events.joc.com · and services in urban areas drive migration to urban areas. ... – all-electric...

TRANSCRIPT

. . . . .

Port Infrastructure Identifying Areas of Greatest Need

December 6, 2016

Dr. Walter Kemmsies Managing Director, Economist and Chief Strategist

JLL Ports Airports and Global Infrastructure

Larry Nye, P. E. Sr. V. P.

Moffatt & Nichol

1

. . . . .

Port Infrastructure Identifying Areas of Greatest Need

• Focus on international container trade

• Focus mainly on East-West container traffic

2

. . . . . Drivers of Global Trade Growth

3

• From 1950 to 2013, manufactured goods trade has grown twice as fast as real GDP. Among other trends, this

is due to:

WORLD REAL GDP AND TRADE INDEXES 1950-2015E

Source: WTO, JLL

• Free Trade Agreements

• Information/Communication Technology

• Maritime and Inland Connectivity Infrastructure

• Demographic Trends

1950 – 2015 CAGR

Manufactured Goods 7.0%

Extraction Goods 3.9%

GDP 3.6%

Agricultural goods 3.6%

Japan

Korea, Taiwan

China

. . . . . International Labor Cost Comparisons in 2001

4

LOCAL MANUFACTURING WAGES CONVERTED INTO US$ AT PREVAILING EXCHANGE RATES IN 2001 AND 2014

Through most of the

several decades

until 2001 wages in

emerging market

economies were

much lower than in

developed

economies.

With younger

populations but a

lower wage base it

was necessary to

offshore production

to emerging market

economies. Latin

America benefitted

first, followed by

Asia.

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

Source: Government statistics agencies,. JLL

. . . . . Ocean Shipping 101

“… the best way to move something heavy from here to there was and is to float it there.”

5

John Szarkowski, Former Director of Photography, New York Museum of Modern Art, A Maritime Album, 100 Photographs and Their Stories:

. . . . . Ocean Shipping 101

“… the best way to move something heavy from here to there was and is to float it there.”

6

John Szarkowski, Former Director of Photography, New York Museum of Modern Art, A Maritime Album, 100 Photographs and Their Stories:

“It is only recently, … and cautiously, that we have moved far from the oceans, to places like Siberia or Nebraska, and it is by no

means clear that places so far removed from the sea are viable in the long term.”

. . . . . Ocean Shipping 101

7

“…the real driving force behind globalization is the declining cost of international transport…”

Journal of Commerce

The Box That Changed the World

. . . . . Ocean Shipping 101

• Ocean Transport is, forever and always, the best way to move stuff on this planet

• Ocean transport has become so cost-efficient, it actually drives trade and thereby pressures ports and land transport infrastructure

8

Relative Container Transport Cost per TEU-MileNorth Asia - US Midwest

Ocean

Land

Relative Container Transport CostNorth Asia - US Midwest

Ocean Transport

US Port

Land Transport

6,500 miles

1,700 miles

. . . . .

People are All Over Our Country They All Need Stuff

US Population Centroid

Nebraska

320M People Each Dot = 7,500

People

By the Way, Stuff Doesn’t Really Care if Trade is Foreign or Domestic

WC Canada

PNW

N. Cal.

S. Cal.

Gulf

S. Atlantic

Mid Atlantic

N. Atlantic

St Lawrence

Our Principle Port Trade Gateways are Where They Are

We Must Have Efficient Port, Road & Rail Infrastructure

9

. . . . .

On the Ocean Side of Ports, We Only Need to be Concerned With The Last “Mile” (or so)

• Build and maintain strong breakwaters

• Dredge and maintain sufficiently deep channels and wide turning basins

• Build high bridges over critical waterways

10

. . . . .

Increasingly Urbanized, Increasingly Congested

11

PERCENTAGE OF URBAN POPULATION AND AGGLOMERATIONS BY SIZE CLASS: 1980 AND 2011

1980 2011

• Three major migration trends in the US are to the south, to the coasts and to urban areas.

• Rest of the world is urbanizing too.

• Substitution of capital for labor in rural areas and higher income offered by manufacturing

and services in urban areas drive migration to urban areas.

• Better services supply in urban areas also attracts retirees.

• In major port cities it is likely that congestion could worsen.

. . . . .

Ecommerce Gaining Share of US Retail Sales – Analogous to “push”

12

ECOMMERCE VS TOTAL RETAIL TRADE SALES

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

200

400

600

800

1,000

1,200

1,400

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Shar

e o

f To

tal

$ B

illio

ns

Ecommerce Share (right axis) E-commerce Total

Ecommerce is gaining

share of consumer

spending in many

countries, with the US

among the countries

leading the trend.

Growing concentrations of

populations in metropolitan

regions and growing

Internet subscriptions are

main driver.

As Ecommerce operations

spread to more urban

locations they will gain

share of US retail sales.

Ecommerce operations

prefer to have marine

freight delivered to many

ports so as to support their

national market

development strategies.

. . . . .

Selected On-Demand Company Fulfillment Time Estimates

13 Source: Mary Meeker @ KPCB

. . . . . US Port Capacity

• Regional throughput is pretty well balanced to regional capacity

7% 1

0%

7%

40

%

12

%

4%

15

%

5%

9%

8%

6%

41

%

14

%

6%

12

%

5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Port Capacity vs Current Throughput

% of US Capacity % of US Throughput

69% 69%64%

67%

0%

10%

20%

30%

40%

50%

60%

70%

80%

West Coast East Coast Gulf Coast US Overall

Estimated Current Regional Ports Percent of Capacity

• US Port regions currently have average of about 30% latent capacity

14

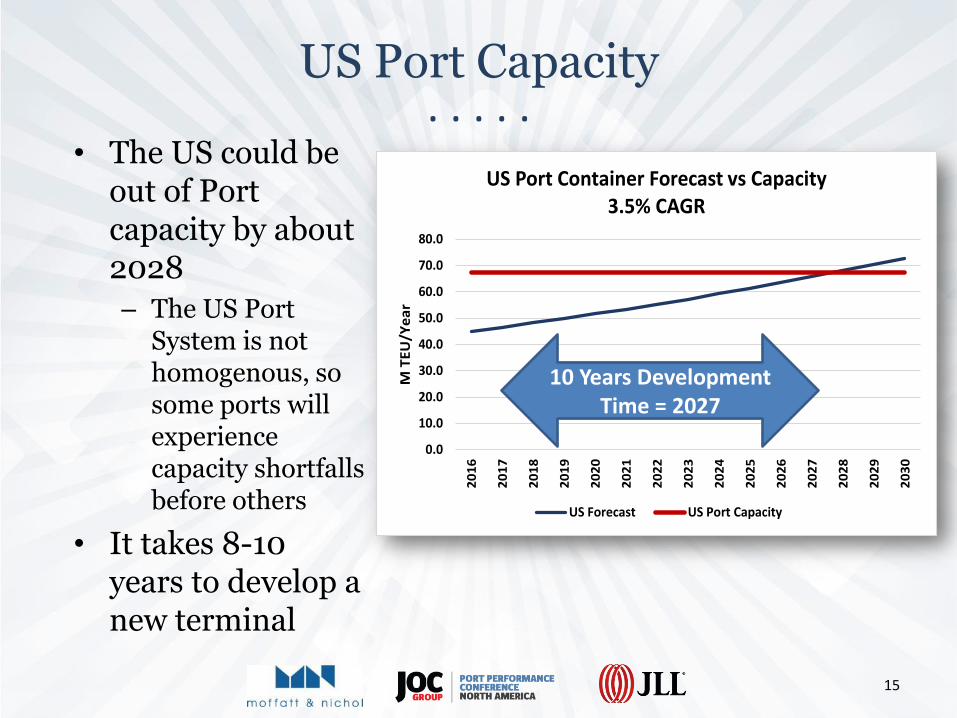

. . . . . US Port Capacity

• The US could be out of Port capacity by about 2028

– The US Port System is not homogenous, so some ports will experience capacity shortfalls before others

• It takes 8-10 years to develop a new terminal

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

M T

EU

/Ye

ar

US Port Container Forecast vs Capacity3.5% CAGR

US Forecast US Port Capacity

10 Years Development Time = 2027

15

. . . . . Port / Terminal Densification & Automation

16

• Can increase terminal capacity by 25-30%

– Densified storage

– Automated handling

• Can increase productivity by 25%-30%

– Vessel

– Gate

– Rail

• Can reduce traffic congestion

– Truck turn times

– Dual transactions

• Can reduce emissions by almost 100%

– All-electric container handling is possible

• Cost is significant

– Per 1M annual TEU Capacity

• Infrastructure $200-300 Million

• Equipment $200 Million

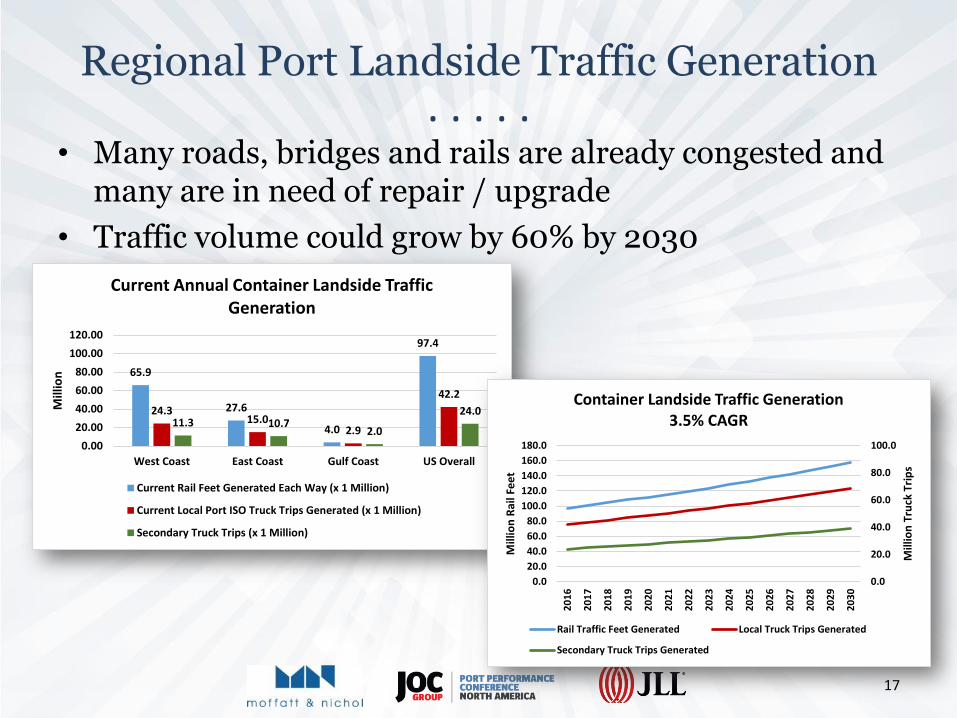

. . . . . Regional Port Landside Traffic Generation

• Many roads, bridges and rails are already congested and many are in need of repair / upgrade

• Traffic volume could grow by 60% by 2030

17

65.9

27.6

4.0

97.4

24.315.0

2.9

42.2

11.3 10.72.0

24.0

0.00

20.00

40.00

60.00

80.00

100.00

120.00

West Coast East Coast Gulf Coast US Overall

Mill

ion

Current Annual Container Landside Traffic Generation

Current Rail Feet Generated Each Way (x 1 Million)

Current Local Port ISO Truck Trips Generated (x 1 Million)

Secondary Truck Trips (x 1 Million)

0.0

20.0

40.0

60.0

80.0

100.0

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

Mill

ion

Tru

ck T

rip

s

Mill

ion

Rai

l Fe

et

Container Landside Traffic Generation3.5% CAGR

Rail Traffic Feet Generated Local Truck Trips Generated

Secondary Truck Trips Generated

. . . . .

Last Mile Intermodal Capacity May be Difficult to Achieve

18

PORT OF NEW YORK AND NEW JERSEY CONTAINER TERMINALS AND INLAND CONNECTIVITY INFRASTRUCTURE

ContainerTerminal

Intermodal

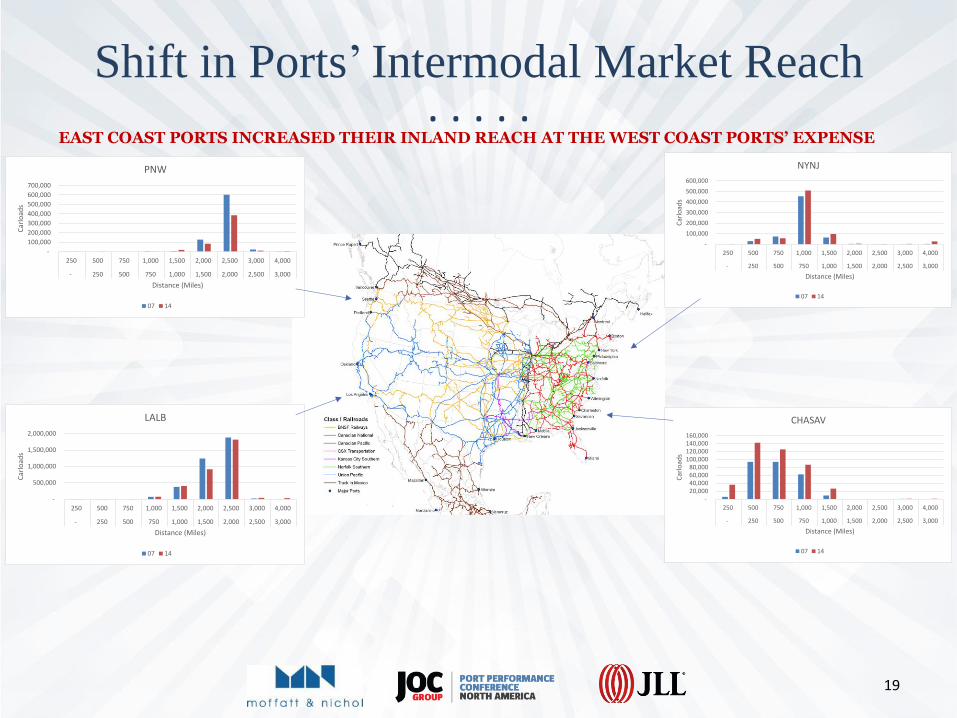

. . . . . Shift in Ports’ Intermodal Market Reach

19

EAST COAST PORTS INCREASED THEIR INLAND REACH AT THE WEST COAST PORTS’ EXPENSE

-

100,000

200,000

300,000

400,000

500,000

600,000

250 500 750 1,000 1,500 2,000 2,500 3,000 4,000

- 250 500 750 1,000 1,500 2,000 2,500 3,000

Car

load

s

Distance (Miles)

NYNJ

07 14

-20,00040,00060,00080,000

100,000120,000140,000160,000

250 500 750 1,000 1,500 2,000 2,500 3,000 4,000

- 250 500 750 1,000 1,500 2,000 2,500 3,000

Car

load

s

Distance (Miles)

CHASAV

07 14

-

500,000

1,000,000

1,500,000

2,000,000

250 500 750 1,000 1,500 2,000 2,500 3,000 4,000

- 250 500 750 1,000 1,500 2,000 2,500 3,000

Car

load

s

Distance (Miles)

LALB

07 14

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

250 500 750 1,000 1,500 2,000 2,500 3,000 4,000

- 250 500 750 1,000 1,500 2,000 2,500 3,000

Car

load

s

Distance (Miles)

PNW

07 14

. . . . . The Oceans are (Still) Large

• The Oceans are fantastic infrastructure and constraint-free highways, … a gift of our planet

• But ocean cargo speed is low and speeding up is expensive – Air 500 mph

– Land 50 mph

– Sea 20-25 mph

• Even with technology “shrinking” our planet, the oceans are still large

• If you are going to travel across the Ocean, best make it worth while

20

Trans Pacific ~6,000 NM 14 Days

6 port + 14 sail + 6 port + 14 sail = 40 days per roundtrip = 9 voyages per year per vessel = 6

vessels required for weekly service

• You need a big boat!

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

0 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

Pe

rce

nt

of

Po

we

r R

eq

'd

Speed (knots)

Main Engine Power Factor

. . . . . Big Ships - 18,000 TEU

21

230 positions above deck

230 positions below deck

Up to 460 Container slots per Bay ~900 moves per bay per call 30 STS crane hours per bay

Photo Courtesy POLB

235 ft tall

~190 feet above water line

1312 ft long

Need ~55 foot water depth at berth

200,000

metric tons

190 ft beam

. . . . . Big Ships - 18,000 TEU

22

Photo Courtesy POLB

• Port approach channels

– 50 - 55 feet deep

– 475 feet wide

• Turning basins

– 1,600 - 1,800 feet diameter

• Bridges

– 200 feet clear height

Photo Courtesy POLB

. . . . . Critical Terminal Infrastructure

• Berths

• Wharves, fenders, & bollards,

• Throughput capacity / stacking density

• Ship-to-shore cranes

• Yard cranes and pavement

• Truck gates

• On-terminal railyards

23

. . . . .

18,000 TEU Vessel Fenders and Bollards

24

1.18 2.65 4.71 7.

36 10.6

0

14.4

3

18.8

4

23.8

5 29.4

4 35.6

2 42.3

9 49.7

5 57.7

0 66.2

4

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

PSF

Wind Speed (mph)

Wind Pressure

Wind pressure at 60 mph = 10.6 psf

186,000 SF x 10.6 PSF = 1.9M Pounds Wind Pressure

Replace 50 MT Bollards with 200 MT Double Bollards Replace Single Fenders with Larger Double Fenders

. . . . .

18,000 TEU Vessel Ship to Shore Cranes & Crane Rails

25

5,000 TEU (Current wharf design

in many US Ports)

135

Containers

per bay

320

Containers

per bay

115 ft 165 ft 115 ft

215 ft

18,000 TEU

30,000 lbs / lf 55,000 – 75,000 lbs / lf

. . . . .

18,000 TEU Vessel Port Impacts by Region

• Beyond vessel size, impacts may vary by region and service

26

6,0005,000

3,000

17,000

8,000

5,000 5,000 5,000

02,0004,0006,0008,000

10,00012,00014,00016,00018,000

30.00% 25.00% 15.00% 85.00% 40.00% 25.00% 25.00% 25.00%

Canada WC NWSA Oakland LA/LB NY/NJ Norfolk CharlestonSavannah

West Coast East Coast

Co

nta

ine

r Li

fts

pe

r C

all

Percent Interchange per Call

Lifts per Call per 18K TEU Service

561,600468,000

280,800

1,591,200

748,800

468,000 468,000 468,000

0200,000400,000600,000800,000

1,000,0001,200,0001,400,0001,600,0001,800,000

30.00% 25.00% 15.00% 85.00% 40.00% 25.00% 25.00% 25.00%

Canada WC NWSA Oakland LA/LB NY/NJ Norfolk CharlestonSavannah

West Coast East Coast

TEU

/Ye

ar/S

erv

ice

Percent Interchange per Call

TEU Throughput per Year per 18K TEU Service

. . . . .

18,000 TEU Vessel Port Impacts by Region

• Productivity demand of 180 gross / 200+ net moves per hour for up to six days requires a paradigm shift in terminal operating systems

27

5.004.00

3.00

8.00

6.00 6.00 6.00 6.00

0.001.002.003.004.005.006.007.008.009.00

30.00% 25.00% 15.00% 85.00% 40.00% 25.00% 25.00% 25.00%

Canada WC NWSA Oakland LA/LB NY/NJ Norfolk Charleston Savannah

West Coast East Coast

Cra

ne

s

Percent Interchange per Call

Ship to Shore Cranes per 18K TEU Service

112

90

67

179

134 134 134 134

020406080

100120140160180200

Can

ada

WC

NW

SA

Oak

lan

d

LA/L

B

NY

/NJ

No

rfo

lk

Ch

arle

sto

n

Sava

nn

ah

West Coast East Coast

Gro

ss M

ove

s p

er

Ho

ur

18k TEU Vessel Productivity Demand

. . . . .

18,000 TEU Vessel Port Impacts by Region

28

51 62

43

20

4

10

7

78

78

7887 10

8

14

0 20

6 28

3

29

7

24

5

68

5

0100200300400500600700800

30.00% 25.00% 15.00% 85.00% 40.00% 25.00% 25.00% 25.00%

CanadaWC

NWSA Oakland LA/LB NY/NJ Norfolk Charleston Savannah

West Coast East Coast

Term

inal

Acr

es

Average Percent Interchange per Call

Terminal Acres Required per 18k TEU Service

Terminal Acres Required per Service Average Current Acres per Terminal

. . . . .

18,000 TEU Vessel Port Impacts by Region

29

024681012141618

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Can

ada

WC

NW

SA

Oak

lan

d

LA/L

B

NY

/NJ

No

rfo

lk

Ch

arle

sto

n

Sava

nn

ah

West Coast East Coast

Ad

de

d S

tora

ge A

cre

s

Inve

nto

ry S

pik

e T

EU

18,000 TEU Initial Discharge Inventory Spike

Inventory Spike (TEU)

Additional Acres of Storage Required for Inventory Spike

230

230

No. of Bays (cranes) x TEU Discharge per Bay

. . . . .

18,000 TEU Vessel Landside Impacts by Region

• Landside traffic generation per 18k TEU Service

30

Not counting secondary truck trips

0%

10%

20%

30%

40%

50%

60%

70%

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

Can

ada

WC

NW

SA

Oak

lan

d

LA/L

B

NY

/NJ

No

rfo

lk

Ch

arle

sto

n

Sava

nn

ah

West Coast East Coast

Rai

l Pe

rce

nt

of

Thro

ugh

pu

t

Rai

l Fe

et

Annual Rail Feet Each Way per 18K TEU Service

Rail feet Each Way Percent Rail

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Can

ada

WC

NW

SA

Oak

lan

d

LA/L

B

NY

/NJ

No

rfo

lk

Ch

arle

sto

n

Sava

nn

ah

West Coast East Coast

Loca

l Tru

ck T

rip

s

Annual Local Port Truck Trips per 18 K TEU Service

. . . . .

18,000 TEU Vessel Port Cost Impacts by Region

• Terminal upgrade cost to accommodate 18,000 TEU vessels

– $100 – $200M per berth or service

31

$0.0

$50.0

$100.0

$150.0

$200.0

$250.0

Can

ada

WC

NW

SA

Oak

lan

d

LA/L

B

NY

/NJ

No

rfo

lk

Ch

arle

sto

n

Sava

nn

ah

West Coast East Coast

20

16

US$

18,000 TEU Berth Upgrade Cost(Per Berth)

Replace STS Cranes

Replace Fenders & Bollards

Strengthen Crane Rails

Deepen Berth

Inventory Spike Storage Area

• Waterside costs vary by Port/Terminal

• Landside costs vary

– But are throughput-driven not vessel size driven

. . . . . Where Will the Money Come From?

Entity

• Government (Fed)

• Ports (State/City) – Landlord

– Operator

– Privatized

– Government/local - state tax subsidies?

• Ocean carriers & Terminal operators

• Investment banks

• Private investment funds

What They Paid For

• Breakwaters, dredging & reclamation

• Terminal infrastructure

• Terminal equipment and

technology

Traditional US Model

32

. . . . . Public Sector Debt is at a Historically High Level

33

GOVERNMENT DEBT AS A PERCENTAGE OF GDP STATE PENSION FUNDING GAP

Sources: Dept of Commerce, http://www.pewtrusts.org/en/research-and-analysis/issue-briefs/2015/07/the-state-pensions-funding-gap-challenges-persist, BEA, Federal Reserve

. . . . .

Thank You

34

Larry Nye. P. E.

Sr. V. P.

Moffatt & Nichol

Dr. Walter Kemmsies Managing Director, Economist and Chief Strategist

JLL Ports Airports and Global Infrastructure