business loans, credit cards with unique

loyalty programs, bank assurance, private banking and

wealth management.

▪ Key innovations include; first bank in the Region to have

early access of Samsung Pay, a best in class and secure

mobile payment service that works as a contactless credit or

debit card, POS Plus - UAE’s first ever handheld payment

acceptance device with built in digital product catalogue

(customers can see a merchant’s entire product line and

variants on a digital tablet);1-click payments; a unique

service that lets merchants collect payments from

customers by sending them an SMS or email; first bank to

integrate Apple’s Siri for voice-powered payments;

introducing UAE’s First Chat Bot; an AI agent to interact with

customers

▪ Launched Mashreq NEO, a full-service digital bank to cater

to the day-to-day needs of a world on the move

▪ Key awards for 2017 include Best Digital Bank in the UAE

and Best Mobile Banking Application in UAE by World

Finance and a number of awards from Global Finance like

Best Consumer Mobile Banking Global, Best Consumer

Digital Bank Middle East, Most Innovative Consumer Digital

Bank Middle East etc

RBG Revenues (AED million)

RBG Assets (AED million)

22

Treasury and Capital Markets (TCM) business

17,58517,00415,657

+9% +3%

Dec-17Dec-16Dec-15

STRUCTURE AND LEADERSHIP

616564553

2017

+2%

20162015

+9%

Business highlights

▪ Treasury & Capital markets accounts for 14% of

assets and 9% of liabilities as of December 2017

▪ Treasury and Capital Markets business consists of

customer flow business and proprietary business.

Customer flow business includes transactions for

FX, derivatives, hedging, investment products,

equities and regional asset management undertaken

on behalf of customers. Proprietary business

includes trading and investing activity undertaken on

behalf of the bank

▪ Mashreq was able to grow its Treasury product suite

across asset classes, supported by an online trading

platform and 24 hour dealing room

▪ The Rates & Structured Solutions business closed

several large ticket hedging transactions for clients

across the region, including a structured profit rate

swap for a real estate loan

▪ Makaseb Income Fund won Thomson Reuters

Lipper Fund award for Best Fund Performance over

5 Years

TCM Revenues (AED million)

TCM Assets (AED million)

23

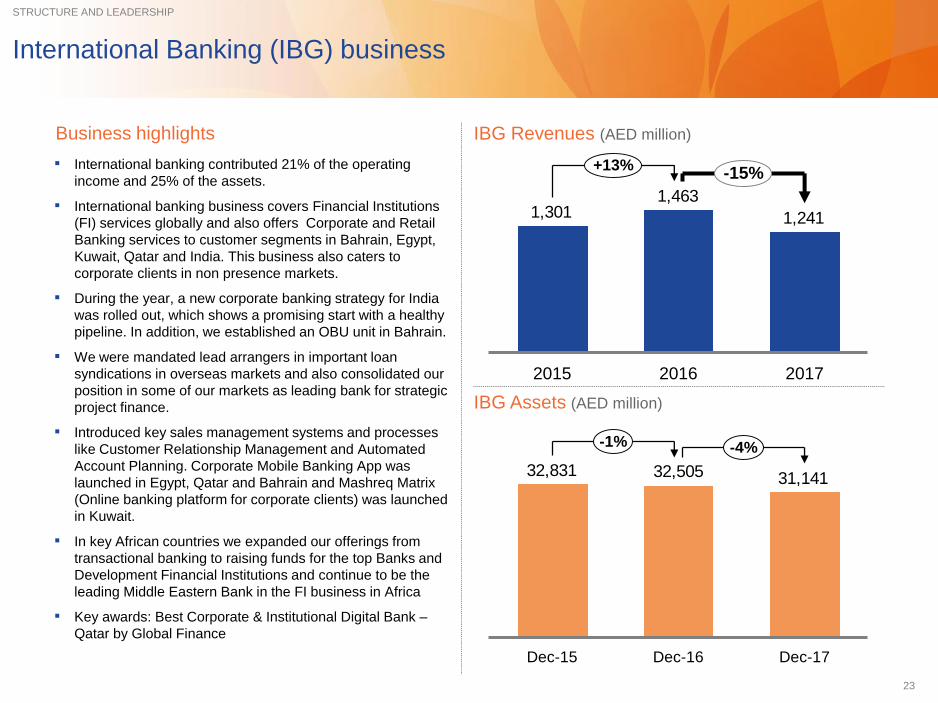

1,241

1,4631,301

2017

+13%

20162015

-15%

International Banking (IBG) business

31,14132,50532,831

-1% -4%

Dec-17Dec-16Dec-15

STRUCTURE AND LEADERSHIP

Business highlights

▪ International banking contributed 21% of the operating

income and 25% of the assets.

▪ International banking business covers Financial Institutions

(FI) services globally and also offers Corporate and Retail

Banking services to customer segments in Bahrain, Egypt,

Kuwait, Qatar and India. This business also caters to

corporate clients in non presence markets.

▪ During the year, a new corporate banking strategy for India

was rolled out, which shows a promising start with a healthy

pipeline. In addition, we established an OBU unit in Bahrain.

▪ We were mandated lead arrangers in important loan

syndications in overseas markets and also consolidated our

position in some of our markets as leading bank for strategic

project finance.

▪ Introduced key sales management systems and processes

like Customer Relationship Management and Automated

Account Planning. Corporate Mobile Banking App was

launched in Egypt, Qatar and Bahrain and Mashreq Matrix

(Online banking platform for corporate clients) was launched

in Kuwait.

▪ In key African countries we expanded our offerings from

transactional banking to raising funds for the top Banks and

Development Financial Institutions and continue to be the

leading Middle Eastern Bank in the FI business in Africa

▪ Key awards: Best Corporate & Institutional Digital Bank –

Qatar by Global Finance

IBG Revenues (AED million)

IBG Assets (AED million)

24

Islamic Banking (ISB) business

10,342

8,797

7,595

+16%

+18%

Dec-17Dec-16Dec-15

STRUCTURE AND LEADERSHIP

479

321308

2017

+5%

20162015

+49%

Business highlights

▪ Mashreq Al Islami is the Islamic Banking arm of Mashreq

(Mashreq Al Islami Finance Company PJSC and Islamic

Banking Division, Mashreqbank PSC) and offers a wide

range of Shari’ah compliant products and services

▪ Amongst the top ten Islamic institutions in the UAE based

on market share as per MEED

▪ Products offered include Ijara home finance, Mudarabah

deposit and savings, Musharaka finance, Murabaha

commodity finance, Ijara equipment finance, sukuk

underwriting, Musharaka LC, Murabaha LC, TR Murabaha,

Kafala, Wakala deposit, Reserve Murabaha deposit and

sukuk advisory

▪ Successfully closed a 5 year USD 500 million senior

secured syndicated facility for Ezdan Holding Group

Company, the largest private sector real estate developer in

Qatar - Mashreq Al Islami UAE acted as Mandated Lead

Arranger, Sole Book Runner and Facility Agent for the

facility

▪ “Most Innovative Islamic Banking Solution Provider” by

Global Banking & Finance Review

ISB Revenues (AED million)

ISB Assets (AED million)

25

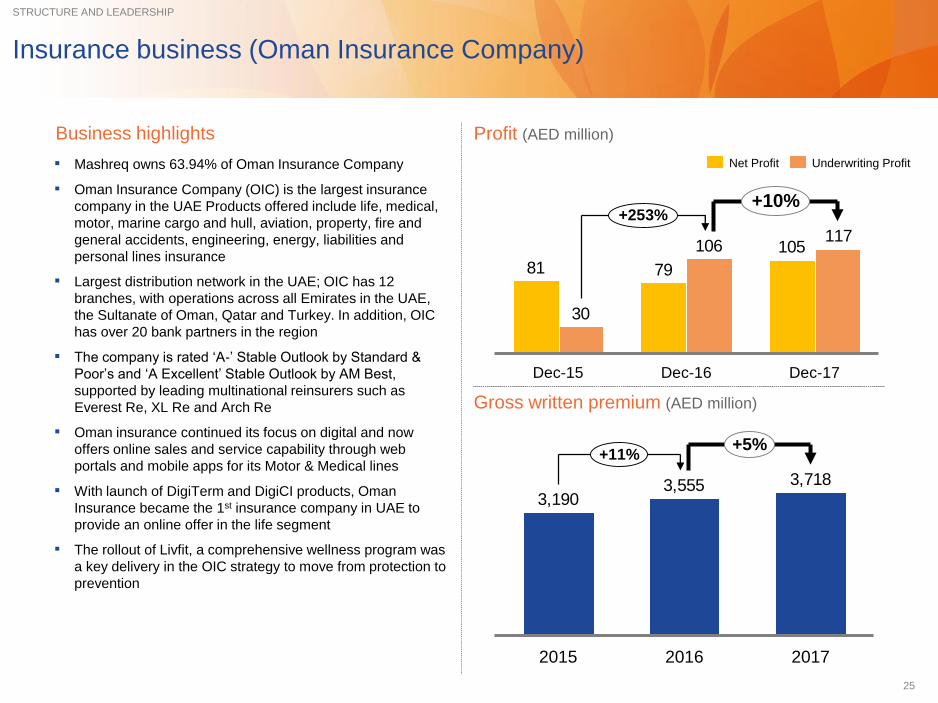

Insurance business (Oman Insurance Company)

STRUCTURE AND LEADERSHIP

Business highlights

▪ Mashreq owns 63.94% of Oman Insurance Company

▪ Oman Insurance Company (OIC) is the largest insurance

company in the UAE Products offered include life, medical,

motor, marine cargo and hull, aviation, property, fire and

general accidents, engineering, energy, liabilities and

personal lines insurance

▪ Largest distribution network in the UAE; OIC has 12

branches, with operations across all Emirates in the UAE,

the Sultanate of Oman, Qatar and Turkey. In addition, OIC

has over 20 bank partners in the region

▪ The company is rated ‘A-’ Stable Outlook by Standard &

Poor’s and ‘A Excellent’ Stable Outlook by AM Best,

supported by leading multinational reinsurers such as

Everest Re, XL Re and Arch Re

▪ Oman insurance continued its focus on digital and now

offers online sales and service capability through web

portals and mobile apps for its Motor & Medical lines

▪ With launch of DigiTerm and DigiCI products, Oman

Insurance became the 1st insurance company in UAE to

provide an online offer in the life segment

▪ The rollout of Livfit, a comprehensive wellness program was

a key delivery in the OIC strategy to move from protection to

prevention

Profit (AED million)

Gross written premium (AED million)

3,7183,5553,190

2017

+11%

20162015

+5%

105

7981

117106

30

+10%

Dec-17

+253%

Dec-16Dec-15

Underwriting ProfitNet Profit

26

Profile of Senior Management

STRUCTURE AND LEADERSHIP

Abdul-Aziz Abdullah Al-GhurairChief Executive Officer

• A Graduate of California Polytechnic State University, H.E. Abdul-Aziz Al-

Ghurair joined Mashreq, then Bank of Oman, in 1977

• He worked in different Divisions and through rigorous training in various

assignments climbed to his current position as of March 1991

Ali Raza KhanHead of Corporate Affairs

• Ali Raza Khan is a Member of the Institute of Chartered Accountants of

India (1978)

• Joined Mashreq in 1980; as Head of Corporate Affairs, he is

responsible for Finance, HR and Administrative functions in the bank

Nabeel Waheed ShaikhHead of Treasury & Capital Markets

• Nabeel Waheed Shaikh has a BSc from Syracuse University, New York

• Joined Mashreq in 1996, from Bank of America, Pakistan where he

spent over 15 years and held various positions including Head of

Corporate Banking

• Jan-Willem Sudmann has a Masters in Economics from the University of

Hamburg, Germany

• Joined Mashreq in 2015; prior to joining Mashreq he was a Managing

Director at Commerzbank Shanghai

• Before joining Commerzbank he worked for close to two decades at

Dresdner Bank across various geographies such as Germany, UK and Egypt

Jan-Willem Sudmann Head of International Banking Group

Arif UsmaniHead of Risk Management Group• Arif Usmani is an alumni of the Imperial College of Science and Technology,

University of London and holds a Bsc (Hon) in Physics

• He recently joined Mashreq from ADIB where he was the Head of Wholesale

banking since 2012

• Before joining ADIB, Arif worked for over three decades with Citigroup across

various geographies such as Pakistan, Saudi Arabia, West Africa, Slovakia,

Hong Kong and Singapore

Sandeep ChouhanHead of Operations & Technology

• Sandeep Chouhan has a Masters in Technology, Management &

Systems from IIT, Delhi, India

• Joined Mashreq in 2015 from CBQ, Qatar

• Prior to this, he was CIO with Barclays and Morgan Stanley

• Nasser A. Paracha has a BSc from the University of Leeds. He completed a

General Management Program from HBS

• Joined Mashreq in 1995 from Deutsche Bank AG in Pakistan

• Overall banking experience of approximately 25 years, covering corporate

banking, internal audit and compliance

Nasser A. Paracha Head of Audit, Fraud & Compliance Group

Ahmed AbdelaalHead of Corporate Banking Group

Subroto SomHead of Retail Banking Group

• Subroto Som is a graduate of IIT Delhi and has an MBA from IIM

Ahmedabad

• Joined Mashreq in 2015 from the Boston Consulting Group

• Prior to this, he has experience at senior positions at Citibank,

Standard Chartered & Seoul First Bank

• Ahmed Abdelaal is an MBA from the London Business School

• Recently joined Mashreq from HSBC where he was the Regional Head

of Corporate Clients Coverage MENAT and Head of Commercial

Banking UAE

• Prior to this, he has experience at senior positions at ABN Amro,

American Express and Arab Bank

27

Mashreq

Investor

Presentation

UAE economy

Mashreq heritage

Structure and Leadership

Strategy

Financial track record

Trading history, rating and dividends

Corporate governance

Accolades

28

Well Defined Strategic Objectives…

“To be the

region’s most progressive

bank enabling innovative

possibilities for our clients,

colleagues and

communities”

VISION

Strategic Objectives

Become primary bank & grow

‘New to Bank’

Enhance brand

Foster innovation & drive digital

transformation

Strategic cost management & middle

office rationalization

Enhance human capital

Leader in service excellence/ customer

experience

Ethical, regulatory, internal policy

compliance – zero tolerance

Additional risk taken into

consideration

Delivering superior service to clients

Actively contributing to the community

through responsible banking

Leading with innovation

Treating colleagues with dignity

and fairness

Pursuing opportunities that grow

shareholders’ value

Mission

Build longterm relationships by:

Further leverage Islamic Banking

opportunities

STRATEGIC OBJECTIVES

29

…Supported by Clearly Laid Down Business Objectives

Accelerate

domestic growth

Win new customers and increase customer penetration through a differentiated customer

centric, service oriented approach and focus on continued product innovation

Leverage balance sheet strength and liquidity position to grow market share

Capitalize on leadership position in fee-generating businesses

Grow international

contribution

Support franchise client needs internationally and international client needs in our franchise

by providing solutions to corporate clients across network

Provide cross border accessibility to clients, such as offshore booking location for private and

gold customers and non-resident proposition across the network

Maintain momentum in our core South Asia FI market and build scale in Egypt & Africa

Optimize balance

sheet

Optimize liability mix to lower cost of funds and enhance margins

Increase leverage and deploy liquid assets into higher yielding opportunities

Drive operational

efficiencies

Leverage existing infrastructure to drive growth and returns

Significantly improve efficiencies across the bank to bring cost/income ratio in line with

market

Strengthen risk

management and

asset quality

Reduce charge-to-loans ratio through continued focus on portfolio and asset quality

Selective portfolio / asset sales as part of an ongoing portfolio balancing strategy

Business objectives are strongly integrated with the long-term strategic direction of Mashreq

BUSINESS OBJECTIVES

30

Business segments outlook

Diversified earnings base with strong growth potential

Gross Loans portfolio split as of December 2017

27.3%

2.6%15.4%

6.0%

13.4%

14.5%7.1%

13.7%

Financial institutions

Personal

Services

Govt/GRE

Transport & Comm.

Trade

Construction

Manufacturing

DIVERSIFICATION

Revenue split FY 2017 Asset split as of December 2017

25.4%

22.6%

10.2%

5.8%7.3%

8.0%

20.6%

53.1%15.5%

11.2%

8.2%

12.0%Cash and balances with CB

Loans & Advances

Interbank deposits & balances

Other assets

Financial Investments

Retail

International

Corporate

Treasury &

Capital markets

Insurance

Others

Islamic

(AED 66.1 bn)

(AED 6.0 bn) (AED 125.2 bn)

▪ UAE Retail: Pick up in mortgage business; strong growth in

cards and payment business and wealth management

▪ UAE Corporate: Strong growth from trade, manufacturing,

tourism and logistics driving overall UAE GDP in the coming

years leading to increased demand for credit & trade services

▪ International Banking: Tap and strengthen Regional market

footprint to assist local corporations operating regionally

▪ Insurance: As the largest insurance company in the UAE,

Mashreq’s Oman Insurance Company (OIC) subsidiary is

expected to grow in line with the market

▪ Treasury: Build on the market leading menu of TCM products

including hedging and FX products and increase cross-sell

31

Strategic Advantage through Product and Service Innovation

Introduce a comprehensive corporate

cash management solution offering (GTS)

Integrate Emirates ID with bank account

and allow its usage as a Debit Card

Introduce Point-of-Sale terminalsCentralized branch operations and

foreign trade services

Introduce “Branch of the future – self

service autonomous branches”

Introduce “Tap & Go”, mobile NFC

sticker payment method

Offer Visa Connectivity across the

worldInstall ATM cash dispensers

Issue debit/credit cards Offer a direct banking centre

Launch full service digital bank “Mashreq

Neo“

Launch UAE’s first fully EMV Chip & PIN

compliant mobile POS solution

Innovation

Introduce consumer

loans

Mashreq was the first bank in the UAE to:

INNOVATION

32

Mashreq

Investor

Presentation

UAE economy

Mashreq heritage

Structure and Leadership

Strategy

Financial track record

Trading history, rating and dividends

Corporate governance

Accolades

33

Solid performance over the past decade

FINANCIAL TRACK RECORD

Net loans and advances (AED billion)

Net profit (AED million)

2,0521,9261,806

1,312

8208031,000

1,6431,901

2,4022,401

+1%

20172016201520142013201220112010200920082007

63616058

50

4138

41

48

55

35

2015

+6%

2016 20172008 2009 2010 2011 2012 20132007 2014

34

Rapid improvement in performance over the last four years

FINANCIAL TRACK RECORD

Loans & Advances (AED billion) Customer deposits (AED billion)

Total Revenue (AED million)

62.761.060.258.050.4

2017

6%

2016201520142013

76.177.073.668.558.6

2017

7%

2016201520142013

Net profit (AED million)

2,445 3,125 3,423 3,567 3,579

2,3932,720 2,555

2017

6%

2016

6,169

2,602

2015

5,978

2014

5,845

2013

4,837

6,016

2,437

Net interest income1)Fee and other income

13.1% 15.7%ROE

2,0521,9262,4022,401

1,806

20172016

3%

201520142013

1 NII component booked under net investment income as per IFRS, reclassified under NII

14.2% 10.6% 10.5%

35

Tier I Capital Ratio

Total Capital Ratio

Efficiency Ratio

Liquid Assets to Total Assets

Advances to Deposits

NPL Coverage Ratio

NPL to Gross Advances

ROA

Net Interest Margin

ROE

Capital adequacy

Liquidity

Asset quality

Performance

Fee and other income to total income

16.0%

16.9%

39.0%

30.4%

79.2%

31 Dec 2016

151.1%

3.1%

1.6%

3.52%

10.6%

42.2%

Key financial ratios

FINANCIAL TRACK RECORD

17.1%

18.0%

39.6%

26.7%

85.0%

30 Sep 2017

134.4%

3.7%

1.8%

3.45%

11.5%

39.8%

17.4%

18.3%

39.2%

29.6%

82.5%

31 Dec 2017

149.7%

2.9%

1.7%

3.41%

10.5%

40.5%

36

Well-funded balance sheet …

FINANCIAL TRACK RECORD

Operating leverage (%)

Liquidity (%)

29.6%30.4%

20172016

26.5%29.9%

2014

27.7%

20152013

2015 2016

81.7% 79.2%84.8%

2013

86.1%

2014

82.5%

2017

Loan to Deposits

Liability by type as of December 2017

73.1%

9.5%

1.5%

6.0%

9.9%

Liquid Assets to Total Assets

Customer deposits

Due to Banks

Insurance Funds

Med. Term FRN

Other Liabilities

18.7%

7.1%

2.3%

7.2%

8.9%24.5%

31.3%

International

Islamic

Insurance

Others

Treasury &

Capital markets

Retail

Corporate

(AED 104.1 bn)

Liability segment split as of December 2017

(AED 104.1 bn)

37

Capital adequacy (%)

Risk weighted assets (AED million) Tier 1 and Tier 2 capital (AED million)

…along with stable adequacy

20172016

16.9%16.0%

2015

16.9%15.9%

2014

16.6%15.3%

2013

18.1%16.4%

17.4% 18.3%Total Capital ratio

Tier I Capital ratio

117,969118,874113,514

106,628

88,975

20172016201520142013

20,042

1,077

18,965

2016 20172015

1,178

18,001

2014

17,726

1,450

16,277

2013

16,146

1,568

14,578

21,627

20,514

1,11319,179

Tier 2 capitalTier 1 capital

FINANCIAL TRACK RECORD

38

123

125

+1.9%

7971,961

AUHDXB

+5.3%

1,165

1,1341,863 730

63

61

+2.9%

DXB

+3.6%

AUH

428 6451,073

1,112 471 641

76

77

-1.3%

7385541,292

AUHDXB

+6.1%

506 7111,217

6.0

6.2

-2.5%

64.2 29.7

DXB

27.965.6 37.7

34.5

AUH

-2.1%

Total assets (AED billionn)

Peer group1) Mashreq

Total deposits (AED billionn)

Peer group1) Mashreq

Total loans (AED billion)

Total revenue (AED billion)

Peer group1) Mashreq

Peer group1) Mashreq

Dec '16

9.2% 2.7% 9.8% (0.5%)

9.5% 3.8% 6.2% (8.3%)

Dec ‘17

Dec '16

Dec ‘17

Dec '16

Dec ‘17

YE ’16

YE ’17

Market performance in YE 2017

FINANCIAL TRACK RECORD

Source: Banks’ financial statements

1 Peer group includes 8 banks: ENBD, FAB, ADCB, CBD, UNB, ADIB, DIB and RAK

39

Bank

FAB

UNB

Total assets

RAK

ADIB

Mashreq

49

70

108

123

125

207

265

470

669

Total loans (net) Total deposits

Growth vs

Dec '17

CBD

3%

14%

10%

3%

1%

2%

3%

5%

18%

32

47

71

77

63

133

163

258

330 (1%)

12%

13%

(3%)

(2%)

3%

3%

6%

16%

163

327

396

147

32

48

79

100

76

4%

9%

11%

2%

1%

(1%)

5%

5%

20%

Growth vs

Dec '17

Growth vs

Dec '17

ENBD

ADCB

DIB

Source: Banks’ financial statements

1) Total growth over the period and not CAGR

Market position in UAE

FINANCIAL TRACK RECORD – DECEMBER’17 (AED BILLION)

40

Bank Revenue Net interest income Fee & other income

YoYgrowth

YoYgrowth

YoYgrowth

2.6

16.4

3.6

3.8

5.6

6.0

7.7

8.9

15.5

UNB

RAK

ADIB

Mashreq

(19%)

7%

4%

(1%)

5%

(2%)

5%

4%

14%

CBD

(16%)

6%

1%

(4%)

(4%)

4%

8%

7%

14%

(26%)

12%

15%

7%

27%

(10%)

(4%)

(1%)

14%

Source: Banks’ financial statements

1) Total growth over the period and not CAGR

ENBD

ADCB

DIB

1.8

2.6

2.7

3.8

3.5

5.3

6.7

10.8

11.4

2.4

2.2

2.5

0.8

1.0

1.1

1.9

4.7

5.0FAB

Market position in UAE

FINANCIAL TRACK RECORD – DECEMBER’17 (AED BILLION)

41

Source: Banks’ financial statements

1) Shareholders equity excludes tier 1 capital notes and their interest expense is deducted from net profits

2) Total net profits (including minority) divided by total assets

ROE1) [%]

ROA2) [%]

1.31.51.51.61.71.71.71.82.0

RA

K

DIB

Ø 1.6

FA

B

UN

B

CB

D

AD

CB

MA

SQ

EN

BD

AD

IB

Bank Net profit [AED billion]

8.3

9.1

0.8

1.0

1.6

2.1

2.3

4.3

4.3

YoYgrowth

(19%)

21%

0%

5%

7%

18%

20%

15%

3%

UNB

RAK

ADIB

Mashreq

CBD

9.410.010.410.511.315.016.520.721.5

Ø 14

UN

B

FA

B

RA

K

MA

SQ

CB

D

AD

CB

EN

BD

AD

IB

DIBReturn on RWA [%]

1.51.71.81.82.12.12.52.52.9D

IB

EN

BD

Ø 2.1

UN

B

MA

SQ

CB

D

FA

B

AD

CB

AD

IB

RA

K

ENBD

ADCB

DIB

FAB

Market position in UAE

FINANCIAL TRACK RECORD – DECEMBER’17 (AED BILLION)

42

Mashreq

Investor

Presentation

UAE economy

Mashreq heritage

Structure and Leadership

Strategy

Financial track record

Trading history, rating and dividends

Corporate governance

Accolades

43

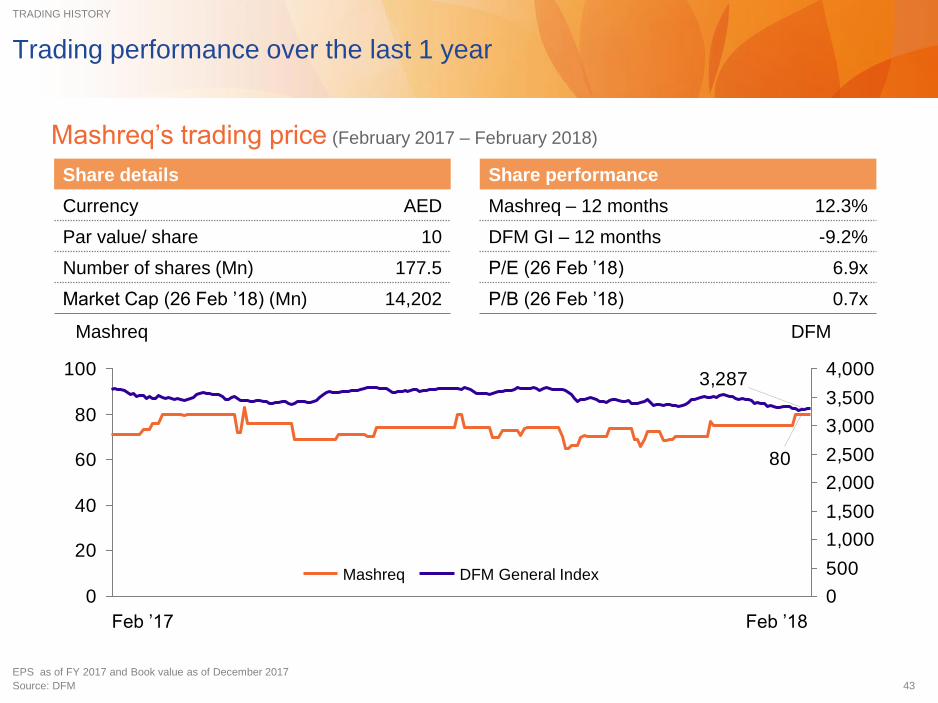

Trading performance over the last 1 year

Mashreq’s trading price (February 2017 – February 2018)

Feb ’17 Feb ’18

80

3,287

0

20

40

60

80

100

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Mashreq DFM

DFM General IndexMashreq

Share performance

Mashreq – 12 months 12.3%

DFM GI – 12 months -9.2%

P/E (26 Feb ’18) 6.9x

P/B (26 Feb ’18) 0.7x

Share details

Currency AED

Par value/ share 10

Number of shares (Mn) 177.5

Market Cap (26 Feb ’18) (Mn) 14,202

TRADING HISTORY

EPS as of FY 2017 and Book value as of December 2017

Source: DFM

44

2,0521,926

2,4022,401

1,806

710710710676676

0

500

1,000

1,500

2,000

2,500

20162014 201720152013

Progressive dividend policy based on solid performance

Net profit and Cash Payout (AED million) and Cash dividend (%)

Net profit Cash payout

10.68 11.5613.53 13.53 10.56EPS

(AED)

1)

85.45 119.0091.04 100.09 105.66BVPS

(AED)

DIVIDENDS

40%40%40%40%38%

Cash dividend (%)

1 Plus 5% Bonus Shares

45

Rated by four rating agencies

Rating Agency Long term Short term

Baa1 P-2

BBB+ A-2

A F1

A- A1

CREDIT RATING

46

Mashreq

Investor

Presentation

UAE economy

Mashreq heritage

Structure and Leadership

Strategy

Financial track record

Trading history, rating and dividends

Corporate governance

Accolades

47

Mashreq is regulated by the UAE Central Bank and follows international

banking standards

Basel II and III Accounting Standard

Bank monitoring - liquidity Credit Limit

CORPORATE GOVERNANCE

Supervisory Authority

▪ Mashreq’s home supervisory authority is the UAE Central Bank which is responsible for

licensing, monitoring and supervising banks, finance companies and exchange companies in

the UAE

▪ Internationally, Mashreq comes under the purview of respective country regulators such as

the Federal Reserve and NYSDFS in the USA and Prudential Regulation Authority &

Financial Conduct Authority in the UK

▪ Lending limits fixed by the Central Bank in relation to capital:

– Commercial entities of Federal Govts and UAE Local Govts:

25%, 100% aggregate

– UAE Local Govts and non-Commercial entities: 25%

Individual, 100% aggregate

– Principal shareholders and their related entities: 20%

Individual, 50% aggregate

▪ Cash reserve ratio requirements (1% on Time Deposits and 14%

on Demand Savings and Call deposits)

▪ Maintenance of 1:1 ratio is mandatory, i.e. utilization of funds

should not exceed stable sources

▪ As per Basel III, liquidity coverage ratio (LCR) and net stable

funding ratio (NSFR) is under implementation. In the meantime

Central Bank has introduced ‘eligible liquid assets ratio (ELAR)’ as

a surrogate for LCR. Banks will continue to report Advances/

Stable resources in place of NSFR.

▪ UAE CB has approved Mashreq submission to follow LCR from

31st March 2018

▪ Banks are expected to follow the Standardized Approach for both

credit and operational risks.

▪ UAE CB has rolled out Capital Adequacy Ratio (CAR) as per

Basel III effective 1 Jan 2018

▪ The Central Bank made it mandatory in 2000 for all Banks to

publish their Annual Financial Statement as per International

Financial Reporting Standards (IFRS)

▪ Banks are expected to follow IFRS 9 w.e.f 1st Jan2018

48

Board and Management Committees

CORPORATE GOVERNANCE

Chairman, Vice-Chairman and 4 Directors form Mashreq’s Board. Two of the six board members are independent

CEO is the only executive director

The Board of Directors meet at least once every quarter

Management issues are raised at Board level where the bank’s senior management presents details to the Board

Board has delegated certain powers to CEO for effective day-to-day management

Information

Security

Committee

Audit &

Compliance

Committee

Risk

Committee

ALCO

Committee

Investment

Committee

Technology

Steering

Committee

Human

Resources

Committee

Management Supervision

Executive Management Committee

Board Supervision

Executive Management Committee (reporting to the CEO) discusses and debates bank-wide issues, develops

strategic plans for the Board’s approval and takes decisions on pan-bank issues.

Remuneration Committee Audit Committee

49

Mashreq

Investor

Presentation

UAE economy

Mashreq heritage

Structure and Leadership

Strategy

Financial track record

Trading history, rating and dividends

Corporate governance

Accolades

50

Key Awards

ACCOLADES

Gallup Great Workplace Award 2017, 2016, 2015,

2014

CSR Label – Dubai Chambers – 2017,2016,

2015, 2014, 2013, 2012 & 2011

Banker ME Product Awards

▪ Best Mobile Banking Service – Snapp

▪ Best Customer Loyalty Programme – Salaam

▪ Best Premium Credit Card – Solitaire

▪ Best Trade Finance Offering – Trade Finance

▪ Best Real Estate Advisory 2017

Global Finance 2017

▪ Innovator in Transaction Services (for the Card less

Cash Withdrawal Using Internet Banking offering in

the product innovation category for 2017)

▪ Best Treasury and Cash Management Bank in the

UAE

Banker ME Industry Awards

▪ Best Regional Retail Bank 2016, 2015, 2014

▪ Best Banking Innovation

▪ Best Real Estate Finance

Euromoney’s 13th annual private banking survey

▪ Best Private Bank for Super Affluent Clients in the

UAE

MEFTECH Innovation Awards

▪ Best Customer Experience Initiative

Annual Islamic Business & Finance Awards

▪ Best Innovation in Islamic Banking Solution

World Finance Awards

▪ Best Digital Bank – UAE

▪ Best Mobile Banking Application – UAE

Daman Corporate Health Awards

▪ Best Corporate Health and Wellness Organization

Award

Gulf Business Awards

▪ Business Leader of the Year – Banking Industry

(H.E. AbdulAziz Al Ghurair)

Retail Banking Conference & Awards: London

▪ Middle East Retail Bank of the Year

Global Banking & Finance Review Awards 2016

▪ Best Retail Bank UAE

▪ Best Customer Experience UAE

▪ Best Digital Bank UAE

▪ Best Corporate Bank Qatar

Cards & Payment Middle East 2016

▪ Best Credit Card

▪ Most Improved Payment Card

Islamic Finance News Awards

▪ Corporate Finance Deal of the Year – ENOC US$

1.5 Billion Syndicated Loan Facility

▪ Syndicated Deal of the Year – Aujan Coca Cola

Beverages AED900 Million Commodity Murabahah

Financing

511) NII component booked under net investment income as per IFRS, reclassified under NII; Includes Income from Islamic Financing

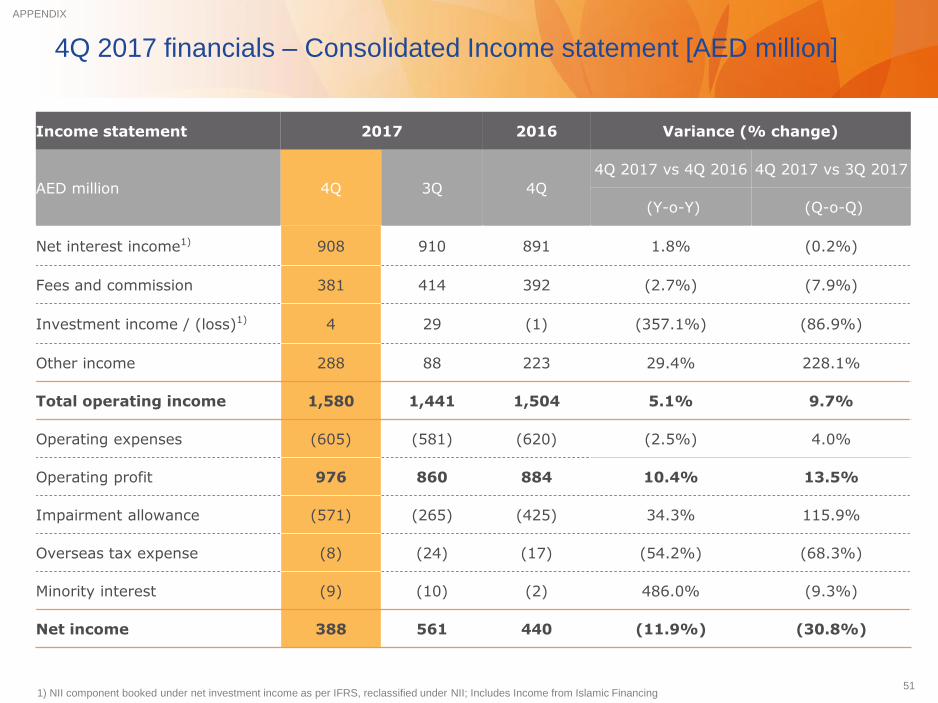

4Q 2017 financials – Consolidated Income statement [AED million]

Income statement 2017 2016 Variance (% change)

AED million 4Q 3Q 4Q

4Q 2017 vs 4Q 2016 4Q 2017 vs 3Q 2017

(Y-o-Y) (Q-o-Q)

Net interest income1) 908 910 891 1.8% (0.2%)

Fees and commission 381 414 392 (2.7%) (7.9%)

Investment income / (loss)1) 4 29 (1) (357.1%) (86.9%)

Other income 288 88 223 29.4% 228.1%

Total operating income 1,580 1,441 1,504 5.1% 9.7%

Operating expenses (605) (581) (620) (2.5%) 4.0%

Operating profit 976 860 884 10.4% 13.5%

Impairment allowance (571) (265) (425) 34.3% 115.9%

Overseas tax expense (8) (24) (17) (54.2%) (68.3%)

Minority interest (9) (10) (2) 486.0% (9.3%)

Net income 388 561 440 (11.9%) (30.8%)

APPENDIX

521) NII component booked under net investment income as per IFRS, reclassified under NII; Includes Income from Islamic Financing

FY 2017 financials – Consolidated Income statement [AED million]

Income statement 2017 2016 Variance (% change)

AED million FY FY

FY 2017 vs FY 2016

(Y-o-Y)

Net interest income1) 3,579 3,567 0.3%

Fees and commission1,558

1,685 (7.5%)

Investment income / (loss)1) 107 58 84.9%

Other income 772 859 (10.1%)

Total operating income 6,016 6,169 (2.5%)

Operating expenses (2,361) (2,407) (1.9%)

Operating profit 3,655 3,762 (2.8%)

Impairment allowance (1,488) (1,734) (14.2%)

Overseas tax expense (78) (74) 4.5%

Non Controlling interest (37) (28) 35.3%

Net income 2,052 1,926 6.5%

APPENDIX

53

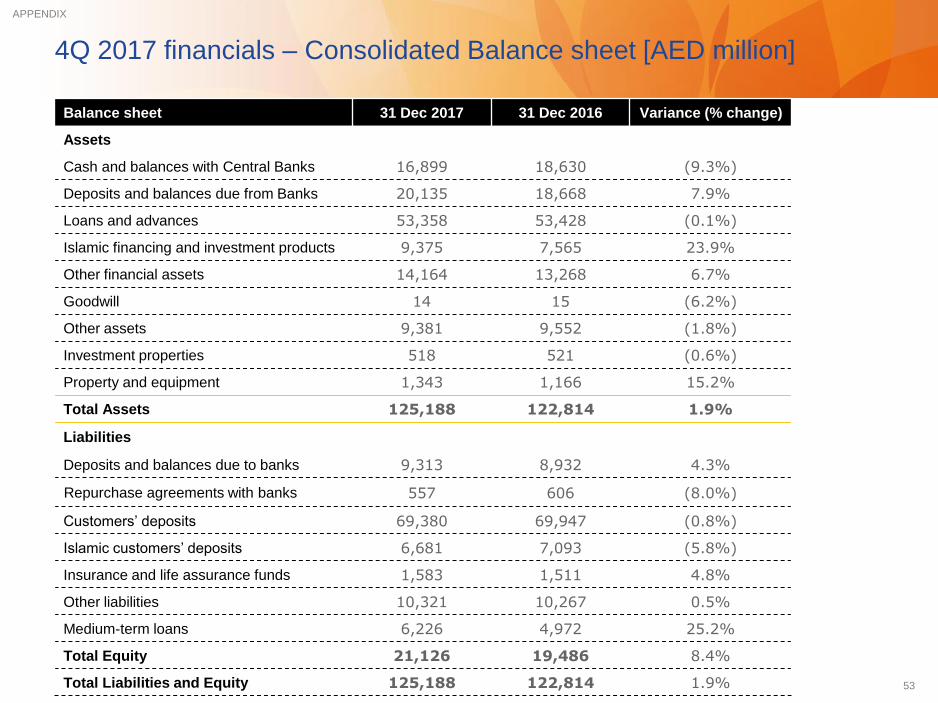

s

Balance sheet 31 Dec 2017 31 Dec 2016 Variance (% change)

Assets

Cash and balances with Central Banks 16,899 18,630 (9.3%)

Deposits and balances due from Banks 20,135 18,668 7.9%

Loans and advances 53,358 53,428 (0.1%)

Islamic financing and investment products 9,375 7,565 23.9%

Other financial assets 14,164 13,268 6.7%

Goodwill 14 15 (6.2%)

Other assets 9,381 9,552 (1.8%)

Investment properties 518 521 (0.6%)

Property and equipment 1,343 1,166 15.2%

Total Assets 125,188 122,814 1.9%

Liabilities

Deposits and balances due to banks 9,313 8,932 4.3%

Repurchase agreements with banks 557 606 (8.0%)

Customers’ deposits 69,380 69,947 (0.8%)

Islamic customers’ deposits 6,681 7,093 (5.8%)

Insurance and life assurance funds 1,583 1,511 4.8%

Other liabilities 10,321 10,267 0.5%

Medium-term loans 6,226 4,972 25.2%

Total Equity 21,126 19,486 8.4%

Total Liabilities and Equity 125,188 122,814 1.9%

4Q 2017 financials – Consolidated Balance sheet [AED million]

APPENDIX

54