semiconductor industry: how value chain is about...

TRANSCRIPT

© 2010

Copyrights © Yole Développement SARL. All rights reserved.

Semiconductor Industry: How

Value Chain is about to

Change… JC Eloy

CEO, YOLE Développement.

Infineon

Nokia FCI

NXPSTATs ChipPAC

AT&S

© 2010 • 2Copyrights © Yole Développement SARL. All rights reserved.

Yole DeveloppementCompany Presentation

© 2010 • 3Copyrights © Yole Développement SARL. All rights reserved.

Yole Développement

• Yole Développement is a market research and strategy consulting company, founded in 1998 and involved in the following fields:

• MEMS, including microfluidics

• Advanced packaging (3D IC, TSV, SoC, WLP…)

• Power electronics

• LED & HB LED

• Compound semiconductor business (SiC, GaN, AlN, ZnO, Thick SOI…) at substrate and device level

• Photovoltaic, from equipment and materials to cell business

• Our research is performed by in-house personnel conducting open-endeddiscussion based interviews.

• 20 full time analysts with technical and marketing degrees

• Primary research includes over 2,500 interviews annually

• Our customers‟ base and perspectives are global.

© 2010 • 4Copyrights © Yole Développement SARL. All rights reserved.

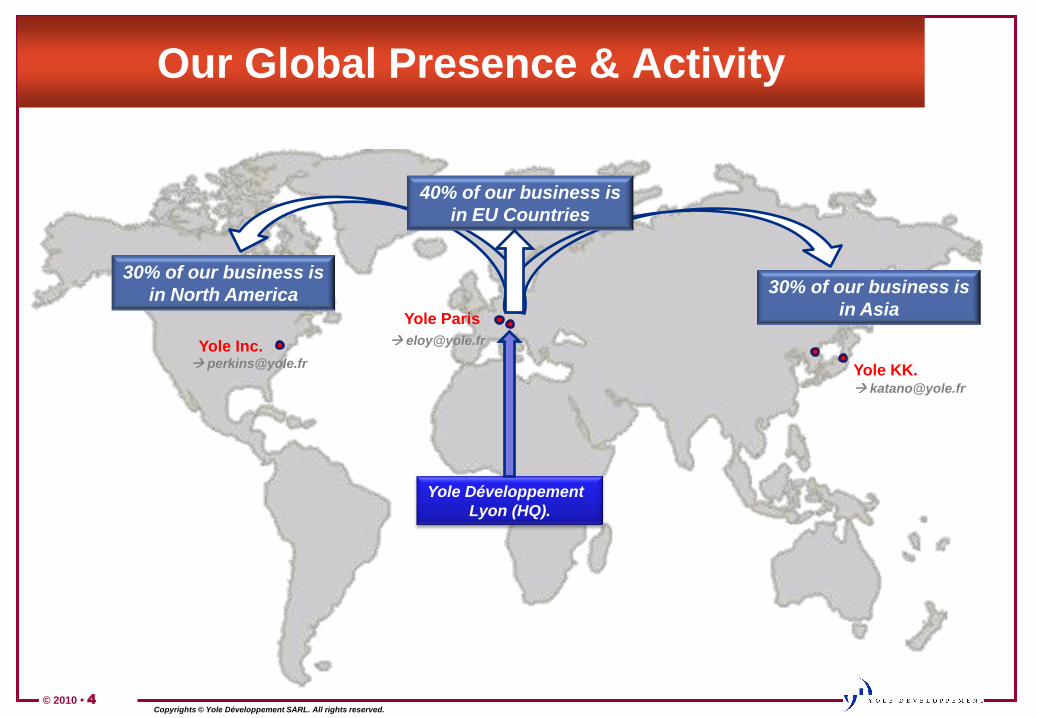

Our Global Presence & Activity

Yole Inc.

Yole Développement

Lyon (HQ).

Yole Paris

Yole KK.

30% of our business is

in North America 30% of our business is

in Asia

40% of our business is

in EU Countries

© 2010 • 5Copyrights © Yole Développement SARL. All rights reserved.

Some of Our Customers

Financial investors

& industry advocates

R&D Organizations

Suppliers (equipment, wafers, materials)

Component manufacturers

Integrators, system manufacturers and end users

© 2010 • 6Copyrights © Yole Développement SARL. All rights reserved.

Custom Analysis Services

• Market research and marketing analysis• Identification of new applications and markets

• Set-up of market segmentation

• Proposal of marketing and action plans

• Strategic analysis• Analysis of positioning to create value

• Development of action plans to improve company performance

• Support in implementation and fund raising

• Technology evaluation• Analysis of technical areas and definition of technology strategy

• Process cost analysis and cost comparison

• Development of product and technology roadmap

• Specific services for investors by Yole Finance• Evaluation and analysis of business plans

• Evaluation of production infrastructure

• Expertise and due diligence before M&A– Company, market and technology expertise

– Strategy, marketing and technical due diligence

© 2010 • 7Copyrights © Yole Développement SARL. All rights reserved.

About Yole‟s Advanced Packaging Analysts

Jean-Marc Yannou– Jean-Marc joined Yole

Développement as technology and

market expert in the fields of

advanced packaging and Integrated

Passive Devices. He has 15-years of

experience in the semiconductor

industry. He worked for Texas

Instruments and Philips (then NXP

semiconductors) where he served

as “Innovation Manager” for

System-in-Package technologies

Contact: [email protected]

Jerome Baron– Jerome is leading the MEMS &

Advanced Packaging market

research at Yole Developpement.

He has been following the 3D

packaging market evolution since

its early beginnings at device,

equipment and material levels. He

was granted a Master of Science

degree in Nanotechnologies from

the National Institute of Applied

Sciences in Lyon, France

Contact: [email protected]

Phil Garrou– Phil recently joined Yole

Développement forces as

senior technical advisor in the

fields of advanced packaging.

Phil as more than 20 years

extensive experiences in the

semiconductor industry where

he mainly served as global

marketing manager for DOW

Chemical‟s BCB polymer

business

Contact: [email protected]

Christophe Zinck– Christophe joined Yole

Developpement after several

positions in the wafer fab and

packaging environments of

CEA-Leti, STMicroelectronics

and then Triquint

Semiconductor, where he was

lead manager for flip-chip and

wafer-level-packaging

technologies implementation

Contact: [email protected]

© 2010 • 8Copyrights © Yole Développement SARL. All rights reserved.

Some of Our Customers

Financial investors

& industry advocates

R&D Organizations

Suppliers (equipment, wafers, materials)

Component manufacturers

Integrators, system manufacturers and end users

© 2010 • 9Copyrights © Yole Développement SARL. All rights reserved.

Via First vs. Via Last?3D integration Scenarios

I

M

E

C

S

i

l

e

x

F

r

e

e

s

c

a

l

e

N

o

k

i

a

D

u

P

o

n

t

TSV +Cost Analysis Tool for

your 3D IC manufacturing

3D IC & TSV 2010 Market Analysis

I

M

E

C

S

i

l

e

x

F

r

e

e

s

c

a

l

e

N

o

k

i

a

D

u

P

o

n

t

$27

7% $23

6%

$109

26%

$82%$37

9%$92%

$317%

$168

41%

TSV Scenario Cost structure breakdown

Via / Etching Drilling

Via Isolation

Via filling

Temporary bonding

Thinning

Stress release

BEOL (Pads)

Bonding

IPD – 2009 ReportIntegrated Passive Devices

Wafer Level Packaging2009 Report

N

o

k

i

a

3D Glass & Silicon

interposers - 2010 Report

© 2010

Copyrights © Yole Développement SARL. All rights reserved.

Advanced PackagingEquipment & Materials

NEC-Schott

SUSS Brewer ScienceSTSEVG

DuPont

© 2009

Copyrights © Yole Développement SARL. All rights reserved.

HB-LED Packaging Technology & Market Trends

IR

Osram

© 2010

CMOS Image Sensors Technologies & Markets Trends

BC TechTessera

Chipworks

More to

come…

Advanced packaging reports from YOLE

© 2010 • 10Copyrights © Yole Développement SARL. All rights reserved.

Advanced Packaging

evolutions…

© 2010 • 11Copyrights © Yole Développement SARL. All rights reserved.

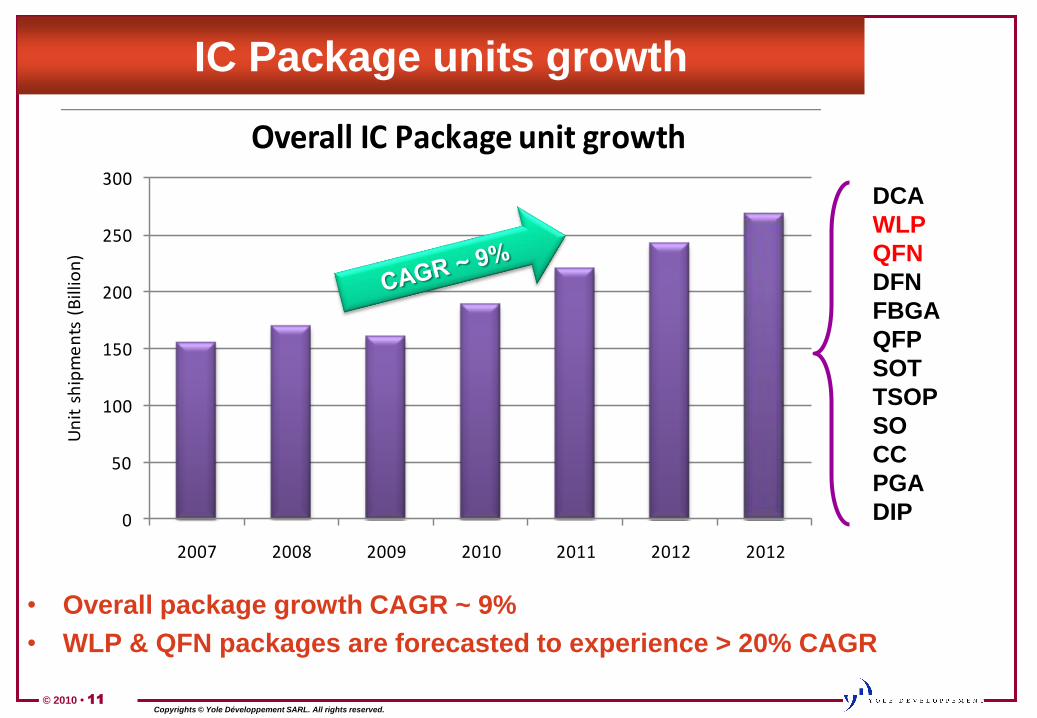

IC Package units growth

• Overall package growth CAGR ~ 9%

• WLP & QFN packages are forecasted to experience > 20% CAGR

0

50

100

150

200

250

300

2007 2008 2009 2010 2011 2012 2012

Un

it s

hip

me

nts

(B

illio

n)

Overall IC Package unit growth

DCA

WLP

QFN

DFN

FBGA

QFP

SOT

TSOP

SO

CC

PGA

DIP

© 2010 • 12Copyrights © Yole Développement SARL. All rights reserved.

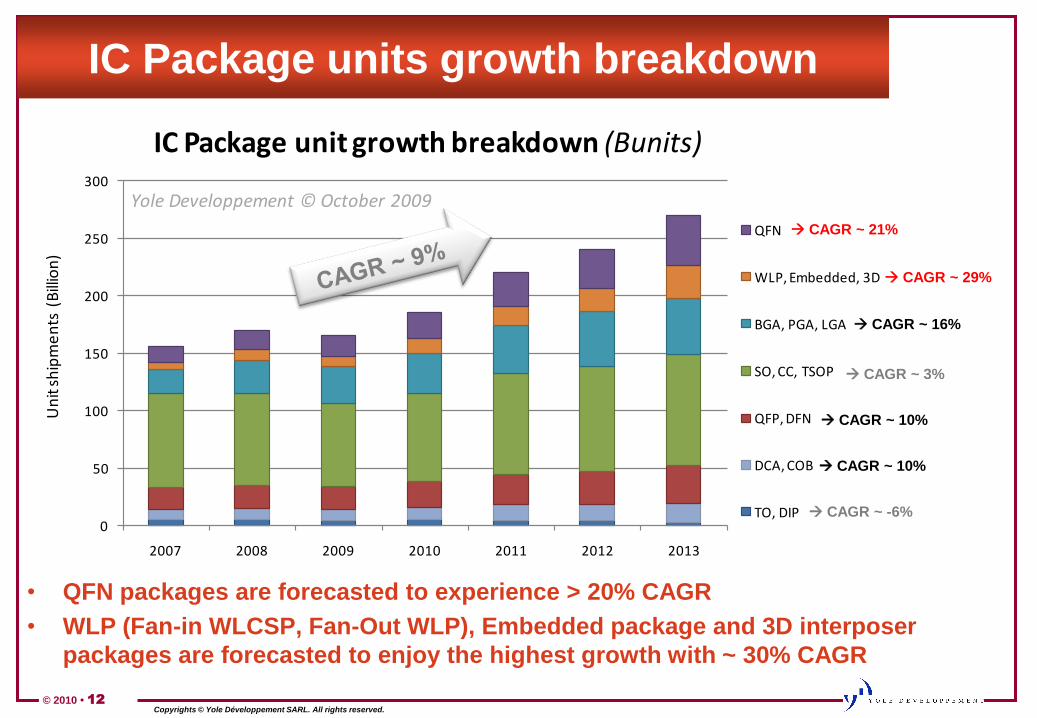

IC Package units growth breakdown

0

50

100

150

200

250

300

2007 2008 2009 2010 2011 2012 2013

Un

it s

hip

me

nts

(B

illio

n)

IC Package unit growth breakdown (Bunits)

QFN

WLP, Embedded, 3D

BGA, PGA, LGA

SO, CC, TSOP

QFP, DFN

DCA, COB

TO, DIP

Yole Developpement © October 2009

CAGR ~ 21%

CAGR ~ 29%

CAGR ~ 16%

CAGR ~ 10%

CAGR ~ 3%

CAGR ~ 10%

CAGR ~ -6%

• QFN packages are forecasted to experience > 20% CAGR

• WLP (Fan-in WLCSP, Fan-Out WLP), Embedded package and 3D interposer

packages are forecasted to enjoy the highest growth with ~ 30% CAGR

© 2010 • 13Copyrights © Yole Développement SARL. All rights reserved.

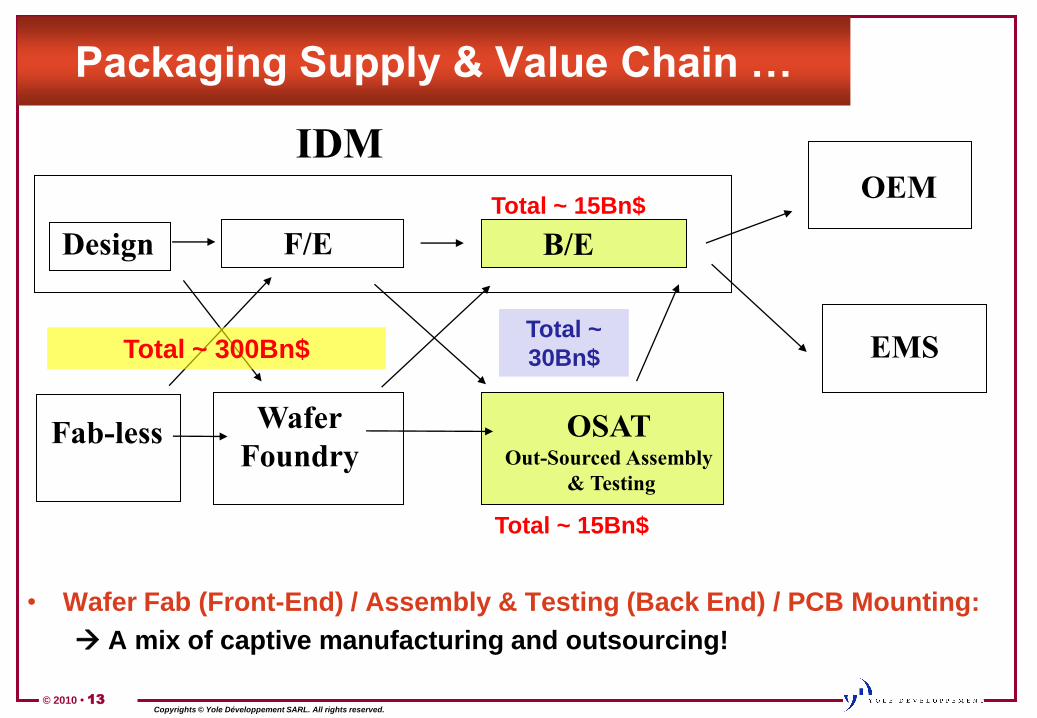

Packaging Supply & Value Chain …

• Wafer Fab (Front-End) / Assembly & Testing (Back End) / PCB Mounting:

A mix of captive manufacturing and outsourcing!

EMS

Wafer

FoundryOSAT

Out-Sourced Assembly

& Testing

IDMOEM

F/E B/E

Fab-less

Total ~ 15Bn$

Total ~ 15Bn$

Design

Total ~ 300Bn$Total ~

30Bn$

© 2010 • 14Copyrights © Yole Développement SARL. All rights reserved.

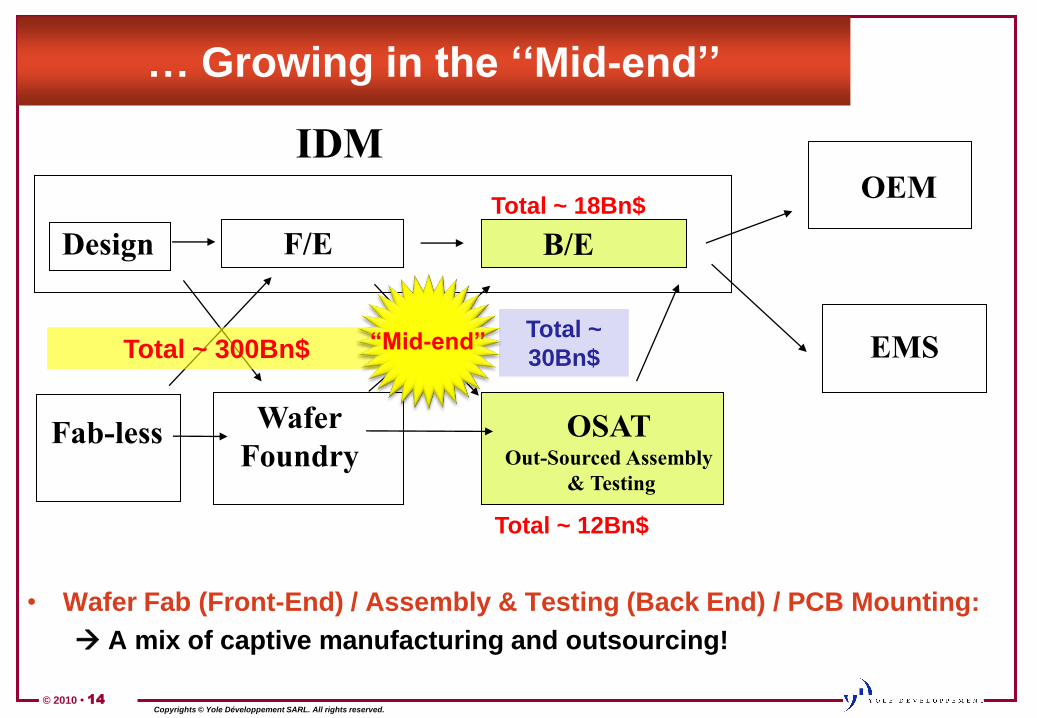

… Growing in the „„Mid-end‟‟

• Wafer Fab (Front-End) / Assembly & Testing (Back End) / PCB Mounting:

A mix of captive manufacturing and outsourcing!

EMS

Wafer

FoundryOSAT

Out-Sourced Assembly

& Testing

IDMOEM

F/E B/E

Fab-less

Total ~ 18Bn$

Total ~ 12Bn$

Design

Total ~ 300Bn$Total ~

30Bn$“Mid-end”

© 2010 • 15Copyrights © Yole Développement SARL. All rights reserved.

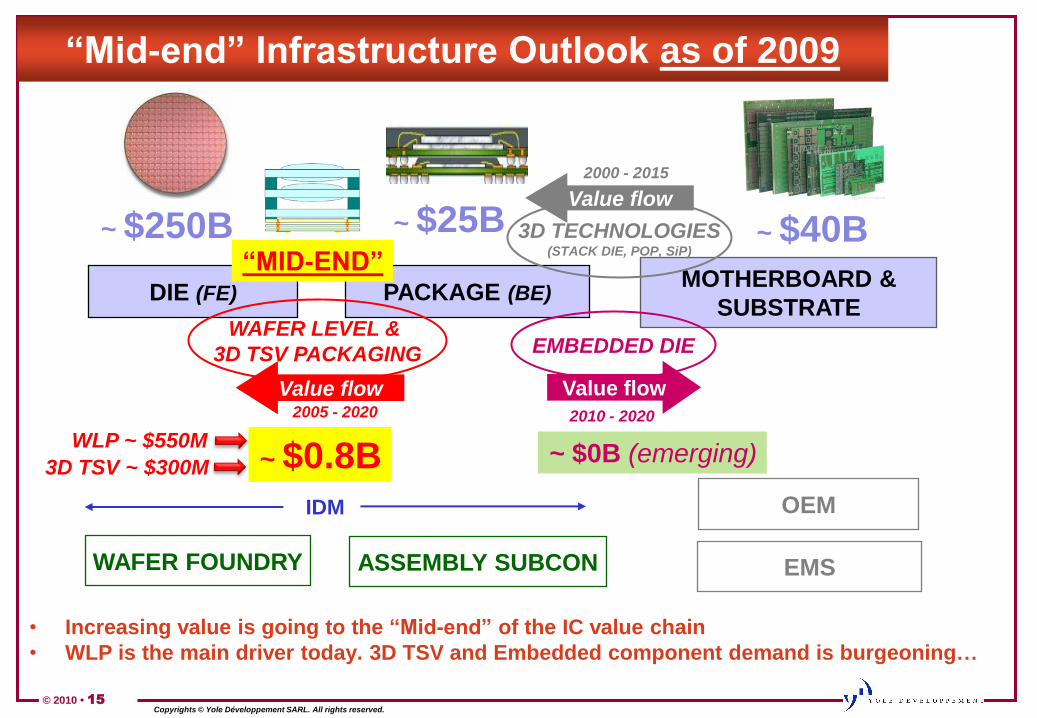

MOTHERBOARD &

SUBSTRATE

“Mid-end” Infrastructure Outlook as of 2009

DIE (FE) PACKAGE (BE)

WAFER FOUNDRY ASSEMBLY SUBCON

IDM

“MID-END”

EMBEDDED DIE

EMS

OEM

WAFER LEVEL &

3D TSV PACKAGING

Value flow Value flow

3D TECHNOLOGIES(STACK DIE, POP, SiP)

Value flow

2000 - 2015

2010 - 20202005 - 2020

~ $250B ~ $25B

~ $0.8B

~ $40B

~ $0B (emerging)

• Increasing value is going to the “Mid-end” of the IC value chain

• WLP is the main driver today. 3D TSV and Embedded component demand is burgeoning…

WLP ~ $550M

3D TSV ~ $300M

© 2010 • 16Copyrights © Yole Développement SARL. All rights reserved.

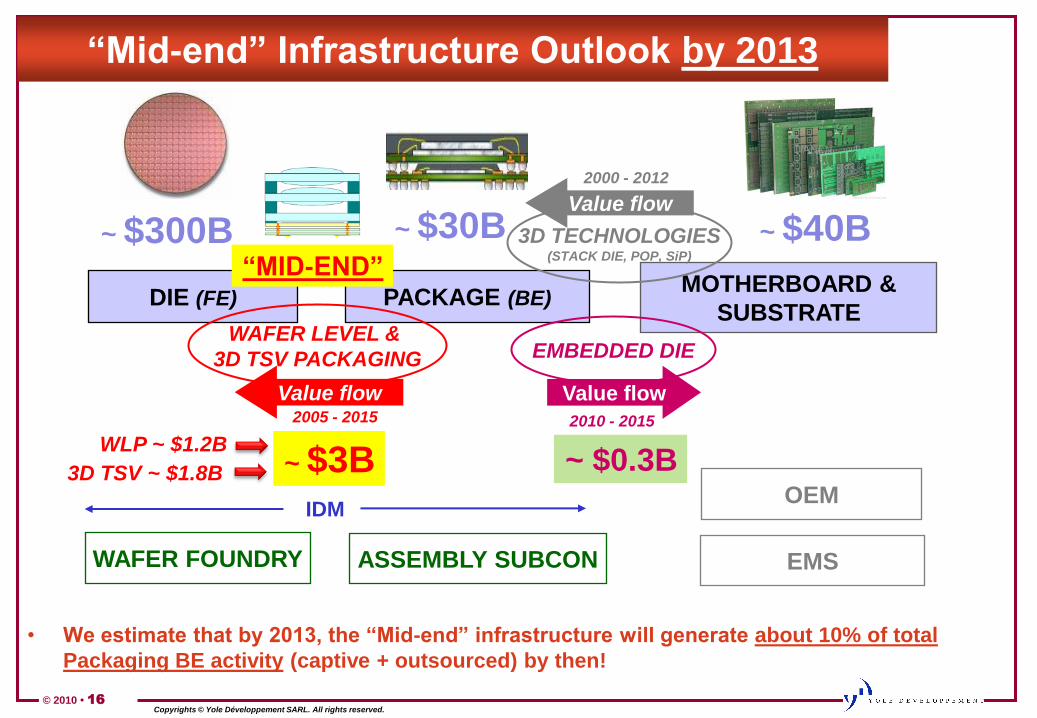

MOTHERBOARD &

SUBSTRATE

“Mid-end” Infrastructure Outlook by 2013

DIE (FE) PACKAGE (BE)

WAFER FOUNDRY ASSEMBLY SUBCON

IDM

“MID-END”

EMBEDDED DIE

EMS

OEM

WAFER LEVEL &

3D TSV PACKAGING

Value flow Value flow

3D TECHNOLOGIES(STACK DIE, POP, SiP)

Value flow

2000 - 2012

2010 - 20152005 - 2015

~ $300B ~ $30B

~ $3B

~ $40B

~ $0.3B

• We estimate that by 2013, the “Mid-end” infrastructure will generate about 10% of total

Packaging BE activity (captive + outsourced) by then!

WLP ~ $1.2B

3D TSV ~ $1.8B

© 2010 • 17Copyrights © Yole Développement SARL. All rights reserved.

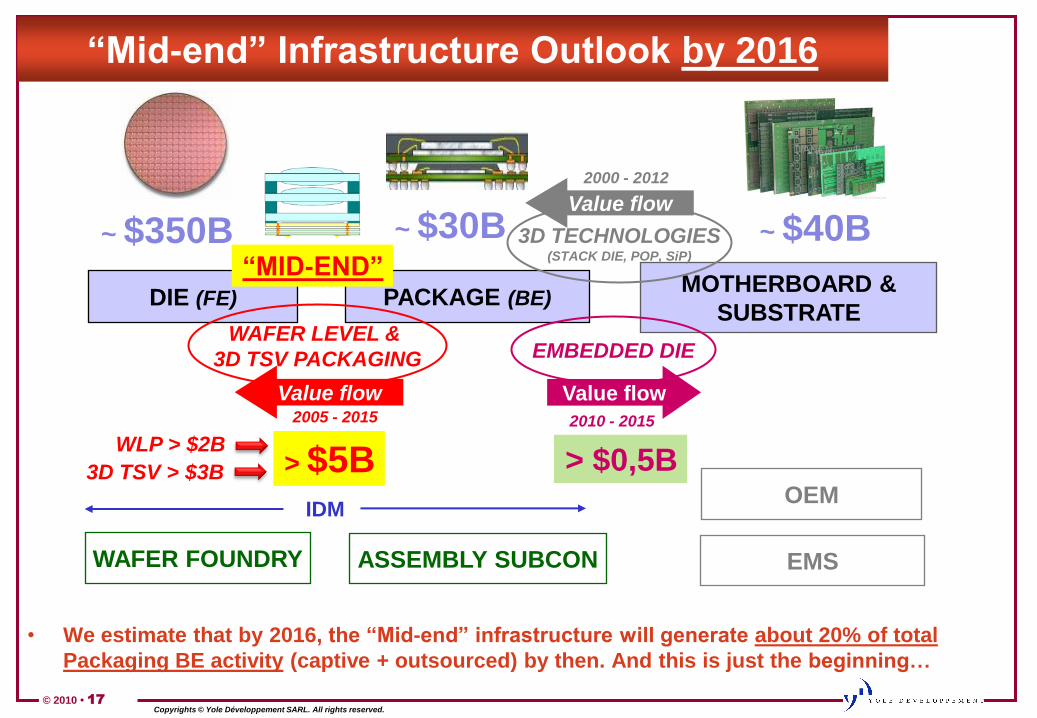

MOTHERBOARD &

SUBSTRATE

“Mid-end” Infrastructure Outlook by 2016

DIE (FE) PACKAGE (BE)

WAFER FOUNDRY ASSEMBLY SUBCON

IDM

“MID-END”

EMBEDDED DIE

EMS

OEM

WAFER LEVEL &

3D TSV PACKAGING

Value flow Value flow

3D TECHNOLOGIES(STACK DIE, POP, SiP)

Value flow

2000 - 2012

2010 - 20152005 - 2015

~ $350B ~ $30B

> $5B

~ $40B

> $0,5B

• We estimate that by 2016, the “Mid-end” infrastructure will generate about 20% of total

Packaging BE activity (captive + outsourced) by then. And this is just the beginning…

WLP > $2B

3D TSV > $3B

© 2010 • 18Copyrights © Yole Développement SARL. All rights reserved.

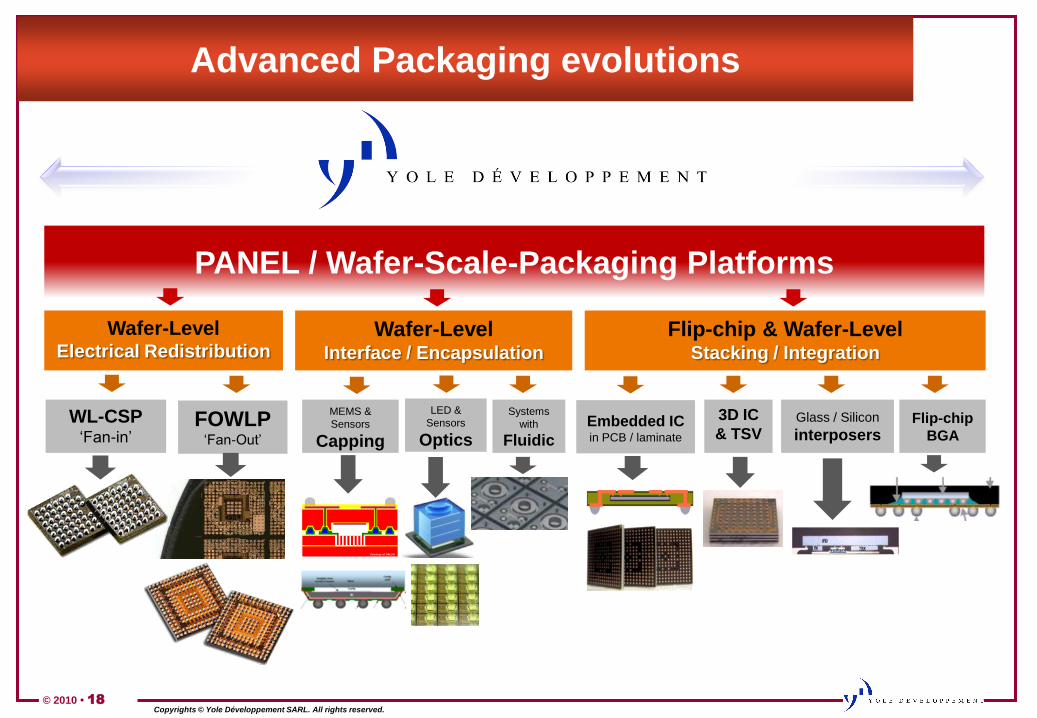

Advanced Packaging evolutions

PANEL / Wafer-Scale-Packaging Platforms

Wafer-Level Electrical Redistribution

Wafer-Level Interface / Encapsulation

Flip-chip & Wafer-LevelStacking / Integration

WL-CSP„Fan-in‟

FOWLP„Fan-Out‟

MEMS &

Sensors

Capping

Systems

with

Fluidic

Glass / Silicon

interposersFlip-chip

BGA

3D IC

& TSVEmbedded IC in PCB / laminate

Courtesy of DALSA

LED &

Sensors

Optics

© 2010 • 19Copyrights © Yole Développement SARL. All rights reserved.

FOCUS ON FAN OUT WLP AND

EMBEDDED DIE.

© 2010 • 20Copyrights © Yole Développement SARL. All rights reserved.

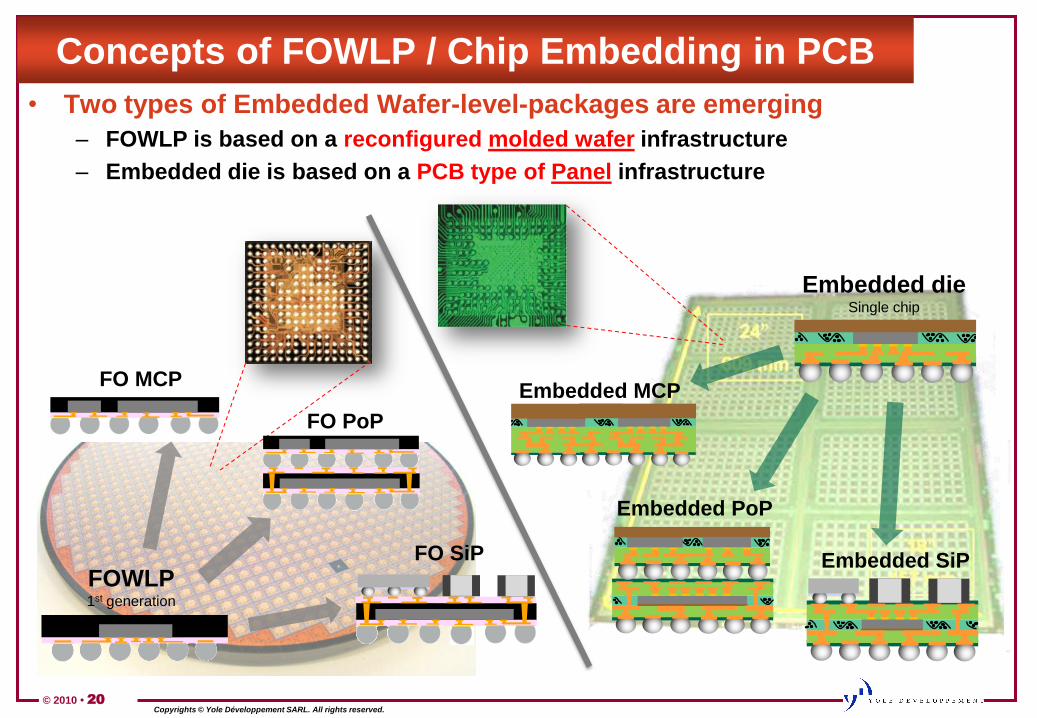

Concepts of FOWLP / Chip Embedding in PCB

• Two types of Embedded Wafer-level-packages are emerging

– FOWLP is based on a reconfigured molded wafer infrastructure

– Embedded die is based on a PCB type of Panel infrastructure

FOWLP1st generation

Embedded dieSingle chip

Embedded SiP

Embedded PoP

FO MCP

FO SiP

FO PoP

Embedded MCP

© 2010 • 21Copyrights © Yole Développement SARL. All rights reserved.

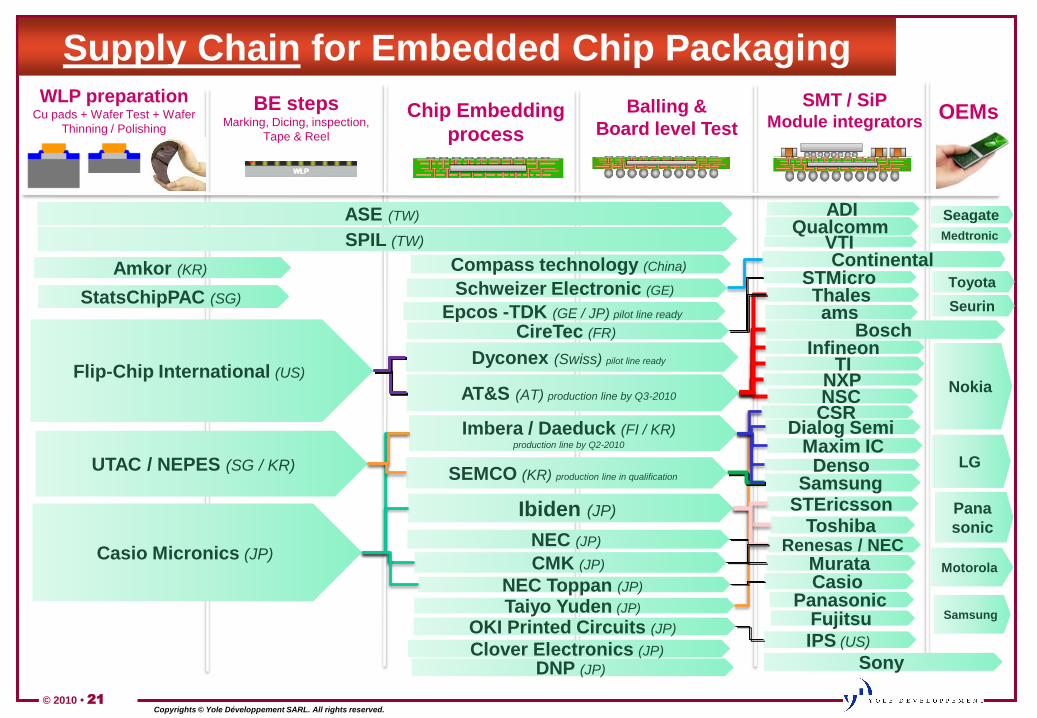

CSR

WLP preparationCu pads + Wafer Test + Wafer

Thinning / Polishing

Supply Chain for Embedded Chip Packaging

OEMsBalling &

Board level Test

AT&S (AT) production line by Q3-2010

Casio Micronics (JP)

Imbera / Daeduck (FI / KR) production line by Q2-2010

Ibiden (JP)

Taiyo Yuden (JP)

Flip-Chip International (US)

SMT / SiPModule integrators

CMK (JP) Murata

Toshiba

NSCNXP

UTAC / NEPES (SG / KR)

Dyconex (Swiss) pilot line ready

Renesas / NEC

TIInfineon

Maxim ICDenso

STEricsson

SEMCO (KR) production line in qualification

Chip Embedding

process

BE stepsMarking, Dicing, inspection,

Tape & Reel

Samsung

Epcos -TDK (GE / JP) pilot line ready

OKI Printed Circuits (JP)

Compass technology (China)

NEC (JP)

Dialog Semi

Bosch

PanasonicNEC Toppan (JP) Casio

CireTec (FR)

STMicro

QualcommVTI

IPS (US)

Fujitsu

Sony

ADI

Thalesams

ASE (TW)

Schweizer Electronic (GE)

Nokia

Pana

sonic

LG

Seagate

ContinentalAmkor (KR)Toyota

Seurin

Medtronic

Motorola

Clover Electronics (JP)

StatsChipPAC (SG)

SPIL (TW)

DNP (JP)

Samsung

© 2010 • 22Copyrights © Yole Développement SARL. All rights reserved.

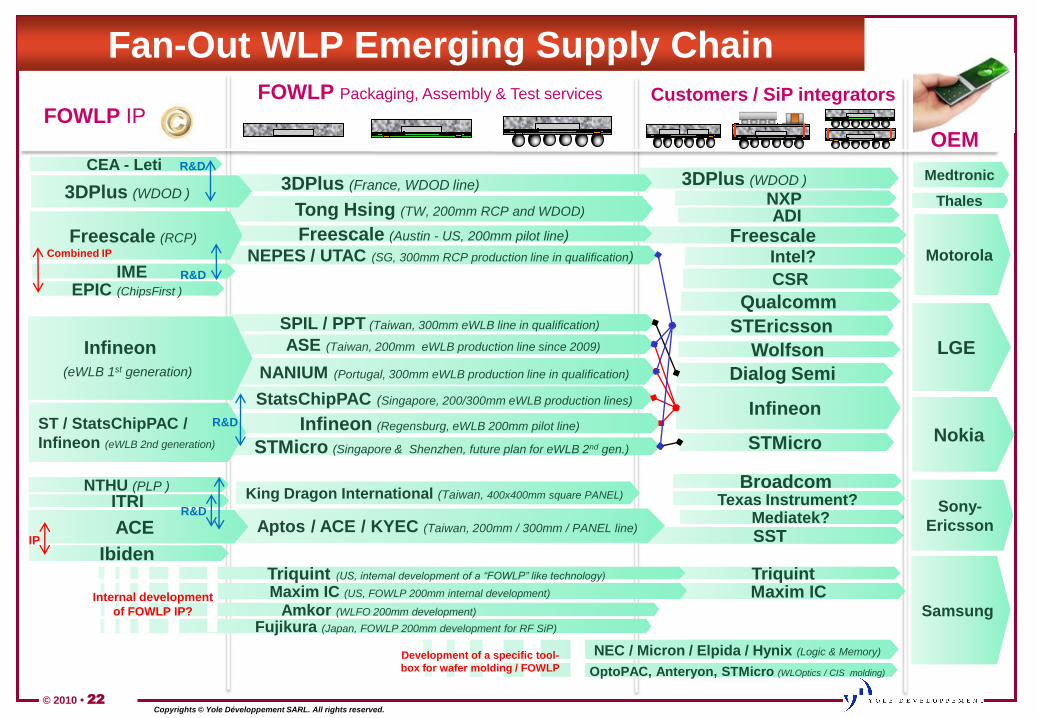

Tong Hsing (TW, 200mm RCP and WDOD)

3DPlus (WDOD )3DPlus (France, WDOD line)

STMicro

Mediatek?

SST

Nokia

Samsung

LGE

Infineon

Freescale

NANIUM (Portugal, 300mm eWLB production line in qualification) Dialog Semi

Wolfson

ADI

STEricsson

Fan-Out WLP Emerging Supply Chain

StatsChipPAC (Singapore, 200/300mm eWLB production lines)

SPIL / PPT (Taiwan, 300mm eWLB line in qualification)

FOWLP IPOEM

ITRI

Aptos / ACE / KYEC (Taiwan, 200mm / 300mm / PANEL line)

IME

Customers / SiP integrators

ASE (Taiwan, 200mm eWLB production line since 2009)

NEC / Micron / Elpida / Hynix (Logic & Memory)

Triquint

NEPES / UTAC (SG, 300mm RCP production line in qualification)

FOWLP Packaging, Assembly & Test services

EPIC (ChipsFirst )

Infineon (Regensburg, eWLB 200mm pilot line)

ACE

Infineon

(eWLB 1st generation)

Freescale (Austin - US, 200mm pilot line) Freescale (RCP)

Ibiden

Intel?

CSR

STMicro (Singapore & Shenzhen, future plan for eWLB 2nd gen.)

ST / StatsChipPAC /

Infineon (eWLB 2nd generation)

Motorola

Sony-

Ericsson

Texas Instrument?

OptoPAC, Anteryon, STMicro (WLOptics / CIS molding)

Combined IP

IP

R&D

R&D

R&D

Development of a specific tool-

box for wafer molding / FOWLP

NTHU (PLP )

3DPlus (WDOD )

CEA - Leti R&D

King Dragon International (Taiwan, 400x400mm square PANEL)

Amkor (WLFO 200mm development)

Qualcomm

Broadcom

Maxim ICMaxim IC (US, FOWLP 200mm internal development)

Fujikura (Japan, FOWLP 200mm development for RF SiP)

Triquint (US, internal development of a “FOWLP” like technology)

Internal development

of FOWLP IP?

Medtronic

ThalesNXP

© 2010 • 23Copyrights © Yole Développement SARL. All rights reserved.

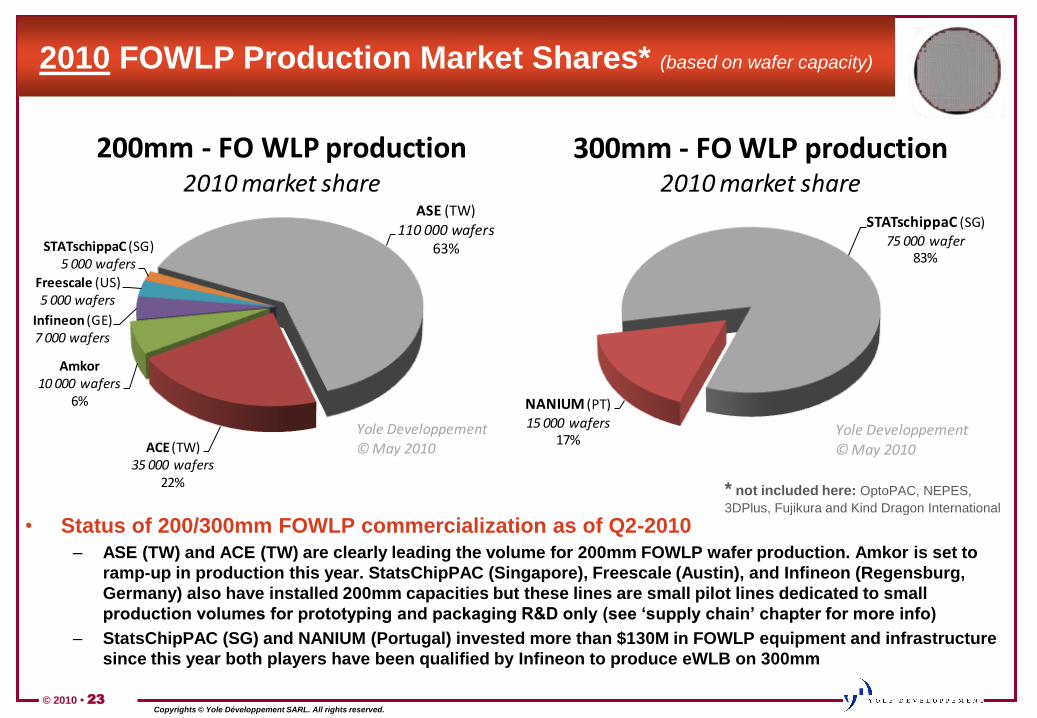

ASE (TW)110 000 wafers

63%

ACE (TW)35 000 wafers

22%

Amkor 10 000 wafers

6%

Infineon (GE)7 000 wafers

Freescale (US)5 000 wafers

STATschippaC (SG)5 000 wafers

200mm - FO WLP production 2010 market share

Yole Developpement

© May 2010

2010 FOWLP Production Market Shares* (based on wafer capacity)

• Status of 200/300mm FOWLP commercialization as of Q2-2010

– ASE (TW) and ACE (TW) are clearly leading the volume for 200mm FOWLP wafer production. Amkor is set to

ramp-up in production this year. StatsChipPAC (Singapore), Freescale (Austin), and Infineon (Regensburg,

Germany) also have installed 200mm capacities but these lines are small pilot lines dedicated to small

production volumes for prototyping and packaging R&D only (see „supply chain‟ chapter for more info)

– StatsChipPAC (SG) and NANIUM (Portugal) invested more than $130M in FOWLP equipment and infrastructure

since this year both players have been qualified by Infineon to produce eWLB on 300mm

* not included here: OptoPAC, NEPES,

3DPlus, Fujikura and Kind Dragon International

STATschippaC (SG)

75 000 wafer83%

NANIUM (PT)

15 000 wafers17%

300mm - FO WLP production 2010 market share

Yole Developpement © May 2010

© 2010 • 24Copyrights © Yole Développement SARL. All rights reserved.

FOCUS ON 3D TSV.

© 2010 • 25Copyrights © Yole Développement SARL. All rights reserved.

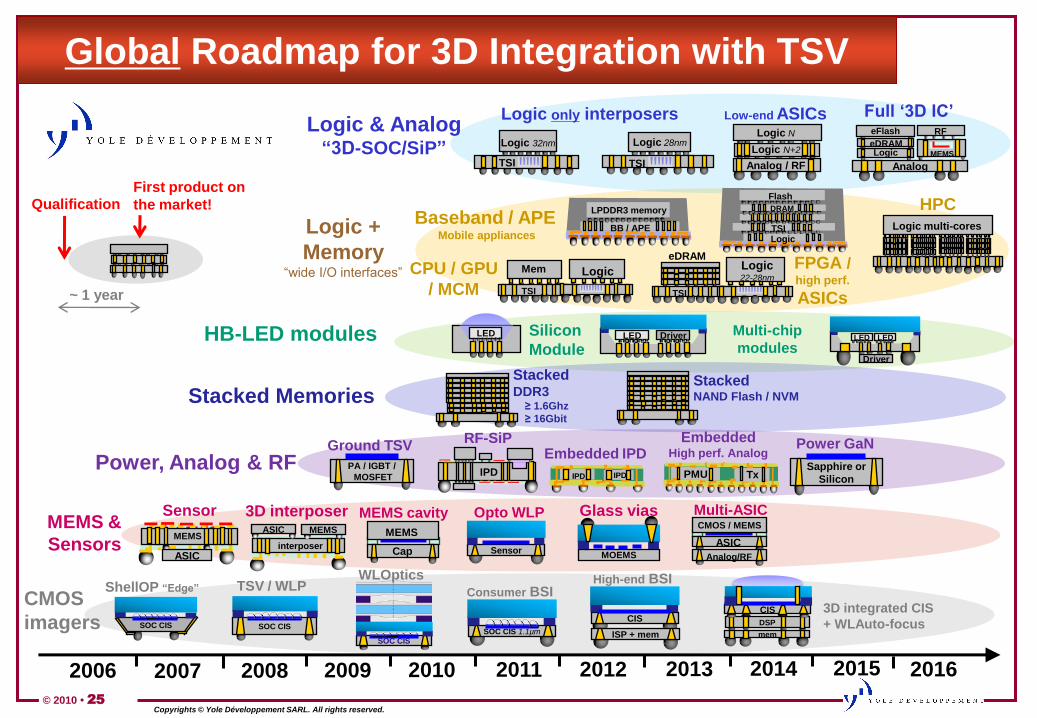

Global Roadmap for 3D Integration with TSV

2007 2008 2009 2010 2011 2012 2013 2014 20162006 2015

MEMS &

Sensors

MEMS cavity

MEMS

Cap

Sensor

ModuleMEMS

ASIC

CMOS

imagersSOC CIS

WLOptics

SOC CIS

ShellOP “Edge”

SOC CIS

TSV / WLP

SOC CIS 1.1µm

Consumer BSI

3D interposer

interposer

ASIC MEMS

Multi-ASICCMOS / MEMS

ASIC

Analog/RFSensor

Opto WLP

MOEMS

Glass vias

Power, Analog & RFIPD IPD

Embedded IPDPA / IGBT /

MOSFET

Ground TSV

Stacked DDR3

≥ 1.6Ghz

≥ 16Gbit

Stacked NAND Flash / NVMStacked Memories

Logic +

Memory “wide I/O interfaces” Mem Logic

TSI

CPU / GPU

/ MCM

eDRAMLogic22-28nm

TSI

FPGA / high perf.

ASICs

Logic & Analog “3D-SOC/SiP”

HB-LED modules LED Driver Multi-chip

modulesLED Silicon

Module

CIS

High-end BSI

ISP + mem

Low-end ASICsLogic N

Logic N+2

Analog / RF

PMU Tx

Embedded High perf. Analog

QualificationFirst product on

the market!

~ 1 year

Baseband / APEMobile appliances

RFeFlash

Logic

Analog

eDRAMMEMS

Full „3D IC‟

Logic multi-cores

HPC

RF-SiP

IPD

Logic 32nm

TSI

Logic only interposers

Logic 28nm

TSI

3D integrated CIS

+ WLAuto-focusDSP

mem

CIS

Logic

Flash

TSI

DRAM

BB / APE

LPDDR3 memory

Sapphire or

Silicon

Power GaN

LED

Driver

LED

© 2010 • 26Copyrights © Yole Développement SARL. All rights reserved.

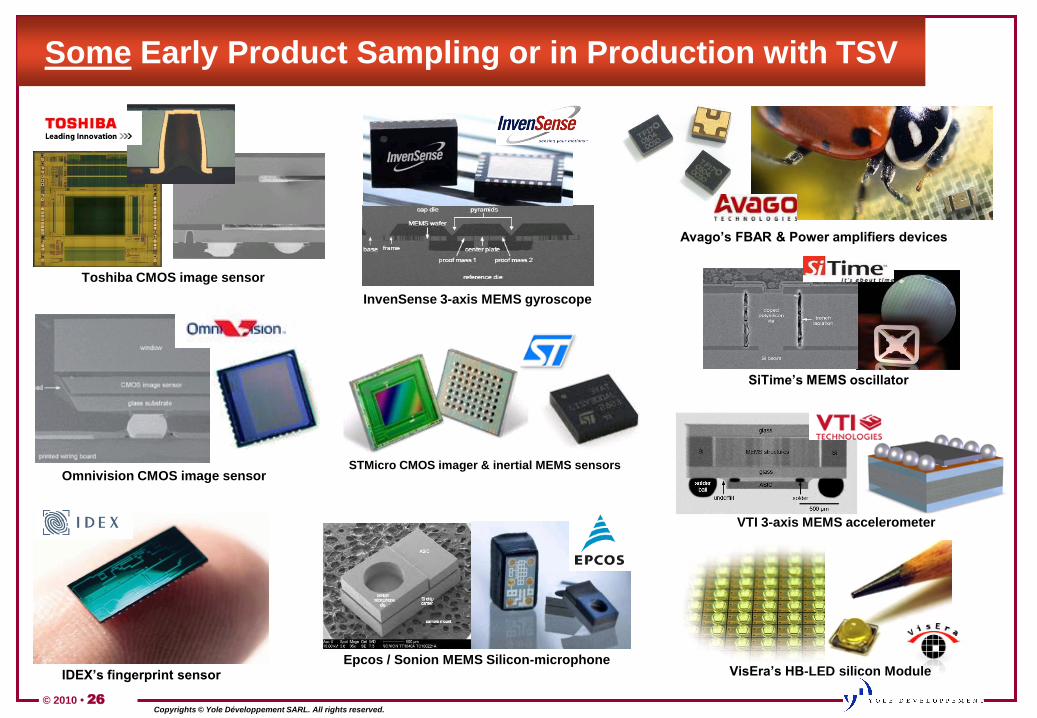

Some Early Product Sampling or in Production with TSV

Avago‟s FBAR & Power amplifiers devices

VTI 3-axis MEMS accelerometer

VisEra‟s HB-LED silicon ModuleIDEX‟s fingerprint sensor

Omnivision CMOS image sensor

Epcos / Sonion MEMS Silicon-microphone

Toshiba CMOS image sensor

InvenSense 3-axis MEMS gyroscope

STMicro CMOS imager & inertial MEMS sensors

SiTime‟s MEMS oscillator

© 2010 • 27Copyrights © Yole Développement SARL. All rights reserved.

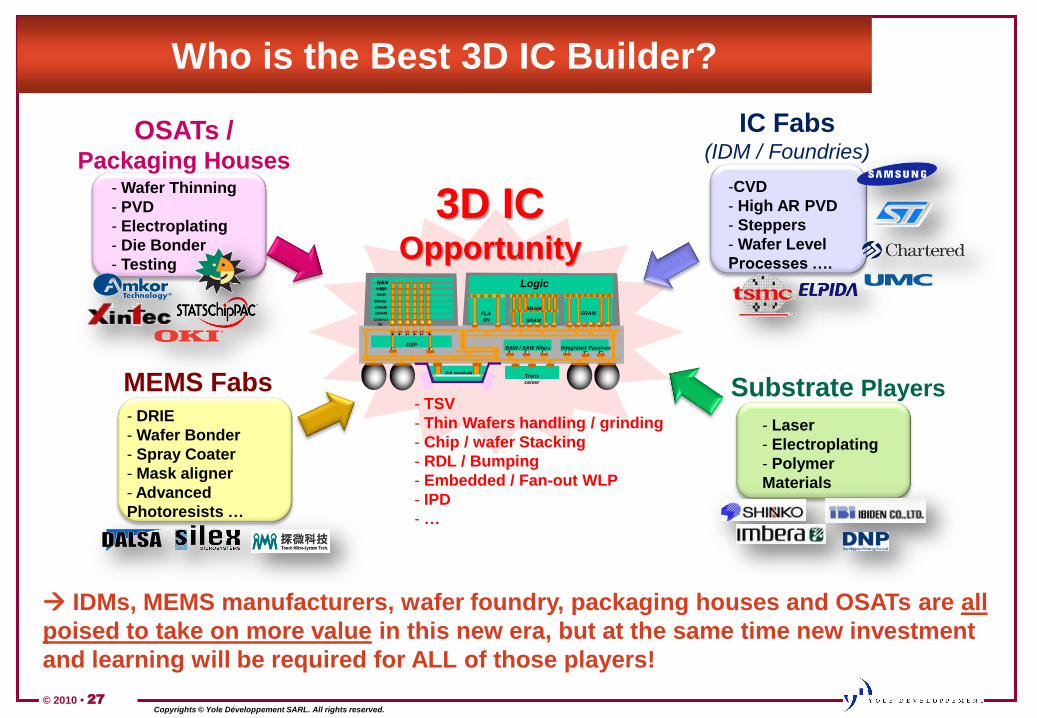

Who is the Best 3D IC Builder?

IDMs, MEMS manufacturers, wafer foundry, packaging houses and OSATs are all

poised to take on more value in this new era, but at the same time new investment

and learning will be required for ALL of those players!

3D IC Opportunity

MEMS Fabs- DRIE

- Wafer Bonder

- Spray Coater

- Mask aligner

- Advanced

Photoresists …

OSATs / Packaging Houses

- Wafer Thinning

- PVD

- Electroplating

- Die Bonder

- Testing

SRAM

SRAM

FLA

SH

Logic

Trans

ceiver

BAW / SAW filters Integrated PassivesDSP

PA module

SRAM

SRAM

DRAM

Control

ler

NOR

DRAM

DRAM

NAND

NAN

D

Substrate Players

- Laser

- Electroplating

- Polymer

Materials

- TSV

- Thin Wafers handling / grinding

- Chip / wafer Stacking

- RDL / Bumping

- Embedded / Fan-out WLP

- IPD

- …

IC Fabs(IDM / Foundries)

-CVD

- High AR PVD

- Steppers

- Wafer Level

Processes ….

© 2010 • 28Copyrights © Yole Développement SARL. All rights reserved.

FOCUS ON SILICON AND GLASS

INTERPOSER.

© 2010 • 29Copyrights © Yole Développement SARL. All rights reserved.

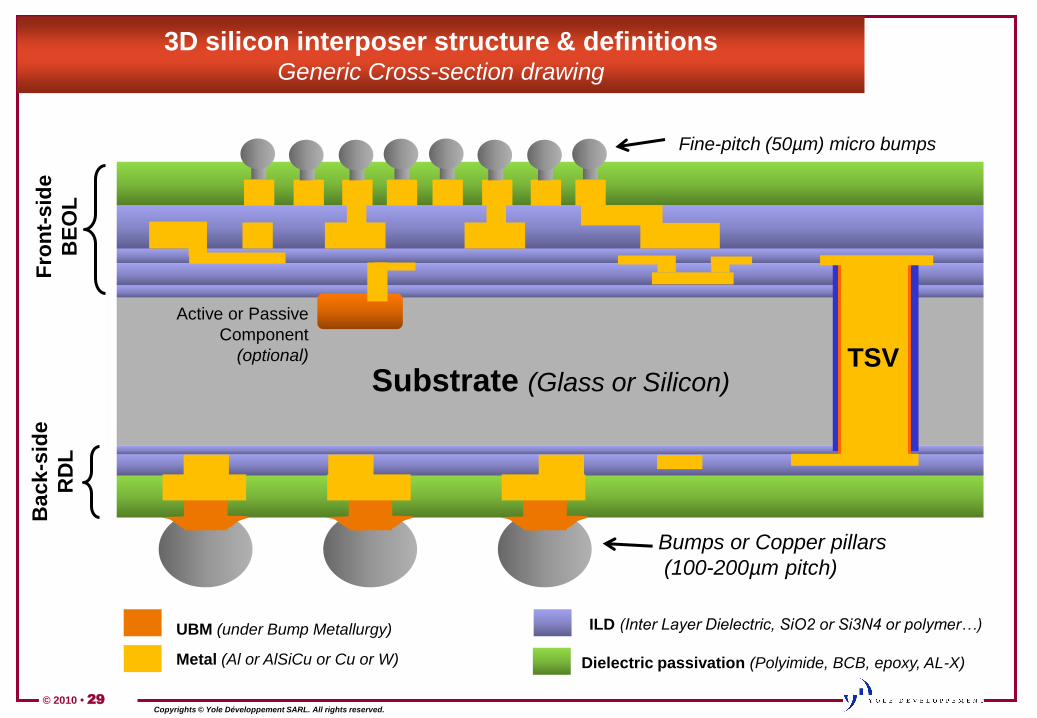

3D silicon interposer structure & definitionsGeneric Cross-section drawing

Substrate (Glass or Silicon)

Fro

nt-

sid

e

BE

OL

Fine-pitch (50µm) micro bumps

Bumps or Copper pillars

(100-200µm pitch)

Active or Passive

Component

(optional) TSV

Back

-sid

e

RD

L

UBM (under Bump Metallurgy)

Metal (Al or AlSiCu or Cu or W) Dielectric passivation (Polyimide, BCB, epoxy, AL-X)

ILD (Inter Layer Dielectric, SiO2 or Si3N4 or polymer…)

© 2010 • 30Copyrights © Yole Développement SARL. All rights reserved.

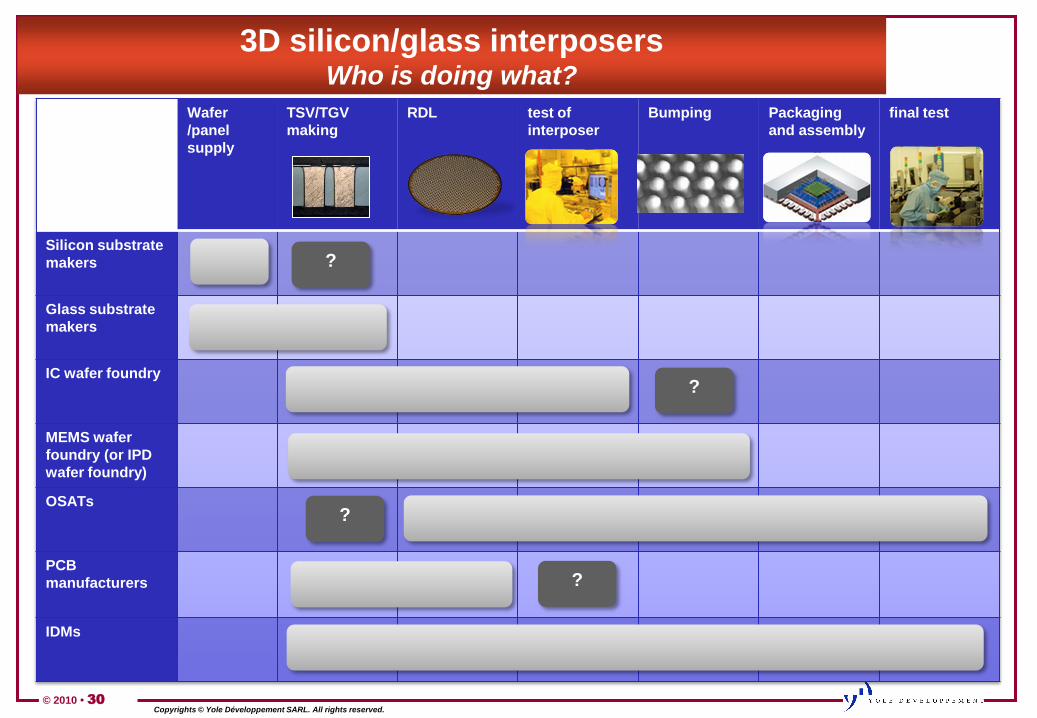

3D silicon/glass interposersWho is doing what?

Wafer

/panel

supply

TSV/TGV

making

RDL test of

interposer

Bumping Packaging

and assembly

final test

Silicon substrate

makers

Glass substrate

makers

IC wafer foundry

MEMS wafer

foundry (or IPD

wafer foundry)

OSATs

PCB

manufacturers

IDMs

?

?

?

?

© 2010 • 31Copyrights © Yole Développement SARL. All rights reserved.

Mid-end Packaging InfrastructureFirst conclusions

• „Mid-end‟ business ~ 20% of BE packager revenues by 2016

– Driver for these players is to sustain growth & preserve margins in this cost

competitive market

– Challenge: annual R&D investment budget usually low

• „Mid-end‟ business ~ 2% of FE semiconductor revenues by 2016 only

– Not driven by revenues generated!

– Rather interested by the potential behind this integration:

• In order to package everything by themselves and not rely on

subcontractors as packaging is now becoming increasingly strategic to

control!

• To climb in the electronic value chain by integrating more additional

functions and moving to “system” integration

• High interest for 3D from system integrator companies in medical (Medtronic,

SJM…) and automotive areas (Honda, Toyota, Denso, Bosch…)

– 3D IC integration with TSV implies possible changes in the electronic value

chain: could OEMs & system integrator players become the next “SOC

makers”?

© 2010 • 32Copyrights © Yole Développement SARL. All rights reserved.

For more information …

Take a look at our websites

www.i-micronews.fr

Please make a stop at Yole booth: N° C2135

Feel free to give me your business card to receive the electronic copy of my slides.