sindhu main project

TRANSCRIPT

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 1/65

INTRODUCTION

Finance and accounting are the exciting subjects as we enter the 21st century.

The study of finance is whether financial executives can increase the value of a firm.

Finance is concerned not only with measuring the profitability but also with setting

minimum standards for profitability and hence with the whole question of measuring

the cost of capital for any given society.

Meaning

Finance is called the science of the money finance is the branch of economics

till 1890. Economies may be defined as the study of the efficient use of scare resource

the decision made by the business firms in the production, marketing, finance and

personal matter in the form of the subject form of the economics, finance is age

process of conversion of accumulated funds to the productive use. In simple terms

finance may be defined as an activity concerned with the planning, raising, controlling

and administering of funds to be used in the business.

Definition

Haward and uptron defined in his book, business finance as an administrative area

(or) set of administration which relates with the arrangement of cash and credits so

that the organization may have means of the objectives as satisfactory as possible”

Financial management

Financial management is that managerial activity which is concerned with the

planning and controlling of the firm’s financial resources. It was a branch of

economics till 1890, and as a separate discipline, it is of recent organization still, it

has no unique body of knowledge of its own, and draws, heavily on economics for its

theoretical concepts even today.

The study of financial management is of immense interest to both the

academicians and practicing managers. It mainly involves raising of funds and their

effectives utilization with the objective of maximizing share of wealth. Financial

management is an operation activity of business I.e., responsible for obtaining and

effectively utilizing the funds necessary for efficient operations.

Meaning

1

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 2/65

Financial management is very important in every type of organization. Financial

management is a managerial activity which is concerned with the planning controlling

of the firm’s financial resources

DefinitionAccording to Howard and uptorn defined financial management is an application of

managerial principle to the area of the financial decision- making

The term financial management can be defined as the management of flow of funds

in a firm and it deals with the financial decision- making of a firm.

Objectives

The important objectives of the financial management is as follows they are

Profit maximizationWealth maximization

The objective of profit maximization measures the performance of a firm by looking

at its total profit. It does not consider the risk which the firm may under take in

maximization of the profit.

The objective of maximization of shareholders wealth considers all future cash

flow, dividend, earnings per share, risk of a decision etc. So the objective of

maximization of the share holders wealth is operational and objectives in its approach.

Functions of financial management

Financial functions deals with the problem of raising funds and their effective

utilization in the business the process of rising funds investing them in assets and

distributing returns are known respectively as financing, investment and paying

dividends the firm performs them continually and simultaneously various decisions

regarding acquisition of assets, specific form of assets, where money is to be invested

and the composition of its liabilities are covered the following are some of the

functions of finance.

Long term assets-mix (or) investment decision

Capital- mix (or) dividend decision

Profit allocation (or) dividend decision

Short –term asset mix (or) liquidity decision

The following of financial management can be broadly classified into three

2

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 3/65

Investment decision

Financial decision

Dividend decision

Investment decisions

The investment decision is concerned with a selection of assets of by which

funds invested by business firms. In business firms includes long term assets (or) long

term finance (or) capital budgeting. Where as short term finance (or) working capital

management.

The financial manager also responsible for efficient management of current

assets that is working capital management. Working capital constitutes an integral

part of the financial management

Financial decisions

The second important decision is financial decision. It is concerned with capital

mix. The term capital structure refers to the proportion of debentures capital and

equity share capital financial decisions of a firm relates to the financing mix. The

financial manager has to bring a trade off between risk and return in maintaining a

proper balance between debt capital and equity capital.

Dividend decisions

The third important major decision is dividend policy. These are concerned with a

distribution of the profits of a firm to share holders. How much of the profits should

be paid as dividends that are dividend payout ratio. The decision will depend upon the

preferences of the share holders. The dividend payout ratio is to be determined the

light of the objectives of maximizing the market value of the share.

OBJECTIVES OF THE STUDY

3

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 4/65

The main objective of the study is to study the overall financial

position of the company from 2006-2010.

To study the financial performance of the company.

To study the sources and applications of the funds.

To offer suggestions for improvement in the relevant aspects.

To find out the financial stability of the firm.

To know how effectively the company is using its resources.

To measure the extent to which the company has been financing its

needs through borrowing.

NEED OF THE STUDY

Andhra Pradesh is the state where there is the highest number of textile

units. So, it can be drawn that there is necessary to gain a more accurate inside in to

the working in to such a unit and the balance that is being brought the utilization of

financial resources.

4

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 5/65

The present study carried out is on “FUNDS FLOW ANALYSIS” of

sree satyanarayana spinning mills ltd. As there is a need for every company to

analysis its present financial position and trend. It was provided with the required data

for analyzing present financial position in through financial statements of last five

years.

SCOPE OF THE STUDY

Present study is undertaken mainly to analysis the financial performance of sree

satyanarayana spinning mills ltd, during period 2005-2010, the funds flows analysis is

one of the important technique of financial analysis and has been used for the study.

The study is confine to look over the sources and application of the company.

5

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 6/65

METHODOLOGY

The systematic and scientific study of any research work the

methodology is very important, because it deals with the choice of selecting the

sample, research work design, data to be collected and the technique to be used for the

collection and analysis of data.

I Primary Data:

6

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 7/65

Primary data is nothing but the first hand information primary data either

through observation or through direct communication with respondents in one form or

another or through personal interviews.

II Secondary Data:

Secondary data means data that are already available i.e., they

refer to the data, which have already been collected and analyzed by someone else.

Secondary data may either be published data or unpublished data. Usually published

data are available in:

The study completely depends upon the secondary data.

Annual reports.

News papers.

Trade journals.

Reference Books.

Magazines, Company websites.

LIMITATIONS OF THE STUDY

7

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 8/65

The time given to complete this project is not sufficient that is 45 days only.

The study is based on accounting information.

The analysis is made from the information given by the organization.

The study was conducted with limited data available and analysis was done

accordingly.

The complexity and confidentiality of various operations is also a limitation to this

study.

TEXTILE INDUSTRY PROFILE

Cotton textile industry is one of the oldest and largest during the last 3 Decades.

The textile industry still occupies a key position in the economy of the country

industries in India. Which has made rapid strides during the century of its existence?

At the end of March 2001 there were 1846 miles in the country 1565 spinning mills

8

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 9/65

and 281 composite mills. At present the industry provides direct employment to

nearly 18 lakhs workers. It also provides indirect employment to many millions like

the cotton growers, processors, handlooms and power looms weavers who alone are

estimated five million and innumerable cloth dealers and shop keepers. The industry

contributes in ever increasing measure to the central and state Governments by way of

taxes and duties.

Being one of the oldest industries it has history of over 150 years. It occupies

a unique position in the world export, where Indian has a 24per cent share in the

global cotton yarn market.

It has influence on agriculture because of its consumption of cotton, wool and

silk and on industries because of its requirements of machinery, dyes and chemicals

and synthetic fibers. Thus the industry has an important role to play both in economic

prosperity of the country and in the supply of essential commodities for the entire

population.

The cotton textile industry consists of 3 distinct categories in the organized sectors.

They are:

1. spinning mills

2. coarse and medium composite mills

3. fine and super fine composite mills

Spinning mills are generally small in size, coarse and medium composite mills

are not able to adjust their cost in the face or rising prices of raw materials and

increases in wages consequently many of them became uneconomic units and ran into

difficulties. Fine and super fine composite mills use foreign cotton. They are not

subject to stock restriction and can therefore carry on stable production program.

India has been a manufacturing nation and export of the fine cotton fabrics to the

entire civilized world.

The firs mill in India was setup by C.N. Dakar in 1854 with an Englishmen as

his partner. It was Dakar’s mills which laid the foundations for a strong and growing

textiles industry in Bombay and soon after in other regions of India. “The Bombay

Mills Owner Association” is the first mill formed association in India in the year 1875

9

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 10/65

When India became independent in 1947, there were ten million three hundred

thousand spindles and lakhs two thousand looms installed in million mills. The mills

were producing nearly 4000 million meters of cloth and handlooms accounted for

approximately 130 millionaires. The mill sector employed nearly 7lakhs of workers

and thus was the largest organized industry in the country.

The industry faced its major post independence crisis in the early sixties up till

then if had been more or less sellers market and most of the mills were making

reasonable profits. But a number of factors contributed to a very big depression in the

market and mills started incurring losses. The result was that in 1967, the spindle

activity came down for 88.2per cent to 73.1per cent. Consequently, textiles become a

postponable item. On the other hand, while the purchasing power of the people went

down, the cost of the production of textiles it increased. And the price of the cloth has

to be raised. As the cloth prices began to go up the Government felt the need for the

production of a cheap, durable cloth for the weaker sections of the population.

Consequently the cloth schemes were introduced in 1964.

States such a Bihar, Orissa, Andhra Pradesh and Kerala have all established

spinning mills many of them in co-operative sector. The growth of cotton spinning

sector, in terms of capacity received an imparitus in 1991 with the regimenting of

spindle age. Installed spindle age has been rising steadily since then. In 1991 the

number of spindle installed was around 26.27 million and the number of spindle went

up to nearly 30 million in 1995. The total spindles installed by 2001 are estimated to

have gone up to 35.53 million.

However adverse factors such as the South East Asian Crises, Worldwide

economic slowdown and increased costs hit the spinning industry which could not

benefit it from the expanded captained capacity. The phenomenal rise in raw cotton

prices in the 1994-1995 seasons added a new dimension to the spinning sector.

All these were reflected in stagnant production in the past four years.

Cotton spun yarn production 2,022 million kg, 2213 million kg in 1997-1998 to 2,022

million kg in 1998- 1999, but recovered to 2,266.86 million kg in 2000-2001. Spindle

capacity utilization which was 76per cent in 1991-1192. Had gone up to 86per cent in

1996-97 fell to 79per cent in 1998-1999 before bouncing back to 85per cent in 2000-

2001.

10

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 11/65

The share of spinning capacity of south Indian mills in all India capacity

is estimated to be around 50per cent as on March 31, 2002. The spinning capacity of

southern mills was 19.53 mills spindles while the all India capacity was 38.33 million

during 2000-2001. While the power loom sector had consumed nearly 42per cent of

the total cotton yarn produced, handlooms consumed around 23per cent was exported.

A major portion of cotton yarn exports is to be non-quota countries. Which is

started with five counts, a wide range of counts is being exported now. In 1991,

exports to quota countries were 31.62 million kg and to non-quota countries 89.49

million kg. In 2001, these were 43.83 million kg and 413.16 million kg respectively.

Thus the percentage of exports to quota countries came down from around 26percent

in 1991 to about 9per cent in 2001. During 1994-2002, some of the major destinations

for India cotton yarn exports had been South Korea, Bangladesh and Hong Kong.

According to a report on “Achieving break through growth in cotton textile export”,

India has a large and modern spinning industry and a major position of its capacity is

in the organized sector.

The cotton yarn spinning units could capitalize on the growth in yarn imports

expected in key Asian destinations.

According to the chairman of South Indian Mills Association {SIMA} V.S.

Velayatham, there has been a revival both in the domestic and export markets.

However, if the revival is to be sustained, certain issues need to be addressed, he

feels. The cost of almost all components-power Raw material, transport, labour has

gone up during the last four or five years. The total cost of product on the cotton yarn

in ring spinning {805} in 1995 was about Rs. 178.40 a kg. In 2001, it had shot up to

Rs. 232.63 a kg. In order to make available raw cotton of good quality at reasonable

price, the thrust is on “integrated cotton farming” now.

Textile Industry in India:

The organized cotton textile industry is one of our oldest and most family

established major industries at the end of March 1994; there were 1,775 mills in the

country {906 spindles and 269 composite mills} with 28 millions spindles and 1.6

lakhs labor. There were 132 closed mills by the end of March 1994.

11

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 12/65

The structure of textile industry complete with the modern, sophisticated and

highly mechanized mill sector on the one hand spinning and hand weaving

{handlooms} sectors on the other. In between falls other decentralized small scale

power looms sectors. If we include all the three sectors the cotton and synthetic textile

industries in India are the largest industries in the country accounting for about 20per

cent of the industrial output providing employment to output 17 million persons and

contributing nearly 30per cent of the value of the exports.

In India textile industry is predominant cotton based 70per cent of the fabric

production of raw cotton, carries from the year to year depending upon rainfall and

weather conditions and price fluctuations in raw cotton effets the industry production

of yarn in a almost entirely in the organized sector and over the year. It has showing a

steadily rising trend as for example from 1600 million kgs in 1993/94 to nearly

28,000 million meters in 1993/94. In the production of fabrics, the decentralized

sectors have roughly 93per cent and mills sectors has approximately 7per cent share

only.

A Perspective of India Textile Industry:

Textile industry is the largest industry of modern India. It contributes about

4per cent of GDP, 20per cent of total output, and together with carpets in handicrafts

it has a share of 38per cent in total value of escorts. The first cotton mill in India was

setup in Calcutta in 1818. However, Indian Textile Industry plays a pirior role through

its contribution of about 14per cent to industrial production, 4per cent to GDP and

16.63per cent to export earnings. Its share in global textiles and apparel is 3.9per cent

and 3per cent respectively. It provides direct employment to over35 million people.

Textiles sector is the second largest provider of employment after agriculture. The

12

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 13/65

close industry to Agriculture and the ancient culture and tradition of the country make

the Indian textiles sector unique in comparison with textiles industry of other

countries. This industry is growing by 9per cent-10per cent and the pace would be

increase to 16per cent in the coming years.

This also provides the Industry with the capacity of

products suitable to different market segments, both within and country. Ahmedabad

had 19per cent of mills are provided employment to 113.6per cent of the workers

outside the Bombay city. Some mills located in the shaper, Baroda and other centers

in Maharashtra.

India textile industry contributes to be predominantly cotton based as

65per cent of fabric consumption in the country is being against the world average of

46.5per cent.

Problems of Cotton Textile Industry:

In the past the cotton mill industry industry suffered from in competent

and selfish managing agent and directors, who were more interested in their own

profits. The maintenance of machinery and modernization of textile units’ had been

defective. The role of the industry has not been helpful. The two most important

factors which have felt disaster to the industry in the last 3decades are government

textile policy and growth of the power loom sector. The result was that many cotton

mills became inefficient and one-third of the cotton mills became sick by end of May

1999.

Government Controls and Heavy Excise Duties:

The cotton industry has suffered badly due to often confused policies of

the government. In the past government has sought control etc., at one-time prices of

cloth were fixed by the government far below cost. Under the yarn distribution 1972

the government made it obligatory on all mills to supply 50per cent of the production

to yarn to the decentralized quite high and it not only made important to cotton quite

expensive but exercised and upward pressure on the price of indigenous cotton. The

excise duties on differed varieties of cotton cloth are quite heavy and beside they are

13

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 14/65

discriminatory. Serious Problems of the Mill Sector Related to Production Of

Controlled Cloth

PROFILE OF SREE SATYANARANA SPINNING MILLS

LIMITED

Sree satyanarayana Spinning Mills Ltd is established in 23 rd JULY 1962.

It was originally incorporated as private Ltd Company on above date. Subsequently it

is converted to public Ltd Company on 9th April 1966. The company entered into

commercial production initially with an installed capacity of 5000 spindles.

They are manufacturing yarn cone and hank form. The company has expanded

is spindles from time to time. Now the spindle capacity of the company is around

31500 spindles. Further more we have registered with government of India to start

other 25000 spindles units as and when the finance is available.

14

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 15/65

The company with 1, 05,010 numbers of shares with each share as Rs.10/-. The

company is declaring dividends continuously for the past 5 years at the rate of 100per

cent. The company barrows substantial amounts from IDBI for the modernization and

expansion of the company. The same was paid back.

The promoter directors are Mr. M. HARISHCHANDRA PRASAD and Y.

NARAYANA RAJU. The company is now running with around 450 workers in the

factory and running in triple shifts on all 7 days of a week. This mill is helping the

rural poor to get employment by paying them decent wages compared to other sector.

The company is continuously under modernization and replacing all the

machinery. Thus the company has now introduced combers and producing combed

yarn also. The company has special quality control department and a laboratory

equipped with latest imported cotton and yarn testing equipment, to obtain a quality

product.

The company’s main objectives are to purchase quality raw materials and to

produce and supply quality yarn to customers. One of its policies is to provide

employment opportunities to local people.

The Industry producers yarn from cotton. They are supply two types of yarn.

1. Cone from- used for weaving on power looms

2. Hank from –used for handlooms.

The company markets its yarn in domestic and also exports some portion through

dealers. In domestic market its product is sold in BOMBAY, CHENNAI, and A.P.

though consignment agents. There exports markets are SRILANKA, BANGLADESH

and MALAYSIA.

Raw cotton is available from Guntur and Bellari. They are using different counts

such as 10, 20, 40, 60, 80, 100 and 120. There are different varieties of cotton. They

are

DCH-32

Long stable varieties

MCU-5

15

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 16/65

Varalakshmi

LK

V-797Medium and short stable varieties

JAYADHAR

LRA

The company is in loss for the first 15 years and now in profits since the last 10 years

and paying dividends to share holders.

There is no separate department for marketing. The accounts department

undergoes marketing activities.

Procurement of raw materials is done through brokers i.e., with the existence

of third party agency. The major contributors are

• N.V. Eicher and CO, Contributors are

•

Galiekotawala, Mumbai80per cent of procurement is done through the above firms and various firms

contribute the remaining.

Marketing of the finished product i.e., yarn is done through various

consignment agents. Few of them are

• K.Veereshkumar and Co

• Radhike Textiles, Itchalakaranji.

• Surajmul Gowri Center, Mumbai

And marketing of finished product is also directly from mill to mill various

mills that procure yarn directly are premier mills. Mafatlal industries, Virudhnagar

textile industries, loyal textile mills, Bombay dyeing and manufacturing co.

Preparation process:

Preparation of yarn cotton is done through the following process

16

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 17/65

• Blow room

• Carding

• Preparatory

• Spinning

• Winding

Considering the following factors does the purchase of cotton

• Staple length

• Fitness

• Strength

•Moisture contest

• Tresh

Purchased cotton has to pass through the following stages for becoming

yarn, which is used by textile industries.

Low Room:

It is the first phase of the process. Cotton purchased is pass through bloom

room machine where dust and wastage i.e., trash content in the cotton in the cotton is

removed. The purified cotton is made in to sheets and is rolled like cylinders or

drums. The main objective of the bloom is to separate the waste content in the cotton.

Carding:

Cotton, which is in the form of cylinders, is further purified and is made in the shape

of threads. Each drum obtained from the room is made in to thread.

Preparatory:

The cotton obtained from carding, which is in the from of threads, is grouped

together. Different threads obtained from carding department are grouped lap formers,

combers and drawing.

Spinning:

17

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 18/65

The cotton obtained from preparatory department is made in to fine threads of

lesser width through spinning. The thread of lesser width called as yarn, which is

obtained from spinning.

Winding:

Winding is the method in which the yarn is made in to packages of different

shapes such as conical and bails etc

Mill Name: Sree Satyanarayana Spinning Mills Ltd

Location: Tanuku

Started: 23rd July 1962

Started size: 10 crores

Commercial production: 1963

Mill area: 10 acres

Total Employees: 450

Shifts: 3shifts [General 8:30 am -4:30pm]

Production Capacity: 10 tones per day

Power consumption: 11kv/430 Volts

Water consumption: 45000 gallons

Grams/ Spindles/8Hrs: 125.72

Capacity utilization: 115.72

Hank Yarn Turns OVER Cone Yarn: 76per cent

Sales centers:

Cone Yarn: Mumbai, Madras, Ichalakaran

Hank Yarn: Chirala, Mangalagiri, Guntur.

Bankers:

18

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 19/65

SBI [STATE BANK OF INDIA]. TANUKU

Auditors:

M/S: Nageswara RAO

M/S: Sivudu [HYD]

Departmentation:

Plant engineer is responsible for the entire production activities. The function

of plant engineer is to rectify mechanical defects, to make machinery running

smoothly and their maintained and co ordination of production activities. Plant

engineer is maintaining his functions which two assistance i.e., department in charge

and the supervisor. Each part of production section is under control of section in

charge, directly to plant engineer.

Products Manufactured:

The mills provide quality cotton yarn and blended spun yarn. Both the power

looses are well received in the year Indian market as well as received in the

international markets the company is providing counted yarn also.

It is supplying 75per cent of the yarn in the cane power supply loams of

Bombay and other places 255 of the yarn in the hank to weavers in our state. The year

is well received in the market for the manufacturing of sarees, dhotis and other

fabrics. The percentage of capacity utilization is 95per cent resulting in more

production and better utilization manpower. The labor is intensive.

The company imports technology, it imports its technology from LMW

[Lakshmi Machinery Work} Coimbatore. This company is total pollution free. As it is

a textile industry, there will be some sound pollution from it

19

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 20/65

Financial Department

Though the company was started with the initial share capital with 13 crores

present it is having share capital of 3.79 crores and it consists reserves and surplus

with the amount of 45 lakes. In the year 2007-2008 the company got net profit 44

lakes.

And it is having 27.45 fixed assets and 82.88 current assets till 2007-08 and

the country consists current liabilities 11.02 crores.

So the company has the working capital 7.18 crores in the current year. The

organization is having current ratio with 2.25 that means it is having optimal

performance with recording as the standard normal current ratio is 2.1

The company is having the liquidity percentage of the assets with the ratio of

0.53

The cowman maintains the debt equity ratio with 8.20 percentages which

shows the relationship between total debt and share holders equity? The inventory is

having a greater role in organization. It can be shown with the inventory ratio by 4.06

The company has following financial institution that is State Bank of India

Tanuku. No specific impact has taken place because of depreciation of rupee on the

financial position of organization. The finance department has been with for pro and

other language especially with the package of Tally9.2.

The company disposes its profits in to two types

• Inform of surplus and reinvestment

• 20 per cent bonus to the worker.

Marketing Wing

The marketing wing having tremendous role in this organization as a company

for the manufacturing

Yarn the cotton is necessary as the raw material for the process of production.

The marketing department takes an effort to minimize the costs regarding from raw

materials purchasing to district of the finished product.

20

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 21/65

As the marketing gives costumers as a choice among products. This

organization provides into the market. This marketing main aim is creating costumers.

For that this company maintaining a better marketing team.

The marketing team is considered members who are situated trough out the

India those members take an achievement concentrated having financial give on the

four P’S Concept.

Product:

Here the marketing product is yarn thread it is produced as a bundle which

consists for kegs. The yarn thread is produced as a bundle which consists 16000

meters. It is high quality product and color of the product is white transparent cover

and well setup in the brown boxes 24 boundless for one box to export.

Place:

The place is the most significant in the marketing. Because the product should be

easily transported and to be sold easily. This product is being exported to the

following places from Tanuku.

• Chennai

• Coimbatore

• Mumbai

Because in those places the textile industries are well estabilished to

manufacture cloth materials.

Price:

The price nothing but the value of the product, the price of the product is fixed

is the organization according to the market fluctuation and inflation rate the Price of

the yarn will be charged. The organization is having effective pricing strategies the

price of the one Kg. Yarn = 155 Rs -160 in the market.

21

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 22/65

Promoters:

Promotion is the necessary as the process of selling are more technical buyers

more sophisticated and the organization promotional activities are taken place to the

agent and merchants. Because as the organization is newly established it does not

depend upon the advertisement. All the marketing activities are based on the order

taking the organization is offering the following promotions.

Informative Promoters:

Offering the information about organization products through the agents.

PERUASIVE Promotion:

The basic purpose of promotion is to persuade customers to buy.

Sales:

The sales of the organization are growing year by year in progressive manner.

Manufacturing Process

Flow Diagram Of Manufacturing

22

Mixing

Manually

To mix different variety of cotton

Blow Room Dust To open the fiber tuft and

Cording To open the fiber to individual stage

Draw frame To parlize the fiber and deposit

Uni Lap To make lap to feed to comber

Comber Extent To make lap to feed to

comber

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 23/65

All the sales activities done to agents of merchants. In the process of sales there

selling expenses will be acquired. If he estimated those expenses as follow [in lakes]

10-11 11-12 12-13 13-14

37.18 37.28 37.28 37.48

Graphical Representation

23

Auto leveler

material in can

To remove short fiber and

deposit the draw frame

Speed Frame To make Roving

Rein frame count To make arn with twist and

Cone windind To wind the form of cone

Packing Intopreseribed Packing of individual cones or

cartoons

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 24/65

CONCEPTUAL FRAME WORK

FUNDS FLOW STATEMENT

INTRODUCTION:

The basic financial statement i.e., the balance sheet and profit and loss account

(or) income statement of business, reveal the net effect of the various transaction on

the operational and financial position of the assets and liabilities of an undertaking at

particular point of time. It reveals the financial status of the company. The assets

side of a balance sheet shows of the deployment of resources of an undertaking while

the liabilities side indicates its obligation i.e., the manner in which these resources

were obtained. The profit and loss account reflects the results of the business

operations for a period of time. It contains a summary of expenses incurred and the

revenues realized in a accounting period. Both these statement provide the essential

basic information on the financial activities of a business. The balance sheet give a

static view of the resources (liabilities) of a business and uses (assets) to which these

resources have been but at a certain point of time. It does not disclose the cause for

changes in the assets and liabilities between two different points of time. The profit

and loss account, in a general way, indicates the resources provided by operations.But there are many transactions that take place in an undertaking and which do not

24

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 25/65

operate through profit and loss account. Thus another statement has to prepare to

show the change in the assets and liabilities from the end of one period of time to the

end of

another period of time. The statement is called a statement of changes in financial

position or a funds flow statements.

The funds flow statement in a statement which shows the movement of funds and

is a report of the financial operations of the business undertakings. It indicates

various means by which funds were obtained during a particular period and the way to

which these funds were employed. In simple words. It is a statement of sources and

applications of funds.

MEANING AND CONCEPT OF FUNDS:

The term ‘funds’ has been defined in a number of ways.

a. In a narrow sense, it means cash only and a funds flow statement

prepared on this basic is called a cash flow statement such a statement

enumerates net effects of various business transactions in cash andtakes into account receipts and disbursements of cash.

b. Ina broader sense the term ‘funds’ refers to money values in whatever

form it may exist. Here ‘funds’ means all financial resources used in

business whether in the form of men, material , money, machinery and

other.

c. In a popular sense the term ‘funds’ means working capital i.e., the

excess of current assets over current liabilities, the working capital

concept of funds has emerged due to the fact that total resources of

business are invested partly in fixed assets in the form of fixed capital

and partly kept inform of liquid or hear liquid form as working capital.

MEANING AND CONCEPT OF ‘FLOW OF FUNDS”

The term ‘flow’ means movement and includes both ‘inflow’ and ‘outflow’ the

term ‘flow of funds’ means transfer of economic values from one assets of equity to

25

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 26/65

another flow of funds is said to have taken place when any transaction makes changes

in the amount of funds available before happening of the transaction. If the effect of

transaction results in the increase of funds. It is called a source of funds and if it

results in the decrease of funds, it is known as an application of funds. Further, in

case the transaction does not change funds. It is said to have not resulted in the flow

of funds. According to the working capital concept of funds, the term ‘flow of funds’

refers to the movement of funds in the working capital. If any transaction results in

the increase in working capital it is said to be a source or inflow of funds and it results

in decrease of working capital, it is said to be an application or outflow funds.

In simple language funds move when a transaction effects.

i. A current assets and a fixed assets, or

ii. A fixed and a current liability.

iii. A current assets and a fixed liability.

iv. A fixed liability and current liability.

And funds do not move when the transaction affects fixed assets and fixed

liability or current assets and current liabilities.

Kenneth medley and Ronald Gibers define the term ‘funds’ as one used in the

sense of spending power, it refers to the value embedded in assets. According to

Bonneville and Dewey ‘funds’ constitute the prime importance in sharing and

operating any business enterprise. In the ordinary parlance. Funds mean cash only,

but it has got several different concepts as mentioned below.

Funds may mean:

a. Cash only

b. Net working capital i.e., current assets less current liabilities.

c. Total resources or total funds.

d. Internal resources only.

26

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 27/65

e. Net worth i.e., owner’s equity capital plus reserves.

CURRENT AND NON-CURRENT ACCOUNTS:

To understand flow of funds it is essential to classify various accounts and balance

sheet items current and non-current categories.

Current accounts can either be current assets or current liabilities. Current assets

are those assets which in the ordinary course of business can be or will be converted

into cash with in a short period of normally one accounting year.

FUNDS FLOW STATEMENT

The following is the list of current or working capital accounts:

List of current or working capital accounts:

Current Liabilities Current Assets

1. Bills payable 1. Cash in hand

2. Sundry creditors or account payable 2. Cash at bank

3. Accrued or outstanding expenses 3. Bills receivable

4. Dividends payable 4. Sundry debtors or accounts

receivable

5. Bank overdraft 5. Short term loans and advance

6. Short term loans advances and deposits 6. Temporary or marketable

investments

7. Provision against current assets 7. Inventories or stocks such as

[a] Raw materials

[b] Work in progress.

27

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 28/65

[c] Stores and spares.

[d] Finished goods

8. Provision for taxation, if it does not amount to

appropriation of profits.

8.. Prepaid expenses

9. Proposed dividends (maybe a current non-current

Liability).

9. Accrued incomes

List of non-Current (or) Permanent Capital Accounts:

Non-current or permanent liabilities Non-current or permanent assets

1. Equity share capital 1. Good will

2. Preference share capital 2. Land

3. Redeemable preference share capital 3. Building

4. Debentures 4. Plant and Machinery

5. Long term loans 5. Furniture and Fittings

6. Share premium account 6. Trade Marks

7. Share forfeited account 7. Patent Rights

8. Profit and loss account (balance of profit ie.,

credit Balance).

8. Long term investment

9. Capital reserve 9. Debit balance of profit and loss

account.

10 Capital redemption reserve 10. Discount on issue of shares

11 Provision for depreciation against fixed assets 11 Discount on issue of debentures

12 Appropriation of profits 12 Other Deferred expenses

[a] General reserve

[b] Dividend equalization Fund

[c] Insurance Fund

[d] Compensation fund

[e] Sinking fund

28

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 29/65

[f] Provision for taxation.

[g] Proposed dividend.

FUNDS FLOW STATEMENT

Funds flow statement is the statement of sources and application of funds. It is

also called as ‘funds where got and where gone statement’ Almond Coleman

observed. “The funds statement in a statement summarizing the significant financial

changes which have occurred between the beginning and the end of company’s

accounting period’.

There are 4 steps involving in preparation of funds flow statement:

a. Ascertain the funds from operations.

b. Preparation of statement of changes.

c. Computation of any missing figures as to profit or loss on Sale of fixed

assets purchases or sale of fixed assets and the amount of depreciation

on fixed assets etc.

d. Finally preparation of funds flow statement.

Foulke defines this statement as:

“A statement of sources and appreciation of funds in technical device designed to

analyse the changes in the financial condition of a business enterprise between two

dates”

In the words of Anthony the funds flow statement describes the sources from

which additional funds were derived and the use to which these sources were put.

F.C.W.A. in glossary of management accounting terms defined funds flow

statement as a statement either prospectus or retrospect’s, setting out the sources and

applications of the funds of an enterprise. The purpose of the statement is to indicate

29

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 30/65

clearly the requirement of funds and how they are proposed to be raised and the

efficient utilization and application of the same.

Thus funds flow statement in a statement which indicates various means by which

the funds have been obtained during a certain period and the ways to which these

funds have been used during that period. The term funds used here means working

capital i.e., the excess of current assets over current liabilities.

Funds flow statement is called by various names such as sources and application

of funds; statement of changes in financial position, sources and uses of duns;

summary of financial operation, where came in and where gone out statement, where

got, where gone statement, movement of working capital statement, movement of

funds statement, funds received and disbursed statement; funds generated and

expended statement; sources of increase and application of decrease; funds statement

etc.

30

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 31/65

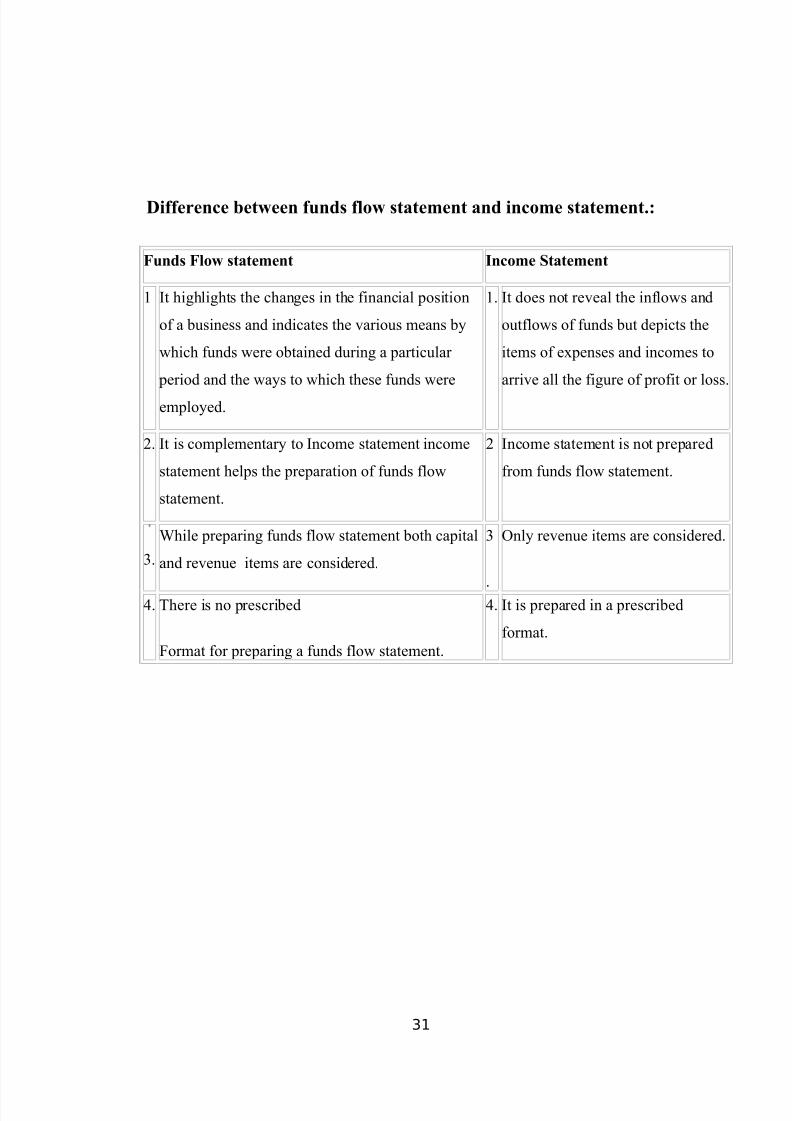

Difference between funds flow statement and income statement.:

Funds Flow statement Income Statement

1 It highlights the changes in the financial position

of a business and indicates the various means by

which funds were obtained during a particular

period and the ways to which these funds were

employed.

1. It does not reveal the inflows and

outflows of funds but depicts the

items of expenses and incomes to

arrive all the figure of profit or loss.

2. It is complementary to Income statement income

statement helps the preparation of funds flow

statement.

2 Income statement is not prepared

from funds flow statement.

3.

While preparing funds flow statement both capital

and revenue items are considered.

3

.

Only revenue items are considered.

4. There is no prescribed

Format for preparing a funds flow statement.

4. It is prepared in a prescribed

format.

31

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 32/65

Difference between funds flow statement and balance sheet :

Funds Flow statement Balance Sheet

1 It is a statement of changes financial

position and hence in dynamic in nature

1. It is a statement of financial position

on a particular date and here is static

in nature.

2. It shows the sources and uses of funds in a

particular period of time

2. It depicts the assets and liabilities at a

particular point of time.

3. It is tool of management for financial

analysis and helps in making decisions.

3. It is not of much help to management

in making decision.

4. Usually schedule of changes in working

capital has to be prepared before preparing

funds flow statement.

4. No such schedule of changes is

required rather profit and loss

account is prepared.

USES, SIGNIFICANCE AND IMPORTANCE OF FUNDS FLOW

STATEMENT:

32

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 33/65

A funds flow statement is an essential tool for the financial analysis and is of

primary importance to the financial management. Now-a-days, it is being widely

used by the financial analysis, credit granting institutions and financial managers.

The basic purpose of a funds flow statement is to reveal the changes in working

capital on the two balance sheets dates. It also describes the sources from which

additional working capital has been financial and the uses to which working capital

has been applied such a statement is particularly useful in assessing the growth of the

firm its resulting financing these needs. By making use of projected funds flow

statement, the management can come to know the adequacy or inadequacy of

working capital even in advance. One can plan the intermediate and long-term

financial of the firm, repayment of long-term debts, expansion of the business,

allocation of resources, etc., the significance or importance of a funds flow statement

can be were followed from its various uses given below:

(1) It helps in the analysis of financial operations:

The financial statements reveal the net effect of various transactions on the

operational and financial position of a concern. The balance sheet gives a static view

of the resources of a business and the uses to which these resources have been put at acertain point of time. But it does not disclose the causes for changes in assets and

liabilities between two different point of time. The funds flow statement explains

causes for such changes and also the effect of these changes no the liquidity position

of the company. Sometimes a concern may operate profitably and yet its cash

position may become more and more course. The funds flow statement gives a clear

answer to such a situation explaining what has happened to the profit of the firm.

(2) It throws light on many perplexing questions of general interest:

Which other wise may be difficult to be answered, such as:

33

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 34/65

a. Why were the net current assets lesser inspite of higher profits and

vice-verse.

b. Why more dividends could not be declared inspite of available Profit?

c. How was it possible to distribute more dividends than the Present

earning?

d. What happened to the net profit? Where did they go?

e. What happened to the proceeds of sale of fixed assets or issue of

Shares, debentures etc?

(3) It helps in the formation of a realistic dividend policy:

Sometime a firm has sufficient profit available for distribution as dividend but

yet it may not be advisable to distribute dividend for lack of liquid or cash resources.

In such causes, a funds flow statement helps in the formation of a realistic dividend

policy.

(4) It helps in the proper allocation of resources:

The resources of a concern are always limited and it works to make the best

use of these resources. A projected funds flow statement constructed for the future

help in making managerial decision. The firm can plan the deployment of its

resources and allocate them among various application.

(5) It acts as a future guide:

A project funds flow statement also acts as a guide for future to the

management. The management can come to know the various problems it is going to

funds can be projected well in advance and also the timing of these needs. The firm

can arrange to finance these needs more effectively and avoid future problem.

(6) It helps in appraising the use of working capital:

34

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 35/65

A funds flow statement helps in explaining how efficiently the management has

used its working capital and also suggests way to improve working capital position of

the firm.

(7) It helps knowing the overall credit worthiness of a firm:

The financial institutions and banks such as state financial institutions, industrial

development corporation, industrial finance corporation of India, industrial

development bank of India etc., all ask for funds flow statement constructed for a

number of years before granting loans to know the credit worthiness and paying

capacity of the firm.

Limitations of Funds Flow Statement:

The funds flow statement has a number of uses; however, it has certain limitations

also, which are listed below:

1. It should be remembered that a funds flow statement is not a substitute

of an income statement or a balance sheet. It provides only some

additional information as regards changes in working capital.

2. It cannot reveal continuous changes.

3. It is not a original statement but simply a re-arrangement of data given

in the financial statement.

4. It is essentially historic in nature and projected funds flow statement

cannot be prepared with much accuracy.

5. Changes in cash are more important and relevant for financial

management than the working capital.

Procedure for Preparing a Funds Flow Statement:

35

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 36/65

Funds flow statement is a method by which are study changes in financial position

of a business enterprise between beginning and ending financial statement dates.

Hence, the funds flow statement is prepared by comparing two balance sheets and

with the help of such other information derived from the accounts as may be needed.

Broadly speaking the preparation of a funds flow statement consists of two parts.

1. Statement of schedule of changes in working capital

2. Statement of sources and application of funds.

(1) Statement of schedule of changes in working capital.

Working capital means the excess of current assets over current liabilities.

Statement of changes in working capital between the two balance sheet dates. This

statement is prepared with the help of current assets and current liabilities derived

from the two balance sheets.

As working capital =current assets – current liabilities.

So, i. An increase in current assets increase working capital.

ii. A decrease in current assets decreasing working capital.

iii. An increase in current liabilities decreasing working capital;

Statement (or) Schedule of Changes in Working Capital

36

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 37/65

Particulars PreviousYear CurrentYear Effect in working

Capital

Increase Decrease

Current Assets

Cash in hand

Cash at Bank

Bills receivable

Sundry debtors

Temporary investment

Stock/inventories

Accrued incomes

Total current assets

Current Liabilities

Bills payable

Sundry creditors

Bank over draft

Dividend payable

Provision for taxation Total

Current liabilities

Working capital (CA-CL)

Net increase/decrease in,(W.C)

Working capital

37

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 38/65

Specimen of report form of fund flows statement:

38

Sources of Funds Rs.

Funds from operations

Issue of share capital

Issue of debentures

Raising of long term loans

Receipts from partly paid share, called up

Sales of non current (fixed) assets

Non-trading receipts such as dividends received

Sale of investment (long term)

Decrease in working capital (as per schedule of changes in working capital)

Total

Applications or uses of funds:

Funds lost in operations

Redemption of preference share capital

Redemption of debentures

Repayment of long-term loans

Purchase of noncurrent (fixed) assets

Purchase of long-term investments

Non-trading payments

Payments of dividends

Payment of tax

Increase in working capital (as per schedule of changes in working capital

Total

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 39/65

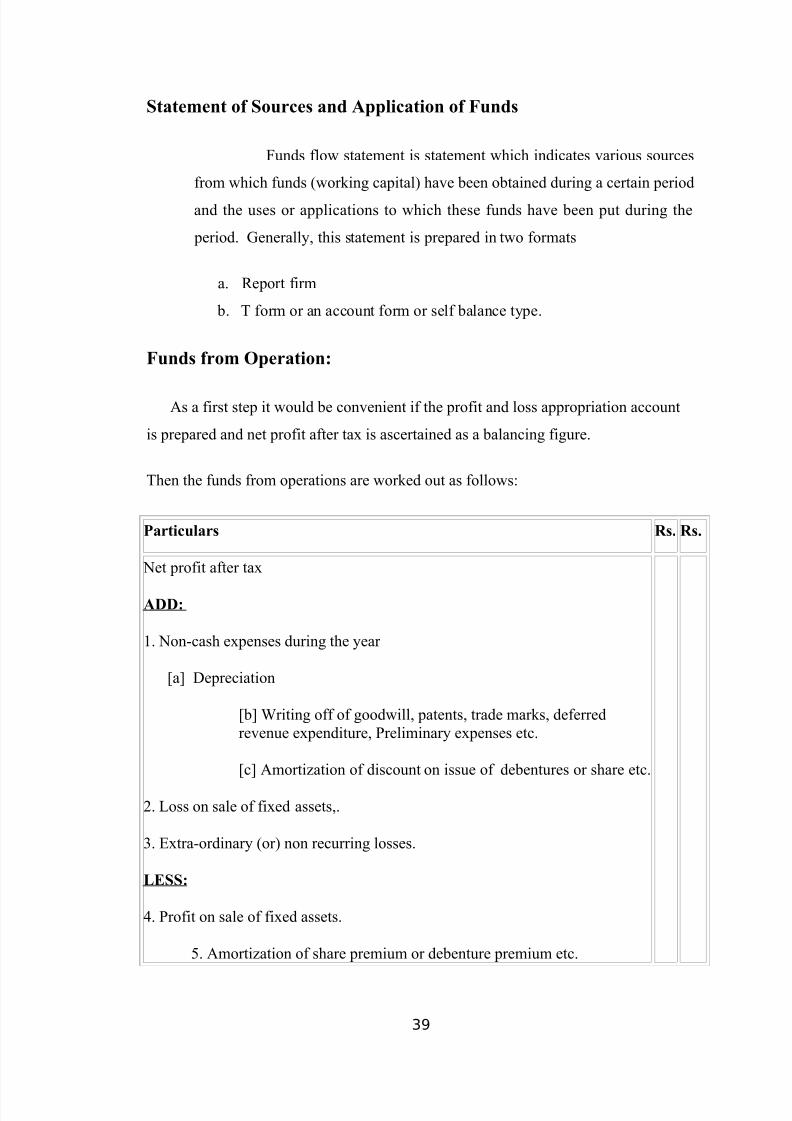

Statement of Sources and Application of Funds

Funds flow statement is statement which indicates various sources

from which funds (working capital) have been obtained during a certain period

and the uses or applications to which these funds have been put during the

period. Generally, this statement is prepared in two formats

a. Report firm

b. T form or an account form or self balance type.

Funds from Operation:

As a first step it would be convenient if the profit and loss appropriation account

is prepared and net profit after tax is ascertained as a balancing figure.

Then the funds from operations are worked out as follows:

Particulars Rs. Rs.

Net profit after tax

ADD:

1. Non-cash expenses during the year

[a] Depreciation

[b] Writing off of goodwill, patents, trade marks, deferred

revenue expenditure, Preliminary expenses etc.

[c] Amortization of discount on issue of debentures or share etc.

2. Loss on sale of fixed assets,.

3. Extra-ordinary (or) non recurring losses.

LESS:

4. Profit on sale of fixed assets.

5. Amortization of share premium or debenture premium etc.

39

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 40/65

Funds from operations:

Funds from operation are a source of fund during period. If it is still a negative

balance it is loss from operations and is shown on the side of “Application of funds”

but if it shows a positive it is a source of funds.

P & L appropriation account

Particulars Amount Particulars Amount

To Interim Dividend

To Proposed equity

Dividend

To Preference dividend

To Transfer to reserve

To Balance c/d

-

-

-

-

-

By balance b/d

By excess provision written back

By income tax provision not required

By Dividend received

By net profit after tax

(balancing figure)

(transferred from P&L account

-

-

-

-

-

40

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 41/65

Funds Flow Statement

(For the year ended….)

Sources Rs Applications Rs

Funds from operations

Issue of share capital

Issue of Debentures

Raising of long-term loans receipt

from partly paid share called up

Sales of non current (fixed)

Assets.

Non trading receipts such as dividends.

Sale of long-term investment

Net decreasing in working capital

Funds lost in operations

Redemption of preference

Share capital

Repayment of long term loans

Purchase of non-current (fixed assets)

Purchase of long-term

Investments

Non trading payment.

Payment of dividends.

Payment of tax.

Net increase in working capital

WORKING CAPITAL MANAGEMENT

41

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 42/65

Working capital is the firms holdings of current assets such as Cash ,

receivables , inventory and marketable securities. Every firm required working

capital for its day to day transactions such as purchasing raw material , for

meeting salaries , wages , rents , rates , advertising etc. But there is much

disagreement among various financial authorities (financial managers , accountants

, businessmen and economists ) as to the exact meaning of the term working

capital.

Significance of working capital:

The world in which real firms function is not perfect. It is characterized by

the firm’s considerable uncertainty regarding the demand, market price, quality and

availability of its own products and those of suppliers. These real world circumstances

introduce problems to the firm must deal. While the firm has many strategies

available to address these circumstances, strategies that utilize investment or

financing with working capital accounts often offer a substantial advantage over the

other techniques. The importance of working capital management is reflected in the

fact that financial managers spend a great deal of time in managing current assets and

current liabilities like.

Arranging short term financing

• Negotiating favorable credit terms

• Controlling the movement of cash

• Administering accounts receivables

• Monitoring investment in receivables

Decisions concerning the above areas play an important role in maximizing

overall value of the firm. Once decisions concerning these areas are reached, the level

of working capital is also determined in active decision sense, but falls out as residual

from the decision just made.

The management of working capital plays an important role in

maintaining the financial health during the normal course of business. This critical

42

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 43/65

role can be enunciated by examining the flow of resources through the firm. By far

the major flow is the working capital cycle.

This is the loop which starts at the cash and the marketable securities account,

goes trough the current account as direct labour and materials which are purchased

and use to produce inventory, which in turn is sold and generates accounts

receivables, which are finally collected to replenish cash. The major point to notice

about this cycle is that the turnover or velocity of resources through this loop is very

high related to the other inflows and outflows of the cash account.

Concept of working capital:

There are two concepts of working capital

1. Gross Working Capital

2. Net Working Capital

Gross Working Capital:

Gross working capital, simply called as working capital refers tothe firm’s investment in current assets. Current assets are the assets, which in ordinary

course of business can be converted into cash within an accounting year.

Examples of Current Assets are:

• Cash and bank balances

• Short term loans and advances

• Bills Receivables

• Sundry Debtors

• Inventory

• Prepaid Expenses

• Accrued Incomes

• Money Receivable in 12 months

The gross working capital concept focuses attention of two aspects of current assetsmanagement.

43

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 44/65

a) Optimum investment in current assets and

b) Financing of current assets.

The consideration of the level of investment in current assets should avoid

two danger points – excessive and inadequate investment in current arranging funds

to finance current assets. When ever a need for working capital funds arises due to the

increasing level of business activity or for any other reason arrangement should be

made quickly.

Net Working Capital:

Net working capital refers to the difference between the current assets and

current liabilities. Current liabilities are those claims of outsiders, which are accepted,

to mature for payment with an accounting year and include creditors, bills payable

and outstanding expenses.

Net Working Capital = Current Assets – Current Liabilities

Net working capital can be positive or negative. A positive net working capital

will arise when current assets exceeds current liabilities. It is a quantitative

concept. It .

1. Indicate the liquidity position of the firm

2. Suggests the extent to which working capital needs may be financed by

permanent sources of funds.

Types of working capital

Working capital can be classified into two categories i.e.

44

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 45/65

1. Permanent working capital

2. Temporary or variable working capital

Permanent working capital:

It is the minimum amount of investment in all current assets which is required

at all times to carry out minimum level of business activities . Tandon

Committee has reserved to this type of working capital as “ Core Current Assets “.

Characteristics of permanent working capital:

•

Amount of permanent working capital remains in the business in oneform or another.

• It also grows with the size of the business. It is permanently needed for the

business, and therefore, it should be financed out of long term funds.

Variable working capital:

The amount of working capital over permanent working capital is

known as variable working capital. The amount of such working capital keeps

on fluctuating from time to time on the business activities . It may again be

subdivided into seasonal working capital and special working capital Seasonal

working capital is required to meet the seasonal demands of busy periods

occurring at stated intervals on the other hand , special working capital is

required to meet extraordinary needs for contingencies.

DATA ANALYSIS AND INTERPRETATION

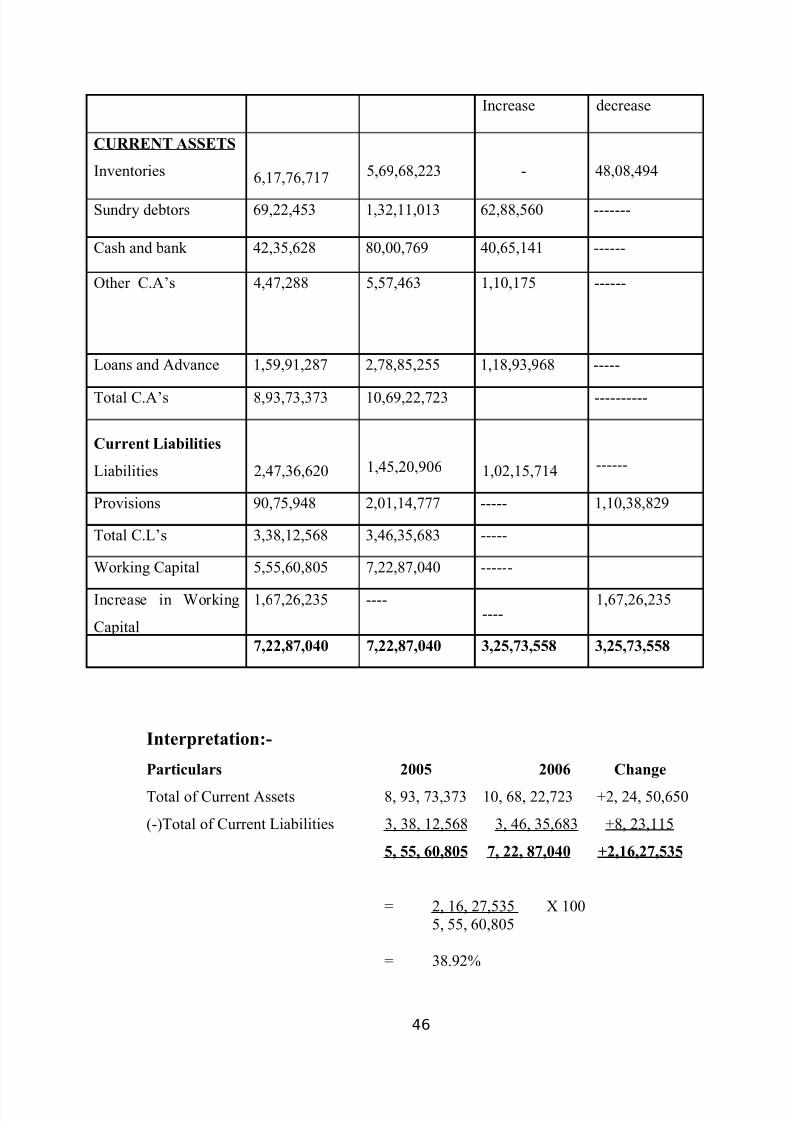

Statement of change in working capital 2005-2006

particulars 2005 2006 Working capital

45

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 46/65

Increase decrease

CURRENT ASSETS

Inventories 6,17,76,717 5,69,68,223 - 48,08,494

Sundry debtors 69,22,453 1,32,11,013 62,88,560 -------

Cash and bank 42,35,628 80,00,769 40,65,141 ------

Other C.A’s 4,47,288 5,57,463 1,10,175 ------

Loans and Advance 1,59,91,287 2,78,85,255 1,18,93,968 -----

Total C.A’s 8,93,73,373 10,69,22,723 ----------

Current Liabilities

Liabilities 2,47,36,620 1,45,20,906 1,02,15,714 ------

Provisions 90,75,948 2,01,14,777 ----- 1,10,38,829

Total C.L’s 3,38,12,568 3,46,35,683 -----

Working Capital 5,55,60,805 7,22,87,040 ------

Increase in Working

Capital

1,67,26,235 --------

1,67,26,235

7,22,87,040 7,22,87,040 3,25,73,558 3,25,73,558

Interpretation:-

Particulars 2005 2006 Change

Total of Current Assets 8, 93, 73,373 10, 68, 22,723 +2, 24, 50,650

(-)Total of Current Liabilities 3, 38, 12,568 3, 46, 35,683 +8, 23,115

5, 55, 60,805 7, 22, 87,040 +2,16,27,535

= 2, 16, 27,535 X 100

5, 55, 60,805

= 38.92%

46

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 47/65

1) The is an increase in the working capital by 2,16,27,535 i.e., 38.92%

2) The sundry debtors have been increased to 90% when compared to previous year

3) The cash and bank balance, other C.A’s and loans and advance were increased

constantly like and advances were increased constantly like 95%, 25% and 74%

respectively.

4) The inventories were decreased to 7.7% with respect to last year.

5) The liabilities were decreased to 4% when compared to last tear.

6) The provisions were increased to 98% gradually when compared to last year.

Hence the companies’ present position is satisfactory

Funds flow statement of 2005-2006

Sources Amount Applications amount

Reserves & surplus 3,02,60,311 Secured loans 1,65,09,934

Unsecured Loans 21,66,000 Differed Tax 6,45,984

Fixed Assets 15,34,142 Increase in the

Working Capital

1,67,26,235

3,39,82,153 3,39,82,153

Interpretation:-

47

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 48/65

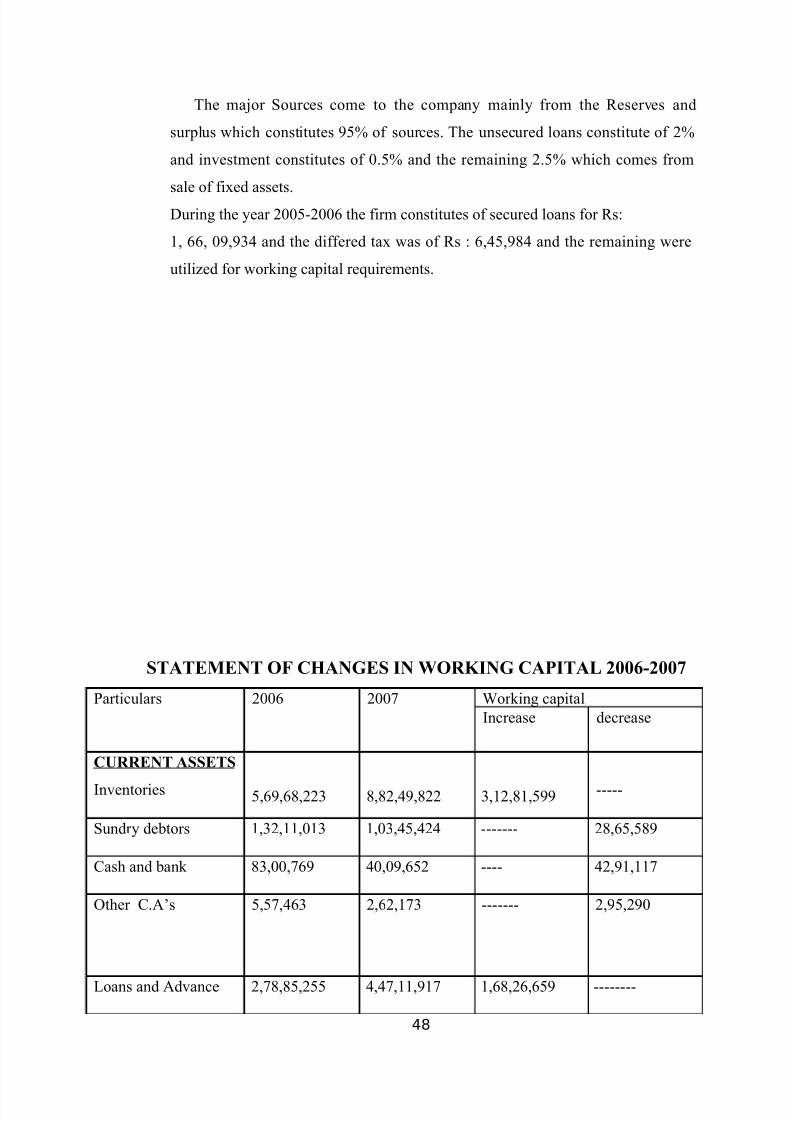

The major Sources come to the company mainly from the Reserves and

surplus which constitutes 95% of sources. The unsecured loans constitute of 2%

and investment constitutes of 0.5% and the remaining 2.5% which comes from

sale of fixed assets.

During the year 2005-2006 the firm constitutes of secured loans for Rs:

1, 66, 09,934 and the differed tax was of Rs : 6,45,984 and the remaining were

utilized for working capital requirements.

STATEMENT OF CHANGES IN WORKING CAPITAL 2006-2007

Particulars 2006 2007 Working capital

Increase decrease

CURRENT ASSETS

Inventories 5,69,68,223 8,82,49,822 3,12,81,599 -----

Sundry debtors 1,32,11,013 1,03,45,424 ------- 28,65,589

Cash and bank 83,00,769 40,09,652 ---- 42,91,117

Other C.A’s 5,57,463 2,62,173 ------- 2,95,290

Loans and Advance 2,78,85,255 4,47,11,917 1,68,26,659 --------

48

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 49/65

Total C.A’s 10,69,22,723 14,75,78,985 ----------

Current Liabilities

Liabilities 1,45,20,906 2,66,19,990-----

1,20,99,084

Provisions 2,01,14,777 2,92,40,145 ----- 91,25,368

Total C.L’s 3,46,35,683 5,58,60,135 -----

Working Capital 7,22,87,040 9,17,18,850 ------

Increase in Working

Capital

1,94,31,810 --------

1,94,31,810

9,17,18,850 9,17,18,850 4,81,08,258 4,81,08,258

INTERPRETATION:-

Particulars 2006 2007 Change

Total of Current Assets 10, 69, 22,723 14, 75, 78,985 +4, 06, 56,262

(-)Total of Current Liabilities 3, 46, 35,683 5, 58, 60,135 +2, 12, 24,4527, 22, 87,040 9, 17, 18,850 +1,94,31,810

= 1, 94, 31,810 X 100

7, 22, 87,040

= 26.88%

There is an increase in the working capital by Rs: 1, 94, and 31,810 i.e. 26.88

%.

The inventories and loans and advances where been increased constantly by

55% and 60% respectively.

Whereas the sundry debtors, cash and bank balance and other current assets

were been decreased to 21%, 51%, and 52% respectively,

The liabilities and provisions were been increased gradually by 83% and 45%.

49

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 50/65

Hence the present position of the company in increase its satisfactory. But the

company has to increase its level of cash and bank balance and other current

assets.

Here the company’s position is quite good.

Funds flow statement of 2006-2007

Sources Amount Applications amount

Reserves & surplus 1,38,38,235 Differed Tax

Increase in the

Working Capital

5,58,221

Secured loans 35,24,313

Unsecured Loans 8,36,000 1,94,31,810

Fixed Assets 17,91,483

1,99,90,031 1,99,90,031

INTERPRETATION:-

Here the major sources come to the company mainly from the reserves and

surplus which constitutes of 945. The secured loans and the unsecured loans

constitutes of 2% and 1% respectively the remaining 3% of sources comes from the

sale of fixed assets.

In this year 2006-2007 the firm mainly constitutes of differed tax of Rs: 5, 58,221

from its applications and the remaining was utilized for the working capital

requirements.

50

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 51/65

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 52/65

9,17,18,850 9,17,18,850 4,50,07,647 4,50,07,647

INTERPRETATION:-

Particulars 2007 2008 Change

Total of Current Assets 14,75,78,98 12, 08, 28,113 -2, 67, 50,872

(-)Total of Current Liabilities 5,58,60,135 5,42,47,38 -16,12754

9,17,18,850 6,65,80,732

-2,51,38,118

= 2, 51, 38,118 X 100

9, 17, 18,850

= 27.40%

There is a decrease in the working capital by Rs:2,51,38,118 i.e. 27.40%

The inventories and loans and advances were decreased by 26% and 39.3%respectively.

Whereas the sundry debtors and cash & bank balance were increased to 86%

and 90% respectively.

And other C.A’s were also gradually increased to 78.6%.

The liabilities were decreased to 16.5% and the provision was increased to

20.5 % respectively.

Hence the company’s position is not favorable so it has to increase its

inventory level and loans and advance to uplift its present position.

52

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 53/65

Funds flow statement of 2007-2008

Particulars Amount Particulars amount

Sources

unsecured loans 12,77,000

Applications

reserves & surplus

secured loans

Differed Tax

Differed Tax( asset)

1,46,79,316

57,76,092

40,67,654

Fixed Assets 13,07,881

Decrease in the working

capital

2,51,38,118 31,99,937

2,77,22,999 2,77,22,999

INTERPRETATION

The major sources of the company constitutes of unsecured loans of 3% and

4% of the fixed assets sale and the remaining 93% are from the decrease in the

working capital.

The major part of the applications consist of reserves and surplus of 60% and

secured loans of 20% differed tax of 10% and remaining 10% are by differed tax

asset.

So, the company has to increase its working capital level for its growth.

53

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 54/65

STATEMENT OF CHANGES IN WORKING CAPITAL 2008-2009

Particulars 2008 2009 Working capital

Increase decrease

CURRENT ASSETS

Inventories 6,52,17,785 7,66,65,507 1,14,47,722

-----

Sundry debtors 1,92,46,481 1,70,35,660 ------- 22,09,821

Cash and bank 87,58,692 33,66,329, ---- 53,92,363

Other C.A’s 4,68,286 5,56,229 87,943 ---

Loans and Advance 2,71,37,869 2,99,72,495 28,34,626 -----

Total C.A’s 12,08,28,113 12,75,96,220 -----

Current Liabilities

Liabilities 3,10,21,555 2,50,62,519 59,59,036 ------

Provisions 2,32,25,826 2,09,60,498 22,65,328 ------

Total C.L’s 5,42,47,381 4,60,23,017 -------- ------

Working Capital 6,65,80,732 8,15,73,203 --------

Increase in Working

Capital

1,49,92,471 ---------

1,49,92,471

8,15,73,203 8,15,73,203 2,25,94,655 2,25,94,655

INTERPRETATION:-

Particulars 2008 2009 Change

Total of Current Assets 12, 08, 28,113 12, 75, 96,220 +67,68,107

54

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 55/65

(-)Total of Current Liabilities 5,42,47,381 4,60,23,017 +82,24,364

6,65,80,732 8,15,73,203

1,49,92,471

= 1, 49, 92,471 X 100

6, 65, 80,732

= 22.5%

There is an increase in the working capital of Rs.1,49,92471 I.e.22.5%

The inventories in the company will gone up to 17.5%

The other C.A’s and loans and advances were also gone up by 18.7% and

10.4%

There was a decrease in the level of the cash and bank balances and sundry

debtors by 61.5 % and 11.4 %

The liabilities and the provisions have been decreased to the 19.2 % and 9.75

% respectively.

Here the company’s position is quite satisfactory because the liabilities have been

paid off to some extent.

Funds flow statement of 2008-2009

55

Sources Amount Applications amount

Reserves & surplus 81,39,903 Unsecured loans

increase in working

capital

6,60,000

Secured loans 39,28,797

Differed Tax Assets 22,81,708 1,49,92,471

Fixed Assets 13,02,063

1,56,52,471 1.56,52,471

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 56/65

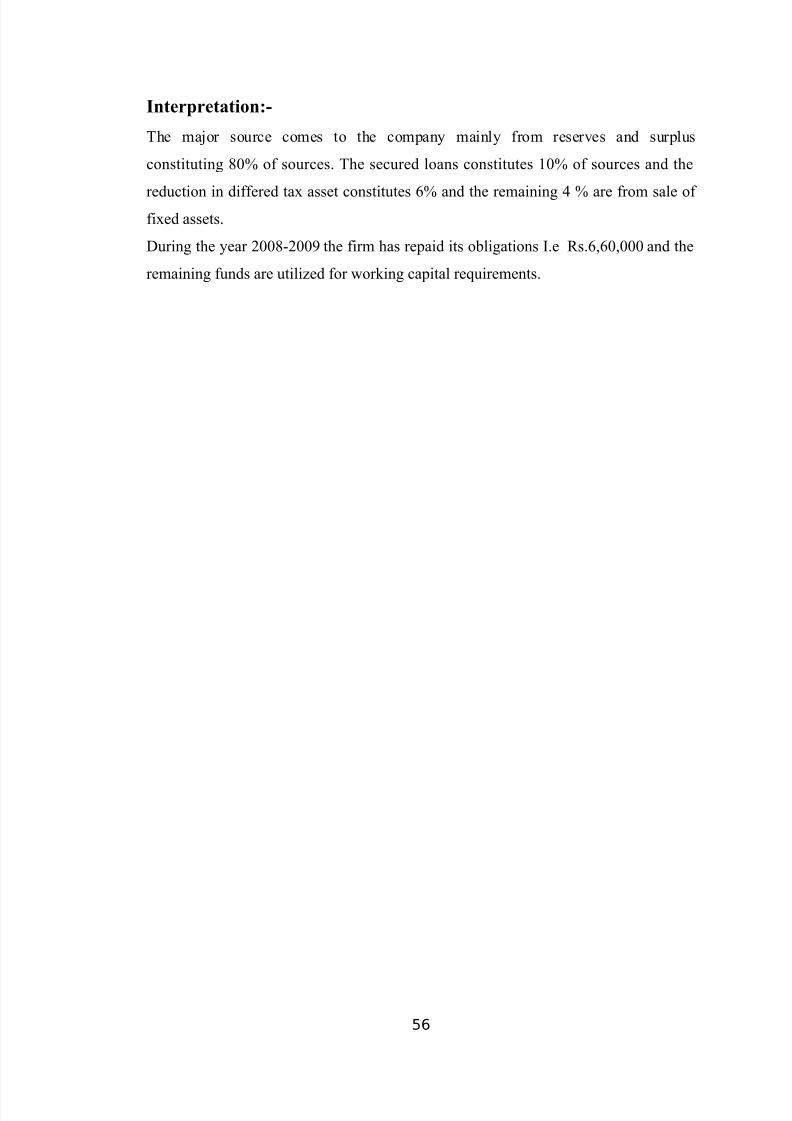

Interpretation:-

The major source comes to the company mainly from reserves and surplus

constituting 80% of sources. The secured loans constitutes 10% of sources and the

reduction in differed tax asset constitutes 6% and the remaining 4 % are from sale of fixed assets.

During the year 2008-2009 the firm has repaid its obligations I.e Rs.6,60,000 and the

remaining funds are utilized for working capital requirements.

56

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 57/65

STATEMENT OF CHANGES IN WORKING CAPITAL 2009-2010

INTERPRETATION:-

Particulars 2009 2010 Change

Total of Current Assets 12, 75, 96,220 14, 59, 57,585 +1,83,61,365

(-)Total of Current Liabilities 4,60,23,017 5,42,40,331 +82,17,314

8,15,73,203 9,17,17,254

+1,01,44,051

57

Particulars 2009 2010 Working capital

Increase decrease

CURRENT ASSETS

Inventories

7,66,65,507 5,58,31,186 ----- 2,08,34,321

Sundry debtors 1,70,35,660 1,76,61,911 6,26,251 ------

Cash and bank 33,66,329, 30,82,331 ---- 2,83,998

Other C.A’s 5,56,229 2,75,853 ---- 2,80,376

Loans and Advance 2,99,72,495 6,91,06,304 3,91,33,809 -----

Total C.A’s 12,75,96,220 14,59,57,585 ------- -----

Current Liabilities

Liabilities2,50,62,519

1,95,14,071 55,48,448

------

Provisions 2,09,60,498 3,47,26,260 ------- 1,37,65,762

Total C.L’s 4,60,23,017 5,42,40,331 -------- ------

Working Capital 8,15,73,203 9,17,17,254 -------- ----

Increase in Working

Capital

1,01,44,051 ---- ----- 1,01,44,,051

9,17,17,254 9,17,17,254 4,53,08,508 4,53,08,508

8/3/2019 Sindhu Main Project

http://slidepdf.com/reader/full/sindhu-main-project 58/65

= 1, 01, 44,051 X 100

8, 15, 73,203

= 12.4%

There was an increase in the working capital of Rs.1,01,44,051 I.e 12.4 %