shoe shine time! o ffers to do shoe shines? how much? d emands for shoe shines? at what price? w ho...

TRANSCRIPT

Shoe Shine time!

•Offers to do shoe shines? How much?

•Demands for shoe shines? At what price?

•Who competes?

Activity: In the Chips

Pri

ce

pe

r ti

ck

et

Equilibrium Point

Finding Equilibrium

Price of a ticket

Quantity demanded

Quantity supplied

Result

Combined Supply and Demand Schedule

$ .50 300 100

$3.50

$3.00

$2.50

$2.00

$1.50

$1.00

$.50

Tickets sold

050 100 150 200 250 300 350

Supply Demand

Balancing the Market The point at which quantity demanded and quantity supplied come together is

known as equilibrium. AKA—”Market Clearing Price”

$2.00

$2.50

$3.00

150

100

50

250

300

350

Surplus from excess supply

$1.50 200 200 Equilibrium

Equilibrium Price

a

Eq

uili

briu

m

Qu

an

tity

$1.00 250 150

Shortage from excess demand

Market Disequilibrium If the market price or quantity supplied is anywhere but at the equilibrium price, the market is in a state called disequilibrium. There are two causes. In either case, interactions between buyers and sellers will always push the market back towards equilibrium.

Excess Demand•Excess demand

occurs when quantity demanded is more than quantity supplied.

Excess Supply•Excess supply

occurs when quantity supplied exceeds quantity demanded.

Price Ceilings/Price Floors (Generally Bad!)

• A price ceiling is a maximum price that can be legally charged for a good.

• An example of a price ceiling is rent control, a situation where a government sets a maximum amount that can be charged for rent in an area.

• A price floor is a minimum price, set by the government, that must be paid for a good or service.

• One well-known price floor is the minimum wage, which sets a minimum price that an employer can pay a worker for an hour of labor.

Agricultural Price Supports

• 1930s: Government offered loan support through Commodity Credit Corporation. CCC stabilized prices and led to food surpluses.

• The CCC switched to deficiency payments to prevent the government from holding surplus food

• 1996: Congress passed the Federal Agricultural Improvement and Reform Act (FAIR). Cash payments replaced price supports and deficiency payments—no cost savings

• 2002: Huge farm subsidy bill passed to continue FAIR benefits.

Why the Minimum Wage Hurts Minority Youth

• With a minimum wage, employment FALLS.

• The Quantity demanded of labor falls.• People who keep jobs get paid more,

but• Who keeps jobs?• Job losses are NOT random• Minorities lose jobs, cannot acquire job

skills

Section 1 Review

1. Equilibrium in a market means which of the following?(a) the point at which quantity supplied and quantity

demanded are the same(b) the point at which unsold goods begin to pile up(c) the point at which suppliers begin to reduce prices(d) the point at which prices fall below the cost of

production

2. The government’s price floor on low wages is called the(a) market equilibrium(b) base wage rate(c) minimum wage(d) employment guarantee

Shifts in SupplyUnderstanding a Shift

– Since markets tend toward equilibrium, a change in supply will set market forces in motion that lead the market to a new equilibrium price and quantity sold.

Excess Supply

– A surplus is a situation in which quantity supplied is greater than quantity demanded. If a surplus occurs, producers reduce prices to sell their products. This creates a new market equilibrium.

A Fall in Supply

– The exact opposite will occur when supply is decreased. As supply decreases, producers will raise prices and demand will decrease.

Shifts in Demand

Excess Demand

– A shortage is a situation in which quantity demanded is greater than quantity supplied.

Search Costs

– Search costs are the financial and opportunity costs consumers pay when searching for a good or service.

A Fall in Demand

– When demand falls, suppliers respond by cutting prices, and a new market equilibrium is found.

$800

$600

$400

$200

0

Pri

ce

Output (in millions)

Graph A: A Change in Supply

1 2 3 4 5

Analyzing Shifts in Supply&Demand

• Graph A shows how the market finds a new equilibrium when there is an increase in supply.

• Graph B shows how the market finds a new equilibrium when there is an increase in demand

Original supply

Demand

a

New supply

b

c

Graph B: A Change in Demand

Output (in thousands)

$60

$50

$40

$30

$20

$10

0

900800700600500400300200100

Pri

ce

Supply

Original demand

a

New demand

c

b

Section 2 Review1. When a new equilibrium is reached after a fall in

demand, the new equilibrium has a(a) lower market price and a higher quantity sold.(b) higher market price and a higher quantity sold.(c) lower market price and a lower quantity sold.(d) higher market price and a lower quantity sold.

2. What happens when any market is in disequilibrium and prices are flexible?(a) Market forces push toward equilibrium.(b) Sellers waste their resources.(c) Excess demand is created.(d) Unsold perishable goods are thrown out.

The Role of Prices• Prices GENERATE INFORMATION. Who is willing to pay?

Who is the highest value user? Who is the low-cost supplier?

• Prices help move land, labor, and capital into the hands of producers, and finished goods into the hands of buyers. They serve as incentives. Prices ration goods.

• Prices create efficient resource allocation for producers and a language both consumers and producers can use. (Competitive Price Theory—contingent on ideal conditions)

• Prices are neutral—favor neither buyer or seller

• Prices allow for “shocks” & unforeseen events. They are more flexible than production and can be easily increased/decreased to solve problems of supply or demand.

• Prices have no administration cost

• Prices are familiar/easily understood

A Look at Rationing

Methods of Rationing

• Auction is normal method• 1st come, 1st served• Dictator• Share equally• Brute force• Contest—Who wants to be a Millionaire?• Need—organs, scholarships• Raffle/Lottery

Advantages of “Auction”

•All can participate•Matches willingness to pay with

desire•Price influences supply•Provides incentives to modify

behavior•Reflects opportunity costs

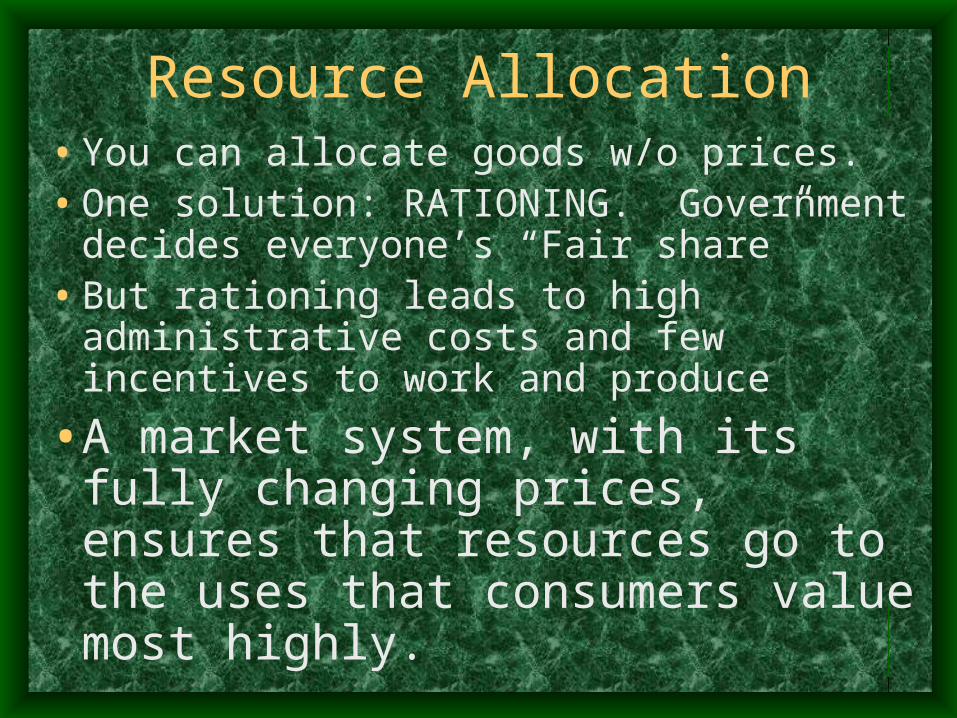

Resource Allocation•You can allocate goods w/o prices. •One solution: RATIONING. Government

decides everyone’s “Fair share”•But rationing leads to high

administrative costs and few incentives to work and produce

•A market system, with its fully changing prices, ensures that resources go to the uses that consumers value most highly.

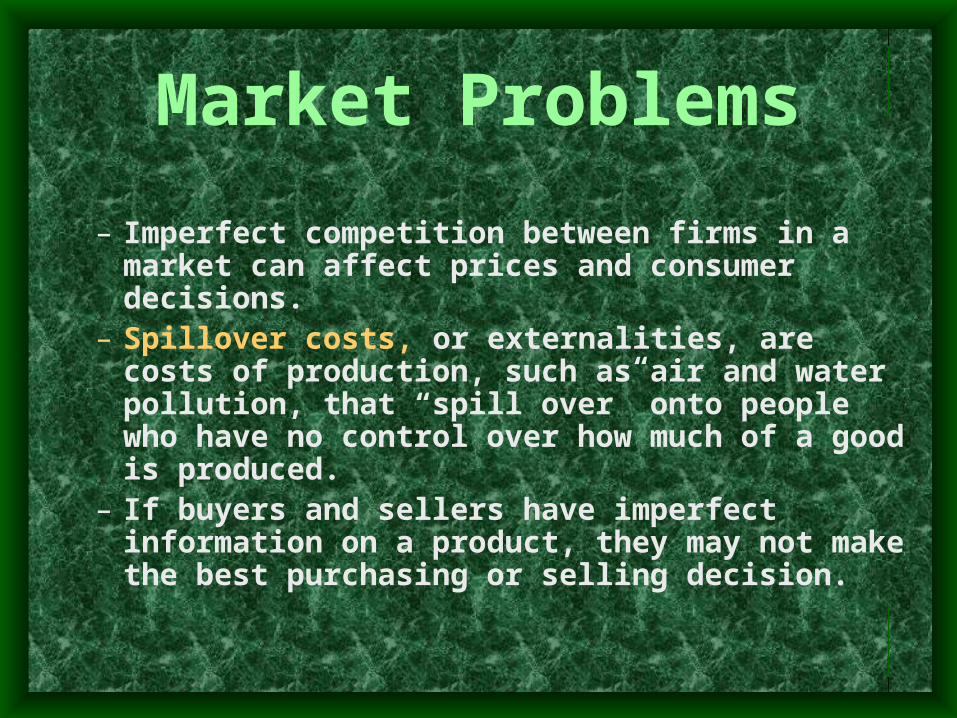

Market Problems

– Imperfect competition between firms in a market can affect prices and consumer decisions.

– Spillover costs, or externalities, are costs of production, such as air and water pollution, that “spill over” onto people who have no control over how much of a good is produced.

– If buyers and sellers have imperfect information on a product, they may not make the best purchasing or selling decision.

But what if…..

• If you have high price suppliers and low price demanders?

•You get NO TRADE and the market will adjust resources.

ACHIEVING Economic Stability

• Misery Index (sum of inflation + unemployment rate) is lower in the U.S. than in other industrialized countries.

• Even so, there is a GDP gap—the difference between actual GDP and the GDP that could be achieved if all resources had been fully employed.

• Economic stability frequently leads to political instability—this explains why some developing countries have so many problems

• Economic instability= Crime, fewer services, less willingness to hire disadvantaged people or provide job training

Aggregate Supply

•An Aggregate Supply Curve shows the amount of real GDP that could be produced at various price levels.

•When costs fall, the graph shifts to the right

•When costs rise, the graph shifts to the left

Aggregate Demand

• An Aggregate Demand Curve shows the amount of real GDP that would be purchased at various price levels.

• A decrease in savings, expectations of a strong economy, an increase in transfer payments, or a tax cut shifts the graph to the right. Prices make it possible.

Critical Thinking Question

•Topographically, why are Bombay and Calcutta so different from New York City?

Section 3 Review1. What prompts efficient resource allocation in a well-

functioning market system?(a) businesses working to earn a profit(b) government regulation(c) the need for fair allocation of resources(d) the need to buy goods regardless of price

2. How do price changes affect equilibrium?(a) Price changes assist the centrally planned economy.(b) Price changes serve as a tool for distributing goods and

services.(c) Price changes limit all markets to people who have the

most money.(d) Price changes prevent inflation or deflation from affecting

the supply of goods.

• Which of the following situations would necessarily lead to an increase in the price of peaches?

• (A) The wage paid to peach farm workers rises at the same time that medical researchers find that eating peaches reduces the chances of a person’s developing cancer.

• (B) While the wages of peach farm workers fall drastically, the peach industry launches a highly successful advertising campaign for

• peaches.• (C) A breakthrough in technology enables peach

farmers to use the same amount of resources as before to produce more peaches

• per acre.• (D) The prices of apples and oranges fall.• (E) Weather during the growing season is ideal

for peach production.