sjms associates budget highlights 2012

TRANSCRIPT

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 1/42

BUDGET HIGHLIGHTS

2012 2

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 2/42

V I S I O N

To be the preferred Accountng and Business Advisory firm

M I S S I O N

Exceed client expectatons by providing solutons

through dedicated people

C O R E VA L U E S

Integrity

We have only one level of service – Excellence

The power of our people

Commitment to each other

Strength from cultural diversity

Carrying out what is promised at the right tme

Innovaton and upgrading of procedures

Keep up-to-date with modern developments

Contnually growing to provide a wide sphere of services

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 3/42

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 4/42

21st November 2011

Dear Client

B U D G E T P R O P O S A L S 2012

This booklet includes the salient features in the budget proposals for 2012, delivered by His Excellency the President

Mahinda Rajapakse in his capacity as Minister of Finance & Planning. This has been prepared as a general guide exclu-

sively for the informaton of our clients and staff . Contents included may be subject to alteraton during the passage of

the legislaton, through the Parliament.

Since the informaton provided are proposals, no final conclusion on any issues should be drawn without further con-

sideraton and consultaton. For additonal informaton or guidance on the issues dealt within the comments, the Tax &

Business Advisory Division of SJMS Associates, an Independent Correspondent Firm to Deloie Touche Tohmatsu will be

pleased to assist you.

This memorandum may be accessed on our website at www.sjmassociates.lk

Yours faithfully,

SJMS ASSOCIATES

Chartered Accountants

P. E. A. Jayewickreme, M. B. Ismail, Ms. A. M. J.. E. A. Jayewickreme M. B. Ismail Ms. A. M. J.P. E. A. Jayewickreme, M. B. Ismail, Ms. A. M. J.. E. A. Jayewickreme M. B. Ismail Ms. A. M. J. Patrick, T. Krishnakumar, Ms. S. L. Jayasuriya, Datrick T. Krishnakum ar Ms. S. L. Jayasuriya D.Patrick, T. Krishnakumar, Ms. S. L. Jayasuriya, D.atrick T. Krishnakum ar Ms. S. L. Jayasuriya D. S. W. Andradi,S. W. AndradiS. W. Andradi,S. W. Andradi

G. J. David, Ms. F. M. Marikkar, Ms. M. S. J. Henr. J. David Ms. F. M. Marikkar Ms. M. S. J. HenrG. J. David, Ms. F. M. Marikkar, Ms. M. S. J. Henr. J. David Ms. F. M. Marikkar Ms. M. S. J. Henry, Ms. A. U. M. Keppetipol Ms. A. U. M. Keppetipolay, Ms. A. U. M. Keppetipola Ms. A. U. M. Keppetipola

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 5/42

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 6/42

Budget

Highlights2012

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 7/42

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 8/42

Budget Highlights 2012

Contents

1. INCOME TAX 8- 12

2. ECONOMIC SERVICE CHARGES 12

3. NATIONS BUILDING TAX 13

4. VALUE ADDED TAX 14 - 16

5. MISCELLANEOUS 17 - 18

6. CUSTOMS DUTIES 19 - 28

7. OUR COMMENTS 29 - 30

Appendix

A – Summary of Corporate Tax Rates 31 - 33

B – Comparisons of Current Corporate Taxes,

Withholding Taxes, Indirect Taxes etc. 34

C – Comparison of eff ectve tax rates

for resident individual 35

D – Retring Benefits 35

7

Budget Highlights 2012

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 9/42

8

Budget Highlights 2012

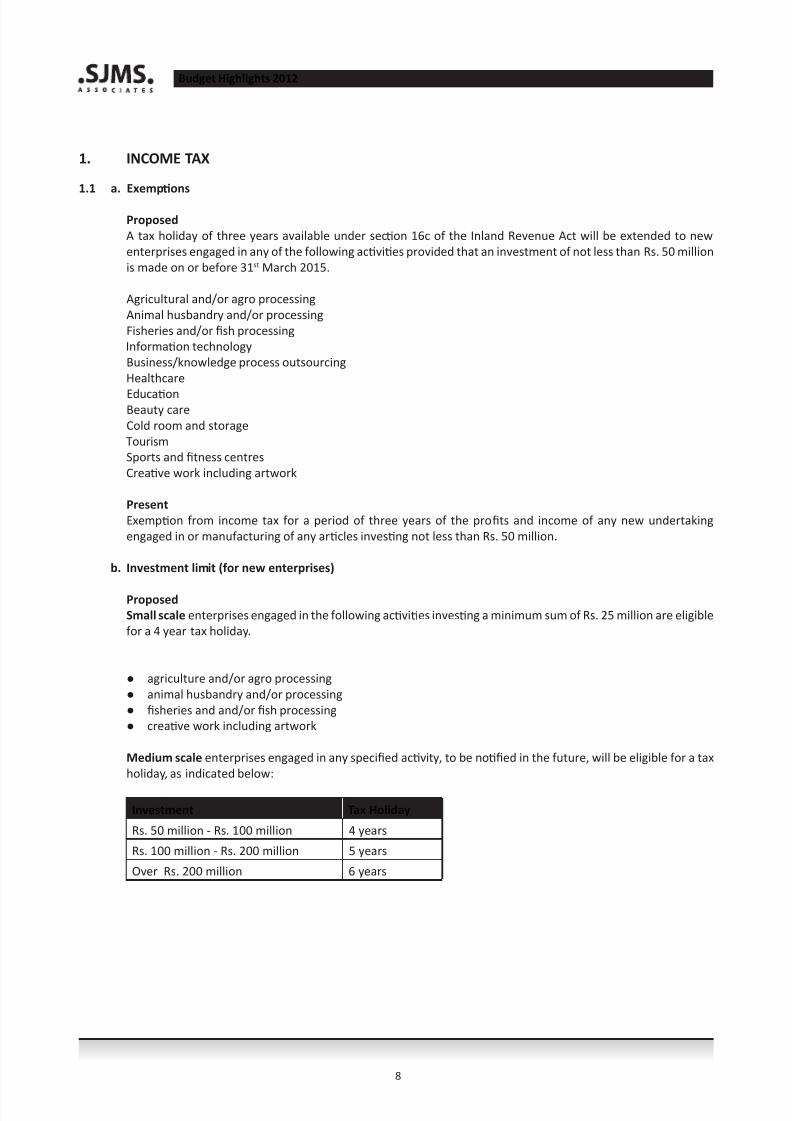

1. INCOME TAX

1.1 a. Exemptons

Proposed

A tax holiday of three years available under secton 16c of the Inland Revenue Act will be extended to new

enterprises engaged in any of the following actvites provided that an investment of not less than Rs. 50 million

is made on or before 31st March 2015.

Agricultural and/or agro processing

Animal husbandry and/or processing

Fisheries and/or fish processing

Informaton technology

Business/knowledge process outsourcing

Healthcare

Educaton Beauty care

Cold room and storage

Tourism

Sports and fitness centres

Creatve work including artwork

Present

Exempton from income tax for a period of three years of the profits and income of any new undertaking

engaged in or manufacturing of any artcles investng not less than Rs. 50 million.

b. Investment limit (for new enterprises)

Proposed

Small scale enterprises engaged in the following actvites investng a minimum sum of Rs. 25 million are eligible

for a 4 year tax holiday.

● agriculture and/or agro processing

● animal husbandry and/or processing

● fisheries and and/or fish processing

● creatve work including artwork

Medium scale enterprises engaged in any specified actvity, to be notfied in the future, will be eligible for a tax

holiday, as indicated below:

Investment Tax Holiday

Rs. 50 million - Rs. 100 million 4 years

Rs. 100 million - Rs. 200 million 5 years

Over Rs. 200 million 6 years

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 10/42

9

Budget Highlights 2012

Large scale enterprises engaged in specified actvites including any processing and solid waste management

will be eligible for tax holiday as follows.

Investment Tax Holiday

Rs.300 million - Rs. 500 million 6 years

Rs.500 million - Rs. 700 million 7 years

Rs.700 million - Rs. 1,000 million 8 years

Rs.1,000 million - Rs. 1,500 million 9 years

Rs.1,500 million - Rs. 2,500 million 10 years

Over Rs.2,500 million 12 years

Present

Certain industries were eligible for tax holiday not exceeding seven year with a minimum investment not

exceeding USD 3 Million.

c. Strategic Import Replacement enterprises

Proposed

The producton of the following items to replace imports by a new enterprise or by way of an expansion of an

existng enterprise with the corresponding investment will be eligible for a 5-year tax holiday followed by a

concessionary income tax rate.

Product Investment limit Concessionary Tax rate

Cement USD 50 million 12%

Steel USD 30 million 12%Pharmaceutcals USD 10 million 12%

Fabric USD 5 million 12%

Milk Powder USD 30 million 12%

A ruling mechanism will be introduced in advance, for investors eligible for tax exemptons, to ensure consistency

in the applicaton of respectve provisions of relevant tax laws.

Present

No exemptons for import replacement actvites.

d. Tax exemptons for Insttutons

Proposed

Profits and income (other than dividends and interest) of the following will be exempt from income tax:

The Insttute of Certfied Management Accountants of Sri Lanka;

The Child Protecton Authority.

Present

Presently, No such exemptons are available.

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 11/42

10

Budget Highlights 2012

e. Tax exemptons from specific sources

Proposed

● Royalty received from outside Sri Lanka will be exempt, if remied to Sri Lanka through a bank;

● Profits and income from the redempton of a unit of a Unit Trust or a Mutual Fund;

● Interest accruing to any person or partnership outside Sri Lanka on a loan granted to any person or

partnership in Sri Lanka;

● Profits and income from the administraton of any sports ground, stadium or sports complex;

● Profits and income of a trainer of any sport, being a non-citzen individual who is brought to Sri Lanka for

that purpose.

Present

Presently, No such exemptons are available.

1.2 CONCESSIONARY RATES

a. Development actvites carried out by specified bank branches

Proposed

The profits and income of a newly set up branch of a commercial bank dedicated to development banking will

be taxed at a lower rate of 24%.

Present

The current tax rate is 28%.

b. Research and development

Proposed The profits and income from the actvites carried out as research and development by a person other than a

company will be reduced to a maximum rate of 16%, and in the case of a company the rate will be reduced to

20%.

Present

There is no concessionary rate of tax for persons who carry out research and development actvites. The rates

applicable at present are as follows:

Company tax rate 28%.

Individuals - Progressive rate.

c. Value Added Tea

Proposed

A grower cum manufacturer or a manufacturer of tea, who establishes a joint venture with a tea exporter for

the purposes of exportng pure Sri Lankan tea (Ceylon Tea), in value added form, with a Sri Lankan brand name,

will be eligible to be taxed at the rate of 12% on the manufacturing income aributable to the quantum of tea

purchased for that purpose by the joint venture.

Present

There is no concessionary rate of tax for manufacture of value added tea. Present rate applicable to a company

is 28%.

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 12/42

11

Budget Highlights 2012

d. Handloom Industry

Proposed

The rate of tax applicable on the profits and income of a person or partnership from locally manufactured

handloom products will be reduced to 12% (maximum).

Present

Company tax rate 28%.

Individuals - Progressive rate.

e. Health Care Services

Proposed

The rate of tax applicable on the profits and income from the health care services will be reduced to a maximum

of 12%.

Present

Company tax rate 28%.

1.3 Ascertainment of Profits and income

The following expenses are allowed to be deducted under Secton 25:

a. Capital Allowance

Cost of any high tech plant, machinery or equipment.

b. Travelling Expenses

I. Expenses incurred by the employer in respect of vehicles used by the employee will be allowed irrespectve

of whether the benefi

t is taxable on such employee.

This change is applicable with eff ect from 01.04.2011.

II. Foreign travelling expenses of a company providing the following services, will be allowed in full if the

expenditure is related to such services:

- Design development

- Product development, or

- product innovaton

c. Maintenance and management expenses incurred by any person in respect of a sports ground, stadium or

sports complex will be allowed in full.

1.4 Deducton from total statutory income (Secton 32)

Pre-commencement expenses of SME

The pre-commencement expenses of SME, with the expected turnover not exceeding Rs. 500 Million incurred

in the immediately year prior to the year in which commercial operatons commenced, will be allowed to be

deducted from its total statutory income of the year of commercial operaton.

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 13/42

12

Budget Highlights 2012

1.5 Qualifying payments (Secton 34)

Expansion of existng enterprises

Investment by an enterprise in its own business (expansion) of not less than Rs. 50 million made prior to 31st

March 2015 will be treated as a qualifying payment deductble from assessable income subject to a maximum

of 25% of the investment for each year of assessment falling within a period of 4 years commencing from the

year of investment.

Expenditure incurred under any community development project carried out in most diffi cult villages as

identfied and gazzeted by the Commissioner General.

Maximum deductble - Individual Rs. 1 Million

- Company Rs. 10 Million

1.6 Audit Certficate

Presently, all quoted public companies are required to submit audit certficates, while other companies have to

submit only if the turnover exceeds Rs. 250 Million or if the net profit exceeds Rs. 100 Million.

According to the proposal, the requirement of furnishing the audit certficate is extended to all companies

within the group, irrespectve of the turnover or profit.

1.7 Definiton of Dividends

“Scrip dividends” have also been included under the interpretaton of the word “dividend”.

2. Economic Service Charge (ESC)

2.1 Exemptons

Proposed

The turnover of following businesses are exempt from ESC :

● any business of which the profits are subject to Income Tax except those incurring losses

● sale of locally manufactured clay roof tles and poery products by the manufacturer

Present

Presently there are no such concessions.

2.2 Threshold

Proposed

The present threshold of Rs 25 Million per quarter has been increased to Rs 50 Million per quarter.

Present

The threshold is Rs 25 Million per quarter.

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 14/42

13

Budget Highlights 2012

3. NATION BUILDING TAX (NBT)

3.1 Exemptons

Proposed

Exemptons have been proposed for the following 4 categories:

● The following artcles have been included under excepted artcles.

Artcle Tax Holiday

Importaton of air craf or ships 8802.118802.3089.0289.07

8802.128802.4089.0589.08

8802.2089.0189.06

Importaton of artficial limbs, crutches, wheel

chairs, hearing aids, accessories for such aids,white canes for the blind, Braille typewriters andparts ,Braille writng papers and boards

87.13

8473.10.10

90.21

8469.00.10

6602.00.10

Importaton of tmber logs 44.03

Importaton of yarn except sewing thread andvegetable fibre based yarn

50.0150.0150.0651.0451.0852.0353.0254.0255.0155.0655.11

50.0250.0251.0151.0551.0952.0553.0354.0355.0255.0756.04

50.0350.0351.0251.0651.1052.0653.0654.0455.0355.0956.05

50.0450.0451.0351.0752.0153.0153.0754.0655.0455.1056.06

Importaton of fabric 5007.1051.1252.1053.1055.1358.0158.0960.03

5007.2051.1352.1154.0755.1458.0258.1160.04

5007.9052.0852.1254.0855.1558.0460.0160.05

51.1152.0953.0955.1255.1658.0660.0260.06

● Wholesale or retail sale of ○

Printed books ( with eff

ect from 1

st

July 2011) ○ Goods to exporters

○ Fresh milk, green leaf, cinnamon, rubber (latex, crepe or sheet rubber) by collectors

○ Petrol, diesel or kerosene in a filling staton

● Sale of locally manufactured clay roof tles and poery products by the manufacturer

● Sale of paintngs by the creator of such paintngs

Present

The above categories are liable.

3.2 Definiton of exporter broadened

The definiton of exporter for the purpose of the NBT Act will be adjusted to also cover a manufacturer of goodswho exports produce through a Trading House established for purpose of export. (eff ectve from 2009)

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 15/42

14

Budget Highlights 2012

4. VALUE ADDED TAX (VAT)

4.1 Exemptons

(a) Import

Item HS codes

Speakers & amplifiers, digital stereo processors & accessories, cinema

media players and digital readers for the improvement of film theatres

with digital technology (the present exempton applicable to the import

of equipment for the cinema industry will be extended by additon of

the above items)

8518.29

8519.81

8518.40

8519.89

Pharmaceutcal machinery and spare parts by manufacturer of

pharmaceutcals (w.e.f. June 1, 2011)

8479.89.90

8413.81

8424.20

8481.80

Machinery for the manufacture of bio mass briquees and pallets bythe manufacturer of such products (w.e.f. June 1, 2011)

8479.30

Green houses , poly tunnels and materials for the constructon of green

houses and poly tunnels by the growers

(b) Supply of:

(i) Locally manufactured goods :

● Hydropower machinery and equipment

● Products using locally procured raw materials for the required specificaton of the tourist hotels and airlines

which promote local value added products

● Canned fish ● Turbines

● Specified products to identfied State Insttuton replacing imports

● Poery product by the manufacturer

(ii) ● Research and development services

● Services by the Department of Commerce

● Paintngs by the creator of such paintng

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 16/42

15

Budget Highlights 2012

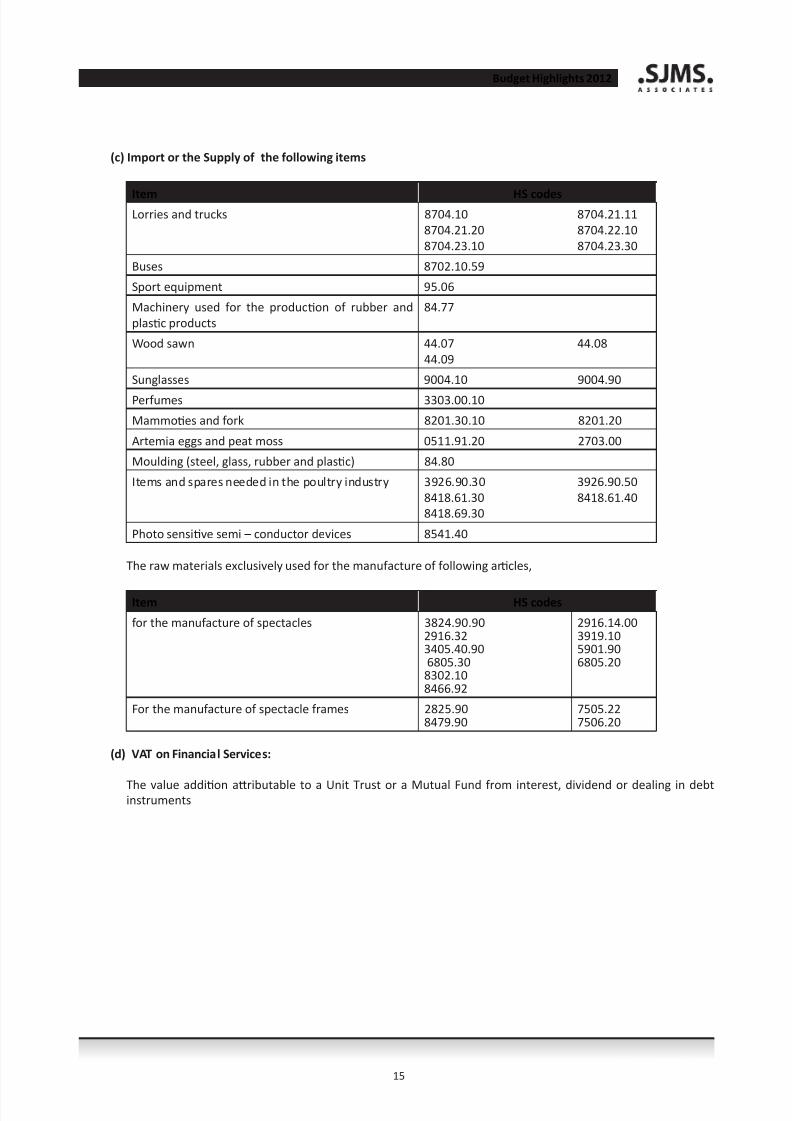

(c) Import or the Supply of the following items

Item HS codesLorries and trucks 8704.10

8704.21.20

8704.23.10

8704.21.11

8704.22.10

8704.23.30

Buses 8702.10.59

Sport equipment 95.06

Machinery used for the producton of rubber and

plastc products

84.77

Wood sawn 44.07

44.09

44.08

Sunglasses 9004.10 9004.90

Perfumes 3303.00.10

Mammotes and fork 8201.30.10 8201.20

Artemia eggs and peat moss 0511.91.20 2703.00

Moulding (steel, glass, rubber and plastc) 84.80

Items and spares needed in the poultry industry 3926.90.30

8418.61.30

8418.69.30

3926.90.50

8418.61.40

Photo sensitve semi – conductor devices 8541.40

The raw materials exclusively used for the manufacture of following artcles,

Item HS codes

for the manufacture of spectacles 3824.90.902916.323405.40.906805.308302.108466.92

2916.14.003919.105901.906805.20

For the manufacture of spectacle frames 2825.908479.90

7505.227506.20

(d) VAT on Financial Services:

The value additon aributable to a Unit Trust or a Mutual Fund from interest, dividend or dealing in debtinstruments

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 17/42

16

Budget Highlights 2012

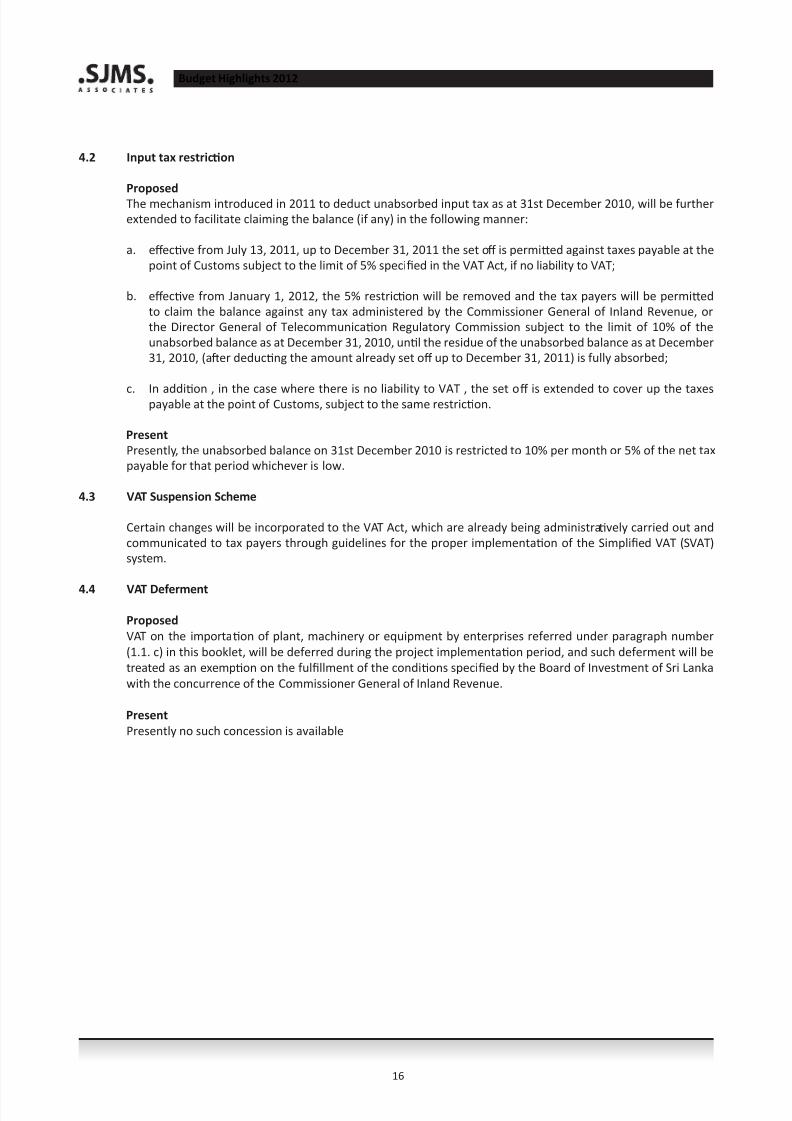

4.2 Input tax restricton

Proposed

The mechanism introduced in 2011 to deduct unabsorbed input tax as at 31st December 2010, will be further

extended to facilitate claiming the balance (if any) in the following manner:

a. eff ectve from July 13, 2011, up to December 31, 2011 the set off is permied against taxes payable at the

point of Customs subject to the limit of 5% specified in the VAT Act, if no liability to VAT;

b. eff ectve from January 1, 2012, the 5% restricton will be removed and the tax payers will be permied

to claim the balance against any tax administered by the Commissioner General of Inland Revenue, or

the Director General of Telecommunicaton Regulatory Commission subject to the limit of 10% of the

unabsorbed balance as at December 31, 2010, untl the residue of the unabsorbed balance as at December

31, 2010, (afer deductng the amount already set off up to December 31, 2011) is fully absorbed;

c. In additon , in the case where there is no liability to VAT , the set off is extended to cover up the taxespayable at the point of Customs, subject to the same restricton.

Present

Presently, the unabsorbed balance on 31st December 2010 is restricted to 10% per month or 5% of the net tax

payable for that period whichever is low.

4.3 VAT Suspension Scheme

Certain changes will be incorporated to the VAT Act, which are already being administratvely carried out and

communicated to tax payers through guidelines for the proper implementaton of the Simplified VAT (SVAT)

system.

4.4 VAT Deferment

Proposed

VAT on the importaton of plant, machinery or equipment by enterprises referred under paragraph number

(1.1. c) in this booklet, will be deferred during the project implementaton period, and such deferment will be

treated as an exempton on the fulfillment of the conditons specified by the Board of Investment of Sri Lanka

with the concurrence of the Commissioner General of Inland Revenue.

Present

Presently no such concession is available

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 18/42

17

Budget Highlights 2012

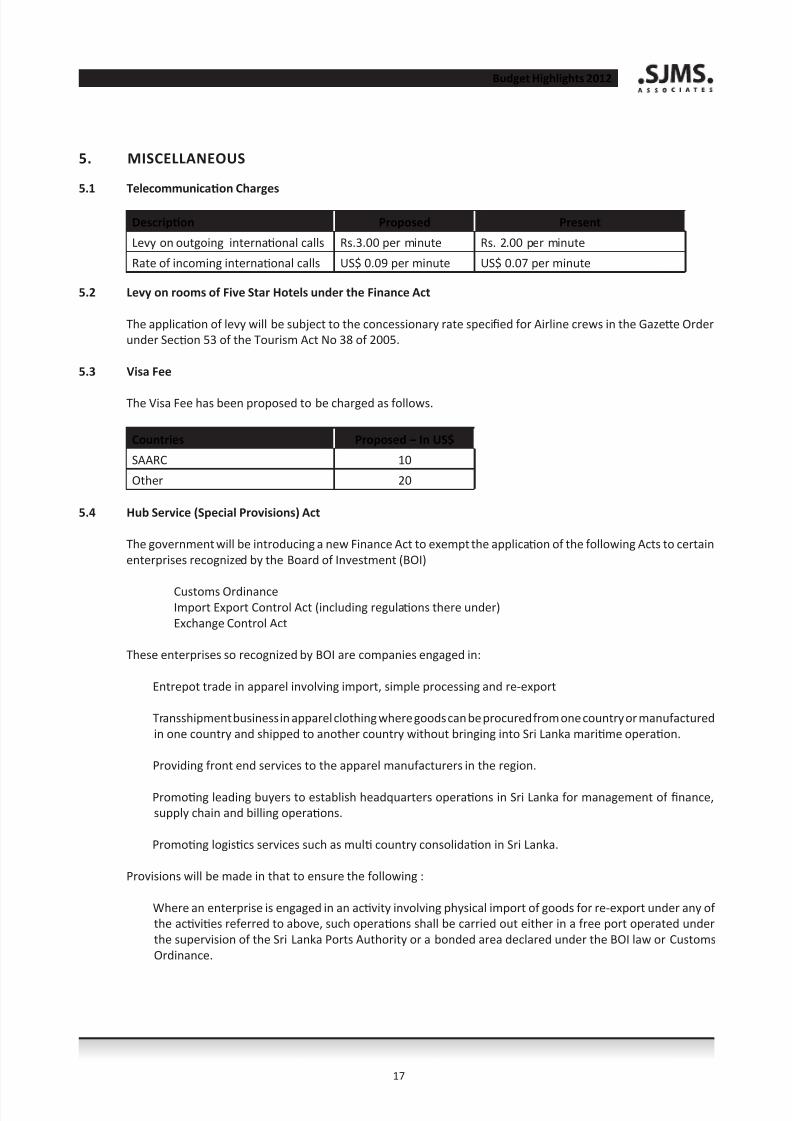

5. MISCELLANEOUS

5.1 Telecommunicaton Charges

Descripton Proposed Present

Levy on outgoing internatonal calls Rs.3.00 per minute Rs. 2.00 per minute

Rate of incoming internatonal calls US$ 0.09 per minute US$ 0.07 per minute

5.2 Levy on rooms of Five Star Hotels under the Finance Act

The applicaton of levy will be subject to the concessionary rate specified for Airline crews in the Gazee Order

under Secton 53 of the Tourism Act No 38 of 2005.

5.3 Visa Fee

The Visa Fee has been proposed to be charged as follows.

Countries Proposed – In US$

SAARC 10

Other 20

5.4 Hub Service (Special Provisions) Act

The government will be introducing a new Finance Act to exempt the applicaton of the following Acts to certain

enterprises recognized by the Board of Investment (BOI)

Customs Ordinance Import Export Control Act (including regulatons there under)

Exchange Control Act

These enterprises so recognized by BOI are companies engaged in:

Entrepot trade in apparel involving import, simple processing and re-export

Transshipment business in apparel clothing where goods can be procured from one country or manufactured

in one country and shipped to another country without bringing into Sri Lanka maritme operaton.

Providing front end services to the apparel manufacturers in the region.

Promotng leading buyers to establish headquarters operatons in Sri Lanka for management of finance,

supply chain and billing operatons.

Promotng logistcs services such as mult country consolidaton in Sri Lanka.

Provisions will be made in that to ensure the following :

Where an enterprise is engaged in an actvity involving physical import of goods for re-export under any of

the actvites referred to above, such operatons shall be carried out either in a free port operated under

the supervision of the Sri Lanka Ports Authority or a bonded area declared under the BOI law or Customs

Ordinance.

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 19/42

18

Budget Highlights 2012

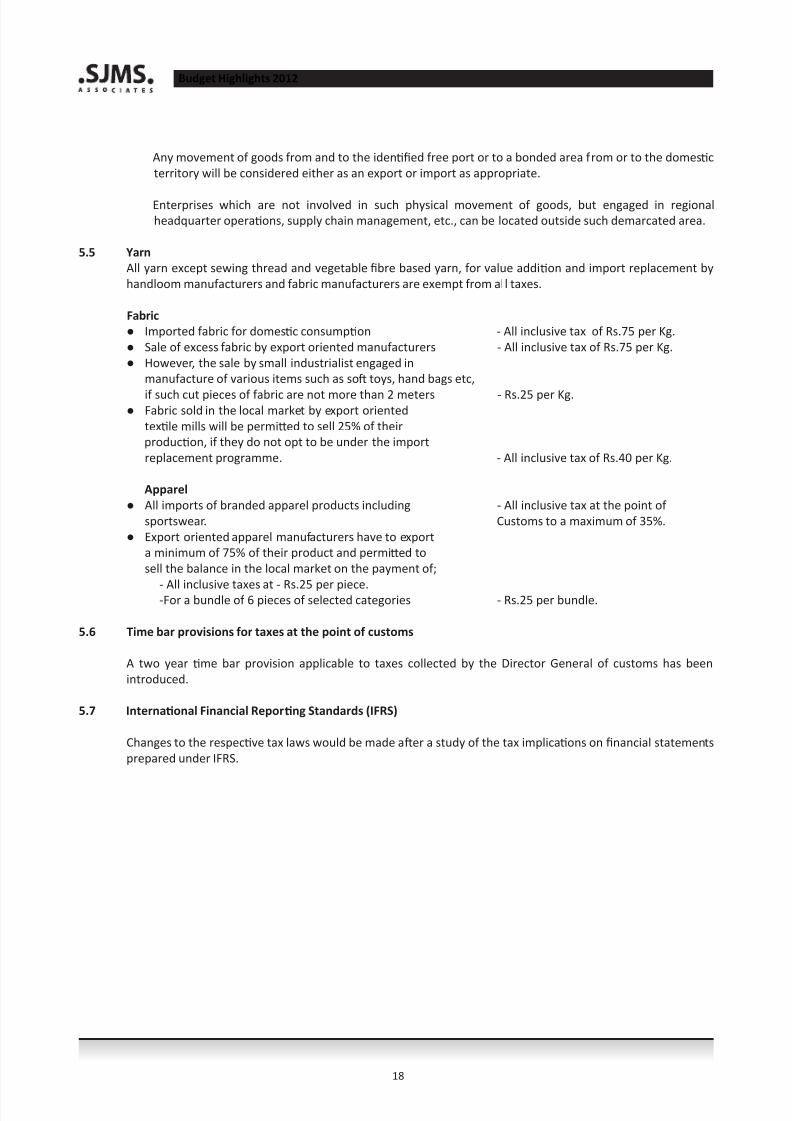

Any movement of goods from and to the identfied free port or to a bonded area from or to the domestc

territory will be considered either as an export or import as appropriate.

Enterprises which are not involved in such physical movement of goods, but engaged in regional

headquarter operatons, supply chain management, etc., can be located outside such demarcated area.

5.5 Yarn

All yarn except sewing thread and vegetable fibre based yarn, for value additon and import replacement by

handloom manufacturers and fabric manufacturers are exempt from all taxes.

Fabric

● Imported fabric for domestc consumpton - All inclusive tax of Rs.75 per Kg.

● Sale of excess fabric by export oriented manufacturers - All inclusive tax of Rs.75 per Kg.

● However, the sale by small industrialist engaged in

manufacture of various items such as sof toys, hand bags etc,

if such cut pieces of fabric are not more than 2 meters - Rs.25 per Kg.● Fabric sold in the local market by export oriented

textle mills will be permied to sell 25% of their

producton, if they do not opt to be under the import

replacement programme. - All inclusive tax of Rs.40 per Kg.

Apparel

● All imports of branded apparel products including - All inclusive tax at the point of

sportswear. Customs to a maximum of 35%.

● Export oriented apparel manufacturers have to export

a minimum of 75% of their product and permied to

sell the balance in the local market on the payment of;

- All inclusive taxes at - Rs.25 per piece. -For a bundle of 6 pieces of selected categories - Rs.25 per bundle.

5.6 Time bar provisions for taxes at the point of customs

A two year tme bar provision applicable to taxes collected by the Director General of customs has been

introduced.

5.7 Internatonal Financial Reportng Standards (IFRS)

Changes to the respectve tax laws would be made afer a study of the tax implicatons on financial statements

prepared under IFRS.

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 20/42

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 21/42

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 22/42

21

Budget Highlights 2012

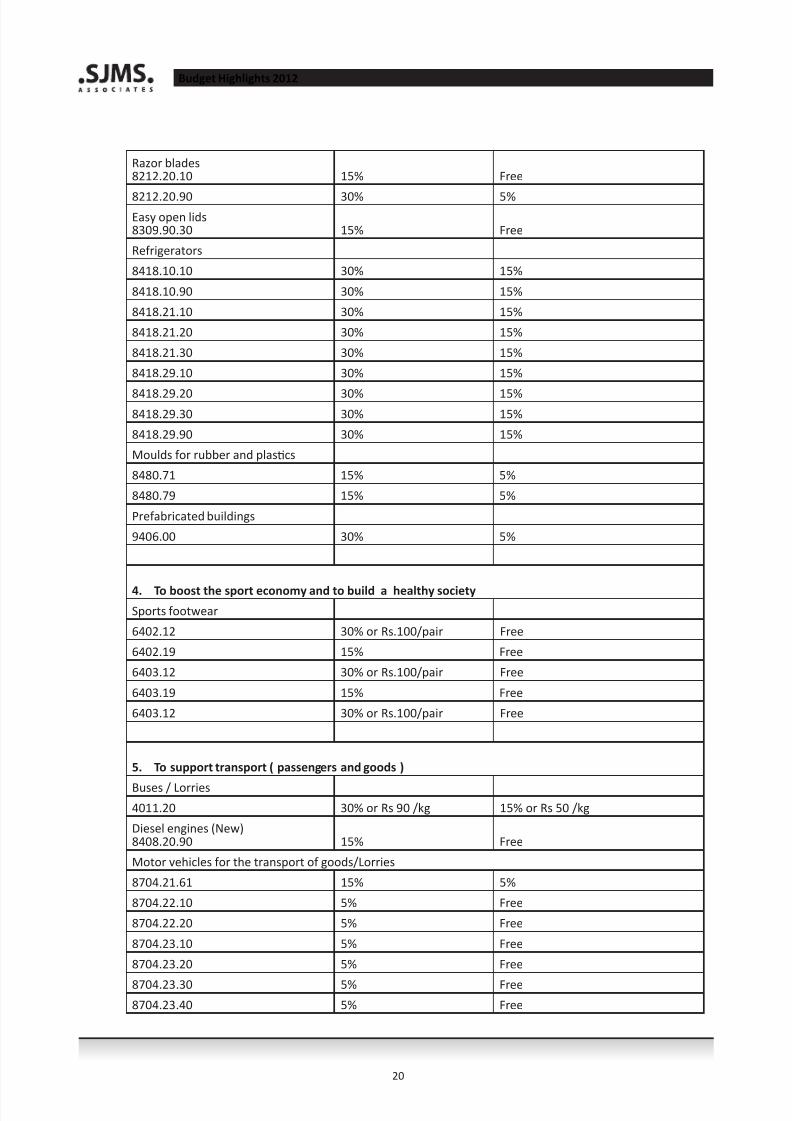

6. To promote the use of energy saving lamps

Lamps/LED mounted in one housing & solar lanterns & sets for decoratve lightning

9405.10.10 15% Free

9405.20.10 15% Free

9405.10.20 15% Free

9405.20.20 15% Free

9405.30 30% Free

9405.40.30 15% Free

9405.40.40 15% Free

7. To promote ICT and BPO Sector

Automated data processing machines/ computers

8471.30.10 5% Free

8471.30.90 5% Free

8471.41.10 5% Free

8471.41.90 5% Free

8471.49.10 5% Free

8471.49.90 5% Free

8471.50.10 5% Free

8471.50.90 5% Free8471.90 5% Free

8. Branded and other goods of interest to tourists

Footwear

6401.10 30% or Rs. 100/pair Rs. 100/pair

6401.92 30% or Rs. 100/pair Rs. 100/pair

6401.99 30% or Rs. 100/pair Rs. 100/pair

6402.20 30% or Rs. 100/pair Rs. 100/pair

6402.91 30% or Rs. 100/pair Rs. 100/pair6402.99 30% or Rs. 100/pair Rs. 100/pair

6403.20 30% or Rs. 100/pair Rs. 100/pair

6403.40 30% or Rs. 100/pair Rs. 100/pair

6403.51 30% or Rs. 100/pair Rs. 100/pair

6403.59 30% or Rs. 100/pair Rs. 100/pair

6403.91 30% or Rs. 100/pair Rs. 100/pair

6403.99 30% or Rs. 100/pair Rs. 100/pair

6404.19 30% Rs. 100/pair

6404.20 30% Rs. 100/pair

6405.10 30% or Rs. 100/pair Rs. 100/pair

6405.20 30% or Rs. 100/pair Rs. 100/pair

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 23/42

22

Budget Highlights 2012

6405.90 30% or Rs. 100/pair Rs. 100/pair

Ornamental porcelain & ceramic products

6913.10 30% or Rs 25/kg Free

6913.90.10 30% or Rs 20/kg Free

6913.90.90 30% or Rs 20/kg Free

Glassware

7013.10 30% 5%

7013.22 30% 5%

7013.33 30% 5%

7013.41 30% 5%

7013.91 30% 5%

Cutleries8211.10 15% Free

8215.10 30% Free

8215.20 30% Free

8215.91 30% Free

8215.99 30% Free

Sunglasses

9004.10 30% Free

9004.90 15% Free

Hair accessories

9615.11 30% Free

9615.19 30% Free

9615.90 30% Free

- Importaton of goods by the following insttutons will be exempt from Customs Duty.

Sri Lankan Air Lines Limited,

Air Lanka Catering Services Ltd.,

Mihin Lanka (Pvt) Ltd.,

- The import of plant and machinery or equipment by an enterprise with an investment not exceeding the

following amounts will be exempt from Customs Duty on the fulfilment of the conditons specified by the

B.O.I. in concurrence with the C.G.I.R.

Product Investment Limit

Cement US$ 50 Mn

Steel US$ 30 Mn.

Pharmaceutcals US$ 10 Mn.

Fabric US$ 5 Mn

Milk Powder US$ 30 Mn

- Changes to Customs Duty will be implemented with immediate eff ect.

Ports and Airports Development Levy ( PAL) (Amendments to PAL Act No. 18 of 2011 )

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 24/42

23

Budget Highlights 2012

The importaton of following goods will be exempt from PAL.:

Item H S Heading / CodeArtficial limbs, crutches, wheel chairs, hearing aids,

accessories for such aids, white canes for the blind,

Braille typewriters and parts, Braille writng papers

and boards

87.13, 90.21, 6602.00.10, 8473.10.10

and 8469.00.10

Timber logs 44.03

Yarn except sewing thread and vegetable fibre based

yarn

50.01, 50.02, 50.03, 50.04, 50.06, 51.01,

51.02, 51.03, 51.04, 51.05, 51.06, 51.07,

51.08, 51.09, 51.10, 52.01, 52.03, 52.05

52.06, 53.01, 53.02, 53.03, 53.06, 53.07,

54.02, 54.03, 54.04, 54.06, 55.01, 55.02,

55.03, 55.04, 55.06, 55.07, 55.09, 55.10,

55.11, 56.04, 56.05 and 56.06

Fabric 5007.10, 5007.20, 5007.90, 51,11, 51.12

51.13, 52.08, 52.09, 52.10, 52.11, 52.12

53.09, 53.10, 54.07, 54.08, 55.12, 55.13

55.14, 55.15, 55.16, 58.01, 58.02, 58.04

58.06, 58.09, 58.11, 60.01, 60.02, 60.03,

60.04, 60.05 and 60.06

- Importaton of goods by the following insttutons will be exempted from Ports and Airport

Development Levy

Sri Lankan Air Lines Limited,

Air Lanka Catering Services Ltd.,

Mihin Lanka (Pvt) Ltd.,

- The import of plant and machinery or equipment by an enterprise with an investment not exceeding

the following amounts will be exempt from Ports and Airport Development Levy on the fulfilment of the

conditons specified by the B.O.I. in concurrence with the C.G.I.R.

Product Investment Limit

Cement US$ 50 Mn Steel US$ 30 Mn.

Pharmaceutcals US$ 10 Mn.

Fabric US$ 5 Mn

Milk Powder US$ 30 Mn

- Changes to Ports and Airport Development Levy will be implemented with immediate eff ect.

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 25/42

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 26/42

25

Budget Highlights 2012

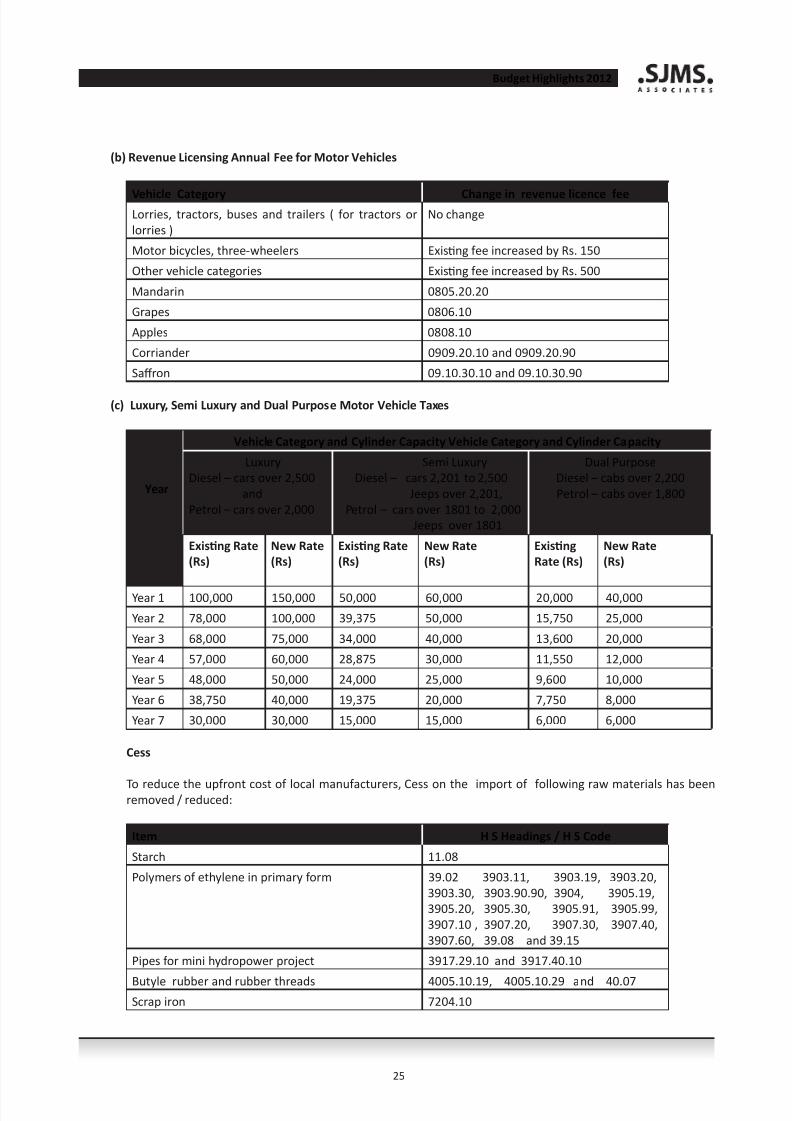

(b) Revenue Licensing Annual Fee for Motor Vehicles

Vehicle Category Change in revenue licence feeLorries, tractors, buses and trailers ( for tractors or

lorries )

No change

Motor bicycles, three-wheelers Existng fee increased by Rs. 150

Other vehicle categories Existng fee increased by Rs. 500

Mandarin 0805.20.20

Grapes 0806.10

Apples 0808.10

Corriander 0909.20.10 and 0909.20.90

Saff ron 09.10.30.10 and 09.10.30.90

(c) Luxury, Semi Luxury and Dual Purpose Motor Vehicle Taxes

Year

Vehicle Category and Cylinder Capacity Vehicle Category and Cylinder Capacity

Luxury

Diesel – cars over 2,500

and

Petrol – cars over 2,000

Semi Luxury

Diesel – cars 2,201 to 2,500

Jeeps over 2,201,

Petrol – cars over 1801 to 2,000

Jeeps over 1801

Dual Purpose

Diesel – cabs over 2,200

Petrol – cabs over 1,800

Existng Rate

(Rs)

New Rate

(Rs)

Existng Rate

(Rs)

New Rate

(Rs)

Existng

Rate (Rs)

New Rate

(Rs)

Year 1 100,000 150,000 50,000 60,000 20,000 40,000

Year 2 78,000 100,000 39,375 50,000 15,750 25,000

Year 3 68,000 75,000 34,000 40,000 13,600 20,000

Year 4 57,000 60,000 28,875 30,000 11,550 12,000

Year 5 48,000 50,000 24,000 25,000 9,600 10,000

Year 6 38,750 40,000 19,375 20,000 7,750 8,000

Year 7 30,000 30,000 15,000 15,000 6,000 6,000

Cess

To reduce the upfront cost of local manufacturers, Cess on the import of following raw materials has beenremoved / reduced:

Item H S Headings / H S Code

Starch 11.08

Polymers of ethylene in primary form 39.02 3903.11, 3903.19, 3903.20,

3903.30, 3903.90.90, 3904, 3905.19,

3905.20, 3905.30, 3905.91, 3905.99,

3907.10 , 3907.20, 3907.30, 3907.40,

3907.60, 39.08 and 39.15

Pipes for mini hydropower project 3917.29.10 and 3917.40.10

Butyle rubber and rubber threads 4005.10.19, 4005.10.29 and 40.07Scrap iron 7204.10

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 27/42

26

Budget Highlights 2012

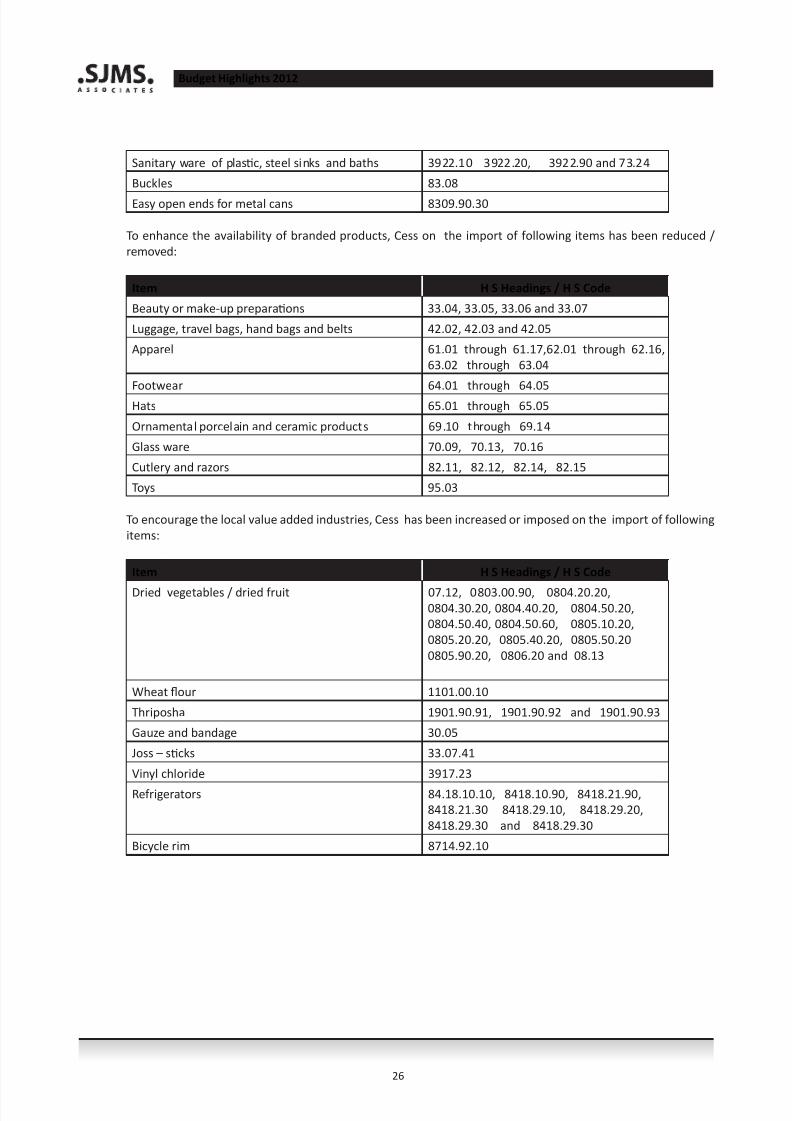

Sanitary ware of plastc, steel sinks and baths 3922.10 3922.20, 3922.90 and 73.24

Buckles 83.08

Easy open ends for metal cans 8309.90.30

To enhance the availability of branded products, Cess on the import of following items has been reduced /

removed:

Item H S Headings / H S Code

Beauty or make-up preparatons 33.04, 33.05, 33.06 and 33.07

Luggage, travel bags, hand bags and belts 42.02, 42.03 and 42.05

Apparel 61.01 through 61.17,62.01 through 62.16,

63.02 through 63.04

Footwear 64.01 through 64.05

Hats 65.01 through 65.05

Ornamental porcelain and ceramic products 69.10 through 69.14

Glass ware 70.09, 70.13, 70.16

Cutlery and razors 82.11, 82.12, 82.14, 82.15

Toys 95.03

To encourage the local value added industries, Cess has been increased or imposed on the import of following

items:

Item H S Headings / H S Code

Dried vegetables / dried fruit 07.12, 0803.00.90, 0804.20.20,0804.30.20, 0804.40.20, 0804.50.20,

0804.50.40, 0804.50.60, 0805.10.20,

0805.20.20, 0805.40.20, 0805.50.20

0805.90.20, 0806.20 and 08.13

Wheat flour 1101.00.10

Thriposha 1901.90.91, 1901.90.92 and 1901.90.93

Gauze and bandage 30.05

Joss – stcks 33.07.41

Vinyl chloride 3917.23

Refrigerators 84.18.10.10, 8418.10.90, 8418.21.90,

8418.21.30 8418.29.10, 8418.29.20,

8418.29.30 and 8418.29.30

Bicycle rim 8714.92.10

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 28/42

27

Budget Highlights 2012

To boost the sport economy and to build a healthy naton, Cess on the import of following items has been

reduced / removed:

Item H S Headings / H S Code

T – shirts and shorts 61.09, 6103.42 and 6104.62

Track –suits and swim wear 61.12 and 62.11

Shoes 64.01 through 64.05

To encourage local value additon, Cess has been increased / imposed on the export of following items:

Item H S Headings / H S Code

Raw rubber 4001.10 and 4001.21

Natural graphite 2504.90.90

Clay 25.07

Sand 2505.90

Phosphate 2510.10

Stones 2513.20

Granite, sand stones 2516.20, 2516.90

Mica 2525.10

Ilmanite 2614.00.10

Rutle 2614.00.20

Titanium 2614.00.90

Zirconium 2615.10Timber logs 4403.99, 44.07, 44.08 and 44.09

- Importaton of goods by the following insttutons will be exempted from Cess.

Sri Lankan Air Lines Limited

Air Lanka Catering Services Ltd

Mihin Lanka (Pvt) Ltd.

- The import of plant and machinery or equipment by an enterprise with an investment not exceeding

the following amounts will be exempt from Cess on the fulfilment of the conditons specified by the B.O.I.

in concurrence with the C.G.I.R.

Product Investment Limit

Cement US$ 50 Mn

Steel US$ 30 Mn.

Pharmaceutcals US$ 10 Mn.

Fabric US$ 5 Mn

Milk Powder US$ 30 Mn

- Changes to Cess will be implemented with immediate eff ect.

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 29/42

28

Budget Highlights 2012

Excise Duty

- Liquor produced from local plant material or plant product will be subject to a lower excise duty of Rs.

100/- per proof litre.

- Importaton of goods by the following insttutons will be exempted from Excise Duty and Excise

( Special Provisions ) Duty:

Sri Lankan Air Lines Limited,

Air Lanka Catering Services Ltd

Mihin Lanka (Pvt) Ltd.

- The following artcles are exempted from Excise (Special Provisions ) Duty;

Electric motor bicycles ( H S Code 8711.90.10 )

Polymers of ethylene in primary forms ( H S Heading 39.01 )

- Changes to Excise Duty and Excise ( Special Provisions ) Duty will be implemented with immediate eff ect.

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 30/42

29

Budget Highlights 2012

Our Comments

Economic growth

The 2012 budget focused on maintaining economic growth at 8 percent, improving domestc productvity to reduce the

cost of living and creatng employment to drive consumer demand.

To improve the compettveness of the export industry, the rupee will be devalued by 3 percent with immediate eff ect.

Creatng a self suffi cient economy was resonant, and to this eff ect the budget proposed to maintain the high Cess to

discourage imports of consumer produce that can be locally cultvated.

To shif Sri Lanka’s status as a net importer, a 5 year tax holiday period and a concessionary income tax rate of 12 percent

are off ered to cement, steel, milk powder and pharmaceutcal replacement industries.

Increased investment impetus

To increase employment opportunites by encouraging new investment by local and foreign investors, a 3 year tax holiday

for investments of more than Rs 50 million given to the manufacturing industry is expanded to include informaton

technology, beauty care, fisheries, agriculture and tourism related industry.

Further it proposes investment limits for new enterprises as small, medium and large. Small scale enterprises have a

minimum investment of Rs 25 million proving a maximum 4 years tax holiday. A medium and large scale enterprise

requires a minimum investment of Rs 50 million and Rs 300 million respectvely. Medium scale companies investng

more than Rs 200 million and large scale companies investng more than Rs 2,500 million will enjoy a maximum of a 6

year and 12 year tax holiday respectvely. The actvites qualifying for the medium and large scale enterprises are yet to

be specified.

The budget takes further strides to build investor confidence by providing existng companies the opportunity to expand

its operatons. It is proposed to allow this as a qualifying payment deductable for income tax at 25% per year over a 4

year period.

Infrastructure investment

Identfying that expansive infrastructure is vital to drive and maintain economic growth, Rs 30 billion is proposed to

improve the rural and agricultural road network as well as the provincial and inter-district road network.

The budget also proposed Rs. 750 million to be allocated in the next year to commence the constructon of airports in

Iranamadu, Nuwara Eliya and Kandy to further integrate the country.

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 31/42

30

Budget Highlights 2012

Concessionary tax rates

The budget identfi

ed specifi

c industries integral to development and requires support to prosper. Therefore the tax rateapplicable to locally manufactured handloom products, health care services and value added tea exportng will enjoy a

12 percent income tax rate.

Research and development actvites carried out by a person will be taxed at a maximum rate of 16%, and 20% for a

company.

Social welfare

Recognizing the invaluable contributon of the armed forces during the ethnic conflict, the budget proposed to contnue

the grant of Rs. 100,000 at the birth of the third child of any member of the security forces extending to those serving

in the Police force.

A sum of Rs 3,000 million will be allocated to support the low income families and improve the welfare of women and

children, expanding these services to the north and the east regions.

Economic Service Charge

Any persons whose profits are subject to income tax will be exempted from the Economic Service Charge.

Also, the Economic Service Charge threshold will be expanded from Rs 25 million to Rs 50 million per quarter.

The changes proposed above will generate free cash flow for investment by the private sector which is essental for

economic growth.

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 32/42

31

Budget Highlights 2012

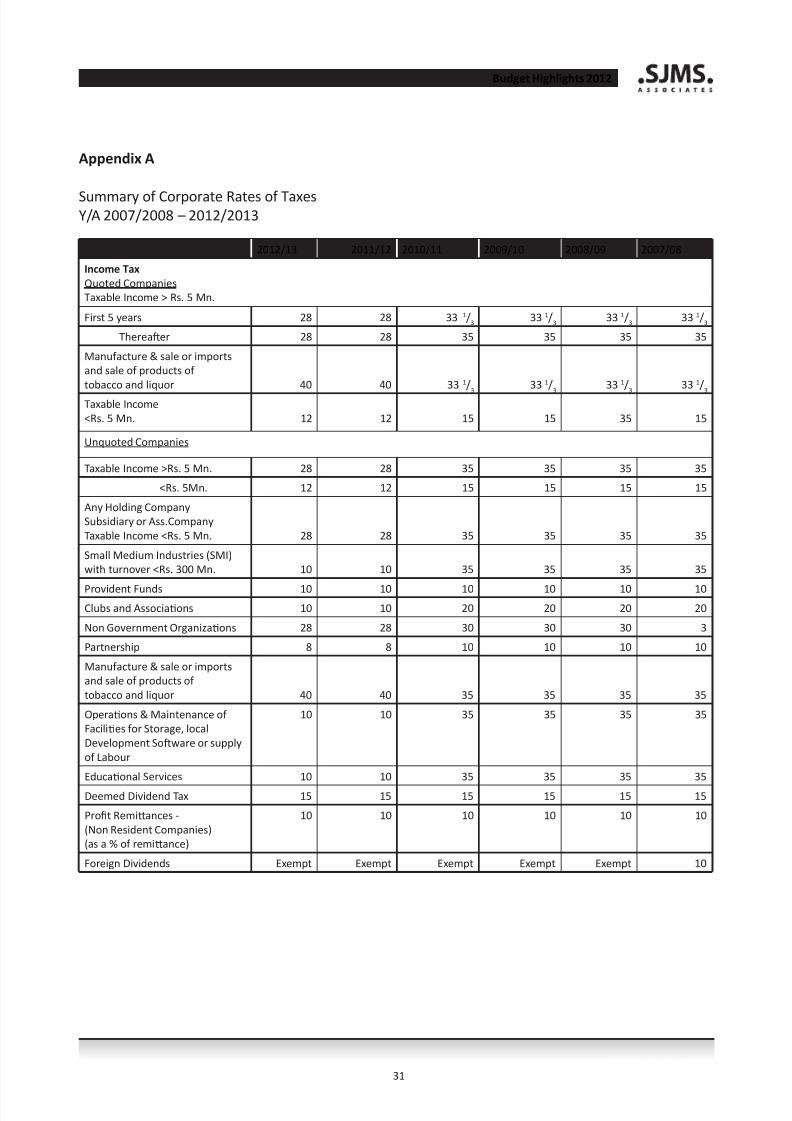

2012/13 2011/12 2010/11 2009/10 2008/09 2007/08

Income Tax

Quoted Companies

Taxable Income > Rs. 5 Mn.

First 5 years 28 28 33 1/3

33 1/3

33 1/3

33 1/3

Thereafer 28 28 35 35 35 35

Manufacture & sale or imports

and sale of products of

tobacco and liquor 40 40 33 1/3

33 1/3

33 1/3

33 1/3

Taxable Income

<Rs. 5 Mn. 12 12 15 15 35 15

Unquoted Companies

Taxable Income >Rs. 5 Mn. 28 28 35 35 35 35

<Rs. 5Mn. 12 12 15 15 15 15

Any Holding Company

Subsidiary or Ass.Company

Taxable Income <Rs. 5 Mn. 28 28 35 35 35 35

Small Medium Industries (SMI)

with turnover <Rs. 300 Mn. 10 10 35 35 35 35

Provident Funds 10 10 10 10 10 10

Clubs and Associatons 10 10 20 20 20 20

Non Government Organizatons 28 28 30 30 30 3

Partnership 8 8 10 10 10 10

Manufacture & sale or imports

and sale of products of

tobacco and liquor 40 40 35 35 35 35

Operatons & Maintenance of

Facilites for Storage, local

Development Sofware or supply

of Labour

10 10 35 35 35 35

Educatonal Services 10 10 35 35 35 35

Deemed Dividend Tax 15 15 15 15 15 15

Profit Remiances -

(Non Resident Companies)

(as a % of remiance)

10 10 10 10 10 10

Foreign Dividends Exempt Exempt Exempt Exempt Exempt 10

Appendix A

Summary of Corporate Rates of TaxesY/A 2007/2008 – 2012/2013

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 33/42

32

Budget Highlights 2012

2012/13 2011/12 2010/11 2009/10 2008/09 2007/08

Withholding Tax

Interest &Royalty paid 10 10 10 10 10 10

Interest & Royalty paid - to a person

outside Sri Lanka ( subject to DTTA ) 15 15 15 15 15 15

Rent, annuites and ground rent

- Non residents 20 20 20 20 20 20

Dividends 10 10 10 10 10 10

Interest on listed debentures & debt

securites

10 10 10 10 10 10

Management fees 5 5 5 5 5 5

Reward payments by Govt.-

Loery Prizes, Winning from-

Be ng and Gambling 10 10 10 10 10 10

Capital Allowances

Buildings 10 10 6 2/3

6 2/3

6 2/3

6 2/3

Plant, Machinery & Fixtures 33 1/3

33 1/3

12 ½. 12 ½ 12 ½ 12 ½

Sofware 25 25 25 25 25 25

Sofware (locally developed) 100 100 100 100 100 100

Commercial vehicles and offi ce

furniture 20 20 20 20 20 20

Bridges, Railway 6 2/3

6 2/3

6 2/3

6 2/3

6 2/3

6 2/3

Plant & Machinery for healthcare,

printng on paper, gem cu ng,

polishing, rice milling & packaging 33 1/3

33 1/3

33 1/3

33 1/3

33 1/3

33 1/3

Energy effi cient high tech plante

machinery and equipment 50 - - - - -

Note :

(1) To be paid by both buyer and seller

(2) Of turnover

(3) Divisible profit in excess of Rs. 600,000/-

2012/2013

%

2011/12

%

2010/11

%

2009/10

%

2008/09

%

2007/08

%

Concessionary Rate

Qualified Export 12 12 15 15 15 15

Profits /Constructon/Tourism 12 12 15 15 15 15

Agriculture 10 10 Exempt Exempt Exempt Exempt

Venture Capital Companies 12 12 20 20 20 20

Petroleum Exploraton 12 12 15 15 15 15

Exports with 65% value additon 10 10 15 15 15 15

Share transacton levy on sale of

shares of quoted companies 0.3 0.3 0.2 0.2 0.2 0.2

ESC 0.1 - 1 (2) 0.1 - 1 (2) 0.05 -1(2) 0.05 -1 (2) 0.05 -1 (2) 0.05-1(2)

Partnership 8 (3) 8 (3) 10 (3) 10 (3) 10 (3) 10 (3)

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 34/42

33

Budget Highlights 2012

2012/2013

%

2011/12

%

2010/11

%

2009/10

%

2008/09

%

2007/08

%

Deducton of Losses (restricted)

Life Insurance business Loss restricted

to Life Insurance

business profit

Loss restricted

to Life Insurance

business profit

Loss restricted

to Life Insurance

business profit

Loss restricted

to Life Insurance

business profit

Loss restricted

to Life Insurance

business profit

35 of

statutory

income

Finance Leasing

business

Loss restricted

to finance

leasing profit

Loss restricted

to finance

leasing profit

Loss restricted

to finance

leasing profit

Loss restricted

to finance

leasing profit

35 of

statutory

income

35 of

statutory

income

Limited to 35 of total

StatutoryIncome

35 of total

StatutoryIncome

35 of total

statutoryincome

35 of total

statutoryincome

35 of total

statutoryincome

35 of

totalstatutory

income

Value Added Tax

Standard 12 12 12 15 15 15

Zero 0 0 0 0 0 0

Luxury 12 12 20 20 20 18 or 20

NBT

Standard 2 2 3 3 - -Retail & Wholesale

business

2 of 50 of

turnover

2 of 50 of

turnover - - - -

Distributors 2 of 25 of

turnover

2 of 25 of

turnover

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 35/42

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 36/42

35

Budget Highlights 2012

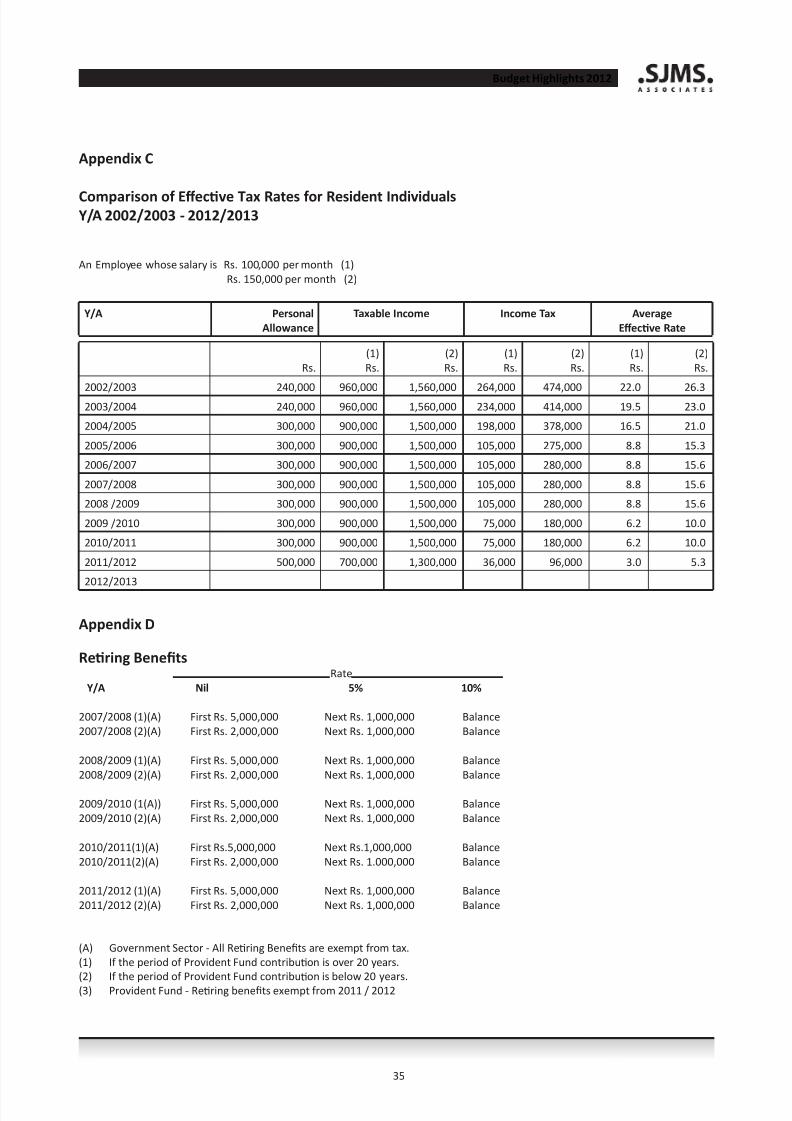

Appendix C

Comparison of Eff ectve Tax Rates for Resident IndividualsY/A 2002/2003 - 2012/2013

An Employee whose salary is Rs. 100,000 per month (1)

Rs. 150,000 per month (2)

Y/A Personal

Allowance

Taxable Income Income Tax Average

Eff ectve Rate

Rs.

(1)

Rs.

(2)

Rs.

(1)

Rs.

(2)

Rs.

(1)

Rs.

(2)

Rs.

2002/2003 240,000 960,000 1,560,000 264,000 474,000 22.0 26.32003/2004 240,000 960,000 1,560,000 234,000 414,000 19.5 23.0

2004/2005 300,000 900,000 1,500,000 198,000 378,000 16.5 21.0

2005/2006 300,000 900,000 1,500,000 105,000 275,000 8.8 15.3

2006/2007 300,000 900,000 1,500,000 105,000 280,000 8.8 15.6

2007/2008 300,000 900,000 1,500,000 105,000 280,000 8.8 15.6

2008 /2009 300,000 900,000 1,500,000 105,000 280,000 8.8 15.6

2009 /2010 300,000 900,000 1,500,000 75,000 180,000 6.2 10.0

2010/2011 300,000 900,000 1,500,000 75,000 180,000 6.2 10.0

2011/2012 500,000 700,000 1,300,000 36,000 96,000 3.0 5.3

2012/2013

Appendix D

Retring Benefits Rate

Y/A Nil 5% 10%

2007/2008 (1)(A) First Rs. 5,000,000 Next Rs. 1,000,000 Balance

2007/2008 (2)(A) First Rs. 2,000,000 Next Rs. 1,000,000 Balance

2008/2009 (1)(A) First Rs. 5,000,000 Next Rs. 1,000,000 Balance

2008/2009 (2)(A) First Rs. 2,000,000 Next Rs. 1,000,000 Balance

2009/2010 (1(A)) First Rs. 5,000,000 Next Rs. 1,000,000 Balance

2009/2010 (2)(A) First Rs. 2,000,000 Next Rs. 1,000,000 Balance

2010/2011(1)(A) First Rs.5,000,000 Next Rs.1,000,000 Balance

2010/2011(2)(A) First Rs. 2,000,000 Next Rs. 1.000,000 Balance

2011/2012 (1)(A) First Rs. 5,000,000 Next Rs. 1,000,000 Balance

2011/2012 (2)(A) First Rs. 2,000,000 Next Rs. 1,000,000 Balance

(A) Government Sector - All Retring Benefits are exempt from tax.

(1) If the period of Provident Fund contributon is over 20 years.

(2) If the period of Provident Fund contribut

on is below 20 years.(3) Provident Fund - Retring benefits exempt from 2011 / 2012

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 37/42

36

Budget Highlights 2012

SRI LANKA TAX DATA 2011/2012PERSONAL TAX

Employee Benefits

Benefit Value for Tax Purpose

Motor Vehicle Vehicle provided or allowance paid up to Rs.50,000/- will be exempt

House Employment income < Rs. 150,000/- p.m. Lower of actual rent or Rs. 120,000/- p.a. Employment income > Rs. 150,000/- p.m. Lower of actual rent or Rs. 180,000/- p.a.Telephone 50% of actual costOther benefits At actual costValue of shares received under employee share opton plan - Normal RateQualifying Payments

o Deducton from Assessable Income

● Donaton to Government ● Investments in specific projects ● Donaton in money to approved charity that providesinsttutonal care for the sick and needy.

o Qualifying payments limited to ● Donatons to approved charity & Insurance - 1/3 ofassessable income or Rs. 75, 000/- whichever is lower.

o An individual is not enttled to deduct Qualifying paymentsfrom any employment income included in the assessableincome

o Tax Free Allowance Rs. 500,000/-

Income Tax & Rate

Taxable Cumulat

ve Rate Tax Cumulat

ve Income (Rs.) Income Tax

On the first 500,000 1,000,000 4% 20,000 20,000

On the next 500,000 1,500,000 8% 40,000 60,000

-do- 500,000 2,000,000 12% 60,000 120,000

-do- 500,000 2,500,000 16% 80,000 200,000

-do- 1,000,000 3,500,000 20% 200,000 400,000

Balance 24%

o Concession & Exempton ● Resident person who is engaged in a profession andearning in foreign currency by rendering services topersons outside Sri Lanka - Exempt ● Profit from constructon work outside Sri Lanka

(Payment made in foreign currency) - Exempt ● Profit from sales of Textle, Leather products footwear

or bags by manufactures in foreign currency to a buyerwhose headquarters established in Sri Lanka (Sec 13)

- Exempt ● Employment income if exceeds Rs. 500,000/- p.a, theexcess up to Rs. 100,000/- - Exempt ● Profits from Tourism and Constructon Industry, Qualified

Exports, and deemed exports - 12% ● Entertainer or artst - 12%

Expatriate ● Employment income - Normal rates ● Entertainers and Artsts - 12%. ● Sri Lankan holding dual citzenship, foreign income is nottaxable during the stay in Sri Lanka.

Terminal Benefits ●

Government - Any Ret

ring Benefi

ts Exempt ● Private Sector- Provident Fund Exempt ● Compensaton for loss of employmentmaximum rate 20%.

● Compensaton paid under Voluntary Retrement Scheme(VRS), up to Rs. 2 million withconditons. Exempt

CORPORATE TAX

Income Tax Companies Taxable Income > Rs. 5 million 28% Taxable income < Rs. 5 million 12% Qualified Export profits and deemed exports, Tourism & Constructon industry 12% Profits and income earned in or outside Sri Lanka providing

any services other than discount, commission or similarpayments for such service rendered in Sri Lanka to a personoutside Sri Lanka and earnings remied in foreign currencyto a resident person or partnership in

Sri Lanka Exempt Provident funds, charites 10%

Clubs and associatons undertaking for operaton andmaintenance of facilites for storage, local sofwaredevelopment or supply of labour 10%

Foreign Dividends remied in foreign currency Exempt Profit remiance - Non-resident Companies 10% Profit aributable to transshipment agency fee

received in foreign currency by shipping agency 15% Interest income of charites applied for children homes,

homes for elders and disabled Exempt Deemed dividend in excess profit of 1/3 of the distributable

profit less dividend distributed 15% Profit or income from manufacture or import of liquor or Tobacco products 40% Venture capital companies, petroleum exploraton 12% Profits from any agricultural seeds or plantng materials and

thire primary processing , and fishing undertaking.

Exempt (5Y) Small & medium enterprises with less than

Rs. 300M turnover 10% Investment not less than Rs. 50M in any new

manufacturing undertaking Exempt (3Y) Investment not less than US $ 3M in selected

projects Exempt (5-7Y) Export or deemed export with 65% value

additons of Sri Lankan brand name 10%

WITHHOLDING TAX

On corporate debt interest 10% On interest - Individuals 2.5% to 8% On interest - Charitable insttutons if exceed

Rs. 500,000/- 8% On interest - Companies 10% On interest and royaltes paid outside Sri Lanka 15% (or the rate applicable under Double Tax Treaty) Royaltes paid in Sri Lanka * 10% (For royalty if exceed of Rs. 50,000 p.m or Rs. 500,000 p.a.) Dividends 10% Reward payments by Government to informant & others 10% Payment of shares of fine etc. by Government 10% Payment of Loery prizes, be ng & gaming when

payment is more than Rs. 500,000 10% Management Fee 5%

* Will not be applicable to any person or partnership paying ESC

CAPITAL ALLOWANCE Rate

Building (constructed) 10% Plant & Machinery 33 1/3% Informaton technology equipment & sofware 25 % Sofware developed in Sri Lanka 100%

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 38/42

37

Budget Highlights 2012

Commercial vehicles & offi ce furniture 20% Bridges, railways, reservoirs, electricity or water distributon & toll roads 6 2/

3%

Scientfic industrial, agricultural research expenditure 200%

DEDUCTION ON LOSSES

Losses on leasing business only against leasing business profit andlosses on life insurance only against life insurance profit.Other losses - limited to 35% of the total statutory income.

PARTNERSHIP TAXOn divisible profit in excess of Rs. 600,000/- 8%

LEVIES UNDER OTHER ACTs ● Economic Service Charge (ESC) 0.1% to 1% ● Share transacton levy - Buyer as well as Seller. 0.3% ● Natons Building Tax (NBT) 2%

VALUE ADDED TAX (VAT) Taxable supplies including Imports Standard rate 12% Direct exports of goods & specified services Zero Financial Services 12%

THRESHOLDVALUE ADDED TAX (VAT)Rs. 2,500,000 per annum / Rs. 650,000 per quarter

ECONOMICS SERVICE CHARGE (ESC)Rs. 25 million per quarter

NATION BUILDING TAX (NBT)Rs. 500,000 per quarterRetail & Wholesale business liable for NBT on 50% of turnoverDistributors liable for NBT on 25% of turnover

SOCIAL RESPONSIBLE LEVY (SRL)SRL payable by companies on income tax abolished from the Y/A2011/2012

Important Tax Dates

Y/A 2011/2012

April 2011 15 Withholding Tax on specified fees and interest, PAYE - Tax

payments - March 2011 15 4th Quarter self-assessment payment to obtain the 10%

discount in the final tax. 20 VAT, NBT & ESC returns and payments for Month /

Quarter ending 31st March 2011. 30 PAYE annual declaraton for the Y/A 2010/2011.

May 2011 15 Payment of income tax 4th quarterly installment for Y/A

2010/201. 15 Withholding Tax on interest, PAYE - Tax payments - April

2011. 20 VAT return and payment - April 2011. 20 NBT payment - April 2011.

June 2011 15 Withholding tax on interest, PAYE - Tax payments - May

2011. 20 VAT return and payment - May 2011. 20 NBT payment - May 2011.

July 2011

15 Withholding Tax on interest, PAYE - Tax payment - June2011.

15 1st Quarter self-assessment payment to obtain the 10%discount in the final tax.

20 VAT & NBT returns and payment - Month / Quarterending 30th June 2011.

20 ESC payment - Quarter ending 30th June 2011.

30 Half year VAT return on Financial Sector

August 2011 15 Payment of income tax 1st quarterly installment for Y/A

2011/2012. 15 Withholding Tax on interest, PAYE - Tax payments - July

2011. 20 VAT return and payment - July 2011. 20 NBT payment - July 2011.

September 2011 15 Withholding Tax on interest, PAYE - Tax payments -

August 2011. 20 VAT return and payment - August 2011. 20 NBT payment - August 2011. 30 Income tax final payment for the Y/A 2010/2011.

30 Last date for the profit distributon to avoid deemeddividend tax for 2011/2012

October 2011 15 Withholding Tax on interest, PAYE - Tax payments -

September 2011. 15 2nd Quarter self-assessment payment to obtain the 10%

discount in the final tax. 20 VAT & NBT returns and payment - Month / Quarter

ending 30th September 2011. 20 ESC payment - Quarter ending 30th September 2011. 31 Deemed dividend tax for the Y/A 2011/2012.

November 2011 15 Payments of income tax 2nd quarterly installment for

2011/2012. 15 Withholding Tax on interest, PAYE - Tax payments -October 2011.

20 VAT return and payment - October 2011. 20 NBT payment - October 2011. 30 Last date for the income tax return - 2010/2011

December 2011 15 Withholding Tax on interest, PAYE - Tax payments -

November 2011. 20 VAT return and payment - November 2011. 20 NBT payment - November 2011.

January 2012 15 Withholding Tax on interest, PAYE - Tax payments -

December 2011.

15 3rd Quarter self-assessment payment to obtain the 10% discount in the final tax. 20 VAT & NBT returns and payment - Month / Quarter

ending 31st December 2011. 20 ESC payment - Quarter ending 31st December 2011.

February 2012 15 Payment of income tax 3rd quarterly installment for the

Y/A 2011/2012. 15 Withholding Tax on interest, PAYE - Tax payments - January

2012. 20 VAT return and payment - January 2012. 20 NBT payment - January 2012.

March 2012

15 Withholding Tax on interest, PAYE - Tax payment -February 2012. 20 VAT return and payment - February 2012. 20 NBT payment - February 2012.

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 39/42

38

Budget Highlights 2012

ABOUT SJMS ASSOCIATES

SJMS Associates is a mult disciplinary professional services firm and is an Independent Correspondent Firm

to Deloie Touche Tohmatsu, an internatonal firm of accountants. SJMS Associates was formed on the 1st of

July 2002 with the merger of SJ Associates with Manoharan&Sangakkara Associates. Both firms have a history

of over thirty five years. The merger has enabled SJMS to establish one of the largest and effi cient professional

service practces in the country. It also expanded the ability to off er such services at a tme when clients must

increasingly contend with the impact of globalizaton on their businesses.

SJMS Associates has over 35 professionals and a staff of 400 with a Branch and Correspondent offi ce in Kandy.SJMSfocuses on improving the growth and compettveness of clients’ businesses through the provision of a

wide range of specialized services.

Services provided :

Audit & Assurance Tax Compliance & Planning

• Financial Assurance • Corporate Tax, Compliance and assessments

• Internal Audits including at appellate levels

• Forensic Services • Indirect Taxaton including VAT and Excise Duty

• Due Diligence • Expatriate Tax Consultng

• Outsourced Accountng Services • Internatonal Taxaton

• Informaton System Audits • Strategic Tax Planning

Management Consultng Restructure & Corporate Recovery

• General Management Consultng • Restructuring / Reorganizaton Services

• Business Strategy Consultng • Corporate Closure Management

• Foreign Investment Services • Liquidaton Services

• Privatzaton Services

• Human Resources Consultng

• Systems and Solutons

Corporate Finance • Mergers and Acquisitons

• Corporate Finance & Private Capital

• Transacton Executon

• Valuatons

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 40/42

39

Budget Highlights 2012

Contacts

SJMS Associates Tel. + 94 11 5444400 / 5444408/09 [email protected] Castle Lane Fax. + 94 11 2586068

Colombo 04.

Ms. S. Kodagoda Tel. +94 11 5444400/ 5444410 [email protected]

Mr. P. Sivasubramaniam Tel. + 94 11 5444400 / 5444408/09

Mr. D. Fernando Tel. + 94 11 5444400 / 5444408/09 [email protected]

Mr. M. Ratnayake, Tel. + 94 11 5444400 / 5444408/09 [email protected]

Ms. I. Karunaratne Tel. + 94 11 5444400 / 5444408/09 [email protected]

Ms. L. Fernando Tel. + 94 11 5444400 / 5444408/09 [email protected]

Polytechnic Building Tel. + 94 11 2501677 / 5667829 / 5624303

30 - 2/1 Galle Road Fax. + 94 11 2507522

Colombo 06

Mr. M. Thavaraj Tel. + 94 11 2501677 / 5667829 / 5624303 [email protected]

Ms. T. Varathaluckshmy Tel. + 94 11 2501677 / 5667829 / 5624303 [email protected]

Branch

SJMS Associates Kandy Tel. + 94 081 2228684 or 5628649

25/1/1 George E. de Silva Fax. +94 081 2203071

Mawatha

Kandy

Mr. R. Rajendran [email protected]

Correspondent Offi ce

RanaweeraNagasinghe& Co. Tel. + 94 041 2222365

41/5B Old Market Road Fax. + 94 041 2221415

Kotuwegoda

Matara

Mr. S.J. Ranaweera [email protected]

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 41/42

40

Budget Highlights 2012

8/12/2019 SJMS Associates Budget Highlights 2012

http://slidepdf.com/reader/full/sjms-associates-budget-highlights-2012 42/42