shanghai, greater china for personal use onlyoutlook for fy2013 . property order book and outlook...

TRANSCRIPT

COVER SLIDE: If you see this text, you must copy the ‘swish’ graphic from a pre-built COVER slide and onto this slide. This text will no longer be visible if done correctly.

PRIVATE & CONFIDENTIAL www.ugllimited.com www.dtz.com

UGL Analyst & Investor Tour Shanghai, Greater China 3 & 4 September 2012

For

per

sona

l use

onl

y

COVER SLIDE: If you see this text, you must copy the ‘swish’ graphic from a pre-built COVER slide and onto this slide. This text will no longer be visible if done correctly.

Welcome and opening Richard Leupen, Managing Director & CEO

1

For

per

sona

l use

onl

y

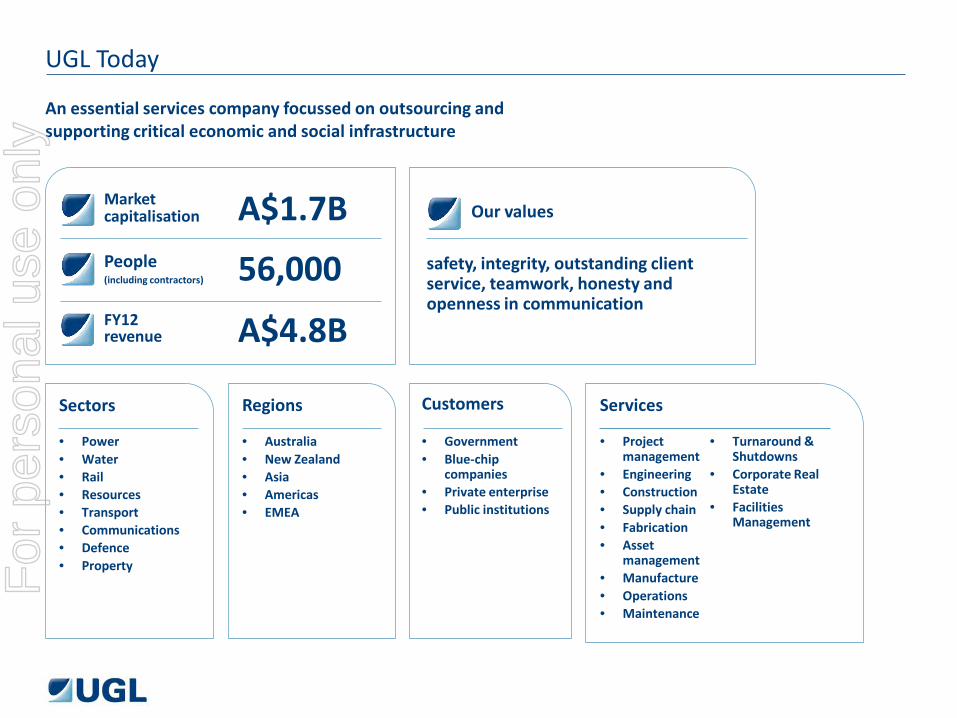

UGL Today

An essential services company focussed on outsourcing and supporting critical economic and social infrastructure

safety, integrity, outstanding client service, teamwork, honesty and openness in communication

People (including contractors)

Market capitalisation

FY12 revenue

Our values

Sectors Regions Customers Services

• Power • Water • Rail • Resources • Transport • Communications • Defence • Property

• Australia • New Zealand • Asia • Americas • EMEA

• Government • Blue-chip

companies • Private enterprise • Public institutions

• Project management

• Engineering • Construction • Supply chain • Fabrication • Asset

management • Manufacture • Operations • Maintenance

• Turnaround & Shutdowns

• Corporate Real Estate

• Facilities Management

56,000

A$1.7B

A$4.8B

For

per

sona

l use

onl

y

DTZ colour palette

Colour used for graphs and pie charts. Use the colours in the following order.

R G B

0 61 121

2

R G B

86 155 190

3

R G B

110 95 63

4

R G B

84 117 141

5

R G B

109 132 173

6

R G B

107 185 195

7

R G B

163 199 219

8

R G B

158 137 137

9

R G B

157 171 187

10

R G B

172 183 210

11

The secondary colours can be accessed from the “Custom Colours” palette The secondary/accent colours should ONLY be used when reporting/using for financials graphics.

R G B

0 139 152

1 Drivers for Growth

• Exposure to long term growth trends

• Significant market opportunities

• Strong technical component

• World class technology

• Balanced trading terms

• Robust systems and processes

• Alliance and cost-plus contracts

• Blue-chip and government clients

• Strong balance sheet • Low capital intensity • Robust cash flow • Flexibility to grow

• Property

• Power & Water Infrastructure

• Resources

• Rail & Transport

• Communications

• Defence

• Balanced recurring revenues

• Diverse earnings streams

• Long term capital works alliances

• Strong order book

• Solid opportunity pipeline

• People

• Safety

• Technology partnerships

• Intellectual property

• Outstanding customer service

Business Positioning

Financial Strength

Risk Management

Sustainable Earnings

Market Leadership

Sector Focus F

or p

erso

nal u

se o

nly

Becoming a Global Leader in Property Services through Selected Acquisitions

UGL acquires facilities services firm UNICCO,

adding 20,000 employees in North

America

UGL acquires Singapore-based

Premas, expanding into 16 major cities

in Asia

UGL acquires the trading operations of CRE company DTZ Holdings plc. expanding presence in the UK, Europe,

Middle East and Asia

2005 2006 2007 2011

UGL acquires Chicago-based CRE firm Equis,

establishing a presence in the US and India

Acquisition of Kilpatrick Green

1998

Acquisition of KFPW

2002

Merged Kilpatrick Green and KFPW

facilities management

business

2004

0.3 0.4

1.1

1.6 1.4 1.3

1.9

FY06 FY07 FY08 FY09 FY10 FY11 FY11 Pro-forma

For

per

sona

l use

onl

y

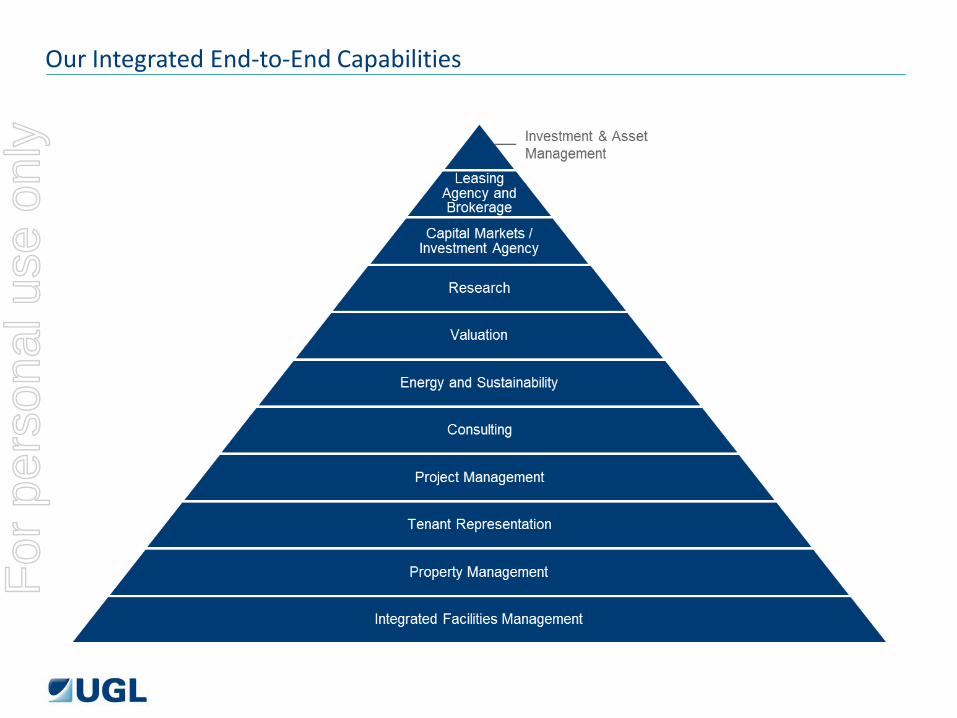

Our Integrated End-to-End Capabilities F

or p

erso

nal u

se o

nly

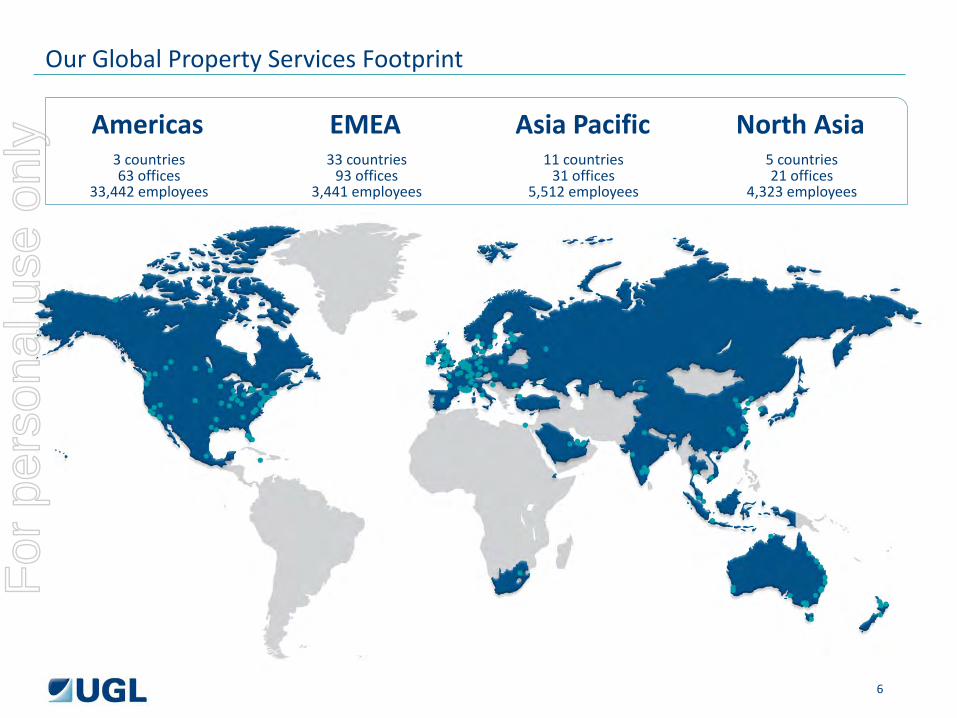

Our Global Property Services Footprint

Americas 3 countries 63 offices

33,442 employees

EMEA 33 countries

93 offices 3,441 employees

Asia Pacific 11 countries

31 offices 5,512 employees

North Asia 5 countries 21 offices

4,323 employees

6

For

per

sona

l use

onl

y

INFORMATION, COMMUNICATION AND TECHNOLOGY

OTHER SECTORS

ENERGY

FINANCIAL/INSURANCE

PHARMA/BIOTECH

Selected clients list F

or p

erso

nal u

se o

nly

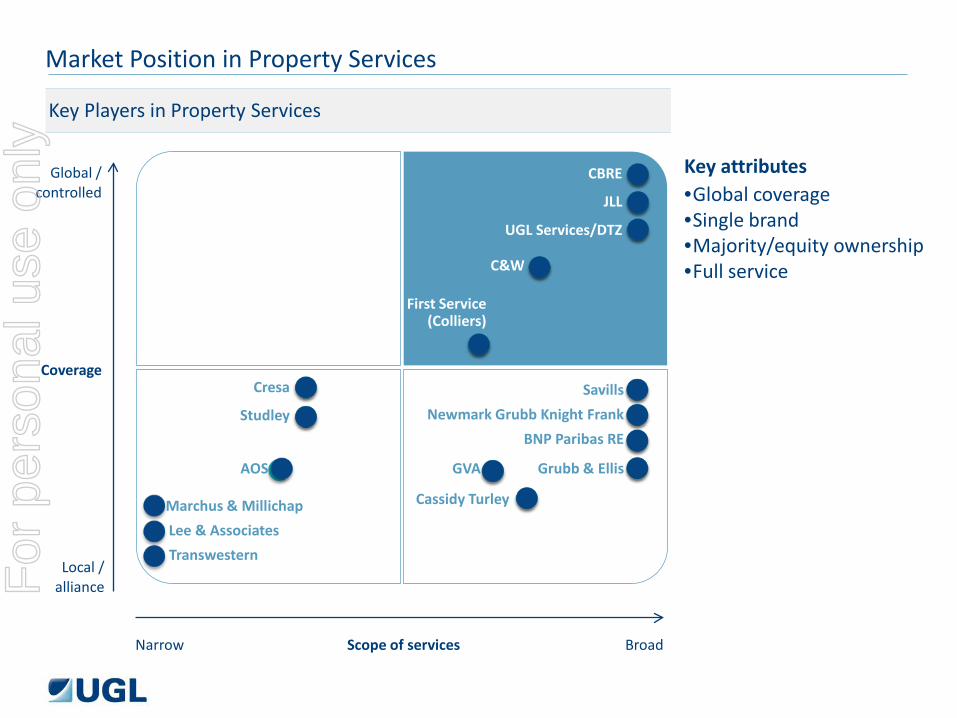

Key Players in Property Services

Key attributes Global / controlled

Coverage

Local / alliance

Narrow Scope of services Broad

•Global coverage •Single brand •Majority/equity ownership •Full service

CBRE

JLL

UGL Services/DTZ

C&W

First Service (Colliers)

Savills

Newmark Grubb Knight Frank

BNP Paribas RE

Grubb & Ellis GVA

Cassidy Turley

AOS

Studley

Cresa

Market Position in Property Services

Marchus & Millichap

Lee & Associates

Transwestern

For

per

sona

l use

onl

y

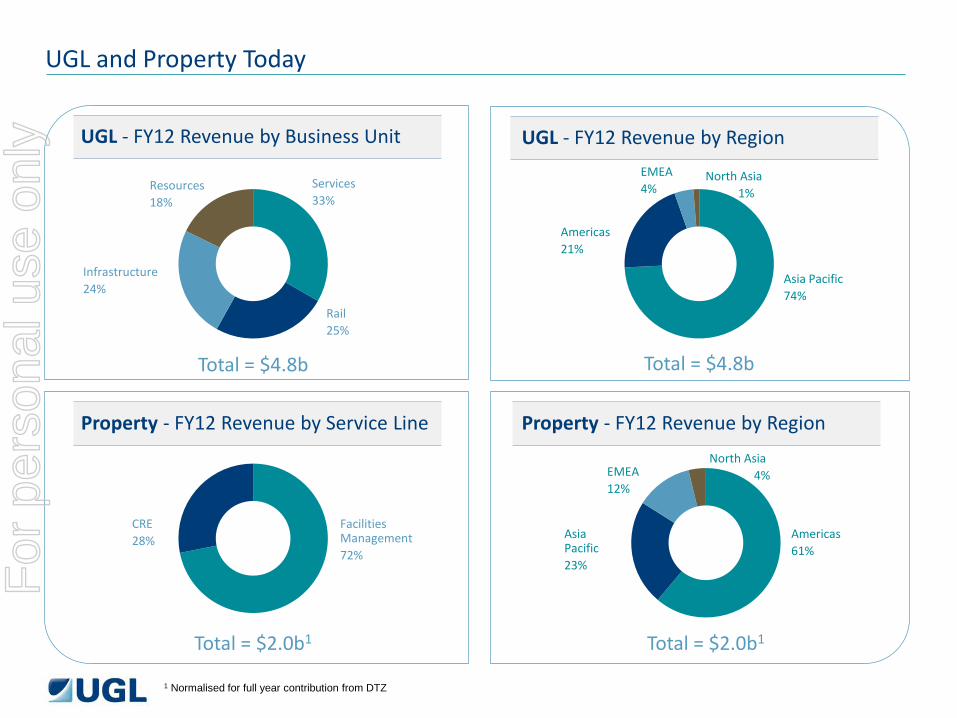

UGL and Property Today

UGL - FY12 Revenue by Business Unit UGL - FY12 Revenue by Region

Property - FY12 Revenue by Region Property - FY12 Revenue by Service Line

Resources 18%

Services 33%

Rail 25%

Infrastructure 24%

Total = $4.8b

North Asia 1%

Asia Pacific 74%

EMEA 4%

Americas 21%

Total = $4.8b

Facilities Management 72%

CRE 28%

Total = $2.0b1

Americas 61%

Asia Pacific 23%

EMEA 12%

North Asia 4%

Total = $2.0b1

1 Normalised for full year contribution from DTZ

For

per

sona

l use

onl

y

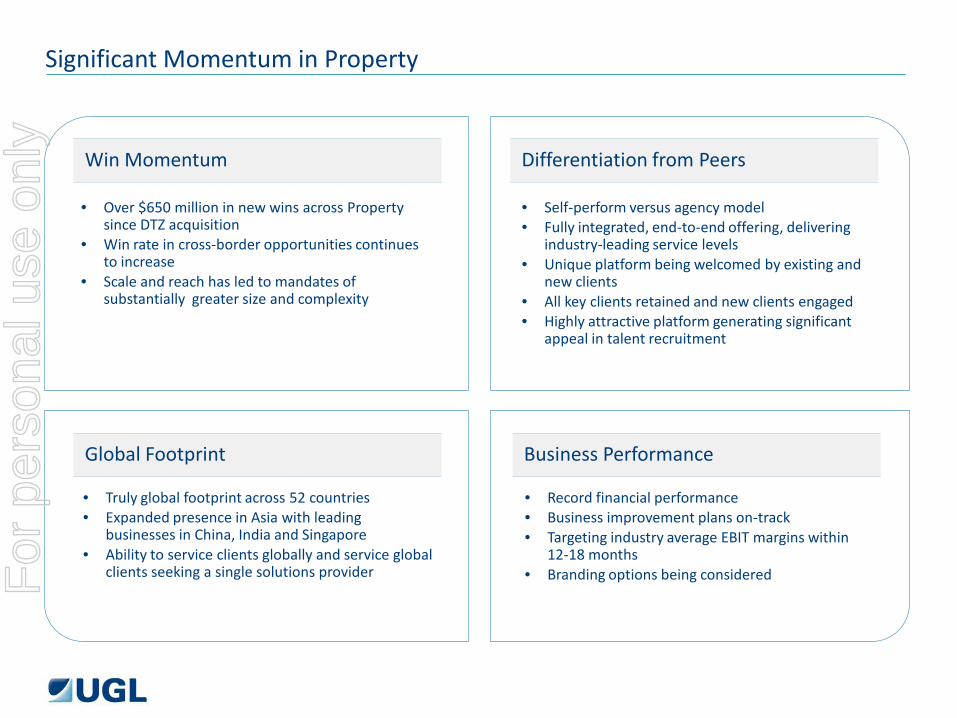

Significant Momentum in Property

Win Momentum Differentiation from Peers

Business Performance Global Footprint

• Over $650 million in new wins across Property since DTZ acquisition

• Win rate in cross-border opportunities continues to increase

• Scale and reach has led to mandates of substantially greater size and complexity

• Self-perform versus agency model • Fully integrated, end-to-end offering, delivering

industry-leading service levels • Unique platform being welcomed by existing and

new clients • All key clients retained and new clients engaged • Highly attractive platform generating significant

appeal in talent recruitment

• Record financial performance • Business improvement plans on-track • Targeting industry average EBIT margins within

12-18 months • Branding options being considered

• Truly global footprint across 52 countries • Expanded presence in Asia with leading

businesses in China, India and Singapore • Ability to service clients globally and service global

clients seeking a single solutions provider For

per

sona

l use

onl

y

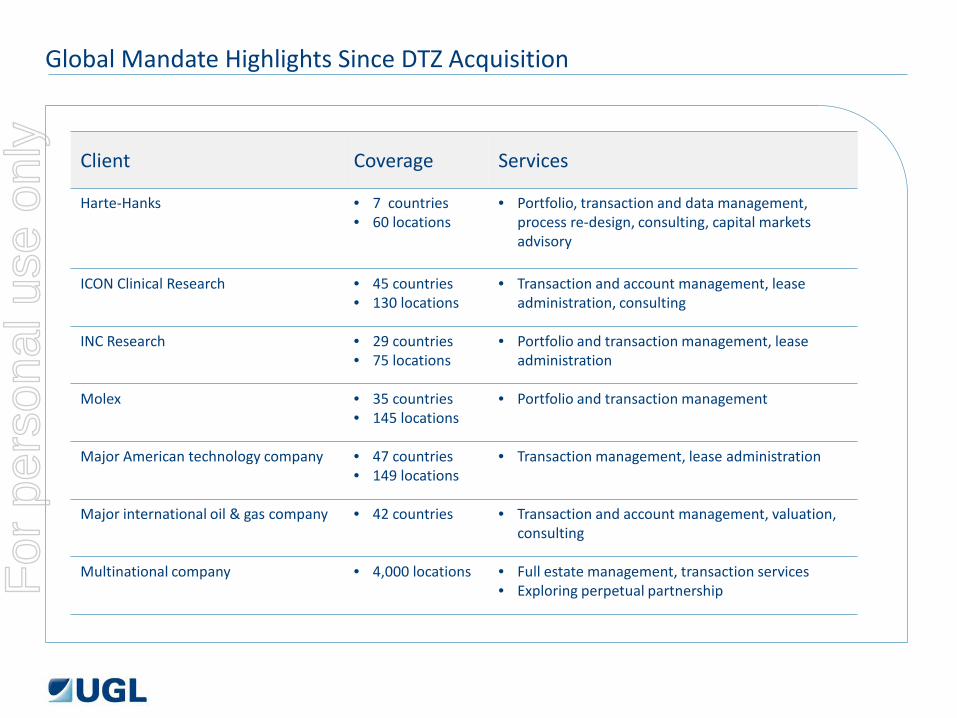

Global Mandate Highlights Since DTZ Acquisition

Client Coverage Services

Harte-Hanks • 7 countries • 60 locations

• Portfolio, transaction and data management, process re-design, consulting, capital markets advisory

ICON Clinical Research • 45 countries • 130 locations

• Transaction and account management, lease administration, consulting

INC Research • 29 countries • 75 locations

• Portfolio and transaction management, lease administration

Molex • 35 countries • 145 locations

• Portfolio and transaction management

Major American technology company • 47 countries • 149 locations

• Transaction management, lease administration

Major international oil & gas company • 42 countries • Transaction and account management, valuation, consulting

Multinational company • 4,000 locations

• Full estate management, transaction services • Exploring perpetual partnership F

or p

erso

nal u

se o

nly

Our Strategic Areas of Focus for Property

Single Global IT Platform Addressable Market

Core Foundations Unchanged Global Outsourcing Trend

• Roll out of a single global property IT platform over the next 12 months

• Industry leading technology will drive distinct competitive advantage for a number of years

• Transforming the way property services solutions are delivered to clients

• Expand share of addressable market by capitalising on unique service offering

• Total global property services market estimated at US$200b

• Top 5 companies represent around10% of total global market

• Opportunities to participate in industry consolidation

• Continued trend to outsource and globalisation of clients creating significant opportunities for future growth

• Further investing in and expanding global delivery model to capitalise on growth opportunities

• Rigorous focus on cost discipline • Financial strength with low capital intensity • Risk management framework delivering quality

growth to order book • Significant ongoing investment in people, systems

and processes

For

per

sona

l use

onl

y

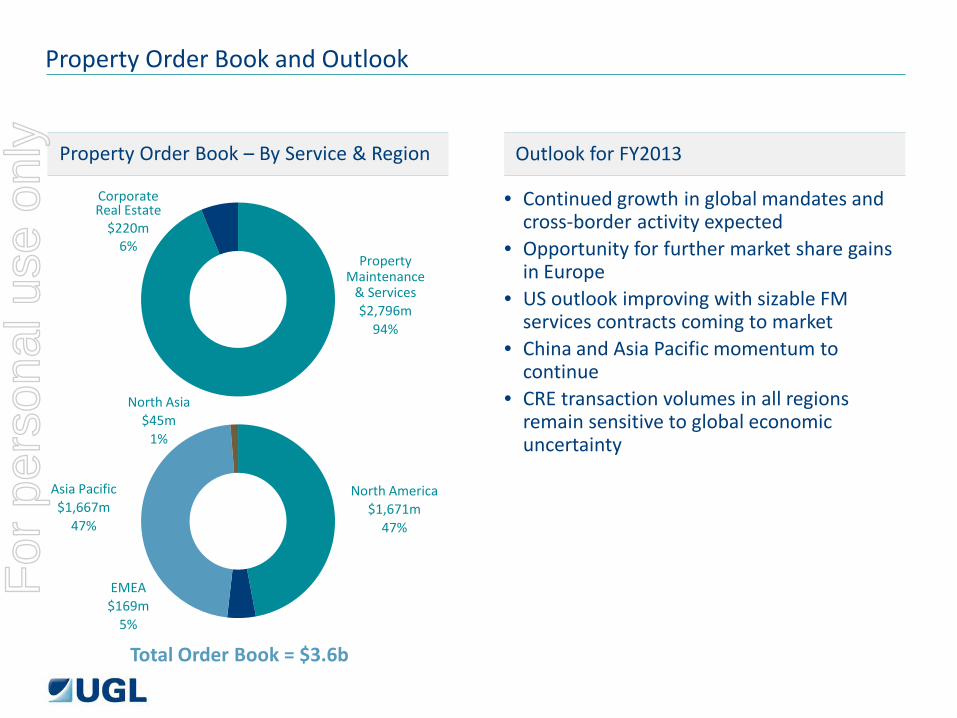

Property Order Book – By Service & Region Outlook for FY2013

Property Order Book and Outlook

• Continued growth in global mandates and cross-border activity expected

• Opportunity for further market share gains in Europe

• US outlook improving with sizable FM services contracts coming to market

• China and Asia Pacific momentum to continue

• CRE transaction volumes in all regions remain sensitive to global economic uncertainty

Total Order Book = $3.6b

Corporate Real Estate

$220m 6%

Property Maintenance

& Services $2,796m

94%

North America $1,671m

47%

Asia Pacific $1,667m

47%

EMEA $169m

5%

North Asia $45m

1%

For

per

sona

l use

onl

y

Robert Shibuya, Group President

UGL Services / DTZ

14

For

per

sona

l use

onl

y

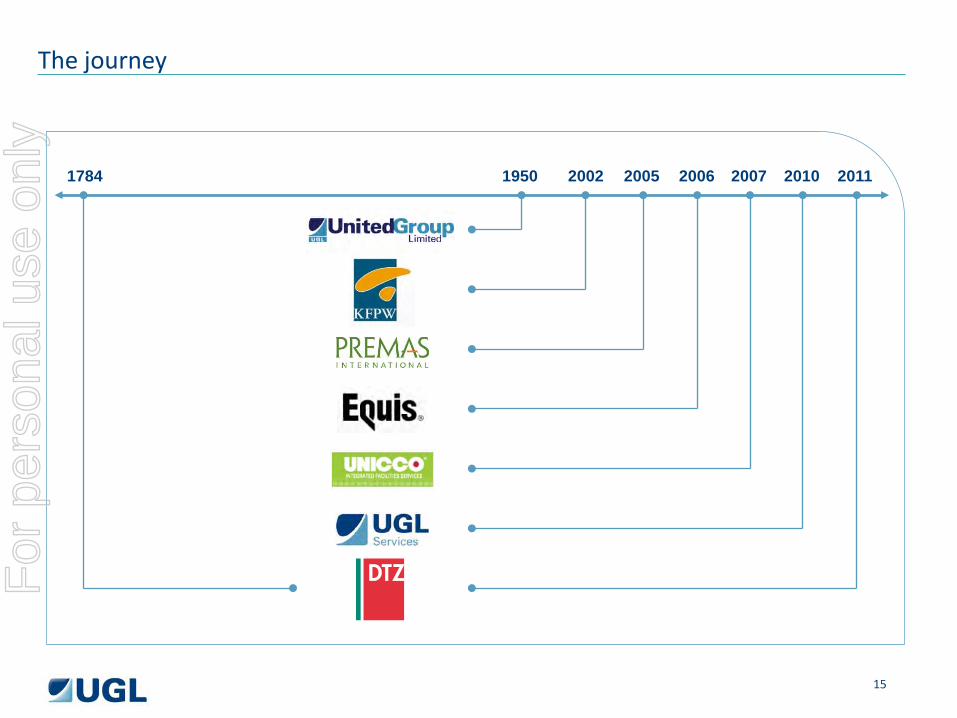

1784 2007 1950 2006 2011 2005 2002 2010

The journey

15

For

per

sona

l use

onl

y

Countries Offices

Geography

Customers

Services

• North America • EMEA • South East Asia • North Asia

• Government • Blue-chip companies • Institutional

investors

• Leasing agency / brokerage

• Integrated property and facilities management

• Valuation • Capital markets • Project management • Investment and

Asset management

52 People (including contractors) 47,000

Values

• Safety • Integrity • Outstanding

customer service

• Teamwork • Honesty • Openness in

communication

208 Global Headquarters Los Angeles

UGL Services /DTZ overview

Global, integrated provider of property services and solutions across investor and occupier property sectors

16

For

per

sona

l use

onl

y

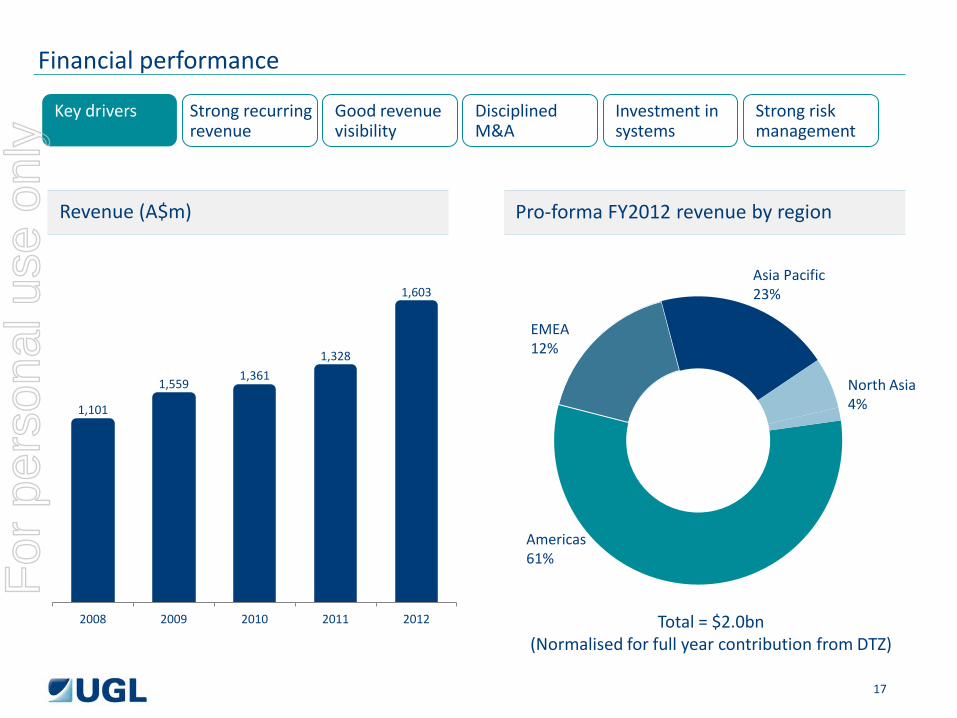

1,101

1,559 1,361

1,328

1,603

2008 2009 2010 2011 2012

Financial performance

Key drivers Strong recurring revenue

Good revenue visibility

Disciplined M&A

Investment in systems

Strong risk management

EMEA 12%

Americas 61%

Asia Pacific 23%

North Asia 4%

Revenue (A$m) Pro-forma FY2012 revenue by region

Total = $2.0bn (Normalised for full year contribution from DTZ)

17

For

per

sona

l use

onl

y

Sustainable platform

Revenue by type – Pre-DTZ acquisition Revenue by type – Post-DTZ acquisition

Transactional revenue 8%

Recurring Revenue 92%

Transactional revenue 28%

Recurring revenue 72%

18

For

per

sona

l use

onl

y

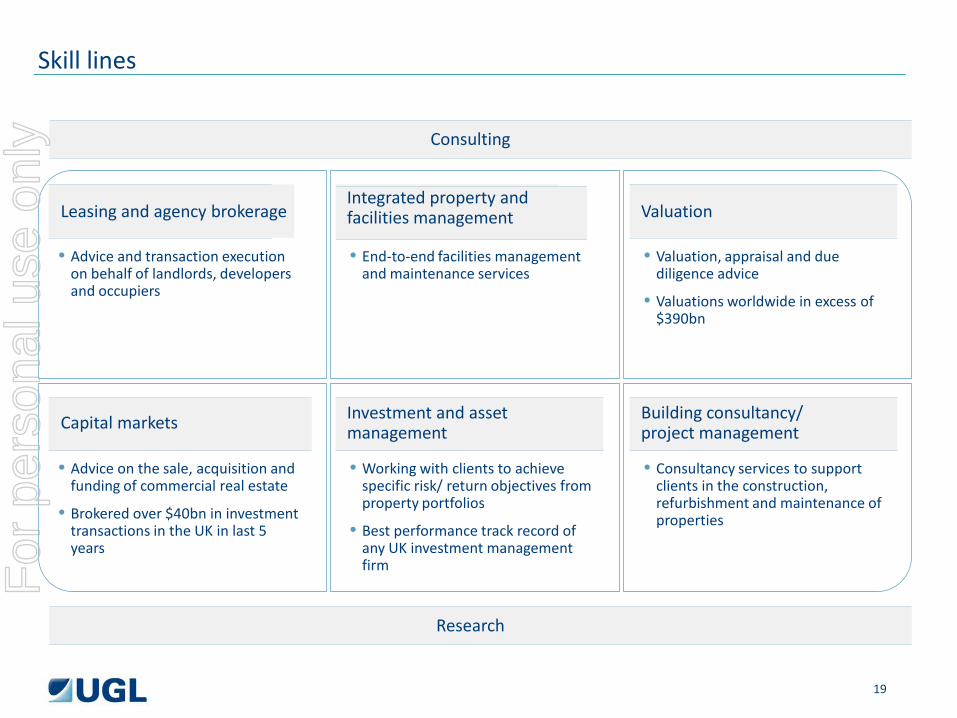

Skill lines

Leasing and agency brokerage

Capital markets

• Advice and transaction execution on behalf of landlords, developers and occupiers

• Advice on the sale, acquisition and funding of commercial real estate

• Brokered over $40bn in investment transactions in the UK in last 5 years

Investment and asset management

• End-to-end facilities management and maintenance services

• Working with clients to achieve specific risk/ return objectives from property portfolios

• Best performance track record of any UK investment management firm

Valuation

Building consultancy/ project management

• Valuation, appraisal and due diligence advice

• Valuations worldwide in excess of $390bn

• Consultancy services to support clients in the construction, refurbishment and maintenance of properties

Consulting

Research

Integrated property and facilities management

19

For

per

sona

l use

onl

y

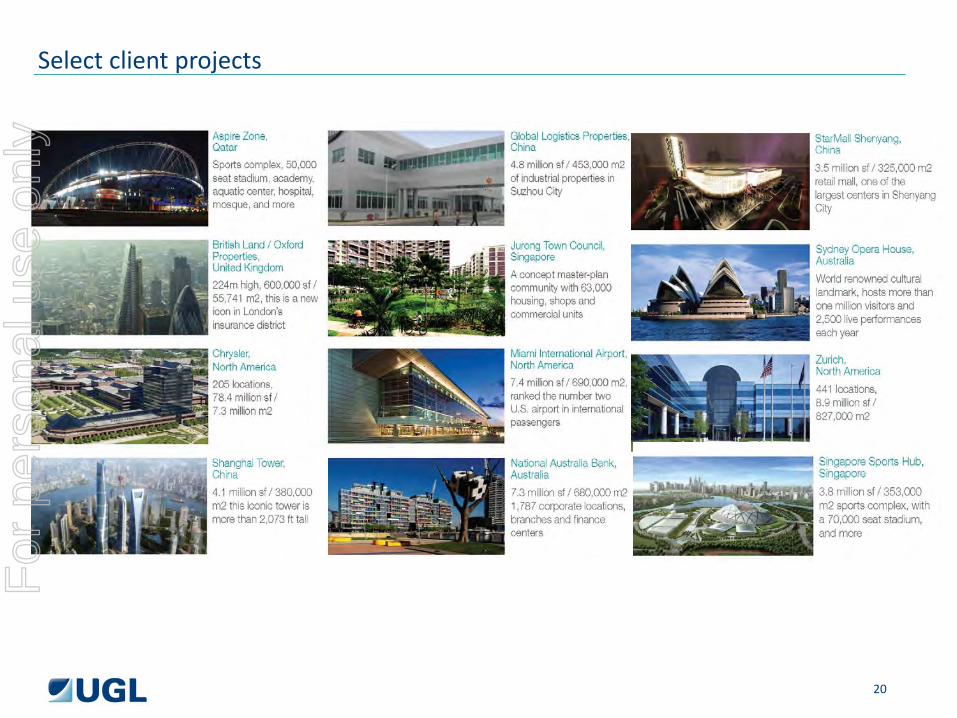

Select client projects

20

For

per

sona

l use

onl

y

Differentiators

• Strong financial performance & balance sheet

• Fully integrated, end-to-end offering, delivering industry-leading service levels

• More than $10bn in Assets Under Management across UK/Europe • Market leading independent global research

• Long term relationship as trusted advisor to Global 200 corporate real estate departments • Global coordinated IT solution • Widest geographic coverage in China among international real estate advisory firms • #1 retail leasing agent in the UK • #1 retail leasing agent in the UK

• #1 in valuations in China, top 3 in UK and key European markets

21

For

per

sona

l use

onl

y

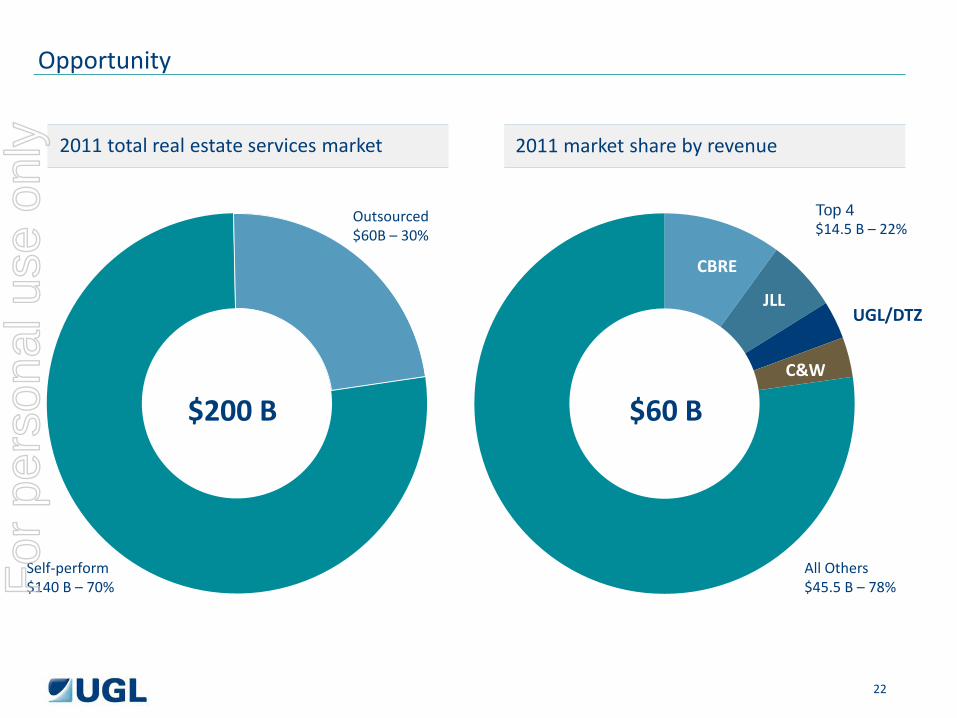

Self-perform $140 B – 70%

CBRE

JLL

C&W

UGL/DTZ

All Others $45.5 B – 78%

Top 4 $14.5 B – 22%

Opportunity

2011 total real estate services market 2011 market share by revenue

Outsourced $60B – 30%

$60 B $200 B

22

For

per

sona

l use

onl

y

Objectives and strategy

Investor

Occupier

Consulting

Leasing agency and brokerage

Building Consultancy/

Project Management

Integrated property and

facilities management

Capital markets Investment and

Asset Management

Valuation

Research

End-to-end

Objective

To be the best firm in the real estate services industry through outstanding customer service to both investor and occupier clients

End-to-end

Strategy

Provide a vertically integrated end-to-end solutions model, creating a unique customer value proposition, seamlessly integrated under a global leadership

23

For

per

sona

l use

onl

y

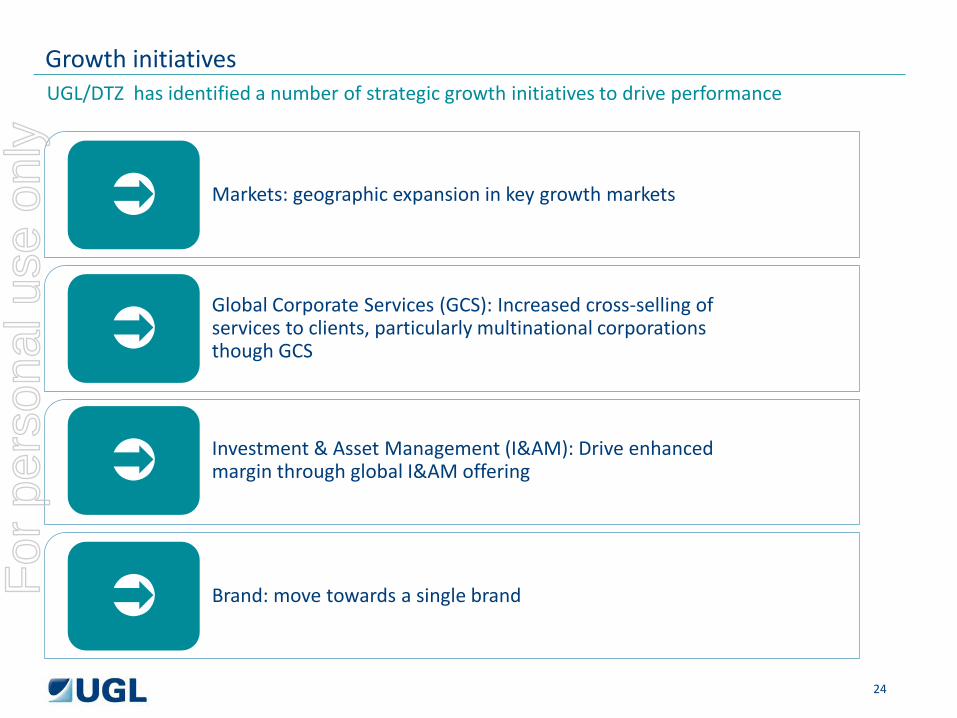

UGL/DTZ has identified a number of strategic growth initiatives to drive performance

Growth initiatives

Markets: geographic expansion in key growth markets

Global Corporate Services (GCS): Increased cross-selling of services to clients, particularly multinational corporations though GCS

Investment & Asset Management (I&AM): Drive enhanced margin through global I&AM offering

Brand: move towards a single brand

24

For

per

sona

l use

onl

y

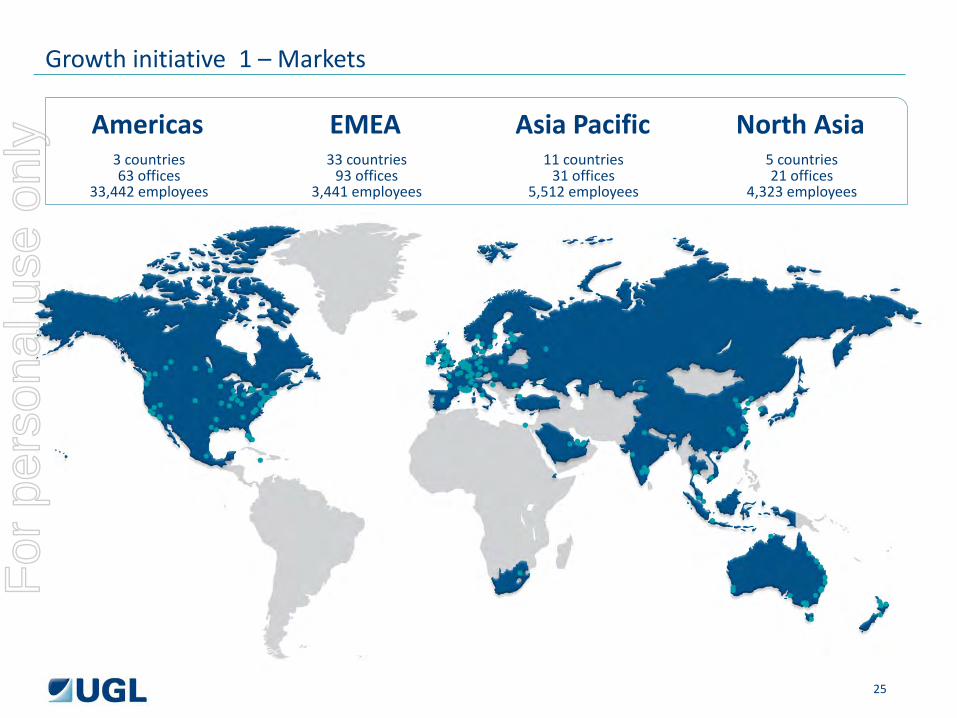

Growth initiative 1 – Markets

Americas 3 countries 63 offices

33,442 employees

EMEA 33 countries

93 offices 3,441 employees

Asia Pacific 11 countries

31 offices 5,512 employees

North Asia 5 countries 21 offices

4,323 employees

25

For

per

sona

l use

onl

y

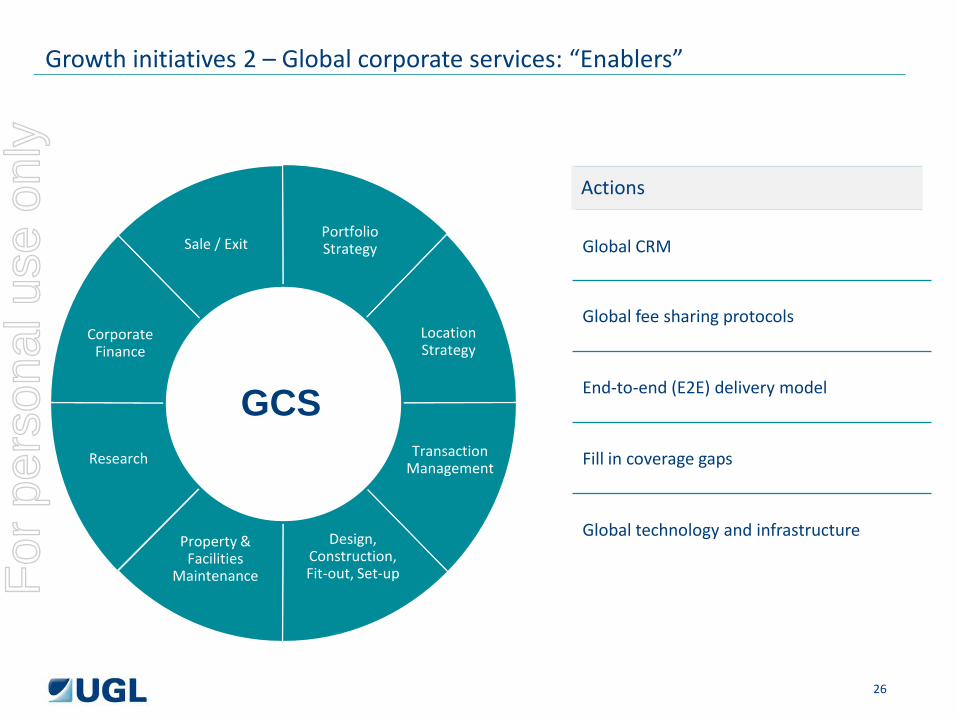

Growth initiatives 2 – Global corporate services: “Enablers”

Location Strategy

Sale / Exit Portfolio Strategy

Design, Construction, Fit-out, Set-up

Research

Corporate Finance

Transaction Management

Property & Facilities

Maintenance

GCS

Actions

Global CRM

Global fee sharing protocols

End-to-end (E2E) delivery model

Fill in coverage gaps

Global technology and infrastructure

26

Actions

For

per

sona

l use

onl

y

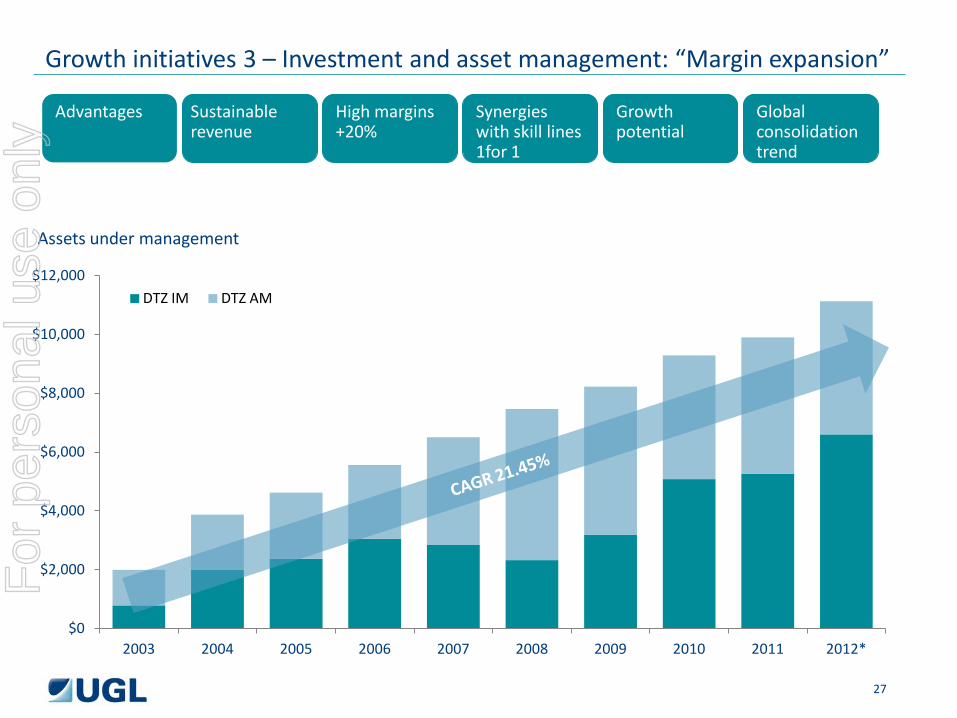

Growth initiatives 3 – Investment and asset management: “Margin expansion”

Location Strategy

Sale / Exit Portfolio Strategy

Design, Construction, Fit-out, Set-up

Research

Corporate Finance

Transaction Management

Property & Facilities

Maintenance

Advantages Sustainable revenue

High margins +20%

Synergies with skill lines 1for 1

Growth potential

Global consolidation trend

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012*

Assets under management

DTZ IM DTZ AM

27

For

per

sona

l use

onl

y

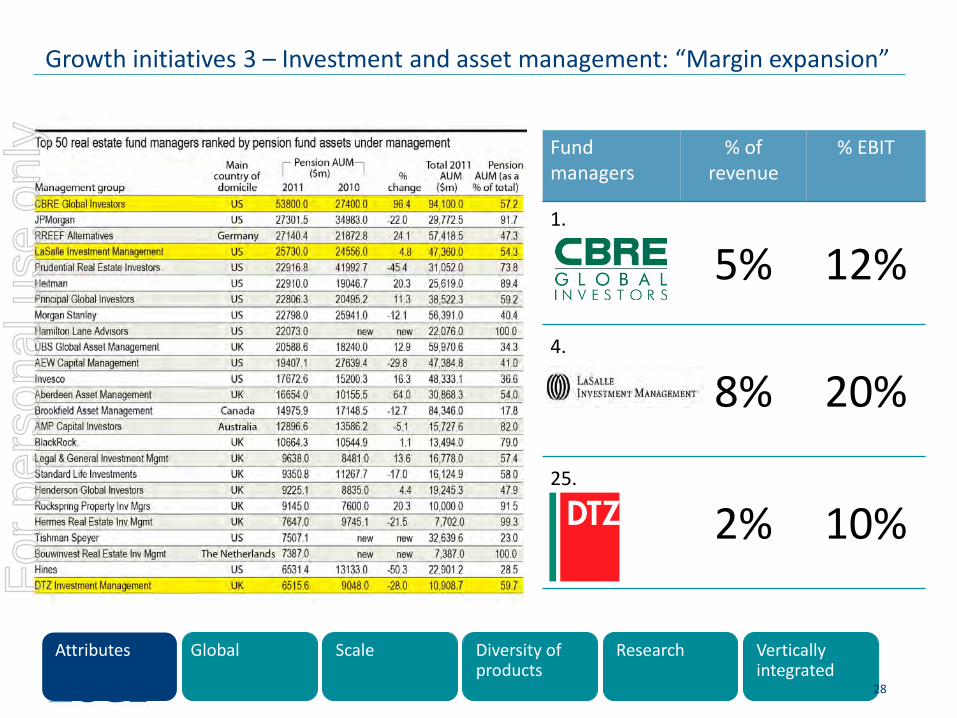

Growth initiatives 3 – Investment and asset management: “Margin expansion”

Attributes Global Scale Diversity of products

Research Vertically integrated

Fund managers

% of revenue

% EBIT

1.

5% 12%

4.

8% 20%

25.

2% 10%

28

For

per

sona

l use

onl

y

Takeaways

• Global coverage

• Full service end-to-end solution

• Scale / institutional acceptability

• Top 3 global platform

• Move towards a single brand

29

For

per

sona

l use

onl

y

John Forrester, Chief Executive

EMEA

30

For

per

sona

l use

onl

y

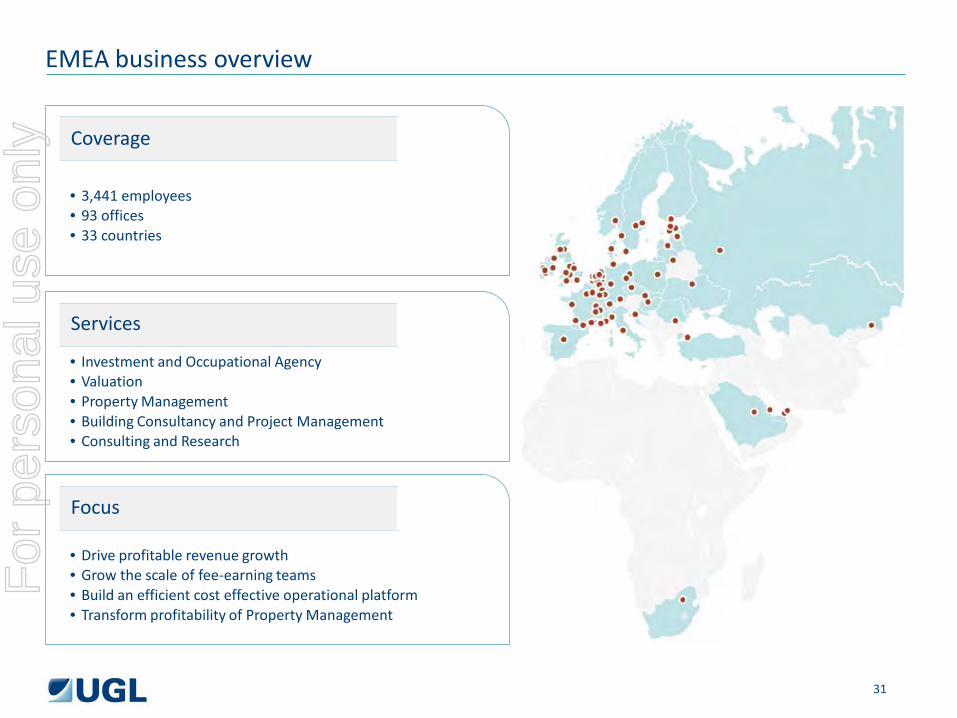

EMEA business overview

Coverage

Services

Focus

• 3,441 employees • 93 offices • 33 countries

• Investment and Occupational Agency • Valuation • Property Management • Building Consultancy and Project Management • Consulting and Research

• Drive profitable revenue growth • Grow the scale of fee-earning teams • Build an efficient cost effective operational platform • Transform profitability of Property Management

31

For

per

sona

l use

onl

y

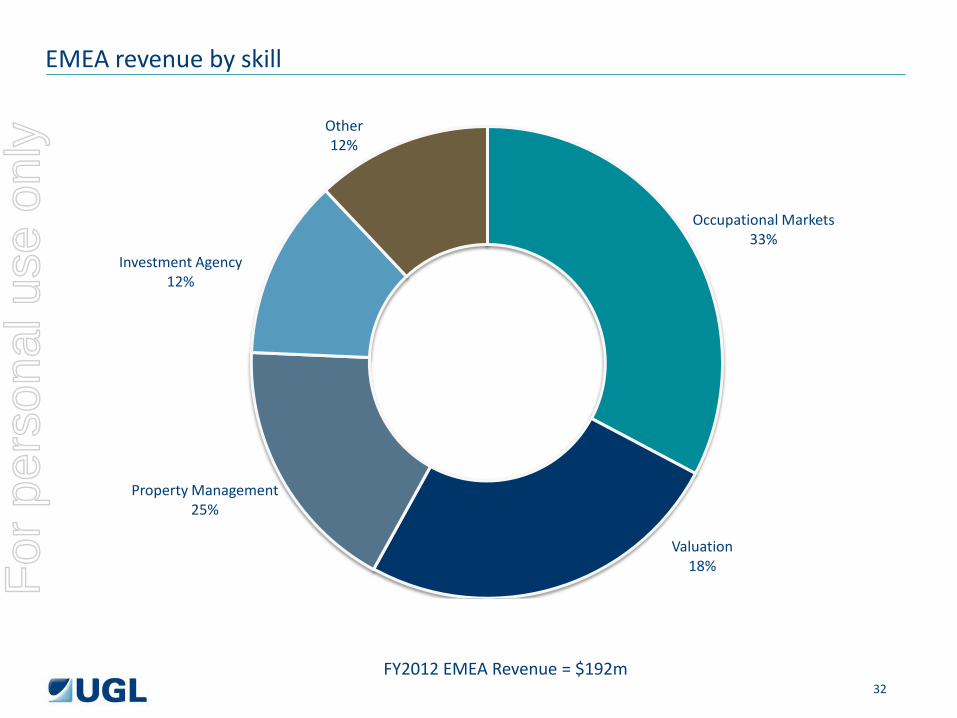

EMEA revenue by skill

Occupational Markets 33%

Property Management 25%

Valuation

18%

Investment Agency 12%

Other 12%

FY2012 EMEA Revenue = $192m 32

For

per

sona

l use

onl

y

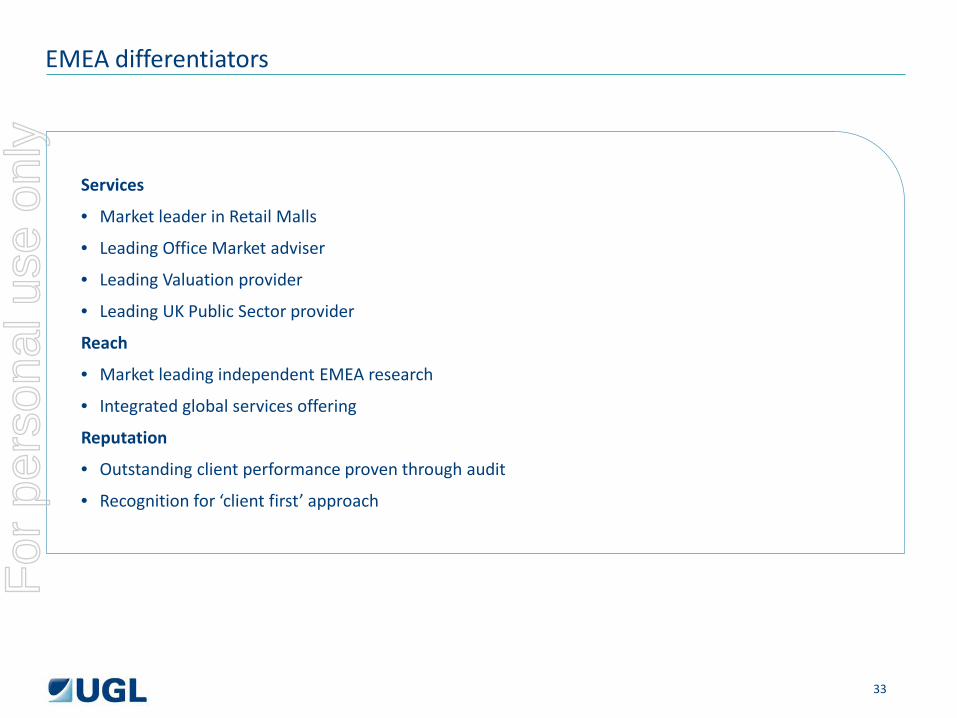

EMEA differentiators

Services

• Market leader in Retail Malls

• Leading Office Market adviser

• Leading Valuation provider

• Leading UK Public Sector provider

Reach

• Market leading independent EMEA research

• Integrated global services offering

Reputation

• Outstanding client performance proven through audit

• Recognition for ‘client first’ approach

33

For

per

sona

l use

onl

y

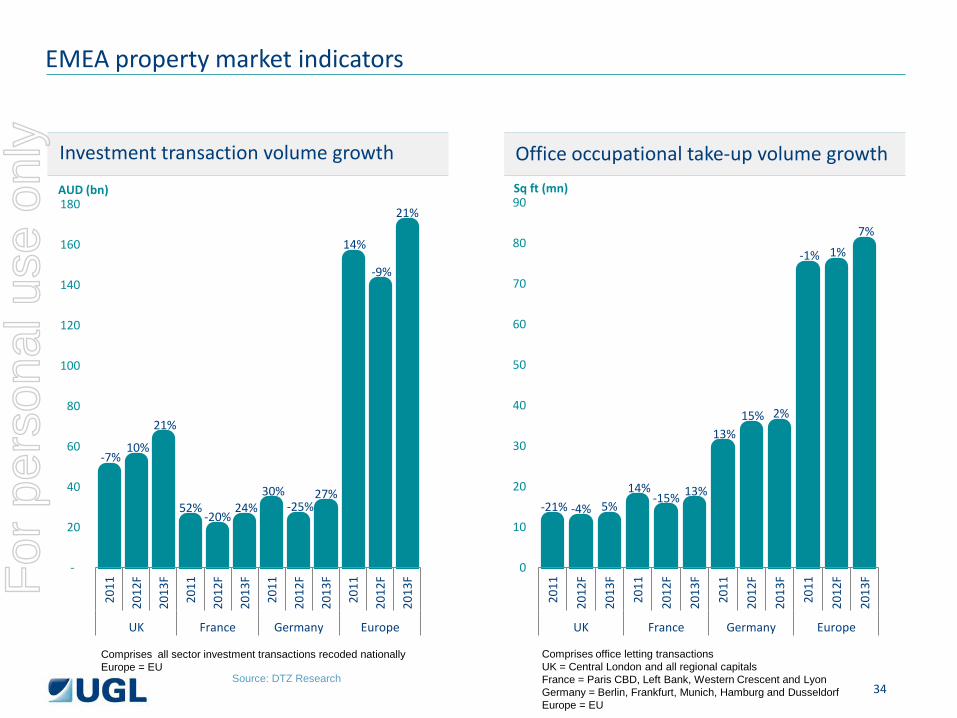

-21% -4% 5% 14%

-15% 13%

13% 15% 2%

-1% 1%

7%

0

10

20

30

40

50

60

70

80

90

2011

2012

F

2013

F

2011

2012

F

2013

F

2011

2012

F

2013

F

2011

2012

F

2013

F

UK France Germany Europe

Investment transaction volume growth Office occupational take-up volume growth

EMEA property market indicators

-7% 10%

21%

52% -20%

24% 30%

-25% 27%

14%

-9%

21%

-

20

40

60

80

100

120

140

160

180

2011

2012

F

2013

F

2011

2012

F

2013

F

2011

2012

F

2013

F

2011

2012

F

2013

F

UK France Germany Europe

AUD (bn)

Comprises all sector investment transactions recoded nationally Europe = EU

Comprises office letting transactions UK = Central London and all regional capitals France = Paris CBD, Left Bank, Western Crescent and Lyon Germany = Berlin, Frankfurt, Munich, Hamburg and Dusseldorf Europe = EU

Sq ft (mn)

Source: DTZ Research 34

For

per

sona

l use

onl

y

EMEA market drivers

Economic growth in EMEA to remain weak in remainder of 2012 and 2013

Overall real estate investment volumes down in FY12 and letting activity now broadly flat on prior year but trending downwards

Corporate occupiers building cash reserves and awaiting better macroeconomic conditions

Investor clients focusing on tenant retention, cash flow and minimising non-recoverable costs

Outlook Actions

Reduce overheads, by delivering on planned cost cutting programme, and establish more efficient systems

Recruit fee-earners in robust markets to improve our market position and drive profitable revenue growth

Implement turnaround of EMEA Property Management

35

For

per

sona

l use

onl

y

EMEA major clients

Advised circa 400 UK public sector organisations – market leader • Consulting, Occupier Markets,

Professional Services, Research and Valuation

A multi-national internet corporation • Agency, Building Consultancy,

Corporate Real Estate Management and Investment Agency

A global retail developer • Retail Leasing, Management

Set-up and Valuation

AEW Europe • Occupier Markets, Professional

Services and Valuation

Aviva Investors • Agency, Building Consultancy,

Investment Agency, Professional Advisory Services, Property Management, Rating, Residential, Retail and Valuation

Henderson Global Investors • Agency, Building Surveying,

Investment, Property Management, Retail and Valuation

36

For

per

sona

l use

onl

y

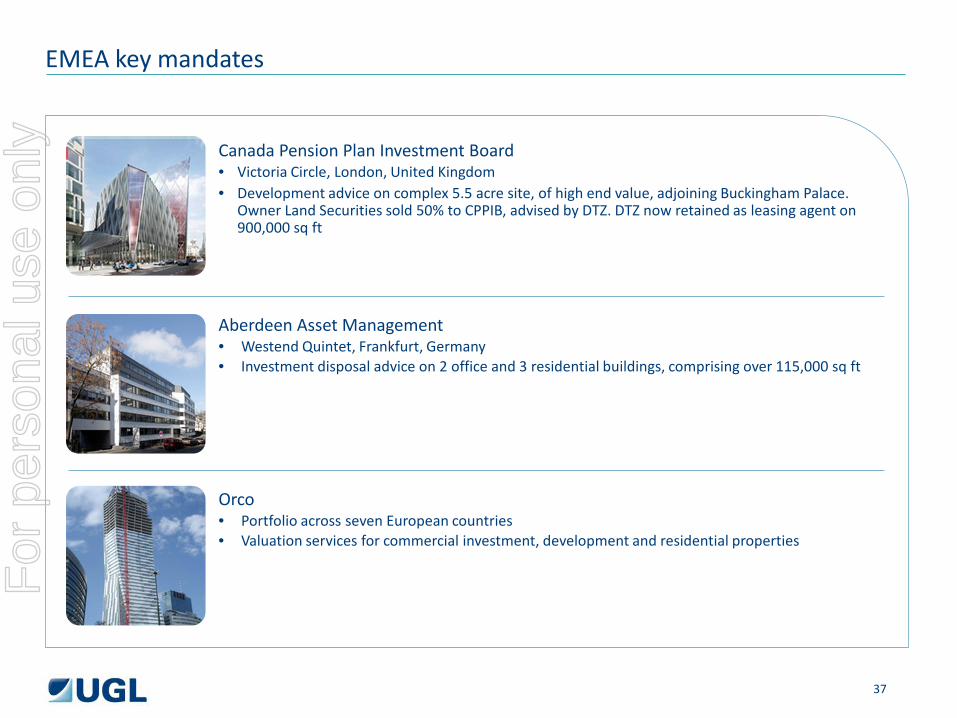

Canada Pension Plan Investment Board • Victoria Circle, London, United Kingdom • Development advice on complex 5.5 acre site, of high end value, adjoining Buckingham Palace.

Owner Land Securities sold 50% to CPPIB, advised by DTZ. DTZ now retained as leasing agent on 900,000 sq ft

EMEA key mandates

Aberdeen Asset Management • Westend Quintet, Frankfurt, Germany • Investment disposal advice on 2 office and 3 residential buildings, comprising over 115,000 sq ft

Orco • Portfolio across seven European countries • Valuation services for commercial investment, development and residential properties

37

For

per

sona

l use

onl

y

Christopher Cooper, UK Managing Director

Investment & Asset Management

38

For

per

sona

l use

onl

y

• The investment and asset management businesses (“IAM”) help our investor clients meet/exceed their return objectives within their risk tolerances by investing in the real estate sector

• The IAM businesses serve a range of investor clients with varying investment horizons and varying

risk requirements. This has enabled us to diversify revenue streams, built on a stable core of recurring income

• The IAM businesses have a history of delivering successful results to clients. This track record has

enabled continued growth of our business, with Assets under Management (“AUM”) increasing by c25% per annum over the last 10 years. This is one of the fastest rates of growth in the market, albeit from a low starting point

• This growth has been achieved organically via targeted additions of staff to our teams. This

approach enabled lower risk growth and delivered high ongoing profitability while growth was realised

39

Introduction to our platform Business overview

For

per

sona

l use

onl

y

Business overview (continued)

The business has four compelling attractions for clients: 1. A unique investment philosophy based on an solid understanding of occupier needs;

2. High quality investment professionals with a long track record with the firm;

3. Disciplined investment processes backed by robust corporate governance; and

4. Top rated long-term investment performance. Future growth priorities are a combination of adding existing service lines to the current platform, and geographic expansion to exploit new sources of capital.

Introduction to our platform

40

For

per

sona

l use

onl

y

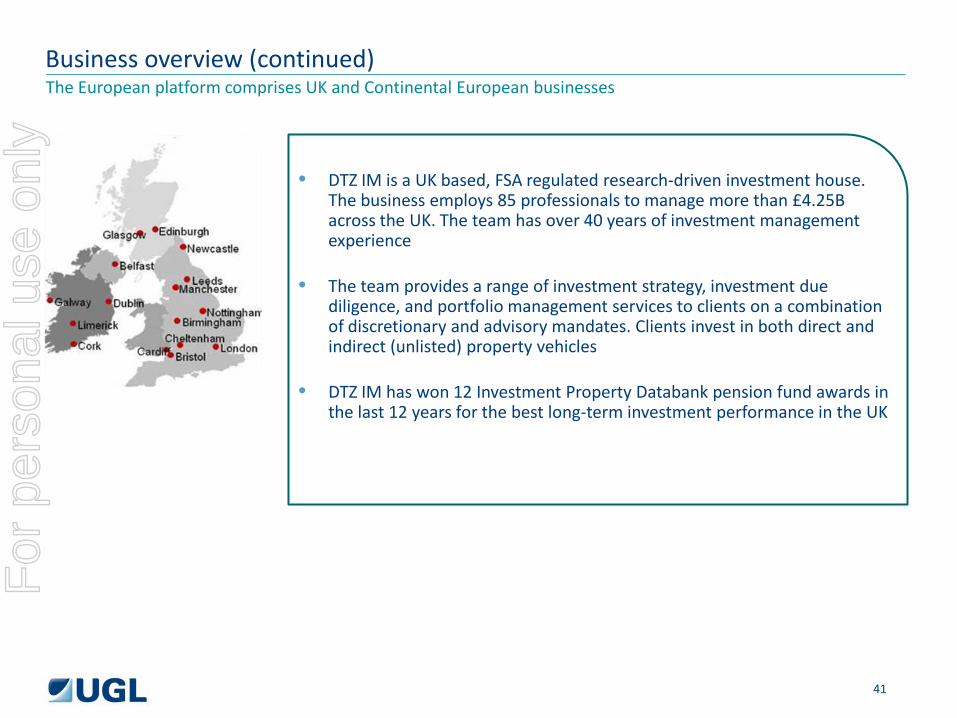

• DTZ IM is a UK based, FSA regulated research-driven investment house. The business employs 85 professionals to manage more than £4.25B across the UK. The team has over 40 years of investment management experience

• The team provides a range of investment strategy, investment due

diligence, and portfolio management services to clients on a combination of discretionary and advisory mandates. Clients invest in both direct and indirect (unlisted) property vehicles

• DTZ IM has won 12 Investment Property Databank pension fund awards in

the last 12 years for the best long-term investment performance in the UK

Business overview (continued) The European platform comprises UK and Continental European businesses

41

For

per

sona

l use

onl

y

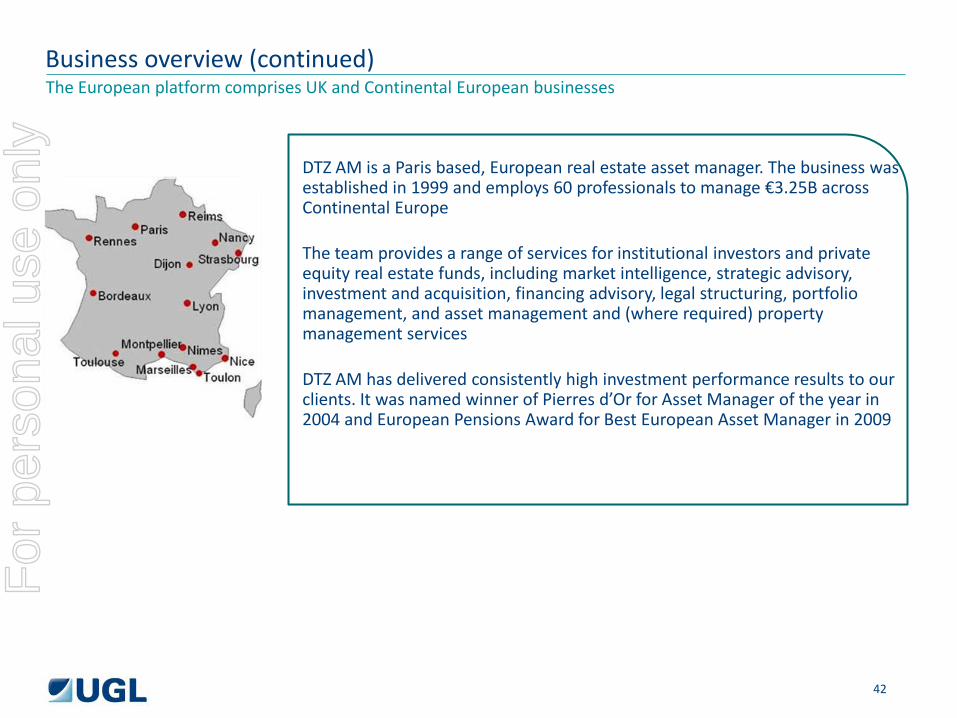

DTZ AM is a Paris based, European real estate asset manager. The business was established in 1999 and employs 60 professionals to manage €3.25B across Continental Europe The team provides a range of services for institutional investors and private equity real estate funds, including market intelligence, strategic advisory, investment and acquisition, financing advisory, legal structuring, portfolio management, and asset management and (where required) property management services DTZ AM has delivered consistently high investment performance results to our clients. It was named winner of Pierres d’Or for Asset Manager of the year in 2004 and European Pensions Award for Best European Asset Manager in 2009

Business overview (continued) The European platform comprises UK and Continental European businesses

42

For

per

sona

l use

onl

y

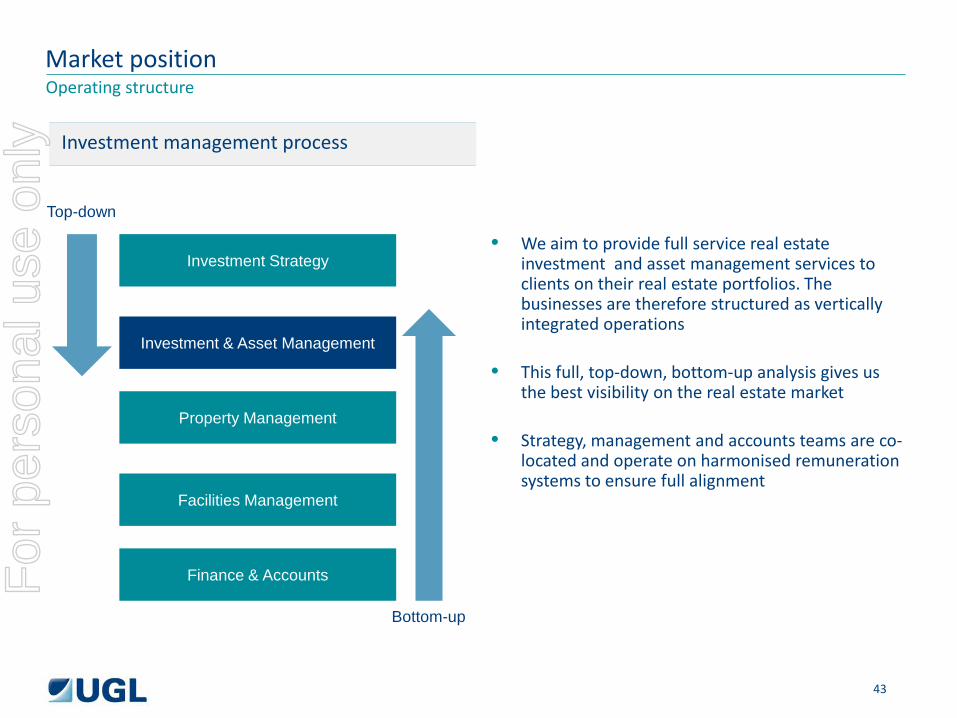

• We aim to provide full service real estate investment and asset management services to clients on their real estate portfolios. The businesses are therefore structured as vertically integrated operations

• This full, top-down, bottom-up analysis gives us

the best visibility on the real estate market • Strategy, management and accounts teams are co-

located and operate on harmonised remuneration systems to ensure full alignment

Market position Operating structure

Investment Strategy

Investment & Asset Management

Property Management

Facilities Management

Finance & Accounts

Top-down

Bottom-up

Investment management process

43

For

per

sona

l use

onl

y

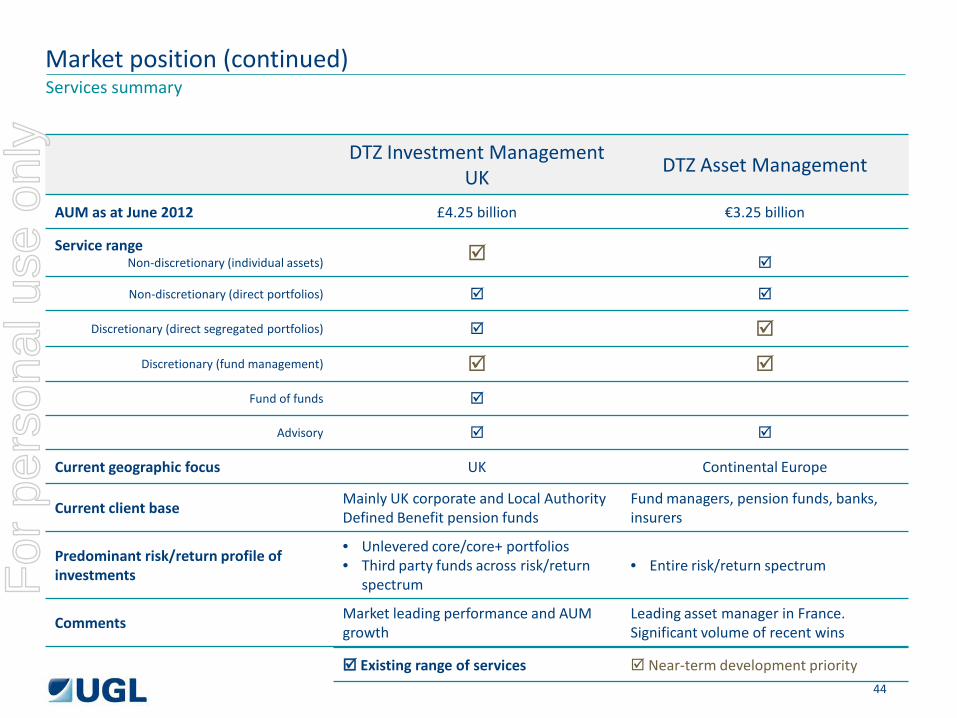

Market position (continued)

DTZ Investment Management UK

DTZ Asset Management

AUM as at June 2012 £4.25 billion €3.25 billion

Service range Non-discretionary (individual assets)

Non-discretionary (direct portfolios)

Discretionary (direct segregated portfolios)

Discretionary (fund management)

Fund of funds

Advisory

Current geographic focus UK Continental Europe

Current client base Mainly UK corporate and Local Authority Defined Benefit pension funds

Fund managers, pension funds, banks, insurers

Predominant risk/return profile of investments

• Unlevered core/core+ portfolios • Third party funds across risk/return

spectrum • Entire risk/return spectrum

Comments Market leading performance and AUM growth

Leading asset manager in France. Significant volume of recent wins

Services summary

Existing range of services Near-term development priority 44

For

per

sona

l use

onl

y

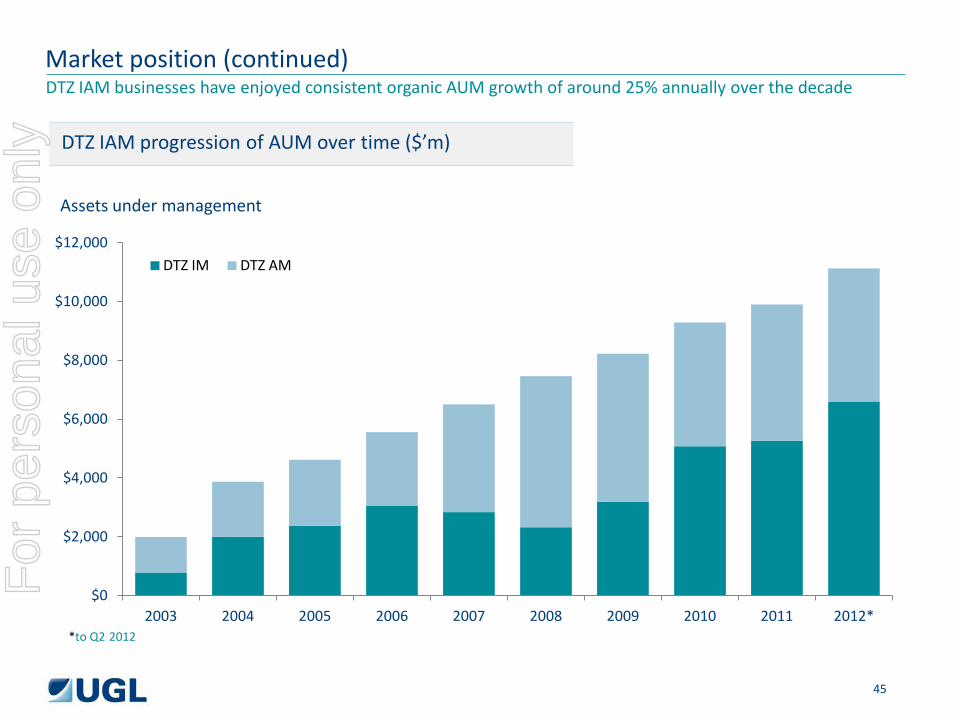

DTZ IAM progression of AUM over time ($’m)

Market position (continued)

*to Q2 2012

DTZ IAM businesses have enjoyed consistent organic AUM growth of around 25% annually over the decade

45

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012*

Assets under management

DTZ IM DTZ AM

For

per

sona

l use

onl

y

39%

41%

15%

5%

Core

Core plus

Value add

Opportunistic

25.6%

35.7%

21.8%

16.9% Retail

Offices

Industrial

Other

0%

20%

40%

60%

Advisory Discretionary 0%

25%

50%

75%

Pension Funds Other Institutions

Market position (continued)

Sector allocation (June 2012) Risk profile (June 2012)

Nature of mandate (June 2012) Sources of capital (June 2012)

We manage exclusively for institutional investors across a range of risk profiles

46

For

per

sona

l use

onl

y

Market position (continued)

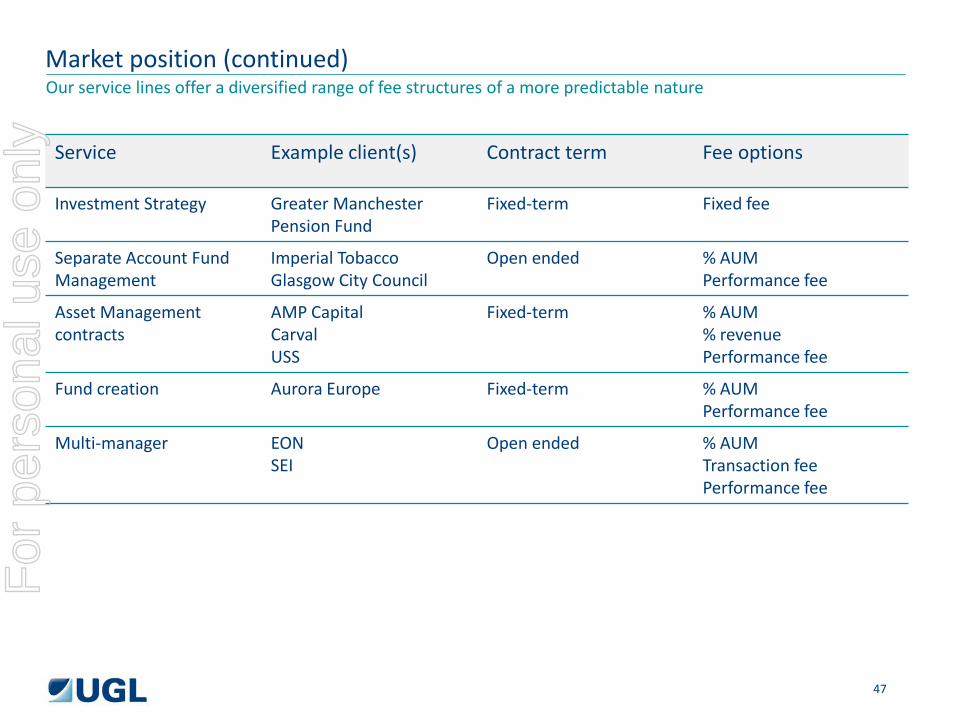

Service Example client(s) Contract term Fee options

Investment Strategy Greater Manchester Pension Fund

Fixed-term Fixed fee

Separate Account Fund Management

Imperial Tobacco Glasgow City Council

Open ended % AUM Performance fee

Asset Management contracts

AMP Capital Carval USS

Fixed-term % AUM % revenue Performance fee

Fund creation Aurora Europe Fixed-term % AUM Performance fee

Multi-manager EON SEI

Open ended % AUM Transaction fee Performance fee

Our service lines offer a diversified range of fee structures of a more predictable nature

47

For

per

sona

l use

onl

y

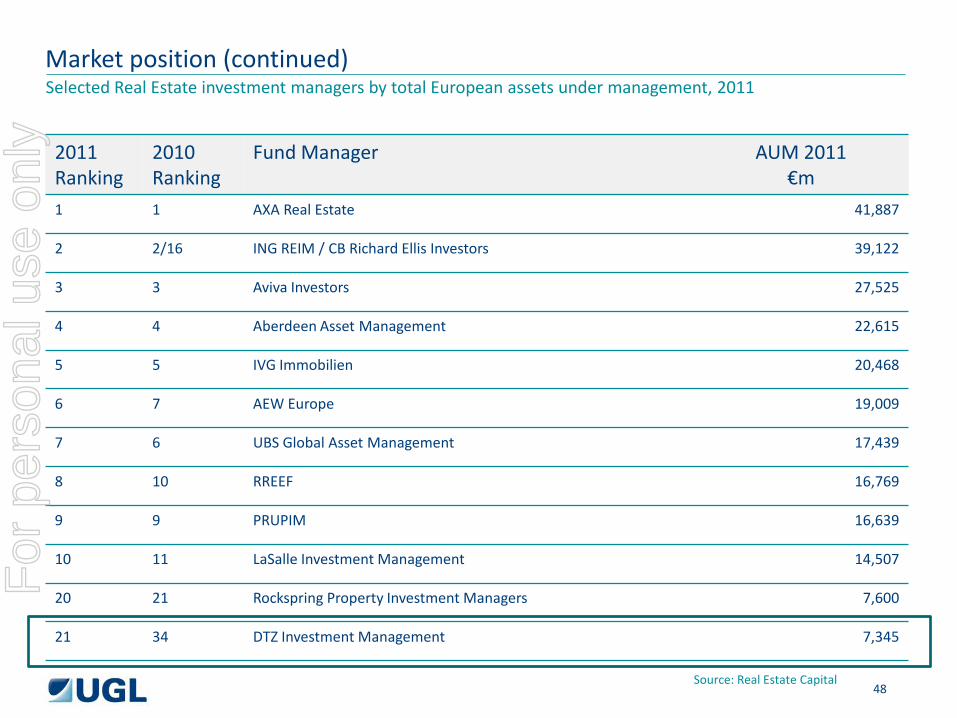

Market position (continued)

2011 Ranking

2010 Ranking

Fund Manager AUM 2011 €m

1 1 AXA Real Estate 41,887

2 2/16 ING REIM / CB Richard Ellis Investors 39,122

3 3 Aviva Investors 27,525

4 4 Aberdeen Asset Management 22,615

5 5 IVG Immobilien 20,468

6 7 AEW Europe 19,009

7 6 UBS Global Asset Management 17,439

8 10 RREEF 16,769

9 9 PRUPIM 16,639

10 11 LaSalle Investment Management 14,507

20 21 Rockspring Property Investment Managers 7,600

21 34 DTZ Investment Management 7,345

Source: Real Estate Capital

Selected Real Estate investment managers by total European assets under management, 2011

48

For

per

sona

l use

onl

y

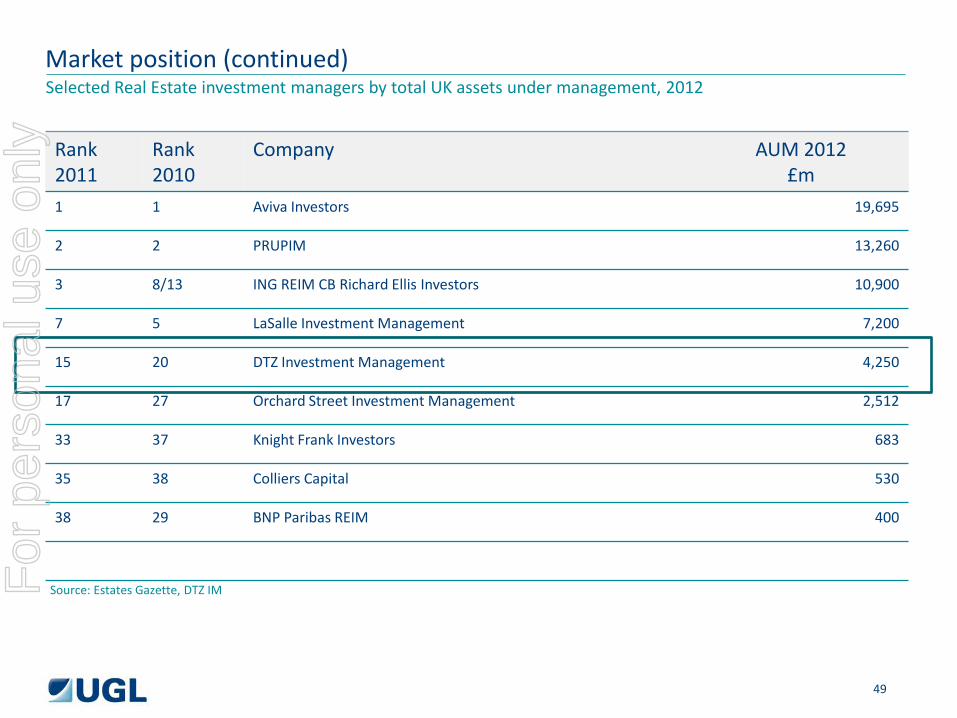

Market position (continued)

Rank 2011

Rank 2010

Company AUM 2012 £m

1 1 Aviva Investors 19,695

2 2 PRUPIM 13,260

3 8/13 ING REIM CB Richard Ellis Investors 10,900

7 5 LaSalle Investment Management 7,200

15 20 DTZ Investment Management 4,250

17 27 Orchard Street Investment Management 2,512

33 37 Knight Frank Investors 683

35 38 Colliers Capital 530

38 29 BNP Paribas REIM 400

Source: Estates Gazette, DTZ IM

Selected Real Estate investment managers by total UK assets under management, 2012

49

For

per

sona

l use

onl

y

Key differentiator 1 – our investment philosophy We have a unique occupier- focused investment philosophy that delivers investment outperformance.

Strategy

Identify economic growth areas, where

occupiers want to locate

Stock Selection Acquire assets that are flexible to occupiers’ needs now and in the

future

Management

Work in partnership with occupiers, so

they remain long-term clients

Occupier

50

For

per

sona

l use

onl

y

Key differentiator 2 – great, loyal people

• Broad range of seasoned investment professionals • Significant experience gained at DTZ IM • Very low levels of staff attrition • Significant non-executive support and governance from independent industry experts

Senior management average more than 25 years’ industry experience, half of which has been spent at DTZ.

51

For

per

sona

l use

onl

y

Key differentiator 3 – top rate long-term performance track record

100

200

300

400

500

600

700

800

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

DTZ IPD

DTZ IM total returns relative to UK index (1991 = 100)

Portfolios managed on a fully discretionary basis by DTZ have significantly outperformed the market

52

For

per

sona

l use

onl

y

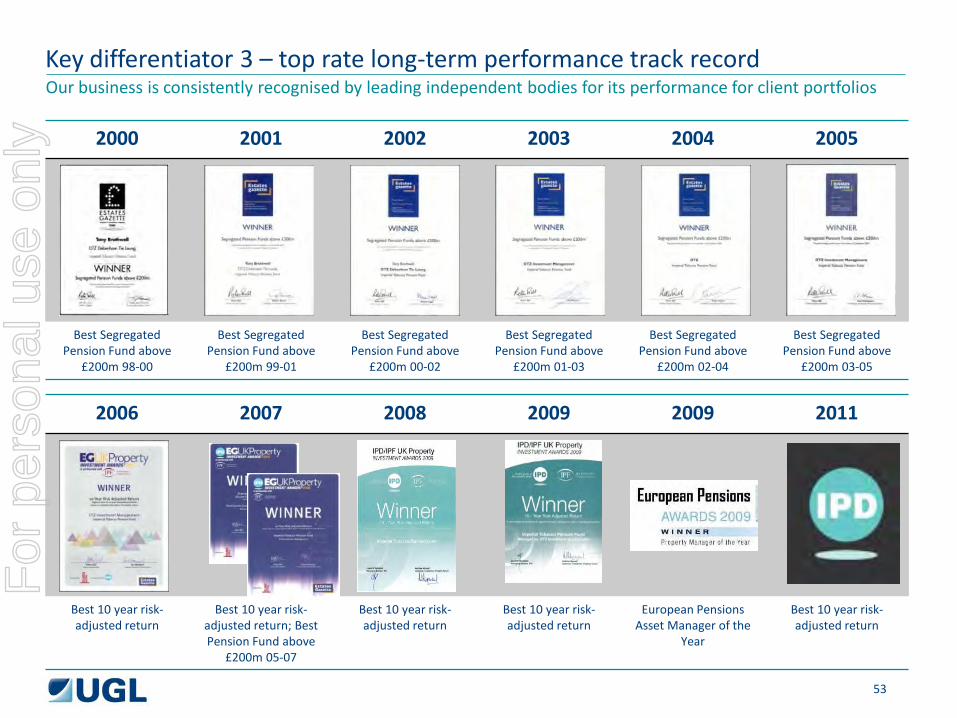

Key differentiator 3 – top rate long-term performance track record

2000 2001 2002 2003 2004 2005

Best Segregated Pension Fund above

£200m 98-00

Best Segregated Pension Fund above

£200m 99-01

Best Segregated Pension Fund above

£200m 00-02

Best Segregated Pension Fund above

£200m 01-03

Best Segregated Pension Fund above

£200m 02-04

Best Segregated Pension Fund above

£200m 03-05

Our business is consistently recognised by leading independent bodies for its performance for client portfolios

2006 2007 2008 2009 2009 2011

Best 10 year risk-adjusted return

Best 10 year risk-adjusted return; Best Pension Fund above

£200m 05-07

Best 10 year risk-adjusted return

Best 10 year risk-adjusted return

European Pensions Asset Manager of the

Year

Best 10 year risk-adjusted return

53

For

per

sona

l use

onl

y

Market drivers

• Property is still viewed as a sensible investment class for institutional investors in the context of a multi-asset class portfolio. This drives demand for our services

• Clients typically recognise the importance of income return. Having hands-on management capability remains

an advantage, with specialist managers seeing the fastest rates of organic growth • Banking turmoil will dominate the real estate investment management arena both in terms of the future

balance of the debt / equity profile in asset ownership, and the future of several major investment management platforms. We expect further consolidation in the fund management industry as a consequence

• Debt maturities and existing funds have a concentration of expiries in 2014-16, which may prove a significant

impact on asset pricing and investor appetite mid-term • Greater scrutiny and regulation is an inevitable consequence of property’s existence at the periphery of the

authorised investment world

54

For

per

sona

l use

onl

y

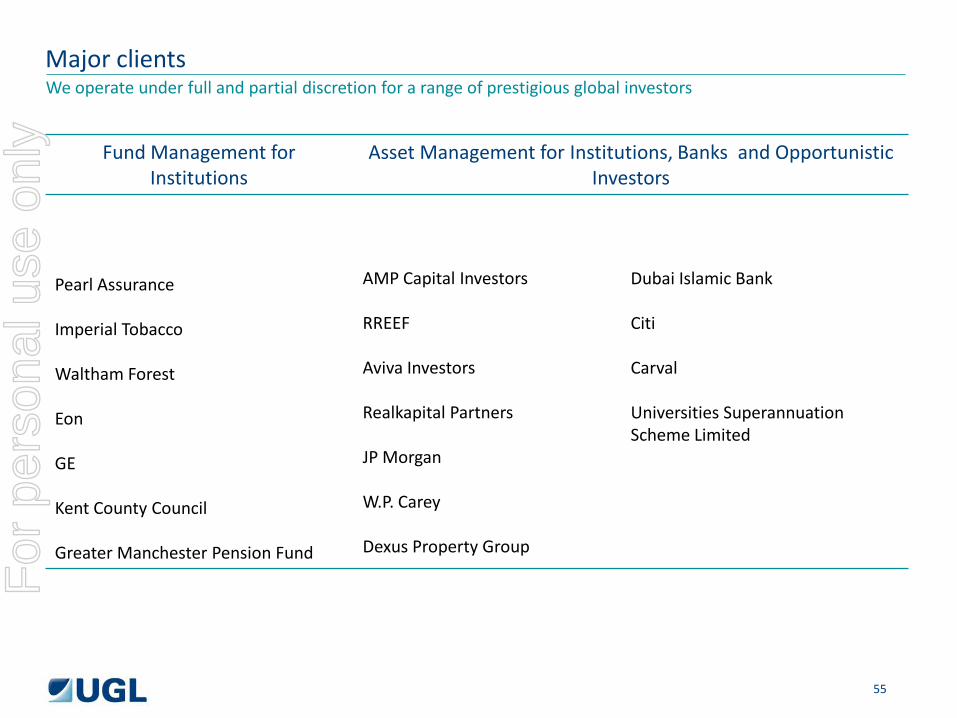

Major clients

Fund Management for Institutions

Asset Management for Institutions, Banks and Opportunistic Investors

Pearl Assurance Imperial Tobacco Waltham Forest Eon GE Kent County Council Greater Manchester Pension Fund

AMP Capital Investors RREEF Aviva Investors Realkapital Partners JP Morgan W.P. Carey Dexus Property Group

Dubai Islamic Bank Citi Carval Universities Superannuation Scheme Limited

We operate under full and partial discretion for a range of prestigious global investors

55

For

per

sona

l use

onl

y

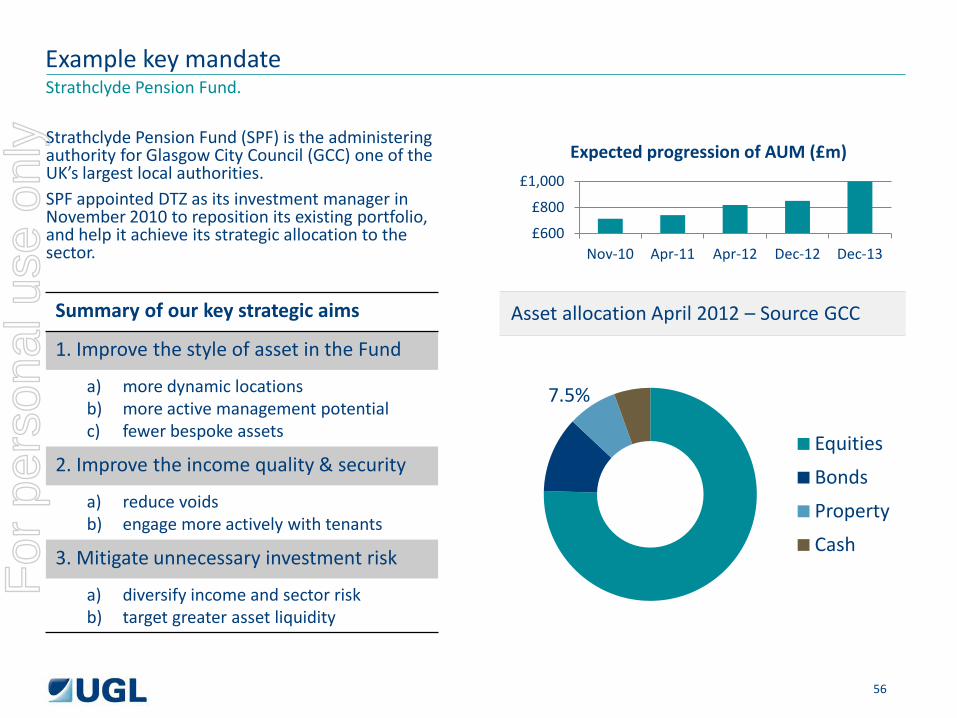

Strathclyde Pension Fund. Example key mandate

Asset allocation April 2012 – Source GCC

Strathclyde Pension Fund (SPF) is the administering authority for Glasgow City Council (GCC) one of the UK’s largest local authorities. SPF appointed DTZ as its investment manager in November 2010 to reposition its existing portfolio, and help it achieve its strategic allocation to the sector.

£600

£800

£1,000

Nov-10 Apr-11 Apr-12 Dec-12 Dec-13

Expected progression of AUM (£m)

Summary of our key strategic aims

1. Improve the style of asset in the Fund

a) more dynamic locations b) more active management potential c) fewer bespoke assets

2. Improve the income quality & security

a) reduce voids b) engage more actively with tenants

3. Mitigate unnecessary investment risk

a) diversify income and sector risk b) target greater asset liquidity

7.5%

Equities

Bonds

Property

Cash

56

For

per

sona

l use

onl

y

George Keches, Chief Executive

Americas

57

For

per

sona

l use

onl

y

Overview

The Americas

3 countries 63 offices 33,442 employees

Locations Alexandria Arlington Atlanta Auburndale Austin Bloomfield Boston Burnaby Calgary Charlotte Chicago

Cincinnati Costa Mesa Dallas Denver Detroit East Hartford Edmonton Halifax Houston Indianapolis Iselin

Kansas City Kelowna Kingston London Los Angeles Mexico City Miami Lakes Milwaukee Minneapolis Mississauga Montreal

Nanaimo New York Niagra Ottawa Palo Alto Penrose Philadelphia Phoenix Pittsburg Raleigh Regina

Reno Richmond Hill Sacramento San Francisco San Jose Seattle South Portland St. Laurent St. Louis Tampa Toronto

Vancouver Victoria Washington, D.C. Waterloo Wilson Winnipeg

58

For

per

sona

l use

onl

y

Facilities Services • Facilities Management • Operations and

Maintenance • Energy Services • Janitorial • Landscaping • Office Services

Overview Service Offerings

Real Estate Services • Portfolio Management • Data Management • Capital Market Services • Project Services • Strategic Consulting • Technology Consulting • Transaction Advisory • Audit and Recovery • Workplace Integration • Development Services • Site Selection and Incentives

Consulting

59

For

per

sona

l use

onl

y

#1 Most Recommended Real Estate Firm in North America Identified as the #1 Tenant Representation firm in the world and the most highly recommended service provider among 23 evaluated corporate real estate services firms.

BOMA Building of the Year TOBY Awards Many of our customers across North America have received this distinction which recognizes excellence in property management, tenant services, customer service, facility services, energy management and other superior performance measures.

Overview Distinctions

60

For

per

sona

l use

onl

y

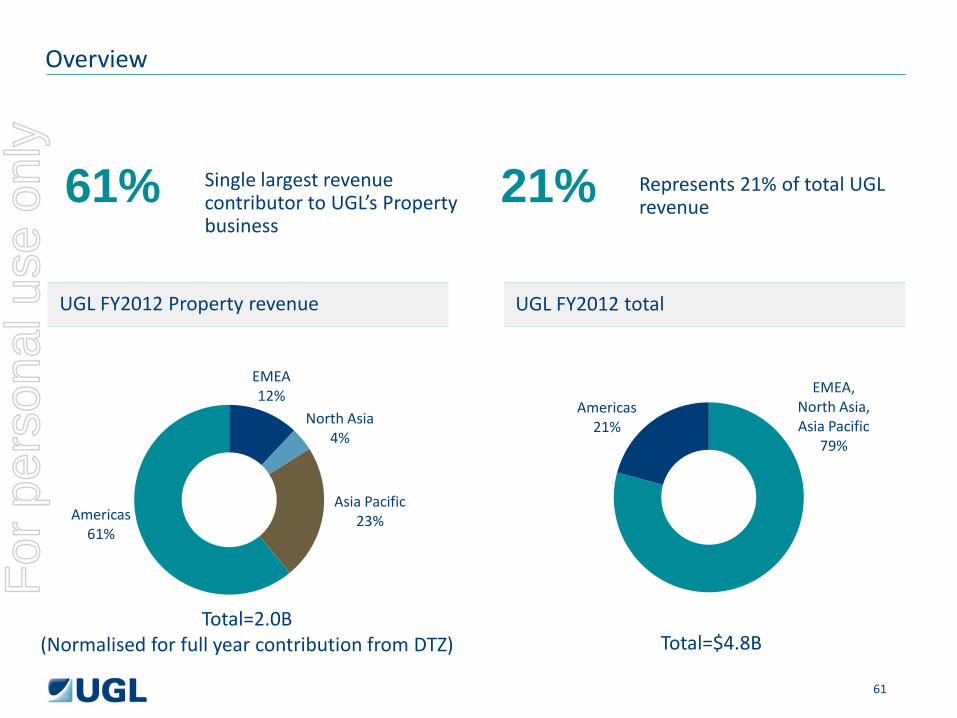

Overview

Total=2.0B (Normalised for full year contribution from DTZ)

Single largest revenue contributor to UGL’s Property business

61% 21%

EMEA, North Asia, Asia Pacific

79%

Americas 21%

Represents 21% of total UGL revenue

Total=$4.8B

EMEA 12%

North Asia 4%

Asia Pacific 23% Americas

61%

UGL FY2012 Property revenue UGL FY2012 total

61

For

per

sona

l use

onl

y

Education 16%

Finance & Insurance 11%

Government 3%

Manufacturing 30% Other 9%

Public Venue 7%

Commercial/ Office 19%

Retail 6%

Overview Broad customer base

Total=$976m

62

For

per

sona

l use

onl

y

Key differentiators

• Leverage large national presence

• Fully integrated, end-to-end services

• 17,000+ in-house workforce

• Majority of services self-performed

• Relationships with multi-levels of buyers

• Consolidated financial reporting

• One-stop shopping

• First-to-market - Sustainability

63

For

per

sona

l use

onl

y

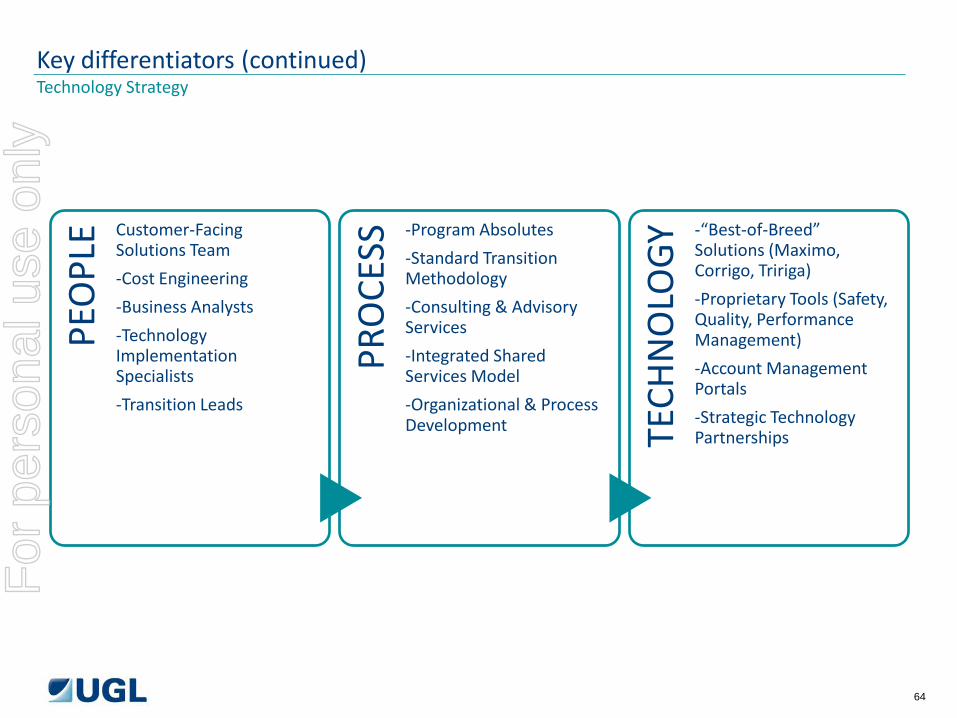

PEO

PLE Customer-Facing

Solutions Team

-Cost Engineering

-Business Analysts

-Technology Implementation Specialists

-Transition Leads

PRO

CESS

-Program Absolutes

-Standard Transition Methodology

-Consulting & Advisory Services

-Integrated Shared Services Model

-Organizational & Process Development TE

CHN

OLO

GY -“Best-of-Breed”

Solutions (Maximo, Corrigo, Tririga)

-Proprietary Tools (Safety, Quality, Performance Management)

-Account Management Portals

-Strategic Technology Partnerships

Key differentiators (continued) Technology Strategy

64

For

per

sona

l use

onl

y

1.9%

2.2%

1.8%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

2011 2012F 2013F

USA

Investment transaction volume growth Office occupational rental growth

Americas property market indicators

12% 2%

28%

-

10

20

30

40

50

60

70

80

2011 2012F 2013F

USA

AUD (bn)

Comprises all sector investment transactions recoded nationally

Annual growth

Comprises office rents

Source: DTZ Research 65

For

per

sona

l use

onl

y

Market drivers

CRE: Grow in Tier I Markets • Big Markets, (i.e. New York, Boston, Dallas, Houston, San Francisco, Los Angeles) drive global transaction

business. Significant potential for growth in these markets Develop Investment Agency/Capital Markets • Big market, robust fees, synergistic with CRE business, can leverage talent on top of our current platform Integrate CRE and FM Capabilities to Secure E2E Accounts • Outsourcing trend increasing • The market desires a third choice

Continued Pressure on Regional Firms will Drive Further Consolidation of Property Services Sector • Scarcity of capital to fund growth and infrastructure will drive smaller players to seek larger platforms Self-Delivery of FM Services Gaining in Popularity • Greater “cost out” value proposition versus managing agent providers Upsell to Existing Customer Base • Significant potential to expand CRE/FM services across multiple locations • Take advantage of existing relationships

66

For

per

sona

l use

onl

y

Recent Wins

Major Retail Grocery Chain

Bank of America World-leading Pharmaceutical Company

Sun Life Stadium

Recent Major Contracts

• 5-year contract for facilities management for the iconic Florida stadium--home to the Miami Dolphins football team.

• 3-year contract to provide facilities management services for 750 stores in North America.

• 5-year contract for Integrated Facilities Management and Project Management.

• United States—”Follow your customer” strategy.

• Relationship began five years ago with locations in Northeast.

• Expanded to Southern California.

• Re-bid has expanded us into Northern California.

• Presence on west coast has opened up business opportunities and recent wins.

67

For

per

sona

l use

onl

y

Major clients

LOGISTICS A US-based logistics services company.

EDUCATION A west coast American private research university with the largest contiguous university campus in the US.

AUTOMOBILE One of the world’s largest automobile manufacturers.

Item

HEALTH CARE A leading health care company headquartered in the US offering insurance products and health and wellness services.

INDUSTRIAL The largest, privately-held corporation (revenue). International producer and marketer of food, agricultural, financial and industrial products and services.

AEROSPACE A world-leading provider of power systems and services for use on land, at sea and in the air.

XpressLetter

68

For

per

sona

l use

onl

y

End-to-end solutions platform built to respond to the exacting needs of our clients

Key Mandates

• Portfolio management • Transaction advisory • Strategic consulting • Project management • Corporate finance • Facilities management • Data management • Software consulting services

• Rolls-Royce, North America • 15 years of service • End-to-end Delivery

• Portfolio management • Transaction advisory • Strategic consulting • Integrated facilities management • Project management

• Zurich, North America • 18 years of service • End-to-end Delivery

74 properties, 7.2 million sq ft 441 locations, 8.9 million sq ft

69

For

per

sona

l use

onl

y

Edward Cheung, Chief Executive

North Asia

70

For

per

sona

l use

onl

y

North Asia business overview

Coverage

Services

Focus

• 4,323 employees • 21 cities • 5 countries

• Investment Agency • Occupational & Development

Markets • Residential agency • Valuation

• Establish a large base of stable revenue streams from professional services

• Further develop one-stop service platforms • Identify and develop emerging high margin business

opportunities • Enhance cross-border deal flows

• Property and Facilities Management

• Building Consultancy & Project Management

• Consulting & Research

71

For

per

sona

l use

onl

y

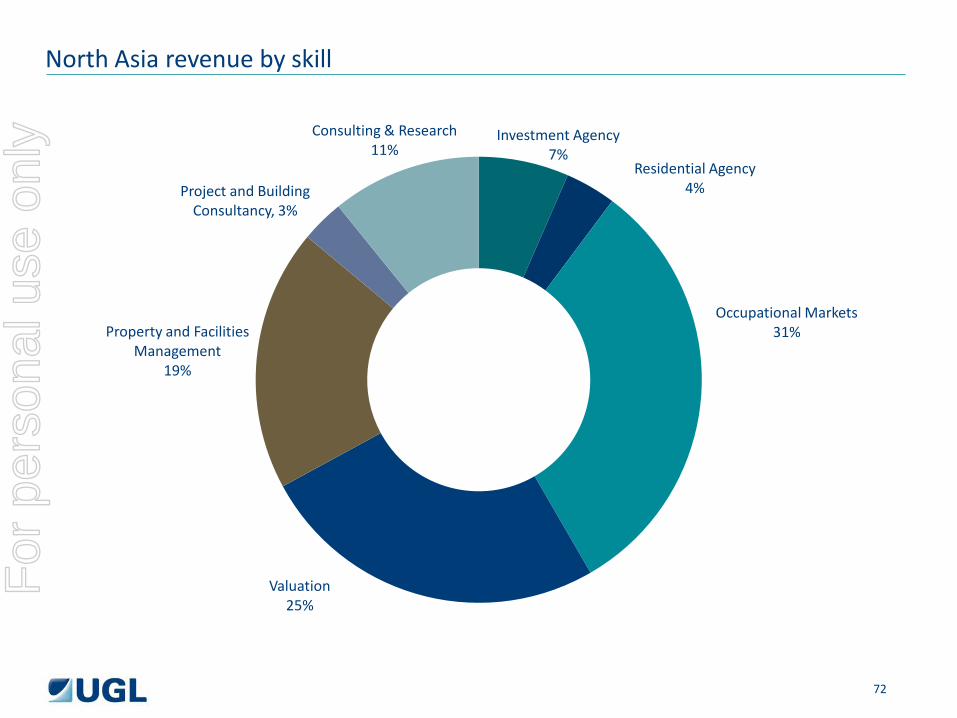

North Asia revenue by skill

Investment Agency 7%

Residential Agency 4%

Occupational Markets 31%

Valuation 25%

Project and Building Consultancy, 3%

Consulting & Research 11%

Property and Facilities Management

19%

72

For

per

sona

l use

onl

y

North Asia differentiators

• With the combined power of UGL and DTZ, we have the most diversified service capability

• We are #1 in valuation business in the North Asia region

• We have the largest foot print in Greater China

• Our brand is synonymous with quality real estate services with integrity in China

• We have the strongest track record of government and local clients appointments

73

For

per

sona

l use

onl

y

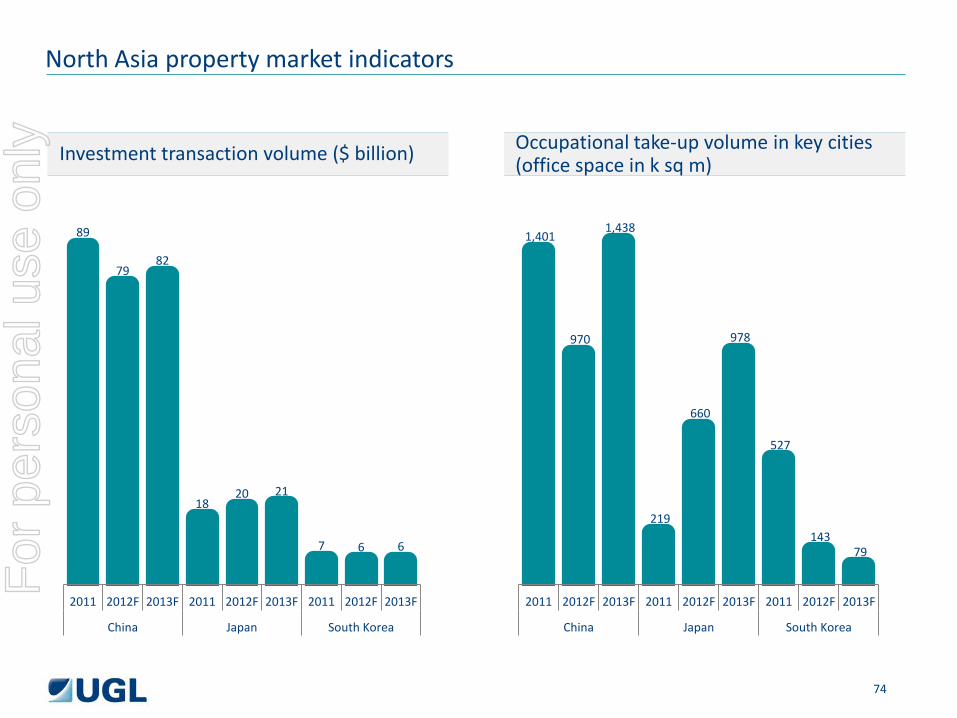

1,401

970

1,438

219

660

978

527

143 79

2011 2012F 2013F 2011 2012F 2013F 2011 2012F 2013F

China Japan South Korea

Investment transaction volume ($ billion) Occupational take-up volume in key cities (office space in k sq m)

North Asia property market indicators

89

79 82

18 20 21

7 6 6

2011 2012F 2013F 2011 2012F 2013F 2011 2012F 2013F

China Japan South Korea

74

For

per

sona

l use

onl

y

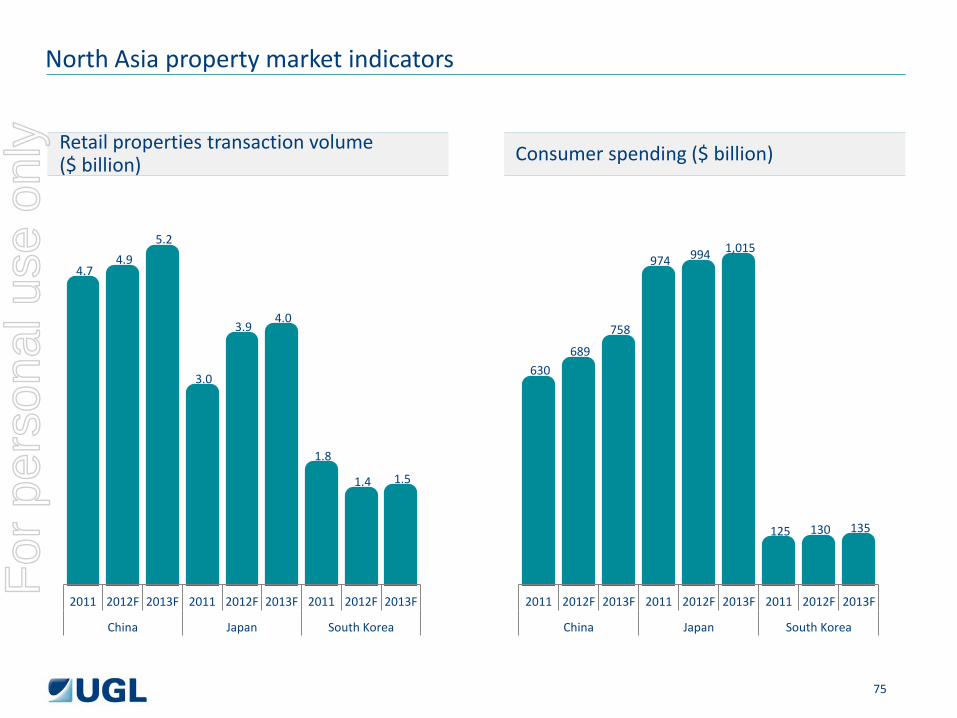

630 689

758

974 994 1,015

125 130 135

2011 2012F 2013F 2011 2012F 2013F 2011 2012F 2013F

China Japan South Korea

Retail properties transaction volume ($ billion) Consumer spending ($ billion)

North Asia property market indicators

4.7 4.9

5.2

3.0

3.9 4.0

1.8

1.4 1.5

2011 2012F 2013F 2011 2012F 2013F 2011 2012F 2013F

China Japan South Korea

75

For

per

sona

l use

onl

y

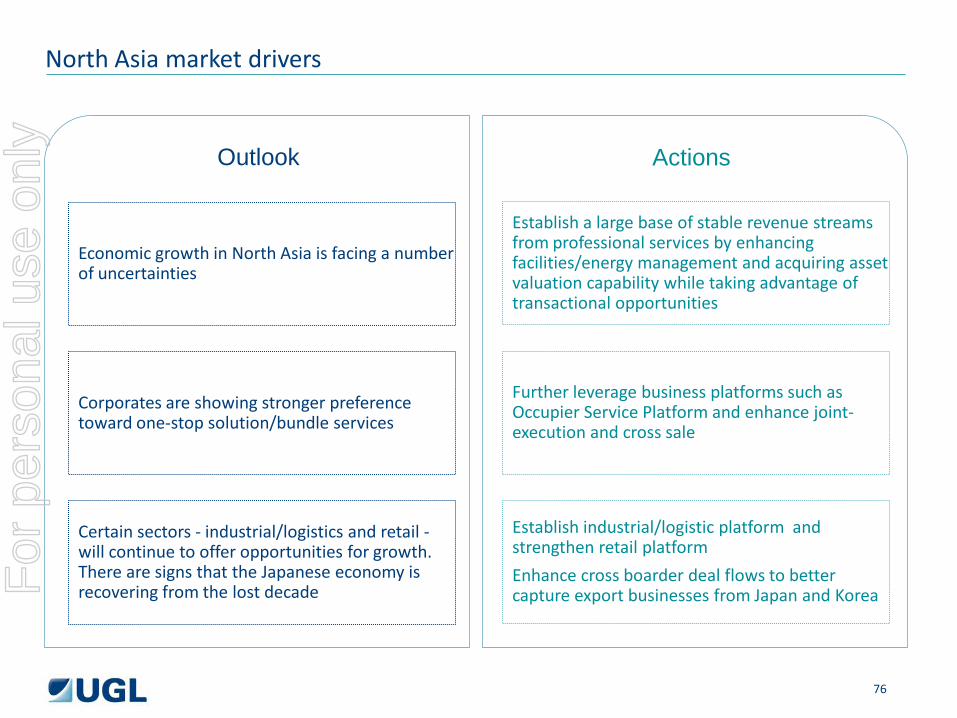

North Asia market drivers

Economic growth in North Asia is facing a number of uncertainties

Corporates are showing stronger preference toward one-stop solution/bundle services

Certain sectors - industrial/logistics and retail - will continue to offer opportunities for growth. There are signs that the Japanese economy is recovering from the lost decade

Outlook Actions

Establish a large base of stable revenue streams from professional services by enhancing facilities/energy management and acquiring asset valuation capability while taking advantage of transactional opportunities

Further leverage business platforms such as Occupier Service Platform and enhance joint-execution and cross sale

Establish industrial/logistic platform and strengthen retail platform

Enhance cross boarder deal flows to better capture export businesses from Japan and Korea

76

For

per

sona

l use

onl

y

North Asia major clients

Volvo • Providing full project management

services for Volvo’s Technical Centre in China

Akzo Nobel • Provided occupier transaction

management and project management services for Akzo Nobel’s office space

Tencent • Providing office space planning and

facilities management consultancy services

HSBC • Working as the exclusive valuer for

the mortgage services of HSBC in Hong Kong

China Merchant Group • Providing development

consultancy and property management services for multiple properties

77

Intel • Provided investment agency

service for Intel’s site disposal in Shanghai F

or p

erso

nal u

se o

nly

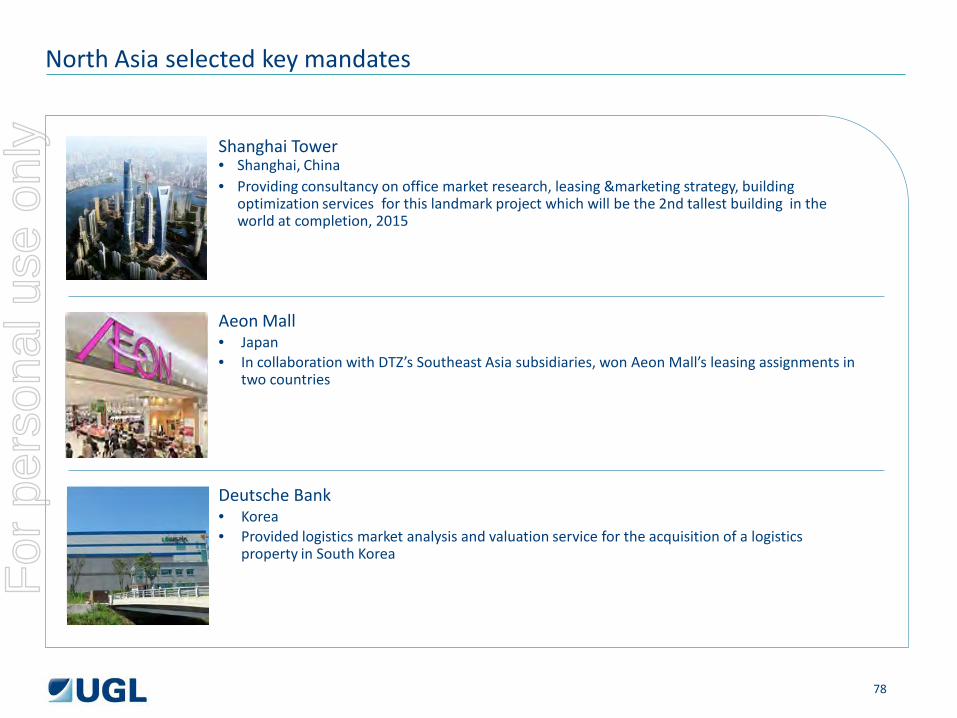

Shanghai Tower • Shanghai, China • Providing consultancy on office market research, leasing &marketing strategy, building

optimization services for this landmark project which will be the 2nd tallest building in the world at completion, 2015

North Asia selected key mandates

Aeon Mall • Japan • In collaboration with DTZ’s Southeast Asia subsidiaries, won Aeon Mall’s leasing assignments in

two countries

Deutsche Bank • Korea • Provided logistics market analysis and valuation service for the acquisition of a logistics

property in South Korea

78

For

per

sona

l use

onl

y

Adam Catchpole

Global Corporate Services - Asia

79

For

per

sona

l use

onl

y

GCS business overview

Coverage

Services

Focus

• 9 FT employees • Core hubs in US, UK and Asia (Hong Kong/Singapore) • Deliver across all UGL/DTZ geographies

• Client management and sales support • Transaction management • Real estate administration • Portfolio planning and strategy • Delivery portal for E2E service delivery

• Drive profitable revenue growth • Grow the scale of fee-earning team • Consolidate platform and infrastructure to deliver E2E

80

For

per

sona

l use

onl

y

• Extensive knowledge of best practices and dedication to

continual improvement

• Core team accountability

• Experienced global account management capabilities

• Technology sector experts • Senior level engagement

• Collaboration and innovation

GCS key differentiators

81

For

per

sona

l use

onl

y

GCS market drivers

Global outsourcing is continuing - no longer a trend or fad

Corporations are strengthening the financial accounting and control over lease and other associated RE expenditures – in light of FASB 6 changes

Portfolio software is being also centralized into global property databases – with corporations owning the system vs. suppliers but outsourcing collection and management

Supplier outsourcing models are getting more regionalized with a focus on best in class broker model - Consolidation of suppliers e.g TNT 8 into 2

Our access to that market is increasing due to our enhanced ability to deliver globally and across multiple skill lines

C-suite is tasking CRE to become more strategic to support the business. Facilities Management, Lease Administration, Brokerage, Workplace Services, Project Management

82

For

per

sona

l use

onl

y

GCS opportunities : growth drivers

Services

• Development of E2E delivery platform

• Development of Occupier Services platform across the region

• Building export opportunities from India and China

• Developing the regional platform for GCS - India and China

• Leveraging the global platform

Resources

• Enhance talent resources through selective hire

• Training and development

83

For

per

sona

l use

onl

y

GCS market drivers Evolution of the corporate real estate outsourcing market

Pre- 1980s ‘80s to mid-’90s

Mid-’90s to 2000

Early 2000s to mid-2000s

Mid-2000s and onward

Self-perform Out-tasking Outsourcing Integrated facilities management

Global integrated business services

Most, if not all, activities are performed in-house

Low-tech services such as cleaning, security, food services and landscaping are individually sourced by different locations to external providers.

A combination of low-tech and high-tech services - such as electrical, mechanical and environmental – are outsourced in service bundles.

Facilities management and real estate services are outsourced to a single service provider, which manages sub contractors.

Facilities management and real estate services are organizationally aligned with other support services – such as finance, HR, procurement and IT – and outsourced in a global bundle across business units. Bundled business process outsourcing (BPO) across multiple functions is emerging as an option.

84

For

per

sona

l use

onl

y

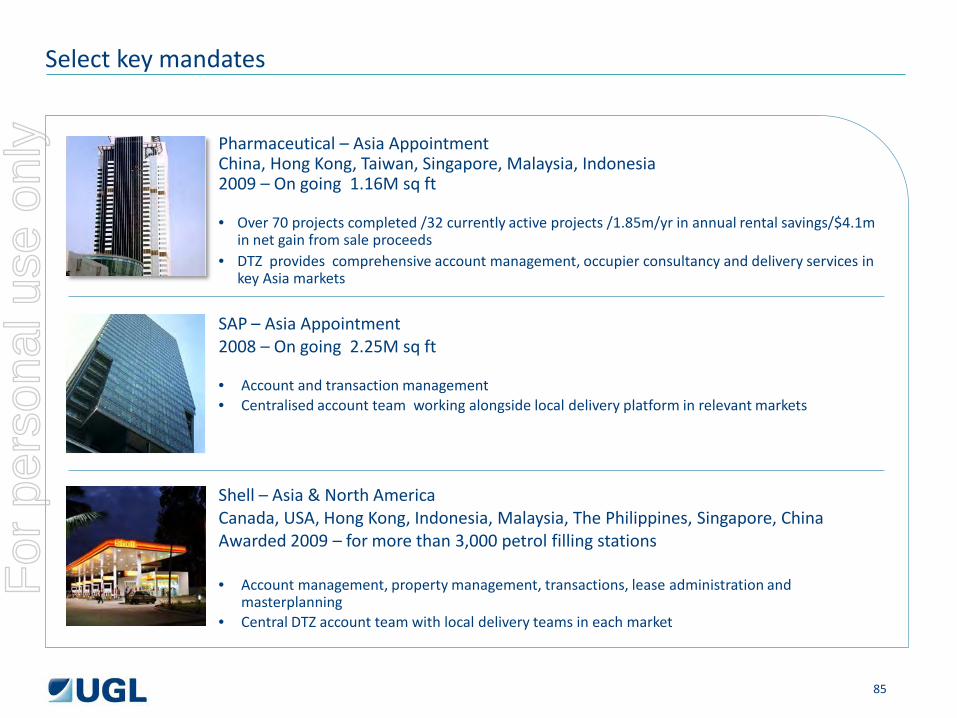

Pharmaceutical – Asia Appointment China, Hong Kong, Taiwan, Singapore, Malaysia, Indonesia 2009 – On going 1.16M sq ft • Over 70 projects completed /32 currently active projects /1.85m/yr in annual rental savings/$4.1m

in net gain from sale proceeds • DTZ provides comprehensive account management, occupier consultancy and delivery services in

key Asia markets

Select key mandates

SAP – Asia Appointment 2008 – On going 2.25M sq ft • Account and transaction management • Centralised account team working alongside local delivery platform in relevant markets

Shell – Asia & North America Canada, USA, Hong Kong, Indonesia, Malaysia, The Philippines, Singapore, China Awarded 2009 – for more than 3,000 petrol filling stations • Account management, property management, transactions, lease administration and

masterplanning • Central DTZ account team with local delivery teams in each market

85

For

per

sona

l use

onl

y

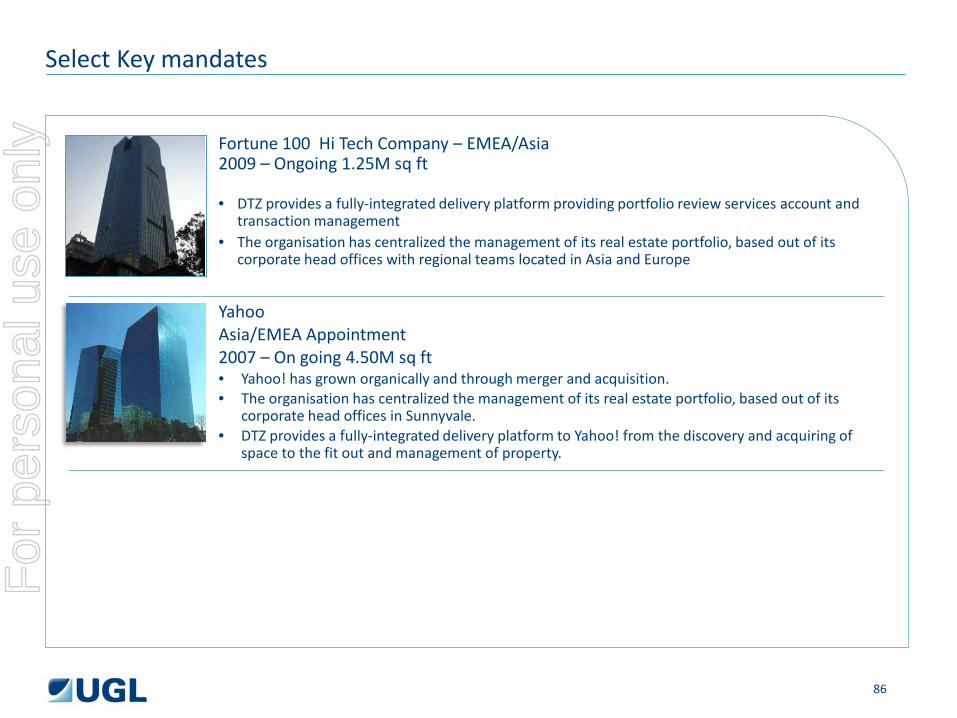

Fortune 100 Hi Tech Company – EMEA/Asia 2009 – Ongoing 1.25M sq ft

• DTZ provides a fully-integrated delivery platform providing portfolio review services account and

transaction management • The organisation has centralized the management of its real estate portfolio, based out of its

corporate head offices with regional teams located in Asia and Europe

Select Key mandates

Yahoo Asia/EMEA Appointment 2007 – On going 4.50M sq ft • Yahoo! has grown organically and through merger and acquisition. • The organisation has centralized the management of its real estate portfolio, based out of its

corporate head offices in Sunnyvale. • DTZ provides a fully-integrated delivery platform to Yahoo! from the discovery and acquiring of

space to the fit out and management of property.

86

For

per

sona

l use

onl

y

Mark Price, Head of Business Space, North Asia

Occupier and Development Markets (ODM), North Asia

87

For

per

sona

l use

onl

y

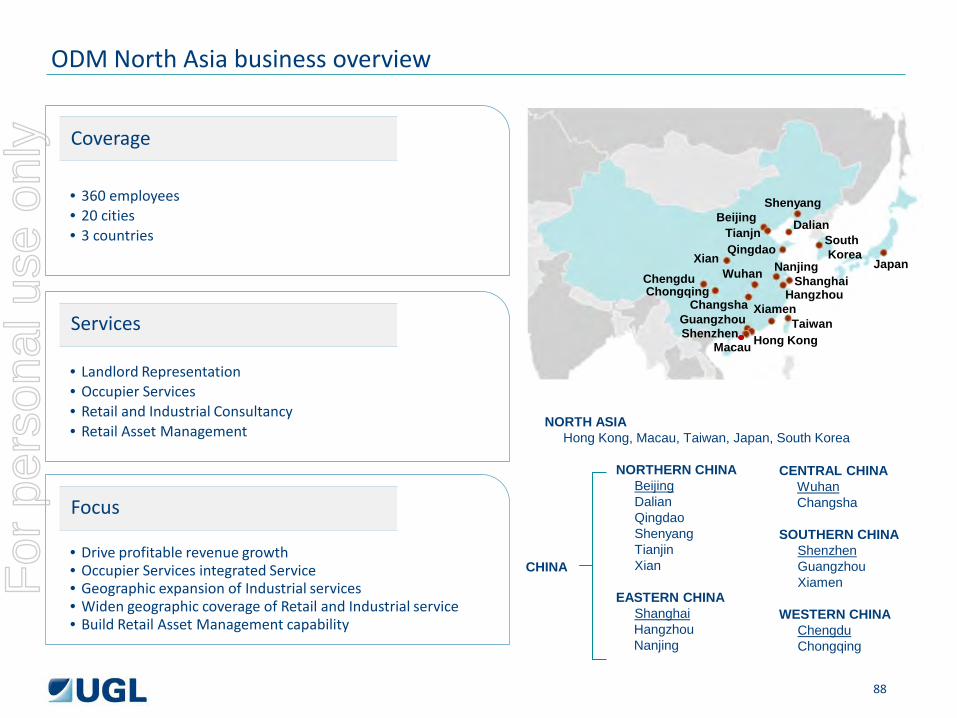

ODM North Asia business overview

Coverage

Services

Focus

• 360 employees • 20 cities • 3 countries

• Landlord Representation • Occupier Services • Retail and Industrial Consultancy • Retail Asset Management

• Drive profitable revenue growth • Occupier Services integrated Service • Geographic expansion of Industrial services • Widen geographic coverage of Retail and Industrial service • Build Retail Asset Management capability

NORTH ASIA Hong Kong, Macau, Taiwan, Japan, South Korea

CENTRAL CHINA Wuhan Changsha

SOUTHERN CHINA

Shenzhen Guangzhou Xiamen

WESTERN CHINA

Chengdu Chongqing

Guangzhou Shenzhen

Xiamen

Chengdu Chongqing

Xian

Beijing Dalian Tianjn Qingdao

Hangzhou

Wuhan

Changsha

Nanjing Shanghai

Taiwan Hong Kong

South Korea

Japan

Macau

NORTHERN CHINA Beijing Dalian Qingdao Shenyang Tianjin Xian

EASTERN CHINA

Shanghai Hangzhou Nanjing

CHINA

Shenyang

88

For

per

sona

l use

onl

y

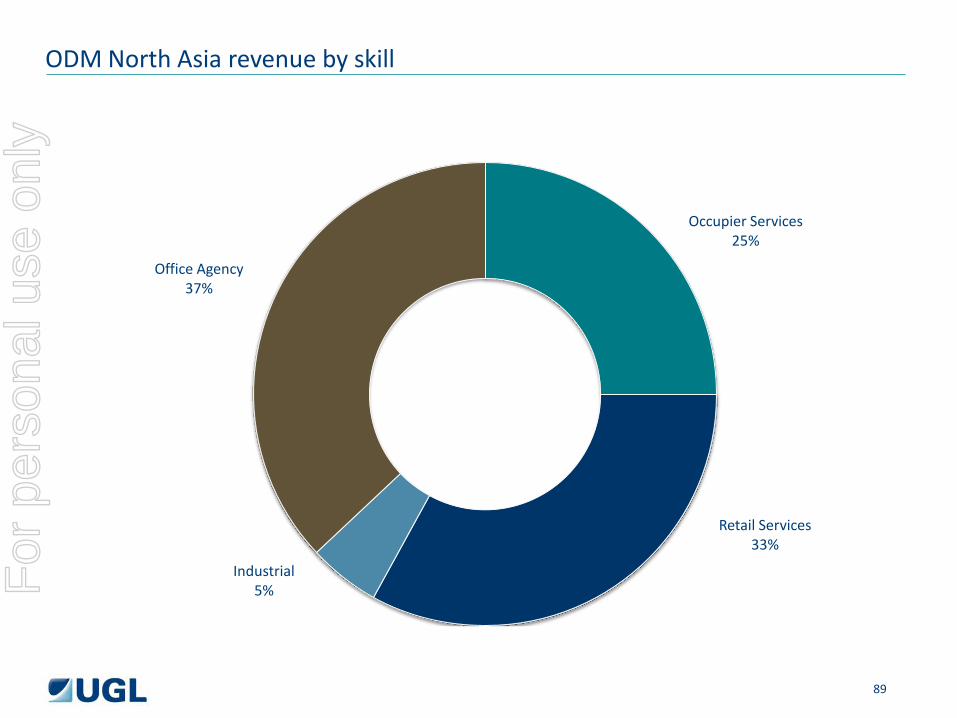

ODM North Asia revenue by skill

Occupier Services 25%

Retail Services 33%

Industrial 5%

Office Agency 37%

89

For

per

sona

l use

onl

y

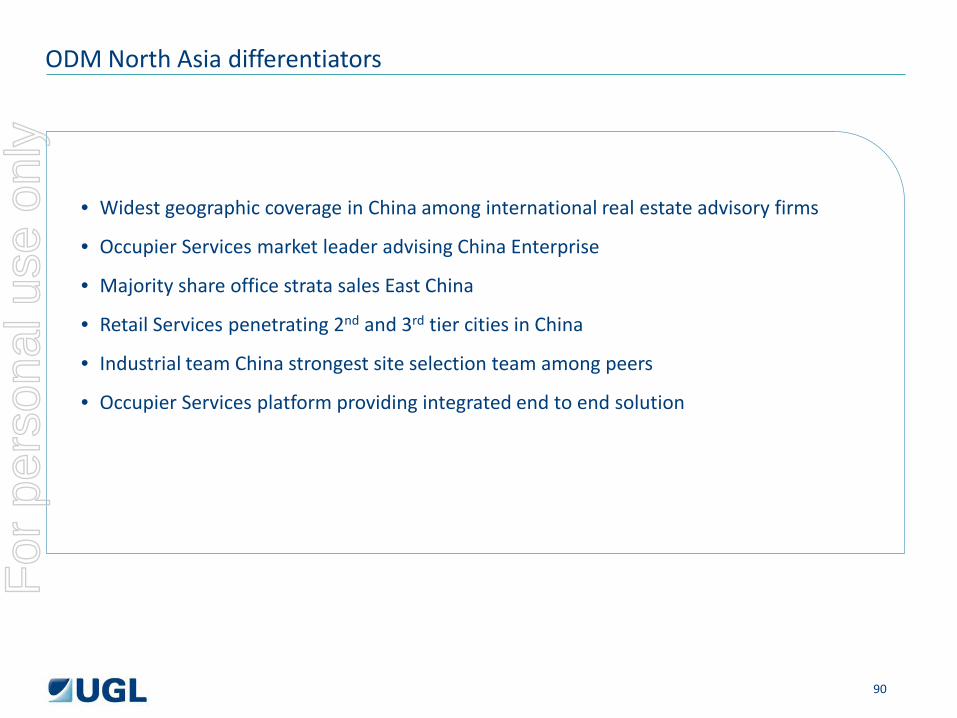

ODM North Asia differentiators

• Widest geographic coverage in China among international real estate advisory firms

• Occupier Services market leader advising China Enterprise

• Majority share office strata sales East China

• Retail Services penetrating 2nd and 3rd tier cities in China

• Industrial team China strongest site selection team among peers

• Occupier Services platform providing integrated end to end solution

90

For

per

sona

l use

onl

y

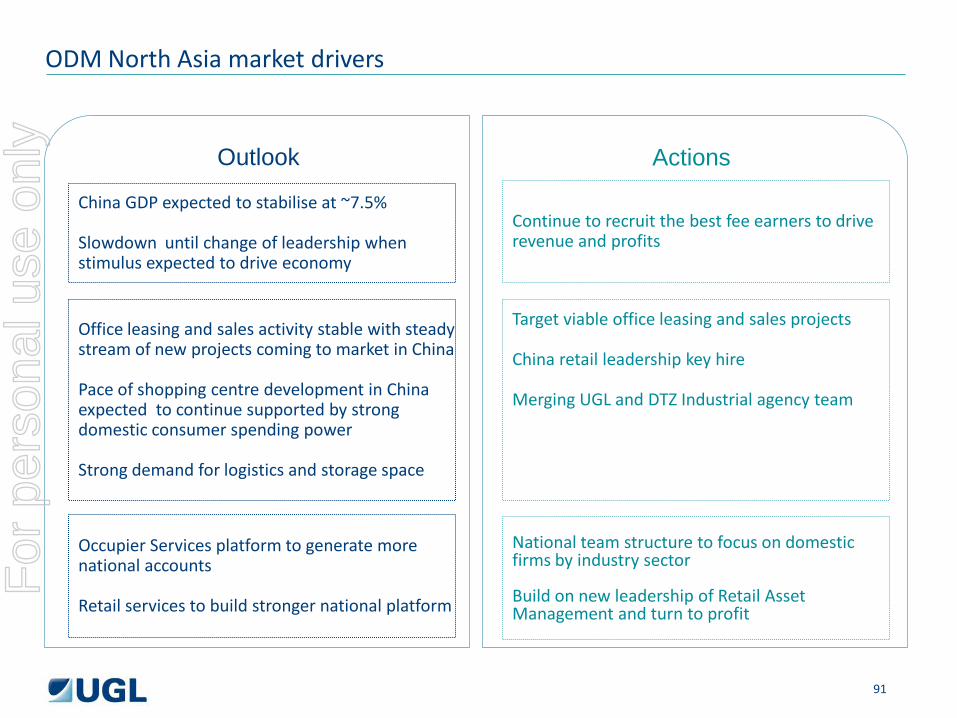

ODM North Asia market drivers

China GDP expected to stabilise at ~7.5% Slowdown until change of leadership when stimulus expected to drive economy

Office leasing and sales activity stable with steady stream of new projects coming to market in China Pace of shopping centre development in China expected to continue supported by strong domestic consumer spending power Strong demand for logistics and storage space

Occupier Services platform to generate more national accounts Retail services to build stronger national platform

Outlook Actions

Continue to recruit the best fee earners to drive revenue and profits

Target viable office leasing and sales projects China retail leadership key hire Merging UGL and DTZ Industrial agency team

National team structure to focus on domestic firms by industry sector Build on new leadership of Retail Asset Management and turn to profit

91

For

per

sona

l use

onl

y

ODM North Asia major clients

Regus • Occupier Services

• Lease acquisitions in multiple cities China

Alibaba • Occupier Services

• Lease acquisitions China

International Bank • Occupier Services

• Bank branch roll out program in 30 plus cities in China

Vanke • Retail Consultancy and leasing

services for 2 new shopping centres North China

Rreef • Leasing services for 800k sq ft

office tower Dalian China

Intel • Site disposal in Weigeijao Shanghai

92

Banking client

For

per

sona

l use

onl

y

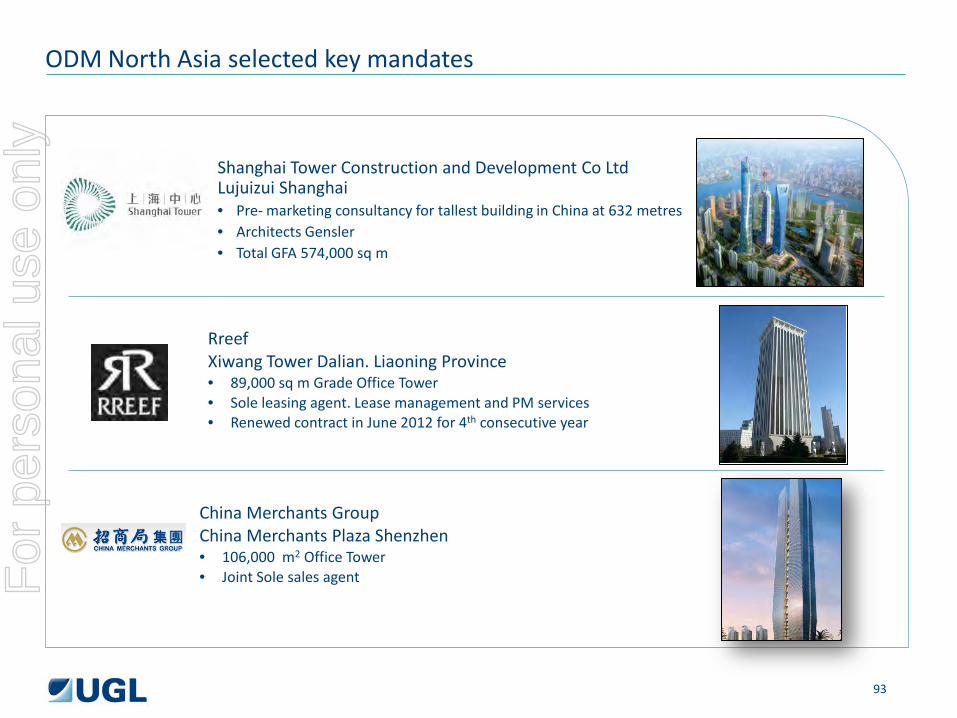

Shanghai Tower Construction and Development Co Ltd Lujuizui Shanghai • Pre- marketing consultancy for tallest building in China at 632 metres • Architects Gensler • Total GFA 574,000 sq m

ODM North Asia selected key mandates

Rreef Xiwang Tower Dalian. Liaoning Province • 89,000 sq m Grade Office Tower • Sole leasing agent. Lease management and PM services • Renewed contract in June 2012 for 4th consecutive year

China Merchants Group China Merchants Plaza Shenzhen • 106,000 m2 Office Tower • Joint Sole sales agent

93

For

per

sona

l use

onl

y

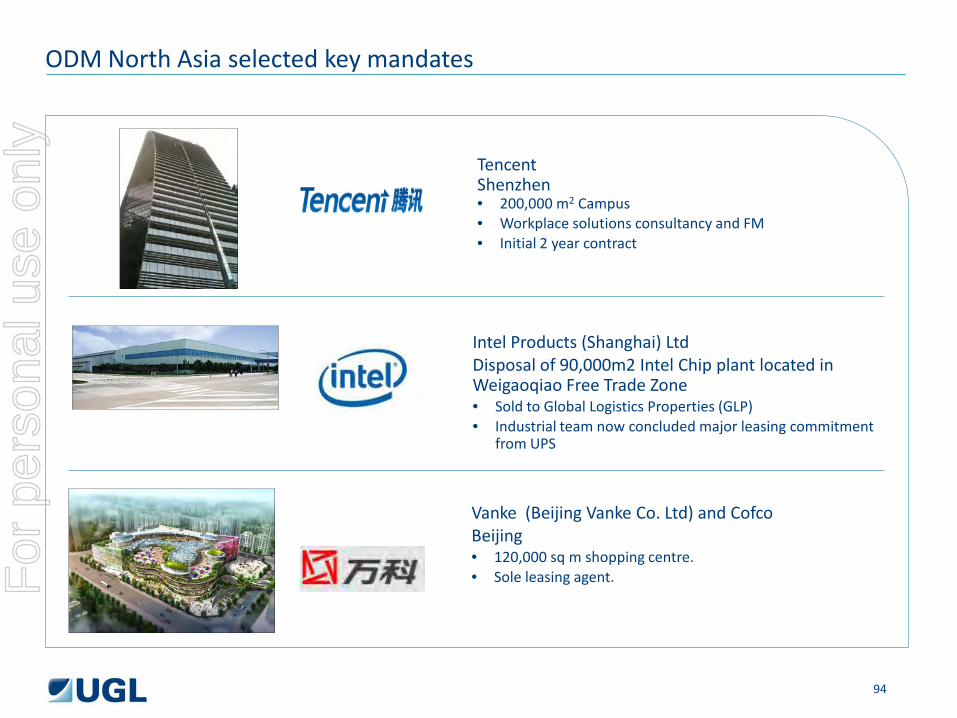

Intel Products (Shanghai) Ltd Disposal of 90,000m2 Intel Chip plant located in Weigaoqiao Free Trade Zone • Sold to Global Logistics Properties (GLP) • Industrial team now concluded major leasing commitment

from UPS

Tencent Shenzhen • 200,000 m2 Campus • Workplace solutions consultancy and FM • Initial 2 year contract

Vanke (Beijing Vanke Co. Ltd) and Cofco Beijing • 120,000 sq m shopping centre. • Sole leasing agent.

ODM North Asia selected key mandates

94

For

per

sona

l use

onl

y

Henry Arundel, Chief Executive Southeast Asia / Australia and New Zealand

Asia Pacific

95

For

per

sona

l use

onl

y

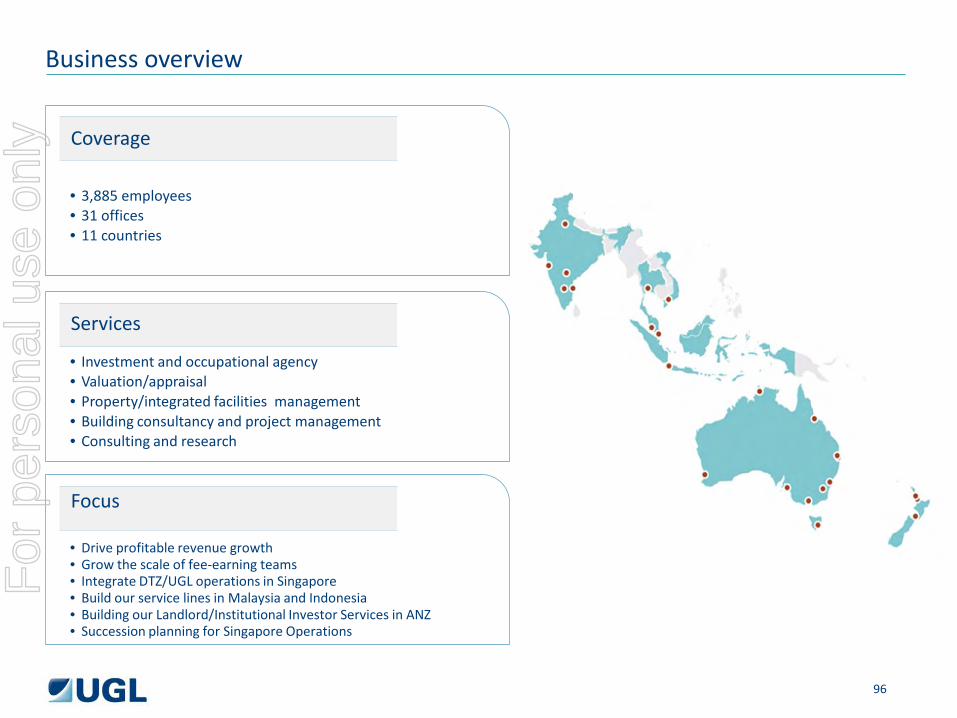

Business overview

Coverage

Services

Focus

• 3,885 employees • 31 offices • 11 countries

• Investment and occupational agency • Valuation/appraisal • Property/integrated facilities management • Building consultancy and project management • Consulting and research

• Drive profitable revenue growth • Grow the scale of fee-earning teams • Integrate DTZ/UGL operations in Singapore • Build our service lines in Malaysia and Indonesia • Building our Landlord/Institutional Investor Services in ANZ • Succession planning for Singapore Operations

96

For

per

sona

l use

onl

y

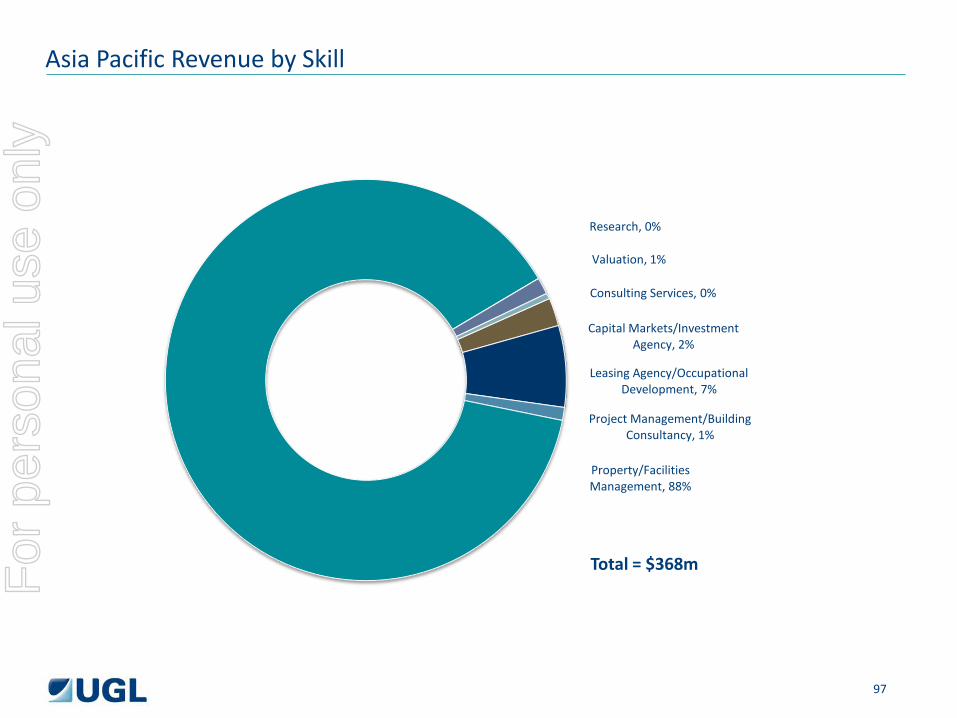

Asia Pacific Revenue by Skill

Capital Markets/Investment Agency, 2%

Leasing Agency/Occupational Development, 7%

Project Management/Building Consultancy, 1%

Property/Facilities Management, 88%

Research, 0%

Valuation, 1%

Consulting Services, 0%

Total = $368m

97

For

per

sona

l use

onl

y

Asia Pacific differentiators

• #1 by revenues in Asia Pacific region

• #1 in ANZ market

• #1 in Singapore market. (Top #3 in Singapore & Malaysia markets for DTZ )

• Singapore – Only International Consultancy providing specialist Hospitality Management services (e.g.

Award winning “Treetops Executive Residences”)

• Singapore - #1 in Residential Resales/brokerage with 2000+ Associate agents.

• Malaysia- #1 in Retail Development Consultancy & Leasing

• Only IPC in India with a niche private banking practice and raised over USD 1.8 Bn

• Only IPC in India with base build project experience for high-rise buildings

• India Valuations team developed RICS Red Book for Valuations standards in India

• India, Awarded ‘Best Property Consultancy of India’ for 3 consecutive years: 2010-2012

98

For

per

sona

l use

onl

y

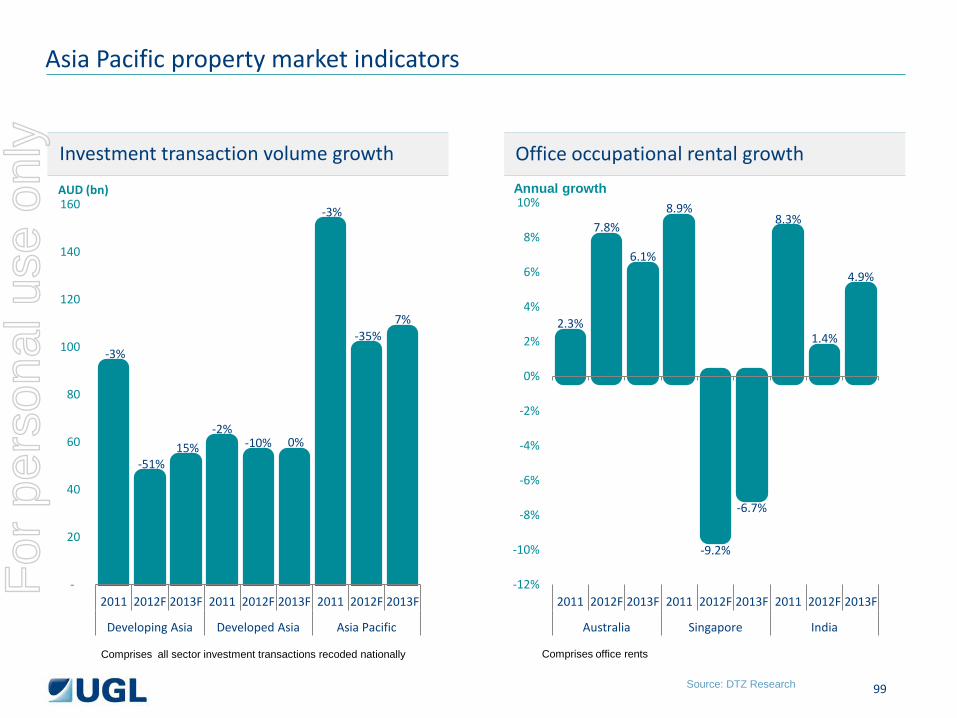

Investment transaction volume growth Office occupational rental growth

Asia Pacific property market indicators

-3%

-51% 15%

-2% -10% 0%

-3%

-35% 7%

-

20

40

60

80

100

120

140

160

2011 2012F 2013F 2011 2012F 2013F 2011 2012F 2013F

Developing Asia Developed Asia Asia Pacific

AUD (bn)

Comprises all sector investment transactions recoded nationally Comprises office rents

Annual growth

2.3%

7.8%

6.1%

8.9%

-9.2%

-6.7%

8.3%

1.4%

4.9%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2011 2012F 2013F 2011 2012F 2013F 2011 2012F 2013F

Australia Singapore India

Source: DTZ Research 99

For

per

sona

l use

onl

y

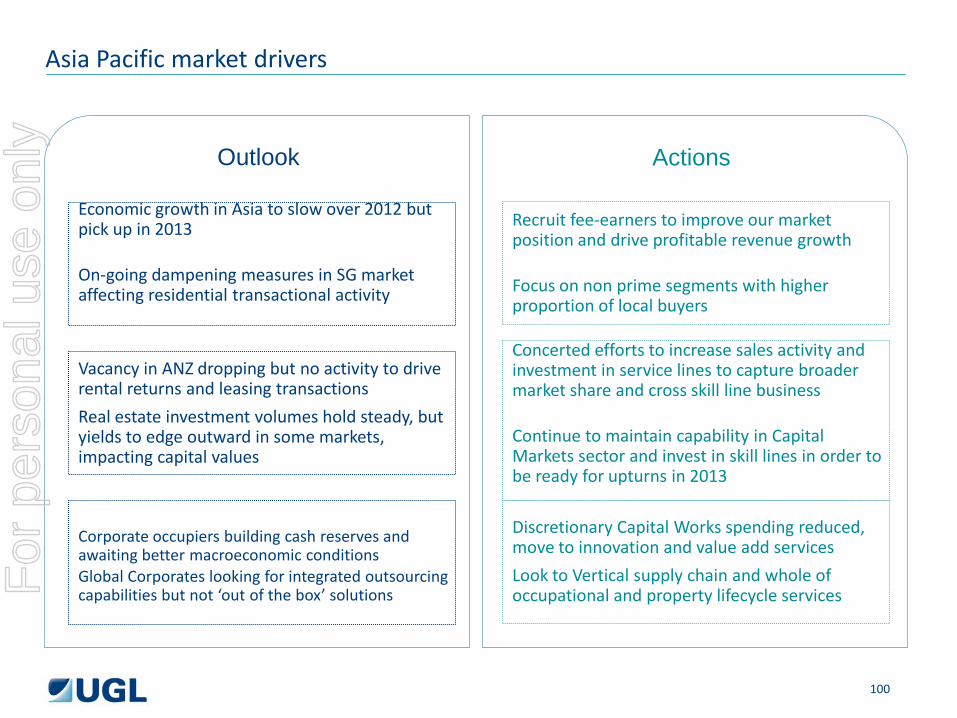

Asia Pacific market drivers

Economic growth in Asia to slow over 2012 but pick up in 2013 On-going dampening measures in SG market affecting residential transactional activity

Vacancy in ANZ dropping but no activity to drive rental returns and leasing transactions

Real estate investment volumes hold steady, but yields to edge outward in some markets, impacting capital values

Corporate occupiers building cash reserves and awaiting better macroeconomic conditions Global Corporates looking for integrated outsourcing capabilities but not ‘out of the box’ solutions

Outlook Actions

Recruit fee-earners to improve our market position and drive profitable revenue growth Focus on non prime segments with higher proportion of local buyers

Concerted efforts to increase sales activity and investment in service lines to capture broader market share and cross skill line business Continue to maintain capability in Capital Markets sector and invest in skill lines in order to be ready for upturns in 2013

Discretionary Capital Works spending reduced, move to innovation and value add services

Look to Vertical supply chain and whole of occupational and property lifecycle services

100

For

per

sona

l use

onl

y

Opportunities: growth drivers

Full Service across the region • Driving depth of service to existing customers • Development of new service lines in geographic areas where we currently have no capability • Developing domestic clients in Indonesia, India • Developing the project management business across the region • Moving to full service in Australia • Moving to full service in India • Developing the regional platform for GCS

Talent Acquisition • Capitalisation on momentum created by new combined company • Opportunity to create connected local and regional teams that capitalise on existing local and

regional capabilities Innovation • Leverage innovation from different parts of the business to create opportunities in other markets –

e.g Energy and Beyond Green

101

For

per

sona

l use

onl

y

Asia Pacific major clients

• Yahoo, India

• Transaction Advisory

• Jurong Town Council, Singapore

• Township Management

• Hong Leong/CDL Group, Singapore

• Transacted portfolio of Commercial office/industrial buildings

• Development Consultants and sole Marketing Agents

• National Australia Bank, Australia

• Strategic consulting • Transaction Advisory • Office services • Data Centre Management • Integrated facilities/property/

portfolio management

Sydney Opera House

• Facilities management – building fabric maintenance services

• Singapore Sports Hub, Singapore

• 25 years PPP contract

• Integrated facility management

102

For

per

sona

l use

onl

y

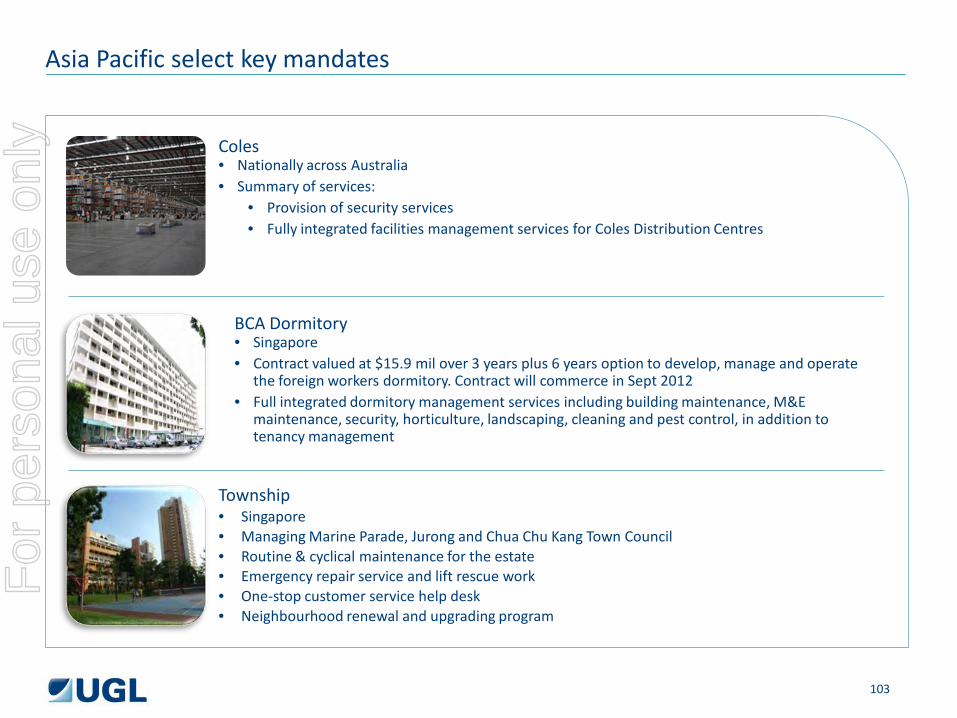

Coles • Nationally across Australia • Summary of services:

• Provision of security services • Fully integrated facilities management services for Coles Distribution Centres

Asia Pacific select key mandates

BCA Dormitory • Singapore • Contract valued at $15.9 mil over 3 years plus 6 years option to develop, manage and operate

the foreign workers dormitory. Contract will commerce in Sept 2012 • Full integrated dormitory management services including building maintenance, M&E

maintenance, security, horticulture, landscaping, cleaning and pest control, in addition to tenancy management

Township • Singapore • Managing Marine Parade, Jurong and Chua Chu Kang Town Council • Routine & cyclical maintenance for the estate • Emergency repair service and lift rescue work • One-stop customer service help desk • Neighbourhood renewal and upgrading program

103

For

per

sona

l use

onl

y

Alva To, Senior Director, Head of Consulting, North Asia

Consulting – North Asia

104

For

per

sona

l use

onl

y

Business overview

Coverage

Services

• 140 employees • 19 cities • 3 countries

• Greenfield Development • Urban Renewal and Conversion • New Township Development • Metro • Tourism and Leisure • Market Studies and Strategic Advice (IPO)

105

For

per

sona

l use

onl

y

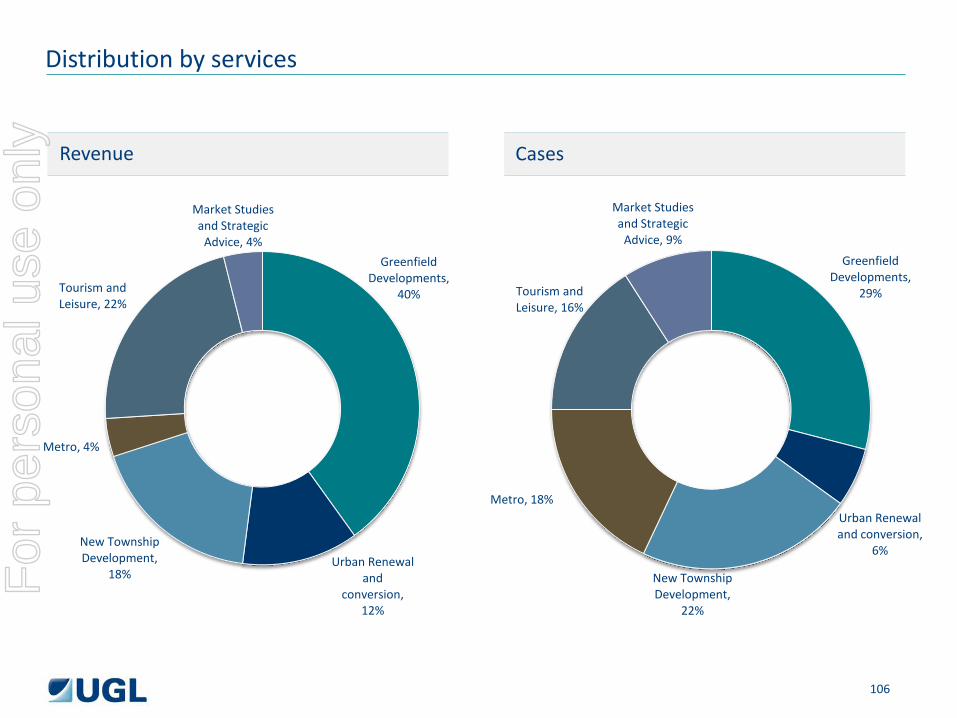

Distribution by services

Greenfield Developments,

40%

Urban Renewal and

conversion, 12%

New Township Development,

18%

Metro, 4%

Tourism and Leisure, 22%

Market Studies and Strategic

Advice, 4% Greenfield

Developments, 29%

Urban Renewal and conversion,

6%

New Township Development,

22%

Metro, 18%

Tourism and Leisure, 16%

Market Studies and Strategic

Advice, 9%

106

Revenue Cases

For

per

sona

l use

onl

y

Differentiators

• Deep history

• Strong track record

• Broad geographic coverage

• Experienced staff and expertise from different disciplines including; surveyors, architects, economists, engineers & town planners

• Support of broader internal network

107

For

per

sona

l use

onl

y

Market drivers

Government policies (5-year plan) to stimulate • rate of urbanization which initiates township

development • development of tourism industries which

creates a lot of tourism projects. • huge investment in infrastructure including

high speed rail and metro

• Growing overseas interests to invest in China

Outlook Actions

• Establish a tourism specialist team • Hold regular road shows, seminars with

government and professional • promote our expertise in all services

• Line up Chinese clients with Korea & Japan investors

108

For

per

sona

l use

onl

y

Major clients

• Lenovo

• Greenfield Development

• Shell

• Strategic Advice

• MTR

• Metro

• HSBC

• Strategic Advice

• Swire Properties

• Market Studies (IPO)

• Sun Hung Kai Properties

• Greenfield Development

109

For

per

sona

l use

onl

y

Key mandates

Lenovo Global Headquarter Project

MTR – Nanjing Project HSBC – HK & Singapore Property Mkt Project

Shell - Petro Station Project

• Overview of Regulations in relation to Petrol Station in China

• Truck Route Analysis • Motorway Analysis • Preliminary Investment

Feasibility of NTI Opportunities

• Overview of SZ real estate markets including retail, office, service apartment & mixed use developments

• Case studies • Positioning • Pedestrian flow • Financial Analysis • Negotiation with government

• Market Modeling, Forecasting and Assessment of Risk Indicators

• Comparative Analysis of the Hong Kong, Singapore, London and New York Commercial Property Markets

• Impact Assessment of a Commercial Property Market Downturn on the HBAP Loan Portfolio

• Overview of Nanjing Residential & Serviced Apartment Market

• Overview of Nanjing Retail Property Market

• Overview of Nanjing Office Market

• Site Analysis

110

For

per

sona

l use

onl

y

KK Chiu, Head of Valuation & Advisory, North Asia

Valuation and Advisory Services

111

For

per

sona

l use

onl

y

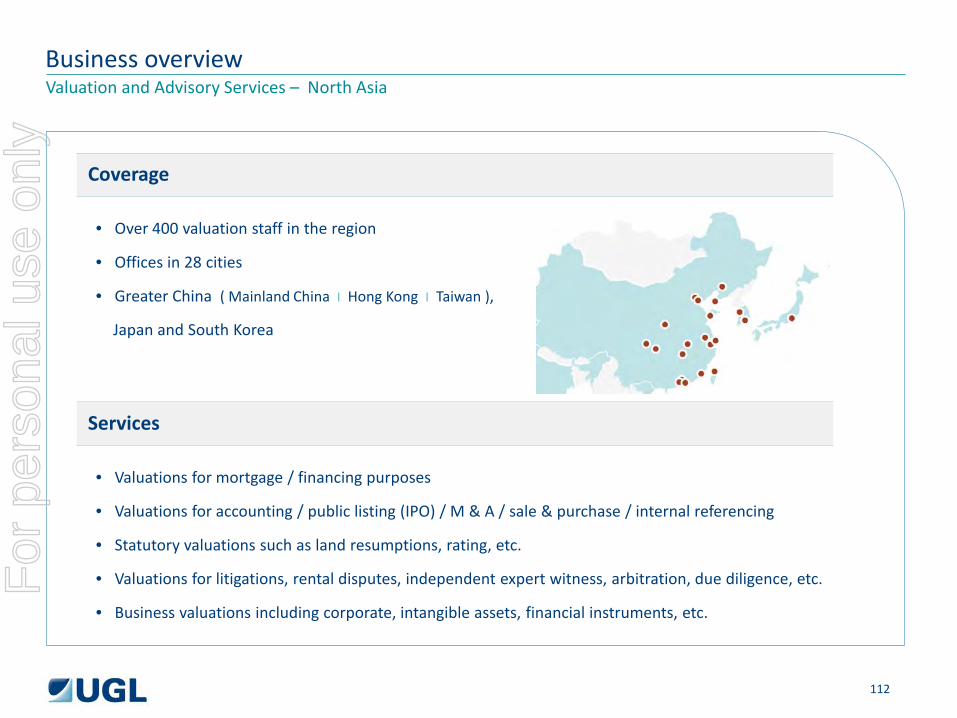

Business overview Valuation and Advisory Services – North Asia

Coverage

Services

• Over 400 valuation staff in the region

• Offices in 28 cities

• Greater China ( Mainland China I Hong Kong I Taiwan ),

Japan and South Korea

• Valuations for mortgage / financing purposes

• Valuations for accounting / public listing (IPO) / M & A / sale & purchase / internal referencing

• Statutory valuations such as land resumptions, rating, etc.

• Valuations for litigations, rental disputes, independent expert witness, arbitration, due diligence, etc.

• Business valuations including corporate, intangible assets, financial instruments, etc.

112

For

per

sona

l use

onl

y

Market position Valuation and Advisory Services – North Asia

Greater China Mainland China I Hong Kong I Taiwan

Japan

• The largest valuation practice among all international real estate services firms in Greater China with

over 360 team members and over 100 qualified valuers thereof

• Sole valuer for HSBC mortgage valuation in Hong Kong and retained market shares of over 30% of

overall mortgage valuation in Hong Kong

• Ranked 2nd in IPO valuation market of Hong Kong and has carried out over 200 IPO valuations for

companies successfully listed in the Main Board of HKEx

• The 2nd largest valuation practice among international real estate services firms in Japan

• Nationwide track records from northernmost Hokkiado to southernmost Okinawa

South Korea

• The largest valuation practice among international real estate services firms in South Korea

• Head office in Seoul and 8 branch offices in Gyeongbuk, Gyeongin, Gwangju & Jeonnam, Gyeonggi,

Busan , Chungcheong, North Gyeonggi and Daegu

113

For

per

sona

l use

onl

y

Key differentiators Valuation and Advisory Services – North Asia

Greater China Mainland China I Hong Kong I Taiwan

Japan

• Extensive office coverage (in 16 major cities of Mainland China)

• The first, if not the only, international firm with both the PRC national Grade A Real Estate and Land

Valuation Licences held under our Shenzhen office in Mainland China

• Strong self-performance capabilities

• Fully integrated, end-to-end offering, delivering industry-leading service levels

• Established relationships with international investors

• Extensive cross-border portfolio valuation assignment experience

South Korea

• National Valuation licensed appraisers

• Experienced valuation professionals with local and international valuation qualifications

114

For

per

sona

l use

onl

y

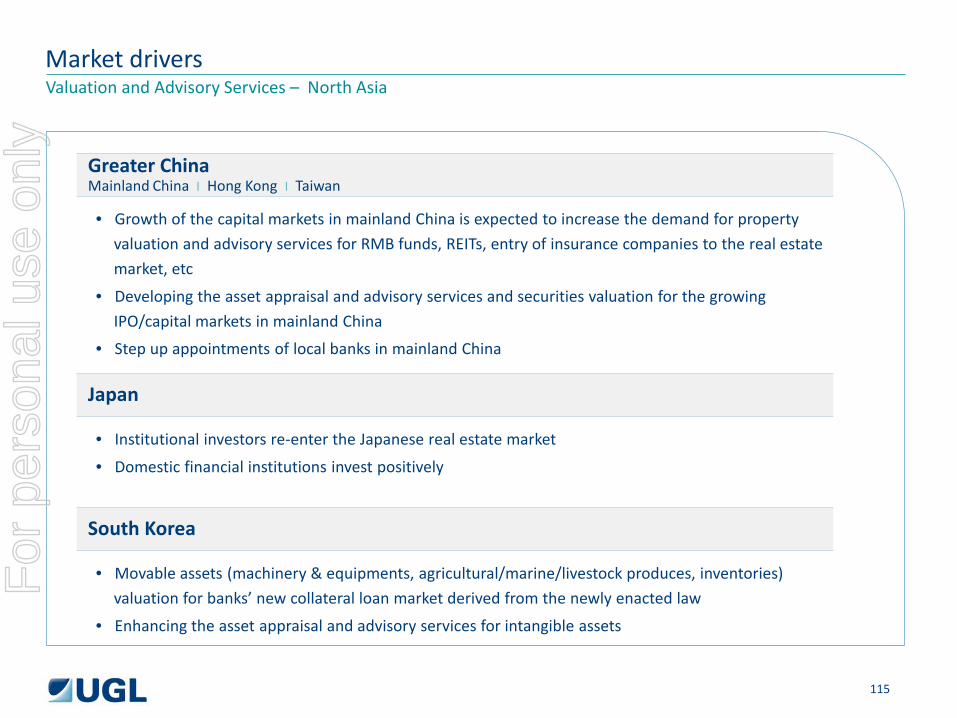

Market drivers Valuation and Advisory Services – North Asia

Greater China Mainland China I Hong Kong I Taiwan

Japan

• Growth of the capital markets in mainland China is expected to increase the demand for property

valuation and advisory services for RMB funds, REITs, entry of insurance companies to the real estate

market, etc

• Developing the asset appraisal and advisory services and securities valuation for the growing

IPO/capital markets in mainland China

• Step up appointments of local banks in mainland China

• Institutional investors re-enter the Japanese real estate market

• Domestic financial institutions invest positively

South Korea

• Movable assets (machinery & equipments, agricultural/marine/livestock produces, inventories)

valuation for banks’ new collateral loan market derived from the newly enacted law

• Enhancing the asset appraisal and advisory services for intangible assets

115

For

per

sona

l use

onl

y

Selected key mandates Valuation and Advisory Services – Asia Pacific

Engagement

• Sole valuer for HSBC mortgage valuation in Hong Kong

• 2002 to present

Essentials

• providing verbal valuation indication and valuation services to HSBC

• Providing DTZ e-valuation platform implanted to HSBC’s information system

116

For

per

sona

l use

onl

y

Selected key mandates Valuation and Advisory Services – Asia Pacific

Engagement

• Interim and year-end valuations for the Group’s investment properties portfolio from 2011 onwards

• In compliance with the International Accounting Standard (IAS)

Essentials

• Current portfolio of over 1,000 properties spread over 300 cities in China

117

For

per

sona

l use

onl

y

Selected key mandates Valuation and Advisory Services – Asia Pacific

Engagement

• Interim and year end valuations on part of their investment properties portfolio in Asia Pacific region

in the past few years

118

For

per

sona

l use

onl

y

Selected key mandates Valuation and Advisory Services – Asia Pacific

Engagement

• Property valuer for the Company’s listing on the Main Board of

HKEx in January 2012.(Stock Code:1972)

Essentials

• Valuations of over 200 properties in Hong Kong, China, United

States and the United Kingdom

119

For

per

sona

l use

onl

y

Francis Li Head of Investment, North Asia

Investment Agency

120

For

per

sona

l use

onl

y

Business Overview Investment Agency and Advisory Services in North Asia

Mainland China

Hong Kong

Taiwan

Japan

South Korea

Greater China

121

For

per

sona

l use

onl

y

Key differentiators

• Pioneer in China: One of the first international property consultants to have made a foothold in China Investment Market back in 2005

• Regional coverage: Direct, effective and fast cross-border communication, providing a truly “one stop” service in Greater China

• Client relationship: Effective CRM system ensuring quality and attentive service from top to bottom

• Strong track record: Sizable transaction volume achieved in China annually, in terms of both number of deals and transaction amount

• Diverse product offering: Services include consultancy , acquisition/ disinvestment, investment advisory to due diligence

• Experience: Unrivalled professional network with local government officials, domestic investors and institutional investors

• People: An exceptional team with a blend of local and international trained GP surveyors and CFAs

122

For

per

sona

l use

onl

y

Market drivers

Mainland

China

Office / Retail Rental

Growth High GDP Growth in

China

Capital Appreciation

Growing Disposal Income

Rising Local Consumption

Urbanization

Growing Domestic

Investment Market

RMB Appreciation

123

For

per

sona

l use

onl

y

Track Record

Shama Century Park, China