severance plans and erisa compliance: limiting liability...

TRANSCRIPT

Severance Plans and ERISA Compliance:

Limiting Liability in Design and

Implementation of Severance Arrangements

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

TUESDAY, JUNE 12, 2018

Presenting a live 90-minute webinar with interactive Q&A

Kenneth J. Laverriere, Partner, Shearman & Sterling, New York

Cydni Waldner, Of Counsel, Hawley Troxell, Boise, Idaho

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-258-2056 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address

the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 2.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

SEVERANCE PLANS: ERISA AND SECTION 409A COMPLIANCE

KENNETH J. LAVERRIEREPARTNER AT SHEARMAN & STERLING [email protected]

CYDNI WALDNEROF COUNSEL AT HAWLEY [email protected]

June 12, 2018

6Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• ERISA framework

• Pension vs. welfare plans

• Severance arrangements vs. plans

• Issues, benefits and burdens of ERISA compliance

• Application of Section 409A of the IRC to severance plans

• Overview

• Application to severance plans

• Exceptions

• Compliance

TOPICS

7Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

APPLICATION OF ERISA TO SEVERANCE ARRANGEMENTS

Shearman & Sterling LLP 8Presentation and Pitch Template Instructions

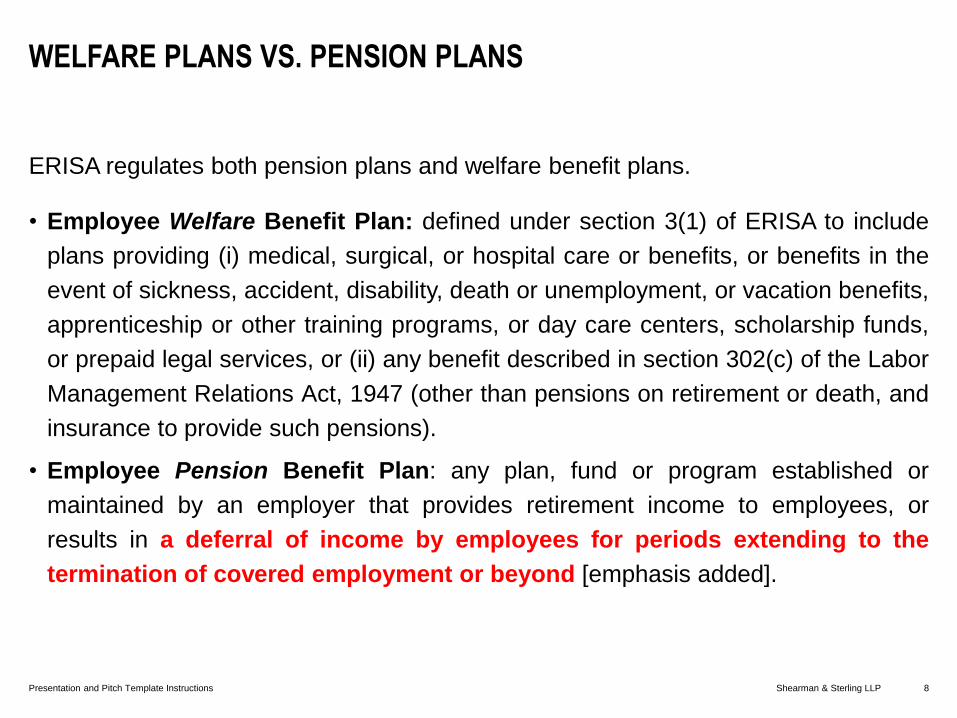

• Employee Welfare Benefit Plan: defined under section 3(1) of ERISA to include

plans providing (i) medical, surgical, or hospital care or benefits, or benefits in the

event of sickness, accident, disability, death or unemployment, or vacation benefits,

apprenticeship or other training programs, or day care centers, scholarship funds,

or prepaid legal services, or (ii) any benefit described in section 302(c) of the Labor

Management Relations Act, 1947 (other than pensions on retirement or death, and

insurance to provide such pensions).

• Employee Pension Benefit Plan: any plan, fund or program established or

maintained by an employer that provides retirement income to employees, or

results in a deferral of income by employees for periods extending to the

termination of covered employment or beyond [emphasis added].

WELFARE PLANS VS. PENSION PLANS

ERISA regulates both pension plans and welfare benefit plans.

9Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Reporting

• Disclosure

• Fiduciary/prohibited transaction rule

• Claim procedures

REQUIREMENTS GENERALLY APPLICABLE TO ALL PLANS

10Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Minimum participation standards

• Minimum funding requirement

• Vesting requirements

PENSION BENEFIT PLANS ARE SUBJECT TO SPECIAL REQUIREMENTS

11Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

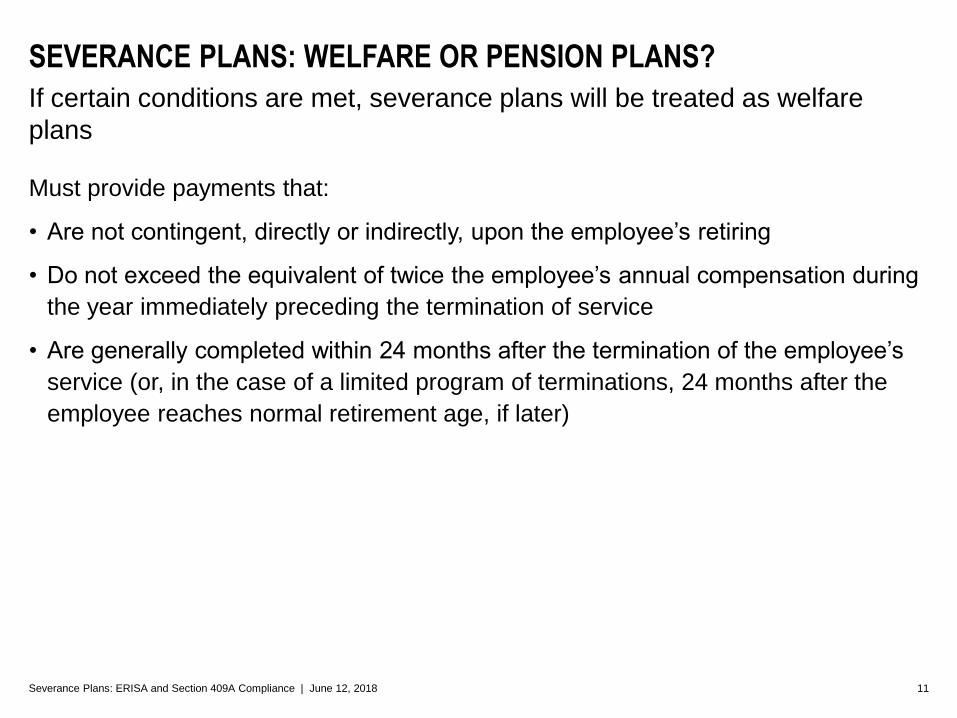

Must provide payments that:

• Are not contingent, directly or indirectly, upon the employee’s retiring

• Do not exceed the equivalent of twice the employee’s annual compensation during

the year immediately preceding the termination of service

• Are generally completed within 24 months after the termination of the employee’s

service (or, in the case of a limited program of terminations, 24 months after the

employee reaches normal retirement age, if later)

SEVERANCE PLANS: WELFARE OR PENSION PLANS?

If certain conditions are met, severance plans will be treated as welfare

plans

12Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

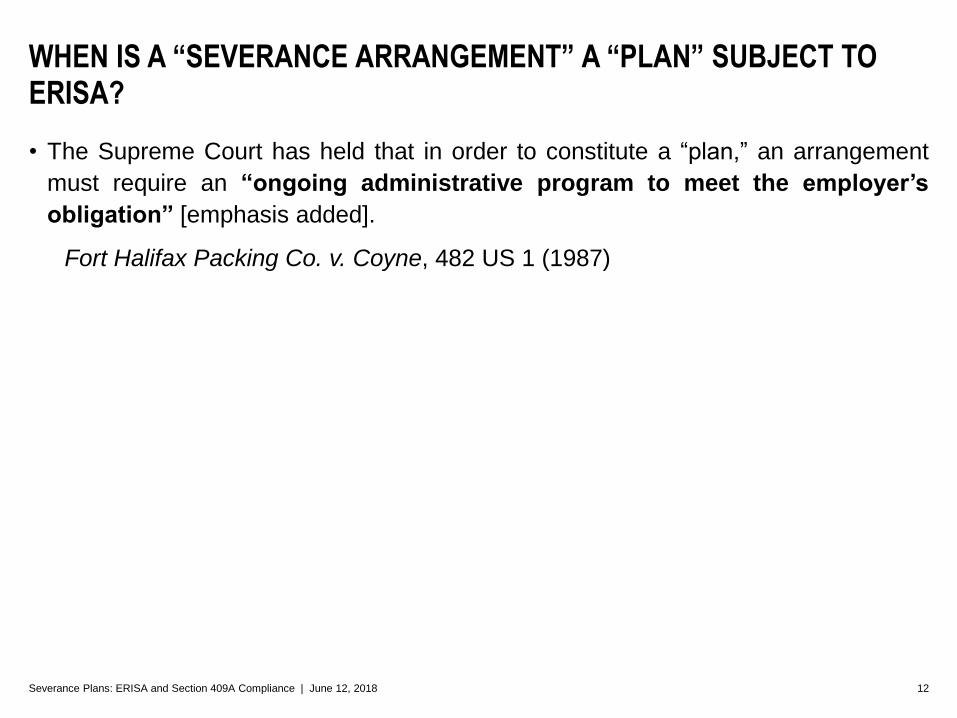

• The Supreme Court has held that in order to constitute a “plan,” an arrangement

must require an “ongoing administrative program to meet the employer’s

obligation” [emphasis added].

Fort Halifax Packing Co. v. Coyne, 482 US 1 (1987)

WHEN IS A “SEVERANCE ARRANGEMENT” A “PLAN” SUBJECT TO ERISA?

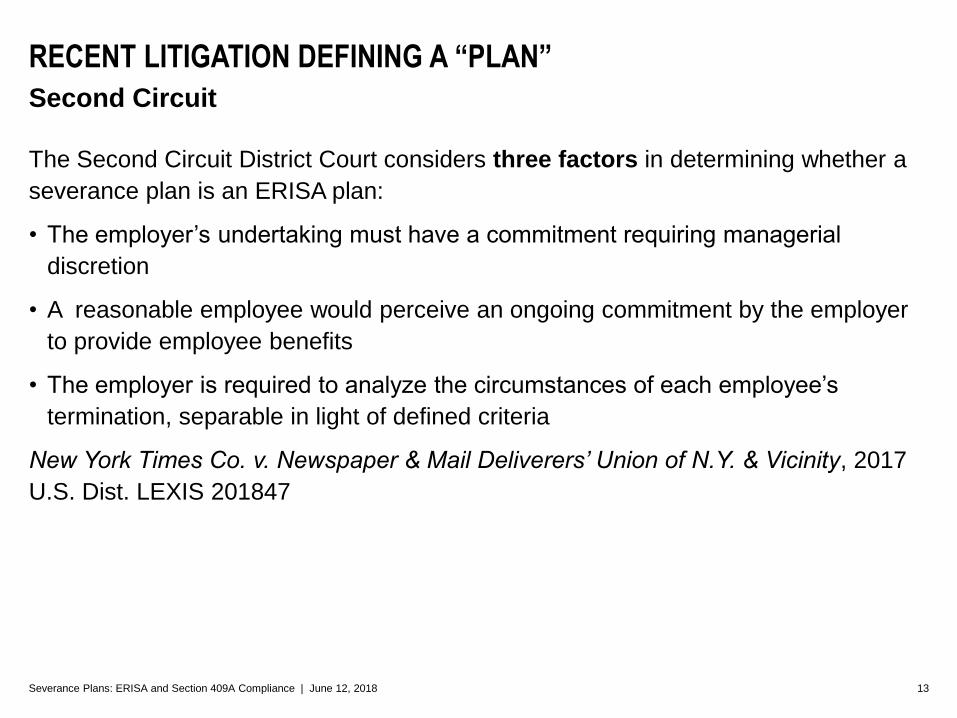

13Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

The Second Circuit District Court considers three factors in determining whether a

severance plan is an ERISA plan:

• The employer’s undertaking must have a commitment requiring managerial

discretion

• A reasonable employee would perceive an ongoing commitment by the employer

to provide employee benefits

• The employer is required to analyze the circumstances of each employee’s

termination, separable in light of defined criteria

New York Times Co. v. Newspaper & Mail Deliverers’ Union of N.Y. & Vicinity, 2017

U.S. Dist. LEXIS 201847

RECENT LITIGATION DEFINING A “PLAN”

Second Circuit

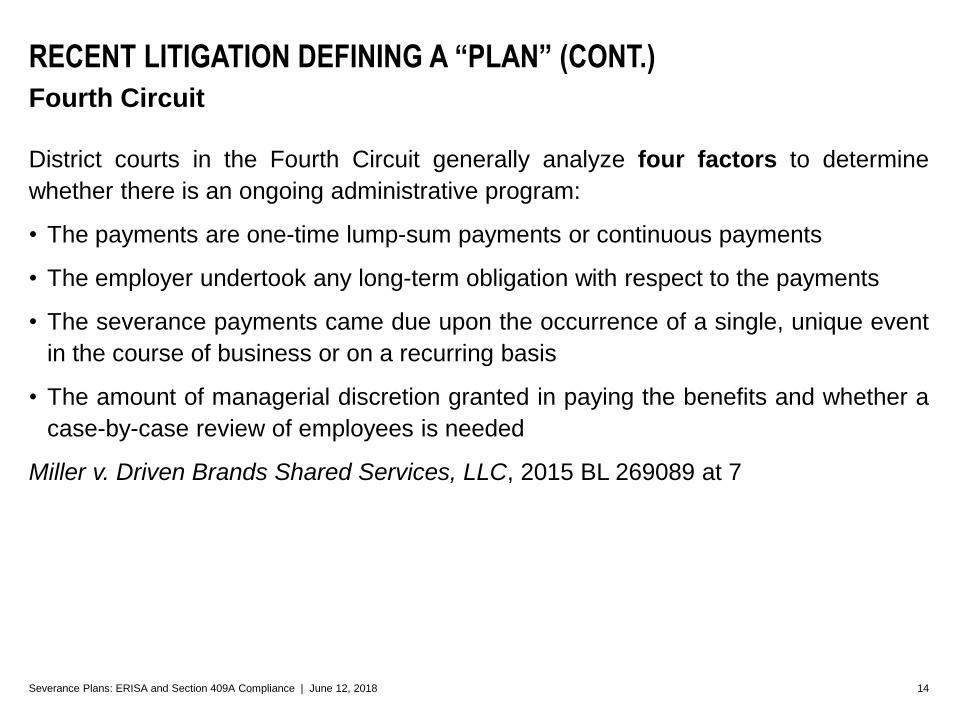

14Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

District courts in the Fourth Circuit generally analyze four factors to determine

whether there is an ongoing administrative program:

• The payments are one-time lump-sum payments or continuous payments

• The employer undertook any long-term obligation with respect to the payments

• The severance payments came due upon the occurrence of a single, unique event

in the course of business or on a recurring basis

• The amount of managerial discretion granted in paying the benefits and whether a

case-by-case review of employees is needed

Miller v. Driven Brands Shared Services, LLC, 2015 BL 269089 at 7

RECENT LITIGATION DEFINING A “PLAN” (CONT.)

Fourth Circuit

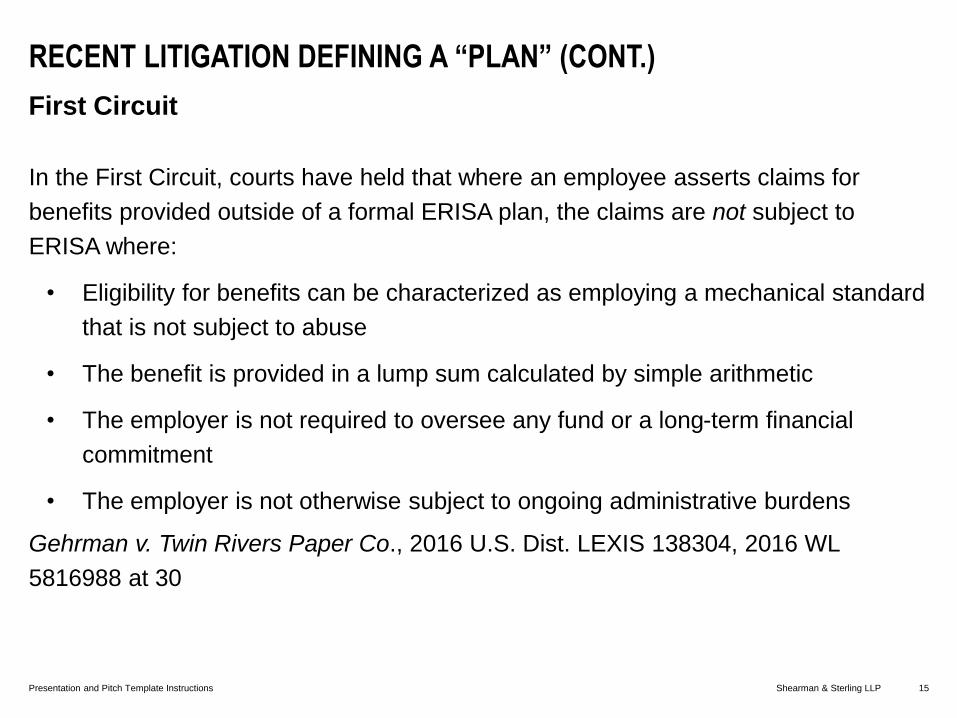

Shearman & Sterling LLP 15Presentation and Pitch Template Instructions

In the First Circuit, courts have held that where an employee asserts claims for

benefits provided outside of a formal ERISA plan, the claims are not subject to

ERISA where:

• Eligibility for benefits can be characterized as employing a mechanical standard

that is not subject to abuse

• The benefit is provided in a lump sum calculated by simple arithmetic

• The employer is not required to oversee any fund or a long-term financial

commitment

• The employer is not otherwise subject to ongoing administrative burdens

Gehrman v. Twin Rivers Paper Co., 2016 U.S. Dist. LEXIS 138304, 2016 WL

5816988 at 30

RECENT LITIGATION DEFINING A “PLAN” (CONT.)

First Circuit

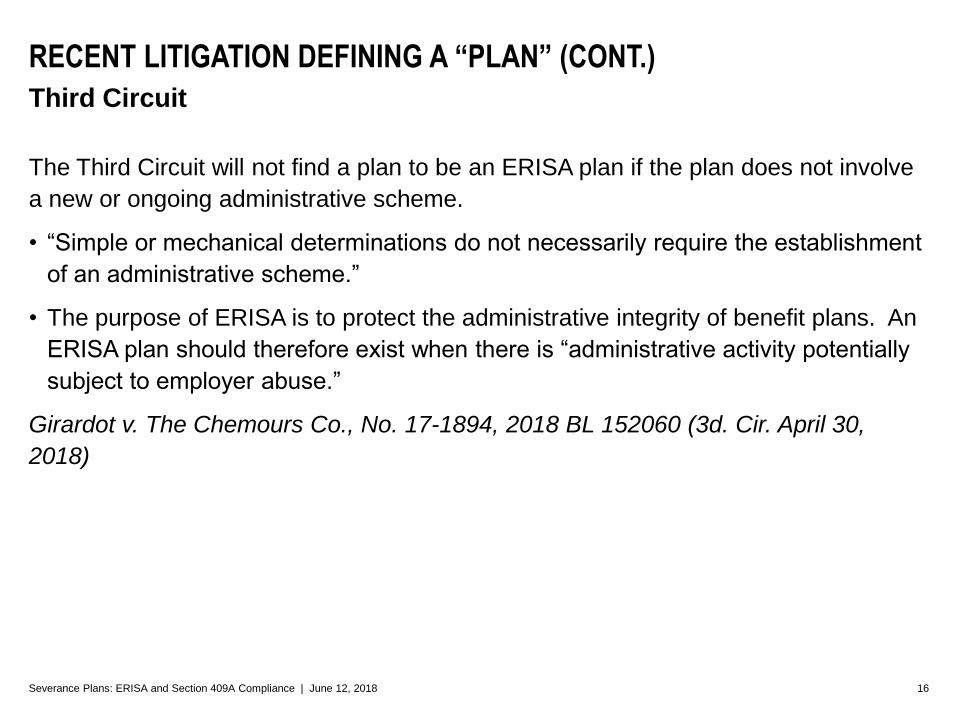

16Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

The Third Circuit will not find a plan to be an ERISA plan if the plan does not involve

a new or ongoing administrative scheme.

• “Simple or mechanical determinations do not necessarily require the establishment

of an administrative scheme.”

• The purpose of ERISA is to protect the administrative integrity of benefit plans. An

ERISA plan should therefore exist when there is “administrative activity potentially

subject to employer abuse.”

Girardot v. The Chemours Co., No. 17-1894, 2018 BL 152060 (3d. Cir. April 30,

2018)

RECENT LITIGATION DEFINING A “PLAN” (CONT.)

Third Circuit

17Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Plans Typically Covered by ERISA:

• Broad-based severance plans

• Detailed policy statements (although often times they are not treated as such)

• Plans Not Typically Covered by ERISA:

• Employment agreements (unless there are many agreements)

• Individual separation agreements

• Non-binding statements of intent in personnel policies

TYPES OF SEVERANCE PLANS

18Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• A formal document plan and a summary plan description (“SPD”)

• Distribution of the SPD and other documents to participants, reflecting the plan in a

clear manner so as to be understood by the average participant

• A Form 5500 annual report must be filed with the Department of Labor within seven

months of the close of the plan year

• Adherence to a formal claims procedure

KEY REQUIREMENTS A SEVERANCE ARRANGEMENT MUST SATISFY IF IT IS CONSIDERED A “WELFARE PLAN” GOVERNED BY ERISA

19Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Plan must include a statement of ERISA rights

• Plan must be administered in accordance with ERISA’s fiduciary obligations

• Summary Annual Report must be furnished to plan participants within nine months

of the close of the plan year

Exception: Any employee benefit welfare plan that has fewer than 100 employees

at the start of the plan year is exempt from the Form 5500 requirement, as well as

Summary Annual Report requirement.

KEY REQUIREMENTS A SEVERANCE ARRANGEMENT MUST SATISFY IF IT IS CONSIDERED A “WELFARE PLAN” GOVERNED BY ERISA (CONT.)

20Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

Broad-based welfare plans are subject to ERISA’s fiduciary, reporting and disclosure

requirements, as discussed. This imposes an obvious burden on employers to meet

those requirements.

• Compliance with these requirements minimizes the regulatory risk that an

arrangement styled as a “severance policy” may not be in compliance with

ERISA.

• ERISA preempts state laws, and therefore limits the types of claims that can be

brought against an employer in respect of a severance plan.

• ERISA generally limits claims by employees to claims for benefits and breaches

of fiduciary duty.

ISSUES, BENEFITS AND BURDENS OF HAVING A PLAN SUBJECT TO ERISA

21Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• ERISA participants are required to exhaust a claims and appeals procedure

before filing a lawsuit.

• Courts generally defer to the decision of the plan administrator following a proper

review of a claim.

• In addition, the evidence presented to the court is typically limited to the evidence

presented to the plan administrator.

ISSUES, BENEFITS AND BURDENS OF HAVING A PLAN SUBJECT TO ERISA (CONT.)

22Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• ERISA litigation is usually decided by a judge, not a jury.

• A reasonable statute of limitations can be included to limit the time period in

which a participant may file a suit.

• The plan document can generally dictate which state’s law applies (to the extent

a portion of the plan is not preempted by ERISA).

• The plan document can provide maximum discretion to determine eligibility and

to calculate benefits.

ISSUES, BENEFITS AND BURDENS OF HAVING A PLAN SUBJECT TO ERISA (CONT.)

23Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Although ERISA contemplates both a plan document and a summary plan

description, “plan sponsors commonly use a single document to satisfy both

requirements, and courts have blessed the practice” (See Rhea v Alan Ritchey, Inc.

Welfare Plan, 858 F.3d 340 at 344 (5th Cir. 2017).)

• Determine whether you can take advantage of the exception from certain filings

and deliverables for smaller plans.

• Consider including the severance policy as part of a “wrap-around” employee

welfare benefit plan which would require the filing of only one Form 5500.

• Ensure your plan documents include the required claims procedure and statement

of ERISA rights.

TIPS TO SIMPLIFY ERISA COMPLIANCE

24Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

If your severance arrangement qualifies as an ERISA plan, and you do not comply

with ERISA requirements, you will be subject to penalties, which include, without

limitation:

• criminal penalties for wilful violation of reporting and disclosure requirements (29

USC § 1131)

• civil penalties for failure to provide notice, or failure to implement regulations, for

each day for which failure continues (29 USC § 1452)

• civil penalties for failure or refusal to file the annual report (29 USC § 1132)

FAILURE TO COMPLY WITH ERISA REQUIREMENTS

25Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• WARN Act: If the Company must provide 60 days notice due to a plant closing or

mass layoff, severance amounts may be reduced by required notice (but not the

reverse)

• State Laws: Many states have laws similar to WARN

• Amendment and Termination: Provide the plan administrator with the maximum

amount of discretion to amend and/or terminate the plan

• Clawback Policies: Ensure amounts payable under the plan are subject to any

company clawback or recoupment policy

• Release of Claims: Require plan participants to execute a release of claims prior

to receiving any severance

ADDITIONAL CONSIDERATIONS

Plan Provisions to Consider

26Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

APPLICATION OF SECTION 409A OF IRC TO SEVERANCE ARRANGEMENTS

27Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Enacted as part of the American Jobs Creation Act of 2004

• Covers “non-qualified deferred compensation”

• Amounts for which a legally binding right exists in one year and payment

could occur in a future year

• “Legally binding right”

• Covers “service providers”; broader than just employees

SECTION 409A BACKGROUND

28Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Non-qualified and deferred compensation plans:

• Must be in writing

• May only pay out upon certain specified distribution events

• Must restrict acceleration of payment

• Must comply with timing of deferral elections

SECTION 409A COMPLIANCE

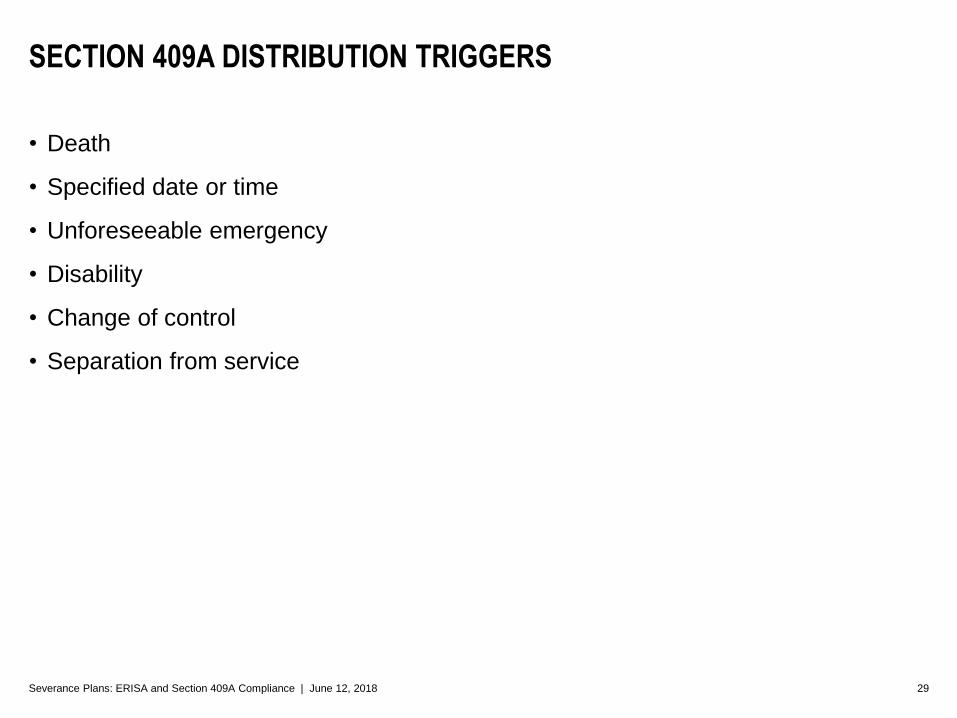

29Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Death

• Specified date or time

• Unforeseeable emergency

• Disability

• Change of control

• Separation from service

SECTION 409A DISTRIBUTION TRIGGERS

30Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

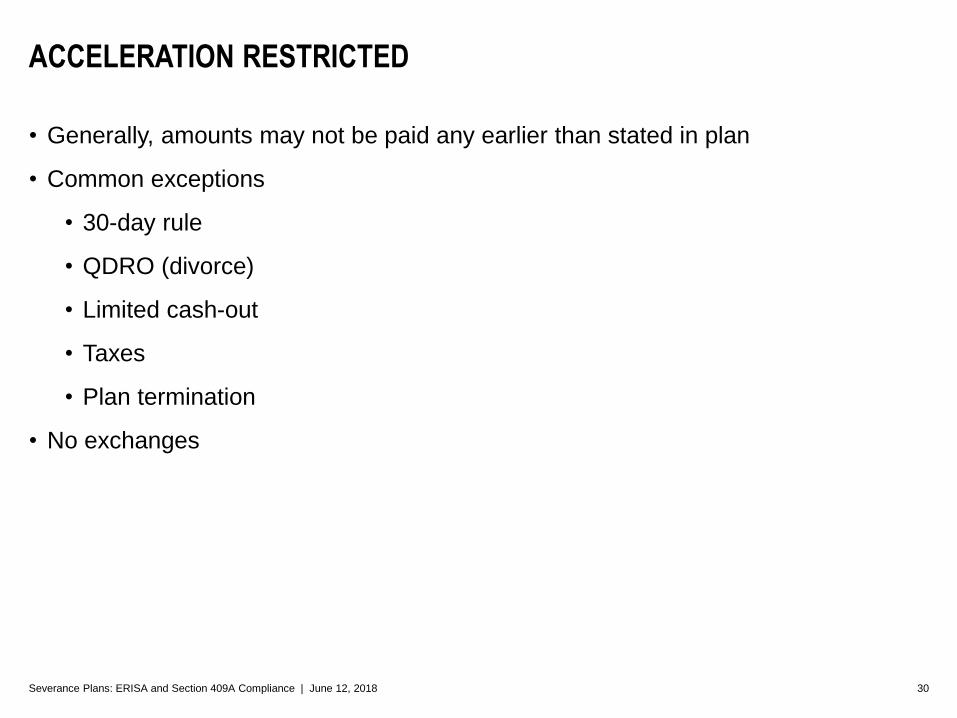

• Generally, amounts may not be paid any earlier than stated in plan

• Common exceptions

• 30-day rule

• QDRO (divorce)

• Limited cash-out

• Taxes

• Plan termination

• No exchanges

ACCELERATION RESTRICTED

31Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

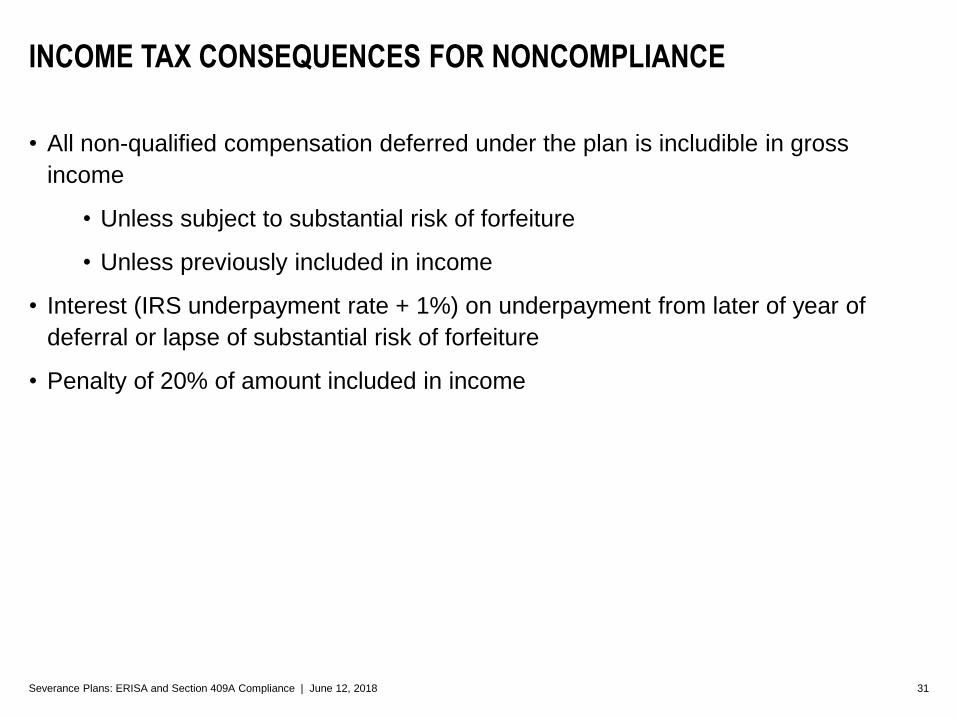

• All non-qualified compensation deferred under the plan is includible in gross

income

• Unless subject to substantial risk of forfeiture

• Unless previously included in income

• Interest (IRS underpayment rate + 1%) on underpayment from later of year of

deferral or lapse of substantial risk of forfeiture

• Penalty of 20% of amount included in income

INCOME TAX CONSEQUENCES FOR NONCOMPLIANCE

32Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

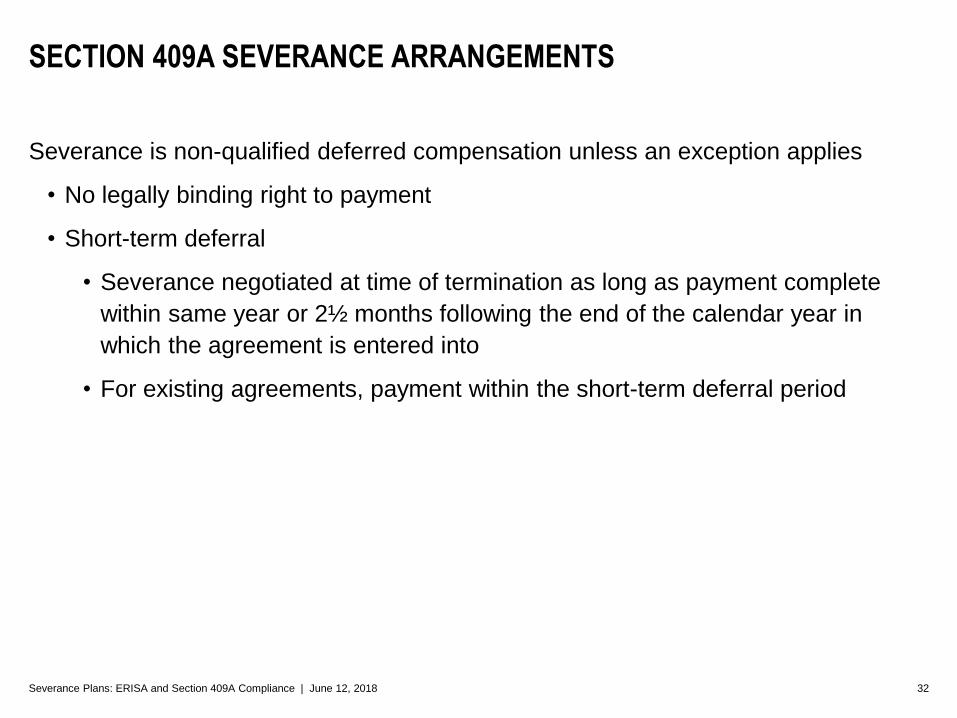

Severance is non-qualified deferred compensation unless an exception applies

• No legally binding right to payment

• Short-term deferral

• Severance negotiated at time of termination as long as payment complete

within same year or 2½ months following the end of the calendar year in

which the agreement is entered into

• For existing agreements, payment within the short-term deferral period

SECTION 409A SEVERANCE ARRANGEMENTS

33Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

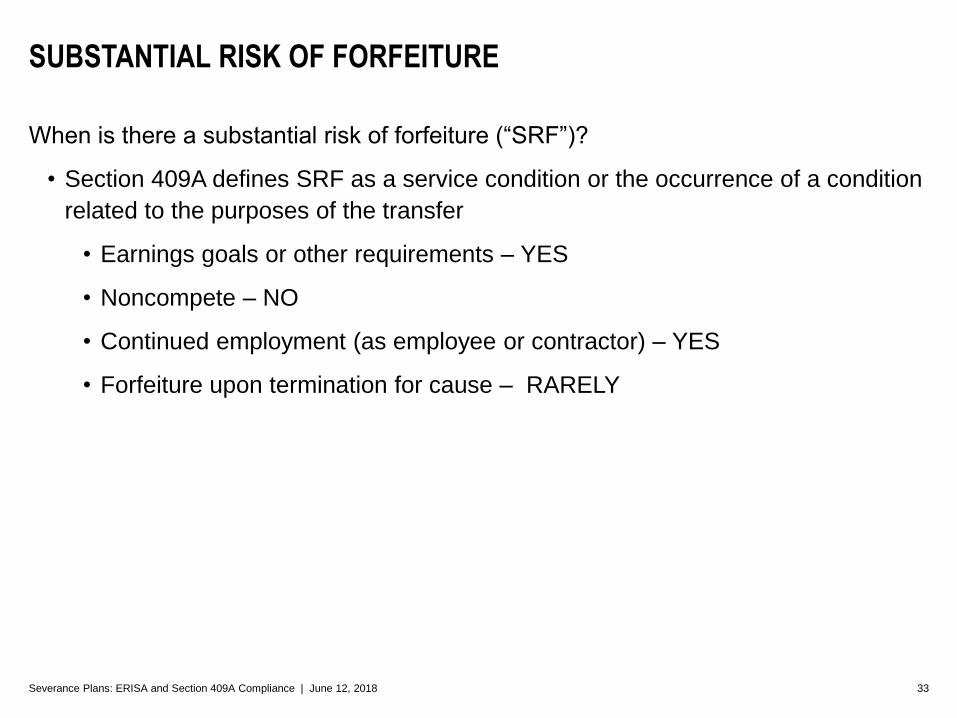

When is there a substantial risk of forfeiture (“SRF”)?

• Section 409A defines SRF as a service condition or the occurrence of a condition

related to the purposes of the transfer

• Earnings goals or other requirements – YES

• Noncompete – NO

• Continued employment (as employee or contractor) – YES

• Forfeiture upon termination for cause – RARELY

SUBSTANTIAL RISK OF FORFEITURE

34Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

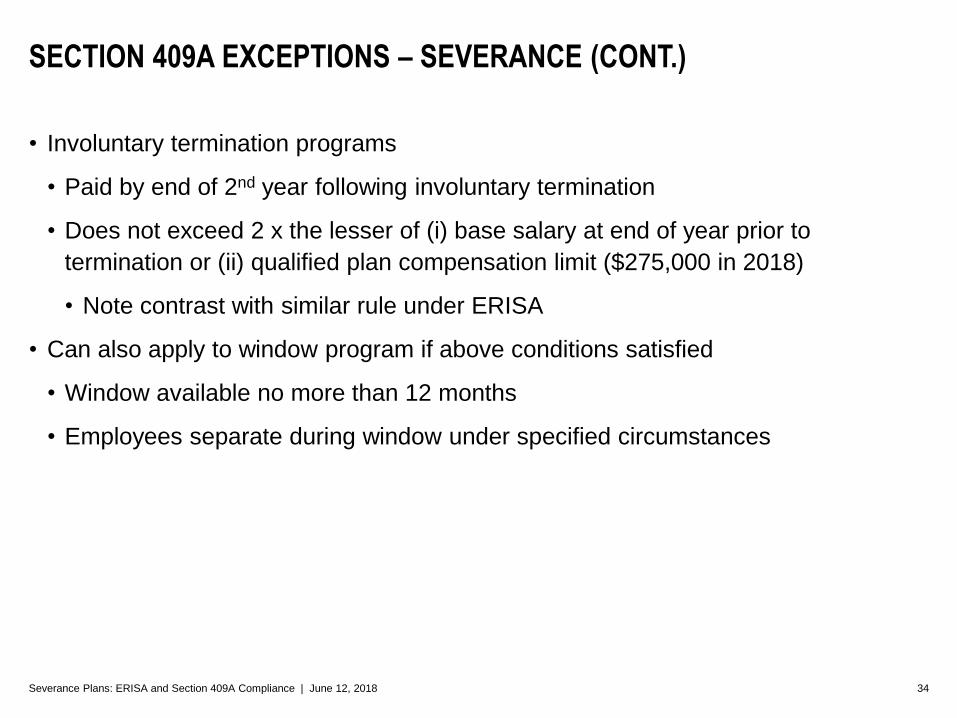

• Involuntary termination programs

• Paid by end of 2nd year following involuntary termination

• Does not exceed 2 x the lesser of (i) base salary at end of year prior to

termination or (ii) qualified plan compensation limit ($275,000 in 2018)

• Note contrast with similar rule under ERISA

• Can also apply to window program if above conditions satisfied

• Window available no more than 12 months

• Employees separate during window under specified circumstances

SECTION 409A EXCEPTIONS – SEVERANCE (CONT.)

35Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

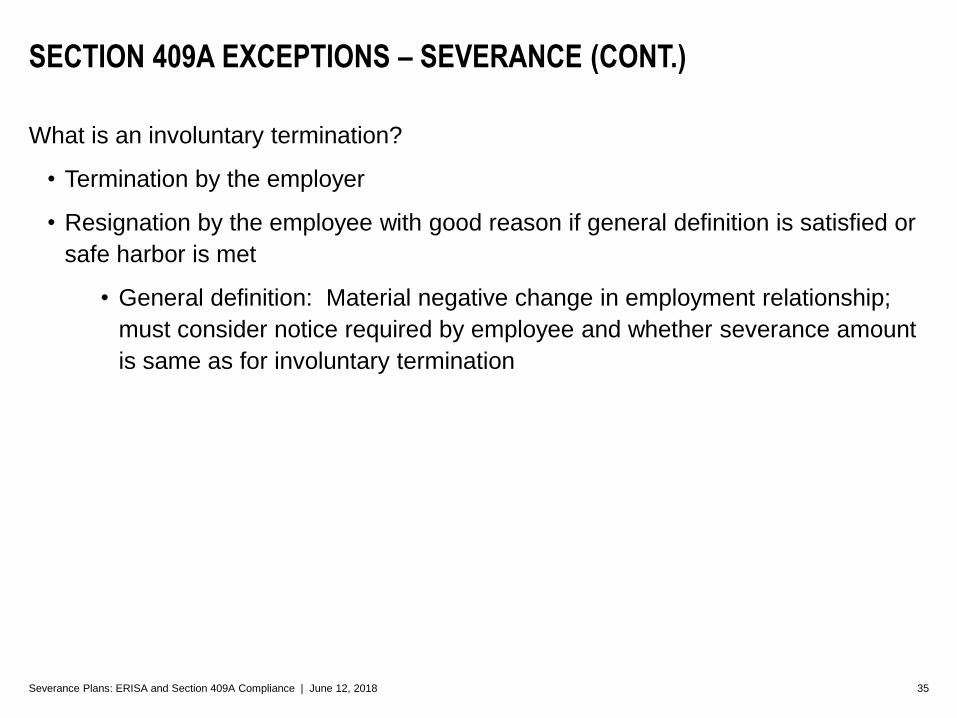

What is an involuntary termination?

• Termination by the employer

• Resignation by the employee with good reason if general definition is satisfied or

safe harbor is met

• General definition: Material negative change in employment relationship;

must consider notice required by employee and whether severance amount

is same as for involuntary termination

SECTION 409A EXCEPTIONS – SEVERANCE (CONT.)

36Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

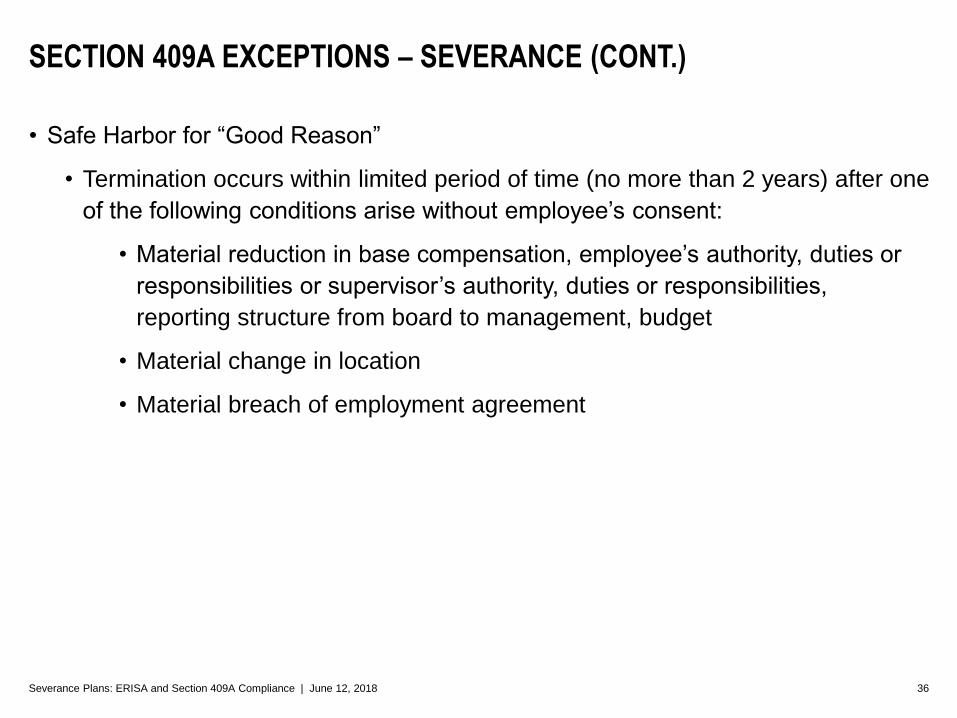

• Safe Harbor for “Good Reason”

• Termination occurs within limited period of time (no more than 2 years) after one

of the following conditions arise without employee’s consent:

• Material reduction in base compensation, employee’s authority, duties or

responsibilities or supervisor’s authority, duties or responsibilities,

reporting structure from board to management, budget

• Material change in location

• Material breach of employment agreement

SECTION 409A EXCEPTIONS – SEVERANCE (CONT.)

37Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Safe Harbor for Good Reason (cont.)

• Amount, timing and form of payment of severance must be substantially identical

to payment made upon involuntary termination

• Employee must give notice of condition within 90 days and employer has 30 days

to cure

SECTION 409A EXCEPTIONS – SEVERANCE (CONT.)

38Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Disputed entitlement

• Lump sum payment in settlement

• Amount cannot exceed 75% of employee’s claim

• Collectively bargained plans

• Severance upon involuntary separation or window program

• Exception only applies to union employees covered by the CBA

SECTION 409A EXCEPTIONS – SEVERANCE (CONT.)

39Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Expense reimbursements

• Amounts employee could otherwise deduct under Code Section 162 or 167

• Reasonable outplacement and moving expenses

• In-kind benefits

• Expense incurred or benefit provided by end of 2nd year following year of

separation

• Reimbursements paid by end of 3rd year following year of separation

SECTION 409A EXCEPTIONS – SEVERANCE (CONT.)

40Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Continued medical coverage and medical reimbursement that is not taxable to

employee

• Potential issue for discriminatory self-insured medical plan

• Continued life and disability coverage

• Exempt as welfare benefits even though could be taxable

SECTION 409A EXCEPTIONS – SEVERANCE (CONT.)

41Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Limited amount exception

• Any payment(s) not exceeding Section 402(g) limit in the aggregate ($18,500

in 2018)

SECTION 409A EXCEPTIONS – SEVERANCE (CONT.)

42Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Easiest – use exceptions to avoid Section 409A

• Exceptions are “stackable”

• Avoid impermissible toggles

• Exception for multiple payments

• Complicating issues

• Payment over time

• “Good reason”

• Requiring release

HOW TO COMPLY WITH SECTION 409A

43Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Timing issues with respect to signing

• Failure to meet short-term deferral rule

• Violation of Section 409A

• Corrections

• Agreement does not specify when payment begins or is made

• Agreement specifies period longer than 90 days

• Agreement specifies period of 90 days or less but commences payment upon

signing

COMPLICATIONS OF RELEASE

44Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Separation from service

• Definition

• Continued service in different capacity

• Change in control issues

• Good reason

• Payment timing

• No acceleration – 30 days

• No substitution

HOW TO COMPLY WITH SECTION 409A (CONT.)

45Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• “Specified employee” issues

• Who is a specified employee

• Six-month delay applies to:

• Payments subject to Section 409A

• Which are payable due to separation from service

HOW TO COMPLY WITH SECTION 409A (CONT.)

46Severance Plans: ERISA and Section 409A Compliance | June 12, 2018

• Review Section 409A compliance

• Document how exceptions apply (if they do)

• Implement compliance plan to the extent necessary

• Modify plans/agreements if required to meet Section 409A

exception/compliance goals

• Assure both documentary and operational compliance

BEST PRACTICES