sector sample slides ruby consulting

TRANSCRIPT

SECTOR SAMPLE SLIDES RUBY CONSULTINGStrictly Private & ConfidentialFor Corporate & Investor Presentation Purpose

2Sample Document I Not For Circulation

This Sector Sample Slides (“Sample Document”) is being delivered with the intention to assist the recipient in deciding whether to proceed with a further discussion in respect of thematters stated herein (the “Business”). This Sample Document does not purport to be all-inclusive or to necessarily contain all the information that a prospective client may desire in.This Sample Document does not constitute an offer or form part of any offer for sale of Ruby Consulting (the “Company”) or of securities of the Company or otherwise, nor will anyinformation contained herein will form the basis of any contract. The content of this Sample Document should not be considered as any investment advice or recommendation.Reliance on any content of this Sample Document for the purpose of engaging in any speculative activity may expose the recipient to a significant risk of losing all of the property orother assets invested. Recipient should inform themselves as to the legal requirements applicable to them for any of the activities contemplated under this Sample Document.Further, the recipients should carry out their own investigations and analysis of the Company/Business and of the data referred to in this Sample Document and should consult theirown advisors.

By accepting this Sample Document, the recipient agrees to keep permanently the information confidential which is contained herein or made available in connection with any furtherdiscussion of the Business. This Presentation may not be photocopied, reproduced, or distributed to others at any time without the prior written consent of the Company. Theinformation contained in this Sample Document is intended solely for the recipient and may not be further distributed by the recipient. The Company accept no liability whatsoeverfor the actions of third parties.

This Sample Document does not contain any direct, indirect and/or deemed offer of any securities to the public as such or otherwise and does not constitute or form part of any offeror invitation to subscribe for, underwrite or purchase securities. Any such offer will be made strictly on a private placement basis by means of an information memorandum to beissued in compliance with applicable securities laws, which information memorandum will contain information about the issuer, its business operations and its management.

This Sample Document has been prepared for information purposes only and upon the express understanding that it will be used only for the purposes set forth above. The Companydoes not make any express or implied representation or warranty as to the accuracy or completeness or adequacy of the information contained herein or made available inconnection with any further investigation of the Business, or any investment decision made. The Company expressly disclaims any and all liability which may be based on suchinformation, errors therein or omissions there from. The recipient shall be entitled to rely solely on the representation and warranties made to it in any final definitive agreements.

The recipient assumes the entire risk arising from any use made of this information. In furnishing this Sample Document, the Company does not undertake any obligation to providethe recipient with access to any additional information. This Sample Document shall not be deemed to be an indication of the state of affairs of the Company/Business nor shall itconstitute an indication that there has been no change in the business or affairs of the Company/Business since the date hereof. The Sample Document includes certain statements,estimates and projections with respect to the anticipated future. Such statements, estimates and projections reflect various judgments and assumptions, which may or may not proveto be correct. Accordingly, there can be no assurance that the projected results will be attained.

Notwithstanding anything contained in this Sample Document, no responsibility or liability whatsoever is accepted for any loss or damage including any lost profits or savings orspecial, incidental, or consequential damage howsoever arising that you may directly or indirectly suffer as a result of this Sample Document and any and all responsibility and liabilityis expressly disclaimed by the Company and their respective directors, partners, officers, affiliates, employees, advisors or agents.

3Sample Document I Not For Circulation

America

• Processes like purchasing, warehousing, and inventory management handled separately

• Not much coordination between function

Early

• Internal integration within the company

• Better coordination between functions

• Individual contracts given for transportation, storage, forwarding etc

• Shift from godowns to function warehouses

Growth

• Greater external integration

• Bundling of services with the help of 3PL players

• Companies focus on core competencies and outsource logistics requirements to 3PL players

• World class warehouse higher automation

Consolidation• Strategic focus on reducing

cost redundancies and customers

• Supply chain management

• Global operations

• Single operator managing the supply chain of multiple geographies

• Move towards 4PL’s and 7PL’s

Mature

Under-Developed

India

China

Evolution of Logistics Industry

4Sample Document I Not For Circulation

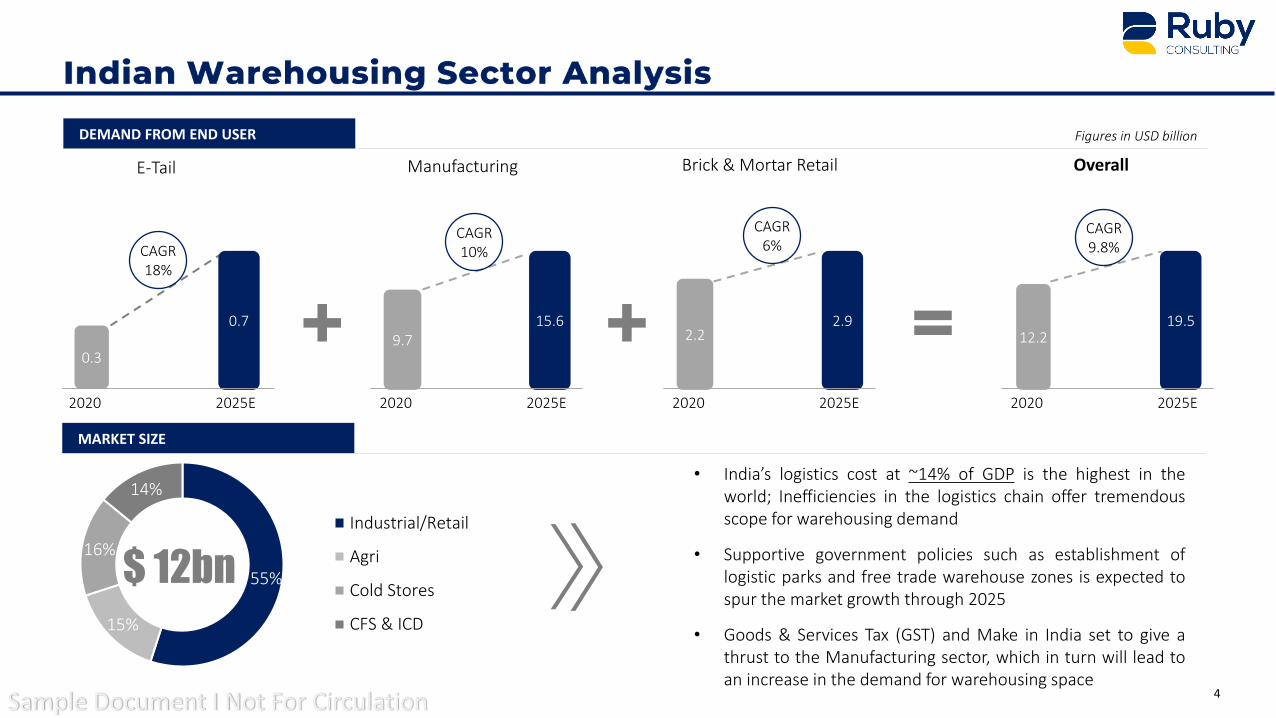

0.3

0.7

CAGR18%

12.219.5

CAGR9.8%

9.715.6

CAGR10%

2.22.9

CAGR6%

+ + =

Overall E-Tail Manufacturing Brick & Mortar Retail

2020 2025E 2020 2025E2020 2025E 2020 2025E

55%

15%

16%

14%

Industrial/Retail

Agri

Cold Stores

CFS & ICD

DEMAND FROM END USER

• India’s logistics cost at ~14% of GDP is the highest in theworld; Inefficiencies in the logistics chain offer tremendousscope for warehousing demand

• Supportive government policies such as establishment oflogistic parks and free trade warehouse zones is expected tospur the market growth through 2025

• Goods & Services Tax (GST) and Make in India set to give athrust to the Manufacturing sector, which in turn will lead toan increase in the demand for warehousing space

$ 12bn

MARKET SIZE

Figures in USD billion

5Sample Document I Not For Circulation

USD 95 Bn

15%

150x

2 ZETTABYTES

60%

8.4%

6Sample Document I Not For Circulation

• • • •

•

•

•

•

•

•

7Sample Document I Not For Circulation

Digital Contribution to Middle East Economy is Low Compared with Benchmarks

Source: Mckinsey Report

18.0

15.2

8.4

United States Europe Middle East

13.6

7.6 6.6

16.4

11.5

8.2

14.9

Bahrain Kuwait Egypt UAE Saudi Arabia Oman Qatar

8.06.2

4.1

United States Europe Middle East

8.0

5.1 4.4 4.3 3.8

0.9 0.4

Bahrain Kuwait Egypt UAE Saudi Arabia Oman Qatar

Share of Digital Contribution to GDP (%)

Source: Mckinsey Report

Digital Contribution to Middle East Economy is Low Compared with Benchmarks

The Middle East captures just a fraction of its Digital Potential

Captured Digital Potential by Country (%)

8Sample Document I Not For Circulation

36

47

50

61

97

Source: Mckinsey Report Source: Mckinsey Report

9Sample Document I Not For Circulation

$50bn

2020

$200bn

2030

15% CAGR

Global Market Size

54%46%

2020

Worldwide Share of Infrastructure Hardware Spending for Cloud and

Traditional Environments

• Pandemic induced Digital Transformation

• Growth of Big Data

• Use of cloud-based services by SMEs

• Rollout of 5G

• Artificial Intelligence & IoT in major sectors

• Higher consumption of data by consumers through e-commerce and social media platforms

Demand Drivers

Source: Global Market Insights, Internal Analysis, IDC

US$ 128 bn

2024

US$ 168 bn

Traditional Infrastructure

Cloud Infrastructure

Increasing need to store & process massive data generated globally will drive the need for Data Center colocation services

63%

37%

10Sample Document I Not For Circulation

$3.1bn

2019

$3.7bn

2025

MENA Market Revenue

3% CAGR

Source: Business Insider

The IoT revenue in the Middle East is expected to grow at a CAGR of over 15% by 2025

Adoption of 5G networks and provision for high-capacity connection up to 10gp/s

Increase in smart city initiatives is expected to develop the demand for edge computing and edge data centers among countries in GCC

Renewable Energy Powered Facilities to grow in Middle East

Cloud Adoption fueling Data Center Investments

Increased Government Support to Boost Digital Economy in Middle East

11Sample Document I Not For Circulation

-0.6

-0.3

0

0.3

0.6

0.9

1.2

1.5

1.8

2016-2020 2020-2025 2025-2030 2030-2035 2035-2040

Average Annual Oil Demand Growth (in Mb/d)

Eurasia DCs (excl China and India) China India OECD World

0%

20%

40%

60%

80%

100%

America(2016)

America(2040)

Europe (2016) Europe (2040) Asia Oceania(2016)

Asia Oceania(2040)

China (2016) China (2040)

Composition of New Passenger Car Sales by Technology

Conventional NGV HEV Electric FCV

Source: World Oil Outlook (2017)Note: Mb/d is Million Barrels per Day

Source: World Oil Outlook (2017)Note: NGV is Natural Gas Vehicle, HEV is Hybrid Electric Vehicle, FCV is Fuel Cell Vehicle

Expected decline in demand along with the conscious effort by countries to shift to environmentally friendly alternatives to oil would force GCC countries to diversify revenue sources

12Sample Document I Not For Circulation

0

1

2

3

4

US Brazil Canada Russia Kazakhystan Norway

Contributors to Non-OPEC Incremental Supply Change, 2016-2022 (Mb/d)

Source: World Oil Outlook (2017)Note: Mb/d is Million Barrels per Day

150

200

250

300

2010 2011 2012 2013 2014 2015 2016 2017

Drilling Cost of Oil and Gas Wells in the US – 2004 Base of 100

Source: World Oil Outlook (2017)Note: Cost of drilling was adjusted to 100 in 2004 and then the cost for latter years was based on that

• Non-OPEC supply is expected to increase due to recovery and improved outlook for US oil production

• Growth is heavily concentrated geographically as more than 75% is from US on the back of a resurgence in tight oil production

• Due to advancement in technology, more wells can be drilled faster, more cheaply and with higher individual output levels

• Hence, rig counts in US have rebounded sharply, more than doubling from a low of 332 in 2016

13Sample Document I Not For Circulation

2021: ↓ 8% in elec consumption and ↓ 14% in peak demand

Renewable Energy Targets

Energy Efficiency Targets

2020: 3.45 GW2023: 9.5 GW 2030: 30% of generation from renewables and others (mainly nuclear)

Saudi Arabia

2020: ↑ 5% generation efficiency2030: ↑ 15% generation efficiency and ↓ 30% energy consumption

2030: 15% of electricity generation

Kuwait

2025: ↓ 6% electricity consumption

2025: 5% of electricity generation2035: 10% of electricity generation

Bahrain

2030: Dubai: ↓ 30% electricity consumption2050: ↓ 40% electricity consumption

2020: Abu Dhabi: 7% of capacity2020: Dubai: 7% of electricity generation2021: 27% clean energy2040: Ras Al Khaimah 25%-30% clean energy2050: 44% of capacity

UAE

Source: IRENA GCC (2019)

14Sample Document I Not For CirculationSource: Global Market Insights, Internal Analysis, IDC

1Strategic Vision 2030 Initiatives• Saudi Arabia has categorized its milestones for achieving its Vision 2030• Focus is to increase the penetration of ICT programs into the oil and non-oil sectors• Initiatives to focus on improving the ranking in ease of doing business, Healthcare & Tourism sector and plot itself as Global Hub attracting investments

2Strong ICT Ecosystem• Nationwide 90% 4G network, with plans to increase Internet speed by 300% and fiber-optic coverage by 7%• Saudi Arabia’s ICT sector plays an important role in its economy and accounts for 6% of its GDP and 10% of non-oil GDP and is focused on gaining more

through implementation of Vision 2030

3Highly Skilled Labour• Almost 75% of the Saudi population is under 29, which presents a huge opportunity to provide a young workforce with skills and capabilities • Around 94.4% of population is literate and the government has set aside $51 Bn for education sector to eradicate illiteracy by 2024 in view of Vision 2030• About 60% of population are well versed with Digital environment with a sharp increase in e-literacy Y-o-Y

4Liberal Business Environment• Extensive incentives for foreign investors like - No restriction on repatriation of capital, Tax incentives on registering the company in less developed

economic cities, lower minimum capital requirements• 100% foreign ownership of property and companies allowed in certain industries

15Sample Document I Not For Circulation

Even With Aggressive Fuel Switching By 2035, Oil And Gas Are Expected To Maintain Dominance in Energy Consumption

34%

23%

28%

4%7% 4%

FY17 FY35

29%

26%

21%

4%

7%

13%

Oil Gas Coal RenewablesNuclear Hydro

Oil & Gas (57%):~7,700 MTOE

Source: BP Energy Outlook, 2019

Primary Energy Consumption – Breakdown by Fuel Type

Oil & Gas (55%):~9,200 MTOE

Renewable energy is the fastest growing source of energy with its share in primary energy expected to increase from 4% to 13% by 2035

Oil consumption is expected to slow down and grow at low single digits by 2035 – Growth primarily led by developing economies

Gas consumption expected to grow faster than oil and expected to overtake coal as 2nd

largest source of global energy1 2 3

16Sample Document I Not For Circulation

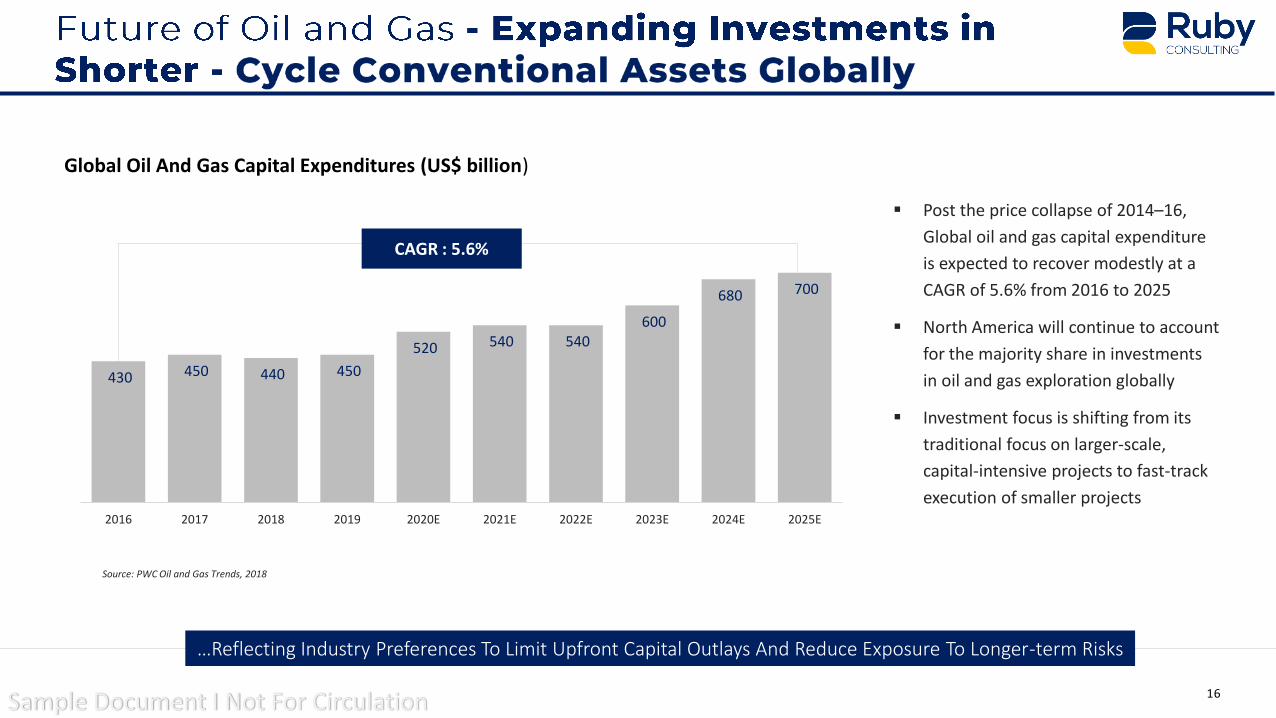

Global Oil And Gas Capital Expenditures (US$ billion)

430 450 440 450

520 540 540 600

680 700

2016 2017 2018 2019 2020E 2021E 2022E 2023E 2024E 2025E

▪ Post the price collapse of 2014–16,

Global oil and gas capital expenditure

is expected to recover modestly at a

CAGR of 5.6% from 2016 to 2025

▪ North America will continue to account

for the majority share in investments

in oil and gas exploration globally

▪ Investment focus is shifting from its

traditional focus on larger-scale,

capital-intensive projects to fast-track

execution of smaller projects

CAGR : 5.6%

Source: PWC Oil and Gas Trends, 2018

…Reflecting Industry Preferences To Limit Upfront Capital Outlays And Reduce Exposure To Longer-term Risks

17Sample Document I Not For Circulation

97.7 110

2.6

3.5

1.60.6 (1.6) 0.6

1.32.3

1.4

20

17

Ch

ina

India

Re

st

of A

sia

No

rth

Am

eri

ca

Euro

pe

Ru

ssia

an

dC

asp

ian

La

tin

Am

erica

Mid

dle

Ea

st

Afr

ica

20

35

Source: Wood Mackenzie

Growth in Oil Demand : 2017-2035Primary Energy Growth : 2017 – 2035

4.3%

3.5%

2.4%2.1%

1.3%

0.3%

Ind

ia

Afr

ica

Bra

zil

Mid

dle

East

Ch

ina

Ru

ssia

India Leads the Way

➢ India is expected to be the world’s largest oil demand growth centre in the next ~20 years

➢ Government of India is promoting aggressive domestic oil production for meeting excess demand and to reduce import imbalance

➢ Energy consumption growth in India during 2017-2035 is expected to be 3x of global average growth

➢ Rapid growth in India’s energy demand backed by robust economic growth

➢ India 2nd biggest driver of global energy consumption in 2019

(Million b/d)(Annualized %)

Source: BP Energy Outlook, 2019

18Sample Document I Not For Circulation

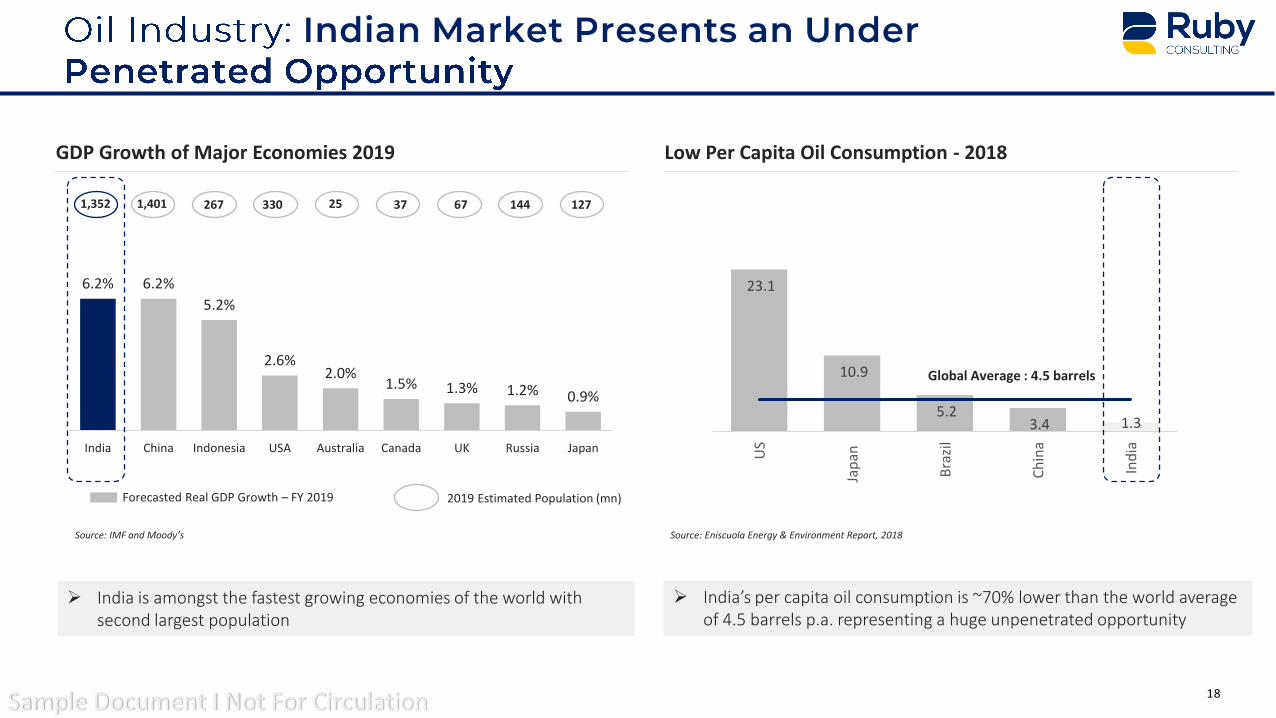

127

Low Per Capita Oil Consumption - 2018

23.1

10.9

5.2 3.4 1.3

US

Jap

an

Bra

zil

Ch

ina

Ind

ia

Source: Eniscuola Energy & Environment Report, 2018

GDP Growth of Major Economies 2019

6.2% 6.2%

5.2%

2.6%2.0%

1.5% 1.3% 1.2% 0.9%

India China Indonesia USA Australia Canada UK Russia Japan

Forecasted Real GDP Growth – FY 2019 2019 Estimated Population (mn)

1,352 1,401 267 330 3725 67 144

Source: IMF and Moody’s

Global Average : 4.5 barrels

➢ India’s per capita oil consumption is ~70% lower than the world average of 4.5 barrels p.a. representing a huge unpenetrated opportunity

➢ India is amongst the fastest growing economies of the world with second largest population

19Sample Document I Not For Circulation

Strategic Positioning of the Company

Small

E&P

CLIENT

Serv

ice

s

Medium Large

Revenue - $5 Bn+Revenue - $100-5,000 mnRevenue up to $100mn

Selan Exploration

Dolphin Offshore

(1)

(1)

• Very few companies offering E&P + Services +Retailing Play

• Client aims to create plays in opportunistic & low-risk smaller onshore oil blocks and specialized series, thereby creating a unique business model

Note 1: Only considered Oil & Gas related businesses of these companies

20Sample Document I Not For Circulation

Business momentum continues to be very strong

Large addressable market in China and overseas

• Addressable market in China expected to grow at 15 – 20% annually over the next few years from US$3.0BN in 2020E to US$5.7Bn in 2025E

– Chinese technology giant Huawei-3Com currently holds 31% market share in Global telecom equipment revenue

• Global router and LAN switch market is close to US$45Bn in size, growing at mid-single-digit growth rates

– Benefits from rapid growth in enterprise sector

Tremendous room for further growth

Strong growth track record enhanced by comprehensive product portfolio

• Revenues expected to grow from US$1.46 Bn in 2017, based on rapid increases in China sales and increasing traction in overseas markets

• Highest growth (19.2% CAGR) in the data networking industry, outperforming all major global competitors

• Expanding product portfolio which has grown from routers and LAN switches to voice/VoIP, data security and data storage

Enables Huawei-3Com to continue to out-compete its rivals

Long-term competitive cost advantage

• R&D cost per head is on average approximately 80% less than its U.S. competitors (US$47.3K vs. US$238.4K for Cisco)

– Still consistently spends around 14% of sales in R&D in line with peers

– R&D headcount has been grown to 2,500 from 700 in 2016, while R&D/Sales has been maintained in line with peers at 14% of sales

A highly regarded brand name in the industry

Strong brand recognition in China, and increasingly, globally

• Benefits from Huawei ownership, the leading network equipment player in China

• Provides strong reputational sponsorship to Huawei-3Com in the China and overseas markets and a captive market through OEM business

Strong earnings and cash flow outlook results in rapid delivering

Improving profit margins and strong cash flow generation capability

• Operating cash flow has significantly increased with scale from US$(20.5)MM in 2020 to US$141.0MM in 2026E

• Driven by low capex requirements and relatively short working capital cycle, cash flow generation capability continues to improve

• Rapid delevering from 6.5x Total Debt / EBITDA at launch to 3.8x by 2020E

Sustainable business modelUnique industry dynamics • Cisco, given dominant market position, sets a “pricing umbrella” to maintain its own gross margins

• Allows JV to set prices ~30% lower (which they are able to given low-cost structure)

– JV wins businesses on compelling price for quality products

– Cisco will not react and bring down all its prices globally

• The market is looking for a “Cisco alternative”

21Sample Document I Not For Circulation

PRODUCT VARIANT SELECTED VENDORS PRODUCT USE PRODUCT VARIANT SELECTED VENDORS PRODUCT USE

• Alcoholic• Non-Alcoholic

• Medline Inc.-USA• 3M Co- USA• Aqua Chem Industry Co.

Ltd- China

• Used for disinfecting surfaces and decontamination

• Alcoholic• Non-Alcoholic

• Medline Inc.-USA• P&G Co- USA• Hangzhou Special

Nonwovens-China

• Handheld• Backpack

• Medline Inc.-USA• Clorox Co- USA• Xiamen-China

• Alcoholic and Latex• Non-Alcoholic and Latex

Free

• Medline Inc.-USA• Kimberly Clark- USA• Oriental Enterprises.-

India

• McKesson.-USA• Surgo- Canada• ASP Medical-Malaysia

• Single Pouch• Multiple Pouch

• Cardinal Health.-USA• Medline Inc.- USA• Yantai Bagmart

Packaging Co-China

• Used for isolation of patient specimen documents

• Automatic• Manual

• Cardinal Health-USA• J&J Inc.- USA• Biobase Biotech Co Ltd-

China

• AAMI Level 3• AAMI Level 4

• Provides comfortable attire for executing medical operations

• Used for treating Wounds and highly infectious disease cases

• Reduce cross-contamination and smell, cleanup after patient Sickness

• Ideal for sanitizing, disinfecting, odor control and more

• Safe fluid system to transport infectious waste into sanitary sewer

• Used for disinfecting surfaces and decontamination

• Cardinal Health.-USA• Medline Inc- USA• Vi Pha Co-Vietnam

• High Density• Low Density

Disinfective Wipes

Emesis Bags

Specimen Bags

Electrostatic Sprayer

Fluid Management Devices

Surgical Drapes & Gowns

Bleach SolutionCritical Response Cleansing Cloth

22Sample Document I Not For Circulation

Global Market Size

Key Growth Drivers

• High incidence of hospital-acquired infections

• Increasing number of surgical procedures;

• Growing geriatric population and increasing incidence of chronic diseases;

• Growing focus on food sterilization and disinfection

• Technological advancements in sterilization equipment; and the increasing outsourcing of sterilization services among pharmaceutical companies, hospitals, and medical device manufacturers.

US$ 44.7 bn

US$ 52.7 bn

2021 2026

• Geographically, North America dominates the global infection control market, followed by Europe and Asia-Pacific

• However, Asia-Pacific is expected to grow at the fastest CAGR during the forecast period

• Based on product type, the cleaning & disinfection segment is estimated to account for the largest share of the overall infection control market

• On the other hand, the endoscope reprocessing products segment is expected to grow at the fastest growth rate due to the growing importance of diagnostic and therapeutic endoscopy procedures

• Based on end user, the hospitals & clinics segment is estimated to command the largest share of the overall infection control market

CAGR: 3.4%

Source: Markets & Markets

23Sample Document I Not For Circulation

Renewable Electricity

Fossil Fuels 73.8%Hydropower 45%

Geothermal power, Nuclear CSP & Ocean

13%

Solar PV

Global Energy Composition %

26.2%

31%

6%

Bio-Power 5% Wind

Source:– International Energy Agency

ESTIMATED RENEWABLE ENERGY SHARE OF GLOBAL ELECTRICITY PRODUCTION, 2018 RENEWABLE POWER CAPACITIES (GW) IN WORLD ,TOP TEN COUNTRIES, 2020

Source: International Energy Agency

925.2

311.3

150 138.9 137.1 123.3 101.462.4 59.2 57.1

Ch

ina

USA

Brazil

Ind

ia

Ge

rman

y

Japan

Can

ada

Spain

Italy

France

Inst

alle

d C

apac

ity

(GW

)

24Sample Document I Not For Circulation

Investment2013 2020($ bn p.a.)

CapacityAddition

2013 2020(GW p.a.)

15.67

25

9.1

18.7

GLOBAL OFFSHORE MARKET (CAPACITY IN MW)

0.411

1.6

13

0 0.5 0.012

Denmark 1,706.7(4.8%)

Sweden 201(0.57%)

N’lands 2441(6.9%)

UK 10,237 (29%)

Belgium 2300 (6.51%)

Germany 7766 (22%)

China 9884 (28%)

Existing Offshore

Plans for Offshore

No Activity

Europe Europe

Asia-Pac Asia-Pac

North-Am North-Am

Currently concentrated in NW Europe, China catching up

25Sample Document I Not For Circulation

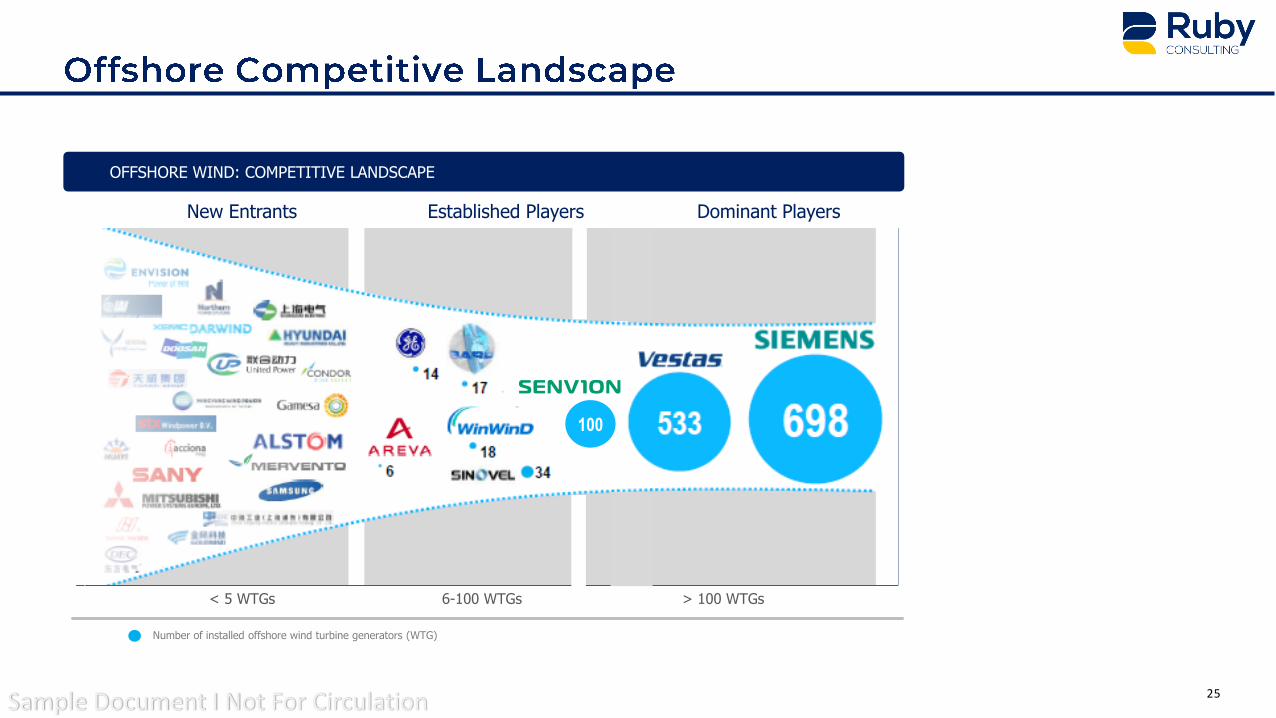

New Entrants Established Players Dominant Players

< 5 WTGs 6-100 WTGs > 100 WTGs

OFFSHORE WIND: COMPETITIVE LANDSCAPE

Number of installed offshore wind turbine generators (WTG)

100

26Sample Document I Not For Circulation

18%

20%

30%

40%

56%

80%85%

India China Indonesia Thailand Malaysia UK US

Source: IBEF, January 2021; Business Insider; Planet Retail and Technopack Advisors, 2019

ORGANISED RETAIL PENETRATION PROJECIONS 2021(%)

15 Mn

Mom & Pop shops in India

20-25%

Organised Retail CAGR

24%

Organised Retail share in Total Retail by 2020

Indian Retail is highly Unorganized and Lagging Behind Global Counterparts

Note: Organized retail includes modern grocery retailing, home shopping, Internet retailing and direct selling

INDIAN RETAIL STATS

Source: Delloite

27Sample Document I Not For Circulation

Rising Disposable Income and Discretionary Spending

Increasing Penetration of Mobile and Television

Growing Acceptance of Virtual Shopping by Indian Consumers

Improving Logistics and Payment Methods

Increasing Demand for Innovative Products and Brand Consciousness

50+ $1 bn+

C o re Divis ions Why Us

C o n t a c t Us

Corporate Finance Support

Investment Research

Business Analytics & Reporting

Consulting Support

Team Members

Global Clients

300+Assignments

Executed

1000+Transactions Supported

Deep Expertise

Global Delivery Capabilities

Flexible Engagement Models

Standardised Processes