since 1968 · direct tax rates for the fy 2018‐19 2 for individual below the age of 60 for sr....

TRANSCRIPT

Since 1968

DIRECT TAX RATES FOR THE FY 2018‐19

WWW.DKMONLINE.COM 2

For Individual below the age of 60

For Sr. Citizen above the age of 60 but below 80

For Sr. Citizen above the age of 80

Rebate u/s 87A – Available for residentIndividuals whose income does not exceedINR 3,50,000 for the amount of INR 2,500 ortheir actual tax payable, whichever lower.

Health & Education Cess of 4% on total tax, forall taxpayers to continue

Flat 20% tax deduction with no tax credit, in case PAN is not provided

Standard Deduction for INR 40000 OR Taxable Income whichever is less

WWW.DKMONLINE.COM 3

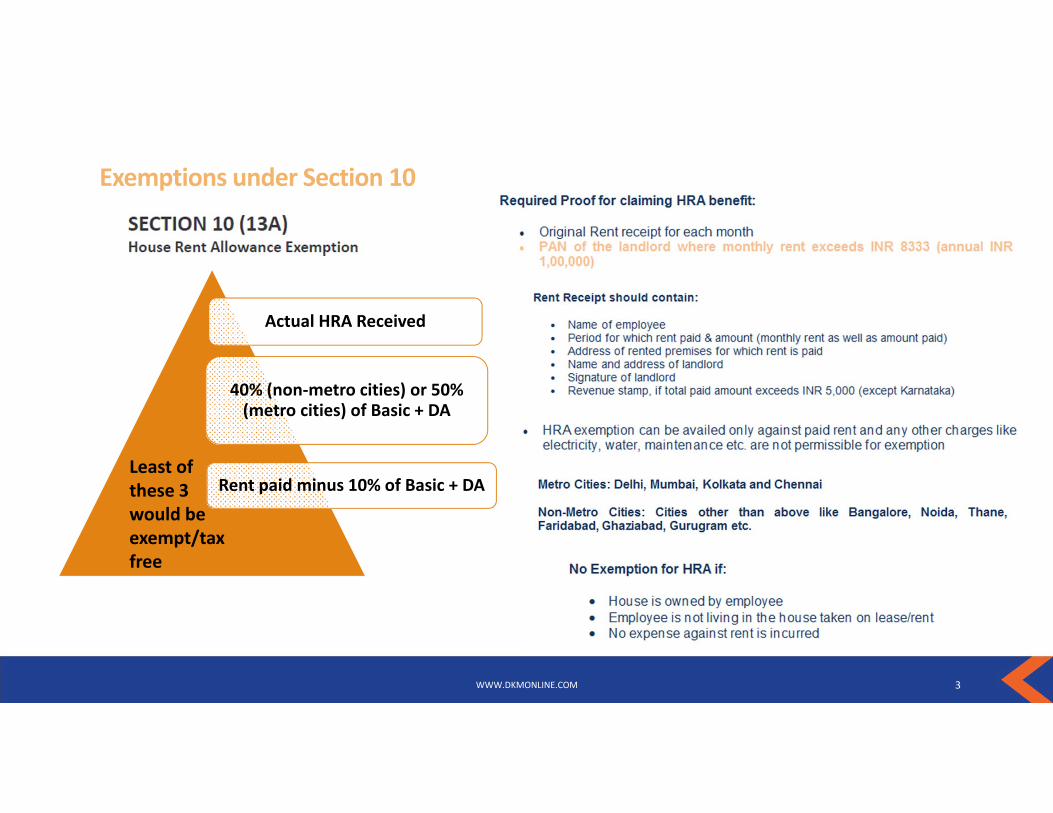

Exemptions under Section 10

Actual HRA Received

40% (non‐metro cities) or 50% (metro cities) of Basic + DA

Rent paid minus 10% of Basic + DALeast of these 3 would be exempt/tax free

WWW.DKMONLINE.COM 4

Exemptions under Section 10 continued…

Leave Travel Assistance Exemption Section 10 (5)

WWW.DKMONLINE.COM 5

Set‐off Income/Loss from House Property

Home Loan Interest Section 24

• INR 2,00,000For Aquisition/construction

• INR 30,000For

Rennovation/Reconstruction/Repair/Renewal

Maximum allowable loss in a FY can not exceed INR

2,00,000 irrespective of the property status i.e. Self Occupied and Let‐out

Unabsorbed Loss can be carried over to next years (max 8 years). Overall Limit of the year would remain to be INR 2,00,000 after inclusion of carry over

loss also

WWW.DKMONLINE.COM 6

Set‐off Income/Loss from House Property continued…

Home Loan Interest Benefit can be claimed only if Construction is completed or Possession is taken

Only 1 property can be treated as self‐occupied. Thus if an individual own more than 1 property, can choose the property to be self‐occupied, other property would be Deemed to be Let‐out. Need to submit estimated deemed rental income for the calculation

Pre Construction/Pre Possession Period: Period starting from date of borrowing to the immediately preceding FY in which Construction is completed or Possession is taken

Co owner and Co applicant: Co owner is the person who has ownership share in the property. Co applicant not necessary to be owner of the property. Thus benefit against property can be taken only if employee do have ownership share in the property

Clarifications

WWW.DKMONLINE.COM 7

Set‐off Income/Loss from House Property continued…

Documents required to claim tax benefit

Copy of the possession letter or a construction completion certificate

Copy of certificate from the person/Bank/Institution to whom interest on housing loan has been paid/payable

In case of joint ownership, the employee will have to submit a declaration (will be generated online by system itself, you just need to fill the details and sign/get signed) from the joint owner (for not claiming benefit of interest on housing loan) to claim benefit of 100% of the amount.

Rental income/Deemed income

Copy of Receipt of Municipal taxes paid (if paid in current FY)

In addition, following also to be submitted if Property is Let‐out/Deemed to be let‐out

WWW.DKMONLINE.COM 8

Deductions under Chapter VIA – Section 80C

Investment Allowable for Document Required

LIPSelf, Spouse and Children Copy of premium paid certificate/receipt

ULIPSelf, Spouse and Children Copy of premium paid certificate/receipt

PPFSelf, Spouse and Children Copy of PPF passbook/receipt

NSC Self Copy of NSC

FD Self Copy of receipt

Mutual fund Self Copy of fund statement

ELSS Self Copy of account statement

Principal repayment of home loan including stamp duty and registration charges Self

Copy certificate from Bank/Financial Institution

Tution fee 2 children Copy of receipt

Bonds issued by NABARD Self Copy of Bonds

Senior Citizen Saving Scheme Self copy of deposit receipt

Sukanya Samriddhi SchemeFor girl child (max 2) upto the age of 10 yr copy of deposit receipt

PF Self Will be taken automatically from payroll

Documents required to claim tax benefit

Benefit under section 80C can be availed up to maximum of INR 1,50,000

WWW.DKMONLINE.COM 9

Investment SectionMax allowable amount Required Document

Contribution to notified Pension funds 80CCC

INR 1,50,000, within the overall limit of section 80C

Copy of contribution statement/payment receipt

Contribution to NPS 80CCD(1)

10% of Basic + DA or INR 1,50,000 whichever is less

Copy of contribution statement/payment receipt/Will be taken automatically from payroll if deducted from payroll

Employer Contribution to NPS 80CCD(2) 10% of Basic + DA

Will be taken automatically from payroll

Contribution to NPS 80CCD(1B)

INR 50,000, over and above the limit of INR 1,50,000 under section 80C

Copy of contribution statement/payment receipt

Deductions under Chapter VIA – Section 80CCC/80CCDContribution to Pension Fund/Scheme

WWW.DKMONLINE.COM 10

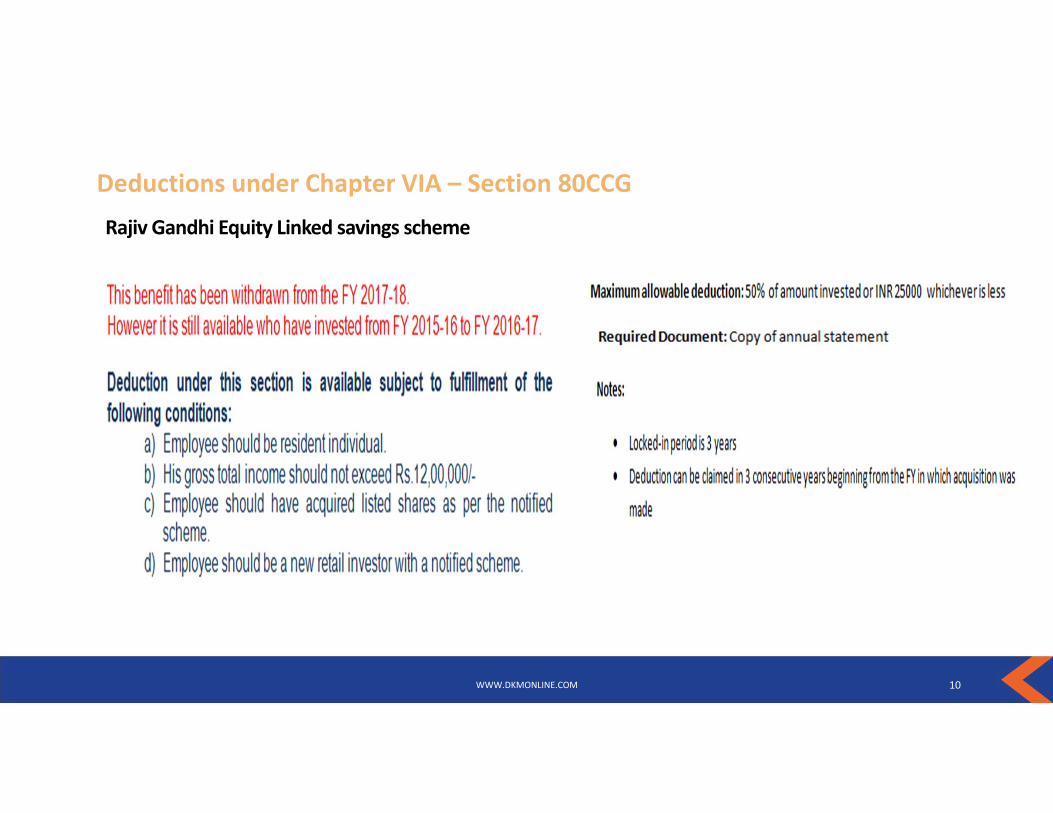

Deductions under Chapter VIA – Section 80CCGRajiv Gandhi Equity Linked savings scheme

WWW.DKMONLINE.COM 11

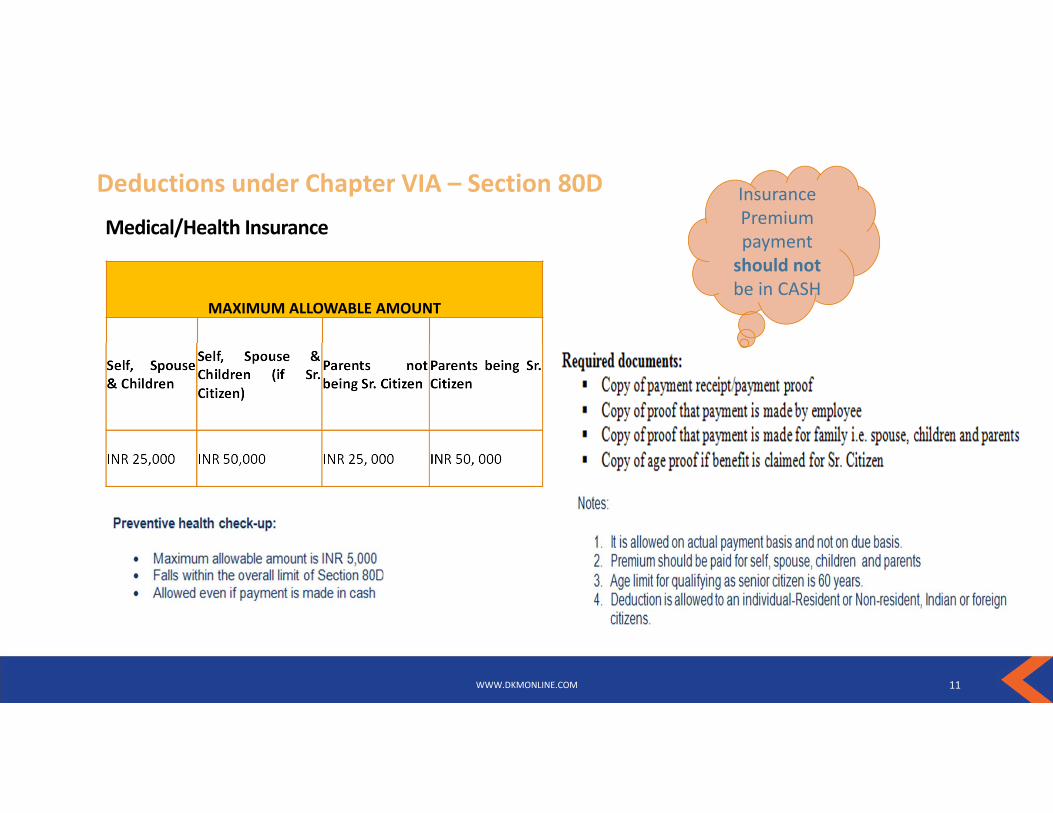

Deductions under Chapter VIA – Section 80D

MAXIMUM ALLOWABLE AMOUNT

Self, Spouse& Children

Self, Spouse &Children (if Sr.Citizen)

Parents notbeing Sr. Citizen

Parents being Sr.Citizen

INR 25,000 INR 50,000 INR 25, 000 INR 50, 000

Medical/Health InsuranceInsurance Premium payment should notbe in CASH

WWW.DKMONLINE.COM 12

Particulars 80DD 80U 80DDBEligible person Resident Individual Resident Individual Resident Individual

Allowable for

Spouse, children, parents, brothers and sisters, who are dependent on him/her Self

Spouse, children, parents, brothers and sisters, who are dependant on him/her

Maximum Allowable Amount where disability exceeds 40% but less than 80% INR 75,000 INR 75,000

Maximum Allowable Amount where disability exceeds 80% (severe disability) INR 1,25,000 INR 1,25,000

Maximum Allowable AmountActual exepense or INR 40,000 whichever is less

Maximum Allowable Amount where age is above 60

Actual expense or INR 1,00,000 whichever is less

Required Document Form 10IA from Medical AuthorityForm 10IA from Medical Authority

Original bills of expenditure and Prescription from a specialist

Deductions under Chapter VIA – Section 80DD, 80U & 80DDB

WWW.DKMONLINE.COM 13

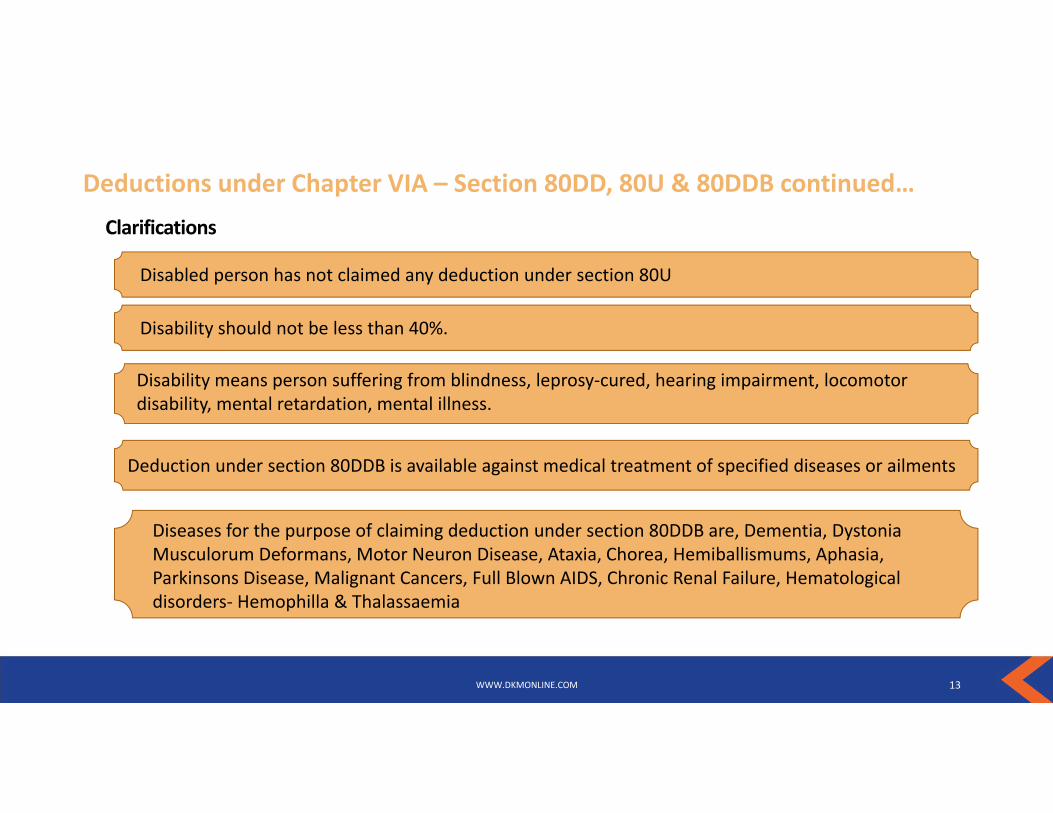

Deductions under Chapter VIA – Section 80DD, 80U & 80DDB continued…Clarifications

Disabled person has not claimed any deduction under section 80U

Disability should not be less than 40%.

Disability means person suffering from blindness, leprosy‐cured, hearing impairment, locomotor disability, mental retardation, mental illness.

Deduction under section 80DDB is available against medical treatment of specified diseases or ailments

Diseases for the purpose of claiming deduction under section 80DDB are, Dementia, Dystonia Musculorum Deformans, Motor Neuron Disease, Ataxia, Chorea, Hemiballismums, Aphasia, Parkinsons Disease, Malignant Cancers, Full Blown AIDS, Chronic Renal Failure, Hematological disorders‐ Hemophilla & Thalassaemia

WWW.DKMONLINE.COM 14

Deductions under Chapter VIA – Section 80E

Loan must have been taken from any bank or financial institution or an

approved charitable institution approved for the purpose of providing educational

loans.

Deduction in respect of Interest on Education Loan taken

Allowed for the higher education of self, spouse and children or that student for

whom the individual is the legal guardian. Higher education means all fields of studies (including vocational studies) pursued after passing the senior secondary examination or its equivalent from any

school, board or university recognized by the central government or state government or local authority or by any other authority authorized by the central or state

government or local authority to do so.

Deduction is allowed for continuously 8 years starting from the year in which

employee starts paying the interest or until the above interest is paid in full, whichever

is earlier.

Principal repayment does not quality for deduction

Required Document: Copy of certificate indicating interest paid

Quantum of deduction: no limit

WWW.DKMONLINE.COM 15

Deductions under Chapter VIA – Section 80EEDeduction in respect of Interest on Home loan taken for first house

WWW.DKMONLINE.COM 16

Previous Employment Income and Income other than salary

Previous Employment

Income

Applicable only for the Employees who have

joined current organization in current

FY

Required Document: Copy of tax

computation sheet (at the time of exit/F&F or provisional Form 16

with seal and signature

Please do not submit pay slips and projection

details

Interest on Saving Bank Account

Would be added to Taxable income as Other Income

Deduction under section 80TTA would be provided against it up to max of INR

10,000

Senior citizen can not avail deduction under

this section

Interest on Deposits

Would be added to Taxable income as Other Income

Deduction under section 80TTB would be provided against it

up to max of INR 50,000

Only Senior citizen (Age>60) are eligible

for it

Other Income

Any other Income like, rental income, fee etc. can also be submitted so that tax can be deducted along with salary

If any tax is deducted at source,

Proof of tax deduction is to be submitted, i.e. Form 16A or Form 26AS

WWW.DKMONLINE.COM 17