security national insurance company · report on examination of security national insurance company...

TRANSCRIPT

REPORT ON EXAMINATION

OF

SECURITY NATIONAL INSURANCE

COMPANY

PLANTATION, FLORIDA

AS OF

DECEMBER 31, 2013

BY THE

FLORIDA OFFICE OF INSURANCE REGULATION

TABLE OF CONTENTS LETTER OF TRANSMITTAL ........................................................................................................... -

SCOPE OF EXAMINATION ....................................................................................................... 1

SUMMARY OF SIGNIFICANT FINDINGS ................................................................................. 2

CURRENT EXAM FINDINGS ........................................................................................................ 2 PRIOR EXAM FINDINGS ............................................................................................................. 2

HISTORY ................................................................................................................................... 3

GENERAL ................................................................................................................................ 3 DIVIDENDS TO STOCKHOLDERS................................................................................................. 3 CAPITAL STOCK AND CAPITAL CONTRIBUTIONS .......................................................................... 3 SURPLUS NOTES ..................................................................................................................... 4 ACQUISITIONS, MERGERS, DISPOSALS, DISSOLUTIONS AND PURCHASE OR SALES THROUGH

REINSURANCE ......................................................................................................................... 4

CORPORATE RECORDS ......................................................................................................... 4

CONFLICT OF INTEREST ............................................................................................................ 5

MANAGEMENT AND CONTROL .............................................................................................. 5

MANAGEMENT ......................................................................................................................... 5 AFFILIATED COMPANIES ........................................................................................................... 7 SIMPLIFIED ORGANIZATIONAL CHART ........................................................................................ 8 TAX ALLOCATION AGREEMENT .................................................................................................. 9 AGENCY AGREEMENT .............................................................................................................. 9 SERVICE AGREEMENT .............................................................................................................10 QUOTA SHARE REINSURANCE AGREEMENT ..............................................................................10

FIDELITY BOND AND OTHER INSURANCE ...........................................................................10

PENSION, STOCK OWNERSHIP AND INSURANCE PLANS .................................................11

TERRITORY AND PLAN OF OPERATIONS ............................................................................11

TREATMENT OF POLICYHOLDERS .............................................................................................11

COMPANY GROWTH ..............................................................................................................11

PROFITABILITY OF COMPANY ...................................................................................................12

LOSS EXPERIENCE ................................................................................................................12

REINSURANCE ........................................................................................................................12

ASSUMED ...............................................................................................................................12 CEDED ...................................................................................................................................13

ACCOUNTS AND RECORDS ..................................................................................................13

CUSTODIAL AGREEMENT .........................................................................................................14 INDEPENDENT AUDITOR AGREEMENT .......................................................................................14

INFORMATION TECHNOLOGY REPORT ...............................................................................14

STATUTORY DEPOSITS .........................................................................................................15

FINANCIAL STATEMENTS PER EXAMINATION ....................................................................16

ASSETS ..................................................................................................................................17 LIABILITIES, SURPLUS AND OTHER FUNDS ................................................................................18 STATEMENT OF INCOME ..........................................................................................................19 COMPARATIVE ANALYSIS OF CHANGES IN SURPLUS ..................................................................20

COMMENTS ON FINANCIAL STATEMENTS ..........................................................................21

LIABILITIES .............................................................................................................................21 CAPITAL AND SURPLUS ...........................................................................................................21

SUMMARY OF RECOMMENDATIONS ....................................................................................22

CONCLUSION ..........................................................................................................................23

May 22, 2015 Kevin M. McCarty Commissioner Office of Insurance Regulation State of Florida Tallahassee, Florida 32399-0326 Dear Sir: Pursuant to your instructions, in compliance with Section 624.316, Florida Statutes, Rule 69O-138.005, Florida Administrative Code, and in accordance with the practices and procedures promulgated by the National Association of Insurance Commissioners (NAIC), we have conducted an examination as of December 31, 2013, of the financial condition and corporate affairs of:

SECURITY NATIONAL INSURANCE COMPANY 900 S. PINE ISLAND ROAD, SUITE 600

PLANTATION, FLORIDA 33324 Hereinafter referred to as the “Company.” Such report of examination is herewith respectfully submitted.

1

SCOPE OF EXAMINATION

This examination covered the period of January 1, 2012 through December 31, 2013. The

Company was last examined by representatives of the Florida Office of Insurance Regulation

(Office) as of December 31, 2011. This examination commenced with planning at the Office on

November 17, 2014 to November 21, 2014. The fieldwork commenced on November 17, 2014

and concluded as of May 22, 2015.

This financial examination was an association examination conducted in accordance with the

Financial Condition Examiners Handbook, Accounting Practices and Procedures Manual and

Annual Statement Instructions promulgated by the NAIC as adopted by Rules 69O-137.001(4) and

69O-138.001, Florida Administrative Code, with due regard to the statutory requirements of the

insurance laws and rules of the State of Florida.

The Financial Condition Examiners Handbook requires that the examination be planned and

performed to evaluate the financial condition and identify prospective risks of the Company by

obtaining information about the Company including corporate governance, identifying and

assessing inherent risks within the Company, and evaluating system controls and procedures

used to mitigate those risks. An examination also includes assessing the principles used and

significant estimates made by management, as well as evaluating the overall financial statement

presentation and management's compliance with Statutory Accounting Principles and Annual

Statement Instructions when applicable to domestic state regulations.

All accounts and activities of the Company were considered in accordance with the risk-focused

examination process.

2

This report of examination is confined to significant adverse findings, a material change in the

financial statements or other information of regulatory significance or requiring regulatory action.

The report comments on matters that involved departures from laws, regulations or rules, or which

were deemed to require special explanation or description.

SUMMARY OF SIGNIFICANT FINDINGS

Current Exam Findings

The following is a summary of material adverse findings, significant non-compliance findings, or

material changes in the financial statements noted during this examination.

Accounts and Records

The Company did not disclose that a $25 per policy fee was being charged in its Agency

Agreement with its affiliate Bristol West Insurance Services, Inc. of Florida, which is not in

compliance with Section 626.7451 (11) Managing General Agents; required contract provisions,

Florida Statutes.

Prior Exam Findings

Accounts and Records

During the review of policyholder balances, it was noted that the Company did not age its

agents’ balances on a separate, policy by policy basis. The Company was in violation of Rule

69O-138.024 (2), Florida Administrative Code. Resolution: The Company implemented

procedures to age agents’ balances on a policy by policy basis; no issues were noted in the

current exam.

3

HISTORY

General

The Company was incorporated in Florida on March 1, 1989, and commenced business on April 6,

1989, as a stock property and casualty insurer. On June 29, 2007, the Company’s parent, Bristol

West Holdings, Inc. was acquired by Farmers Group, Inc. and re-sold to Farmers Insurance

Exchange (37.5%) Truck Insurance Exchange (8.75%) Fire Insurance Exchange (3.75%) and Mid-

Century Insurance Company (50%). In 2008, Farmer’s Insurance Exchange acquired an additional

(4.5%) ownership by purchasing 2.5% from Mid-Century Insurance Company and 2% from Truck

Insurance Exchange. The ultimate controlling persons of the holding company are Zurich Financial

Service Ltd. and Farmers Insurance Exchange.

The Company was authorized to transact the following insurance coverage in Florida on April 6,

1989 and continued to be authorized as of December 31, 2013:

Private Passenger Auto Physical Damage Private Passenger Auto Liability

The Articles of Incorporation and the bylaws were not amended during the period covered by this

examination.

Dividends to Stockholders

The Company did not declare or pay any dividends during the period of this examination.

Capital Stock and Capital Contributions

As of December 31, 2013, the Company’s capitalization was as follows:

Number of authorized common capital shares 1,000,000 Number of shares issued and outstanding 1,000,000 Total common capital stock $3,000,000 Par value per share $3.00

4

Control of the Company was maintained by its parent, Bristol West Holdings, Inc. (Bristol West),

who owned 100% of the stock issued by the Company. Bristol West is wholly owned by Farmers

Insurance Exchange, Fire Insurance Exchange and Truck Insurance Exchange (collectively the

Exchanges), and their subsidiary Mid-Century Insurance Company. On July 3, 2007, the

Exchanges and Mid-Century Insurance Company acquired all of the outstanding shares of

Bristol West, thus making Security National a part of the Farmers Holding Company System.

Farmers Insurance Exchange has a controlling interest in Security National because of its 80%

direct and indirect stock ownership interest in Bristol West.

Surplus Notes

The Company did not have any surplus notes during the period of this examination.

Acquisitions, Mergers, Disposals, Dissolutions and Purchase or Sales through Reinsurance

The Company had no acquisitions, mergers, disposals, dissolutions and purchase or sales

through reinsurance during the period of this examination.

CORPORATE RECORDS

The recorded minutes of the Shareholders, Board of Directors (Board) and certain internal

committees were reviewed for the period under examination. The recorded minutes of the Board

adequately documented its meetings and approval of Company transactions and events, in

compliance with the NAIC Financial Condition Examiners Handbook adopted by Rule 69O-

138.001, Florida Administrative Code including the authorization of investments as required by

Section 625.304, Florida Statutes.

5

Conflict of Interest

The Company adopted a policy statement requiring periodic disclosure of conflicts of interest in

accordance with the NAIC Financial Condition Examiners Handbook adopted by Rule 69O-

138.001, Florida Administrative Code.

MANAGEMENT AND CONTROL

Management

The annual shareholder meeting for the election of directors was held in accordance with Section

628.231, Florida Statutes. Directors serving as of December 31, 2013, were:

Name and Location Principal Occupation

Kenneth Wayne Bentley Vice President, Community Affairs, Los Angeles, California Nestlé USA, Inc. Peter David Kaplan (a) Retired Los Angeles, California David Wayne Louie (b) First Vice President, Los Angeles, California CB Richard Ellis, Inc. Timothy Martin Madden President, Bristol West Holdings, Inc. Tampa, Florida Dale Anne Marlin (b) Retired Naples, Florida Ronald Gregory Myhan Chief Financial Officer, Laguna Beach, California Farmers Insurance Exchange

Donald Eugene Rodriguez Executive Director, Boys and Girls Club of Long Beach, California Long Beach, CA John Tsu-Chao Wuo President, Arcadia, California Golden Apple Group International, Inc.

(a) Peter David Kaplan resigned as Director effective October 18, 2014. (b) David Wayne Louie and Dale Anne Marlin resigned as Directors, effective June 4, 2014,

with Ronald Lee Marrone joining as a Director.

6

In accordance with the Company’s bylaws, the Board appointed the following senior officers:

Name Title

Timothy Martin Madden President Maria Eugenia Aguilera Treasurer Martin Robert Brown Secretary Ronald Gregory Myhan Vice President Jeffrey Michael Sauls (c) Vice President Karyn Leigh Williams Vice President Todd Michael Williams Vice President

(c) Jeffery Michael Sauls was replaced by Victoria Louise McCarthy effective March 18, 2014.

Audit Committee Investment Committee

Guy M. Hanson 1 Peter Tuescher 1

Thomas Brown Jeffrey J. Dailey

Fredrick H. Kruse Scott R. Lindquist

Gary R. Martin Ronald G. Myhan

Gerald A. McElroy

Donnell Reid

Stanley R. Smith

O. Joel Wallace

1 Chairman

The Company delegates its Investment Committee and Audit Committee duties to the Farmer’s

Insurance Exchange Investment and Audit Committees.

7

Affiliated Companies

The most recent holding company registration statement was filed with the Office on February

28, 2014, as required by Section 628.801, Florida Statutes, and Rule 69O-143.046, Florida

Administrative Code.

A simplified organizational chart as of December 31, 2013, reflecting the holding company

system, is shown on the following page. Schedule Y of the Company’s 2013 annual statement

provided a list of all related companies of the holding company group.

8

SECURITY NATIONAL INSURANCE COMPANY

SIMPLIFIED ORGANIZATIONAL CHART

DECEMBER 31, 2013

FIRE INSURANCE EXCHANGE

4%

BRISTOL WEST HOLDINGS, INC.

SECURITY NATIONAL INSURANCE

COMPANY

INSURANCE DATA SYSTEMS G.P.

FARMERS INSURANCE EXCHANGE

42%

TRUCK INSURANCE EXCHANGE

7%

MID-CENTURY

INSURANCE COMPANY

47%

ZURICH FINANCIAL SERVICES, LTD.

BRISTOL WEST INSURANCE

SERVICES, INC. OF FLORIDA

75% 25%

9

The following agreements were in effect between the Company and its affiliates:

Tax Allocation Agreement

The Company, along with its parent, Bristol West, filed a consolidated federal income tax return.

The Company, with its parent and affiliates, participated in a tax-sharing agreement amended and

restated effective September 1, 2013, whereby any tax liability or benefit is computed on a

separate tax return basis, as if each member filed its return separately. Farmers Insurance

Exchange (FIE) is the party primarily responsible for filing and making all tax payments on behalf of

the Company and FIE’s other subsidiaries. Intercompany balances are settled monthly and the

final settlement is made within thirty days after the filing date of the consolidated return.

Agency Agreement

The Company entered into an Agency Agreement with Bristol West Insurance Services, Inc. of

Florida on July 10, 1998. Effective October 1, 2012, the agreement was terminated and

superseded with the current Agency Agreement. The Company appointed Bristol West Insurance

Services, Inc. of Florida to represent it for the production and servicing of all lines of insurance the

Company is authorized to write, for which rates, policies and forms have been filed with the Office.

The Company did not disclose that a $25 per policy fee was being charged in its Agency

Agreement with its affiliate Bristol West Insurance Services, Inc. of Florida, which is not in

compliance with Section 626.7451 (11) Managing General Agents; required contract provisions,

Florida Statutes. Fees incurred under this agreement during 2013 amounted to $19,254,945.

10

Service Agreement

Effective March 1, 2010, the Company entered into a service agreement with FIE, whereby FIE

provided various services to the Company as necessary for the Company to discharge its

obligations to its policyholders, shareholders, and regulators. This agreement broadly

encompasses, claims adjustment services, investment management services, preparation of

insurance policies, billing and collections, and other administrative services. The agreement

continues in force for a term of five years and will automatically renew, unless otherwise terminated

within the guidelines of the agreement. Fees incurred under this agreement during 2013 amounted

to $19,159,674.

Quota Share Reinsurance Agreement

Effective December 31, 2010, the Company entered into a new quota share reinsurance

agreement with FIE. Under this agreement, the Company agreed to cede 100% of its net business,

as well as 100% of its net unearned premium reserves.

FIDELITY BOND AND OTHER INSURANCE

The Company maintained fidelity bond coverage up to $10,000,000 with a deductible of

$1,000,000 which reached the suggested minimum as recommended by the NAIC.

The Company also maintained commercial general liability, commercial umbrella excess liability,

other liability policies, executive liability and indemnification insurance, excess directors' and

officers' coverage, auto coverage and fiduciary liability insurance.

11

PENSION, STOCK OWNERSHIP AND INSURANCE PLANS

The Company had no employees and therefore no pension, stock ownership or insurance plans.

TERRITORY AND PLAN OF OPERATIONS

The Company was authorized to transact insurance in Florida and Texas.

Treatment of Policyholders

The Company established procedures for handling written complaints in accordance with Section

626.9541(1) (j), Florida Statutes. The Company maintained a claims procedure manual that

included detailed procedures for handling each type of claim in accordance with Section

626.9541(1) (i) 3a, Florida Statutes.

COMPANY GROWTH

The Company has continued to utilize its affiliated insurance agency, Bristol West Insurance

Services, Inc. of Florida, which is a wholly owned subsidiary of Bristol West, a member of the

Zurich holding company. The Company's gross written premium decreased from 2011 through

2013, due largely to the decrease in writings in Texas, which continued in run-off, but also due

to decreases in writings in Florida. Net premium remained at zero, due to the 100% quota share

reinsurance agreement with FIE. Capital and surplus over the examination period was stable,

with decreases due to net losses that were offset in part by changes in non-admitted assets.

12

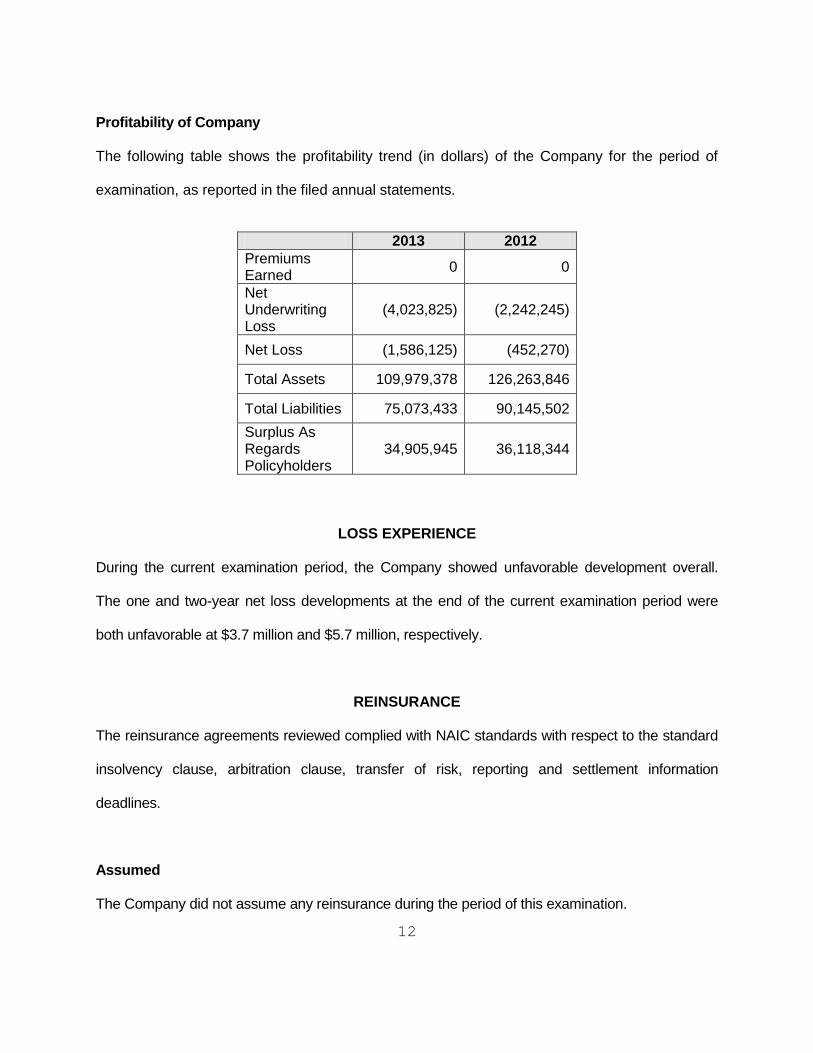

Profitability of Company

The following table shows the profitability trend (in dollars) of the Company for the period of

examination, as reported in the filed annual statements.

2013 2012

Premiums Earned

0 0

Net Underwriting Loss

(4,023,825) (2,242,245)

Net Loss (1,586,125) (452,270)

Total Assets 109,979,378 126,263,846

Total Liabilities 75,073,433 90,145,502

Surplus As Regards Policyholders

34,905,945 36,118,344

LOSS EXPERIENCE

During the current examination period, the Company showed unfavorable development overall.

The one and two-year net loss developments at the end of the current examination period were

both unfavorable at $3.7 million and $5.7 million, respectively.

REINSURANCE

The reinsurance agreements reviewed complied with NAIC standards with respect to the standard

insolvency clause, arbitration clause, transfer of risk, reporting and settlement information

deadlines.

Assumed

The Company did not assume any reinsurance during the period of this examination.

13

Ceded

Effective December 31, 2010, the Company entered into a new quota share reinsurance

agreement with FIE. Under this agreement, the Company ceded 100% of its net business, as

well as 100% of its net unearned premium reserves as of December 31, 2013. The Company

still carries net loss and loss adjustment expenses reserves and incurred losses as a result of

claims incurred prior to the effective date of this agreement.

The reinsurance contracts were reviewed by the Company’s appointed actuary and were utilized in

determining the ultimate loss opinion.

ACCOUNTS AND RECORDS

The Company maintained its principal operational offices in Plantation, Florida.

An independent CPA audited the Company’s statutory basis financial statements annually for the

years 2012 and 2013, in accordance with Section 624.424(8), Florida Statutes. Supporting work

papers were prepared by the CPA as required by Rule 69O-137.002, Florida Administrative Code.

The Company’s books and records were maintained by electronic processing equipment. The

accounting system, which is fully automated, produces a general ledger, subsidiary ledgers and

other reports as required for the preparation of financial statements and other management or

regulatory reporting.

14

The Company and non-affiliates had the following agreements:

Custodial Agreement

The Company maintained a custodial agreement with JP Morgan Chase Bank, N.A., which was

executed on October 15, 2007. The agreement was in compliance with Rule 69O-143.042, Florida

Administrative Code.

Independent Auditor Agreement

An independent CPA audited the Company’s statutory basis financial statements annually for the

years 2012 and 2013, in accordance with Section 624.424(8), Florida Statutes. Supporting work

papers were prepared by the CPA as required by Rule 69O-137.002, Florida Administrative Code.

INFORMATION TECHNOLOGY REPORT

Ernst & Young LLP performed an evaluation of the information technology and computer

systems of the Company. Results of the evaluation were noted in the Information Technology

Report provided to the Company.

15

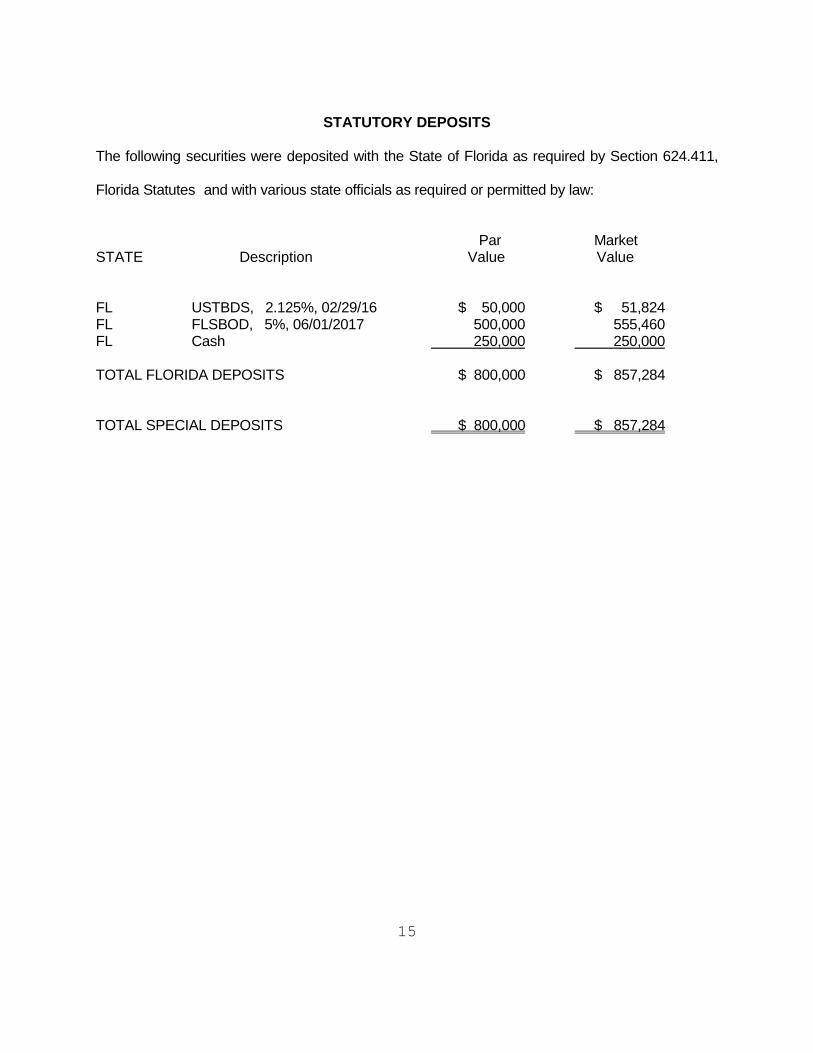

STATUTORY DEPOSITS

The following securities were deposited with the State of Florida as required by Section 624.411,

Florida Statutes and with various state officials as required or permitted by law:

Par Market STATE Description Value Value

FL USTBDS, 2.125%, 02/29/16 $ 50,000 $ 51,824 FL FLSBOD, 5%, 06/01/2017 500,000 555,460 FL Cash 250,000 250,000 TOTAL FLORIDA DEPOSITS $ 800,000 $ 857,284 TOTAL SPECIAL DEPOSITS $ 800,000 $ 857,284

16

FINANCIAL STATEMENTS PER EXAMINATION

The following pages contain financial statements showing the Company’s financial position as of

December 31, 2013, and the results of its operations for the year then ended as determined by this

examination. Adjustments made as a result of the examination are noted in the section of this

report captioned, “Comparative Analysis of Changes in Surplus.”

17

SECURITY NATIONAL INSURANCE COMPANY

Assets

DECEMBER 31, 2013

Per Company Examination Per Examination

Adjustments

Bonds $53,628,757 $0 $53,628,757

Cash and Short-Term Investments 1,824,346 1,824,346

Investment income due and accrued 311,915 311,915

Agents' Balances:

Uncollected premium 1,429,864 1,429,864

Deferred premium 38,399,763 38,399,763

Reinsurance recoverable 11,242,687 11,242,687

Net deferred tax asset 762,010 762,010

Receivable from parents, subsidiaries

and affiliates 2,380,036 2,380,036

Totals $109,979,378 $0 $109,979,378

18

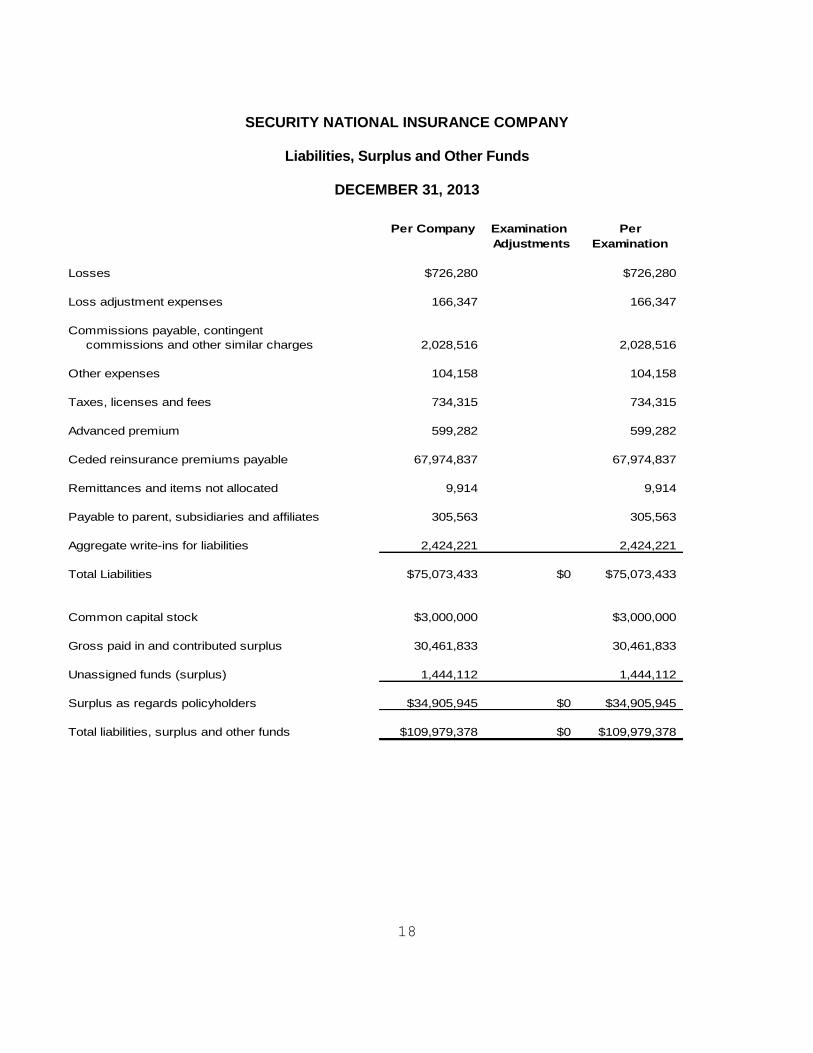

SECURITY NATIONAL INSURANCE COMPANY

Liabilities, Surplus and Other Funds

DECEMBER 31, 2013

Per Company Examination Per

Adjustments Examination

Losses $726,280 $726,280

Loss adjustment expenses 166,347 166,347

Commissions payable, contingent

commissions and other similar charges 2,028,516 2,028,516

Other expenses 104,158 104,158

Taxes, licenses and fees 734,315 734,315

Advanced premium 599,282 599,282

Ceded reinsurance premiums payable 67,974,837 67,974,837

Remittances and items not allocated 9,914 9,914

Payable to parent, subsidiaries and affiliates 305,563 305,563

Aggregate write-ins for liabilities 2,424,221 2,424,221

Total Liabilities $75,073,433 $0 $75,073,433

Common capital stock $3,000,000 $3,000,000

Gross paid in and contributed surplus 30,461,833 30,461,833

Unassigned funds (surplus) 1,444,112 1,444,112

Surplus as regards policyholders $34,905,945 $0 $34,905,945

Total liabilities, surplus and other funds $109,979,378 $0 $109,979,378

19

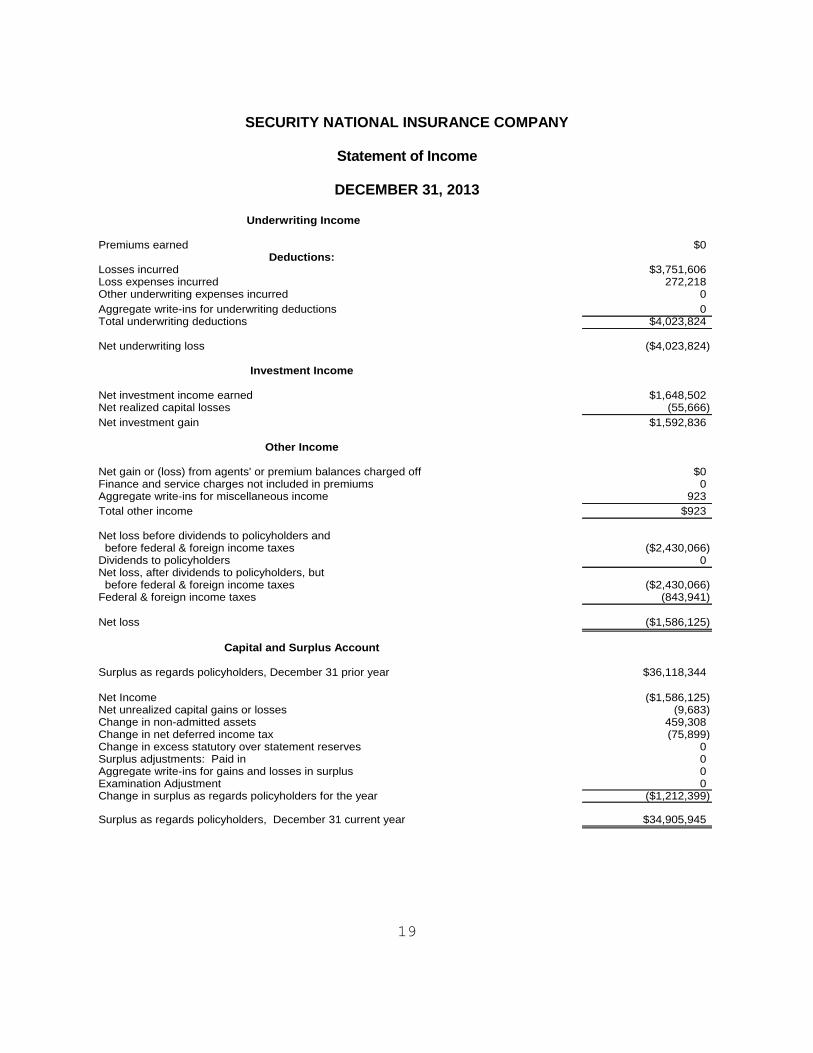

SECURITY NATIONAL INSURANCE COMPANY

Statement of Income

DECEMBER 31, 2013

Underwriting Income

Premiums earned $0Deductions:

Losses incurred $3,751,606Loss expenses incurred 272,218Other underwriting expenses incurred 0

Aggregate write-ins for underwriting deductions 0Total underwriting deductions $4,023,824

Net underwriting loss ($4,023,824)

Investment Income

Net investment income earned $1,648,502Net realized capital losses (55,666)

Net investment gain $1,592,836

Other Income

Net gain or (loss) from agents' or premium balances charged off $0Finance and service charges not included in premiums 0Aggregate write-ins for miscellaneous income 923

Total other income $923

Net loss before dividends to policyholders and before federal & foreign income taxes ($2,430,066)Dividends to policyholders 0Net loss, after dividends to policyholders, but before federal & foreign income taxes ($2,430,066)Federal & foreign income taxes (843,941)

Net loss ($1,586,125)

Capital and Surplus Account

Surplus as regards policyholders, December 31 prior year $36,118,344

Net Income ($1,586,125)Net unrealized capital gains or losses (9,683)Change in non-admitted assets 459,308Change in net deferred income tax (75,899)Change in excess statutory over statement reserves 0Surplus adjustments: Paid in 0Aggregate write-ins for gains and losses in surplus 0Examination Adjustment 0Change in surplus as regards policyholders for the year ($1,212,399)

Surplus as regards policyholders, December 31 current year $34,905,945

20

SECURITY NATIONAL INSURANCE COMPANY

Comparative Analysis of Changes in Surplus

DECEMBER 31, 2013

Surplus as Regards PolicyholdersDecember 31, 2013, per Annual Statement $34,905,945

INCREASEPER PER (DECREASE)

COMPANY EXAM IN SURPLUS

ASSETS:No Adjustment

LIABILITIES:No Adjustment

Net Change in Surplus: 0

Surplus as Regards PolicyholdersDecember 31, 2013, Per Examination $34,905,945

The following is a reconciliation of surplus as regards policyholders between that reported by the Company and as determined by the examination.

21

COMMENTS ON FINANCIAL STATEMENTS

Liabilities

Losses and Loss Adjustment Expenses $ 892,627 An outside actuarial firm appointed by the Board of Directors, rendered an opinion that the

amounts carried in the balance sheet as of December 31, 2013, made a reasonable provision for

all unpaid loss and loss expense obligations of the Company under the terms of its policies and

agreements.

The Office consulting actuary, as contracted by the California Department of Insurance, Charles

Letourneau, FCAS, MAAA, ARM, AIS, consulting actuary of American Actuarial Consulting

Group LLC, reviewed the loss and loss adjustment expense workpapers provided by the Company

and he was in concurrence with this opinion.

Capital and Surplus

The amount of capital and surplus reported by the Company of $34,905,945, exceeded the

minimum of $7,189,097 required by Section 624.408, Florida Statutes.

22

SUMMARY OF RECOMMENDATIONS

Accounts and Records

We recommend that the Company disclose in the Agency Agreement with affiliate, Bristol West

Insurance Services, Inc of Florida, its $25 per policy fee included in premium, under Section

627.403, Florida Statutes.

23

CONCLUSION

The insurance examination practices and procedures as promulgated by the NAIC have been

followed in ascertaining the financial condition of Security National Insurance Company as of

December 31, 2013, consistent with the insurance laws of the State of Florida.

Per examination findings, the Company’s surplus as regards policyholders was $34,905,945,

which exceeded the minimum of $7,189,097 required by Section 624.408, Florida Statutes.

In addition to the undersigned, Patricia Casey Davis, CFE, CPA, INSRIS, Examination Manager,

participated in the examination. Additionally, Sarah Lucibello, CPA, CFE, Examiner-In-Charge,

and Ryne Davison, CFE, Participating Examiner, both with Lewis and Ellis, Inc., participated in

the examination. Additionally, as contracted by the California Department of Insurance Charles

Letourneau, FCAS, MAAA, ARM, AIS, consulting actuary of American Actuarial Consulting

Group LLC and the IT staff of Ernst & Young LLP participated in the examination. Marie

Stuhlmuller, Financial Specialist, of the Office also participated in the examination.

Respectfully submitted,

___________________________

Robin Brown, CFE Chief Examiner

Florida Office of Insurance Regulation