section 1 -capital raisings

DESCRIPTION

Basic idea of corporate laws related to raising capitalTRANSCRIPT

FUNDAMENTALS OF CORPORATE LAWMSc in Corporate Finance

ANNÉE SCOLAIRE / ACADEMIC YEAR 2013-2014

Intervenant/Lecturer: Me Bastien BERNARD

CAPITAL RAISINGS

Section 1

Fundamentals of Corporate Law 2

FINANCING

• Can be achieved through debt (creditors) or equity (shareholders)

• Debt can be provided as

- (i) loan by suppliers (abuse of mass market retailers), banks (also Zopa in 2005in UK or Lending Club in the US), shareholders accounts (above 5% of sharecapital), cash pooling agreements between companies of a same group or ;

- (ii) debt instruments

• Equity is provided by investors through share capital subscriptions

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.1.1. Fund raisings1.1.2. Financial securities

3Fundamentals of Corporate Law

4

FINANCIAL SECURITIES

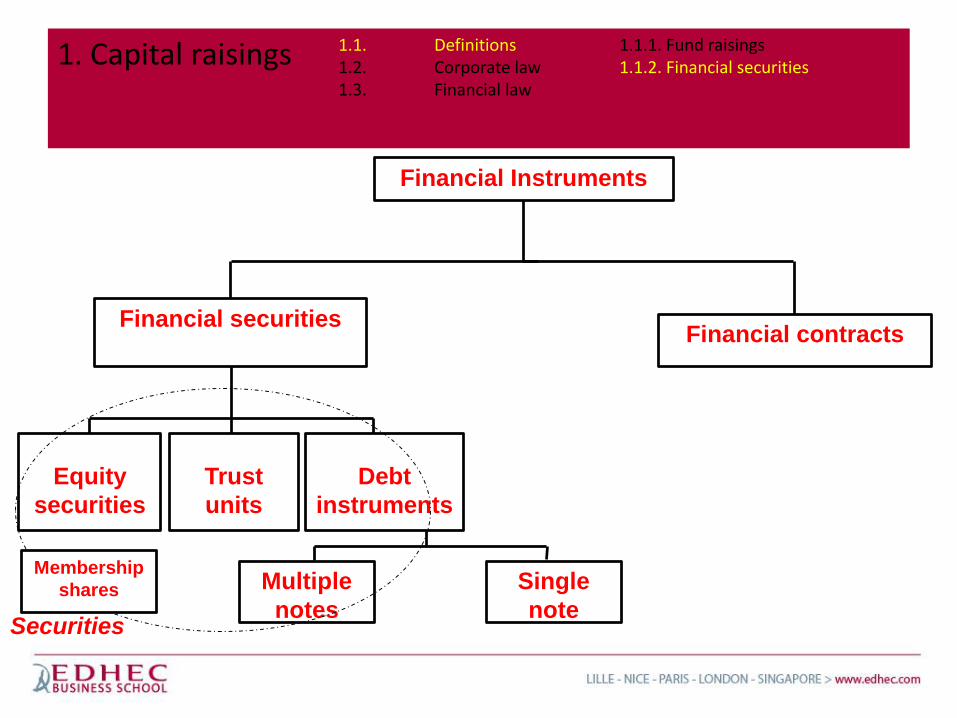

• The financial instruments include the financial securities and the financialcontracts.

• Financial contracts are options, forwards and futures.

• The financial securities include the equity securities, the debt instruments, and trustunits :

- Equity securities include shares and other instruments granting or which could grant access to the share capital or voting rights, such as warrants.

They represent financial rights (proportionate or not, leonine clause) and political rights (with or without voting rights, or multiple voting rights). Example of preferred shares with no voting rights which recover it in case no dividend is paid, no PSR

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.1.1. Fund raisings1.1.2. Financial securities

5

FINANCIAL SECURITIES

- Debt instruments are liens against the company, but can be converted into equity such as convertible bonds, exchangeable bonds (equity cannot be converted into debt because the ranking or reimbursement is superior);

- Trust units issued by collective placement vehicles, securitizations vehicles.

• Securities are also financial securities and membership shares granting the same type of rights per category.

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.1.1. Fund raisings1.1.2. Financial securities

Financial Instruments

Financial securities

Equity

securities

Trust

units

Debt

instruments

Multiple

notes

Single

note

Financial contracts

Securities

Membership

shares

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.1.1. Fund raisings1.1.2. Financial securities

CHARACTERISTICS OF FINANCIAL INSTRUMENTS

• Dematerialization: Financial securities are submitted to applicable law of theregistered office. They must be registered in a registry held by the issuer or anintermediary duly authorized

• Ownership of the financial securities: The register is opened to the name of oneor several owners, holding the property of the registered financial securities;– Presumption of property: the owner is holding the property of the shares and

not a debt against the intermediary holding the register (difference betweenUS and Europe);

– Protection of the property: no one can contest the property of a financialsecurity acquired in good faith by the owner of the financial securities held inthe register

• Negotiability: financial securities are negotiable:– Negotiation is simplified compared to the transmission pursuant to the civil

Code for example;– The financial securities can be transmitted through registration in the

accounts of the register. Note Carbone certificate follows the same regime butare not financial instruments

7Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.1.1. Fund raisings1.1.2. Financial securities

BOND ISSUES

• Bond issue is decided by BOD, management board, manager. Delegation is possiblefor 1 year.

• Nominal value, interest rate, duration of the bonds, subordination.– More and more complex (minimum information to be provided by financial advisors)

– Junk Bonds

– MTF NYSE Bondmatch

• Bond holders are gathered in a group represented by 1 person (cannot bemanager of the company). Bond holders can gather in BGM to rule upon theapplication of the bond contract and the protection of the bondholders.

8Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Bond issues1.2.2. Equity issues

EQUITY ISSUES

• Equity issue is decided by the extraordinary SGM. Delegation is possible to the BOD (more flexible issues), the managementboard, President, manager. Competence (yes or no), Power (characteristics).

• Contribution can be in cash, in kind, or sweat equity (can be a way to have equal participation).

• In France, when there is a contribution in cash, a share capital increase in favor of the employees must be proposed to theESGM (enhance employees participation).

• It is possible to provide for a variable capital: minimum share capital and a maximum one and to allow a variation withinthose limits without any additional decision from the SGM or amendment of the articles of association (allows shareholderto come in and out).

• The issue of new shares can occur upon:– Contributions from shareholders or third parties– Incorporations of reserves, premium (can also lead to increase the par value of the shares)– Conversion or reimbursement of bonds– Exercise of rights granting access to share capital– Merger– Conversion of preferred shares into ordinary shares

• Issue can take different forms:– To all shareholders– To a category of persons– To identified persons– To the public

Fundamentals of Corporate Law 9

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Bond issues1.2.2. Equity issues

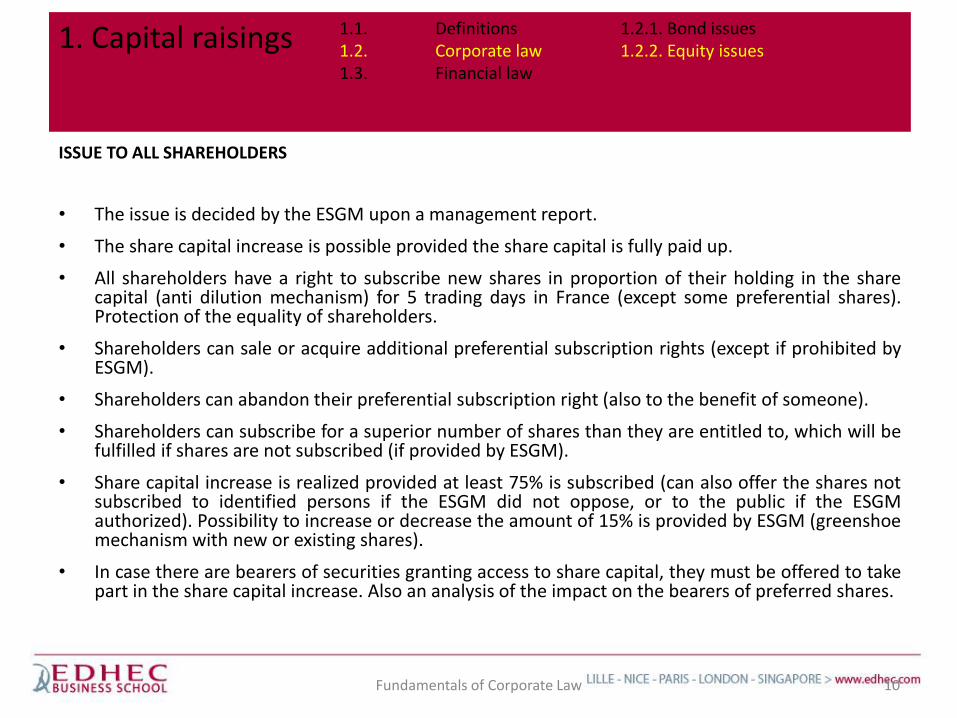

ISSUE TO ALL SHAREHOLDERS

• The issue is decided by the ESGM upon a management report.

• The share capital increase is possible provided the share capital is fully paid up.

• All shareholders have a right to subscribe new shares in proportion of their holding in the sharecapital (anti dilution mechanism) for 5 trading days in France (except some preferential shares).Protection of the equality of shareholders.

• Shareholders can sale or acquire additional preferential subscription rights (except if prohibited byESGM).

• Shareholders can abandon their preferential subscription right (also to the benefit of someone).

• Shareholders can subscribe for a superior number of shares than they are entitled to, which will befulfilled if shares are not subscribed (if provided by ESGM).

• Share capital increase is realized provided at least 75% is subscribed (can also offer the shares notsubscribed to identified persons if the ESGM did not oppose, or to the public if the ESGMauthorized). Possibility to increase or decrease the amount of 15% is provided by ESGM (greenshoemechanism with new or existing shares).

• In case there are bearers of securities granting access to share capital, they must be offered to takepart in the share capital increase. Also an analysis of the impact on the bearers of preferred shares.

10Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Bond issues1.2.2. Equity issues

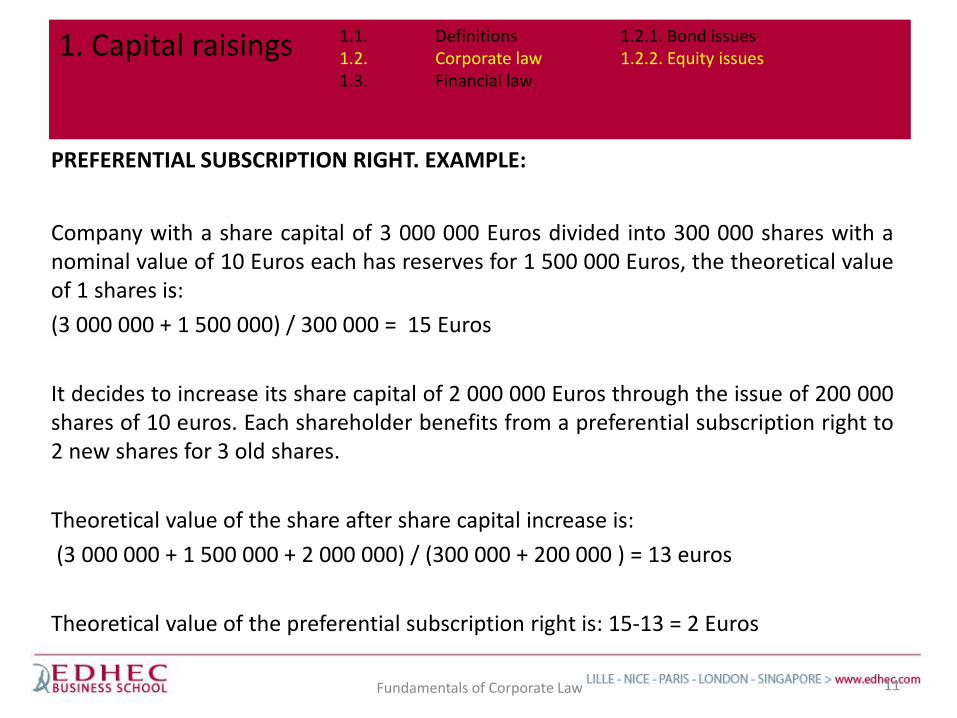

PREFERENTIAL SUBSCRIPTION RIGHT. EXAMPLE:

Company with a share capital of 3 000 000 Euros divided into 300 000 shares with anominal value of 10 Euros each has reserves for 1 500 000 Euros, the theoretical valueof 1 shares is:

(3 000 000 + 1 500 000) / 300 000 = 15 Euros

It decides to increase its share capital of 2 000 000 Euros through the issue of 200 000shares of 10 euros. Each shareholder benefits from a preferential subscription right to2 new shares for 3 old shares.

Theoretical value of the share after share capital increase is:

(3 000 000 + 1 500 000 + 2 000 000) / (300 000 + 200 000 ) = 13 euros

Theoretical value of the preferential subscription right is: 15-13 = 2 Euros

11Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Bond issues1.2.2. Equity issues

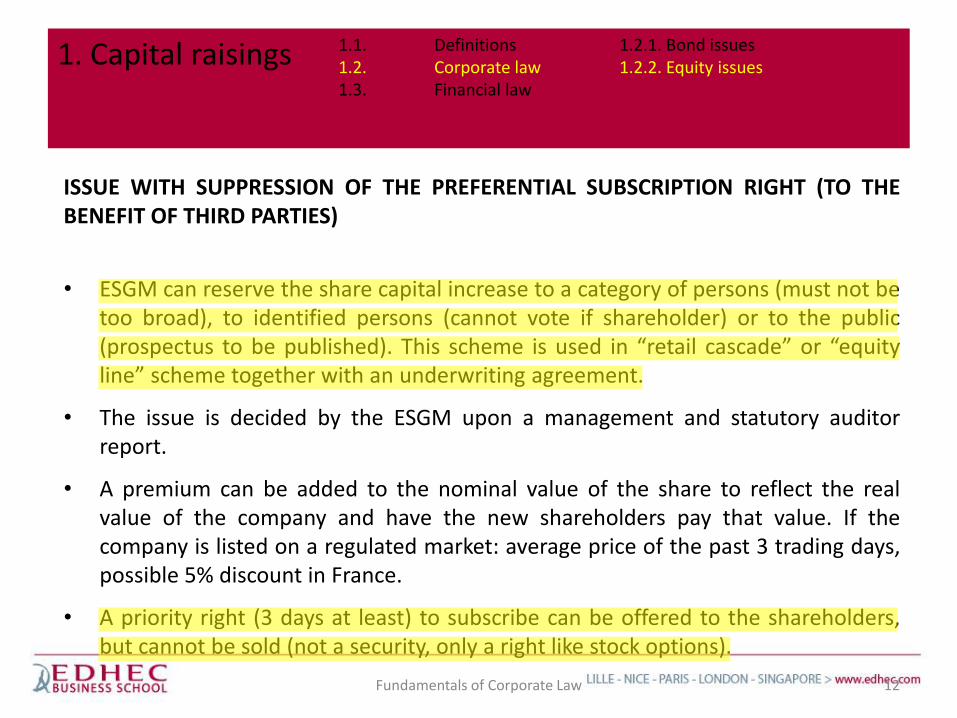

ISSUE WITH SUPPRESSION OF THE PREFERENTIAL SUBSCRIPTION RIGHT (TO THEBENEFIT OF THIRD PARTIES)

• ESGM can reserve the share capital increase to a category of persons (must not betoo broad), to identified persons (cannot vote if shareholder) or to the public(prospectus to be published). This scheme is used in “retail cascade” or “equityline” scheme together with an underwriting agreement.

• The issue is decided by the ESGM upon a management and statutory auditorreport.

• A premium can be added to the nominal value of the share to reflect the realvalue of the company and have the new shareholders pay that value. If thecompany is listed on a regulated market: average price of the past 3 trading days,possible 5% discount in France.

• A priority right (3 days at least) to subscribe can be offered to the shareholders,but cannot be sold (not a security, only a right like stock options).

12Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Bond issues1.2.2. Equity issues

SPECIFIC CASES

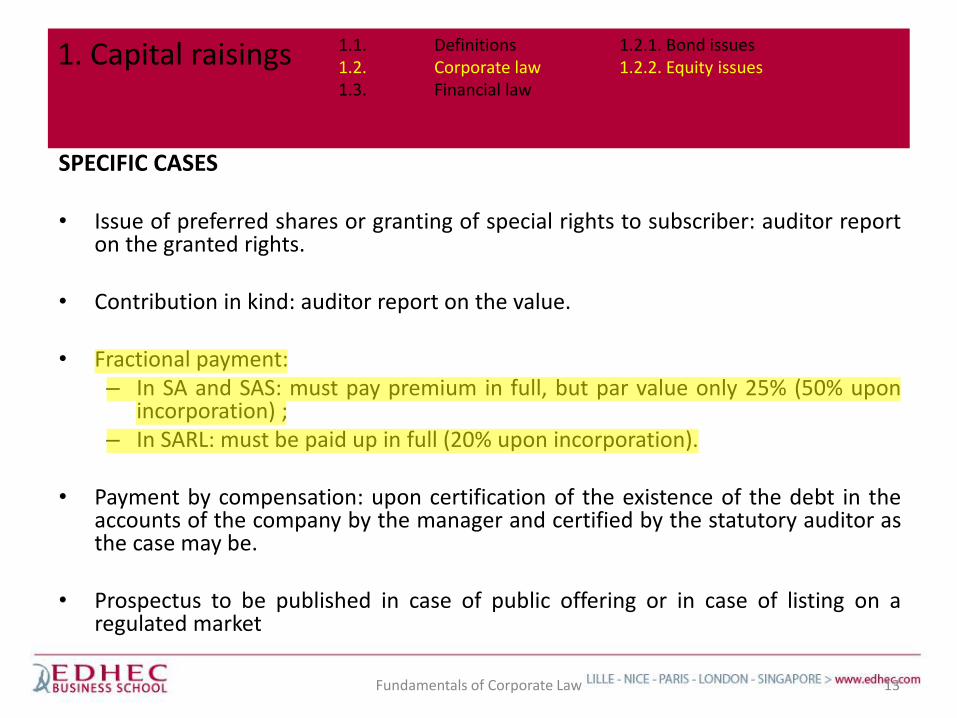

• Issue of preferred shares or granting of special rights to subscriber: auditor reporton the granted rights.

• Contribution in kind: auditor report on the value.

• Fractional payment:– In SA and SAS: must pay premium in full, but par value only 25% (50% upon

incorporation) ;– In SARL: must be paid up in full (20% upon incorporation).

• Payment by compensation: upon certification of the existence of the debt in theaccounts of the company by the manager and certified by the statutory auditor asthe case may be.

• Prospectus to be published in case of public offering or in case of listing on aregulated market

13Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Bond issues1.2.2. Equity issues

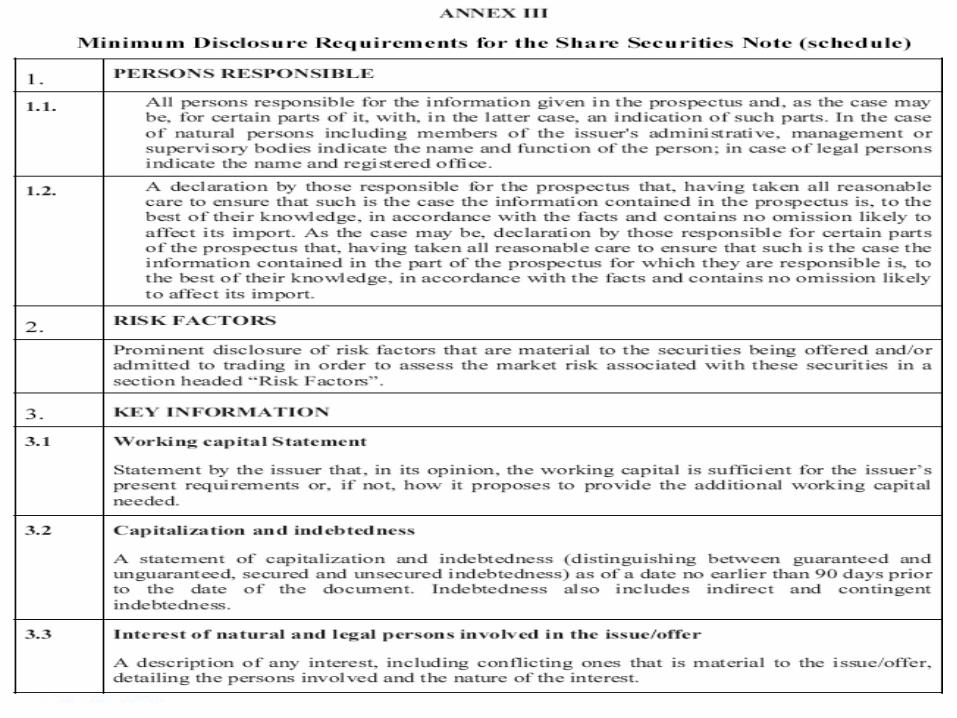

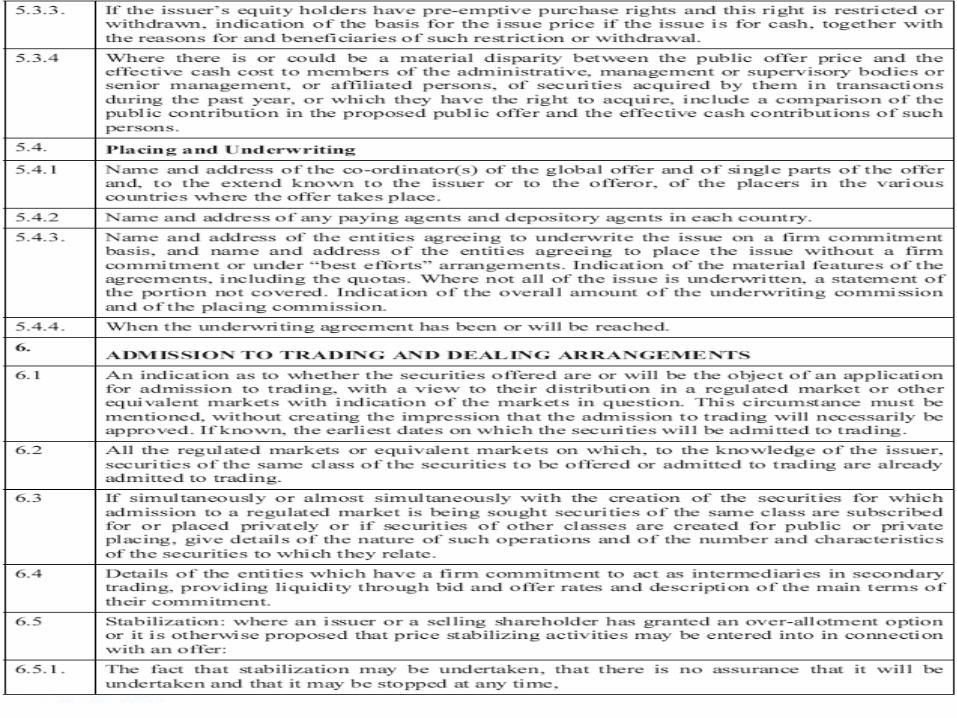

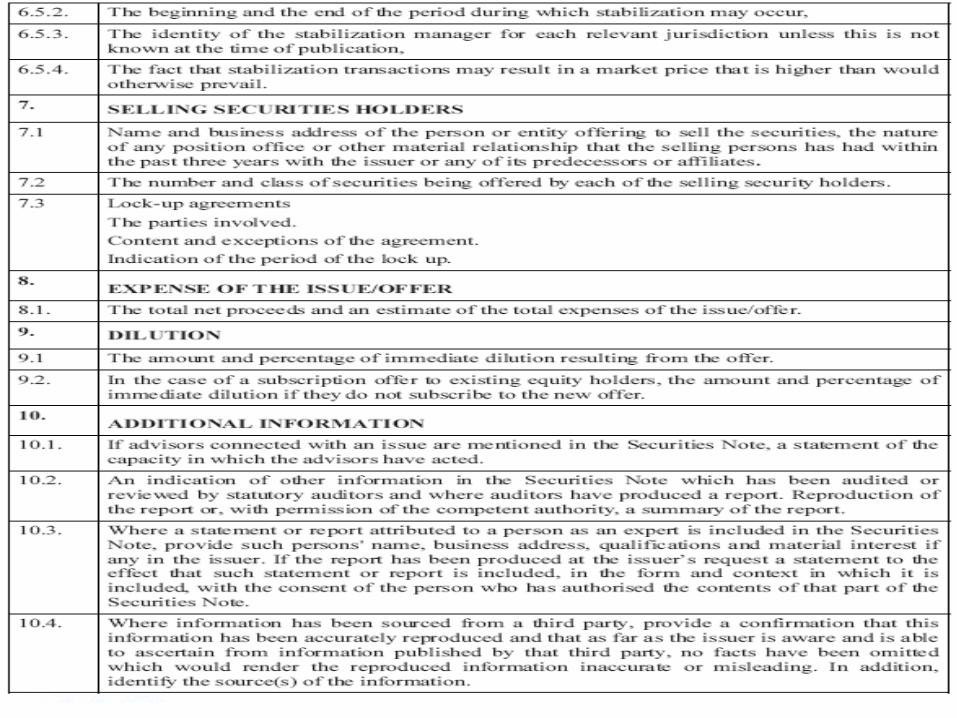

THE MANDATORY INFORMATION: THE PROSPECTUS

Without prejudice to the other provisions applicable thereto,persons or entities making a public offering or admission totrading of a regulated market of financial securities shall, priorto doing so, publish and make available to any interestedparty a document designed to inform the public concerningthe content and terms and conditions of the process which isthe subject thereof and the issuer's organization, financialsituation and business prospects and those of any guarantorof the financial instruments included in that process, asdetermined in the General Regulations of the FinancialMarkets Authority.

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Bond issues1.2.2. Equity issues

PUBLIC OFFERING:

Pursuant to the Prospectus Directive 2003/71/EC on the Prospectus to be publishedwhen securities are offered to the public or admitted to trading, the offer of Financialsecurities to the public is triggered by one of the following operations:

1. A communication addressed to persons under any form and by any mean,presenting sufficient information on the terms of the offer and of the securities to beoffered, to enable an investor to decide to purchase or subscribe these securities(internet, selling restrictions, information, purpose,…).

2. The placing of securities through financial intermediaries.

15Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

EXEPTIONS TO PUBLIC OFFERINGS:

Prospectus Directive provides for a list of operations which do not constitute a publicoffer.

Some exceptions are based:

- (i) on the quality of the investors and the fact that they do not need to beprotected;

- (ii) on the amount of the offer;

- (iii) on the number of investors;

- (iv) exclusion based on individual thresholds.

16Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

(i) The quality of the investors

• Qualified investors (professional client) is a person or entity possessing theexpertise and facilities required to apprehend the risks inherent in transactionsrelating to financial instruments.

17Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

(ii) The amount of the offer

• 1° The total amount is less than EUR 100,000 or the foreign currency equivalentthereof;

• 2° The total amount is between EUR 100,000 and EUR 5,000,000 or the foreigncurrency equivalent thereof and the transaction concerns financial securitiesaccounting for no more than 50% of the share capital of the issuer.

• The total amount of the transaction referred to in Points 1° or 2° shall becalculated over a twelve-month period from the date of the first transaction.When the issuer is listed, press releases are necessary to inform the market,

18Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

(iii) The number of investors

A restricted circle of investors has a number of members below a threshold of 150 persons.

(iv) Individual thresholds

The transaction is intended for investors acquiring at least EUR 100,000 worth, or the foreign currency equivalent thereof, per investor and per transaction, of the relevant financial securities;

The transaction concerns financial securities with a minimum denomination of at least EUR 100,000 or the foreign currency equivalent thereof.

19Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

ADMISSION TO TRADING ON A REGULATED MARKET

Regulated markets are multilateral trading facility which enable multiple sellers andbuyers’ interests on financial instruments expressed by third parties, to meet on thisbasis pursuant to non discriminatory rules, in order to enter into agreements onfinancial instruments which were admitted to trading in accordance with the rules andmarket systems, which functions in accordance with applicable regulation(2004/109/CE Transparency and 2003/6/CE Market Abuse Directives).

There are basically three main types of markets in France:

– Regulated markets (rules approved by the regulators, protection, marketoperator,…);

– Free markets (multi trading facility);

– Organized markets (submit their rules to the regulator,…).

20Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

REGULATED MARKETS

The identification of regulated market is no issue since they are officially recognized bythe Member State competent authorities and published in the official Journal of theEU:

• ” Euronext Paris market” formerly Eurolist, regarding financial instruments

– Compartment A: Capitalizations above 1 billion Euros;

– Compartment B: Capitalizations between150 million and 1 billion Euros;

– Compartment C: Less than 150 M Euros.

– Professional compartment for QI, including a fast path with US listings

• Marché à Terme international de France (MATIF) and the Marché des OptionsNégociables de Paris (MONEP) regarding options and forward markets.

21Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

IN FRANCE, THERE ARE 2 FREE MARKETS MANAGED BYEURONEXT PARIS:

• “free market” created in 1996, ruled by an organizational noticewhich only has a contractual binding force. The admission to tradingon the free market can be initiated by a shareholder or the issuer,but the issuer must not oppose this admission to trading (cannotoppose if already admitted to trading on a regulated market).

• The “compartment of the values delisted from a regulated market”,created in 1996 to temporarily welcome, on the demand of theissuer and after appreciation of Euronext, equity securities or titlegranting access to the share capital of issuers delisted from theregulated markets. The organization notice is the same as for thefree market, except when stated.

22Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

ORGANIZED MARKETS

• This distinction between regulated markets and free markets is blurred in Franceby the existence of an intermediary category of “Organized” markets which arecharacterized by the intervention of a market undertaking slightly on the model ofregulated markets. The AMF has created the category of “organized multilateralfacilities“ whose rules are approved by the AMF on their demand, and who submitthemselves to the rules on market abuse, which daily report to the AMF the orderreceived on the listed instruments, and which provides for a standing market offeras far as shares are concerned.

• Alternext is the best example. It was created in May 2005. It is operated byEuronext Paris and aims at permitting to companies to search financialopportunities on the stock market, through a simplified listing process thoughoffering the investors satisfactory transparency.

23Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

THE MANDATORY INFORMATION: THE PROSPECTUS

Without prejudice to the other provisions applicable thereto, persons or entitiesmaking a public offering or admission to trading of a regulated market of financialsecurities shall, prior to doing so, publish and make available to any interested party adocument designed to inform the public concerning the content and terms andconditions of the process which is the subject thereof and the issuer's organization,financial situation and business prospects and those of any guarantor of the financialinstruments included in that process, as determined in the General Regulations of theFinancial Markets Authority.

Note one can be admitted to trading on a regulated market without making a publicoffering (Euronext Professional Compartment, Fast-path), or be admitted to trading ona non regulated market and make a public offering (Alternext listing).

24Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

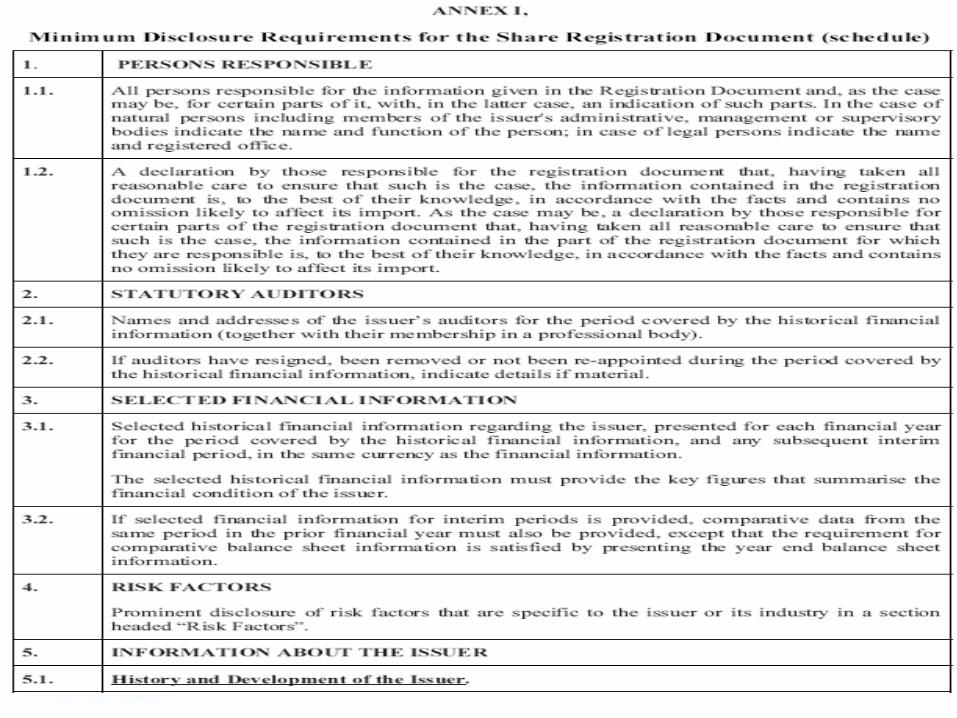

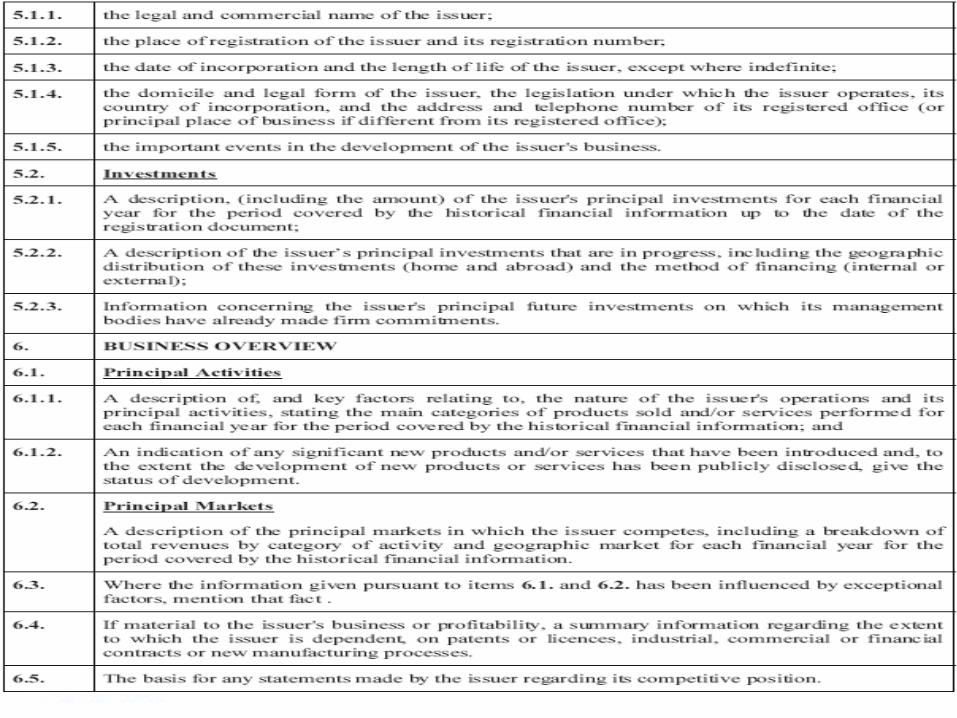

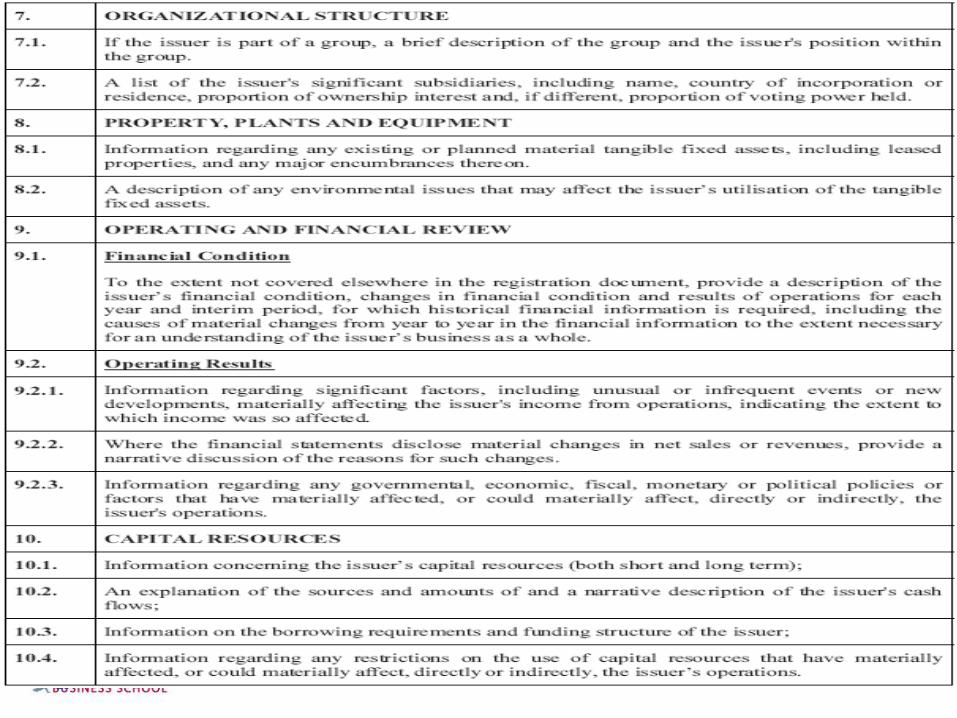

CONTENT OF THE PROSPECTUS

• must be published by the initiator of the public offer, except use of retail cascade ifauthorized.

• The prospectus can be established in one single document or several documents: basedocument, security note and summary. It can also refer to other documents previouslypublished.

• It includes all the information necessary to enable the investors to evaluate thepatrimony, financial situation, the perspectives, and guarantor of the financialinstruments offered or to be listed, as well as the rights attached to the financial titlesand their conditions of issuance.

• This information is organized pursuant to the scheme of EU regulation 809/2004 datedApril 29, 2004 (US S-1 equivalent) which can be adapted in case of risk of the public orthe issuer or in case of small or medium sized company (less than 250 employees,balance sheet EUR 43M maximum and annual turnover not more than EUR 50M).

25Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

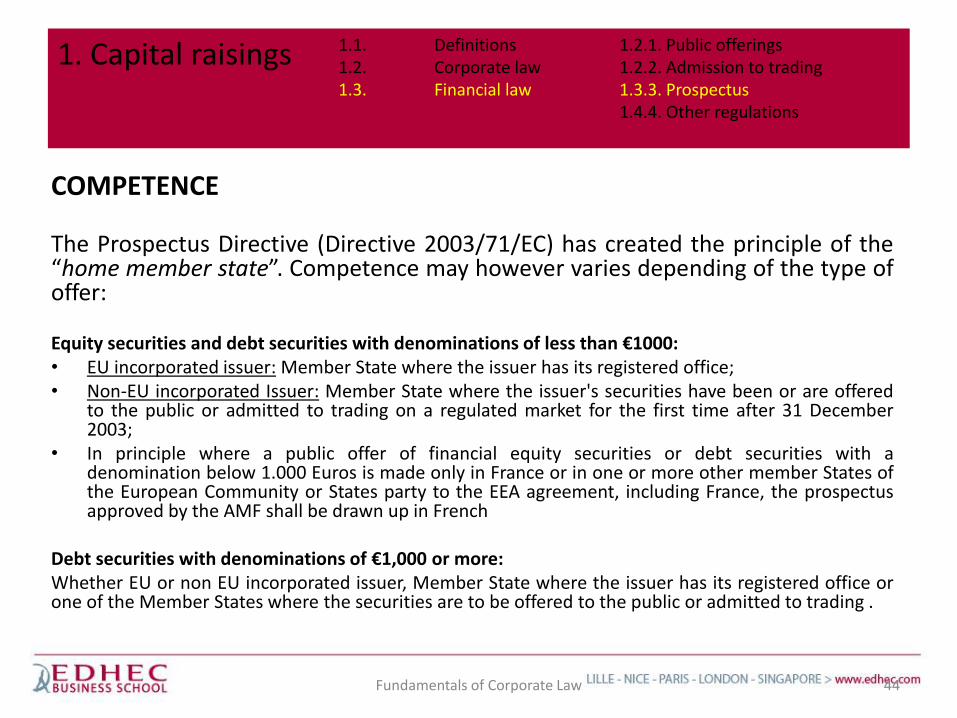

COMPETENCE

The Prospectus Directive (Directive 2003/71/EC) has created the principle of the“home member state”. Competence may however varies depending of the type ofoffer:

Equity securities and debt securities with denominations of less than €1000:• EU incorporated issuer: Member State where the issuer has its registered office;• Non-EU incorporated Issuer: Member State where the issuer's securities have been or are offered

to the public or admitted to trading on a regulated market for the first time after 31 December2003;

• In principle where a public offer of financial equity securities or debt securities with adenomination below 1.000 Euros is made only in France or in one or more other member States ofthe European Community or States party to the EEA agreement, including France, the prospectusapproved by the AMF shall be drawn up in French

Debt securities with denominations of €1,000 or more:Whether EU or non EU incorporated issuer, Member State where the issuer has its registered office orone of the Member States where the securities are to be offered to the public or admitted to trading .

44Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

PROSPECTUS DIRECTIVES ENABLES A TRUE PASSPORTING PROCESS

• Only one competent authority in Europe (in the "Home Member State") isrequired to approve a single prospectus“.

• The approved Prospectus can be used in any Member State.

• The prospectus approved by the Home Member State and any supplementsthereto shall be valid 1 year for the public offer or the admission to trading in anynumber of Host Member States, provided that the competent authority of eachHost Member State is notified.

45Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

SOME SALES OR ISSUES ARE PROSPECTUS EXEMPTED :

The obligation to publish a prospectus does not apply to public offers of the followingfinancial securities:

- Shares issued in substitution for shares of the same class already issued, if theissuing of such new shares does not involve an increase in the issuer's capital;

- Financial securities offered in connection with a public exchange offer andcontaining information equivalent to that of the prospectus, is made available bythe issuer;

- Financial securities offered, allotted or to be allotted in connection with a merger,demerger or spin-off, provided that a document, subject to AMF scrutiny

- Offers of non-equity securities issued in a continuous or repeated manner bycredit institutions whose total consideration in the EEA is less than €75 million

46Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

- Shares offered, allotted or to be allotted free of charge to shareholders, anddividends paid out in the form of shares, and provided that a document containinginformation on the number and nature of the securities and the reasons for anddetails of the offer is made available by the issuer.

- Financial securities offered, allotted or to be allotted to directors, to companyofficers (free shares) and current and former employees, and provided that adocument containing information on the number and nature of the securities andthe reasons for and details of the offer is made available by the issuer.

47Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

Investment services (Directive 2004/39/EC on Market In Financial Instruments)

• (1) Reception and transmission of orders in relation to one or more financial instruments.

• (2) Execution of orders on behalf of clients: acting to conclude agreements to buy or sell one or more financial instruments on behalf of clients;

• (3) Dealing on own account: trading against proprietary capital resulting in the conclusion of transactions in one or more financial instruments;

• (4) Portfolio management (AIFM): managing portfolios in accordance with mandates given by clients on a discretionary client-by-client basis where such portfolios include one or more financial instruments

• (5) Investment advice: means the provision of personal recommendations to a client, either upon its request or at the initiative of the investment firm, in respect of one or more transactions relating to financial instruments;

• (6) Underwriting of financial instruments and/or placing of financial instruments on a firm commitment basis.

• (7) Placing of financial instruments without a firm commitment basis

• (8) Operation of Multilateral Trading Facilities.

48Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations

Banking or financial promotion in France

Banking or financial promotion, or solicitation, consists in contacting a person, by whatevermeans, in order to offer:

- Transactions in financial instruments (Article L.211-1);

- Banking or ancillary transactions (Articles L. 311-1 and L.311-2);

- Investment services or ancillary services (Articles L. 321-1 and L.321-2);

- Transactions in miscellaneous assets (Article L.550-1);

- Investment advice (I of Article L.541-1).

- The person may be contacted by any means (personal visit, mail, telephone), either at home,at his or her place of work, or in any other place not intended for the marketing of financialproducts or services. For example, if a person is approached at a shopping mall, he or she isbeing solicited, but this is not the case if he or she is waiting in line at a bank.

49Fundamentals of Corporate Law

1. Capital raisings 1.1. Definitions1.2. Corporate law1.3. Financial law

1.2.1. Public offerings1.2.2. Admission to trading1.3.3. Prospectus1.4.4. Other regulations