session 10 pd, who pays your last credit card bill? final ... · higher premium per 1000 ... often...

TRANSCRIPT

Session 10 PD, Who Pays Your Last Credit Card Bill? Final Expense Insurance 101

Moderator: Helen Colterman, FSA, CERA, ACIA

Presenters:

Jing Lang, ASA, ACIA Jeffrey Shaw, ChFC, CLU

Brian A. Sibley, FSA, MAAA

Final Expense Market in the US

Who Pays Your Last Credit Card Bill?Final Expense Insurance 101

SOA Life & Annuity MeetingNew York, NYMay 4, 2015

Brian Sibley FSA, MAAA

RGA Reinsurance CompanyVP Business Development

Final Expense Defined Target Market Market Size Typical Sale Product Design Pricing Considerations Applicant and Agent Characteristics Challenges Management Innovations

Final Expense Insurance 101 Final Expense Topics Covered

2

Final Expense Insurance is: Life Insurance purchased to cover funeral expenses, burial costs,

medical and hospital bills, loan balances, and credit card debts Small face amounts Whole life (sometimes term) Simplified issue underwriting

Final Expense is not Pre-Need which is a different product sold a different way to pre-pay a funeral

Final Expense Defined What is final expense life insurance?

3

Aging population in the US 10,000 Baby Boomers turn 65 every day. This will go on for at least

15 more years In 2015, there will be 100 million people between ages 50-80 36% have no savings, retirement or investments 35% live on social security alone Many of these people don’t have any life insurance

Sources: Social Security AdministrationUS Census Bureau Population projections

Final Expense US Market Size Why are companies targeting final expense?

4

High premium volume Product line has growth Demographics support it Undersold market

Final Expense US Market Size Why are companies selling final expense?

5

Year New Policies New Premium (000’s)2014 1,867,972 $1,250,0002015 1,876,806 $1,269,0002016 1,897,033 $1,294,0002017 1,919,570 $1,319,0002018 1,943,871 $1,345,000

Source: LIC/CSG Final Expense Survey Report 2013

Final Expense US Market Size Best Estimate Projection for new policies and premiums

6

Year Inforce Policies Inforce Premium (000’s)2014 6,156,537 $3,779,0002015 6,279,897 $3,947,0002016 6,380,281 $4,090,0002017 6,473,570 $4,219,0002018 6,563,595 $4,388,000

Source: LIC/CSG Final Expense Survey Report 2013

Final Expense US Market Size Best Estimate Projection for inforce policies and premiums

7

Small Face Amounts – Average size $10,900 Higher Premium per 1000 - Average annual premium $652 Written at older ages - Average issue age is 61 Mostly simplified issue underwriting

Limited application questions Ht./Wt. Chart (64%) Phone interview (59%) MIB Report (54%) Rx Check (46%).

Mostly sold by independent agents (82%), captive agents (17%) and Direct (<1%)

Mostly whole life coverage with some term

Source: LIC/CSG Final Expense Survey Report 2013

Final Expense Typical Sale What does a typical final expense sale look like?

8

Whole Life Products – 3 main types1. Level Death Benefit – (tightest SI underwriting) 2. Graded Death Benefit – often 30% of level DB in first year and 70% in

year 2, moving to 100% by year 3. (looser underwriting than 1) 3. Modified Death Benefit – returns premium often at 10% interest if

death in the first two years. (looser underwriting than 1 and 2) Term Products1. Graded Death Benefit Term – 2 year grade in for death benefits and

decreasing term after the level period2. Term products can be 10, 20 and 30 year term

Note: Graded and Modified Products often pay full death benefits in the first two years on accidental death

Final Expense Product Design What life insurance product designs are normally used?

9

Mortality Lapse Interest Expenses

Final Expense Pricing What are the key components of pricing for final expense products?

10

Critical to having a profitable final expense product Cost is often 50% or less of the total retail premiums because

commissions are very high on agent sold products If pricing mortality is off by 10% it can swing your profit margin up to

50% Driven by distribution, the application, the underwriting screening,

and rescission rates Important to reflect a bump up in pricing mortality in year 3+ after the

contestable period Many products are unismoke (aggregate) (i.e.10/20/60) Reinsurers and consultants can help with mortality- ensure they have

the experience data to back up the mortality assumptions provided

Final Expense Pricing Mortality

11

Fully UnderwrittenResidual StandardFace Amounts $100k - $250k100%

Non-MedicalStandardFace Amounts< $100k110% - 150%

Mortgage Term,Bank Sold Term, Worksite StandardFace Amounts< $250k170% - 390%

Final ExpenseLevel Death Benefit300% - 775%

Final Expense Pricing Mortality Spectrum RGA Mortality Experience by Market

Normalized to Fully Underwritten Residual Standard Non-smoker ExperienceRanges include variations by company, underwriting, target market, and issue age.

12

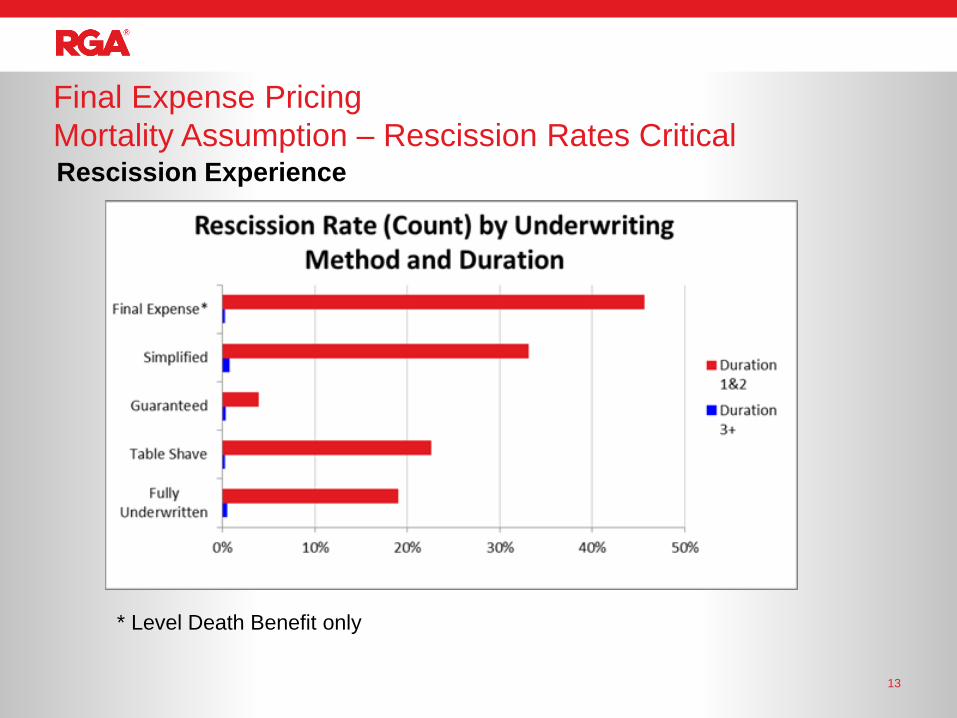

Final Expense Pricing Mortality Assumption – Rescission Rates CriticalRescission Experience

* Level Death Benefit only

13

Key in pricing because you need policies to persist to make up for high first year commissions and acquisition costs

According to the LIC/CSG survey, on average after 4 years only 50 percent of issued policies are still in force

Many people can’t afford the coverage or have been sold too much coverage and therefore lapse

According to the LIC/CSG survey, the few companies that take credit card payments have experienced worse persistency

Watch for lapse skewness as policies tend to lapse early in the policy year even for monthly mode

Watch for churning of the business which causes problems for final expense writers

Final Expense Pricing Lapses

14

Important in whole life pricing Low interest environment typically means low earned rates in pricing

Drives up your retail premiums

Low interest rates can also require higher cash values according to Standard Non-forfeiture Law Also drives up your retail premiums

Be prudent in your approach

Final Expense Pricing Interest Rates

15

Expenses are also very important in pricing High first year and renewal commissions including commission

related expenses are big expenses to cover in pricing Consider the cost of capital to fund the high commissions paid for

selling the final expense product Factor in the cost of all your underwriting evidence, Rx checks and

MIB Include the costs to manage this business Make sure to include claims adjudication costs to reflect the cost of

contestable claim rescissions

Final Expense Pricing Expenses

16

Monthly incomes of $2000 or less Education level – High school or less Single, divorced, never been married or widowed More females applicants than males May live in their original home Often have or had blue collar careers Often have children with similar characteristics sometimes living at

home

Final Expense Applicant CharacteristicsWhat are the characteristics of a typical applicant?

17

Often have the same characteristics as the people they sell to Many agents live pay check to pay check, but have higher incomes Agents need to keep selling final expense to have income from future

commissions to pay their costs Agents go out and pay for leads, gas and hotel bills so more

pressure to make sales Agents often pay between $22 and $45 per lead Agents paying more than $40 usually won’t be successful Agents under high pressure to sell the customer something

Like to qualify for final expense companies’ lavish trips/conference

Final Expense Agent Characteristics What are the characteristics of a typical agent?

18

“ANTI-SELECTION” Agent misconduct can steer the process for their benefit only Applicants can “forget” things when disclosing on the application Non-disclosure by the agent or applicant causes problems in this

market

Final Expense Challenges Challenges of the Final Expense Market

19

Agents know the companies that don’t do Rx, MIB, or do Tele-interviews or that have “holes” in their application. Sell to clients based on this knowledge

Company advanced large commissions to the agents and agents don’t pay the company for chargebacks

Non-disclosure or coaching applicant to get the insurance which means policy often rescinded at claim time. Can lead to reputation risk for the writing company

Sell too high of premium the customer can’t afford leads to not taken policies and high lapses

Final Expense Challenges Agent examples of anti-selection or not writing good business:

20

Applicants will lie about medications they are on or conditions they have

Can stack policies if passed underwriting before and can afford more coverage

Final Expense ChallengesApplicants Anti-selection

21

1. Agents Contracted2. Agent Commissions3. Application4. Underwriting Used5. Underwriting Process6. Billing for Final Expense7. Claims Adjudication 8. Administration and Tracking

Final Expense Management Management of Final Expense Business is Critical for its success for a company

22

The predictive nature of credit data is coming to the life insurance market including final expense In our recent company studies, we have determined FCRA compliant

credit data is highly predictive of mortality and lapse The TransUnion TrueRisk Life credit data can be used in the following

ways: Improve mortality results Improve persistency results Improve leads Make more appropriate offers of level death benefit versus modified

Final Expense Innovations Are there any innovations coming to this market?

23

Final Expense business is a growing life insurance market Final Expense business requires close monitoring of your experience

to ensure you meet your pricing assumptions and hit profit targets Most companies who enter the market write unprofitable business at

the beginning before they learn to adjust or tweak their program for improvement

Many companies underestimate mortality for this market when they enter and fail. Seek advice if you are newer to this market

The producers are key to getting a good block of final expense business. Non-disclosure is a big problem in this market

With 100 million people in the US, age 50-80, and 10,000 people turning 65 every day for 15 more years, Final Expense Life Insurance fills a growing need for life insurance in our society

Final Expense Takeways for the US Market Conclusions and Key TakeAways

24

So, we haven’t talked you out of it yet?10 Key Steps to Getting Started!

Jeffrey S. Shaw, CLU, ChFCExecutive Director

Life Insurers Council

1). Know your distribution

You need a partnership – even if it’s not 50 – 50 Communicate and agree upfront about pricing

assumptions and performance expectations Understand your place in their briefcase – it may not be

the reason you think (or the one they tell you)

2). Know your product’s place in the final expense universe

Spreadsheet your product BEFORE they do Distribution and competition is changing all the time –

your position will change, too Even good agents (especially good agents) can anti-

select

3). You won’t get it right the first time

And fixing it won’t be as simple as tweaking rates and comp

4). Grow Slowly

Fast growth is easy – controlled growth is hard It takes time for problems to become apparent – do you

prefer big problems or small problems? Manage your capital proactively

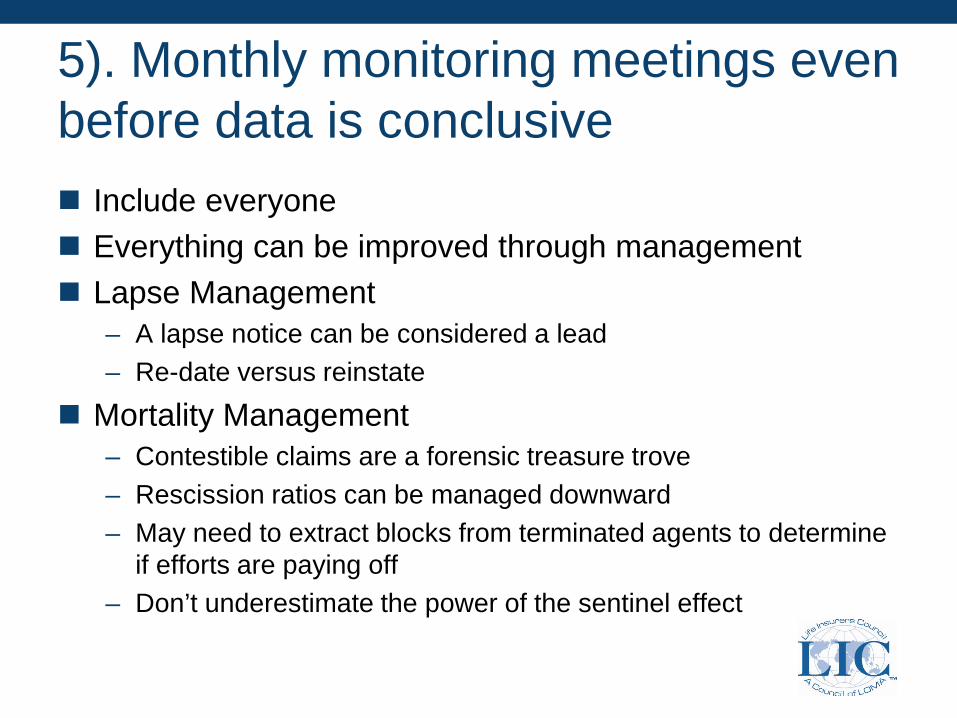

5). Monthly monitoring meetings even before data is conclusive Include everyone Everything can be improved through management Lapse Management

– A lapse notice can be considered a lead– Re-date versus reinstate

Mortality Management– Contestible claims are a forensic treasure trove– Rescission ratios can be managed downward– May need to extract blocks from terminated agents to determine

if efforts are paying off– Don’t underestimate the power of the sentinel effect

6). Monthly field management meetings Field Management

– Actual to Expected results on an agent, GA, and IMO level– Bad agents are rarely black and white – need clearly defined

standards and stick to them– But ratios alone can also be misleading– Identifying good agents is just as important as the bad

Agents Guide – they won’t read it but you can refer to it– What’s the definition of treatment?

Watch your contracting costs -- Lots of agents do not equal lots of sales but they do equal lots of expense

Spend time in the field with agents – their world is NOT your world

7). Don’t reinvent the wheel

Start where everyone is moving to/has moved to– Phone interviews– RX database– Paperless– Voice/e-signature– Direct express/nth day billing

8). Take advantage of available resources

CSG Actuarial Competiscan Life Insurers Council (LIC) Milliman Trans Union Credit/Mortality Prediction

9). Consider some differentiating options

Riders/Alternative products Cross selling inforce block directly

– Michael Edwards Direct

Lead management– Reduce anti-selection

Creative lead generation– Home Security customers

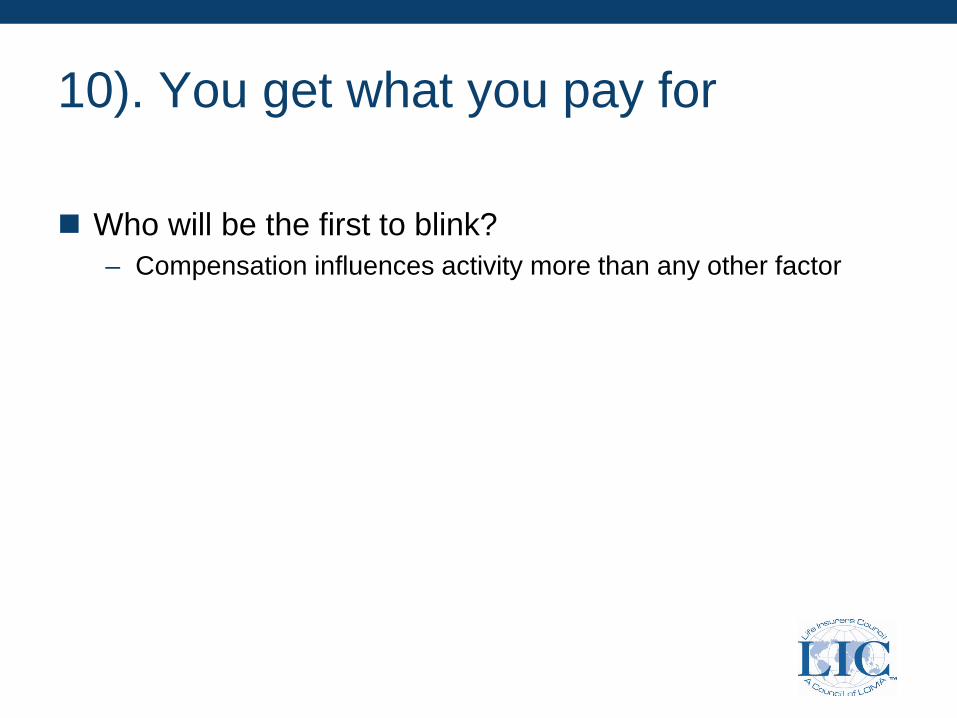

10). You get what you pay for

Who will be the first to blink?– Compensation influences activity more than any other factor

Session 10: Final Expense Insurance 101International Trends

Jing Lang

UK & Ireland

UK & Ireland Age at issue: 50 to 75 or 85 Min/max premium: GBP4/GBP100 per month

Many insurers limit the premium to GBP50 per plan with an overall max of GBP100

Max cover: GBP25k May apply per plan or to all plans Irish max: EUR65k

Inflation protection (or lack thereof)

UK & Ireland Moratorium period: 1 or 2 years Cover during moratorium:

Full face amount on accidental death and 100% to 150% ROP on non accidental death

Cover after moratorium: Full face amount with increase of up to 2X cover on

accidental death

UK & Ireland Premium payment

Sex and/or smoking status distinct rates Level premium based on age at issue Payable WL or limited to a max term (i.e. 30) and/or a

max age (i.e. 90) WL premium have been criticized as some lives will pay

significantly more in premium than the benefit

UK & Ireland Distribution:

Telephone, online, direct mail Tesco, post offices Newspaper/magazine adverts

Marketing: mostly direct through TV and internet Use of popular and well respected figures

Sir Michael Parkinson (AXA Sun Life) Cillia Black (Liverpool Victoria)

UK & Ireland

UK & Ireland Additional options:

Funeral Benefit Option Protected Payout Option Accidental Serious Injury Rider

UK & Ireland Reinsurance:

Net premium or YRT basis Reinsurance premium can follow the office premium

payment pattern or cease reinsurance cover when the office premium ceases

Can be structured so reinsurer is not on risk for the ROP during moratorium period

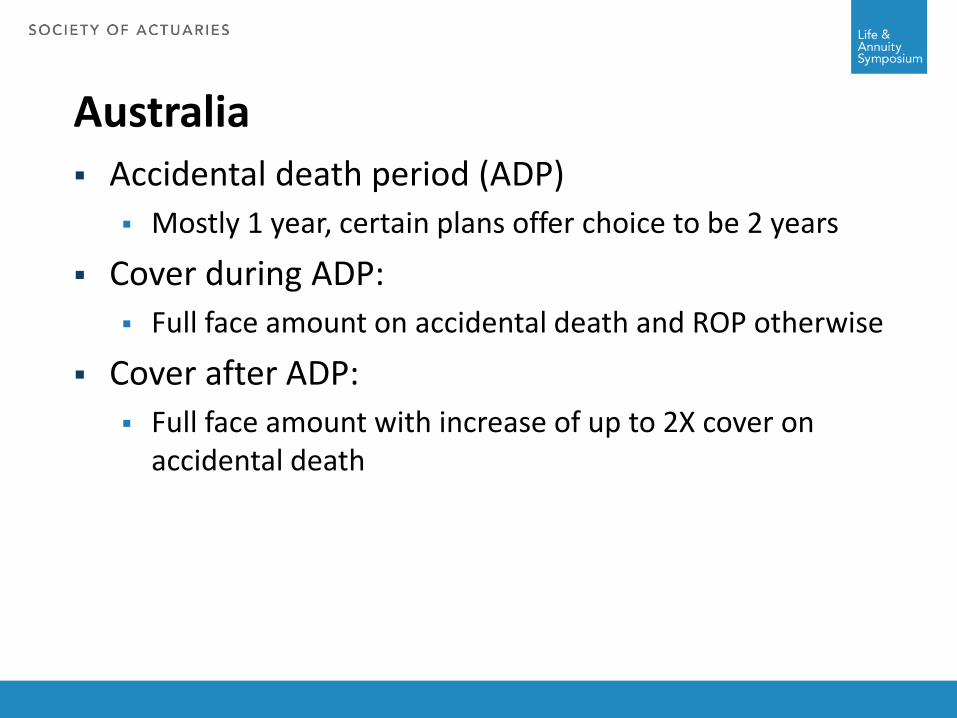

Australia

Australia Age at issue: 18 to 79, some specify 50 to 75 Max coverage: AUD30k

Lower limit if choose level premium

Coverage period: life Some pay cover at a certain age (90) if still alive

Forms of plan: Single, joint, or family Max benefit applies

Australia Accidental death period (ADP)

Mostly 1 year, certain plans offer choice to be 2 years

Cover during ADP: Full face amount on accidental death and ROP otherwise

Cover after ADP: Full face amount with increase of up to 2X cover on

accidental death

Australia Automatic indexation

Cover increases by 5% to 10% each year Up to a certain age (say 80) Premium will increase accordingly Automatic increase if do not decline

Premium Age-based or level Payable until age 85 or 90 Payable annual, monthly, fortnightly

Australia 30 day money back guarantee Value promise Marketing

Much more aggressive advertising than UK

Australia

Australia Additional options:

Early Payment Benefit Premium Pause Benefit 10% Cash Back Benefit Premium Freeze Benefit Paid Up Value feature Accidental Serious Injury Rider

Canada

Canada Age at issue: 40 to 85 Range of coverage: CAD1k to 50k Simplified underwriting with no medical exams Many claim to have no waiting period Accidental death provide 4X cover Premium

Guaranteed and payable till age 100 (for life) Payable annual or monthly

Canada Indexation is optional

Subject to a lower cover limit

Additional features Living benefit at no additional cost Accidental fracture rider Dividend and/or cash value

Distribution: similar to US, mostly sold by agents

Summary Similarities and differences between markets:

underwriting premium coverage & indexation additional benefits and/or options distribution and marketing

End of session

Q&A