session ii: innovative islamic structures: catalysts for...

TRANSCRIPT

© INCEIF 2012.

Islamic Finance A Catalyst for Inclusive Growth & Sustainable Development

Session II: Innovative Islamic Structures: Catalysts for

Economic Development and Sustainability.

Obiyathulla Ismath Bacha

World Bank, Washington DC 18th April 2013

© INCEIF 2012.

Intended Outcomes:

• Show how Islamic Finance based on Risk Sharing can change the Debt/ Equity tradeoff, effectively making Debt less attractive.

• Present emergent risk sharing structures for

funding development without the vulnerability typical of conventional finance.

2

© INCEIF 2012.

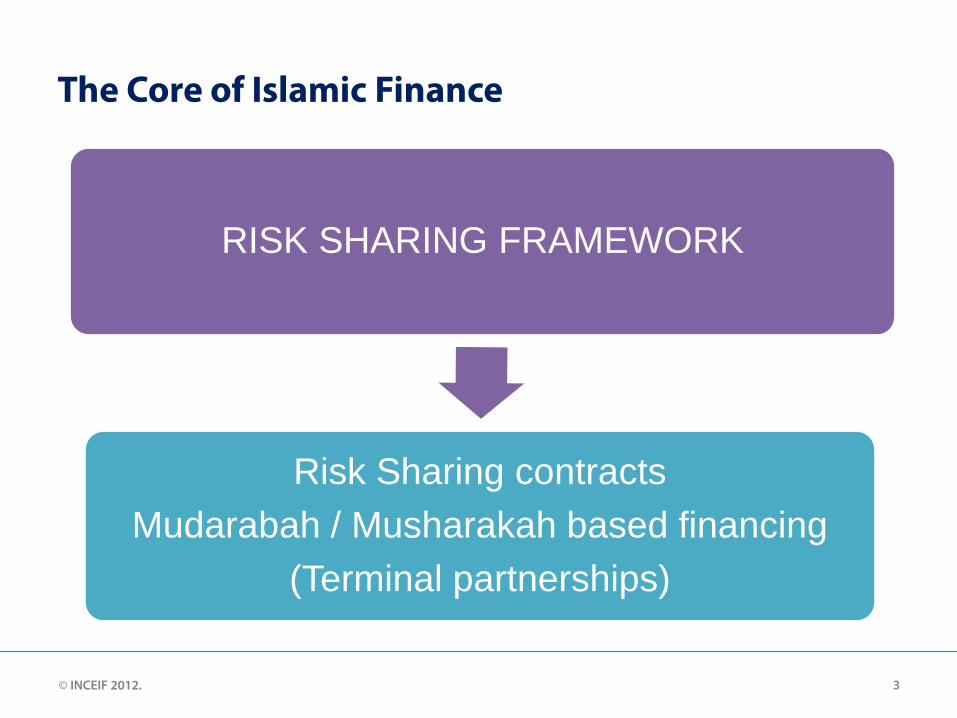

The Core of Islamic Finance

RISK SHARING FRAMEWORK

Risk Sharing contracts Mudarabah / Musharakah based financing

(Terminal partnerships)

3

© INCEIF 2012.

The tradeoff between Debt and Equity

If issue debt

• Increase leverage, BEP • Increase volatility of

returns

If issue new

equity

• Less risky than debt but dilution of ownership / earns.

4

© INCEIF 2012.

The tradeoff between Debt and Equity

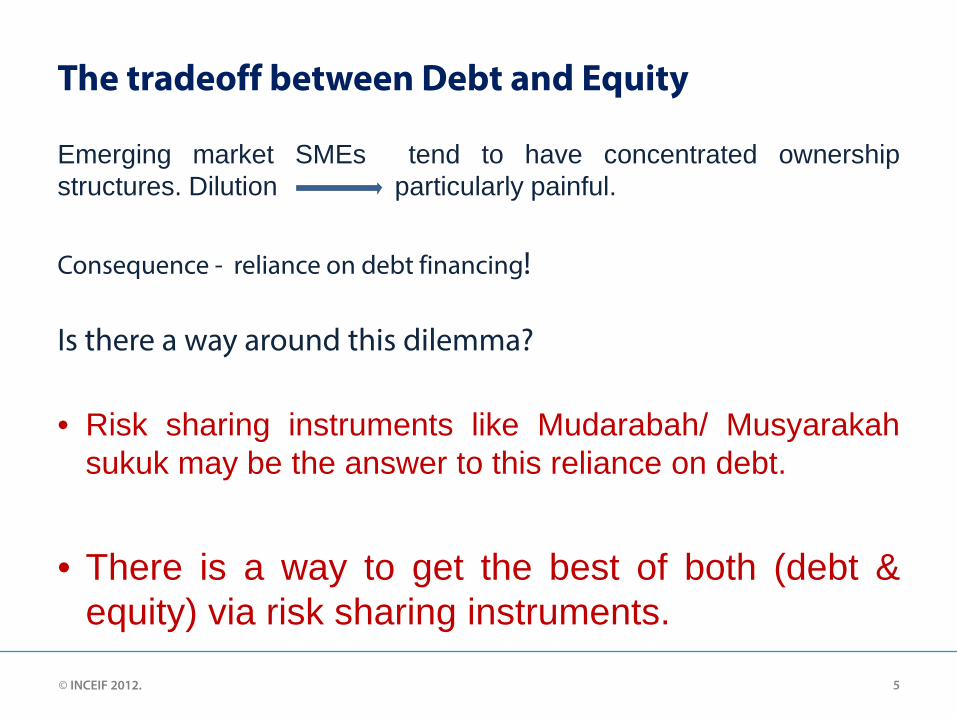

Emerging market SMEs tend to have concentrated ownership structures. Dilution particularly painful.

Consequence - reliance on debt financing! Is there a way around this dilemma?

• Risk sharing instruments like Mudarabah/ Musyarakah sukuk may be the answer to this reliance on debt.

• There is a way to get the best of both (debt &

equity) via risk sharing instruments.

5

© INCEIF 2012.

Risk Sharing Finance - MTF

• MTF (mudarabah type financing), sukuk is a hybrid instrument that has the features of both debt & equity.

• A risk sharing instrument – like equity

• But terminal – like debt.

• Thus, while the equity-like portion would mean dilution, the dilution is limited and not perpetual.

6

© INCEIF 2012.

Risk Sharing Finance relative to debt

• What if shareholders of a firm (SME) choose to fund new needs by way of risk-sharing MTF Sukuk instead of conventional debt or equity?

• As a risk-sharing instrument, sukuk returns based on profits/losses.

• No fixed claim on the company’s cash flow. • No increase in the firm’s break-even point.

7

© INCEIF 2012.

Risk Sharing Finance – relative to debt

• Nor will there be an increase in the firm’s financial leverage. (no increase in risk!)

• The one-way option that leverage provides, does not

exist. (incentives for moral hazard) • With returns tied to company earnings, financing by way

of MTF sukuk acts as an in-built stabilizer.

• The firm, post sukuk issuance is a more stable entity.

8

© INCEIF 2012.

Risk Sharing Finance – relative to equity

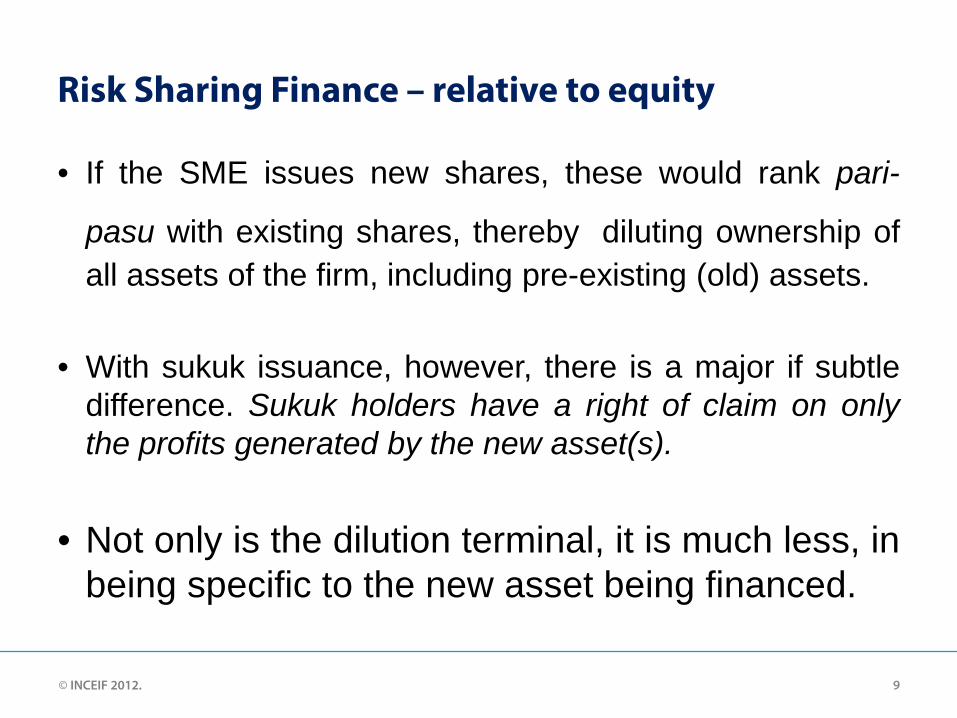

• If the SME issues new shares, these would rank pari-

pasu with existing shares, thereby diluting ownership of all assets of the firm, including pre-existing (old) assets.

• With sukuk issuance, however, there is a major if subtle

difference. Sukuk holders have a right of claim on only the profits generated by the new asset(s).

• Not only is the dilution terminal, it is much less, in being specific to the new asset being financed.

9

© INCEIF 2012.

RSF versus, Debt & Equity

• Note: With RSF, the SME gets the benefit of equity issuance without the dilution!

• Yet, like equity issuance, there is reduced cash flow volatility while financial flexibility is intact.

Implication Reduced risk premiums

10

© INCEIF 2012.

Risk Sharing Finance - MTF

• The company’s equity and debtholders experience a gain in wealth simply because the new sukuk holders come-in to share the risk of the new asset being acquired by the firm.

• The gains experienced here are real and do not

come at the expense of others.

11

© INCEIF 2012. 12

© INCEIF 2012.

Emerging Sukuk Structures

• Of late, there have been proposals to have sukuk that are based not only on the performance of a single underlying asset but on such things as GDP growth, a price index of a nation’s export commodities and the like.

• Linking sukuk returns to GDP performance is not unlike the proposal for “Trills” that have been made in the conventional space.

13

© INCEIF 2012.

Emerging Sukuk Structures

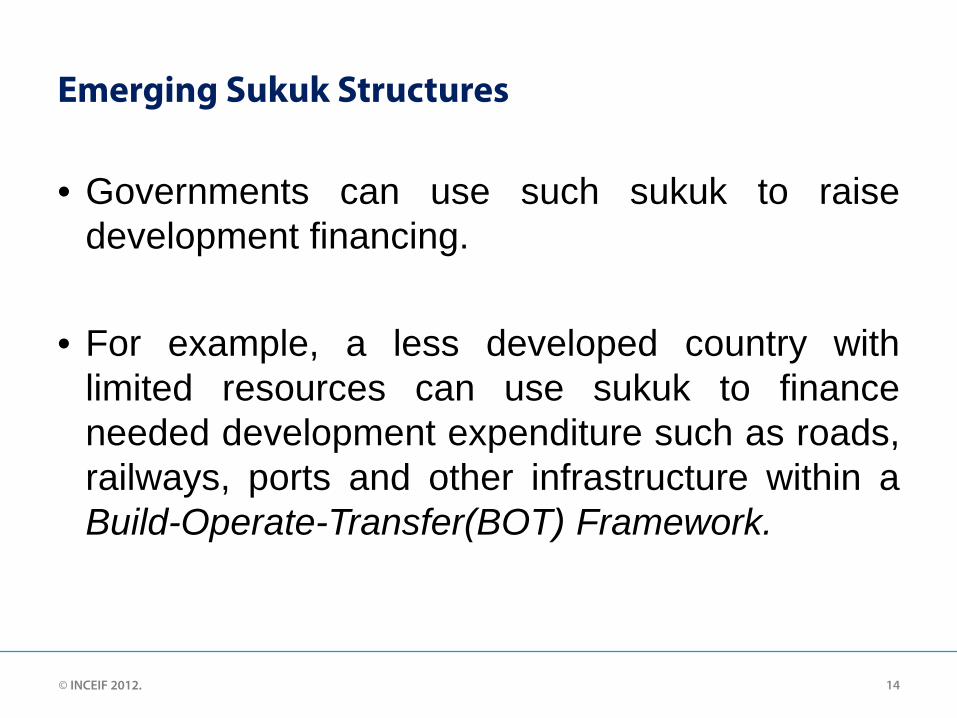

• Governments can use such sukuk to raise development financing.

• For example, a less developed country with

limited resources can use sukuk to finance needed development expenditure such as roads, railways, ports and other infrastructure within a Build-Operate-Transfer(BOT) Framework.

14

© INCEIF 2012.

Emerging Sukuk Structures

• A needed highway project could be undertaken by issuing sukuk whose returns during the period of construction is a percentage tied to export earnings of the country and on completion would get returns which are a percent of toll collected over say, the subsequent 30 years.

• Such a risk-sharing instrument, aside from avoiding any economic vulnerability to the issuer has the added advantage of removing the bottleneck of limited funds.

15

© INCEIF 2012.

Emerging Sukuk Structures

• The government suffers no loss of ownership of the asset financed.

• Currency risk could also be shared by denominating returns in the main currency of the issuing country’s export earnings. Post construction, return could be in the home currency of the issuer.

• The percent of profit due to the sukuk holders should obviously depend on all risks, including currency.

16

© INCEIF 2012.

Emerging Sukuk Structures

• Several other variants of the sukuk structure above are also possible.

• Financing of projects which are highly capital intensive and require extensive upfront investments like, power generation plants, Intra City Mass Rapid Transit (MRT) systems and the like have always been problematic for developing countries.

17

© INCEIF 2012.

Emerging Sukuk Structures

• Given infantile and shallow domestic capital markets, such projects have typically been financed largely with debt usually foreign sourced. But, two inherent problems

• First, Currency mismatch

• Second, due to the long gestation period for these projects and the

compounding nature of debt, the projects come on stream carrying a massive debt overload.

• The usual result, either perpetual subsidy from the government or nationalization, which then shifts the debt burden to the government.

18

© INCEIF 2012.

Emerging Sukuk Structures

• It is precisely projects of this nature that would be well suited for sukuk based financing.

• An MRT system that typically requires several years of construction but would provide stable cash flow for a long period subsequently, could be financed with sukuk that pays nothing in the initial years but converts into a profit sharing instrument for say the subsequent 30 years could still be a very attractive investment.

19

© INCEIF 2012.

Emerging Sukuk Structures

• The advantage is that such financing would place no strain on government budgets but gets development going.

• Post 30 years the government owns a very lucrative asset that it “never paid for” but only facilitated.

20

© INCEIF 2012.

Emerging Sukuk Structures

Many other alternative structures are possible. • Perpetual sukuk - to meet Basle Tier 1Capital Ratios. • Sukuk with Embedded options – - overcome information asymmetries. - to avoid fixity “Spanning” can allow for any number of variations, provided they conform with stipulations of the shariah.

21

© INCEIF 2012.

Concluding Remarks • The risk-sharing framework obviously has much promise, especially

for the development financing of poorer/less developed countries.

What Risk Sharing promises; - a changed trade off profile – making debt “less” attractive

- broader participation of the population in development (divisibility) - dissipation of risk, thereby minimizing macro economic vulnerability. - returns that are anchored on real asset returns (uncluttered by leverage) - a new asset class of instruments, being asset based, would have returns uncorrelated with other asset classes.

22

© INCEIF 2012.

What’s needed

• Aside from a need to modify some of the contracts (shariah issues), Islamic finance being rooted in trust and goodwill, would require the strengthening of governance structures.

23