singapore's participation in global value chains: perspectives of trade in value-added

DESCRIPTION

Singapore's Participation in Global Value Chains: Perspectives of Trade in Value-AddedTRANSCRIPT

ERIA-DP-2015-50

ERIA Discussion Paper Series

Singapore’s Participation in Global Value

Chains: Perspectives of Trade in Value-

Added

Mun-Heng TOH

National University of Singapore

July 2015

Abstract: This paper reviews the cluster-based development strategy adopted in

Singapore. That strategy has enabled Singapore to be plugged into global value

chains (GVAs) to benefit from inflows of foreign investment and participation in

international trade. The OECD-WTO Trade in Value-Added (TiVA) database was

made public recently and has been mostly used in studies relating to trade policies

and GVCs. This paper makes use of information and indicators of GVC participation

from the TiVA database with specific reference to Singapore. New concepts and the

implications of trade in value-added are appraised to provide new perspectives of,

and prospects for, continued sustainable growth of Singapore’s economy.

Key words: global value chain, trade in value-added, cluster development,

agglomeration, foreign direct investment

JEL Classification: F14, F24, O19, and O24.

1

In this paper, we begin with an overview of the economic development

performance of Singapore’s economy since the 1960s. In the process, we explore new

concepts and implications of trade in value-added and global value chains (GVCs) that

can provide new perspectives of, and prospects for, continued sustainable growth of

the economy. Following this introduction, Section 2 provides an overview of

Singapore’s economic development history. Included in the section are the twin pillars

of growth in Singapore’s economy: international trade and inflows of foreign

investment are profiled. Section 2 is dedicated to the discussion of Singapore’s

economic development strategies adopted amidst intensification of the globalisation

phenomenon, especially so after the fall of Berlin Wall in 1989. In Section 3, the advent

of the new concepts and interest in trade in value-added are considered with particular

attention to the likely impact on economic development policy. Section 4 summarises

the major findings, together with the implications for economic management and policy

formulation.

1. Overview of Singapore’s Economy

The development history of Singapore’s economy is not a long one. Before 1960,

Singapore was simply a trading post in Southeast Asia for the British Colonial

Administration. With the eclipse of the British Empire, and rising fervour for self-

government and independence by inhabitants of the island, Singapore was granted self-

government in 1959. Following a brief period of amalgamation with Malaysia from

1963, Singapore became an independent sovereign state on 9 August 1965. Its earlier

hopes for economic emancipation lay in the adoption of an import substitution strategy

supported by a Pan-Malayan market. When Singapore separated from Malaysia, the

development strategy had to switch to one of export-oriented industrialisation

dependent on foreign investment and global markets, management expertise and

technological know-how. Capitalising on its strategic geographical location linking

major markets of the eastern and western hemispheres, transportation infrastructure in

seaports and airports were built and continuously upgraded to attract shipping lines and

airlines, generating excellent connectivity to facilitate trade and investment.

2

Singapore’s economy has evolved from an entrepôt economy in the early 1960s

into one that is powered by modern industries, such as electronics, chemicals and

pharmaceuticals, and sophisticated service industries in the areas of finance, business

consultancies, and medical and education services. It is now a hub for many types of

economic activities: financial services, IT services, medical services, electronics,

aviation, and education services. Over a period of five decades, from 1973 to 2013,

GDP at constant 2005 prices increased by 37 times, from S$8,745 million to S$324,592

million. The average annual growth rate during the same period was 7.2 percent.

Singapore’s GDP per capita on a PPP basis stood at $64,584 in 2013, ranking Singapore

third in the IMF’s list of countries. A summary of the economic statistics is presented

in Table A1 in the Appendix.

1.1. International Trade

The remarkable growth performance of Singapore’s economy is attributed to the

twin strategies of trade expansion and powering its industrialisation driven by foreign

capital, technology and international market access.

Following the recommendation of a United Nations study mission, import

substitution industrialisation was selected as a solution to move Singapore away from its

overdependence on entrepôt trade. Beginning in 1960, tariffs and quotas on manufactured

goods were introduced for the first time. The objective was to encourage the setting-up of

import-substituting firms. The import substitution policy was intensified when

Singapore joined Malaysia in 1963. By the end of 1965, import duties had been

imposed on 157 items including steel bars, sugar, cement, chocolates and a range of

plastic and chemical products, whilst 230 commodities were subject to import quotas.

It was believed that a Pan-Malaysia market would ensure success of the policy.

However, the policy of import substitution proved to be ineffective, because it tended

to develop inefficient domestic manufacturing industries, especially at a time when the

domestic market was limited and lacked sophistication. Inflows of foreign capital were

unimpressive despite the various fiscal incentives and concessions provided by the

Government through the investment promotion agency, the Economic Development

Board (EDB), established in 1961. The separation of Singapore from Malaysia in 1965

spelt the end of the import substitution phase.

3

The policy that gave Singapore a head start in attracting foreign capital was the

Government’s highly liberal stance on ownership, at a time when foreign investment

was viewed with suspicion by other developing countries following the experience of

the Latin American economies. Transnational corporations (TNCs) were footloose and

exploitative. After 1965, the Government consistently maintained an open policy

towards foreign ownership and operations. There were no restrictions on equity

ownership, no foreign-exchange controls and no limits on the repatriation of capital,

dividends, interest or royalties. There were no restrictions on foreign borrowings from

the domestic capital market and no regulations governing the transfer of technology.

Furthermore, the Government was willing to co-invest with foreign companies if there

was a need for risk-sharing and the nurturing of business confidence.

Nonetheless, the transition from an import substitution mindset towards an export

promotion strategy was far from easy. Several structural adjustments had to be made.

In Singapore’s case, the domestic market was small and unable to absorb the goods

manufactured by foreign enterprises. It was therefore vital to gain access to foreign

markets, which in turn required Singapore to become an open economy. Free trade

zones that were previously restricted to areas around the ports expanded their coverage

to include the whole island. Except for a few import duties on ‘sinful’ goods such as

alcohol and tobacco, tariffs were rapidly removed. New institutions and codes of

practice were put in place. In this new environment, there was no place for xenophobia,

and once the course of action had been decided, there was no turning back. The

environment had to be made conducive for investment and growth. Resources had to

be mobilised and used effectively, whilst the welfare of workers and citizens had to be

given concerted attention. Low levels of investment would have meant that fewer jobs

would be created with the risk that increasing unemployment could have led to

desperation, in turn leading to social unrest and increasing levels of crime. In such a

vicious circle, growing social unrest and crime would have also had an adverse impact

on the investment climate.

Table 1 illustrates the reliance on trade expansion to power economic growth over

the five decades from 1965.

4

Table 1: Export, Import, and GDP in Singapore, 1965–2013 (S$ million)

Export

Domestic

Export Import

Re-

Export

Nominal

GDP

Export

GDP

(%)

Import

GDP

(%)

Re-Export

GDP

(%)

1965 3,004 - 3,807 2,982 100.7 127.7 -

1970 4,756 1,832 7,534 2,924 5,876 80.9 128.2 61.5

1975 12,758 7,540 19,270 5,218 13,722 93.0 140.4 40.9

1980 41,452 25,805 51,345 15,647 25,117 165.0 204.4 37.7

1985 50,179 32,576 57,818 17,603 39,036 128.5 148.1 35.1

1990 95,206 62,754 109,806 32,452 66,778 142.6 164.4 34.1

1995 167,515 98,473 176,313 69,042 119,470 140.2 147.6 41.2

2000 237,826 135,938 232,175 101,888 159,840 148.8 145.3 42.8

2005 382,532 207,448 333,191 175,084 201,313 190.0 165.5 45.8

2010 478,841 248,610 423,222 230,231 318,096 150.5 133.0 48.1

2013 513,391 274,192 466,762 239,199 370,065 138.7 126.1 46.6

Source: Singapore Yearbook of Statistics, Department of Statistics, Ministry of Trade and Industry,

Singapore.

When Singapore became an independent nation in 1965, the merchandise exports-

to-GDP ratio was already a high 101 percent. Subsequently, the ratio reached a peak of

190 percent in 2005, before declining to 139 percent in 2013. Over the period, imports

grew at a rate that was commensurate with that of exports, reflecting the high

dependence of export activities on imports. Imported materials, parts and components

were used to produce final goods and services that were then sold both locally and

abroad.

Singapore’s role as an entrepôt port for the region did not really decline when the

country embarked on its industrialisation strategy. Its strategic geographical location

has made Singapore a key dissemination centre for the region. Goods are imported into

Singapore in bulk before being broken into smaller consignments to be re-exported to

other destinations. Re-exports as a proportion of total exports were high, at 62 percent

in 1970, but this later declined to 34 percent in 1990, before rising to 47 percent in

2013. It has often been said by analysts that entrepôt activities are low in value-added

5

and attention should be focused on domestic exports, the other component of total

exports.1

Singapore’s domestic exports are exports of Singaporean origin and comprise, (i)

primary commodities grown or produced in Singapore; and (ii) goods that have been

transformed, i.e., manufactured, assembled or processed in Singapore, including those

with imported materials or parts. In recent years, almost half of the total exports are

domestic exports, compared with about 40 percent in 1970.

The changing composition of goods exported over the years (1970 to 2013) is

shown in Figure 1. The shares of conventional items, such as food, beverages and

tobacco, crude material and non-mineral oil in total exports have continually declined.

In contrast, the shares of goods classified as machinery and transport equipment

(including computers, electronic products and components) exhibited a distinct upward

trend between 1970 and 2000, before switching to a declining trend. International crises

such as the Asian financial crisis in 1997, the dot.com bubble in 2000, and competition

from the mega emerging economies such as China and India, may account for the

declining shares. The exports of goods classified as machinery and transport equipment

are examples of Singapore-based enterprises participating in the GVCs or global

production networks (GPNs). This will be elaborated upon in the next section.

1 Total Export = Domestic Exports + Re-exports.

6

Figure 1: Percentage Composition of Merchandise Exports &

Services Export as Percentage of Total Merchandise Exports, 1970-2013

Source: Yearbook of Statistics, Singapore Department of Statistics.

Another category of goods that has recorded a rising share of total exports is

chemicals. Chemicals exports increased from less than 3 percent in 1970 to more than

12 percent in 2013. The shares of exports of mineral oil products such as petroleum

and lubricants, exhibit a pattern of changes that is opposite to that of machinery and

transport equipment starting in 1982. Declining oil prices starting in the early 1980s

suppressed its export contribution. This declining share was reversed in the 2000s when

oil prices moved upwards.

Figure 1 also shows the share of services exports as a percentage share of total

merchandise exports. Although the share varies from year to year, it remains relatively

stable within a band of 20 to 40 percent since 1983. Participation in GVCs, as some

analysts have claimed, allows the contribution of services exports to be maintained.

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

19

70

19

73

19

76

19

79

19

82

19

85

19

88

19

91

19

94

19

97

20

00

20

03

20

06

20

09

20

12

PER

CEN

TAG

E (%

)

Food, Bev & Tobacco

Crude Material & Non-MinOil

Mineral Oil

Chemicals

Manufactured Goods

Machinery & TransportEquipment

MiscellaneousManufactured Goods

Services Export

7

1.2. Foreign Direct Investment

The unemployment situation in the post-independence years was serious.

According to the household survey conducted in 1966, the unemployment rate was 9.2

percent. Job creation became a priority. Local entrepreneurship and expertise essential

for kick-starting the industrialisation campaign were lacking. Many of the leaders and

owners of local enterprises had made their fortunes as shrewd traders rather than

successful industrialists. Policymakers in the Government decided to invite foreign

capital and entrepreneurs to come to Singapore to establish their production bases and

to create employment opportunities. In modern terminology, Singapore became an

outsourcing centre for the foreign multi-national companies (MNCs). A government

agency called the Economic Development Board (EDB) was tasked with providing a

one-stop service centre to facilitate and hasten the setting-up of foreign enterprises in

Singapore. Fiscal incentives such as tax holidays, and the restriction-free repatriation

of profits, as well as incentives and grants for export expansion, were put in place.

Complementing these fiscal incentives were industrial sites with pre-fabricated factory

buildings and physical infrastructure such as communications, telecommunications and

transportation, all of which contributed directly to efficiency and competitiveness. Human

resource development in both education and skills training is vital for Singapore as its

labour force is its only renewable resource. As the locational factor has been attenuated

by information technology and telecommunications, breaking the tyranny of time and

space, so the human factor as a competitive strategy has become more important.

The many efforts made to attract foreign capital to Singapore soon bore fruit. FDI

not only supplemented the limited savings and capital formation in Singapore. Foreign

enterprises also brought along their technological know-how, managerial skills, and

market accessibility in developed economies, in addition to the many jobs created to

be filled by local workers. Indeed, about seven years after independence, in 1972, the

labour market was already tight and foreign workers from neighbouring countries, as

well as from sources in South Asia, were being tapped.

The National Wages Council (NWC) was formed in 1972 to ensure orderly wage

increases in tandem with Singapore's international competitiveness. Furthermore, the

Secretary General of the National Trade Union Congress (NTUC) was also made a cabinet

minister, enabling direct feedback regarding labour concerns to the ruling echelon, a

8

reflection of the importance placed on harmonious employee-employer relationships in

fostering wealth creation. By and large, healthy industrial relations and favourable labour

market conditions formed a virtuous circle and created a conducive environment for FDI.

Inflows of FDI enabled Singapore to become plugged into GVCs and GPNs2

relatively quickly. It is not surprising that the industrialisation drive attracted

predominantly FDI in the manufacturing sector in the initial years. However, as the

manufacturing sector grew, so did demand for supporting services in logistics, finance,

and professional business services, and FDI in these sectors increased in tandem. In

1985, as indicated in Table 2, stock of FDI in manufacturing was about half of the total

stock of FDI of S$22.4 billion in Singapore. In 2012, the stock of FDI in financial and

insurance services was half of the total S$747 billion, whilst the share of stock of

manufacturing FDI shrank to about 17 percent.

Table 2: Singapore - Foreign Direct Investment by Industry (S$ million)

1985 1995 2000 2005 2010 2012

Total FDI 22,355 84,267 191,453 323,821 626,383 746,690

Manufacturing 11,288 30,626 69,078 103,666 133,591 128,515

Computer, Electronic and Optical

Products - 12,223 34,435 29,796 41,139 41,177

Construction 231 969 2,079 925 1,468 2,626

Wholesale & retail trade 2,964 11,697 27,448 54,548 108,722 126,821

Restaurants & hotels 2,016 2,044 3,812 4,827

Transport & storage -85 2,655 8,446 17,652 36,794 37,711

Information & communications 1,191 3,693 5,937 7,700

Financial & insurance services 7,884 38,238 68,440 121,659 271,261 359,576

Real estate, rental & leasing 6,831 8,274 20,083 27,091

Business services 5,737 10,939 35,174 39,575

Others 188 422 9,542 12,248

Source: Yearbook of Singapore, Department of Statistics.

2 The value chain describes the full range of activities that firms and workers do to bring a product

from its conception to its end use and beyond. This includes activities such as design, production,

marketing, distribution and support to the final consumer. The activities are often carried out in

different parts of the world, hence the term global value chain. The fragmentation of production

along GVCs to take the form of a global production networks (GPNs). More detail discussion of

the concepts can be found in Kaplinsky (2000) and Wood (2001).

9

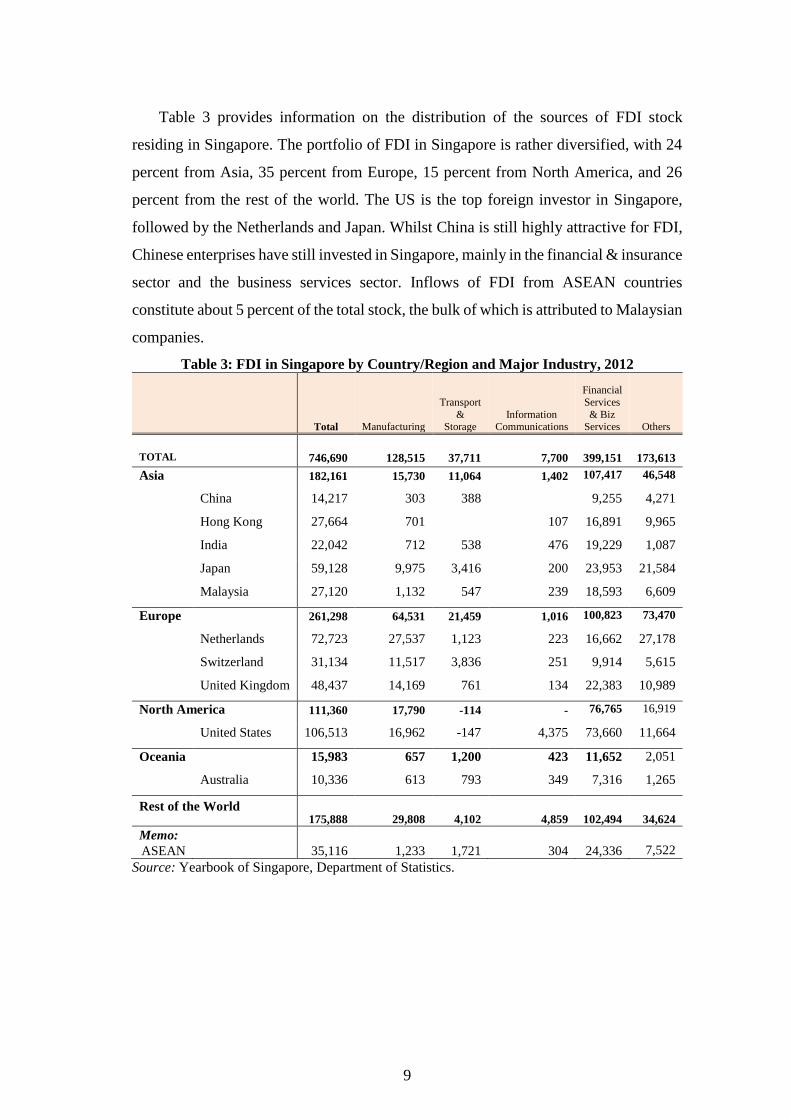

Table 3 provides information on the distribution of the sources of FDI stock

residing in Singapore. The portfolio of FDI in Singapore is rather diversified, with 24

percent from Asia, 35 percent from Europe, 15 percent from North America, and 26

percent from the rest of the world. The US is the top foreign investor in Singapore,

followed by the Netherlands and Japan. Whilst China is still highly attractive for FDI,

Chinese enterprises have still invested in Singapore, mainly in the financial & insurance

sector and the business services sector. Inflows of FDI from ASEAN countries

constitute about 5 percent of the total stock, the bulk of which is attributed to Malaysian

companies.

Table 3: FDI in Singapore by Country/Region and Major Industry, 2012

Total Manufacturing

Transport

& Storage

Information Communications

Financial

Services

& Biz Services Others

TOTAL 746,690 128,515 37,711 7,700 399,151 173,613

Asia 182,161 15,730 11,064 1,402 107,417 46,548

China 14,217 303 388 9,255 4,271

Hong Kong 27,664 701 107 16,891 9,965

India 22,042 712 538 476 19,229 1,087

Japan 59,128 9,975 3,416 200 23,953 21,584

Malaysia 27,120 1,132 547 239 18,593 6,609

Europe 261,298 64,531 21,459 1,016 100,823 73,470

Netherlands 72,723 27,537 1,123 223 16,662 27,178

Switzerland 31,134 11,517 3,836 251 9,914 5,615

United Kingdom 48,437 14,169 761 134 22,383 10,989

North America 111,360 17,790 -114 - 76,765 16,919

United States 106,513 16,962 -147 4,375 73,660 11,664

Oceania 15,983 657 1,200 423 11,652 2,051

Australia 10,336 613 793 349 7,316 1,265

Rest of the World 175,888 29,808 4,102 4,859 102,494 34,624

Memo:

ASEAN 35,116 1,233 1,721 304 24,336 7,522

Source: Yearbook of Singapore, Department of Statistics.

10

2. Economic Development Philosophy and Strategy

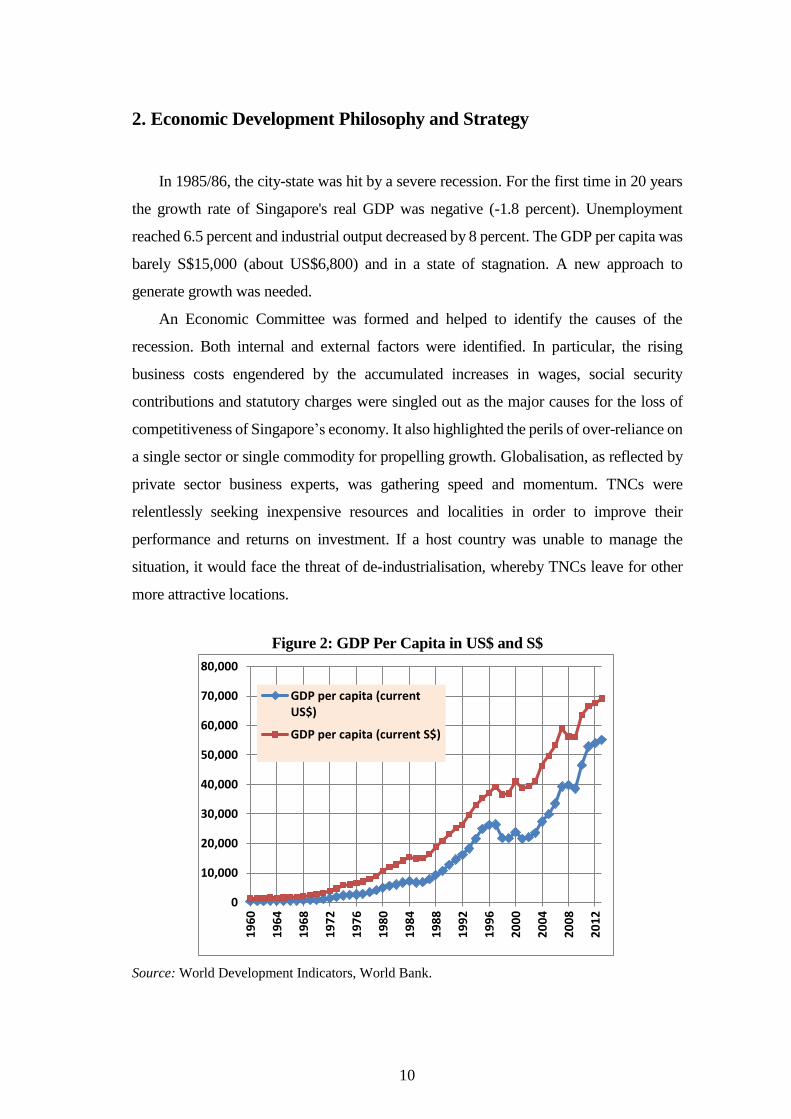

In 1985/86, the city-state was hit by a severe recession. For the first time in 20 years

the growth rate of Singapore's real GDP was negative (-1.8 percent). Unemployment

reached 6.5 percent and industrial output decreased by 8 percent. The GDP per capita was

barely S$15,000 (about US$6,800) and in a state of stagnation. A new approach to

generate growth was needed.

An Economic Committee was formed and helped to identify the causes of the

recession. Both internal and external factors were identified. In particular, the rising

business costs engendered by the accumulated increases in wages, social security

contributions and statutory charges were singled out as the major causes for the loss of

competitiveness of Singapore’s economy. It also highlighted the perils of over-reliance on

a single sector or single commodity for propelling growth. Globalisation, as reflected by

private sector business experts, was gathering speed and momentum. TNCs were

relentlessly seeking inexpensive resources and localities in order to improve their

performance and returns on investment. If a host country was unable to manage the

situation, it would face the threat of de-industrialisation, whereby TNCs leave for other

more attractive locations.

Figure 2: GDP Per Capita in US$ and S$

Source: World Development Indicators, World Bank.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

19

60

19

64

19

68

19

72

19

76

19

80

19

84

19

88

19

92

19

96

20

00

20

04

20

08

20

12

GDP per capita (currentUS$)

GDP per capita (current S$)

11

The Economic Committee report had a profound influence on subsequent investment

policies in Singapore. The services sector was seen to be another source of growth. In

1986, the EDB set up the Services Promotion Division (SPD), which focused on the

development of financial and engineering services, telecommunications, and information

technology, as well as educational and medical services.

The Pioneer Incentives Act and the Economic Expansion Act legislated in 1968 were

extended to include promotion of investment in services. Between April 1985 and April

1986 alone, the EDB awarded pioneer status to 14 companies in the services sector. The

importance of local entrepreneurs was recognised and concerted efforts were made to

promote local small and medium enterprises (SME). An iconoclastic initiative known as

the local industry upgrading programme (LIUP) was started in 1986 by the EDB to foster

closer cooperation and partnerships between TNCs and local enterprises. TNCs provided

mentorship to local SMEs in the form of elevating managerial skills and raising technical

competence to achieve quality standards demanded in international markets. The SMEs

were helped through such programmes to be more effective in supporting industries.

Some of them have since grown to become TNCs in their own right.

To help industries regain their international competitiveness, a substantial reduction

(15 percent) in the social security contributions (CPF) by the employers was introduced.

As a longer-term solution, the workers’ remuneration structure was reformed to take into

consideration the variability in economic performance due mainly to external demand

shocks. Furthermore, rising business and production costs could only be ameliorated if

land- and labour-intensive activities could be strategically guided to relocate to

neighbouring countries that were better endowed with land and labour. This marked the

beginning of the concept of ‘growth triangle’ whereby industrial sites, with the approval

and cooperation of the private sector and governments of neighbouring countries, were

developed to enable the incumbent TNCs to expand and upgrade their production

activities in the region.3 Meanwhile, new foreign investment could also be attracted to the

region to foster greater economic growth.

The publication of the Strategic Economic Plan (SEP) by the Ministry of Trade and

Industry in 1991 marked the beginning of a new development philosophy. It incorporated

3 For more detailed discussion of the concept of growth triangles and their role in regional economic

development, see Toh and Low (1993).

12

concepts such as competitive advantage, value chains and agglomeration economies in

industrial development and strategic business management.

The Strategic Economic Plan sets the strategies and programmes for Singapore

to realize a vision - to attain the status and characteristics of a first league

developed country within the next 30 to 40 years. Key facets of the Vision are

economic dynamism, a high quality of life, a strong national identity and the

configuration of a global city.

Strategies for the long term, which will also produce some benefits for

Singapore in the short to medium term, are directed at maintaining and

extending the nation's inter-national competitiveness. Eight strategic thrusts

have been identified to help propel Singapore's economic and social progress to

that of a developed country.

They are:

Enhancing Human Resources

Promoting National Teamwork

Becoming Internationally Oriented

Creating a Conducive Climate for Innovation

Developing Manufacturing and Service Clusters

Spearheading Economic Redevelopment

Maintaining International Competitiveness

Reducing Vulnerability

- MITI (1991), Executive Summary

Strategic Economic Plan, page 1

Obviously, from the excerpt above, we can note all the sound bites and concepts

resembling those found in the modern industrial organisation and business strategic

management literature. They are arduously advocated by competitiveness gurus such as

Michael Porter, Bruce Scott, and Gary Hammel. Singapore adopted the cluster-based

approach in economic development.4 In fact, as a precursor to the Strategic Economic

Plan, the EDB in an international forum called ‘Global Strategies: The Singapore

Partnership’ declared Singapore’s development philosophy:

If it cannot be the final destination of goods, Singapore can still be a place to

send them on their way. Even if it cannot absorb much more large industry within

its borders, it can facilitate and help manage industrial operations in a nearby

location. . . .

4 For extant discussion on cluster approach to economic development can be found in Best (1999),

Cortright (2006) and Porter (1990). A related area is ‘new economic geography’ associated with the work of Fujita, et al. (1999); Krugman (1991 and 1995).

13

First, competitiveness, differentiation, as opposed to low cost, is pursued.

Singapore cannot be as cheap as other up-and-coming developing countries.

What Singapore can do is to provide superior and technical skills. Businesses

will derive maximum value by operating from Singapore.

Second, Singapore considers the nation as part of a chain of value adding

activities. It will look at the total value chain, seeking to optimize every part of

it. This means close coordination of infrastructure development, manpower

training, development of industrial estates and business parks, education

policies, and labor policies.

Third, at the corporate level the same value chain analysis will also be applied

by positioning itself to be highly competitive in certain part of the value chain.

Other part of the chain can be established in other countries. It will not only

support the establishment of such activities, either according to vertical or

horizontal division of labor, but will also actively network the Singapore

operation and related ones in other countries.

Finally, it will monitor its overall competitive position closely so that any signs

of the economy losing its competitiveness will be dealt with quickly.

- Economic Development Board

(1988),

Global Strategies: The Singapore

Partnership, pp.10–11

In the Strategic Economic Plan (SEP, Ministry of Trade and Industry, 1991), it was

recognised that an industrial policy that takes into account the relative strengths of

Singapore in specific areas and that intelligently supports those cluster enterprises with

the best chance of becoming world-class, would counter the limitations of small size.

However, the identified clusters still needed to be subject to market tests for efficiency

and competitiveness. Based on an extensive survey of industries, 14 clusters were

identified comprising of commodity trading, shipping, precision engineering, electronics,

information technology, petroleum and petrochemical, construction, heavy engineering,

finance, insurance, general supporting industries, tourism, international hub and domestic

industries. Each of these clusters included enterprises that had some common features or

core capabilities in the form of natural advantages, created competitive advantages or

industry structures or attributes. The Government gave assurances to investors in these

core capabilities or provided special incentives to accelerate their development.

14

Government agencies and statutory boards previously assigned the task of

overseeing the performance and development of specific industries had to re-orientate

and review their scope of responsibilities and coordination from the viewpoint of

cluster development. The EDB, Singapore’s premier agency in charge of attracting

foreign investment and the development of the manufacturing sector, spearheaded the

national cluster development programme. Manufacturing is a key engine of

Singapore’s economy, accounting for some 20 to 25 percent of the GDP. Since 1990,

the manufacturing sector has been re-organised into six major industrial clusters:

electronics, chemicals, precision engineering, biomedical, transport engineering, and

general manufacturing.

The EDB considered how the cluster approach could enable the electronics industry

to achieve further expansion and growth. With rising wages and rentals, Singapore risked

losing its manufacturing base and the threat of industrial hollowing out could not be

ignored. The solution came in the form of two transitions that Singapore had to navigate:

first, an internal transition for TNCs, from labour-intensive to automation; and second,

from automation to integrated manufacturing, and from vertically integrated TNCs to

dynamic clusters. Singaporean operations shed labour-intensive activities and focused

more on engineering-intensive activities, including automation, product redesign,

design for manufacture, and logistics functions associated with regional procurement

including complementary business, logistics, marketing and financial services. For

example, the division for product development projects focused on industrial design,

and engineering activities in Singapore. Assembly and other repetitive manufacturing

operations were relocated primarily in Malaysia, followed by Thailand, Indonesia and

China (Best, 1999).

The threat of de-industrialisation was addressed by relocation and re-organising value

chains. TNCs were enlightened enough to take a cluster and value-chain view of their

production decisions. TNCs did not relocate their entire operations to lower-wage, labour-

surplus destinations. Instead, they maintained non-labour-intensive manufacturing and

higher value-added services related activities in Singapore, and relocated only the

labour-intensive activities off-shore. From the perspective of the focal industry, namely

electronics, all vertically-linked industries became ‘supporting industries’. Horizontal

linkages connect a focal industry with other industries that are complementary in

technology and/or marketing. All such industries involved horizontal linkages are

15

called ‘related industries’. Figure 3 shows the set of industries that can cluster around

electronics.

Figure 3: Industries around Microelectronics

Source: Kotler, P., S. et al. (1997).

In the mid-1990s, the electronics industry remained Singapore’s most important

manufacturing industry, accounting for 36 percent of manufacturing value-added, 25

percent of the manufacturing workforce, and contributed 12 percent of the island’s

GDP. The feasibility and benefits of helping companies to relocate labour- and land-

intensive activities to locations where such resources were in abundance provided support

for Singapore’s active participation in cross-border regional development projects, such

as the SIJORI growth triangle (Toh and Low, 1993; Toh and Ng, 2009), and the

collaborative cross-country establishment of industrial parks such as the Singapore-

Suzhou Industrial Park in China, the Singapore-Bangalore Information Technology Park

in India, and the Viet Nam-Singapore Industrial Park in Hanoi. They provided the space

and opportunities for expansion of Singapore-based enterprises, and the loss in low value-

added activities was compensated for by enhanced returns in the form of advanced

processes and headquarters activities retained in Singapore. Such initiatives serve as nodes

16

of clusters and will eventually develop value chains that spark economic development and

growth benefiting local communities and Singapore.

2.1. Jurong Chemical Island Project – Chemical Hub

Another example of cluster development during this phase of development is the

Jurong Island project, started in 1993 to establish a world-class regional hub for the

chemical industry. In 1990, Singapore was already the home of several world-class

refineries and also the third-largest refining centre in the world. The development of

the petrochemical industry in Singapore is a natural progression, given Singapore's

strong base in petroleum refining, which provides feed stocks such as naphtha for the

petrochemical industry. Figure 4 provides a graphic view of the chemical industry’s

clusters and their linkages to other industries and clusters. The petrochemical industry

could benefit from the expansion of the industries expected to accompany growth of

emerging economies in Asia.

Figure 4: The Chemical Cluster

Source: Economic Development Board.

17

Jurong Island is an artificial island located to the southwest of the main island of

Singapore, off Jurong Industrial Estate. It was formed from the amalgamation of seven

offshore islands, through land reclamation. The Jurong Island project was implemented

based on a total approach to industry development. Central to the industry cluster

concept and development of Jurong Island as an integrated complex was the sharing of

common facilities. These include marine facilities, such as jetties and other berthing

facilities; services such as warehousing, waste treatment, fire-fighting, medical and

emergency response; a common service corridor and infrastructure such as roads and

drains. The objective was to reduce capital investment and minimise operational costs

through creating synergistic linkages, one of which was the concept of sharing

facilities. For instance, feedstock transportation and handling costs could be minimised

and economies of scale generated through the provision of centralised logistics and

common corridors for materials flow.

Currently, Jurong Island hosts over 95 global companies, including heavyweights

such as Shell, ExxonMobil, Chevron, DuPont™, BASF, Sumitomo Chemicals and

Mitsui Chemicals. Jurong Island has drawn cumulative fixed-asset investments of over

S$40 billion and employed about 10,000 in 2012.

Singapore needs to maintain its relevance in GVCs and GPNs. As a result, EDB

officers have worked hard to design viable schemes to enable MNCs to ‘justify’ their

presence in Singapore, despite many emerging competitive locations that now beckon

them. One of these schemes is the Business Headquarters (BHQ) scheme introduced in

1994. The BHQ scheme complements the Overseas Headquarters scheme. The latter

helps local service-oriented companies and TNCs expand in the region. Because

production can be easily shifted based on cost considerations, core business support

capabilities such as product development, logistics operations and management,

merchandising and data management give manufacturers a critical competitive advantage

and broadens Singapore's expertise along the value-added chain. Both the Overseas

Headquarters and the BHQ schemes have a tax holiday for 10 years, but the latter is more

flexible. The five pioneer companies awarded the business headquarters include two

foreign (Baker Hughes, DNV Petroleum Services) and three local firms.

18

2.2. Prospects for Future Growth amidst Global Value Chains

Quest for a Knowledge-Based Economy

Singapore has managed to thrive on GVCs. However, it is not an easy task to

maintain Singapore’s relevance in GVCs. From a long-term perspective, the

Government adheres to the plan of developing Singapore into a knowledge-based

economy. It decided to move upstream in GVCs. Technology and human capital

development took on renewed importance in the new millennium. Under the EDB

Industry 21 initiative, industrial sector development placed emphasis on R&D, product

design and development, process engineering, testing and market research. The

Ministry of Manpower launched its Manpower 21 blueprint, which seeks to transform

Singapore into a country known for its talent, ideas and capital flows. It envisages that

the Singapore of the future will thrive on innovation and knowledge exchanges,

encouraging further innovation amongst its people and attracting creative visitors from

overseas.

The emphasis on technology remains pertinent for continued growth and

sustainability. The National Technology Plan (NTP) implemented since 1991 was

reviewed and continued with a new agenda and new targets under the latest Research,

Innovation and Enterprise (RIE) Plan launched in 2011. Complementing the ESC, the

target for gross expenditure on R&D (GERD) in 2015 is 3.5 percent of GDP, with

private sector R&D increasing its share. Between 2011 and 2015, the Government will

invest S$16.1 in RIE. At the same time, the emphasis on commercialisation of R&D

will be strengthened. The RIE 2015 Plan sets out Singapore’s key R&D strategies, to

support the long-term vision to become a research-intensive, innovative and

entrepreneurial economy similar to Sweden, Finland, or Israel.

Dedicated ministries of technology and other public agencies in charge of

technological development and R&D can be found in several countries. In Singapore,

the Agency for Science, Technology and Research (A*STAR) (formerly known as the

National Science and Technology Board) plays that role. A*STAR comprises 12

research institutes (RIs), with five RIs under the Biomedical Research Council

(BMRC) and seven RIs under the Science and Engineering Research Council (SERC).

A*STAR has a rich talent pool of more than 1,800 research scientists and engineers,

19

half of whom have PhDs. The biomedical science sector is targeted to be a new growth

engine for the economy5 (A*Star, 2009).

As an island state that is highly dependent on trade for economic survival,

Singapore is fully committed to an environment in which trade and investment flows

freely and unfettered. A rules-based trading environment is one that will ensure fair

treatment of all traders, large and small. With the limited progress seen in global multi-

lateral trade liberalisation championed by the WTO, Singapore had embarked on a very

intensive programme to established bilateral free-trade agreements (FTAs) with its

trading partners. The existing ASEAN Free Trade Agreement (AFTA) is an important

first step for regional economic integration and there is still much more that can be

done. FTAs are superhighways that connect Singapore to major economies and new

markets. With FTAs, Singapore-based exporters and investors stand to enjoy a myriad

of benefits, such as tariff concessions, preferential access to certain sectors, faster entry

into markets and intellectual property (IP) protection (IES, 2006). In fact, Singapore is

the most ‘promiscuous’ country in the world in establishing FTAs. Singapore is well-

connected to the world through an extensive network of FTAs. It has so far concluded

18 regional and bilateral FTAs, and is actively negotiating 10 more. In terms of

economic output, the 83 FTA partners together account for over 50 percent of the

world’s GDP. They also represent most of Singapore’s major trading partners,

accounting for more than 30 percent of its domestic exports.

A recent initiative to raise productivity in the economy was the establishment of

the Economic Strategy Committee (ESC) in 2009 to chart out the new roadmap for

Singapore. The ESC recommended seven broad strategies to help Singapore sustains

long-term growth of 3 to 5 percent over the next decade. The seven key strategies are:

1. Growing through skills and innovation

2. Anchor Singapore as a global-Asia hub

3. Build a vibrant and diverse corporate ecosystem

4. Make innovation pervasive, and strengthen commercialisation of R&D

5. Become a smart energy economy

5 A more detailed discussion of the Singapore’s cluster development of the Biomedical Science

sector can be found in Toh and Thangavelu (2008) and Wong, et al. (2009).

20

6. Enhance land productivity to secure future growth

7. Build a distinctive global city and an endearing home

ESC recommendations represent a bold strategic shift towards a focus on

productivity. It recommends a paradigm shift away from population-driven or

immigration-driven economic growth towards productivity-driven economic growth.

Basically, the intention is to make skills, innovation and productivity the drivers of

growth. It recognises that Singapore needs to readjust its economic policies and model

to address its over-reliance on developed markets, the importation of foreign workers

and declining productivity.

The ESC believes that competitive development advantages powered by skills and

innovation will need continuous upgrading of skills through retraining, and

encouraging R&D and investment in technology. The quantity and quality of foreign

workers will be managed through phased increases in foreign-worker levies.

Developing Singapore as a key Global-Asia hub in manufacturing, finance and logistics

will facilitate enterprises based in Singapore to tap into opportunities offered by a rising

Asia. It will help to develop a deeper base of globally competitive Singaporean

enterprises. This is another example of Singapore’s deliberate intention to remain

relevant in GVCs.

3. Global Value Chains and Trade in Value-Added: Importance and

Implications for Development Policies in Singapore

Trade data based on gross flows are increasingly inadequate as a basis for

understanding modern trade, as the value of a final good now comes from many

countries (Grossman, 2010). Around 80 percent of all trade takes place within the

international production networks of TNCs, including contractual relationships

between firms. But around one-third of global trade is now estimated to be intra-firm

trade, occurring within the ownership structure of a single firm or TNC (UNCTAD,

2013). Current trade data, based on gross flows, are failing to capture this shift,

hampering a thorough understanding of modern trade within GVCs.

21

Policymakers need to better understand where production is taking place and how

value is being added. This can only be known through understanding the proportion of

subcontracting components made elsewhere. The input–output technique pioneered by

Nobel Laureate Leontief (1951) offers one way of estimating the source(s) of value (by

country and industry) that is added in producing goods and services for export (and

import). It recognises that growing GVCs mean that a country's exports increasingly

rely on significant intermediate imports (and so, value-added by industries in upstream

countries). The availability of global I-O matrices6 has led to the development of

methodological contributions suggesting more general metrics of GVCs. In particular,

it helps to quantify the value-added embodied in the goods and services traded

internationally. Several recent articles generalise the vertical specialisation concept of

Hummels et al. (2001) and capture different dimensions of value-added embedded in

trade. Essentially, these new databases measure the extent to which countries are

involved in vertically fragmented production.7 This is approximated by the sum of the

value of imported inputs in the overall exports of a country (the backward linkage) plus

the percentage of exported goods and services used as imported inputs to produce other

countries’ exports (the forward linkage). The value-added shares describe the

participation of a country in GVCs, both as a user of foreign inputs and as a supplier of

intermediate goods and services used in other countries’ exports.

3.1. Singapore Participation in GVCs from the Perspective of Trade in Value-

Added

The OECD-WTO Trade in Value-Added (TiVA) database was made public

recently and has been used in many policy-oriented studies. OECD (2013) summarises

the main evidence and policy implications of the OECD’s work on GVCs, including

trade and investment policies targeted to GVCs. In addition, the OECD has produced

6 A recent special issue of the Economic Systems Research provides a very useful and detailed

description of several global multi-regional I-O databases currently available (see Tukker and

Dietzenbacher, 2013). 7 The first studies on the measurement of the value-added of trade in an international I-O framework

were those of Johnson and Noguera (2012a) Daudin, et al. (2011), and Koopman, et al. (2013),

using the Global Trade Analysis Project (GTAP) database.

22

several comparable country notes, including indicators on the relevance of value-added

trade and the participation in GVCs.8

According to information gathered from the OECD-WTO TiVA database, in 2009,

world gross exports amounted to US$17.05 trillion. However, world value-added

exports amounted to US$13.7 trillion (around 19 percent lower than gross exports),

emphasising the extent of double-counting in total trade due to trade in intermediate

inputs related to production network spanning across countries. Whilst world gross

exports as a proportion of GDP increased from 19 percent in 1995 to 25 percent in

2005, and then to 29 percent in 2009, world value-added exports were much lower and

increased from 16 to 18 percent in 2005, and then to 24 percent in 2009. In this paper

we use the information in the OECD-WTO TiVA database to consider Singapore’s

participation in GVCs in the light of the new TiVA indicators available.

Composition of Value-Added in Gross Exports

The global input–output table enables users and policymakers to decompose the

entire value of any good, exported by industry I, into the following components:

(a) Direct domestic value-added from industry I;

(b) Indirect domestic value-added generated via purely domestic transactions,

disaggregated by all domestic industries;

(c) Indirect domestic value-added embodied in imports (broken down by all

domestic industries);

(d) Indirect imported (foreign) value-added (broken down by producing

country and industry)

In Table 4, at the aggregate level, the gross exports of Singapore for selected years

between 1995 and 2009 are decomposed into the four VA components. Foreign value-

added (FVA) made up about 50 percent of gross exports in 2009, and this proportion

is higher than that in 1995 and slightly lower than in 2005.

8 Description of the database and the methodologies used in the computation of the various TiVA

indicators are available in Backer and Miroudot (2013) and Nadim Ahmad (2013).

23

Table 4: Decomposition of Singapore Gross Exports into VA Components

Gross

Export

(US$ m)

Direct

Domestic

VA

Indirect

Domestic

VA

Reimported

Domestic

VA

Total

Domestic

VA

Foreign VA

in Gross

Export

2009 212449 72616 33143 643 106401 106048

2005 160821 51422 24695 519 76636 84185

2000 91860 28321 16571 374 45265 46595

1995 80306 24843 17757 205 42804 37501

Percentage Distribution

2009 100.0 34.2 15.6 0.3 50.1 49.9

2005 100.0 32.0 15.4 0.3 47.7 52.3

2000 100.0 30.8 18.0 0.4 49.3 50.7

1995 100.0 30.9 22.1 0.3 53.3 46.7

Source: OECD-WTO Trade in Value-added (TiVA) Data Base, May 2013.

The global IO tables help in estimating the 'domestic value-added’ content in gross

exports of a country. ‘Domestic value-added exports' will therefore differ from ‘Gross

exports’ and can be estimated by subtracting FVA, i.e., value-added created in other

countries that is imported and enters exports of the country. In Figure 5, the gross

exports and domestic value-added exports for each of the 21 selected countries are

shown. The figures in percent for each country indicate the excess of gross exports over

domestic value-added export expressed as a percentage of gross exports.

24

Figure 5: Domestic Value-Added Exports and Gross Exports, 2009

Source: OECD WTO Trade in Value-Added (TIVA), May 2013.

The extent of the difference between gross exports, and domestic value-added

exports (which equals the FVA in gross exports), varies across countries depending on

a country’s engagement in network trade. The difference in gross exports and value-

added exports is most prominent for Newly Industrialised Countries tier 1 (NICs 1),

such as Singapore (50 percent); Chinese Taipei (42 percent); Korea (41 percent);

followed by NICs 2, namely, Malaysia (38 percent); the Philippines (38 percent);

Thailand (35 percent); and then China (33 percent); Hong Kong, China (28 percent).

For most developed countries FVA in gross exports is less than 30 percent, with the

UK at 17 percent, the US at 11 percent, and Germany at 27 percent.

The share of domestic value-added in gross exports indicates the value-added gains

for a country from exports. The information from the OECD-WTO TiVA database

enables the comparison of the ratio over time. In Figure 6, we plot the percentage point

changes of the ratio between 2009 and 1995 for the 21 selected countries.

Domestic value-added in gross exports has declined substantially for many

developing countries, indicating a rise of foreign value addition in their gross exports.

25

However, for some countries domestic value-added increased in this period. These are

the UK, Italy, Malaysia, the Russian Federation, and Hong Kong, China. The decline

in the US has been marginal (3 percentage points) but very high for countries such as

China (21 percentage points), and Korea (17 percentage points). Singapore, Chinese

Taipei, and Korea have lower domestic value-added shares in gross exports between

1995 and 2009, shaving off 3, 6 and 17 percentage points, respectively.

Figure 6: Percentage Point Change in Share of Domestic Value-Added

in Gross Exports: 2009 over 1995

Source: OECD-WTO Trade in Value-Added (TiVA), May 2013.

Typically, the share of re-imported domestic value-added in gross exports is small.

However, it is an indicator that measures the intensity of value-added crossing borders

and returning to its originating source. It is a rather intuitive measure of participation

in the global production network. Table 5 presents reimported domestic VA share for

the top 20 countries in each of the four benchmark years. Germany and the US have

been consistently ranked amongst the top three in the list. The shares for Singapore

have relatively stable around 0.3 percent for all years except 2000. Worthy of note is

-20.8-16.9

-12.2-8.1-7.9-7.4

-5.7-4.7

-3.2-2.9

-1.9-1.1-0.7

0.30.7

1.82.4

3.43.8

5.812.1

-25.0 -20.0 -15.0 -10.0 -5.0 0.0 5.0 10.0 15.0

ChinaKorea

Viet NamCambodia

JapanPhilippines

Chinese TaipeiThailand

SingaporeUnited States

DenmarkNew Zealand

AustraliaIndonesia

BrazilItaly

MalaysiaUnited Kingdom

Russian FederationBrunei Darussalam

Hong Kong, China

Percentage Points

26

the share of China. This was only 0.13 percent in 1995, increasing steadily over the

years to register 1.1 percent in 2009, displacing Germany as the top performer. A

similar pace of achievement can be seen in the two Asian NIEs: Chinese Taipei and

Korea.

Table 5: Top 20 Countries in Terms of the Share of Reimported Domestic VA

in Gross Exports

Ran

k 2009

ReIm

DVA 2005

ReIm

DVA 2000

ReIm

DVA 1995

ReIm

DVA

1 China 1.10 Germany 1.20 Germany 1.01 Germany 0.81

2 Germany 1.03 China 0.86 USA 0.91 USA 0.45

3 USA 0.58 USA 0.74 France 0.54 France 0.40

4 Chinese Taipei 0.53 Chinese

Taipei 0.59 UK 0.49 UK 0.39

5 Korea 0.48 France 0.50 Malaysia 0.46 Netherlands 0.36

6 Netherlands 0.40 Korea 0.50 Canada 0.41 Belgium 0.35

7 France 0.39 Malaysia 0.47 Singapore 0.41 Canada 0.28

8 Malaysia 0.38 Netherlands 0.45 Netherlands 0.37 Sweden 0.26

9 Japan 0.37 Japan 0.43 Japan 0.36 Italy 0.26

10 Singapore 0.30 UK 0.41 Italy 0.33 Malaysia 0.26

11 Belgium 0.28 Belgium 0.38 Belgium 0.32 Singapore 0.26

12 Switzerland 0.28 Italy 0.36 Sweden 0.27 Czech Rep 0.26

13 UK 0.26 Canada 0.34 Spain 0.25 Japan 0.22

14 Norway 0.25 Singapore 0.32 Norway 0.24 Norway 0.21

15 Sweden 0.24 Denmark 0.30 China 0.23 Slovak Rep 0.19

16 Italy 0.24 Sweden 0.30 Austria 0.23 Austria 0.18

17 Czech Rep 0.23 Spain 0.26 Czech Rep 0.19 Spain 0.17

18 Austria 0.23 Czech Rep 0.25 Chinese

Taipei 0.19 Switzerland 0.16

19 Canada 0.22 Austria 0.25 Korea 0.18 Chinese

Taipei 0.15

20 Philippines 0.22 Norway 0.24 Switzerland 0.17 China 0.13

Source: OECD-WTO Trade in Value-Added (TiVA) Database, May 3013.

FVA in gross exports of a country reflects the total value-added created in other

countries that enters the exports of a country. This measure is viewed to be a better

indicator than the 'import content of exports' measure. Banga (2013) highlighted three

aspects. First, FVA will not double-count, as it includes FVA in all inputs of the

products only once and the number of times the inputs cross borders will not affect its

calculation. It also includes the services component that enters the value addition.

Second, in the GVCs, the FVA will contain not just the FVA content in bilateral trade

but also FVA included in exports of the country's bilateral trading partner. For example,

27

if Singapore imports intermediate products from Malaysia, FVA content in Singapore's

exports will be the sum of value-added created in Malaysia, as well as value-added

created in other countries from where Malaysia, imported its inputs for producing its

intermediate product. It therefore includes all direct imports, as well as indirect imports

(from countries where there is no direct trade). This can have important implications

for bilateral trade balance. Third, the re-imported domestic value-added will be netted

out.

Table 6: Total FVA in Gross Exports (%), 1995–2009

2009 2005 2000 1995

Singapore 49.9 52.4 50.7 46.7 Chinese Taipei 41.5 42.2 35.4 35.8

Korea 40.6 37.7 32.9 23.7

Philippines 38.4 45.6 45.9 30.9

Malaysia 37.9 41.5 43.0 40.3

Viet Nam 36.7 35.0 29.6 24.4

Thailand 34.5 38.5 34.8 29.9

Cambodia 34.1 37.9 34.5 26.0

China 32.6 36.4 18.8 11.9

Denmark 32.0 32.0 26.2 30.1

Hong Kong, China 28.5 28.3 32.6 40.6

Italy 20.1 27.1 25.3 21.9

New Zealand 18.4 19.6 20.2 17.4

United Kingdom 17.3 20.3 18.4 20.7

Japan 14.8 13.8 9.9 6.9

Indonesia 14.4 17.8 19.3 14.7

Australia 12.5 13.0 13.5 11.8

Brunei Darussalam 11.3 6.8 10.4 17.1

United States 11.3 11.1 8.9 8.4

Brazil 9.0 13.0 11.5 9.7

Russian Federation 6.9 8.2 12.5 10.7

Source: OECD-WTO Trade in Value-Added (TiVA) database, May 2013.

Table 6 reports FVA in gross exports (percent) in 21 selected countries. The Asian

tiger economies, i.e., Singapore, Chinese Taipei, and Korea, have relatively high shares

of FVA in gross exports. Indeed, other than Luxembourg, Singapore has the highest

share in 2009. Korea and Chinese Taipei were ranked fifth and sixth, respectively, in

the same year. Other Asian economies, such as the Philippines, Malaysia, Thailand,

28

and Viet Nam, have also experienced a steady rise in their share of FVA in gross

exports, whilst there has been a steady decline in case of Hong Kong, China.

Shares of FVA in gross exports for most developed countries have remained at less

than 30 percent, whilst those of Japan, the US, the UK and Australia have remained at

less than 20 percent. This brings us to the question of whether FVA in gross exports is

an appropriate indicator for measuring the extent of a country’s participation in GVCs.

We examine this issue in some detail in the next section.

Participation in GVCs confers considerable benefits. It may allow suppliers in

developing countries to meet standards and regulations that give them access to

developed country markets; it may allow imports under privileged tariff treatment for

intra-firm trade; it may permit the utilisation of network technology that would not

otherwise be available; and it may open up new sources of capital. The OECD-WTO

database provides an indicator (participation index) that measures the extent of

participation in GVCs. The measure is based on the share of exports involved in a

vertically fragmented production process (Hummels, et al., 2001; Koopman, et al.,

2010). The index is expressed as a percentage of gross exports and indicates the share

of foreign inputs (backward participation) and domestically produced inputs used in

third countries’ exports (forward participation).

The participation index at the country level is represented on Figure 7 for selected

countries. Open economies such as Singapore, Chinese Taipei are amongst the top 10

economies with the high participation index. Small open economies such as Singapore

source more inputs from abroad in GVCs than large countries, such as the US or Japan.

The forward and backward participation indices, which sum to give the participation

index, offer additional information on the type of participation. Singapore and Chinese

Taipei share the same score in the participation index. However, Singapore’s backward

participation is larger than that of Chinese Taipei, reflecting Singapore’s relatively

greater reliance on foreign inputs and value-added to support its export activities. If

gains are measured in terms of ‘net value-added’ by participation in GVCs, then the

higher the forward linkages compared with backward linkages, the higher the gains.

This would imply that by its participation in GVCs, a country is creating and exporting

more domestic value-added than the FVA that it is importing. The ratio of forward to

backward participation therefore can be a measure of the extent of net gains. From this

29

perspective, the Chinese Taipei economy has a ratio that is higher than Singapore, and

hence enjoyed a higher gain in participation in GVCs in 2009.

Figure 7: GVC Participation Index for Selected Economies, 2009

Note: Foreign inputs (backward participation) and domestically produced inputs used in third

countries’ exports (forward participation), as a share of gross exports (%).

Source: OECD-WTO Trade in Value-Added (TiVA), May 2013.

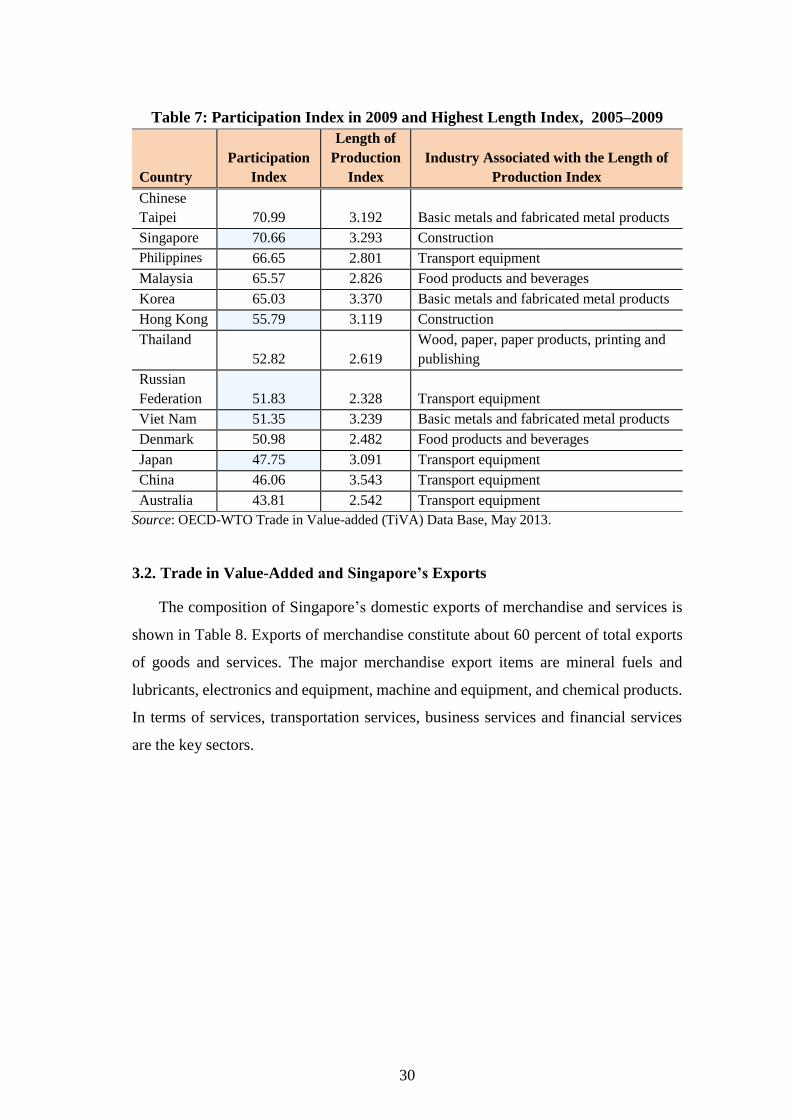

Another popular indicator of participation in GVCs is the index of the number of

production stages. The length of production (LoP) index takes a value of 1 if there is a

single production stage in the final industry and its value increases when inputs from

the same or other industries are used.9 In Table 7, we present the LoP index together

with the participation index for Singapore and other top 10 countries shown in Figure

7. The LoP indices shown correspond to the highest scores achieved during the period

2005-09. As would be expected, the number of production stages can be more than

three in the case of the transport equipment sector, which includes the automobile

manufacturing industry. Other sectors that have a high LoP index include basic metal

and fabricated metal product industries, food products and beverages, and construction

services industries.

9 The formula for computation is found in Backer an Miroudot (2013), page 45, and is included in

the OCED-WTO TiVA database

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Chinese…

Sin

gap

ore

Philippi…

Mal

aysi

a

Ko

rea

Hong…

Thai

lan

d

Russian…

Vie

t N

am

De

nm

ark

Jap

an

Ch

ina

Au

stra

lia

Ind

on

esi

a

Brunei…

United…

Ital

y

Cam

bo…

United…

Bra

zil

New

…

Per

cen

t (%

)

Forward Backward

30

Table 7: Participation Index in 2009 and Highest Length Index, 2005–2009

Country

Participation

Index

Length of

Production

Index

Industry Associated with the Length of

Production Index

Chinese

Taipei 70.99 3.192 Basic metals and fabricated metal products

Singapore 70.66 3.293 Construction

Philippines 66.65 2.801 Transport equipment

Malaysia 65.57 2.826 Food products and beverages

Korea 65.03 3.370 Basic metals and fabricated metal products

Hong Kong 55.79 3.119 Construction

Thailand

52.82 2.619

Wood, paper, paper products, printing and

publishing

Russian

Federation 51.83 2.328 Transport equipment

Viet Nam 51.35 3.239 Basic metals and fabricated metal products

Denmark 50.98 2.482 Food products and beverages

Japan 47.75 3.091 Transport equipment

China 46.06 3.543 Transport equipment

Australia 43.81 2.542 Transport equipment

Source: OECD-WTO Trade in Value-added (TiVA) Data Base, May 2013.

3.2. Trade in Value-Added and Singapore’s Exports

The composition of Singapore’s domestic exports of merchandise and services is

shown in Table 8. Exports of merchandise constitute about 60 percent of total exports

of goods and services. The major merchandise export items are mineral fuels and

lubricants, electronics and equipment, machine and equipment, and chemical products.

In terms of services, transportation services, business services and financial services

are the key sectors.

31

Table 8: Export of Merchandise and Services in 2009 and 2013

2009 2013 2009 2013

S$ m S$ m % %

Total Export (Merchandise and Services) 319,023 445,996 100.0 100.0

Domestic Exports – Merchandise 200,003 274,192 62.7 61.5

Food 3,138 4,948 1.0 1.1

Beverages & tobacco 403 579 0.1 0.1

Crude materials 1,115 1,798 0.3 0.4

Mineral fuels & lubricants 58,655 106,476 18.4 23.9

Animal & vegetable oils 246 228 0.1 0.1

Chemicals & chemical products 36,821 46,397 11.5 10.4

Manufactured goods 5,427 6,243 1.7 1.4

Electronics & equipment 51,404 48,872 16.1 11.0

Machine & equipment (non-electronics) 24,062 29,992 7.5 6.7

Miscellaneous manufactures 15,484 25,349 4.9 5.7

Miscellaneous 3,248 3,310 1.0 0.7

Services Exports 119,020 171,803 37.3 38.5

Transport 43,552 56,041 13.7 12.6

Travel 13,418 24,151 4.2 5.4

Telecommunication 3,804 6,117 1.2 1.4

Construction 1,545 2,198 0.5 0.5

Finance & insurance 19,447 27,683 6.1 6.2

Business services 25,916 40,520 8.1 9.1

Others 11,340 15,093 3.6 3.4

Source: International Enterprise Singapore and Department of Statistics.

The main export markets for Singapore are shown in Table 9. The ASEAN

countries absorb more than a quarter of Singapore’s domestic exports of merchandise.

Malaysia and Indonesia account for more than 70 percent of Singapore’s merchandise

exports to ASEAN. China is the second-largest export market, followed closely by the

EU-27. In the case of services export, ASEAN is an important market but has a smaller

share than that of the US or the EU-27. All other destinations in the world market take

up a larger share of services exports than that of merchandise exports.

32

Table 9: Major Export Markets for Singapore

Domestic Export of Goods Export of Services

2009 2013 2009 2013 2009 2013P 2009 2013

S$ m S$ m % % S$ m S$ m % %

Total

200,00

3

274,19

2

100.

0

100.

0

119,02

0

171,80

3

100.

0

100.

0

ASEAN 48,232 76,768 24.1 28.0 12,483 17,202 10.5 10.0

Indonesia 13,462 22,964 6.7 8.4 3,821 4,513 3.2 2.6

Malaysia 18,923 31,474 9.5 11.5 4,096 4,758 3.4 2.8

China 18,026 30,568 9.0 11.1 5,706 8,825 4.8 5.1

Hong Kong,

China 20,781 25,863 10.4 9.4 4,371 5,029 3.7 2.9

Chinese Taipei 6,997 11,222 3.5 4.1 2,054 2,182 1.7 1.3

Korea 6,882 8,785 3.4 3.2 2,303 2,673 1.9 1.6

Japan 9,677 10,614 4.8 3.9 5,629 8,495 4.7 4.9

US 15,755 17,330 7.9 6.3 13,628 20,353 11.5 11.8

EU-27 24,841 25,397 12.4 9.3 19,471 22,932 16.4 13.3

Others 48,811 67,645 24.4 24.7 53,375 84,114 44.8 49.0

Source: Yearbook of Statistics 2013 , Singapore Department of Statistics.

Figures 8A and 8B depict the gross exports of nine commodities10 in 2009 and

1995, respectively. The gross exports are decomposed into direct domestic value-

added, indirect domestic value-added and FVA. The reimported domestic value-added

is miniscule, ranging from 0.1 to 0.3 percent of gross exports, is omitted from the

charts.

We can discern from the charts, the share of FVA has perceptibly increased

between 1995 and 2009 for every commodity except chemical and non-metallic

mineral products. Generally, the increase is matched by a decrease in the share of

indirect domestic value-added. This is another indication of rising involvement in

outsourcing activities and increasing participation in GVCs and is corroborated by the

comparison of foreign value-added export ratios (FVAX) in Figure 9.

10 The nine export commodities constituted more than 97 percent of the gross exports in 2009.

33

Figure 8A: Composition of Gross Exports in 2009

Source: OECD WTO Trade in Value-Added (TIVA), May 2013.

Figure 8B: Composition of Gross Exports in 1995

Source: OECD WTO Trade in Value-Added (TIVA), May 2013.

The shares of FVA in gross exports (FVAX) for each of the commodities reported

in the TiVA database are shown in Figure 9 for 1995 and 2009. The commodities are

arranged in descending order according to the difference of the FVAX in the two years.

34

Figure 9: Foreign Value-Added Share in Gross Exports, 1995 vs. 2009

Source: OECD-WTO Trade in Value-added (TiVA) Data Base, May 2013.

Every commodity, except for chemicals and non-metallic mineral products, has a

larger FVA share in 2009 relative to that in 1995. The machinery and equipment sector

has the largest increase in the FVA ratio. The electrical and optical equipment sector,

which includes electronic peripheral and components, already had a high FVA share of

58 percent in 1995, has managed to increase its share to 61 percent in 2009.

Of interest is to determine those countries/regions that are contributing to FVA in

gross exports. The tables in the TiVA database enable that information to be extracted

and this is tabulated in Table 10. In 2009, half of the value-added embodied in the

35

aggregate exports is foreign. The EU-27 contribute 11.4 percent of the total VA, whilst

8.3 percent and 5 percent of total VA originate from the US and ASEAN region,

respectively.

Electronic products are included in the category of electrical and optical

equipment. The export of commodities from this category has the lowest share of

domestic value-added amongst all the categories listed in the table. Slightly more than

60 percent of the value-added originated from abroad. The EU-27, the US, and the NIEs

contribute between 10 to 13 percent each to the total VA embodied in gross exports of

this category.

As expected, exports from the services sector have higher domestic value-added

content than the non-services sectors. In particular, the financial services sector has the

highest domestic VA share of 73 percent and the bulk of its foreign VA originates from

the EU-27 region.

36

Table 10: Sources of Value-Added for Singapore Sectoral Gross Exports by Country/Region in 2009

Total Singapore ASEAN-S China NIEs Japan USA EU-27 Row

Sectoral Commodities

Total 212,449 106,401 10,687 6,324 7,991 8,246 18,243 24,242 30,315

Chemicals & non-metal mineral products 54,972 24,373 3,134 1,124 994 1,430 4,101 5,220 14,596

Electrical and optical equipment 44,867 17,392 3,969 2,733 4,390 2,129 4,701 5,710 3,843

Machinery & equipment 10,897 4,745 510 385 290 696 1,586 1,603 1,083

Transport equipment 7,152 3,976 220 157 149 239 1,314 635 462

Basic & fabricated metal product 3,890 1,913 345 143 119 249 203 321 598

Financial services 12,775 9,291 78 121 118 124 1,027 1,559 457

Business services 11,531 6,764 242 308 216 286 992 1,786 937

Transport & store, post & telecom 30,890 14,639 1,032 664 1,016 1,906 2,358 4,161 5,115

Wholesale & retail, hotel & restaurant 28,805 19,579 511 438 544 957 1,558 2,696 2,521

Others

OEC 6,670 3,730 648 251 155 231 402 551 702

Percentage Distribution

Total 100.0 50.1 5.0 3.0 3.8 3.9 8.6 11.4 14.3

Chemicals & non-metal mineral product 100.0 44.3 5.7 2.0 1.8 2.6 7.5 9.5 26.6

Electrical and optical equipment 100.0 38.8 8.8 6.1 9.8 4.7 10.5 12.7 8.6

Machinery & equipment 100.0 43.5 4.7 3.5 2.7 6.4 14.6 14.7 9.9

Transport equipment 100.0 55.6 3.1 2.2 2.1 3.3 18.4 8.9 6.5

Basic & fabricated metal product 100.0 49.2 8.9 3.7 3.1 6.4 5.2 8.2 15.4

Financial services 100.0 72.7 0.6 0.9 0.9 1.0 8.0 12.2 3.6

Business services 100.0 58.7 2.1 2.7 1.9 2.5 8.6 15.5 8.1

Transport & store, post & telecom 100.0 47.4 3.3 2.2 3.3 6.2 7.6 13.5 16.6

Wholesale & retail, hotel & restaurant 100.0 68.0 1.8 1.5 1.9 3.3 5.4 9.4 8.8

Others 100.0 55.9 9.7 3.8 2.3 3.5 6.0 8.3 10.5

Source: OECD-WTO Trade in Value-Added (TiVA) Database, May 2013.

37

3.3. Services Export and Service Value-Added in Exports

The share of services exports in total exports has risen steadily over the years to

reach 38.5 percent in 2013 (Table 8). Based on TiVA database information for

Singapore, the value-added contribution of services exports to the economy increased

considerably between 2000 and 2009, rising from 24 percent of GDP to 34 percent of

GDP.

According to the OECD research brief,11 accounting for the value-added by

services in the production of goods shows that the services sector contributes over 50

percent of total exports in the US, the UK, France, Germany and Italy and nearly one-

third in China, with a significant contribution (typically one third in 2009) across all

manufactured goods provided by both foreign and domestic service providers, with the

contribution rising between 5 and 10 percent in many countries since 1995.

In Table 11, the services content of Singapore’s gross exports and the sources of

services value-added are extracted from the information available in the TiVA

database.

Table 11: Services Value-Added Embodied in Gross Exports by Source

Country, as % of Gross Exports

2009 2005 2000 1995

Total 56.5 51.1 47.6 49.3

Singapore 30.0 25.7 24.9 30.2

ASEAN 1.3 1.1 1.6 2.0

China 1.0 0.6 0.4 0.6

NIEs 1.8 1.7 1.7 1.4

Japan 2.3 2.3 2.5 3.3

US 5.6 6.0 5.7 3.4

EU-27 8.9 9.2 6.9 6.1

Others 5.6 4.6 4.0 2.3

Source: OECD-WTO Trade in Value-Added (TiVA) Database, May 3013.

The services VA content of Singapore gross exports increased from 49 percent in

1995 to 57 percent in 2009. The bulk of the services VA originated from Singapore,

whilst the triad, namely, the EU-27, the US, and Japan, are the main contributors of

the foreign services VA content in Singapore’s gross exports.

11 OECD (2013), Measuring Trade in Value-Added.

38

Figure 10: Services VA Content of Export of Goods, 2009

Source: OECD-WTO Trade in Value-Added (TiVA) Database, May 3013.

The service VA content by sectors is shown in Figure 10. Amongst the exports of

goods, the average service VA content was 34 percent in 2009. In the electrical and

optical equipment sector, the services content of exports was over 35 percent. This

could possibly reflect the increase knowledge intensity (e.g., design, R&D, software)

of electrical and optical equipment.

The importance of services exports to Singapore’s economy is expected to

continue to increase, supported by three broad trends.12 First, the demarcation between

manufacturing and services is becoming more obscure. Increasing the services content

in commoditised manufacturing products has become a way to maintain product

differentiation and competitiveness. A well-known example is the Rolls Royce

company, famous for its aircraft engine manufacturing, which now earns more than 60

percent of its revenue by undertaking a wide spectrum of activities, including R&D,

12 Ministry of Trade and Industry, Singapore: Economic Survey of Singapore, 2nd Quarter 2014.

1519

811 13 10 8 7 10

22

12

19

1817

21

17 2029

18

19

0

5

10

15

20

25

30

35

40

45

Agr

i, F

ore

st &

Fis

hin

g

Foo

d, B

eve

rage

s &

To

bac

co

Text

iles,

Le

ath

er

& F

oo

twea

r

Wo

od

, Pap

er,

Pri

nt

&P

ub

lish

ing

Ch

em