section 2 – real estate settlement ...training.cuna.org/self_study/regtrac/member_regtrac/...a bit...

TRANSCRIPT

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-1

SECTION 2 – REAL ESTATE SETTLEMENT

PROCEDURES ACT AND CFPB’S REGULATION X

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-2

Overview

The world of regulatory compliance is filled with a wide variety of complexities and detail. Nowhere is that more true than in the area of real estate transac-tions. Just as real estate transactions in general require more paperwork and legal hurdles to clear than other less complicated lending transactions, so too are the regulatory requirements for mort-gage loans more cumbersome than those for other transactions, thanks in no small part to RESPA—an acronym that quickly becomes familiar to even the most nov-ice mortgage lender. Despite developing familiarity with the term “RESPA”, the detailed compliance requirements are a bit more difficult to digest. This sec-tion of the book is an attempt to address those requirements in some detail.

The Real Estate Settlement Procedures Act (12 USC 2601 et seq), much more commonly referred to by its initials, RESPA, is a consumer protection statute that serves two pri-mary purposes: first, to help borrowers become better shoppers for real estate settlement services; and second, to eliminate kickbacks and referral fees that add unnecessary costs to real estate transactions. RESPA also sets forth specific rules regarding the administra-tion of escrow accounts. The statute is implemented by Regulation X at 12 CFR 1024 (Reg X), which, since July 21, 2011, is administered by the Consumer Financial Protection Bureau (CFPB).

Previously, Reg X had been adminis-tered by the Department of Housing and Urban Development (HUD).

The Dodd-Frank Act of 2010 estab-lished the CFPB and transferred certain consumer financial protection regula-tions from seven agencies, include HUD, to the new agency. The CFPB basically incorporated HUD’s existing Reg X. It did not impose any new substantive obli-gations on credit unions.

RESPA was first enacted by Congress in 1974, and has been amended several times since then, including in 1976, 1983, 1990, 1992, 1994, 1996 and most recently in late 2008. Not surpris-ingly, Reg X has undergone several revi-sions as well since HUD first adopted it in 1975. In January 2013, the CFPB issued final rules amending Reg X by adding mortgage servicing requirements and reorganizing the rule.

RESPA includes very specific restric-tions on the credit union’s relationships with various settlement service provid-ers. Penalties for violations of RESPA and Reg X can range from civil (including class action) liability to criminal liability.

Coverage

When it was first passed in 1974, RESPA covered only first liens on residential real property. Through later amendments it was expanded to include not only first liens but refinancing and subordinate lien transactions as well. In general, RESPA now covers all loans

Section 2 – Real Estate Settlement Procedures Act and CFPB’s Regulation X

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-3

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

secured with a mortgage placed on a one-to-four family residential prop-erty. This means most purchase money loans, assumptions, refinances, property improvement loans, and home equity lines of credit are within the scope of the law and regulation.

RESPA and Reg X apply to “feder-ally related mortgage loans.” A loan is a “federally related mortgage loan” if:

1. It is secured by either a first or a subordinate lien on residential property.

2. The residential property contains or will contain a one-to-four family structure.

3. The lender is federally regulated or federally insured.

It is not necessary for the security interest to be created through a mort-gage instrument in order for RESPA to apply. The document evidencing the lien can be called a mortgage, a deed of trust, or any similar document that cre-ates a consensual (that is a voluntary) lien on the property.

Reg X expressly provides that a “reverse mortgage is covered if the other requirements of a federally related mort-gage loan are met.” Under a reverse mort-gage transaction (also known as an equity conversion mortgage) no initial disburse-ment is made by the lender. Instead, the periodic “payments” are made to the homeowner, allowing the principal and interest to accumulate over time. The loan which is secured by the borrower’s home is then repaid in a lump sum when the property is sold. Although not widely used by credit unions at the present time, reverse mortgages are gradually becom-ing more popular as a means for mem-bers—particularly elderly members—to put the equity in their homes to use.

The sale of real estate for cash is not covered by RESPA as no mortgage lien is involved in that type of transaction. There is a presumption that the pur-chase of a home by land contract (also known as a lease-purchase agreement or a contract for deed) is not covered by RESPA as no mortgage lien is created. However, Regulation X provides that any “installment sales contract, land con-tract, or contract for deed or otherwise qualifying residential property is a feder-ally related mortgage loan if the contract is funded in whole or in part by proceeds of a loan made by any maker of (feder-ally related) mortgage loans.”

As mentioned above, RESPA and Reg X now apply to transactions where the credit union takes a subordinate lien on its member’s residence, or when the transaction is a refinance. Reg X pro-vides that a refinancing occurs when the existing debt obligation, presumably the note, is satisfied and a new obliga-tion is entered into with the same or a new lender. However, the definition of refinancing in Regulation X contains five exceptions. The following are not consid-ered refinancings and are therefore not covered by RESPA and Reg X:

• Renewal of a single payment obligation with no change in terms.

• Reduction in the Annual Percentage Rate (APR) with a corresponding change in the payment schedule.

• An agreement involving a court proceeding.

• A work-out agreement as a result of the member’s default that results in a change in the collateral or payment schedule, unless the rate is increased

NOTE:

The terms “federally related mortgage loan” and “mortgage loan” are used interchangeably in Regulation X.

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-4

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

or the amount of the debt is increased over what was owed at the time of the original note.

• Renewal of optional insurance where the premium is added to the existing debt.

Note: These exceptions from the definition of “refinancing” are nearly identical to the exceptions from the defi-nition of “refinancing” found in Truth In Lending and Regulation Z.

RESPA applies only when the residen-tial property contains either a structure designed principally for occupancy by one-to-four families or where this type of structure is built or placed on the resi-dential property as a result of the loan. The structure can be a condominium unit, a cooperative unit, or a manufac-tured home. The dwelling does not need to exist at the time the loan is made and the lien is acquired, as long as the pro-ceeds of the loan are used to build a one-to-four family structure or to purchase a manufactured home to be placed on real property. A loan is covered by RESPA only if the lien securing the loan applies to both the structure of the manufac-tured home and the real property.

RESPA does not require that the structure be the member/borrower’s principal residence. Therefore, vacation or second homes, as well as time-share interests, are covered. Although there is no requirement that the member live in the structure, a business purpose excep-tion provides that loans on rental prop-erty are not covered by RESPA.

The use the structure was designed for—not the member’s intended use—determines whether RESPA applies. When in doubt, however, credit unions

would be wise to assume that RESPA applies. For example, if the member is purchasing a property with commercial uses on the first floor and apartments on the second and third floors, it may not be clear whether the property would be “designed principally” for residential or commercial purposes. In such circum-stances, it is suggested that the loan comply with RESPA. At least one court has held, in McCarrick v. Polonia Fed. Sav. & Loan Ass’n, 502 F. Supp. 654 (ED Pa. 1980), that RESPA applied to the sale of the building in which the first floor had a commercial use and the upper floors were to be renovated for residen-tial purposes.

If a loan is for construction purposes, the application of RESPA rests on whether the loan can be converted into permanent financing with or without conditions, at the end of the construc-tion. If there is no right to convert the loan to permanent financing, it is not covered by RESPA unless the construc-tion loan is for more than two years. A construction loan, other than to a bona fide builder, for more than two years, is presumed to be covered by RESPA.

Exemptions

Regulation X specifically exempts cer-tain transactions from RESPA. Following is a list of exempt loans:

• Loans where the property securing the loan is twenty-five acres or more. In addition, loans that would otherwise be covered by RESPA if they are pri-marily for a business, commercial, or agriculture purpose.

• Loans secured by nonowner-occupied

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-5

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

rental property.

Note: The existence of an individual guarantor to a business, commercial or agriculture loan would not invalidate this exemption.

• Bridge loans or swing loans.

• Mortgage loans on vacant land.

Note: When making a loan secured by vacant land, the credit union has an obli-gation to ensure that the loan proceeds will not be used to build a one-to-four family structure or to purchase a manu-factured home within two years. The credit union should have the member sign a statement indicating that the loan will not be used for those purposes.

• Loans where the security interest is only in a manufactured home and not in the underlying real estate.

• Loan assumptions where the credit union does not retain the express right to approve the subsequent borrower.

Note: if the credit union’s approval is both required and obtained, RESPA applies to the assumption.

• A loan conversion that is consistent with the original mortgage and does not require a new note. For example, if the credit union converts a mortgage loan from a floating rate to a fixed rate, that conversion would not be subject to RESPA.

• Transactions in the secondary mort-gage market. However, Regulation X makes it clear that a secondary mort-gage transaction must be a bona fide secondary market transaction to be exempt. Reg X states that “HUD will consider the real source of funding and

the real interest of the funding lender” in determining if the loan qualifies for the exemption.

A transaction where a person brokers a loan between a mortgage broker deal-ing with the borrower and an investor who will buy the loan is not a second-ary market transaction. The regulation clearly states that the provisions dealing with servicing of mortgage loans and the administration of escrow accounts still apply to loans transferred in secondary market transactions. For a transaction to qualify as a secondary market transac-tion, the mortgage originator must fund the loan from its own money or from a line of credit for which it is liable, close the loan in its own name, and then sell it to a third party.

Mortgage broker transactions that are table funded are not secondary market transactions. RESPA defines table fund-ing as a “contemporaneous advance of loan funds and an assignment of the loan to the person advancing the funds.” If a mortgage broker closes the loan in its own name as part of a table funded transaction, the lender is the person to whom the obligation is initially assigned.

A mortgage broker is defined as a per-son (not an employee or exclusive agent of a lender) who brings the borrower and lender together and performs some of the services necessary for loan process-ing or origination.

Dealer loans are subject to RESPA requirements and are not considered secondary market transactions. A dealer is defined as a seller, contractor, or sup-plier of goods or services in the home improvement setting or a person in the business of selling manufactured homes at retail. A dealer loan is one where a

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-6

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

dealer assists the borrower in obtaining a federally related mortgage loan and then, in return for receipt of the pro-ceeds of the loan, assigns the dealer’s interests to the lender. Dealer loans are not considered secondary market trans-actions.

General Disclosure Requirements

RESPA requires credit unions to pro-vide members with the following disclo-sures:

• Affiliated Business Arrangement Disclosure

• Transfer Notice

• Initial Escrow Account Statement

• Annual Escrow Account Statement

Each of these disclosures will be addressed in more detail following.

Affiliated Business Arrangement disclosure

An Affiliated Business Arrangement disclosure must be provided to members no later than the time of a referral, or, if the credit union requires the use of a particular settlement service provider, at the time the credit union receives a mortgage loan application. The RESPA and Reg X provisions regarding affiliated business arrangements are discussed in more detail following, (see the discus-sion on antikickback provisions) but they are mentioned here because, if the credit union has an affiliated business arrangement, the proper disclosures must be made at the outset of the mort-gage transaction with the member.

Prohibition against requiring the use of affiliates

RESPA currently allows businesses to make referrals to their affiliates that provide loan services, as long as the con-sumer is not required to use the service. The November 2008 RESPA final rule clarifies that this will include incentives, as well as disincentives, although these provisions are not intended to eliminate the use of legitimate consumer discounts if they are not tied to the use of a specif-ic settlement provider. An example of an incentive would be providing a discount to the borrower if an affiliate is used for a certain service, which may not be ben-eficial if the affiliate charges more than other competitors or if the discount is offset by higher costs elsewhere.

However, providing a package of ser-vices in which the total price is less than the sum of the prices of the individual services will be permitted, assuming the use of the package is optional and that the lower price is not offset by higher costs elsewhere.

RESPA does not prevent a settle-ment service provider or anyone else from offering a discount or other thing of value directly to the consumer. However, RESPA and this final rule limit tying such a discount to the use of an affiliat-ed settlement service provider. The rule is intended for consumers to affiliated and preferred businesses if the costs of using those businesses are lower than the costs associated with similar ser-vices from other providers. The final rule provides that settlement service provid-ers can offer ‘‘a combination of bona fide settlement services at a total price lower than the sum of the market prices

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-7

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

of the individual settlement services and will not be found to have required the use of the settlement service providers as long as: (1) The use of any such com-bination is optional to the purchaser; and (2) the lower price for the combina-tion is not made up by higher costs else-where in the settlement process.”

Transfer of Servicing Rights Disclosure Statement

With limited exceptions, the assign-ment, sale or transfer of servicing rights triggers additional disclosures. However, if there is no change in the person to whom payment is to be made, the address to which the payment is sent, the account number, or the amount of the payment due, no disclosure is required. The types of transfers that are exempt if these conditions are met include:

• The transfer of servicing rights between affiliates.

• A transfer resulting from a merger or acquisition.

• Transfers between master servicers where the subservicer remains the same.

A “master servicer” is a person who owns the servicing rights but who may use another person—the subservicer—to perform the actual servicing.

However, if disclosure is required, both the transferor servicer and the transferee servicer must make a disclo-sure to the borrower at the time of any transfer of servicing rights. These notic-

es can be sent separately or combined. The timing of the disclosures relates to the effective date of the transfer. The effective date is the date the first pay-ment is due to the transferee servicer. With certain exceptions, the transferor servicer must make its disclosure not less than 15 days before the effective date and the transferee servicer must

Figure 2.1 Closing Costs

Closing costs are a combination of loan costs and other costs. The following items are typical loan costs and other costs required to complete the real estate closing process.

Loan Costs• Loan Points

• Application Fees

• Underwriting Fees

• Appraisal Fee

• Credit Report Fee

• Flood Determination Fee

• Flood Monitoring Fee

• Tax Status Research Fee

• Pest Inspection Fee

• Survey Fee

• Title – Insurance Binder

• Title – Lender’s Title Policy

• Title – Settlement Agent Fee

• Title – Title Search

Other Costs• Recording Fees and Other Taxes

• Transfer Taxes

• Homeowners Insurance Premium

• Mortgage Insurance Premium

• Prepaid Interest

• Property Taxes

• Homeowners Insurance

• Mortgage Insurance

• Property Taxes

• Title – Owner’s Title Policy (optional)

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-8

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

make its disclosures not more than 15 days after the effective date. If a com-bined disclosure is made, it must be made not less than 15 days prior to the effective date. The disclosure must be sent by first class mail, postage prepaid, or be made at settlement. Disclosures made as a part of settlement are deemed to meet the timing requirements.

The disclosure must contain the fol-lowing:

• The effective date of the transfer.

• The name, address, and telephone number (toll free or collect call) of the transferee.

• An appropriate contact number (toll free or collect call) of both the trans-feror’s and the transferee’s offices, to allow the borrower to ask questions about the transfer.

• The date after which the payment will no longer be accepted by the transferor and must be made to the transferee.

• Any effect the transfer will have on the terms of—or the member/borrower’s ability to maintain—optional insurance, such as mortgage, life, or disability insurance and what, if anything, the member/borrower must do to maintain such insurance.

• A statement that the transfer does not affect any term of the security instru-ment other than the servicing provi-sions.

• If a separate address must be used to make a written inquiry under the dispute resolution mechanism, that address must be given.

• A statement of the member/borrower’s rights under the dispute resolution mechanism.

There is a model form for making this disclosure. It contains the following required information in addition to the above list:

• A disclosure that during the 60-day period following the effective date of the transfer, a timely payment to the old servicer may not be treated as late by the servicer and no late fee may be assessed.

• A description of the dispute resolution mechanism and the protections for the member/borrower during this dispute resolution.

• A definition of “business day”.

• A statement that damages and costs may be recovered for violations of Section 6 of RESPA and that member/borrower should seek legal advice if he or she thinks a violation has occurred.

The rule also contains sample notice of transfer of servicing rights (the Notice of Assignment, Sale, or Transfer of Servicing Rights), that includes all of the required information set forth in the previous requirements. See Regulation X Real Estate Settlement Procedures Appendix MS-2 for sample language.

For 60 calendar days from the effec-tive date of the transfer, no late fee can be charged and the payment may not be deemed late for any other purpose if the payment is made in a timely fashion to the transferor. This is to ensure that the member/borrower will not be adversely affected by the transfer. The effec-tive day of transfer is not the date the

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-9

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

assignment, sale, or transfer is effective between the transferor and the trans-feree. It is the date the first payment is due to the transferee. In the case of a home equity conversion mortgage or a reverse mortgage, the effective date of the transfer is the date agreed upon by the transferor and transferee.

Initial and annual escrow account statements

An escrow account is an account established or controlled by a servicer of a federally related mortgage loan to col-lect sums to pay charges, such as taxes and insurance related to the property subject to the mortgage.

In addition to escrowing for taxes and insurance, many credit unions also administer an escrow account for any charges related to the mortgage prop-erty, including but not limited to pri-vate mortgage insurance, FHA monthly premiums, and credit life insurance. Regulation X provides that where an escrow item can be paid in installments and there is no discount for lump sum payment, such items must be paid by installments.

RESPA does not mandate escrow accounts. But it does set very particu-lar limits on the amount that can be required to be paid into a permitted escrow account, and requires specific disclosures with regard to those escrow accounts, both at settlement and there-after.

As mentioned above, an escrow account is an account established or controlled by a servicer of a federally related mortgage loan to collect sums to pay various charges related to that mort-

gage. A servicer is defined as the person responsible for the servicing of a loan, including the person who makes or holds the loan if such person also services the loan. Servicing is defined as:

The process of receiving any scheduled periodic payments from a borrower pursuant to the terms of any mortgage servicing the loan, including the amounts for escrow accounts under Section 10 of RESPA, and making the payments of principal and interest and such other payments with respect to the amounts received from the borrow-er to the owner of the loan or other third parties as may be required pursuant to the terms of the mort-gage loan documents or servicing contract.

Normally, a credit union will collect 12 mortgage payments and receive 12 escrow deposits between the time one escrow disbursement is made and the next time it is due. However, during the first year of the mortgage there may be fewer than 12 months between the date of the first mortgage payment after settlement and the date on which a pay-ment (for example, property taxes) is due and payable. As a result, the escrow fund will be short the amount needed to make the payment. HUD issued regula-tions that required lenders to use an aggregate analysis for all new loans and to switch from single-item analysis to aggregate analysis on existing loans. HUD also issued regulations that phased out pre-accrual practices. Pre-accrual refers to the requirement that the funds necessary for the payment of an escrow

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-10

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

item be on hand for some period (often up to one month) prior to the date the payment is due.

Escrow account analysis

At the outset of the servicing of a mortgage with an escrow account, the servicer must perform an escrow account analysis. The goal of this analysis is to determine a “target balance.” A target balance is the amount that is enough to pay the necessary disbursements throughout the course of the coming year, plus any allowed cushion.

The first step in preparing an escrow account analysis is to create a 13-month calendar beginning with the month before the first payment is due. For example, if a settlement is on May 15th and the first payment into the escrow account is due July 1st, the calendar would begin with June and end with June. An initial trial balance is created showing three items. First, the disburse-ments are listed in the months they are to be made. In determining when the disbursements are to be made, the ser-vicer assumes that each disbursement will be made on or before the deadline to take advantage of any discount, or the deadline to avoid a penalty. If the actual charge is known for the upcoming year, that amount is used. If the charge is unknown, the servicer must make an estimate of the charge. This is calcu-lated by using the prior year’s charge and applying the National Consumer Price Index for all Urban Consumers (CPI, All Items). If the property sub-ject to the escrow is unassessed new construction, the estimate must be based on assessments of comparable

properties in the market area. In addi-tion, month-end accounting is to be used. Under the month-end accounting, the time of disbursements and pay-ment within the month is irrelevant. For example, if items are to be disbursed in July, September, and December they are listed in those months.

For the next step in the analysis, 1/12th of the total disbursements is listed for each of the 12 months, begin-ning with the first payment date (in this example, July). A balance is then calcu-lated for each of the months, assuming each escrow payment and each escrow disbursement is made on time. This will produce some months in which there is a negative balance.

The next step is to find the lowest monthly balance (that is, the monthly balance with the highest negative amount), and add to the first month an amount that will bring the lowest month-ly balance to zero. All of the monthly balances are then calculated taking into account this added first month payment. This newly calculated running balance is called the Adjusted Trial Balance. Note that this results in the escrow account balance falling to zero at the end of one month during the period.

The next step is to add to the first month (in this example, June), the per-missible cushion, if any, and to adjust the monthly balances. This creates a trial balance with the cushion. Reg X does not require that a cushion be added but permits a cushion of no more than two months of escrow payments. Both the mortgage documents and state laws must be consulted in determining the permitted cushion. The lowest of the cushions permitted by Regulation X,

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-11

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

state law, or the mortgage documents controls. If the mortgage documents either are silent or provide that a cush-ion may be up to the limit of RESPA, the two-month cushion may be used unless state law has a lower limit. Once the amount of the limited permitted cush-ion, if any, is determined and added, the trial balance must be redone and checked to ensure the lowest monthly balance at any time during the upcom-ing year does not exceed the amount of the permissible cushion.

Not all items that are escrowed are paid on a yearly basis. Examples of such charges are flood insurance that is paid on a three-year cycle and assessments for public improvements that may be paid over multiple years. In such cases, the escrow account analysis must be made on the appropriate multiple-year basis. The effect of this analysis is that the escrow balance must still fall to no more than the permitted cushion, but this will occur only once in the multi-ple-year cycle when the escrow items include items that are payable less fre-quently than annually.

Regulation X sets out the limitation on the escrow payment the service may require at the time of settlement or when the escrow account is first created. The permitted payment is calculated by com-puting the amount that would normally have been paid into escrow from the date the charge or charges were last paid until the first escrow payment is due, plus a cushion equivalent to two months payment.

Aggregate analysis presents a problem for the settlement agent in listing the escrow amounts on the HUD-1 and the HUD-1A Settlement Statements. This is

because these statements require that the different items that make up the escrow payment be listed separately. Obviously, that requires each item to be calculated on an individual rather than an aggregate basis. To the extent that a cushion is needed, the total amount will exceed the limits set forth previously using aggregate analysis. The regula-tions provide a mechanism for dealing with this problem, however. It requires that an escrow account analysis be performed to determine the total initial escrow payment. The settlement agent may then calculate each item individu-ally and apply the permitted cushion to that item. The total of all these items is then added together and the amount of the initial payment is calculated using the escrow account analysis and is sub-tracted from that total. The difference is listed as a negative number on the last line of the 1000 series on the HUD-1 Settlement Statement. This number should be identified as “adjustment for aggregate analysis.” This effectively reduces the total deposit to the amount permitted under the aggregate analysis. This calculation is made by the ser-vicer, and the information is then given to the settlement agent to enter on the Settlement Statement.

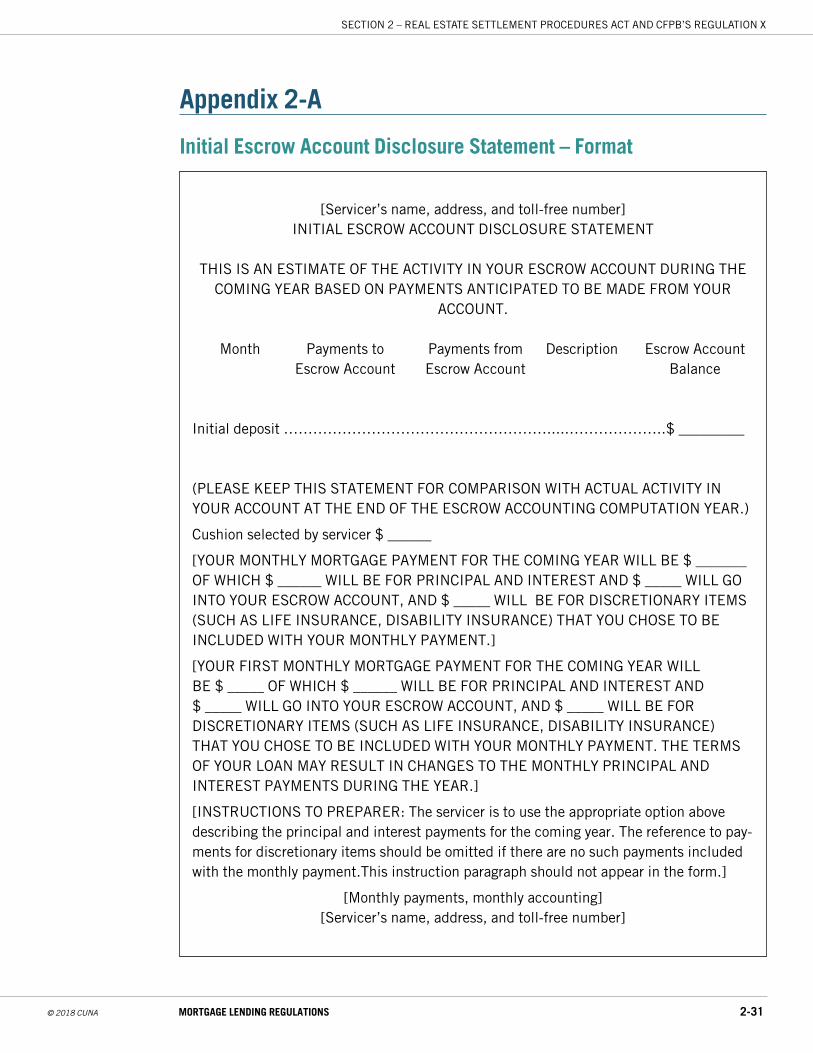

The monthly escrow payment col-lected after settlement is limited to an amount that will produce sufficient funds reasonably anticipated to pay the charges when they are due, plus any amount necessary to maintain the permissible cushion. This amount must be set forth on a disclosure called the Initial Escrow Account Disclosure Statement, which must be presented to the borrower at settlement or within 45

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-12

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

days following settlement. See Appendix 2-D for a sample statement.

Annual escrow account analysis

An escrow account must be reana-lyzed at least once every 12 months. To complete an annual escrow account analysis, the servicer creates an “escrow account computation year” which is the 12th month beginning with the initial payment date and each 12th month thereafter. The escrow account must be analyzed at the end of each escrow account computation year. The informa-tion resulting from the annual escrow account analysis must be disclosed to the member/borrower within thirty cal-endar days of the close of the escrow account computation year on a notice called the Annual Escrow Account Statement. The servicer is permitted to reanalyze the escrow account prior to the normal end of the escrow account com-putation year to allow it to change the effective date of the member/borrower’s annual escrow computation year to even-ly distribute its workload over the year.

If the servicing of an escrow account is transferred and the new servicer changes the amount of the payment, the account must be reanalyzed and a disclosure made to the member/borrower in the form of an Initial Escrow Account Statement. This has the effect of creat-ing a new annual escrow computation year. If the servicer must advance funds to pay a disbursement, which is not the result of a failure of the member/borrower to make a required payment, the servicer may wish to reanalyze the escrow account to determine the extent of the deficiency in the account. This

step is necessary before the servicer can attempt to collect the deficiency.

Escrow deficiencies

If a deficiency exists in an escrow account, the servicer must give the member/borrower notice of the defi-ciency at least once during the escrow account computation year. The notice can be a special notice or be part of the Annual Escrow Accountant Statement. The servicer also has the option of sim-ply allowing the deficiency to exist. However, if the servicer decides to col-lect the deficiency, the options depend on whether the amount of the deficiency is equal to, greater than, or less than the amount of the monthly escrow pay-ment. If the deficiency is equal to or greater than the monthly escrow pay-ment, the servicer “may require the borrower to repay the deficiency in two or more monthly installments.” If the deficiency is less than the amount of the monthly escrow payment, the servicer may require the member/borrower to repay the deficiency within 30 days or “may require the borrower to repay the deficiency in two or more equal monthly payments.”

If an outstanding payment is more than 30 days past the due date, the servicer may use the remedies provided in the loan documents to recover the deficiency. A shortage is the amount by which the balance in the escrow account falls short of the target balance at the time of an escrow account analysis. The target balance is the amount necessary to pay the required disbursements over the following year plus the allowed cush-ion. An account can have both a defi-

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-13

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

ciency and a shortage. However, if the member/borrower is not current on the loan payments, the servicer may retain the surplus in the escrow account pur-suant to the terms in the mortgage loan document.

There are no criminal penalties or civil remedies expressly set out in RESPA or Regulation X for violation of the Escrow Account Rules (Section 10(a)). However, there is conflicting case law on whether a civil action may be brought under Section 10(a) of Regulation X.

In general, Reg X requires two disclo-sures with respect to escrow accounts, the Initial Escrow Account Statement and the Annual Escrow Account Statement. A credit union may not charge a fee for the preparation and/or delivery of either of these disclosures.

The servicer is required to deliver the Initial Escrow Account Statement to the member/borrower and must be given at the time the escrow account is established. If the escrow account is established as a condition of the loan, the Initial Escrow Account Statement must be delivered to the member/bor-rower within 45 calendar days of settle-ment, or can be delivered at settlement. If there is a transfer of servicing and the new servicer changes the monthly pay-ment amount, the new servicer must provide the member/borrower with a new Initial Escrow Account Statement (as discussed earlier) within 60 days of the date of the servicing transfer.

The regulation specifically requires the following information in the Initial Escrow Account Statement:

• The amount of the monthly mortgage payments.

• The portion of the monthly payment going into the escrow account.

• Any discretionary payment made part of the mortgage payment.

• An itemization of the types and amount of charges that the servicer reasonably anticipates will be paid out of the escrow account over the follow-ing twelve months.

• The anticipated disbursement dates for each of the charges.

• The permitted cushion chosen by the servicer.

• A trial running balance of the account.

The disbursement must be identi-fied as to the nature of the charge. For example, identifiers such as “taxes” and “insurance” may be used rather than a specific payee. However, if there is more than one of a particular type of charge, for example, “school taxes” and “city taxes” each one must be identified indi-vidually.

The regulations provide a format for the Initial Escrow Account Statement labeled the Initial Escrow Account Disclosure Statement. If the mort-gage loan is paid on a biweekly basis, the Initial Escrow Account Disclosure Statement must reflect 26 payments rather than monthly payments. The Initial Escrow Account Statement may be incorporated into the HUD-1 or HUD-1A Settlement Statement either as part of the basic text or as an attachment. If the servicer does not incorporate the statement into the HUD-1 or HUD-1A Settlement Statement, it must be sub-mitted to the member/borrower as a separate document.

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-14

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

The timing of the delivery of the Annual Escrow Account Statement relates to what the regulations refer as to the escrow account computation year. The escrow account computation year is the 12-month period beginning on the date of the member/borrowers first payment into the escrow account and each subsequent twelve-month period, beginning on the anniversary of the initial payment. Normally, the servicer must deliver the Annual Escrow Account Statement to the member/borrower with-in 30 calendar days of the completion of each escrow account computation year.

If the servicer wishes to change the anniversary date of the escrow account computation year to even out the work load as discussed earlier, a short term Annual Escrow Account Statement (referred to as a Short Year Statement) can be delivered to the member/borrow-er. The Short Year Statement must be delivered within sixty calendar days of the end of the shortened escrow account computation year.

A transfer of service typically creates a shortened escrow accountant compu-tation year. The end of this shortened computation year is the effective date of the transfer of the servicing, which is the date on which the mortgage payment is first due to the new servicer. In that case, a Short Year Statement must be delivered by the old servicer to the mem-ber/borrower within sixty calendar days of the effective date of the transfer.

When a member/borrower pays off a mortgage loan, this typically creates a shortened escrow account computation year as well. The end of the shortened computation year in that case is the date the servicer receives the pay-off funds

from the member/borrower. The Short Year Statement must be delivered by the servicer to the member/borrower within sixty calendar days from the receipt of the pay-off funds.

As discussed earlier, no Annual Escrow Account Statement is required if the member/borrower is more than thirty calendar days overdue on the loan payment. Similarly, if the servicer has started a foreclosure action as a result of a default under the mortgage loan or is in bankruptcy proceedings, no Annual Escrow Account Statement is required. If such a loan subsequently becomes current, the service provider must pro-vide a history of the account within ninety days of the date the loan becomes current.

The Annual Escrow Account State-ment must contain a history of the escrow account during the prior escrow account computation year and a projec-tion of the activity in the escrow account for the next escrow account computation year. The servicer is also required to pro-vide the member/borrower with a copy of the Initial Escrow Account Statement, if it is the end of the first escrow account computation year, or the previous year’s projection if it is the end of a subse-quent escrow account computation year. The regulations specifically require, at a minimum, the following additional infor-mation in the Annual Escrow Account Statement:

• The amount of the past year’s monthly payment by the member/borrower.

• The portion of the past year’s monthly payment that is going into the escrow account.

• The portion of the last year’s monthly

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-15

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

payment that is going to discretionary payments.

• The total amount paid into the escrow account during the past year.

• The total amount paid out of the escrow account for the prior year for the various escrow items.

• The balance in the escrow account at the end of the escrow account compu-tation year.

• An explanation of how any surplus is being handled.

• An explanation of how any shortage or deficiency is to be paid.

• An explanation of the reason or reasons why the estimated low monthly bal-ance was not reached, if this occurs.

• The amount of the borrower’s current monthly payment that is going into the escrow account.

The regulations provide a format for the Annual Escrow Account Statement entitled “Annual Escrow Account Disclosure Statement.” The regulations permit the servicer to deliver the Annual Escrow Account Statement to the bor-rower with other statements or materials. See Appendix 2-E for a sample Annual Escrow Account Disclosure Statement.

Section 8: Anti-kickback Rules

Section 8 of RESPA contains a broad prohibition against referral fees and unearned fee arrangements in relation to any federally related mortgage loan.

The two basic sections of RESPA which prohibit referral fees and unearned fee arrangements are Section 8(a) and 8(b). These provisions have been amplified by Reg X. Section 8(a) prohibits the giving and accepting of “any fee, kickback, or thing of value” in return for the referral of settlement services business. Section 8(b) prohibits the giving and accepting of any portion of the fee or price paid by the member/borrower for settlement services other than for services actually performed. The payment of a referral fee or the fee splitting arrangement must be in the context of settlement services for a federally related loan in order for Section 8 to apply. RESPA provides that a settlement service “includes any service provided in connection with a real estate settlement.”

The list of settlement services con-tained in Regulation X is as follows:

• The origination, processing, or funding of a federally related mortgage loan.

• The rendering of services by a mort-gage broker (including counseling, taking of applications, obtaining verifi-cations and appraisals and other loan processing and origination services, and communicating with the borrower and lender).

• The providing of any services related to the origination, processing, or funding of a federally related mortgage loan.

• The providing of title services, includ-ing title searches, title examinations, abstract preparation, insurability deter-minations, and the issuance of title com-mitments and title insurance policies.

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-16

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

• The rendering of services by an attorney.

• The preparing of documents, including notarization, delivery, and recordation.

• The rendering of credit reports and appraisals.

• The rendering of inspections, includ-ing inspections required by applicable law or any inspections required by the sales contract or mortgage documents prior to transfer of title.

• The conducting of settlement by a settlement agent and any related services.

• The providing of services involving mortgage insurance.

• The providing of services involving haz-ard, flood, or other casualty insurance of homeowner’s warranties.

• The providing of services involving mortgage, life, disability or similar insurance designed to pay a mortgage loan upon disability or death of a mem-ber/borrower, if required by the credit union as a condition of the loan.

• The providing of services involving real property taxes or any other assess-ments or charges on the real property.

• The rendering of services by a real estate agent or broker.

• The providing of any other services for which a settlement service provider requires a member/borrower or seller to pay.

HUD intended to include any activity related to a federally related mortgage loan transaction as a settlement ser-

vice. Reg X also extends the coverage of Section 8 to “business incident to or part of a settlement service”.

Secondary market transactions are not settlement services and are therefore exempt from RESPA. Reg X provides that a “bona fide transfer of the obli-gation in the secondary market is not covered by RESPA”. However, Reg X specifically states that table financing, where a mortgage broker closes and sells the loan at the same time so that the buyer of the mortgage effectively funds the loan, is not a secondary transaction.

Illustration Number five in Appendix B to Reg X includes an example of a transaction that meets the requirements of a secondary transaction:

Facts: A mortgage originator receives loan applications, funds the loan with its own money or with the wholesale line of credit for which A is liable, and closes the loan in A’s own name. Subsequently B, a mortgage lender, purchases the loan and compen-sates A for the value of the loans, as well as for any mortgage servicing rights.

Comments: Compensation for the sale of a mortgage loan and servicing rights con-stitutes a secondary market transaction, rather than a referral fee, and is beyond the scope of Section 8 of RESPA. For purposes of Section 8, in determining whether a bona fide transfer of the loan obligation has taken place, HUD examines the real source of funding and the real interest of the named settlement lender.

To violate Section 8(a) and Regulation X, Section 3500.14(b), three elements must be present:

1. There must be a payment or giving of a thing of value;

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-17

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

2. It must be pursuant to an agreement to refer business; and

3. A referral must occur.

Both RESPA and Regulation X sug-gest the following examples of what con-stitutes a thing of value:

• Money

• Things

• Discount

• Salary

• Commissions

• Fees

• Duplicate payment of a charge

• Stock

• Dividends

• Distribution of partnership profit.

• Franchise royalty

• Credits representing monies that may be paid at a future date

• The opportunity to participate in a money making program

• Retained or increased earnings

• Increased equity in a parent or subsidiary entity

• Special bank deposits or accounts

• Special or unusual banking terms

• Services of all types at special or free rates

• Sales or rentals at special prices or rates

• Lease or rental payments based in whole or in part on the amount of business referred

• Trips and payments of another person’s expenses

• Reduction in credit against an existing obligation

Reg X provides that “the fact that the transfer of the thing of value does not result in an increase of any charge made by the person giving the thing of value is irrelevant in determining whether the act is prohibited.”

The rule does not contain any provi-sion concerning the legality of yield-spread payments. A yield-spread pre-mium is an amount paid by a lender to a mortgage broker for obtaining a rate on a loan that is higher than the rate at which the lender would have been willing to lend. The special information booklet contains the statement: “your mortgage broker may be paid by the lender, you as the borrower, or both.” This language suggests that yield-spread premiums are not per se illegal. The lender is getting something beyond the referral itself for its payment — a higher yielding loan. The real question is whether the yield-spread premium is a competitive one. If so, there is an excess payment for the referral itself. However, if the yield-spread premium is higher than generally paid in the particular market place, the excess could be viewed as a payment for the referral of the particular mortgage.

Reg X clearly covers a computer loan origination system (CLOs), particularly given the fact that a settlement service includes “business incident to or part of a settlement service.” CLOs that pro-vide services to customers may charge customers for services performed. Such payments by member/borrowers must be disclosed on the Good-Faith Estimate and the Settlement Statement. There is no requirement regarding the timing of these payments, but if made prior to

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-18

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

settlement, they must be shown as P.O.C. on the Settlement Statement. A settlement service provider whose prod-ucts are made available on CLOs may reimburse the member/borrower for any fee charged to the member/borrower by the CLO.

Reg X defines referral as “any oral or written action directed to a person which has the effect of affirmatively influenc-ing the selection by any person of a provider of a settlement service or busi-ness incident to or part of a settlement service,” where the person pays for the service.

The major interpretative question on a referral is what constitutes “affirmatively influencing.” Obviously, a statement by a broker that a member/borrower should use a particular title company would meet the definition. However, if the bro-ker gave the member/borrower a list of three title companies in the area, would that constitute a referral since it has some affirmative influences? It seems that the credit union may offer a neutral information list “that ranks lenders and their mortgage products on the basis of some factor relevant to the borrower’s choice of product, such as APR calculat-ed to include all charges and to account for the expected tenure of the buyer.”

As mentioned earlier, Reg X provides that the use of a particular settlement provider is required if the availability of a particular service is conditioned on the use of the settlement provider. However, the offering of services in a package at a reduced rate is not a required use of any of those services if the package is optional and the discount is a true dis-count.

RESPA specifically prohibits payment

to employees for referrals to subsidiaries through indirect means. Reg X states: “a company may not pay another company or the employees of another company for the referral of settlement service busi-ness.” Any employee, regardless of that employee’s job function, may be paid a fee for referring business to his or her own employer but not for referring busi-ness to an affiliate or a third party. Reg X expressly prohibits such payments between business entities.

A violation of RESPA occurs in a set-ting where payment exceeds the value of the goods and services delivered by the payee. The excess payment is likely to be the referral of business. The mere fact that some services are rendered or goods are delivered does not mean there is no violation. The services may not be ones that in reality inure to the payor’s benefit. The payment may not be greater than the reasonable value of the services rendered or goods provided. Perhaps the best test of this would be to ask two questions. First, are these services or goods that the payer of the fee would reasonably require? That is, are the ser-vices or goods necessary? If the answer is no, then the services or goods are probably a pretext for the payment of the fee and that payment will likely violate Section 8 of RESPA. Second, assuming that the payer of the fee would reason-ably require the services or goods, is the fee reasonable in light of the services actually performed or goods actually delivered? If the answer is no, then the fee is excessive and again the payment would violate Section 8 of RESPA.

There have been a number of com-plaints that lenders were leasing desks or office space in real estate brokerage

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-19

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

offices at higher than market rates in exchange for referrals of business. Prior to the CFPB’s authority, HUD indicated that it would analyze this type of situa-tion based on a comparison of the rent paid to the brokerage office to the gen-eral market rent that a non-settlement service provider would pay for the same amount of space and services in the same or comparable building. If the rent is higher, it would likely be deemed a payment for the referral. This test uses a general market rate paid by non-settlement service providers and not the rate paid by other settlement service providers. HUD stated that “if the rental payment is conditioned on the number or value of the referrals made, then HUD will consider the rental payment to be for the referral of business in violation Section 8(a).”

HUD also took an informal position on the legality of captive reinsurance programs. In such a program, a mortgage lender has a fully licensed reinsurance affiliate. The reinsurance affiliate enters into a contract with an unaffiliated pri-mary mortgage insurer, in which the reinsurance affiliate is paid a portion of the mortgage insurance fee received by the primary mortgage insurer for insur-ing loans originated by the credit union. The payment of the fee is in turn for the reinsurance affiliate’s taking on some of the risk. There is no violation of RESPA if reinsurance is actually provided and the fee paid to the reinsurance affiliate does not exceed the value of the reinsurance.

The payment of an unearned fee also arises in the case where the party performing the services or providing the goods for which it receives a fee is already obligated to perform those servic-

es or provide those goods. Regulation X states that when a person is already being paid for services in the transaction, any additional payment by a service provider “must be for services that are actual, necessary and distinct from the primary services provided by such person.”

Two court cases of interest

Two federal appellate cases in the Fourth and Seventh Circuits have adopt-ed interpretations of Section 8(b) of RESPA that differ from interpretations that have been previously issued by HUD.

In Boulware v. Crossland Mortgage Corp. in the Fourth Circuit and Echevarria v. Chicago Title & Trust Co. in the Seventh Circuit, the court ruled that Section 8(b) permits the “mark up” of settlement services under certain circumstances, which includes the practice of charg-ing a consumer more for a third party’s settlement services than is actually paid to the third party.

Therefore, for property located in the Fourth and Seventh Circuits, which includes Illinois, Indiana, Maryland, North Carolina, South Carolina, Virginia, West Virginia, and Wisconsin, NCUA examiners will not cite a violation of Section 8(b) of RESPA under the follow-ing situation:

• The consumer is charged more for a settlement service provided by a third party than is actually paid to that third party, and

• The third party is not involved in the mark up.

For more information, refer to NCUA Regulatory Alert No. 03-RA-01

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-20

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

Payments allowed under Section 8

Section 8(c) of RESPA expressly excludes certain payments from the gen-eral prohibitions of Section 8. These are restated and augmented by Reg X. The excluded transactions in the statue and the regulations, include:

• Payment of a fee to an attorney for ser-vices actually rendered.

• Payment of a fee to a duly appointed agent of a title company by that com-pany for services actually performed in issuing the title policy.

• Payment of a fee by a lender to a duly appointed agent of that lender for ser-vices actually performed in making the loan.

• Payment of a bona fide salary to any person for services actually performed.

• Payment of any compensation for goods or facilities actually furnished or services actually performed.

• Payments pursuant to a cooperative brokerage arrangement or arrange-ments between real estate agents and brokers.

• An affiliated business arrangement.

Reg X adds two additional exceptions. The first deals with employer payments to employees for referral of settlement services. The other deals with “normal promotional and educational activities.” Under the second exemption, the giv-ing of a thing of value which is a normal promotional or educational activity, to a person in a position to refer business, is not considered a violation of RESPA.

The RESPA antikickback provisions are of great importance to credit unions, in that many of them work for brokers who in turn compensate those credit unions for their business. These arrangements are permissible, as long as whatever compen-sation the credit union receives is justified by the work the credit union has done. HUD previously published additional guid-ance in this area in its “RESPA Statement of Policy 1999-1 Regarding Lender Payments to Mortgage Brokers.”

Affiliated business arrangements

Affiliated business arrangements generally refer to a situation where a person or firm is in a position to refer purchasers of settlement services to a settlement service provider that is owned in whole or in part by the referring party. Although the referring party receives no direct payment for the referral, it benefits through the ownership interest in the service provider. The basic objection to this arrangement is that it creates what is known as “reverse competition.”

The concept of reverse competition arises when there is no direct market-ing of the services to the consumer. The marketing is to referral sources who make decisions for the consumer. The argument here is that in those situa-tions, the provider of the service is not encouraged to attract business by reduc-ing prices or increasing quality. Instead, it attracts business by increasing the benefit given to the referral source. It is further argued that in the affiliated-business setting there is no incentive to reduce prices or increase services since the referral source owns the service pro-vider. Additionally, there is no need to

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-21

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

give the referral source a direct benefit since, as the owner of the service pro-vider, the referral source receives the benefits earned. However, the argument that an affiliated business relationship is anticompetitive has been challenged.

An affiliated-business arrangement is defined very broadly under both RESPA and Reg X. It exists when a person or an associate of a person in a position to refer settlement service business has an affiliate relationship with or a direct beneficial ownership of more than 1% in a provider of settlement services and, where a federally related mortgage is involved, the person directly or indi-rectly refers business to that provider or affirmatively influences the selection of that provider. If an entity is not a bona fide provider of settlement services, but is merely a sham arrangement to act as a conduit for referral fees, then the arrangement does not meet the definition of an affiliated-business arrangement even if all other requirements of the affili-ated business exemption are met.

There are ten factors that may be considered when determining whether an entity is a bona fide settlement service provider or a sham arrangement. They are:

1. Does the service provider have sufficient initial capital and net worth, typical in the industry, to conduct the settlement service business for which it was cre-ated? Or is it undercapitalized to do the work it promises to provide?

2. Is the service provider staffed with its own employees to perform the services it provides? Or does it use “loaned” employees of one of the parent providers?

3. Does the service provider manage its own business affairs? Or is an entity that helped create it running the service pro-vider for the parent provider making the business referrals?

4. Does the service provider have an office for business that is separate from one of the parent providers? If the service provider is located at the same business address as one of the parent providers, does it pay a general market value rent for the facilities actually furnished?

5. Are substantial services being provided, for example, the essential functions of the real estate settlement service, for which the entity receives a fee? Does it assume the risks and receive the rewards of any comparable enterprise operating in the market place?

6. Does the service provider perform all of the substantial services itself? Or does it contract out part of the work? If so, how much of the work is contracted out?

7. If the service provider contracts out some of its essential functions, does it contract services from an independent third party? Or are the services con-tracted from a parent, affiliated provider or an entity that helped create it? If the service provider contracts out work to a parent, affiliated provider or an entity that helped create it, does the service provider provide any functions that are of value to the settlement process?

8. If the service provider contracts out work to another party, is the party performing the contracted services receiving pay-ment for the services or facilities provided that bears a reasonable relationship to the value of the services or goods received?

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-22

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

Or is the contractor providing services or goods at a charge such that the service provider is receiving a “thing of value” for referring settlement service business to the party performing the service?

9. Is the service provider actively compet-ing in the market place for business? Does the service provider receive or attempt to obtain business from settle-ment service providers other than one of the settlement service providers that it created?

10. Is the service provider sending business exclusively to one of the settlement service providers that created it (such as the title application for a title policy to a title insurance underwriter or a loan package to a lender)? Or does the ser-vice provider send business to a num-ber of entities, which may include one of the providers that created it?

A person who is in a position to refer settlement service business is expressly defined in Reg X. Real estate brokers or agents, lenders, mortgage brokers, builders or developers, attorneys, title companies or title agents always falls into this category. Any other person falls into this category only if the person receives “a significant portion of his or her gross income from providing settle-ment services.”

If an affiliated business arrangement exists, the person making the referral must meet the following three condi-tions to be protected from liability under Section 8:

1. The person making the referral gives an appropriate Affiliated Business Arrangement Disclosure Statement to each person a referral is made to.

2. With certain exceptions, the person to whom the referral is made is not required to use the referred settlement service provider.

3. The only thing of value received from the arrangement is a return on an ownership interest or franchise relationship.

See Regulation X Real Estate Settle-ment Procedures Appendix D for sample language.

Incidental and uncompensated referrals, such as brochures in a credit union’s lobby or street directions given by an employee is not considered a referral that requires an affiliated busi-ness disclosure. However, if the employ-ee making the referral is compensated for the referral, he or she must meet the exemptions for payments by employers to employees.

The person making the referral must disclose the following to each person referred:

• The existence and nature of the rela-tionship between the referring party and the settlement service provider.

• An estimate of the charge or the range of charges for the settlement services that would be provided by the settle-ment service provider.

• With certain exceptions, that the person receiving the referral is not required to use the referred settlement service provider, and that a lower rate may be made available by other settle-ment service providers.

If there is an ownership interest, the percentage of ownership must be dis-closed. The intent of this disclosure is to alert the party receiving the referral that

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-23

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

the party making the referral has a self-interest in the use of the referred settle-ment service provider and that the party being referred may wish to consider comparison shopping.

Reg X requires that the charges be listed in the affiliated business dis-closure using the same terminology, as far as practical, used in Section L of the HUD-1 or HUD-1A Settlement Statement. Also, they must be the esti-mated charges or range of charges of the particular settlement service provider to whom the referral is being made.

As protection, the referring party should routinely give the affiliated busi-ness disclosures, preferably at the very beginning of the relationship, to avoid an inadvertent oral referral before the disclosures are made. Reg X requires that the mortgage applicant sign the affiliated business disclosure, acknowl-edging that the applicant has read and understood the document. If there are multiple mortgage applicants, Reg X only requires one to sign.

Inadvertent error

Because the affiliated business dis-closure raises a number of interpretative issues, both RESPA and Reg X provide some protection for an inadvertent error. Reg X states:

Failure to comply with the Disclosure Requirement of this section may be overcome if the person making a referral can prove by a preponderance of the evi-dence that procedures reasonably adopted to result in compliance with these conditions was uninten-tional and the result of a bona fide

error. An error of legal judgment with respect to a person’s obliga-tions under RESPA is not a bona fide error.

There are two situations where the referring party can require the referred party to use an affiliated-settlement ser-vice provider without violating Section 8. The first situation is where a credit union requires the use of a particular “attorney, credit reporting agency or real estate appraiser chosen by the lender to represent the lender’s interest in a real estate transaction.” The second situation is where a lawyer or law firm arranges for a client it represents in a real estate transaction, to obtain “a title insurance policy directly as agent or through a separate corporate title insur-ance agency that may be established by that attorney or law firm and operated as an adjunct to the law practice of the attorney or law firm.”

The final requirement to fit within the affiliated business exception is that the person in a position to refer the settlement service business receive “only a return on ownership interest or franchise relationship.” Reg X sets out certain return on ownership or franchise interests that do not meet these require-ments. These are:

• Payments where there is no appar-ent basis for calculation other than the amount of referrals the person receives.

• Payments that vary according to the relative amount of the referrals by the recipients of similar payments.

• Payments on ownership shares that are readjusted based on previous referrals.

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-24

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

The following questions may be con-sidered in determining whether the pay-ment is a return on ownership interest or a payment for referrals:

• Has each owner or participant in the service provider made an investment of its own capital, as compared to a “loan” from an entity that receives the benefits of referrals?

• Have the owners or participants of the service provider received an ownership or participant’s interest based on a fair value contribution? Or is it based on the expected referrals to be provided by the referring owner or participant to a particular sale or division within the entity?

• Are the dividends, partnership distributions or other payments made in proportion to the ownership interest (proportional to the investment in the entity as a whole)? Or does the payment vary to reflect the amount of business referred to the service provider or a unit of it?

• Are the ownership interests in the service provider free from tie-ins to referrals of business? Or have there been any adjustments to the ownership interest based on the amount of business referred?

An affiliated business disclosure must be retained by the credit union for five years. It is advised that the credit union retain all documentation relating to any transactions between the party in a position to make a referral, the person to whom the referral is made and the settlement service provider for a period of five years.

Penalties for Violations of RESPA and Reg X

Failure to provide the Affiliated Business Arrangement Disclosures, or failure to abide the rules regarding mort-gage servicing, can result in civil liability for the credit union, both in terms of individual plaintiffs or in a class action.

Individual claimants can recover any actual damages. In addition, if the court finds that there is a pattern or practice of the type of violation complained of, a court can assess additional damages up to $1,000. In a class action, each mem-ber of the class is entitled to actual dam-ages as well as up to $1,000 additional damages if there is a pattern or practice of this type of violation. The additional damages are limited to the lesser of $500,000 or 1% of the net worth of the credit union. In addition to damages, the member/borrower is entitled to costs and reasonable attorney’s fees in case of a successful action.

As discussed above, RESPA and Regulation X provide a procedure by which a member/borrower can obtain information about his or her escrow account. Violations of those provisions do not give the member/borrower an express cause of action — that is, they cannot sue the credit union merely for failing to provide an escrow disclosure or otherwise violating the escrow account-ing rules. Despite this protection from civil liability to the borrower, the CFPB may impose a civil penalty of $55 for each failure to submit an Initial Escrow Account Statement or Annual Escrow Account Statement. This civil penalty may not exceed $110,000 for violations

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-25

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

in any 12-month period. If the violations are found to be intentional, the civil pen-alty is increased to $110 per violation, with no annual limitation on the amount of penalties that may be assessed.

Parties violating the prohibitions against kickbacks and unearned fees can be subject to civil and criminal penalties. Civil liability can equal three times the amount of the refer-ral fee, kickback, or unearned fees. Criminal penalties include a fine of up to $10,000, imprisonment for no more than one year, or both. In addition, the credit union can be required to pay court costs and reasonable attorney’s fees.

Recordkeeping Requirements

In general, evidence of compliance with all aspects of RESPA must be maintained for five years.

Relation to state lawsRESPA provides that state laws

addressing mortgage settlements are invalid only to the extent they are incon-sistent with RESPA. If state law gives greater protection to members, it cannot be deemed inconsistent with RESPA and the state law can be enforced.

Electronic disclosures and the E-Sign Act

The disclosures required under RESPA may be delivered electronically, pursuant to the Electric Signatures in Global and National Commerce Act (E-Sign).

Frequently Asked Questions

The following frequently asked ques-tions about RESPA and Regulation X should provide the reader with a review of the Act and the regulation and assist as a review for the test:

1. What kinds of transactions are covered under RESPA?

Transactions involving a federally related mortgage loan, which includes most loans secured by a lien (first or subordinate position) on residen-tial property. This includes home purchase loans, refinances, lender approved assumptions, property improvement loans, equity lines of credit, and reverse mortgages.

2. What types of transactions are generally not covered?

An all cash sale, a sale where the individual home seller takes back the mortgage, a rental property transac-tion or other business purpose trans-action.

3. Is a “time share” a covered transaction under RESPA?

Yes, if the credit union’s interest is secured by a lien on residential property.

4. Is a loan secured by a condominium unit or a cooperative share a covered transaction under RESPA?

Yes, as long as the units are not used for business purposes.

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-26

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

5. Is a loan secured by a manufactured home (mobile home) a covered transaction under RESPA?

Yes, but only if the manufactured home is located on real property (land) on which the credit union’s interest is secured by a lien.

6. Does a federally related mortgage loan only involve FHA, VA, or other government sponsored loans?

No, RESPA covers most conventional loans too.

7. Are home equity loans covered under RESPA?

Yes, home equity loans secured by residential property are covered.

8. How does the coverage of home equity loans and subordinate lien loans differ from other RESPA covered loans?

If the loan involves an open-end line of credit, providing the disclosures required by Regulation Z satisfies the RESPA requirements.

Both subordinate lien loans and open-end lines of credit (home equity loans) in first lien position are exempted from the loan servicing requirements.

9. Are construction loans covered under RESPA?

No. Unless: (1) the loan is used as, or may be converted to permanent financing by the same lender; or (2) the lender issues a commitment for permanent financing; or (3) the loan is used to finance a transfer of title to the first user; (4) the loan is for a

term of two years or more, unless it is to a bona fide builder.

10. If a loan is sold within one to seven days of closing to another lender, does the sale of that loan fall within RESPA’s coverage?

The sale of a loan after the original funding of the loan at settlement is a secondary market transaction. Such a sale is exempt from RESPA coverage as a secondary market transaction. However, any transfer of ownership and/or servicing rights is subject to RESPA’s requirements in Section 6.

11. Does the exemption from RESPA for the sale of a land parcel of at least 25 acres apply even if there are two homes on the property?

Yes, as long as the property is a single parcel.

12. Can a credit agency provide a credit union with a dedicated printer to expedite communication between the credit agency and the credit union?

Yes, provided the printer can only be used for communication with the credit union and not for general use. If it is for general use it may be con-sidered payment for the referral of business.

13. Can a flood zone certification company examine a credit union’s existing loan portfolio for free or at a reduced rate, in exchange for the credit union sending the company future business?

© 2018 CUNA MORTGAGE LENDING REGULATIONS 2-27

SECTION 2 – REAL ESTATE SETTLEMENT PROCEDURES ACT AND CFPB’S REGULATION X

No. Flood zone certification is a covered settlement service, therefore RESPA would apply to agreements by companies or persons providing portfolio reviews. Providing free or reduced reviews is a thing of value. Providing this service in exchange for referrals of future flood insurance business would violate Section 8(a) of RESPA.

14. Can a credit union set up a contest for real estate agents under which the agent who provides the credit union with the most business will win a trip?

No. Under RESPA, the trip itself, and even the opportunity to win the trip, would be a thing of value given in exchange for the referral of business.

15. Can a credit union give a member borrower an incentive, such as a chance to win a trip or a rebate, for doing business with the credit union?

RESPA does not prohibit a credit union or other settlement provider from giving the member/borrower an incentive for doing business with it as long as the incentive is not based on the member/borrower referring business to the credit union.

16. Can a mortgage banker and a real estate broker advertise their services together, for example, on the same brochure or newspaper advertisement?

Nothing in RESPA prevents joint advertising. However, if one party is paying less than a pro-rata share

for the brochure or advertisement, there could be a RESPA violation.

17. Can a credit union give a real estate agent note pads with the credit union’s name on it?