small business & agriculture advisory council federal ... you plan to increase investment in...

TRANSCRIPT

Small Business & Agriculture Advisory Council Federal Reserve Bank of New York

33 Liberty Street 10F, Paul Volcker Boardroom

Thursday, November 20 AGENDA 10:30am Introductory Remarks

Christine Cumming, First Vice President 10:40am-11:10am The National Economy

Richard Peach, Senior Vice President 11:10am-11:30am Regional Update

Jason Bram, Vice President 11:30am-12:00pm International Update

John Clark, Senior Vice President

12:00pm 12:15pm 12:15pm-1:55pm

Adjourn to NWCR-10F Lunch Round Table Discussion with William Dudley, President Questions for discussion with President Dudley: Your experience and that of your customers and suppliers can give us insight into current economic conditions. 1. Did your firm’s sales volume increase, decrease or stay the

same in the second half of the year? 2. Next year, do you expect your firms’ sales to increase, decrease, or stay the same? 3. Do you plan to increase investment in your firm (plant &

equipment) next year? 4. Has your firm faced any shortage of labor that has limited your

ability to meet demand? 5. Do you plan to increase employment next year? 6. Do you expect input prices to increase next year? Do you

expect prices of products/services sold to increase? 7. Over the past six months, how have the terms and conditions

for obtaining financing changed (tightened, eased, not changed)?

2:00 pm Adjourn

Small Business & Agricultural Advisory Council Federal Reserve Bank of New York

33 Liberty Street New York, NY

Thursday, November 20, 2014

ATTENDEE LIST

Council Members Michael Arnoff President Arnoff Moving & Storage Stewart Brunhouse President A&A Company, Inc. William Byrne Chairman of the Board Byrne Dairy, Inc. Eric Caslow President Acme Smoked Fish

David Campbell President and CEO Rings End, Inc. Peter Maglathlin Chief Executive Officer MBI, Inc. Patrick Marotta President/CEO Marotta Controls Edward J. Tregurtha President Moran Towing Corporation

Federal Reserve Bank of New York William Dudley President Christine Cumming Richard Peach John Clark

First Vice President SVP, Research & Statistics SVP, Development Studies & Foreign Research

Kausar Hamdani Anand Marri Rae Rosen Claire Kramer Jason Bram Luis Uranga David Parkinson

SVP, Communication & Outreach VP, Head of Outreach & Education VP, Outreach & Education AVP, Outreach & Education Officer, Research & Statistics Sr. Associate, Chief of Staff’s Office Counsel, Legal

US Macro Overview November 20, 2014

GDP Trillions of 2009 US$ Trillions of 2009 US$

Source: Bureau of Economic Analysis, Congressional Budget Office

2000Q1 to 2007Q4: 2.5% Growth Rate

2009Q2 to 2014Q3: 2.3% Growth Rate

Time Period Potential GDP (CBO)

2000 - 2005 3.14%

2005 – 2010 2.11%

2010 – 2015 1.55%

2015 – 2020 2.18%

2

56

58

60

62

64

66

68

0

2

4

6

8

10

12

2000 2002 2004 2006 2008 2010 2012 2014

Labor Market Indicators

Source: Bureau of Labor Statistics

Unemployment Rate (Left Axis)

Labor Force Participation Rate

(Right Axis)

Percent Percent

Employment to Population

Ratio (Right Axis)

3

PCE Deflator

% Change – Year to Year % Change – Year to Year

Source: Bureau of Economic Analysis

Total PCE

Core PCE

FOMC Objective

4

Disposable Income, Consumption, and Wealth

% Change over 20 Quarters, Annual Rate % of Disposable Income

Real Personal Consumption

(Left Axis)

Real Disposable Income

(Left Axis)

Household Net Worth

(Right Axis)

Source: Bureau of Economic Analysis, Federal Reserve Board 5

0

2

4

6

8

10

12

400 450 500 550 600 650 7000

2

4

6

8

10

12

Source: Bureau of Economic Analysis and Federal Reserve Board Households’ Net Worth as a Percent of Disposable Income

2006-2007

2008Q2

2009Q2

Note: Fitted line is from 1983Q1 to 2005Q4.

2011Q2

Personal Saving Rate and Household Net Worth Personal Saving Rate (Percent) Personal Saving Rate (Percent)

2010Q2

2014Q3E

(630, 5.5)

2012Q2 If SFP 500 at 1800

(618, 5.5)

6

-15

-10

-5

0

5

10

15

20

25

30

-15

-10

-5

0

5

10

15

20

25

30

2000 2002 2004 2006 2008 2010 2012 2014

Consumer Debt by Credit Score % Change – Year to Year % Change – Year to Year

Source: FRBNY Consumer Credit Panel

1st Quintile (Highest)

2nd Quintile

3rd Quintile 4th Quintile

5th Quintile (Lowest)

Note: Includes Student Loans 7

-30

-20

-10

0

10

20

30

-30

-20

-10

0

10

20

30

305 - 603 604 - 679 680 - 749 750 - 801 802 - 842

Change in Debt 2013Q3-2014Q3 By Credit Score Quintile Percent Percent

Equifax Risk Score Quintiles*

Mortgage/HELOC Auto Credit Card Inquiries

Note: * 2013Q3 Quintiles 8

Housing Starts Thousands, 3 MMA Thousands, 3 MMA

Source: Census Bureau

Total Multifamily (Right Axis)

1 Unit (Left Axis)

9

3

4

5

6

7

8

9

10

11

12

13

20

50

80

110

140

170

200

230

2000 2002 2004 2006 2008 2010 2012 2014

Single Family Housing Market Index, January 2000 = 100 Months’ Supply

Source: CoreLogic, National Association of Realtors

CoreLogic House Price Index

(Left Axis)

Months’ Supply (Right Axis)

“Normal” Range for Months’ Supply

10

-1000

-500

0

500

1000

1500

2000

1999 2001 2003 2005 2007 2009 2011 2013-1000

-500

0

500

1000

1500

2000

Household Formations 2 Year Avg. Change 2 Year Avg. Change

Source: Bureau of the Census

Total

Owner Occupied

Renter Occupied

11 11

Homeownership rate down to 64.3% from peak of 69.4% in 2004Q2. (6 million fewer homeowners)

500

550

600

650

700

750

800

500

550

600

650

700

750

800

1999 2002 2005 2008 2011 2014

About 35 to 40 Million People

Credit Score at Mortgage Origination: All First Mortgages Credit Score Credit Score

Source: FRBNY Consumer Credit Panel.

Median

10th Percentile

25th Percentile

12

Share of GDP Share of GDP

Source: Bureau of Economic Analysis / Haver Analytics

Structures

Equipment

Intellectual Property

Private Nonresidential

Private Nonresidential Fixed Investment Spending

13

Equipment Investment Spending and Capacity Real Business Investment in New Equipment (% Change – Year to Year)

Real Business Investment in New Equipment (% Change – Year to Year)

Source: Federal Reserve Board, Bureau of Economic Analysis

Manufacturing Capacity Utilization (Percent of Capacity)

2014Q3:

(77.3, 7.7)

14

0

1

2

3

4

5

6

0

1

2

3

4

5

6

1948 1960 1972 1984 1996 2008

Real Net Stock of Private Fixed Nonresidential Capital Year/Year % Change Year/Year % Change

Source: Bureau of Economic Analysis

Includes structures, equipment, and intellectual property products.

15

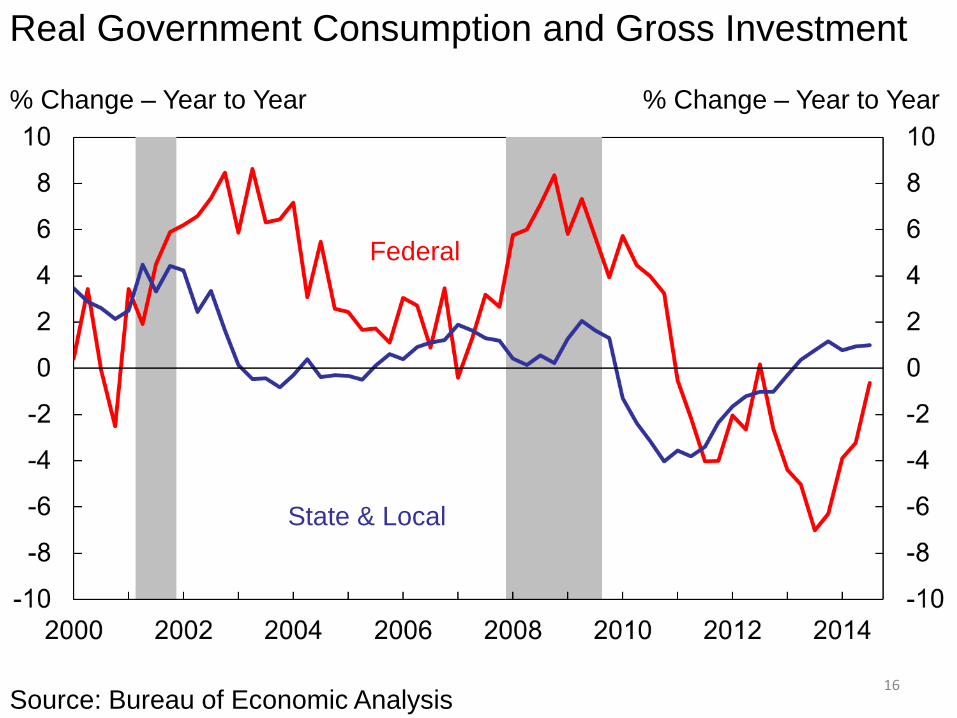

Real Government Consumption and Gross Investment

% Change – Year to Year % Change – Year to Year

Source: Bureau of Economic Analysis

Federal

State & Local

16

Growth of Real Exports of Goods and Manufacturing Output

-20

-10

0

10

20

-20

-10

0

10

20

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Percent Change Over Year Percent Change Over Year

Sources: BEA, FRB / Haver

Real Exports of Goods (SAAR, Chn.2009$)

Industrial Production: Manufacturing

r = 0.84

95

105

115

125

135

145

155

165

175

95

105

115

125

135

145

155

165

175

2010 2011 2012 2013 2014

Goods Exports by Destination Index, Q1 2010 = 100 Index, Q1 2010 = 100

Asia NIE

Japan

NAFTA

China

EU15

Source: Census Bureau. Data are 4 Quarter moving averages

Share of imports: NAFTA 33%, EU 17%, China 8%, Asia NIE 9%,Japan 4%. 18

Private Nonfarm Payroll Employment and Hours % Change – Year to Year

Source: Bureau of Labor Statistics

Hours*

Employment

% Change – Year to Year

* Note: Production and Non-Supervisory, Employees Only

19

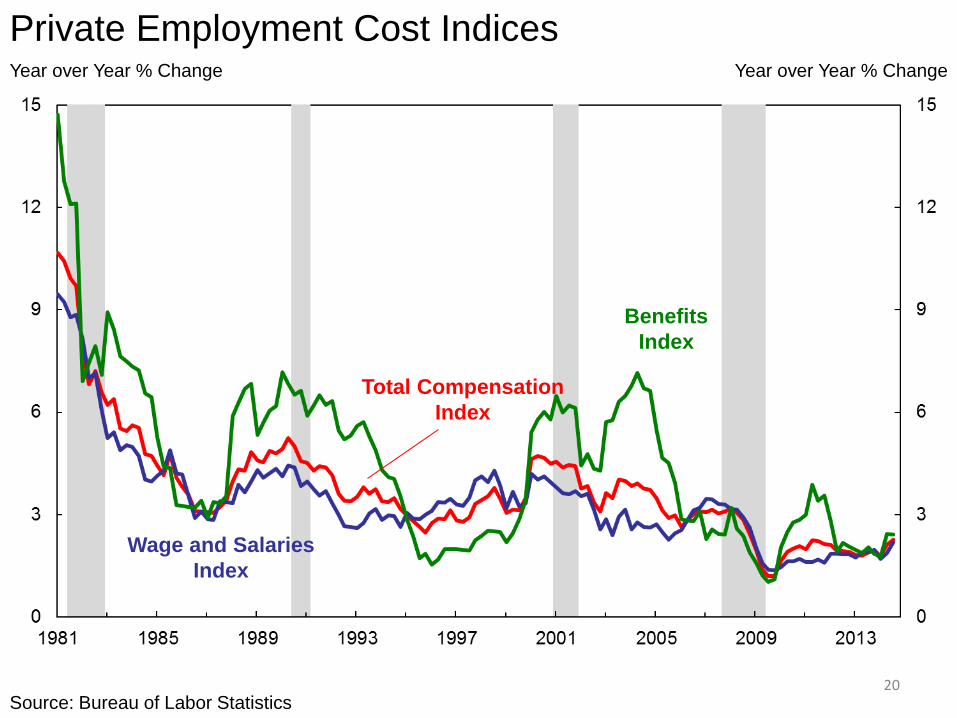

Private Employment Cost Indices Year over Year % Change Year over Year % Change

Source: Bureau of Labor Statistics

Total Compensation Index

Benefits Index

Wage and Salaries Index

20

-1

-0.5

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1991 1994 1997 2000 2003 2006 2009 2012

Long-Term Trends in Productivity and Compensation 5 % Year Change, AR 5 Year % Change, AR

Source: Bureau of Labor Statistics, and Bureau of Economic Analysis

Real Output Per Hour

(Left Axis)

Real Compensation

Per Hour (Left Axis)

21

Job-Finding Rate and Job-to-Job Transitions 12 MMA

Source: Bureau of Labor Statistics

U-to-E (Left Axis)

E-to-E (Right Axis)

12 MMA

22

CPI Inflation: Core, Core Goods and Core Services Yr/Yr % Change Yr/Yr % Change

Source: Bureau of Labor Statistics / Haver Analytics

Core Goods

Core Services

23

Rent inflation continues to increase, but inflation in medical care services and transportation services has slowed.

Continued appreciation of the dollar may put renewed downward pressure on core good prices.

Dollar Exchange Rate and Nonoil Import Prices % Change – Year to Year % Change – Year to Year

-8

-6

-4

-2

0

2

4

6

8

-20

-15

-10

-5

0

5

10

15

20

2000 2002 2004 2006 2008 2010 2012 2014Sources: Federal Reserve Board, Bureau of Labor Statistics. Dollar is Board’s Trade-Weighted M

Nonoil Import Prices (right axis)

Dollar (left axis)

r = -0.61

24

-1

0

1

2

3

4

5

-1

0

1

2

3

4

5

2003 2005 2007 2009 2011 2013

Rent of Primary Residence and Owner’s Equivalent Rent

% Change – Year to Year % Change – Year to Year

Source: Bureau of Labor Statistics

Owner’s Equivalent Rent

(22.5%)

Rent of Primary Residence

(6.5%)

25

Personal Consumption Expenditures: Health Care Price Index % Change – Year to Year

Source: Bureau of Economic Analysis / Haver Analytics

% Change – Year to Year

17% of total PCE deflator 19% of core PCE deflator

26

Producer Price Index: General Medical and Surgical Hospitals by Patient Type LN(Index) LN(Index)

Source: Bureau of Labor Statistics PPI Note: Jan-2005 set to 1

Medicare Patients (26.1%)

Medicaid Patients (18.1%)

Private Insurance and all other

Patients (55.8%)

27

TIPS Based Inflation Expectations

Source: Federal Reserve Board

Percent Percent

Note: Dashed lines represent 2 Standard Deviations from the mean

5-10 Years

3.06 (+2 SD)

2.63 (-2 SD) 2011 – Present

Average 2.63

November 12: 2.16

-10

-5

0

5

10

15

20

-10

-5

0

5

10

15

20

2000 2002 2004 2006 2008 2010 2012 2014

% Change – Year to Year % Change – Year to Year

Loans and Leases at Banks

Source: Federal Reserve Board Note: "Large Banks" include the 25 largest domestically chartered banks, ranked by assets (about 2/3 of the total).

All Domestically Chartered Banks

Small Banks

Large Banks

29

Actual and Expected Fed Funds Target Percent Percent

Source: Federal Reserve Board

Actual

June 16, 2014

Jul 14, 2014

May 14, 2014

30

Sep 15, 2014

Oct 15, 2014 Oct 27, 2014

31

Reference Charts

0

10

20

30

40

50

60

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20140

10

20

30

40

50

60

Transition of Mortgage Accounts from 30-60 Days Late Percent Percent

Source: FRBNY Consumer Credit Panel

To Current

To 90+ Days Late

32 32

33

% SA % SA

Source: BLS, Haver Analytics

25-54 (left axis)

55+ (right axis)

Labor Force Participation Rate by Age Group

34

% %

Source: BLS, Haver Analytics

25-54 (left axis)

55+ (right axis)

Population Shares by Age Group (4Q MA)

Components of Net Lending/Borrowing as a Share of GDP Share of GDP Share of GDP

Source: Federal Reserve Board, BEA Note: Shading represents NBER recessions.

-15

-10

-5

0

5

10

-15

-10

-5

0

5

10

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Government

Business

Households

35

Net Lending

35

Regional Economic Outlook Presentation to the Advisory Council on Small Business and Agriculture

Jason Bram, Officer November 20, 2014

The views expressed here are those of the presenter and do not necessarily represent the views of the Federal Reserve Bank of New York or the Federal Reserve System.

Regional Economic Activity Index of Coincident Economic Indicators (CEI)

3 Source: Federal Reserve Bank of New York; Puerto Rico Government Development Bank. Note: The Puerto Rico composite index is based on a different methodology than the indexes produced by the FRBNY.

80

90

100

110

120

130

2007 2008 2009 2010 2011 2012 2013 2014

Index (December 2007 = 100)

Shading indicates NBER recession

New Jersey

New York City

New York State

Puerto Rico

Sep

Apr08 Mar08 Nov05

Jan08

Nov09

Oct09 Nov10

Current Economic Conditions FRBNY Business Surveys, Current Conditions

Source: Federal Reserve Bank of New York. 4

-60

-40

-20

0

20

40

60

2007 2008 2009 2010 2011 2012 2013 2014 2015

NBER

Empire State Manufacturing Survey

Business Leaders Survey

Nov

Diffusion Index

Shading indicates NBER recession

Total Employment Seasonally Adjusted Index

Source: Bureau of Labor Statistics and Moody’s Economy.com. 5

88

92

96

100

104

108

2007 2008 2009 2010 2011 2012 2013 2014

Index (December 2007 = 100)

Shading indicates NBER recession

Dashed Line Indicates U.S. Employment Trough (February 2010)

Oct

Sep

Puerto Rico

New York State

New Jersey

United States

New York City

Total Employment Seasonally Adjusted Index

Source: Bureau of Labor Statistics and Moody’s Economy.com. 6

88

92

96

100

104

108

2007 2008 2009 2010 2011 2012 2013 2014

Index (December 2007 = 100)

Shading indicates NBER recession

Dashed Line Indicates U.S. Employment Trough (February 2010)

Oct

United States

New York City

Northern New Jersey

Putnam- Rockland-

Westchester

Long Island

Sep

Dashed Line Indicates U.S. Employment Trough (February 2010)

Total Employment Seasonally Adjusted Index

Source: Bureau of Labor Statistics and Moody’s Economy.com. 7

80

90

100

110

120

130

2007 2008 2009 2010 2011 2012 2013 2014

Index (December 2007 = 100)

Shading indicates NBER recession

Nevada

North Dakota

Florida

New York City

United States

New Jersey

Sep

Oct

Status of Jobs Recovery Share of Lost Jobs Gained Back During Local Recovery, September 2014

8

Source: Bureau of Labor Statistics and Moody’s Economy.com. Note: Putnam and Bergen are the Putnam-Rockland-Westchester and Bergen-Hudson-Passaic Special BLS Areas.

Newark

Glens Falls

Elmira Binghamton

Putnam Fair- field

Edison

Kingston

Buffalo

Rochester Syracuse

Utica

Albany

Ithaca

NYC

Recovered All Lost Jobs Recovered At Least 75 percent of Lost Jobs Recovered Less Than 75 percent of Lost Jobs No Recovery

US = 113 percent (115% through Oct14)

Puerto Rico

Job Growth by Sector Year-Over-Year Percent Change, September 2014

Source: Bureau of Labor Statistics and Moody’s Economy.com. 9

United States

New Jersey

New York City

New York State

3.9 -6.5 1.9 3.0 3.6 1.6 3.1 2.7 2.7 4.6 0.8 0.7 2.6 -3.2 4.1 2.5 2.0 1.4 4.0 2.2

1.9 1.4 0.2 0.2 1.7 1.6 4.6 2.0 1.4 0.6 0.3 -2.3

1.2 -1.4 1.7 0.7 1.1 -1.8 -2.2 -1.1 0.5 -0.3 -0.4 -0.3

2.0 0.1 2.4 1.3

Construction Professional & Business Services

Transportation & Utilities Leisure & Hospitality

Education & Health Services

Wholesale Trade Retail Trade

Manufacturing

Financial Activities Information

State & Local Government

Total

Job Growth by Sector Year-Over-Year Percent Change, September 2014

Source: Bureau of Labor Statistics and Moody’s Economy.com. 10

Fairfield County

Puerto Rico

0.0 8.7 4.6 0.0 5.7 1.4

-1.0 1.8 0.1 0.8

0.7 -1.0 2.7 -1.1 3.3 -0.7

-1.0 -1.1 0.8 2.1 3.3 -0.3

1.8 0.2

Construction Professional & Business Services

Transportation & Utilities Leisure & Hospitality

Education & Health Services

Wholesale Trade Retail Trade

Manufacturing

Financial Activities Information

State & Local Government

Total

United States

3.9 3.6 2.7 2.6 2.0

1.9 1.7 1.4

1.2 1.1 0.5

2.0

State and Local Government Seasonally Adjusted Index

Source: Bureau of Labor Statistics and Moody’s Economy.com.

11

95

96

97

98

99

100

101

102

2007 2008 2009 2010 2011 2012 2013 2014

Shading indicates NBER recession

Note: Dotted line smoothes fluctuations due to summer jobs programs.

Oct

Sep

United States

New York State

New Jersey

Index (December 2007 = 100)

Financial Activities Employment Seasonally Adjusted

Source: Bureau of Labor Statistics and Moody’s Economy.com. 12

200

225

250

275

300

325

350

375

400

350

375

400

425

450

475

500

525

550

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Sep New York City

(left scale)

New Jersey (right scale)

Sep01

Thousands – New York City Thousands – New Jersey

Shading indicates NBER recessions

Financial Activities Employment Sep 2014

NYC 444,730 NJ 250,600

New York City Industrial Specialization 2012 Employment and Earnings Location Quotients

13 Source: U.S. Census Bureau, County Business Patterns.

Professional & Business

Food & Drink

Ambulatory Health

Education

Securities

Information Real Estate

Credit Intermediation

Manufacturing

Arts & Sports

Museums

Auto Dealers

Gas Stations

Employment Location Quotient 2012: Log (Ratio) Scale

Earn

ings

Loc

atio

n Q

uotie

nt 2

012:

Log

(Rat

io) S

cale

1/16 1/8 1/4 1/2 1 2 4 8 16

16

8

4

2

1

1/2

1/4

1/8

1/16

Bubble Size Represents Number of Employees in 2012

(Star represents the U.S. average)

Home Prices CoreLogic Home Price Index, Seasonally Adjusted

14 Source: CoreLogic Home Price Index (including distressed sales); Seasonally adjusted by FRBNY staff. Note: ‘NYC Metro’ refers to the ‘New York-White Plains-Wayne NY-NJ Metro Division.’

40

50

60

70

80

90

100

110

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Sep

NYC Metro

New York State

United States

New Jersey

Northern New Jersey

Dec11 Shading indicates NBER recessions

Index (U.S. Peak of March 2006 = 100)

Backlog of Foreclosures Share of Mortgages in Foreclosure

15 Source: CoreLogic LoanPerformance (LP) and Lender Processing Services Mortgage Performance data (LPS).

0%

2%

4%

6%

8%

10%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Downstate New York includes Ulster, Dutchess, Orange, and all New York counties to the south. Upstate New York

includes all metropolitan counties to the north. Northern New Jersey includes Ocean, Monmouth, Middlesex,

Somerset, Hunterdon and all counties to the north.

Shading indicates NBER recession

Jul

Downstate NY

United States

Northern NJ

Upstate NY

Office Vacancy Rates Overall Vacancy Rates

16 Source: Cushman & Wakefield.

0%

5%

10%

15%

20%

25%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Shading indicates NBER recessions

Q3

Northern NJ

NYC Midtown

NYC Downtown

Central NJ

Office Vacancy Rates Overall Vacancy Rates

17 Source: Cushman & Wakefield.

0%

5%

10%

15%

20%

25%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Shading indicates NBER recessions

Q3

Long Island

Westchester County

Fairfield County

Appendix

Unemployment Rates in the Nation Seasonally Adjusted, September 2014

19 Source: Bureau of Labor Statistics and Moody’s Economy.com.

4.9% or Less 4.9% to 6.9% 6.9% or More

U.S. Rate in Sept = 5.9%

Unemployment Rates in the Region Seasonally Adjusted, September 2014

20 Source: Bureau of Labor Statistics and Moody’s Economy.com.

0%

2%

4%

6%

8%

New

Jersey

New York

City New York State United

States

Connecticut

5.9% (5.8% Oct)

6.2%

6.8% 6.5% 6.4%

Household Debt Total Debt Balance Per Capita

Source: FRBNY Consumer Credit Panel/Equifax.

21

$0

$20

$40

$60

$80

$100

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Thousands

Shading indicates NBER recession

New York State

United States

Nevada

California

Texas

New Jersey

Q2

International UpdatePresentation to the Small Business and AgricultureAdvisory Council

John ClarkNovember 20, 2014

-6

-4

-2

0

2

4

6

8

10

12

14

-6

-4

-2

0

2

4

6

8

10

12

14

07 08 09 10 11 12 13 14

Advanced and EM Economies: GDP GrowthPercent change from year ago quarter

Source: National authorities, FRBNY estimates for Q3 2014Data as of November 20, 2014

EMEs Ex. China

China

AdvancedForeign

Economies

Percent

US

Figure 1: Advanced and EM Economies: GDP GrowthPercent change form a year ago quarter Percent

-10

-8

-6

-4

-2

0

2

4

6

-10

-8

-6

-4

-2

0

2

4

6

07 08 09 10 11 12 13 14

Advanced and EM Economies: GDP GrowthPercent change from year ago quarter

Source: National authorities, FRBNY estimates

Euro Area

Percent

Japan

UnitedStates

United Kingdom

Figure 2: Advanced Economies: GDP GrowthPercent change form a year ago quarter Percent

4

6

8

10

12

14

16

18

20

4

6

8

10

12

14

16

18

20

1999 2001 2003 2005 2007 2009 2011 2013

Euro Area Unemployment RatesPercent, SA Percent, SA

1/ GDP-w eighted: Italy, Spain, Greece, Ireland, Portugal.Source: EuroStat. Data as of 11/18.

Other EMU

Peripheral 1/

Germany

Figure 3: Euro Area Unemployment RatesPercent, SA Percent, SA

0

1

2

3

4

0

1

2

3

4

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Euro Area: Headline and Core InflationPercent y/y Percent

Headline

Core

Source: Haver. Data as of November 18, 2014

October0.8

0.4

2% TargetCeiling

Figure 4: Euro Area: Headline and Core InflationPercent y/y Percent

1.7

1.8

1.9

2.0

2.1

2.2

2.3

2.4

1.7

1.8

1.9

2.0

2.1

2.2

2.3

2.4

Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14

Euro Area: Long-term Inflation Expectations5Y5Y Inflation forward swap rates Percent

Source: Bloomberg. Data through November 18, 2014

President Draghi's Jackson Hole speech on

August 22

Figure 5: Euro Area: Long-term Inflation Expectations5Y5Y Inflation forward swap rates Percent

0

500

1000

1500

2000

2500

3000

3500

0

500

1000

1500

2000

2500

3000

3500

Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

European Central Bank: Total Asset HoldingsBillions of euros Billions of euros

Sources: National authorities, Haver. Data as of November 18, 2014.

Figure 6: European Central Bank: Total Asset HoldingsBillions of euros Billions of euros

-8

-6

-4

-2

0

2

4

6

-8

-6

-4

-2

0

2

4

6

Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 Jun-14

Europe: Bank Credit GrowthPercent, Nominal Y/Y Percent

Core euro-area

Peripheral euro-area

Total euro-area

Source: ECB. Most recent data point is end-September 2014.

Figure 7: Europe: Bank Credit GrowthPercent, Nominal Y/Y Percent

35

40

45

50

55

60

65

-6

-4

-2

0

2

4

6

1999 2001 2003 2005 2007 2009 2011 2013 2015

Euro Area GDP Growth and Composite PMIPercent SAAR Index

GDP Growth (LHS)

CompositePMI (RHS)

Correlation: .86

Source: Haver, Markit. Data as of November 18, 2014

November51.4

0.6Q3

Figure 8: Euro Area GDP Growth and Composite PMIPercent SAAR Index

051015202530354045505560657075

05

1015202530354045505560657075

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Monetary BasePercent of GDP Percent of GDP

Source: National authorities. Data as of November 18th, 2014.

Japan

US

Euro Area

Figure 9: Monetary BasePercent of GDP Percent

-8

-6

-4

-2

0

2

4

6

8

10

-8

-6

-4

-2

0

2

4

6

8

10

Japan: GDP growth (seasonally-adjusted annual rate)Percent Percent

Sources: Cabinet Office, Bloomberg. Data as of October 1, 2014. 1/ Bloomberg.

Q/(Q-4)

Average analyst forecast

1/Q/Q SAAR

Tohokuearthquake

Figure 10: Japan GDP Growth (SAAR)Percent Percent

3.0

3.5

4.0

4.5

5.0

5.5

6.0

-6

-4

-2

0

2

4

6

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Japan: Unemployment and labor earningsPercent y/y, 6mma

1/ total workers * average monthly earnings Source: Country Authorities, data as of November 18th, 2014

Labor income1/ (LHS)

Percent

Unemployment (RHS)

Figure 11: Japan: Unemployment and Labor EarningsPercent y/y, 6mma Percent

-60

-40

-20

0

20

40

60

-60

-40

-20

0

20

40

60

Mar-82 Mar-87 Mar-92 Mar-97 Mar-02 Mar-07 Mar-12

Japan: Tankan Business Conditions SurveyDiffusion index for large manufacturers Index

Source: Haver Analytics, data as of November 18th, 2014.

Figure 12: Japan: Tankan Business Conditions SurveyDiffusion index for large manufacturers Index

-60

-40

-20

0

20

40

60

-60

-40

-20

0

20

40

60

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Japan: Industrial Production and Real ExportsPercent 3m saar

IP

Exports

Source: Japan METI, data as of November 18th, 2014.

T hokuearthquake

Figure 13 Japan Industrial Production and Real ExportsPercent 3m saar Percent

-3

-2

-1

0

1

2

3

4

-3

-2

-1

0

1

2

3

4

1990 1994 1998 2002 2006 2010 2014

Japan: Headline and Core CPIPercent Percent

Headline

Core

Source: Haver, data as of November 18th, 2014.

Target (2%)

Excluding impact of VAT hikeApril 1997

VAT hike

Figure 14: Japan: Headline and Core CPIPercent Percent

0

2

4

6

8

10

12

14

16

18

0

2

4

6

8

10

12

14

16

18

05 06 07 08 09 10 11 12 13 14

China: Real GDP growthPercent, y/y and q/q saar

y/y

Percent

Source: CEIC, FRBNY. Data as of November 19, 2014.

Q/Q SAAR, FRBNY est.

Figure 15: China: Real GDP GrowthPercent, y/y and q/q saar Percent

0

10

20

30

40

50

60

0

10

20

30

40

50

60

2008 2009 2010 2011 2012 2013 2014

China: Bank and Non-traditional Credit, Total FinancingPercent, y/y Percent, y/y

Source: CEIC, data as of November 18, 2014.1/Total financing includes bank loans, off-balance sheet & trust loans, net corp debt/equity

Bank credit

Total financing 1/

Non-traditional credit (off-balance sheet &

trust loans)

Figure 16: China: Bank and Non-traditional Credit, Total FinancingPercent, y/y Percent, y/y

5

10

15

20

47

50

53

56

2010 2011 2012 2013 2014

TitleDiffusion Index Percent, rolling q/q saar

1/ Official PMI is seasonably adjusted by FRBNY staff. Industrial Production is "Value Added of Industry".Source: CEIC, Haver. Data updated as of November 18.

Average of Official and HSBC/Markit

PMIs 1/ (LHS)

Industrial Production 1/ (RHS)

Figure 17: China: Manufacturing PMI and IPDiffusion Index Percent, rolling q/q saar

-60

-40

-20

0

20

40

60

80

100

-60

-40

-20

0

20

40

60

80

100

Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13

China: Commercial and Residential Real EstatePercent Y/Y, 3mma, Floor Percent

Source: CEIC, data as of November 18, 2014.

Construction, ytd Sales

Starts

Figure 18: China: Commercial and Residential Real EstatePercent Y/Y, 3mma, Floor Percent

4.0

4.5

5.0

5.5

6.0

4.0

4.5

5.0

5.5

6.0

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14

EMEs: Evolution of Consensus Growth ForecastsPercent y/y Percent y/y

Source: Consensus Forecasts through October

2013

2014

2015

Figure 19: EMEs: Evolution of Consensus Growth ForecastsPercent y/y Percent y/y

0

1

2

3

4

5

6

0

1

2

3

4

5

6

Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14

EMEs: Evolution of 2014 Growth Forecasts% y/y % y/y

Source: Consensuse forecasts, through October

Asia (ex-China)

LatAm

EMEA

Figure 20: EMEs: Evolution of 2014 Growth Forecasts% y/y % y/y

50

60

70

80

90

100

110

60

70

80

90

100

110

120

Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14

Oil, Grain, and Industrial Metals PricesUSD/Barrel Index

Sources: S&P, Haver, data as of November 18th

Brent Crude(LHS)

Grains(RHS)

Industrial Metals(RHS)

Figure 21: Oil, Grain, and Industrial Metals PricesUSD/Barrel Index

-4

-3

-2

-1

0

1

2

3

4

5

-15

-10

-5

0

5

10

15

20

Mar-92 Mar-95 Mar-98 Mar-01 Mar-04 Mar-07 Mar-10 Mar-13

Emerging Economies: Exports and AE GDPPercent change, Q/Q-4 Percent

Sources: National authorities, Netherlands Bureau of Economic Policy Analysis, Haver. Data as of November 19.

EM Exports (LHS)

AE GDP (RHS)

Figure 22: EMEs: Export Volumes and AE GDPPercent change, Q/Q-4 Percent

HungaryChina

TaiwanKorea

Indonesia

Malaysia

ArgentinaRussia

Poland

Colombia Mexico

PhilippinesThailand

ChileTurkey

India

South AfricaBrazil

-20

-15

-10

-5

0

5

-20

-15

-10

-5

0

5

-50 -40 -30 -20 -10 0 10 20 30

Current Account Balances vs. Recent CurrencyPerformance

Source: Bloomberg, Consensus Estimates

Current Account Balance as a % of Goods Exports (2013p)N

omin

al c

urre

ncy

mov

es fr

omM

ay 1

to A

ug 2

7

Peru

Figure 23: Current Account Balance vs. Recent Currency Performance

CNY

INRIDR

KRW

MYRPHP

THB

CZKHUF

PLN

TRY

BRL

CLP

COP

MXN

PENZAR

-20

-15

-10

-5

0

5

-20

-15

-10

-5

0

5

-60 -40 -20 0 20 40 60 80

Exchange Rate Changes (since July 2014) vs. Net Commodity Export Share

Source: Unctad, Bloomberg, data as of Nov 19

Net commodity exports as share of total goods exports (%)

EMFX

vs.

USD

sin

ce J

uly

1

PercentPercent

RUB(-27%)

Percent

Figure 24: Exchange Rate Changes (since July 2014) vs. Net Commodity Export SharePercent Percent

100

200

300

400

500

600

100

200

300

400

500

600

Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14

Bond Spreads to TreasuriesBasis points Bps

Source: Bloomberg, JP Morgan. Data through 11/18.

US High Yield

BBB Rated U.S. Corporates

EM Sovereign Bonds(EMBIG)

EM Corporate Bonds (CEMBI)

Figure 25: Bond Spreads to TreasuriesBasis points Bps

-350

-300

-250

-200

-150

-100

-50

0

-350

-300

-250

-200

-150

-100

-50

0

Jan-10 Aug-10 Mar-11 Oct-11 May-12 Dec-12 Jul-13 Feb-14 Sep-14

Cumulative changes in EM 5-yr. and U.S. 10-yr. yieldsBasis points, changes from 1/1/2010 bps

Source: Bloomberg

EM 5yr

US 10yr

Figure 26: Cumulative Changes in EM-yr. and US 10-yr. yieldsBasis points, changes from 1/1/2010 Bps

Leading Structural Challenges

Argentina Brazil China India Indonesia Korea Mexico Russia Saudi Arabia

South Africa Turkey

Distortionary Tax Code 153 159 120 158 137 25 118 56 3 24 71

Inadequate Power 80 14 119 111 121 2 133 117 15 150 49

Inadequate Infrastructure 120 71 74 85 61 23 66 93 22 66 49

Excessive Energy Subsidies 2.9 0.2 3.8 4.5 5.4 1.5 2.4 6.3 16.7 4.3 1.0

Excessive Red Tape 57 121 19 186 147 2 71 10 127 80 38

Labor Market Rigidities 144 92 34 99 103 78 113 72 70 116 130

Health & Primary Education 61 89 40 102 72 18 73 71 53 135 59Sources: IMF, World Bank, World Economic Forum

Figure 27: EMEs: Structural Challenges

Major EME Elections in 2014

Month Country Winner 1/March Turkey (Municipal) IncApril South Africa (Legislature and President) 2/ Inc

Indonesia (Parliament) 0ppMay India (Parliament) 0ppJuly Indonesia (President) 0ppAugust Turkey (Presidential) IncOctober Brazil (President, Legislature, Governors) Inc

1/ Incumbent (Inc) or Opposition (Opp) party2/ The National Assembly elects the President following its election.

Figure 28 Major EM Elections in 2014

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14

Advanced Economies: 10yr Bond YieldsPercent Percent

Source: Bloomberg, data through 11/19.

Germany

US

Japan

UK

Figure 29: AE 10yr Bond YieldsPercent Percent

88

90

92

94

96

98

100

102

104

88

90

92

94

96

98

100

102

104

Jan-14 Mar-14 May-14 Jul-14 Sep-14 Nov-14

Currency Performance vs USDIndex, 1 Jan 2014 = 100 Index, 1 Jan 2014 = 100

1/ JP Morgan EMFX Index (includes China)Source: Bloomberg, data as of 11/18/2014

Euro

Yen

EMEs 1/

Figure 30: Currency Performance vs USDIndex, 1 Jan 2014 = 100 Index

since Feb2013 2014 2015 2014 2015

Advanced 1/ 0.0 1.7 2.2 -0.4 0.0o/w: United States 2.2 2.2 3.0 -0.7 0.0

Euro Zone 0.0 0.8 1.2 -0.2 -0.2United Kingdom 1.7 3.0 2.6 0.5 0.2Japan 1.5 0.9 1.3 -0.8 -0.1

Emerging Markets 1/ 0.0 4.2 4.6 -0.6 -0.6o/w: China 7.7 7.3 7.0 -0.2 -0.3

Brazil 2.5 0.3 1.1 -2.0 -1.5India 4.7 5.5 6.1 0.3 0.1Russia 1.3 0.2 0.8 -2.2 -2.1Mexico 1.1 2.4 3.6 -1.0 -0.3Korea 3.0 3.5 3.6 -0.1 -0.2

ForecastsConsensus Forecast change

Data as of November 18. Sources: Blue Chip as of November where available, Consensus as of October. 1/ Dollar-GDP weighted average

Figure 31: Growth ForecastsPercent, yoy