skoll centre for social entrepreneurship1 session 6 social entrepreneurship and social innovation

TRANSCRIPT

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP1

Session 6Session 6

Social Social Entrepreneurship and Entrepreneurship and

Social InnovationSocial Innovation

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP2

Towards A Social Towards A Social Finance Market-PlaceFinance Market-Place

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP3

OverviewOverview

• Background• Context• Landscape• Brokerage models• Social stock market

• Case studies: Traidcraft; cafedirect; Compartamos

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP4

BackgroundBackground

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP5

Role Of Private Role Of Private SectorSector• Wealth creation• Return on capital• Profit maximisation

• Innovation• Market making

• Individual rational actor maximising personal utility in one off transactions?

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP6

Role Of GovernmentRole Of Government

• Govern for the common good• Democratic mandate and accountability

• Authorise• Procedural rights

• Coerce• Substantive rights

• Responsible for societal equality and fairness• Equality of outcome?• Equality of opportunity?

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP7

Role Of GovernmentRole Of Government

• Solve free-rider issues• Regulation for public benefit• Address individual hyperbolic discounting

• Ensure economic efficiencies• Utilities• Infrastructures• Welfare goods• Address market failures in public goods

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP8

Government And Government And FinanceFinance• Sets the economic context• Regulates via legislation• History of financial markets• Consequences of deregulation• Track record in social finance since 1997

• Non-UK examples

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP9

Role of Third SectorRole of Third Sector

• Value(s) driven• Absence of government

• Heterogeneous demand for public goods

• Absence of private sector• Non-market goods

• Reassurance of non-distribution structure• Complex goods/services• Third party beneficiaries• Unreliable beneficiaries• Pooled input resources(DiMaggio and Anheier, (DiMaggio and Anheier,

1990)1990)

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP10

ContextContext

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP11

Financial MarketsFinancial Markets

• Cost efficient• Low transaction costs

• Information rich• Up-to-date

• Value driven allocation of funds• Success is rewarded

• Flexible and responsive• High liquidity

Meehan et al (2004)Meehan et al (2004)

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP12

Social Finance MarketSocial Finance Market

• Inefficient• High transaction costs

• Information poor• Inconsistent or non-existent metrics

• Cause driven allocation of funds• Success goes unmeasured and unrewarded

• Static and inflexible• Low liquidity, limited resources

Meehan et al (2004)Meehan et al (2004)

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP13

InefficientInefficient

Unlike resource allocation in Unlike resource allocation in the business world, where the business world, where

investors and companies seek investors and companies seek one another out in an one another out in an

information-rich environment, information-rich environment, philanthropy is largely a one-philanthropy is largely a one-

way streetway street

Meehan et al (2004)Meehan et al (2004)

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP14

Application ProcessApplication Process

• Time consuming and inefficient• Different for each cause• Different for each source of funds

• Organisation, not mission, focussed

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP15

High CostHigh Cost

• Raising funds:• For-profit capital market: $2-4 per $100• Legal• Marketing • Admin

• Not-for-profit capital market: $10-24 per $100• Buying donor lists• Direct mail/Telephone calls

• Not-for-profit CEOs spend 30-60% of time on fund-raisingMeehan et al (2004)Meehan et al (2004)

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP16

High CostHigh Cost

• Allocating funds:• Foundations: $12-19 per $100

• General overhead• Reviewing applications

• Intermediary groups (eg. United Way): $13 per $100

• Total cost: $22-43 per $100

Meehan et al (2004)Meehan et al (2004)

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP17

Information PoorInformation Poor

• Only 38% US charities filed a ‘Form 990’ IRS return (2002)• Hard to obtain• Of these, 15% included serious errors

• No uniform not-for-profit accounting standards

• No single regulatory authority• Very fragmented market

Meehan et al (2004)Meehan et al (2004)

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP18

Resource AllocationResource Allocation

• Distorted by:• Cause/mission focus• History of institutional loyalty• Lack of performance driven resource allocation

Meehan et al (2004)Meehan et al (2004)

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP19

Static MarketStatic Market

• Financial contributions are largely final and irreversible• Grant not investment

• Cannot be withdrawn easily• Lack information to judge subsequent funding

Meehan et al (2004)Meehan et al (2004)

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP20

Landscape of Social Landscape of Social FinanceFinance

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP21 SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP

Drivers Behind Social Drivers Behind Social FinanceFinance

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP22 SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP

Social FinanceSocial Finance

TheThe system of finance supply and system of finance supply and distribution to support socially distribution to support socially

entrepreneurial approaches to public and entrepreneurial approaches to public and environmental challenges. Social finance, environmental challenges. Social finance, therefore, is more than just the flow of therefore, is more than just the flow of

money into social or environmental money into social or environmental projects. It is conceived as an ethos projects. It is conceived as an ethos

about the way money is used…social finance about the way money is used…social finance can be seen as the discourse around such can be seen as the discourse around such flows that is developing in concrete terms flows that is developing in concrete terms

in the new institutions of supply, in the new institutions of supply, intermediation, and demand. This is a intermediation, and demand. This is a

discourse in flux with competing discourse in flux with competing perspectives driving the debateperspectives driving the debate

Nicholls with Pharoah (2008)

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP23

Social Investment Social Investment OptionsOptions• Not-for-profit/charity that generates Not-for-profit/charity that generates exclusively social valueexclusively social value• Non-market rateNon-market rate

• Social enterprise that is profit-making but Social enterprise that is profit-making but also has a clear social/environmental also has a clear social/environmental purposepurpose• Sub-market/market rateSub-market/market rate

• Commercial opportunities in deprived areasCommercial opportunities in deprived areas• Market rateMarket rate

• ‘‘Social firms’ that employ disenfranchised Social firms’ that employ disenfranchised members of the communitymembers of the community• Sub-market/market rateSub-market/market rate

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP24

Spectrum of Financial Spectrum of Financial ReturnReturn

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP25

Spectrum Of Social Spectrum Of Social FinanceFinanceFinancial Financial InstrumentInstrument

Purpose of Purpose of FinanceFinance

Type of FinanceType of Finance ExampleExample

Private Private GrantGrant

Fulfilling Fulfilling Mission Mission Capacity BuildingCapacity Building

(Venture) Philanthropy(Venture) PhilanthropyPRIPRIMRIMRI

Impetus TrustImpetus TrustFB Heron FoundationFB Heron FoundationCalvert FoundationCalvert Foundation

Government Government GrantGrant

RegenerationRegenerationMarket Market DevelopmentDevelopment

Community Development Community Development LoansLoansUnclaimed AssetsUnclaimed Assets

Community Development Finance Community Development Finance Institution (CDFI)Institution (CDFI)Social Investment BackSocial Investment Back

Government Government ContractsContracts

Outsourcing Outsourcing Welfare ServicesWelfare Services

Contractual ExchangeContractual Exchange Greenwich LeisureGreenwich LeisureEaling Community TransportEaling Community Transport

DebtDebt Economic and Economic and Social Social DevelopmentDevelopment

Micro-FinanceMicro-Finance Grameen BankGrameen BankCitiBankCitiBank

Quasi-EquityQuasi-Equity Growth CapitalGrowth Capital Share of OwnershipShare of Ownership Bridges Community VenturesBridges Community VenturesCatalystCatalyst

Sub-Market Sub-Market EquityEquity

Growth CapitalGrowth Capital Restricted ‘Ethical’ Restricted ‘Ethical’ SharesShares

CafedirectCafedirectEthical Property CompanyEthical Property Company

MarketMarket EquityEquity

Growth CapitalGrowth Capital Standard SharesStandard Shares London Bridge CapitalLondon Bridge CapitalCompartamos BankCompartamos Bank

JointJoint EquityEquity Start-up/Start-up/Growth CapitalGrowth Capital

Co-operative Ownership Co-operative Ownership (IPS)(IPS)

MondragonMondragonBayWindBayWind

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP26

DemandsideDemandside

• Charities • 168,000 • Total income of £40bn

• Social enterprises• 55,000• Total income of £27bn

• Community Interest Companies (CICs)• 2,000 since 2005• No information on income

• Co-ops

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP27

Charity FinanceCharity Finance

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP28

SupplysideSupplyside

Risk level

Minimal Low Medium High

Provider Banks(Triodos)

CDFIsCharity BankLocal Investment FundsBridges C.V.

VenturesomeImpetusAdventure Capital Fund BigInvestFutureBuilders

CharitableTrustsGovernmentEquity

Current Funds Available

Extensive

£181m£62.5m£40m

£15-20m£3.5m£12m£250m1m EURO

£2.7bn£5bn>£10m

Potential

Loss

<1% 1-10% 10-50% 100%

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP29

Structured FinanceStructured Finance

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP30

The Investor UniverseThe Investor Universe

- 100% + 8%0%

Capital-protected Market-rate returnGrant-makers

- 15%

?

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP31

Structured FinanceStructured Finance

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP32 SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP

Supply And DemandSupply And Demand

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP33

Credit

Unions

Micro-Finance InstitutionsETHEX

Government

Social

FirmsCommercial Investors

Social Enterpris

es

Micro-Entrepreneu

rs

Tax-Payers

Philanthropists

Banks

Dedicated Intermediar

ies

Ethical

Investors

VP Funds

Foundations

SIB

Charities

N-F-P Social

Entrepreneurs

Co-ops

Members

Market Transaction

s

DEMAND SUPPLY

INTERMEDIARIES

Landscape of Social Landscape of Social FinanceFinance

CDFIs

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP34

Brokerage ModelsBrokerage Models

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP35

Policy and Social Policy and Social EnterpriseEnterprise• The formation of a Social Enterprise

Unit within DTI (2002), now incorporated within the Office of the Third Sector

• The establishment of an Office of the Third Sector within the Cabinet Office with its own Minister (2006)

• Key objectives:• To better understand the sector and its impacts

• To provide an ‘enabling environment’ for it to flourish

• Tory policy too now!

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP36

Policy and Social Policy and Social EnterpriseEnterprise• To find solutions to some of societies’ most entrenched social problems• Over half social enterprises surveyed in 2005 were located in the 40% most deprived areas

• To support the growth in ethical markets • Between 1999 and 2004 the sale of Fair Trade marked food grew by more than 640%

• To support the development of a social finance marketplace

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP37

• SEs improve public services• Social enterprises are active in many public sector markets – particularly health and social care

• At their best they offer a high level of engagement with users and a capacity to build trust

• SEs increase overall levels of enterprise• 55,000 social enterprises generate £8.4bn to GDP pa

• The social enterprise model appears to be more attractive to women and certain ethnic minority groups than conventional business models

Policy and Social Policy and Social EnterpriseEnterprise

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP38

• Not to create social entrepreneurs but to create the environment in which they can succeed

• That means government can act as • Catalyst – government can help to overcome address market failures or barriers to growth

• Customer – government can purchase services from SEs

• Champion – government can help to overcome information failures

Policy and Social Policy and Social EnterpriseEnterprise

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP39

Policy and Social Policy and Social InvestmentInvestment• Social Investment Task Force (2002)• Phoenix Fund (2002) to capitalise CDFIs• Bridges Community Ventures Ltd (2002) to provide investment specifically for small businesses in deprived areas• Founded by Sir Ronald Cohen (Apax Partners, 3I) and Tom Singh (New Look)

• Initially raised £20 million from the private sector and £20 million in government matching investment

• Started investing a second fund in 2006

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP40

Policy and Social Policy and Social InvestmentInvestment• Adventure Capital Fund (2002), worth

£15 million, to offer longer-term financial and development investment to support community enterprise growth

• Community Asset Transfer fund of £30 million to support local authority asset transfers into community ownership (2002)

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP41

Policy and Social Policy and Social InvestmentInvestment• Community Investment Tax Relief (2003) to provide investors with an income tax break on investment in social purpose organisations in deprived areas• CITR has attracted around £40 million of investment in the sector

• Longer term contracting between government and social enterprises (DTI, 2003)

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP42

Policy and Social Policy and Social InvestmentInvestment• Futurebuilders (2005) fund worth £215 million to offer investment packages of grants/loans/technical support for organisations to bid for government service-delivery contracts

• Two pilot funds (2006), worth £200k, for innovation in encouraging private sector investment in social enterprise

• £10 million fund for social enterprise (2006) in recognition of the need to stimulate growth

• Social Investment Bank?

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP43 SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP

Landscape Of Social FinanceLandscape Of Social Finance

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP44

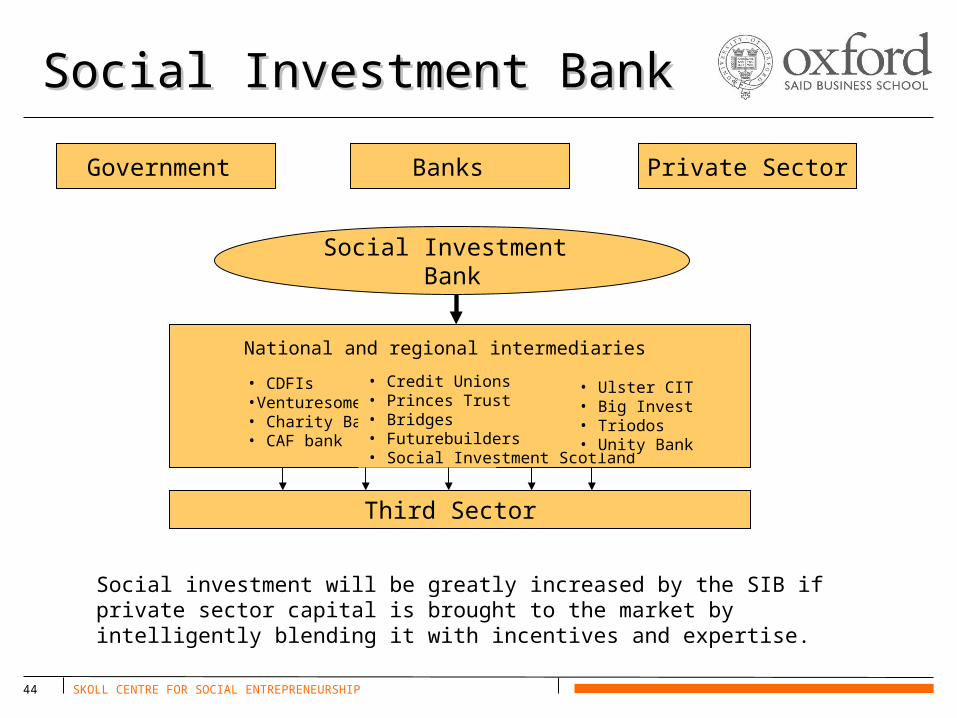

Government Banks Private Sector

Social Investment Bank

Third Sector

National and regional intermediaries

• CDFIs •Venturesome• Charity Bank• CAF bank

• Credit Unions • Princes Trust• Bridges• Futurebuilders• Social Investment Scotland

• Ulster CIT• Big Invest• Triodos• Unity Bank

Social investment will be greatly increased by the SIB if private sector capital is brought to the market by intelligently blending it with incentives and expertise.

Social Investment Social Investment BankBank

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP45

• Four initial activities that should attract significant additional finance into the sector: • Capitalise present financial intermediaries and fill gaps in the marketplace

• Develop the provision of advice, support and higher -risk investment so as to accelerate the growth of demand for repayable finance

• Develop programmes of sustained investment in specific markets such as community regeneration and financial inclusion

• Support existing and new intermediaries in their efforts to raise private capital

Social Investment Social Investment BankBank

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP46

Market Building Market Building ActivitiesActivities• Bond issues supporting community finance

• Opportunity for an SIB to support structural reform of the social fund (currently a government delivered soft loan fund)

• Opportunity to raise capital from bond issues that would then be lent on through credit unions and CDFIs

• Funds could also be lent on through new direct banking services

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP47

Private Brokerage Private Brokerage ModelsModels• Xigi

• www.xigi.net

• GEXSI• New Philanthropy Capital

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP48

• Founders:• Bain & Company • Deutsche Bank• Foursome Investments• GTZ-Deutsche Gesellschaft für Technische Zusammenarbeit

• Open Society Institute• Schwab Foundation for Social Entrepreneurship

• PricewaterhouseCoopers

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP49

• Social investment aims:• Quality: by way of greater social investment effectiveness in the finance and social entrepreneurship sectors

• Quantity: by way of financial ‘additionality’, enlarging globally the revenue pool available for social investment

• Operational 2004http://www.gexsi.org/index.htmlhttp://www.gexsi.org/index.html

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP50

• Development deals• Support civil society projects and programs

• Bring together private and public social investors with social entrepreneurs and social purpose organizations

• Created in tandem with ACCESS (Keystone) • Ratings agency designed to give SEs recognition under a common, global profiling system

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP51

• Quality assurance and risk management• Based on new, independent rating, implementation reviews, and assessments of effectiveness

• Strategic advice• GEXSI, in association with the institutions of its founders, and especially with GTZ, can tap into a worldwide system of on-the-ground development experts in some 120 countries

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP52

• Founded 2001• A bridge between donors and charities

• Researching a social issue and highlighting effective organisations that will flourish with additional funding

• Employs analytical tools used in finance and business in the voluntary sector

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP53

• International in scope• 2001-4, advice on:

• £18m donations• £20k-£1.5m per donation• 50 charities

• Global Philanthropy Forum

http://http://www.philanthropycapital.org/www.philanthropycapital.org/

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP54

EthexEthex

• Founded by Triodos Bank• Matched bargain market• Listings

• Ethical Property• cafedirect• Renewable Energy Fund• Golden Lane Housing• Triodos Bank NV shares

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP55

Social Stock MarketSocial Stock Market

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP

Impetus (venture philanthropy 4m)

Futurebuilders (public services 125m)

Grants(100%)

Foundations, Government

No Trading Revenue

Potentially

sustainable - 75%+ Trading Revenue

Profitable - Surplus

Not Distributed

Trading Revenue

And Grants

Breakeven - All Revenue from Trading

Profit Distributing -

Socially Driven

Profit Maximizing

Patient Capital(50%)

High default risk

Low default risk

Loans(1-10%)

CDFIs and Banks (Triodos 50m, Charity Bank 10m)

Equity and equity/like capital (10-20%)

Foursome (40m)

CDVC Funds

Adventure Capital (community 2.7m)

Venturesome (2m)

Regional funds*

Objective 1 and 2 funds*

London Rebuilding Society (0.5m)

Gap for Social Equity Capital

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP57

Equity-Like CapitalEquity-Like Capital

Equity-like capital is not Equity-like capital is not centrally based on ownership of centrally based on ownership of the shares of the company which the shares of the company which

avoids problems that social avoids problems that social enterprises have historically enterprises have historically

had with issuing equity. Equity-had with issuing equity. Equity-like capital is structured as like capital is structured as subordinated debt, which has subordinated debt, which has

equity-like featuresequity-like featuresHoward (2004)Howard (2004)

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP58

Social EquitySocial Equity

• Alternative Public Offering (APO)• Off-market

• EthEX (Triodos)

• Restricted control• Soft returns (0-3%)

• Traidcraft• Cafedirect• Ethical Property

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP59

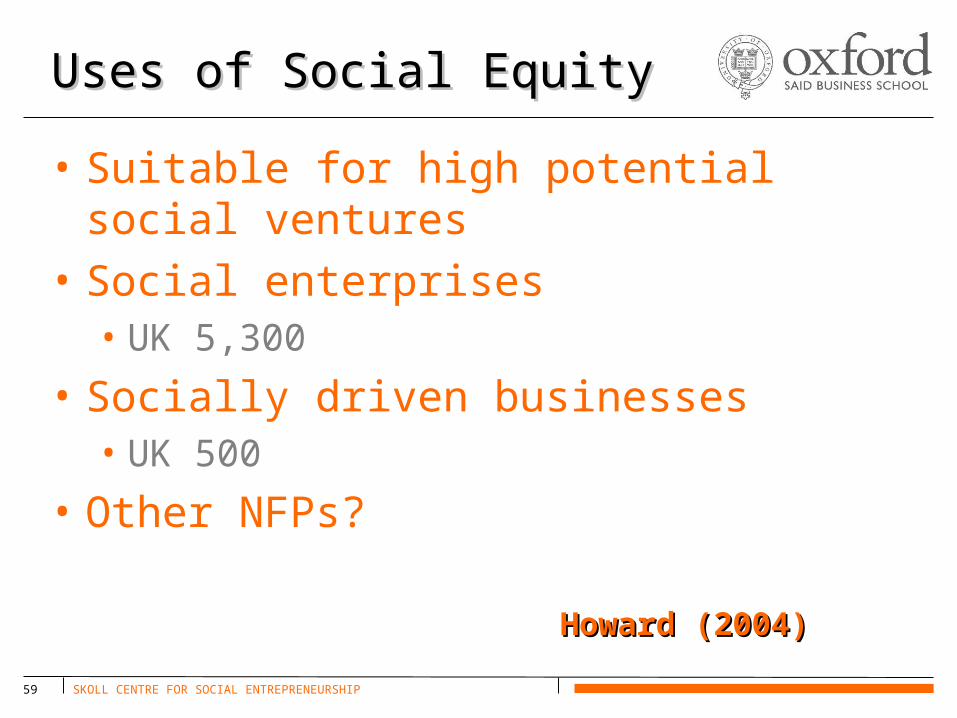

Uses of Social EquityUses of Social Equity

• Suitable for high potential social ventures

• Social enterprises• UK 5,300

• Socially driven businesses• UK 500

• Other NFPs?

Howard (2004)Howard (2004)

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP60

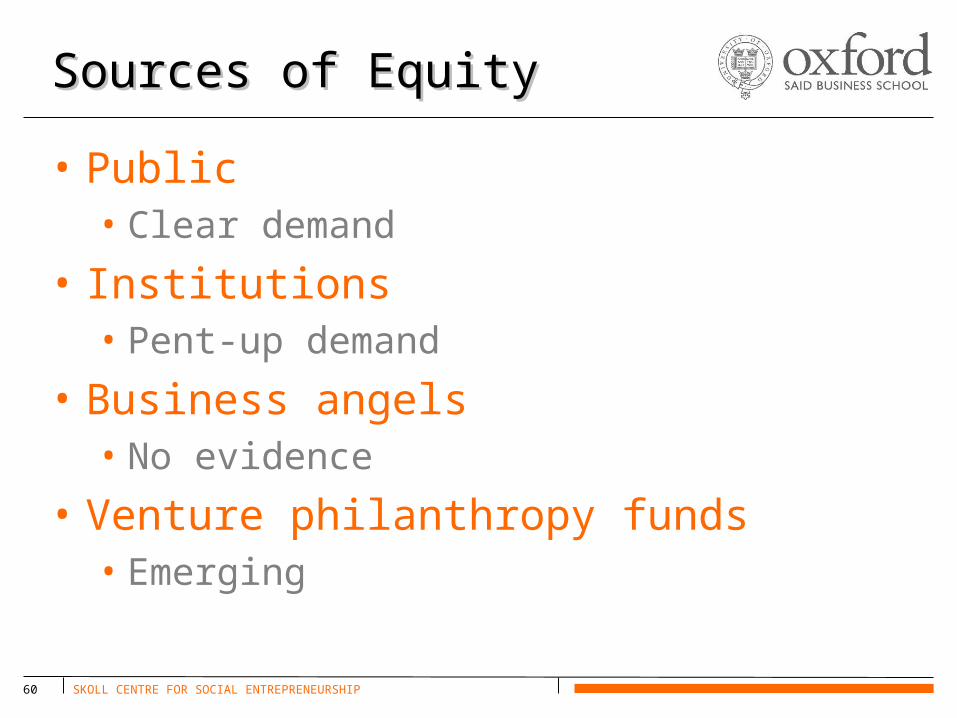

Sources of EquitySources of Equity

• Public• Clear demand

• Institutions• Pent-up demand

• Business angels• No evidence

• Venture philanthropy funds• Emerging

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP61

Equity ConstraintsEquity Constraints

• Market Liquidity• Exit strategies

• Financial returns• Unfavourable risk-return profile

• Legal structures• Control issues• Ownership role of grants

• Role of prior investments?

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP62

Social Equity Issues Social Equity Issues 1984-20051984-2005

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP63

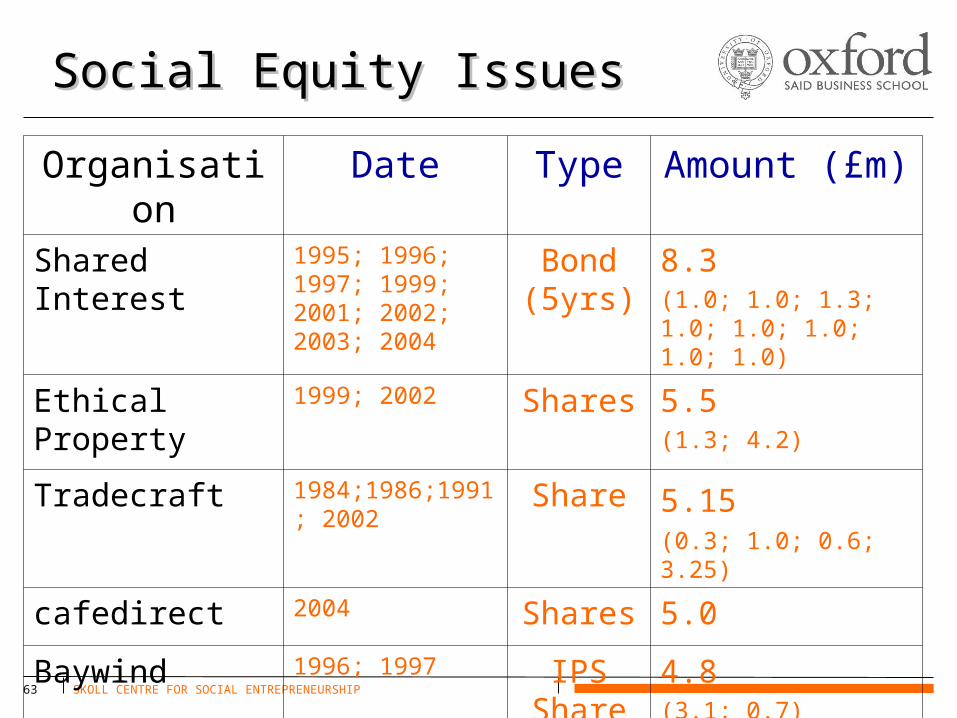

Social Equity IssuesSocial Equity Issues

Organisation

Date Type Amount (£m)

Shared Interest

1995; 1996; 1997; 1999; 2001; 2002; 2003; 2004

Bond (5yrs)

8.3(1.0; 1.0; 1.3; 1.0; 1.0; 1.0; 1.0; 1.0)

Ethical Property

1999; 2002 Shares 5.5(1.3; 4.2)

Tradecraft 1984;1986;1991; 2002

Share 5.15 (0.3; 1.0; 0.6; 3.25)

cafedirect 2004 Shares 5.0

Baywind 1996; 1997 IPS Share

4.8(3.1; 0.7)

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP64

Case StudiesCase Studies

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP65

Traidcraft CaseTraidcraft Case

• What are the financing options for growth open to Traidcraft?

• What are the implications of offering equity?

• How can Traidcraft best balance mission and commercial objectives?

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP66

cafedirectcafedirect

• 2004 APO: £5m = 51% of company• £1 per share

• Four founders retained 40.5% of total equity and held one Guardians’ Share

• Maximum stock holding = 15%

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP67

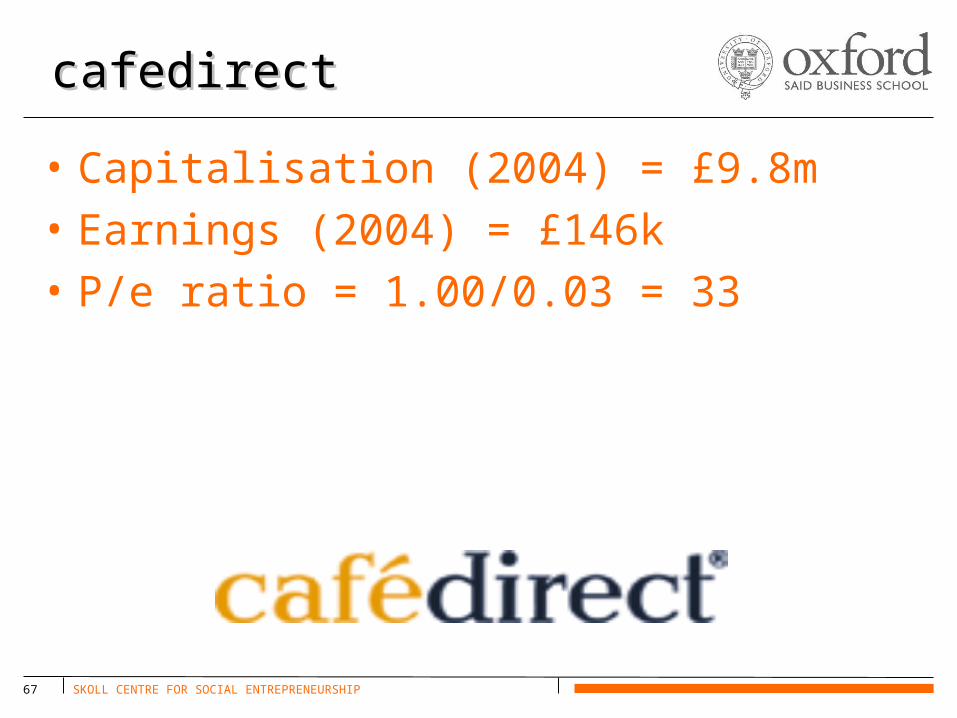

cafedirectcafedirect

• Capitalisation (2004) = £9.8m• Earnings (2004) = £146k• P/e ratio = 1.00/0.03 = 33

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP68

cafedirectcafedirect

Number of Shares

Number of Shareholder

s

% of total shares

1-300 1233 4.1

301-500 1531 8.4

501-1000 1185 12.5

1001-5000 548 16.8

5001-10000 32 3.2

10001 and over

29 55

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP69

• Earnings multiple• Trading not asset-basedTrading not asset-based• Expectation of sustainable earnings Expectation of sustainable earnings • Advised by Brewin Dolphin to 14xAdvised by Brewin Dolphin to 14x

• 7.1% return after tax7.1% return after tax

• IssuesIssues• Interest rates 3%Interest rates 3%• Inflation 2%Inflation 2%• FTSE food/beverage returns 6% (P/E 16.7)FTSE food/beverage returns 6% (P/E 16.7)• Ease of selling (liquidity)Ease of selling (liquidity)

Moving Share PriceMoving Share Price

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP70

• Profit before taxProfit before tax• Adjusted:Adjusted:

• Add back 80% of PPP investment Add back 80% of PPP investment • ‘‘Normalise’ for long-term US$ rateNormalise’ for long-term US$ rate• Deduct tax chargeDeduct tax charge

EarningsEarnings

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP71

• Recognises that ‘financial return’ is Recognises that ‘financial return’ is reducedreduced

•Due to ‘social return’ from investment Due to ‘social return’ from investment in producer organisationsin producer organisations

•But recognises that this gives financial But recognises that this gives financial benefit of 20% (eg continuity of supply benefit of 20% (eg continuity of supply during price volatility)during price volatility)

Adding Back 80% of Adding Back 80% of PPP?PPP?

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP72

• Recognises profitability is subject Recognises profitability is subject to fluctuations in the US$to fluctuations in the US$

• Adjustment ‘normalises’ profit using Adjustment ‘normalises’ profit using long-term average of $1.72 long-term average of $1.72

0

5

10

15

20

25

30

35

40

45

50

2000 2001 2002 2003 2004 2005

0

0.5

1

1.5

2

Adjust For US$ Rate?Adjust For US$ Rate?

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP73

5-year average

5-year forward

share issue planning

US$1.72?US$1.72?

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP74

(£k)(£k)

Profit before taxProfit before tax 802.2802.2

add:add: 80% of PPP investment 80% of PPP investment ( £574.0) ( £574.0)

459.2459.2

adjustadjust::

Long-term US$ exchange rate Long-term US$ exchange rate $1.72$1.72

(250.0)(250.0)

1,011.41,011.4

less:less: Tax charge, based on adjusted Tax charge, based on adjusted profitprofit

(290.3)(290.3)

EarningsEarnings 721.1721.1

Earnings x multiple of 14Earnings x multiple of 14 £10,095.8£10,095.8

Divide by: No of Shares in Divide by: No of Shares in issueissue

8,995.48,995.4

Price per sharePrice per share £1.12£1.12

Adjusted Share PriceAdjusted Share Price

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP75

CompartamosCompartamos

• 1990 Established as an NGO• 2000 Moved operations to a regulated finance company

• 2002 Issued debt on Mexican bond market

• 2006 Authorised to operate as a full-service bank

• 2007 IPO

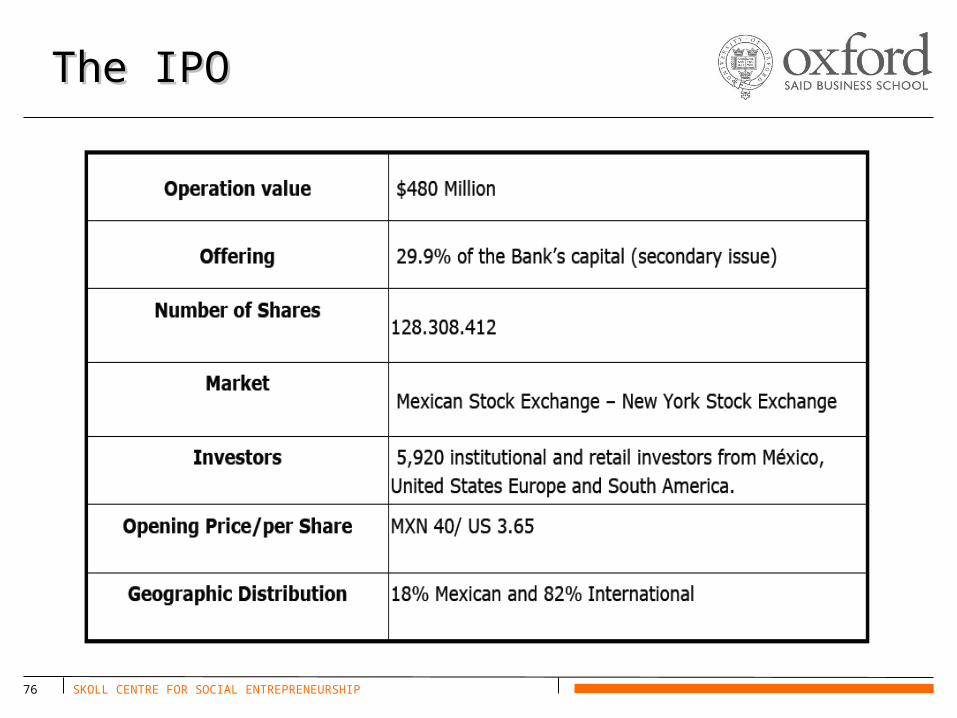

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP76

The IPOThe IPO

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP77

APO Or IPO?APO Or IPO?

•Pre-IPO: $6.3M in grants catalyzed Pre-IPO: $6.3M in grants catalyzed $130M in private, commercial resources$130M in private, commercial resources•CGAP: $2M grant included no covenants CGAP: $2M grant included no covenants about future interest rates or profit about future interest rates or profit levels levels • Was the aid money from early years used Was the aid money from early years used inappropriately to enrich private inappropriately to enrich private investors?investors?

• Are Compartamos’ exceptional profits and Are Compartamos’ exceptional profits and high interest rates they are built on high interest rates they are built on defensible in light of the company’s defensible in light of the company’s social bottom line? social bottom line?

• Are they in line with the development Are they in line with the development objectives of its principal shareholders?objectives of its principal shareholders?

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP78

Grants And Soft LoansGrants And Soft Loans

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP79

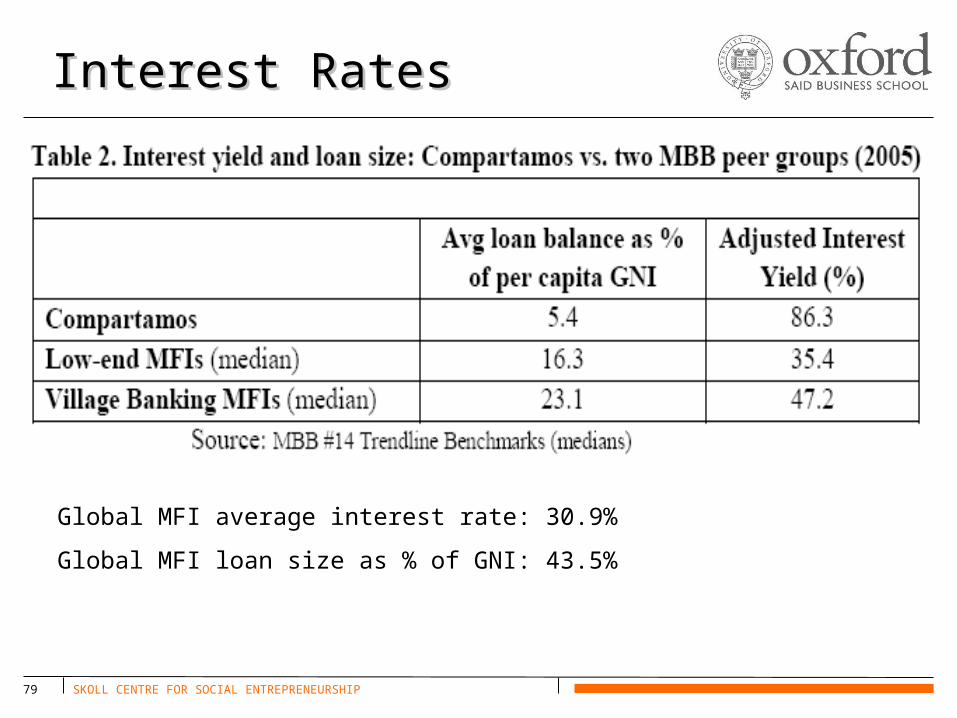

Interest RatesInterest Rates

Global MFI average interest rate: 30.9%

Global MFI loan size as % of GNI: 43.5%

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP80

Interest RatesInterest Rates

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP81

Interest RatesInterest Rates

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP82

Interest RatesInterest Rates

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP83

Interest RatesInterest Rates

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP84

Interest RatesInterest Rates

Largest share

Cost of funds is significant contributor

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP85

Interest RatesInterest Rates

For-profit corporation formed

All earnings retained up to this point

2006: ¼ earnings paid in dividends

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP86

Interest RatesInterest Rates

SKOLL CENTRE FOR SOCIAL ENTREPRENEURSHIP87

Key Issues in APOsKey Issues in APOs

• Share price• Role of ‘social’ investment banks

• Exits and profits• For whom?• How distributed?

• Trading and price• Liquidity• Speculation• Profiteering